Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - DAVEY TREE EXPERT CO | dt2017q410kex322.htm |

| EX-32.1 - EXHIBIT 32.1 - DAVEY TREE EXPERT CO | dt2017q410kex321.htm |

| EX-31.2 - EXHIBIT 31.2 - DAVEY TREE EXPERT CO | dt2017q410kex312.htm |

| EX-31.1 - EXHIBIT 31.1 - DAVEY TREE EXPERT CO | dt2017q410kex311.htm |

| EX-23 - EXHIBIT 23 - DAVEY TREE EXPERT CO | dt2017q410kex23.htm |

| EX-21 - EXHIBIT 21 - DAVEY TREE EXPERT CO | dt2017q410kex21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______________ to ______________

Commission file number 000-11917

THE DAVEY TREE EXPERT COMPANY

(Exact name of registrant as specified in its charter)

Ohio | 34-0176110 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

1500 North Mantua Street

P.O. Box 5193

Kent, Ohio 44240

(Address of principal executive offices) (Zip code)

(330) 673-9511

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common Shares, $1.00 par value

Indicate by check mark if the registrant is a well-known seasoned issuer (as defined in Rule 405 of the Securities Act). Yes ¨ No x | ||||||||

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x | ||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨ | ||||||||

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T(§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨ | ||||||||

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨ | ||||||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. | ||||||||

(Check one): | ¨ | Large Accelerated Filer | x | Accelerated Filer | ¨ | Emerging Growth Company | ||

¨ | Non-Accelerated Filer (Do not check if a smaller reporting company) | ¨ | Smaller Reporting Company | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ¨ | ||||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x | ||||||||

There were 24,227,668 Common Shares outstanding as of March 9, 2018. The aggregate market value of the Common Shares held by nonaffiliates of the registrant as of July 1, 2017 was $390,025,072. For purposes of this calculation, it is assumed that the registrant's affiliates include the registrant's Board of Directors and its executive officers.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive Proxy Statement for the 2018 Annual Meeting of Shareholders, to be held on May 15, 2018, are incorporated by reference into Part III (to be filed within 120 calendar days of the registrant’s fiscal year end).

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report on Form 10-K contains forward-looking statements (within the meaning of the Private Securities Litigation Reform Act of 1995) in "Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations," "Item 7A - Quantitative and Qualitative Disclosures About Market Risk," and elsewhere. These statements relate to future events or our future financial performance. In some cases, forward-looking statements may be identified by terminology such as "may," "will," "should," "expects," "plans," "anticipates," "believes," "estimates," "predicts," "potential," "continue" or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors that may cause our or our industry's actual results, levels of activity, performance or achievements to differ materially from what is expressed or implied in these forward-looking statements. Some important factors that could cause actual results to differ materially from those in the forward-looking statements include:

▪ | Our business, other than tree services to utility customers, is highly seasonal and weather dependent. |

▪ | Various economic factors may adversely impact our customers’ spending and pricing for our services, and impede our collection of accounts receivable. |

▪ | Significant customers, particularly utilities, may experience financial difficulties, resulting in payment delays or delinquencies. |

▪ | The seasonal nature of our business and changes in general and local economic conditions, among other factors, may cause our quarterly results to fluctuate, and our prior performance is not necessarily indicative of future results. |

▪ | The uncertainties in the credit and financial markets may limit our access to capital. |

▪ | Significant increases in fuel prices for extended periods of time will increase our operating expenses. |

▪ | Fluctuations in foreign currency exchange rates may have a material adverse impact on our operating results. |

▪ | We have significant contracts with our utility, commercial and government customers that include liability risk exposure as part of those contracts. Consequently, we have substantial excess-umbrella liability insurance, and increases in the cost of obtaining adequate insurance, or the inadequacy of our self-insurance accruals or insurance coverages, could negatively impact our liquidity and financial condition. |

▪ | Because no public market exists for our common shares, the ability of shareholders to sell their common shares is limited. |

▪ | Significant increases in health care costs could negatively impact our results of operations or financial position. |

▪ | We are subject to intense competition. |

▪ | Our failure to comply with environmental laws could result in significant liabilities, fines and/or penalties. |

▪ | The impact of regulations initiated as a response to possible changing climate conditions could have a negative effect on our results of operations or our financial condition. |

▪ | We may encounter difficulties obtaining surety bonds or letters of credit necessary to support our operations. |

▪ | We are dependent, in part, on our reputation of quality, integrity and performance. If our reputation is damaged, we may be adversely affected. |

▪ | We may be unable to attract and retain a sufficient number of qualified employees for our field operations, and we may be unable to attract and retain qualified management personnel. |

▪ | Our facilities could be damaged or our operations could be disrupted, or our customers or vendors may be adversely affected, by events such as natural disasters, pandemics, terrorist attacks or other external events. |

▪ | A disruption in our information technology systems, including a disruption related to cybersecurity, could adversely affect our financial performance. |

▪ | We may be subject to third-party and governmental regulatory claims and litigation that may have an adverse effect on us. |

▪ | We may misjudge a competitive bid and be contractually bound to an unprofitable contract. |

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. We are under no duty to update any of the forward-looking statements after the date of this annual report on Form 10-K to conform these statements to actual future results.

Page 1

THE DAVEY TREE EXPERT COMPANY FORM 10-K For the Year Ended December 31, 2017 TABLE OF CONTENTS | |

Page | |

PART I | |

PART II | |

PART III | |

PART IV | |

“We,” “Us,” “Our,” “Davey” and “Davey Tree,” unless the context otherwise requires, means The Davey Tree Expert Company and its subsidiaries.

Page 2

PART I

Item 1. Business.

General

The Davey Tree Expert Company, which was founded in 1880 and incorporated in Ohio in 1909, and its subsidiaries ("we" or "us") provides a wide range of arboricultural, horticultural, environmental and consulting services to our customers throughout the United States and Canada. We have two reportable operating segments organized by type or class of customer: Residential and Commercial, and Utility.

Our Residential and Commercial segment provides services to our residential and commercial customers including: the treatment, preservation, maintenance, removal and planting of trees, shrubs and other plant life; the practice of landscaping, grounds maintenance, tree surgery, tree feeding and tree spraying; the application of fertilizer, herbicides and insecticides; and, natural resource management and consulting, forestry research and development, and environmental planning.

Our Utility segment is principally engaged in providing services to our utility customers--investor-owned, municipal utilities, and rural electric cooperatives--including: the practice of line-clearing and vegetation management around power lines, rights-of-way and chemical brush control; and, natural resource management and consulting, forestry research and development and environmental planning.

We also maintain research, technical support and laboratory diagnostic facilities.

Competition and Customers

Our Residential and Commercial segment is one of the largest national tree care organizations in the United States, and competes with other national and local firms with respect to its services. On a national level, our competition is primarily landscape construction and maintenance companies as well as residential and commercial lawn care companies. At a local and regional level, our competition comes mainly from small, local companies which are engaged primarily in tree care and lawn services. Our Utility segment is the second largest organization in the industry in the United States, and competes principally with one major national competitor, The Asplundh Tree Expert Co., as well as several smaller regional firms.

Principal methods of competition in both operating segments are customer service, marketing, image, performance and reputation. Our program to meet our competition stresses the necessity for our employees to have and project to customers a thorough knowledge of all horticultural services provided, and utilization of modern, well-maintained equipment. Pricing is not always a critical factor in a customer's decision with respect to our Residential and Commercial segment; however, pricing is generally the principal method of competition for our Utility segment, although in most instances consideration is given to reputation and past production performance.

We provide a wide range of horticultural services to private companies, public utilities, local, state and federal agencies, and a variety of industrial, commercial and residential customers. During 2017, we had revenues of approximately $104 million, or approximately 11% of total revenues, from Pacific Gas & Electric Company ("PG&E"), our largest customers.

