Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Stock Yards Bancorp, Inc. | ex_106112.htm |

| EX-32.1 - EXHIBIT 32.1 - Stock Yards Bancorp, Inc. | ex_106111.htm |

| EX-31.2 - EXHIBIT 31.2 - Stock Yards Bancorp, Inc. | ex_106110.htm |

| EX-31.1 - EXHIBIT 31.1 - Stock Yards Bancorp, Inc. | ex_106109.htm |

| EX-23 - EXHIBIT 23 - Stock Yards Bancorp, Inc. | ex_106108.htm |

| EX-21 - EXHIBIT 21 - Stock Yards Bancorp, Inc. | ex_106107.htm |

| EX-14 - EXHIBIT 14 - Stock Yards Bancorp, Inc. | ex_106105.htm |

| EX-10.37 - EXHIBIT 10.37 - Stock Yards Bancorp, Inc. | ex_106106.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Form 10-K

Annual Report Pursuant to Section 13

or 15(d) of the Securities Exchange Act of 1934

|

For the Fiscal Year Ended |

Commission File Number |

|

|

December 31, 2017 |

1-13661 |

STOCK YARDS BANCORP, INC.

1040 East Main Street

Louisville, Kentucky 40206

(502) 582-2571

|

Incorporated in Kentucky |

I.R.S. No. 61-1137529 |

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class: |

Name of each exchange on which registered: |

|

Common Stock, no par value |

NASDAQ |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer (as defined in Rule 405 of the Securities Act).

Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☑ | Accelerated filer | ☐ |

| Non-accelerated filer (Do not check if a smaller reporting company) | ☐ | Smaller reporting company | ☐ |

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☑

The aggregate market value of registrant’s voting stock (Common Stock, no par value) held by non-affiliates of the registrant as of June 30, 2017 (the last business day of the registrant’s most recently completed second fiscal quarter) was $802,453,551.

The number of shares of the registrant’s Common Stock, no par value, outstanding as of February 23, 2018, was 22,715,321.

Documents Incorporated By Reference

Portions of Registrant’s definitive proxy statement related to Registrant’s Annual Meeting of Shareholders to be held on April 26, 2018 (the “Proxy Statement”), to be filed with the Securities and Exchange Commission, are incorporated by reference into Part III of this Form 10-K.

STOCK YARDS BANCORP, INC.

Form 10-K

Index

|

|

|

|

|

Item 1. |

1 |

|

|

Item 1A. |

3 |

|

|

Item 1B. |

8 |

|

|

Item 2. |

8 |

|

|

Item 3. |

8 |

|

|

Item 4. |

8 |

|

|

|

|

|

|

Item 5. |

10 |

|

|

|

|

|

|

Item 6. |

12 |

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

13 |

|

Item 7A. |

46 |

|

|

Item 8. |

46 |

|

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

96 |

|

Item 9A. |

96 |

|

|

Item 9B. |

99 |

|

|

|

|

|

|

Item 10. |

99 |

|

|

Item 11. |

99 |

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

99 |

|

|

|

|

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

100 |

|

Item 14. |

100 |

|

|

|

|

|

|

Item 15. |

100 |

|

|

Item 16. |

103 |

|

|

Signatures |

|

104 |

Glossary of Acronyms and Terms

The following listing provides a comprehensive reference of common acronyms and terms used throughout the document:

|

ASU |

Accounting Standards Update |

|

Bancorp |

Stock Yards Bancorp, Inc. |

|

Bank |

Stock Yards Bank & Trust Company |

|

BOLI |

Bank Owned Life Insurance |

|

BP |

Basis Point = 1/100th of one percent |

|

COSO |

Committee of Sponsoring Organizations |

|

CRA |

Community Reinvestment Act of 1977 |

|

Dodd-Frank Act |

Dodd-Frank Wall Street Reform and Consumer Protection Act |

|

EPS |

Earnings Per Share |

|

FASB |

Financial Accounting Standards Board |

|

FDIC |

Federal Deposit Insurance Corporation |

|

FHA |

Federal Housing Administration |

|

FHC |

Financial Holding Company |

|

FHLB |

Federal Home Loan Bank |

|

FHLMC |

Federal Home Loan Mortgage Corporation |

|

FNMA |

Federal National Mortgage Association |

|

GLB Act |

Gramm-Leach-Bliley Act |

|

GNMA |

Government National Mortgage Association |

|

WM&T |

Wealth management and trust |

|

KSOP |

Combined employee profit sharing and stock ownership plan |

|

LIBOR |

London Interbank Offered Rate |

|

MSA |

Metropolitan Statistical Area |

|

MSR |

Mortgage Servicing Right |

|

OAEM |

Other Assets Especially Mentioned |

|

Oldham |

THE BANCORP, Inc. |

|

OREO |

Other Real Estate Owned |

|

OTTI |

Other-Than-Temporary Impairment |

|

PSU |

Performance Stock Unit |

|

RSU |

Restricted Stock Unit |

|

SAR |

Stock Appreciation Right |

|

SEC |

Securities and Exchange Commission |

|

TDRs |

Troubled Debt Restructurings |

|

US GAAP |

United States Generally Accepted Accounting Principles |

|

VA |

U.S. Department of Veterans Affairs |

|

Item 1. |

Business |

Stock Yards Bancorp, Inc. (“Bancorp” or “Company”), headquartered in Louisville, Kentucky, is the holding company for Stock Yards Bank & Trust Company (“Bank”). Bancorp, which was incorporated in 1988 in Kentucky, is registered with, and subject to supervision, regulation and examination by, the Board of Governors of the Federal Reserve System. The Bank is wholly owned and is a state chartered bank. Because Bancorp has no significant operations of its own, its business and that of the Bank are essentially the same. The operations of the Bank are fully reflected in the consolidated financial statements of Bancorp. Accordingly, references to “Bancorp” in this document may encompass both the holding company and the Bank.

Stock Yards Bank & Trust Company

Stock Yards Bank & Trust Company is the banking and sole subsidiary of Bancorp and was chartered in 1904. The Bank is headquartered in Louisville, Kentucky and provides commercial and personal banking services in the Louisville, Kentucky, Indianapolis, Indiana and Cincinnati, Ohio metropolitan markets through 37 full service banking offices. The Bank is chartered under the laws of the Commonwealth of Kentucky. In addition to traditional commercial and personal banking activities, the Bank has a wealth management and trust department (WM&T) offering a wide range of investment management, trust, employee benefit plan, estate administration, and financial planning services. The Bank also originates and sells single-family residential mortgages. Additionally, the Bank offers securities brokerage services via its branch network through an arrangement with a third party broker-dealer. See Note 25 to Bancorp’s consolidated financial statements for information relating to the Bank’s business segments and “Item 2. Properties” for information regarding owned and leased properties.

At December 31, 2017, Stock Yards Bank & Trust Company had 580 full-time equivalent employees. Employees of Stock Yards Bank & Trust Company are entitled to participate in a variety of employee benefit programs including a combined employee profit sharing and stock ownership plan (“KSOP”). Management of Bancorp strives to be an employer of choice and considers the relationship with employees to be good.

Supervision and Regulation

Bank holding companies and commercial banks are extensively regulated under both federal and state laws. Changes in applicable laws or regulations may have a material effect on the business and prospects of Bancorp.

Bancorp, as a registered bank holding company, is subject to the supervision of and regulation by the Federal Reserve Board under the Bank Holding Company Act of 1956. In addition, Bancorp is subject to the provisions of Kentucky’s banking laws regulating bank acquisitions and certain activities of controlling bank shareholders.

Kentucky and federal banking statutes delineate permissible activities for Kentucky state-chartered banks. Kentucky’s statutes, however, contain a super parity provision for Kentucky chartered banks having one of the top two ratings in its most recent regulatory examination. This provision allows these state banks to engage in any banking activity in which a national bank, a state bank operating in any other state, or a federally chartered thrift could engage. The bank must first obtain a legal opinion specifying the statutory or regulatory provisions that permit the activity.

