Attached files

| file | filename |

|---|---|

| EX-32.1 - CERTIFICATION - Home Bistro, Inc. /NV/ | f10k2017ex32-1_gratitude.htm |

| EX-31.1 - CERTIFICATION - Home Bistro, Inc. /NV/ | f10k2017ex31-1_gratitude.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number: 333-185083

GRATITUDE HEALTH, INC.

(Exact Name of Registrant as Specified in Charter)

| Nevada | 333-185083 | 27-1517938 | ||

| (State

or Other Jurisdiction of Incorporation) |

(Commission File Number) | (IRS

Employer Identification Number) |

11231 US Highway One

Suite 200

North Palm Beach, Fl. 33408

(Address of Principal Executive Offices, Zip Code)

Registrant’s telephone number, including area code: (561) 227-2727

Vapir Enterprises, Inc.

3511 Ryder Street, Santa Clara, California 95051

(Former Name or Former Address, if Changed Since Last Report)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☐ No ☒

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check One)

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ (Do not check if a smaller reporting company) | Smaller reporting company | ☒ |

| Emerging growth company | ☐ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Exchange Act subsequent to the distribution of securities under a plan confirmed by a court. Yes ☒ No ☐

As of March 29, 2018, the Company had 53,141,833 shares of its common stock, $0.001 par value per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

| Item 1. | Business |

Vapir, Inc., the wholly owned subsidiary of Vapir Enterprises, Inc., a Nevada corporation, was incorporated on October 26, 2006 in the State of California.

On March 26, 2018, Gratitude Health, Inc. f/ka Vapir Enterprises, Inc., a corporation organized under the laws of Nevada (the “Acquiror” or “Company”), Hamid Emarlou, the principal shareholder of the Acquiror (the “Acquiror Principal Shareholder”), Gratitude Health, Inc. (FL), a corporation organized under the laws of Florida (the “Acquiree”), and each of the Persons who are shareholders of the Acquiree (collectively, the “Acquiree Shareholders,” and individually an “Acquiree Shareholder”) entered into a Share Exchange Agreement (the “Agreement”) pursuant to which the Acquiree Shareholders (who are the holders of all of the issued and outstanding shares of common stock of the Acquiree (the “Acquiree Interests”)) have agreed to transfer to the Acquiror, and the Acquiror has agreed to acquire from the Acquiree Shareholders, all of the Acquiree Interests, in exchange for the issuance of 520,000 shares of Series A Preferred Stock and 500,000 shares of Series B Preferred Stock, to the Acquiree Shareholders the “Acquiror Shares”), which Acquiror Shares shall, upon conversion into 102,000,000 shares of common stock of the Acquiror, constitute approximately 85.84% on a fully diluted basis of the issued and outstanding shares of Acquiror Common Stock immediately after the closing of the transactions contemplated herein, in each case, on the terms and conditions as set forth in the Agreement. For accounting purposes, the Share Exchange was treated as an acquisition of Acquiror and a recapitalization of Acquiree. Acquiree is the accounting acquirer, and the result is of its operations carryover. On the Closing Date, Acquiror Principal Shareholder entered into a Spin Off Agreement with Acquiror for the sale of the existing wholly owned Vapir, Inc. subsidiary of the Acquiror in exchange for Acquiror Principal Shareholder’s shares of Common Stock of Acquiror. The Spin Off Agreement shall not close less than five (5) days from the closing of the Agreement. As of the date of filing this Annual Report on Form 10-K, the disposition of the Company’s Vapir business has not been consummated. This Business description described both the traditional business of the Company as it existed on December 31, 2017, the end of the fiscal year for which this Form 10-K is filed, and the new business of Gratitude Health, Inc. after the March 26, 2018 share exchange.

Business of Vapir, Inc.

Vapir, Inc. specializes in the revolutionary technology of digital aromatherapy which is the art and science of utilizing naturally extracted aromatic essences from plants to balance and harmonize while freshening the environment with pleasant and distinctive fragrances. We invent, develop and produce revolutionary and easy to use digital aromatherapy devices. The unique value proposition of the Company’s proprietary technology (US Patent 6,095,153) is to prevent the creation of toxic by-products whenever plant materials are inhaled. This is accomplished by using convection heat that induces the safe release of plant essences without burning the source material. Our devices are designed in San Jose, California and manufactured in Guang Dong, China.

Our Industry

In general, “Vaporizers” are battery-powered products that enable users to inhale vapor without smoke, Vaporizers are not like traditional cigarettes, and their construction is comprised of three functional components:

| ● | Digital temperature control, means you have the ability to choose the warmth of your vaporizer’s heating element. The heating element that vaporizes liquid and/or botanicals so that it can be inhaled; | |

| ● | Vaporizers either heat the liquid or botanicals with direct contact with a heating element (conduction) or by exposing the herb to hot air (convection); and | |

| ● | Vaporizers require energy when hot. Depending on the intention behind the vaporizer’s design - the energy source will match the portable or stationary model paradigm. |

| 1 |

Our Products

Vaporizers

As of December 31, 2017, we marketed 5 vaporizers, the Prima, VapirRise 2.0 ultimate, VAPIR NO2 Portable Digital Vaporizer and VAPIR Oxygen Mini Corded Vaporizer, and the New Vapir Pen.

Prima

Prima is a digital vaporizer that supports extracts and botanicals. The unit is equipped with a removable/rechargeable lithium battery, a removable stainless steel vapor path and removable mouth piece which allows for easy cleaning, and four (4) pre-set temperatures which maintains pre-set heat levels by turning the heating element on and off as needed. Once the optimal temperature is reached, a green light on the casing will indicate that the device is now ready. This relatively simple technology enables the vaporizers to maintain heat levels.

| ● | Prima measures in at just 4.7 inches, and weighs 5.7 oz, and comes in four (4) different colors (Blue, Black, Silver, and Orange). |

VapirRise 2.0 Ultimate

| 2 |

The VapirRise 2.0 Ultimate is designed for loose-leaf herbs and essential oils. It supports both balloon inflation and direct inhalation. It can serve up to 4 users simultaneously. It has touch pad controls, an LCD temperature display and medical grade stainless steel vapir path and a ceramic heating element.

As the ceramic heating element of the device reaches the pre-set temperature, a fan blows air through the heating element. A sensor, which is located in the chamber of the unit, will constantly monitor the air temperature and maintain pre-set heat levels by turning the heating element on and off as needed. Once the optimal temperature is reached, a green light on the casing will indicate that the device is now ready. This relatively simple technology enables the vaporizers to maintain heat levels.

This convection vaporizer is a stationary desktop model - which means it isn’t intended for on-the-go consumption. The VapirRise offers an exceptional approach to the at-home vaporization experience.

Users can control the temperature (in both degrees Celsius & Fahrenheit); control the Fan Speed (ten options including a fanless setting); pick between a balloon or hose inhalation methods; and choose to serve up to four people at once with the exclusive hookah adapter.

VAPIR NO2 Portable Digital Vaporizer

The VAPIR NO2 is designed for loose-leaf herbs and direct inhalation. It is compact, portable and rechargeable. It has a medical grade pure brass element, an LCD temperature display and a silent operation. The VAPIR NO2 will be your number one portable vaporizer.

This compact portable vaporizer features touch-to-heat digital controls, an LCD thermostat, an internal rechargeable battery, and 100% silent operation. The NO2 vaporizer is designed for use with raw herbs and heats up in less than a minute. You can even vaporize while it’s charging.

The NO2 requires little to no maintenance for optimal operation and it even remembers your favorite temperature settings for quick and consistent vapor at the touch of a button.

| 3 |

VAPIR OXYGEN MINI CORDED

The VAPIR Oxygen Mini Corded is designed for loose-leaf herbs and direct inhalation. It is small and lightweight and is a corded vaporizer. It has an LCD temperature display and silent operation. Every portable vaporizer needs to produce clouds, not a mere mist. The Vapir Oxygen lets you live and breathe premium vapor. This herbal vaporizer harnesses premium materials and innovative design to deliver everything you’d expect from a premium vaporizer.

