Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

|

☑

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

|

|

For the quarterly period ended March 31, 2018

|

or

|

☐

|

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

|

For the transition period from __________________ to

__________________

Commission file number: 000-54887

Bright Mountain Media, Inc.

(Exact name of registrant as specified in its charter)

|

Florida

|

27-2977890

|

|

(State or other jurisdiction of incorporation or

organization)

|

(I.R.S. Employer Identification No.)

|

|

6400 Congress Avenue, Suite 2050, Boca Raton, Florida

|

33487

|

|

(Address of principal executive offices)

|

(Zip Code)

|

|

561-998-2440

|

|

(Registrant's telephone number, including area code)

|

|

not applicable

|

|

(Former name, former address and former fiscal

year, if changed since last report)

|

Indicate by check mark whether the registrant (1)

has filed all reports required to be filed by Section 13 or 15(d)

of the Securities Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing

requirements for the past 90 days. ☑ Yes ☐ No

Indicate by check mark whether the registrant has

submitted electronically and posted on its corporate Website, if

any, every Interactive Data File required to be submitted and

posted pursuant to Rule 405 of Regulation S-T (§232.405 of

this chapter) during the preceding 12 months (or for such shorter

period that the registrant was required to submit and post such

files). ☑ Yes ☐ No

Indicate

by check mark whether the registrant is a large accelerated filer,

an accelerated filer, a non-accelerated filer, smaller reporting

company, or an emerging growth company. See the definitions of

“large accelerated filer,” “accelerated

filer,” “smaller reporting company,” and

“emerging growth company” in Rule 12b-2 of the Exchange

Act.

|

Large accelerated filer

|

☐

|

Accelerated filer

|

☐

|

|

Non-accelerated filer

|

☐

|

Smaller reporting company

|

☑

|

|

|

|

Emerging growth company

|

☑

|

If an emerging growth company, indicate by

checkmark if the registrant has elected not to use the extended

transition period for complying with any new or revised financial

accounting standards provided pursuant to Section 13(a) of the

Exchange Act. ☐

Indicate by check mark whether the registrant is a

shell company (as defined in Rule 12b-2 of the Exchange

Act) ☐ Yes ☑ No

As

of May15, 2018 the issuer had 47,941,364 shares of its common stock

outstanding.

TABLE OF CONTENTS

|

|

|

Page No.

|

|

|

PART I - FINANCIAL INFORMATION

|

|

|

|

|

|

|

ITEM 1.

|

FINANCIAL STATEMENTS.

|

4

|

|

|

|

|

|

ITEM 2.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS.

|

|

|

|

|

|

|

ITEM 3.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET

RISK.

|

29

|

|

|

|

|

|

ITEM 4.

|

CONTROLS AND PROCEDURES.

|

29

|

|

|

|

|

|

|

PART II - OTHER INFORMATION

|

|

|

|

|

|

|

ITEM 1.

|

LEGAL PROCEEDINGS.

|

31

|

|

|

|

|

|

ITEM 1A.

|

RISK FACTORS.

|

31

|

|

|

|

|

|

ITEM 2.

|

UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF

PROCEEDS.

|

31

|

|

|

|

|

|

ITEM 3.

|

DEFAULTS UPON SENIOR SECURITIES.

|

31

|

|

|

|

|

|

ITEM 4.

|

MINE SAFETY DISCLOSURES.

|

31

|

|

|

|

|

|

ITEM 5.

|

OTHER INFORMATION.

|

31

|

|

|

|

|

|

ITEM 6.

|

EXHIBITS.

|

33

|

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING

INFORMATION

Various

statements in this report contain or may contain forward-looking

statements that are subject to known and unknown risks,

uncertainties and other factors which may cause actual results,

performance or achievements to be materially different from any

future results, performance or achievements expressed or implied by

such forward-looking statements. These forward-looking statements

were based on various factors and were derived from utilizing

numerous assumptions and other factors that could cause our actual

results to differ materially from those in the forward-looking

statements. These factors include, but are not limited

to:

●

our

history of losses and our ability to raise additional capital and

continue as a going concern;

●

our

ability to successfully integrate the operations of the Black

Helmet Apparel business;

●

our

ability to successfully integrate the Daily Engage Media

acquisition and fully develop the Bright Mountain Media Ad Network

and services platform;

●

a

failure to successfully transition to primarily advertising based

revenue model;

●

the

impact of seasonal fluctuations on our revenues;

●

once

established, our failure to detect advertising fraud;

●

our

dependence on our relationships with Amazon and

PayPal;

●

our

dependence on a limited number of vendors;

●

our

dependence on our relationship with Google AdSense;

●

acquisitions

of new businesses and our ability to integrate those businesses

into our operations;

●

online

security breaches;

●

failure

to effectively promote our brand;

●

our

ability to protect our content;

●

our

ability to protect our intellectual property rights and our

proprietary content;

●

the

success of our technology development efforts;

●

additional

competition resulting from our business expansion

strategy;

●

liability

related to content which appears on our websites;

●

regulatory

risks;

●

dependence

on executive officers and certain key employees and

consultants;

●

our

ability to hire qualified personnel;

●

third

party content;

●

possible

problems with our network infrastructure;

●

the

historic illiquid nature of our common stock;

●

risks

associated with securities litigation;

●

material

weaknesses in our internal control over financial

reporting;

●

the

lack of cash dividends on our common stock;

●

provisions

of our charter and Florida law which may have anti-takeover

effects;

●

control

of our company by our management; and

●

the

dilutive effect of conversion of our 10% Series A and Series E

convertible preferred stock and/or the payment of stock and cash

dividends on those shares to our common shareholders.

Most

of these factors are difficult to predict accurately and are

generally beyond our control. You should consider the areas of risk

described in connection with any forward-looking statements that

may be made herein. Readers are cautioned not to place undue

reliance on these forward-looking statements and readers should

carefully review this report, our Annual Report on Form 10-K for

the year ended December 31, 2017, as filed with the Securities and

Exchange Commission on April 2, 2018 and our other filings with the

Securities and Exchange Commission in their entirety. Except for

our ongoing obligations to disclose material information under the

Federal securities laws, we undertake no obligation to release

publicly any revisions to any forward-looking statements, to report

events or to report the occurrence of unanticipated events. These

forward-looking statements speak only as of the date of this

report, and you should not rely on these statements without also

considering the risks and uncertainties associated with these

statements and our business.

OTHER PERTINENT INFORMATION

Unless

specifically set forth to the contrary, when used in this report

the terms “Bright Mountain”, the “Company,”

“we”, “us”, “our” and similar

terms refer to Bright Mountain Media, Inc., a Florida corporation,

and its subsidiaries, and "Daily Engage Media" refers to Daily

Engage Media Group LLC, a New Jersey limited liability company and

wholly owned subsidiary of the Company. In addition, when used in

this report, “first quarter of 2018” refers to the

three months ended March 31, 2018, "first quarter of 2017" refers

to the three months ended March 31, 2017, “2018” refers

to the year ending December 31, 2018 and “2017” refers

to the year ended December 31, 2017.

