Attached files

| file | filename |

|---|---|

| EX-32.1 - CERTIFICATION - Sino-Global Shipping America, Ltd. | f10q0318ex32-1_sinoglobal.htm |

| EX-31.2 - CERTIFICATION - Sino-Global Shipping America, Ltd. | f10q0318ex31-2_sinoglobal.htm |

| EX-31.1 - CERTIFICATION - Sino-Global Shipping America, Ltd. | f10q0318ex31-1_sinoglobal.htm |

U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

☒ Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the period ended March 31, 2018

☐ Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from ___________ to ___________.

Commission File Number 001-34024

Sino-Global Shipping America, Ltd.

(Exact name of registrant as specified in its charter)

| Virginia | 11-3588546 | |

| (State or other jurisdiction of | (I.R.S. employer | |

| Incorporation or organization) | identification number) |

1044 Northern Boulevard, Suite 305

Roslyn, New York 11576-1514

(Address of principal executive offices and zip code)

(718) 888-1814

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☐ (Do not check if a smaller reporting company) | Smaller reporting company ☒ |

| Emerging Growth Company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date. As of May 11, 2018, the Company has 12,435,535 issued and outstanding shares of common stock.

SINO-GLOBAL SHIPPING AMERICA, LTD.

FORM 10-Q

INDEX

| PART I. FINANCIAL INFORMATION | 1 |

| Item 1. Financial Statements | 1 |

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations | 25 |

| Item 3. Quantitative and Qualitative Disclosures about Market Risk | 42 |

| Item 4. Controls and Procedures | 42 |

| PART II. OTHER INFORMATION | 43 |

| Item 6. Exhibits | 43 |

i

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This document contains certain statements of a forward-looking nature. Such forward-looking statements, including but not limited to projected growth, trends and strategies, future operating and financial results, financial expectations and current business indicators are based upon current information and expectations and are subject to change based on factors beyond the control of the Company. Forward-looking statements typically are identified by the use of terms such as “look,” “may,” “will,” “should,” “might,” “believe,” “plan,” “expect,” “anticipate,” “estimate” and similar words, although some forward-looking statements are expressed differently. The accuracy of such statements may be impacted by a number of business risks and uncertainties that could cause actual results to differ materially from those projected or anticipated, including but not limited to the following:

| ● | Our ability to timely and properly deliver our services; |

| ● | Our dependence on a limited number of major customers and related parties; |

| ● | Political and economic factors in the Peoples’ Republic of China (“PRC”); |

| ● | Our ability to expand and grow our lines of business; |

| ● | Unanticipated changes in general market conditions or other factors, which may result in cancellations or reductions in the need for our services; |

| ● | Economic conditions which would reduce demand for services provided by the Company and could adversely affect profitability; |

| ● | The effect of terrorist acts, or the threat thereof, on the demand for the shipping and logistic industry which could, adversely affect the Company’s operations and financial performance; |

| ● | The acceptance in the marketplace of our new lines of business; |

| ● | Foreign currency exchange rate fluctuations; |

| ● | Hurricanes or other natural disasters; and |

| ● | Our ability to attract, retain and motivate skilled personnel. |

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company undertakes no obligation to update this forward-looking information unless required by applicable law or regulations.

ii

PART I. FINANCIAL INFORMATION

| Item 1. | Financial Statements |

SINO-GLOBAL SHIPPING AMERICA, LTD. AND AFFILIATES

INDEX TO FINANCIAL STATEMENTS

| PAGE | |

| UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS: | |

| Condensed Consolidated Balance Sheets as of March 31, 2018 (unaudited) and June 30, 2017 | 2 |

| Unaudited Condensed Consolidated Statements of Operations and Comprehensive Income for the Three and Nine Months Ended March 31, 2018 and 2017 | 3 |

| Unaudited Condensed Consolidated Statements of Cash Flows for the Nine Months Ended March 31, 2018 and 2017 | 4 |

| Notes to the Unaudited Condensed Consolidated Financial Statements | 5 |

1

SINO-GLOBAL SHIPPING AMERICA, LTD. AND AFFILIATES

CONDENSED CONSOLIDATED BALANCE SHEETS

| March 31, | June 30, | |||||||

| 2018 | 2017 | |||||||

| (Unaudited) | ||||||||

| Assets | ||||||||

| Current assets | ||||||||

| Cash and cash equivalents | $ | 9,549,942 | $ | 8,733,742 | ||||

| Accounts receivable, less allowance for doubtful accounts of $1,350,531 and $185,821 as of March 31, 2018 and June 30, 2017, respectively | 4,757,547 | 2,569,141 | ||||||

| Other receivables, less allowance for doubtful accounts of $145,244 and $145,244 as of March 31, 2018 and June 30, 2017, respectively | 167,018 | 37,811 | ||||||

| Advances to suppliers-third parties | 442,137 | 54,890 | ||||||

| Advances to suppliers-related party | 3,601,421 | 3,333,038 | ||||||

| Prepaid expenses and other current assets | 397,368 | 311,136 | ||||||

| Due from related parties, net | 2,249,544 | 1,715,130 | ||||||

| Total Current Assets | 21,164,977 | 16,754,888 | ||||||

| Property and equipment, net | 536,282 | 187,373 | ||||||

| Intangible assets, net | 168,889 | - | ||||||

| Prepaid expenses | - | 6,882 | ||||||

| Other long-term assets | 137,850 | 117,478 | ||||||

| Deferred tax assets | 1,670,100 | 749,400 | ||||||

| Total Assets | $ | 23,678,098 | $ | 17,816,021 | ||||

| Liabilities and Equity | ||||||||

| Current Liabilities | ||||||||

| Advances from customers | $ | 373,172 | $ | 369,717 | ||||

| Accounts payable | 472,085 | 206,211 | ||||||

| Taxes payable | 2,401,934 | 1,886,216 | ||||||

| Due to related parties | - | 206,323 | ||||||

| Accrued expenses and other current liabilities | 423,877 | 418,029 | ||||||

| Total Current Liabilities | 3,671,068 | 3,086,496 | ||||||

| Income tax payable - noncurrent portion | 440,219 | - | ||||||

| Total Liabilities | 4,111,287 | 3,086,496 | ||||||

| Commitments and Contingencies | ||||||||

| Equity | ||||||||

| Preferred stock, 2,000,000 shares authorized, no par value, none issued. | - | - | ||||||

| Common stock, 50,000,000 shares authorized, no par value; 12,611,032 and 10,281,032 shares issued as of March 31, 2018 and June 30, 2017, respectively; 12,435,535 and 10,105,535 outstanding as of March 31, 2018 and June 30, 2017, respectively | 22,046,330 | 20,535,379 | ||||||

| Additional paid-in capital | 2,386,864 | 688,934 | ||||||

| Treasury stock, at cost, 175,497 shares as of March 31, 2018 and June 30, 2017 | (417,538 | ) | (417,538 | ) | ||||

| Retained earnings (accumulated deficit) | 105,939 | (893,907 | ) | |||||

| Accumulated other comprehensive income (loss) | 153,775 | (414,564 | ) | |||||

| Total Sino-Global Shipping America Ltd. Stockholders' Equity | 24,275,370 | 19,498,304 | ||||||

| Non-controlling Interest | (4,708,559 | ) | (4,768,779 | ) | ||||

| Total Equity | 19,566,811 | 14,729,525 | ||||||

| Total Liabilities and Equity | $ | 23,678,098 | $ | 17,816,021 | ||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements

