Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - COLUMBUS MCKINNON CORP | a033118exhibit321.htm |

| EX-31.2 - EXHIBIT 31.2 - COLUMBUS MCKINNON CORP | a033118exhibit312.htm |

| EX-31.1 - EXHIBIT 31.1 - COLUMBUS MCKINNON CORP | a033118exhibit311.htm |

| EX-23.1 - EXHIBIT 23.1 - COLUMBUS MCKINNON CORP | a033118exhibit231.htm |

| EX-21.1 - EXHIBIT 21.1 - COLUMBUS MCKINNON CORP | a033118exhibit211.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 (FEE REQUIRED) |

For the fiscal year ended March 31, 2018

Commission file number 0-27618

_________________

COLUMBUS McKINNON CORPORATION

(Exact name of Registrant as specified in its charter)

New York | 16-0547600 | |

(State of Incorporation) | (I.R.S. Employer Identification Number) | |

205 Crosspoint Parkway

Getzville, New York 14068

(Address of principal executive offices, including zip code)

(716) 689-5400

(Registrant’s telephone number, including area code)

_________________

Securities pursuant to section 12(b) of the Act:

NONE

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.01 Par Value (and rights attached thereto)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No ý

Indicate by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K ý.

Indicate by checkmark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “accelerated filer,” “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Act.

Large accelerated filer x | Accelerated filer o |

Non-accelerated filer o | Smaller reporting company o |

Emerging Growth Company o | |

If an Emerging Growth Company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the voting stock held by non-affiliates of the Registrant as of September 30, 2017 (the second fiscal quarter in which this Form 10-K relates) was approximately $868 million, based upon the closing price of the Company’s common shares as quoted on the Nasdaq Stock Market on such date. The number of shares of the Registrant’s common stock outstanding as of May 25, 2018 was 23,090,255 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s proxy statement for its 2018 Annual Meeting of Shareholders to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after the end of the Registrant’s fiscal year ended March 31, 2018 are incorporated by reference into Part III of this report.

1

COLUMBUS McKINNON CORPORATION

2018 Annual Report on Form 10-K

This annual report contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements involve known and unknown risks, uncertainties and other factors that could cause our actual results to differ materially from the results expressed or implied by such statements, including general economic and business conditions, conditions affecting the industries served by us and our subsidiaries, conditions affecting our customers and suppliers, competitor responses to our products and services, the overall market acceptance of such products and services, the integration of acquisitions and other factors set forth herein under “Risk Factors.” We use words like “will,” “may,” “should,” “plan,” “believe,” “expect,” “anticipate,” “intend,” “future” and other similar expressions to identify forward looking statements. These forward looking statements speak only as of their respective dates and we do not undertake and specifically decline any obligation to publicly release the results of any revisions to these forward-looking statements that may be made to reflect any future events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated changes. Our actual operating results could differ materially from those predicted in these forward-looking statements, and any other events anticipated in the forward-looking statements may not actually occur.

2

TABLE OF CONTENTS

Part I | |||

Item 1. | Business | ||

Item 1A. | Risk Factors | ||

Item 1B. | Unresolved Staff Comments | ||

Item 2. | Properties | ||

Item 3. | Legal Proceedings | ||

Item 4. | Mine Safety Disclosures | ||

Part II | |||

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | ||

Item 6. | Selected Financial Data | ||

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | ||

Item 7A | Quantitative and Qualitative Disclosures About Market Risk | ||

Item 8. | Financial Statements and Supplemental Data | ||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosures | ||

Item 9A. | Controls and Procedures | ||

Item 9B. | Other Information | ||

Part III. | |||

Item 10. | Directors and Executive Officers of Registrant | ||

Item 11. | Executive Compensation | ||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||

Item 13. | Certain Relationships and Related Transactions, and Director Independence | ||

Item 14. | Principal Accountant Fees and Services | ||

Part IV | |||

Item 15 | Exhibits and Financial Statement Schedules | ||

3

PART I

Item 1. Business

General

Columbus McKinnon is a leading worldwide designer, manufacturer and marketer of motion control products, technologies, systems and services that efficiently and ergonomically move, lift, position and secure materials. Key products include hoists, cranes, actuators, rigging tools, light rail work stations, and digital power and motion control systems. The Company is focused on commercial and industrial applications that require the safety and quality provided by its superior design and engineering know-how. Our products are used for mission critical industrial applications where we have established trusted brands with significant customer retention. Our targeted market verticals includes general industrial, construction and infrastructure, mining, oil & gas, energy, aerospace, transportation, automotive, heavy equipment manufacturing and entertainment.

In the U.S., we are the market leader for hoists and material handling drive systems, our principal line of products, as well as certain chain, forged fittings, and actuator products. We have achieved this leadership position through strategic acquisitions, our extensive, diverse, and well-established distribution channels and our commitment to product innovation and quality. We believe the breadth of our product offering and expansive distribution channels provide us a strategic advantage in our markets. Additionally, we believe we are the market leader for manual hoist and actuator products in Europe. Our market leadership and strong brands enable us to sell more products than our competition through our extensive distribution channels in the U.S. and Europe. The acquisition of STAHL CraneSystems (STAHL) in fiscal 2017, which is well renowned for its custom engineering of lifting solutions and hoisting technology, advanced our position as a global leader in the production of explosion-protected hoists. STAHL serves independent crane builders and Engineering Procurement and Construction (EPC) firms, providing products to a variety of end markets including automotive, general manufacturing, oil and gas, steel and concrete, power generation, as well as process industries such as chemical and pharmaceuticals.

Our business strategy, Blueprint 2021, is a three-phased strategy to increase the earnings power of the company and transform us into a growth-oriented industrial technology company. The goal of our strategy is to increase our earnings power and expand EBITDA margins, as well as improve our Return on Invested Capital. Phase I, which began early in fiscal 2018, was focused on attaining operational control and instilling a performance based culture to drive results. We formed four teams of cross-functional experts (tiger teams) to address specific areas:

• | Grow the North American core business, |

• | Leverage the Magnetek acquisition, |

• | Create value with the STAHL acquisition, and |

• | Pay down debt incurred as a result of the STAHL acquisition. |

We also instituted a new operating system, Earnings Power Acceleration or “E-PAS™.” E-PAS™ includes a set of tools that we will use to improve the efficiency of our business and deliver meaningful profit improvement.

We completed Phase I during fiscal 2018. In doing so, we believe we grew market share in the U.S. and achieved $6 million of synergies related to the STAHL acquisition. In addition, we introduced several new products incorporating smart hoist technologies and repaid $60 million of our long-term debt.

We began Phase II of the strategy in November 2017. This phase is focused on operational excellence and profitable growth and is about simplifying the business structure and product platforms, improving operating performance, and focusing our R&D expenditures to grow profitably. Investment in R&D will advance our smart hoist technology and enhance our customers’ digital experience so we can capitalize on the automation megatrend. We expect to double R&D expenditures by fiscal 2021 from fiscal 2017 levels, including approximately $5 million related to STAHL. Research and development costs were $13,617,000, $10,482,000, and $7,393,000 in fiscal years 2018, 2017, and 2016, respectively.

Phase III of the strategy is centered on business development including the assessment of our current product portfolio as well as an acquisition strategy to advance our transformation into a leading industrial technology company. Our acquisitions of Magnetek, Inc. and STAHL and our efforts to leverage their technology are well aligned with our transformation efforts. We have demonstrated our ability to acquire companies and achieve significant synergies and growth. We will look for acquisitions in the material handling and motion control markets. We believe the automation megatrend will provide a deep pipeline of attractive, high margin companies that will continue to transform us.

4

Our business is cyclical in nature and sensitive to changes in general economic conditions, including changes in industrial capacity utilization, industrial production, and general economic activity indicators, like GDP growth. Both U.S. and Eurozone capacity utilization are leading market indicators for our Company.

