Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Protalix BioTherapeutics, Inc. | tv486893_ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Protalix BioTherapeutics, Inc. | tv486893_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Protalix BioTherapeutics, Inc. | tv486893_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - Protalix BioTherapeutics, Inc. | tv486893_ex31-1.htm |

| EX-23.1 - EXHIBIT 23.1 - Protalix BioTherapeutics, Inc. | tv486893_ex23-1.htm |

| EX-10.16 - EXHIBIT 10.16 - Protalix BioTherapeutics, Inc. | tv486893_ex10-16.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

FOR ANNUAL AND TRANSITION REPORTS PURSUANT TO SECTIONS 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

001-33357

(Commission file number)

PROTALIX BIOTHERAPEUTICS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 65-0643773 | |

| State or other jurisdiction | (I.R.S. Employer | |

| of incorporation or organization | Identification No.) | |

| 2 Snunit Street | ||

| Science Park | ||

| POB 455 | ||

| Carmiel, Israel | 20100 | |

| (Address of principal executive offices) | (Zip Code) |

972-4-988-9488

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered |

| Common stock, par value $0.001 per share | NYSE AMERICAN |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (check one):

| Large accelerated filer | ¨ | Accelerated filer | x | |

| Non-accelerated filer | ¨ | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

| Emerging growth company | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting common equity held by non-affiliates of the Registrant, as of June 30, 2017 was approximately $105.4 million, based upon a per share price equal to $0.84, the closing price for shares of the Registrant’s common stock reported by the NYSE American for such date.

On March 1, 2018, approximately 145,569,955 shares of the Registrant’s common stock, par value $0.001 per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for its 2018 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission no later than May 1, 2018 and to be delivered to shareholders in connection with the 2018 Annual Meeting of Stockholders, are herein incorporated by reference in Part III of this Form 10-K.

FORM 10-K

TABLE OF CONTENTS

i

Except where the context otherwise requires, the terms, “we,” “us,” “our” or “the Company,” refer to the business of Protalix BioTherapeutics, Inc. and its consolidated subsidiaries, and “Protalix” or “Protalix Ltd.” refers to the business of Protalix Ltd., our wholly-owned subsidiary and sole operating unit.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

The statements set forth under the captions “Business,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Risk Factors,” and other statements included elsewhere in this Annual Report on Form 10-K, which are not historical, constitute “forward-looking statements” within the meanings of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, including statements regarding expectations, beliefs, intentions or strategies for the future. When used in this report, the terms “anticipate,” “believe,” “estimate,” “expect,” “can,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “will,” “would” and other words or phrases of similar import, as they relate to our company or our subsidiaries or our management, are intended to identify forward-looking statements. We intend that all forward-looking statements be subject to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are only predictions and reflect our views as of the date they are made with respect to future events and financial performance, and we undertake no obligation to update or revise, nor do we have a policy of updating or revising, any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events, except as may be required under applicable law. Forward-looking statements are subject to many risks and uncertainties that could cause our actual results to differ materially from any future results expressed or implied by the forward-looking statements.

Examples of the risks and uncertainties include, but are not limited to, the following:

| · | failure or delay in the commencement or completion of our preclinical studies and clinical trials, which may be caused by several factors, including: slower than expected rates of patient recruitment; unforeseen safety issues; determination of dosing issues; lack of effectiveness during clinical trials; inability or unwillingness of medical investigators and institutional review boards to follow our clinical protocols; inability to monitor patients adequately during or after treatment; and or lack of sufficient funding to finance our clinical trials; |

| · | the risk that the results of our clinical trials will not support the applicable claims of superiority, safety or efficacy and that our product candidates will not have the desired effects or will have undesirable side effects or other unexpected characteristics; |

| · | risks relating to our ability to manage our relationship with Chiesi Farmaceutici S.p.A., or Chiesi, and any other collaborator, distributor or partner; |

| · | risks relating to our ability to make scheduled payments of the principal of, to pay interest on or to refinance or satisfy conversions of our outstanding convertible notes or any other indebtedness; |

| · | risks relating to our ability to defease the remaining outstanding 4.5% convertible notes on or prior to June 16, 2018; |

| · | risks relating to the compliance by Fundação Oswaldo Cruz, or Fiocruz, an arm of the Brazilian Ministry of Health, or the Brazilian MoH, with its purchase obligations under our supply and technology transfer agreement, which may have a material adverse effect on our company and may also result in the termination of such agreement; |

| · | our dependence on performance by third-party providers of services and supplies, including without limitation, clinical trial services; |

| · | risks relating to our ability to finance our research programs; |

| 1 |

| · | delays in preparing and filing applications for regulatory approval of our product candidates in the United States, the European Union and elsewhere; |

| · | the impact of development of competing therapies and/or technologies by other companies; |

| · | the risk that products that are competitive to our product candidates may be granted orphan drug status in certain territories and, therefore, one or more of our product candidate may become be subject to potential marketing and commercialization restrictions; |

| · | risks related to our supply of drug product to Pfizer Inc., or Pfizer, pursuant to our amended and restated exclusive license and supply agreement with Pfizer; |

| · | risks related to the commercialization efforts for taliglucerase alfa in Brazil; |

| · | risks related to our expectations with respect to the potential commercial value of our product and product candidates; |

| · | the inherent risks and uncertainties in developing the types of drug platforms and products we are developing; |

| · | potential product liability risks, and risks of securing adequate levels of product liability and clinical trial insurance coverage; |

| · | the possibility of infringing a third party’s patents or other intellectual property rights; |

| · | the uncertainty of obtaining patents covering our products and processes and in successfully enforcing our intellectual property rights against third parties; |

| · | risks relating to changes in healthcare laws, rules and regulations in the United States or elsewhere; and |

| · | the possible disruption of our operations due to terrorist activities and armed conflict, including as a result of the disruption of the operations of regulatory authorities, our subsidiaries, our manufacturing facilities and our customers, suppliers, distributors, collaborative partners, licensees and clinical trial sites. |

Companies in the pharmaceutical and biotechnology industries have suffered significant setbacks in advanced or late-stage clinical trials, even after obtaining promising earlier trial results or preliminary findings for such clinical trials. Even if favorable testing data is generated from clinical trials of a drug product, the U.S. Food and Drug Administration, or the FDA, or foreign regulatory authorities may not accept or approve a marketing application filed by a pharmaceutical or biotechnology company for the drug product.

These forward-looking statements reflect our current views with respect to future events and are based on assumptions and subject to risks and uncertainties. Given these uncertainties, you should not place undue reliance on these forward-looking statements. These and other risks and uncertainties are detailed under the heading “Risk Factors” in this Annual Report and are described from time to time in the reports we file with the U.S. Securities and Exchange Commission, or the Commission.

| 2 |

| Item 1. | Business |

We are a biopharmaceutical company focused on the development and commercialization of recombinant therapeutic proteins based on our proprietary ProCellEx® protein expression system. We developed our first commercial drug product, Elelyso®, using our ProCellEx system and we are now focused on utilizing the system to develop a pipeline of proprietary, clinically superior versions of recombinant therapeutic proteins that primarily target large, established pharmaceutical markets and that in most cases rely upon known biological mechanisms of action. With our experience to date, we believe ProCellEx will enable us to develop additional proprietary recombinant proteins that are therapeutically superior to existing recombinant proteins currently marketed for the same indications, including applying the unique properties of our ProCellEx system for the oral delivery of therapeutic proteins.

