Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

þ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2018

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______________________ to __________________________

Commission File Number 001-31921

Compass Minerals International, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 36-3972986 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

9900 West 109th Street

Suite 100

Overland Park, KS 66210

(913) 344-9200

(Address of principal executive offices, zip code and telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes: þ No: ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes: þ No: ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

Emerging growth company ¨ | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes: ¨ No: þ

The number of shares outstanding of the registrant’s common stock, $0.01 par value per share, as of April 27, 2018, was 33,850,352 shares.

COMPASS MINERALS INTERNATIONAL, INC.

TABLE OF CONTENTS

Page | ||

PART I. FINANCIAL INFORMATION | ||

PART II. OTHER INFORMATION | ||

1

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

COMPASS MINERALS INTERNATIONAL, INC.

CONSOLIDATED BALANCE SHEETS

(in millions, except share data)

(Unaudited) | |||||||

March 31, 2018 | December 31, 2017 | ||||||

ASSETS | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 44.5 | $ | 36.6 | |||

Receivables, less allowance for doubtful accounts of $10.8 in 2018 and $10.9 in 2017 | 275.0 | 344.5 | |||||

Inventories | 217.2 | 289.9 | |||||

Other | 59.8 | 66.5 | |||||

Total current assets | 596.5 | 737.5 | |||||

Property, plant and equipment, net | 1,124.8 | 1,138.1 | |||||

Intangible assets, net | 138.0 | 143.6 | |||||

Goodwill | 402.8 | 405.0 | |||||

Investment in equity method investee | 24.6 | 24.6 | |||||

Other | 126.1 | 122.2 | |||||

Total assets | $ | 2,412.8 | $ | 2,571.0 | |||

LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||

Current liabilities: | |||||||

Current portion of long-term debt | $ | 32.3 | $ | 32.1 | |||

Accounts payable | 109.0 | 123.5 | |||||

Accrued expenses | 64.4 | 54.4 | |||||

Accrued salaries and wages | 18.6 | 23.9 | |||||

Income taxes payable | 21.1 | 25.9 | |||||

Accrued interest | 5.7 | 8.2 | |||||

Total current liabilities | 251.1 | 268.0 | |||||

Long-term debt, net of current portion | 1,218.2 | 1,330.4 | |||||

Deferred income taxes, net | 125.0 | 127.0 | |||||

Other noncurrent liabilities | 149.4 | 151.0 | |||||

Commitments and contingencies (Note 9) | |||||||

Stockholders’ equity: | |||||||

Common stock: $0.01 par value, 200,000,000 authorized shares; 35,367,264 issued shares | 0.4 | 0.4 | |||||

Additional paid-in capital | 103.7 | 102.5 | |||||

Treasury stock, at cost — 1,517,797 shares at March 31, 2018 and 1,539,763 shares at December 31, 2017 | (2.9 | ) | (2.9 | ) | |||

Retained earnings | 660.8 | 672.5 | |||||

Accumulated other comprehensive loss | (92.9 | ) | (77.9 | ) | |||

Total stockholders’ equity | 669.1 | 694.6 | |||||

Total liabilities and stockholders’ equity | $ | 2,412.8 | $ | 2,571.0 | |||

The accompanying notes are an integral part of the consolidated financial statements.

2

COMPASS MINERALS INTERNATIONAL, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited, in millions, except share and per share data)

Three Months Ended March 31, | |||||||

2018 | 2017 | ||||||

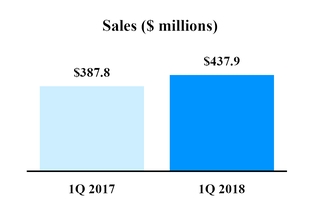

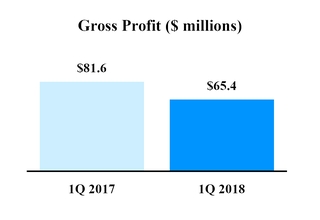

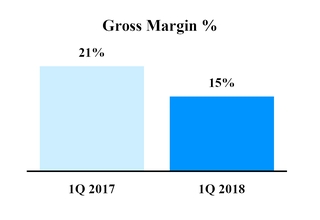

Sales | $ | 437.9 | $ | 387.8 | |||

Shipping and handling cost | 120.1 | 93.7 | |||||

Product cost | 252.4 | 212.5 | |||||

Gross profit | 65.4 | 81.6 | |||||

Selling, general and administrative expenses | 38.8 | 40.2 | |||||

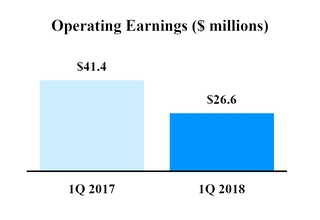

Operating earnings | 26.6 | 41.4 | |||||

Other expense (income): | |||||||

Interest expense | 13.7 | 13.7 | |||||

Net loss in equity investee | 0.1 | — | |||||

Other, net | (4.2 | ) | (0.1 | ) | |||

Earnings before income taxes | 17.0 | 27.8 | |||||

Income tax expense | 4.4 | 6.3 | |||||

Net earnings | $ | 12.6 | $ | 21.5 | |||

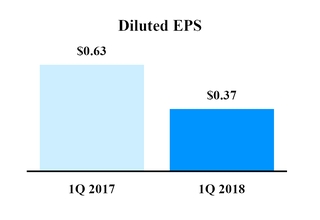

Basic net earnings per common share | $ | 0.37 | $ | 0.63 | |||

Diluted net earnings per common share | $ | 0.37 | $ | 0.63 | |||

Weighted-average common shares outstanding (in thousands): | |||||||

Basic | 33,836 | 33,802 | |||||

Diluted | 33,836 | 33,803 | |||||

Cash dividends per share | $ | 0.72 | $ | 0.72 | |||

The accompanying notes are an integral part of the consolidated financial statements.

3

COMPASS MINERALS INTERNATIONAL, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) INCOME

(Unaudited, in millions)

Three Months Ended March 31, | |||||||

2018 | 2017 | ||||||

Net earnings | $ | 12.6 | $ | 21.5 | |||

Other comprehensive income (loss): | |||||||

Unrealized gain from change in pension obligations, net of tax of $0.0 in both 2018 and 2017 | 0.1 | 0.1 | |||||

Unrealized loss on cash flow hedges, net of tax of $0.3 in both 2018 and 2017 | (0.5 | ) | (0.5 | ) | |||

Cumulative translation adjustment | (14.4 | ) | 14.8 | ||||

Comprehensive (loss) income | $ | (2.2 | ) | $ | 35.9 | ||

The accompanying notes are an integral part of the consolidated financial statements.

4

COMPASS MINERALS INTERNATIONAL, INC.

CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY

For the three months ended March 31, 2018

(Unaudited, in millions)

Common Stock | Additional Paid-In Capital | Treasury Stock | Retained Earnings | Accumulated Other Comprehensive Loss | Total | ||||||||||||||||||

Balance, December 31, 2017 | $ | 0.4 | $ | 102.5 | $ | (2.9 | ) | $ | 672.5 | $ | (77.9 | ) | $ | 694.6 | |||||||||

Comprehensive income (loss) | 12.6 | (14.8 | ) | (2.2 | ) | ||||||||||||||||||

Stranded tax effect from tax reform | 0.2 | (0.2 | ) | — | |||||||||||||||||||

Dividends on common stock | 0.1 | (24.5 | ) | (24.4 | ) | ||||||||||||||||||

Stock-based compensation | 1.1 | 1.1 | |||||||||||||||||||||

Balance, March 31, 2018 | $ | 0.4 | $ | 103.7 | $ | (2.9 | ) | $ | 660.8 | $ | (92.9 | ) | $ | 669.1 | |||||||||

The accompanying notes are an integral part of the consolidated financial statements.

