Attached files

| file | filename |

|---|---|

| EX-10.53 - EXHIBIT 10.53 - KENNAMETAL INC | kmt630201810kex1053.htm |

| EX-32.1 - EXHIBIT 32.1 - KENNAMETAL INC | kmt630201810kex321.htm |

| EX-31.2 - EXHIBIT 31.2 - KENNAMETAL INC | kmt630201810kex312.htm |

| EX-31.1 - EXHIBIT 31.1 - KENNAMETAL INC | kmt630201810kex311.htm |

| EX-23 - EXHIBIT 23 - KENNAMETAL INC | kmt630201810kex23.htm |

| EX-21 - EXHIBIT 21 - KENNAMETAL INC | kmt630201810kex21.htm |

| EX-10.61 - EXHIBIT 10.61 - KENNAMETAL INC | kmt630201810kex1061.htm |

| EX-10.60 - EXHIBIT 10.60 - KENNAMETAL INC | kmt630201810kex1060.htm |

| EX-10.16 - EXHIBIT 10.16 - KENNAMETAL INC | kmt630201810kex1016.htm |

| EX-10.12 - EXHIBIT 10.12 - KENNAMETAL INC | kmt630201810kex1012.htm |

| EX-10.6 - EXHIBIT 10.6 - KENNAMETAL INC | kmt630201810kex106.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED JUNE 30, 2018

Commission File Number 1-5318

KENNAMETAL INC.

(Exact name of registrant as specified in its charter)

Pennsylvania | 25-0900168 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

600 Grant Street | ||

Suite 5100 | ||

Pittsburgh, Pennsylvania | 15219-2706 | |

(Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (412) 248-8000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Capital Stock, par value $1.25 per share | New York Stock Exchange | |

Preferred Stock Purchase Rights | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [X] No [ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer [X] | Accelerated filer [ ] | |||||

Non-accelerated filer [ ] (Do not check if smaller reporting company) | Smaller reporting company [ ] | |||||

Emerging growth company [ ] | ||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

As of December 31, 2017, the aggregate market value of the registrant’s Capital Stock held by non-affiliates of the registrant, estimated solely for the purposes of this Form 10-K, was approximately $2,922,300,000. For purposes of the foregoing calculation only, all directors and executive officers of the registrant and each person who may be deemed to own beneficially more than 5% of the registrant’s Capital Stock have been deemed affiliates.

As of July 31, 2018, there were 81,647,556 of the Registrant’s Capital Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 2018 Annual Meeting of Shareholders are incorporated by reference into Part III.

Item No. | Page | |

1 | ||

1A. | ||

1B. | ||

2. | ||

3. | ||

4. | ||

5. | ||

6. | ||

7. | ||

7A. | ||

8. | ||

9. | ||

9A. | ||

9B. | ||

10. | ||

11. | ||

12. | ||

13. | ||

14. | ||

15. | ||

16. | ||

2

FORWARD-LOOKING INFORMATION

Statements and financial discussion and analysis contained herein and in the documents incorporated by reference herein that are not historical facts are "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). For example, statements about Kennametal's outlook for earnings, sales volumes, cash flow, and capital expenditures for its fiscal year 2019, its expectations regarding future growth and any statements regarding future operating or financial performance or events are forward-looking. We have also included forward-looking statements in this Annual Report on Form 10-K ("Annual Report") concerning, among other things, our strategy, goals, plans and projections regarding our financial position, liquidity and capital resources, results of operations, market position, and product development. Forward-looking statements are based on management's beliefs, assumptions and estimates using information available to us at the time the statements are made. These statements are not guarantees of future events or performance and are subject to various risks and uncertainties that are difficult to predict. Should one or more of these risks or uncertainties materialize, or should the assumptions underlying the forward-looking statements prove incorrect, our actual results could vary materially from our current expectations. There are a number of factors that could cause our actual results to differ from those indicated in the forward-looking statements. They include: downturns in the business cycle or economic downturns; our ability to achieve all anticipated benefits of our restructuring, simplification and modernization initiatives; risks related to our foreign operations and international markets, such as fluctuations in currency exchange rates, different regulatory environments, trade barriers, exchange controls, and social and political instability; changes in the regulatory environment in which we operate, including environmental, health and safety regulations; potential for future goodwill and other intangible asset impairment charges; our ability to protect and defend our intellectual property; continuity and security of information technology infrastructure; competition; our ability to retain our management and employees; demands on management resources; availability and cost of the raw materials we use to manufacture our products; product liability claims; integrating acquisitions and achieving the expected savings and synergies; global or regional catastrophic events; demand for and market acceptance of our products; business divestitures; labor relations; and implementation of environmental remediation matters. We provide additional information about many of the specific risks we face in the "Risk Factors" section of this Annual Report. We can give no assurance that any goal or plan set forth in forward-looking statements can be achieved and readers are cautioned not to place undue reliance on such statements, which speak only as of the date made. Except as required by law, we do not intend to release publicly any revisions to forward-looking statements as a result of future events or developments, except as otherwise required by law.

3

PART I

ITEM 1 - BUSINESS

OVERVIEW Kennametal Inc. was incorporated in Pennsylvania in 1943 as a manufacturer of tungsten carbide metal cutting tooling. From this beginning, the Company has grown into a global leader in the development and application of tungsten carbides, ceramics, super-hard materials and solutions used in metal cutting and mission-critical wear applications to combat extreme conditions associated with wear fatigue, corrosion and high temperatures. The Company's reputation for material technology, metal cutting application knowledge, as well as expertise and innovation in the development of custom solutions and services, contributes to its leading position in its primary markets.

Our product offering includes a wide selection of standard and customized technologies for metalworking applications, such as turning, milling, hole making, tooling systems and services. End users of the Company's metalworking products include manufacturers engaged in a diverse array of industries including: the manufacturers of transportation vehicles and components, machine tools and light and heavy machinery; airframe and aerospace components; and energy-related components for the oil and gas industry, as well as power generation.

We also produce specialized wear components and metallurgical powders that are used for custom-engineered and challenging applications. End users of these products include producers and suppliers in equipment-intensive operations such as coal mining, road construction, quarrying, oil and gas exploration, refining, production and supply.

Unless otherwise specified, any reference to a “year” refers to our fiscal year ending on June 30.

BUSINESS SEGMENT REVIEW The Company operates in three segments: Industrial, Widia and Infrastructure. The Company's reportable operating segments have been determined in accordance with the Company's internal management structure, which is organized based on operating activities, the manner in which we organize segments for making operating decisions and assessing performance and the availability of separate financial results. Sales and operating income by segment are presented in Management’s Discussion and Analysis of Financial Condition and Results of Operations set forth in Item 7 of this Annual Report (MD&A). Additional segment data is provided in Note 20 of our consolidated financial statements set forth in Item 8 of this Annual Report which is incorporated herein by reference.

INDUSTRIAL In the Industrial segment, we focus on customers in the transportation, general engineering, aerospace and defense market sectors, delivering high performance metalworking tools for specified purposes. Our customers in these end markets use our products and services in the manufacture of engines, airframes, automobiles, trucks, ships and various other types of industrial equipment. The technology and customization services we provide vary by customer, application and industry. Industrial goes to market under the Kennametal® brand through its direct sales force, a network of independent and national chain distributors, integrated supplier channels and via the Internet. Application engineers and technicians are critical to the sales process and directly assist our customers with specified product design, selection, application and support.

WIDIA In the Widia segment, we offer a focused assortment of standard and custom metal cutting solutions to general engineering, aerospace, energy and transportation customers. We serve our customers primarily through a network of value added resellers, integrated supplier channels and via the Internet. Widia markets its products under the WIDIA®, WIDIA Hanita® and WIDIA GTD® brands.