The following table summarizes our current product candidates and their respective stages of clinical development:

On October 19, 2017, Protalix Ltd., our wholly-owned subsidiary, and Chiesi entered into an Ex-US license and collaboration agreement, which we refer to as the Chiesi Agreement, pursuant to which Chiesi was granted an exclusive, license for all markets outside of the United States to develop and commercialize pegunigalsidase alfa. Pegunigalsidase alfa, or PRX-102, is our chemically modified version of the recombinant protein alpha-Galactosidase-A protein that is currently being evaluated in phase III clinical trials for the treatment of Fabry disease. Under the terms and conditions of the Chiesi Agreement, Protalix Ltd. retained the right to commercialize pegunigalsidase alfa in the United States. Under the Chiesi Agreement, Chiesi made an upfront payment to Protalix Ltd. of $25.0 million in connection with the execution of the agreement and Protalix Ltd. is entitled to additional payments of up to $25 million in development costs, capped at $10 million per year. Protalix Ltd. is also eligible to receive an additional up to $320 million, in the aggregate, in regulatory and commercial milestone payments. Protalix Ltd. and Chiesi have agreed to a specific allocation of the responsibilities for the continued development efforts for pegunigalsidase alfa. Protalix Ltd. will manufacture all of the PRX-102 needed for all purposes under the agreement, subject to certain exceptions, and Chiesi will purchase pegunigalsidase alfa from Protalix, subject to certain terms and conditions. Chiesi will make tiered payments of 15% to 35% of its net sales, depending on the amount of annual sales, as consideration for the supply of pegunigalsidase alfa. The Chiesi Agreement also provides for reimbursement by Chiesi of certain costs to be incurred by Protalix Ltd.

| 3 |

In December 2017, the European Commission granted Orphan Drug Designation for pegunigalsidase alfa for the treatment of Fabry disease. The designation was granted after the EMA’s Committee for Orphan Medicinal Products, or the COMP, issued a positive opinion supporting the designation noting that we had established that there was medically plausible evidence that pegunigalsidase alfa will provide a significant benefit over existing approved therapies in the European Union for the treatment of Fabry disease. The COMP cited clinical and non-clinical justifications we provided to establish the significant benefit of pegunigalsidase alfa, noting that the COMP considered the justifications to constitute a clinically relevant advantage. Orphan Drug Designation for pegunigalsidase alfa qualifies Protalix Ltd. for access to a centralized marketing authorization procedure, including applications for inspections and for protocol assistance. If the orphan drug designation is maintained at the time pegunigalsidase alfa is approved for marketing in the European Union, if at all, we expect that PRX-102 will benefit from 10 years of market exclusivity within the European Union. The market exclusivity will not have any effect on Fabry disease treatments already approved at that time.

In January 2018, FDA granted Fast Track designation to PRX-102. Fast Track designation is a process designed to facilitate the development and expedite the review of drugs and vaccines for serious conditions that fill an unmet medical need.

On May 1, 2012, the FDA approved for sale our first commercial product, taliglucerase alfa for injection, an enzyme replacement therapy, or ERT, for the long-term treatment of adult patients with a confirmed diagnosis of type 1 Gaucher disease. Subsequently, taliglucerase alfa was approved for marketing by the regulatory authorities of other countries. Taliglucerase alfa is called alfataliglicerase in Brazil and certain other Latin American countries, where it is marketed under the name alfataliglicerase. Taliglucerase alfa is marketed under the name Elelyso in other territories.

Since its approval by the FDA, taliglucerase alfa has been marketed by Pfizer, as provided in the exclusive license and supply agreement by and between Protalix Ltd. and Pfizer, which we refer to as the Pfizer Agreement. In October 2015, we entered into an Amended and Restated Exclusive License and Supply Agreement, or the Amended Pfizer Agreement, which amends and restates the Pfizer Agreement in its entirety. Pursuant to the Amended Pfizer Agreement, we sold to Pfizer our share in the collaboration created under the initial Pfizer Agreement for the commercialization of Elelyso in exchange for a cash payment equal to $36.0 million. As part of the sale, we agreed to transfer our rights to Elelyso in Israel to Pfizer, while gaining full rights to Elelyso in Brazil. We will continue to manufacture drug substance for Pfizer, subject to certain terms and conditions. Under the Amended Pfizer Agreement, Pfizer is responsible for 100% of expenses, and entitled to all revenues, globally for Elelyso, excluding Brazil, where we are responsible for all expenses and retain all revenues.

For the first 10-year period after the execution of the Amended Pfizer Agreement, we have agreed to sell drug substance to Pfizer for the production of Elelyso, and Pfizer maintains the right to extend the supply period for up to two additional 30-month periods subject to certain terms and conditions. Any failure to comply with our supply commitments may subject us to substantial financial penalties, which will have a material adverse effect on our business, results of operations and financial condition. The Amended Pfizer Agreement also includes customary provisions regarding cooperation for regulatory matters, patent enforcement, termination, indemnification and insurance requirements.

On June 18, 2013, we entered into a Supply and Technology Transfer Agreement, or the Brazil Agreement, with Fiocruz, an arm of the Brazilian MoH, for taliglucerase alfa.

In 2017, we received a purchase order from the Brazilian MoH for the purchase of approximately $24.3 million of alfataliglicerase for the treatment of Gaucher patients in Brazil. The purchase order consists of a number of shipments in increasing volumes. Shipments started in June 2017. Fiocruz’s purchases of alfataliglicerase to date have been significantly below certain agreed upon purchase milestones and, accordingly, we have the right to terminate the Brazil Agreement. Notwithstanding, we are, at this time, continuing to supply alfataliglicerase to Fiocruz under the Brazil Agreement, and patients continue to be treated with alfataliglicerase in Brazil. We are discussing with Fiocruz potential actions that Fiocruz may take to comply with its purchase obligations and, based on such discussions, we will determine what we believe to be the course of action that is in the best interest of our company.

| 4 |

Our Strategy

Our strategy centers around prioritizing existing and new pipeline candidates to focus on products that we believe offer a clear competitive advantage over existing treatments. The strategy was the culmination of an intensive review by our management of our internal resources and of the markets in which we expect we can operate. The following highlights the details of the strategic plan as it relates to our development of an innovative product pipeline using our ProCellEx protein expression system.

Pegunigalsidase alfa (PRX-102) for the Treatment of Fabry Disease. pegunigalsidase alfa, or PRX-102, is designed to be an improved enzyme replacement therapy product for the treatment of Fabry disease given its potential for clinically superior outcomes and enhanced safety when compared to currently marketed enzyme replacement therapies. The product candidate is a key focus for us. We are continuing to enroll patients and recruit clinical sites for our phase III clinical trials of PRX-102, and our phase I/II clinical trial remains ongoing in an extension period.

alidornase alfa (PRX-110) for the Treatment of Cystic Fibrosis. alidornase alfa, our proprietary plant cell recombinant human Deoxyribonuclease 1, is under development for the treatment of cystic fibrosis (CF), to be administered by inhalation. alidornase alfa has an actin inhibition resistance that is designed to improve lung function and lower the incidence of recurrent infections by enhancing the enzyme’s efficacy in patients’ sputa. We released the final results of our phase II clinical trial of alidornase alfa for the treatment of CF in April 2017. We are currently studying the final results of the trial and are considering different collaboration alternatives as part of our further development plans.

Oral Anti-TNF (OPRX-106) Anti Inflammatory. Oral anti-TNF represents a novel mode of administering a recombinant anti-TNF protein. It is under development as an orally-delivered anti-inflammatory treatment using plant cells as a natural capsule for the expressed protein. Currently, the first 14 patients have completed our phase II proof of concept efficacy study of OPRX-106 for the treatment of ulcerative colitis, and four patients are currently in treatment and follow-up. The trial is evaluating key efficacy endpoints including clinical response and remission utilizing the Mayo score, as well as safety and pharmacokinetics. Interim data generated from the first 14 patients that completed the trial was released in January 2018. We expect to release complete results by the end of March, 2018. Upon review of the final proof of concept data, we intend to identify and collaborate with a well-suited partner for further development.