Regulation and Environment

Our facilities and operations, in common with those of the industry generally, are subject to governmental regulations designed to protect the environment. This is particularly important with respect to our services regarding insect and disease control, because these services involve, to a considerable degree, the blending and application of spray materials, which require formal licensing in most areas. Constant changes in environmental conditions, environmental awareness, technology and social attitudes make it necessary for us to maintain a high degree of awareness of the impact such changes have on the market for our services. We believe that we comply in all material respects with existing federal, state and local laws regulating the use of materials in our spraying operations as well as the other aspects of our business that are subject to any such regulation.

Marketing

We solicit business from residential customers principally through referrals, direct mail programs and to a lesser extent through the placement of advertisements in national magazines and trade journals, local newspapers and "yellow pages" telephone directories. We also employ online marketing and lead generation strategies, including email marketing campaigns,

Page 3

search engine optimization, search engine marketing, and social media communication. Business from utility and commercial customers is obtained principally through negotiated contracts and competitive bidding. We carry out all of our sales and services through our employees. We generally do not use agents, and do not franchise our name or business.

Seasonality

Our business is seasonal, primarily due to fluctuations in horticultural services provided to Residential and Commercial customers and to a lesser extent by budget constraints imposed on our Utility customers. Because of this seasonality, we have historically incurred losses in the first quarter, while sales and earnings are generally highest in the second and third quarters of the calendar year. Consequently, this has created heavy demands for additional working capital at various times throughout the year. We borrow primarily against bank commitments in the form of a revolving credit facility to provide the necessary funds for our operations. You can find more information about our bank commitments in “Liquidity and Capital Resources” on pages 23-26 of this report under “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Other Factors

Due to rapid changes in equipment technology and intensity of use, we must constantly update our equipment and processes to ensure that we provide competitive services to our customers and continue our compliance with the Occupational Safety and Health Act.

We own several trademarks including "Davey," "Davey and Design," "Arbor Green Pro," "Arbor Green," and "Davey Resource Group." Through substantial advertising and use, we believe that these trademarks have become of value in the identification and acceptance of our products and services.

Employees

We employed approximately 8,200 employees at December 31, 2017. However, employment levels fluctuate due to seasonal factors affecting our business. We consider our employee relations to be good.

Domestic and Foreign Operations

We sell our services to customers in the United States and Canada.

We do not consider the risks attendant to our business with foreign customers, other than currency exchange risks, to be materially different from those attendant to our business with domestic customers.

Financial Information About Segments and Geographic Areas

Certain financial information regarding our operations by segment and geographic area is contained in Note S to our consolidated financial statements, which are included in Part II, Item 8 of this report.

Access to Company Information

Davey Tree’s internet address is http://www.davey.com. Through our internet website, by hyperlink to the Securities and Exchange Commission (“SEC”) website (http://www.sec.gov), we make available, free of charge, our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports. Availability of the reports occurs contemporaneously with the electronic posting to the SEC’s website as the reports are electronically filed with or furnished to the SEC. The information on our website is not a part of this Annual Report on Form 10-K.

The following documents are also made available on our website and a copy will be mailed, without charge, upon request to our Corporate Secretary:

▪ | Code of Ethics |

▪ | Code of Ethics for Financial Matters |

Page 4

Item 1A. Risk Factors.

The factors described below represent the principal risks we face. Except as otherwise indicated, these factors may or may not occur and we are not in a position to express a view on the likelihood of any such factor occurring. Other factors may exist that we do not consider to be significant based on information that is currently available or that we are not currently able to anticipate.

Our business is highly seasonal and weather dependent.

Our business, other than tree services to utility customers, is highly seasonal and weather dependent, primarily due to fluctuations in horticultural services provided to Residential and Commercial customers. We have historically incurred losses in the first quarter, while revenue and operating income are generally highest in the second and third quarters of the calendar year. Inclement weather, such as uncharacteristically low or high (drought) temperatures, in the second and third quarters could dampen the demand for our horticultural services, resulting in reduced revenues that would have an adverse effect on our results of operations.

Economic conditions may adversely impact our customers’ future spending as well as pricing and payment for our services, thus negatively impacting our operations and growth.

Various economic factors may adversely impact the demand for our services and potentially result in depressed prices for our services and the delay or cancellation of projects. That may make it difficult to estimate our customers' requirements for our services and, therefore, add uncertainty to customer demand. Various economic factors and customers' confidence in future economic conditions may cause a reduction in our customers' spending for our services and may also impact the ability of our customers to pay amounts owed, which could reduce our cash flow and adversely impact our debt or equity financing. These events could have a material adverse effect on our operations and our ability to grow at historical levels.

Financial difficulties or the bankruptcy of one or more of our major customers could adversely affect our results.

Our ability to collect our accounts receivable and future sales depends, in part, on the financial strength of our customers. We grant credit, generally without collateral, to our customers. Consequently, we are subject to credit risk related to changes in business and economic factors throughout the United States and Canada. In the event customers experience financial difficulty, and particularly if bankruptcy results, our profitability may be adversely impacted by our failure to collect our accounts receivable in excess of our estimated allowance for uncollectible accounts. Additionally, our future revenues could be reduced by the loss of a customer due to bankruptcy. Our failure to collect accounts receivable and/or the loss of one or more major customers could have an adverse effect on our net income and financial condition.

Our business is dependent upon service to our utility customers and we may be affected by developments in the utility industry.

We derive approximately 51% of our total revenues from our Utility segment. Significant adverse developments in the utility industry generally, or specifically for our major utility customers, could result in pressure to reduce costs by utility industry service providers (such as us), delays in payments of our accounts receivable, or increases in uncollectible accounts receivable, among other things. As a result, such developments could have an adverse effect on our results of operations.

Our quarterly results may fluctuate.

We have experienced and expect to continue to experience quarterly variations in revenues and operating income as a result of many factors, including:

▪ | the seasonality of our business; |

▪ | the timing and volume of customers' projects; |

▪ | budgetary spending patterns of customers; |

▪ | the commencement or termination of service agreements; |

▪ | costs incurred to support growth internally or through acquisitions; |

▪ | changes in our mix of customers, contracts and business activities; |

▪ | fluctuations in insurance expense due to changes in claims experience and actuarial assumptions; and |

▪ | general and local economic conditions. |

Page 5

Accordingly, our operating results in any particular quarter may not be indicative of the results that you can expect for any other quarter or for the entire year.

We may not have access to capital in the future due to uncertainties in the financial and credit markets.

We may need new or additional financing in the future to conduct our operations, expand our business or refinance existing indebtedness. Future changes in the general economic conditions and/or financial markets in the United States or globally could affect adversely our ability to raise capital on favorable terms or at all. From time-to-time we have relied, and may also rely in the future, on access to financial markets as a source of liquidity for working capital requirements, acquisitions and general corporate purposes. Our access to funds under our revolving credit facility is dependent on the ability of the financial institutions that are parties to the facility to meet their funding commitments. Those financial institutions may not be able to meet their funding commitments if they experience shortages of capital and liquidity or if they experience excessive volumes of borrowing requests within a short period of time. Economic disruptions and any resulting limitations on future funding, including any restrictions on access to funds under our revolving credit facility, could have a material adverse effect on us.

We are subject to the risk of changes in fuel costs.

The cost of fuel is a major operating expense of our business. Significant increases in fuel prices for extended periods of time will cause our operating expenses to fluctuate. An increase in cost with partial or no corresponding compensation from customers would lead to lower margins that would have an adverse effect on our results of operations.

We are subject to the effect of foreign currency exchange rate fluctuations, which may have a material adverse impact on us.

We are exposed to foreign currency exchange rate risk resulting from our operations in Canada, where we provide a comprehensive range of horticultural services. Fluctuations in foreign currency exchange rates may make our services more expensive for others to purchase or increase our operating costs, affecting our competitiveness and our profitability. Our financial results could be affected by factors such as changes in the foreign currency exchange rate or differing economic conditions in the Canadian markets as compared with the markets for our services in the United States. Our earnings are affected by translation exposures from currency fluctuations in the value of the U.S. dollar as compared to the Canadian dollar.