INFRASTRUCTURE In the Infrastructure segment, we focus on customers in the energy and earthworks market sectors that support primary industries such as oil and gas, power generation and chemicals; underground, surface and hard-rock mining; highway construction and road maintenance; and process industries such as food and feed. Our success is determined by our ability to gain an in-depth understanding of our customers’ engineering and development needs, to provide complete system solutions and high-performance capabilities to optimize and add value to their operations. Infrastructure markets its products primarily under the Kennametal® brand and sells through a direct sales force as well as through distributors.

INTERNATIONAL OPERATIONS During 2018, we generated 59 percent of our sales in markets outside of the United States of America (U.S.), with principal international operations in Western Europe, Asia and Canada. We also operate manufacturing and distribution facilities in Israel, Latin America and South Africa, while serving customers through sales offices, agents and distributors in Eastern Europe and other parts of the world. While geographic diversification helps to minimize the sales and earnings impact of demand changes in any one particular region, our international operations are subject to normal risks of doing business globally, including fluctuations in currency exchange rates and changes in social, political and economic environments.

4

Our international assets and sales are presented in Note 20 of the Company’s consolidated financial statements, set forth in Item 8 of this Annual Report and are incorporated herein by reference. Further information about the effects and risks of currency exchange rates is presented in the Quantitative and Qualitative Disclosures About Market Risk section, as set forth in Item 7A of this Annual Report.

STRATEGY AND GENERAL DEVELOPMENT OF BUSINESS In fiscal 2018, we continued making progress on our three initiatives to transform the Company through growth, simplification and modernization. While each of these initiatives will continue during the coming years, we have made significant achievements in each of these areas.

Growth

• | Transitioning customers from the direct to indirect channel to both improve customer service and refocus our direct sales force on larger accounts, enabling our commercial team to grow sales on an account basis |

• | Continued development and refining of our channel strategy |

• | Implementing customer classification and customer relationship management (CRM) software for sales planning and strategy |

Simplification and Modernization

• | Reducing the number of stock keeping units, powder formulations, grades and coatings to reduce manufacturing and supply chain complexity |

• | Enforcing our established minimum order quantities and economic order quantities to improve manufacturing efficiency |

• | Initiated Industrial segment headcount reduction actions expected to deliver annualized pre-tax savings of approximately $10 million within the first half of fiscal 2019 |

• | Completed our legacy restructuring programs in fiscal 2018, achieving ongoing annualized savings of approximately $165 million |

• | Multi-year modernization program for our manufacturing facilities still in early stages |

• | Modernization of Rogers, Arkansas facility, largely complete |

Markets were more positive than in the prior year and exceeded the expectations we set when we embarked on fiscal 2018. Total sales growth was 15.0 percent with year-over-year growth in all segments, end markets and regions, reflecting not only continued strong end market demand but improving commercial execution. We delivered fiscal 2018 results in-line with our multi-year profitability improvement plan. We also expect fiscal 2019 to be on-track and represent another significant step forward in improved profitability and growth for the company.

The cost savings achieved through our restructuring programs do not include the anticipated benefits from our Modernization initiative. The results of these programs are anticipated to accrue to the Company over the next three years. At the same time, we continue to focus on cash flow and liquidity to support our planned investments. Our operating flexibility was enhanced with an amendment to our five-year, multi-currency, revolving credit facility that increased borrowing capacity from $600.0 million to $700.0 million and was extended to June 2023. Further, on June 7, 2018, we completed the offering of $300.0 million of 4.625 percent Senior Unsecured Notes due June 15, 2028. Net proceeds were used for redemption of our previously outstanding $400.0 million of 2.650 percent Senior Unsecured Notes with an original maturity of November 1, 2019 in July 2018. Further discussion and analysis of the development of our business is set forth in MD&A.

ACQUISITIONS AND DIVESTITURES We continue to evaluate new opportunities for the expansion of our existing product lines into new market areas where appropriate. We also continue to evaluate opportunities for the introduction of new and/or complementary product offerings into new and/or existing market areas where appropriate. In the near term, we expect to continue to grow our business and further enhance our market position through the investment opportunities that exist within our core businesses, though we may evaluate acquisition opportunities that have the potential to strengthen or expand our business.

RAW MATERIALS AND SUPPLIES Our major metallurgical raw materials consist of tungsten ore concentrates and scrap carbide, which is used to make tungsten oxide, as well as compounds and secondary materials such as cobalt. Although an adequate supply of these raw materials currently exists, our major sources for raw materials are located abroad and prices fluctuate at times. We have entered into extended raw material supply agreements and expect to implement product price increases as necessary to mitigate rising costs. For these reasons, we exercise great care in selecting, purchasing and managing availability of raw materials. We also purchase steel bars and forgings for making toolholders and other tool parts, as well as for producing rotary cutting tools and accessories. We purchase products for use in manufacturing processes and for resale from thousands of suppliers located in the U.S. and abroad. Our internal capabilities provide access to additional sources of raw materials and offer tungsten carbide recycling capabilities, and therefore, help mitigate our reliance on third parties. Although the trade environment is evolving, we currently do not expect tariffs to have a material effect on our sales or cost structure.

5

RESEARCH AND DEVELOPMENT Our product development efforts focus on providing solutions to our customers’ manufacturing challenges and productivity requirements. Our product development program provides discipline and focus to the product development process by establishing “gateways,” or sequential tests, during the development process to remove inefficiencies and accelerate improvements. This program speeds and streamlines development into a series of actions and decision points, combining efforts and resources to produce new and enhanced products faster. It is designed to assure a strong link between customer requirements and corporate strategy, and to enable us to gain the full benefits of our investment in new product development.

We hold a number of patents and trademarks which, in the aggregate, are material to the operation of our businesses. The duration of our patent protection varies throughout the world by jurisdiction.

Research and development expenses included in operating expense totaled $38.9 million, $38.0 million and $39.4 million in 2018, 2017 and 2016, respectively.

SEASONALITY Our business is affected by seasonal variations to varying degrees by traditional summer vacation shutdowns of customers’ plants and holiday shutdowns that affect our sales levels during the first and second quarters of our fiscal year.

BACKLOG Our backlog of orders generally is not significant to our operations.

COMPETITION As one of the world’s leading producers of metalworking tools and specialty wear-resistant components and coating solutions, we maintain a leading competitive position in major markets worldwide. We continually strengthen our competitive position by developing new and innovative metalworking and earth cutting products and services, innovative surface and wear solutions and innovative products for mining, construction and road milling applications among many others. We actively compete in the sale of all our products with several large global competitors and with many smaller niche businesses offering various capabilities to customers around the world. While several of our competitors are divisions of larger corporations, our industry remains largely fragmented, containing several hundred fabricators, toolmakers and niche specialty coating businesses. Many of our competitors operate relatively small facilities, producing a limited selection of tools while buying cemented tungsten carbide components from original producers of cemented tungsten carbide products, including Kennametal. We also supply coating solutions and other engineered wear-resistant products to both larger corporations and smaller niche businesses. Given the fragmentation, opportunities for consolidation exist from both U.S.-based and internationally-based firms, as well as among thousands of industrial supply distributors.

The principal competitive differentiators in our businesses include customer focused support and application expertise, custom and standard product innovation, product performance and quality, as well as service, pricing and productivity delivered ascribed to our brands. We derive competitive advantage from our premium brand positions, global presence, application expertise and ability to address unique customer needs with new and improved tools, innovative surface and wear solutions, highly engineered components, consistent quality, traditional and digital customer service and technical assistance capabilities, state-of-the-art manufacturing and multiple sales channels. With these strengths, we are able to sell products based on the value-added productivity we deliver to our customers, rather than competing solely on price.

REGULATION From time to time, we are a party to legal claims and proceedings that arise in the ordinary course of business, which may relate to our operations or assets, including real, tangible, or intellectual property assets. While we currently believe that the amount of ultimate liability, if any, we may face with respect to these actions will not materially affect our financial position, results of operations or liquidity, the ultimate outcome of any litigation is uncertain. Were an unfavorable outcome to occur or if protracted litigation were to ensue, the impact on us could be material.