5

COMPASS MINERALS INTERNATIONAL, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited, in millions)

Three Months Ended March 31, | |||||||

2018 | 2017 | ||||||

Cash flows from operating activities: | |||||||

Net earnings | $ | 12.6 | $ | 21.5 | |||

Adjustments to reconcile net earnings to net cash flows provided by operating activities: | |||||||

Depreciation, depletion and amortization | 34.3 | 28.4 | |||||

Finance fee amortization | 0.6 | 0.6 | |||||

Stock-based compensation | 1.1 | 1.3 | |||||

Deferred income taxes | 0.3 | (1.2 | ) | ||||

Gain on settlement of acquisition-related contingent consideration | — | (1.9 | ) | ||||

Other, net | 0.4 | (2.6 | ) | ||||

Changes in operating assets and liabilities: | |||||||

Receivables | 68.9 | 97.9 | |||||

Inventories | 71.3 | 44.4 | |||||

Other assets | 0.5 | (2.8 | ) | ||||

Accounts payable and accrued expenses | (17.8 | ) | (61.0 | ) | |||

Other liabilities | 0.8 | 0.6 | |||||

Net cash provided by operating activities | 173.0 | 125.2 | |||||

Cash flows from investing activities: | |||||||

Capital expenditures | (23.0 | ) | (21.0 | ) | |||

Other, net | (0.6 | ) | (1.3 | ) | |||

Net cash used in investing activities | (23.6 | ) | (22.3 | ) | |||

Cash flows from financing activities: | |||||||

Proceeds from revolving credit facility borrowings | 63.8 | 18.3 | |||||

Principal payments on revolving credit facility borrowings | (186.2 | ) | (101.7 | ) | |||

Proceeds from issuance of long-term debt | 16.0 | 10.9 | |||||

Principal payments on long-term debt | (5.6 | ) | (21.3 | ) | |||

Acquisition-related contingent consideration payment | — | (14.7 | ) | ||||

Dividends paid | (24.5 | ) | (24.4 | ) | |||

Deferred financing costs | (0.3 | ) | — | ||||

Proceeds received from stock option exercises | — | 0.2 | |||||

Other, net | — | 0.7 | |||||

Net cash used in financing activities | (136.8 | ) | (132.0 | ) | |||

Effect of exchange rate changes on cash and cash equivalents | (4.7 | ) | 0.6 | ||||

Net change in cash and cash equivalents | 7.9 | (28.5 | ) | ||||

Cash and cash equivalents, beginning of the year | 36.6 | 77.4 | |||||

Cash and cash equivalents, end of period | $ | 44.5 | $ | 48.9 | |||

Supplemental cash flow information: | |||||||

Interest paid, net of amounts capitalized | $ | 14.7 | $ | 14.4 | |||

Income taxes paid, net of refunds | $ | 5.0 | $ | 12.1 | |||

The accompanying notes are an integral part of the consolidated financial statements.

6

COMPASS MINERALS INTERNATIONAL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. | Accounting Policies and Basis of Presentation: |

Compass Minerals International, Inc. (“CMI”), through its subsidiaries (collectively, the “Company”), is a leading producer of essential minerals that solve nature’s challenges, including salt for winter roadway safety and other consumer, industrial and agricultural uses, specialty plant nutrition minerals that improve the quality and yield of crops, and specialty chemicals for water treatment and other industrial processes. The Company’s principal products are salt, consisting of sodium chloride and magnesium chloride, sulfate of potash (“SOP”), various micronutrient products, and specialty chemicals for water treatment and other industrial processes. The Company’s production sites are located in the United States (“U.S.”), Canada, Brazil and the United Kingdom (the “U.K.”). Except where otherwise noted, references to North America include only the continental U.S. and Canada, and references to the U.K. include only England, Scotland and Wales. References to “Compass Minerals,” “our,” “us” and “we” refer to CMI and its consolidated subsidiaries. The Company also provides records management services to businesses located in the U.K. In October 2016, the Company acquired Produquímica Indústria e Comércio S.A. (“Produquímica”), which operates two primary businesses in Brazil – agricultural productivity and chemical solutions.

CMI is a holding company with no significant operations other than those of its wholly-owned subsidiaries. The consolidated financial statements include the accounts of CMI and its wholly-owned subsidiaries. All significant intercompany balances and transactions have been eliminated in consolidation.

The Company uses the equity method of accounting for equity securities when it has significant influence or when it has more than a minor ownership interest or more than minor influence over an investee’s operations but does not have a controlling financial interest. Initial investments are recorded at cost (including certain transaction costs) and are adjusted by the Company’s share of the investees’ undistributed earnings and losses.

The accompanying unaudited consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete financial statements. These unaudited consolidated financial statements should be read in conjunction with the consolidated financial statements of the Company for the year ended December 31, 2017, as filed with the Securities and Exchange Commission in its Annual Report on Form 10-K. In the opinion of management, all adjustments, consisting of normal recurring adjustments considered necessary for a fair presentation, have been included.

The Company experiences a substantial amount of seasonality in its sales with respect to its deicing salt products. As a result, sales and operating income are generally higher in the first and fourth quarters and lower during the second and third quarters of each year. In particular, sales of highway and consumer deicing salt and magnesium chloride products vary based on the severity of the winter conditions in areas where the products are used. Following industry practice in North America and the U.K., the Company seeks to stockpile sufficient quantities of deicing salt throughout the second, third and fourth quarters to meet the estimated requirements for the upcoming winter season. Production of deicing salt can also vary based on the severity or mildness of the preceding winter season. Due to the seasonal nature of the deicing product lines, operating results for the interim periods are not necessarily indicative of the results that may be expected for the full year.

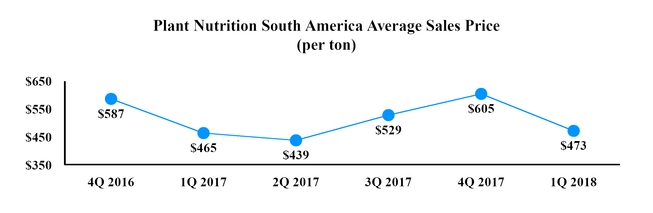

The Company’s plant nutrition business is also seasonal. For example, the strongest demand for the Company’s plant nutrition products in Brazil typically occurs during the spring planting season. As a result, the Company and its customers generally build inventories during the low demand periods of the year to ensure timely product availability during the peak sales season. The seasonality of this demand results in the Company’s sales volumes and sales for the Plant Nutrition South America segment usually being the highest during the third and fourth quarters of each year (as the spring planting season begins in September in Brazil).

Significant Accounting Policies

The Company’s significant accounting policies are detailed in “Note 2 – Summary of Significant Accounting Policies” within Item 8 of the Company’s Annual Report on Form 10-K for the year ended December 31, 2017. Significant changes to these accounting policies as a result of adopting ASU 2014-09, Revenue from Contracts with Customers (Topic 606), can be found in “Note 2 – Revenues.”

7

Recent Accounting Pronouncements

In February 2018, the Financial Accounting Standards Board (the “FASB”) issued guidance to address income tax accounting treatment of tax effects within accumulated other comprehensive income (“AOCI”) due to the enactment of the U.S. Tax Cuts and Jobs Act (the “Act”). This guidance allows entities to elect to reclassify tax effects of the change in U.S. income tax rates from AOCI to retained earnings. The guidance is effective for periods beginning after December 15, 2018, although early adoption is permitted. The Company early adopted this standard in the first quarter of 2018 and has elected to reclassify to retained earnings the effect of the change in the U.S. income tax rate on items remaining in AOCI as of the enactment date of the Act. The Company reclassified $0.2 million to retained earnings from AOCI as a result of the Company’s cash flow hedges. See the Consolidated Statement of Stockholders’ Equity for details on the reclassification.

In August 2017, the FASB issued guidance which amends the current hedge accounting model and requires certain new or modified disclosures to enable entities to better portray the economics of their risk management activities in their financial statements. The modifications include a tabular disclosure related to the effect on the income statement of fair value and cash flow hedges and eliminate the requirement to disclose the ineffective portion of the change in fair value of hedging instruments. The amendments also require new tabular disclosures related to cumulative basis adjustments for fair value hedges. The guidance is effective for fiscal years beginning after December 15, 2018 and interim periods within those fiscal years, although early adoption is permitted. The Company is currently assessing the impact this guidance will have on its consolidated financial statements.

In March 2017, the FASB issued guidance on the presentation of net periodic pension and postretirement benefit costs in the income statement and on the components eligible for capitalization. This guidance requires that an entity report the service cost component of the net periodic benefit costs in the same income statement line item as other compensation costs arising from services rendered by employees during the period. The non-service-cost components of net periodic benefit costs are to be presented in the income statement separately from the service cost components and outside a subtotal of income from operations. The guidance also allows for the capitalization of the service cost components, when applicable. The guidance is effective for annual periods beginning after December 15, 2017, including interim periods within those annual periods. The Company adopted this guidance in the first quarter of 2018. The impact of the adoption was not material to the Company’s consolidated financial statements.

In January 2017, the FASB issued guidance to simplify the accounting for goodwill impairment. The guidance removes Step 2 of the goodwill impairment test, which requires a hypothetical purchase price allocation. A goodwill impairment will now be the amount by which a reporting unit’s carrying value exceeds its fair value, not to exceed the carrying amount of goodwill. All other goodwill impairment guidance remains largely unchanged. The guidance is effective for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years. Early adoption is permitted for annual and interim goodwill impairment testing dates after January 1, 2017. The Company is still evaluating the impact of adopting this guidance.