2

SINO-GLOBAL SHIPPING AMERICA, LTD. AND AFFILIATES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME

(UNAUDITED)

| For the Three Months Ended March 31, | For the Nine Months Ended March 31, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Net revenues - third parties | $ | 4,699,170 | $ | 1,984,834 | $ | 14,179,256 | $ | 4,591,381 | ||||||||

| Net revenues - related party | 501,000 | 762,777 | 1,621,406 | 2,229,180 | ||||||||||||

| Total revenues | 5,200,170 | 2,747,611 | 15,800,662 | 6,820,561 | ||||||||||||

| Cost of revenues | (3,405,435 | ) | (1,132,213 | ) | (10,447,231 | ) | (1,789,348 | ) | ||||||||

| Gross profit | 1,794,735 | 1,615,398 | 5,353,431 | 5,031,213 | ||||||||||||

| General and administrative expenses | (1,477,514 | ) | (612,441 | ) | (4,067,885 | ) | (2,248,639 | ) | ||||||||

| Selling expenses | (35,363 | ) | (41,245 | ) | (393,090 | ) | (153,429 | ) | ||||||||

| Total operating expenses | (1,512,877 | ) | (653,686 | ) | (4,460,975 | ) | (2,402,068 | ) | ||||||||

| Operating income | 281,858 | 961,712 | 892,456 | 2,629,145 | ||||||||||||

| Other income (expense) | ||||||||||||||||

| Financial income (expense), net | 170,134 | 34,167 | 392,729 | (57,737 | ) | |||||||||||

| Total other income (expense) | 170,134 | 34,167 | 392,729 | (57,737 | ) | |||||||||||

| Net income before provision for income taxes | 451,992 | 995,879 | 1,285,185 | 2,571,408 | ||||||||||||

| Income tax benefit (expense) | (216,095 | ) | 303,196 | 58,597 | 158,184 | |||||||||||

| Net income | 235,897 | 1,299,075 | 1,343,782 | 2,729,592 | ||||||||||||

| Net income (loss) attributable to non-controlling interest | 150,943 | 4,021 | 343,936 | (104,083 | ) | |||||||||||

| Net income attributable to Sino-Global Shipping America, Ltd. | $ | 84,954 | $ | 1,295,054 | $ | 999,846 | $ | 2,833,675 | ||||||||

| Comprehensive income (loss) | ||||||||||||||||

| Net income | $ | 235,897 | $ | 1,299,075 | $ | 1,343,782 | $ | 2,729,592 | ||||||||

| Foreign currency translation income (loss) | 164,446 | 4,871 | 309,763 | (114,011 | ) | |||||||||||

| Comprehensive income | 400,343 | 1,303,946 | 1,653,545 | 2,615,581 | ||||||||||||

| Less: Comprehensive income (loss) attributable to non-controlling interest | 30,785 | (19,419 | ) | 92,150 | 4,702 | |||||||||||

| Comprehensive income attributable to Sino-Global Shipping America Ltd. | $ | 369,558 | $ | 1,323,365 | $ | 1,561,395 | $ | 2,610,879 | ||||||||

| Earnings per share | ||||||||||||||||

| -Basic | $ | 0.01 | $ | 0.14 | $ | 0.10 | $ | 0.33 | ||||||||

| -Diluted | $ | 0.01 | $ | 0.14 | $ | 0.10 | $ | 0.33 | ||||||||

| Weighted average number of common shares used in computation | ||||||||||||||||

| -Basic | 10,835,535 | 8,994,146 | 10,433,272 | 8,514,080 | ||||||||||||

| -Diluted | 10,870,221 | 9,028,928 | 10,479,555 | 8,534,701 | ||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements

3

SINO-GLOBAL SHIPPING AMERICA LTD. AND AFFILIATE

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| For

the Nine months ended March 31, | ||||||||

| 2018 | 2017 | |||||||

| Operating Activities | ||||||||

| Net income | $ | 1,343,782 | $ | 2,729,592 | ||||

| Adjustment to reconcile net income to net cash provided by (used in) operating activities: | ||||||||

| Amortization of stock options | 9,665 | 77,320 | ||||||

| Amortization of stock - based compensation to consultants | 432,125 | 547,138 | ||||||

| Amortization of stock - based compensation to employees | 182,000 | - | ||||||

| Depreciation and amortization | 63,402 | 36,432 | ||||||

| Provision for (recovery of) doubtful accounts - accounts receivable | 1,164,710 | (107,608 | ) | |||||

| Provision for doubtful accounts - due from related parties | 243,433 | - | ||||||

| Deferred tax benefit | (920,700 | ) | (387,900 | ) | ||||

| Changes in assets and liabilities | ||||||||

| Accounts receivable | (3,246,911 | ) | 517,463 | |||||

| Other receivables | (80,145 | ) | 184,753 | |||||

| Advances to suppliers - third parties | 50,465 | 816,715 | ||||||

| Prepaid expense and other current assets | (84,147 | ) | 65,279 | |||||

| Due from related parties | (784,363 | ) | (2,843,131 | ) | ||||

| Other long-term assets | - | (14,185 | ) | |||||

| Advances from customers | (23,218 | ) | 324,476 | |||||

| Accounts payable | 243,380 | 312,883 | ||||||

| Taxes payable | 798,012 | 201,259 | ||||||

| Due to related parties | (206,323 | ) | 156,841 | |||||

| Accrued expenses and other current liabilities | 889 | 514,445 | ||||||

| Net cash provided by (used in) operating activities | (813,944 | ) | 3,131,772 | |||||

| Investing Activities | ||||||||

| Acquisition of property and equipment | (379,917 | ) | (55,474 | ) | ||||

| Acquisition of intangible assets | (190,000 | ) | - | |||||

| Prepayment for intangible assets | (437,357 | ) | - | |||||

| Net cash used in investing activities | (1,007,274 | ) | (55,474 | ) | ||||

| Financing Activities | ||||||||

| Proceeds from issuance of common stock, net | 2,585,091 | 4,319,988 | ||||||

| Proceeds from exercise of stock options | - | 82,500 | ||||||

| Net cash provided by financing activities | 2,585,091 | 4,402,488 | ||||||

| Effect of exchange rate fluctuations on cash and cash equivalents | 52,327 | (24,591 | ) | |||||

| Net increase in cash and cash equivalents | 816,200 | 7,454,195 | ||||||

| Cash and cash equivalents at beginning of period | 8,733,742 | 1,385,994 | ||||||

| Cash and cash equivalents at end of period | $ | 9,549,942 | $ | 8,840,189 | ||||

| Supplemental information | ||||||||

| Income taxes paid | $ | 60,162 | $ | 89,324 | ||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements

4

SINO-GLOBAL SHIPPING AMERICA, LTD. AND AFFILIATES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Note 1. ORGANIZATION AND NATURE OF BUSINESS

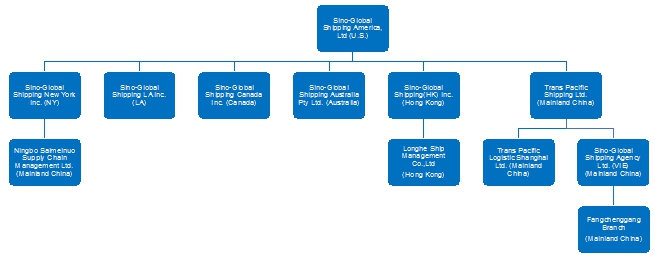

Founded in the United States (the “U.S.”) in 2001, Sino-Global Shipping America, Ltd., a Virginia corporation (“Sino-Global” or the “Company”), is a non-asset based global shipping and freight logistics integrated solutions provider. The Company provides tailored solutions and value-added services for its customers to drive effectiveness and control in related links throughout the entire shipping and freight logistics chain. The Company conducts its business primarily through its wholly-owned subsidiaries in the U.S., the People’s Republic of China, including Hong Kong (the “PRC”), Australia and Canada. Currently, a significant portion of the Company’s business is generated from clients located in the PRC and the U.S.

The Company’s Chinese subsidiary, Trans Pacific Shipping Limited, a wholly-owned foreign enterprise (“Trans Pacific Beijing”), is the 90% owner of Trans Pacific Logistics Shanghai Limited (“Trans Pacific Shanghai”). Trans Pacific Beijing and Trans Pacific Shanghai are referred to collectively as “Trans Pacific”.

The Company’s inland transportation management services are operated by its subsidiaries in the PRC, Hong Kong and the U.S. The Company’s freight logistics services are operated by its subsidiaries in the PRC and the U.S. The Company’s container trucking services are currently operated by its subsidiaries in the PRC and through a joint venture in the U.S. The Company’s newly added bulk cargo container trucking services are currently operated by its subsidiary in the U.S. The Company has increased its business in the U.S. since the launch of the short haul container truck services web-based platform.

In August 2016, the Company’s Board of Directors (the “Board”) authorized management to move forward with the development of a mobile application that will provide a full-service logistics platform between the U.S. and the PRC for short-haul trucking in the U.S. Upon the completion of the platform, the Company signed two significant agreements with COSCO Beijing International Freight Co., Ltd. (“COSFRE Beijing”) and Sino-Trans Guangxi in December 2016. Pursuant to the agreement with COSFRE Beijing, the Company will receive a percentage of the total amount of each transportation fee for the arrangement of inland transportation services for COSFRE Beijing’s container shipments into U.S. ports. For the strategic cooperation framework agreement with Sino-Trans Guangxi, which is a subsidiary of Sino-Trans Limited, the Company expects to utilize both parties’ existing resources and establish an integrated logistics plan to provide an end-to-end supply chain solution for customers shipping soybeans and sulfur products from the U.S. to southern PRC via container.