Unless specifically set forth to the contrary, the

information which appears on our website at www.brightmountainmedia.com is not part of this

report.

3

PART 1 - FINANCIAL INFORMATION

ITEM

1.

FINANCIAL

STATEMENTS.

BRIGHT MOUNTAIN MEDIA, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

|

|

March

31,

|

December

31,

|

|

|

2018

|

2017

|

|

|

(unaudited)

|

|

|

ASSETS

|

|

|

|

Current assets

|

|

|

|

Cash

and Cash Equivalents

|

$166,267

|

$140,022

|

|

Accounts

Receivable, net

|

878,879

|

879,770

|

|

Inventories,

net

|

511,925

|

611,468

|

|

Prepaid

Expenses and Other Current Assets

|

109,001

|

145,732

|

|

Total current

assets

|

1,666,072

|

1,776,992

|

|

Property and Equipment, net

|

84,186

|

89,500

|

|

Website

Acquisition Assets, net

|

332,795

|

393,417

|

|

Intangible

Assets, net

|

915,673

|

967,774

|

|

Goodwill

|

446,426

|

446,426

|

|

Other

Assets

|

46,588

|

44,608

|

|

Total Assets

|

$3,491,740

|

$3,718,717

|

|

|

|

|

|

LIABILITIES

AND SHAREHOLDERS' EQUITY

|

|

|

|

Current Liabilities

|

|

|

|

Accounts

Payable

|

$1,098,766

|

$1,172,827

|

|

Accrued

Expenses

|

85,185

|

90,000

|

|

Premium

Finance Loan Payable

|

40,909

|

63,133

|

|

Deferred

Rent - Short Term

|

3,779

|

2,468

|

|

Deferred

Revenues

|

8,236

|

9,735

|

|

Long Term Debt, Current Portion

|

769,527

|

767,071

|

|

Total Current

Liabilities

|

2,006,402

|

2,105,234

|

|

|

|

|

|

Long

term Deferred Rent

|

15,184

|

16,418

|

|

Long

Term Debt to Related Parties, net

|

1,249,100

|

1,198,893

|

|

Long

Term Debt, net

of current portion

|

-

|

54,950

|

|

Total Liabilities

|

3,270,686

|

3,375,495

|

|

Commitments and contingencies

|

|

|

|

Shareholders' Equity

|

|

|

|

Preferred

Stock, par value $0.01, 20,000,000 shares authorized,

|

|

|

|

600,000

and 100,000 shares issued and outstanding

|

|

|

|

Series

A, 2,000,000 shares designated, 100,000 and

|

|

|

|

100,000

shares issued and outstanding

|

1,000

|

1,000

|

|

Series

B, 1,000,000 shares designated, 0 and

|

|

|

|

0

shares issued and outstanding

|

—

|

—

|

|

Series

C, 2,000,000 shares designated, 0 and

|

|

|

|

0

shares issued and outstanding

|

—

|

—

|

|

Series

D, 2,000,000 shares designated, 0 and

|

|

|

|

0

shares issued and outstanding

|

—

|

—

|

|

Series

E, 2,500,000 shares designated, 1,875,000 and

|

|

|

|

1,375,000

issued and outstanding

|

18,750

|

13,750

|

|

Common

Stock, par value $0.01, 324,000,000 shares authorized,

|

|

|

|

47,941,364

and 44,901,531 issued and outstanding

|

479,414

|

461,689

|

|

Additional

Paid-in Capital

|

12,585,594

|

11,685,685

|

|

Accumulated

Deficit

|

(12,863,704)

|

(11,818,902)

|

|

Total

Shareholders' Equity

|

221,054

|

343,222

|

|

Total Liabilities and Shareholders' Equity

|

$3,491,740

|

$3,718,717

|

See accompanying notes to unaudited condensed consolidated

financial statements

4

BRIGHT MOUNTAIN MEDIA, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

|

|

For the Three Months Ended

|

|

|

|

March 31,

|

|

|

|

2018

|

2017

|

|

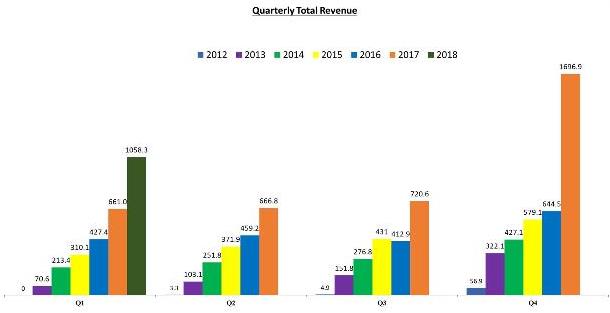

Revenues

|

|

|

|

Product

|

$375,286

|

$551,355

|

|

Advertising

|

683,058

|

109,743

|

|

Total

revenues

|

1,058,344

|

661,098

|

|

|

|

|

|

Cost

of revenue

|

|

|

|

Products

|

291,565

|

372,546

|

|

Advertising

|

510,704

|

3,510

|

|

Total

Cost of revenue

|

802,269

|

376,056

|

|

Gross

profit

|

256,075

|

285,042

|

|

|

|

|

|

Selling,

general and administrative expenses

|

1,185,954

|

884,203

|

|

|

|

|

|

Loss

from operations

|

(929,879)

|

(599,161)

|

|

|

|

|

|

Other

income (expense)

|

|

|

|

Interest

income

|

288

|

82

|

|

Interest

expense

|

(15,353)

|

(35,160)

|

|

Interest

expense - related party

|

(99,858)

|

(49,008)

|

|

Total

other income (expense)

|

(114,923)

|

(84,086)

|

|

|

|

|

|

|

|

|

|

Net

Loss

|

(1,044,802)

|

(683,247)

|

|

|

|

|

|

Preferred

stock dividends

|

|

|

|

Series

A and Series E preferred stock

|

14,763

|

1,973

|

|

|

|

|

|

Net

loss attributable to common shareholders

|

$(1,059,565)

|

$(685,220)

|

|

|

|

|

|

|

|

|

|

Basic

and diluted net loss per share

|

$(0.02)

|

$(0.02)

|

|

|

|

|

|

Weighted

average shares O/S - basic and diluted

|

45,807,289

|

44,913,531

|

See accompanying notes to unaudited condensed consolidated

financial statements

5

BRIGHT MOUNTAIN MEDIA, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGE IN SHAREHOLDERS'