Compliance with government laws and regulations pertaining to the discharge of materials or pollutants into the environment or otherwise relating to the protection of the environment did not have a material effect on our capital expenditures or competitive position for the years covered by this Annual Report, nor is such compliance expected to have a material effect on us in the future.

Among other environmental laws, we are subject to the Comprehensive Environmental Response Compensation and Liability Act of 1980 (Superfund), under which we have been designated by the United States Environmental Protection Agency (USEPA) as a potentially responsible party (PRP) with respect to environmental remedial costs at certain Superfund sites. We have evaluated our claims and potential liability associated with these Superfund sites based upon the best information currently available to us. We believe our environmental accruals will be adequate to cover our portion of the environmental remedial costs at those Superfund sites where we have been designated a PRP, to the extent these expenses are probable and reasonably estimable.

6

Reserves for other potential environmental liabilities at June 30, 2018 and 2017 were $12.5 million and $12.4 million, respectively. The reserves that we have established for our potential environmental liabilities represent our best current estimate of the costs of addressing all identified environmental situations, based on our review of currently available evidence, taking into consideration our prior experience in environmental remediation and the experiences of other companies, as well as public information released by the USEPA, other governmental agencies, and by the PRP groups in which we are participating. Although our reserves currently appear to be sufficient to cover our potential environmental liabilities, there are uncertainties associated with environmental remediation matters, and we can give no assurance that our estimate of any environmental liability will not increase or decrease in the future. Our reserved and unreserved liabilities for environmental matters could change substantially due to factors such as the nature and extent of contamination, changes in remedial requirements, technological changes, discovery of new information, the financial strength of other PRPs, the identification of new PRPs and the involvement of and direction taken by the U.S. government on these matters.

We maintain a Corporate Environmental, Health and Safety (EHS) Department to monitor our compliance with environmental regulations and to oversee our remediation activities. In addition, we have designated EHS coordinators who are responsible for each of our manufacturing facilities. Our financial management team periodically meets with members of the Corporate EHS Department and the Corporate Legal Department to review and evaluate the status of environmental projects and contingencies. On a quarterly basis, we review financial provisions and reserves for environmental contingencies and adjust these reserves when appropriate.

EMPLOYEES We employed approximately 10,500 people at June 30, 2018, of which approximately 3,400 were located in the U.S. and 7,100 were located in other parts of the world, principally Europe, Asia Pacific and India. At June 30, 2018, approximately 3,200 of our employees were represented by labor unions. We consider our labor relations to be generally good.

AVAILABLE INFORMATION Our Internet address is www.kennametal.com. On the SEC Filings page of our Website, which is accessible under the "About Us" tab, under Investor Relations, we post the following filings as soon as reasonably practicable after they are electronically filed with or furnished to the Securities and Exchange Commission (SEC): our annual reports on Form 10-K, our annual proxy statements, our annual conflict minerals disclosure and reports on Form SD, our annual reports on Form 11-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. The SEC Filings page of our Website also includes Forms 3, 4 and 5 filed pursuant to Section 16(a) of the Exchange Act. All filings posted on our SEC Filings page are available to be viewed on our Website free of charge. On the Corporate Governance page of our Website, which is accessible under the "About Us" tab, under Investor Relations, we post the following charters and guidelines: Audit Committee Charter, Compensation Committee Charter, Nominating/Corporate Governance Committee Charter, Kennametal Inc. Corporate Governance Guidelines and Kennametal Inc. Stock Ownership Guidelines. On the Ethics and Compliance page of our Website, which is under the "About Us" tab, under Company Profile, we post our Code of Conduct and our Conflict Minerals Statement. All charters and guidelines posted on our Website are available to be viewed free of charge. Information contained on our Website is not part of this Annual Report or our other filings with the SEC. Copies of this Annual Report and those items disclosed on the Corporate Governance and Ethics and Compliance pages of our Website are available without charge upon written request to: Investor Relations, Kennametal Inc., 600 Grant Street, Suite 5100, Pittsburgh, Pennsylvania 15219-2706. The public may read and copy any materials we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

RISK FACTORS

This section describes material risks to our business that are currently known to us. Our business, financial condition or results of operations may be materially affected by a number of factors. Our management regularly monitors the risks inherent in our business, with input and assistance from our Enterprise Risk Management department. In addition to real time monitoring, we periodically conduct a formal enterprise-wide risk assessment to identify factors and circumstances that might present significant risk to the Company. Many of these risks are discussed throughout this report. The risks below, however, are not exhaustive. We operate in a rapidly changing environment. Other risks that we currently believe to be immaterial could become material in the future. We are also subject to legal and regulatory changes. New factors could emerge, and it is not possible to predict the outcome of all such risk factors on our business, financial condition or results of operations. The following discussion details the material risk factors and uncertainties that we believe could cause Kennametal’s actual results to differ materially from those projected in any forward-looking statements.

7

Downturns in the business cycle could adversely affect our sales and profitability. Our business has historically been cyclical and subject to significant impact from economic downturns. Global economic downturn coupled with global financial and credit market disruptions have had a negative impact on our sales and profitability historically. These events could contribute to weak end markets, a sharp drop in demand for our products and services and higher costs of borrowing and/or diminished credit availability. Although we believe that the long-term prospects for our business remain positive, we are unable to predict the future course of industry variables or the strength and pace or sustainability of economic development.

Our restructuring efforts may not have the intended effects. We recently completed our legacy multi-year restructuring programs, and in the future may implement additional programs to improve our manufacturing costs and operating expenses. However, there is no assurance that these efforts, or that any other actions that we have taken or may take, will be sufficient to counter any future economic or industry disruptions. We cannot provide assurance that we will not incur additional restructuring charges or impairment charges, or that we will achieve all of the anticipated benefits from the restructuring actions we have taken or plan to take in the future. If we are unable to effectively restructure our operations in the light of evolving market conditions, it could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Our modernization initiative began in fiscal 2017. The purpose of this initiative is to invest in our plants, equipment and processes to automate and lower our overall labor cost. These capital investments are expected to result in substantial savings from reduced labor, maintenance and supply costs, while at the same time improving the quality of our products. We cannot provide any assurances that we will achieve all of the anticipated savings from these planned actions. These initiatives are expected to put pressure on our cash flows for the near-term. Further, as demand has grown faster than initially expected, it is possible that we may not be able to modernize fast enough to keep up with demand in select locations, causing us to keep direct hourly employment in certain circumstances somewhat higher than previously anticipated. If we are unable to effectively execute our plans, it could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Our international operations pose certain risks that may adversely impact sales and earnings. We have manufacturing operations and assets located outside of the U.S., including but not limited to those in Western Europe, Brazil, Canada, China, India, Israel and South Africa. We also sell our products to customers and distributors located outside of the U.S. During the year ended June 30, 2018, 59 percent of our consolidated sales were derived from non-U.S. markets. These international operations are subject to a number of special risks, in addition to the risks of our domestic operations, including currency exchange rate fluctuations, differing protections of intellectual property, trade barriers, exchange controls, regional economic uncertainty, differing (and possibly more stringent) labor regulations, labor unrest, risk of governmental expropriation, domestic and foreign customs and tariffs, current and changing regulatory environments (including, but not limited to, the risks associated with the importation and exportation of products and raw materials), risk of failure of our foreign employees to comply with both U.S. and foreign laws, including antitrust laws, trade regulations and the Foreign Corrupt Practices Act, difficulty in obtaining distribution support, difficulty in staffing and managing widespread operations, differences in the availability and terms of financing, political instability and unrest and risks of increases in taxes. Also, in some foreign jurisdictions, we may be subject to laws limiting the right and ability of entities organized or operating therein to pay dividends or remit earnings to affiliated companies unless specified conditions are met. To the extent we are unable to effectively manage our international operations and these risks, our international sales may be adversely affected, we may be subject to additional and unanticipated costs, and we may be subject to litigation or regulatory action. As a consequence, our business, financial condition and results of operations could be seriously harmed.

Changes in the regulatory environment, including environmental, health and safety regulations, could subject us to increased compliance and manufacturing costs, which could have a material adverse effect on our business.