Potential Pipeline Candidates. We aim to expand our pipeline by leveraging the advantages of our proprietary ProCellEx protein expression technology. The focus is expected to be on biologics with significantly improved clinical profiles than the currently marketed proteins for these indications. Biosimilars will not be a market on which we focus, and will only be considered in the case of proteins that are highly difficult to express or that represent opportunities for early market entry arising from the intellectual property advantages arising from ProCellEx.

Except for the rights to commercialize taliglucerase alfa worldwide (other than Brazil), which we licensed to Pfizer, and the rights to PRX-102 which we licensed to Chiesi for territories outside the United States, we hold the worldwide commercialization rights to all of our proprietary development candidates. We continuously evaluate potential strategic marketing partnerships as well as collaboration programs with biotechnology and pharmaceutical companies and academic research institutes.

ProCellEx: Our Proprietary Protein Expression System

ProCellEx is our proprietary production system. We have developed our ProCellEx system based on our plant cell culture technology for the development, expression and manufacture of recombinant proteins. Our protein expression system does not involve mammalian or animal components or transgenic field-grown, whole plants at any point in the production process. Our ProCellEx system consists of a comprehensive set of capabilities and proprietary technologies, including advanced genetic engineering and plant cell culture technology, which enables us to produce complex, proprietary and biologically equivalent proteins for a variety of human diseases. This protein expression system facilitates the creation and selection of high expressing, genetically stable cell lines capable of expressing recombinant proteins. The entire protein expression process, from initial nucleotide cloning to large-scale production of the protein product, occurs under cGMP-compliant, controlled processes. Our plant cell culture technology uses plant cells, such as carrot and tobacco cells, which undergo advanced genetic engineering and are grown on an industrial scale in a flexible bioreactor system. Cell growth, from scale up through large-scale production, takes place in flexible, sterile, polyethylene bioreactors which are confined to a clean-room environment. Our bioreactors are well-suited for plant cell growth using a simple, inexpensive, chemically-defined growth medium as a catalyst for growth. The reactors are custom-designed and optimized for plant cell cultures, easy to use, entail low initial capital investment, are rapidly scalable at a low cost and require less hands-on maintenance between cycles.

| 5 |

Our ProCellEx system is capable of producing proteins with an amino acid sequence and three dimensional structure practically equivalent to that of the desired human protein, and with a very similar, although not identical, glycan, or sugar, structure, as demonstrated in our internal research and external laboratory studies. In collaboration with the Weizmann Institute of Science, we have demonstrated that the three-dimensional structure of a protein expressed in our proprietary plant cell-based expression system retains the same three-dimensional structure as exhibited by the mammalian cell-based expressed version of the same protein. In addition, proteins produced by our ProCellEx system maintain the biological activity that characterize that of the naturally-produced proteins. Based on these results, we believe that proteins developed using our ProCellEx protein expression system have the intended composition and correct biological activity of their human equivalent proteins.

We believe that our ProCellEx system will enable us to develop recombinant therapeutic proteins yielding substantial cost advantages, accelerated development and other competitive benefits when compared to mammalian cell-based protein expression systems. In addition, our ProCellEx system may enable us, in certain cases, to develop and commercialize recombinant proteins without infringing upon the method-based patents or other intellectual property rights of third parties. The major elements of our ProCellEx system are patent protected in most major countries. Moreover, we expect to enjoy method-based patent protection for the proteins we develop using our proprietary ProCellEx protein expression technology, although there can be no assurance that any such patents will be granted. In some cases, we may be able to obtain patent protection for the compositions of the proteins themselves. We have filed for United States and international composition of matter patents for taliglucerase alfa.

We have successfully demonstrated the feasibility of our ProCellEx system through: (i) the FDA’s approval of taliglucerase alfa, and its subsequent approval by other regulatory authorities; (ii) the clinical and preclinical studies we have performed to date, including the positive efficacy and safety data in our clinical trials for taliglucerase alfa, pegunigalsidase alfa, alidornase alfa and OPRX-106 for the treatment of ulcerative colitis; (iii) preclinical results in well-known models in our enzyme for each of Fabry disease, DNase and antiTNF; and (iv) by expressing, on an exploratory, research scale, many additional complex therapeutic proteins belonging to different drug classes, such as enzymes, hormones, monoclonal antibodies, cytokines and vaccines. The therapeutic proteins we have expressed to date in research models have produced the intended composition and similar or superior biological activity compared to their respective human-equivalent proteins. Moreover, several of such proteins demonstrated advantageous biological activity when compared to the biotherapeutics currently available in the market to treat the applicable disease or disorder. We believe that the FDA’s approval of taliglucerase alfa represents a strong proof-of-concept of our ProCellEx system and plant cell-based protein expression technology. We also believe that the significant benefits of our ProCellEx system, if further substantiated in clinical trials and in the successful commercialization of taliglucerase alfa and our other product candidates, have the potential to transform the industry standard for the development of complex therapeutic proteins.

Mammalian cell-based expression technology is based on the introduction of a human gene encoding for a specific therapeutic protein into the genome of a mammalian cell, and such systems have become the dominant system for the expression of recombinant proteins due to their capacity for sophisticated, proper protein folding (which is necessary for proteins to carry out their intended biological activity), assembly and post-expression modification, such as glycosilation (the addition of sugar residues to a protein which is necessary to enable specific biological activity by the protein). Many of the biotechnology industry’s largest and most successful therapeutic proteins, including Epogen®, Neupogen®, Cerezyme®, Rituxan®, Humira®, Enbrel®, Neulasta®, Remicade® and Herceptin® are produced through mammalian cell-based expression systems. Mammalian cell-based expression systems can produce proteins with superior quality and efficacy compared to proteins expressed in bacteria and yeast cell-based systems. As a result, the majority of currently approved therapeutic proteins, as well as those under development, are produced in mammalian cell-based systems.

While bacterial and yeast cell-based expression systems were the first protein expression systems developed by the biotechnology industry and remain cost-effective compared to mammalian cell-based production methodologies, proteins expressed in bacterial and yeast cell-based systems lack the capacity for sophisticated protein folding, assembly and post-expression modifications, which are key factors of mammalian cell-based systems. Accordingly, such systems cannot be used to produce glycoproteins or other complex proteins and, therefore, bacterial and yeast cell-based systems are limited to the expression of the most basic, simple proteins, such as insulin and growth hormones.

| 6 |

Several companies and research institutions have been exploring the expression of human proteins in genetically-modified organisms, or GMOs, such as transgenic field-grown, whole plants and transgenic animals. However, these alternate techniques may be restricted by regulatory and environmental risks regarding contamination of agricultural crops and by the difficulty in applying cGMP standards of the pharmaceutical industry to these expression technologies and none of these technologies have been approved by the regulatory agencies with jurisdiction over any substantial market.

To date, our manufacturing facility, in which we utilize our ProCellEx system, was determined to be acceptable by each of the FDA, the European Medicines Agency, or the EMA, ANVISA, the Israeli MOH, the Australian Therapeutic Goods Administration, or the TGA, and Health Canada, after GMP inspections were performed as part of their respective reviews for marketing approval of taliglucerase alfa.