EQUITY

For the Three months ended March 31, 2018

(Unaudited)

|

|

|

|

|

|

Additional

|

|

Total

|

|

|

Preferred Stock

|

Common Stock

|

Paid-in

|

Accumulated

|

Shareholders'

|

||

|

|

Shares

|

Amount

|

Shares

|

Amount

|

Capital

|

Deficit

|

Equity

|

|

Balance -

December 31, 2017

|

1,475,000

|

$14,750

|

46,168,864

|

$461,689

|

$11,685,685

|

$(11,818,902)

|

$343,222

|

|

|

|

|

|

|

|

|

|

|

Common stock

issued for 10% dividend payment pursuant to Series A

preferred stock Subscription Agreements

|

|

|

10,000

|

100

|

(100)

|

|

-

|

|

Issuance of

Series E preferred stock ($0.40/share)

|

500,000

|

5,000

|

|

|

195,000

|

|

200,000

|

|

Series E 10%

preferred stock dividend

|

|

|

|

|

(14,763)

|

|

(14,763)

|

|

Stock option

vesting expense

|

|

|

|

|

7,344

|

|

7,344

|

|

Warrants

issued for services

|

|

|

|

|

95,552

|

|

95,552

|

|

Units issued

for cash ($0.40/share)

|

|

|

1,762,500

|

17,625

|

616,876

|

|

634,501

|

|

Net loss for

the three months ended March 31, 2018

|

|

|

|

|

|

(1,044,802)

|

(1,044,802)

|

|

Balance -

March 31, 2018

|

1,975,000

|

$19,750

|

47,941,364

|

$479,414

|

$12,585,594

|

$(12,863,704)

|

$221,054

|

See accompanying notes to unaudited condensed consolidated

financial statements

6

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

MARCH 31, 2018

(Unaudited)

|

|

For

the Three months ended

|

|

|

|

March

31, 2018

|

|

|

|

2018

|

2017

|

|

Cash flows from operating activities:

|

|

|

|

Net

loss

|

$(1,044,802)

|

$(683,247)

|

|

Adjustments

to reconcile net loss to net cash and cash equivalents used in

operations:

|

|

|

|

Depreciation

|

6,339

|

5,489

|

|

Amortization

of debt discount

|

47,712

|

28,887

|

|

Amortization

|

112,723

|

75,806

|

|

Stock

option compensation expense

|

7,344

|

38,259

|

|

Common

stock and warrants issued for services

|

95,552

|

3,060

|

|

Provision

for bad debts

|

(26,281)

|

—

|

|

Changes in operating assets and liabilities:

|

|

|

|

Accounts

receivable

|

27,172

|

88,667

|

|

Inventories

|

99,543

|

(82,021)

|

|

Prepaid

expenses and other current assets

|

36,731

|

63,077

|

|

Other

assets

|

(1,980)

|

(36,332)

|

|

Accounts

payable and accrued expense

|

(78,876)

|

42,105

|

|

Deferred

rents

|

77

|

11,192

|

|

Deferred

revenues

|

(1,499)

|

—

|

|

Net

cash used in operating activities

|

(720,245)

|

(445,058)

|

|

|

|

|

|

Cash flows from investing activities:

|

|

|

|

Purchase

of property and equipment

|

(1,023)

|

(8,035)

|

|

Net

cash used in investing activities

|

(1,023)

|

(8,035)

|

|

|

|

|

|

Cash flows from financing activities:

|

|

|

|

Proceeds

from issuance of common units, net

|

634,501

|

—

|

|

Proceeds

from issuance of preferred stock

|

200,000

|

—

|

|

Repayments

on insurance premium notes payable

|

(22,224)

|

(25,242)

|

|

Dividend

payments

|

(14,763)

|

—

|

|

Principal

payment on long-term debt - Non-Related party

|

(50,000)

|

—

|

|

Long-term

debt - Related parties

|

—

|

350,000

|

|

Net

cash provided by financing activities

|

747,513

|

324,758

|

|

|

|

|

|

Net

increase (decrease) in cash

|

26,245

|

(128,335)

|

|

Cash

and cash equivalents at beginning of period

|

140,022

|

162,795

|

|

Cash

and cash equivalents at end of period

|

$166,267

|

$34,460

|

|

|

|

|

|

Supplemental disclosure of cash flow information

|

|

|

|

Cash

paid for:

|

|

|

|

Interest

|

$51,647

|

$20,216

|

|

Income

taxes

|

$—

|

$—

|

|

|

|

|

|

Non-cash investing and financing activities

|

|

|

|

Premium

finance loan payable recorded as prepaid

|

$66,131

|

$28,401

|

|

Debt

discount on convertible notes payable

|

$—

|

$245,000

|

See accompanying notes to unaudited condensed consolidated

financial statements

7

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES.

Organization and Nature of Operations

Bright

Mountain Media, Inc. is a Florida corporation formed on May 20,

2010. Its wholly owned subsidiaries, Bright Mountain LLC, and The

Bright Insurance Agency, LLC, were formed as Florida limited

liability companies in May 2011. Its wholly owned subsidiary,

Bright Watches, LLC was formed as a Florida limited liability

company in December 2015, and Daily Engage Media Group LLC

(“Daily Engage Media”) was formed as a New Jersey

limited liability company in February 2015. When used herein, the

terms "BMTM, " the "Company," "we," "us," "our" or "Bright

Mountain" refers to Bright Mountain Media, Inc. and its

subsidiaries.

Bright

Mountain Media is a digital media holding company whose primary

focus is connecting brands with consumers as a full advertising

services platform. The Company’s assets include an ad

network, an ad exchange platform and 25 websites (owned and/or

managed) that provide content, services and products. In addition,

the Bright Mountain Media Ad Exchange Network will be fully

developed and implemented in the third quarter of 2018. The

websites are primarily geared for a young, male audience with

several that focus on active, reserve and retired military

audiences as well as law enforcement and first responders. With the

acquisition of Daily Engage Media, the Company has acquired the

software, expertise and human resources to scale this side of the

business. Two of our websites operate as eCommerce platforms, one

of which, Bright Watches, is non strategic to the current direction

of our business.

In

December 2016, we acquired the assets, constituting the Black

Helmet Apparel business (“Black Helmet Apparel”), from

Sostre Enterprises, Inc. Assets acquired included various website

properties and content, social media content, inventory and other

intellectual property rights.

On

September 19, 2017, under the terms of an Amended and Restated

Membership Interest Purchase Agreement with Daily Engage Media, and

its members, the Company acquired 100% of the membership interests

of Daily Engage Media. Launched in 2015, Daily Engage Media is an

ad network that connects advertisers with approximately 200 digital

publications worldwide.

Principles of Consolidation and Basis of

Presentation

The

condensed consolidated financial statements include the accounts of

the Company and all of its wholly-owned subsidiaries. All

intercompany accounts and transactions have been eliminated in the

condensed consolidated financial statements. The accompanying

unaudited financial statements for the three months ended March 31,

2018 and 2017 have been prepared in accordance with generally

accepted accounting principles applicable to interim financial

information and the requirements of Form 10-Q and Article 10 of

Regulation S-X of the SEC. Accordingly, they do not include all of

the information and disclosures required by accounting principles

generally accepted in the United States for complete consolidated

financial statements. In the opinion of management, such condensed

consolidated financial statements include all adjustments

(consisting of normal recurring accruals) necessary for the fair

presentation of the condensed consolidated financial position and

the condensed consolidated results of operations. The condensed

consolidated results of operations for periods presented are not

necessarily indicative of the results to be expected for the full

year. The condensed consolidated balance sheet information as of

December 31, 2017 was derived from the audited consolidated

financial statements included in the Company's Annual Report on

Form 10-K for the year ended December 31, 2017. The interim

condensed consolidated financial statements should be read in

conjunction with that report.