Health and Safety Regulations. Certain of our products contain hard metals, including tungsten and cobalt. Hard metal dust is being studied for potential adverse health effects by organizations in several regions throughout the world, including the U.S., Europe and Japan. Future studies on the health effects of hard metals may result in our products being classified as hazardous to human health, which could lead to new regulations in countries in which we operate that may restrict or prohibit the use of, and/or exposure to, hard metal dust. New regulation of hard metals could require us to change our operations, and these changes could affect the quality of our products and materially increase our costs.

8

Environmental Regulations. We are subject to various environmental laws, and any violation of, or our liabilities under, these laws could adversely affect us. Our operations necessitate the use and handling of hazardous materials and, as a result, we are subject to various federal, state, local and foreign laws, regulations and ordinances relating to the protection of the environment, including those governing discharges to air and water, handling and disposal practices for solid and hazardous wastes, the cleanup of contaminated sites and the maintenance of a safe workplace. These laws impose penalties, fines and other sanctions for noncompliance and liability for response costs, property damages and personal injury resulting from past and current spills, disposals or other releases of, or exposure to, hazardous materials. We could incur substantial costs as a result of noncompliance with or liability for cleanup or other costs or damages under these laws. We may be subject to more stringent environmental laws in the future. If more stringent environmental laws are enacted in the future, these laws could have a material adverse effect on our business, financial condition and results of operations.

Regulations affecting the mining and drilling industries or utilities industry. Some of our principal customers are mining and drilling companies and utility companies. Many of our mining and drilling customers supply coal, oil, gas or other fuels as a source of energy to utility companies in the U.S. and other industrialized regions. The operations of these mining and drilling companies are geographically diverse and are subject to or affected by a wide array of regulations in the jurisdictions where they operate, such as applicable environmental laws and regulations governing the mining and drilling industry and the utilities industry. As a result of changes in regulations and laws relating to these industries, our customers’ operations could be disrupted or curtailed by governmental authorities. The high cost of compliance with these regulations may also induce customers to discontinue or limit their operations, and may discourage companies from developing new opportunities. As a result of these factors, demand for our mining- and drilling-related products could be substantially affected by regulations adversely impacting the mining and drilling industries or altering the consumption patterns of utilities.

Impairment of goodwill and other intangible assets with indefinite lives could result in a negative impact on our financial condition and results of operations. At June 30, 2018, goodwill and other indefinite-lived intangible assets totaled $319.4 million, or 11 percent of our total assets. Goodwill results from acquisitions, representing the excess of cost over the fair value of the net tangible and other identifiable intangible assets we have acquired. We assess at least annually whether there has been impairment in the value of our intangible assets. If future operating performance at one or more of our reporting units were to fall significantly below current levels, we could record, under current applicable accounting rules, a non-cash impairment charge for goodwill or other intangible asset impairment. Any determination requiring the impairment of a significant portion of goodwill or other intangible assets would negatively affect our financial condition and results of operations.

Our continued success depends on our ability to protect and defend our intellectual property. Our future success depends in part upon our ability to protect and defend our intellectual property. We rely principally on nondisclosure agreements and other contractual arrangements and trade secret laws and, to a lesser extent, trademark and patent laws, to protect our intellectual property. However, these measures may be inadequate to protect our intellectual property from infringement by others or prevent misappropriation of our proprietary rights. In addition, the laws of some foreign countries do not protect proprietary rights to the same extent as do U.S. laws. If one of our patents is infringed upon by a third party, we may need to devote significant time and financial resources to defend our rights with respect to such patent. We may not be successful in defending our patents. Similarly, while we do not knowingly infringe on the patents, copyrights or other intellectual property rights of others, we may be required to spend a significant amount of time and financial resources to resolve any infringement claims against us, and we may not be successful in defending our position or negotiating alternative remedies. Our inability to protect our proprietary information and enforce or defend our intellectual property rights in proceedings initiated by us or brought against us could have a material adverse effect on our business, financial condition and results of operations.

Failure of, or a breach in security of, our information technology systems could adversely affect our business. We rely on information technology infrastructure to achieve our business objectives. Any disruption of our infrastructure could negatively impact our ability to record or process orders, manufacture and ship in a timely manner, or otherwise carry on business in the normal course. Any disruption could cause us to lose customers or revenue and could require us to incur significant expense to remediate.

In recent years, cybersecurity attacks have become more sophisticated and more prevalent. A security breach of our information technology systems could interrupt or damage our operations or harm our reputation. In addition, we could be subject to liability if confidential information relating to customers, employees, vendors and the extended supply chain or other parties is misappropriated from our computer system. We do not believe we have been the target of a material successful cyber attack. While we have dedicated increased resources to fortify our security measures, our systems may be vulnerable to physical break-ins, computer viruses, human error, programming errors or similar disruptive problems. Therefore, we cannot assure that our system improvements will be sufficient to prevent or limit the damage from any cyber attack or network disruption.

9

We operate in a highly competitive environment. Our domestic and foreign operations are subject to significant competitive pressures. We compete directly and indirectly with other manufacturers and suppliers of metalworking tools, engineered components and advanced materials. Some of our competitors are larger than we are and may have greater access to financial resources or be less leveraged than us. In addition, the industry in which our products are used is a large, fragmented industry that is highly competitive.

If we are unable to retain our qualified management and employees, our business may be negatively affected. Our ability to provide high quality products and services depends in part on our ability to retain our skilled personnel in the areas of management, product engineering, servicing and sales. Competition for such personnel is intense, and our competitors can be expected to attempt to hire our management and skilled employees from time to time. In addition, our restructuring activities and strategies for growth have placed, and are expected to continue to place, increased demands on our management’s skills and resources. If we are unable to retain our management team and professional personnel, our customer relationships and level of technical expertise could be negatively affected, which may materially and adversely affect our business.

Any interruption of our workforce, including interruptions due to our restructuring initiatives, unionization efforts, changes in labor relations or shortages of appropriately skilled individuals could impact our business.

Our future operating results may be affected by fluctuations in the prices and availability of raw materials. The raw materials we use for our products include tungsten ore concentrates and scrap carbide, which is used to make tungsten oxide, as well as compounds and secondary materials such as cobalt. A significant portion of our raw materials is supplied by sources outside of the U.S. The raw materials industry as a whole is highly cyclical and at times pricing and supply can be volatile due to a number of factors beyond our control, including natural disasters, general economic and political conditions, labor costs, competition, import duties, tariffs and currency exchange rate fluctuations. This volatility can significantly affect our raw material costs. In an environment of increasing raw material prices, competitive conditions can affect how much of these price increases we can recover in the form of higher sales prices for our products. To the extent we are unable to pass on any raw material price increases to our customers, our profitability could be adversely affected. Furthermore, restrictions in the supply of tungsten, cobalt and other raw materials could adversely affect our operating results. If the prices for our raw materials increase or we are unable to secure adequate supplies of raw materials on favorable terms, our profitability could be impaired. If the prices for our raw materials decrease, we could face product pricing challenges.

Product liability claims could have a material adverse effect on our business. The sale of metalworking, mining, highway construction and other tools and related products as well as engineered components and advanced materials entails an inherent risk of product liability claims. We cannot give any assurances that the coverage limits of our insurance policies will be adequate or that our policies will cover any particular loss. Insurance can be expensive, and we may not always be able to purchase insurance on commercially acceptable terms, if at all. Claims brought against us that are not covered by insurance or that result in recoveries in excess of our insurance coverage could have a material adverse affect on our business, financial condition and results of operations.

We may not be able to complete, manage or integrate acquisitions successfully. We have acquired companies in the past and we may continue to evaluate acquisition opportunities that have the potential strengthen or expand our business. We can give no assurances, however, that any acquisition opportunities will arise or if they do, that they will be consummated, or that additional financing, if needed, will be available on satisfactory terms. In addition, acquisitions involve inherent risks that the businesses acquired will not perform in accordance with our expectations. We may not be able to achieve the synergies and other benefits we expect from the integration of acquisitions as successfully or rapidly as projected, if at all. Our failure to consummate an acquisition or effectively integrate newly acquired operations could prevent us from realizing our expected strategic growth and rate of return on an acquired business and could have a material and adverse effect on our results of operations and financial condition.