On January 5, 2017, the Company entered into a joint venture agreement and formed a new joint venture company named ACH Trucking Center Corp. (“ACH Center”) with Jetta Global Logistics Inc. (“Jetta Global”). Along with the establishment of ACH Center, the Company began providing short haul trucking transportation and logistics services to customers located in the New York and New Jersey areas. The Company holds a 51% ownership stake in ACH Center. Although the establishment of ACH Center brought benefited for the Company and Jetta Global, it could not satisfy long term development for both the Company and Jetta Global. The Company signed a termination agreement with Jetta Global to terminate the joint venture agreement on December 4, 2017. As ACH Center’s operating revenue was less than 1% of the Company’s consolidated revenue and the termination did not constitute a strategic shift that would have a major effect on the Company’s operations and financial results, the results of operations for ACH Center was not reported as discontinued operations under the guidance of Accounting Standards Codification 205.

5

On January 9, 2017, the Company entered into a strategic cooperation agreement with China Ocean Shipping Agency Qingdao Co. Ltd. (“COSCO Qingdao”). COSCO Qingdao will utilize the Company’s full-service logistics platform to arrange the transportation of its container shipments into U.S. ports. Sino-Global will receive a percentage of the total amount of each transportation fee in exchange for the arrangement of inland transportation services for COSCO Qingdao’s container shipments into U.S. ports.

On February 18, 2017, the Company entered into a cooperative transportation agreement with a related party, Zhiyuan International Investment & Holding Group (Hong Kong) Co., Ltd. (the “Buyer” or “Zhiyuan Hong Kong”). Zhiyuan Hong Kong, jointly with China Minmetals Corporation and China Metallurgical Group Corporation, acts as the general designer, general equipment provider and general service contractor in the upgrade and renovation project of Perwaja Steel, located in Malaysia (the “Project”). The Company agreed to provide high-quality services, including the design of a detailed transportation plan as well as execution and necessary supervision of the plan at Zhiyuan Hong Kong’s demand, in consideration for which the Company will receive a 1% to 1.25% transportation fee incurred in the Project as a commission for its services rendered (see Note 3 and Note 16). On July 7, 2017, the Company signed a supplemental agreement with the Buyer, pursuant to which the Company will cooperate with Zhiyuan Hong Kong exclusively on the entire Project’s transportation needs. Pursuant to the supplemental agreement, the Company agrees to make prepayments to Zhiyuan Hong Kong for its share of packaging and transporting costs related to the Project; in return, the Company will receive 15% of the cost incurred in the Project from Zhiyuan Hong Kong as a service fee. The Project is expected to be completed in one to two years and the Company will collect its service fee in accordance with Project completion.

On September 11, 2017, the Company set up a new wholly-owned subsidiary, Ningbo Saimeinuo Supply Chain Management Ltd. (“Sino Ningbo”), via the wholly-owned entity, Sino-Global Shipping New York Inc. This subsidiary primarily engages in supply chain management and freight logistics services. Sino Ningbo plans to start business activities in the fourth quarter of fiscal year 2018.

Note 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(a) Basis of Presentation

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“US GAAP”) for information pursuant to the rules and regulations of the Securities Exchange Commission (“SEC”).

In the opinion of management, all adjustments, consisting only of normal recurring adjustments, considered necessary to give a fair presentation have been included. Interim results are not necessarily indicative of results of a full year. The information in this Form 10-Q should be read in conjunction with information included in the annual report for the fiscal year ended June 30, 2017 on Form 10-K filed with the SEC on September 27, 2017.

(b) Basis of Consolidation

The unaudited condensed consolidated financial statements include the accounts of the Company, its subsidiaries, and its affiliates. All significant intercompany transactions and balances are eliminated in consolidation. A subsidiary is an entity in which the Company, directly or indirectly, controls more than one half of the voting power or has the power to: govern the financial and operating policies; appoint or remove the majority of the members of the board of directors; cast a majority of votes at the meeting of the board of directors.

U.S. GAAP provides guidance on the identification of variable interest entity (“VIE”) and financial reporting for entities over which control is achieved through means other than voting interests. The Company evaluates each of its interests in an entity to determine whether or not the investee is a VIE and, if so, whether the Company is the primary beneficiary of such VIE. In determining whether the Company is the primary beneficiary, the Company considers if the Company (1) has power to direct the activities that most significantly affects the economic performance of the VIE, and (2) receives the economic benefits of the VIE that could be significant to the VIE. If deemed the primary beneficiary, the Company consolidates the VIE. Sino-Global Shipping Agency Ltd., a PRC corporation (“Sino-China”), is considered a VIE, with the Company as the primary beneficiary. The Company, through Trans Pacific Beijing, entered into certain agreements with Sino-China, pursuant to which the Company receives 90% of Sino-China’s net income. The Company does not receive any payments from Sino-China unless Sino-China recognizes net income during its fiscal year. These agreements do not entitle the Company to any consideration if Sino-China incurs a net loss during its fiscal year. If Sino-China incurs a net loss during its fiscal year, the Company is not required to absorb such net loss.

As a VIE, Sino-China’s revenues are included in the Company’s total revenues, and any loss from operations is consolidated with that of the Company. Because of contractual arrangements between the Company and Sino-China, the Company has a pecuniary interest in Sino-China that requires consolidation of the financial statements of the Company and Sino-China.

6

The Company has consolidated Sino-China’s operating results because the entities are under common control in accordance with ASC 805-10, “Business Combinations”. The agency relationship between the Company and Sino-China and its branches is governed by a series of contractual arrangements pursuant to which the Company has substantial control over Sino-China. Management makes ongoing reassessments of whether the Company remains the primary beneficiary of Sino-China. As mentioned elsewhere in this report, due to the worsening market conditions in the shipping industry, Sino-China’s shipping agency business suffered a significant decrease in revenue due to a reduced number of ships served. As a result, the Company has temporarily suspended this business. Sino-China is also providing services in other related business segments of the Company.

The carrying amount and classification of Sino-China’s assets and liabilities included in the Company’s unaudited condensed consolidated balance sheets were as follows:

| March 31, | June 30, | |||||||

| 2018 | 2017 | |||||||

| Total current assets | $ | 10,509,999 | $ | 9,327,990 | ||||

| Total assets | 10,650,688 | 9,472,651 | ||||||

| Total current liabilities | 12,785 | 4,517 | ||||||

| Total liabilities | 12,785 | 4,517 | ||||||

(c) Fair Value of Financial Instruments

We follow the provisions of ASC 820, Fair Value Measurements and Disclosures, which clarifies the definition of fair value, prescribes methods for measuring fair value, and establishes a fair value hierarchy to classify the inputs used in measuring fair value as follows:

Level 1 — Observable inputs such as unadjusted quoted prices in active markets for identical assets or liabilities available at the measurement date.

Level 2 — Inputs other than quoted prices that are observable for the asset or liability in active markets, quoted prices for identical or similar assets and liabilities in markets that are not active, inputs other than quoted prices that are observable, and inputs derived from or corroborated by observable market data.

Level 3 — Unobservable inputs that reflect management’s assumptions based on the best available information.

The carrying value of accounts receivable, other receivables, other current assets and current liabilities approximate their fair values because of the short-term nature of these instruments.

(d) Use of Estimates and Assumptions

The preparation of the Company’s unaudited condensed consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the dates of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Estimates are adjusted to reflect actual experience when necessary. Significant accounting estimates reflected in the Company’s unaudited condensed consolidated financial statements include revenue recognition, fair value of stock based compensation, cost of revenues, allowance for doubtful accounts, deferred income taxes, and the useful lives of property and equipment. Since the use of estimates is an integral component of the financial reporting process, actual results could differ from those estimates.