Competitive Advantages of Our ProCellEx Protein Expression System

We intend to continue to leverage the multiple unique advantages of our proprietary ProCellEx protein expression system, including our advanced genetic engineering technology and plant cell-based protein expression methods, to develop our pipeline. Significant advantages of our ProCellEx system over mammalian, bacterial, yeast and transgenic cell-based expression technologies, include the following:

Biologic Optimization. ProCellEx has internal capabilities developed to improve the biologic dynamics of an expressed protein. For example, the proteins produced through our system have uniform glycosilation patterns and therefore do not require the lengthy and expensive post-expression modifications that are required for certain proteins produced by mammalian cell-based systems. Such post-expression modifications in mammalian cell-produced proteins are made in order to expose the terminal mannose sugar residues, which are structures on a protein that are key elements in allowing the expressed protein to bind to a target cell and subsequently be taken into the target cell for therapeutic benefit. In addition, these steps do not guarantee the exposure of all of the required terminal mannose sugar residues, resulting in potentially lower effective yields and inconsistency in potency from batch to batch. We believe this quality increases the potency and consistency of the expressed proteins, and thus, the effectiveness of the protein which presents an additional cost advantage of ProCellEx over competing protein expression methodologies.

Ability to Penetrate Certain Patent-Protected Markets. ProCellEx has the potential to provide workaround manufacturing that does not infringe the method-based patents or other intellectual property rights of third parties. Certain biotherapeutic proteins available for commercial sale are not protected by patents that cover the compound and are available for use in the public domain. Rather, the process of expressing the protein product in mammalian or bacterial cell systems is protected by method-based patents. Using our plant cell-based protein expression technology, we are able to express an equivalent protein without infringing upon these method-based patents. Moreover, we expect to enjoy method-based patent protection for the proteins we develop using our ProCellEx system, although there can be no assurance that any such patents will be granted. In some cases, we may be able to obtain patent protection for the compositions of the proteins themselves. We have filed for U.S. and international composition of matter patents for PRX-102 and certain of our other product candidates.

Broad Range of Expression Capabilities. ProCellEx is able to produce a broad array of complex glycosilated proteins, which are difficult to produce in other systems, such as bacterial and yeast cell-based systems, as well as CHO systems. We have successfully demonstrated the feasibility of our ProCellEx system by producing, on an exploratory, research scale, a variety of therapeutic proteins belonging to different classes of recombinant drugs, such as enzymes, hormones, monoclonal antibodies, cytokines and vaccines. We have demonstrated that the recombinant proteins we have expressed to date have the intended composition and correct biological activity of their human-equivalent protein, with several of such proteins demonstrating advantageous biological activity compared to the currently available biotherapeutics. In specific cases, we have been successful in expressing proteins that have not been successfully expressed in other production systems.

Significantly Lower Capital and Production Costs. ProCellEx entails a lower cost of scale-up and of production. Plant cells grow rapidly under a variety of conditions and are not as sensitive as mammalian cells are to temperature, pH and oxygen levels which generally can only be grown under near perfect conditions. Our system, therefore, does not require the highly complex, expensive, stainless steel bioreactors typically used in mammalian cell-based production systems to maintain very specific temperature, pH and oxygen levels. Instead, we use simple polyethylene bioreactors that can be maintained at the room temperature of the clean-room in which they are placed. This system also reduces ongoing production and monitoring costs typically associated with mammalian cell-based expression technologies. Furthermore, while mammalian cell-based systems require very costly growth media at various stages of the production process to achieve target yields of proteins, plant cells require only simple and much less expensive solutions based on sugar, water and microelements at infrequent intervals to achieve target yields. Mammalian cell-based expression systems require large quantities of sophisticated and expensive growth medium to accelerate the expression process.

| 7 |

Elimination of the Risk of Viral Transmission or Infection by Mammalian Components. By nature, plant cells do not carry the risk of infection by human or other animal viruses. Mammalian cells, to the contrary, are susceptible to viral infections, including human viruses, and several cases of viral contamination have occurred. As a result, the risk of contamination of our products under development and the potential risk of viral transmission from our product and product candidates to future patients, whether from known or unknown mammalian viruses, is eliminated. Because our products and product candidates do not bear the risk of mammalian viral transmission, we are not required by the FDA or other regulatory authorities to perform the constant monitoring procedures for mammalian viruses during the protein expression process that are required in mammalian cell-based production. In addition, the production process of our ProCellEx system is void of any mammalian components which are susceptible to the transmission of prions, such as those related to bovine spongiform encephalopathy (commonly known as “mad-cow disease”). These factors further reduce the risks and operating costs of ProCellEx compared to mammalian cell-based expression systems.

The FDA and other regulatory authorities require viral inactivation and other rigorous and detailed procedures for mammalian cell-based manufacturing processes in order to address these potential hazards, thereby increasing the cost and time demands of such expression systems. Furthermore, the current FDA and other procedures only ensure screening for scientifically identified, known viruses. Accordingly, compliance with current FDA and other procedures does not fully guarantee that patients are protected against transmission of unknown or new potentially fatal viruses that may infect mammalian cells.

Potential ability to administer active therapeutic proteins orally. We are using ProCellEx to produce active recombinant proteins through oral administration of plant cells expressing biotherapeutic proteins. In such method, an enzyme is naturally encapsulated within plant cells genetically engineered to express the targeted enzyme. Plant cells have the unique attribute of a cellulose cell wall which makes them resistant to enzyme degradation when passing through the digestive tract. The plant cell itself serves as a delivery vehicle, once released and absorbed, to transport an enzyme in active form to the bloodstream. If proven effective, this would be the first time an enzyme will be administered orally rather than through intravenous therapy. To date we have completed successful preclinical animal studies for oral GCD and oral antiTNF, and early clinical trials of oral GCD in Gaucher patients. In addition, we have completed a phase IIa proof of concept trial of oral antiTNF as well as a phase I clinical trial of oral antiTNF in healthy volunteers.

Our First Commercial Product – Elelyso for the Treatment of Gaucher Disease

Elelyso (taliglucerase alfa), our first commercial product, is a plant cell expressed recombinant glucocerebrosidase enzyme (GCD) for the treatment of Gaucher disease. On May 1, 2012, the FDA approved Elelyso for injection as an enzyme replacement therapy (ERT) for the long-term treatment of adult patients with a confirmed diagnosis of type 1 Gaucher disease. It was subsequently approved by the Israeli MOH, ANVISA and the regulatory authorities of other countries. In August 2014, the FDA approved Elelyso for injection for pediatric patients, and other jurisdictions, including Brazil, approved pediatric indications thereafter.

Gaucher disease, a hereditary, genetic disorder with severe and debilitating symptoms, is the most prevalent lysosomal storage disorder in humans. Lysosomal storage disorders are metabolic disorders in which a lysosomal enzyme, a protein that degrades cellular substrates in the lysosomes of cells, is mutated or deficient. Lysosomes are small membrane-bound cellular structures within cells that contain enzymes necessary for intracellular digestion. Gaucher disease is caused by mutations or deficiencies in the gene encoding GCD, a lysosomal enzyme that catalyzes the degradation of the fatty substrate, glucosylceramide (GlcCer). Patients with Gaucher disease lack or otherwise have dysfunctional GCD and, accordingly, are not able to break down GlcCer. The GlcCer accumulates in lysosomes of certain white blood cells called macrophages which consequently become highly enlarged. The enlarged cells accumulate in the spleen, liver, lungs, bone marrow and brain. Signs and symptoms of Gaucher disease may include enlarged liver and spleen, abnormally low levels of red blood cells and platelets and skeletal complications. In some cases, the patient may suffer an impairment of the central nervous system.

| 8 |

The standard of care for Gaucher disease is enzyme replacement therapy using recombinant GCD to replace the mutated or deficient natural GCD enzyme. Enzyme replacement therapy is a medical treatment in which recombinant enzymes are injected into patients in whom the enzyme is lacking or dysfunctional. Cerezyme® and VPRIV® are the only other ERTs currently available for the treatment of Gaucher disease. In addition, Cerdelga® (eliglustat) is a substrate reduction therapy for Gaucher disease that was approved for marketing by the FDA in August 2014 and by the European Commission in January 2015. Finally, Zavesca (miglustat) is a small molecule drug for the treatment of Gaucher disease. Zavesca has been approved by the FDA for use in the United States as an oral treatment. However, it has many side effects and the FDA has approved it only for administration to those patients who cannot be treated through ERT, and, accordingly, have no other treatment alternative. As a result, the use of Zavesca has been limited with respect to the treatment of Gaucher disease. However, Zavesca is also used to treat other rare disorders.

