Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - JAKKS PACIFIC INC | a51771406ex32_2.htm |

| EX-32.1 - EXHIBIT 32.1 - JAKKS PACIFIC INC | a51771406ex32_1.htm |

| EX-31.2 - EXHIBIT 31.2 - JAKKS PACIFIC INC | a51771406ex31_2.htm |

| EX-31.1 - EXHIBIT 31.1 - JAKKS PACIFIC INC | a51771406ex31_1.htm |

| EX-23.1 - EXHIBIT 23.1 - JAKKS PACIFIC INC | a51771406ex23_1.htm |

| EX-21 - EXHIBIT 21 - JAKKS PACIFIC INC | a51771406ex21.htm |

| EX-10.8.5 - EXHIBIT 10.8.5 - JAKKS PACIFIC INC | a51771406ex10_85.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

☒

|

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

For the Fiscal Year Ended December 31, 2017

|

|

|

|

|

☐

|

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ____________ to ____________

Commission File Number 0-28104

JAKKS PACIFIC, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

95-4527222

|

|

(State or other jurisdiction of

|

(I.R.S. Employer

|

|

incorporation or organization)

|

Identification No.)

|

|

2951 28th St.

|

|

|

Santa Monica, California

|

90405

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: (424) 268-9444

Securities registered pursuant to Section 12(b) of the Exchange Act:

|

Title of each class

|

Name of each exchange

on which registered

|

|

Common Stock, $.001 par value per share

|

Nasdaq Global Select

|

Securities registered pursuant to Section 12(g) of the Exchange Act:

Title of Class

Common Stock, $.001 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15 of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (check one):

|

☐ Large Accelerated Filer

|

☒ Accelerated Filer

|

☐ Non-Accelerated Filer

|

☐ Smaller Reporting Company

|

☐ Emerging growth company |

|

|

|

(Do not check if a Smaller Reporting Company)

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the voting and non-voting common equity (the only such common equity being Common Stock, $.001 par value per share) held by non-affiliates of the registrant (computed by reference to the closing sale price of the Common Stock on June 30, 2017 of $4.00) is $107,392,952.

The number of shares outstanding of the registrant’s Common Stock, $.001 par value (being the only class of its common stock), is 29,159,324 as of March 15, 2018.

Documents Incorporated by Reference

None.

1

JAKKS PACIFIC, INC.

INDEX TO ANNUAL REPORT ON FORM 10-K

For the Fiscal Year ended December 31, 2017

Items in Form 10-K

|

|

|

Page

|

|

|

PART I

|

|

|

3

|

||

|

12

|

||

|

Item 1B.

|

Unresolved Staff Comments

|

None

|

|

18

|

||

|

19

|

||

|

20

|

||

|

|

PART II

|

|

|

21

|

||

|

24

|

||

|

26

|

||

|

36

|

||

|

37

|

||

|

Item 9.

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure

|

None

|

|

72

|

||

|

Item 9B.

|

Other Information

|

None

|

|

|

PART III

|

|

|

74

|

||

|

79

|

||

|

99

|

||

|

101

|

||

|

101

|

||

|

|

PART IV

|

|

|

103

|

||

|

105

|

||

|

|

106

|

|

|

Certifications

|

|

|

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

This report includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. For example, statements included in this report regarding our financial position, business strategy and other plans and objectives for future operations, and assumptions and predictions about future product demand, supply, manufacturing, costs, marketing and pricing factors are all forward-looking statements. When we use words like “intend,” “anticipate,” “believe,” “estimate,” “plan” or “expect,” we are making forward-looking statements. We believe that the assumptions and expectations reflected in such forward-looking statements are reasonable, based upon information available to us on the date hereof, but we cannot assure you that these assumptions and expectations will prove to have been correct or that we will take any action that we may presently be planning. We have disclosed certain important factors that could cause our actual results to differ materially from our current expectations elsewhere in this report. You should understand that forward-looking statements made in this report are necessarily qualified by these factors. We are not undertaking to publicly update or revise any forward-looking statement if we obtain new information or upon the occurrence of future events or otherwise.

2

PART I

In this report, “JAKKS,” the “Company,” “we,” “us” and “our” refer to JAKKS Pacific, Inc., its subsidiaries and our majority owned joint venture.

Company Overview

We are a leading multi-line, multi-brand toy company that designs, produces, markets and distributes toys and related products, consumables and related products, electronics and related products, kids indoor and outdoor furniture, and other consumer products. We focus our business on acquiring or licensing well-recognized trademarks and brand names, most with long product histories (“evergreen brands”). We seek to acquire these evergreen brands because we believe they are less subject to market fads or trends. We also develop proprietary products marketed under our own trademarks and brand names, and have historically acquired complementary businesses to further grow our portfolio. For accounting purposes, our products have been divided into three segments: (i) U.S. and Canada, (ii) International and (iii) Halloween. Segment information with respect to revenues, assets and profits or losses attributable to each segment is contained in Note 3 to the audited consolidated financial statements contained below in Item 8. Our products include:

Traditional Toys and Electronics

|

●

|

Action figures and accessories, including licensed characters, principally based on Batman®, Star Wars® and Nintendo® franchises;

|

|

|

|

|

●

|

Toy vehicles, including Max Tow®, Road Champs®, Fly Wheels® and MXS® toy vehicles and accessories;

|

|

●

|

Dolls and accessories, including small dolls, large dolls, fashion dolls and baby dolls based on licenses, including Disney’s Frozen, Disney Princess, Disney Fairies, infant and pre-school toys based on PBS’s Daniel Tiger’s Neighborhood®;

|

|

|

|

|

●

|

Private label products as “exclusives” for a myriad of retail customers in many product categories; and

|

|

|

|

|

●

|

Foot-to-floor ride-on toys based on Fisher Price®, Kawasaki®, and DC Comics®, inflatable environments, tents and wagons.

|

|

|

Role Play, Novelty and Seasonal Toys

|

●

|

Role play, dress-up, pretend play and novelty products for boys and girls based on well-known brands and entertainment properties such as Disney’s Frozen, Black & Decker®, McDonald’s®, Disney Princess and Disney Fairies, as well as those based on our own proprietary brands;

|

|

|

|

|

●

|

Indoor and outdoor kids’ furniture, activity trays and tables and room décor; kiddie pools, seasonal and outdoor products, including those based on Crayola®, Disney characters and more, and Funnoodle® pool floats;

|

|

|

|

|

●

|

Halloween and everyday costumes for all ages based on licensed and proprietary non-licensed brands, including Spiderman®, Toy Story, Sesame Street®, Power Rangers®¸Hasbro® brands and Disney’s Frozen, Disney Princess and related Halloween accessories; and

|

|

|

|

|

●

|

Junior sports and outdoor activity toys including Skyball® hyper-charged balls and sport sets and Wave Hoops® toy hoops marketed under our Maui ® brand.

|

3

We continually review the marketplace to identify and evaluate popular and evergreen brands and product categories that we believe have the potential for growth. We endeavor to generate growth within these lines by:

|

|

●

|

creating innovative products under our established licenses and brand names;

|

|

|

●

|

adding new items to the branded product lines that we expect will enjoy greater popularity;

|

|

|

●

|

infusing innovation and technology when appropriate to make them more appealing to today’s kids; and

|

|

|

●

|

focusing our marketing efforts to enhance consumer recognition and retailer interest.

|

Our Business Strategy

In addition to developing our own proprietary brands and marks, licensing popular trademarks enables us to use these high-profile marks at a lower cost than we would incur if we purchased these marks or developed comparable marks on our own. By licensing trademarks, we have access to a far greater range of marks than would be available for purchase. We also license technology developed by unaffiliated inventors and product developers to enhance the design and functionality of our products.