The Bank is subject to the supervision of the Kentucky Department of Financial Institutions and the Federal Deposit Insurance Corporation. The Federal Deposit Insurance Corporation (“FDIC”) insures the deposits of the Bank to the current maximum of $250,000 per depositor.

The Gramm-Leach-Bliley Act (the “GLB Act”) allows for affiliations among banks, securities firms and insurance companies by means of a financial holding company (“FHC”). The GLB Act requires that, at the time of establishment of an FHC, all depository institutions within that corporate group must be “well managed” and “well capitalized” and must have received a rating of “satisfactory” or better under its most recent Community Reinvestment Act examination. Further, non-banking financial firms (for example an insurance company or securities firm) may establish an FHC and acquire a depository institution. While the distinction between banks and non-banking financial firms has been blurring over recent years, the GLB Act makes it less cumbersome for banks to offer services “financial in nature” but beyond traditional commercial banking activities. Likewise, non-banking financial firms may find it easier to offer services that had, heretofore, been provided primarily by depository institutions. In 2012, management of Bancorp chose to become an FHC.

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”) was signed into law in 2010. Generally, the Dodd-Frank Act was effective the day after it was signed into law, but different effective dates apply to specific sections of the law. This extensive and complex legislation contained many provisions affecting the banking industry, including:

|

● |

Creation of a Bureau of Consumer Financial Protection overseeing banks with assets totaling $10 billion or greater while writing and maintaining several regulations that apply to all banks, |

|

● |

Determination of debit card interchange rates by the Federal Reserve Board, |

|

● |

New regulation over derivative instruments, |

|

● |

Phase outs of certain forms of trust preferred debt and hybrids previously included as bank capital, and |

|

● |

Increases to FDIC deposit coverage, revised calculations for assessing bank premiums, and numerous other provisions affecting financial institution regulation, oversight of certain non-banking organizations, investor protection, etc. |

Bancorp continues to be subject to regulation under the Dodd-Frank Act; however, the current presidential administration has instructed federal agencies to reduce the regulatory burden on financial institutions.

The Community Reinvestment Act of 1977 (CRA) requires depository institutions to assist in meeting the credit needs of their market areas consistent with safe and sound banking practice. Under the CRA, each depository institution is required to help meet the credit needs of its market areas by, among other things, providing credit to low- and moderate-income individuals and communities. Depository institutions are periodically examined for compliance with the CRA, and banking regulators take into account CRA ratings when considering approval of certain applications. An unsatisfactory CRA rating could, among other things, result in the denial or delay of corporate applications filed by Bancorp or the Bank for proposed activities such as branch openings or relocations and applications to acquire, merge or consolidate with another banking institution or holding company.

The federal banking regulators have adopted rules limiting the ability of banks and other financial institutions to disclose non-public information about consumers to unaffiliated third parties. These limitations require disclosure of privacy policies to consumers and, in some circumstances, allow consumers to prevent disclosure of certain personal information to an unaffiliated third party. These regulations affect how consumer information is conveyed to outside vendors. The Bank is also subject to regulatory guidelines establishing standards for safeguarding customer information. These guidelines describe the federal banking agencies’ expectations for the creation, implementation and maintenance of an information security program, which would include administrative, technical and physical safeguards appropriate to the size and complexity of the institution and the nature and scope of its activities.

The Bank is subject to the Bank Secrecy Act and the USA Patriot Act. These statutes and related rules and regulations impose requirements and limitations on specified financial transactions and accounts and other relationships intended to guard against money laundering and terrorism financing. Financial institutions must take certain steps to assist government agencies in detecting and preventing money laundering and report certain types of suspicious transactions. Regulatory authorities routinely examine financial institutions for compliance with these obligations, and failure of a financial institution to maintain and implement adequate programs to combat money laundering and terrorist financing, or to comply with all of the relevant laws or regulations, could have serious legal and reputational consequences for the institution, including causing applicable bank regulatory authorities not to approve merger or acquisition transactions when regulatory approval is required or to prohibit such transactions even if approval is not required.

In 2013, the Federal Reserve Board and the FDIC approved rules that substantially amended the regulatory risk-based capital rules applicable to Bancorp and Bank. The rules implemented the regulatory capital reforms of the Basel Committee on Banking Supervision reflected in “Basel III: A Global Regulatory Framework for More Resilient Banks and Banking Systems” (“Basel III”) and changes required by the Dodd-Frank Act. The Basel III regulatory capital reforms became effective for Bancorp and Bank on January 1, 2015, and included new minimum risk-based capital and leverage ratios. The minimum capital level requirements applicable to bank holding companies and banks subject to the rules are:

|

● |

a common equity Tier 1 capital ratio of 4.5%, |

|

● |

a Tier 1 risk-based capital ratio of 6% (increased from 4%), |

|

● |

a total risk-based capital ratio of 8% (unchanged from previous rules), and |

|

● |

a Tier 1 leverage ratio of 4% for all institutions. |

The rules also established a “capital conservation buffer” of 2.5%, to be phased in over three years, above the regulatory minimum risk-based capital ratios, and will result in the following minimum ratios once the capital conservation buffer is fully phased in:

|

● |

a common equity Tier 1 risk-based capital ratio of 7.0%, |

|

● |

a Tier 1 risk-based capital ratio of 8.5%, and |

|

● |

a total risk-based capital ratio of 10.5%. |

The capital conservation buffer requirement began being phased in January 2016 at 0.625% of risk-weighted assets and will increase each year until fully implemented in January 2019. An institution will be subject to limitations on paying dividends, engaging in share repurchases and paying discretionary bonuses if capital levels fall below minimum levels plus the buffer amounts. These limitations establish a maximum percentage of eligible retained income that could be utilized for such actions.

Under these rules, Tier 1 capital generally consists of common stock (plus related surplus) and retained earnings, limited amounts of minority interest in the form of additional Tier 1 capital instruments, and non-cumulative preferred stock and related surplus, subject to certain eligibility standards, less goodwill and other specified intangible assets and other regulatory deductions. The definition of Tier 2 capital is generally unchanged for most banking organizations, subject to certain new eligibility criteria.

Common equity Tier 1 capital generally consists of common stock, additional paid-in capital and retained earnings plus limited amounts of minority interest in the form of common stock, less goodwill and other specified intangible assets and other regulatory deductions.

The rules allowed banks and their holding companies with less than $250 billion in assets a one-time opportunity to opt-out of a requirement to include unrealized gains and losses in accumulated other comprehensive income in their capital calculation. Bancorp opted-out of this requirement.

As of December 31, 2017, Bancorp met the requirements to be considered well-capitalized and is not subject to limitations due to the capital conservation buffer.

Available Information

Bancorp files reports with the SEC including the Annual Report on Form 10-K, quarterly reports on Form 10-Q, current event reports on Form 8-K, and proxy statements, as well as any amendments to those reports. The public may read and copy any materials the Registrant files with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at http://www.sec.gov. Bancorp’s Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to section 13(a) or 15(d) of the Exchange Act are also accessible at no cost on Bancorp’s web site at http://www.syb.com after they are electronically filed with the SEC.

|

Item 1A. |

Risk Factors |

Investment in Bancorp’s common stock involves risk, and Bancorp’s profitability and success may be affected by a number of factors including those discussed below.

Financial condition and profitability depend significantly on local and national economic conditions.

The Company’s success depends on general economic conditions both locally and nationally. Most of Bancorp’s customers are in the Louisville, Indianapolis, and Cincinnati metropolitan areas. Compared to regional or national financial institutions, Bancorp is less able to spread the risks of unfavorable local economic conditions across a large number of diversified economies. Some of Bancorp’s customers are directly impacted by the local economy while others have more national or global business dealings. Deterioration in the quality of the credit portfolio could have a material adverse effect on financial condition, results of operations, and ultimately capital.