Our Oxygen Vaporizer features digital controls, portable design, and consistent vapor sessions with little maintenance.

VAPIR PEN

| 4 |

The Vapir Pen is a sleek and portable device that may be used with both concentrate and wax substances. It features an ergonomic mouthpiece that leads to a deep chamber. The Vapir Pen comes equipped with two different type of atomizers; the Coil-less Ceramic Atomizer and the Quartz Double-Rod Titanium Atomizer, both with Ceramic Chamber. The temperature controlled battery allows for a range of 3 pre-set temperatures. The Vapir Pen is directly charged through a Micro USB charging port at the bottom of the battery. This feature allows the device to be charged with any regular USB charger anywhere, whether at home or on the go. It is also included a USB charging cord in the box that can be connected directly to the device. The Vapir Pen has an elevated air flow system which reduces the likelihood of clogging or leakage.

Our Vaporizers and Accessories

Our vaporizers are sold with all the essentials that are needed to begin the vaporizing experience. In addition to the vaporizers, we also sell approximately 100 different accessories and spare parts that ranges from replacement batteries, replacement mouthpieces, recharging pieces, and all other essential accessories and spare parts.

Seasonality of our Business

We do not consider our business to be seasonal.

Marketing

We offer our vaporizers and related products through our website, distributors, online stores and retail stores. Retailers of our products include small-box smoke shops, vape stores, and online retailers throughout the United States and the world.

Competition

Competition in the vaporizer industry is intense and we anticipate that competition will likely remain intense for the foreseeable future. We compete with other sellers of vaporizers that are similar to our products and our competitors use the same sales practices and marketing strategies as we use and as a result, we face a continuing challenge in attempting to differentiate our products.

The nature of our competitors is varied as the market is highly fragmented and the barriers to entry into the business are low. Our direct competitors sell products that are substantially similar to ours and through the same channels through which we sell our vaporizers. We compete with these direct competitors for sales through distributors, wholesalers and retailers and we cannot assure you that we will be successful in meeting the competitive challenges that we face that will allow us to achieve unit sales volumes at levels that will allow us to achieve profitability and positive cash flow or if we achieve either or both of these objectives, that we can sustain either or both thereafter.

Our current competitive position in the vaporizer industry is difficult to gauge as most of our competition are also smaller companies or are privately held and do not publicly report their earnings. We do know of several competitors, but, like us, many are in their initial stages of development and are focusing on different areas of this industry. We also believe that the industry likely will attract other larger companies that possess greater financial and managerial resources with the result that we are likely to face greater competitive pressures that will adversely affect our sales volume, profits, and cash flow.

As a general matter, we have access to and market and sell similar products as our competitors, and since we sell our products at substantially similar prices as our competitors; accordingly, the key competitive factors for our success is the quality of service and design we offer our customers, the scope and effectiveness of our marketing efforts, including media advertising campaigns and, increasingly, the ability to identify and develop new sources of customers by attending trade shows and word of mouth. We cannot assure you that we will be successful in these efforts or, if we are successful, that we can maintain any competitive advantages that we may currently have.

| 5 |

Regulatory Matters/Compliance

The United States Food and Drug Administration (the “FDA”) regulates electronic cigarettes as “tobacco products” under the Family Smoking Prevention and Tobacco Control Act of 2009 (the “Tobacco Control Act”). The FDA is not permitted to regulate electronic cigarettes as “drugs” or “devices” or a “combination product” under the Federal Food, Drug and Cosmetic Act unless they are marketed for therapeutic purposes.

The Tobacco Control Act imposes significant new restrictions on the advertising and promotion of tobacco products. The law also requires the FDA to issue future regulations regarding the promotion and marketing of tobacco products sold or distributed over the internet, by mail order or through other non-face-to-face transactions in order to prevent the sale of tobacco products to minors.

It is likely that the Tobacco Control Act could result in a decrease in tobacco product sales in the United States, including sales of our electronic cigarettes and vaporizers.

The Tobacco industry expects significant regulatory developments to take place over the next few years, driven principally by the World Health Organization’s Framework Convention on Tobacco Control (“FCTC”). The FCTC is the first international public health treaty on tobacco, and its objective is to establish a global agenda for tobacco regulation with the purpose of reducing initiation of tobacco use and encouraging cessation. Regulatory initiatives that have been proposed, introduced or enacted include:

| ● | the levying of substantial and increasing tax and duty charges; | |

| ● | restrictions or bans on advertising, marketing and sponsorship; | |

| ● | the display of larger health warnings, graphic health warnings and other labeling requirements; | |

| ● | restrictions on packaging design, including the use of colors and generic packaging; | |

| ● | restrictions or bans on the display of tobacco product packaging at the point of sale, and restrictions or bans on cigarette vending machines; | |

| ● | requirements regarding testing, disclosure and performance standards for tar, nicotine, carbon monoxide and other smoke constituents levels; | |

| ● | requirements regarding testing, disclosure and use of tobacco product ingredients; | |

| ● | increased restrictions on smoking in public and work places and, in some instances, in private places and outdoors; | |

| ● | elimination of duty free allowances for travelers; and | |

| ● | encouraging litigation against tobacco companies. |

If electronic cigarettes or vaporizers are subject to one or more significant regulatory initiatives, our business, results of operations and financial condition could be materially and adversely affected.

Intellectual Property

Patents

We currently own four domestic utility patents and two design patents relating to vaporizers, as well as two utility patent applications and one design application pending in the United States as described below. There is no assurance that we will be awarded patents for of any of these pending patent applications. Further, we have not obtained an independent evaluation of our patent tights or any of our intellectual property rights. As a result, we cannot assure you that our patents and all of our intellectual property rights do not infringe upon those rights claimed by others. In that event we may be exposed to superior claims asserted by others and thereby we may be liable for significant damages arising out of any such infringement claims.

| 6 |

US Patent # 9,155,848 Method and System for Vaporization of a Substance

We have a utility patent for an apparatus for the vaporization of materials that releases active constituents for inhalation without the creation of harmful byproducts such as carcinogens associated with combustion and inhalation of substances. This patent expires on October 13, 2035.

U.S. Patent # 6,095,153 - Vaporization of volatile materials

We have a utility patent for the vaporization of volatile materials while avoiding combustion and denaturation of such material provide an alternative to combustion as means of volatilizing bioactive and flavor compounds to make such compounds available for inhalation without generating toxic or carcinogenic substances that are by-products of combustion and pyrolysis. This patent expires on June 19, 2018.

U.S. Patent # 6,772,756 - Method and System for Vaporization of a Substance

We have a utility patent for an apparatus for the vaporization of materials that releases active constituents for inhalation without the creation of harmful byproducts such as carcinogens associated with combustion and inhalation of substances. This patent expires on February 9, 2022.

U.S. Patent # 6,990,978 - Method and System for Vaporization of a Substance

We have a utility patent for an apparatus for the vaporization of materials that releases active constituents for inhalation without the creation of harmful byproducts such as carcinogens associated with combustion and inhalation of substances. This patent expires on January 31, 2026.

U.S. Design Patent # 489,448 - Vaporization Apparatus

We have a design patent for the ornamental design for the vaporization apparatus. This patent expires on May 4, 2018.

U.S. Design Patent # 508,119 - Mesh Filter with Glass Insert

We have a design patent for the ornamental design for a component for a vaporizer. This patent expires on August 2, 2019.

U.S. Patent Application # 11/872,040 - Method and System for Vaporization of a Substance

We have a utility patent (filed on October 15, 2007) pending for an apparatus for the vaporization of materials that releases active constituents for inhalation without the creation of harmful byproducts such as carcinogens associated with combustion and inhalation of substances.