7

(e) Translation of Foreign Currency

The accounts of the Company and its subsidiaries, including Sino-China and each of its branches are measured using the currency of the primary economic environment in which the entity operates (the “functional currency”). The Company’s functional currency is the U.S. dollar (“USD”) while its subsidiaries in the PRC, including Sino-China, report their financial positions and results of operations in Renminbi (“RMB”). The accompanying unaudited condensed consolidated financial statements are presented in USD. Foreign currency transactions are translated into USD using the fixed exchange rates in effect at the time of the transaction. Generally, foreign exchange gains and losses resulting from the settlement of such transactions are recognized in the unaudited condensed consolidated statements of operations. The Company translates the foreign currency financial statements of Sino-China, Sino-Global Shipping Australia, Sino-Global Shipping Hong Kong, Sino-Global Shipping Canada, Trans Pacific Beijing, Trans Pacific Shanghai and Sino Ningbo in accordance with ASC 830-10, “Foreign Currency Matters”. Assets and liabilities are translated at current exchange rates quoted by the People’s Bank of China at the balance sheet dates and revenues and expenses are translated at average exchange rates in effect during the year. The resulting translation adjustments are recorded as other comprehensive income (loss) and accumulated other comprehensive loss as a separate component of equity of the Company, and also included in non-controlling interests.

The exchange rates as of March 31, 2018 and June 30, 2017 and for the three and nine months ended March 31, 2018 and 2017 are as follows:

| March 31, | June 30, | Three months ended March 31, | Nine months ended March 31, | |||||||||||||||||||||

| 2018 | 2017 | 2018 | 2017 | 2018 | 2017 | |||||||||||||||||||

| Foreign currency | Balance Sheet | Balance Sheet | Profits/Loss | Profits/Loss | Profits/Loss | Profits/Loss | ||||||||||||||||||

| RMB:1USD | 6.2753 | 6.7806 | 6.3589 | 6.8885 | 6.5482 | 6.7960 | ||||||||||||||||||

| AUD:1USD | 1.3020 | 1.3028 | 1.2722 | 1.3196 | 1.2799 | 1.3249 | ||||||||||||||||||

| HKD:1USD | 7.8448 | 7.8059 | 7.8268 | 7.7604 | 7.8164 | 7.7582 | ||||||||||||||||||

| CAD:1USD | 1.2896 | 1.2982 | 1.2640 | 1.3233 | 1.2627 | 1.3210 | ||||||||||||||||||

(f) Cash and Cash Equivalents

Cash and cash equivalents consist of cash on hand and other highly liquid investments which are unrestricted as to withdrawal or use, and which have an original maturity of three months or less when purchased. The Company maintains cash and cash equivalents with various financial institutions mainly in the PRC, Australia, Hong Kong, Canada and the U.S. As of March 31, 2018 and June 30, 2017, cash balances of $7,413,222 and $6,246,337, respectively, were maintained at financial institutions in the PRC, which were not insured by any of the Chinese authorities. As of March 31, 2018 and June 30, 2017, cash balance of $2,077,680 and $2,462,792, respectively, were maintained at U.S. financial institutions, and were insured by the Federal Deposit Insurance Corporation or other programs subject to certain limitations.

(g) Receivables and Allowance for Doubtful Accounts

Accounts receivable are presented at net realizable value. The Company maintains allowances for doubtful accounts and for estimated losses. The Company reviews the accounts receivable on a periodic basis and makes general and specific allowances when there is doubt as to the collectability of individual receivable balances. In evaluating the collectability of individual receivable balances, the Company considers many factors, including the age of the balances, customers’ historical payment history, their current credit-worthiness and current economic trends. Receivables are considered past due after 180 days. Accounts Receivable are written off against the allowances only after exhaustive collection efforts.

Other receivables represent mainly prepaid employee insurance and welfare benefits, which will be subsequently deducted from the employee payroll, guarantee deposits on behalf of ship owners as well as office lease deposits.

8

(h) Property and Equipment, net

Net property and equipment are stated at historical cost less accumulated depreciation. Historical cost comprises the asset’s purchase price and any directly attributable costs of bringing the asset to its working condition and location for its intended use. Depreciation is calculated on a straight-line basis over the following estimated useful lives:

| Buildings | 20 years | |

| Motor vehicles | 5-10 years | |

| Furniture and office equipment | 3-5 years | |

| Leasehold improvements | Shorter of lease term or useful life |

The carrying value of a long-lived asset is considered impaired by the Company when the anticipated undiscounted cash flows from such asset are less than the asset’s carrying value. If impairment is identified, a loss is recognized based on the amount by which the carrying value exceeds the fair value of the long-lived asset. Fair value is determined primarily using the anticipated cash flows discounted at a rate commensurate with the risk involved or based on independent appraisals. Management has determined that there were no impairments as of the balance sheet dates.

(i) Intangible Assets, net

Intangible assets are recorded at cost less accumulated amortization. Amortization is calculated on a straight-line basis over the following estimated useful lives:

| Software | 3-5 years |

The Company evaluates intangible assets for impairment whenever events or changes in circumstances indicate that the assets might be impaired. There was no such impairment as of March 31, 2018.

(j) Revenue Recognition

Revenue is recognized when all of the following have occurred: (i) persuasive evidence of an arrangement exists, (ii) delivery has occurred or services have been rendered, (iii) the price is fixed or determinable, and (iv) the ability to collect is reasonably assured

| ● | Revenues from inland transportation management services are recognized when commodities are being released from the customers’ warehouse. |

| ● | Revenues from freight logistics services are recognized when the related contractual services are rendered. |

| ● | Revenues from container trucking services are recognized when the related contractual services are rendered. |

| ● | Revenues from bulk cargo container services are recognized when the related contractual services are rendered. Bulk cargo container services included shipping of products, arranging cargo container shipping from U.S. to China port. Revenue is recognized upon completion of shipping arrangements agreed with customers at customer’s designated port. |

9

(k) Taxation

Because the Company and its subsidiaries and Sino-China are incorporated in different jurisdictions, they file separate income tax returns. The Company uses the asset and liability method of accounting for income taxes in accordance with U.S. GAAP. Deferred taxes, if any, are recognized for the future tax consequences of temporary differences between the tax basis of assets and liabilities and their reported amounts in the unaudited condensed consolidated financial statements. A valuation allowance is provided against deferred tax assets if it is more likely than not that the asset will not be utilized in the future.

The Company recognizes the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. The Company recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense.

Income tax returns for the years prior to 2014 are no longer subject to examination by U.S. tax authorities.

On December 22, 2017, the “Tax Cuts and Jobs Act” (the “Act”) was enacted. Under the provisions of the Act, the U.S. corporate tax rate decreased from 35% to 21%. As the Company has a June 30 fiscal year-end, the lower corporate income tax rate will be phased in, resulting in a U.S. statutory federal rate of approximately 28% for our fiscal year ending June 30, 2018, and 21% for subsequent fiscal years. Additionally, the Tax Act imposes a one-time transition tax on deemed repatriation of historical earnings of foreign subsidiaries, and future foreign earnings are subject to U.S. taxation. The change in rate has caused us to re-measure all U.S. deferred income tax assets and liabilities for temporary differences and net operating loss (“NOL”) carryforwards and recorded one time income tax payable to be paid over 8 years.

PRC Enterprise Income Tax

PRC enterprise income tax is calculated based on taxable income determined under the PRC Generally Accepted Accounting Principles (“PRC GAAP”) at 25%. Sino-China and Trans Pacific are registered in PRC and governed by the Enterprise Income Tax Laws of the PRC.

PRC Business Tax and Surcharges

Revenues from services provided by the Company’s PRC subsidiaries and affiliates, including Sino-China and Trans Pacific are subject to the PRC business tax of 5%. Business tax and surcharges are paid on gross revenues generated minus the costs of services which are paid on behalf of the customers.

Enterprises or individuals who sell commodities, engage in services or selling of goods in the PRC are subject to a value added tax (“VAT”) in accordance with PRC laws. All of the Company’s revenue generated in the PRC are subject to a VAT on the gross sales price. The VAT rates are 6% and 11%, depending on the type of services provided. The Company is entitled to a deduction or offset for VAT paid on the services rendered by the vendors against the VAT when the Company engage in services.

In addition, under PRC regulations, the Company’s PRC subsidiaries and affiliates are required to pay city construction taxes (7%) and education surcharges (3%) based on calculated business tax payments.

The Company’s PRC subsidiaries and affiliates report revenues net of PRC’s VAT, business tax and surcharges for all the periods presented in the consolidated statements of operations.