Business Description

ASC Topic 280 “Segment Reporting” establishes the standards for reporting information about operating segments in financial statements. We provide our products and services through one operating and reportable segment.

We design, manufacture, and distribute a broad range of material handling products for various applications. Products include a wide variety of electric, air-powered, lever, and hand hoists, hoist trolleys, explosion-protected hoists, winches, industrial crane systems such as steel bridge, gantry, and jib cranes, and aluminum work stations; alloy and carbon steel chain; forged attachments, such as hooks, shackles, textile slings, clamps, and load binders; mechanical and electromechanical actuators and rotary unions; below-the-hook special purpose lifters and tire shredders; power and motion control systems, such as AC and DC drive systems, radio remote controls, push button pendant stations, brakes, and collision avoidance and power delivery subsystems. These products are typically manufactured for stock or assembled to order from standard components and are sold primarily through a variety of commercial distributors and to a lesser extent, directly to end-users. The acquisition of STAHL brings market leadership with independent crane builders and EPC firms. The diverse end-users of our products are in a variety of industries including manufacturing, power generation and distribution, utilities, wind power, warehouses, commercial construction, oil and gas exploration and refining, petrochemical, marine, ship building, transportation and heavy duty trucking, agriculture, logging and mining. We also serve a niche market for the entertainment industry including permanent and traveling concerts, live theater, and sporting venues.

Products

Of our fiscal 2018 sales, $443,433,000 or 53% were U.S. and $395,986,000 or 47% were non-U.S. The following table sets forth certain sales data for our products, expressed as a percentage of net sales for fiscal 2018 and 2017:

Fiscal Years Ended March 31, | ||||||

2018 | 2017 | |||||

Hoists | 63 | % | 56 | % | ||

Chain and rigging tools | 10 | 11 | ||||

Digital power control and delivery systems | 10 | 12 | ||||

Actuators and rotary unions | 9 | 11 | ||||

Industrial cranes | 4 | 5 | ||||

Elevator application drive systems | 3 | 3 | ||||

Other | 1 | 2 | ||||

100 | % | 100 | % | |||

Hoists - We manufacture a wide variety of electric chain hoists, electric wire rope hoists, hand-operated hoists, winches, lever tools, and air-powered hoists. Load capacities for our hoist product lines range from one-eighth of a ton to nearly 140 tons with the acquisition of STAHL. These products are sold under our Budgit, Chester, CM, Coffing, Little Mule, Pfaff, Shaw-Box, Yale, STAHL, and other recognized brands. Our hoists are sold for use in numerous general industrial applications, as well as for use in the construction, energy, mining, food services, entertainment, and other markets. We also supply hoist trolleys, driven manually or by electric motors, that are used in conjunction with hoists.

We also offer several lines of standard and custom-designed, below-the-hook tooling, clamps, and textile strappings. Below-the-hook tooling, textile, and chain slings and associated forgings, and clamps are specialized lifting apparatus used in a variety of lifting activities performed in conjunction with hoisting or lifting applications.

STAHL primarily manufactures explosion-protected hoists and custom engineered hoists, including wire rope and manual and electric chain hoists. STAHL products are sold to a variety of end markets including automotive, general manufacturing, oil and gas, steel and concrete, power generation as well as process industries such as chemical and pharmaceuticals.

5

Chain and Rigging Tools - We manufacture alloy and carbon steel chain for various industrial and consumer applications. U.S. federal regulations require the use of alloy chain, which we first developed, for overhead lifting applications because of its strength and wear characteristics. A line of our alloy chain is sold under the Herc-AlloyTM brand name for use in overhead lifting, pulling, and restraining applications. In addition, we also sell specialized load chain for use in hoists, as well as three grades and multiple sizes of carbon steel welded-link chain for various load securing and other non-overhead lifting applications.

We produce a broad line of alloy and carbon steel closed-die forged chain attachments, including hooks, shackles, HammerloksTM, and master links. These forged attachments are used in chain, wire rope, and textile rigging applications in a variety of industries, including transportation, mining, construction, marine, logging, petrochemical, and agriculture.

In addition, we manufacture carbon steel forged and stamped products, such as load binders, logging tools, and other securing devices, for sale to the industrial and logging markets through industrial distributors, hardware distributors, mass merchandiser outlets, and OEMs.

Digital Power Control and Delivery Systems - Through our fiscal 2016 acquisition of Magnetek, we are a leading provider of innovative power control and delivery systems and solutions for overhead material handling applications used in a number of diverse industries, including aerospace, automotive, steel, aluminum, paper, logging, mining, ship loading, nuclear power plants, and heavy movable structures. We are a major supplier in North America of power and motion control systems, which include AC and DC drive systems, radio remote controls, push button pendant stations, brakes, and collision avoidance and power delivery subsystems. While we sell primarily to OEMs of overhead cranes and hoists, we spend a great deal of effort understanding the needs of end users to gain specification. We can combine our products with engineered services to provide complete customer-specific systems solutions.

We are also a leading independent supplier of AC and DC digital motion control systems for underground coal mining equipment. Our systems are used in coal hauling vehicles, shuttle cars, scoops, and other heavy mining equipment.

Actuators and Rotary Unions - Through our Duff-Norton and Pfaff divisions, we design and manufacture industrial components such as mechanical and electromechanical actuators and rotary unions. Actuators are linear motion devices used in a variety of industries, including the transportation, paper, steel, energy, aerospace, and many other commercial industries. Rotary unions are devices that transfer a liquid or gas from a fixed pipe or hose to a rotating drum, cylinder or other device. Rotary unions are used in a variety of industries including pulp and paper, printing, textile and fabric manufacturing, rubber, and plastic.

Industrial Cranes - We participate in the crane industry, predominately in the U.S. market, but also globally in certain product offerings, through our offering of overhead steel jib and gantry cranes. Our products are marketed under the Unified, CES, Abell-Howe, and Washington Equipment brands. Crane builders represent a specific distribution channel for electric wire rope hoists, chain hoists, and other crane components. We also manufacture and market overhead aluminum light rail workstations primarily used in automotive and other industrial applications.

Elevator Application Drive Systems - We design, build, sell, and support elevator application-specific drive products that efficiently deliver power used to control motion, primarily in high-rise, high-speed elevator applications. We are recognized as an industry leader for DC high-performance elevator drives, as well as for AC drives used with low- and high-performance traction elevators, due to our extensive application expertise and product reliability. Our elevator product offerings are comprised of highly integrated subsystems and drives, sold mainly to elevator OEMs. In addition, our product options include a number of regenerative controls for both new building installations and elevator modernization projects that help building owners save energy.

Other - This category primarily includes tire shredders. We have developed and patented a line of heavy equipment that shred whole tires, for use in recycling the various components of a tire including rubber and steel. These recycled products are used as aggregate for playgrounds, sports surfaces, landscaping, and other such applications, as well as scrap steel.

Distribution and Markets

Our distribution channels include a variety of commercial distributors. In addition, we sell overhead bridge, jib, and gantry cranes and aluminum light rail systems, as well as certain motion technology products directly to end-users. The following describes our global distribution channels:

General Distribution Channels - Our global general distribution channels consist of:

— Industrial distributors that serve local or regional industrial markets and sell a variety of products for maintenance repair, operating, and production, or MROP, applications through their own direct sales force.

