Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - LCNB CORP | lcnbform10-k12312017ex32.htm |

| EX-31.2 - EXHIBIT 31.2 - LCNB CORP | lcnbform10-k12312017ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - LCNB CORP | lcnbform10-k12312017ex311.htm |

| EX-23 - EXHIBIT 23 - LCNB CORP | lcnbform10-k12312017ex23.htm |

| EX-21 - EXHIBIT 21 - LCNB CORP | lcnbform10-k12312017ex21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

or

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______________________ to ______________________

Commission File Number 000-26121

LCNB Corp.

(Exact name of registrant as specified in its charter)

Ohio | 31-1626393 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

2 North Broadway, Lebanon, Ohio 45036

(Address of principal executive offices, including Zip Code)

(513) 932-1414

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

Title of Each Class | Name of each exchange on which registered | |

None | None | |

Securities registered pursuant to 12(g) of the Exchange Act:

COMMON STOCK, NO PAR VALUE

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

☒ Yes ☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

☐ Large accelerated filer | ☒ Accelerated filer |

☐ Non-accelerated filer (Do not check if a smaller reporting company) | ☐ Smaller reporting company |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☒ No

The aggregate market value of the registrant’s outstanding voting common stock held by nonaffiliates on June 30, 2017, determined using a per share closing price on that date of $20.00 as quoted on the NASDAQ Capital Market, was $192,316,000.

As of March 8, 2018, 10,026,203 common shares were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement included in the Notice of Annual Meeting of Shareholders to be held April 24, 2018, which Proxy Statement will be mailed to shareholders within 120 days from the end of the fiscal year ended December 31, 2017 are incorporated by reference into Part III.

LCNB CORP.

For the Year Ended December 31, 2017

TABLE OF CONTENTS

PART I | |

Item 1. Business | |

Item 1A. Risk Factors | |

Item 1B. Unresolved Staff Comments | |

Item 2. Properties | |

Item 3. Legal Proceedings | |

Item 4. Mine Safety Disclosures | |

PART II | |

Item 6. Selected Financial Data | |

Item 9A. Controls and Procedures | |

Item 9B. Other Information | |

PART III | |

Item 11. Executive Compensation | |

PART IV | |

-3-

PART I

Item 1. Business

FORWARD-LOOKING STATEMENTS

Certain statements made in this document regarding LCNB’s financial condition, results of operations, plans, objectives, future performance and business, are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. These forward-looking statements are identified by the fact they are not historical facts and include words such as “anticipate”, “could”, “may”, “feel”, “expect”, “believe”, “plan”, and similar expressions.

These forward-looking statements reflect management's current expectations based on all information available to management and its knowledge of LCNB’s business and operations. Additionally, LCNB’s financial condition, results of operations, plans, objectives, future performance and business are subject to risks and uncertainties that may cause actual results to differ materially. These factors include, but are not limited to:

1. | the success, impact, and timing of the implementation of LCNB’s business strategies; |

2. | LCNB’s ability to integrate future acquisitions, including the pending merger with Columbus First Bancorp, Inc., may be unsuccessful, or may be more difficult, time-consuming or costly than expected; |

3. | LCNB’s ability to obtain regulatory approvals of the proposed merger of LCNB with Columbus First Bancorp, Inc. on the proposed terms and schedule, and approval of the merger by the shareholders of LCNB or Columbus First Bancorp, Inc. may be unsuccessful; |

4. | LCNB may incur increased charge-offs in the future; |

5. | LCNB may face competitive loss of customers; |

6. | changes in the interest rate environment may have results on LCNB’s operations materially different from those anticipated by LCNB’s market risk management functions; |

7. | changes in general economic conditions and increased competition could adversely affect LCNB’s operating results; |

8. | changes in other regulations and government policies affecting bank holding companies and their subsidiaries, including changes in monetary policies, could negatively impact LCNB’s operating results; |

9. | LCNB may experience difficulties growing loan and deposit balances; |

10. | the current economic environment poses significant challenges for us and could adversely affect our financial condition and results of operations; |

11. | deterioration in the financial condition of the U.S. banking system may impact the valuations of investments LCNB has made in the securities of other financial institutions resulting in either actual losses or other than temporary impairments on such investments; |

12. | difficulties with technology or data security breaches, including cyberattacks, that could negatively affect LCNB's ability to conduct business and its relationships with customers, vendors, and others; and |

13. | government intervention in the U.S. financial system, including the effects of recent legislative, tax, accounting and regulatory actions and reforms, including the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), the Jumpstart Our Business Startups Act, the Consumer Financial Protection Bureau, the capital ratios of Basel III as adopted by the federal banking authorities and the Tax Cuts and Jobs Act. |

Forward-looking statements made herein reflect management's expectations as of the date such statements are made. Such information is provided to assist shareholders and potential investors in understanding current and anticipated financial operations of LCNB and is included pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. LCNB undertakes no obligation to update any forward-looking statement to reflect events or circumstances that arise after the date such statements are made.

-4-

DESCRIPTION OF LCNB CORP.'S BUSINESS

General Description

LCNB Corp., an Ohio corporation formed in December 1998, is a financial holding company headquartered in Lebanon, Ohio. Substantially all of the assets, liabilities and operations of LCNB Corp. are attributable to its wholly-owned subsidiary, LCNB National Bank (the "Bank"). LCNB Risk Management, Inc., a captive insurance agency, was incorporated in Nevada by LCNB Corp. during the second quarter 2017. LCNB Corp. and its subsidiaries are herein collectively referred to as “LCNB.” The predecessor of LCNB Corp., the Bank, was formed as a national banking association in 1877. On May 19, 1999, the Bank became a wholly-owned subsidiary of LCNB Corp.

On January 11, 2013, LCNB consummated a merger with First Capital Bancshares, Inc. (“First Capital”) in a stock and cash transaction valued at approximately $20.2 million. Immediately following the merger of First Capital into LCNB, Citizens National Bank (“Citizens National”), a wholly-owned subsidiary of First Capital, was merged into LCNB National Bank. At that time, Citizens National’s six full–service offices became offices of LCNB. Three of these offices are located in Chillicothe, Ohio and one office is located in each of Frankfort, Ohio, Clarksburg, Ohio, and Washington Court House, Ohio. The office in Clarksburg, Ohio was closed on January 24, 2017.

On January 24, 2014, LCNB purchased all of the outstanding stock of Eaton National Bank & Trust Co. ("Eaton National") from its holding company, Colonial Banc Corp., in a cash transaction totaling $24.75 million. Upon consummation of the transaction, Eaton National was merged into the Bank and its five offices became offices of the Bank. Two of these offices are located in Eaton, Ohio and one office is located in each of New Paris, Ohio, Lewisburg, Ohio, and West Alexandria, Ohio.

On April 30, 2015, LCNB consummated a merger with BNB Bancorp, Inc. (“BNB”) in a stock and cash transaction valued at approximately $13.5 million. Immediately following the merger of BNB into LCNB, Brookville National Bank ("Brookville National"), a wholly-owned subsidiary of BNB, was merged into LCNB National Bank. At that time, Brookville National's two offices, both located in Brookville, Ohio, became offices of LCNB. The office located on Hay Avenue in Brookville was closed on November 10, 2017.

On December 20, 2017, LCNB and Columbus First Bancorp, Inc. (“CFB”) entered into an Agreement and Plan of Merger pursuant to which CFB will be merged into LCNB in an all-stock transaction valued at $66.9 million. Immediately following the merger of CFB into LCNB, Columbus First Bank (“Columbus First”), a wholly-owned subsidiary of CFB, will be merged into the Bank. Columbus First operates one full-service office in Worthington, Ohio. This office will become a branch of the Bank after the merger. The transaction is expected to close in the second quarter of 2018, assuming shareholder approval by LCNB and CFB shareholders and all applicable governmental approvals have been received by that date and all other conditions precedent to the merger have been satisfied or waived.