We sell our products through our in-house sales staff and independent sales representatives to toy and mass-market retail chain stores, department stores, office supply stores, drug and grocery store chains, club stores, toy specialty stores and wholesalers. Our three largest customers are Wal-Mart, Target and Toys ‘R’ Us, which accounted for approximately 25.5%, 17.8% and 11.3%, respectively, of our net sales in 2017. No other customer accounted for more than 10.0% of our net sales in 2017.

Our Growth Strategy

In 2016 and 2017, we generated net sales of $706.6 million and $613.1 million, respectively, and net income of $1.2 million in 2016 and a net loss of $83.1 million in 2017. Key elements of our growth strategy include:

● Expand Core Products. We manage our existing and new brands through strategic product development initiatives, including introducing new products, modifying existing products and extending existing product lines to maximize their longevity. Our marketing teams and product designers strive to develop new products or product lines to offer added technological, aesthetic and functional improvements to our extensive portfolio.

● Enter New Product Categories. We use our extensive experience in the toy and other consumer product industries to evaluate products and licenses in new product categories and to develop additional product lines. We began marketing licensed classic video games for simple plug-in use with television sets and expanded into several related categories by infusing additional technologies such as motion gaming and through the licensing of this category from our current licensors, such as Disney and Viacom which owns Nickelodeon®.

● Pursue Strategic Acquisitions. We supplement our internal growth with selected strategic acquisitions. In October 2016, we acquired the operating assets of the C’est Moi™ performance makeup and youth skincare product lines whose distribution is limited primarily to Asia. We expect to launch a full line of makeup and skincare products branded under the C’est Moi name in the U.S. and Canada in the first quarter of 2018. We will continue focusing our acquisition strategy on businesses or brands that we believe have compatible product lines and/or offer valuable trademarks or brands.

4

● Acquire Additional Character and Product Licenses. We have acquired the rights to use many familiar brand and character names and logos from third parties that we use with our primary trademarks and brands. Currently, among others, we have license agreements with Nickelodeon®, Disney and Warner Bros.®, as well as with the licensors of the many popular licensed children’s characters previously mentioned, among others. We intend to continue to pursue new licenses from these entertainment and media companies and other licensors. We also intend to continue to purchase additional inventions and product concepts through our existing network of inventors and product developers.

● Expand International Sales. We believe that foreign markets, especially Europe, Australia, Canada, Latin America and Asia, offer us significant growth opportunities. In 2017, our sales generated outside the United States were approximately $134.0 million, or 21.9% of total net sales. We intend to continue to expand our international sales and further expand distribution agreements in Europe to capitalize on our experience and our relationships with foreign distributors and retailers. We expect these initiatives to contribute to our international growth in 2018.

● Capitalize On Our Operating Efficiencies. We believe that our current infrastructure and operating model can accommodate growth without a proportionate increase in our operating and administrative expenses, thereby increasing our operating margins.

The execution of our growth strategy, however, is subject to several risks and uncertainties and we cannot assure you that we will continue to experience growth in, or maintain our present level of net sales (see “Risk Factors,” in Item 1A). For example, our growth strategy will place additional demands upon our management, operational capacity and financial resources and systems. The increased demand upon management may necessitate our recruitment and retention of additional qualified management personnel. We cannot assure you that we will be able to recruit and retain qualified personnel or expand and manage our operations effectively and profitably. To effectively manage future growth, we must continue to expand our operational, financial and management information systems and to train, motivate and manage our work force. While we believe that our operational, financial and management information systems will be adequate to support our future growth, no assurance can be given they will be adequate without significant investment in our infrastructure. Failure to expand our operational, financial and management information systems or to train, motivate or manage employees could have a material adverse effect on our business, financial condition and results of operations.

Moreover, implementation of our growth strategy is subject to risks beyond our control, including competition, market acceptance of new products, changes in economic conditions, our ability to obtain or renew licenses on commercially reasonable terms and our ability to finance increased levels of accounts receivable and inventory necessary to support our sales growth, if any.

Furthermore, we cannot assure you that we can identify attractive acquisition candidates or negotiate acceptable acquisition terms, and our failure to do so may adversely affect our results of operations and our ability to sustain growth.

Finally, our acquisition strategy involves a number of risks, each of which could adversely affect our operating results, including difficulties in integrating acquired businesses or product lines, assimilating new facilities and personnel and harmonizing diverse business strategies and methods of operation; diversion of management attention from operation of our existing business; loss of key personnel from acquired companies; and failure of an acquired business to achieve targeted financial results.

5

Industry Overview

According to Toy Industry Association, Inc., the leading toy industry trade group, the United States is the world’s largest toy market, followed by Japan and Western Europe. Total retail sales of toys, excluding video games, in the United States, were approximately $20.7 billion in 2017. We believe the two largest United States toy companies, Mattel and Hasbro, collectively hold a dominant share of the domestic non-video toy market. In addition, hundreds of smaller companies compete in the design and development of new toys, the procurement of character and product licenses, and the improvement and expansion of previously introduced products and product lines.

Over the past few years, the toy industry has experienced substantial consolidation among both toy companies and toy retailers. We believe that the ongoing consolidation of toy companies provides us with increased growth opportunities due to retailers’ desire to not be entirely dependent upon a few dominant toy companies. Retailer concentration also enables us to ship products, manage account relationships and track point of sale information more effectively and efficiently.

Products

We focus our business on acquiring or licensing well-recognized trademarks or brand names, and we seek to acquire evergreen brands which are less subject to market fads or trends. Generally, our license agreements for products and concepts call for royalties ranging from 1% to 21% of net sales, and some may require minimum guarantees and advances. Our principal products include:

Traditional Toys

Wheels Products

Motorized and plastic toy vehicles and accessories.

Our extreme sports offerings include our MXS® line of motorcycles with generic and well-known riders and other vehicles include off-road vehicles and skateboards, which are sold individually and with playsets and accessories. In 2014, we launched our proprietary line of motorized vehicles under the brand Max Tow®, and in 2015, we expanded the product line to include higher performance versions as well as mini size vehicles and play sets under the Max Tow®Mini line. In 2017, we launched Real Workin’ Buddies™ with Mr. Dusty, the talking cleaning dump truck.