U.S. Patent # 14/254,723 - Multi-User Inhalation Adaptor

We have a utility patent (filed on April 16, 2014) pending for a component of a vaporizer that allows multiple users to inhale the vapors of materials.

U.S. Design Patent # 29/473,910 - Vaporizer

We have a design patent (filed on November 26, 2013) for the ornamental design for the vaporization apparatus.

Trademarks

We own trademarks on certain of our products, including: Digital Air®, Nicohale®, and Vapir®.

| 7 |

Employees

As of December 31, 2017, we have three full-time and two part-time employees. None of these employees are represented by collective bargaining agreements and the Company considers it relations with its employees to be good.

Business of Gratitude Health, Inc.

Effective March 26, 2018, we acquired all the issued and outstanding shares of Acquiree pursuant to the Exchange Agreement and Acquiree became our wholly-owned subsidiary. The acquisition was accounted for as a recapitalization effected by a share exchange, wherein Acquiree is considered the acquirer for accounting and financial reporting purposes. The assets and liabilities of Acquiree have been brought forward at their book value and no goodwill has been recognized.

At the time of the acquisition, the Company was engaged in the business of engaged in inventing, developing and producing aromatherapy devices and vaporizers. As a result of the acquisition of all the issued and outstanding shares of common stock of Acquiree, we have now assumed Acquiree’s business operations as our own. The acquisition of Acquiree is treated as a reverse acquisition, and the business of Acquiree became the business of the Company.

Business Plan

The Company manufactures, sells and markets functional RTD (Ready to Drink) beverages sold under the Gratitude trademark. The Company’s first five drinks are Chinese Dragon Well Green Teas. Second and third functional-drink lines are now in development. The Gratitude mission is to disrupt this beverage market through our manufacturing and marketing of functional beverages that specifically promote healthy aging and to never produce a product that in any way will adversely affect the health of our customer. The Gratitude vision is to work with research partners to develop functional drinks that can easily be incorporated into one’s daily lifestyle and fit their nutritional goals.

THE PRODUCTS AND PACKAGING:

Gratitude Health, Inc. is building the “Gratitude” brand with the launch of unique, naturally flavored and unsweetened RTD (Ready To Drink) teas.

Today, tea is the second largest drink category in America and is an obvious driver and mainstay in delivery systems across food and beverage categories. Americans and, especially, Millennial Americans are increasingly becoming more and more aware of the generous levels of cancer-fighting antioxidants found in tea.

While Green, White and Black teas are the most common types consumed in America, research shows that their growth is solid year-over-year but barely above flat. We believe this is due to two factors:

| ● | The category is staid and boring and, | |

| ● | RTD teas are not delivering on their health promises. |

We will address these issues with unique varieties of tea that not only have interesting and curious names but also health research that supports their benefits. Naturally, we will be calorie and carb free and always strive for maximum antioxidant delivery. Our teas are sourced from Dragon Well in China. Our initial five flavors are:

| ● | Wildberry | |

| ● | Blood Orange | |

| ● | Mint | |

| ● | Original | |

| ● | Peach |

| 8 |

Supporting these unique flavors and key to our brand-building presentation will be our package, a first-to- RTD-market “mason jar” like 16-oz bottle featuring artistic, graphic designs actually etched onto the glass-container.

We will promote this unique presentation as more than eco-friendly (“eco” being of great importance to millennials) because they will be collectibles and advertised as such thus making their collectability and reuse arguably the eco-friendliest mass-market beverage bottle in the world. To even further support this unique presentation, artistic and colorful labels (logo, art, nutritional and redemption information) will cover the etchings driving the desires for those that keep them to buy their “missing” collectible.

Interestingly, the 2017 Natural Beverage Guide (Bevnet, Inc) displays hundreds of Natural-Drink companies and not one has a “Mason” jar configuration. We believe this packaging will be widely preferred to the predominantly plastic bottles in the market today, we further expect modern consumers to understand and appreciate the flavor profile and obvious nutritional benefits of the teas.

Having identified the opportunity and clearly focused upon the healthy features and benefits available in Gratitude’s tea offerings, Gratitude will shortly introduce its first five flavors of tea. This will kick off sales efforts in earnest for the larger chained retail accounts across the Country. These accounts generally review new products for “planogram” resets during calendar Q-1 with a view to begin new product offering and new sets in April each year.

This gives Gratitude three months to sell and arrange for new product authorizations in regional and national accounts while managing our initial placements in New York City and smaller accounts with whom we have relationships in the Northeastern United States.

| 9 |

MARKET INFORMATION AND THE VALUE CHAIN AND ROUTES TO MARKET

According to Beverage Marketing Corporation’s 2017 “DrinkTell” database, RTD tea sales totaled $10.31 billion in 2017 up four percent. Importantly, Gratitude’s market analyses and product development perfectly targets the main attributes fueling this growth. According to this database, “Ready-to-drink tea is leading the growth in its category with new forms and formulations that offer both function and flavor. Consumers are willing to trade up to products that offer them better quality or benefits.” Further according to BMC, “Retailers say refrigerated RTD teas are the leading segment in this category, and new varieties are emerging. In the RTD tea category, reduced-sugar formulations and local and artisanal brands are poised for continued growth.”

We are the first company to introduce Chinese Dragon Well Tea to the mass RTD American market. Dragon Well is subtle in taste with a hint of chestnut and is the most popular tea in China being granted “Imperial” status. Because it is “Green”, our tea will be well known to the US consumer. Because it is “DragonWell”, it will be a welcome new experience to the US RTD market. All our teas are either low calorie--45 per 16z—or totally unsweetened. Our “small batch * hand made” brand positioning features totally unique and first-to-market packaging that meets artisanal characteristics influencing today’s consumer purchase.

According to the Tea Association of the USA, in its 2017-2018 Tea Market Review and Forecast, Ready-to-drink (RTD) tea accounted for some 45.7% of the tea market share in 2017 and will exceed 1.7 billion gallons in 2017. The Review states “Specialty Tea is still driving interest and consumption in the category with consumers grazing for new and different options and flavors and origins. Sustainability of these high quality, higher priced teas confirms that the analogy to wine is stronger than ever.” Furthermore, according to the Tea Association: “Naturalness continues to drive consumers who demand foods that are closer to their unrefined or pure state, seeking “less processed” drinks, incentivizing companies to remove artificial ingredients. This trend will also encourage consumers to reach for foods in their most natural, original form, such as true teas, for health benefits, instead of supplements and nutraceuticals. Tea is a natural, simple and whole food.”

By marrying a famous and revered green tea in China with such organic flavors as Peach, Mint, Wildberry and Blood Orange and putting those complementary flavors in a totally unique glass package, Gratitude is well positioned for our targeted consumer audience.