The Bank is a full service community bank offering a wide range of commercial and personal banking services. Deposit services include checking accounts, NOW accounts, savings accounts, Christmas and vacation club accounts, money market deposit accounts, Lifetime Checking accounts (a senior citizen program), individual retirement accounts, and certificates of deposit. Additional supportive services include online banking, bill pay, mobile banking and telephone banking. Commercial customers also have both cash management and remote deposit capture products as potential options. Deposits of the Bank are insured up to applicable limits by the Deposit Insurance Fund, which is administered by the Federal Deposit Insurance Corporation (the “FDIC”).

Loan products offered include commercial and industrial loans, commercial and residential real estate loans, agricultural loans, construction loans, various types of consumer loans, and Small Business Administration loans. The Bank's residential mortgage lending activities consist primarily of loans for purchasing or refinancing personal residences, home equity lines of credit, and loans for commercial or consumer purposes secured by residential mortgages. Most fixed-rate residential real estate loans are sold to the Federal Home Loan Mortgage Corporation with servicing retained. Consumer lending activities include automobile, boat, home improvement and personal loans.

The Trust and Investment Management Division of the Bank provides complete trust administrative, estate settlement, and fiduciary services and also offers investment management of trusts, agency accounts, individual retirement accounts, and foundations/endowments.

-5-

Security brokerage services are offered by the Bank through arrangements with LPL Financial LLC, a registered broker/dealer. Licensed brokers offer a full range of investment services and products, including financial needs analysis, mutual funds, securities trading, annuities, and life insurance.

Other services offered include safe deposit boxes, night depositories, cashier's checks, bank-by-mail, ATMs, cash and transaction services, debit cards, wire transfers, electronic funds transfer, utility bill collections, notary public service, personal computer-based cash management services, 24 hour telephone banking, PC Internet banking, mobile banking, and other services tailored for both individuals and businesses.

The Bank is not dependent upon any one significant customer or specific industry. Business is not seasonal to any material degree.

The address of the main office of the Bank is 2 North Broadway, Lebanon, Ohio 45036; telephone (513) 932-1414.

Primary Market Area

The Bank considers its primary market area to consist of counties where it has a physical presence and neighboring counties, which includes Southwestern and South Central Ohio. At December 31, 2017, the Bank had:

• | 34 offices, including a main office in Warren County, Ohio and branch offices in Warren, Butler, Clinton, Clermont, Hamilton, Montgomery, Preble, Ross, and Fayette Counties, Ohio, |

• | a loan production office in Franklin County, Ohio, |

• | an Operations Center in Warren County, Ohio, |

• | and 38 ATMs. |

Competition

The Bank faces strong competition both in making loans and attracting deposits. The deregulation of the banking industry and the wide spread enactment of state laws that permit multi-bank holding companies as well as the availability of nationwide interstate banking has created a highly competitive environment for financial services providers. The Bank competes with other national and state banks, savings and loan associations, credit unions, finance companies, mortgage brokerage firms, realty companies with captive mortgage brokerage firms, mutual funds, insurance companies, brokerage and investment banking companies, and other financial intermediaries operating in its market and elsewhere, many of whom have substantially larger financial and managerial resources.

The Bank seeks to minimize the competitive effect of other financial institutions through a community banking approach that emphasizes direct customer access to the Bank's CEO/President and other officers in an environment conducive to friendly, informed, and courteous personal services. Management believes that the Bank is well positioned to compete successfully in its primary market area. Competition among financial institutions is based upon interest rates offered on deposit accounts, interest rates charged on loans and other credit and service charges, the quality and scope of the services rendered, the convenience of the banking facilities, and, in the case of loans to commercial borrowers, relative lending limits.

The ability to access and use technology is an increasingly competitive factor in the finance services industry. Technology relating to the delivery of financial services, the security and privacy of customer information, and the processing of information is evolving rapidly. LCNB must continually make technology investments to remain competitive in the finance services industry.

Management believes the commitment of the Bank to personal service, innovation, and involvement in the communities and primary market areas it serves, as well as its commitment to quality community banking service, are factors that contribute to its competitive advantage.

Supervision and Regulation

LCNB Corp., as a financial holding company, is regulated under the Bank Holding Company Act of 1956, as amended (the "Act"), and is subject to the supervision and examination of the Board of Governors of the Federal Reserve System (the "Federal Reserve Board").

-6-

The Bank is subject to the provisions of the National Bank Act. The Bank is subject to primary supervision, regulation and examination by the Office of the Comptroller of the Currency (the "OCC"). The Bank is also subject to the rules and regulations of the Board of Governors of the Federal Reserve System and the FDIC.

LCNB Corp. and the Bank are subject to an extensive array of banking laws and regulations that are intended primarily for the protection of the Bank's customers and depositors. These laws and regulations govern such areas as permissible activities, loans and investments, and rates of interest that can be charged on loans and reserves. LCNB and the Bank also are subject to general U.S. federal laws and regulations and to the laws and regulations of the State of Ohio. Set forth below are brief descriptions of selected laws and regulations applicable to LCNB and the Bank.

The Financial Reform, Recovery and Enforcement Act of 1989 ("FIRREA") provides that a holding company and its controlled insured depository institutions are liable for any loss incurred by the FDIC in connection with the default of any FDIC assisted transaction involving an affiliated insured bank or savings association.

The Federal Deposit Insurance Corporation Improvement Act of 1991 ("FDICIA") substantially revised the bank regulatory and funding provisions of the Federal Deposit Insurance Act and several other federal banking statutes. Among its many reforms, FDICIA, as amended:

1. | Required regulatory agencies to take "prompt corrective action" with financial institutions that do not meet minimum capital requirements; |

2. | Established five capital tiers: well capitalized, adequately capitalized, undercapitalized, significantly undercapitalized, and critically undercapitalized; |

3. | Imposed significant restrictions on the operations of a financial institution that is not rated well-capitalized or adequately capitalized; |

4. | Prohibited a depository institution from making any capital distributions, including payments of dividends or paying any management fee to its holding company, if the institution would be undercapitalized as a result; |

5. | Implemented a risk-based premium system; |

6. | Required an audit committee to be comprised of outside directors; |

7. | Required a financial institution with more than $500 million in total assets to issue annual, audited financial statements prepared in conformity with U.S. generally accepted accounting principles; and |

8. | Required a financial institution with more than $1 billion in total assets to document, evaluate, and report on the effectiveness of the entity's internal control system and required an independent public accountant to attest to management's assertions concerning the bank's internal control system. |

The members of an audit committee for banks with more than $1 billion in total assets must be independent of management. FDICIA does not relieve financial institutions that are public companies, such as LCNB, from internal control reporting and attestation requirements or audit committee independence requirements prescribed by the Sarbanes-Oxley Act of 2002 (see below).

The Gramm-Leach-Bliley Act, which amended the Bank Holding Company Act of 1956 and other banking related laws, was signed into law on November 12, 1999. The Gramm-Leach-Bliley Act repealed certain sections of the Glass-Steagall Act and substantially eliminated the barriers separating the banking, insurance, and securities industries. Effective March 11, 2000, qualifying bank holding companies could elect to become financial holding companies. Financial holding companies have expanded investment powers, including affiliating with securities and insurance firms and engaging in other activities that are "financial in nature or incidental to such financial activity," as defined in the act, or "complementary to a financial activity."