10

(l) Earnings per Share

Basic earnings per share is computed by dividing net income attributable to holders of common shares of the Company by the weighted average number of common shares of the Company outstanding during the applicable period. Diluted earnings per share reflect the potential dilution that could occur if securities or other contracts to issue common shares of the Company were exercised or converted into common shares of the Company. Common share equivalents are excluded from the computation of diluted earnings per share if their effects would be anti-dilutive.

For the three and nine months ended March 31, 2018, the basic average shares outstanding and diluted average shares of the Company outstanding were not the same because the effect of potential shares of common stock of the Company was dilutive since the exercise prices for options were lower than the average market price for the related periods. For the three and nine months ended March 31, 2018, a total of 34,686 and 46,283 unexercised options were dilutive and were included, respectively, in the computation of diluted earnings per share. For the three and nine months ended March 31, 2017, a total of 34,782 and 20,621 unexercised options were dilutive, respectively, and were included in the computation of diluted EPS.

(m) Comprehensive Income (loss)

The Company reports comprehensive income (loss) in accordance with the Financial Accounting Standards Board (“FASB”) issued authoritative guidance which establishes standards for reporting comprehensive income (loss) and its component in financial statements. Comprehensive income (loss), as defined, includes all changes in equity during a period from non-owner sources.

(n) Stock-based Compensation

Stock-based payment transactions with employees are measured on the grant-date fair value of the equity instrument issued and recognized as compensation expense over the requisite service period. Valuations are based upon highly subjective assumptions about the future, including stock price volatility and exercise patterns. The fair value of share-based payment awards was estimated using the Black-Scholes option pricing model. Expected volatilities are based on the historical volatility of the Company’s stock. The Company uses historical data to estimate option exercise and employee terminations. The expected term of options granted represents the period of time that options granted are expected to be outstanding. The risk-free rate for periods within the expected life of the option is based on the U.S. Treasury yield curve in effect at the time of the grant.

(o) Risks and Uncertainties

The Company’s business, financial position and results of operations may be influenced by the political, economic, and legal environments in the PRC, as well as by the general state of the PRC economy. The Company’s operations in the PRC are subject to special considerations and significant risks not typically associated with companies in North America and Western Europe. These include risks associated with, among others, the political, economic and legal environment and foreign currency exchange. The Company’s results may be adversely affected by changes in the political, regulatory and social conditions in the PRC, and by changes in governmental policies or interpretations with respect to laws and regulations, anti-inflationary measures, currency conversion, remittances abroad, and rates and methods of taxation, among other things. Moreover, the Company’s ability to grow its business and maintain its profitability could be negatively affected by the nature and extent of services provided to its major customers, Tianjin Zhiyuan Investment Group Co., Ltd. (the “Zhiyuan Investment Group”) and Tengda Northwest Ferroalloy Co., Ltd. (“Tengda Northwest”).

(p) Reclassification

Certain prior periods amounts have been reclassified to conform to the current period presentation, including reclassification of $504,815 revenue and $504,815 cost of revenue from freight logistics service segment to bulk cargo container service segment. These reclassifications have no effect on the results of operations and cash flows.

(q) Recent Accounting Pronouncements

Revenue Recognition: In May 2014, the FASB issued Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers: Topic 606 (ASU 2014-09), to supersede nearly all existing revenue recognition guidance under U.S. GAAP. The core principle of ASU 2014-09 is to recognize revenues when promised goods or services are transferred to customers in an amount that reflects the consideration that is expected to be received for those goods or services. ASU 2014-09 defines a five step process to achieve this core principle and, in doing so, it is possible more judgment and estimates may be required within the revenue recognition process than are required under existing U.S. GAAP, including identifying performance obligations in the contract, estimating the amount of variable consideration to include in the transaction price and allocating the transaction price to each separate performance obligation. ASU 2014-09 is effective for the Company in the first quarter of fiscal year 2018 using either of two methods: (i) retrospective to each prior reporting period presented with the option to elect certain practical expedients as defined within ASU 2014-09 (full retrospective method); or (ii) retrospective with the cumulative effect of initially applying ASU 2014-09 recognized at the date of initial application and providing certain additional unaudited condensed as defined per ASU 2014-09 (modified retrospective method). The Company is currently assessing the impact to its unaudited condensed financial statements, and has not yet selected a transition approach.

11

Leases: In February 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842) (“ASU 2016-2”), which provides guidance on lease amendments to the FASB Accounting Standard Codification. This ASU will be effective for us beginning in May 1, 2019. The Company is currently in the process of evaluating the impact of the adoption of ASU 2016-2 on unaudited condensed financial statements.

Statement of Cash Flows: In August 2016, the FASB issued ASU 2016-15, Statement of Cash Flows (Topic 230): The amendments in this Update apply to all entities, including both business entities and not-for-profit entities that are required to present a statement of cash flows under Topic 230. The amendments in this Update provide guidance on the following eight specific cash flow issues. The amendments are an improvement to GAAP because they provide guidance for each of the eight issues, thereby reducing the current and potential future diversity in practice described above. ASU 2016-15 is effective for the Company for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years. Early adoption is permitted, including adoption in an interim period. The Company is still evaluating the effect that this guidance will have on the Company’s unaudited condensed financial statements and related disclosures.

Business Combination: In January 2017, the FASB issued Accounting Standards Update No. 2017-01, Business Combinations (Topic 805): Clarifying the Definition of a Business (ASU 2017-01), which revises the definition of a business and provides new guidance in evaluating when a set of transferred assets and activities is a business. This guidance will be effective for us in the fiscal year beginning after December 15, 2017 and interim periods within those periods on a prospective basis, and early adoption is permitted. The Company does not expect the standard to have a material impact on its consolidated financial statements.

Stock-based Compensation: In May 2017, the FASB issued ASU No. 2017-09, “Compensation—Stock compensation (Topic 718): Scope of modification accounting” (“ASU 2017-09”). The purpose of the amendment is to clarify which changes to the terms or conditions of a share-based payment award require an entity to apply modification accounting. For all entities that offer share based payment awards, ASU 2017-09 is effective for interim and annual reporting periods beginning after December 15, 2017. The Company is currently assessing the impact of ASU 2017-09 on its unaudited condensed financial statements.

Stock-based Compensation: In July 2017, the FASB issued ASU 2017-11, “Earnings Per Share (Topic 260)”, Distinguishing Liabilities from Equity (Topic 480), Derivatives and Hedging (Topic 815). The amendments in Part I of this Update change the classification analysis of certain equity-linked financial instruments (or embedded features) with down round features. When determining whether certain financial instruments should be classified as liabilities or equity instruments, a down round feature no longer precludes equity classification when assessing whether the instrument is indexed to an entity’s own stock. The amendments also clarify existing disclosure requirements for equity-classified instruments. The amendments in Part II of this Update recharacterize the indefinite deferral of certain provisions of Topic 480 that now are presented as pending content in the Codification, to a scope exception. Those amendments do not have an accounting effect. For public business entities, the amendments in Part I of this Update are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018. Early adoption is permitted for all entities, including adoption in an interim period. If an entity early adopts the amendments in an interim period, any adjustments should be reflected as of the beginning of the fiscal year that includes that interim period. The Company does not expect that the adoption of this guidance will have a material impact on its unaudited condensed financial statements.

Revenue Recognition and Leases: In September 2017, the FASB issued ASU 2017-13, Revenue from Contracts with Customers (Topic 606) and Leases (Topic 842). The main objective of this pronouncement is to clarify the effective date of the adoption of ASC Topic 606 and ASC Topic 842 and the definition of public business entity as stipulated in ASU 2014-09 and ASU 2016-02. ASU 2014-09 provides that a public business entity and certain other specified entities adopt ASC Topic 606 for annual reporting periods beginning after December 15, 2017, including interim reporting periods within that reporting period. All other entities are required to adopt ASC Topic 606 for annual reporting periods beginning after December 15, 2018, and interim reporting periods within annual reporting periods beginning after December 15, 2019. ASU 2016-12 requires that “a public business entity and certain other specified entities adopt ASC Topic 842 for fiscal years beginning after December 15, 2018, and interim periods within those fiscal years. All other entities are required to adopt ASC Topic 842 for fiscal years beginning after December 15, 2019, and interim periods within fiscal years beginning after December 15, 2020”. ASU 2017-13 clarifies that the SEC would not object to certain public business entities electing to use the non-public business entities effective dates for applying ASC 606 and ASC 842. ASU 2017-13, however, limits such election to certain public business entities that “otherwise would not meet the definition of a public business entity except for a requirement to include or inclusion of its financial statements or financial information in another entity’s filings with the SEC”. Management does not expect the adoption of ASU 2017-13 to have any material impact on its financial positions and results of operations or cash flows.