Gratitude’s retail shelf price is between $2.99 to $3.49 per bottle. We have established cost for finished product per bottle and per 12-count case. We will approach and engage the same retail systems and value chain structure relative to all RTD beverage brands in the industry.

| 10 |

There will be three routes to market:

| 1. | Direct-to-Retail sales (grocery, big box, and drug chains). | |

| 2. | Direct Store Delivery (DSD) with shelf management for C-stores, specialty accounts, and such institutions as colleges and universities. | |

| 3. | Direct-to-Consumer sales via the internet. We will partner with Amazon for fulfillment. |

| 1. | Value chain for channel one includes delivered pricing from Gratitude direct to the retailer. We will target a suggested retail price in these accounts. Knowing that these accounts demand net delivery to their warehouses and a SET gross margin, Gratitude will price cases at wholesale to this channel of trade at a set price per bottle per cost of goods sold as calculated so that the Company has already calculated its margin less cost of freight for delivery. |

| 2. | Sales to DSD delivery systems require a more competitive wholesale price and higher retail price, which enables a structure where a distributor can earn a meaningful margin in an extremely competitive environment. The DSD retail customer is often a C-Store or Specialty store that requires regular deliveries and in-store management of inventory in “reaches”, meaning that often the DSD merchandises the shelf for his customer. This service cost is passed to the wholesaler. Therefore, to accommodate this pricing model, Gratitude must be more competitively priced to the DSD. The retailer also needs room to mark up the brand to accommodate their gross margin goals. So, Gratitude will reduce its gross margin in this channel and the DSD distributor will expect a set gross margin. The C-Store retailer usually expects a minimum set gross margin at his level. |

| 3. | The third sales model is direct consumer sales through the internet. These sales are always made by the case with an added delivery fee to the individual. We will partner with Amazon to handle orders and fulfillment and simply deliver to their regional warehouses. These sales provide great opportunity for gross margin having eliminated the distributor and retailer margin, but require significant digital marketing programs and advertising. We will use this channel immediately to service consumers that have heard of the brand but can’t find it at their local store yet. We know this channel will not be a large business initially but, as the brand grows, we plan to build this segment aggressively. |

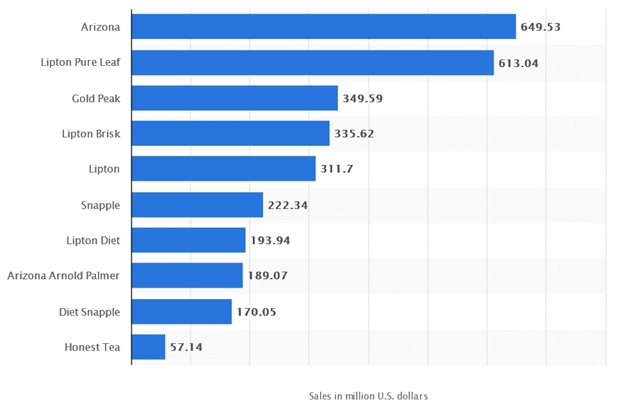

COMPETITION

Source: Statista 2018

| 11 |

RESEARCH, DEVELOPMENT AND PHILANTHROPY

Gratitude’s RD&P (Research, Development and Philanthropy) is working with a number of institutions to develop, license and/or acquire valid and proven intellectual property that fights cancer and promotes healthy aging. To that end, Gratitude has solely licensed patented technology from a prominent U.S. university research foundation for their patent (U.S. Patent #: 6,713,605) for the use of tea polyphenol esters for cancer prevention and treatment. The patented invention relates to novel polyphenol esters derived from green teas, which are potent inhibitors of the growth of cancerous cells, and their use in the prevention and treatment of conditions characterized by abnormal cellular proliferation. Gratitude will fund our charities from our sales and, in addition to giving away product to those who cannot afford them, we will contribute to university and institutional research studies that focus on chemo-protection, healthy aging, phytochemical superfoods and clean nutrition.

Corporation Information

Our principal executive offices are now located at 11231 US Highway One, Suite 200, North Palm Beach, Fl. 33408

. Our phone number is (561) 227-2727

. Our website is www.gratitudehealth.com.

| Item 1A. | Risk Factors |

We are a small public company and we face ever-increasing challenges in fulfilling the ever-rising costs of regulatory compliance under our federal, state, and other laws.

As a small company we have limited financial resources and we face compliance and regulatory costs that are increasing yearly. While we believe that our business strategies are sound, we cannot assure you that we will not incur such costs and have the ability to pass these increased costs onto our customers. As a result, we may incur significant operating losses and negative cash flow for the foreseeable future with resulting adverse impact on our continued existence as a corporation.

Our Total Current Liabilities were greater than our Total Current Assets as of December 31, 2017.

As our Total Current Liabilities as of December 31, 2017 were $1,889,243 and our Total Current Assets were only $203,889, we are and remain insolvent in that as of December 31, 2017 our Current Ratio (defined as Total Current Assets divided by Total Current Liabilities) was only 0.11. As a result, we do not have sufficient cash or other liquid current assets to meet our current financial obligations that become due within the twelve-months.

We incurred significant losses in 2017 and our cash flow is limited and volatile with the result that we face constant financial challenges in meeting our monthly operating and other financial obligations.

We incurred significant losses in 2017 and we cannot assure you that we will achieve profitability or if we do achieve it that we can sustain any profitability in the future. Further and as a small company, our cash flow is limited and we do not have a diversified customer base with diversified customers and markets compared to larger companies. As a result, our monthly cash flow is limited and more volatile than other larger companies. For this reason we are exposed to greater financial risks and persons who acquire our common stock could lose all or substantially all of their investment.

Continuing and increasing losses may directly impact our ability to remain in business.

We incurred approximately $365,000 in net losses for the year ended December 31, 2017. While we believe that if circumstances and market conditions allow, we may be able to achieve profitability, there can be no assurance that we will be successful in these efforts or if we are successful, that we can sustain any profitability. If are not successful in achieving and sustaining profitability and positive cash flow, then persons who acquire our common stock could lose all or substantially all of their investment.

Limited trading market and limited and sporadic trading of our Common Stock.

The trading market for our Common Stock is limited and any holder of our Common Stock will likely find it difficult to sell their shares in any large amount without incurring protracted delays and difficulty and without a significant reduction in the market price of the overall trading market for our Common Stock. The trading market for our Common Stock is limited and sporadic and there can be no assurance that any liquid trading market will develop or if it does develop that it can be sustained. As a result, any purchase of our Common Stock or any conversion of any debt instrument that is convertible into our Common Stock should only be considered by those who can afford to own a relatively illiquid investment and the likelihood that they may incur the total loss of their investment.

| 12 |

| Item 2. | Properties |

The Company’s corporate headquarters is located in Florida at 11231 US Highway One, Suite 200, North Palm Beach, Fl. 33408. Our telephone number, including area code, is (561) 227-2727

| Item 3. | Legal Proceedings. |

From time to time, the Company is involved in litigation matters relating to claims arising from the ordinary course of business. While the results of such claims and legal actions cannot be predicted with certainty, the Company’s management does not believe that there are claims or actions, pending or threatened against the Company, the ultimate disposition of which would have a material adverse effect on our business, results of operations, financial condition or cash flows.

| Item 4. | Mine Safety Disclosure |

Not Applicable

| 13 |

PART II

| Item 5. | Market For Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market Information

Our common stock is currently approved for quotation on the OTC Bulletin Board (OTCQB) maintained by the Financial Industry Regulatory Authority, Inc. under the symbol “GRTD”. There were no trades of our stock prior to April 6, 2015. The table below sets forth the high and low closing price per share of our common stock for each quarter during 2016 and 2017. These prices represent inter-dealer quotations without retail markup, markdown, or commission and may not necessarily represent actual transactions.

| Fiscal Quarter Ended | High | Low | ||||||

| 31-Mar-16 | $ | 0.35 | $ | 0.06 | ||||

| 30-Jun-16 | $ | 0.16 | $ | 0.05 | ||||

| 30-Sep-16 | $ | 0.16 | $ | 0.08 | ||||

| 31-Dec-16 | $ | 0.22 | $ | 0.08 | ||||

| 31-Mar-17 | $ | 0.12 | $ | 0.01 | ||||

| 31-June-17 | $ | 0.07 | $ | 0.0151 | ||||

| 31-Sep-17 | $ | 0.035 | $ | 0.012 | ||||

| 31-Dec-17 | $ | 0.11 | $ | 0.021 | ||||

Holders

As of March 29, 2018, there were approximately 64 holders of record of our common stock, and an indeterminate number of holders of unrestricted shares.