Financial condition and profitability depend on real estate values in the Company’s market area.

Bancorp offers a variety of secured loans, including commercial lines of credit, commercial term loans, real estate, construction, home equity, consumer and other loans. Bancorp’s loans are secured by real estate (both residential and commercial) primarily in Bancorp’s market areas. In instances where borrowers are unable to repay their loans and there has been deterioration in the value of the loan collateral, Bancorp could experience higher loan losses which could have a material adverse effect on financial condition, and results of operations.

If actual loan losses are greater than Bancorp’s assumption for loan losses, earnings could decrease.

Bancorp’s loan customers may not repay their loans according to the terms of these loans, the collateral securing the payment of these loans may be insufficient to ensure repayment and the wealth of guarantors providing guarantees to support these loans may be insufficient to aid in the repayment of these loans. Accordingly, Bancorp might experience significant credit losses which could have a material adverse effect on operating results. Bancorp makes various assumptions and judgments about the collectability of the loan portfolio, including the creditworthiness of borrowers and the value of collateral for repayment of many loans. In determining the adequacy of the allowance for loan losses, Bancorp considers, among other factors, an evaluation of economic conditions and Bancorp’s loan loss experience. If Bancorp’s assumptions prove to be incorrect or economic problems are worse than projected, the current allowance may not be sufficient to cover loan losses and adjustments may be necessary to allow for different economic conditions or adverse developments in the loan portfolio. Such additions to the allowance, if necessary, could have a material adverse impact on financial results.

Federal and state regulators annually review Bancorp’s allowance for loan losses and may require an increase in the provision for loan losses or loan charge-offs. If regulatory agencies require any increase in the provision for loan losses or loan charge-offs for which Bancorp had not allocated, it would have a negative effect on financial results.

Fluctuations in interest rates could reduce profitability.

Bancorp’s primary source of income is from the net interest spread, the difference between interest earned on loans and investments and the interest paid on deposits and borrowings. Bancorp expects to periodically experience gaps in interest rate sensitivities of Bancorp’s assets and liabilities, meaning that either interest-bearing liabilities will be more sensitive to changes in market interest rates than interest-earning assets, or vice versa. In either event, if market interest rates should move contrary to Bancorp’s position, this gap will work against Bancorp and earnings will be negatively affected.

Many factors affect fluctuation of market interest rates, including, but not limited to the following:

|

● |

inflation or deflation |

|

● |

recession |

|

● |

a rise in unemployment |

|

● |

tightening money supply |

|

● |

international disorder and instability in foreign financial markets |

|

● |

the Federal Reserve’s actions to control interest rates |

The Federal Reserve increased the overnight federal funds rate three times in 2017 which led to the prime lending rate increasing from 3.75% to 4.50%. Bancorp benefits from rates increasing as the majority of variable rate loans are tied to prime with a lesser amount tied to LIBOR. While variable rate loans have re-priced at higher rates Bancorp has largely held deposit rates unchanged. Deposit rates generally do not reprice as quickly as loans which positively affects earnings as rates rise in the short term. Market expectations for 2018 include three additional 25 bps federal funds rate increases. Bancorp recognizes that eventually deposit rates will be adjusted upward which poses a risk to earnings. Migration of deposits out of Bancorp, as customers pursue higher rates, could impact liquidity and earnings as Bancorp competes for deposits. Changes in the mix of deposits could result in increased average rates paid on deposits, and lower earnings to Bancorp. Bancorp’s asset-liability management strategy, which is designed to mitigate risk from changes in market interest rates, may not be able to prevent changes in interest rates from having a material adverse effect on Bancorp’s results of operations and financial condition. Bancorp’s most recent earnings simulation model estimated the impact of changing interest rates on earnings for the next 12 months indicates net interest income will decrease approximately 3% if interest rates immediately increase 200 basis points and decrease approximately 5% if rates decrease 200 basis points.

Bancorp is subject to funding risk.

Funding risk represents the dependence Bancorp has on large commercial deposit relationships. Approximately 40% of Bancorp’s total deposits are centralized in accounts with balances $500,000 or greater. Bancorp considers these deposits core funds as they represent long-standing relationships and are a testament to Bancorp’s commitment to partner with business clients by providing exemplary service and competitive products. A sudden shift in customer behavior within these deposits resulting in balances being reduced or moved out of the bank altogether could impact Bancorp’s ability to capitalize on growth opportunities and meet current obligations. Bancorp has secondary sources of funding to draw upon as needed but the cost of those funds would be higher than typical deposit accounts which would negatively impact the financial condition and results of operation.

Significant stock market volatility could negatively affect Bancorp’s financial results.

Income from wealth management and trust constitutes approximately 44% of non-interest income. Trust assets under management are expressed in terms of market value, and a significant portion of fee income is based upon those values. A large majority of wealth management and trust fees are based on market values which generally fluctuate with the overall capital markets.

Capital and credit markets experience volatility and disruption from time to time. These conditions place downward pressure on credit availability, credit worthiness and customers’ inclinations to borrow. Prolonged volatility or a significant disruption could negatively impact customers’ ability to seek new loans or to repay existing loans. The personal wealth of many borrowers and guarantors has historically added a source of financial strength to certain loans and would be negatively impacted by severe market declines. Sustained reliance on their personal assets to make loan payments would result in deterioration of their liquidity, and could result in loan defaults.

Competition with other financial institutions could adversely affect profitability.

Bancorp operates in a highly competitive industry that could become even more so as a result of earnings pressure of contending banks, legislative, regulatory and technological changes and continued consolidation. Bancorp faces vigorous competition in price and structure of financial products from banks and other financial institutions. In recent years, credit unions have expanded their lending mix and now compete heavily with banks in the commercial real estate market. Their high risk tolerance for fixed rate, long-term loans has adversely affected Bancorp’s net loan growth and results of operations. Bancorp also competes with other non-traditional providers of financial services, such as brokerage firms and insurance companies. As internet-based financial services continue to grow in acceptance, Bancorp must remain relevant as a place where consumers and businesses value personal service while competitors offer these services without human interaction. The variety of sources of competition may reduce or limit margins on banking services, reduce market share and adversely affect results of operations and financial condition. Bancorp’s growth and expansion may adversely affect customer perceptions of the community based, customer oriented service Bancorp provides, thus damaging Bancorp’s image in the market.

An extended disruption of vital infrastructure could negatively impact Bancorp’s business, results of operations, and financial condition.

Bancorp’s operations depend upon, among other things, infrastructure, including equipment and facilities. Extended disruption of vital infrastructure by fire, power loss, natural disaster, telecommunications failure, information systems breaches, terrorist activity or the domestic and foreign response to such activity, or other events outside of Bancorp’s control could have a material adverse impact on the financial services industry as a whole and on Bancorp’s business, results of operations and financial condition. Bancorp’s business continuity plan may not work as intended or may not prevent significant interruption of operations. Occurrence of any failures, interruptions, or security breaches of information systems could damage Bancorp’s reputation, result in loss of customer business, subject the Company to additional regulatory scrutiny, or expose Bancorp to civil litigation and possible financial liability, any of which could have an adverse effect on Bancorp’s financial condition and results of operation.

Security breaches or incidences of fraud could negatively impact Bancorp’s business, results of operations, and financial condition.

Bancorp’s assets which are at risk for cyber-attacks include financial assets and non-public information belonging to customers. Cyber security risks include cyber espionage, blackmail, ransom, theft, and corporate account takeovers. Bancorp employs many preventive and detective controls to protect its assets, and provides mandatory recurring information security training to all employees. Bancorp has invested in multiple preventative tools in an attempt to protect customers from cyber threats and corporate account takeover. Bancorp regularly provides educational information regarding cyber threats to customers. Bancorp utilizes multiple third-party vendors who have access to the Company’s assets via electronic media. While Bancorp requires third parties, many of whom are small companies, to have similar or superior controls in place there is no guarantee that a breach of information could occur. Activities of the Bank that subject Bancorp to risk of fraud by customers, employees, vendors, or members of the general public include ACH transactions, wire transactions, ATM transactions, checking transactions, and loan originations. Repeated incidences of fraud or a single large occurrence would adversely impact Bancorp’s reputation and results of operation.