Reclassification

Certain

reclassifications have been made to the December 31, 2017

consolidated balance sheet to conform to the March 31, 2018

consolidated balance sheet presentation.

Use of Estimates

Our

consolidated financial statements are prepared in accordance with

Accounting Principles Generally Accepted in the United States

(“GAAP”). These accounting principles require

management to make certain estimates, judgments, and assumptions.

We believe that the estimates, judgments, and assumptions upon

which we rely are reasonable based upon information available to us

at the time that these estimates, judgments, and assumptions are

made. These estimates, judgments, and assumptions can affect the

reported amounts of assets and liabilities as of the date of our

consolidated financial statements as well as reported amounts of

revenue and expenses during the periods presented. Our consolidated

financial statements would be affected to the extent there are

material differences between these estimates and actual results. In

many cases, the accounting treatment of a particular transaction is

specifically dictated by GAAP and does not require management's

judgment in its application. There are also areas in which

management's judgment in selecting any available alternative would

not produce a materially different result. Significant estimates

included in the accompanying consolidated financial statements

include revenue recognition, the fair value of acquired assets for

purchase price allocation in business combinations, valuation of

inventory, valuation of intangible assets, estimates of

amortization period for intangible assets, estimates of

depreciation period for fixed assets and the valuation of equity

based transactions.

8

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES (continued).

Cash and Cash Equivalents

The

Company considers all highly liquid investments with an original

maturity of three months or less when purchased to be cash

equivalents.

Fair Value of Financial Instruments and Fair Value

Measurements

The

Company measures its financial assets and liabilities in accordance

with GAAP. For certain of our financial instruments, including

cash, accounts payable, accrued expenses, and the short-term

portion of long-term debt, the carrying amounts approximate fair

value due to their short maturities.

We adopted accounting guidance for financial and

non-financial assets and liabilities in accordance with Accounting

Standards Codification (“ASC”) 820

“Fair

Value Measurements and Disclosures.” This standard defines fair value,

provides guidance for measuring fair value and requires certain

disclosures. This standard does not require any new fair value

measurements, but rather applies to all other accounting

pronouncements that require or permit fair value measurements. This

guidance does not apply to measurements related to share-based

payments. This guidance discusses valuation techniques, such as the

market approach (comparable market prices), the income approach

(present value of future income or cash flow), and the cost

approach (cost to replace the service capacity of an asset or

replacement cost). The guidance utilizes a fair value hierarchy

that prioritizes the inputs to valuation techniques used to measure

fair value into three broad levels. The following is a brief

description of those three levels:

Level 1:

Observable

inputs such as quoted prices (unadjusted) in active markets for

identical assets or liabilities.

Level 2:

Inputs

other than quoted prices that are observable, either directly or

indirectly. These include quoted prices for similar assets or

liabilities in active markets and quoted prices for identical or

similar assets or liabilities in markets that are not

active.

Level 3:

Unobservable

inputs in which little or no market data exists, therefore

developed using estimates and assumptions developed by us, which

reflect those that a market participant would use.

Accounts Receivable

Accounts

receivable are recorded at fair value on the date revenue is

recognized. The Company provides allowances for doubtful accounts

for estimated losses resulting from the inability of its customers

to repay their obligation. If the financial condition of the

Company's customers were to deteriorate, resulting in an impairment

of their ability to repay, additional allowances may be required.

The Company provides for potential uncollectible accounts

receivable based on specific customer identification and historical

collection experience adjusted for existing market conditions. If

market conditions decline, actual collection experience may not

meet expectations and may result in decreased cash flows and

increased bad debt expense.

The

policy for determining past due status is based on the contractual

payment terms of each customer, which are generally net 60 or net

90 days. Once collection efforts by the Company and its collection

agency are exhausted, the determination for charging off

uncollectible receivables is made.

The

determination of past due status for the Daily Engage Media

customers is based on the contractual payment terms of each

customer, which are generally net 60, net 90, or net 120 days. Once

collection efforts by the Company and its collection agency are

exhausted, the determination for charging off uncollectible

receivables is made. It is common in this industry to have accounts

receivable invoices age 60 to 90 days past the customer terms. This

is the result of the generally smaller size customers that we have

and they usually have to wait until they get paid for them to issue

payment to us. We work closely with all of our customers and

monitor the aging of the receivables on a weekly basis to ensure

our comfort that we will get paid. This is a time consuming

process, as we have to evaluate and analyze most customers on an

individual basis due to different circumstances and relationships

we have with each of them.

9

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES (continued).

Inventories

Inventories

consist of finished goods and are stated at the lower of cost or

market using the first in, first out (FIFO) method. Provisions have

been made to reduce excess or obsolete inventories to their net

realizable value.

Revenue Recognition

The Company recognizes revenue on our products in

accordance with ASC 605, “Revenue

Recognition.” Under these

guidelines, revenue is recognized on sales transactions when all of

the following exist: persuasive evidence of an arrangement did

exist; delivery of the product or advertising has occurred; the

sales price to the buyer is fixed or determinable; and

collectability is reasonably assured. The Company has several

revenue streams generated directly from its website and specific

revenue recognition criteria for each revenue stream is as

follows:

●

Sale

of merchandise directly to consumers: The Company's product sales

are recognized either FOB shipping point or FOB destination,

dependent on the customer. Revenues are therefore recognized at

point of ownership transfer, accordingly;

●

Advertising

revenue is received directly form companies who pay the Company a

monthly fee for advertising space and;

●

Advertising

revenues are generated by users “clicking” on website

advertisements utilizing several ad network partners. Revenues are

recognized net of their fees for Company owned websites upon

receipt of payment by the ad network partner since the revenue is

not determinable until it is received.

Our

advertising revenue generated from the Daily Engage and Bright

Mountain Media businesses are consistent with the above section.

However, the two scenarios that arise from revenue generation and

recognition include our owned and operated website advertising

revenue which requires little to no cost of revenue, as well as

advertising on non-owned websites which creates costs to those

website owners and the Company makes approximately 20% gross

profit.