Action Figures and Accessories

We currently develop, manufacture and distribute other action figures and action figure accessories including those based on Star Wars® and Batman®, capitalizing on the expertise we built in the action figure category.

Our line of Big-Figs™ large scale action figures features an assortment of 20” figures, 31” figures, and 48” figures of characters including Superman®, Power Rangers®, Star Wars® and Teenage Mutant Ninja Turtles®.

6

Dolls

Dolls and accessories include small dolls, large dolls, fashion dolls and baby dolls based on licenses, including Disney’s Frozen, Disney Princess, Disney Fairies, including an extensive line of baby doll accessories that emulate real baby products that mothers today use; plush, infant and pre-school toys, and private label fashion dolls for other retailers and sold to Disney Stores and Disney Parks and Resorts. In 2016, we launched lines of dolls based on Disney’s animated feature Moana and animated television series Elena of Avalor.

Role Play, Novelty & Seasonal

Role Play and Dress-up Products

Our line of role play and dress-up products for boys and girls features entertainment and consumer products properties such as Disney’s Frozen, Disney Princess, Disney Fairies, Moana, Elena of Avalor and Black & Decker®. These products generated a significant amount of sales in 2015, 2016 and 2017.

Seasonal/ Outdoor Products

We have a wide range of seasonal toys and outdoor and leisure products including our Maui® line of proprietary products including Sky Ball®, Sky Bouncer® and Wave Hoop® among other outdoor toys. Our Funnoodle® pool toys include basic Funnoodle® pool floats and a variety of other pool toys.

Indoor and Outdoor Kids’ Furniture

We produce an extensive array of licensed indoor and outdoor kids' furniture and activity tables, and room decor. Our licensed portfolio includes character licenses, including Crayola®, Disney Princess, Toy Story, Mickey Mouse, Paw Patrol®, and others. Products include children’s puzzle furniture, tables and chairs to activity sets, trays, stools and a line of licensed molded kiddie pools, among others.

Halloween and Everyday Costume Play

We produce an expansive and innovative line of Halloween costumes and accessories which includes a wide range of non-licensed Halloween costumes such as horror, pirates, historical figures and aliens to animals, vampires, angels and more, as well as popular licensed characters from top intellectual property owners including Disney, Hasbro®, Sesame Workshop®, Mattel®, and many others. In 2016, we launched new licenses including Lego® brands.

7

Sales, Marketing and Distribution

We sell all of our products through our own in-house sales staff and independent sales representatives to toy and mass-market retail chain stores, department stores, office supply stores, drug and grocery store chains, club stores, toy specialty stores and wholesalers. Our three largest customers are Wal-Mart, Target and Toys ‘R’ Us, which accounted for approximately 54.9% of our net sales in 2016 and 54.6% of our net sales in 2017. We generally sell products to our customers pursuant to letters of credit or, in some cases, on open account with payment terms typically varying from 30 to 90 days. From time to time, we allow our customers credits against future purchases from us in order to facilitate their retail markdown and sales of slow-moving inventory. We also sell our products through e-commerce sites, including Walmart.com, Target.com, Toysrus.com and Amazon.com.

We contract the manufacture of most of our products to unaffiliated manufacturers located in The People’s Republic of China (“China”). We sell the finished products on a letter of credit basis or on open account to our customers, many of whom take title to the goods in Hong Kong or China. These methods allow us to reduce certain operating costs and working capital requirements. A portion of our sales originate in the United States, so we hold certain inventory in our warehouses and fulfillment facilities. To date, a majority of all of our sales has been to domestic customers. We intend to continue expanding distribution of our products into foreign territories and, accordingly, we have:

|

|

●

|

entered into a joint venture in China,

|

|

|

●

|

engaged representatives to oversee sales in certain foreign territories,

|

|

|

●

|

engaged distributors in certain foreign territories,

|

|

|

●

|

established direct relationships with retailers in certain foreign territories,

|

|

|

●

|

opened sales offices in Europe and Mexico,

|

|

|

●

|

opened sales offices and a distribution center in Canada, and

|

|

|

●

|

expanded in-house resources dedicated to product development and marketing of our lines.

|

8

Outside of the United States, we currently sell our products primarily in Europe, Australia, Canada, Latin America and Asia. Sales of our products abroad accounted for approximately $134.0 million, or 21.9% of our net sales in 2017 and approximately $162.5 million, or 23.0% of our net sales in 2016. We believe that foreign markets present an attractive opportunity, and we plan to intensify our marketing efforts and further expand our distribution channels abroad.

We establish reserves for sales allowances, including promotional allowances and allowances for anticipated defective product returns, at the time of shipment. The reserves are determined as a percentage of net sales based upon either historical experience or upon estimates or programs agreed upon by our customers and us.

We obtain, directly, or through our sales representatives, orders for our products from our customers and arrange for the manufacture of these products as discussed below. Cancellations generally are made in writing, and we take appropriate steps to notify our manufacturers of these cancellations. We may incur costs or other losses as a result of cancellations.

We maintain a full-time sales and marketing staff, many of whom make on-site visits to customers for the purpose of showing product and soliciting orders for products. We also retain a number of independent sales representatives to sell and promote our products, both domestically and internationally. Together with retailers, we occasionally test the consumer acceptance of new products in selected markets before committing resources to large-scale production.

We publicize and advertise our products in trade and consumer magazines and other publications, market our products at international, national and regional toy and other specialty trade shows, conventions and exhibitions and carry on cooperative advertising programs with toy and mass market retailers and other customers which include the use of print and television ads and in-store displays. We also produce and broadcast television commercials for several of our product lines, if we expect that the resulting increase in our net sales will justify the relatively high cost of television advertising.

Product Development

Each of our product lines has an in-house manager responsible for product development. The in-house manager identifies and evaluates inventor products and concepts and other opportunities to enhance or expand existing product lines or to enter new product categories. In addition, we create proprietary products to fully exploit our concept and character licenses. Although we have the capability to create and develop products from inception to production, we also use third-parties to provide a portion of the sculpting, sample making, illustration and package design required for our products in order to accommodate our increasing product innovations and introductions. Typically, the development process takes from three to nine months from concept to production and shipment to our customers.

We employ a staff of designers for all of our product lines. We occasionally acquire our other product concepts from unaffiliated third parties. If we accept and develop a third party’s concept for new toys, we generally pay a royalty on the sale of the toys developed from this concept, and may, on an individual basis, guarantee a minimum royalty. Royalties payable to inventors and developers generally range from 1% to 5% of the wholesale sales price for each unit of a product sold by us. We believe that utilizing experienced third-party inventors gives us access to a wide range of development talent. We currently work with numerous toy inventors and designers for the development of new products and the enhancement of existing products.

Safety testing of our products is done at the manufacturers’ facilities by quality control personnel employed by us or by independent third-party contractors engaged by us. Safety testing is designed to meet or exceed regulations imposed by federal and state, as well as applicable international governmental authorities, our retail partners, licensors and the Toy Industry Association. We also closely monitor quality assurance procedures for our products for safety purposes. In addition, independent laboratories engaged by some of our larger customers and licensors test certain of our products.