Bancorp’s credit metrics are at historically strong levels.

During 2017, Bancorp’s solid asset quality metrics trended within a narrow range and exceeded solid benchmarks of the past several years to reach historically strong levels. Bancorp realizes that present asset quality metrics are exceptionally positive and, recognizing the cyclical nature of the lending business, the Company anticipates this trend will most likely normalize over time.

Bancorp’s accounting policies and methods are critical to how Bancorp reports its financial condition and results of operations. They require management to make estimates about matters that are uncertain.

Accounting policies and methods are fundamental to how Bancorp records and reports its financial condition and results of operations. Bancorp must exercise judgment in selecting and applying these accounting policies and methods so they comply with United States generally accepted accounting principles (“US GAAP”).

Bancorp has identified certain accounting policies as being critical because they require management’s judgment to ascertain the valuations of assets, liabilities, commitments and contingencies. A variety of factors could affect the ultimate value that is obtained either when earning income, recognizing an expense, recovering an asset, or reducing a liability. Bancorp has established detailed policies and control procedures intended to ensure these critical accounting estimates and judgments are well controlled and applied consistently.

The policies and procedures are intended to ensure that the process for changing methodologies occurs in an appropriate manner. Because of the uncertainty surrounding Bancorp’s judgments and the estimates pertaining to these matters, there can be no assurances that actual results will not differ from those estimates. See the “Critical Accounting Policies” in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for more information.

Bancorp operates in a highly regulated environment and may be adversely affected by changes to or lack of compliance with federal, state and local laws and regulations.

Bancorp is subject to extensive regulation, supervision and examination by federal and state banking authorities. Any change in applicable regulations or federal or state legislation could have a substantial impact on Bancorp and its operations. Additional legislation and regulations may be enacted or adopted in the future that could significantly affect Bancorp’s powers, authority and operations, which could have a material adverse effect on Bancorp’s financial condition and results of operations. If Bancorp’s policies, procedures and systems are deemed deficient, the Company would be subject to liability, including fines and regulatory actions, which may include restrictions on the ability to pay dividends and the requirement to obtain regulatory approvals to proceed with certain aspects of Bancorp’s business plan, including branching and acquisition plans.

Bancorp’s ability to stay current on technological changes in order to compete and meet customer demands is constantly being challenged.

The financial services industry is constantly undergoing rapid technological changes, with frequent introductions of new technology-driven products and services. Future success of Bancorp will depend, in part, upon its ability to address the needs of its customers by using technology to provide products and services that will satisfy customer demands for convenience, as well as to create additional operational efficiencies and greater privacy and security protection for customers and their personal information. Many of Bancorp’s competitors have substantially greater resources to invest in technological improvements. Bancorp may not be able to effectively implement new technology-driven products and services as quickly as competitors or be successful in marketing these products and services to its customers. Bancorp relies on third party providers for many of its technology-driven banking products and services. Some of these companies may be slow to respond with upgrades or enhancements to their products to keep pace with improvements in technology or the introduction of competing products. Failure to successfully keep pace with technological change affecting the financial services industry could impair Bancorp’s ability to effectively compete to retain or acquire new business and could have an adverse impact on its business, financial position, results of operations and liquidity.

Bancorp is dependent upon outside third parties for the processing and handling of the Company’s records and data.

Bancorp relies on software developed by third-party vendors to process various transactions. In some cases, Bancorp has contracted with third parties to run their proprietary software on the Company’s behalf. While Bancorp performs a review of controls instituted by the applicable vendors over these programs in accordance with industry standards and performs testing of user controls, the Company relies on the continued maintenance of controls by these third-party vendors, including safeguards over the security of client data. Bancorp may incur a temporary disruption in the Company’s ability to conduct business or process transactions, or incur reputational, if the third-party vendor fails to adequately maintain internal controls or institute necessary changes to systems. Such a disruption or breach of security could have a material adverse effect on Bancorp’s business. Further, if these third-party service providers experience difficulties, or should terminate their services, and the Company is unable to replace them on a timely basis, Bancorp’s business operations could be interrupted. If an interruption were to continue for a significant period of time, the Company’s business, financial condition and results of operations could be adversely affected.

Bancorp may not be able to attract and retain skilled people.

Bancorp’s success depends, in large part, on its ability to attract and retain key people. Competition for the best people in the industry and the markets in which Bancorp engages can be intense, and the Company may not be able to retain or hire the people wanted or needed. To attract and retain qualified employees, Bancorp must compensate them at market levels. If Bancorp is unable to continue to attract and retain qualified employees, or do so at rates necessary to maintain the Company’s competitive position, Bancorp’s performance, including the Company’s competitive position, could suffer, and, in turn, adversely affect Bancorp’s business, financial condition or results of operations.

Bancorp invests in partnerships that generate federal income tax savings and these may not continue.

Bancorp invests in certain partnerships that yield federal income tax credits resulting in higher net income for Bancorp. These transactions may also include lending to the developer, further enhancing the profitability of the transaction. These transactions typically involve a very limited number of counterparties. The availability and suitability of these transactions are not particularly predictable and may not continue to be favorable to Bancorp. The recently enacted income tax reform could result in fewer transactions and the extent to which federal income tax credits favorably effect Bancorp’s net income. Therefore the positive effect on Bancorp’s net income may not continue.

Changes in customer use of banks could adversely affect Bancorp’s financial condition and results of operation.

The rapid evolution of non-bank alternatives for initiation and completion of financial transactions puts Bancorp at risk of losing sources of revenue and funding. The ability of customers to pay bills, transfer funds, and purchase assets without utilizing the banking system could result in loss of fee income, deposits, and loans. If Bancorp is unable to continue timely development of competitive new products and services, its business, financial condition and results of operations could be adversely affected.

The Current Expected Credit Loss (CECL) accounting standard will result in a significant change in how Bancorp recognizes credit losses and may have a material impact on the Company’s financial condition or results of operations.

In June 2016, the Financial Accounting Standards Board issued an accounting standard update, “Financial Instruments-Credit Losses (Topic 326), Measurement of Credit Losses on Financial Instruments,” which replaces the current “incurred loss” model for recognizing credit losses with an “expected loss” model. Whereas the incurred loss model delays recognition of loss on financial instruments until it is probable a loss has occurred, the expected loss model will necessitate recognizing a loss at the time the loan is first added to the balance sheet. As result of this differing methodology, Bancorp expects the adoption of the CECL model will materially affect the determination of the allowance for loan losses and could require a significant increase to the allowance. Any material increase to the required level of loan loss allowance could adversely affect Bancorp’s business, financial condition, and results of operation.

The CECL standard will become effective for Bancorp for fiscal years beginning after December 15, 2019 and for interim periods beginning with the first quarter of 2020. While the impact of implementing the CECL model cannot be quantified at this time, Bancorp expects to recognize a one-time cumulative-effect adjustment to the allowance for loan losses and stockholders’ equity in the first quarter of 2020, consistent with interagency guidance issued in 2016.

|

Item 1B. |

Unresolved Staff Comments |

Bancorp has no unresolved SEC staff comments.

|

Item 2. |

Properties |

The principal offices of Bancorp are located at 1040 East Main Street, Louisville, Kentucky. Bancorp’s operations center is at a separate location. In addition to the main office complex and the operations center, Bancorp owned 20 branch properties at December 31, 2017, two of which are located on leased land. At that date, Bancorp also leased 17 branch facilities as well as its wealth management and trust facility. Of the 37 banking locations, 28 are located in the Louisville Metropolitan Statistical Area (“MSA”), four are located in the Indianapolis MSA and five are located in the Cincinnati MSA. See Notes 6 and 19 to Bancorp’s consolidated financial statements for the year ended December 31, 2017, for additional information relating to amounts invested in premises and equipment and lease commitments.

|

Item 3. |

Legal Proceedings |

See Note 19 to Bancorp’s consolidated financial statements for the year ended December 31, 2017, for information relating to legal proceedings.

|

Item 4. |

Mine Safety Disclosures |

Not applicable.