In August 2016, the FASB issued guidance to clarify how certain cash receipts and payments should be presented and classified in the statement of cash flows. The guidance is effective for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years, and early adoption is permitted. The Company adopted this guidance in the first quarter of 2018 using the retrospective transition method, as required by the new standard. Adoption of this new standard did not have a material impact on the Company’s Consolidated Statements of Cash Flows.

In June 2016, the FASB issued guidance for estimating credit losses on certain types of financial instruments, including trade receivables, by introducing an approach based on expected losses. The expected loss approach will require entities to incorporate considerations of historical information, current information and reasonable and supportable forecasts. The guidance is effective for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years, requires a modified retrospective transition method and early adoption is permitted. The Company is currently evaluating the impact of the adoption of this guidance on its consolidated financial statements.

In February 2016, the FASB issued guidance which requires lessees to recognize on their balance sheet a right-of-use asset which represents a lessee’s right to use the underlying asset. Under this guidance, an entity must also recognize a lease liability which represents a lessee’s obligation to make lease payments for the right to use the asset. In addition, the standard requires expanded qualitative and quantitative disclosures. The guidance is effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years, and requires a modified retrospective transition method. The Company is currently in the process of gathering its lease contracts and evaluating the impact of the adoption of this guidance on its consolidated financial statements.

8

2. Revenues:

In May 2014, the FASB issued new guidance, "Revenue from Contracts with Customers." The new guidance provides a single, comprehensive model for recognizing revenue from contracts with customers. The new revenue recognition model supersedes existing guidance and requires revenue recognition to depict the transfer of promised goods or services to customers in an amount that reflects the consideration an entity expects to receive in exchange for those goods or services. The Company adopted the new guidance effective January 1, 2018 using the modified retrospective transition method, which requires the cumulative effect of adoption, if any, to be recognized as an adjustment to opening retained earnings in the period of adoption. The Company’s revenue arrangements generally consist of a single performance obligation to transfer promised goods or services. As a result, the Company did not identify any material differences in the amount and timing of revenue recognition for its revenue streams. Accordingly, the Company did not record any transition adjustment upon adoption of the new guidance.

Substantially all of the Company’s revenue will continue to be recognized at a point-in-time when control of the goods transfers to the customer. The adoption of the guidance results in expanded disclosures regarding the nature, amount, timing and uncertainty of revenues and cash flows from contracts with customers.

Revenue Recognition

Nature of Products and Services

The Company’s Salt segment products include salt and magnesium chloride for use in road deicing and dust control, food processing, water softeners, and agricultural and industrial applications. The Company’s plant nutrition products include SOP, specialty plant nutrients, and magnesium chloride for agricultural purposes and chemicals for the industrial chemical industry. In the U.K., the Company operates a records management business utilizing excavated areas of the Winsford salt mine with one other location in London, England.

Identifying the Contract

The Company accounts for a customer contract when there is approval and commitment from both parties, the rights of the parties and payment terms are identified, the contract has commercial substance and collectability of consideration is probable.

Identifying the Performance Obligations

At contract inception, the Company assesses the goods and services it has promised to its customers and identifies a performance obligation for each promise to transfer to the customer a distinct good or service (or bundle of goods or services). Determining whether products and services are considered distinct performance obligations that should be accounted for separately or aggregated together may require significant judgment.

Identifying and Allocating the Transaction Price

The Company’s revenues are measured based on consideration specified in the customer contract, net of any sales incentives and amounts collected on behalf of third parties such as sales taxes. In certain cases, the Company’s customer contracts may include promises to transfer multiple products and services to a customer. For multiple-element arrangements, the Company generally allocates the transaction price to each performance obligation in proportion to its stand-alone selling price.

When Performance Obligations Are Satisfied

The vast majority of the Company’s revenues are recognized at a point in time when the performance obligations are satisfied based upon transfer of control of the product or service to a customer. To determine when the control of goods is transferred, the Company typically assesses, among other things, the shipping terms of the contract, as shipping is an indicator of transfer of control. Some of the Company’s products are sold when the control of the goods transfers to the customer at the time of shipment. There are also instances when the Company provides shipping services to deliver its products. Shipping and handling costs that occur before the customer obtains control of the goods are deemed to be fulfillment activities and are accounted for as fulfillment costs. The Company has made an accounting policy election to recognize any shipping and handling costs that are incurred after the customer obtains control of the goods as fulfillment costs which are accrued at the time of revenue recognition.

Significant Payment Terms

The customer contract states the final terms of the sale, including the description, quantity and price of each product or service purchased. Payment is typically due in full within 30 days of delivery. As a practical expedient, the Company does not adjust the consideration for the effects of a significant financing component if the Company expects, at contract inception, that the period between when the good or service is transferred to the customer and when the customer pays for that good or service will be one year or less.

9

Refunds, Returns and Warranties

The Company’s products are generally not sold with a right of return and the Company does not generally provide credits or incentives, which may be required to be accounted for as variable consideration when estimating the amount of revenue to be recognized. The Company uses historical experience to estimate accruals for refunds due to manufacturing or other defects.

Practical Expedients and Accounting Policy Elections

Upon adoption of the new guidance, the Company elected: (i) to exclude disclosures of transaction prices allocated to remaining performance obligations when the Company recognized such revenue for all periods prior to the date of initial application of the new guidance, (ii) not to adjust the amount of consideration for the effects of a significant financing component when the Company expects, at contract inception, that the period between the Company's transfer of a product or service to a customer and when the customer pays for that product or service will be one year or less, (iii) to expense costs to obtain a contract as incurred for costs when the Company expects that the amortization period would have been one year or less, (iv) not to recast revenue for customer contracts that begin and end in the same fiscal period, and (v) not to assess whether promised goods or services are performance obligations if they are immaterial in the context of the customer contract.

See Note 10 for disaggregation of revenue by segment, type and geographical region.

3. | Acquisition: |

Background and Financing

On December 16, 2015, Compass Minerals do Brasil Ltda., a wholly owned subsidiary of the Company (“Compass Minerals Brazil”), entered into (i) a subscription agreement and other covenants (as amended, the “Subscription Agreement”) with certain Produquímica shareholders and Produquímica and (ii) a share purchase and sale agreement and other covenants (the “Purchase Agreement”) with certain Produquímica shareholders and Produquímica. Pursuant to the Subscription Agreement and the Purchase Agreement, Compass Minerals Brazil acquired 35% of the issued and outstanding capital stock of Produquímica on December 23, 2015, for R$452.4 million Brazilian reais (“R” or “BRL”), or $114.1 million U.S. dollars at closing, and paid additional consideration of $4.7 million in the second quarter of 2016 related to Produquímica’s 2015 financial performance.

The Subscription Agreement also contained a put right (the “Put”), allowing the Produquímica shareholders to sell the remainder of their interests in Produquímica to Compass Minerals Brazil. On August 12, 2016, Produquímica shareholders notified Compass Minerals Brazil of their exercise of the Put. On October 3, 2016, the Company acquired the remaining 65% of the issued and outstanding capital stock of Produquímica.

The Company entered into a new $100.0 million term loan tranche in the fourth quarter of 2015 to fund the acquisition of the 35% of Produquímica’s equity. In September 2016, the Company entered into a new $450.0 million term loan tranche to fund the acquisition of the remaining 65% of Produquímica’s equity. See Note 8 for more information regarding these financings.

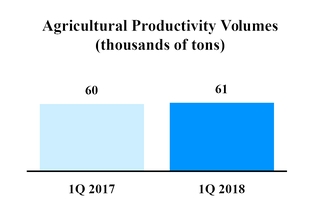

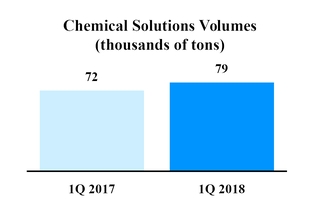

Based in São Paulo, Brazil, Produquímica operates two primary businesses – agricultural productivity and chemical solutions. The agricultural productivity division manufactures and distributes a broad offering of specialty plant nutrition solution-based products. These include micronutrients, controlled release fertilizers and other specialty supplements that are used in direct soil and foliar applications, as well as through irrigation systems and for seed treatment. Many of these products are developed through Produquímica’s research and development capabilities. Produquímica also manufactures and markets specialty chemicals used primarily in the industrial chemical and water treatment industries in Brazil. The acquisition broadens the Company’s geographic scope of operations and expands its specialty plant nutrition portfolio while reducing the Company’s dependence on winter weather conditions.

Purchase Price Allocation

The Company accounted for the Produquímica acquisition as a business combination in accordance with U.S. GAAP. The accounting guidance for business combinations requires estimates and judgments regarding expectations for future cash flows of the acquired entity as well as other valuation assumptions and an allocation to the net assets acquired. The fair values assigned to tangible and intangible assets acquired and liabilities assumed, including contingent consideration, are based on management’s best estimates. As of September 30, 2017, the purchase price allocation was finalized.