9

Manufacturing and Supplies

Most of our products are currently produced by overseas third-party manufacturers, which we choose on the basis of quality, reliability and price. Consistent with industry practice, the use of third-party manufacturers enables us to avoid incurring fixed manufacturing costs, while maximizing flexibility, capacity and production technology. Substantially all of the manufacturing services performed overseas for us are paid for on open account with the manufacturers. To date, we have not experienced any material delays in the delivery of our products; however, delivery schedules are subject to various factors beyond our control, and any delays in the future could adversely affect our sales. Currently, we have ongoing relationships with over eighty different manufacturers. We believe that alternative sources of supply are available to us although we cannot be assured that we can obtain adequate supplies of manufactured products.

Although we do not conduct the day-to-day manufacturing of our products, we are extensively involved in the design of the product prototype and production tools, dyes and molds for our products and we seek to ensure quality control by actively reviewing the production process and testing the products produced by our manufacturers. We employ quality control inspectors who rotate among our manufacturers’ factories to monitor the production of substantially all of our products.

The principal raw materials used in the production and sale of our toy products are plastics, zinc alloy, plush, printed fabrics, paper products and electronic components, all of which are currently available at reasonable prices from a variety of sources. Although we do not manufacture our products, we own the majority of the tools, dyes and molds used in the manufacturing process, and these are transferable among manufacturers if we choose to employ alternative manufacturers. Tools, dyes and molds represent a substantial portion of our property and equipment with a net book value of $15.7 million in 2016 and $17.0 million in 2017; substantially all of these assets are located in China.

Trademarks and Copyrights

Most of our products are produced and sold under trademarks owned by or licensed to us. We typically register our properties, and seek protection under the trademark, copyright and patent laws of the United States and other countries where our products are produced or sold. These intellectual property rights can be significant assets. Accordingly, while we believe we are sufficiently protected, the loss of some of these rights could have an adverse effect on our business, financial condition and results of operations.

Competition

Competition in the toy industry is intense. Globally, certain of our competitors have greater financial resources, larger sales and marketing and product development departments, stronger name recognition, longer operating histories and benefit from greater economies of scale. These factors, among others, may enable our competitors to market their products at lower prices or on terms more advantageous to customers than those we could offer for our competitive products. Competition often extends to the procurement of entertainment and product licenses, as well as the marketing and distribution of products and the obtaining of adequate shelf space. Competition may result in price reductions, reduced gross margins and loss of market share, any of which could have a material adverse effect on our business, financial condition and results of operations. In each of our product lines we compete against one or both of the toy industry’s two dominant companies, Mattel and Hasbro. In addition, we compete in our Halloween costume lines with Rubies. We also compete with numerous smaller domestic and foreign toy manufacturers, importers and marketers in each of our product categories.

Seasonality and Backlog

In 2017, approximately 65.1% of our net sales were made in the third and fourth quarters. Generally, the first quarter is the period of lowest shipments and sales in our business and in the toy industry and therefore it is also the least profitable quarter due to various fixed costs. Seasonality factors may cause our operating results to fluctuate significantly from quarter to quarter. However, our seasonal products are primarily sold in the spring and summer seasons. Our results of operations may also fluctuate as a result of factors such as the timing of new products (and related expenses) introduced by us or our competitors, the advertising activities of our competitors, delivery schedules set by our customers and the emergence of new market entrants. We believe, however, that the low retail price of most of our products may be less subject to seasonal fluctuations than higher priced toy products.

We ship products in accordance with delivery schedules specified by our customers, who generally request delivery of products within three to six months of the date of their orders for orders shipped FOB China or Hong Kong and within three days for orders shipped domestically. Because customer orders may be canceled at any time, often without penalty, our backlog may not accurately indicate sales for any future period.

10

Government and Industry Regulation

Our products are subject to the provisions of the Consumer Product Safety Act (“CPSA”), the Federal Hazardous Substances Act (“FHSA”), the Flammable Fabrics Act (“FFA”) and the regulations promulgated there under. The CPSA and the FHSA enable the Consumer Products Safety Commission (“CPSC”) to exclude from the market consumer products that fail to comply with applicable product safety regulations or otherwise create a substantial risk of injury, and articles that contain excessive amounts of a banned hazardous substance. The FFA enables the CPSC to regulate and enforce flammability standards for fabrics used in consumer products. The CPSC may also require the repurchase by the manufacturer of articles. Similar laws exist in some states and cities and in various international markets. We maintain a quality control program designed to ensure compliance with all applicable laws.

Employees

As of February 28, 2018, we employed 751 people, all of whom are full-time employees, including three executive officers. We employed 409 people in the United States, 9 people in Canada, 4 people in Mexico, 203 people in Hong Kong, 100 people in China, 20 people in the United Kingdom, 3 people in France and 3 people in Germany. We believe that we have good relationships with our employees. None of our employees are represented by a union.

Environmental Issues

We are subject to legal and financial obligations under environmental, health and safety laws in the United States and in other jurisdictions where we operate. We are not currently aware of any material environmental liabilities associated with any of our operations.

Available Information

We make available free of charge on or through our Internet website, www.jakks.com, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The contents of our website are not incorporated in or deemed to be a part of any such report.

Our Corporate Information

We were formed as a Delaware corporation in 1995. Our principal executive offices are located at 2951 28th Street, Santa Monica, California 90405. Our telephone number is (424) 268-9444 and our Internet Website address is www.jakks.com. The contents of our website are not incorporated in or deemed to be a part of this Annual Report on Form 10-K.

11

From time to time, including in this Annual Report on Form 10-K, we publish forward-looking statements, as disclosed in our Disclosure Regarding Forward-Looking Statements, beginning immediately following the Table of Contents of this Annual Report. We note that a variety of factors could cause our actual results and experience to differ materially from the anticipated results or other expectations expressed or anticipated in our forward-looking statements. The factors listed below are risks and uncertainties that may arise and that may be detailed from time to time in our public announcements and our filings with the Securities and Exchange Commission, such as on Forms 8-K, 10-Q and 10-K. We undertake no obligation to make any revisions to the forward-looking statements contained in this Annual Report on Form 10-K to reflect events or circumstances occurring after the date of the filing of this report.

Our inability to redesign, restyle and extend our existing core products and product lines as consumer preferences evolve, and to develop, introduce and gain customer acceptance of new products and product lines, may materially and adversely impact our business, financial condition and results of operations.