The Sarbanes-Oxley Act of 2002 ("SOX") became effective on July 30, 2002. The purpose of SOX is to strengthen accounting oversight and corporate accountability by enhancing disclosure requirements, increasing accounting and auditor regulation, creating new federal crimes, and increasing penalties for existing federal crimes. SOX directly impacts publicly traded companies, certified public accounting firms auditing public companies, attorneys who work for public companies or have public companies as clients, brokerage firms, investment bankers, and financial analysts who work for brokerage firms or investment bankers. Key provisions affecting LCNB include:

1. | Certification of financial reports by the chief executive officer ("CEO") and the chief financial officer ("CFO"), who are responsible for designing and monitoring internal controls to ensure that material information relating to the issuer and its consolidated subsidiaries is made known to the certifying officers by others within the company; |

-7-

2. | Inclusion of an internal control report in annual reports that include management's assessment of the effectiveness of a company's internal control over financial reporting and a report by the company's independent registered public accounting firm attesting to the effectiveness of internal control over financial reporting; |

3. | Accelerated reporting of stock trades on Form 4 by directors and executive officers; |

4. | Disgorgement requirements of incentive pay or stock-based compensation profits received within twelve months of the release of financial statements if the company is later required to restate those financial statements due to material noncompliance with any financial reporting requirement that resulted from misconduct; |

5. | Disclosure in a company's periodic reports stating if it has adopted a code of ethics for its CFO and principal accounting officer or controller and, if such code of ethics has been implemented, immediate disclosure of any change in or waiver of the code of ethics; |

6. | Disclosure in a company's periodic reports stating if at least one member of the audit committee is a "financial expert," as that term is defined by the Securities and Exchange Commission (the "SEC"); and |

7. | Implementation of new duties and responsibilities for a company's audit committee, including independence requirements, the direct responsibility to appoint the outside auditing firm and to provide oversight of the auditing firm's work, and a requirement to establish procedures for the receipt, retention, and treatment of complaints from a company's employees regarding questionable accounting, internal control, or auditing matters. |

In addition, the SEC adopted final rules on September 5, 2002, which rules were amended in December, 2005, requiring accelerated filing of quarterly and annual reports. Under the amended rules, “large accelerated filers” includes companies with a market capitalization of $700 million or more and “accelerated filers” includes companies with a market capitalization between $75 million and $700 million. Large accelerated filers are required to file their annual reports within 60 days of year-end and quarterly reports within 40 days. Accelerated filers are required to file their annual and quarterly reports within 75 days and 40 days, respectively. These new accelerated filing deadlines were effective for fiscal years ending on or after December 15, 2005. Under the amended rules, LCNB is considered an accelerated filer.

The Federal Deposit Insurance Reform Act of 2005 and the Federal Deposit Insurance Reform Conforming Amendments Act of 2005 (collectively, the “Deposit Insurance Reform Acts”) were both signed into law during February, 2006. The provisions of the Deposit Insurance Reform Acts included:

1. | Merging the Bank Insurance Fund and the Savings Association Insurance Fund into a new fund called the Deposit Insurance Fund, effective March 31, 2006; |

2. | Increasing insurance coverage for retirement accounts from $100,000 to $250,000, effective April 1, 2006; and |

3. | Eliminating a 1.25% hard target Designated Reserve Ratio, as defined, and giving the FDIC discretion to set the Designated Reserve Ratio within a range of 1.15% to 1.50% for any given year. |

The Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) became effective on July 21, 2010. The Dodd-Frank Act includes provisions that specifically affect financial institutions and other entities providing financial services and other corporate governance and compensation provisions that will affect most public companies.

The Dodd-Frank Act established a new independent regulatory body within the Federal Reserve System known as the Consumer Financial Protection Bureau (the “CFPB”). The CFPB has assumed responsibility for most consumer protection laws and has broad authority, with certain exceptions, to regulate financial products offered by banks and non-banks. The CFPB has authority to supervise, examine, and take enforcement actions with respect to depository institutions with more than $10 billion in assets, non-bank mortgage industry participants, and other CFPB-designated non-bank providers of consumer financial services. The primary regulator for depository institutions with $10 billion or less in assets will continue to have primary examination and enforcement authority for these institutions. The regulations enforced, however, will be the regulations written by the CFPB.

The Dodd-Frank Act directs federal bank regulators to develop new capital requirements for holding companies and depository institutions that address activities that pose risk to the financial system, such as significant activities in higher risk areas, or concentrations in assets whose reported values are based on models.

The Dodd-Frank Act permanently raised the FDIC maximum deposit insurance amount to $250,000. In addition, the Dodd-Frank Act places a floor on the FDIC’s reserve ratio at 1.35% of estimated insured deposits or the comparable percentage of the assessment base.

-8-

General corporate governance provisions included in the Dodd-Frank Act include expanding executive compensation disclosures to be included in the annual proxy statement, requiring non-binding shareholder advisory votes on executive compensation at annual meetings, enhancing independence requirements for compensation committee members and any advisers used by the compensation committee, and requiring the adoption of certain compensation policies including the recovery of executive compensation in the event of a financial statement restatement.

Noncompliance with laws and regulations by bank holding companies and banks can lead to monetary penalties and/or an increased level of supervision or a combination of these two items. Management is not aware of any current significant instances of noncompliance with laws and regulations and does not anticipate any problems maintaining compliance on a prospective basis. Recent regulatory inspections and examinations of LCNB and the Bank have not disclosed any significant instances of noncompliance.

The earnings and growth of LCNB are affected not only by general economic conditions, but also by the fiscal and monetary policies of the federal government and its agencies, particularly the Federal Reserve Board. Its policies influence the amount of bank loans and deposits and the interest rates charged and paid thereon and thus have an effect on earnings. The nature of future monetary policies and the effect of such policies on the future business and earnings of LCNB and the Bank cannot be predicted.

A substantial portion of LCNB's cash revenues is derived from dividends paid by the Bank. These dividends are subject to various legal and regulatory restrictions. Generally, dividends are limited to the aggregate of current year retained net income, as defined, plus the retained net income of the two prior years. In addition, dividend payments may not reduce capital levels below minimum regulatory guidelines.

Employees

As of December 31, 2017, LCNB employed 310 full-time equivalent employees. LCNB is not a party to any collective bargaining agreement. Management considers its relationship with its employees to be very good. Employee benefit programs are considered by management to be competitive with benefit programs provided by other financial institutions and major employers within LCNB’s market area.

Availability of Financial Information

LCNB files unaudited quarterly financial reports on Form 10-Q, annual financial reports on Form 10-K, current reports on Form 8-K, and amendments to these reports are filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 with the SEC. Copies of these reports are available free of charge in the shareholder information section of the Bank's website, www.lcnb.com, as soon as reasonably practicable after they are electronically filed or furnished to the SEC, or by writing to:

Robert C. Haines II

Executive Vice President, CFO

LCNB Corp.

2 North Broadway

P.O. Box 59

Lebanon, Ohio 45036

Financial reports and other materials filed by LCNB with the SEC may also be read and copied at the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained from the SEC by calling 1-800-SEC-0330. The SEC also maintains an internet site (www.sec.gov) that contains reports, proxy and information statements, and other information regarding registrants that file reports electronically, as LCNB does.

FINANCIAL INFORMATION ABOUT FOREIGN AND DOMESTIC OPERATIONS AND EXPORT SALES

LCNB and its subsidiaries do not have any offices located in foreign countries and have no foreign assets, liabilities or related income and expense for the years presented.

-9-

STATISTICAL INFORMATION

The following tables and certain tables appearing in Item 7, Management's Discussion and Analysis present additional statistical information about LCNB Corp. and its operations and financial condition. They should be read in conjunction with the consolidated financial statements and related notes and the discussion included in Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations, and Item 7A, Quantitative and Qualitative Disclosures about Market Risk.

Distribution of Assets, Liabilities and Shareholders' Equity; Interest Rates and Interest Differential

The table presenting an average balance sheet, interest income and expense, and the resultant average yield for average interest-earning assets and average interest-bearing liabilities is included in Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations.

The table analyzing changes in interest income and expense by volume and rate is included in Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations.

Investment Portfolio

The following table presents the carrying values of securities for the years indicated:

At December 31, | |||||||||

2017 | 2016 | 2015 | |||||||

(In thousands) | |||||||||

Securities available-for-sale: | |||||||||

U.S. Treasury notes | $ | 2,259 | 28,145 | 72,846 | |||||

U.S. Agency notes | 83,261 | 85,400 | 139,889 | ||||||

U.S. Agency mortgage-backed securities | 67,153 | 71,047 | 29,378 | ||||||

Certificates of deposit | — | — | 249 | ||||||

Municipal securities | 122,540 | 132,860 | 132,420 | ||||||

Mutual funds | 2,542 | 2,482 | 2,466 | ||||||

Trust preferred securities | 50 | 48 | 50 | ||||||

Equity securities | 667 | 677 | 680 | ||||||

Total securities available-for-sale | 278,472 | 320,659 | 377,978 | ||||||

Securities held-to-maturity: | |||||||||

Municipal securities | 32,571 | 41,003 | 22,633 | ||||||

Federal Reserve Bank stock | 2,732 | 2,732 | 2,732 | ||||||

Federal Home Loan Bank stock | 3,638 | 3,638 | 3,638 | ||||||

Total securities | $ | 317,413 | 368,032 | 406,981 | |||||

-10-

Contractual maturities of securities at December 31, 2017, were as follows. Actual maturities may differ from contractual maturities when issuers have the right to call or prepay obligations.