Revenues from customers in Canada are subject to foreign currency exchange. Thus, certain revenues and expenses have been, and are expected to be, subject to the effect of foreign currency fluctuations, and these fluctuations may have a material adverse impact on our operating results, asset values and could reduce shareholders’ equity. In addition, if we expand our Canadian operations, exposures to gains and losses on foreign currency transactions may increase.

We could be negatively impacted if our self-insurance accruals or our insurance coverages prove to be inadequate.

We are generally self-insured for losses and liabilities related to workers' compensation, vehicle liability and general liability claims (including any wildfire-related claims, up to certain retained coverage limits). A liability for unpaid claims and associated expenses, including incurred but not reported losses, is actuarially determined and reflected in our consolidated balance sheet as an accrued liability. The determination of such claims and expenses, and the extent of the need for accrued liabilities, are continually reviewed and updated. If we were to experience insurance claims or costs above our estimates and were unable to offset such increases with earnings, our business could be adversely affected. Also, where we self-insure, a deterioration in claims management, whether by our management or by a third-party claims administrator, could lead to delays in settling claims, thereby increasing claim costs, particularly as it relates to workers’ compensation. In addition, catastrophic uninsured claims filed against us or the inability of our insurance carriers to pay otherwise-insured claims would have an adverse effect on our financial condition.

Furthermore, many customers, particularly utilities, prefer to do business with contractors with significant financial resources, who can provide substantial insurance coverage. Should we be unable to renew our excess liability insurance and other commercial insurance policies at competitive rates, this loss would have an adverse effect on our financial condition and results of operations.

Increases in our health insurance costs and uncertainty about federal health care policies could adversely affect our results of operations and cash flows.

The costs of employee health care insurance have been increasing in recent years due to rising health care costs, legislative changes, and general economic conditions. We cannot predict what other health care programs and regulations will ultimately

Page 6

be implemented at the federal or state level or the effect of any future legislation or regulations on our business, results of operations and cash flows. In addition, we cannot predict when and if Congress will repeal and/or replace certain health care programs and regulations at the federal level and the impact that such changes would have on our business. A continued increase in health care costs or additional costs incurred as a result of the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010 or other future health care reform laws imposed by Congress or state legislatures could have a negative impact on our financial position, results of operations and cash flows.

The unavailability or cancellation of third-party insurance coverage may have a material adverse effect on our financial condition and results of operations as well as disrupt our operations.

Any of our existing excess insurance coverage may not be renewed upon the expiration of the coverage period or future coverage may not be available at competitive rates for the required limits. In addition, our third-party insurers could fail, suddenly cancel our coverage or otherwise be unable to provide us with adequate insurance coverage. If any of these events occur, they may have a material adverse effect on our financial condition and results of operations as well as disrupt our operations. For example, we have operations in California, which has an environment prone to wildfires. Should our third-party insurers determine to exclude coverage for wildfires in the future, we could be exposed to significant liabilities, having a material adverse effect on our financial condition and results of operations and potentially disrupting our California operations.

Because no public market exists for our common shares, your ability to sell your common shares may be limited.

Our common shares are not traded on any national exchange, market system or over-the-counter bulletin board. Because no public market exists for our common shares, your ability to sell these shares is limited.

We are subject to intense competition.

We believe that each aspect of our business is highly competitive. Principal methods of competition in our operating segments are customer service, marketing, image, performance and reputation. Pricing is not always a critical factor in a customer’s decision with respect to our Residential and Commercial segment; however, pricing is generally the principal method of competition for our Utility segment, although in most instances consideration is given to reputation and past production performance. On a national level, our competition is primarily landscape construction and maintenance companies as well as residential and commercial lawn care companies. At a local and regional level, our competition comes mainly from small, local companies which are engaged primarily in tree care and lawn services. Our Utility segment competes principally with one major national competitor, as well as several smaller regional firms. Furthermore, competitors may have lower costs because privately-owned companies operating in a limited geographic area may have significantly lower labor and overhead costs. Our competitors may develop the expertise, experience and resources to provide services that are superior in both price and quality to our services. These strong competitive pressures could inhibit our success in bidding for profitable business and may have a material adverse effect on our business, financial condition and results of operations.

Our failure to comply with environmental laws could result in significant liabilities.

Our facilities and operations are subject to governmental regulations designed to protect the environment, particularly with respect to our services regarding insect and tree, shrub and lawn disease management, because these services involve to a considerable degree the blending and application of spray materials, which require formal licensing in most areas. Continual changes in environmental laws, regulations and licensing requirements, environmental conditions, environmental awareness, technology and social attitudes make it necessary for us to maintain a high degree of awareness of the impact such changes have on our compliance programs and the market for our services. We are subject to existing federal, state and local laws, regulations and licensing requirements regulating the use of materials in our spraying operations as well as certain other aspects of our business. If we fail to comply with such laws, regulations or licensing requirements, we may become subject to significant liabilities, fines and/or penalties, which could adversely affect our financial condition and results of operations.

We cannot predict the impact that policies regarding changing climate conditions, including legal, regulatory and social responses thereto, may have on our business.

Many scientists, environmentalists, international organizations, political activists, regulators and other commentators believe that global climate change has added, and will continue to add, to the unpredictability, frequency and severity of natural disasters in certain parts of the world. In response, a number of legal and regulatory measures and social initiatives have been introduced in an effort to reduce greenhouse gas and other carbon emissions that these parties believe may be contributors to global climate change. These proposals, if enacted, could result in a variety of regulatory programs, including potential new

Page 7

regulations, additional charges and taxes to fund energy efficiency activities, or other regulatory actions. Any of these actions could result in increased costs associated with our operations and impact the prices we charge our customers.

We cannot predict the impact, if any, that changing climate conditions will have on us or our customers. However, it is possible that the legal, regulatory and social responses to real or imagined climate change could have a negative effect on our results of operations or our financial condition.

We may be adversely affected if we are unable to obtain necessary surety bonds or letters of credit.

Surety market conditions are currently difficult as a result of significant losses incurred by many sureties in recent years, both in the construction industry as well as in certain larger corporate bankruptcies. As a result, less bonding capacity is available in the market and terms have become more expensive and restrictive. Further, under standard terms in the surety market, sureties issue or continue bonds on a project-by-project basis and can decline to issue bonds at any time or require the posting of collateral as a condition to issuing or renewing any bonds. If surety providers were to limit or eliminate our access to bonding, we would need to post other forms of collateral for project performance, such as letters of credit or cash. We may be unable to secure sufficient letters of credit on acceptable terms, or at all. Accordingly, if we were to experience an interruption or reduction in the availability of bonding capacity, our liquidity may be adversely affected.

We may be adversely affected if our reputation is damaged.

We are dependent, in part, upon our reputation of quality, integrity and performance. If our reputation were damaged in some way, it may impact our ability to grow or maintain our business.

We may be unable to employ a sufficient workforce for our field operations.

Our industry operates in an environment that requires heavy manual labor. We may experience slower growth in the labor force for this type of work than in the past. As a result, we may experience labor shortages or the need to pay more to attract and retain qualified employees.

We may be unable to attract and retain skilled management.

Our success depends, in part, on our ability to attract and retain key managers. Competition for the best people can be intense and we may not be able to promote, hire or retain skilled managers. The loss of services of one or more of our key managers could have a material adverse impact on our business because of the loss of the manager's skills, knowledge of our industry and years of industry experience, and the difficulty of promptly finding qualified replacement personnel.

Natural disasters, pandemics, terrorist attacks and other external events could adversely affect our business.

Natural disasters, pandemics, terrorist attacks and other adverse external events could materially damage our facilities or disrupt our operations, or damage the facilities or disrupt the operations of our customers or vendors. The occurrence of any such event could adversely affect our business, financial condition and results of operations.

A disruption in our information technology systems, including a disruption related to cybersecurity, could adversely affect our financial performance.