Our business and operating results depend largely upon the appeal of our products. Our continued success in the toy industry will depend upon our ability to redesign, restyle and extend our existing core products and product lines as consumer preferences evolve, and to develop, introduce and gain customer acceptance of new products and product lines. Several trends in recent years have presented challenges for the toy industry, including:

|

|

●

|

the phenomenon of children outgrowing toys at younger ages, particularly in favor of interactive and high technology products;

|

|

|

●

|

increasing use of technology;

|

|

|

●

|

shorter life cycles for individual products; and

|

|

|

●

|

higher consumer expectations for product quality, functionality and value.

|

We cannot assure you that:

|

|

●

|

our current products will continue to be popular with consumers;

|

|

|

●

|

the products that we introduce will achieve any significant degree of market acceptance;

|

|

|

●

|

the life cycles of our products will be sufficient to permit us to recover licensing, design, manufacturing, marketing and other costs associated with those products.

|

|

|

●

|

our inclusion of new technology will result in higher sales or increased profits.

|

Our failure to achieve any or all of the foregoing benchmarks may adversely affect our business, financial condition and results of operations.

The failure of our character-related and theme-related products to become and/or remain popular with children may materially and adversely impact our business, financial condition and results of operations.

The success of many of our character-related and theme-related products depends upon the popularity of characters in movies, television programs, live sporting exhibitions, and other media and events. We cannot assure you that:

|

|

●

|

media associated with our character-related and theme-related product lines will be released at the times we expect or will be successful;

|

|

|

●

|

the success of media associated with our existing character-related and theme-related product lines will result in substantial promotional value to our products;

|

|

|

●

|

we will be successful in renewing licenses upon expiration on terms that are favorable to us; or

|

|

|

●

|

we will be successful in obtaining licenses to produce new character-related and theme-related products in the future.

|

Our failure to achieve any or all of the foregoing benchmarks may cause the infrastructure of our operations to fail, thereby adversely affecting our business, financial condition and results of operations.

12

There are risks associated with our license agreements.

|

|

●

|

Our current licenses require us to pay minimum royalties

|

Sales of products under trademarks or trade or brand names licensed from others account for substantially all of our net sales. Product licenses allow us to capitalize on characters, designs, concepts and inventions owned by others or developed by toy inventors and designers. Our license agreements generally require us to make specified minimum royalty payments, even if we fail to sell a sufficient number of units to cover these amounts. In addition, under certain of our license agreements, if we fail to achieve certain prescribed sales targets, we may be unable to retain or renew these licenses.

|

|

●

|

Some of our licenses are restricted as to use

|

Under the majority of our license agreements, the licensors have the right to review and approve our use of their licensed products, designs or materials before we may make any sales. If a licensor refuses to permit our use of any licensed property in the way we propose, or if their review process is delayed, our development or sale of new products could be impeded.

|

|

●

|

New licenses are difficult and expensive to obtain

|

Our continued success will substantially depend upon our ability to obtain additional licenses. Intense competition exists for desirable licenses in our industry. We cannot assure you that we will be able to secure or renew significant licenses on terms acceptable to us. In addition, as we add licenses, the need to fund additional royalty advances and guaranteed minimum royalty payments may strain our cash resources.

|

|

●

|

A limited number of licensors account for a large portion of our net sales

|

We derive a significant portion of our net sales from a limited number of licensors. If one or more of these licensors were to terminate or fail to renew our license or not grant us new licenses, our business, financial condition and results of operations could be adversely affected.

The toy industry is highly competitive and our inability to compete effectively may materially and adversely impact our business, financial condition and results of operations.

The toy industry is highly competitive. Globally, certain of our competitors have financial and strategic advantages over us, including:

|

|

●

|

greater financial resources;

|

|

|

●

|

larger sales, marketing and product development departments;

|

|

|

●

|

stronger name recognition;

|

|

|

●

|

longer operating histories; and

|

|

|

●

|

greater economies of scale.

|

In addition, the toy industry has no significant barriers to entry. Competition is based primarily upon the ability to design and develop new toys, procure licenses for popular characters and trademarks and successfully market products. Many of our competitors offer similar products or alternatives to our products. Our competitors have obtained and are likely to continue to obtain licenses that overlap our licenses with respect to products, geographic areas and markets. We cannot assure you that we will be able to obtain adequate shelf space in retail stores to support our existing products, expand our products and product lines or continue to compete effectively against current and future competitors.

13

We may not be able to sustain or manage our product line growth, which may prevent us from increasing our net revenues.

Historically, we have experienced growth in our product lines through acquisitions of businesses, products and licenses. This growth in product lines has contributed significantly to our total revenues over the last few years. Even though we had no significant acquisitions since 2012, comparing our future period-to-period operating results may not be meaningful and results of operations from prior periods may not be indicative of future results. We cannot assure you that we will continue to experience growth in, or maintain our present level of, net sales.

Our growth strategy calls for us to continuously develop and diversify our toy business by acquiring other companies, entering into additional license agreements, refining our product lines and expanding into international markets, which will place additional demands upon our management, operational capacity and financial resources and systems. The increased demand upon management may necessitate our recruitment and retention of qualified management personnel. We cannot assure you that we will be able to recruit and retain qualified personnel or expand and manage our operations effectively and profitably. To effectively manage future growth, we must continue to expand our operational, financial and management information systems and to train, motivate and manage our work force. There can be no assurance that our operational, financial and management information systems will be adequate to support our future operations. Failure to expand our operational, financial and management information systems or to train, motivate or manage employees could have a material adverse effect on our business, financial condition and results of operations.

In addition, implementation of our growth strategy is subject to risks beyond our control, including competition, market acceptance of new products, changes in economic conditions, our ability to obtain or renew licenses on commercially reasonable terms, our ability to identify acquisition candidates and conclude acquisitions on acceptable terms, and our ability to finance increased levels of accounts receivable and inventory necessary to support our sales growth, if any. Accordingly, we cannot assure you that our growth strategy will be successful.

If we are unable to acquire and integrate companies and new product lines successfully, we will be unable to implement a significant component of our growth strategy.

Our growth strategy depends, in part, upon our ability to acquire companies and new product lines. Future acquisitions, if any, may succeed only if we can effectively assess characteristics of potential target companies and product lines, such as:

|

|

●

|

attractiveness of products;

|

|

|

●

|

suitability of distribution channels;

|

|

|

●

|

management ability;

|

|

|

●

|

financial condition and results of operations; and

|

|

|

●

|

the degree to which acquired operations can be integrated with our operations.

|

We cannot assure you that we can identify attractive acquisition candidates or negotiate acceptable acquisition terms, and our failure to do so may adversely affect our results of operations and our ability to sustain growth. Our acquisition strategy involves a number of risks, each of which could adversely affect our operating results, including:

|

|

●

|

difficulties in integrating acquired businesses or product lines, assimilating new facilities and personnel and harmonizing diverse business strategies and methods of operation;

|

|

|

●

|

diversion of management attention from operation of our existing business;

|

|

|

●

|

loss of key personnel from acquired companies;

|

|

|

●

|

failure of an acquired business to achieve targeted financial results; and

|

|

|

●

|

Limited capital to finance acquisitions.

|

14

A limited number of customers account for a large portion of our net sales, so that if one or more of our major customers were to experience difficulties in fulfilling their obligations to us, cease doing business with us, significantly reduce the amount of their purchases from us or return substantial amounts of our products, it could have a material adverse effect on our business, financial condition and results of operations.