10

A summary of the acquisition-date fair value of the consideration transferred is presented in the table below:

Fair Value of Consideration Transferred (in millions) | October 3, 2016 | ||

Cash paid at closing | $ | 317.1 | |

Additional cash due at closing | 20.6 | ||

Fair value of contingent consideration | 31.4 | ||

Fair value of 35% equity investment | 178.7 | ||

Total | $ | 547.8 | |

The calculation of the purchase price at closing was based in part on an estimate of full-year 2016 operating results of Produquímica. As of the acquisition closing date, some of the periods included in the 2016 operating results of Produquímica had not ended and actual results were not known. The portion of the purchase price which was based on management’s estimate of results relating to periods which occurred after the closing date was classified as contingent consideration. There were no thresholds or tiers in the payment structure, and management used an income approach to estimate the acquisition date fair value of the contingent consideration. As of the closing date, the Company had estimated the fair value of contingent consideration to be $31.4 million.

During the first quarter of 2017, the purchase price was adjusted based on the final full-year 2016 operating results of Produquímica, and a final payment was made to the Produquímica shareholders. The difference between the estimated closing date fair value of the contingent consideration and the final amount paid resulted in the recognition of a gain of $1.9 million in the first quarter of 2017, which was included as a component of operating earnings in the Company’s Plant Nutrition South America segment.

Prior to the acquisition closing date, the Company accounted for its 35% interest in Produquímica as an equity method investment. The acquisition-date fair value of the previously held equity investment was $178.7 million and is included in the consideration transferred. To measure the acquisition closing date fair value of the equity interest, the Company utilized a market-based approach which relied on Level 3 inputs (see Note 13 for a discussion of the levels in the fair value hierarchy). The Company recognized a $59.3 million non-cash gain during the fourth quarter of 2016 as a result of remeasuring its prior equity interest in Produquímica held before the business combination.

Under the acquisition method of accounting, the total purchase price was allocated on a preliminary basis to Produquímica’s assets and liabilities based upon their estimated fair value as of the closing date of the acquisition. During the first nine months of 2017, the Company adjusted the preliminary purchase price allocation based on additional information obtained regarding facts and circumstances which existed as of the acquisition date. These adjustments resulted in a decrease of $3.6 million to goodwill, a decrease of $4.4 million to other noncurrent liabilities and an increase of $0.8 million to net deferred income taxes. Additionally, during the third quarter of 2017 in connection with finalizing the accounting for the acquisition, the Company recorded an adjustment increasing depreciation expense by $1.9 million. This adjustment resulted from finalizing the Company’s estimate of the useful lives of acquired tangible assets.

11

Based upon the final purchase price and the updated valuation, the final purchase price allocation is presented in the table below:

Recognized amounts of identifiable assets acquired and liabilities assumed (in millions): | Purchase Price Allocation | ||

Cash and cash equivalents | $ | 73.8 | |

Accounts receivable | 89.4 | ||

Inventories | 77.1 | ||

Other current assets | 13.7 | ||

Property, plant and equipment | 189.4 | ||

Intangible assets | 81.2 | ||

Investment in equity method investee | 24.5 | ||

Other noncurrent assets | 6.9 | ||

Accounts payable | (27.1 | ) | |

Accrued expenses | (40.3 | ) | |

Current portion of long-term debt | (129.6 | ) | |

Other current liabilities | (14.0 | ) | |

Long-term debt, net of current portion | (62.0 | ) | |

Deferred income taxes, net | (66.0 | ) | |

Other noncurrent liabilities | (21.9 | ) | |

Total identifiable net assets | 195.1 | ||

Goodwill | 352.7 | ||

Total fair value of business combination | $ | 547.8 | |

The total purchase price in excess of the net identifiable assets has been recognized as goodwill in the amount of $352.7 million and has been assigned to the Company’s Plant Nutrition South America segment. The goodwill recognized is attributable primarily to expected synergies with the Company’s existing plant nutrition business and the assembled workforce of Produquímica. The future deductibility of the goodwill for income tax purposes is uncertain at this time.

The Company determined that the book value of the accounts receivables included in the purchase price allocation approximates their fair value due to their short-term nature. The gross contractual amounts of the receivables exceeded their fair value by the amount of an allowance for doubtful accounts of approximately $8 million.

In connection with the acquisition, the Company acquired identifiable intangible assets which consisted principally of trade names, developed technologies and customer relationships. The fair values were determined using Level 3 inputs (see Note 13 for a discussion of the levels in the fair value hierarchy). The fair values of the identifiable intangible assets were estimated using an income approach method.

The estimated fair values and weighted average amortization period of the identifiable intangible assets are presented in the table below:

Estimated Fair Value (in millions) | Weighted-Average Amortization Period (in years) | |||

Trade names | $ | 36.9 | 11.0 | |

Developed technology | 37.5 | 5.3 | ||

Customer relationships | 6.8 | 13.5 | ||

Total identifiable intangible assets | $ | 81.2 | 8.6 | |

Impact on Operating Results

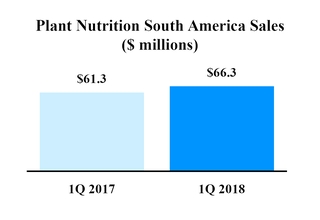

During the three months ended March 31, 2018 and 2017, respectively, Produquímica contributed revenues of $66.3 million and $61.3 million, respectively, and net losses of $2.7 million and $2.6 million, respectively, to the Company.

12

4. | Inventories: |

Inventories consist of the following (in millions):

March 31, 2018 | December 31, 2017 | ||||||

Finished goods | $ | 130.0 | $ | 208.4 | |||

Raw materials and supplies | 87.2 | 81.5 | |||||

Total inventories | $ | 217.2 | $ | 289.9 | |||

5. | Property, Plant and Equipment, Net: |

Property, plant and equipment, net, consists of the following (in millions):

March 31, 2018 | December 31, 2017 | ||||||

Land, buildings and structures, and leasehold improvements | $ | 560.7 | $ | 552.5 | |||

Machinery and equipment | 995.9 | 942.3 | |||||

Office furniture and equipment | 53.5 | 53.1 | |||||

Mineral interests | 172.3 | 173.1 | |||||

Construction in progress | 143.1 | 213.4 | |||||

1,925.5 | 1,934.4 | ||||||

Less accumulated depreciation and depletion | (800.7 | ) | (796.3 | ) | |||

Property, plant and equipment, net | $ | 1,124.8 | $ | 1,138.1 | |||

6. | Goodwill and Intangible Assets, Net: |

Aggregate amortization expense for the Company’s finite-lived intangible assets was $4.1 million for both three-month periods ended March 31, 2018 and 2017, respectively.

The Company had goodwill of $402.8 million and $405.0 million as of March 31, 2018 and December 31, 2017, respectively, in its Consolidated Balance Sheets. Of these amounts, $55.7 million and $57.3 million as of March 31, 2018 and December 31, 2017, respectively, were recorded in the Company’s Plant Nutrition North America segment, and $340.9 million and $341.6 million as of March 31, 2018 and December 31, 2017, respectively, were recorded in the Company’s Plant Nutrition South America segment. The remaining amounts in both periods were immaterial and recorded in the Company’s Salt segment and corporate and other. The change in goodwill between December 31, 2017 and March 31, 2018 was primarily due to the impact from translating foreign-denominated amounts to U.S. dollars.

7. | Income Taxes: |

The Company’s effective income tax rate differs from the U.S. statutory federal income tax rate primarily due to U.S. statutory depletion, state income taxes (net of federal tax benefit), foreign income tax rate differentials, foreign mining taxes and interest expense recognition differences for book and tax purposes. The Company’s effective rate is impacted by permanent tax deductions which have a less favorable impact as pretax income increases.

The Company has recorded a one-time mandatory tax on unremitted foreign earnings of $55.2 million (recorded in the fourth quarter of 2017) offset by $8.6 million ($8.4 million recorded in the fourth quarter of 2017) of benefit related to the remeasurement of the Company’s deferred tax liabilities at the new income tax rate in accordance with the Act (which is commonly referred to as “U.S. tax reform”), enacted on December 22, 2017. The Company believes the $46.6 million net charge represents a reasonable estimate; however, this amount is provisional and additional work is necessary to do a more detailed analysis of historical foreign earnings as well as any potential corresponding adjustments.

In addition, the Company is still evaluating the Global Low-Taxed Intangible Income provisions of the Act and their impact, if any, on its consolidated financial statements. As a result, the Company has not included an estimate of any potential tax exposure related to this item as of March 31, 2018.

