Attached files

| file | filename |

|---|---|

| EX-23.3 - EX-23.3 - PENSKE AUTOMOTIVE GROUP, INC. | pag-20171231ex233bfd32e.htm |

| EX-32 - EX-32 - PENSKE AUTOMOTIVE GROUP, INC. | pag-20171231xex32.htm |

| EX-31.2 - EX-31.2 - PENSKE AUTOMOTIVE GROUP, INC. | pag-20171231ex312b05362.htm |

| EX-31.1 - EX-31.1 - PENSKE AUTOMOTIVE GROUP, INC. | pag-20171231ex311a4dfe9.htm |

| EX-23.2 - EX-23.2 - PENSKE AUTOMOTIVE GROUP, INC. | pag-20171231ex232b2e3a9.htm |

| EX-23.1 - EX-23.1 - PENSKE AUTOMOTIVE GROUP, INC. | pag-20171231ex23157dbf2.htm |

| EX-21 - EX-21 - PENSKE AUTOMOTIVE GROUP, INC. | pag-20171231ex219d508b9.htm |

| EX-12 - EX-12 - PENSKE AUTOMOTIVE GROUP, INC. | pag-20171231ex12b89aaec.htm |

| EX-10.18 - EX-10.18 - PENSKE AUTOMOTIVE GROUP, INC. | pag-20171231ex1018d5f4f.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10‑K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2017 |

|

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

|

Commission file number 1‑12297

Penske Automotive Group, Inc.

(Exact name of registrant as specified in its charter)

|

Delaware |

22‑3086739 |

|

2555 Telegraph Road |

48302‑0954 |

(248) 648‑2500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class |

Name of Each Exchange on Which Registered |

|

Voting Common Stock, par value $0.0001 per share |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well‑known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S‑T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S‑K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10‑K or any amendment to this Form 10‑K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☒ |

Accelerated filer ☐ |

Non‑accelerated filer ☐ |

Smaller reporting company ☐ |

|

|

|

|

Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting common stock held by non‑affiliates as of June 30, 2017 was $1,573,072,588. As of February 16, 2018, there were 85,787,007 shares of voting common stock outstanding.

Documents Incorporated by Reference

Certain portions, as expressly described in this report, of the registrant’s proxy statement for the 2018 Annual Meeting of the Stockholders to be held May 10, 2018 are incorporated by reference into Part III, Items 10‑14.

We are a diversified international transportation services company that operates automotive and commercial truck dealerships principally in the United States, Canada and Western Europe, and distributes commercial vehicles, diesel engines, gas engines, power systems and related parts and services principally in Australia and New Zealand. We employ more than 26,000 people worldwide.

In 2017, our business generated $21.4 billion in total revenue, which is comprised of approximately $19.8 billion from retail automotive dealerships, $1.0 billion from retail commercial truck dealerships and $0.5 billion from commercial vehicle distribution and other operations. We generated $3.2 billion in gross profit, which is comprised of $2.9 billion from retail automotive dealerships, $165.8 million from retail commercial truck dealerships and $131.9 million from commercial vehicle distribution and other operations.

Retail Automotive Dealership. We believe we are the second largest automotive retailer headquartered in the U.S. as measured by the $19.8 billion in total retail automotive dealership revenue we generated in 2017. As of December 31, 2017, we operated 343 retail automotive franchises, of which 155 franchises are located in the U.S. and 188 franchises are located outside of the U.S. The franchises outside the U.S. are located primarily in the U.K. In 2017, we retailed and wholesaled more than 618,900 vehicles. We are diversified geographically, with 59% of our total retail automotive dealership revenues in 2017 generated in the U.S. and Puerto Rico and 41% generated outside the U.S. We offer over 40 vehicle brands, with 70% of our retail automotive dealership revenue in 2017 generated from premium brands, such as Audi, BMW, Mercedes-Benz and Porsche. Each of our dealerships offers a wide selection of new and used vehicles for sale. In addition to selling new and used vehicles, we generate higher-margin revenue at each of our dealerships through maintenance and repair services and the sale and placement of third-party finance and insurance products, third-party extended service and maintenance contracts, and replacement and aftermarket automotive products.

In the first quarter of 2017, we acquired CarSense in the U.S. and CarShop in the U.K., both businesses representing stand-alone used vehicle dealerships, which we believe complement our existing franchised retail automotive dealership operations and provide scalable opportunities across our market areas. Our CarSense operations consist of five locations operating in the Philadelphia and Pittsburgh, Pennsylvania market areas, including southern New Jersey. Our CarShop operations consist of five retail locations and a vehicle preparation center operating principally throughout Southern England. In January 2018, we expanded our U.K. stand-alone used vehicle dealerships by acquiring The Car People, one of the U.K.’s leading retailers of used vehicles. The Car People has four retail locations operating across Northern England, which complements CarShop’s locations principally in Southern England.