Our three largest customers accounted for 54.6% of our net sales in 2017. Except for outstanding purchase orders for specific products, we do not have written contracts with or commitments from any of our customers and pursuant to the terms of certain of our vendor agreements, even some purchase orders may be cancelled without penalty up until delivery. A substantial reduction in or termination of orders from any of our largest customers could adversely affect our business, financial condition and results of operations. In addition, pressure by large customers seeking price reductions, financial incentives, and changes in other terms of sale or for us to bear the risks and the cost of carrying inventory could also adversely affect our business, financial condition and results of operations. If one or more of our major customers were to experience difficulties in fulfilling their obligations to us, cease doing business with us, significantly reduce the amount of their purchases from us or return substantial amounts of our products, it could have a material adverse effect on our business, financial condition and results of operations. In addition, the bankruptcy or other lack of success of one or more of our significant retailers could negatively impact our revenues and bad debt expense.

Liquidity problems or bankruptcy of our key customers, including the recent bankruptcy filing by Toys “R” Us, could have a significant adverse effect on our business, financial condition and results of operations.

Our sales to customers are typically made on credit without collateral. There is a risk that key customers will not pay, or that payment may be delayed, because of bankruptcy, concentration of credit availability to such customers, weak retail sales or other factors beyond our control, which could increase our exposure to losses from bad debts. In addition, if key customers were to cease doing business as a result of bankruptcy or significantly reduce the number of stores operated, it could have a significant adverse effect on our business, financial condition, and results of operations.

On September 18, 2017, Toys “R” Us, Inc. (“Toys R Us”), accounting for 11.3% and 12.8% of our net sales for the fiscal years ended December 31, 2017 and 2016, announced that certain of its U.S. subsidiaries and its Canadian subsidiary voluntarily filed for relief under Chapter 11 of the Bankruptcy Code in the U.S. and that its Canadian subsidiary also began parallel proceedings under the Companies’ Creditors Arrangement Act (“CCAA”) in Canada.

On March 15, 2018, Toys R Us filed a motion to conduct an orderly wind down of its operations in the U.S. and commence store closing sales at all 735 US stores. Our worldwide Toys R Us accounts receivable balance as of March 15, 2018 is $35.9 million (unaudited). Due to the evolving nature of this matter, it is too early to assess the impact on the collectibility of this receivable and on future revenues we generate from this customer relationship (See Notes 3 and 22).

We depend upon our Chief Executive Officer and any loss or interruption of his services could adversely affect our business, financial condition and results of operations.

Our success has been largely dependent upon the experience and continued services of Stephen G. Berman, our President and Chief Executive Officer. We cannot assure you that we would be able to find an appropriate replacement for Mr. Berman should the need arise, and any loss or interruption of the services of Mr. Berman could adversely affect our business, financial condition and results of operations.

We depend upon third-party manufacturers, and if our relationship with any of them is harmed or if they independently encounter difficulties in their manufacturing processes, we could experience product defects, production delays, cost overruns or the inability to fulfill orders on a timely basis, any of which could adversely affect our business, financial condition and results of operations.

We depend upon many third-party manufacturers who develop, provide and use the tools, dyes and molds that we generally own to manufacture our products. However, we have limited control over the manufacturing processes themselves. As a result, any difficulties encountered by the third-party manufacturers that result in product defects, production delays, cost overruns or the inability to fulfill orders on a timely basis could adversely affect our business, financial condition and results of operations.

We do not have long-term contracts with our third-party manufacturers. Although we believe we could secure other third-party manufacturers to produce our products, our operations would be adversely affected if we lost our relationship with any of our current suppliers or if our current suppliers’ operations or sea or air transportation with our overseas manufacturers were disrupted or terminated even for a relatively short period of time. Our tools, dyes and molds are located at the facilities of our third-party manufacturers.

Although we do not purchase the raw materials used to manufacture our products, we are potentially subject to variations in the prices we pay our third-party manufacturers for products, depending upon what they pay for their raw materials.

We have substantial sales and manufacturing operations outside of the United States, subjecting us to risks common to international operations.

We sell products and operate facilities in numerous countries outside the United States. Sales to our international customers comprised approximately 21.9% of our net sales for the year ended December 31, 2017 and approximately 23.0% of our net sales for the year ended December 31, 2016. We expect our sales to international customers to account for a greater portion of our revenues in future fiscal periods. Additionally, we utilize third-party manufacturers, located principally in China, and are subject to the risks normally associated with international operations, including:

|

|

●

|

currency conversion risks and currency fluctuations;

|

|

|

●

|

limitations, including taxes, on the repatriation of earnings;

|

|

|

●

|

political instability, civil unrest and economic instability;

|

15

|

|

●

|

greater difficulty enforcing intellectual property rights and weaker laws protecting such rights;

|

|

|

●

|

complications in complying with laws in varying jurisdictions and changes in governmental policies;

|

|

|

●

|

greater difficulty and expenses associated with recovering from natural disasters, such as earthquakes, hurricanes and floods;

|

|

|

●

|

transportation delays and interruption;

|

|

|

●

|

work stoppages;

|

|

|

●

|

the potential imposition of tariffs; and

|

|

|

●

|

the pricing of intercompany transactions may be challenged by taxing authorities in both foreign jurisdictions and the United States, with potential increases in income taxes.

|

Our reliance upon external sources of manufacturing can be shifted, over a period of time, to alternative sources of supply, should such changes be necessary. However, if we were prevented from obtaining products or components for a material portion of our product line due to medical, political, labor or other factors beyond our control, our operations would be disrupted while alternative sources of products were secured. Also, the imposition of trade sanctions by the United States against a class of products imported by us from, or the loss of “normal trade relations” status by, China could significantly increase our cost of products imported from that nation. Because of the importance of international sales and international sourcing of manufacturing to our business, our financial condition and results of operations could be significantly and adversely affected if any of the risks described above were to occur.

Our business is subject to extensive government regulation and any violation by us of such regulations could result in product liability claims, loss of sales, diversion of resources, damage to our reputation, increased warranty costs or removal of our products from the market, and we cannot assure you that our product liability insurance for the foregoing will be sufficient.

Our business is subject to various laws, including the Federal Hazardous Substances Act, the Consumer Product Safety Act, the Flammable Fabrics Act and the rules and regulations promulgated under these acts. These statutes are administered by the CPSC, which has the authority to remove from the market products that are found to be defective and present a substantial hazard or risk of serious injury or death. The CPSC can require a manufacturer to recall, repair or replace these products under certain circumstances. We cannot assure you that defects in our products will not be alleged or found. Any such allegations or findings could result in:

|

|

●

|

product liability claims;

|

|

|

●

|

loss of sales;

|

|

|

●

|

diversion of resources;

|

|

|

●

|

damage to our reputation;

|

|

|

●

|

increased warranty and insurance costs; and

|

|

|

●

|

removal of our products from the market.

|

Any of these results may adversely affect our business, financial condition and results of operations. There can be no assurance that our product liability insurance will be sufficient to avoid or limit our loss in the event of an adverse outcome of any product liability claim.