Available-for-Sale | Held-to-Maturity | ||||||||||||||||||

Amortized Cost | Fair Value | Yield | Amortized Cost | Fair Value | Yield | ||||||||||||||

(Dollars in thousands) | |||||||||||||||||||

U.S. Treasury notes: | |||||||||||||||||||

Within one year | $ | — | — | — | % | $ | — | — | — | % | |||||||||

One to five years | — | — | — | % | — | — | — | % | |||||||||||

Five to ten years | 2,283 | 2,259 | 2.07 | % | — | — | — | % | |||||||||||

After ten years | — | — | — | % | — | — | — | % | |||||||||||

Total U.S. Treasury notes | 2,283 | 2,259 | 2.07 | % | — | — | — | % | |||||||||||

U.S. Agency notes: | |||||||||||||||||||

Within one year | 998 | 998 | 1.40 | % | — | — | — | % | |||||||||||

One to five years | 38,235 | 37,805 | 1.77 | % | — | — | — | % | |||||||||||

Five to ten years | 45,604 | 44,458 | 2.02 | % | — | — | — | % | |||||||||||

After ten years | — | — | — | % | — | — | — | % | |||||||||||

Total U.S. Agency notes | 84,837 | 83,261 | 1.90 | % | — | — | — | % | |||||||||||

Municipal securities (1): | |||||||||||||||||||

Within one year | 10,224 | 10,269 | 3.29 | % | 4,043 | 4,047 | 3.15 | % | |||||||||||

One to five years | 54,665 | 54,648 | 2.73 | % | 4,128 | 4,045 | 2.90 | % | |||||||||||

Five to ten years | 54,633 | 54,119 | 2.94 | % | 8,415 | 8,286 | 3.04 | % | |||||||||||

After ten years | 3,640 | 3,504 | 2.80 | % | 15,985 | 15,972 | 5.81 | % | |||||||||||

Total Municipal securities | 123,162 | 122,540 | 2.93 | % | 32,571 | 32,350 | 4.40 | % | |||||||||||

U.S. Agency mortgage-backed securities | 68,347 | 67,153 | 2.17 | % | — | — | — | % | |||||||||||

Mutual funds | 2,586 | 2,542 | 2.23 | % | — | — | — | % | |||||||||||

Trust preferred securities | 49 | 50 | 7.78 | % | — | — | — | % | |||||||||||

Equity securities | 574 | 667 | 3.59 | % | — | — | — | % | |||||||||||

Totals | $ | 281,838 | 278,472 | 2.40 | % | 32,571 | 32,350 | 4.40 | % | ||||||||||

(1) | Yields on tax-exempt obligations are computed on a taxable-equivalent basis based upon a 34.0% statutory Federal income tax rate. |

Excluding holdings in U.S. Treasury securities and U.S. Government Agencies, there were no investments in securities of any issuer that exceeded 10% of LCNB's consolidated shareholders' equity at December 31, 2017.

Loan Portfolio

Administration of the lending function is the responsibility of the Chief Lending Officer and certain senior lenders. Lenders perform their duties subject to oversight and policy direction from the Board of Directors and the Loan Committee. The Loan Committee consists of LCNB’s Chief Executive Officer/President, Chief Financial Officer, Cashier, Chief Lending Officer, Chief Credit Officer, Loan Operations Officer, Loan Review Officer, Credit Analysis Officer, and the officers in charge of the commercial, agricultural, and retail loan portfolios.

-11-

Employees authorized to accept loan applications have various, designated lending limits for the approval of loans. A loan application for an amount outside a particular employee’s lending limit needs to be approved by an employee with a lending limit sufficient for that loan. Loans secured by residential or commercial real estate require the approval of two individuals with appropriate lending authority: Chief Executive Officer/President, Chief Lending Officer, Chief Credit Officer, Senior Vice President ("SVP") of Commercial Lending, SVP of Mortgage Lending, SVP of Consumer Lending, Assistant Vice President of Secondary Market Lending, or other board-designated lending officers. Board approval is required on any loan with policy exceptions or that will exceed 50% of the Bank's legal lending limit, rounded down to the previous $100,000, in aggregate credit to any one borrower or entity, as defined by the OCC in 12 C.F.R § 32.2(b).

Interest rates charged by LCNB vary with degree of risk, type of loan, amount, complexity, repricing frequency and other relevant factors associated with the loan.

The following table summarizes the distribution of the loan portfolio for the years indicated:

At December 31, | ||||||||||||||||||||||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||||||||||||||||

Amount | % | Amount | % | Amount | % | Amount | % | Amount | % | |||||||||||||||||||||||||

(Dollars in thousands) | ||||||||||||||||||||||||||||||||||

Commercial and industrial | $ | 36,057 | 4.2 | % | $ | 41,878 | 5.1 | % | $ | 45,275 | 5.9 | % | $ | 35,424 | 5.1 | % | $ | 29,337 | 5.1 | % | ||||||||||||||

Commercial, secured by real estate | 527,947 | 62.2 | % | 477,275 | 58.2 | % | 419,633 | 54.5 | % | 379,141 | 54.3 | % | 314,252 | 54.7 | % | |||||||||||||||||||

Residential real estate | 251,582 | 29.6 | % | 265,788 | 32.5 | % | 273,139 | 35.4 | % | 254,087 | 36.4 | % | 215,587 | 37.6 | % | |||||||||||||||||||

Consumer | 17,450 | 2.1 | % | 19,173 | 2.3 | % | 18,510 | 2.4 | % | 18,006 | 2.5 | % | 12,643 | 2.2 | % | |||||||||||||||||||

Agricultural | 15,194 | 1.8 | % | 14,802 | 1.8 | % | 13,479 | 1.7 | % | 11,472 | 1.6 | % | 2,472 | 0.4 | % | |||||||||||||||||||

Other loans, including deposit overdrafts | 539 | 0.1 | % | 633 | 0.1 | % | 665 | 0.1 | % | 680 | 0.1 | % | 91 | — | % | |||||||||||||||||||

848,769 | 100.0 | % | 819,549 | 100.0 | % | 770,701 | 100.0 | % | 698,810 | 100.0 | % | 574,382 | 100.0 | % | ||||||||||||||||||||

Deferred origination costs (fees), net | 291 | 254 | 237 | 146 | (28 | ) | ||||||||||||||||||||||||||||

Total loans | 849,060 | 819,803 | 770,938 | 698,956 | 574,354 | |||||||||||||||||||||||||||||

Less allowance for loan losses | 3,403 | 3,575 | 3,129 | 3,121 | 3,588 | |||||||||||||||||||||||||||||

Loans, net | $ | 845,657 | $ | 816,228 | $ | 767,809 | $ | 695,835 | $ | 570,766 | ||||||||||||||||||||||||

As of December 31, 2017, there were no concentrations of loans exceeding 10% of total loans that are not already disclosed as a category of loans in the above table, except for loans secured by multifamily properties. Loans secured by multifamily properties, which are included in the commercial, secured by real estate category in the above table, totaled $85,853,000, or 10.1% of total loans, at December 31, 2017.