Natural disasters or other global or regional catastrophic events could disrupt our operations and adversely affect results. Despite our concerted effort to minimize risk to our production capabilities and corporate information systems and to reduce the effect of unforeseen interruptions to us through business continuity planning, we still may be exposed to interruptions due to catastrophe, natural disaster, pandemic, terrorism or acts of war, which are beyond our control. Disruptions to our facilities or systems, or to those of our key suppliers, could also interrupt operational processes and adversely impact our ability to manufacture our products and provide services and support to our customers. As a result, our business, our results of operations, financial position, cash flows and stock price could be adversely affected.

ITEM 1B – UNRESOLVED STAFF COMMENTS

None.

10

ITEM 2 – PROPERTIES

Our principal executive offices are located at 600 Grant Street, Suite 5100, Pittsburgh, Pennsylvania, 15219. Our corporate and technology center is located at 1600 Technology Way, P.O. Box 231, Latrobe, Pennsylvania, 15650. A summary of our principal manufacturing facilities and other materially important properties is as follows:

Primary Segment | ||||||

Location | Owned/Leased | Principal Products | IND(1) | WID(2) | INF(3) | |

United States: | ||||||

Gurley, Alabama | Owned | Metallurgical Powders | X | |||

Huntsville, Alabama | Owned | Metallurgical Powders | X | |||

Madison, Alabama | Owned | Tungsten Heavy Alloy | X | |||

Rogers, Arkansas | Owned/Leased | Carbide Products, Pelletizing Die Plates and Downhole Drilling Carbide Components | X | |||

Rockford, Illinois | Owned | Indexable Tooling | X | |||

Goshen, Indiana | Leased | Powders; Welding Rods, Wires and Machines | X | |||

New Albany, Indiana | Leased | High Wear Coating for Steel Parts | X | |||

Greenfield, Massachusetts | Owned | High-Speed Steel Taps | X | |||

Traverse City, Michigan | Owned | Wear Parts | X | |||

Fallon, Nevada | Owned | Metallurgical Powders | X | |||

Asheboro, North Carolina | Owned | Carbide Round Tools | X | |||

Henderson, North Carolina | Owned | Metallurgical Powders | X | |||

Roanoke Rapids, North Carolina | Owned | Metalworking Inserts | X | |||

Cleveland, Ohio | Leased | Distribution | X | |||

Orwell, Ohio | Owned | Metalworking Inserts | X | |||

Solon, Ohio | Owned | Metalworking Toolholders | X | |||

Whitehouse, Ohio | Owned | Metalworking Inserts and Round Tools | X | |||

Bedford, Pennsylvania | Owned/Leased | Mining and Construction Tools, Wear Parts and Distribution | X | |||

Irwin, Pennsylvania | Owned | Carbide Wear Parts | X | |||

New Castle, Pennsylvania | Owned/Leased | Specialty Metals and Alloys | X | |||

Johnson City, Tennessee | Owned | Metalworking Inserts | X | |||

La Vergne, Tennessee | Owned | Metalworking Inserts | X | |||

New Market, Virginia | Owned | Metalworking Toolholders | X | |||

International: | ||||||

La Paz, Bolivia | Owned | Tungsten Concentrate | X | |||

Indaiatuba, Brazil | Leased | Metalworking Carbide Drills and Toolholders | X | |||

Belleville, Canada | Owned | Casting Components, Coatings and Powder Metallurgy Components | X | |||

Victoria, Canada | Owned | Wear Parts | X | |||

Fengpu, China | Owned | Intermetallic Composite Ceramic Powders and Parts | X | |||

Shanghai, China | Owned | Powders, Welding Rods and Wires and Casting Components | X | |||

Shanghai, China | Owned | Distribution | X | |||

Tianjin, China | Owned | Metalworking Inserts, Carbide Round Tools and Metallurgical Powders | X | X | ||

Xuzhou, China | Leased | Mining Tools | X | |||

Ebermannstadt, Germany | Owned | Metalworking Inserts | X | |||

Essen, Germany | Owned | Metalworking Inserts | X | |||

Königsee, Germany | Leased | Metalworking Carbide Drills | X | |||

Lichtenau, Germany | Owned | Metalworking Toolholders | X | |||

Mistelgau, Germany | Owned | Wear Parts and Metallurgical Powders | X | |||

Nabburg, Germany | Owned | Metalworking Toolholders and Metalworking Round Tools, Drills and Mills | X | |||

Neunkirchen, Germany | Owned | Distribution | X | |||

11

Primary Segment | ||||||

Location | Owned/Leased | Principal Products | IND(1) | WID(2) | INF(3) | |

Schongau, Germany | Owned | Ceramic Vaporizer Boats | X | |||

Vohenstrauss, Germany | Owned | Metalworking Carbide Drills | X | |||

Bangalore, India | Owned | Metalworking Inserts, Toolholders and Wear Parts | X | X | X | |

Shlomi, Israel | Owned | High-Speed Steel and Carbide Round Tools | X | |||

Zory, Poland | Leased | Mining and Construction Conicals | X | |||

Boksburg, South Africa | Leased | Mining and Construction Conicals | X | |||

Barcelona, Spain | Leased | Metalworking Cutting Tools | X | |||

Kingswinford, United Kingdom | Leased | Distribution | X | |||

Newport, United Kingdom | Owned | Intermetallic Composite Powders | X | |||

(1) | Industrial segment |

(2) | Widia segment |

(3) | Infrastructure segment |

We also have a network of warehouses and customer service centers located throughout North America, Europe, India, Asia Pacific and Latin America, a significant portion of which are leased. The majority of our research and development efforts are conducted at our technology center located in Latrobe, Pennsylvania, U.S., as well as at our facilities in Rogers, Arkansas, U.S.; Fürth, Germany and Bangalore, India.

We use all of our significant properties in the businesses of powder metallurgy, tools, tooling systems, engineered components and advanced materials. Our production capacity is adequate for our present needs. We believe that our properties have been adequately maintained, are generally in good condition and are suitable for our business as presently conducted.

ITEM 3 - LEGAL PROCEEDINGS

The information set forth in Part I, Item 1, of this Annual Report under the caption “Regulation” is incorporated by reference into this Item 3. From time to time, we are party to legal claims and proceedings that arise in the ordinary course of business, which may relate to our operations or assets, including real, tangible or intellectual property. Although certain of these types of actions are currently pending, we do not believe that any individual proceeding is material or that our pending legal proceedings in the aggregate are material to Kennametal.

ITEM 4 - MINE SAFETY DISCLOSURES

Not applicable.

EXECUTIVE OFFICERS OF THE REGISTRANT

Incorporated by reference into this Part I is the information set forth in Part III, Item 10 of this Annual Report under the caption “Executive Officers of the Registrant.”

12

PART II

ITEM 5 - MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our capital stock is traded on the New York Stock Exchange under the symbol "KMT." The number of shareholders of record as of July 31, 2018 was 1,545. Stock price ranges and dividends declared and paid for 2018 and 2017 were as follows:

Quarter ended | September 30 | December 31 | March 31 | June 30 | ||||||||||||

Fiscal 2018 | ||||||||||||||||

High | $ | 40.78 | $ | 49.31 | $ | 52.52 | $ | 41.51 | ||||||||

Low | 32.23 | 39.89 | 39.40 | 34.37 | ||||||||||||

Dividends | 0.20 | 0.20 | 0.20 | 0.20 | ||||||||||||

Fiscal 2017 | ||||||||||||||||

High | $ | 29.35 | $ | 35.66 | $ | 39.94 | $ | 43.09 | ||||||||

Low | 20.40 | 26.79 | 31.28 | 36.14 | ||||||||||||

Dividends | 0.20 | 0.20 | 0.20 | 0.20 | ||||||||||||

The information incorporated by reference into Part III, Item 12 of this Annual Report from our 2018 Proxy Statement under the heading “Equity Compensation Plans – Equity Compensation Plan Information” is hereby incorporated by reference into this Item 5.