6

— | Rigging shops that are distributors with expertise in rigging, lifting, positioning, and load securing. Most rigging shops assemble and distribute chain, wire rope and synthetic slings, and distribute manual hoists and attachments, chain slings, and other products. |

— | Independent crane builders that design, build, install, and service overhead crane and light-rail systems for general industry and also distribute a wide variety of hoists and crane components. We sell electric wire rope hoists and chain hoists as well as crane components, such as end trucks, trolleys, drives, and electrification systems to crane builders. |

Specialty Distribution Channels - Our global specialty distribution channels consist of:

— | National and regional distributors that market a variety of MROP supplies, including material handling products, either exclusively through large, nationally distributed catalogs, or through a combination of catalog, internet, and branch sales and a field sales force. |

— | Material handling specialists and integrators that design and assemble systems incorporating hoists, overhead rail systems, trolleys, scissor lift tables, manipulators, air balancers, jib arms, and other material handling products to provide end-users with solutions to their material handling problems. |

— | Entertainment equipment distributors that design, supply, and install a variety of material handling and rigging equipment for concerts, theaters, ice shows, sporting events, convention centers, and night clubs. |

Pfaff International Direct - Our German-based Pfaff business markets and sells most of its actuators directly to end-users, providing an additional method to market for us in the European region.

Crane End-Users - We market and sell overhead bridge, jib and gantry cranes, parts and service to end-users through our wholly owned crane builder, Crane Equipment & Service, Inc. (“CES”). CES includes the Abell-Howe and Washington Equipment brands. CES designs, manufactures, installs, and services a variety of cranes with capacities up to 100 tons.

Service-After-Sale Distribution Channel - Service-after-sale distributors include our authorized network of 18 chain repair service stations and over 221 certified hoist service and repair stations globally. This service network is designed for easy parts and service access for our large installed base of hoists and related equipment in that region.

OEM/Government Distribution Channels - This channel consists of:

— | OEMs that supply various component parts directly to other industrial manufacturers as well as private branding and packaging of our traditional products for material handling, lifting, positioning, and special purpose applications. |

— | Government agencies, including the U.S. and Canadian Navies and Coast Guards, that primarily purchase load securing chain and forged attachments. We also provide our products to the U.S. and other governments for a variety of military applications. |

Independent Crane Builders and Engineering Procurement and Construction (EPC) firms - In addition to the Distribution channels mentioned above, STAHL sells explosion-protected hoists and custom engineered off-standard hoists to independent crane builders and EPC firms. Independent crane builders are lifting solution developers and final crane assemblers that source hoists as components. EPC firms are responsible for project management or construction management of production facilities that purchase lifting solutions from crane and hoist builders.

Backlog

Our backlog of orders at March 31, 2018 was approximately $177,387,000 compared to approximately $154,450,000 at March 31, 2017. Our orders for standard products are generally shipped within one week. Orders for products that are manufactured to customer specifications are generally shipped within four to twelve weeks. Given the short product lead times, we do not believe that the amount of our backlog of orders is a reliable indication of our future sales. Fluctuations in backlog can reflect the project oriented nature of certain aspects of our business.

7

Competitive Conditions

The material handling industry remains fragmented. We face competition from a wide range of regional, national, and international manufacturers globally. In addition, we often compete with individual operating units of larger, highly diversified companies.

The principal competitive factors affecting our business include customer service and support as well as product availability, performance, functionality, brand reputation, reliability, and price. Other important factors include distributor relationships and territory coverage.

We believe we have leading U.S. market share in various products categories including: hoists, trolleys and components, AC and DC material handling drives, screw jacks, tire shredders, and elevator DC drives. These product categories represent 64% of our U.S. net sales.

Major competitors for hoists are Konecranes, which acquired Terex's Material Handling and Part Solutions business segment, and Kito (and its U.S. subsidiary Harrington); for chain are Campbell Chain, Peerless Chain Company (acquired by Kito), and American Chain and Cable Company; for digital power control systems are Konecranes, Power Electronics International, Inc., Cattron Group International (a division of Laird Technologies), Conductix-Wampfler (a division of Delachaux Group), Control Techniques (a division of Emerson Electric), OMRON Corporation, KEB GmbH, and Fujitec; for forged attachments are The Crosby Group and Brewer Tichner Company; for cranes are Konecranes and a variety of independent crane builders; for actuators and rotary unions are Deublin, Joyce-Dayton, and Nook Industries; and for tire shredders, Granutech.

Employees

At March 31, 2018, we had 3,328 employees globally. Approximately 10% of our employees are represented under three separate U.S. or Canadian collective bargaining agreements which terminate at various times between May 2020 and September 2021. We also have various labor agreements with our non-U.S. employees which we negotiate from time to time. We have good relationships with our employees and positive, productive relationships with our unions. The risk of employee or union led disruption in production is remote.

Raw Materials and Components

Our principal raw materials and components are steel, consisting of structural steel, processed steel bar, forging bar steel, steel rod and wire, steel pipe and tubing and tool steel; electric motors; bearings; gear reducers; castings; steel and aluminum enclosures and wire harnesses; electro-mechanical components and standard variable drives. These commodities are all available from multiple sources. We purchase most of these raw materials and components from a limited number of strategic and preferred suppliers under long-term agreements which are negotiated on a company-wide basis through our global purchasing group to take advantage of volume discounts. We have historically passed on materials price increases to our channel partners and end-user customers. We continue to monitor our costs and reevaluate our pricing policies. Our ability to pass on these increases is determined by market conditions. Although raw materials and some components such as motors, bearings, gear reducers, steel and aluminum enclosures and wire harnesses, castings, electro-mechanical components, and standard variable drives are purchased, our vertical integration enables us to produce many of the components used in the manufacturing of our products.

Environmental and Other Governmental Regulation

Like most manufacturing companies, we are subject to various federal, state, and local laws relating to the protection of the environment. To address the requirements of such laws, we have adopted a corporate environmental protection policy which provides that all of our owned or leased facilities shall, and all of our employees have the duty to comply with all applicable environmental regulatory standards, and we have initiated an environmental auditing program for our facilities to ensure compliance with such regulatory standards. We have also established managerial responsibilities and internal communication channels for dealing with environmental compliance issues that may arise in the course of our business. We have made and could be required to continue to make significant expenditures to comply with environmental requirements. Because of the complexity and changing nature of environmental regulatory standards, it is possible that situations will arise from time to time requiring us to incur additional expenditures to ensure environmental regulatory compliance. However, we are not aware of any environmental condition or any operation at any of our facilities, either individually or in the aggregate, which would cause expenditures having a material adverse effect on our results of operations, financial condition or cash flows.

We notified the North Carolina Department of Environment and Natural Resources (the “DENR”) in April 2006 of the presence of certain contaminants in excess of regulatory standards at our facility in Wadesboro, North Carolina. We filed an application with the DENR to enter its voluntary cleanup program and the State accepted our proposal. We investigated under the supervision

8

of a DENR Registered Environmental Consultant (“the REC”) and have commenced voluntary clean-up at the facility. At this time, additional remediation costs are not expected to be material and are fully reserved.

We have been a part of the Pendleton Site PRP Group since about 1993. Many years ago, we sent pickle liquor wastes from Tonawanda, NY to the Pendleton Site for treatment and disposal. The Pendleton Site PRP Group signed an Order on Consent with the NYS DEC in 1996 and the cleanup was concluded in the early 2000s. The Order on Consent required a post-construction operation and maintenance period of 30 years and we are required to pay our share of the costs associated with the operation and maintenance period. The total annual costs are approximately $50,000 of which we pay 13.4% or $6,700. Reserves on the books are sufficient to cover these costs for the remainder of the operations and maintenance period.

Our subsidiary Magnetek has also been identified by the United States Environmental Protection Agency and certain state agencies as a potentially responsible party for cleanup costs associated with alleged past waste disposal practices at several previously utilized, owned or leased facilities and offsite locations. Its remediation activities as a potentially responsible party were not material in fiscal year 2018. Although the materiality of future expenditures for environmental activities may be affected by the level and type of contamination, the extent and nature of cleanup activities required by governmental authorities, the nature of Magnetek's alleged connection to the contaminated sites, the number and financial resources of other potentially responsible parties, the availability of indemnification rights against third parties and the identification of additional contaminated sites, Magnetek's estimated share of liability, if any, for environmental remediation, including its indemnification obligations, is not expected to be material.