-12-

The following table summarizes the commercial and agricultural loan maturities and sensitivities to interest rate change at December 31, 2017:

(In thousands) | |||

Maturing in one year or less | $ | 32,732 | |

Maturing after one year, but within five years | 57,451 | ||

Maturing beyond five years | 489,015 | ||

Total commercial and agricultural loans | $ | 579,198 | |

Loans maturing beyond one year: | |||

Fixed rate | $ | 199,916 | |

Variable rate | 346,550 | ||

Total | $ | 546,466 | |

Risk Elements

The following table summarizes non-accrual, past-due, and accruing restructured loans for the dates indicated:

At December 31, | |||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||

(Dollars in thousands) | |||||||||||||||

Non-accrual loans | $ | 2,965 | 5,725 | 1,723 | 5,599 | 2,961 | |||||||||

Past-due 90 days or more and still accruing | — | 23 | 559 | 203 | 250 | ||||||||||

Accruing restructured loans | 10,469 | 11,731 | 13,723 | 14,269 | 15,151 | ||||||||||

Total | $ | 13,434 | 17,479 | 16,005 | 20,071 | 18,362 | |||||||||

Percent to total loans | 1.58 | % | 2.13 | % | 2.08 | % | 2.87 | % | 3.20 | % | |||||

LCNB is not committed to lend additional funds to debtors whose loans have been modified to provide a reduction or deferral of principal or interest because of deterioration in the financial position of the borrower.

At December 31, 2017, there were no material additional loans not classified as acquired credit impaired or already disclosed as non-accrual, accruing restructured, or accruing past due 90 days or more where known information about possible credit problems of the borrowers causes management to have serious doubts as to the ability of such borrowers to comply with present loan repayment terms.

Summary of Loan Loss Experience

The table summarizing the activity related to the allowance for loan losses is included in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations.

-13-

Allocation of the Allowance for Loan Losses

The following table presents the allocation of the allowance for loan loss:

At December 31, | ||||||||||||||||||||||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||||||||||||||||

Amount | Percent of Loans in Each Category to Total Loans | Amount | Percent of Loans in Each Category to Total Loans | Amount | Percent of Loans in Each Category to Total Loans | Amount | Percent of Loans in Each Category to Total Loans | Amount | Percent of Loans in Each Category to Total Loans | |||||||||||||||||||||||||

(Dollars in thousands) | ||||||||||||||||||||||||||||||||||

Commercial and industrial | $ | 378 | 4.2 | % | $ | 350 | 5.1 | % | $ | 244 | 5.9 | % | $ | 129 | 5.1 | % | $ | 175 | 5.1 | % | ||||||||||||||

Commercial, secured by real estate | 2,178 | 62.2 | % | 2,179 | 58.2 | % | 1,908 | 54.5 | % | 1,990 | 54.3 | % | 2,520 | 54.7 | % | |||||||||||||||||||

Residential real estate | 717 | 29.6 | % | 885 | 32.5 | % | 854 | 35.4 | % | 926 | 36.4 | % | 826 | 37.6 | % | |||||||||||||||||||

Consumer | 76 | 2.1 | % | 96 | 2.3 | % | 54 | 2.4 | % | 63 | 2.5 | % | 66 | 2.2 | % | |||||||||||||||||||

Agricultural | 53 | 1.8 | % | 60 | 1.8 | % | 66 | 1.7 | % | 11 | 1.6 | % | — | 0.4 | % | |||||||||||||||||||

Other loans, including deposit overdrafts | 1 | 0.1 | % | 5 | 0.1 | % | 3 | 0.1 | % | 2 | 0.1 | % | 1 | — | % | |||||||||||||||||||

Unallocated | — | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||

Total | $ | 3,403 | 100.0 | % | $ | 3,575 | 100.0 | % | $ | 3,129 | 100.0 | % | $ | 3,121 | 100.0 | % | $ | 3,588 | 100.0 | % | ||||||||||||||

Deposits

The statistical information regarding average amounts and average rates paid for the deposit categories is included in the "Distribution of Assets, Liabilities and Shareholders' Equity" table included in Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations.

The following table presents the contractual maturity of time deposits of $100,000 or more at December 31, 2017:

(In thousands) | |||

Maturity within 3 months | $ | 4,311 | |

After 3 but within 6 months | 2,830 | ||

After 6 but within 12 months | 14,526 | ||

After 12 months | 44,940 | ||

$ | 66,607 | ||

Return on Equity and Assets

The statistical information regarding the return on assets, return on equity, dividend payout ratio, and equity to assets ratio is presented in Item 6, Selected Financial Data.

-14-

Item 1A. Risk Factors

There are risks inherent in LCNB’s operations, many beyond management’s control, which may adversely affect its financial condition and results from operations and should be considered in evaluating the Company. Credit, market, operational, liquidity, interest rate and other risks are described elsewhere in this report. Other risk factors may include the items described below.

New capital requirements could adversely affect LCNB’s capital ratios

On July 2, 2013, the Federal Reserve Board approved the final rules implementing the Basel Committee on Banking Supervision’s capital guidelines for U.S. bank holding companies as well as state banks that are members of the Federal Reserve System and savings and loan holding companies (commonly known as Basel III). On July 9, 2013, the OCC adopted the same rules for national banks and federal savings associations, and the FDIC approved the same provisions, as an interim final rule, for state nonmember banks and state savings associations.

Under the final rules, minimum requirements will increase for both the quantity and quality of capital held by banks and savings associations. The rules include a new common equity Tier 1 capital to risk-weighted assets ratio of 4.5% and a common equity Tier 1 capital conservation buffer of 2.5% of risk-weighted assets. The final rules also raise the minimum ratio of Tier 1 capital to risk-weighted assets from 4.0% to 6.0% and require a minimum leverage ratio of 4.0%.

The phase-in period for the final rules began for LCNB on January 1, 2015, with full compliance with all of the final rules' requirements phased in over a multi-year schedule through January 1, 2019. While management expects that LCNB's capital ratios under Basel III will continue to exceed the well capitalized minimum capital requirements, there can be no assurance that such will be the case. If LCNB is unable to meet or exceed the applicable minimum capital requirements, it may become subject to supervisory actions ranging in severity from losing its financial holding company status, to being precluded from making acquisitions or engaging in new activities or becoming subject to informal or formal regulatory enforcement actions.

LCNB’s earnings are significantly affected by market interest rates.

Fluctuations in interest rates may negatively impact LCNB’s profitability. A primary source of income from operations is net interest income, which is equal to the difference between interest income earned on loans and investment securities and the interest paid for deposits and other borrowings. These rates are highly sensitive to many factors beyond LCNB’s control, including general economic conditions, the slope of the yield curve (that is, the relationship between short and long-term interest rates), and the monetary and fiscal policies of the United States Federal government. LCNB expects the current level of interest rates and the current slope of the yield curve will cause further downward pressure on its net interest margin.

Increases in general interest rates could have a negative impact on LCNB’s results of operations by reducing the ability of borrowers to repay their current loan obligations. Some residential real estate mortgage loans, most home equity line of credit loans, and many of LCNB’s commercial loans have adjustable rates. Borrower inability to make scheduled loan payments due to a higher loan cost could result in increased loan defaults, foreclosures, and write-offs and may necessitate additions to the allowance for loan losses. In addition, increases in the general level of interest rates may decrease the demand for new consumer and commercial loans, thus limiting LCNB’s growth and profitability. A general increase in interest rates may also result in deposit disintermediation, which is the flow of deposits away from banks and other depository institutions into direct investments that have the potential for higher rates of return, such as stocks, bonds, and mutual funds. If this occurs, LCNB may have to rely more heavily on borrowings as a source of funds in the future, which could negatively impact its net interest margin.

Gains from sales of mortgage loans may experience significant volatility.

Gains from sales of mortgage loans are highly influenced by the level and direction of mortgage interest rates, real estate activity, and refinancing activity. Current historically low market interest rates created a refinancing demand for residential fixed-rate mortgage loans. The increased volume of refinancing activity increased gains from sales of mortgage loans as LCNB sold most of these loans to the Federal Home Loan Mortgage Corporation. An increase in market interest rates may decrease the demand for refinanced loans and decrease the gains from sales of mortgage loans recognized in LCNB’s consolidated statements of income. Gains from sales of mortgage loans may also be impacted by changes in LCNB’s strategy to manage its residential mortgage portfolio. For example, LCNB may occasionally change the proportion of loan originations that are sold in the secondary market and instead add a greater proportion to its loan portfolio.