We have licensed to Pfizer the worldwide rights to Elelyso with the exception of Brazil, a market where we have retained own full rights.

Our Pipeline Drug Candidates

PRX-102 for the Treatment of Fabry Disease

We are developing PRX-102, our proprietary plant cell expressed chemically modified version of the recombinant alpha-GAL-A protein, a therapeutic enzyme, for the treatment of Fabry disease, a rare genetic lysosomal storage disorder. We believe that PRX-102 has the potential to be a significantly improved version of the currently marketed Fabry disease enzymes, Fabrazyme® and Replagal®, with improved activity in the Fabry disease target organs and significantly longer half-life due to higher stability, which together can potentially lead to improved substrate clearance and significantly lower formation of antibodies, as observed in our phase I/II clinical trial in Fabry patients. We believe that the treatment of Fabry disease is a specialty clinical niche with the potential for high growth as there is a significant unmet medical need for Fabry disease treatments.

Fabry Disease Background

Fabry disease is a serious, life-threatening condition. It is a disease or condition associated with morbidity that has a substantial impact on survival, day-to-day function, and the likelihood that the disease, if left untreated, will progress from a less severe condition to a more serious one. Fabry disease is an X-linked multisystem lysosomal storage disorder caused by the absence or reduction of α-galactosidase-A (α-Gal-A) activity, which is a lysosomal enzyme that catalyzes the hydrolysis of globotriaosylceramide (Gb3) from oligosaccharides, glycoproteins and glycolipids. The absence or reduction of this enzymatic activity leads to the progressive accumulation of glycolipids, especially Gb3, in capillary endothelial cells, podocytes, tubular cells, glomerular endothelial cells, mesangial cells, interstitial cells, cardiomyocytes, fibroblasts, and neurons. The accumulation of glycosphingolipids (e.g., Gb3) leads to chronic pain, skin lesions, cardiac, deficiencies, and, in particular, renal involvement. End-stage renal failure and cardiomyopathy often lead to early death in Fabry patients. Fabry disease causes substantial reduction in life-expectancy, by an average of 15 years in female patients and 20 years in male patients, compared to the general population.

Current Treatments of Fabry Disease

Currently there are two enzyme replacement therapies drugs available on the market to treat Fabry disease. Fabrazyme, marketed by Genzyme Corporation (acquired by Sanofi), is approved for the treatment of Fabry disease in the United States and the European Union. Sanofi reported €722 million (approximately $865 million) in worldwide sales of Fabrazyme in 2017. The other approved enzyme replacement therapy for the treatment of Fabry disease in the European Union is Replagal, which is marketed by Shire. Shire reported $472 million in sales of Replagal in 2017. In April 2016, GalafoldTM, a chaperone therapy manufactured by Amicus Therapeutics, Inc., or Amicus, was approved in the European Union as a monotherapy for Fabry disease in patients with amenable mutations. Galafold has also been accepted for marketing in a number of other countries. Amicus reported revenues of approximately $36 million in sales of Galafold in 2017.

| 9 |

PRX-102 Development Program

In October 2016, the first patient was dosed in our global phase III clinical trial of PRX-102 for the treatment of Fabry disease. Over 40 sites are currently participating in this trial. The phase III efficacy and safety clinical trial, which we refer to as the BALANCE Study, is a multi-center, randomized, double-blind, active control study of PRX-102 in Fabry patients with impaired renal function. The trial is designed to enroll 78 patients previously treated with Fabrazyme (agalsidase beta) with a stable dose for at least six months. Enrolled patients are randomized to continue treatment with 1 mg/kg of either Fabrazyme or PRX-102, at a 2:1 ratio of PRX-102 to Fabrazyme, respectively. Patients are to be treated via intravenous (IV) infusions every two weeks. The sites are recruiting adult symptomatic Fabry patients with plasma and/or leucocyte alpha galactosidase activity (by activity assay) less than 30% mean normal levels. All patients must have had treatment with a dose of 1 mg/kg agalsidase beta per infusion every two weeks for at least one year. In addition, to be included in the trial, patients need to have certain eGFR values and a meaningful decline in annualize eGFR slope.

The primary endpoint for the BALANCE study, which was agreed with both the FDA and the EMA, is the comparison in the rate of decline of eGFR slope between Fabrazyme and PRX-102. At 12 months, we intend to conduct an interim analysis to test for non-inferiority to support an anticipated regulatory filing with the EMA. At the same time, we intend to approach the FDA to request its review of the then totality of data. Notwithstanding, patients enrolled in the study will continue to be treated for a total of 24 months, at which point the data will be analyzed to test for superiority, which is the original guidance we received from the FDA.

Concurrently with the BALANCE study, we are also performing a supportive phase III clinical trial of PRX-102, which we refer to as the BRIDGE Study. The BRIDGE study is an open-label, single-arm, switchover study to assess the efficacy and safety of PRX-102 in Fabry patients currently treated with Replagal. The trial is designed to enroll 22 patients. The objective of the study is to generate safety and efficacy data of patients switched from Replagal to PRX-102 over a 12-month period. The endpoints of the study are safety, mean annualized change (slope) in eGFR, pain, plasma lyso GB3, immunogenicity and Quality of Life.

In addition to the BALANCE and BRIDGE studies, we are performing a third clinical trial to evaluate the safety and efficacy of administering 2 mg/kg of PRX-102 once monthly in Fabry patients. PRX-102 with a 2 mg/kg dose was found to be safe and well tolerated with no formation of antibodies in our phase I/II clinical trial of PRX-102 for the treatment of Fabry disease. Additionally, in our phase I/II clinical trial, 2 mg/kg of PRX-102 demonstrated approximately a 40 times higher circulatory half-life compared with other enzyme replacement therapies, and, as demonstrated in a Fabry mice model, with materially higher active enzyme reaching target organs affected by Fabry disease. Pharmacokinetic (PK) analysis and modeling from the phase I/II clinical trial indicate that PRX-102 levels at the second week after infusion remain 10 times higher than published Fabrazyme levels at the day of infusion. Moreover, the amount of PRX-102 in the circulation at weeks three and four, are higher than those of Fabrazyme during the two-week treatments. These results provide strong rationale for the clinical evaluation of a once-monthly dosing.

We plan to enroll up to 30 Fabry patients currently treated with an approved enzyme replacement therapy in this study. A safety and efficacy evaluation will occur at 12 months with additional long term follow-up.

Phase I/II Clinical Data

Our phase I/II clinical trial of PRX-102, which we completed in 2015, was a worldwide, multi-center, open label, dose ranging study to evaluate the safety, tolerability, pharmacokinetics, immunogenicity and efficacy parameters of PRX-102 in adult Fabry patients. Sixteen adult naive Fabry patients (9 male and 7 female) completed the trial, each in one of three dosing groups, 0.2 mg/kg, 1mg/kg and 2mg/kg. Each patient received intravenous infusions of PRX-102 every two weeks for 12 weeks, with efficacy follow-up after six-month and twelve-month periods. All patients that completed the trial opted to continue to receive 1 mg/kg of PRX-102 in an open-label, 60-month extension study under which all patients have been switched to receive 1 mg/kg of the drug, the selected dose for our phase III studies of PRX-102.