In 1986, Magnetek acquired the stock of Universal Manufacturing Corporation (“Universal”) from a predecessor of Fruit of the Loom (“FOL”), and the predecessor agreed to indemnify Magnetek against certain environmental liabilities arising from pre-acquisition activities at a facility in Bridgeport, Connecticut. Environmental liabilities covered by the indemnification agreement included completion of additional cleanup activities, if any, at the Bridgeport facility and defense and indemnification against liability for potential response costs related to offsite disposal locations. Magnetek's leasehold interest in the Bridgeport facility was assigned to the buyer in connection with the sale of Magnetek's transformer business in June 2001. FOL, the successor to the indemnification obligation, filed a petition for Reorganization under Chapter 11 of the Bankruptcy Code in 1999 and Magnetek filed a proof of claim in the proceeding for obligations related to the environmental indemnification agreement. Magnetek believes that FOL had substantially completed the clean-up obligations required by the indemnification agreement prior to the bankruptcy filing. In November 2001, Magnetek and FOL entered into an agreement involving the allocation of certain potential tax benefits and Magnetek withdrew its claims in the bankruptcy proceeding. FOL's obligation to the state of Connecticut was not discharged in the reorganization proceeding.

In January 2007, the Connecticut Department of Environmental Protection (“DEP”) requested parties, including Magnetek, to submit reports summarizing the investigations and remediation performed to date at the site and the proposed additional investigations and remediation necessary to complete those actions at the site. The DEP then requested additional information relating to site investigations and remediation. Magnetek and the DEP agreed to the scope of the work plan in November 2010. The Company has implemented the work plan and has recorded a liability of $283,000 related to the Bridgeport facility, representing the best estimate of future site investigation costs and remediation costs which are expected to be incurred in the future.

In September of 2017, Magnetek received a request for defense and indemnification from Monsanto Company, Pharmacia, LLC, and Solutia, Inc. (collectively, “Monsanto”) with respect to: (1) lawsuits brought by plaintiffs claiming that Monsanto manufactured polychlorinated biphenyls ("PCBs"), exposure to which allegedly caused injury to plaintiffs; (2) lawsuits brought by municipalities and municipal entities claiming that Monsanto should be responsible for a variety of damages due to the presence of PCBs in bodies of water in those municipalities and/or in water treated by those municipal entities. Monsanto claims to be entitled to defense and indemnification from Magnetek under a so-called “Special Undertaking” apparently executed by Universal in January of 1972, which purportedly required Universal to defend and indemnify Monsanto from liabilities “arising out of or in connection with the receipt, purchase, possession, handling, use, sale or disposition of” PCBs by Universal.

Magnetek has declined Monsanto’s tender, and believes that it has meritorious legal and factual defenses to the demands made by Monsanto. Magnetek is vigorously defending against those demands and has commenced litigation to, among other things, declare the Special Undertaking void and unenforceable. Monsanto has, in turn, commenced an action to enforce the Special Undertaking. Magnetek intends to continue to vigorously prosecute its declaratory judgment action and to defend against Monsanto’s action against it. As of March 31, 2018 the Company has recorded $400,000 for legal costs incurred to date and expected to be incurred related to this matter. We cannot reasonably estimate a potential range of loss with respect to Monsanto’s tender because there is insufficient information regarding the underlying matters. Management believes, however, that the potential additional costs related to such matters, if any, will not have a material effect on the financial condition of the Company or its liquidity, although the effect of any future liabilities recorded could be material to earnings in a future period.

9

For all of the currently known environmental matters, we have accrued as of March 31, 2018 a total of $1,029,000 which, in our opinion, is sufficient to deal with such matters. Further, we believe that the environmental matters known to, or anticipated by us should not, individually or in the aggregate, have a material adverse effect on our operating results or financial condition. However, there can be no assurance that potential liabilities and expenditures associated with unknown environmental matters, unanticipated events, or future compliance with environmental laws and regulations will not have a material adverse effect on us.

Our operations are also governed by many other laws and regulations, including those relating to workplace safety and worker health, principally OSHA in the U.S. and others outside the U.S. and regulations thereunder. We believe that we are in substantial compliance with these laws and regulations and do not believe that future compliance with such laws and regulations will have a material adverse effect on our operating results, financial condition, or liquidity.

Available Information

Our internet address is www.cmworks.com. We make available free of charge through our website our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after such documents are electronically filed with, or furnished to, the Securities and Exchange Commission.

10

Item 1A. Risk Factors

Columbus McKinnon is subject to a number of risk factors that could negatively affect our results from business operations or cause actual results to differ materially from those projected or indicated in any forward looking statement. Such factors include, but are not limited to, the following:

Adverse changes in global economic conditions may negatively affect our industry, business, and results of operations.

Our industry is affected by changes in economic conditions outside our control, which can result in a general decrease in product demand from our customers. Such economic developments may affect our business in a number of ways. Reduced demand may drive us and our competitors to offer products at promotional prices, which would have a negative impact on our profitability. In addition, the tightening of credit in financial markets may adversely affect the ability of our customers and suppliers to obtain financing for significant purchases and operations and could result in a decrease in, or cancellation of, orders for our products. If demand for our products slows down or decreases, we will not be able to maintain our revenue and we may run the risk of failing to satisfy the financial and other restrictive covenants to which we are subject under our existing indebtedness. Reduced revenue as a result of decreased demand may also reduce our planned growth and otherwise hinder our ability to improve our performance in connection with our long term strategy.

Our business is cyclical and is affected by industrial economic conditions.

Many of the end-users of our products are in highly cyclical industries, such as manufacturing, power generation and distribution, commercial construction, oil and gas exploration and refining, transportation, agriculture, logging, and mining that are sensitive to changes in general economic conditions. Their demand for our products, and thus our results of operations, is directly related to the level of production in their facilities, which changes as a result of changes in general economic conditions and other factors beyond our control. If there is deterioration in the general economy or in the industries we serve, our business, results of operations, and financial condition could be materially adversely affected. In addition, the cyclical nature of our business could at times also adversely affect our liquidity and ability to borrow under our revolving credit facility.

Our business is highly competitive and subject to consolidation of competitors. Increased competition could reduce our sales, earnings, and profitability.

The principal markets that we serve within the material handling industry are fragmented and highly competitive. Competition is based primarily on customer service and support as well as product availability, performance, functionality, brand reputation, reliability, and price. Our competition in the markets in which we participate comes from companies of various sizes, some of which have greater financial and other resources than we do. Increased competition could force us to lower our prices or to offer additional services at a higher cost to us, which could reduce our gross margins and net income.

The greater financial resources or the lower amount of debt of certain of our competitors may enable them to commit larger amounts of capital in response to changing market conditions. Certain competitors may also have the ability to develop product or service innovations that could put us at a disadvantage. In addition, through consolidation, some of our competitors have achieved substantially more market penetration in certain of the markets in which we operate. If we are unable to compete successfully against other manufacturers of material handling equipment, we could lose customers and our revenues may decline. There can also be no assurance that customers will continue to regard our products favorably, that we will be able to develop new products that appeal to customers, that we will be able to improve or maintain our profit margins on sales to our customers or that we will be able to continue to compete successfully in our core markets.

The acquisition of STAHL on January 31, 2017 resulted in a significant increase to the Company’s long term borrowings.

The increased amount of long term borrowings could, among other things, require the Company to dedicate a large portion of its cash flow to the servicing and repayment of its outstanding indebtedness, thereby reducing funds available for other operating activities, which could adversely affect our financial condition and results of operations, and adversely affect our ability to pay dividends.

In connection with the acquisition of STAHL, we assumed an unfunded pension obligation which will further require cash flow to pay benefit obligations as they become due.

The STAHL pension obligation assumed in the acquisition is an unfunded pension plan valued at $85,851,000 at March 31, 2018. Therefore, the Company will be required to make current and future benefit payment obligations in addition to payments required to pay down other long term borrowings.