-15-

Banking competition in Southwestern and South Central Ohio is intense.

LCNB faces strong competition for deposits, loans, trust accounts, and other services from other banks, savings banks, credit unions, mortgage brokers, and other financial institutions. Many of LCNB’s competitors include major financial institutions that have been in business for many years and have established customer bases, numerous branches, and substantially higher regulatory lending limits. Competitors in the Southwestern and South Central Ohio areas include U.S. Bank, PNC Bank, Fifth Third Bank, Chase, KeyBank, Park National Bank, Huntington National Bank, and First Financial Bank. In addition, credit unions are growing larger due to more flexible membership requirement regulations and are offering more financial services than they legally could in the past.

LCNB also competes with numerous real estate brokerage firms, some owned by realty companies, for residential real estate mortgage loans. Incentives offered by captive finance companies owned by the major automobile companies have limited the banking industry’s opportunities for growth in the new automobile loan market. The banking industry now competes with brokerage firms and mutual fund companies for funds that would have historically been held as bank deposits. Technology has lowered barriers to entry and made it possible for non-banks to offer products and services traditionally provided by banks, such as automatic transfer and automatic payment systems. Many of these competitors have fewer regulatory constraints and may have lower cost structures.

If LCNB is unable to attract and retain loan, deposit, brokerage, and trust customers, its growth and profitability levels may be negatively impacted.

Economic conditions in Southwestern and South Central Ohio could adversely affect LCNB’s financial condition and results of operations.

LCNB conducts its operations from offices that are located in nine Southwestern and South Central Ohio counties, from which substantially all of its customer base is drawn. Because of this geographic concentration of operations and customer base, LCNB's financial performance is heavily influenced by economic conditions in these areas. Any material deterioration in economic conditions in these markets could have material direct or indirect adverse impacts on LCNB's customers and on LCNB. Such deterioration could increase the number of customers experiencing financial distress, negatively impacting their ability to obtain new loans or to repay existing loans. As a result, LCNB may experience increases in the levels of impaired loans, increased charge-offs, and increased provisions for loan losses. Deteriorating economic conditions may also affect the ability of depositors to maintain or add to deposit balances and may affect the demand for loans, trust, brokerage, and other products and services offered by LCNB. Such losses and decreased demand could have material adverse affects on LCNB's financial position, results of operations, and cash flows.

The allowance for loan losses may be inadequate.

The provision for loan losses is determined by management based upon its evaluation of the amount needed to maintain the allowance for loan losses at a level considered appropriate in relation to the estimated risk of losses inherent in the portfolio. In addition to historic charge-off percentages, factors taken into consideration to determine the adequacy of the allowance for loan losses include the nature, volume, and consistency of the loan portfolio, overall portfolio quality, a review of specific problem loans, the fair value of any underlying collateral, borrowers’ cash flows, and current economic conditions that may affect borrowers’ ability to make payments. Increases in the allowance result in an expense for the period. By its nature, the evaluation is imprecise and requires significant judgment. Actual results may vary significantly from management’s assumptions. If, as a result of general economic conditions or a decrease in asset quality, management determines that additional increases in the allowance for loan losses are necessary, LCNB will incur additional expenses.

LCNB’s loan portfolio includes a substantial amount of commercial and industrial loans and commercial real estate loans, which may have more risks than residential or consumer loans.

LCNB’s commercial and industrial and commercial real estate loans comprise a substantial portion of its total loan portfolio. These loans generally carry larger loan balances and involve a greater degree of financial and credit risk than home equity, residential mortgage, or consumer loans. The increased financial and credit risk associated with these types of loans is a result of several factors, including the concentration of principal in a limited number of loans, the size of loan balances, the effects of general economic conditions on income-producing properties, and the increased difficulty of evaluating and monitoring these types of loans.

-16-

The repayment of loans secured by commercial real estate is often dependent upon the successful operation, development, or sale of the related real estate or commercial business and may, therefore, be subject to adverse conditions in the real estate market or economy. If the cash flow from operations is reduced, the borrower’s ability to repay the loan may be impaired. In such cases, LCNB may take one or more actions to protect its financial interest in the loan. Such actions may include foreclosure on the real estate securing the loan, taking possession of other collateral that may have been pledged as security for the loan, or modifying the terms of the loan. If foreclosed on, commercial real estate is often unique and may not be as salable as a residential home.

The fair value of LCNB’s investments could decline.

Most of LCNB’s investment securities portfolio is designated as available-for-sale. Accordingly, unrealized gains and losses, net of tax, in the estimated fair value of the available-for-sale portfolio is recorded as other comprehensive income, a separate component of shareholders’ equity. The fair value of LCNB’s investment portfolio may decline, causing a corresponding decline in shareholders’ equity. Management believes that several factors will affect the fair values of the investment portfolio including, but not limited to, changes in interest rates or expectations of changes, the degree of volatility in the securities markets, inflation rates or expectations of inflation, and the slope of the interest rate yield curve. These and other factors may impact specific categories of the portfolio differently and the effect any of these factors may have on any specific category of the portfolio cannot be predicted.

Many state and local governmental authorities have experienced deterioration of financial condition in recent years due to declining tax revenues, increased demand for services, and various other factors. To the extent LCNB has any municipal securities in its portfolio from issuers who are experiencing deterioration of financial condition or who may experience future deterioration of financial condition, the value of such securities may decline and could result in other-than-temporary impairment charges, which could have an adverse effect on LCNB’s financial condition and results of operations. Additionally, a general, industry-wide decline in the fair value of municipal securities could significantly affect LCNB’s financial condition and results of operations.

Changes in income tax laws or interpretations or in accounting standards could materially affect LCNB’s financial condition or results of operations.

Changes in income tax laws could be enacted, or interpretations of existing income tax laws could change, causing an adverse effect to LCNB’s financial condition or results of operations. Similarly, new accounting standards may be issued by the Financial Accounting Standards Board (the “FASB”) or existing standards revised, changing the methods for preparing financial statements. These changes are not within LCNB’s control and may significantly impact its reported financial condition and results of operations.

LCNB is subject to environmental liability risk associated with lending activities.

A significant portion of the Bank’s loan portfolio is secured by real property. During the ordinary course of business, the Bank may foreclose on and take title to properties securing certain loans. In doing so, there is a risk that hazardous or toxic substances could be found on these properties. If hazardous or toxic substances are found, the Bank may be liable for remediation costs, as well as for personal injury and property damage. Environmental laws may require the Bank to incur substantial expenses and may materially reduce the affected property’s value or limit the Bank’s ability to use or sell the affected property. In addition, future laws or more stringent interpretations or enforcement policies with respect to existing laws may increase the Bank’s exposure to environmental liability. Although the Bank has policies and procedures to perform an environmental review before initiating any foreclosure action on real property, these reviews may not be sufficient to detect all potential environmental hazards. The remediation costs and any other financial liabilities associated with an environmental hazard could have a material adverse effect on LCNB’s financial condition and results of operations.

The banking industry is highly regulated.

LCNB is subject to regulation, supervision, and examination by the Federal Reserve Board and the Bank is subject to regulation, supervision, and examination by the OCC. LCNB and the Bank are also subject to regulation and examination by the FDIC as the deposit insurer. The CFPB is responsible for most consumer protection laws and has broad authority, with certain exceptions, to regulate financial products offered by banks. Federal and state laws and regulations govern numerous matters including, but not limited to, changes in the ownership or control of banks, maintenance of adequate capital, permissible business operations, maintenance of deposit insurance, protection of customer financial privacy, the level of reserves held against deposits, restrictions on dividend payments, the making of loans, and the acceptance of deposits. See the previous section titled “Supervision and Regulation” for more information on this subject.

-17-

Federal regulators may initiate various enforcement actions against a financial institution that violates laws or regulations or that operates in an unsafe or unsound manner. These enforcement actions may include, but are not limited to, the assessment of civil money penalties, the issuance of cease-and-desist or removal orders, and the imposition of written agreements.