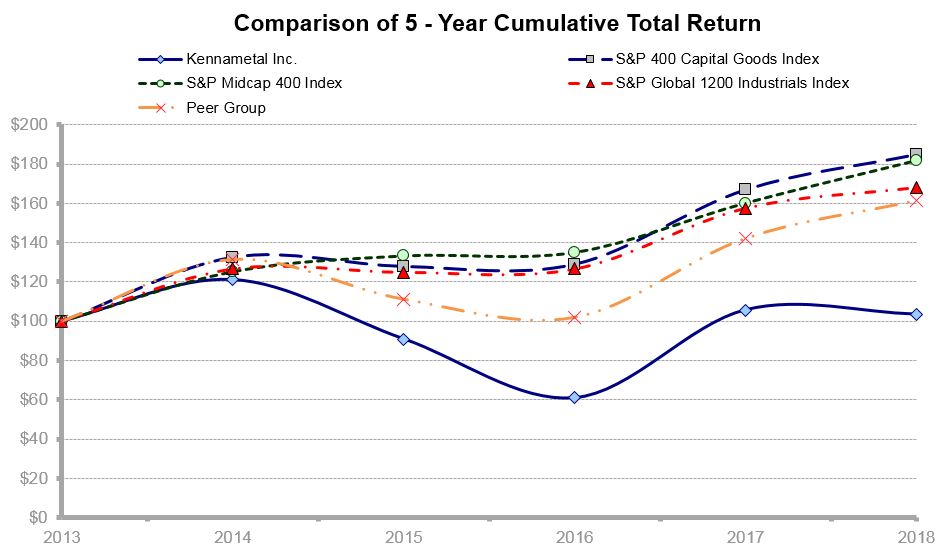

PERFORMANCE GRAPH

The following graph compares cumulative total shareholder return on our capital stock with the cumulative total shareholder return on the common stock of the companies in the Standard & Poor’s Mid-Cap 400 Market Index (S&P Midcap 400), the Standard & Poor’s 400 Capital Goods (S&P 400 Capital Goods), the Standard & Poor's Global 1200 Industrials Index (S&P Global 1200 Industrials) and the peer group of companies determined by us for the period from July 1, 2012 to June 30, 2018.

The Peer Group consists of the following companies: Actuant Corporation; Allegheny Technologies Incorporated; Ametek, Inc.; Barnes Group Inc.; Carpenter Technology Corporation; Crane Co.; Donaldson Company, Inc.; Flowserve Corporation; Graco Inc.; Harsco Corporation; IDEX Corporation; ITT Inc.; Lincoln Electric Holdings, Inc.; The Manitowoc Company, Inc.; Nordson Corporation; Rexnord Corporation; Sandvik AB, Corp.; SPX Corporation; SPX FLOW, Inc.; The Timken Company; and Woodward, Inc.

13

Assumes $100 Invested on July 1, 2013 and All Dividends Reinvested

2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |||||||||||||

Kennametal | $ | 100.00 | $ | 121.09 | $ | 90.95 | $ | 60.95 | $ | 105.70 | $ | 103.48 | ||||||

Peer Group Index | 100.00 | 131.45 | 111.23 | 101.92 | 142.17 | 161.46 | ||||||||||||

S&P Midcap 400 | 100.00 | 125.24 | 133.25 | 135.02 | 160.09 | 181.71 | ||||||||||||

S&P 400 Capital Goods | 100.00 | 132.62 | 128.00 | 129.08 | 166.96 | 184.90 | ||||||||||||

S&P Global 1200 Industrials | 100.00 | 126.67 | 125.00 | 126.65 | 157.56 | 168.15 | ||||||||||||

ISSUER PURCHASES OF EQUITY SECURITIES

Period | Total Number of Shares Purchased(1) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs (2) | ||||||||

April 1 through April 30, 2018 | — | $ | — | — | 10,100,100 | |||||||

May 1 through May 31, 2018 | 2,049 | 38.04 | — | 10,100,100 | ||||||||

June 1 through June 30, 2018 | 39 | 37.28 | — | 10,100,100 | ||||||||

Total | 2,088 | $ | 38.03 | — | ||||||||

(1) | During the fourth quarter of 2018, 1,391 shares were purchased on the open market on behalf of Kennametal to fund the Company’s dividend reinvestment program. Employees also delivered 697 shares of restricted stock to Kennametal, upon vesting, to satisfy tax withholding requirements. |

(2) | On July 25, 2013, the Company publicly announced an open-ended, amended repurchase program for up to 17 million shares of its outstanding common stock outside of the Company's dividend reinvestment program. |

UNREGISTERED SALES OF EQUITY SECURITIES

None.

14

ITEM 6 - SELECTED FINANCIAL DATA

2018 | 2017 | 2016 | 2015 | 2014 | |||||||||||||

OPERATING RESULTS (in thousands) | |||||||||||||||||

Sales | $ | 2,367,853 | $ | 2,058,368 | $ | 2,098,436 | $ | 2,647,195 | $ | 2,837,190 | |||||||

Cost of goods sold | 1,535,561 | 1,400,661 | 1,482,369 | 1,841,202 | 1,940,187 | ||||||||||||

Operating expense | 498,152 | 463,167 | 494,975 | 554,895 | 589,768 | ||||||||||||

Restructuring and asset impairment charges | (1 | ) | 11,907 | 65,018 | 143,810 | 582,235 | 17,608 | ||||||||||

Loss on divestiture | — | — | 131,463 | — | — | ||||||||||||

Interest expense | 30,081 | 28,842 | 27,752 | 31,466 | 32,451 | ||||||||||||

Provision (benefit) for income taxes | 69,981 | 29,895 | 25,313 | (16,654 | ) | 66,611 | |||||||||||

Income (loss) from continuing operations attributable to Kennametal | 200,180 | 49,138 | (225,968 | ) | (373,896 | ) | 158,366 | ||||||||||

Net income (loss) attributable to Kennametal | 200,180 | 49,138 | (225,968 | ) | (373,896 | ) | 158,366 | ||||||||||

FINANCIAL POSITION (in thousands) | |||||||||||||||||

Working capital | $ | 659,635 | $ | 652,423 | $ | 648,066 | $ | 775,802 | $ | 962,440 | |||||||

Total assets | 2,925,737 | 2,415,496 | 2,362,783 | 2,843,655 | 3,860,726 | ||||||||||||

Long-term debt, including capital leases, excluding current maturities | 591,505 | 694,991 | 693,548 | 730,011 | 974,306 | ||||||||||||

Total debt, including capital leases and notes payable | 991,705 | 695,916 | 695,443 | 745,713 | 1,054,423 | ||||||||||||

Total Kennametal shareholders' equity | 1,194,325 | 1,017,294 | 964,323 | 1,345,807 | 1,929,256 | ||||||||||||

PER SHARE DATA ATTRIBUTABLE TO KENNAMETAL SHAREHOLDERS | |||||||||||||||||

Basic earnings (loss) from continuing operations | (2 | ) | $ | 2.45 | $ | 0.61 | $ | (2.83 | ) | $ | (4.71 | ) | $ | 2.01 | |||

Basic earnings (loss) | (2 | ) | 2.45 | 0.61 | (2.83 | ) | (4.71 | ) | 2.01 | ||||||||

Diluted earnings (loss) from continuing operations | (2 | ) | 2.42 | 0.61 | (2.83 | ) | (4.71 | ) | 1.99 | ||||||||

Diluted earnings (loss) | (2 | ) | 2.42 | 0.61 | (2.83 | ) | (4.71 | ) | 1.99 | ||||||||