Executive Officers of the Registrant

The following table lists the names and ages as of December 31, 2017 of all current executive officers of Bancorp and the Bank. Each executive officer is appointed by Bancorp’s Board of Directors to serve at the discretion of the Board.

There is no arrangement or understanding between any executive officer of Bancorp or the Bank and any other person(s) pursuant to which he/she was or is to be selected as an officer.

|

Name and Age |

Position and Offices |

|

|

David P. Heintzman |

Chairman of the Board of Directors and Chief Executive Officer of Bancorp and the Bank |

|

|

James A. Hillebrand |

President and Director of Bancorp and the Bank |

|

|

Kathy C. Thompson |

Senior Executive Vice President and Director of Bancorp and the Bank |

|

|

Nancy B. Davis |

Executive Vice President, Treasurer and Chief Financial Officer of Bancorp and the Bank |

|

|

William M. Dishman III |

Executive Vice President and Chief Risk Officer of the Bank |

|

|

Philip S. Poindexter |

Executive Vice President and Chief Lending Officer of the Bank |

|

|

T. Clay Stinnett |

Executive Vice President and Chief Strategic Officer of Bancorp and the Bank |

|

|

Michael J. Croce |

Executive Vice President and Director of Retail Banking of the Bank |

Mr. Heintzman was appointed Chairman and Chief Executive Officer in January 2006. Prior thereto, he served as President of Bancorp and the Bank since 1992. Mr. Heintzman joined the Bank in 1985.

Mr. Hillebrand was appointed President in July 2008. Prior thereto, he served as Executive Vice President and Director of Private Banking of the Bank since 2005. From 2000 to 2004, he served as Senior Vice President of Private Banking. Mr. Hillebrand joined the Bank in 1996.

Ms. Thompson was appointed Senior Executive Vice President in January 2006. Prior thereto, she served as Executive Vice President of Bancorp and the Bank. She joined the Bank in 1992 and is Manager of the Wealth Management and Trust Department.

Ms. Davis was appointed Executive Vice President of Bancorp and the Bank in 1999 and Chief Financial Officer in 1993. She joined the Bank in 1991.

Mr. Dishman joined the Bank as Executive Vice President and Chief Risk Officer in February 2009.

Mr. Poindexter was appointed Chief Lending Officer in July 2008. Prior thereto, he served as Executive Vice President and Director of Commercial Banking. Mr. Poindexter joined the Bank in 2004.

Mr. Stinnett was appointed Executive Vice President and Chief Strategic Officer in February 2011. Prior thereto, he served as Senior Vice President and Chief Strategic Officer since 2005. Mr. Stinnett joined the Bank in 2000.

Mr. Croce was appointed Executive Vice President and Director of Retail Banking in July 2014. Prior thereto, he served as Senior Vice President and Division Manager of Business Banking. Mr. Croce joined the Bank in 2004.

|

Item 5. |

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Bancorp’s common stock is traded on the NASDAQ Global Select Market under the ticker symbol SYBT. The table below sets forth the quarterly high and low market closing prices of Bancorp’s common stock and dividends declared per share. In April 2016, Bancorp declared a 3 for 2 stock split which was effected as a 50% stock dividend. Share and per share information has been adjusted for this split. The payment of dividends by the Bank to Bancorp is subject to the restriction described in Note 18 to the consolidated financial statements. Management believes that Bancorp will continue to generate adequate earnings to continue to pay dividends on a quarterly basis. On December 31, 2017, Bancorp had approximately 1,600 shareholders of record, and approximately 5,300 beneficial owners holding shares in nominee or “street” name.

|

2017 |

2016 |

|||||||||||||||||||||||

|

Cash Dividends |

Cash Dividends |

|||||||||||||||||||||||

|

Quarter |

High |

Low |

Declared |

High |

Low |

Declared |

||||||||||||||||||

|

First |

$ | 47.50 | $ | 39.25 | $ | 0.19 | $ | 26.09 | $ | 23.27 | $ | 0.17 | ||||||||||||

|

Second |

43.75 | 36.20 | 0.20 | 29.03 | 24.55 | 0.18 | ||||||||||||||||||

|

Third |

40.00 | 32.25 | 0.20 | 33.25 | 27.52 | 0.18 | ||||||||||||||||||

|

Fourth |

41.60 | 36.50 | 0.21 | 46.95 | 32.93 | 0.19 | ||||||||||||||||||

The following table shows information relating to the repurchase of shares of common stock by Bancorp during the three months ended December 31, 2017.

|

Total number of |

Average price paid per share |

Total number of shares purchased as part of publicly announced plan |

Maximum number of shares that may yet be purchased under the plan |

|||||||||||||

|

October 1-October 31 |

2,095 | $ | 38.97 | – | – | |||||||||||

|

November 1-November 30 |

4,300 | 38.58 | – | – | ||||||||||||

|

December 1-December 31 |

748 | 38.02 | – | – | ||||||||||||

|

Total |

7,143 | $ | 38.64 | – | – | |||||||||||

Activity represents shares of stock withheld to satisfy employee tax obligations due upon the exercise of stock appreciation rights, on lapsed shares of restricted stock and on performance stock unit awards. Bancorp does not have an active stock repurchase program.

The following performance graphs and data shall not be deemed filed for purposes of Section 18 of the Securities Exchange Act of 1934 or otherwise subject to the liabilities of that section, nor shall it be deemed soliciting material or subject to Regulation 14A of the Exchange Act or incorporated by reference in any filing under the Exchange Act or the Securities Act of 1933, except as shall be expressly set forth by specific reference in such filing.

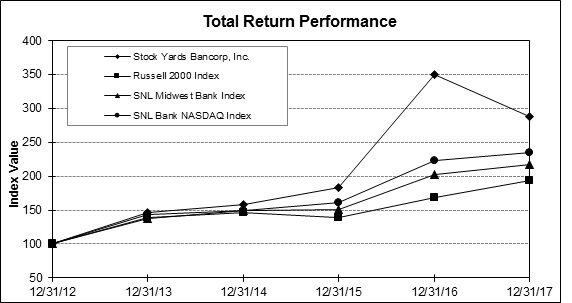

The first graph below compares performance of Bancorp Common Stock to the Russell 2000 index, the SNL NASDAQ Bank index and the SNL Midwest Bank index for Bancorp’s last five fiscal years. The graph assumes the value of the investment in Bancorp Common Stock and in each index was $100 at December 31, 2012 and that all dividends were reinvested.