The data set forth below was recorded at 24 months from 11 patients enrolled and treated in the long-term open-label extension trial. Patients who did not continue in the extension trial included female patients who became or planned to become pregnant, and therefore were unable to continue in accordance with the study protocol, and patients that relocated to a location where treatment was not available under the clinical study.

| 10 |

Efficacy

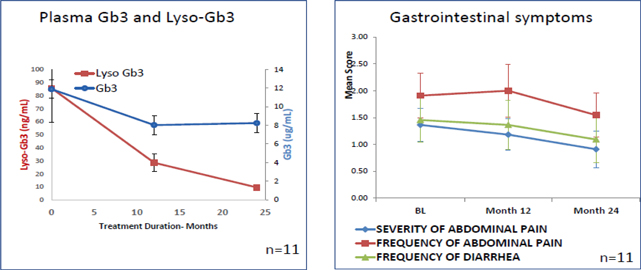

| · | Lyso Gb3 levels decreased approximately 90% from baseline (see Figure 1); |

| · | Renal function remained stable with mean eGRF levels of 108.02 and 107.20 at baseline and 24 months, respectively with a modest annual eGFR slope of -2.1; (see Figure 2) |

| · | An improvement across all the gastrointestinal symptoms evaluated, including severity and frequency of abdominal pain and frequency of diarrhea, were noted (see Figure 1); |

| · | Cardiac parameters, including LVM, LVMI and EF, remained stable with no cardiac fibrosis development detected; |

| · | In conclusion, an improvement of over 40% in disease severity was shown as measured by the Mainz Severity Score Index (MSSI), a score compiling the different elements of the disease severity including neurological, renal and cardiovascular parameters; and |

| · | An improvement was noted in each of the individual parameters of the MSSI. |

Figure 1. Continuous reductions observed over 24 months

Figure 2. Continuous clinical stability observed over 24 months

| 11 |

Safety

| · | The majority of adverse events were mild to moderate in severity, and transient in nature; |

| · | During the first 12 months of treatment, only three of 16 patients (less than 19%) formed anti-drug antibodies (ADA), of which two of these patients (less than 13%) had neutralizing antibodies; |

| · | Importantly, however, the ADAs turned negative for all three of these patients following 12 months of treatment; and |

| · | The ADA positivity effect had no observed impact on the safety, efficacy or continuous biomarker reduction of PRX-102. |

alidornase Alfa (PRX-110) for the Treatment of Cystic Fibrosis

alidornase alfa is our proprietary plant cell recombinant form of human deoxyribonuclease I (DNase I) that we are developing for the treatment of CF, to be administered by inhalation. DNase I cleaves extracellular DNA and thins the thick mucus that accumulates in the lungs of CF patients. Currently, Pulmozyme® is the only DNase I commercially available, with annual sales of approximately CHF 730 million (approximately $748 million) in sales for 2017 according to public reports by F. Hoffman-La Roche Ltd.

In vitro studies with PRX-110 demonstrated improved enzyme kinetics, significantly reduced sensitivity to inhibition by actin and improved ex vivo efficacy when compared to Pulmozyme. Preclinical studies of alidornase alfa administered by inhalation showed substantial enzymatic activity in lungs.

We designed alidornase alfa, through chemical modification, to be resistant to inhibition by actin so as to improve lung function and lower the incidence of recurrent infections by enhancing the enzyme’s efficacy in patients’ sputa. Actin, a potent inhibitor of DNase, is found in high concentration in CF patients’ sputum. As demonstrated in Figure 3, the activity of alidornase alfa, as demonstrated in in vitro studies, remains almost with no change in the relevant actin concentration found in CF patients while Pulmozyme is degraded significantly.

Figure 3. Actin and DNase concentrations in human sputum tested in in vitro assays; Rheology Data Analysis in in human sputum samples

| 12 |

In addition, alidornase alfa has demonstrated improved disease parameters in human models sputum testing when compared to the currently marketed product. In particular, alidornase alfa has demonstrated a reduction in mucus viscosity in human sputum samples when compared to the currently marketed product. See Figure 3.

alidornase alfa Development Program

We completed a phase I clinical trial of alidornase alfa with 18 healthy volunteers in which alidornase alfa was found to be safe and tolerable.

In July 2016 we commenced a phase IIa clinical trial of alidornase alfa for the treatment of CF, and we released the final results of the study in April 2017. Sixteen patients were enrolled in the study, all of whom completed the study. The phase II trial was a 28-day switchover study to evaluate the safety and efficacy of alidornase alfa in CF patients previously treated with Pulmozyme (currently the only commercially available DNase therapy). Participation in the trial was preceded by a two-week washout period from Pulmozyme before treatment with alidornase alfa via inhalation.

The primary efficacy results show that treatment with alidornase alfa resulted in clinically meaningful lung function improvement, as demonstrated by a mean absolute increase in the percent predicted forced expiratory volume in one second (ppFEV1) of 3.4 points from baseline. Moreover, a mean absolute increase in ppFEV1 of 2.8 points was also observed in patients participating in the trial when compared to measurements taken from patients at initiation before the switch from Pulmozyme to alidornase alfa. See Figure 4.

Figure 4. Phase II trial demonstrates clinically meaningful lung function improvement

A commercially available small molecule CFTR modulator for the treatment of CF has reported a mean absolute increase in ppFEV1 of 2.5 from baseline in its registration clinical study. This score was achieved while 74% of the patients participating in the trial of the CFTR modulator were also treated with the modulator on top of Pulmozyme. While this marketed CFTR addresses a certain mutation applicable to less than 50% of CF patients, alidornase alfa is being developed to treat all CF patients.

Sputa available DNA samples were analyzed for approximately half of the patients. A mean reduction of over 70% in DNA content from baseline was observed, and a mean reduction of over 90% from baseline was observed for sputa visco-elasticity. Correlation between improvement in sputa parameters and pulmonary function was observed. See Figure 5.

| 13 |

Figure 5. Decrease in sputum DNA content and sputum viscosity upon alidornase alfa treatment initiation

In addition, an in vitro study of alidornase alfa demonstrated a significant inhibition of Pseudomonas Aeruginosa, with alidornase alfa treated colonies reduced by over 50%, compared to baseline. Pseudomonas, strains of bacteria that are widely found in the environment, are a major cause of lung infections in CF patients. Chronic pulmonary infection is a leading cause of morbidity and mortality in CF patients, despite the aggressive use of antibiotics, and Pseudomonas is the most prevalent organism in the airway colonization of CF patients.

PK analysis performed indicated alidornase alfa is not absorbed into a patient’s circulatory system, suggesting higher levels of alidornase alfa remains available in the patient’s lungs. This provides further support for the potential that alidornase alfa may offer additional efficacy to CF patients.

The above-mentioned material decrease in visco-elasticity and DNA presence in CF patients’ sputa, coupled with the significant inhibition of Pseudomonas and higher levels of alidornase alfa available in the patients’ lungs, provides further supportive evidence of improved lung function after treatment with alidornase alfa, as demonstrated by the increase in FEV1.

alidornase alfa was well tolerated with no serious adverse events reported.

OPRX-106; Oral antiTNF for the treatment of inflammatory diseases

OPRX-106, our oral antiTNF product candidate, is a recombinant antiTNF (Tumor, Necrosis Factor) protein that we are expressing through ProCellEx. Auto-immune-mediated inflammatory disorders are conditions that are characterized by common pathways that lead to inflammation and are caused or triggered by a compromised or dysregulation of the normal immune response. Immune-mediated inflammatory disorders can cause organ damage, and are associated with increased morbidity. Common auto-immune diseases include rheumatoid arthritis, inflammatory bowel disease (IBD) such as ulcerative colitis and crohn’s disease, psoriasis, and others. Some of the major treatments are antiTNF drugs, administered as subcutaneous injections or as intravenous infusions. Sales of anti-TNF drugs exceeded $30 billion annually. Well-known antiTNF drugs include Humira, Remicade and Enbrel.