Cost of Revenues

Components of costs

of revenues for the products segment include product costs,

shipping costs to customers and any inventory adjustments for

product sales. Cost of revenue for the advertising segment consists

of revenue share payments to media providers and website publishers

that are directly related to a revenuegenerating event. The

Company becomes obligated to make the revenue share payments in the

period the advertising impressions, clickthroughs, actions or

leadbased information are delivered or occur. The Daily

Engage portion of the advertising segment cost of revenue consists

of revenue share payments to media providers and website publishers

that are directly related to a revenuegenerating event. The

Company becomes obligated to make the revenue share payments in the

period the advertising impressions, clickthroughs, actions or

leadbased information are delivered or occur.

Shipping and Handling Costs

The

Company includes shipping and handling fees billed to customers as

revenues and shipping and handling costs for shipments to customers

as cost of revenues.

Sales Return Reserve Policy

Our

return policy generally allows our end users to return purchased

products for refund or in exchange for new products. We estimate a

reserve for sales returns, if any, and record that reserve amount

as a reduction of sales and as a sales return reserve liability.

Sales to consumers on our web site generally may be returned within

a reasonable period of time.

10

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES (continued).

Property and Equipment

Property

and equipment is recorded at cost. Depreciation is computed using

the straight-line method based on the estimated useful lives of the

related assets of five to seven years for office furniture and

equipment, and five years for computer equipment. Leasehold

improvements are amortized over the lesser of the lease term or the

useful life of the improvements. Expenditures for maintenance and

repairs along with fixed assets with a purchase price below our

capitalization threshold of $500 are expensed as

incurred.

Website Development Costs

The Company accounts for its website development

costs in accordance with ASC 350-50, “Website Development

Costs” (“ASC

350-50”). These costs, if any, are included in intangible

assets in the accompanying consolidated financial statements or

expensed immediately if the Company cannot support recovery of

these costs from positive future cash flows.

ASC

350-50 requires the expensing of all costs of the preliminary

project stage and the training and application maintenance stage

and the capitalization of all internal or external direct costs

incurred during the application and infrastructure development

stage. Upgrades or enhancements that add functionality are

capitalized while other costs during the operating stage are

expensed as incurred. The Company amortizes the capitalized website

development costs over an estimated life of five

years.

For the

three months ended March 31, 2018 and 2017, all platform and

website development costs have been expensed.

Amortization and Impairment of Long-Lived Assets

Amortization and impairment of long-lived assets

are non-cash expenses relating primarily to intangible assets. The

Company accounts for long-lived assets in accordance with the

provisions of ASC 360-10 “Accounting for the Impairment

or Disposal of Long-Lived Assets.” This statement requires that long-lived

assets and certain identifiable intangibles be reviewed for

impairment whenever events or changes in circumstances indicate

that the carrying amount of an asset may not be

recoverable.

Website

acquisition costs are amortized over three years and intangible

assets are amortized over five years. Recoverability of assets to

be held and used is measured by a comparison of the carrying amount

of an asset to future undiscounted net cash flows expected to be

generated by the asset. If such assets are considered to be

impaired, the impairment to be recognized is measured by the amount

by which the carrying amount of the assets exceeds the fair value

of the assets. Assets to be disposed of are reported at the lower

of the carrying amount or fair value less costs to sell.

While

it is likely that we will have significant amortization expense as

we continue to acquire websites, we believe that intangible assets

represent costs incurred by the acquired website to build value

prior to acquisition and the related amortization and impairment

charges of assets, if applicable, are not ongoing costs of doing

business. Amortization expense is included in selling, general and

administrative expenses on the accompanying condensed consolidated

statement of operations.

Stock-Based Compensation

The Company accounts for stock-based instruments

issued to employees for services in accordance with ASC 718

“Compensation – Stock

Compensation.” ASC 718

requires companies to recognize in the statement of operations the

grant-date fair value of stock options and other equity based

compensation issued to employees. The value of the portion of an

employee award that is ultimately expected to vest is recognized as

an expense over the requisite service periods using the

straight-line attribution method. The Company accounts for

non-employee share-based awards in accordance with the measurement

and recognition criteria of ASC 505-50, “Equity-Based Payments to

Non-Employees.” The

Company estimates the fair value of stock options by using the

Black-Scholes option-pricing model. Non- cash stock-based stock

option compensation is expensed over the requisite service period

and are included in selling, general and administrative expenses on

the accompanying condensed consolidated statement of operations.

For the three months ended March 31, 2018 and 2017, non-cash

stock-based stock option compensation expense was $7,344 and

$38,259, respectively.

11

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES (continued).

Advertising, Marketing and Promotion Costs

Advertising,

marketing and promotion expenses are expensed as incurred and are

included in selling, general and administrative expenses on the

accompanying statement of operations. For the three months ended

March 31, 2018 and 2017, advertising, marketing and promotion

expense was $60,923 and $92,288, respectively.

Income Taxes

We

use the asset and liability method to account for income taxes.

Under this method, deferred income taxes are determined based on

the differences between the tax basis of assets and liabilities and

their reported amounts in the consolidated financial statements

which will result in taxable or deductible amounts in future years

and are measured using the currently enacted tax rates and laws. A

valuation allowance is provided to reduce net deferred tax assets

to the amount that, based on available evidence, is more likely

than not to be realized.

The Company follows the provisions of ASC

740-10 “Accounting for Uncertain

Income Tax Positions.”

When tax returns are filed, it is highly certain that some

positions taken would be sustained upon examination by the taxing

authorities, while others are subject to uncertainty about the

merits of the position taken or the amount of the position that

would be ultimately sustained. In accordance with the guidance of

ASC 740-10, the benefit of a tax position is recognized in the

financial statements in the period during which, based on all available

evidence, management believes it is more likely than not that the

position will be sustained upon examination, including the

resolution of appeals or litigation processes, if any. Tax

positions taken are not offset or aggregated with other positions. Tax positions

that meet the more-likely-than-not recognition threshold are

measured as the largest amount of tax benefit that is more than 50% likely

of being realized upon settlement with the applicable taxing

authority. The portion of the benefits associated with tax

positions taken that exceeds the amount measured as described above

should be reflected as a liability for unrecognized tax benefits in the

accompanying consolidated balance sheets along with any associated

interest and penalties that would be payable to the taxing authorities upon

examination.

As

of March 31, 2018, tax years 2017, 2016, and 2015 remain open for

IRS audit. The Company has received no notice of audit or any

notifications from the IRS for any of the open tax

years.

Basic and Diluted Net Earnings (Loss) Per Common Share

In accordance with ASC 260-10

“Earnings Per

Share,” basic net

earnings (loss) per common share is computed by dividing the net

earnings (loss) for the period by the weighted average number of

common shares outstanding during the period. Diluted earnings

(loss) per share are computed using the weighted average number of

common and dilutive common stock equivalent shares outstanding

during the period. As of March 31, 2018 and 2017, there were

approximately 2,072,000 and 2,281,000 common stock equivalent

shares outstanding as stock options, respectively, 1,475,000 and

100,000 common stock equivalents from the conversion of preferred

stock, respectively, and 4,070,000 and 1,850,000 common stock

equivalents from the conversion of notes payable, respectively.