We rely on the accuracy, capacity and security of our information technology systems. Despite the security measures that we have implemented, including those measures related to cybersecurity, our systems could be breached or damaged by computer viruses, natural or man-made incidents or disasters or unauthorized physical or electronic access. A breach could result in business disruption, theft of our intellectual property, trade secrets or customer information and unauthorized access to personnel information. To the extent that our business is interrupted or data is lost, destroyed or inappropriately used or disclosed, such disruptions could adversely affect our competitive position, reputation, relationships with our customers, financial condition, operating results and cash flows. In addition, we may be required to incur significant costs to protect against the damage caused by these disruptions or security breaches in the future.

We are subject to third-party and governmental regulatory claims and litigation.

From time-to-time, customers, vendors, employees, governmental regulatory authorities and others may make claims and take legal action against us. Whether these claims and legal actions are founded or unfounded, if such claims and legal actions are not resolved in our favor, they may result in significant financial liability. Any such financial liability could have a

Page 8

material adverse effect on our financial condition and results of operations. Any such claims and legal actions may also require significant management attention and may detract from management's focus on our operations.

We may be adversely affected if we enter into a major unprofitable contract.

Our Residential and Commercial segment and our Utility segment frequently operate in a competitive bid contract environment. As a result, we may misjudge a bid and be contractually bound to an unprofitable contract, which could adversely affect our results of operations.

Item 1B. Unresolved SEC Staff Comments.

There are no unresolved comments from the Staff of the Securities and Exchange Commission.

Item 2. Properties.

Our corporate headquarters campus is located in Kent, Ohio, which, along with several other properties in the surrounding area, includes The Davey Institute's research, technical support and laboratory diagnostic facilities.

We conduct administrative functions through our headquarters and our offices in Livermore, California (Utility Services). Our Canadian operations’ administrative functions are conducted through properties located in the provinces of Ontario and British Columbia. We believe our properties are well maintained, in good condition and suitable for our present operations. A summary of our properties follows:

Segment | Number of Properties | How Held | Square Footage | Number of States or Provinces | |||||

Residential and Commercial | 29 | Owned | 274,271 | 15 | |||||

Utility | 3 | Owned | 36,037 | 3 | |||||

Residential and Commercial, and Utility | 3 | Owned | 30,080 | 3 | |||||

We also rent approximately 151 properties in 31 states and four provinces.

None of our owned or rented properties used by our business segments is individually material to our operations.

Item 3. Legal Proceedings.

In November 2017, a suit was filed against Davey Tree, its subsidiary, Wolf Tree, Inc., a former Davey employee, two Wolf employees, and a former Wolf employee alleging various acts of negligence and seeking compensatory and punitive damages for wrongful death and assault and battery of the plaintiff’s husband, a Wolf Tree employee in Savannah, Georgia, who was killed in August 2017. The Company has denied all liability and is vigorously defending the action. It also has retained separate counsel for three of the individual defendants, each of whom has denied all liability and also is vigorously defending the action.

On a quarterly basis, we assess our liabilities and contingencies in connection with outstanding legal proceedings utilizing the latest information available. Where it is probable that we will incur a loss and the amount of the loss can be reasonably estimated, we record a liability in our consolidated financial statements. These legal reserves may be increased or decreased to reflect any relevant developments on a quarterly basis. Where a loss is not probable or the amount of the loss is not estimable, we do not accrue legal reserves, consistent with applicable accounting guidance. Based on information currently available to us, advice of counsel, and available insurance coverage, we believe that our established reserves are adequate and the liabilities arising from the legal proceedings will not have a material adverse effect on our consolidated financial condition. We note, however, that in light of the inherent uncertainty in legal proceedings there can be no assurance that the ultimate resolution of a matter will not exceed established reserves. As a result, the outcome of a particular matter or a combination of matters may be material to our results of operations for a particular period, depending upon the size of the loss or our income for that particular period.

Item 4. Mine Safety Disclosures.

Not applicable.

Page 9

Executive Officers of the Company.

Our executive officers and their present positions and ages as of March 1, 2018 follow:

Name | Age | Position | Years with Company | Served as an Executive Officer Since |

Patrick M. Covey | 54 | President and Chief Executive Officer | 26 | 2007 |

Joseph R. Paul, CPA | 56 | Executive Vice President, Chief Financial Officer and Secretary | 12 | 2005 |

Lawrence S. Abernathy | 67 | Vice President, Davey Tree Surgery Company | 48 | 2015 |

Christopher J. Bast, CPA, CTP | 50 | Vice President and Treasurer | 4 | 2013 |

James E. Doyle | 49 | Executive Vice President and General Manager, Davey Tree Expert Co. of Canada, Limited | 28 | 2014 |

Gregory M. Ina | 46 | Executive Vice President, The Davey Institute and Employee Development | 22 | 2016 |

Dan A. Joy | 60 | Executive Vice President and General Manager, Commercial Landscape Services and Operations Support Services | 41 | 2013 |

Brent R. Repenning | 46 | Executive Vice President, U.S. Utility and Davey Resource Group | 23 | 2014 |

Thea R. Sears, CPA | 49 | Vice President and Controller | 24 | 2010 |

James F. Stief | 63 | Executive Vice President, U.S. Residential Operations | 39 | 2010 |

Mark J. Vaughn | 63 | Vice President and General Manager, Eastern Utility Services | 45 | 2013 |

Mr. Covey was appointed Chief Executive Officer effective July 21, 2017 and served as President and Chief Operating Officer since March 4, 2016 and as a Director since May 20, 2014. He previously served as President and Chief Operating Officer, U.S. Operations, having been appointed in April 2014, and as Chief Operating Officer, U.S. Operations, having been appointed in February 2012. Prior to that time, Mr. Covey served as Executive Vice President, having been appointed in January 2007, Vice President and General Manager of the Davey Resource Group, having been appointed in March 2005, and Vice President, Southern Operations, Utility Services, having been appointed in January 2003. Previously, having joined Davey Tree in August 1991, Mr. Covey held various managerial positions, including Manager of Systems and Process Management and Administrative Manager, Utility Services.

Mr. Paul was elected Executive Vice President, Chief Financial Officer and Secretary effective March 4, 2016 and served as Chief Financial Officer and Secretary, having been appointed in March 2013. Prior to that time, he served as Vice President and Treasurer, having been appointed in May 2011. Mr. Paul joined Davey Tree as Treasurer in December 2005.

Page 10

Mr. Abernathy was elected Vice President, Davey Tree Surgery Company, effective November 1, 2107 having previously served as Vice President and General Manager, Davey Tree Surgery Company, since April 2012, and as Senior Vice President, Davey Tree Surgery Company, having been appointed in July 2010. Prior to that time, he served as Vice President, Utility Operations, having been appointed in April 1995. Previously, having joined Davey Tree in 1969, Mr. Abernathy held various managerial positions, including Operations Manager, Area Manager and Account Manager.

Mr. Bast was elected Vice President effective September 18, 2017 having previously served as Treasurer since April 2013. Mr. Bast joined Davey Tree in March 2013 and prior to joining us, served in various management positions from 1994 to 2013 at Diebold, Incorporated, a provider of self-service delivery and security systems.

Mr. Doyle was elected Executive Vice President and General Manager, Davey Tree Expert Co. of Canada, Limited (“Davey Tree Limited”), effective May 21, 2014 and served as Vice President and General Manager, Davey Tree Limited, having been appointed in February 2012. Prior to that time, he served as Vice President and General Manager, Operations, Davey Tree Limited, having been appointed in May 2011 and Vice President, Operations, Davey Tree Limited, having been appointed in January 2006. Previously, having joined Davey Tree in 1989, Mr. Doyle held various managerial positions, including District Manager and Operations Manager.

Mr. Ina was elected Executive Vice President, The Davey Institute and Employee Development in July 2017, having previously served as Vice President and General Manager of Research, Recruiting and Human Resource Development effective April 4, 2016, and having previously been elected an officer effective March 4, 2016. Prior to this time, he served as Vice President and General Manager of the Davey Institute, having been appointed in May 2009 and General Manager of the Davey Institute, having been appointed in May 2006. Previously, having joined Davey Tree in 1996, Mr. Ina held various managerial and operational positions in the Davey Institute and Davey Resource Group.