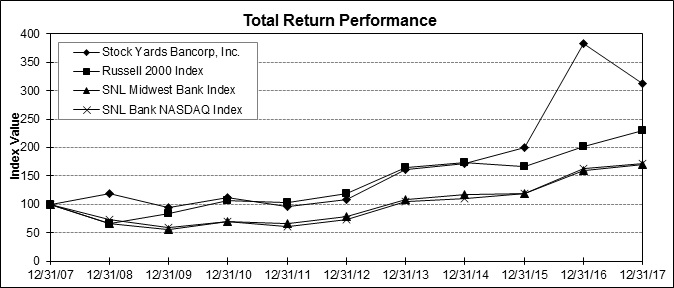

In addition to the five-year period required by the SEC, the ten-year period is presented because it provides additional perspective, and Bancorp management believes that longer-term performance is of greater interest. The ten-year graph assumes the value of the investment in Bancorp Common Stock and in each index was $100 at December 31, 2007 and that all dividends were reinvested.

|

Period Ending |

||||||||||||||||||||||||

|

Index |

12/31/12 |

12/31/13 |

12/31/14 |

12/31/15 |

12/31/16 |

12/31/17 |

||||||||||||||||||

|

Stock Yards Bancorp, Inc. |

$ | 100.00 | $ | 146.87 | $ | 157.88 | $ | 183.76 | $ | 350.33 | $ | 287.39 | ||||||||||||

|

Russell 2000 Index |

100.00 | 138.82 | 145.62 | 139.19 | 168.85 | 193.58 | ||||||||||||||||||

|

SNL Midwest Bank Index |

100.00 | 136.91 | 148.84 | 151.10 | 201.89 | 216.95 | ||||||||||||||||||

|

SNL Bank NASDAQ Index |

100.00 | 143.73 | 148.86 | 160.70 | 222.81 | 234.58 | ||||||||||||||||||

|

Period Ending |

||||||||||||||||||||||||||||||||||||||||||||

|

Index |

12/31/07 |

12/31/08 |

12/31/09 |

12/31/10 |

12/31/11 |

12/31/12 |

12/31/13 |

12/31/14 |

12/31/15 |

12/31/16 |

12/31/17 |

|||||||||||||||||||||||||||||||||

|

Stock Yards Bancorp, Inc. |

$ | 100.00 | $ | 118.05 | $ | 94.46 | $ | 111.79 | $ | 96.62 | $ | 109.17 | $ | 160.34 | $ | 172.37 | $ | 200.62 | $ | 382.47 | $ | 312.04 | ||||||||||||||||||||||

|

Russell 2000 Index |

100.00 | 66.21 | 84.20 | 106.82 | 102.36 | 119.09 | 165.33 | 173.42 | 165.76 | 201.08 | 230.54 | |||||||||||||||||||||||||||||||||

|

SNL Midwest Bank Index |

100.00 | 65.79 | 55.75 | 69.23 | 65.39 | 78.71 | 107.76 | 117.15 | 118.92 | 158.90 | 170.75 | |||||||||||||||||||||||||||||||||

|

SNL Bank NASDAQ Index |

100.00 | 72.62 | 58.91 | 69.51 | 61.67 | 73.51 | 105.65 | 109.42 | 118.12 | 163.78 | 172.43 | |||||||||||||||||||||||||||||||||

|

Item 6. |

Selected Financial Data |

Selected Consolidated Financial Data

|

(In thousands except |

Years ended December 31 |

|||||||||||||||||||

|

per share data and ratios) |

2017 |

2016 |

2015 |

2014 |

2013 |

|||||||||||||||

|

Income statement data |

||||||||||||||||||||

|

Interest income |

$ | 110,849 | $ | 102,172 | $ | 93,170 | $ | 89,087 | $ | 86,464 | ||||||||||

|

Interest expense |

7,246 | 4,918 | 4,852 | 5,330 | 9,166 | |||||||||||||||

|

Net interest income |

103,603 | 97,254 | 88,318 | 83,757 | 77,298 | |||||||||||||||

|

Provision (credit) for loan losses |

2,550 | 3,000 | 750 | (400 | ) | 6,550 | ||||||||||||||

|

Non-interest income |

45,120 | 43,537 | 39,950 | 39,155 | 39,002 | |||||||||||||||

|

Non-interest expenses |

90,991 | 81,520 | 73,398 | 73,209 | 71,352 | |||||||||||||||

|

Income before income taxes |

55,182 | 56,271 | 54,120 | 50,103 | 38,398 | |||||||||||||||

|

Income tax expense |

17,139 | 15,244 | 16,933 | 15,281 | 11,228 | |||||||||||||||

|

Net income |

$ | 38,043 | $ | 41,027 | $ | 37,187 | $ | 34,822 | $ | 27,170 | ||||||||||

|

Per share data |

||||||||||||||||||||

|

Net income, basic |

$ | 1.69 | $ | 1.84 | $ | 1.68 | $ | 1.59 | $ | 1.27 | ||||||||||

|

Net income, diluted |

1.66 | 1.80 | 1.65 | 1.57 | 1.26 | |||||||||||||||

|

Cash dividends declared |

0.80 | 0.72 | 0.64 | 0.59 | 0.54 | |||||||||||||||

|

Book value |

14.71 | 13.88 | 12.80 | 11.75 | 10.47 | |||||||||||||||

|

Market value |

37.70 | 46.95 | 25.19 | 22.23 | 21.28 | |||||||||||||||

|

Weighted average common and common equivalent shares - diluted |

22,983 | 22,792 | 22,459 | 22,144 | 21,530 | |||||||||||||||

|

Balance sheet data |

||||||||||||||||||||

|

Total assets |

$ | 3,239,646 | $ | 3,039,481 | $ | 2,816,801 | $ | 2,563,868 | $ | 2,389,262 | ||||||||||

|

Loans |

2,409,570 | 2,305,375 | 2,033,007 | 1,868,550 | 1,721,350 | |||||||||||||||

|

Allowance for loan losses |

24,885 | 24,007 | 22,441 | 24,920 | 28,522 | |||||||||||||||

|

Available for sale securities |

574,524 | 570,074 | 565,876 | 513,056 | 490,031 | |||||||||||||||

|

Deposits |

2,578,295 | 2,520,548 | 2,371,702 | 2,123,627 | 1,980,937 | |||||||||||||||

|

Federal funds purchased |

161,352 | 47,374 | 22,477 | 47,390 | 55,295 | |||||||||||||||

|

Federal Home Loan Bank advances |

49,458 | 51,075 | 43,468 | 36,832 | 34,329 | |||||||||||||||

|

Stockholders’ equity |

333,644 | 313,872 | 286,519 | 259,895 | 229,444 | |||||||||||||||

|

Average balances |

||||||||||||||||||||

|

Stockholders’ equity |

$ | 327,798 | $ | 304,151 | $ | 274,451 | $ | 245,425 | $ | 220,107 | ||||||||||

|

Assets |

3,037,581 | 2,886,396 | 2,573,901 | 2,398,430 | 2,232,868 | |||||||||||||||

|

Federal Home Loan Bank advances |

50,300 | 45,455 | 41,041 | 35,709 | 32,518 | |||||||||||||||

|

Long-term debt |

– | – | – | – | 30,477 | |||||||||||||||

|

Selected ratios |

||||||||||||||||||||

|

Return on average assets |

1.25 | % | 1.42 | % | 1.44 | % | 1.45 | % | 1.22 | % | ||||||||||

|

Return on average stockholders’ equity |

11.61 | 13.49 | 13.55 | 14.19 | 12.34 | |||||||||||||||

|

Average stockholders’ equity to average assets |

10.79 | 10.54 | 10.66 | 10.23 | 9.86 | |||||||||||||||

|

Net interest rate spread |

3.52 | 3.51 | 3.59 | 3.67 | 3.59 | |||||||||||||||

|

Net interest rate margin, fully tax-equivalent |

3.63 | 3.59 | 3.67 | 3.75 | 3.74 | |||||||||||||||

|

Efficiency ratio |

60.86 | 57.56 | 56.81 | 59.09 | 60.82 | |||||||||||||||

|

Non-performing loans to total loans |

0.31 | 0.29 | 0.44 | 0.64 | 1.33 | |||||||||||||||

|

Non-performing assets to total assets |

0.31 | 0.39 |

|

0.48 |

|

0.70 |

|

1.19 | ||||||||||||

|

Net charge offs to average loans |

0.07 | 0.07 | 0.17 | 0.18 | 0.60 | |||||||||||||||

|

Allowance for loan losses to total loans |

1.03 | 1.04 |

|

1.10 |

|

1.33 |

|

1.66 | ||||||||||||

Share and per share information has been adjusted to reflect the April 2016 3 for 2 stock-split effected in the form of a 50% stock dividend.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Financial Section Summary

The financial section of this Form 10-K includes management’s discussion and analysis, consolidated financial statements, and the notes to those financial statements. Bancorp has prepared the following summary to assist in your review of the financial section. It is designed to give you an overview of Stock Yards Bancorp, Inc. and summarize some of the more important activities and events that occurred during 2017. Share and per share information has been adjusted to reflect the April 2016 3 for 2 stock-split which was effected in the form of a 50% stock dividend.