Income taxes: In March 2018, the FASB issued ASU 2018-05 — Income Taxes (Topic 740): Amendments to SEC Paragraphs Pursuant to SEC Staff Accounting Bulletin No. 118 (“ASU 2018-05”), which amends the FASB Accounting Standards Codification and XBRL Taxonomy based on the Tax Cuts and Jobs Act (the “Act”) that was signed into law on December 22, 2017 and Staff Accounting Bulletin No. 118 (“SAB 118”) that was released by the Securities and Exchange Commission. The Act changes numerous provisions that impact U.S. corporate tax rates, business-related exclusions, and deductions and credits and may additionally have international tax consequences for many companies that operate internationally. The Company has evaluated the impact of the Act as well as the guidance of SAB 118 and incorporated the changes into the determination of a reasonable estimate of its deferred tax liability and appropriate disclosures in the notes to its consolidated financial statements (See Note 9). The Company will continue to evaluate the impact this tax reform legislation may have on its results of operations, financial position, cash flows and related disclosures.

Except for the ASU’s described above, no ASU’s are expected to have a material impact on the unaudited condensed consolidated financial statements upon adoption.

12

Note 3. ACCOUNTS RECEIVABLE, NET

The Company’s net accounts receivable is as follows:

| March 31, | June 30, | |||||||

| 2018 | 2017 | |||||||

| Trade accounts receivable | $ | 6,108,078 | $ | 2,754,962 | ||||

| Less: allowances for doubtful accounts | (1,350,531 | ) | (185,821 | ) | ||||

| Accounts receivables, net | $ | 4,757,547 | $ | 2,569,141 | ||||

Movement of allowance for doubtful accounts is as follows:

Nine months ended March 31, | Year ended June 30, | |||||||

| Beginning balance | $ | 185,821 | $ | 207,028 | ||||

| Provision for doubtful accounts | 1,182,832 | - | ||||||

| Less: write-off/recovery | (24,638 | ) | (18,912 | ) | ||||

| Exchange rate effect | 6,516 | (2,295 | ) | |||||

| Ending balance | $ | 1,350,531 | $ | 185,821 | ||||

For the three and nine months ended March 31, 2018, the provision for doubtful accounts increased by $586,547 and $1,182,832, respectively. No provision was made in same period 2017.

Note 4. ADVANCES TO SUPPLIERS

The Company’s advances to third - party suppliers are as follows:

| March 31, | June 30, | |||||||

| 2018 | 2017 | |||||||

| Intelligent logistics system deposit | $ | 437,356 | $ | - | ||||

| Freight fees | - | 29,960 | ||||||

| Others | 4,781 | 24,930 | ||||||

| Total advances to suppliers - third parties | $ | 442,137 | $ | 54,890 | ||||

On December 27, 2017, with the approval of the Board of the Company, the Company signed a contract with Tianjin Anboweiye Technology Ltd Co.(“Tianjin Anboweiye”), to develop a more complete and intelligent system based on the Company’s current container trucking platform. The purpose is to help the Company make better connections with the system used by state-owned companies in China, and to satisfy such state-owned companies’ demand for container trucks in the United States. The Company made $437,356 as prepayment to Tianjin Anboweiye in March, 2018.

As of March 31, 2018, advances to third-party suppliers were primarily related to freight logistics services.

13

The Company’s advances to related-party suppliers are as follows:

| March 31, | June 30, | |||||||

| 2018 | 2017 | |||||||

| Freight fees | $ | 3,601,421 | $ | 3,333,038 | ||||

| Total advances to suppliers - related party | $ | 3,601,421 | $ | 3,333,038 | ||||

As discussed in Note 1, on February 18, 2017, the Company entered into a cooperative transportation agreement with Zhiyuan Hong Kong, which is owned by the Company’s largest shareholder. Pursuant to this agreement, the Company will be a supplier for part of the project’s logistics solutions and, in return, the Company will receive a 1% to 1.25% fee incurred as a commission for its services rendered. On July 7, 2017, the Company signed a supplemental agreement, pursuant to which the Company will cooperate with Zhiyuan Hong Kong exclusively on the Project’s transportation needs with respect to transporting construction materials from manufacturers to the port of Malaysia and to the factory site. Pursuant to the supplemental agreement, the Company agrees to make prepayments to Zhiyuan Hong Kong for its share of packaging and transporting costs related to the Project; in return the Company will receive 15% of the cost incurred in the Project from Zhiyuan Hong Kong as a service fee. The Company will complete its services pursuant to the supplemental agreement and will receive approval from Zhiyuan Hong Kong that the related services fees will be earned by June 2018. The Company also expects the entire advance will be collected by October 2018.

Note 5. PREPAID EXPENSES AND OTHER ASSETS

The Company’s prepaid expenses and other current assets are as follows:

| March 31, | June 30, | |||||||

| 2018 | 2017 | |||||||

| Consultant fees (1) | $ | 39,537 | $ | 158,150 | ||||

| Advance to employees | 74,199 | 64,160 | ||||||

| Other (including prepaid insurance, rent , public relation services) | 283,632 | 95,708 | ||||||

| Total | 397,368 | 318,018 | ||||||

| Less: current portion | 397,368 | 311,136 | ||||||

| Total noncurrent portion | $ | - | $ | 6,882 | ||||

(1) The Company entered into a management consulting services agreement with a consulting company on November 12, 2015, pursuant to which the consulting company shall assist the Company with its regulatory filings during the period from July 1, 2016 to June 30, 2018. In return for its services, as approved by the Board, a total of RMB 2,100,000 ($316,298) was paid to the consulting company. The above-mentioned consulting fees have been and will be ratably charged to expense over the terms of the above-mentioned agreement.

14

Note 6. PROPERTY AND EQUIPMENT, NET

The Company’s net property and equipment as follows:

| March 31, | June 30, | |||||||

| 2018 | 2017 | |||||||

| Land and Buildings | $ | 214,497 | $ | 198,512 | ||||

| Motor vehicles | 632,130 | 542,471 | ||||||

| Computer equipment | 161,440 | 155,141 | ||||||

| Office equipment | 88,392 | 66,097 | ||||||

| Furniture and fixtures | 169,234 | 163,219 | ||||||

| System software | 126,787 | 117,733 | ||||||

| Leasehold improvements | 386,629 | 62,857 | ||||||

| Total | 1,779,109 | 1,306,030 | ||||||

| Less: Accumulated depreciation | 1,242,827 | 1,118,657 | ||||||

| Property and equipment, net | $ | 536,282 | $ | 187,373 | ||||

Depreciation expense for the three months ended March 31, 2018 and 2017 were $15,827 and $11,025, respectively.

Depreciation expense for the nine months ended March 31, 2018 and 2017 were $42,291 and $36,432, respectively.

Note 7. INTANGIBLE ASSETS, NET

Net intangible assets consisted of the following at:

| March 31, | June 30, | |||||||

| 2018 | 2017 | |||||||

| Full service logistics platforms | $ | 190,000 | $ | - | ||||

| Total intangible assets | 190,000 | - | ||||||

| Less: Accumulated amortization | 21,111 | - | ||||||

| Intangible asset, net | $ | 168,889 | $ | - | ||||

As part of the above-mentioned intelligent logistics platform (see Note 3), four information applications were completed by Tianjin Anboweiye in November 2017 and placed into service, including route planning and route execution for customers in China. The platforms are amortized over five years.

Amortization expense of intangible assets amounted to $15,833 and $nil for the three months ended March 31, 2018 and 2017, respectively, and $21,111 and $nil for the nine months ended March 31, 2018 and 2017, respectively.

15

Note 8. STOCK OPTIONS

The issuance of the Company’s options is exempted from registration under of the Securities Act of 1933, as amended (the “Act”). The Common Stock underlying the Company’s options granted may be sold in compliance with Rule 144 under the Act. Each option may be exercised to purchase one share of the common stock of the Company, no par value per share (the “Common Stock”). Payment for the options may be made in cash or by exchanging shares of Common Stock at their fair market value. The fair market value will be equal to the average of the highest and lowest registered sales prices of Company Stock on the date of exercise.

The term of the options granted in 2009 is for 10 years and the exercise price of the 56,000 options is $7.75 which vested over 5 years and were fully vested as of March 31, 2018. The fair value of the stock options was estimated using the Black-Scholes option-pricing model.