Dividends | 0.80 | 0.80 | 0.80 | 0.72 | 0.72 | ||||||||||||

Book value (at June 30) | 14.63 | 12.61 | 12.10 | 16.96 | 24.52 | ||||||||||||

Market Price (at June 30) | 35.90 | 37.42 | 22.11 | 34.12 | 46.28 | ||||||||||||

OTHER DATA (in thousands, except number of employees) | |||||||||||||||||

Capital expenditures | $ | 171,004 | $ | 118,018 | $ | 110,697 | $ | 100,939 | $ | 117,376 | |||||||

Number of employees (at June 30) | 10,491 | 10,744 | 11,178 | 12,718 | 13,521 | ||||||||||||

Basic weighted average shares outstanding | 81,544 | 80,351 | 79,835 | 79,342 | 78,678 | ||||||||||||

Diluted weighted average shares outstanding | 82,754 | 81,169 | 79,835 | 79,342 | 79,667 | ||||||||||||

KEY RATIOS | |||||||||||||||||

Sales growth (decline) | (3 | ) | 15.0 | % | (1.9 | )% | (20.7 | )% | (6.7 | )% | 9.6 | % | |||||

Gross profit margin | 35.1 | 32.0 | 29.4 | 30.4 | 31.6 | ||||||||||||

Operating margin | (4 | ) | 13.0 | 5.5 | (8.3 | ) | (13.5 | ) | 9.3 | ||||||||

(1) | In 2018, 2017 and 2014, all charges were related to restructuring. In 2016, the charges related to intangible asset impairment of $108.5 million, restructuring charges of $30.0 million and fixed asset disposal charges of $5.4 million. In 2015, the charges related to intangible asset impairment of $541.7 million and restructuring charges of $40.5 million. |

(2) | 2018 included restructuring and related charges of $0.16, impact of an out of period adjustment to the provision for income taxes of $0.06 and net impact of tax reform of $0.01. 2017 included restructuring and related charges of $0.89 and Australia deferred tax valuation allowance of $0.02. 2016 included U.S. deferred tax valuation allowance of $1.02, divestiture and related charges of $1.39, intangible asset impairment charges of $0.96, restructuring and related charges of $0.50, fixed asset disposal charges of $0.05 and operations of divested businesses of $0.02. 2015 included intangible asset impairment charges of $6.13 and restructuring and related charges of $0.56. |

(3) | Divestiture impact of sales decline was negative 4 percent and negative 5 percent in 2017 and 2016, respectively. |

(4) | Included restructuring and related charges of $15.9 million, $76.2 million, $53.5 million and $58.1 million in 2018, 2017, 2016 and 2015, respectively; intangible asset impairment of $108.5 million and $541.7 million in 2016 and 2015, respectively; and divestiture and related charges of $131.5 million in 2016. |

15

ITEM 7 - MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion should be read in connection with the consolidated financial statements of Kennametal Inc. and the related financial statement notes included in Item 8 of this Annual Report. Unless otherwise specified, any reference to a “year” is to our fiscal year ended June 30. Additionally, when used in this Annual Report, unless the context requires otherwise, the terms “we,” “our” and “us” refer to Kennametal Inc. and its subsidiaries.

OVERVIEW Kennametal Inc. was incorporated in Pennsylvania in 1943 as a manufacturer of tungsten carbide metal cutting tooling. From this beginning, the Company has grown into a global leader in the development and application of tungsten carbides, ceramics, super-hard materials and solutions used in metal cutting and mission-critical wear applications to combat extreme conditions associated with wear fatigue, corrosion and high temperatures. The Company's reputation for material technology, metal cutting application knowledge, as well as expertise and innovation in the development of custom solutions and services, contributes to its leading position in its primary markets.

Our product offering includes a wide selection of standard and customized technologies for metalworking applications, such as turning, milling, hole making, tooling systems and services. End users of the Company's metalworking products include manufacturers engaged in a diverse array of industries including: the manufacturers of transportation vehicles and components, machine tools and light and heavy machinery; airframe and aerospace components; and energy-related components for the oil and gas industry, as well as power generation.

We also produce specialized wear components and metallurgical powders that are used for custom-engineered and challenging applications. End users of these products include producers and suppliers in equipment-intensive operations such as coal mining, road construction, quarrying, oil and gas exploration, refining, production and supply.

Throughout the MD&A, we refer to measures used by management to evaluate performance. We also refer to a number of financial measures that are not defined under accounting principles generally accepted in the United States of America (U.S. GAAP), including organic sales growth, constant currency regional sales growth (decline) and constant currency end market sales growth (decline). The explanation at the end of the MD&A provides the definition of these non-GAAP financial measures as well as details on their use and a reconciliation to the most directly comparable GAAP financial measures.

Operational results in 2018 were strong, and we made progress on our growth and margin expansion initiatives in the year. Every business segment reported significant growth and profitability improvement. Sales grew in all end markets and regions as a result of strong end market demand and from our focus on commercial execution. Overall results for 2018 were in-line with our multi-year profitability improvement plan, and our expectations for the next year are also on-track, representing another significant step forward in improved profitability for the Company.

Price realization outpaced raw material cost inflation in 2018, and we expect that price realization to offset anticipated raw material cost inflation in fiscal 2019. Although the trade environment is evolving, we do not currently expect tariffs to have a material effect on our sales or cost structure.

For 2018, sales were $2,367.9 million, an increase of 15 percent compared to prior year sales of $2,058.4 million, driven by organic sales growth and favorable currency exchange, partially offset by a slight decrease due to fewer business days. Operating income was $307.6 million compared to $112.9 million in the prior year. The increase was driven primarily by organic sales growth, lower restructuring and related charges, incremental restructuring benefits, favorable currency exchange and mix and modernization benefits, partially offset by higher raw material costs, salary inflation and higher variable compensation expense due to higher than expected operating results. Earnings per diluted share (EPS) was $2.42 in 2018.

We substantially completed our legacy restructuring program in the September quarter of 2018. Pre-tax benefits from these restructuring actions delivered full fiscal 2018 year-over-year incremental savings of approximately $55 million. In association with our simplification initiative, we recorded $8 million of restructuring and related charges for simplification-related employment reduction in the Industrial segment in the June quarter of fiscal 2018. Annualized run-rate pre-tax savings of approximately $10 million are expected to be achieved in the first half of fiscal 2019 in connection with this initiative. While our modernization efforts are starting to drive improved results along with continuing benefits from simplification, incrementally higher results of those programs are anticipated to accrue to the Company over the next few years.

Our effective tax rate for 2018 was higher than anticipated at the beginning of the fiscal year. This increase in the tax rate is due primarily to the earlier than expected release of substantially all of the valuation allowance on U.S. deferred tax assets. The release of the valuation allowance in the December quarter of fiscal 2018 was triggered by the application of the toll tax provision in the Tax Cuts and Jobs Act of 2017 (TCJA). Along with full-year income in the U.S. in 2018, our domestic deferred taxes are in a net liability position as of June 30, 2018. After other remaining provisions of TCJA are adopted, we anticipate our long-term tax rate will decrease from mid-20s to low-20s. See Note 12 of our consolidated financial statements set forth in Item 8 of this Annual Report (Note 12).

16

We generated cash flow from operating activities of $277.3 million in 2018, driven primarily by higher cash from operations before changes in certain other assets and liabilities and lower restructuring payments. We made capital expenditures of $171.0 million during the year, and returned $65.1 million to shareholders through dividends.

We further enhanced liquidity and strengthened our financial position by issuing $300.0 million of 4.625 percent Senior Unsecured Notes due 2028 (New Notes). Net proceeds were used for redemption of our previously outstanding $400.0 million of 2.650 percent Senior Unsecured Notes with an original maturity of November 1, 2019 ($400.0 million Notes) on July 9, 2018. We also entered into an amendment to the five-year, multi-currency, revolving credit facility. The amendment extends the tenor for a new five-year term to June 2023 and expands borrowing capacity from $600 million to $700 million. The prior facility was scheduled to mature in April 2021. The new facility has lower LIBOR borrowing margins and enhanced commercial terms.