Mr. Joy was elected Executive Vice President and General Manager, Commercial Landscape Services and Operations Support Services, effective August 15, 2014 and served as Executive Vice President and General Manager, Commercial Landscape Services, having been appointed in May 2014. Prior to that time, he served as Vice President and General Manager, Commercial Landscape Services, having been appointed in May 2013, and Vice President, Commercial Landscape Services, having been appointed in December 2004. Previously, having joined Davey Tree in 1976, Mr. Joy held various managerial positions, including Operations Manager, District Manager and Assistant District Manager.

Mr. Repenning was elected Executive Vice President, U.S. Utility and Davey Resource Group in July 2017, having previously served as Senior Vice President, Davey Resource Group and Eastern Utility, effective October 2, 2016 and served as Vice President and General Manager, Davey Resource Group, having been appointed in June 2010. Prior to that time, he served as Vice President, Davey Resource Group, having been appointed in October 2009. Previously, having joined Davey Tree in 1994, Mr. Repenning held various managerial and operational positions, including Regional Manager, Production Manager and Supervisor.

Ms. Sears was elected Vice President effective September 18, 2017 having served as Controller since September 16, 2016 and prior to that, served as Assistant Controller, having been appointed in May 2010. Prior to that time, she served as Manager of Financial Accounting, having been appointed in April 1998, and as Supervisor of Financial Accounting, having been appointed in September 1995. Having joined Davey Tree in 1993, Ms. Sears has held a variety of roles in financial reporting, managerial reporting and operations accounting.

Mr. Stief was elected Executive Vice President, U.S. Residential Operations, effective February 12, 2012 and previously served as Vice President and General Manager, Residential/Commercial Services, since January 2010. Prior to that time, Mr. Stief served as Vice President and General Manager, South, West and Central Residential/Commercial Operations, having been appointed in January 2007, and Vice President South, West and Central Residential/Commercial Operations, having been appointed in January 1997. Previously, having joined Davey Tree in 1978, Mr. Stief held various managerial positions, including Operations Manager and District Manager.

Mr. Vaughn was elected Vice President and General Manager, Eastern Utility Services, effective June 6, 2010, and served as Vice President, Eastern Utility Services, having been appointed in December 2007. Prior to that time, he served as Vice President, Northern Operating Group, Utility Services, having been appointed in July 2002. Previously, having joined Davey Tree in 1972, Mr. Vaughn held various managerial positions, including Operations Manager and Regional Manager.

Our officers serve from the date of their election to the next organizational meeting of the Board of Directors and until their respective successors are elected.

Page 11

PART II

Item 5. Market for Company’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common shares are not listed or traded on an established public trading market and market prices are, therefore, not available. Semiannually, for purposes of the Davey 401KSOP and ESOP, the fair market value of our common shares is determined by an independent stock valuation firm, based upon our performance and financial condition, using a peer group of comparable companies selected by that firm. The peer group currently consists of: ABM Industries Incorporated; Comfort Systems USA, Inc.; Dycom Industries, Inc.; MYR Group, Inc.; Quanta Services, Inc.; Rollins, Inc.; and Scotts Miracle-Gro Company. The semiannual valuations are effective for a period of six months and the per-share price established by those valuations is the price at which our Board of Directors has determined our common shares will be bought and sold during that six-month period in transactions involving Davey Tree or one of its employee benefit or stock purchase plans. Since 1979, we have provided a ready market for all shareholders through our direct purchase of their common shares, although we are under no obligation to do so (other than for repurchases pursuant to the put option under The Davey 401KSOP and ESOP Plan, as described in Note N). These purchases are added to our treasury stock.

Record Holders and Common Shares

On March 9, 2018 we had 3,800 record holders of our common shares.

On March 9, 2018 we had 24,227,668 common shares outstanding and options exercisable to purchase 800,615 common shares, partially-paid subscriptions for 764,382 common shares and purchase rights outstanding for 309,389 common shares.

Dividends

The following table sets forth, for the periods indicated, the cash dividends declared per common share (in cents). The numbers in the following table have been adjusted for a two-for-one stock split, effected in the form of a 100% stock dividend paid on June 15, 2017 to shareholders of record at the close of business on June 1, 2017.

Year Ended December 31, | ||||||

Quarter | 2017 | 2016 | ||||

1 | 2.50 | 2.50 | ||||

2 | 2.50 | 2.50 | ||||

3 | 2.50 | 2.50 | ||||

4 | 2.50 | 2.50 | ||||

Total | 10.00 | 10.00 | ||||

We presently expect to pay comparable cash dividends in 2018.

Recent Sales of Unregistered Securities

None.

Page 12

Purchases of Equity Securities

The following table provides information on purchases made by the Company of our common shares during the fiscal year ended December 31, 2017. The numbers in the following table have been adjusted for a two-for-one stock split, effected in the form of a 100% stock dividend paid on June 15, 2017 to shareholders of record at the close of business on June 1, 2017.

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number (or Approximate Dollar Value) of Shares that May Yet Be Purchased Under the Plans or Programs | |||||||||

Fiscal 2017 | |||||||||||||

January 1 to January 28 | 610 | $ | 16.95 | n/a | n/a | ||||||||

January 29 to February 25 | 548 | 16.95 | n/a | n/a | |||||||||

February 26 to April 1 | 117,878 | 17.60 | n/a | n/a | |||||||||

Total First Quarter | 119,036 | 17.59 | |||||||||||

April 2 to April 29 | 270,158 | 17.60 | n/a | n/a | |||||||||

April 30 to May 27 | 434,290 | 17.60 | — | 200,000 | |||||||||

May 28 to July 1 | 118,551 | 17.60 | — | 200,000 | |||||||||

Total Second Quarter | 822,999 | 17.60 | |||||||||||

July 2 to July 29 | 550 | 17.60 | — | 200,000 | |||||||||

July 30 to August 26 | 72,969 | 18.30 | — | 200,000 | |||||||||

August 27 to September 30 | 64,237 | 18.30 | — | 200,000 | |||||||||

Total Third Quarter | 137,756 | 18.30 | |||||||||||

October 1 to October 28 | 385,955 | 18.30 | 59,705 | 140,295 | |||||||||

October 29 to December 2 | 181,822 | 18.30 | 10,534 | 129,761 | |||||||||

December 3 to December 31 | 50,156 | 18.30 | — | 129,761 | |||||||||

Total Fourth Quarter | 617,933 | 18.30 | 70,239 | ||||||||||

Total Year to Date | 1,697,724 | $ | 17.91 | 70,239 | — | ||||||||

n/a--Not applicable. There were no publicly announced plans or programs to purchase common shares. | |||||||||||||

At the Annual Meeting of Shareholders of the Company held on May 16, 2017, the shareholders of the Company approved proposals to amend the Company's Articles of Incorporation to (i) expand the Company's current right of first refusal with respect to proposed transfers of shares of the Company's common shares, (ii) clarify provisions regarding when the Company may provide notice of its decision to exercise its right of first refusal with respect to proposed transfers of common shares by the estate or personal representative of a deceased shareholder, and (iii) grant the Company a right to repurchase common shares held by certain shareholders of the Company.

On May 10, 2017, the Board of Directors of the Company adopted a policy regarding the Company's exercise of the repurchase right granted to the Company through amendments to the Company's Articles of Incorporation, as approved by shareholders on May 16, 2017.

Until further action by the Board, it will be the policy of the Company not to exercise its repurchase rights under the amended Articles with respect to shares of the Company's common shares held by current and retired employees and current and

Page 13

former directors of the Company (subject to exceptions set forth in the policy) (collectively, "Active Shareholders"), their spouses, their first-generation descendants and trusts established exclusively for their benefit.