The term of the 10,000 options granted in 2013 is for 10 years and the exercise price of the options is $2.01. The fair value of the 10,000 stock options was calculated at the grant date using the Black-Scholes option-pricing model with the following assumptions: volatility of 452.04%, risk free interest rate of 0.88% and expected life of 10 years. The total fair value of the options was $19,400. These options are fully vested as of March 31, 2018.

Pursuant to the Company’s 2014 Stock Incentive Plan, effective on July 26, 2016, the Company granted options to purchase a total of 150,000 shares of the Company’s Common Stock to two employees with a one-year vesting period, one half of which vested on October 26, 2016, and the other half vested on July 26, 2017. The exercise price of the options is $1.10, which was equal to the share price of the Company’s Common Stock on July 26, 2016. The grant date fair value of such options was $0.77 per share. The fair value of the options was calculated using the Black-Scholes options pricing model with the following assumptions: volatility of 99.68%, risk free interest rate of 1.15%, and expected life of 5 years. The total fair value of the options was $115,979. In accordance with the vesting periods, $nil and $28,995 were expensed related to these options for the three months ended March 31, 2018 and 2017, respectively. $9,665 and $77,320 were expensed related to these options for the nine months ended March 31, 2018 and 2017, respectively. In February 2017, 75,000 of these options were exercised by the two employees.

Pursuant to the Company’s 2014 Stock Incentive Plan, the Company granted a total of 800,000 options on December 14, 2016, to purchase an aggregate of 800,000 shares of Common Stock to seven employees, with a vesting period from one to three years. The grant date fair value of such options was $2.24 per option. The fair value of the options was calculated using the Black-Scholes options pricing model with the following assumptions: volatility of 112.70%, risk free interest rate of 2.02%, with an expected life of 5 years. The total fair value of the options was $1,788,985. With the seven employees’ consent, the Company cancelled the 800,000 options, effective February 16, 2017 and nil was recorded for these options for the three and nine months ended March 31, 2018 and 2017, respectively.

A summary of the options is presented in the table below:

| Shares | Weighted Average Exercise Price | |||||||

| Options outstanding, as of June 30, 2017 | 141,000 | $ | 3.81 | |||||

| Granted | - | - | ||||||

| Exercised | - | - | ||||||

| Cancelled | - | - | ||||||

| Options outstanding, as of March 31, 2018 | 141,000 | $ | 3.81 | |||||

| Options exercisable, as of March 31, 2018 | 139,000 | $ | 3.83 | |||||

16

Following is a summary of the status of options outstanding and exercisable as of March 31, 2018

| Outstanding Options | Exercisable Options | |||||||||||||||||

| Exercise Price | Number | Average Remaining Contractual Life | Average Exercise Price | Number | Average Remaining Contractual Life | |||||||||||||

| $ | 7.75 | 56,000 | 0.13 years | $ | 7.75 | 56,000 | 0.13 years | |||||||||||

| $ | 2.01 | 10,000 | 4.84 years | $ | 2.01 | 8,000 | 4.84 years | |||||||||||

| $ | 1.10 | 75,000 | 3.32 years | $ | 1.10 | 75,000 | 3.32 years | |||||||||||

| 141,000 | 139,000 | |||||||||||||||||

Note 9. EQUITY TRANSACTIONS

On June 6, 2014, the Company entered into management consulting and advisory services agreements with two consultants, pursuant to which the consultants assisted the Company in, among other things, financial and tax due diligence, business evaluation and integration, and development of pro forma financial statements. In return for their services, as approved by the Company’s Board of Directors, a total of 600,000 shares of the Company’s common stock were to be issued to these two consultants. In June 2014, 200,000 shares of the Company’s common stock were issued to the consultants as a prepayment for their services. The value of their consulting services was determined using the fair value of the Company’s common stock of $2.34 per share when the shares were issued to the consultants. Their service agreements were for the period July 1, 2014 to December 31, 2016. The remaining 400,000 shares of the Company’s common stock were then issued to the consultants on September 30, 2014 at $1.68 per share, and the service terms are from September 2014 to November 2016. These shares were valued at $1,140,000 and the related consulting fees have been ratably charged to expense over the term of the agreements. Consulting expenses for the above services were $nil and $nil for the three months ended March 31, 2018 and 2017, respectively. Consulting expenses for the above services were $nil and $218,045 for the nine months ended March 31, 2018 and 2017, respectively.

On May 5, 2015, the Company entered into management consulting and advisory services agreements with three consultants, pursuant to which the consultants assisted the Company in, among other things, review of time charter agreements; crew management advisory; development of permanent and preventive maintenance standards related to dry dockings and ship repairs; development of regular technical and marine vessel inspections and quality control procedures; and development and implementation of alternative remedial actions to address technical problems that may arise. In return for their services, as approved by the Company’s Board of Directors, a total of 500,000 shares of the Company’s common stock were to be issued to these three consultants at $1.50 per share. Their service agreements are for a period of 18 months, effective May 2015. These shares were valued at $750,000 and the related consulting fees have been ratably charged to expense over the term of the agreements. Consulting expenses for the above services were $nil and $ nil for the three months ended March 31, 2018 and 2017, respectively. Consulting expenses for the above services were $nil and $173,137 for the nine months ended March 31, 2018 and 2017, respectively

On December 9, 2015, the Company entered into a consulting and advisory services agreement with a consultant, pursuant to which the consultant will assist the Company with corporate restructuring, business evaluation and capitalization during the period from November 20, 2015 to November 19, 2016. In return for such services, the Company issued 250,000 shares of the Company’s common stock to this consultant for services to be rendered during the first half of the service period. Such shares were issued as restricted shares at $1.02 per share on December 9, 2015. On May 23, 2016, the Company issued an additional 250,000 shares of common stock to this consultant at $0.72 per share to cover the services from the seventh month to November 19, 2016. These shares were valued at $435,000. Consulting expenses were $nil and $ nil for the three months ended March 31, 2018 and 2017, respectively. Consulting expenses were $nil and $138,387 for the nine months ended March 31, 2018 and 2017, respectively.

17

In March 2017, the Company entered into a consulting and advisory services agreement with Jianwei Li, who will provide management consulting services that include marketing program designing and implementation and cooperative partner selection and management. The service period is from March 2017 to February 2020. The Company issued 250,000 shares of common stock as the remuneration for the services, which were issued as restricted shares at $2.53 per share on March 22, 2017 to the consultant. These shares were valued at $632,500. Consulting expenses were $52,708 and $17,569 for the three months ended March 31, 2018 and 2017 respectively. Consulting expenses were $158,125 and $17,569 for the nine months ended March 31, 2018 and 2017, respectively.

On October 23, 2017, the Company issued 130,000 shares to its employees of its restricted common stock valued at $2.80 per share. Quarter of the total number of common shares shall become vested on each of November 16, 2017, February 16, 2018, May 16, 2018 and August 16, 2018. These shares were valued at $364,000. $91,000 and $nil are recorded in the Company’s general and administrative expenses for the three months ended March 31, 2018 and 2017, respectively. $182,000 and $nil are recorded in the Company’s general and administrative expenses for the nine months ended March 31, 2018 and 2017, respectively.

On October 27, 2017, the Company issued 200,000 shares of restricted common stock on the grant date with a fair value of $548,000 to a consulting company pursuant to a consulting agreement. The scope of services primarily covers advising on business development, strategic planning and compliance during the one-year service period from October 17, 2017 to October 16, 2018. Consulting expenses were $137,000 and $nil for the three months ended March 31, 2018 and 2017, respectively. Consulting expenses were $274,000 and $nil for the nine months ended March 31, 2018 and 2017, respectively.

Total consulting expenses were $280,709 and $17,569 for the three months ended March 31, 2018 and 2017, respectively. Total consulting expenses were $432,125 and $547,138 for the nine months ended March 31, 2018 and 2017, respectively.

On March 12, 2018, the Company entered into a Securities Purchase Agreement with investors pursuant to which the Company sold to the investors in a registered direct offering, an aggregate of 2,000,000 shares of the common stock of the Company, no par value per share, at a purchase price of $1.50 per Share, for aggregate gross proceeds of $3 million. The placement agent received a cash commission fee equal to 7.5% of the gross proceeds. The offering was closed on March 14, 2018. The offering of the shares of the 2 million common stock is being made pursuant to the Company’s effective shelf registration statement on Form S-3 (File No. 333-222098), which was originally filed with the SEC on December 15, 2017, and was declared effective by the SEC on February 16, 2018. The Company agreed in the purchase agreement that it would not issue any common stock for 60 calendar days following the closing of the offering and each of the Company’s executive officers and directors have agreed to a lock-up period of 60 days from the date of the purchase agreement.