We invested further in technology and innovation to continue delivering high quality products to our customers. Research and development expenses included in operating expense totaled $38.9 million for 2018.

RESULTS OF CONTINUING OPERATIONS

SALES Sales of $2,367.9 million in 2018 increased 15 percent from $2,058.4 million in 2017 reflecting a 12 percent increase from organic sales growth and favorable currency exchange impact of 4 percent, partially offset by 1 percent decrease due to fewer business days. Sales increased by 16 percent in the Infrastructure segment, 15 percent in the Industrial segment and 12 percent in the Widia segment.

Sales of $2,058.4 million in 2017 decreased 2 percent from $2,098.4 million in 2016 reflecting a 4 percent divestiture impact and a 2 percent unfavorable currency exchange impact, partially offset by 4 percent organic sales growth. Sales increased by 4 percent in the Widia segment and 3 percent in the Industrial segment, while sales decreased by 9 percent in the Infrastructure segment.

End Market Sales Growth (Decline): | As Reported | Constant Currency | |||||||||

Year Ended June 30, 2018 | Year Ended June 30, 2017 | Year Ended June 30, 2018 | Year Ended June 30, 2017 | ||||||||

Energy | 19 | % | 2 | % | 17 | % | 9 | % | |||

General engineering | 15 | 2 | 11 | 6 | |||||||

Aerospace and defense | 15 | 2 | 11 | 4 | |||||||

Transportation | 13 | (1 | ) | 8 | 2 | ||||||

Earthworks | 10 | (10 | ) | 7 | (4 | ) | |||||

Regional Sales Growth (Decline): | As Reported | Constant Currency | |||||||||

Year Ended June 30, 2018 | Year Ended June 30, 2017 | Year Ended June 30, 2018 | Year Ended June 30, 2017 | ||||||||

Asia Pacific | 19 | % | 4 | % | 15 | % | 8 | % | |||

Europe, the Middle East and Africa (EMEA) | 16 | (9 | ) | 7 | — | ||||||

Americas | 13 | — | 13 | 4 | |||||||

GROSS PROFIT Gross profit increased $174.6 million to $832.3 million in 2018 from $657.7 million in 2017. This increase was primarily due to organic sales growth, incremental restructuring benefits of approximately $42 million, favorable currency exchange impact of $29.6 million, favorable mix, modernization benefits of approximately $9 million and $4.3 million less restructuring-related charges, partially offset by higher raw material and overtime costs and salary inflation. The gross profit margin for 2018 was 35.1 percent compared to 32.0 percent in 2017.

Gross profit increased $41.6 million to $657.7 million in 2017 from $616.1 million in 2016. This increase was primarily due to incremental restructuring benefits of approximately $36 million, better absorption and productivity, organic sales growth and lower raw material costs, partially offset by an unfavorable currency exchange impact of $12.6 million, unfavorable business mix and divestiture impact of $11.4 million. The gross profit margin for 2017 was 32.0 percent compared to 29.4 percent in 2016.

17

OPERATING EXPENSE Operating expense in 2018 was $498.2 million, an increase of $35.0 million, or 7.6 percent, compared to $463.2 million in 2017. The increase was primarily due to higher variable compensation expense of $14 million due to higher than expected operating results, an unfavorable currency exchange impact of $14.5 million and salary inflation, partially offset by incremental restructuring benefits of approximately $13 million and $2.5 million less in restructuring-related charges.

Operating expense in 2017 was $463.2 million, a decrease of $31.8 million, or 6.4 percent, compared to $495.0 million in 2016. The decrease was primarily due to incremental restructuring benefits of approximately $36 million, divestiture impact of $10.5 million, $12.7 million less in restructuring-related charges and a favorable foreign currency exchange impact of $5.1 million, offset partially by higher performance-based compensation.

RESTRUCTURING AND RELATED CHARGES AND ASSET IMPAIRMENT CHARGES

Restructuring and Related Charges

Legacy Restructuring

In prior years, we implemented certain actions to streamline the Company's cost structure. The purpose of this restructuring initiative was to improve the alignment of our cost structure with the operating environment through employee reductions and to consolidate certain manufacturing facilities. These restructuring actions were substantially completed in the September quarter of 2018, were mostly cash expenditures and achieved annual run rate ongoing pre-tax savings of approximately $165 million.

Total restructuring and related charges since inception of $152.7 million have been recorded for these programs through June 30, 2018: $85.6 million in Industrial, $13.9 million in Widia, $45.9 million in Infrastructure and $7.3 million in Corporate.

Industrial Simplification

In the June quarter of 2018, we implemented and substantially completed restructuring actions to streamline the Industrial segment's cost structure by directing resources to more profitable business and increasing sales force productivity. These actions are currently anticipated to deliver annual ongoing pre-tax savings of approximately $10 million in the first half of fiscal 2019 and are anticipated to be mostly cash expenditures. Total restructuring and related charges since inception of $8.2 million have been recorded for this program in the Industrial segment through June 30, 2018.

Combined Restructuring

During 2018, we recorded restructuring and related charges of $15.9 million, net of a $4.7 million gain on sale of the previously closed Houston manufacturing location that was part of our legacy restructuring programs. Of this amount, restructuring charges totaled $16.4 million, of which benefit of $0.2 million was related to inventory and were recorded in cost of goods sold. Restructuring-related charges of $3.7 million were recorded in cost of goods sold and $0.5 million were recorded in operating expense during 2018.

During 2017, we recorded restructuring and related charges of $76.2 million. Of this amount, restructuring charges totaled $65.6 million, of which $0.6 million were charges related to inventory and were recorded in cost of goods sold. Restructuring-related charges of $7.1 million were recorded in cost of goods sold and $3.5 million were recorded in operating expense during 2017.

During 2016, we recorded restructuring and related charges of $53.5 million. Of this amount, restructuring charges totaled $30.0 million. Restructuring-related charges of $7.3 million were recorded in cost of goods sold and $16.2 million in operating expense during 2016.

Asset Impairment Charges

During 2016, we recorded non-cash pre-tax goodwill and other intangible asset impairment charges of $108.5 million. See Note 2 of our consolidated financial statements set forth in Item 8 of this Annual Report (Note 2).

During 2016, we identified specific machinery and equipment that was no longer being utilized in the manufacturing organization, which we disposed of by abandonment. As a result of this review, we recorded property, plant, and equipment impairment charges of $5.4 million during 2016, which has been presented as restructuring and asset impairment charges in our consolidated statement of income.

LOSS ON DIVESTITURE We recognized a pre-tax loss on the sale of non-core businesses of $131.5 million in 2016, which includes the impact of estimated working capital adjustments, deal costs and transaction costs. Of this amount, $127.9 million and $3.6 million were recorded in the Infrastructure and Industrial segments, respectively. See Note 4 of our consolidated financial statements set forth in Item 8 of this Annual Report.

18

AMORTIZATION OF INTANGIBLES Amortization expense was $14.7 million, $16.6 million and $20.8 million in 2018, 2017 and 2016, respectively. The decrease of $1.9 million from 2017 to 2018 was driven primarily by certain finite-lived intangible assets being fully amortized in 2018, and the decrease of $4.2 million from 2016 to 2017 was driven primarily by the impact of divestiture.

INTEREST EXPENSE Interest expense increased $1.2 million to $30.1 million in 2018, compared with $28.8 million in 2017 primarily due to the incremental interest expense on the New Notes, partially offset by lower average borrowings in 2018. Interest expense increased $1.1 million to $28.8 million in 2017, compared with $27.8 million in 2016 due to higher average borrowings and a higher credit facility fee. The portion of our debt subject to variable rates of interest was less than 1 percent at June 30, 2018, 2017 and 2016.

OTHER EXPENSE (INCOME), NET In 2018, other expense, net was $2.4 million compared to $2.2 million in 2017. Prior year income from transition services provided related to a prior divestiture that did not repeat and a gain on sale of an investment that did not repeat were partially offset by higher interest income and foreign currency transaction gains.