11

Our operations outside the U.S. pose certain risks that may adversely impact sales and earnings.

We have operations and assets located outside of the United States, primarily in China, Mexico, Germany, the United Kingdom, France, and Hungary. In addition, we import a portion of our hoist product line from Asia, and sell our products to distributors located in approximately 50 countries. In our fiscal year ended March 31, 2018, approximately 47% of our net sales were derived from non-U.S. markets. These non-U.S. operations are subject to a number of special risks, in addition to the risks of our U.S. business, differing protections of intellectual property, trade barriers, labor unrest, exchange controls, regional economic uncertainty, differing (and possibly more stringent) labor regulation, risk of governmental expropriation, U.S. and foreign customs and tariffs, current and changing regulatory environments, difficulty in obtaining distribution support, difficulty in staffing and managing widespread operations, differences in the availability, and terms of financing, political instability and risks of increases in taxes. Also, in some foreign jurisdictions we may be subject to laws limiting the right and ability of entities organized or operating therein to pay dividends or remit earnings to affiliated companies unless specified conditions are met. These factors may adversely affect our future profits.

Part of our strategy is to expand our worldwide market share and reduce costs by strengthening our international distribution capabilities and sourcing components in lower cost countries, in particular in China, Mexico, and Hungary. Implementation of this strategy may increase the impact of the risks described above, and we cannot assure you that such risks will not have an adverse effect on our business, results of operations or financial condition.

Our strategy depends on successful integration of acquisitions.

Acquisitions are a key part of our growth strategy. Our historical growth has depended, and our future growth is likely to depend on our ability to successfully implement our acquisition strategy, and the successful integration of acquired businesses into our existing business. We intend to continue to seek additional acquisition opportunities in accordance with our acquisition strategy, both to expand into new markets and to enhance our position in existing markets throughout the world. If we are unable to successfully integrate acquired businesses into our existing business or expand into new markets, our sales and earnings growth could be reduced.

Our products involve risks of personal injury and property damage, which exposes us to potential liability.

Our business exposes us to possible claims for personal injury or death and property damage resulting from the products that we sell. We maintain insurance through a combination of self-insurance retentions and excess insurance coverage. We monitor claims and potential claims of which we become aware and establish accrued liability reserves for the self-insurance amounts based on our liability estimates for such claims. We cannot give any assurance that existing or future claims will not exceed our estimates for self-insurance or the amount of our excess insurance coverage. In addition, we cannot give any assurance that insurance will continue to be available to us on economically reasonable terms or that our insurers would not require us to increase our self-insurance amounts. Claims brought against us that are not covered by insurance or that are in excess of insurance coverage could have a material adverse effect on our results, financial condition, or liquidity.

In addition, like many industrial manufacturers, we are also involved in asbestos-related litigation. In continually evaluating costs relating to our estimated asbestos-related liability, we review, among other things, the incidence of past and recent claims, the historical case dismissal rate, the mix of the claimed illnesses and occupations of the plaintiffs, our recent and historical resolution of the cases, the number of cases pending against us, the status and results of broad-based settlement discussions, and the number of years such activity might continue. Based on this review, we estimate our share of liability to defend and resolve probable asbestos related personal injury claims. This estimate is highly uncertain due to the limitations of the available data and the difficulty of forecasting with any certainty the numerous variables that can affect the range of the liability. We continue to study the variables in light of additional information in order to identify trends that may become evident and to assess their impact on the range of liability that is probable and estimable. We believe that the potential additional costs for claims will not have a material effect on the financial condition of the Company or its liquidity, although the effect of any future liabilities recorded could be material to earnings in a future period. See Note 15 to our March 31, 2018 consolidated financial statements included in Item 8 of this form 10K.

As indicated above, our self-insurance coverage is effected through our captive insurance subsidiary. The reserves of our captive insurance subsidiary are subject to periodic adjustments based upon actuarial evaluations, which adjustments impact our overall results of operations. These periodic adjustments can be favorable or unfavorable.

12

We are subject to currency fluctuations from our sales outside the U.S.

Our products are sold in many countries around the world. Thus, a portion of our revenues (approximately $395,986,000 in our fiscal year ended March 31, 2018) are generated in foreign currencies, including principally the Euro, the British Pound, the Canadian Dollar, the South African Rand, the Brazilian Real, the Mexican Peso, and the Chinese Yuan, and while much of the costs incurred to generate those revenues are incurred in the same currency, a portion is incurred in other currencies. Since our financial statements are denominated in U.S. dollars, changes in currency exchange rates between the U.S. dollar and other currencies have had, and will continue to have, a currency translation impact on our earnings. Currency fluctuations may impact our financial performance in the future.

Our future operating results may be affected by fluctuations in steel or other material prices. We may not be able to pass on increases in raw material costs to our customers.

The principal raw material used in our chain, forging and crane building operations is steel. The steel industry as a whole is highly cyclical, and at times pricing and availability can be volatile due to a number of factors beyond our control, including general economic conditions, labor costs, competition, import duties, tariffs, and currency exchange rates. This volatility can significantly affect our raw material costs. In an environment of increasing raw material prices, competitive conditions will determine how much of the steel price increases we can pass on to our customers. During historical rising cost periods, we were generally successful in adding and maintaining a surcharge to the prices of our high steel content products or incorporating them into price increases, with a goal of margin neutrality. In the future, to the extent we are unable to pass on any steel price increases to our customers, our profitability could be adversely affected.

We rely in large part on independent distributors for sales of our products.

For the most part, we depend on independent distributors to sell our products and provide service and aftermarket support to our end-user customers. Distributors play a significant role in determining which of our products are stocked at their locations, and hence are most readily accessible to aftermarket buyers, and the price at which these products are sold. Almost all of the distributors with whom we transact business offer competitive products and services to our end-user customers. For the most part, we do not have written agreements with our distributors. The loss of a substantial number of these distributors or an increase in the distributors' sales of our competitors' products to our ultimate customers could materially reduce our sales and profits.

We are subject to various environmental laws which may require us to expend significant capital and incur substantial cost.

Our operations and facilities are subject to various federal, state, local, and foreign requirements relating to the protection of the environment, including those governing the discharges of pollutants in the air and water, the generation, management and disposal of hazardous substances and wastes, and the cleanup of contaminated sites. We have made, and will continue to make, expenditures to comply with such requirements. Violations of, or liabilities under, environmental laws and regulations, or changes in such laws and regulations (such as the imposition of more stringent standards for discharges into the environment), could result in substantial costs to us, including operating costs and capital expenditures, fines and civil and criminal sanctions, third party claims for property damage or personal injury, clean-up costs, or costs relating to the temporary or permanent discontinuance of operations. Certain of our facilities have been in operation for many years, and we have remediated contamination at some of our facilities. Over time, we and other predecessor operators of such facilities have generated, used, handled, and disposed of hazardous and other regulated wastes. Additional environmental liabilities could exist, including clean-up obligations at these locations or other sites at which materials from our operations were disposed, which could result in substantial future expenditures that cannot be currently quantified and which could reduce our profits or have an adverse effect on our financial condition, operations, or liquidity.

We may face claims of infringement on the intellectual property of others, or others may infringe upon our intellectual property.

Our future success depends in part on our ability to prevent others from infringing on our proprietary rights, as well as our ability to operate without infringing upon the proprietary rights of others. We may be required at times to take legal action to protect our proprietary rights and, despite our best efforts, we may be sued for infringing on the patent rights of others. Patent litigation is costly and, even if we prevail, the cost of such litigation could adversely affect our financial condition. In addition, we could be adversely affected financially should we be judged to have infringed upon the intellectual property of others.

We rely on subcontractors or suppliers to perform their contractual obligations.