13

The Company had $45.7 million and $46.1 million as of March 31, 2018 and December 31, 2017, respectively, of gross foreign federal net operating loss (“NOL”) carryforwards that have no expiration date. In addition, the Company had $5.5 million and $5.7 million as of March 31, 2018 and December 31, 2017, respectively, of gross foreign federal NOL carryforwards which expire beginning in 2033 and $0.7 million as of March 31, 2018 and December 31, 2017 of tax-effected state NOL carryforwards which expire beginning in 2033.

Canadian provincial tax authorities have challenged tax positions claimed by one of the Company’s Canadian subsidiaries and have issued tax reassessments for years 2002-2012. The reassessments are a result of ongoing audits and total $103.6 million, including interest, through March 31, 2018. The Company disputes these reassessments and will continue to work with the appropriate authorities in Canada to resolve the dispute. There is a reasonable possibility that the ultimate resolution of this dispute, and any related disputes for other open tax years, may be materially higher or lower than the amounts the Company has reserved for such disputes. In connection with this dispute, local regulations require the Company to post security with the tax authority until the dispute is resolved. The Company has posted collateral in the form of a $65.0 million performance bond, has paid $38.0 million to the Canadian tax authorities (most of which is recorded in other assets in its Consolidated Balance Sheets) and the remaining balance of $0.6 million, which is necessary to proceed with future appeals or litigation, is expected to be addressed later this year.

The Company expects that it will be required by local regulations to provide security for additional interest on the above unresolved disputed amounts and for any future reassessments issued by these Canadian tax authorities in the form of cash, letters of credit, performance bonds, asset liens or other arrangements agreeable with the tax authorities until the disputes are resolved.

The Company expects that the ultimate outcome of these matters will not have a material impact on its results of operations or financial condition. However, the Company can provide no assurance as to the ultimate outcome of these matters, and the impact could be material if they are not resolved in the Company’s favor. As of March 31, 2018, the Company believes it has adequately reserved for these reassessments.

Additionally, the Company has other uncertain tax positions as well as assessments and disputed positions with taxing authorities in its various jurisdictions, which are consistent with those matters disclosed in the Company’s Annual Report on Form 10-K for the year ended December 31, 2017.

Settlement

In the fourth quarter of 2017, the Company, the Canadian Revenue Authority and the U.S. Internal Revenue Service reached a settlement agreement on transfer pricing issues for the Company’s 2007-2012 tax years. As a result of this settlement, the Company recognized $13.8 million of tax expense in its 2017 Consolidated Statements of Operations related to the Company’s Canadian tax positions for the years 2007-2016. The agreement resulted in intercompany cash payments from the Company’s U.S. subsidiary to its Canadian subsidiary of $85.7 million during the first quarter of 2018.

In addition, the Company will make tax payments to Canadian taxing authorities of $22.7 million with a corresponding tax refund due from U.S. taxing authorities of $22.8 million. The timing of the refund is expected to lag the payment to the Canadian tax authorities by one year or more. Additionally, the reassessed Canadian tax, penalties and interest for the Company for years 2007 and 2008 of approximately $34.2 million are effectively resolved.

14

8. | Long-term Debt: |

Long-term debt consists of the following (in millions):

March 31, 2018 | December 31, 2017 | ||||||

Term Loans due July 2021 | $ | 835.2 | $ | 837.4 | |||

Revolving Credit Facility due July 2021 | 46.5 | 168.9 | |||||

4.875% Senior Notes due July 2024 | 250.0 | 250.0 | |||||

Rabobank Loan due November 2019 | 21.1 | 21.1 | |||||

Banco Itaú Loans due May 2019 to April 2020 | 1.7 | 1.9 | |||||

Financiadora de Estudos e Projetos Loan due November 2023 | 12.5 | 13.1 | |||||

Banco do Brasil Loan due February 2018 | — | 0.2 | |||||

Banco do Brasil Loan due May 2018 and September 2018 | 0.6 | — | |||||

Banco Santander Loan due September 2019 | 19.5 | 19.6 | |||||

Banco Santander Loan due November 2019 | 24.1 | 24.1 | |||||

Banco Itaú Loan due March 2019 | 10.0 | 12.4 | |||||

3.7% Banco Itaú Loan due March 2020 | 15.4 | — | |||||

Banco Scotiabank Loan due September 2019 | 20.5 | 20.5 | |||||

1,257.1 | 1,369.2 | ||||||

Less unamortized debt issuance costs | (6.6 | ) | (6.7 | ) | |||

Total debt | 1,250.5 | 1,362.5 | |||||

Less current portion | (32.3 | ) | (32.1 | ) | |||

Long-term debt | $ | 1,218.2 | $ | 1,330.4 | |||

In September 2017, the Company entered into an amendment to its credit agreement, which increased the maximum allowed leverage ratio under the credit agreement through September 2018. In connection with this amendment, the Company paid fees totaling $0.6 million ($0.1 million was recorded as an expense and $0.5 million was capitalized as deferred financing costs).

In the second half of 2017, the Company refinanced $54.3 million of its Brazilian loans using proceeds from approximately $87 million of new loans. The new variable rate loans bear interest rates ranging from 108.7% and 118% of CDI, an overnight inter-bank lending rate in Brazil, and mature in September and November 2019. In the first quarter of 2018, the Company entered into a new U.S. dollar denominated loan which matures in March 2020. No material fees were paid in connection with these transactions. A portion of the loans are denominated in U.S. dollars and a portion of the loans are denominated in Brazilian reais. The Company has also entered into foreign currency agreements whereby the Company agreed to swap interest and principal payments on the loans denominated in U.S. dollars for principal and interest payments denominated in Brazilian reais, Produquímica’s functional currency (see Note 12 for further discussion).

As of March 31, 2018, the term loans and revolving credit facility under the credit agreement were secured by substantially all existing and future U.S. assets, the Goderich mine in Ontario, Canada, and capital stock of certain subsidiaries.

9. | Commitments and Contingencies: |

The Company was involved in proceedings alleging unfair labor practices at its Cote Blanche, Louisiana mine. This matter arose out of a labor dispute between the Company and the United Steelworkers Union over the terms of a contract for certain employees at the mine. These employees initiated a strike that began on April 7, 2010 and ended on June 15, 2010. In September 2012, the U.S. National Labor Relations Board (the “NLRB”) issued a decision finding that the Company had committed unfair labor practices in connection with the labor dispute. Under the ruling, the Company is responsible for back pay to affected employees as a result of changes made in union work rules and past practices beginning April 1, 2010. In the fourth quarter of 2013, this ruling was upheld by an appeals court. As of December 31, 2016, the Company had recorded a reserve of $7.4 million in its consolidated financial statements related to expected payments, including interest, required to resolve the dispute.

15

In March 2017, the Company reached a settlement with the United Steelworkers Union and the NLRB with respect to this matter. Under the terms of the agreement, the Company paid $7.7 million to the affected employees in the second quarter of 2017. As a result of the settlement, the Company recognized an immaterial loss in its consolidated financial statements in 2017.

The Wisconsin Department of Agriculture, Trade and Consumer Protection (“DATCP”) has information indicating that agricultural chemicals are present within the subsurface area of the Company’s Kenosha, Wisconsin plant. The agricultural chemicals were used by previous owners and operators of the site. None of the identified chemicals have been used in association with the Company’s operations since it acquired the property in 2002. DATCP directed the Company to conduct further investigations into the possible presence of agricultural chemicals in soil and ground water at the Kenosha plant. The Company has completed initial on-property investigations and has provided the findings to DATCP. All investigations and mitigation activities to date, and any potential future remediation work, are being conducted under the Wisconsin Agricultural Chemical Cleanup Program (the “ACCP”), which provides for reimbursement of some of the costs. The Company may seek participation by, or cost reimbursement from, other parties responsible for the presence of any agricultural chemicals found in soil and ground water at this site if the Company does not receive an acknowledgment of no further action and is required to conduct further investigation or remedial work that may not be eligible for reimbursement under the ACCP.

The Company conducts business operations in several countries and is subject to various federal and local labor, social security, environmental and tax laws. While the Company believes it complies with such laws, they are complex and subject to interpretation. In addition to the tax assessments discussed in Note 7, the Company’s Brazilian subsidiaries are party to administrative tax proceedings and claims which totaled $18.2 million and $18.1 million as of March 31, 2018 and December 31, 2017, respectively, and relate primarily to value added tax, state tax (ICMS) and social security tax (PIS and COFINS) assessments. The Company has assessed the likelihood of a loss at less than probable and therefore, has not established a reserve for these matters. The Company also assumed liabilities for labor-related matters in connection with the acquisition of Produquímica, which are primarily related to compensation, labor benefits and consequential tax claims and totaled $10.0 million and $10.5 million as of March 31, 2018 and December 31, 2017, respectively. The Company believes the maximum exposure for these other labor matters totaled approximately $40 million and $41 million as of March 31, 2018 and December 31, 2017, respectively.