Equivalent shares were not utilized, as the effect is

anti-dilutive.

Segment Information

In accordance with the provisions of ASC 280-10,

“Disclosures about Segments of

an Enterprise and Related Information”, the Company is required to report

financial and descriptive information about its reportable

operating segments. The Company has two identifiable operating

segments based on the activities of the Company in accordance with

the ASC 280-10 The Company's two segments are product sales and

advertising as of March 31, 2018. The product sales segment sells

merchandise directly to customers thorough e-commerce distributor

portals such as Amazon and eBay and through our proprietary

websites and our retail location. The advertising segment is

focused on producing advertising revenue generated by users

“clicking on” and/or viewing website advertisements

utilizing several ad network partners and direct advertisers and

subscription revenue generated by the sale of access to premium

versions of our websites and to career postings on one of our

websites. The subscription revenues are about .66% of the total

advertising segment revenue.

12

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES (continued).

Recent Accounting Pronouncements

May

2014, the FASB issued ASU 2014-09, "Revenue from Contracts with

Customers (Topic 606).” ASU 2014-09, which has been modified

on several occasions, provides new guidance designed to enhance the

comparability of revenue recognition practices across entities,

industries, jurisdictions and capital markets. The core principle

of the new guidance is that an entity recognizes revenue to depict

the transfer of promised goods or services to customers in an

amount that reflects the consideration to which the entity expects

to be entitled in exchange for those goods and services. The new

guidance also requires disclosures about the nature, amount, timing

and uncertainty of revenue and cash flows arising from contracts

with customers. We are currently reviewing the provisions of

this ASU and subsequent updates and evaluating the potential impact

on our results of operations, cash flows or financial condition as

well as related disclosures. As an emerging growth company, we have

elected to adopt this guidance under the private company

guidelines, which will go into effect on January 1,

2019.

In July 2015, FASB issued ASU No.

2015-11,

“Inventory (Topic 330): Simplifying the Measurement of

Inventory”. The

amendments in this ASU do not apply to inventory that is measured

using last-in, first-out (LIFO) or the retail inventory method. The

amendments apply to all other inventory, which includes inventory

that is measured using first-in, first-out (FIFO) or average cost.

An entity should measure inventory within the scope of this Update

at the lower of cost and net realizable value. Net realizable value

is the estimated selling prices in the ordinary course of business,

less reasonably predictable costs of completion, disposal, and

transportation. Subsequent measurement is unchanged for inventory

measured using LIFO or the retail inventory

method. For public business entities, this ASU is

effective for fiscal years beginning after December 15, 2016,

including interim periods within those fiscal years. For all other

entities, this ASU is effective for fiscal years beginning after

December 15, 2016, and interim periods within fiscal years

beginning after December 15, 2017. The amendments in this ASU

should be applied prospectively with earlier application permitted

as of the beginning of an interim or annual reporting

period. The adoption of ASU No. 2015-11 did not have a

material effect on our condensed consolidated financial

statements.

In February 2016, the FASB issued ASU 2016-02

“Leases,” which will amend current lease accounting

to require lessees to recognize (i) a lease liability, which is a

lessee’s obligation to make lease payments arising from a

lease, measured on a discounted basis, and (ii) a right-of-use

asset, which is an asset that represents the lessee’s right

to use, or control the use of, a specified asset for the lease

term. ASU 2016-02 does not significantly change lease accounting

requirements applicable to lessors; however, certain changes were

made to align, where necessary, lessor accounting with the lessee

accounting model. This standard will be effective for fiscal years

beginning after December 15, 2018, including interim periods within

those fiscal years. We are currently reviewing the provisions of

this ASU to determine the impact on our results of operations, cash

flows or financial condition.

In April 2016, the FASB issued ASU No.

2016-15, “Classification of

Certain Cash Receipts and Cash Payments” ASU 2016- provides guidance regarding the

classification of certain items within the statement of cash flows.

ASU 2016-15 is effective for annual periods beginning after

December 15, 2017 with early adoption permitted. We do not believe

this ASU will have an impact on our results of operation, cash

flows, other than presentation, or financial

condition.

In June 2016, the FASB issued ASU 2016-13

“Financial

Instruments – Credit Losses” which replaces the incurred loss model with a

current expected credit loss (“CECL”) model. The CECL

model applies to financial assets subject to credit losses and

measured at amortized cost and certain off-balance sheet exposures.

Under current U.S. GAAP, an entity reflects credit losses on

financial assets measured on an amortized cost basis only when

losses are probable and have been incurred, generally considering

only past events and current conditions in making these

determinations. ASU 2016-13 prospectively replaces this approach

with a forward-looking methodology that reflects the expected

credit losses over the lives of financial assets, starting when

such assets are first acquired. Under the revised methodology,

credit losses will be measured based on past events, current

conditions and reasonable and supportable forecasts that affect the

collectability of financial assets.

13

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES (continued).

ASU 2016-13 also revises the approach to

recognizing credit losses for available-for-sale securities by

replacing the direct write-down approach with the allowance

approach and limiting the allowance to the amount at which the

security’s fair value is less than the amortized cost. In

addition, ASU 2016-13 provides that the initial allowance for

credit losses on purchased credit impaired financial assets will be

recorded as an increase to the purchase price, with subsequent

changes to the allowance recorded as a credit loss expense. ASU

2016-13 also expands disclosure requirements regarding an

entity’s assumptions, models and methods for estimating the

allowance for credit losses. The amendments of this Update are

effective for fiscal years, and interim periods within those fiscal

years, beginning after December 15, 2019. Early adoption is

permitted as of January 1, 2019. The Company is currently

evaluating the impact the adoption of this new standard will have

on its consolidated financial statements.

In November 2016, the FASB issued ASU

2016-18, “Statement of Cash Flows

–Restricted Cash” which requires entities to present the changes in

total cash, cash equivalents, restricted cash and restricted cash

equivalents in the statement of cash flows. The new guidance also

requires a reconciliation of the totals in the statement of cash

flows to the related captions in the balance sheet if restricted

cash and restricted cash equivalents are presented in a different

line item in the balance sheet. The amendments of this Update,

which should be applied using a retrospective transition method to

each period presented, are effective for fiscal years, and interim

periods within those fiscal years, beginning after December 15,

2017. Early adoption is permitted. The adoption of this standard is

not expected to have an impact on our statement of cash

flows.

In January 2017, the FASB issued 2017-04,

Intangibles -

Goodwill and Other (Topic 350):

Simplifying the Test for Goodwill Impairment. The amendments in

this ASU simplify the subsequent measurement of goodwill by

eliminating Step 2 from the goodwill impairment test and

eliminating the requirement for a reporting unit with a zero or

negative carrying amount to perform a qualitative assessment.