Until further action by the Board, it will also be the policy of the Company not to exercise its rights under the amended Articles to repurchase shares of the Company's common shares proposed to be transferred by an Active Shareholder to his or her spouse, a first-generation descendant, or a trust established exclusively for the benefit of one or more of an Active Shareholder, his or her spouse and first-generation descendants of an Active Shareholder, or upon the death of an Active Shareholder, such transfers from the estate or personal representative of a deceased Active Shareholder. The Board may suspend, change or discontinue the policy at any time without prior notice.

On May 17, 2017, in accordance with the amendments to the Articles approved by the Company's shareholders at the Annual Meeting, the Company's Board of Directors authorized the Company to repurchase up to 100,000 common shares (200,000 common shares on a post-split basis). Share repurchases may be made from time to time and the timing of any repurchases and the actual number of shares repurchased will depend on a variety of factors. The Company is not obligated to purchase any shares, and repurchases may be commenced, suspended or discontinued from time to time without prior notice. The repurchase program does not have an expiration date.

Page 14

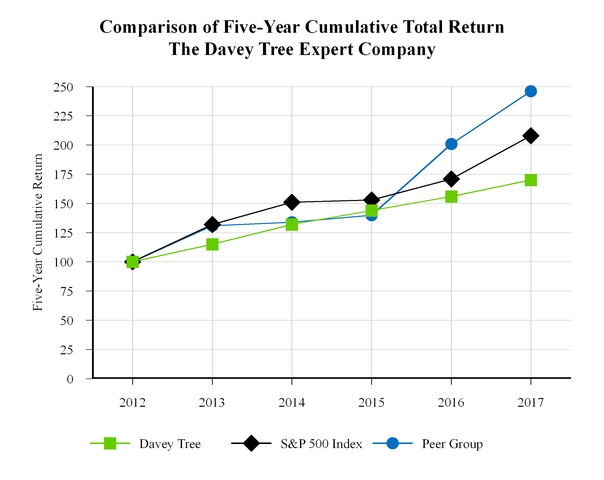

Stock Performance Graph

Comparison of five-year cumulative return among The Davey Tree Expert Company, S&P 500 Stock Index and Selected Peer Group Companies Index

The following Performance Graph compares cumulative total shareholder returns for The Davey Tree Expert Company common shares during the last five years to the Standard & Poor’s 500 Stock Index and to an index of selected peer group companies. The peer group, which is the same group used by Davey’s independent stock valuation firm, consists of: ABM Industries Incorporated; Comfort Systems USA, Inc.; Dycom Industries, Inc.; MYR Group, Inc.; Quanta Services, Inc.; Rollins, Inc.; and Scotts Miracle-Gro Company. Each of the three measures of cumulative total return assumes reinvestment of dividends.

2012 | 2013 | 2014 | 2015 | 2016 | 2017 | |||||||

Davey Tree | 100 | 115 | 132 | 144 | 156 | 170 | ||||||

S&P 500 Index | 100 | 132 | 151 | 153 | 171 | 208 | ||||||

Peer Group | 100 | 131 | 134 | 140 | 201 | 246 | ||||||

The Performance Graph and related information above shall not be deemed “soliciting material” or be “filed” with the Securities and Exchange Commission, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933 or Securities Exchange Act of 1934, each as amended, except to the extent that we specifically incorporate it by reference into such filing.

Page 15

Item 6. Selected Financial Data.

Fiscal Year Ended December 31, | |||||||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||

(In thousands, except ratio and per share data) | |||||||||||||||||||

Operating Statement Data: | |||||||||||||||||||

Revenues | $ | 915,958 | $ | 845,678 | $ | 821,904 | $ | 789,911 | $ | 713,848 | |||||||||

Costs and expenses: | |||||||||||||||||||

Operating | 587,333 | 541,486 | 528,899 | 508,677 | 462,646 | ||||||||||||||

Selling | 167,934 | 152,106 | 144,234 | 140,027 | 120,842 | ||||||||||||||

General and administrative | 64,589 | 61,789 | 59,798 | 54,970 | 50,654 | ||||||||||||||

Depreciation | 50,702 | 47,284 | 44,677 | 40,970 | 38,231 | ||||||||||||||

Amortization of intangible assets | 2,384 | 2,306 | 2,214 | 2,070 | 1,980 | ||||||||||||||

Gain on sale of assets, net | (3,989 | ) | (4,664 | ) | (2,026 | ) | (806 | ) | (1,294 | ) | |||||||||

Income from operations | 47,005 | 45,371 | 44,108 | 44,003 | 40,789 | ||||||||||||||

Interest expense | (4,886 | ) | (4,393 | ) | (3,355 | ) | (2,948 | ) | (2,708 | ) | |||||||||

Interest income | 292 | 255 | 249 | 295 | 311 | ||||||||||||||

Other expense | (4,417 | ) | (3,989 | ) | (5,744 | ) | (3,050 | ) | (2,827 | ) | |||||||||

Income before income taxes | 37,994 | 37,244 | 35,258 | 38,300 | 35,565 | ||||||||||||||

Income taxes | 15,874 | 14,960 | 13,460 | 15,131 | 12,712 | ||||||||||||||

Net income | $ | 22,120 | $ | 22,284 | $ | 21,798 | $ | 23,169 | $ | 22,853 | |||||||||

Earnings per share--diluted * | $ | .83 | $ | .82 | $ | .78 | $ | .81 | $ | .79 | |||||||||

Shares used for computing per share amounts--diluted * | 26,697 | 27,247 | 27,955 | 28,477 | 29,205 | ||||||||||||||

Other Financial Data: | |||||||||||||||||||

Depreciation and amortization | $ | 53,086 | $ | 49,590 | $ | 46,891 | $ | 43,040 | $ | 40,211 | |||||||||

Capital expenditures | 57,100 | 56,646 | 56,047 | 55,731 | 45,205 | ||||||||||||||

Cash flow provided by (used in): | |||||||||||||||||||

Operating activities | 56,776 | 55,370 | 62,689 | 49,279 | 56,310 | ||||||||||||||

Investing activities | (59,518 | ) | (54,808 | ) | (56,046 | ) | (64,060 | ) | (43,205 | ) | |||||||||

Financing activities | 6,410 | (7,721 | ) | (7,140 | ) | 17,335 | (16,891 | ) | |||||||||||

Cash dividends declared per share * | $ | .1000 | $ | .1000 | $ | .1000 | $ | .0925 | $ | .0900 | |||||||||

Page 16

As of December 31, | |||||||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||

(In thousands, except ratio and per share data) | |||||||||||||||||||

Balance Sheet Data: | |||||||||||||||||||

Working capital | $ | 80,468 | $ | 59,868 | $ | 48,984 | $ | 49,916 | $ | 39,030 | |||||||||

Current ratio | 1.63 | 1.50 | 1.44 | 1.46 | 1.37 | ||||||||||||||

Property and equipment, net | 193,183 | 179,436 | 166,422 | 160,883 | 136,884 | ||||||||||||||

Total assets | 473,135 | 423,939 | 393,586 | 381,004 | 330,814 | ||||||||||||||

Long-term debt | 119,210 | 92,623 | 85,104 | 81,306 | 50,034 | ||||||||||||||

Other long-term liabilities | 63,878 | 60,565 | 55,464 | 54,854 | 44,371 | ||||||||||||||

Redeemable common shares related to 401KSOP and Employee Stock Ownership Plan (ESOP) | 123,520 | 124,201 | 127,089 | 123,668 | 113,694 | ||||||||||||||

Total common shareholders' equity | 37,870 | 27,978 | 14,450 | 12,826 | 19,347 | ||||||||||||||

Redeemable common shares * | 6,467 | 7,057 | 7,773 | 8,217 | 8,613 | ||||||||||||||