The Company is also involved in legal and administrative proceedings and claims of various types from the ordinary course of the Company’s business.

Management cannot predict the outcome of legal claims and proceedings with certainty. Nevertheless, management believes that the outcome of legal proceeding and claims, which are pending or known to be threatened, even if determined adversely, will not, individually or in the aggregate, have a material adverse effect on the Company’s results of operations, cash flows or financial position.

10. | Operating Segments: |

The Company’s reportable segments are strategic business units that offer different products and services, and each business requires different technology and marketing strategies. The Company has three reportable segments: Salt, Plant Nutrition North America and Plant Nutrition South America. The Salt segment produces and markets salt and magnesium chloride for use in road deicing and dust control, food processing, water softeners and agricultural and industrial applications. SOP crop nutrients, industrial-grade SOP, micronutrients and magnesium chloride for agricultural purposes are produced and marketed through the Plant Nutrition North America segment. This segment operates two primary businesses in Brazil – agricultural productivity and chemical solutions. See Note 3 for a further discussion of the acquisition. The agricultural productivity division manufactures and distributes a broad offering of specialty plant nutrition solution-based products that are used in direct soil and foliar applications, as well as through irrigation systems and for seed treatment. The Company’s Plant Nutrition South America segment also manufactures and markets specialty chemicals for the industrial chemical industry.

16

Segment information is as follows (in millions):

Three Months Ended March 31, 2018 | Salt | Plant Nutrition North America | Plant Nutrition South America | Corporate & Other(a) | Total | |||||||||||||||

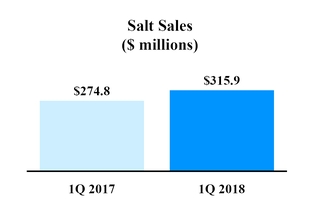

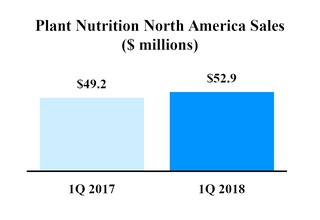

Sales to external customers | $ | 315.9 | $ | 52.9 | $ | 66.3 | $ | 2.8 | $ | 437.9 | ||||||||||

Intersegment sales | — | 0.2 | 0.4 | (0.6 | ) | — | ||||||||||||||

Shipping and handling cost | 109.5 | 6.4 | 4.2 | — | 120.1 | |||||||||||||||

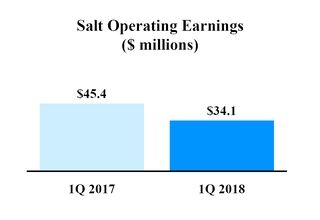

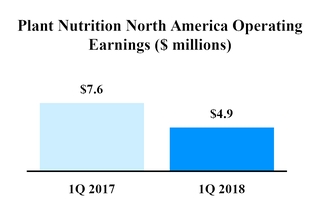

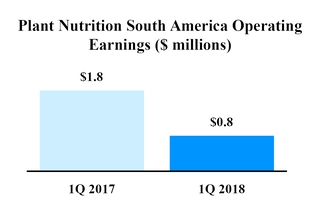

Operating earnings (loss) | 34.1 | 4.9 | 0.8 | (13.2 | ) | 26.6 | ||||||||||||||

Depreciation, depletion and amortization | 14.7 | 11.3 | 5.9 | 2.4 | 34.3 | |||||||||||||||

Total assets (as of end of period) | 885.7 | 580.0 | 816.8 | 130.3 | 2,412.8 | |||||||||||||||

Three Months Ended March 31, 2017 | Salt | Plant Nutrition North America | Plant Nutrition South America | Corporate & Other(a) | Total | |||||||||||||||

Sales to external customers | $ | 274.8 | $ | 49.2 | $ | 61.3 | $ | 2.5 | $ | 387.8 | ||||||||||

Intersegment sales | — | 0.9 | — | (0.9 | ) | — | ||||||||||||||

Shipping and handling cost | 83.0 | 6.7 | 4.0 | — | 93.7 | |||||||||||||||

Operating earnings (loss) | 45.4 | 7.6 | 1.8 | (13.4 | ) | 41.4 | ||||||||||||||

Depreciation, depletion and amortization | 12.9 | 8.9 | 5.3 | 1.3 | 28.4 | |||||||||||||||

Total assets (as of end of period) | 854.4 | 583.4 | 834.7 | 50.8 | 2,323.3 | |||||||||||||||

Disaggregated revenue by product type is as follows (in millions):

Three Months Ended March 31, 2018 | Salt | Plant Nutrition North America | Plant Nutrition South America | Corporate & Other(a) | Total | |||||||||||||||

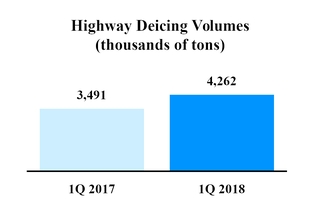

Highway Deicing Salt | $ | 235.4 | $ | — | $ | — | $ | — | $ | 235.4 | ||||||||||

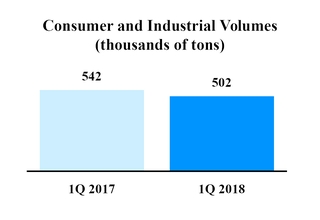

Consumer & Industrial Salt | 80.5 | — | — | — | 80.5 | |||||||||||||||

SOP and Specialty Plant Nutrients | — | 53.1 | 39.9 | — | 93.0 | |||||||||||||||

Industrial Chemicals | — | — | 26.8 | — | 26.8 | |||||||||||||||

Eliminations & Other | — | (0.2 | ) | (0.4 | ) | 2.8 | 2.2 | |||||||||||||

Sales to external customers | $ | 315.9 | $ | 52.9 | $ | 66.3 | $ | 2.8 | $ | 437.9 | ||||||||||

(a) | Corporate and other includes corporate entities, records management operations and other incidental operations and eliminations. Operating earnings (loss) for corporate and other includes indirect corporate overhead, including costs for general corporate governance and oversight, as well as costs for the human resources, information technology, legal and finance functions. |

The Company’s revenue by geographic area is as follows (in millions):

Revenue | Three Months Ended March 31, 2018 | |||

United States(a) | $ | 242.2 | ||

Canada | 90.8 | |||

Brazil | 65.6 | |||

United Kingdom | 36.7 | |||

Other | 2.6 | |||

Total Revenue | $ | 437.9 | ||

(a) United States sales exclude product sold to foreign customers at U.S. ports. | ||||

17

11. | Stockholders’ Equity and Equity Instruments: |

In May 2015, the Company’s stockholders approved the 2015 Incentive Award Plan (the “2015 Plan”), which authorizes the issuance of 3,000,000 shares of Company common stock. Since the date the 2015 Plan was approved, the Company ceased issuing equity awards under the 2005 Incentive Award Plan (the “2005 Plan”). The 2005 Plan and 2015 Plan allow for grants of equity awards to executive officers, other employees and directors, including restricted stock units (“RSUs”), performance stock units (“PSUs”), stock options and deferred stock units. The grants occur following approval by the compensation committee of the Company’s board of directors, with the amount and terms communicated to employees shortly thereafter.

Options

Substantially all stock options granted under the 2005 Plan and 2015 Plan vest ratably, in tranches, over a four-year service period. Unexercised options expire after seven years. Options do not have dividend or voting rights. Upon vesting, each option can be exercised to purchase one share of the Company’s common stock. The exercise price of options is equal to the closing stock price on the grant date.

To estimate the fair value of options on the grant date, the Company uses the Black-Scholes option valuation model. Award recipients are grouped according to expected exercise behavior. Unless better information is available to estimate the expected term of the options, the estimate is based on historical exercise experience. The risk-free rate, using U.S. Treasury yield curves in effect at the time of grant, is selected based on the expected term of each group. The Company’s historical stock price is used to estimate expected volatility.

RSUs

Substantially all of the RSUs granted under the 2005 Plan and 2015 Plan vest after three years of service, entitling the holders to one share of common stock for each vested RSU. Unvested RSUs do not have voting rights but are entitled to receive non-forfeitable dividends (generally after a performance hurdle has been satisfied for the year of the grant) or other distributions equal to those declared on the Company’s common stock for RSUs that are earned as a result of the satisfaction of the performance hurdle. The closing stock price on the grant date is used to determine the fair value of RSUs.