Proposals to change the laws governing financial institutions are periodically introduced in Congress and proposals to change regulations are periodically considered by the regulatory bodies. Such future legislation and/or changes in regulations could increase or decrease the cost of doing business, limit or expand permissible activities, or affect the competitive balance among banks, savings associations, credit unions, and other financial institutions. The likelihood of any major changes in the future and their effects are impossible to predict.

Federal income tax reform could have unforeseen effects on our financial condition and results of operations.

On December 22, 2017, the President of the United States signed into law H.R. 1, originally known as the “Tax Cuts and Jobs Act.” The Company is still in the process of analyzing the Tax Cuts and Jobs Act and its possible effects on the Company. The Tax Cuts and Jobs Act includes a number of provisions, including the lowering of the U.S. corporate tax rate from 35 percent to 21 percent, effective January 1, 2018. There are also provisions that may partially offset the benefit of such rate reduction. Financial statement impacts include adjustments for, among other things, the re-measurement of deferred tax assets and liabilities. While there are benefits, there is also substantial uncertainty regarding the details of U.S. Tax Reform. The intended and unintended consequences of the Tax Cuts and Jobs Act on our business and on holders of our common shares is uncertain and could be adverse. The Company anticipates that the impact of the Tax Cuts and Jobs Act may be material to our business, financial condition and results of operations.

FDIC deposit insurance assessments may materially increase in the future.

Deposits of LCNB are insured up to statutory limits by the Federal Deposit Insurance Corporation (FDIC) and, accordingly, LCNB and other banks and financial institutions pay quarterly premiums to the FDIC to maintain the Deposit Insurance Fund. The likelihood and extent of future rate increases are indeterminable.

Future growth and expansion opportunities may contain risks.

From time to time LCNB may seek to acquire other financial institutions or parts of those institutions or may open new branch offices. It may also consider and enter into new lines of business or offer new products or services. Such activities involve a number of risks, which may include potential inaccuracies in estimates and judgments used to evaluate the expansion opportunity, diversion of management and employee attention, lack of experience in a new market or product or service, and difficulties in integrating a future acquisition or introducing a new product or service. There is no assurance that such growth or expansion activities will be successful or that they will achieve desired profitability levels.

The financial services industry, as well as the broader economy, may be subject to new legislation, regulation, and government policy.

At this time, it is difficult to predict the legislative and regulatory changes that will result from the combination of a new President of the United States and the first year since 2010 in which both Houses of Congress and the White House have majority memberships from the same political party. In recent years, however, both the new President and senior members of the House of Representatives have advocated for significant reduction of financial services regulation, to include amendments to the Dodd-Frank Act and structural changes to the CFPB. The new Administration and Congress also may cause broader economic changes due to changes in governing ideology and governing style. New appointments to the Board of Governors of the Federal Reserve could affect monetary policy and interest rates and changes in fiscal policy could affect broader patterns of trade and economic growth. Future legislation, regulation, and government policy could affect the banking industry as a whole, including LCNB's business and results of operations, in ways that are difficult to predict. In addition, LCNB's results of operations could be adversely affected by changes in the way in which existing statutes and regulations are interpreted or applied by courts and government agencies.

LCNB’s controls and procedures may fail or be circumvented.

Management regularly reviews and updates LCNB’s internal controls, disclosure controls and procedures, and corporate governance policies and procedures. Any system of controls, however well designed and operated, is based in part on certain assumptions and can provide only reasonable, not absolute, assurances that the objectives of the system are met. Any failure or circumvention of LCNB’s controls and procedures or failure to comply with regulations related to its controls and procedures could have a material adverse effect on LCNB’s business, results of operations, and financial condition.

-18-

LCNB’s information systems may experience an interruption, cyberattack, or other breach in security.

LCNB relies heavily on communications and information systems to conduct its business. Significant resources are devoted to maintaining and regularly updating LCNB's data systems, there can be no assurance that these security measures will provide absolute security. Any failure, interruption, cyberattack, or other breach in security of these systems could result in failures or disruptions in LCNB’s customer relationship management, general ledger, deposit, loan, and other systems. While LCNB has policies and procedures designed to prevent or limit the effect of the failure, interruption, cyberattack, or other security breach of its information systems, there can be no assurance that any such occurrences will not occur or, if they do occur, that they will be adequately addressed. The occurrence of any failures, interruptions, cyberattacks, or other security breaches of LCNB’s information systems could significantly disrupt LCNB's operations, allow misappropriation of LCNB's confidential information, allow misappropriation of customer confidential information, damage LCNB’s reputation, result in a loss of customer business, subject LCNB to additional regulatory scrutiny, or expose LCNB to significant civil litigation and possible financial liability, any of which could have a material adverse effect on its financial condition and results of operations.

LCNB continually encounters technological change.

The financial services industry is continually undergoing rapid technological change with frequent introductions of new technology-driven products and services. LCNB’s future success depends, in part, upon its ability to address customer needs by using technology to provide products and services that will satisfy customer demands, as well as to create additional efficiencies in LCNB’s operations. LCNB may not be able to effectively implement new technology-driven products and services or be successful in marketing these products and services to its customers. Failure to successfully keep pace with technological change affecting the financial services industry could negatively affect LCNB’s growth, revenue and profit.

Emergence of nonbank alternatives to the financial system.

Consumers may decide not to use banks to complete their financial transactions. Technology and other changes, including the emergence of “Fintech Companies,” are allowing parties to complete financial transactions through alternative methods that historically have involved banks. For example, consumers can complete transactions, such as paying bills and/or transferring funds, directly without the assistance of banks. The process of eliminating banks as intermediaries, known as “disintermediation,” could result in the loss of fee income, as well as the loss of customer deposits and the related income generated from those deposits. The loss of these revenue streams and the lower cost of deposits as a source of funds could have a material adverse effect on our financial condition and results of operations.

Risk factors related to LCNB’s trust business.

Competition for trust business is intense. Competitors include other commercial bank and trust companies, brokerage firms, investment advisory firms, mutual fund companies, accountants, and attorneys.

LCNB’s trust business is directly affected by conditions in the debt and equity securities markets. The debt and equity securities markets are affected by, among other factors, domestic and foreign economic conditions and the monetary and fiscal policies of the United States Federal government, all of which are beyond LCNB’s control. Changes in economic conditions may directly affect the economic performance of the trust accounts in which clients’ assets are invested. A decline in the fair value of the trust accounts caused by a decline in general economic conditions directly affects LCNB’s trust fee income because such fees are primarily based on the fair value of the trust accounts. In addition, a sustained decrease in the performance of the trust accounts or a lack of sustained growth may encourage clients to seek alternative investment options.

The management of trust accounts is subject to the risk of mistaken distributions, poor investment choices, and miscellaneous other incorrect decisions. Such mistakes may give rise to surcharge actions by beneficiaries, with damages substantially in excess of the fees earned from management of the accounts.

LCNB’s ability to pay cash dividends is limited.

LCNB is dependent upon the earnings of the Bank for funds to pay dividends on its common shares. The payment of dividends by LCNB and the Bank is subject to certain regulatory restrictions. As a result, any payment of dividends in the future will be dependent, in large part, on the ability of LCNB and the Bank to satisfy these regulatory restrictions and on the Bank’s earnings, capital levels, financial condition, and other factors. Although LCNB’s financial earnings and financial condition have allowed it to declare and pay periodic cash dividends to shareholders, there can be no assurance that the current dividend policy or the amount of dividend distributions will continue in the future.

-19-

Item 1B. Unresolved Staff Comments

Not applicable.