OPRX-106 is a plant cell-expressed form of the fused protein that is naturally encapsulated within BY-2 cells genetically engineered to express the enzyme. Plant cells have the unique attribute of a cellulose cell wall which makes them resistant to enzyme degradation when passing through the digestive tract. The plant cell itself serves as a delivery vehicle, once released and absorbed, to transport the enzyme in active form to the bloodstream. If proven effective, our experimental oral antiTNF would be the first protein to be administered orally rather than through injection. We believe that our oral delivery mechanism could be applied to additional proteins and has the potential to change the method of protein administration in certain indications.

| 14 |

OPRX-106 Development Program

OPRX-102 for the treatment of ulcerative colitis is currently the subject of a phase IIa clinical trial. The first patient was enrolled in the trial in November 2016. The phase II clinical trial is a randomized, open label, 2-arm study of OPRX-106 in patients with active mild to moderate ulcerative colitis. A total of 24 patients were enrolled and randomized to receive 2 mg or 8 mg of OPRX-106, administered orally, once daily, for 8 weeks. Currently, the first 14 patients have completed the study, and four patients are currently in treatment and follow-up. The trial evaluated key efficacy endpoints including clinical response and remission utilizing the Mayo score, as well as safety and pharmacokinetics. Interim data generated from the first 14 patients that completed the trial was released in January 2018. The interim data demonstrates that 57% of the patients achieved clinical response and 36% achieved clinical remission at week 8. In the rectal bleeding analysis, a sub category of the Mayo score, 79% of those patients show an improvement. In addition, the majority of those patients show improvement in the study’s additional efficacy endpoints, with 86% of the patients achieved an improvement in calprotectin, a protein biomarker present in the feces indicating intestinal inflammation, and 64% have an improved Geboes score, a histopathological scoring for the assessment of disease activity in ulcerative colitis. We except to release complete results by the end of March, 2018.

For purposes of the study, clinical response at week 8 is defined as a decrease in the Mayo score of at least 3 points and either a decrease in the sub-score for rectal bleeding of at least 1 point from baseline, or rectal bleeding sub-score of 0 or 1. Clinical remission at week 8 is defined as clinically symptom free, a Mayo score ≤ 2, with no individual sub-score exceeding 1 point after treatment.

Treatment was well tolerated and the majority of adverse events have been mild to moderate and transient in nature, with headaches being the most common. No immunosuppression was evident.

The results from our phase I clinical trial of OPRX-106 demonstrated that the drug was safe and well tolerated, and showed biological activity in the gut. The phase I clinical trial was a randomized, parallel-design, open-label study designed to evaluate the safety and pharmacokinetics of OPRX-106 in healthy volunteers. The trial enrolled 14 subjects that were randomized to one of three dosing cohorts receiving OPRX-106 doses equivalent to 2mg, 8mg or 16mg Tumor Necrosis Factor receptor-Fc fusion protein. Subjects received once daily oral administrations for five consecutive days. The results demonstrated that oral administration of OPRX-106 is safe and well tolerated. No major side effects were noted, and no suppression of the immune system was observed. Regulatory T cell activation showing biological activity in the gut was observed. Fluorescence-activated cell sorting analysis (FACS) was performed using various antibodies for surface markers, and it was observed that all three dosages of OPRX-106 promoted the induction of various subsets of T cells, some of which are correlated with anti-inflammatory response.

Commercialization Agreement with Chiesi Farmaceutici

On October 19, 2017, Protalix Ltd. and Chiesi entered into the Chiesi Agreement pursuant to which Chiesi was granted an exclusive, license for all markets outside of the United States to develop and commercialize pegunigalsidase alfa. Protalix Ltd. retained the right to commercialize pegunigalsidase alfa in the United States. Chiesi made an upfront payment to Protalix Ltd. of $25.0 million in connection with the execution of the agreement and Protalix Ltd. is entitled to additional payments of up to $25 million in development costs, capped at $10 million per year. Protalix Ltd. is also eligible to receive an additional up to $320 million, in the aggregate, in regulatory and commercial milestone payments. Protalix Ltd. and Chiesi have agreed to a specific allocation of the responsibilities for the continued development efforts for pegunigalsidase alfa. Protalix Ltd. agreed to manufacture all of the PRX-102 needed for all purposes under the agreement, subject to certain exceptions, and Chiesi will purchase pegunigalsidase alfa from Protalix, subject to certain terms and conditions. Chiesi is required to make tiered payments of 15% to 35% of its net sales, depending on the amount of annual sales, as consideration for the supply of pegunigalsidase alfa. The Chiesi Agreement also provides for reimbursement by Chiesi of certain costs to be incurred by Protalix Ltd.

We are required to pay a royalty equal to 3% of the PRX-102-related revenues Chiesi records under the Chiesi Agreement to the National Authority for Technological Innovation, or NATI.

| 15 |

Technology Transfer Agreement with Fiocruz

Our Brazil Agreement became effective in January 2014. The technology transfer is designed to be completed in four stages and is intended to transfer to Fiocruz the capacity and skills required for the Brazilian government to construct its own manufacturing facility, at its sole expense, and to produce a sustainable, high-quality, and cost-effective supply of taliglucerase alfa. The initial term of the technology transfer is seven years. The agreement contains certain purchase commitments by Fiocruz. If Fiocruz fails to comply with the purchase commitments, we may terminate the agreement, and all of our rights to the technology will be returned.

In 2017, we received a purchase order from the Brazilian MoH for the purchase of approximately $24.3 million of alfataliglicerase for the treatment of Gaucher patients in Brazil. The purchase order consists of a number of shipments in increasing volumes. Shipments started in June 2017. Fiocruz’s purchases of alfataliglicerase to date have been significantly below certain agreed upon purchase milestones and, accordingly, we have the right to terminate the Brazil Agreement. Notwithstanding, we are, at this time, continuing to supply alfataliglicerase to Fiocruz under the Brazil Agreement, and patients continue to be treated with alfataliglicerase in Brazil. We are discussing with Fiocruz potential actions that Fiocruz may take to comply with its purchase obligations and, based on such discussions, we will determine what we believe to be the course of action that is in the best interest of our company.

The Brazil Agreement may be extended for an additional five-year term, as needed, to complete the technology transfer. All of the terms of the arrangement, including the minimum annual purchases, will apply during the additional term. Upon completion of the technology transfer, and subject to Fiocruz receiving approval from ANVISA to manufacture taliglucerase alfa in its facility in Brazil, the agreement will enter into the final term and will remain in effect until our last patent in Brazil expires. During such period, Fiocruz will be the sole provider of this important treatment option for Gaucher patients in Brazil and shall pay us a single-digit royalty on net sales.

Intellectual Property

We maintain a proactive intellectual property strategy which includes patent filings in multiple jurisdictions, including the United States and other commercially significant markets. As of December 31, 2017, we held, or had license rights to, 69 patents and 58 pending patent applications with respect to various compositions, methods of production and methods of use relating to our ProCellEx protein expression system and our proprietary product pipeline. Of the above, one is a joint patent, eight are joint patent applications, and one is a licensed patent application.