The financial section includes the following:

Management’s discussion and analysis, or MD&A provides information regarding the consolidated financial condition and results of operations of Bancorp. It contains management’s view about industry trends, risks, uncertainties, accounting policies that Bancorp views as critical in light of its business, results of operations including discussion of the key performance drivers, financial position, cash flows, commitments and contingencies, important events, transactions that have occurred over the last three years, and forward-looking information, as appropriate.

Financial statements include Consolidated Balance Sheets as of the end of the last two years, and Consolidated Statements of Income, Comprehensive Income, Changes in Stockholders’ Equity, and Cash Flows, for each of the last three years. Bancorp’s financial statements are prepared in accordance with US GAAP.

Notes to the financial statements provide insight into, and are an integral part of, the financial statements. These notes contain explanations of significant accounting policies, details about certain captions on the financial statements, information about significant events or transactions that have occurred, discussions about legal proceedings, commitments and contingencies, and selected financial information relating to business segments. The notes to the financial statements also are prepared in accordance with US GAAP.

Reports related to the financial statements and internal controls over financial reporting include the following:

|

● |

A report from KPMG LLP, an independent registered public accounting firm, which includes their opinion on the presentation of Bancorp’s consolidated financial statements in conformity with US GAAP based on their audits; |

|

● |

A report from management indicating Bancorp’s responsibility for financial reporting and the financial statements; |

|

● |

A report from management indicating Bancorp’s responsibility for the system of internal control over financial reporting, including an assessment of the effectiveness of those controls; and |

|

● |

A report from KPMG LLP, which includes their opinion on the effectiveness of Bancorp’s internal control over financial reporting. |

Our Business

Stock Yards Bancorp, Inc. was incorporated in 1988, and its business is substantially the same as that of its wholly owned subsidiary, Stock Yards Bank & Trust Company. The Bank has operated continuously since it opened in 1904. The Bank conducted business at one location for 85 years and began branching in 1989. At December 31, 2017, the Bank had 28 full service banking locations in the Louisville MSA, 4 full service banking locations in the Indianapolis MSA, and 5 full service banking locations in the Cincinnati MSA. Bancorp’s focus on flexible, attentive customer service has been key to its growth and profitability. The wide range of services provided by wealth management and trust, investment product sales, and mortgage origination helps support the corporate philosophy of capitalizing on full service customer relationships.

Forward-Looking Statements

This report contains forward-looking statements under the Private Securities Litigation Reform Act that involve risks and uncertainties. These forward-looking statements may be identified by the use of words such as “expect”, “anticipate”, “plan”, “foresee”, “believe” or other words with similar meaning. Although Bancorp believes assumptions underlying forward-looking statements contained herein are reasonable, any of these assumptions could be inaccurate. Factors that could cause actual results to differ from results discussed in forward-looking statements include, but are not limited to: economic conditions both generally and more specifically in markets in which Bancorp and its subsidiary operate; competition for Bancorp’s customers from other providers of financial services; government legislation and regulation which change from time to time and over which Bancorp has no control; changes in interest rates; material unforeseen changes in liquidity, deterioration in the real estate market, results of operations or financial condition of Bancorp’s customers; or other risks detailed in Bancorp’s filings with the Securities and Exchange Commission and Item 1A of this Form 10-K, all of which are difficult to predict and many of which are beyond the control of Bancorp.

Critical Accounting Policies

Bancorp has prepared consolidated financial information in this report in accordance with US GAAP. In preparing the consolidated financial statements, Bancorp makes estimates and assumptions that affect the reported amount of assets and liabilities, disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenue and expenses during the reporting period. There can be no assurances that actual results will not differ from those estimates.

Management has identified the accounting policy related to the allowance and provision for loan losses as critical to the understanding of Bancorp’s results of operations and discussed this conclusion with the Audit Committee of the Board of Directors. Since the application of this policy requires significant management assumptions and estimates, it could result in materially different amounts to be reported if conditions or underlying circumstances were to change. The provision for loan losses reflects an allowance methodology driven by risk ratings, historical losses, specific loan loss allocations, and qualitative factors. Assumptions include many factors such as changes in borrowers’ financial condition which can change quickly or historical loss ratios related to certain loan portfolios which may or may not be indicative of future losses. In the first quarter of 2017, Bancorp extended the historical period used to capture Bancorp’s historical loss ratios from 24 quarters to 28 quarters. This extension of the historical period was applied to all classes and segments of our portfolio. The expansion of the look-back period for the quantitative historical loss rate caused us to review the overall methodology for the qualitative factors to ensure we were appropriately capturing the risk not addressed in the quantitative historical loss rate. Management believes the extension of the look-back period is appropriate to capture the impact of a full economic cycle and more accurately represents the current level of risk inherent in the loan portfolio.

The quarterly allowance calculation has both quantitative and qualitative factors which support the total balance of the allowance at period end. The effect of the extension of the look-back period to 28 quarters in the first quarter of 2017 resulted in a net decrease to the calculated quantitative portion of the allowance, but this was more than offset by an increase to the qualitative factors. The net impact of the extension of the look-back period was an increase in the allowance during the first quarter of 2017 of approximately $474 thousand. The change in methodology was consistent with management’s judgment regarding the risk in the loan portfolio and consistent with internal analysis showing continued strong asset quality related not only in the Company’s loan portfolio, but the Bank’s peer group as well, validating the continuation of the current economic cycle and thus the reasoning to extend the look-back period. Management will continue to evaluate the appropriateness of the look-back period based on the status of the economic cycle. To the extent that management’s assumptions prove incorrect, results from operations could be materially affected by a higher or lower provision for loan losses. The accounting policy related to the allowance for loan losses is applicable to the commercial banking segment of Bancorp. The impact and any associated risks related to this policy on Bancorp’s business operations are discussed in the “Allowance for Loan Losses” section below.

The allowance for loan losses is management’s estimate of probable losses inherent in the loan portfolio as of the balance sheet date. Loan losses are charged against the allowance when management believes the uncollectibility of a loan balance is confirmed. Subsequent recoveries, if any, are credited to the allowance.

Bancorp’s allowance calculation includes allocations to loan portfolio segments at December 31, 2017 for qualitative factors including, among other factors, local economic and business conditions in each of our primary markets, quality and experience of lending staff and management, exceptions to lending policies, levels of and trends in past due loans and loan classifications, concentrations of credit such as collateral type, trends in portfolio growth, trends in value of underlying collateral for collateral-dependent loans, effect of other external factors such as the national economic and business trends, quality and depth of the loan review function, and management’s judgement of current trends and potential risks. Bancorp utilizes the sum of all allowance amounts derived as described above as the appropriate level of allowance for loan and lease losses. Changes in criteria used in this evaluation or availability of new information could cause the allowance to be increased or decreased in future periods. In addition, bank regulatory agencies, as part of their examination process, may require adjustments to the allowance for loan and lease losses based on their judgments and estimates.

Overview of 2017

The following discussion should be read in conjunction with Bancorp’s consolidated financial statements and accompanying notes and other schedules presented elsewhere in this report.

In 2017, Bancorp completed another strong year of revenue, asset, and deposit growth. Total revenue, comprising net interest income and non-interest income, increased 6% to $148.7 million in 2017 from $140.8 million in 2016. Net income for the year ended December 31, 2017, was $38.0 million or $1.66 per diluted share compared with $41.0 million or $1.80 per diluted shares for 2016. Net income for the fourth quarter and full year 2017 reflected a non-cash charge of $5.9 million or $0.25 per diluted share to revalue the Company’s net deferred tax asset in connection with the Tax Cuts and Jobs Act (tax reform) enacted on December 22, 2017.