Some of our contracts involve subcontracts with other companies upon which we rely to perform a portion of the services we must provide to our customers. There is a risk that we may have disputes with our subcontractors, including disputes regarding the quality and timeliness of work performed by our subcontractor or customer concerns about the subcontractor. Failure by our

13

subcontractors to satisfactorily provide on a timely basis the agreed-upon supplies or perform the agreed upon services may materially and adversely impact our ability to perform our obligations as the prime contractor. A delay in our ability to obtain components and equipment parts from our suppliers may affect our ability to meet our customers' needs and may have an adverse effect upon our profitability.

We are subject to debt covenant restrictions.

Our revolving credit facility and Term Loan contain a financial leverage covenant and other restrictive covenants. A significant decline in our operating income or cash generating ability could cause us to violate our leverage ratio in our bank credit facility. Other material adverse changes in our business could cause us to be in default of our debt covenants. This could result in our being unable to borrow under our bank credit facility or being obliged to refinance and renegotiate the terms of our indebtedness.

Our business operations may be adversely affected by information systems interruptions or intrusion.

We depend on various information technologies throughout our company to administer, store, and support multiple business activities. If these systems are damaged, cease to function properly, or are subject to cyber-security attacks, such as those involving unauthorized access, malicious software and/or other intrusions, we could experience production downtimes, operational delays, other detrimental impacts on our operations or ability to provide products and services to our customers, the compromising of confidential or otherwise protected information, destruction or corruption of data, security breaches, other manipulation or improper use of our systems or networks, financial losses from remedial actions, loss of business or potential liability, and/or damage to our reputation. While we attempt to mitigate these risks by employing a number of measures, including employee training, technical security controls, and maintenance of backup and protective systems, our systems, networks, products, and services remain potentially vulnerable to known or unknown threats, any of which could have a material adverse affect on our business, financial condition or results of operations.

We depend on our senior management team and the loss of any member could adversely affect our operations.

Our success is dependent on the management and leadership skills of our senior management team. The loss of any of these individuals or an inability to attract, retain, and maintain additional personnel could prevent us from implementing our business strategy. We cannot assure you that we will be able to retain our existing senior management personnel or to attract additional qualified personnel when needed.

We continually evaluate and assess our personnel and may make additional changes to the members or assignments of our senior management team in the future.

We have entered into employment agreements with the following senior management personnel: Werner Wagner (our STAHL Managing Director) and Mark D. Morelli (our President and CEO).

Item 1B. Unresolved Staff Comments

None.

14

Item 2. Properties

We maintain our corporate headquarters in Getzville, New York (an owned property) and, as of March 31, 2018, conducted our principal manufacturing at the following facilities:

Location | Products/Operations | Square Footage | Owned or Leased | ||||||

1 | Kunzelsau, Germany | Hoists | 345,000 | Leased | |||||

2 | Wadesboro, NC | Hoists | 180,000 | Owned | |||||

3 | Lexington, TN | Chain | 164,000 | Owned | |||||

4 | Asia operation: | ||||||||

Hangzhou, China | Hoists | 70,000 | Owned | ||||||

Hangzhou, China | Hoists | 82,000 | Owned | ||||||

5 | Charlotte, NC | Actuators and Rotary Unions | 146,000 | Leased | |||||

6 | Menomonee Falls, WI | Power control systems | 144,000 | Leased | |||||

7 | Tennessee forging operation: | ||||||||

Chattanooga, TN | Forged attachments | 81,000 | Owned | ||||||

Chattanooga, TN | Forged attachments | 59,000 | Owned | ||||||

8 | Wuppertal, Germany | Hoists | 124,000 | Leased | |||||

9 | Kissing, Germany | Hoists, winches, and actuators | 107,000 | Leased | |||||

10 | Damascus, VA | Hoists | 97,000 | Owned | |||||

11 | Eureka, IL | Cranes | 91,000 | Owned | |||||

12 | Ohio hoist operation: | ||||||||

Salem, OH | Hoists | 49,000 | Leased | ||||||

Lisbon, OH | Hoists | 37,000 | Owned | ||||||

13 | Hamm, Germany | Lifting tools and forged parts | 82,000 | Owned | |||||

14 | Chester, England | Plate clamps | 56,000 | Owned | |||||

15 | Santiago Tianguistenco, Mexico | Hoists | 54,000 | Owned | |||||

16 | Howell, MI | Overhead light rail workstations | 35,000 | Leased | |||||

17 | Sarasota, FL | Tire shredders | 25,000 | Owned | |||||

18 | Szekesfehervar, Hungary | Textiles and textile strappings | 24,000 | Leased | |||||

19 | Romeny-sur-Marne, France | Rotary unions | 22,000 | Owned | |||||

In addition, we have a total of 45 sales offices, distribution centers, and warehouses. We believe that our properties have been adequately maintained, are in generally good condition and are suitable for our business as presently conducted. We also believe our existing facilities provide sufficient production capacity for our present needs and for our anticipated needs in the foreseeable future. Upon the expiration of our current leases, we believe that either we will be able to secure renewal terms or enter into leases for alternative locations at market terms.

15

Item 3. Legal Proceedings

From time to time, we are named a defendant in legal actions arising out of the normal course of business. We are not a party to any pending legal proceeding other than ordinary, routine litigation incidental to our business. We do not believe that any of our pending litigation will have a material impact on our business. We maintain comprehensive general product liability insurance against risks arising out of the use of our products sold to customers through our wholly-owned New York State captive insurance subsidiary of which we are the sole policy holder. The per occurrence limits on the self-insurance for general and product liability coverage were $2,000,000 from inception through fiscal 2003 and $3,000,000 for fiscal 2004 and thereafter. In addition to the per occurrence limits, our coverage is also subject to an annual aggregate limit, applicable to losses only. These limits range from $2,000,000 to $6,000,000 for each policy year from inception through fiscal 2018. We obtain additional insurance coverage from independent insurers to cover potential losses in excess of these limits.

Like many industrial manufacturers, we are also involved in asbestos-related litigation. In continually evaluating costs relating to our estimated asbestos-related liability, we review, among other things, the incidence of past and recent claims, the historical case dismissal rate, the mix of the claimed illnesses and occupations of the plaintiffs, our recent and historical resolution of the cases, the number of cases pending against us, the status and results of broad-based settlement discussions, and the number of years such activity might continue. Because this liability is likely to extend over many years, management believes that the potential additional costs for claims will not have a material effect on the financial condition of the Company or its liquidity, although the effect of any future liabilities recorded could be material to earnings in a future period.

The Company believes that a share of its previously incurred asbestos-related expenses and future asbestos-related expenses are covered by pre-existing insurance policies. The Company has engaged in a legal action against the insurance carriers of those policies to recover past expenses and to recover future costs incurred. The Company recovered $2,362,000 from insurance carriers during fiscal 2018. When the Company resolves this legal action, it is expected that an additional gain will be recorded for previously expensed cost that is recovered.

See Note 15 to our March 31, 2018 consolidated financial statements for more information on our matters involving litigation.

Item 4. Mine Safety Disclosures.

Not Applicable.

16

PART II

Item 5. Market for the Company’s Common Stock and Related Security Holder Matters

Our common stock is traded on the Nasdaq Global Select Market under the symbol ‘‘CMCO.” As of April 30, 2018, there were 381 holders of record of our common stock.

During fiscal 2018, the Company declared quarterly cash dividends totaling $3,903,000. On March 26, 2018, the Company's Board of Directors declared regular quarterly dividends of $0.05 per common share. The dividend was paid on May 14, 2018 to shareholders of record on May 4, 2018 and totaled approximately $1,150,000.

Our current credit agreement allows, but limits our ability to pay dividends.

The following table sets forth, for the fiscal periods indicated, the high and low sale prices per share for our common stock as reported on the Nasdaq Global Select Market.