Instead, under this pronouncement, an entity would perform its

annual, or interim, goodwill impairment test by comparing the fair

value of a reporting unit with its carrying amount and would

recognize an impairment change for the amount by which the carrying

amount exceeds the reporting unit’s fair value; however, the

loss recognized is not to exceed the total amount of goodwill

allocated to that reporting unit. In addition, income tax effects

will be considered, if applicable. This ASU is effective for fiscal

years, and interim periods within those fiscal years, beginning

after December 15, 2019. Early adoption is permitted. The Company

is currently evaluating the impact of this ASU on its consolidated

financial statements and related disclosures.

NOTE 2 - GOING CONCERN.

The

accompanying condensed consolidated financial statements have been

prepared on a going concern basis, which contemplates the

realization of assets and the satisfaction of liabilities in the

normal course of business. The Company sustained a net loss of

$1,044,802 and used net cash in operating activities of $720,245

for the three months ended March 31, 2018. The Company had an

accumulated deficit of $12,863,704 at March 31, 2018. These factors

raise substantial doubt about the ability of the Company to

continue as a going concern. The Company's continuation as a going

concern is dependent upon its ability to generate revenues and its

ability to continue receiving investment capital from related

parties to sustain its current level of operations.

Management

plans to continue to raise additional capital through private

placements and is exploring additional avenues for future

fund-raising through both public and private sources.

The

condensed consolidated financial statements do not include any

adjustments relating to the recoverability and classification of

recorded asset amounts or the amounts and classification of

liabilities that might be necessary should the Company be unable to

continue as a going concern.

14

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 3 – ACQUISITIONS

On

September 19, 2017 the parties entered into an Amended and Restated

Membership Interest Purchase Agreement under which the Company

acquired 100% of the membership interests of Daily Engage Media in

exchange for common stock, promissory notes and the satisfaction of

certain debt obligations of the acquired entity totaling

approximately $1,088,000.

Under

the terms of the Daily Engage Purchase Agreement, upon Daily Engage

Media achieving certain revenue and operating income tests, we

agreed to issue additional consideration as follows:

●

if

Daily Engage Media's revenues are at least $20,228,954, and it has

operating income of at least $3,518,623 (the "Year-One Daily Engage

Target") during the first 12 months following the closing date (the

"Year-One Earn out Period") as determined by us in accordance with

GAAP, we agreed to pay former members and executives collectively

an additional $500,000 in cash and issue an additional 1,008,547

shares of our common stock (the "Year-One Earn out

Shares");

●

if

Daily Engage Media's revenues are at least $60,385,952, and

operating income of at least $11,380,396 (the "Year-Two Daily

Engage Target") during the first 12 months following the Year-One

Earnout Period (the "Year-Two Earnout Period") as determined by us

in accordance with GAAP, we agreed to pay the pay former members

and executives an additional $500,000 in cash and issue an

additional 796,221 shares of our common stock (the "Year-Two

Earnout Shares"). In addition, if the Year-Two Daily Engage Target

is met, at the time of payment of the Year-Two Earnout Shares and

the year-two earnout cash, the former members and executives

collectively will also be entitled to receive the Year-One Earnout

Shares and the year-one earnout cash to the extent not previously

received; and

●

if

Daily Engage Media's revenues are at least $96,512,204, and it has

operating income of at least $18,524,967 (the "Year-Three Daily

Engage Target") during the 12 months following the Year-Two Earnout

Period (the "Year-Three Earnout Period") as determined by us in

accordance with GAAP, we agreed to pay former members and

executives an additional $550,000 in cash and issue an additional

723,523 shares of our common stock (the "Year-Three Earnout

Shares"). In addition, if the Year-Three Daily Engage Target is

met, at the time of payment of the Year-Three Earnout Shares and

the year-three earnout cash, the pay former members and executives

collectively will also be entitled to receive the Year-One Earnout

Shares, the year-one earnout cash, the Year-Two Earnout Shares and

the year-two earnout cash, to the extent not previously

received.

The

preliminary allocation of the purchase price to the assets acquired

and liabilities assumed based on the estimated fair values was as

follows:

|

Tangible

assets acquired

|

$361,770

|

|

Liabilities

assumed

|

(562,006)

|

|

Net

liabilities assumed

|

$(200,236)

|

|

|

|

|

Exchange

platform

|

$50,000

|

|

Tradename

|

150,000

|

|

Customer

relationships

|

250,000

|

|

Non-compete

agreements

|

192,000

|

|

Goodwill

|

446,426

|

|

Total

purchase price

|

$1,088,426

|

The

final accounting for the acquisition is expected to be completed in

the third quarter of 2018

15

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 3 – ACQUISITIONS (continued).

Pro forma results

The following table sets forth a summary of the unaudited pro forma

results of the Company as if the acquisition of the assets

constituting the Daily Engage Media business, which was closed in

September 2017, had taken place on the first day of the periods

presented. These combined results are not necessarily indicative of

the results that may have been achieved had the assets been

acquired as of the first day of the periods presented.

|

|

Three Months Ended

|

|

|

March 31, 2017

|

|

Total

revenue

|

$1,224,716

|

|

Total

expenses

|

(1,871,679)

|

|

Preferred

stock dividend

|

(1,973)

|

|

Net

loss attributable to common shareholders

|

$(648,936)

|

|

Basic

and diluted net loss per share

|

$(0.01)

|

NOTE 4 – INVENTORIES.

At March 31, 2018 and December 31, 2017 inventories consisted of

the following:

|

|

March 31,

2018

|

December 31,

2017

|

|

Product

inventory: clocks and watches

|

$351,361

|

$453,852

|

|

Product

inventory: other inventory

|

183,012

|

180,064

|

|

Total

inventory balance

|

534,373

|

633,916

|

|

Less:

Inventory allowance for slow moving

|

(22,448)

|

(22,448)

|

|

Total

inventory balance, net

|

$511,925

|

$611,468

|

NOTE 5 – PREPAID COSTS AND EXPENSES.

At

March 31, 2018 and December 31, 2017, prepaid expenses and other

current assets consisted of the following:

|

|

March

31,

2018

|

December

31,

2017

|

|

Prepaid

rent

|

$39,877

|

$50,417

|

|

Prepaid

insurance

|

66,131

|

92,322

|

|

Prepaid

inventory

|

2,993

|

2,993

|

|

Prepaid

expenses and other current assets

|

$109,001

|

$145,732

|

16

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 6 – PROPERTY AND EQUIPMENT.

At

March 31, 2018 and December 31, 2017, property and equipment

consisted of the following:

|

|

Useful Lives

|

March 31, 2018

|

December 31, 2017

|

|

Furniture

and fixtures

|

3-5

years

|

$79,993

|

$78,994

|

|

Computer

equipment

|

3

years

|

59,510

|

59,511

|

|

Leasehold

improvements

|

5

years

|

39,385

|

39,384

|

|

Total

fixed assets

|

|

178,888

|

177,889

|

|

Less:

accumulated depreciation

|

|

(94,702)

|

(88,389)

|

|

Total

fixed assets, net

|

|

$84,186

|

$89,500

|

Depreciation

expense for the three months ending March 31, 2018 and 2017, was

$6,339 and $5,489, respectively.