-20-

Item 2. Properties

The Bank conducts its business from the following offices:

Name of Office | Address | County | ||||||

1. | Main Office | 2 North Broadway Lebanon, Ohio 45036 | Warren | Owned | ||||

2. | Auto Bank | Silver and Mechanic Streets Lebanon, Ohio 45036 | Warren | Owned | ||||

3. | Barron Street Office | 1697 North Barron Street Eaton, Ohio 45320 | Preble | Leased | ||||

4. | Bridge Street Office | 1240 North Bridge Street Chillicothe, Ohio 45601 | Ross | Owned | ||||

5. | Brookville Office | 225 West Upper Lewisburg Salem Road Brookville, Ohio 45309 | Montgomery | Owned | ||||

6. | Centerville Office | 9605 Dayton-Lebanon Pike Centerville, Ohio 45458 | Montgomery | Owned | ||||

7. | Chillicothe Office | 33 West Main Street Chillicothe, Ohio 45601 | Ross | Owned | ||||

8. | Colerain Township Office | 3209 West Galbraith Road Cincinnati, Ohio 45239 | Hamilton | Owned | ||||

9. | Columbus Avenue Office | 730 Columbus Avenue Lebanon, Ohio 45036 | Warren | Owned | ||||

10. | Eaton Office | 110 West Main Street Eaton, Ohio 45320 | Preble | Owned | ||||

11. | Fairfield Office | 765 Nilles Road Fairfield, Ohio 45014 | Butler | Leased | ||||

12. | Frankfort Office | Springfield and Main Streets Frankfort, Ohio 45628 | Ross | Owned | ||||

13. | Goshen Office | 6726 Dick Flynn Blvd. Goshen, Ohio 45122 | Clermont | Owned | ||||

14. | Hamilton Office | 794 NW Washington Blvd. Hamilton, Ohio 45013 | Butler | Owned | ||||

15. | Hunter Office | 3878 State Route 122 Franklin, Ohio 45005 | Warren | Owned | ||||

16. | Lewisburg Office | 522 South Commerce Street Lewisburg, Ohio 45338 | Preble | Owned | ||||

17. | Loveland Office | 500 Loveland-Madeira Road Loveland, Ohio 45140 | Hamilton | Owned | ||||

-21-

Name of Office | Address | County | ||||||

18. | Maineville Office | 7795 South State Route 48 Maineville, Ohio 45039 | Warren | Owned | ||||

19. | Mason/West Chester Office | 1050 Reading Road Mason, Ohio 45040 | Warren | Owned | ||||

20. | Middletown Office | 4441 Marie Drive Middletown, Ohio 45044 | Butler | Owned | ||||

21. | Monroe Office | 101 Clarence F. Warner Drive Monroe, Ohio 45050 | Butler | Owned | ||||

22. | New Paris Office | 201 South Washington Street New Paris, Ohio 45347 | Preble | Owned | ||||

23. | Oakwood Office | 2705 Far Hills Avenue Oakwood, Ohio 45419 | Montgomery | (2) | ||||

24. | Otterbein Office | Otterbein Retirement Community State Route 741 Lebanon, Ohio 45036 | Warren | Leased | ||||

25. | Oxford Office (1) | 30 West Park Place Oxford, Ohio 45056 | Butler | (2) | ||||

26. | Rochester/Morrow Office | Route 22-3 at 123 Morrow, Ohio 45152 | Warren | Owned | ||||

27. | South Lebanon Office | 603 Corwin Nixon Blvd. South Lebanon, Ohio 45065 | Warren | Owned | ||||

28. | Springboro/Franklin Office | 525 West Central Avenue Springboro, Ohio 45066 | Warren | Owned | ||||

29. | Warrior Office | Lebanon High School 1916 Drake Road Lebanon, Ohio 45036 | Warren | Leased | ||||

30. | Washington Court House Office | 100 Crossings Drive Washington Court House, Ohio 43160 | Fayette | Owned | ||||

31. | Waynesville Office | 9 North Main Street Waynesville, Ohio 45068 | Warren | Owned | ||||

32. | West Alexandria Office | 55 East Dayton Street West Alexandria, Ohio 45381 | Preble | Owned | ||||

33. | Western Avenue Office | 1006 Western Avenue Chillicothe, Ohio 45601 | Ross | Owned | ||||

34. | Wilmington Office | 1243 Rombach Avenue Wilmington, Ohio 45177 | Clinton | Owned | ||||

35. | Loan Production Office | 1500 West Third Ave., Suite 205 & 209 Grandview Heights, Ohio 43212 | Franklin | Leased | ||||

-22-

Name of Office | Address | County | ||||||

36. | Operations Center | 105 North Broadway Lebanon, Ohio 45036 | Warren | Owned | ||||

(1) | Excess space in this office is leased to third parties. |

(2) | The Bank owns the Oakwood and Oxford office buildings and leases the land. |

Item 3. Legal Proceedings

Except for routine litigation incidental to its businesses, LCNB is not a party to any material pending legal proceedings and none of its property is the subject of any material proceedings.

Item 4. Mine Safety Disclosures

Not Applicable.

-23-

PART II

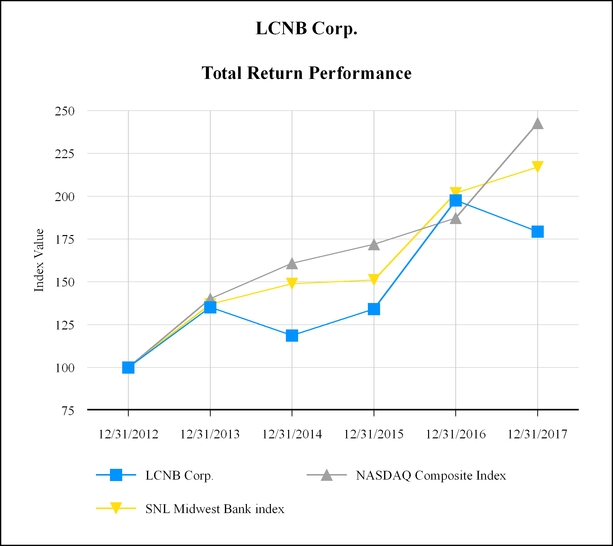

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters, and Issuer Purchases of Equity Securities.

LCNB had approximately 962 registered holders of its common stock as of December 31, 2017. The number of shareholders includes banks and brokers who act as nominees, each of whom may represent more than one shareholder. LCNB’s stock trades on the NASDAQ Capital Market exchange under the symbol “LCNB.”

Trade prices for shares of LCNB Common Stock and cash dividends per share declared and paid are set forth below. The trade prices shown below are interdealer without retail markups, markdowns, or commissions.

2017 | 2016 | |||||||||||||||||

High | Low | Dividends Declared | High | Low | Dividends Declared | |||||||||||||

First Quarter | $ | 24.35 | 20.80 | 0.16 | 17.75 | 15.51 | 0.16 | |||||||||||

Second Quarter | 23.90 | 19.00 | 0.16 | 17.24 | 15.69 | 0.16 | ||||||||||||

Third Quarter | 21.85 | 18.05 | 0.16 | 19.13 | 15.73 | 0.16 | ||||||||||||

Fourth Quarter | 22.84 | 19.40 | 0.16 | 25.00 | 16.55 | 0.16 | ||||||||||||

Total dividends declared | 0.64 | 0.64 | ||||||||||||||||

It is expected that LCNB will continue to pay dividends on a similar schedule, to the extent permitted by business and potential factors beyond management's control.

LCNB depends on dividends from the Bank for the majority of its liquid assets, including the cash needed to pay dividends to its shareholders. National banking law limits the amount of dividends the Bank may pay to the sum of retained net income, as defined, for the current year plus retained net income for the previous two calendar years. Prior approval from the OCC, the Bank’s primary regulator, would be necessary for the Bank to pay dividends in excess of this amount. In addition, dividend payments may not reduce capital levels below minimum regulatory guidelines. Management believes the Bank will be able to pay anticipated ordinary dividends to LCNB without needing to request approval.

During the period of this report, LCNB did not sell any of its securities that were not registered under the Securities Act.

On April 17, 2001, LCNB's Board of Directors authorized three separate stock repurchase programs, two of which continue to be in effect – the “Market Repurchase Program and the “Private Sale Repurchase Program.” Any shares purchased will be held for future corporate purposes.

Under the Market Repurchase Program, LCNB was originally authorized to purchase up to 200,000 shares of its stock through market transactions with a selected stockbroker. On November 14, 2005, the Board of Directors extended the Market Repurchase Program by increasing the shares authorized for repurchase to 400,000 total shares. Through December 31, 2017, 290,444 shares have been purchased under this program. No shares were purchased under the Market Repurchase Program during 2017 and 2016.