PSUs

Substantially all of the PSUs granted under the 2005 Plan and 2015 Plan are either total shareholder return PSUs (“TSR PSUs”) or return on invested capital PSUs (“ROIC PSUs”). The actual number of shares of the Company’s common stock that may be earned with respect to TSR PSUs is calculated by comparing the Company’s total shareholder return to the total shareholder return for each company comprising the Russell 3000 Index (for TSR PSUs granted in 2017 and earlier) or the Company’s peer group (for TSR PSUs granted in 2018) over the three-year performance period and may range from 0% to 150% of the target number of shares based upon the attainment of these performance conditions. The actual number of shares of common stock that may be earned with respect to ROIC PSUs is calculated based on the average of the Company’s annual return on invested capital for each year in the three-year performance period and may range from 0% to 200% of the target number of shares based upon the attainment of these performance conditions.

PSUs represent a target number of shares of the Company’s common stock that may be earned before adjustment based upon the attainment of certain performance conditions. Holders of PSUs do not have voting rights but are entitled to receive non-forfeitable dividends or other distributions equal to those declared on the Company’s common stock for PSUs that are earned, which are paid when the shares underlying the PSUs are paid.

To estimate the fair value of the TSR PSUs on the grant date, the Company uses a Monte-Carlo simulation model, which simulates future stock prices of the Company as well as the companies comprising the Russell 3000 Index. This model uses historical stock prices to estimate expected volatility and the Company’s correlation to the Russell 3000 Index. The risk-free rate was determined using the same methodology as the option valuations as discussed above. The Company’s closing stock price on the grant date was used to estimate the fair value of the ROIC PSUs. The Company will adjust the expense of the ROIC PSUs based upon its estimate of the number of shares that will ultimately vest at each interim date during the vesting period.

During the three months ended March 31, 2018, the Company reissued the following number of shares from treasury stock: no shares related to the exercise of stock options, 15,080 shares related to the release of RSUs which vested, 2,753 shares related to the release of PSUs which vested and 4,314 shares related to stock payments. The Company recognized a tax deficiency of $0.1 million from its equity compensation awards as an increase to income tax expense during the first three months of 2018. During the first three months of 2018 and 2017, the Company recorded $1.1 million and $1.3 million, respectively, of compensation

18

expense pursuant to its stock-based compensation plans. No amounts have been capitalized. The following table summarizes stock-based compensation activity during the three months ended March 31, 2018:

Stock Options | RSUs | PSUs(a) | |||||||||||||||||||

Number | Weighted-average exercise price | Number | Weighted-average fair value | Number | Weighted-average fair value | ||||||||||||||||

Outstanding at December 31, 2017 | 562,877 | $ | 75.89 | 70,856 | $ | 74.63 | 112,036 | $ | 79.48 | ||||||||||||

Granted | — | — | — | — | — | — | |||||||||||||||

Exercised(b) | — | — | — | — | — | — | |||||||||||||||

Released from restriction(b) | — | — | (15,080 | ) | 89.58 | (2,753 | ) | 78.92 | |||||||||||||

Cancelled/expired | (26,075 | ) | 81.94 | (1,344 | ) | 72.63 | (28,440 | ) | 96.97 | ||||||||||||

Outstanding at March 31, 2018 | 536,802 | $ | 75.60 | 54,432 | $ | 70.53 | 80,843 | $ | 73.35 | ||||||||||||

(a) | Until they vest, PSUs are included in the table at the target level at their grant date and at that level represent one share of common stock per PSU. The performance period for the 2015 PSU grant ended in 2017. The Company cancelled 25,897 PSUs in 2018 related to the 2015 PSU grant. |

(b) | Common stock issued for exercised options and for vested and earned RSUs and PSUs was issued from treasury stock. |

Other Comprehensive Income (Loss)

The Company’s comprehensive income (loss) is comprised of net earnings, net amortization of the unrealized loss of the pension obligation, the change in the unrealized gain (loss) on natural gas and foreign currency swap cash flow hedges, and foreign currency translation adjustments. The components of and changes in accumulated other comprehensive income (loss) (“AOCI”) as of and for the three months ended March 31, 2018 and 2017, are as follows (in millions):

Three Months Ended March 31, 2018(a) | Gains and (Losses) on Cash Flow Hedges | Defined Benefit Pension | Foreign Currency | Total | |||||||||||

Beginning balance | $ | (0.9 | ) | $ | (3.9 | ) | $ | (73.1 | ) | $ | (77.9 | ) | |||

Other comprehensive loss before reclassifications(b) | (0.2 | ) | — | (14.4 | ) | (14.6 | ) | ||||||||

Amounts reclassified from accumulated other comprehensive loss | (0.3 | ) | 0.1 | — | (0.2 | ) | |||||||||

Net current period other comprehensive income (loss) | (0.5 | ) | 0.1 | (14.4 | ) | (14.8 | ) | ||||||||

Reclassification of stranded tax out of AOCI to retained earnings(c) | (0.2 | ) | — | — | (0.2 | ) | |||||||||

Ending balance | $ | (1.6 | ) | $ | (3.8 | ) | $ | (87.5 | ) | $ | (92.9 | ) | |||

Three Months Ended March 31, 2017(a) | Gains and (Losses) on Cash Flow Hedges | Defined Benefit Pension | Foreign Currency | Total | |||||||||||

Beginning balance | $ | 0.6 | $ | (3.7 | ) | $ | (101.8 | ) | $ | (104.9 | ) | ||||

Other comprehensive income (loss) before reclassifications(b) | (0.5 | ) | — | 14.8 | 14.3 | ||||||||||

Amounts reclassified from accumulated other comprehensive loss | — | 0.1 | — | 0.1 | |||||||||||

Net current period other comprehensive income (loss) | (0.5 | ) | 0.1 | 14.8 | 14.4 | ||||||||||

Ending balance | $ | 0.1 | $ | (3.6 | ) | $ | (87.0 | ) | $ | (90.5 | ) | ||||

(a) | With the exception of the cumulative foreign currency translation adjustment, for which no tax effect is recorded, the changes in the components of accumulated other comprehensive income (loss) presented in the tables above are reflected net of applicable income taxes. |

(b) | The Company recorded foreign exchange (gains) losses of $(4.4) million and $7.2 million in the three months ended March 31, 2018 and 2017, respectively, in accumulated other comprehensive loss related to intercompany notes which were deemed to be of long-term investment nature. |

(c) | In the first quarter of 2018, the Company adopted guidance which allows entities to reclassify tax effects of the change in U.S. income tax rates from AOCI to retained earnings (see Note 1). |

19

The amounts reclassified from AOCI to expense for the three months ended March 31, 2018 and 2017, are shown below (in millions):

Three Months Ended March 31, 2018 | Three Months Ended March 31, 2017 | Line Item Impacted in the Consolidated Statement of Operations | |||||||

Gains and (losses) on cash flow hedges: | |||||||||

Natural gas instruments | $ | — | $ | — | Product cost | ||||

Foreign currency swaps | (0.5 | ) | — | Interest expense | |||||

Income tax expense (benefit) | 0.2 | — | |||||||

Reclassifications, net of income taxes | (0.3 | ) | — | ||||||

Amortization of defined benefit pension: | |||||||||

Amortization of loss | $ | 0.1 | $ | 0.1 | Product cost | ||||

Income tax expense (benefit) | — | — | |||||||

Reclassifications, net of income taxes | 0.1 | 0.1 | |||||||

Total reclassifications, net of income taxes | $ | (0.2 | ) | $ | 0.1 | ||||

12. | Derivative Financial Instruments: |

The Company is subject to various types of market risks, including interest rate risk, foreign currency exchange rate transaction and translation risk and commodity pricing risk. Management may take actions to mitigate the exposure to these types of risks, including entering into forward purchase contracts and other financial instruments. Currently, the Company manages a portion of its commodity pricing and foreign currency exchange rate risks by using derivative instruments. The Company does not seek to engage in trading activities or take speculative positions with any financial instrument arrangement. The Company has entered into natural gas derivative instruments and foreign currency derivative instruments with counterparties it views as creditworthy. However, the Company does attempt to mitigate its counterparty credit risk exposures by, among other things, entering into master netting agreements with some of these counterparties.The Company records derivative financial instruments as either assets or liabilities at fair value in the Consolidated Balance Sheets.

Derivatives qualify for treatment as hedges when there is a high correlation between the change in fair value of the derivative instrument and the related change in value of the underlying hedged item. Depending on the exposure being hedged, the Company must designate the hedging instrument as a fair value hedge, a cash flow hedge or a net investment in foreign operations hedge. For the qualifying derivative instruments that have been designated as hedges, the effective portion of the change in fair value is recognized through earnings when the underlying transaction being hedged affects earnings, allowing a derivative’s gains and losses to offset related results from the hedged item in the statements of operations. Any ineffectiveness related to these hedges was not material for any of the periods presented. For derivative instruments that have not been designated as hedges, the entire change in fair value is recorded through earnings in the period of change.