NOTE 7 – Website Acquisition and Intangible

Assets

At

March 31, 2018 and December 31, 2017, respectively, website

acquisitions, net consisted of the following:

|

|

March 31,

2018

|

December 31,

2017

|

|

Website

Acquisition Assets

|

$1,417,189

|

$1,417,189

|

|

Less:

accumulated amortization

|

(873,197)

|

(812,575)

|

|

Less:

accumulated impairment loss

|

(211,197)

|

(211,197)

|

|

Website

Acquisition Assets, net

|

$332,795

|

$393,417

|

At

March 31, 2018 and December 31, 2017, respectively, intangible

assets, net consisted of the following:

|

|

Useful Lives

|

March 31, 2018

|

December 31, 2017

|

|

Tradename

|

5

years

|

$300,000

|

$300,000

|

|

Customer

relationships

|

5

years

|

502,000

|

502,000

|

|

Non-compete

agreements

|

5-8

years

|

312,000

|

312,000

|

|

Total

Intangible Assets

|

|

$1,114,000

|

$1,114,000

|

|

Less:

accumulated amortization

|

|

(148,100)

|

(95,999)

|

|

Less:

accumulated impairment loss

|

|

(50,227)

|

(50,227)

|

|

Intangible

assets, net

|

|

$915,673

|

$967,774

|

Amortization

expense for the three month periods ending March 31, 2018 and 2017

was $112,723 and $75,806, respectively, related to both the website

acquisition costs and the intangibles.

17

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 8 – SEGMENT INFORMATION.

The

Company has two identifiable segments as of March 31, 2018;

products and advertising. The products segment sells merchandise

directly to customers thorough e-commerce distributor portals such

as Amazon and eBay and through our proprietary websites and retail

location. The advertising segment is focused on producing

advertising revenue generated by users “clicking on”

and/or viewing website advertisements utilizing several ad network

partners and direct advertisers and subscription revenue generated

by the sale of access to premium versions of our websites and to

career postings on one of our websites. The subscription revenues

are about 0.7% of the total advertising segment revenue The

following information represents segment activity for the three

month periods ended March 31, 2018 and 2017.

|

|

As of and for the three months ended

|

As of and for the three months ended

|

||||

|

|

March 31, 2018

|

March 31, 2017

|

||||

|

|

Products

|

Services

|

Total

|

Products

|

Services

|

Total

|

|

Revenues

|

$375,286

|

$683,058

|

$1,058,344

|

$551,355

|

$109,743

|

$661,098

|

|

Website

amortization

|

26,615

|

86,108

|

112,723

|

—

|

75,806

|

75,806

|

|

Depreciation

|

2,248

|

4,091

|

6,339

|

4,578

|

911

|

5,489

|

|

Loss

from operations

|

(336,815)

|

(593,064)

|

(929,879)

|

(461,912)

|

(137,249)

|

(599,161)

|

|

Segment

assets

|

1,128,652

|

2,363,088

|

3,491,740

|

1,438,646

|

1,306,714

|

2,745,360

|

|

Purchase

of assets

|

$—

|

$1,023

|

$1,023

|

$8,035

|

$—

|

$8,035

|

NOTE 9 – NOTES PAYABLE.

Long Term Debt to Related Parties

Between

September 2016 and August 2017, the Company issues a series of

convertible notes payable to the Chairman of the Board of

Directors. The notes mature five years from issuance at which time

all principle and interest are payable. Interest rates on the notes

range from 6% to 12% and the notes are convertible at any time

prior to maturity at conversion prices ranging from $0.40 to 0.50

per share. The Company recognized a beneficial conversion feature

when the fair value of the underlying common stock to which the

note is convertible into was in excess of the face value of the

note. For notes payable under this criteria, the intrinsic value of

the beneficial conversion features was recorded as a debt discount

with a corresponding amount to additional paid in capital. The debt

discount is being amortized to interest over the five year life of

the note using the effective interest method.

The

principal balance of these notes payable was $2,035,000 at March

31, 2018 and December 31, 2017 and discounts recognized upon

respective origination dates as a result of the beneficial

conversion feature total $1,018,125. As of March 31, 2018 and

December 31, 2017, the total convertible notes payable to related

party net of discounts was $1,249,100 and $1,198,893,

respectively.

Amortization

of debt discount totaled $50,207 and $26,159 at March 31, 2018 and

2017, respectively. There was no accrued interest expense as of

March 31, 2018 and December 31, 2017. Interest expense on the

convertible notes payable was $49,651 and $22,849, for the periods

ended March 31, 2018 and 2017 respectively.

Notes Payable

On

November 30, 2016, the Company entered into a promissory note

agreement with an unaffiliated party in the principal amount

of $500,000. The note

is unsecured and carries an interest rate of 10% per annum and

matures on June 30, 2018. In the event of default of any loan

provision, the lender can declare all or any portion of the unpaid

principal and interest immediately due and payable. During March

2018 the Company made a payment of $50,000, reducing the note

balance to $450,000.

In

connection with the acquisition of Daily Engage Media, the Company

issued promissory notes totaling $380,000. The notes have no stated

interest rate and mature on September 19, 2018. The balance of the

notes payable at March 31, 2018 and December 31, 2017 was

$254,687.

The

Company has a note payable originating from a prior website

acquisition. At the time of the acquisition, the Company agreed to

pay $150,000, payable monthly in an amount equal to 30% of the net

revenues from the website, when collected, with the total amount of

the earn out to be paid by January 4, 2019. The Company recorded

the future monthly payments totaling

$150,000 at a present value of $117,268, net of a discount of

$32,732. The present value was calculated at a discount rate of 12%

using the estimate future revenues. The balance of the note payable

at March 31, 2018 and December 31, 2017, was $73,932 and $67,895

net of discounts of $9,092 and $11,820 respectively.

Interest

expense on notes payable was $15,353 and $35,160 for the periods

ended March 31, 2018 and 2017, respectively.

18

BRIGHT MOUNTAIN MEDIA, INC., AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2018

(Unaudited)

NOTE 10 – COMMITMENTS AND CONTINGENCIES.

The

Company leases its corporate offices at 6400 Congress Avenue, Suite

2050, Boca Raton, Florida 33487 under a long-term non-cancellable

lease agreement expiring on March 14, 2019. The lease terms

required base rent payments of approximately $9,000 per month for

the first twelve months commencing in October 2014, with a 3%

escalation each year. An additional security deposit of $2,500 was

required. Rent is all-inclusive and includes electricity, heat,

air-conditioning, and water.

The

Company leases retail space for its product sales division at 4900

Linton Boulevard, Bay 17A, Delray Beach, FL 33445 under a two

long-term, non-cancellable lease agreement, which contain renewal

options. The leases commenced in January 2017 and are in effect for

a period of five years. Minimum base rentals total approximately