Price Range of Common Stock | ||||||||

Year Ended March 31, 2017 | High | Low | ||||||

First Quarter | $ | 17.05 | $ | 13.93 | ||||

Second Quarter | 18.54 | 14.34 | ||||||

Third Quarter | 27.59 | 17.18 | ||||||

Fourth Quarter | 28.63 | 24.05 | ||||||

Year Ended March 31, 2018 | ||||||||

First Quarter | $ | 28.98 | $ | 23.54 | ||||

Second Quarter | 37.74 | 24.12 | ||||||

Third Quarter | 40.20 | 36.18 | ||||||

Fourth Quarter | 44.31 | 34.60 | ||||||

On May 25, 2018 the closing price of our common stock on the Nasdaq Global Select Market was $37.75 per share.

17

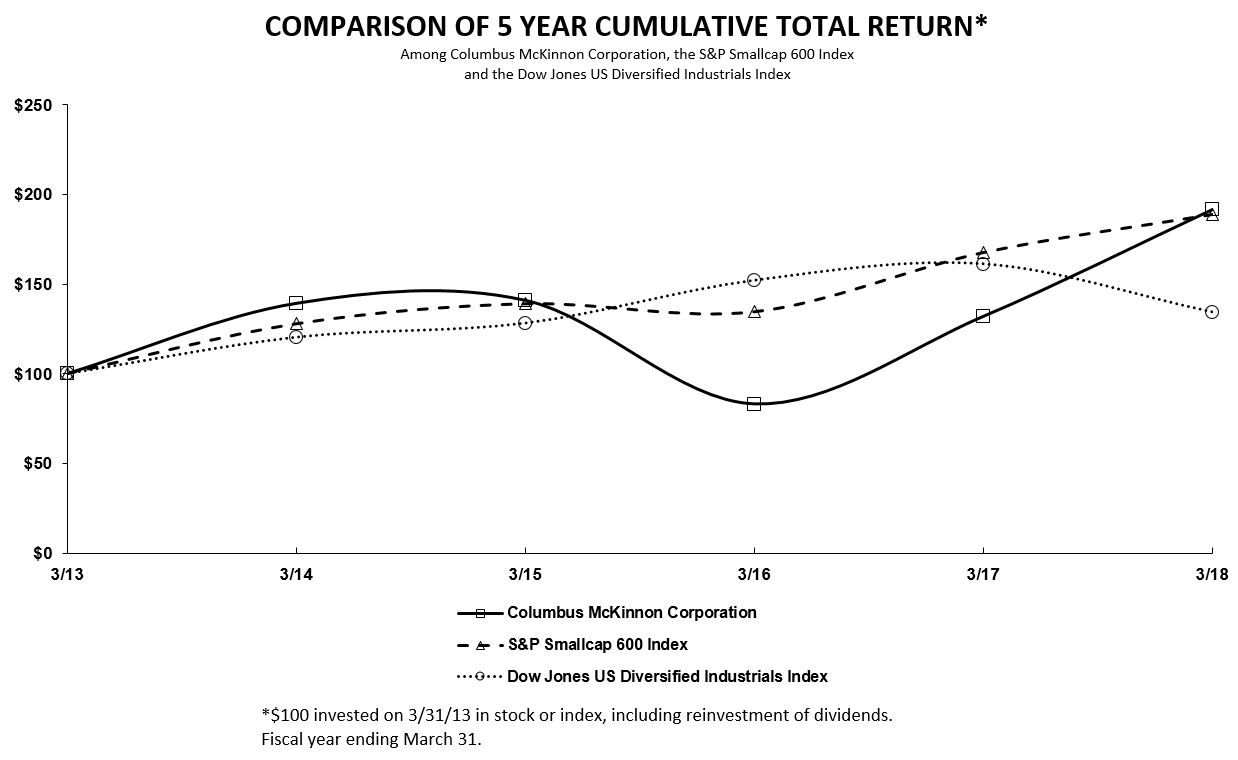

PERFORMANCE GRAPH

The Performance Graph shown below compares the cumulative total shareholder return on our common stock based on its market price, with the total return of the S&P SmallCap 600 Index, and the Dow Jones U.S. Diversified Industrials. The comparison of total return assumes that a fixed investment of $100 was invested on March 31, 2013 in our common stock and in each of the foregoing indices and further assumes the reinvestment of dividends. The stock price performance shown on the graph is not necessarily indicative of future price performance.

18

Item 6. Selected Financial Data

The consolidated balance sheets as of March 31, 2018 and 2017, and the related statements of operations, cash flows, and shareholders’ equity for each of the three years ended March 31, 2018 and notes thereto appear elsewhere in this annual report. The selected consolidated financial data presented below should be read in conjunction with, and are qualified in their entirety by “Management’s Discussion and Analysis of Results of Operations and Financial Condition,” our consolidated financial statements and the notes thereto and other financial information included elsewhere in this annual report.

(In million's, except per share data) | ||||||||||||||||||||

2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

Statements of Operations Data: | ||||||||||||||||||||

Net sales | $ | 839.4 | $ | 637.1 | $ | 597.1 | $ | 579.6 | $ | 583.3 | ||||||||||

Cost of products sold | 554.8 | 444.2 | 409.8 | 398.0 | 402.2 | |||||||||||||||

Gross profit | 284.6 | 192.9 | 187.3 | 181.6 | 181.1 | |||||||||||||||

Selling expenses | 102.0 | 77.3 | 72.9 | 69.8 | 69.0 | |||||||||||||||

General and administrative expenses (1) | 83.4 | 69.9 | 61.4 | 49.7 | 50.3 | |||||||||||||||

Research and development expenses (1) | 13.6 | 10.5 | 7.4 | 5.2 | 5.5 | |||||||||||||||

Impairment of intangible asset | — | 1.1 | — | — | — | |||||||||||||||

Amortization of intangibles | 15.6 | 8.1 | 5.0 | 2.3 | 2.0 | |||||||||||||||

Income (loss) from operations | 70.0 | 26.0 | 40.6 | 54.6 | 54.3 | |||||||||||||||

Interest and debt expense | 19.7 | 11.0 | 7.9 | 12.4 | 13.5 | |||||||||||||||

Cost of debt refinancing | — | 1.3 | — | 8.6 | — | |||||||||||||||

Other (income) and expense, net | 0.6 | 0.7 | 1.1 | (2.4 | ) | (1.9 | ) | |||||||||||||

Income (loss) before income taxes | 49.7 | 13.0 | 31.6 | 36.0 | 42.7 | |||||||||||||||

Income tax expense (benefit) | 27.6 | 4.0 | 12.0 | 8.8 | 12.3 | |||||||||||||||

Net income (loss) | $ | 22.1 | $ | 9.0 | $ | 19.6 | $ | 27.2 | $ | 30.4 | ||||||||||

Diluted earnings (loss) per share from continuing operations | $ | 0.95 | $ | 0.43 | $ | 0.96 | $ | 1.34 | $ | 1.52 | ||||||||||

Basic earnings (loss) per share from continuing operations | $ | 0.97 | $ | 0.44 | $ | 0.98 | $ | 1.36 | $ | 1.55 | ||||||||||

Weighted average shares outstanding – assuming dilution | 23.3 | 20.9 | 20.3 | 20.2 | 20.0 | |||||||||||||||

Weighted average shares outstanding – basic | 22.8 | 20.6 | 20.1 | 19.9 | 19.7 | |||||||||||||||

Balance Sheet Data (at end of period): | ||||||||||||||||||||

Total assets | $ | 1,142.4 | $ | 1,113.8 | $ | 772.9 | $ | 566.1 | $ | 596.9 | ||||||||||

Total debt (2) | 363.3 | 421.3 | 267.6 | 126.5 | 150.5 | |||||||||||||||

Total debt, net of cash and cash equivalents | 300.3 | 343.7 | 216.0 | 63.5 | 38.2 | |||||||||||||||

Total shareholders’ equity | 408.2 | 341.4 | 286.3 | 268.7 | 291.3 | |||||||||||||||

Other Data: | ||||||||||||||||||||

Net cash provided by operating activities | 69.7 | 60.5 | 52.6 | 38.3 | 29.5 | |||||||||||||||

Net cash used in investing activities | (32.3 | ) | (224.0 | ) | (203.2 | ) | (34.1 | ) | (40.4 | ) | ||||||||||

Net cash provided by (used in) financing activities | (59.5 | ) | 190.1 | 137.0 | (48.4 | ) | 1.7 | |||||||||||||

Capital expenditures | (14.5 | ) | (14.4 | ) | (22.3 | ) | (17.2 | ) | (20.8 | ) | ||||||||||

19

(1) | For its fiscal 2018 financial statements, the Company has reclassified research and development expenses previously recorded in general and administrative expense into a separate line item on the consolidated statements of operations. All periods presented above have been revised to reflect this presentation. Please refer to Note 2 of the Company's financial statements for additional information regarding research and development expenses. |

(2) | Total debt includes all debt, including the current portion, notes payable, term loan, and subordinated debt. |

20

Item 7. Management’s Discussion and Analysis of Results of Operations and Financial Condition

This section should be read in conjunction with our consolidated financial statements included elsewhere in this annual report.