Dividends

We have not declared cash dividends on our common stock since our inception and we do not anticipate paying any cash dividends in the foreseeable future. Our current policy is to retain earnings, if any, for use in our operations and in the development of our business. Our future dividend policy will be determined from time to time by our board of directors.

| Item 6. | Selected Financial Data |

Not Applicable as we are a smaller reporting company.

| 14 |

| Item 7 | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

Except for the historical information, the following discussion contains forward-looking statements that are subject to risks and uncertainties. We caution you not to put undue reliance on any forward-looking statements, which speak only as of the date of this report. Our actual results or actions may differ materially from these forward-looking statements for many reasons. Our discussion and analysis of our financial condition and results of operations should be read in conjunction with the financial statements and related notes and with the understanding that our actual future results may be materially different from what we currently expect.

Forward-Looking Statements

Certain information contained in this Annual Report on Form 10-K, as well as other written and oral statements made or incorporated by reference from time to time by the Company and its representatives in other reports, filings with the Securities and Exchange Commission, press releases, conferences or otherwise, may be deemed to be forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934. This information includes, without limitation, statements concerning the Company's future financial position and results of operations, planned expenditures, business strategy and other plans for future operations, the future mix of revenues and business, customer retention, project reversals, commitments and contingent liabilities, future demand and industry conditions. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, it can give no assurance that such expectations will prove to have been correct. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Generally, the words “anticipate,” “believe,” “estimate,” “expect,” “may” and similar expressions, identify forward-looking statements, which generally are not historical in nature. Actual results could differ materially from the results described in the forward-looking statements due to the risks and uncertainties set forth in this Annual Report on Form 10-K, and those described from time to time in our future reports filed with the Securities and Exchange Commission.

The following discussion is qualified in its entirety by, and should be read in conjunction with, the Company's financial statements, including the notes thereto, included in this Annual Report on Form 10-K.

As used herein, the terms “we,” “us,” and “the Company” refers to Gratitude Health, Inc. (f/k/a Vapir Enterprises, Inc.), a Nevada corporation and its subsidiaries.

On March 26, 2018, Gratitude Health, Inc. f/ka Vapir Enterprises, Inc., a corporation organized under the laws of Nevada (the “Acquiror” or “Company”), Hamid Emarlou, the principal shareholder of the Acquiror (the “Acquiror Principal Shareholder”), Gratitude Health, Inc. (FL), a corporation organized under the laws of Florida (the “Acquiree”), and each of the Persons who are shareholders of the Acquiree (collectively, the “Acquiree Shareholders,” and individually an “Acquiree Shareholder”) entered into a Share Exchange Agreement (the “Agreement”) pursuant to which the Acquiree Shareholders (who are the holders of all of the issued and outstanding shares of common stock of the Acquiree (the “Acquiree Interests”)) have agreed to transfer to the Acquiror, and the Acquiror has agreed to acquire from the Acquiree Shareholders, all of the Acquiree Interests, in exchange for the issuance of 520,000 shares of Series A Preferred Stock and 500,000 shares of Series B Preferred Stock, to the Acquiree Shareholders the “Acquiror Shares”), which Acquiror Shares shall, upon conversion into 102,000,000 shares of common stock of the Acquiror, constitute approximately 85.84% on a fully diluted basis of the issued and outstanding shares of Acquiror Common Stock immediately after the closing of the transactions contemplated herein, in each case, on the terms and conditions as set forth in the Agreement. For accounting purposes, the Share Exchange was treated as an acquisition of Acquiror and a recapitalization of Acquiree. Acquiree is the accounting acquirer, and the result is of its operations carryover. On the Closing Date, Acquiror Principal Shareholder entered into a Spin Off Agreement with Acquiror for the sale of the existing wholly owned Vapir, Inc. subsidiary of the Acquiror in exchange for Acquiror Principal Shareholder’s shares of Common Stock of Acquiror. The Spin Off Agreement shall not close less than five (5) days from the closing of the Agreement. As of the date of filing this Annual Report on Form 10-K, the disposition of the Company’s Vapir business has not been consummated. This MD&A, which addresses the Company as of December 31, 2017, describes the traditional business of the Company as it existed on December 31, 2017, the end of the fiscal year for which this Form 10-K is filed. For information on the new business of Gratitude Health, Inc. after the March 26, 2018 share exchange, please refer to Section 1 of this Annual Report on Form 10-K.

| 15 |

Overview

Vapir Enterprises, Inc. was originally incorporated under the laws of the State of Nevada on December 17, 2009 under the name Apps Genius Corp and changed its name to Gratitude Health, Inc. on March 22, 2018. Our original business was to develop, market, publish and distribute social games and software applications that consumers could use on a variety of platforms, including social networks, wireless devices and stand-alone websites. We were unsuccessful in operating our business and on October 7, 2013 we entered into a Membership Interest Purchase Agreement with FAL Minerals LLC and we changed our name to FAL Exploration Corp. The agreement with FAL Minerals LLC has since been terminated and we have now entered into an Exchange Agreement with Vapir, Inc. and its shareholders. In addition, we changed our name to Vapir Enterprises, Inc. to better represent our new business operations.

On December 30, 2014, Vapir, Inc., a private California corporation (“Vapir”), which is the historical business of the Company’s wholly-owned subsidiary, entered into a Share Exchange Agreement with the Company, all of the stockholders of Vapir (the “Vapir Shareholders”), and the Company’s controlling stockholders whereby the Company agreed to acquire all of the issued and outstanding capital stock of Vapir in exchange for 38,624,768 shares of the Company’s common stock. On December 30, 2014, the transaction closed and Vapir is now a wholly-owned subsidiary of the Company. The number of shares issued represented approximately 80.0% of the issued and outstanding common stock immediately after the consummation of the Share Exchange Agreement. In addition, Vapir’s board of directors and management obtained the board and management control of the combined entity stock immediately after the consummation of the Share Exchange Agreement.

Vapir, Inc., our wholly-owned subsidiary, was incorporated on October 26, 2006 in the State of California.

Vapir, Inc. specializes in the revolutionary technology of digital aromatherapy which is the art and science of utilizing naturally extracted aromatic essences from plants to balance and harmonize while freshening the environment with pleasant and distinctive fragrances. We invent, develop and produce revolutionary and easy to use digital aromatherapy devices by utilizing heat and convection air.

Results of Operations

Year Ended December 31, 2017 Compared to the Year Ended December 31, 2016

Net Revenues

Net revenues for the years ended December 31, 2017 and 2016 were $761,102 and $1,086,971 respectively, a decrease of $325,869 or approximately 30%. The decrease in sales during the year ended December 31, 2017 was primarily attributable to a decrease in sales of our Prima vaporizer product as a result of a decline in demand.

Management views future sales level with a fair degree of uncertainty in that management has not been able to identify whether our sales level are trending up or down over the near term. As a result, we believed our sales level are subject to high level of uncertainty and unless market conditions and competitive conditions dramatically improve, we may not achieve or maintain sufficient sales volumes at levels that will allow us to achieve or maintain any profitability or positive cash flow. Our Total Liabilities as of December 31, 2017 far exceed our Total Assets. As a result we are insolvent and face a clear, existential risk of potential bankruptcy or other adverse actions by our creditors that could result in stockholders losing all of their investment.