Common shares: * | |||||||||||||||||||

Issued | 36,447 | 35,857 | 35,141 | 34,697 | 34,301 | ||||||||||||||

Less: In treasury | 18,693 | 17,991 | 17,427 | 16,584 | 16,036 | ||||||||||||||

Net outstanding | 24,221 | 24,923 | 25,487 | 26,330 | 26,878 | ||||||||||||||

Stock options: * | |||||||||||||||||||

Outstanding | 1,529 | 1,599 | 1,634 | 1,540 | 1,324 | ||||||||||||||

Exercisable | 801 | 751 | 834 | 778 | 684 | ||||||||||||||

ESOT valuation per share * | $ | 19.10 | $ | 17.60 | $ | 16.35 | $ | 15.05 | $ | 13.20 | |||||||||

* Prior periods have been adjusted for the two-for-one stock split, effective June 1, 2017, as discussed in Note B to the audited financial statements included in Item 8.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

(Amounts in thousands, except share data)

Management’s Discussion and Analysis of Results of Operations and Financial Condition (“MD&A”) is provided as a supplement to the accompanying consolidated financial statements and notes to help provide an understanding of our financial condition, cash flows and results of operations. MD&A is organized as follows:

▪ | Overview of 2017 Results; |

▪ | Results of Operations, including fiscal 2017 compared to fiscal 2016, fiscal 2016 compared to fiscal 2015, liabilities for uncertain income tax positions, and other matters; |

▪ | Liquidity and Capital Resources, including cash flow summary, off-balance sheet arrangements, and capital resources; |

▪ | Recent Accounting Guidance; |

▪ | Critical Accounting Policies and Estimates; and |

▪ | Market Risk Information, including interest rate risk and foreign currency exchange rate risk. |

OVERVIEW OF 2017 RESULTS

General

We provide a wide range of horticultural, arboricultural, environmental and consulting services to residential, commercial, utility and institutional customers throughout the United States and Canada.

Our Business--We have two reportable operating segments organized by type or class of customer: Residential and Commercial, and Utility.

Page 17

Residential and Commercial--Residential and Commercial provides services to our residential and commercial customers including: the treatment, preservation, maintenance, removal and planting of trees, shrubs and other plant life; the practice of landscaping, grounds maintenance, tree surgery, tree feeding and tree spraying; the application of fertilizer, herbicides and insecticides; and natural resource management and consulting, forestry research and development, and environmental planning.

Utility--Utility is principally engaged in providing services to our utility customers--investor-owned, municipal utilities, and rural electric cooperatives--including: the practice of line-clearing and vegetation management around power lines, rights-of-way and chemical brush control; and natural resource management and consulting, forestry research and development and environmental planning.

All other operating activities, including research, technical support and laboratory diagnostic facilities, are included in “All Other.”

Results of Operations

The following table sets forth our consolidated results of operations as a percentage of revenues and the percentage change in dollar amounts of the results of operations for the periods presented:

Year Ended December 31, | Percentage Change | |||||||||||||

2017 | 2016 | 2015 | 2017/2016 | 2016/2015 | ||||||||||

Revenues | 100.0 | % | 100.0 | % | 100.0 | % | 8.3 | % | 2.9 | % | ||||

Costs and expenses: | ||||||||||||||

Operating | 64.1 | 64.0 | 64.3 | 8.5 | 2.4 | |||||||||

Selling | 18.3 | 18.0 | 17.5 | 10.4 | 5.5 | |||||||||

General and administrative | 7.1 | 7.3 | 7.3 | 4.5 | 3.3 | |||||||||

Depreciation | 5.5 | 5.6 | 5.4 | 7.2 | 5.8 | |||||||||

Amortization of intangible assets | .3 | .3 | .3 | 3.4 | 4.2 | |||||||||

Gain on sale of assets, net | (.4 | ) | (.6 | ) | (.2 | ) | (14.5 | ) | 130.2 | |||||

94.9 | 94.6 | 94.6 | 8.6 | 2.9 | ||||||||||

Income from operations | 5.1 | 5.4 | 5.4 | 3.6 | 2.9 | |||||||||

Other income (expense): | ||||||||||||||

Interest expense | (.5 | ) | (.5 | ) | (.4 | ) | 11.2 | 30.9 | ||||||

Interest income | — | — | — | nm | nm | |||||||||

Other | (.5 | ) | (.5 | ) | (.7 | ) | 10.7 | (30.6 | ) | |||||

Income before income taxes | 4.1 | 4.4 | 4.3 | 2.0 | 5.6 | |||||||||

Income taxes | 1.7 | 1.8 | 1.6 | 6.1 | 11.1 | |||||||||

Net income | 2.4 | % | 2.6 | % | 2.7 | % | (.7 | )% | 2.2 | % | ||||

nm--not meaningful | ||||||||||||||

Revenues of $915,958 were 8.3% higher than last year’s revenues of $845,678. Utility revenues increased 7.7%, and Residential and Commercial revenues increased 8.6% from the prior year.

Overall, income from operations of $47,005 increased 3.6% from the $45,371 experienced in the prior year. Income from operations was $18,223 in Utility (a 5.4% decrease as compared with 2016) and $41,158 for Residential and Commercial (a 12.3% increase as compared with 2016).

Net income of $22,120 was $164 less than the $22,284 earned in 2016. The increase in income from operations was offset by increases in other nonoperating expenses of $428, income taxes of $914 and interest expense of $493.

Operating activities in 2017 provided cash of $56,776 as compared to $55,370 provided in 2016. The $1,406 net increase was primarily attributable to (i) $5,349 less cash used by accounts receivable, (ii) an increase of $3,496 in depreciation and

Page 18

amortization expense, (iii) an increase of $3,693 in deferred income taxes offset by (iv) $12,938 less cash provided from changes in operating assets and liabilities excluding accounts receivable.

Investing activities used $59,518 in cash, or $4,710 more than that used in 2016. Increases in expenditures for equipment, land and buildings and purchases of businesses were partially offset by fewer proceeds from the sales of assets.

Financing activities provided $6,410 in cash in 2017, $14,131 more than the $7,721 of cash used in 2016. The increase in cash provided of $14,131 was primarily attributable to (i) $20,500 more cash provided by our revolving credit facility, (ii) $2,247 more cash used for purchases of common shares, sale of common shares and cash received on common share subscription, net and (iii) $4,206 more cash used for payments of notes payable, long-term debt and capital leases. .

Fiscal 2017 Compared to Fiscal 2016

A comparison of our fiscal year 2017 results to 2016 follows:

Year Ended December 31, | ||||||||||||||

2017 | 2016 | Change | % Change | |||||||||||

Revenues | $ | 915,958 | $ | 845,678 | $ | 70,280 | 8.3 | % | ||||||

Costs and expenses: | ||||||||||||||

Operating | 587,333 | 541,486 | 45,847 | 8.5 | ||||||||||

Selling | 167,934 | 152,106 | 15,828 | 10.4 | ||||||||||

General and administrative | 64,589 | 61,789 | 2,800 | 4.5 | ||||||||||

Depreciation | 50,702 | 47,284 | 3,418 | 7.2 | ||||||||||

Amortization of intangible assets | 2,384 | 2,306 | 78 | 3.4 | ||||||||||

Gain on sale of assets, net | (3,989 | ) | (4,664 | ) | 675 | (14.5 | ) | |||||||

868,953 | 800,307 | 68,646 | 8.6 | |||||||||||

Income from operations | 47,005 | 45,371 | 1,634 | 3.6 | ||||||||||

Other income (expense): | ||||||||||||||

Interest expense | (4,886 | ) | (4,393 | ) | (493 | ) | 11.2 | |||||||

Interest income | 292 | 255 | 37 | 14.5 | ||||||||||

Other | (4,417 | ) | (3,989 | ) | (428 | ) | 10.7 | |||||||

Income before income taxes | 37,994 | 37,244 | 750 | 2.0 | ||||||||||

Income taxes | 15,874 | 14,960 | 914 | 6.1 | ||||||||||

Net income | $ | 22,120 | $ | 22,284 | $ | (164 | ) | (.7 | )% | |||||

Revenues--Revenues of $915,958 increased $70,280 compared with the $845,678 reported in 2016. Utility increased $33,348, or 7.7%, from the prior year. The increase is attributable to additional revenues from storm-related services provided as a result of Hurricane Irma in the Southeast United States and increased work year-over-year on existing accounts as well as new accounts. Residential and Commercial increased $35,150, or 8.6%, from 2016. Increases in tree surgery, spraying, landscaping, pest management as well as storm-related work as a result of Hurricane Irma were partially offset by decreases in snow removal and mowing revenues. Higher contract rates on our tree pruning, tree removal and liquid services, increased storm revenue, increased productivity and additional revenue from the purchase of businesses accounted for the increase. Total consolidated revenue of $915,958 includes production incentive revenue, recognized under the completed-performance method, of $2,336 during 2017 as compared with $2,827 during 2016.