EXECUTIVE OVERVIEW

We are a leading worldwide designer, manufacturer, and marketer of material handling products, systems and services which efficiently and safely move, lift, position, and secure materials. Key products include hoists, rigging tools, cranes, digital power control systems, and actuators. We are focused on serving commercial and industrial applications that require the safety and quality in moving material provided by our superior design and engineering know-how.

Founded in 1875, we have grown to our current size and leadership position through organic growth and acquisitions. We developed our leading market position over our 143-year history by emphasizing technological innovation, manufacturing excellence and superior after-sale service. In addition, acquisitions significantly broadened our product lines and services and expanded our geographic reach, end-user markets and customer base. Ongoing initiatives to increase earnings power include operational excellence and profitable growth. In accordance with Blueprint 2021, we are simplifying the business structure and product platforms, improving operating performance, and focusing our R&D expenditures to grow profitably. Shareholder value will be enhanced by expanding EBITDA margins and return on invested capital (ROIC).

On January 31, 2017 we completed our acquisition of STAHL. STAHL is a leading manufacturer of explosion-protected hoists and crane components and is well known for providing lifting solutions utilizing its custom engineering and hoisting technology. STAHL serves independent crane builders and Engineering Procurement and Construction (EPC) firms, providing products to a variety of end markets including oil and gas, automotive, general manufacturing, steel & concrete, power generation as well as process industries such as chemical and pharmaceuticals. We believe STAHL is an excellent expansion of our global product offering. STAHL's strong position with wire rope and electric chain hoists in Europe immediately complements our leadership position in handheld hoists in that region, and their broad portfolio of ATEX certified explosion-protected products serving the oil and gas, mining, and chemical processing industries significantly extends our global offerings in capability and capacities.

Our revenue base is geographically diverse with approximately 47% derived from customers outside the U.S. for the year ended March 31, 2018. Our expansion within the European market with the acquisition of STAHL further expands our geographic diversity. We believe this will help balance the impact of changes that will occur in local economies, as well as benefit the Company from growth in emerging markets. We monitor both U.S. and Eurozone Industrial Capacity Utilization statistics as indicators of anticipated demand for our products. In addition, we continue to monitor the potential impact of other global and U.S. trends including industrial production, energy costs, steel price fluctuations, interest rates, foreign currency exchange rates, and activity of end-user markets around the globe.

From a strategic perspective, we are leveraging our recent acquisitions and investing in new products as we focus on our greatest opportunities for growth. We maintain a strong North American market share with significant leading market positions in hoists, lifting, and sling chain, forged attachments, actuators, and digital power and motion control systems for the material handling industry. We seek to maintain and enhance our market share by focusing our sales and marketing activities toward select North American and global market sectors including general industrial, energy, automotive, heavy OEM, entertainment, and construction and infrastructure.

Regardless of the economic climate and point in the economic cycle, we constantly explore ways to increase operating margins as well as further improve our productivity and competitiveness. We have specific initiatives related to improved customer satisfaction, reduced defects, shortened lead times, improved inventory turns and on-time deliveries, reduced warranty costs, and improved working capital utilization. The initiatives are being driven by the implementation of our operating system E-PAS™. We are working to achieve these strategic initiatives through product simplification, the creation of centers of excellence, and improved supply chain management. We are also pursuing cost reduction opportunities to enhance future margins.

We continuously monitor market prices of steel. We purchase approximately $25,000,000 to $30,000,000 of steel annually in a variety of forms including rod, wire, bar, structural, and other forms of steel. Generally, as we experience fluctuations in our costs, we reflect them as price increases or surcharges to our customers with the goal of being margin neutral.

We operate in a highly competitive and global business environment. We face a variety of opportunities in those markets and geographies, including trends toward increasing productivity of the global labor force and the expansion of market opportunities in Asia and other emerging markets. While we execute our long-term growth strategy, we are supported by our solid free cash flow as well as our liquidity position and flexible debt structure.

21

RESULTS OF OPERATIONS

Fiscal 2018 Compared to 2017

Fiscal 2018 sales were $839,419,000, an increase of 31.8%, or $202,296,000 compared with fiscal 2017 sales of $637,123,000. Sales for the year were positively impacted by $144,670,000 due to our acquisition of STAHL, $40,993,000 due to an increase in sales volume, and $2,529,000 by price increases. Favorable foreign currency translation increased sales by $14,104,000.

Our gross profit was $284,574,000 and $192,932,000 or 33.9% and 30.3% of net sales in fiscal 2018 and 2017, respectively. The fiscal 2018 increase in gross profit of $91,642,000 or 47.5% is the result of $53,794,000 from the acquisition of STAHL, $4,828,000 in increased productivity and favorable manufacturing costs, $1,361,000 of price increases net of material inflation, $13,227,000 in increased volume, $2,964,000 in decreased product liability costs, $8,852,000 in STAHL inventory amortization related to purchase accounting adjustments incurred in fiscal 2017 that did not reoccur in fiscal 2018, a $2,362,000 increase due to an insurance settlement, offset by $307,000 in STAHL integration costs that are classified as cost of products sold. The translation of foreign currencies had a $4,561,000 favorable impact on gross profit for the year ended March 31, 2018.

Selling expenses were $101,956,000 and $77,319,000, or 12.1% of net sales in fiscal years 2018 and 2017. STAHL contributed an additional $18,396,000 in selling expense and $616,000 of integration costs were incurred related to the acquisition of STAHL that are classified as selling expense, offset by $247,000 in expense that did not reoccur related to the Canadian lump sum pension settlement in the year ended March 31, 2018. The remainder of the increase is largely due to the increase in sales volume, additional marketing expenses, and the transition to a new warehouse in North America. Additionally, foreign currency translation had a $2,151,000 unfavorable impact on selling expenses.

General and administrative expenses were $83,350,000 and $69,928,000 or 9.9% and 11.0% of net sales in fiscal 2018 and 2017, respectively. The fiscal 2018 increase was primarily the result of the STAHL acquisition which added $9,477,000 in recurring general and administrated expenses and $7,840,000 of integration costs were incurred related to the acquisition of STAHL that are classified as general and administrative expense, offset by $8,815,000 in STAHL related acquisition and integration costs incurred in the year ended March 31, 2017. Additionally, $1,589,000 in net legal costs were incurred for a legal action against our product liability insurance carriers, $400,000 in expected litigation costs for a former subsidiary of Magnetek, $619,000 in debt repricing fees, offset by CEO retirement and search costs of $3,085,000 that did not reoccur in fiscal 2018. The remainder of the increase is largely due to higher annual incentive plan costs expected in fiscal 2018 compared to fiscal 2017. Foreign currency translation had a $1,178,000 unfavorable impact on general and administrative expenses.