Cost of Revenues

Cost of revenues for the year ended December 31, 2017 and 2016 were $366,075 and $678,056, respectively, a decrease of $311,981 or approximately 46%. The decrease is primarily due to the decrease in sales of our vaporizer products.

| 16 |

Operating Expenses

Total operating expenses for the year ended December 31, 2017 and 2016 were $661,179 and $1,944,309, respectively, a decrease of $1,283,130 or approximately 66%. The decrease in operating expenses during the year ended December 31, 2017 is primarily due to decrease in stock based consulting and stock based compensation expense of approximately $579,016, decrease in impairment of intangible assets of $126,426, and decrease in compensation of $237,191 as a result of decrease in number of employees. Additionally, an overall decrease in Selling, General and Administrative costs of approximately $281,141 as a result of cost cutting measures. While we implemented these cost cutting measures, we cannot assure you that these measures can be sustained or, if sustained that we will not incur other costs that far exceed the benefits obtained from these cost cutting measures. These and other factors would likely cause us to continue to incur significant and protracted losses in the future with the result that we may be facing claims by our creditors that we cannot satisfy since we are insolvent. As a result, there can be no guarantee that we will be successful in reducing our operating costs to a level that would allow us to achieve profitability, positive cash flow or both of them or if we do achieve these objectives that we can sustain profitability, positive cash flow or both of them. As of December 31, 2017, our Total Liabilities were $1,893,764 and our Total Assets as of that date were $387,655. As a result we are insolvent and any person who acquires our Common Stock or any other instrument that we have or will issue faces a high likelihood that they will lose their entire investment as we face a clear prospect of bankruptcy.

We continue to evaluate our operating cost with an aim of reducing our operating expenses in the future. However, some of our costs are fixed and we face intense competition from others who have more favorable operating cost structures and greater unit volumes that allows them to have an ability to compete aggressively on pricing. These and other factors would likely cause us to continue to incur significant and protracted losses in the future. As a result, there can be no guarantee that we will be successful in reducing our operating costs to a level that would allow us to achieve profitability, positive cash flow or both of them or if we do achieve these objectives that we can sustain profitability, positive cash flow or both of them.

Other Income (Expense), net

Total other expense, net, for the year ended December 31, 2017 and 2016 were $99,145 and $348,176, respectively, a decrease of $249,031 or %72%. The decrease in other expense is the primary result of the decreased amortization of debt discount of approximately $252,000 in connection with the issuance of convertible debentures.

Net loss

Net loss for the year ended December 31, 2017 and 2016 was $365,297 and $1,883,570, respectively, as a result of the items discussed above.

Liquidity and Capital Resources

Liquidity is the ability of a company to generate funds to support its current and future operations, satisfy its obligations, and otherwise operate on an ongoing basis. As of December 31, 2017, our total current liabilities exceeded our total current assets and, as a result, we had a working capital deficit and a further deterioration in our liquidity over the past 12 months.

We are not aware of any known demands, commitments or events that will result in our working capital liquidity increasing or decreasing in any material way. We are not aware of any matters that would have a positive impact on future operations. But over the past twelve months we have had increasing losses that is likely to continue if current market conditions continue.

| 17 |

Our net revenues are not sufficient to fund our operating expenses. At December 31, 2017, we had a cash balance of approximately $5,200 and working capital deficit of $1,685,000. Our cash decreased during the year ended December 31, 2017 by approximately $6,800 from our cash balance at December 31, 2016 of $12,000.

During the year ended December 31, 2017, we received related party advances for a total of $57,000 to fund our operating expenses, pay our obligations, and grow our company. We currently have no material commitments for capital expenditures.

During the year ended December 31, 2016, we borrowed $50,000 by issuing a note payable which will mature in February 2019 and we also received related party advances for a total of $430,000 to fund our operating expenses, pay our obligations, and grow our company. We currently have no material commitments for capital expenditures.

We are facing increasing demands that will likely require that we raise additional funds. If circumstances and market conditions allow, we may be able to raise additional capital but it may be under market conditions that are not favorable with the result that we may incur dilution or be required to accept debt covenants or other conditions that are onerous or which otherwise limit our ability to gain or attract additional financing in the future. Further, there can be no assurance that we will be successful in raising any additional funds or if we are successful, that we will be able to do so on terms that are reasonable in light of our current circumstances. As a small company with a limited product line and limited customer base, we face continuing risks and uncertainties that serve to make our company and an investment in our common stock subject to risks that are beyond our control. We estimate that based on current plans and assumptions, that our cash is not sufficient to satisfy our cash requirements under our present operating expectations, without further financing, for the next 12 months.

Our ability to generate and maintain a positive cash flow from our operations cannot be assured. Based solely on our own internal estimates without the benefit of any independent third party evaluation, we anticipate that our cash and cash flow will not be sufficient to satisfy our cash requirements and we will likely require significant additional external financing. The magnitude of the additional financing and its timing is not yet precisely known and depending on the level of our sales revenues and other operating needs we may be facing a prolonged multi-period scenario of negative cash flows with increasing losses. Further and since our Total Current Liabilities as of December 31, 2017 were $1,889,243 and our Total Current Assets were only $203,889, we are and remain insolvent in that as of December 31, 2017 our Current Ratio (defined as Total Current Assets divided by Total Current Liabilities) was only 0.11. That is, it was far below one (1). Overall, there can be no assurance that we will be successful in raising additional capital on a timely basis or if we are able to raise additional capital that we can raise it on terms that are reasonable in light of our current circumstances. As a result, we face increasing risks and persons who acquire our common stock may incur the loss of all or substantially all of their investment.

On April 3, 2015, we closed a financing transaction by entering into a Securities Purchase Agreement dated April 3, 2015 (the “Securities Purchase Agreement”) with two accredited investors (the “Purchasers”) for an aggregate subscription amount of $500,000 (the “Purchase Price”). Pursuant to the Securities Purchase Agreement, we issued a 6% Convertible Debenture (the “Debenture”) to each investor and warrants exercisable into an aggregate of 500,000 shares of common stock at an exercise price of $0.60 per share (the “Warrants”).

Each Debenture accrues interest at a rate equal to 6% per annum and the Debenture has an extended maturity date of July 26, 2018.

Each Debenture is convertible at any time and from time to time after its issuance date. Each Purchaser has the right to convert the Debenture that they hold into shares of the Company’s common stock at a conversion price equal to ten cents ($0.10). The conversion price, however, is subject to full ratchet anti-dilution in the event that Company issue any securities at a price lower than the conversion price then in effect. We have relied upon the use of debt financing to raise significant amounts of capital and we may continue to do so in the future. Under these circumstances and given our financial condition, any holder of our Common Stock is faced with the risk of the total loss of their investment.

Pursuant to the Securities Purchase Agreement, the Company issued warrants to acquire 500,000 shares of our common stock. The Warrants issued in this transaction are immediately exercisable and currently at an exercise price of ten cents ($0.10) per share, subject to applicable adjustments including full ratchet anti-dilution in the event that the Company issues any securities at a price lower than the exercise price then in effect. The Warrants have an expiration period of five years from the original issue date.

| 18 |

In January 2018, the Company issued an aggregate of 3,375,000 shares of common stock to Purchasers upon the conversion of $327,500 principal amount of note and $10,000 accrued interest pursuant to the conversion terms of the Convertible Debenture.

Currently, we have no other known alternative source for any additional financing except those sources which we have previously used and we cannot be assured that our prior sources will have any willingness to provide us with additional capital or, if they do, that the terms of any such additional financing will be reasonable in light of our current conditions. Further, we cannot assure you that we can continue to rely upon those existing financing sources in the future. We may not have sufficient working capital and funds from the collection of revenues that may allow us to maintain or expand our existing operations, to provide sufficient working capital to meet our operating needs and our outstanding financial obligations. For this reason, we anticipate that, based on current market conditions and our existing financial condition, we will likely need to obtain significant additional capital. In this sense we currently anticipate that we will remain dependent on our ability to secure additional financing.

In the event that we are able to secure a sufficient amount additional financing on a timely basis, it may include the issuance of equity or debt securities, obtaining credit facilities, or entering into other financing arrangements on such terms as then existing market conditions require. The capital market for small or micro-cap companies has been and likely will remain very difficult in the near future. As a result our ability to obtain additional capital on terms that are reasonable in light of current market conditions cannot be assured. We may be forced to obtain additional capital on terms that could limit our long-term ability to remain in business or otherwise materially restrict our operations. Further, our current financial structure and the demands of our existing creditors is such that we face a clear risk of not being able to meet the obligations to our creditors. In that event, we face a clear risk of insolvency with the result that persons who acquire our common stock may lose all or substantially all of their investment.