Operating Expenses--Operating expenses of $587,333 increased $45,847 from the prior year, and as a percentage of revenues increased .1% to 64.1%. Utility experienced an increase of $28,043, or 8.7%, from 2016, and as a percentage of revenues increased .6% to 75.0%. Increases in employee labor and benefits expense, fuel expense, subcontractor expense, disposal expense and crew expenses associated with the increased revenues were partially offset by decreases in repair and maintenance expense and material expense. Residential and Commercial increased $16,234, or 7.5%, compared with 2016 but as a percentage of revenue decreased .4% to 52.2%. Increases primarily in employee labor and benefits expense, repair and maintenance expense, fuel expense, materials expense, subcontractor expense and crew expense account for the increase.

Page 19

Fuel costs increased in 2017 as compared with fuel costs for 2016 and impacted operating expenses within both segments. During 2017, fuel expense of $27,427 increased $4,750, or 20.9%, from the $22,677 incurred in 2016. The $4,750 increase included price increases approximating $3,861 and usage increases approximating $889.

Selling Expenses--Selling expenses of $167,934 increased $15,828 from 2016 and as a percentage of revenues increased .3% to 18.3%. Utility increased $4,916, or 10.8%, from 2016 and as a percentage of revenue increased .3% to 10.8%. Increases in field management wages and incentive expense, office support wage expense, field management auto expense, rent expense and communication expense were partially offset by reductions in field management travel expense, local office expense, computer expense and employee development expense. Residential and Commercial increased $11,062, or 10.1%, from 2016 and as a percentage of revenue increased .3% to 27.1%. Increases primarily in field management wages and incentive expense, office support wage expense, sales and marketing expense, employee development expense, communication expense and field management travel expense were partially offset by a reduction in computer expense.

General and Administrative Expenses--General and administrative expenses increased $2,800 to $64,589, an increase of 4.5% from the $61,789 experienced in 2016 but as a percentage of revenues decreased .2% to 7.1%. Increases in pension expense, salary and incentive expense, stock compensation expense, computer expense and office rent expense were partially offset by a decrease in office expenses, communication expense and management travel expense.

Depreciation and Amortization Expense--Depreciation and amortization expense of $53,086 increased $3,496 from the prior year and as a percentage of revenues decreased .1% to 5.8%. The increase is attributable to higher capital expenditures for equipment, land and buildings and an increase in amortization expense related to our purchases of businesses.

Gain on Sale of Assets--Gain on the sale of assets of $3,989 decreased $675 from the $4,664 experienced in 2016. The decrease is the result of lower average sales prices on units disposed of in 2017 as compared with 2016. In addition, the gain of $4,664 in 2016 also included the sale of a building.

Interest Expense--Interest expense of $4,886 increased $493 from the $4,393 incurred in 2016. The increase is attributable to higher average debt levels and borrowing rates necessary to fund operations and capital expenditures.

Other, Net--Other, net of $4,417 increased $428 from the $3,989 experienced in 2016. Other, net, consisted of nonoperating income and expense, including foreign currency gains on the intercompany account balances of our Canadian operations.

Income Taxes--Income taxes for 2017 were $15,874, an effective tax rate of 41.8%, compared with income taxes for 2016 of $14,960, or an effective tax rate of 40.2%. The increase of 1.6% in the effective tax rate as compared to 2016 relates primarily to changes in our deferred taxes as a result of the Tax Cuts and Jobs Act (the "Tax Reform Act"), as described in Note Q, enacted in the fourth quarter of 2017.

Net Income--Net income of $22,120 was $164 less than the $22,284 earned in 2016. The increase in income from operations of $1,634 was offset by increases in other nonoperating expenses of $428, interest expense of $493 and income taxes of $914.

Page 20

Fiscal 2016 Compared to Fiscal 2015

A comparison of our fiscal year 2016 results to 2015 follows:

Year Ended December 31, | ||||||||||||||

2016 | 2015 | Change | % Change | |||||||||||

Revenues | $ | 845,678 | $ | 821,904 | $ | 23,774 | 2.9 | % | ||||||

Costs and expenses: | ||||||||||||||

Operating | 541,486 | 528,899 | 12,587 | 2.4 | ||||||||||

Selling | 152,106 | 144,234 | 7,872 | 5.5 | ||||||||||

General and administrative | 61,789 | 59,798 | 1,991 | 3.3 | ||||||||||

Depreciation | 47,284 | 44,677 | 2,607 | 5.8 | ||||||||||

Amortization of intangible assets | 2,306 | 2,214 | 92 | 4.2 | ||||||||||

Gain on sale of assets, net | (4,664 | ) | (2,026 | ) | (2,638 | ) | 130.2 | |||||||

800,307 | 777,796 | 22,511 | 2.9 | |||||||||||

Income from operations | 45,371 | 44,108 | 1,263 | 2.9 | ||||||||||

Other income (expense): | ||||||||||||||

Interest expense | (4,393 | ) | (3,355 | ) | (1,038 | ) | 30.9 | |||||||

Interest income | 255 | 249 | 6 | 2.4 | ||||||||||

Other | (3,989 | ) | (5,744 | ) | 1,755 | (30.6 | ) | |||||||

Income before income taxes | 37,244 | 35,258 | 1,986 | 5.6 | ||||||||||

Income taxes | 14,960 | 13,460 | 1,500 | 11.1 | ||||||||||

Net income | $ | 22,284 | $ | 21,798 | $ | 486 | 2.2 | % | ||||||

Revenues--Revenues of $845,678 increased $23,774 compared with the $821,904 reported in 2015. Utility increased $262, or .1%, from the prior year. New contracts obtained and increases in rates and productivity on contracts within both our U.S. and Canadian operations were partially offset by contracts lost and significant reductions in contract scope with two utility providers within our U.S. Utility operations. Residential and Commercial increased $24,551, or 6.4%, from 2015. Higher contract rates on our tree pruning, tree removal and liquid services, increased storm revenue, increased productivity and additional revenue from the purchase of businesses accounted for the increase. Total consolidated revenue of $845,678 includes production incentive revenue, recognized under the completed-performance method, of $2,827 during 2016 as compared with $4,686 during 2015.

Operating Expenses--Operating expenses of $541,486 increased $12,587 from the prior year, and as a percentage of revenues decreased .3% to 64.0%. Utility experienced an increase of $1,971, or .6%, from 2015, and as a percentage of revenues increased .6% to 74.4%. Increases in employee labor and benefits expense, equipment repair and maintenance expense, disposal expense and subcontractor expense were partially offset by decreases in fuel expense, crew expense and material expense. Residential and Commercial increased $12,767, or 6.3%, compared with 2015 and as a percentage of revenue decreased .1% to 52.6%. Increases in employee labor and benefits expense, subcontractor expense, disposal expense, tool and saw expense and material expense were partially offset by decreases in fuel expense and crew expense.

Fuel costs decreased in 2016 as compared with fuel costs for 2015 and impacted operating expenses within both segments. During 2016, fuel expense of $22,677 decreased $3,204, or 12.4%, from the $25,881 incurred in 2015. Substantially all of the $3,204 decrease relates to a decrease in price of fuel.