The Company also agreed to sell to the investors Series “A” warrants to purchase up to an aggregate of 2,000,000 shares of common stock at an exercise price of $1.75 per share and Series “B” warrants to purchase up to an aggregate of 2,000,000 shares of common stock at an exercise price of $1.75 per share. The sale of the Series “A” warrants and Series “B” warrants are a private placement in reliance upon an exemption afforded under Regulation D of the Securities Act. The Series “A” warrants shall be initially exercisable beginning on September 14, 2018, and expire five and a half (5.5) years from the date of issuance. The Series B warrants shall be initially exercisable beginning on September 14, 2018, and expire thirteen (13) months from the date of issuance. The exercise price and the number of shares of Common Stock issuable upon exercise of the Warrants are subject to adjustment in the event of stock splits or dividends, or other similar transactions, but not as a result of future securities offerings at lower prices. Net proceeds to the Company from the sale of the shares and the warrants after deducting offering expenses and placement agent fees is $2,585,091.

On April 26, 2018, the Company filed a registration statement on Form S-1 to register the resale of an aggregate of 4,000,000 shares of common stock underlying the Series A and B Warrants mentioned above. The S-1 was declared effective by the SEC on May 8, 2018.

18

The warrants are classified as equity since they qualify for exception from derivative accounting as they are considered to be indexed to the Company’s own stock and require net share settlement. The fair value of the warrants of $1,074,140 is valued based on Black-Scholes-Merton model and is recorded as additional paid-in capital from common stock based on relative fair value of proceeds received using the following assumptions:

| Series A | Series B | |||||||

| Annual dividend yield | - | - | ||||||

| Expected life (years) | 5.5 | 1.08 | ||||||

| Risk-free interest rate | 2.72 | % | 2.16 | % | ||||

| Expected volatility | 110.31 | % | 73.88 | % | ||||

Following is a summary of the status of warrants outstanding and exercisable as of March 31, 2018:

| Shares | Weighted Average Exercise Price | |||||||

| Warrants outstanding, as of June 30, 2017 | 139,032 | $ | 9.30 | |||||

| Issued | 4,000,000 | 1.75 | ||||||

| Exercised | - | - | ||||||

| Expired | - | - | ||||||

| Warrants outstanding, as of March 31, 2018 | 4,139,032 | $ | 2.00 | |||||

| Warrants exercisable, as of March 31, 2018 | 139,032 | $ | 9.30 | |||||

| Warrants Outstanding | Warrants Exercisable | Weighted Average Exercise Price | Average Remaining Contractual Life | |||||||

| 2008 Warrants | 139,032 | $ | 9.30 | 0.13 years | ||||||

| 2018 Series A 2,000,000 | - | $ | 1.75 | 5.50 years | ||||||

| 2018 Series B 2,000,000 | - | $ | 1.75 | 1.08 years | ||||||

Note 10. NON-CONTROLLING INTEREST

The Company’s non-controlling interest consists of the following:

| March 31, | June 30, | |||||||

| 2018 | 2017 | |||||||

| Sino-China: | ||||||||

| Original paid-in capital | $ | 356,400 | $ | 356,400 | ||||

| Additional paid-in capital | 1,044 | 1,044 | ||||||

| Accumulated other comprehensive income | (41,198 | ) | 217,379 | |||||

| Accumulated deficit | (5,148,533 | ) | (5,421,578 | ) | ||||

| (4,832,287 | ) | (4,846,755 | ) | |||||

| Trans Pacific Logistics Shanghai Ltd. | 123,728 | 46,047 | ||||||

| ACH Trucking Center Corp. | - | 31,929 | ||||||

| Total | $ | (4,708,559 | ) | $ | (4,768,779 | ) | ||

19

Note 11. COMMITMENTS AND CONTINGENCY

Lease Obligations

The Company leases certain office premises and apartments for employees under operating lease agreements with various terms through April 16, 2020. Future minimum lease payments under the operating lease agreements are as follows:

| Amount | ||||

| Twelve months ending March 31, | ||||

| 2019 | $ | 165,170 | ||

| 2020 | 81,666 | |||

| $ | 246,836 | |||

Rental expenses for the three months ended March 31, 2018 and 2017 were $59,183 and $66,642, respectively. Rental expenses for the nine months ended March 31, 2018 and 2017 were $178,490 and $194,532, respectively.

Contingencies

The Labor Contract Law of the PRC requires employers to insure the liability of the severance payments for terminated employees that have worked for the employers for at least two years prior to January 1, 2008. Employers are liable for one month of severance pay per year of service provided by employees. As of March 31, 2018 and June 30, 2017, the Company has estimated its severance payments to be approximately $58,373 and $48,713, respectively. Such payments have not been reflected in its unaudited condensed consolidated financial statements because management cannot predict what the actual payment, if any, will be in the future.

From time to time, the Company is involved in routine litigation that arises in the ordinary course of business. The Company was named a defendant in a breach of service contract lawsuit filed with the California Superior Court on January 19, 2018. Management believes it is too early to predict the outcome of the pending lawsuit but believes it will not likely have a material effect on the Company’s consolidated operations or financial position.

Note 12. INCOME TAXES

On December 22, 2017, the “Tax Cuts and Jobs Act” (the “Act”) was enacted. Under the provisions of the Act, the U.S. corporate tax rate decreased from 35% to 21%. Since the Company has a June 30 fiscal year-end, a blended U.S. statutory federal rate of approximately 28% for the fiscal year ending June 30, 2018 is applied to the provision for income tax, and a 21% for subsequent fiscal years.

The Company re-measured certain deferred tax assets based on blended rate of 28% at which these deferred tax amounts are expected to reverse in the future and the re-measurement resulted in a tax expense of $120,400 being recognized during the three months ended March 31, 2018.

In addition, the Company recorded a provisional amount for its one-time transition tax for all of its foreign subsidiaries, resulting in an increase in income tax expense of approximately $478,000 for the nine months ended March 31, 2018. The one-time transition tax was calculated using the Company’s total post-1986 overseas earnings and profits which amounted to approximately $5.7 million. The one-time transition tax is taxed at the rate of 15.5% for the Company’s cash and cash equivalents and 8% for the other assets and is to be paid over 8 years.

The Company’s income tax benefit (expense) for the three and nine months ended March 31, 2018 and 2017 are as follows:

For the three months ended March 31, | For the nine months ended March 31, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Current | ||||||||||||||||

| USA | $ | - | $ | - | $ | (60,162 | ) | $ | - | |||||||

| Hong Kong | 6,250 | (36,966 | ) | (3,172 | ) | (71,067 | ) | |||||||||

| China | (69,345 | ) | (47,738 | ) | (320,270 | ) | (158,649 | ) | ||||||||

| One-time transition tax on accumulated foreign earnings | - | - | (478,499 | ) | - | |||||||||||

| (63,095 | ) | (84,704 | ) | (862,103 | ) | (229,716 | ) | |||||||||

| Deferred | ||||||||||||||||

| USA | (153,000 | ) | 387,900 | 920,700 | 387,900 | |||||||||||

| Total income tax benefit (expense) | $ | (216,095 | ) | $ | 303,196 | $ | 58,597 | $ | 158,184 | |||||||

The Company recorded income tax expense of $216,095 and benefit of $303,196 in the three months ended March 31, 2018 and 2017. The Company recorded income tax benefit of $58,597 and $158,184 in the nine months ended March 31, 2018 and 2017, respectively.

20

The Company’s deferred tax assets are comprised of the following:

| March 31, | June 30, | |||||||

| 2018 | 2017 | |||||||

| Allowance for doubtful accounts | $ | 568,000 | $ | 106,000 | ||||

| Stock-based compensation | 687,000 | 790,000 | ||||||

| Net operating loss | 1,068,000 | 1,464,000 | ||||||

| Total deferred tax assets | 2,323,000 | 2,360,000 | ||||||

| Valuation allowance | (652,900 | ) | (1,610,600 | ) | ||||

| Deferred tax assets, net - long-term | $ | 1,670,100 | $ | 749,400 | ||||