We depend upon our proprietary rights and our inability to safeguard and maintain the same, or claims of third parties that we have violated their intellectual property rights, could have a material adverse effect on our business, financial condition and results of operations.

We rely upon trademark, copyright and trade secret protection, nondisclosure agreements and licensing arrangements to establish, protect and enforce our proprietary rights in our products. The laws of certain foreign countries may not protect intellectual property rights to the same extent or in the same manner as the laws of the United States. We cannot assure you that we or our licensors will be able to successfully safeguard and maintain our proprietary rights. Further, certain parties have commenced legal proceedings or made claims against us based upon our alleged patent infringement, misappropriation of trade secrets or other violations of their intellectual property rights. We cannot assure you that other parties will not assert intellectual property claims against us in the future. These claims could divert our attention from operating our business or result in unanticipated legal and other costs, which could adversely affect our business, financial condition and results of operations.

16

Market conditions and other third-party conduct could negatively impact our margins and implementation of other business initiatives.

Economic conditions, such as decreased consumer confidence, may adversely impact our margins. In addition, general economic conditions were significantly and negatively affected by the September 11th terrorist attacks and could be similarly affected by any future attacks. Such a weakened economic and business climate, as well as consumer uncertainty created by such a climate, could adversely affect our sales and profitability. Other conditions, such as the unavailability of electronics components, may impede our ability to manufacture, source and ship new and continuing products on a timely basis. Significant and sustained increases in the price of oil could adversely impact the cost of the raw materials used in the manufacture of our products, such as plastic.

We may not have the funds necessary to purchase our outstanding convertible senior notes upon a fundamental change or other purchase date, as required by the indenture governing the notes.

In June 2014 we sold an aggregate of $115.0 million principal amount of 4.875% convertible senior notes due on June 1, 2020, of which $113.0 million are currently outstanding (the “2020 Notes”). In July 2013, we sold an aggregate of $100.0 million principal amount of 4.25% convertible senior notes due on August 1, 2018, of which $21.2 million are currently outstanding (the “2018 Notes”) and $21.5 million were extended to November 1, 2020 (the “3.25% 2020 Notes” and collectively with the 2018 Notes and 2020 Notes, the “Notes”). Holders of the Notes may require us to repurchase for cash all or some of their notes upon the occurrence of a fundamental change (as defined in the Notes). Holders of the Notes may convert their notes upon the occurrence of specified events. Upon conversion, the Notes will be settled in shares of our common stock and/or in cash. Restrictions on borrowings under or loss of our credit facility could have a material adverse effect on our financial condition including an adverse impact on our ability to pay the Notes when due.

Restrictions under or the loss of availability under our credit facility could adversely impact our financial condition and our ability to pay our convertible senior notes when due.

In March 2014, we obtained a $75.0 million revolving line of credit. Any amounts borrowed under the revolving credit line are our senior secured obligations. All outstanding borrowings under the revolving credit line are accelerated and become immediately due and payable (and the revolving credit line terminates) in the event of a default which includes, among other things, failure to comply with financial ratio covenants or breach of representations contained in the credit line documents, defaults under other loans or obligations, involvement in bankruptcy proceedings, an occurrence of a change of control or an event constituting a material adverse effect on us (as such terms are defined in the credit line documents). We are also subject to negative covenants which, during the life of the credit line, prohibit and/or limit us from, among other things, incurring certain types of other debt, acquiring other companies, making certain expenditures or investments, changing the character of our business, and certain changes to our executive officers.

We have a valuation allowance on the deferred taxes on our books since their future realization is uncertain.

Deferred tax assets are realized by prior and future taxable income of appropriate character. Current accounting standards require that a valuation allowance be recorded if it is not likely that sufficient taxable income of appropriate character will be generated to realize the deferred tax assets. We currently believe that based on the available information, it is more likely than not that our deferred tax assets will not be realized, and accordingly we have recorded a valuation allowance against our US federal and state deferred tax assets. Our net operating losses and tax credit carry-forwards can expire if unused, and their utilization could be substantially limited in the event of an "ownership change," as defined in Section 382 of the Internal Revenue Code of 1986, as amended, or the Internal Revenue Code.

An adverse decision in litigation in which we have been named as a defendant could have a material adverse effect on our financial condition and results of operations.

We are defendants in a class action described herein and under “Legal Proceedings” in our periodic reports filed pursuant to the Securities Exchange Act of 1934 (see “Legal Proceedings”). No assurances can be given that the results of these litigation matters will be favorable to us or that an adverse decision in such litigation would not have a material adverse impact on our financial condition and results of operations.

We rely extensively on information technology in our operations, and any material failure, inadequacy, interruption, or security breach of that technology could have a material adverse impact on our business.

We rely extensively on information technology systems across our operations, including for management of our supply chain, sale and delivery of our products and services, reporting our results of operations, collection and storage of consumer data, personal data of customers, employees and other stakeholders, and various other processes and transactions. Many of these systems are managed by third-party service providers. We use third-party technology and systems for a variety of reasons, including, without limitation, encryption and authentication technology, employee email, content delivery to customers, back-office support, and other functions. A small and growing volume of our consumer products and services are web-based, and some are offered in conjunction with business partners or such third-party service providers. We, our business partners and third-party service providers collect, process, store and transmit consumer data, including personal information, in connection with those products and services. Failure to follow applicable regulations related to those activities, or to prevent or mitigate data loss or other security breaches, including breaches of our business partners’ technology and systems could expose us or our customers to a risk of loss or misuse of such information, which could adversely affect our operating results, result in regulatory enforcement, other litigation and could be a potential liability for us, and otherwise harm our business. Our ability to effectively manage our business and coordinate the production, distribution, and sale of our products and services depends significantly on the reliability and capacity of these systems and third-party service providers. Although we have developed systems and processes that are designed to protect customer information and prevent data loss and other security breaches, including systems and processes designed to reduce the impact of a security breach at a third party provider, such measures cannot provide absolute security. We have exposure to similar security risks faced by other large companies that have data stored on their information technology systems. To our knowledge, we have not experienced any material breach of our cybersecurity systems. If we or our third-party service providers systems fail to operate effectively or are damaged, destroyed, or shut down, or there are problems with transitioning to upgraded or replacement systems, or there are security breaches in these systems, any of the aforementioned could occur as a result of natural disasters, software or equipment failures, telecommunications failures, loss or theft of equipment, acts of terrorism, circumvention of security systems, or other cyber-attacks, including denial-of-service attacks, we could experience delays or decreases in product sales, and reduced efficiency of our operations. Additionally, any of these events could lead to violations of privacy laws, loss of customers, or loss, misappropriation or corruption of confidential information, trade secrets or data, which could expose us to potential litigation, regulatory actions, sanctions or other statutory penalties, any or all of which could adversely affect our business, and cause it to incur significant losses and remediation costs.