Further, the market price of our common stock and the uncertainties of the U.S. economy and other factors will likely negatively impact us and the financing options that we may have. Any downturn in the U.S. equity and debt markets could also make it more difficult for us to obtain additional financing.

Even if we are able to raise the additional financing, it is possible that we could incur unexpected costs and expenses, fail to collect amounts owed to us, or experience significant and protracted unexpected cash requirements that would force us to seek other, less-attractive alternative financing on terms that could result in significant dilution and with other terms that are not reasonable in light of our current circumstances.

Currently we do not have any commitment from any outside financing source to meet our anticipated financing needs and we have no basis to believe that any such commitment is forthcoming. Furthermore, in the event that we were to issue additional equity or debt securities, stockholders may experience significant additional dilution or the new equity securities may have rights, preferences or privileges senior to those of existing holders of our common stock. And in the case of any issuance of one or more debt securities, the debt covenants may restrict our operating ability and our ability to raise additional financing from debt.

Overall if we are unable to raise additional capital on terms that are reasonable in light of current market conditions we will likely restrict our ability to grow and may reduce our ability to continue to conduct business operations. We face a clear risk of insolvency unless we are able to successfully raise significant additional capital on terms that will allow us to reduce our financial obligations and improve our profitability and cash flow. If we are unable to obtain significant additional financing, we will likely be required to curtail our marketing and development plans and possibly cease our operations with the clear risk of insolvency.

We anticipate that depending on market conditions and our plan of operations, we may incur operating losses in the foreseeable future. Therefore, there is substantial doubt about our ability to continue as a going concern and persons who acquire our common stock face the risk of losing all or substantially all of their investment.

| 19 |

Inflation and Changing Prices

Neither inflation nor changing prices for the year ended December 31, 2017 had a material impact on our operations.

Off-Balance Sheet Arrangements

None.

Quantitative and Qualitative Disclosures About Market Risk

Not applicable.

Critical Accounting Policies

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“US GAAP”) requires our management to make assumptions, estimates, and judgments that affect the amounts reported, including the notes thereto, and related disclosures of commitments and contingencies, if any. We have identified certain accounting policies that are significant to the preparation of our financial statements. These accounting policies are important for an understanding of our financial condition and results of operations. Critical accounting policies are those that are most important to the portrayal of our financial condition and results of operations and require management’s difficult, subjective, or complex judgment, often as a result of the need to make estimates about the effect of matters that are inherently uncertain and may change in subsequent periods. Certain accounting estimates are particularly sensitive because of their significance to financial statements and because of the possibility that future events affecting the estimate may differ significantly from management’s current judgments.

We believe the following critical accounting policies involve the most significant estimates and judgments used in the preparation of our financial statements. We believe the critical accounting policies in Note 2 to the consolidated financial statements appearing in the Annual Report, Form 10-K for the year ended December 31, 2017, affect our more significant judgments and estimates used in the preparation of our consolidated financial statements.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities, and the reported amounts of revenues and expenses during the period. Actual results could differ from those estimates. Significant matters requiring the use of estimates and assumptions include, but are not limited to allowance for doubtful accounts, inventory obsolescence and markdowns, the useful life of property and equipment, the valuation of deferred tax assets and liabilities, valuation of intangible assets, the assumptions used to calculate fair value of stock options and warrants granted, stock-based compensation and the fair value of common stock issued.

| 20 |

| Item 8. | Financial Statements and Supplementary Data |

GRATITUDE HEALTH, INC. AND SUBSIDIARY

(FORMERLY KNOWN AS VAPIR ENTERPRISES, INC.)

DECEMBER 31, 2017 and 2016

INDEX TO THE CONSOLIDATED FINANCIAL STATEMENTS

CONTENTS

| F-1 |

|

D. Brooks and Associates CPA’s, P.A. Certified Public Accountants ● Certified Valuation Analysts |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and

Stockholders of Gratitude Health, Inc, formerly known as Vapir Enterprises, Inc.

Opinion on the Financial Statements

We have audited the accompanying consolidated balance sheets of Gratitude Health, Inc, formerly known as Vapir Enterprises, Inc. (the “Company”) as of December 31, 2017 and 2016, and the related consolidated statements of operations, stockholders’ deficit, and cash flows for each of the years in the two-year period ended December 31, 2017, and the related notes to the consolidated financial statements (collectively referred to as the financial statements). In our opinion, the consolidated financial statements present fairly, in all material respects, the consolidated financial position of the Company as of December 31, 2017 and 2016, and the results of its operations and its cash flows for each of the years in the two year period ended December 31, 2017, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 3 to the consolidated financial statements, the Company has incurred operating losses, has incurred negative cash flows from operations and has a working capital deficit. These and other factors raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plan regarding these matters is also described in Note 3 to the financial statements. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

| /s/ D. Brooks and Associates CPA’s, P.A | |

| D. Brooks and Associates CPA’s, P.A |

We have served as the Company’s auditor since 2016.

|

Palm Beach Gardens, Florida |

|

| March 30, 2018 |

| F-2 |

GRATITUDE HEALTH, INC. AND SUBSIDIARY

(FORMERLY KNOWN AS VAPIR ENTERPRISES, INC.)

CONSOLIDATED BALANCE SHEETS

| As of | As of | |||||||

| December 31, 2017 | December 31, 2016 | |||||||

| ASSETS | ||||||||

| CURRENT ASSETS: | ||||||||

| Cash | $ | 5,203 | $ | 12,022 | ||||

| Accounts receivable, net | 1,469 | 4,773 | ||||||

| Inventory, net | 112,399 | 155,938 | ||||||

| Prepaid expense and other current assets | 14,078 | 12,486 | ||||||

| Advances to suppliers | 70,740 | 103,274 | ||||||

| Total Current Assets | 203,889 | 288,493 | ||||||

| OTHER ASSETS: | ||||||||

| Property and equipment, net | 38,740 | 64,562 | ||||||

| Intangible assets, net | 142,213 | 181,574 | ||||||

| Deposit | 2,813 | 2,813 | ||||||

| Total Other Assets | 183,766 | 248,949 | ||||||

| TOTAL ASSETS: | $ | 387,655 | $ | 537,442 | ||||

| LIABILITIES AND STOCKHOLDERS' DEFICIT | ||||||||

| CURRENT LIABILITIES: | ||||||||

| Accounts payable and accrued expenses | $ | 266,478 | $ | 299,356 | ||||

| Convertible notes payable | 500,000 | 500,000 | ||||||

| Loan payable | 197,000 | 197,000 | ||||||

| Notes payable - current maturities | 15,858 | 21,722 | ||||||

| Customer deposits | 3,851 | 27,633 | ||||||

| Advances from related party | 892,500 | 795,984 | ||||||

| Deferred rent | 13,556 | 14,191 | ||||||

| Total Current Liabilities | 1,889,243 | 1,855,886 | ||||||

| LONG-TERM LIABILITIES: | ||||||||

| Notes payable, net of current maturities | 4,521 | 20,410 | ||||||

| Total Long-term Liabilities | 4,521 | 20,410 | ||||||

| Total Liabilities | 1,893,764 | 1,876,296 | ||||||

| COMMITMENTS AND CONTINGENCIES | ||||||||

| STOCKHOLDERS' DEFICIT: | ||||||||

| Preferred stock $0.001 par value: 20,000,000 shares authorized; | ||||||||

| none issued and outstanding | - | - | ||||||

| Common stock $0.001 par value: 300,000,000 shares authorized; | ||||||||

| 49,766,819 shares issued and outstanding. | 49,767 | 49,767 | ||||||

| Additional paid in capital | 1,893,349 | 1,501,220 | ||||||

| Accumulated deficit | (3,449,225 | ) | (2,889,841 | ) | ||||

| Total Stockholders' Deficit | (1,506,109 | ) | (1,338,854 | ) | ||||

| Total Liabilities and Stockholders' Deficit | $ | 387,655 | $ | 537,442 | ||||

See accompanying notes to the consolidated financial statements.

| F-3 |

GRATITUDE HEALTH, INC. AND SUBSIDIARY

(FORMERLY KNOWN AS VAPIR ENTERPRISES, INC.)