Key aspects of the Company’s performance for the year included:

|

● |

Solid loan growth during 2017, which increased the Company’s loan portfolio nearly 5% for 2017; |

|

● |

Consistently strong net interest margin; |

|

● |

Credit quality remained at historically strong levels; |

|

● |

Continued growth in fee income, led by the Wealth Management and Trust Group; and |

|

● |

Solid returns on average assets and equity of 1.25% and 11.61%, respectively, despite the negative impact of 0.20% on return on average assets and 1.81% on return on average equity due to the year-end remeasurement charge noted above. |

As is the case with most banks, the primary source of Bancorp’s revenue is net interest income and fees from various financial services provided to customers. Net interest income is the difference between interest income earned on loans, investment securities and other interest earning assets less interest expense on deposit accounts and other interest bearing liabilities. Loan growth and interest rates earned on those loans are critical to overall profitability. Similarly, deposit growth is crucial to funding loans and rates paid on deposits directly impact profitability. New business volume is influenced by economic factors including market interest rates, business spending, consumer confidence and competitive conditions within the marketplace.

As a result of near-record loan production and sustained utilization of available lines of credit, Bancorp was able to overcome elevated loan pre-payment activity and increase the loan portfolio $104 million, or almost 5%, to $2.4 billion as of December 31, 2017. Increasing average rates on interest earning assets, along with the impact of increased volumes on loans contributed to higher interest income for 2017, as interest income increased $8.6 million, or 8%, over the same period in 2016. Deposit growth during 2017, and more significantly higher funding costs on deposits and borrowings, resulted in an increase in interest expense of $2.3 million or 47%, year over year. Bancorp benefited in recent years from historically low costs of funding, so that even a modest increase in interest expense results in a significant percentage change over prior periods. Net interest margin in 2017 increased to 3.63%, as compared with 3.59% in 2016 despite the continuing pressure of a highly competitive lending environment and increasing rates paid on deposits.

Total non-interest income increased $1.6 million, or 4% in 2017, as compared with 2016, and represented 30% of total revenues, down slightly from 31% in 2016. Wealth management and trust department (WM&T) income, service charges on deposits, treasury management fees, and investment products fees all increased in 2017 over 2016, with the greatest dollar increase from WM&T. WM&T represents an important part of the relationship focused philosophy of the Company and, accordingly, income from the department represents approximately 45% of total non-interest income for the Bancorp. The magnitude of WM&T revenue distinguishes Bancorp from other community banks of similar asset size and although the 2017 increase was partially the result of a rising stock market during the year, it also represented a strong year for WM&T in terms of new clients added.

Higher non-interest expenses for 2017 were primarily the result of increased personnel and technology costs, associated with growth and operational support, and increased amortization and impairment charges for investments in tax credit partnerships as the Bancorp increased its commitment to customers pursuing tax-advantaged projects, primarily involving historical redevelopment. Bancorp’s efficiency ratio for 2017 of 60.9% was up from 57.6% in 2016.

For the year ended December 31, 2017, Bancorp recorded a $2.6 million provision for loan losses, compared with $3.0 million for the same period in 2016. The provision for loan losses represents a charge to earnings necessary to maintain an allowance for loan losses that, in management’s evaluation, is adequate to provide coverage for the inherent losses on outstanding loans. The decrease in the provision was a reflection of continued historically strong credit quality metrics. Bancorp’s allowance for loan losses was 1.03% of total loans at December 31, 2017, compared with 1.04% of total loans at December 31, 2016.

Bancorp’s effective tax rate increased to 31.1% in 2017 from 27.1% in 2016 due to the $5.9 million charge to remeasure Bancorp’s net deferred tax asset necessitated by tax reform. Bancorp anticipates an overall effective tax rate of approximately 17% in 2018. Bancorp invests in certain partnerships that yield federal income tax credits. The tax benefit of these investments exceeds the impairment charge associated with them, resulting in a positive impact on net income. In 2018, the Company expects a lower level of participation in tax-credit partnerships due to reduced investment opportunities.

In 2017 Bancorp adopted ASU 2016-09 “Compensation – Stock Compensation Improvements to Employee Share-Based Payment Accounting”. The new standard requires excess tax benefits and deficiencies related to share-based payment awards to be reflected in the statement of operations as a component of the provision for income taxes. In 2017 Bancorp recorded a benefit of $1.5 million for such tax benefits against the provision for income tax expense. Prior to adoption of ASU 2016-09, these tax benefits were recorded directly to additional paid-in capital.

As of December 31, 2017, the Company’s total equity to total assets was 10.30% compared with 10.33% at December 31, 2016. Tangible common equity (TCE), a non-GAAP measure, is a measure of a company’s capital which is useful in evaluating the quality and adequacy of capital. It is calculated by subtracting the value of intangible assets and any preferred equity from Bancorp’s stockholders’ equity. The ratio of tangible common equity to total tangible assets was 10.25% as of December 31, 2017, compared with 10.26% at December 31, 2016. See the Non-GAAP Financial Measures section for details on reconcilement to US GAAP measures.

Challenges for 2018 will include managing net interest margin, achieving continued loan growth, managing credit quality and adapting to technology changes and evolving customer behavior.

|

● |

Considering the increases in short-term interest rates implemented by the Federal Open Market Committee and with the expectation of additional increases in 2018, management anticipates that net interest margins will increase during the coming year. Although rising rates should have a positive effect on net interest margin, competitive pressures on rates for loans and deposits will likely result in a continued pressure on the net interest margin for 2018. Increased deposit rates will also negatively impact this expectation. |

|

● |

Bancorp’s goals for 2018 include net loan growth at a pace greater than that experienced in 2017. This will be impacted by competition, prevailing economic conditions, line of credit utilization and prepayments in the loan portfolio. Bancorp believes there is continued opportunity for loan growth in all three of its markets, and Bancorp’s ability to deliver attractive loan growth over the long-term is linked to Bancorp’s success. |

|

● |

Bancorp has been successful at gathering sufficient deposits to fund loan growth. While deposits in all market areas have grown, the most significant increases arose in the Louisville market. Bancorp will need to continue to increase deposits to support loan growth in all markets. |

|

● |

Bancorp derives significant non-interest income from fees earned from wealth management and trust services. Most of these fees are based upon the market value of assets under management (AUM). To continue growth of this income source Bancorp must attract new customers and retain existing customers. Bancorp believes there is opportunity for net growth in its three markets. Growth in market values of AUM and fees is also dependent upon positive returns in the overall capital markets. Bancorp has no control over market volatility. |

|

● |

Technological advances are consistently providing opportunities for Bancorp to consider potential new products and delivery channels. Bancorp’s customers’ demand for innovative and relevant products and services is expected to trend along with the changing technology. Bancorp will need to continue to make prudent investments in technology while managing associated risks so as to remain competitive with other financial service providers. |

The following sections provide more details on subjects presented in this overview.

Results of Operations

Net income was $38.0 million or $1.66 per share on a diluted basis for 2017 compared with $41.0 million or $1.80 per share for 2016 and $37.2 million or $1.65 per share for 2015.

Net income for 2017 was positively impacted by:

|

● |

a $6.3 million, or 7% increase in net interest income, and |

|

● |

a $1.6 million, or 4% increase in non-interest income, and |

|

● |

a $450 thousand, or 15% decrease in provision for loan losses. |

Net income for 2017 was negatively impacted by:

|

● |

an $9.5 million, or 12% increase in non-interest expense |

|

● |

a $1.9 million, or 12% increase in income tax. |

The following paragraphs provide a more detailed analysis of significant factors affecting operating results.

Net Interest Income