Our competitive position and future success depend in part on our ability, and that of our licensees, to obtain and leverage the intellectual property covering our product candidates, know-how, methods, processes and other technologies, to protect our trade secrets, to prevent others from using our intellectual property and to operate without infringing the intellectual property of third parties. We seek to protect our competitive position by filing United States, European Union, Israeli and other foreign patent applications covering our technology, including both new technology and improvements to existing technology. Our patent strategy includes obtaining patents, where possible, on methods of production, compositions of matter and methods of use. We also rely on know-how, continuing technological innovation, licensing and partnership opportunities to develop and maintain our competitive position.

We issued a series of 7.5% convertible notes in December 2016 and July 2017, which are guaranteed by our subsidiaries and secured by perfected liens on all of our material assets, primarily consisting of our intellectual property assets, including a stock pledge of our foreign subsidiaries in favor of the holders of outstanding 7.5% convertible notes.

As of December 31, 2017, our patent portfolio consisted of several patent families (consisting of patents and/or patent applications) covering our technology, protein expression methodologies and system and product candidates, as follows:

| · | With respect to our ProCellEx protein expression system, we held nine issued patents and seven patent applications relating to the large scale production of proteins in cultured plant cells. The issued patents and any patents to issue in the future based on pending patent applications in this patent family, if at all, are expected to expire in 2028. One patent relating to a separate family, covering methods for culturing and harvesting plant cells and/or tissues in consecutive cycles is expected to expire in 2025. |

| 16 |

| · | We held a patent family containing 24 issued patents and one patent application in India, South Africa, Russian Federation, Australia, China, the United States, Ukraine, Singapore, Japan, Europe, Hong Kong, Mexico, Korea, Canada, Brazil and Israel relating to the production of recombinant glycosylated lysosomal proteins in our plant culture platform, including taliglucerase alfa, and uses of these proteins and cells containing these proteins for the treatment of lysosomal disorders. The issued patents and any patents to issue in the future based on pending patent applications in this patent family, if at all, are expected to expire in 2024. |

| · | We held a patent family containing three granted patents relating to a system and method for production of antibodies in a plant cell culture, and antibodies produced in such a system. The issued patents in this patent family are expected to expire in 2025. |

| · | We held a patent family containing four issued patents in Europe, South Africa, Australia and Israel, and one pending patent application relating to a new method for delivering active recombinant proteins systemically through oral administration of transgenic plant cells. The issued patents and any patents to issue in the future based on patent applications in this patent family, if at all, are expected to expire in 2026. |

| · | We held a patent family containing five granted patents in the United States, Europe, South Africa, Israel and Australia, relating to saccharide containing protein conjugates. The issued patents and any patents to issue in the future based on the patent applications in this patent family, if at all, are expected to expire in 2028. |

| · | We held a patent family containing four granted patents in Japan, United States, Europe and China, and six pending patent applications relating to Nucleic Acid construct for expression of alpha-galactosidase enzyme in plants and plant cells. The patents to issue in the future based on the patent applications in this patent family, if at all, are expected to expire in 2031. |

| · | We held a patent family containing 16 granted patents in Europe, United States, Australia, Japan, Russian Federation, China, Hong Kong, Singapore, New Zealand and South Africa, and eight pending patent applications relating to multimeric protein structures of α-galactosidase and to uses thereof in treating Fabry disease. The issued patents and any patents to issue in the future based on the patent applications in this patent family, if at all, are expected to expire in 2031. |

| · | We held three patent families containing two granted patents in the United States and six pending applications relating to plant recombinant human DNase I and uses in therapy. The patents to issue in the future based on these patent applications, if at all, are expected to expire in 2033. |

| · | We held a a patent family containing 11 patent applications relating to chemically modified plant recombinant human DNase I and uses in therapy. The patents to issue in the future based on this patent application, if at all, are expected to expire in 2036. |

| · | We held three families containing 10 patent applications relating to plant recombinant TNF alpha inhibitor polypeptides. The patents to issue in the future based on these patent applications, if at all, are expected to expire in 2034/2035. |

| · | Our patent portfolio includes a patent that we co-own that covers human glycoprotein hormone and chain splice variants, including isolated nucleic acids encoding these variants. More specifically, this patent covers a new splice variant of human FSH. This patent was issued in the United States and is expected to expire in 2024. |

| 17 |

| · | We co-own and have an exclusive license to a patent family, containing eight pending applications, that covers use of plant cells expressing a TNF alpha polypeptide inhibitor in therapy. The patents to issue in the future based on these patent applications, if at all, are expected to expire in 2034. |

| · | We have licensed the rights to a United States patent application covering oral composition comprising a TNF antagonist. The patents to issue in the future based on this application, if at all, are expected to expire in 2034. |

We are aware of U.S. patents, and corresponding international counterparts of such patents, owned by third parties that contain claims covering methods of producing GCD. We do not believe that, if any claim of infringement were to be asserted against us based upon such patents, taliglucerase alfa would be found to infringe any valid claim under such patents. However, there can be no assurance that a court would find in our favor or that, if we choose or are required to seek a license to any one or more of such patents, a license would be available to us on acceptable terms or at all.

In April 2005, Protalix Ltd. entered into a license agreement with Icon Genetics AG, or Icon, pursuant to which we received an exclusive worldwide license to develop, test, use and commercialize Icon’s technology to express certain proteins in our ProCellEx protein expression system. We are also entitled to a non-exclusive worldwide license to make and have made other proteins expressed by using Icon’s technology in our technology. As consideration for the license, we are obligated to make royalty payments equal to varying low, single-digit percentages of net sales of products by us, our affiliates, or any sublicensees under the agreement. In addition, we are obligated to make milestone payments equal to $350,000, in the aggregate, for each product developed under the license, upon the achievement of certain milestones.

Our license agreement with Icon remains in effect until the earlier of the expiration of the last patent under the agreement or, if all of the patents under the agreement expire, 20 years after the first commercial sale of any product under the agreement. Icon may terminate the agreement upon written notice to us that we are in material breach of our obligations under the agreement and we are unable to remedy such material breach within 30 days after we receive such notice. Further, Icon may terminate the agreement in connection with certain events relating to a wind up or bankruptcy, if we make a general assignment for the benefit of our creditors, or if we cease to conduct operations for a certain period. Icon may also terminate the exclusivity granted to us by written notice if we fail to reach certain milestones within a designated period of time. Notwithstanding the termination date of the agreement, our obligation to pay royalties to Icon under the agreement may expire prior to the termination of the agreement, subject to certain conditions.

Manufacturing

We use our current facility, which has approximately 20,000 sq/ft of clean rooms built according to industry standards, to develop, process and manufacture pegunigalsidase alfa, taliglucerase alfa and other recombinant proteins. Pegunigalsidase alfa and our other drug product candidates, as well as taliglucerase alfa, must be manufactured in a sterile environment and in compliance with cGMPs set by the FDA and other relevant foreign regulatory authorities. We are currently producing Fabry drug substance for our phase III and other clinical trials, as well as the manufacture of the taliglucerase alfa we need in the near future, included the taliglucerase alfa to be purchased by Pfizer under the Pfizer Agreement. In addition, we intend to use our manufacturing space to produce all of the drug substance needed in connection with the clinical trials for our product candidates.

In 2017, the FDA approved the Supplemental New Drug Application (sNDA) we submitted to allow us to convert our manufacturing facility from a single dedicated product facility to a multi-product facility. We expect that the conversion will allow us to realize potentially significant operational savings. Our facility’s current capacity can serve all of our current and expected commercial and clinical needs, and we believe it will be sufficient to serve our production needs for the anticipated commercialization of PRX-102.

Our manufacturing facilities in Carmiel, Israel, have undergone successful audits by the Israeli MOH, the FDA, ANVISA, and the European Union under the European Union’s centralized marketing authorization procedure, the Australian TGA and Health Canada.

| 18 |