17

The following is a listing of the principal leased offices maintained by us as of February 28, 2018:

|

Property

|

Location

|

Approximate

Square Feet

|

Lease Expiration

Date

|

|||

|

US and Canada *

|

|

|

||||

|

Distribution Center

|

City of Industry, California

|

800,000

|

April 30, 2023

|

|||

|

Distribution Center

|

Hickory, North Carolina

|

139,300

|

August 31, 2018

|

|||

|

Sales Office/Showroom

|

Bentonville, Arkansas

|

9,000

|

September 30, 2019

|

|||

|

Disguise Office

|

Poway, California

|

24,200

|

March 31, 2021

|

|||

|

Sales Office

|

Hoffman Estates, Illinois

|

2,102

|

December 31, 2018

|

|||

|

Corporate Office/Showroom

|

Santa Monica, California

|

65,858

|

January 31, 2024

|

|||

|

Showroom

|

Glendale, California

|

5,830

|

January 31, 2020

|

|||

|

Distribution Center

|

Brampton, Ontario, Canada

|

105,700

|

December 31, 2019

|

|||

|

International *

|

|

|

||||

|

Europe Office

|

Berkshire, United Kingdom

|

4,746

|

January 19, 2027

|

|||

|

Hong Kong Headquarters

|

Kowloon, Hong Kong

|

41,130

|

June 30, 2019

|

|||

|

Production Inspection and Testing Office

|

Shenzhen, China

|

5,417

|

May 14, 2019

|

|||

|

Production Inspection and

Testing Lab

|

Kowloon, Hong Kong

|

34,400

|

October 31, 2018

|

|||

*The Halloween segment is included in the properties listed above.

18

We are a party to, and certain of our property is the subject of, various pending claims and legal proceedings that routinely arise in the ordinary course of our business, but we do not believe that any of these claims or proceedings will have a material effect on our business, financial condition or results of operations.

19

Not applicable.

20

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

Our common stock is traded on the Nasdaq Global Select exchange under the symbol “JAKK.” The following table sets forth, for the periods indicated, the range of high and low sales prices for our common stock on this exchange.

|

|

Price Range of

Common Stock

|

|||||||

|

|

High

|

Low

|

||||||

|

2016:

|

||||||||

|

First quarter

|

$

|

7.97

|

$

|

6.17

|

||||

|

Second quarter

|

8.02

|

6.94

|

||||||

|

Third quarter

|

9.75

|

7.57

|

||||||

|

Fourth quarter

|

9.15

|

4.63

|

||||||

|

2017:

|

||||||||

|

First quarter

|

5.85

|

4.78

|

||||||

|

Second quarter

|

5.55

|

3.80

|

||||||

|

Third quarter

|

4.20

|

2.68

|

||||||

|

Fourth quarter

|

3.55

|

2.20

|

||||||

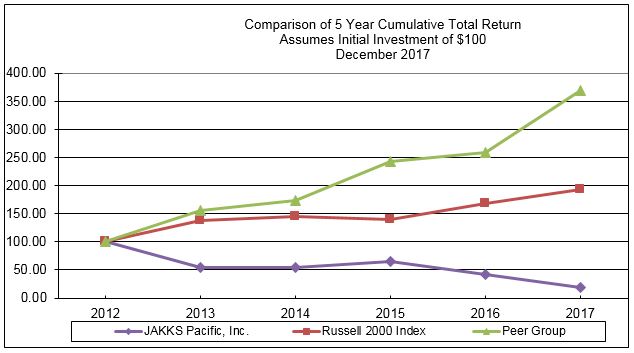

Performance Graph

The graph and tables below display the relative performance of our common stock, the Russell 2000 Price Index (the “Russell 2000”) and a peer group index, by comparing the cumulative total stockholder return (which assumes reinvestment of dividends, if any) on an assumed $100 investment on December 31, 2012 in our common stock, the Russell 2000 and the peer group index over the period from January 1, 2013 to December 31, 2017.

In accordance with recently enacted regulations implemented by the Securities and Exchange Commission, we retained the services of an expert compensation consultant. In the performance of its services, such consultant used a peer group index for its analysis of our compensation policies. We believe that these companies represent a cross-section of publicly-traded companies with product lines and businesses similar to our own throughout the comparison period and, accordingly, we are using the same peer group for purposes of the performance graph. EMak Worldwide Inc. and THQ Inc. were excluded from the performance peer group in 2014, Kid Brands, Inc. was excluded in 2015 and Leapfrog Enterprises, Inc. was excluded in 2016. Deckers Outdoor Corporation was added in 2016 and our peer group index now is comprised of the following companies: Activision Blizzard, Inc., Deckers Outdoor Corporation, Electronic Arts, Inc., Hasbro, Inc., Mattel, Inc. and Take-Two Interactive, Inc.

21

The historical performance data presented below may not be indicative of the future performance of our common stock, any reference index or any component company in a reference index.

Annual Return Percentage

|

|

December 31,

2013

|

December 31,

2014

|

December 31,

2015

|

December 31,

2016

|

December 31,

2017

|

|||||||||||||||

|

JAKKS Pacific

|

(45.6

|

)%

|

1.2

|

%

|

17.1

|

%

|

(35.3

|

)%

|

(54.4

|

)%

|

||||||||||

|

Peer Group

|

55.6

|

11.7

|

39.4

|

7.0

|

42.8

|

|||||||||||||||

|

Russell 2000

|

38.8

|

4.9

|

(4.4

|

)

|

21.3

|

14.7

|

||||||||||||||

Indexed Returns

|

|

January 1,

2013

|

December 31,

2013

|

December 31,

2014

|

December 31,

2015

|

December 31,

2016

|

December 31,

2017

|

||||||||||||||||||

|

JAKKS Pacific

|

$

|

100.0

|

$

|

54.4

|

$

|

55.1

|

$

|

64.4

|

$

|

41.7

|

$

|

19.0

|

||||||||||||

|

Peer Group

|

100.0

|

155.6

|

173.8

|

242.2

|

259.2

|

370.6

|

||||||||||||||||||

|

Russell 2000

|

100.0

|

138.8

|

145.6

|

139.2

|

168.9

|

193.6

|

||||||||||||||||||

Security Holders

To the best of our knowledge, as of March 6, 2018, there were 109 holders of record of our common stock. We believe there are numerous beneficial owners of our common stock whose shares are held in “street name.”

Dividends

The payment of dividends on common stock is at the discretion of the Board of Directors and is subject to customary limitations. We currently intend to retain our future earnings, if any, to finance the growth and development of our business and/or buy back in the market some of our common stock and/or retire some of our outstanding convertible senior notes.

22

Equity Compensation Plan Information

The table below sets forth the following information as of the year ended December 31, 2017 for (i) all compensation plans previously approved by our stockholders and (ii) all compensation plans not previously approved by our stockholders, if any:

(a) the number of securities to be issued upon the exercise of outstanding options, warrants and rights;

(b) the weighted-average exercise price of such outstanding options, warrants and rights; and