Natural Gas Derivative Instruments

Natural gas is consumed at several of the Company’s production facilities, and a change in natural gas prices impacts the Company’s operating margin. The Company’s objective is to reduce the earnings and cash flow impacts of changes in market prices of natural gas by fixing the purchase price of up to 90% of its forecasted natural gas usage. It is the Company’s policy to consider hedging portions of its natural gas usage up to 36 months in advance of the forecasted purchase. As of March 31, 2018, the Company had entered into natural gas derivative instruments to hedge a portion of its natural gas purchase requirements through December 2019. As of March 31, 2018 and December 31, 2017, the Company had agreements in place to hedge forecasted natural gas purchases of 2.0 million and 2.6 million MMBtus, respectively. All natural gas derivative instruments held by the Company as of March 31, 2018 and December 31, 2017 qualified and were designated as cash flow hedges. As of March 31, 2018, the Company expects to reclassify from accumulated other comprehensive loss to earnings during the next twelve months $0.9 million of net losses on derivative instruments related to its natural gas hedges.

Foreign Currency Derivatives Not Designated as Hedges

In February 2018, the Company entered into a forward instrument to swap currency denominated in Brazilian reais to Canadian dollars for the amounts borrowed under an intercompany note. The instrument matures in November 2018 and is for a notional amount of approximately $20 million U.S. dollars. The objective of the instrument is to mitigate the foreign currency fluctuation risk related to holding debt denominated in a currency other than Produquímica’s functional currency. The instrument is not

20

designated as a hedge. During the three months ended March 31, 2018, the Company recognized a gain of $0.3 million in its Consolidated Statements of Operations for the change in fair value of the swap agreements not designated as hedges.

Foreign Currency Swaps Designated as Hedges

The Company has entered into U.S. dollar-denominated debt instruments to provide funds for its operations in Brazil (see Note 8 for more information). The Company may also concurrently enter into foreign currency swap agreements whereby the Company agrees to swap interest and principal payments on loans denominated in U.S. dollars for principal and interest payments denominated in Brazilian reais, Produquímica’s functional currency. The objective of the swap agreements is to mitigate the foreign currency fluctuation risk related to holding debt denominated in a currency other than Produquímica’s functional currency. As of March 31, 2018, the Company had swap agreements in place to hedge $46.2 million of loans denominated in currencies other than Produquímica’s functional currency. Payments on these loans are due on various dates extending through March 2020. As of March 31, 2018, these foreign currency swap derivative instruments qualified and were designated as cash flow hedges. As of March 31, 2018, the Company expects to reclassify from accumulated other comprehensive loss to earnings during the next twelve months $0.8 million of net gains on derivative instruments related to these foreign currency swap agreements.

The following tables present the fair value of the Company’s hedged items as of March 31, 2018 and December 31, 2017 (in millions):

Asset Derivatives | Liability Derivatives | |||||||||||

Derivatives designated as hedging instruments: | Balance Sheet Location | March 31, 2018 | Balance Sheet Location | March 31, 2018 | ||||||||

Commodity contracts | Other current assets | $ | — | Accrued expenses | $ | 0.9 | ||||||

Commodity contracts | Other assets | — | Other noncurrent liabilities | 0.5 | ||||||||

Swap contracts | Other current assets | 0.8 | Accrued expenses | — | ||||||||

Swap contracts | Other assets | 0.3 | Other noncurrent liabilities | — | ||||||||

Total derivatives designated as hedging instruments(a) | 1.1 | 1.4 | ||||||||||

Derivatives not designated as hedging instruments: | ||||||||||||

Forward contracts | Other current assets | $ | 0.3 | Accrued expenses | $ | — | ||||||

Total derivatives not designated as hedging instruments | 0.3 | — | ||||||||||

Total derivatives(b) | $ | 1.4 | $ | 1.4 | ||||||||

(a) | The Company has master netting agreements with its commodity hedge counterparties and accordingly has netted in its Consolidated Balance Sheets an immaterial amount receivable from one counterparty. |

(b) | The Company has commodity hedge and foreign currency agreements with two and three counterparties, respectively. Amounts recorded as liabilities for the Company’s commodity contracts are payable to two counterparties. The amounts recorded as receivables for the Company’s swap contracts are receivable from two counterparties. The amounts recorded as receivables for the Company’s forward contracts are due from one counterparty. |

Asset Derivatives | Liability Derivatives | |||||||||||

Derivatives designated as hedging instruments: | Balance Sheet Location | December 31, 2017 | Balance Sheet Location | December 31, 2017 | ||||||||

Commodity contracts | Other current assets | $ | — | Accrued expenses | $ | 1.0 | ||||||

Commodity contracts | Other assets | — | Other noncurrent liabilities | 0.4 | ||||||||

Swap contracts | Other current assets | 0.9 | Accrued expenses | — | ||||||||

Swap contracts | Other assets | 0.4 | Other noncurrent liabilities | — | ||||||||

Total derivatives designated as hedging instruments(a)(b) | $ | 1.3 | $ | 1.4 | ||||||||

(a) | The Company has master netting agreements with its commodity hedge counterparties and accordingly has netted in its Consolidated Balance Sheets less than $0.1 million of its commodity contracts that are in a receivable position against its contracts in payable positions. |

(b) | The Company has both commodity hedge and foreign currency swap agreements with two counterparties each. Amounts recorded as liabilities for the Company’s commodity contracts are payable to both counterparties, and amounts recorded as assets for the Company’s swap contracts are receivable from both counterparties. |

21

13. | Fair Value Measurements: |

The Company’s financial instruments are measured and reported at their estimated fair value. Fair value is the price that would be received upon the sale of an asset or paid to transfer a liability in an orderly transaction. When available, the Company uses quoted prices in active markets to determine the fair values for its financial instruments (Level 1 inputs) or, absent quoted market prices, observable market-corroborated inputs over the term of the financial instruments (Level 2 inputs). The Company does not have any unobservable inputs that are not corroborated by market inputs (Level 3 inputs) other than those described in Note 3.

The Company holds marketable securities associated with its defined contribution and pre-tax savings plans, which are valued based on readily available quoted market prices. The Company also held short-term investments which were classified as trading securities with any gains or losses recognized through earnings. The Company sold these investments during the first quarter of 2017. The Company utilizes derivative instruments to manage its risk of changes in natural gas prices and its risk of changes in foreign currency exchange rates (see Note 12). The fair value of the natural gas and foreign currency swap derivative instruments are determined using market data of forward prices for all of the Company’s contracts.

The estimated fair values for each type of instrument are presented below (in millions):

March 31, 2018 | Level One | Level Two | Level Three | ||||||||||||

Asset Class: | |||||||||||||||

Mutual fund investments in a non-qualified retirement plan(a) | $ | 1.8 | $ | 1.8 | $ | — | $ | — | |||||||

Derivatives – foreign currency instruments, net | 1.4 | — | 1.4 | — | |||||||||||

Total Assets | $ | 3.2 | $ | 1.8 | $ | 1.4 | $ | — | |||||||

Liability Class: | |||||||||||||||

Liabilities related to non-qualified retirement plan | $ | (1.8 | ) | $ | (1.8 | ) | $ | — | $ | — | |||||

Derivatives – natural gas instruments, net | (1.4 | ) | — | (1.4 | ) | — | |||||||||

Total Liabilities | $ | (3.2 | ) | $ | (1.8 | ) | $ | (1.4 | ) | $ | — | ||||

(a) | Includes mutual fund investments of approximately 25% in common stock of large-cap U.S. companies, 20% in common stock of small to mid-cap U.S. companies, 5% in international companies, 15% in bond funds, 15% in short-term investments and 20% in blended funds. |

December 31, 2017 | Level One | Level Two | Level Three | ||||||||||||

Asset Class: | |||||||||||||||

Mutual fund investments in a non-qualified savings plan(a) | $ | 2.2 | $ | 2.2 | $ | — | $ | — | |||||||

Derivatives – foreign currency swaps, net | 1.3 | — | 1.3 | — | |||||||||||

Total Assets | $ | 3.5 | $ | 2.2 | $ | 1.3 | $ | — | |||||||

Liability Class: | |||||||||||||||

Liabilities related to non-qualified savings plan | $ | (2.2 | ) | $ | (2.2 | ) | $ | — | $ | — | |||||

Derivatives – natural gas instruments, net | (1.4 | ) | — | (1.4 | ) | — | |||||||||

Total Liabilities | $ | (3.6 | ) | $ | (2.2 | ) | $ | (1.4 | ) | $ | — | ||||

(a) | Includes mutual fund investments of approximately 30% in the common stock of large-cap U.S. companies, 15% in the common stock of small to mid-cap U.S. companies, 5% in the common stock of international companies, 10% in bond funds, 20% in short-term investments and 20% in blended funds. |