CONSOLIDATED STATEMENTS OF OPERATIONS

| For the Years Ended | ||||||||

| December 31, 2017 | December 31, 2016 | |||||||

| Revenues, net | $ | 761,102 | $ | 1,086,971 | ||||

| Cost of revenues | 366,075 | 678,056 | ||||||

| Gross profit | 395,027 | 408,915 | ||||||

| OPERATING EXPENSES: | ||||||||

| Selling expenses | 38,678 | 183,382 | ||||||

| Compensation | 387,698 | 839,652 | ||||||

| Impairment of intangible assets | - | 126,426 | ||||||

| Professional and consulting fees | 72,813 | 496,422 | ||||||

| General and administrative | 161,990 | 298,427 | ||||||

| Total Operating Expenses | 661,179 | 1,944,309 | ||||||

| LOSS FROM OPERATIONS | (266,152 | ) | (1,535,394 | ) | ||||

| OTHER EXPENSE: | ||||||||

| Interest expense, net | (99,145 | ) | (348,176 | ) | ||||

| Other expense, net | (99,145 | ) | (348,176 | ) | ||||

| LOSS BEFORE INCOME TAX PROVISION | (365,297 | ) | (1,883,570 | ) | ||||

| INCOME TAX PROVISION | - | - | ||||||

| NET LOSS | $ | (365,297 | ) | $ | (1,883,570 | ) | ||

| LOSS PER SHARE: | ||||||||

| Basic and diluted | $ | (0.007 | ) | $ | (0.04 | ) | ||

| WEIGHTED AVERAGE COMMON SHARES OUTSTANDING: | ||||||||

| Basic and diluted | 49,766,819 | 49,719,009 | ||||||

See accompanying notes to the consolidated financial statements.

| F-4 |

GRATITUDE HEALTH, INC. AND SUBSIDIARY

(FORMERLY KNOWN AS VAPIR ENTERPRISES, INC.)

CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS' DEFICIT

For the Years Ended December 31, 2017 and 2016

| Common Stock $0.001 Par Value | Additional | Total | ||||||||||||||||||

| Number of | Paid-in | Accumulated | Stockholders' | |||||||||||||||||

| Shares | Amount | Capital | Deficit | Deficit | ||||||||||||||||

| Balance, December 31, 2015 | 48,466,819 | $ | 48,467 | $ | 31,374 | $ | (514,806 | ) | $ | (434,965 | ) | |||||||||

| Common stock issued for services | 1,300,000 | 1,300 | 338,700 | - | 340,000 | |||||||||||||||

| Stock-based compensation in connection with options granted | - | - | 437,058 | - | 437,058 | |||||||||||||||

| Cumulative effect adjustment upon adoption of ASU 2017-11 | - | - | 694,088 | (491,465 | ) | 202,623 | ||||||||||||||

| Net loss | - | - | - | (1,883,570 | ) | (1,883,570 | ) | |||||||||||||

| Balance, December 31, 2016 | 49,766,819 | 49,767 | 1,501,220 | (2,889,841 | ) | (1,338,854 | ) | |||||||||||||

| Cumulative effect adjustment upon adoption of ASU 2017-11 | - | - | 194,087 | (194,087 | ) | - | ||||||||||||||

| Stock-based compensation in connection with options granted | - | - | 198,042 | - | 198,042 | |||||||||||||||

| Net loss | - | - | - | (365,297 | ) | (365,297 | ) | |||||||||||||

| Balance, December 31, 2017 | 49,766,819 | $ | 49,767 | $ | 1,893,349 | $ | (3,449,225 | ) | $ | (1,506,109 | ) | |||||||||

See accompanying notes to the consolidated financial statements.

| F-5 |

GRATITUDE HEALTH, INC. AND SUBSIDIARY

(FORMERLY KNOWN AS VAPIR ENTERPRISES, INC.)

CONSOLIDATED STATEMENTS OF CASH FLOWS

| For the Years Ended | ||||||||

| December 31, 2017 | December 31, 2016 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net loss | $ | (365,297 | ) | $ | (1,883,570 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities | ||||||||

| Bad debt expense (recovery) | (3,013 | ) | 1,619 | |||||

| Depreciation | 25,822 | 25,906 | ||||||

| Inventory markdown | - | 39,734 | ||||||

| Amortization of intangible assets | 39,361 | 67,176 | ||||||

| Amortization of deferred financing cost | - | 11,352 | ||||||

| Amortization of debt discount | - | 252,276 | ||||||

| Impairment of intangible assets | - | 126,426 | ||||||

| Stock based compensation | 198,042 | 777,058 | ||||||

| Changes in assets and liabilities: | ||||||||

| Accounts receivable | 6,317 | 18,126 | ||||||

| Prepaid expense and other current assets | (1,592 | ) | (5,414 | ) | ||||

| Advances to suppliers | 32,534 | 33,153 | ||||||

| Inventory | 43,539 | 16,739 | ||||||

| Accounts payable and accrued expenses | 6,638 | 73,444 | ||||||

| Deferred rent | (635 | ) | 3,463 | |||||

| Customer deposits | (23,782 | ) | 7,024 | |||||

| NET CASH USED IN OPERATING ACTIVITIES | (42,066 | ) | (435,488 | ) | ||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Purchase of property and equipment | - | (2,800 | ) | |||||

| NET CASH USED IN OPERATING ACTIVITIES | - | (2,800 | ) | |||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Advances from related party | 57,000 | 430,000 | ||||||

| Repayments to related party for advances | - | (4,630 | ) | |||||

| Proceeds received from notes payable | - | 50,000 | ||||||

| Repayments of notes payable | (21,753 | ) | (32,918 | ) | ||||

| NET CASH PROVIDED BY FINANCING ACTIVITIES | 35,247 | 442,452 | ||||||

| NET CHANGE IN CASH | (6,819 | ) | 4,164 | |||||

| CASH - beginning of year | 12,022 | 7,858 | ||||||

| CASH - end of year | $ | 5,203 | $ | 12,022 | ||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION: | ||||||||

| Interest paid | $ | 12,709 | $ | 18,875 | ||||

| Income taxes paid | $ | - | $ | - | ||||

See accompanying notes to the consolidated financial statements.

| F-6 |

GRATITUDE HEALTH, INC. AND SUBSIDIARY

(FORMERLY KNOWN AS VAPIR ENTERPRISES, INC.)

NOTES TO CONSOLIDATED FINANCIAL

STATEMENTS

DECEMBER 31, 2017 and 2016

Note 1 - Organization and Operations

Gratitude Health, Inc., (formerly known as Vapir Enterprises Inc.) ( the “Company”) was incorporated in the State of Nevada on December 17, 2009. Effective March 23, 2018, the Company changed its name to Gratitude Health, Inc. The Company’s principal business was focused on inventing, developing and producing aromatherapy devices and vaporizers. The Company’s aromatherapy devices utilize heat and convection air and thereby extract natural essences and produce fresh fragrances. Vapir, Inc. (“Vapir”) is a wholly owned subsidiary of the Company and was incorporated in the State of California in October 2006.

Note 2 - Significant and Critical Accounting Policies and Practices