Retail automotive dealerships represented 92.7% of our total revenues and 90.8% of our total gross profit in 2017.

1

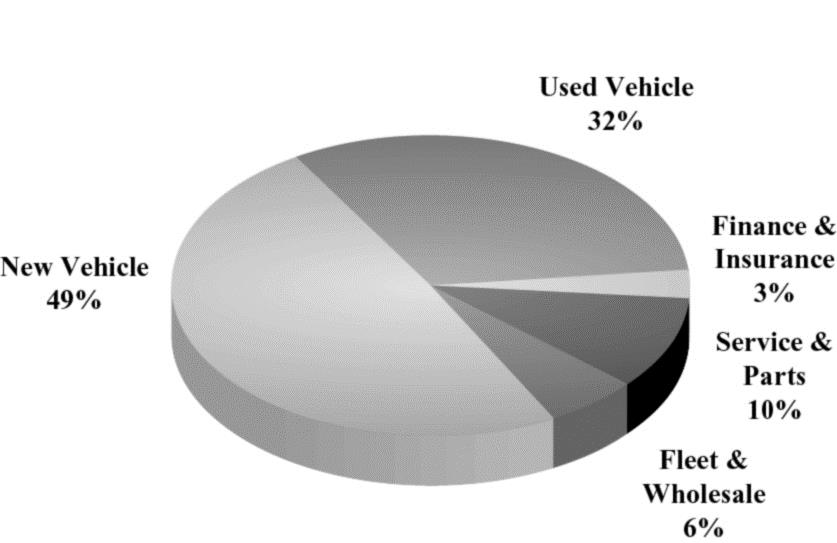

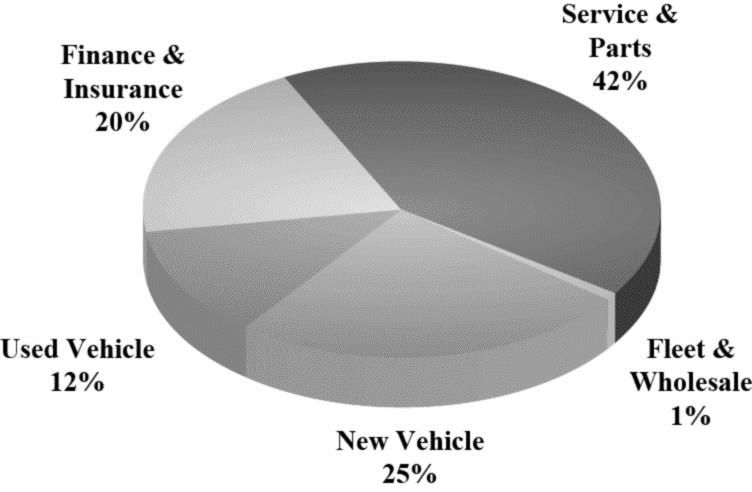

We believe our diversified retail automotive income streams help to mitigate the historical cyclicality found in some elements of the automotive sector. Revenues from higher margin service and parts sales include warranty work, customer paid work, collision repair services, and wholesale parts sales. Service and parts sales are typically less cyclical than retail vehicle sales and generate the largest part of our retail automotive gross profit. The following graphics show the percentage of our total retail automotive dealership revenues by product area and their respective contribution to our retail automotive gross profit:

|

Revenue Mix |

Gross Profit Mix |

|

|

|

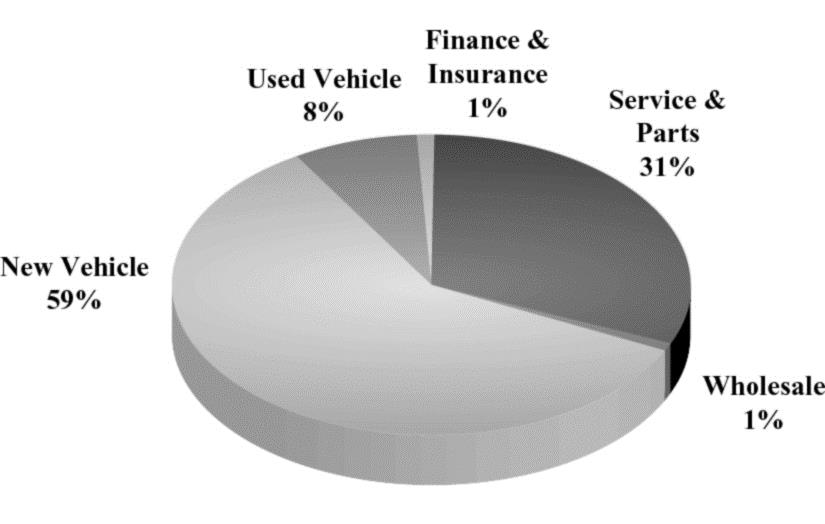

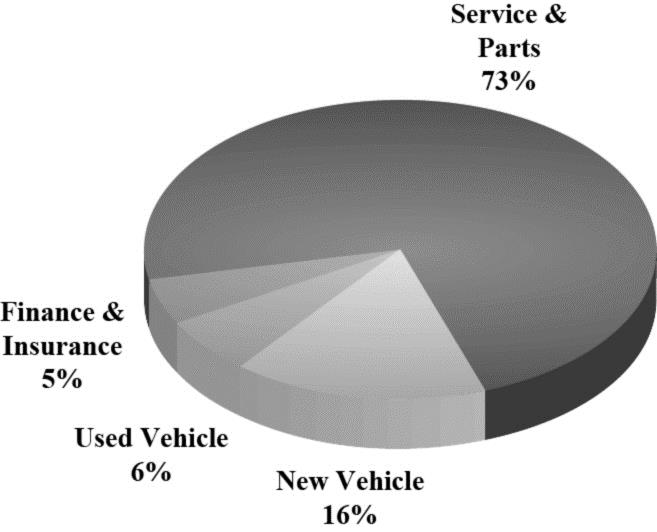

Retail Commercial Truck Dealership. We operate a heavy and medium-duty truck dealership group known as Premier Truck Group (“PTG”) with locations in Texas, Oklahoma, Tennessee, Georgia, and Canada. As of December 31, 2017, PTG operated twenty locations, including fourteen full-service dealerships and six collision centers, offering primarily Freightliner and Western Star branded trucks. Four of these locations were acquired in April 2016 in the greater Toronto, Canada market area, and two of these locations were acquired in December 2016 in the Niagara Falls, Canada market area. PTG also offers a full range of used trucks available for sale as well as service and parts departments, providing a full range of maintenance and repair services.

This business represented 4.9% of our total revenues and 5.1% of our total gross profit in 2017.

Our retail commercial truck business also benefits from diversified income streams similar to those of the retail automotive sector. The following graphics show the percentage of our total retail commercial truck dealership revenues by product area and their respective contribution to our retail commercial truck gross profit:

|

Revenue Mix |

Gross Profit Mix |

|

|

|

2

Commercial Vehicle Distribution. We are the exclusive importer and distributor of Western Star heavy-duty trucks (a Daimler brand), MAN heavy and medium-duty trucks and buses (a VW Group brand), and Dennis Eagle refuse collection vehicles, together with associated parts, across Australia, New Zealand and portions of the Pacific. This business, known as Penske Commercial Vehicles Australia (“PCV Australia”), distributes commercial vehicles and parts to a network of more than 70 dealership locations, including eight company-owned retail commercial vehicle dealerships.

We are also a leading distributor of diesel and gas engines and power systems, principally representing MTU, Detroit Diesel, Mercedes-Benz Industrial, Allison Transmission and MTU Onsite Energy. This business, known as Penske Power Systems (“PPS”), offers products across the on- and off-highway markets in Australia, New Zealand and portions of the Pacific and supports full parts and aftersales service through a network of branches, field locations and dealers across the region. The on-highway portion of this business complements our PCV Australia distribution business, including integrated operations at retail locations selling PCV brands.

These businesses represented 2.4% of our total revenues and 4.1% of our total gross profit in 2017.

Penske Truck Leasing. We currently hold a 28.9% ownership interest in Penske Truck Leasing Co., L.P. (“PTL”), a leading provider of transportation services and supply chain management. PTL is capable of meeting customers’ needs across the supply chain with a broad product offering that includes full-service truck leasing, truck rental and contract maintenance, along with logistic services such as dedicated contract carriage, distribution center management, transportation management and lead logistics provider. On July 27, 2016, we acquired an additional 14.4% ownership interest in PTL from subsidiaries of GE Capital Global Holdings, LLC (collectively, “GE Capital”) for approximately $498.5 million in cash to bring our ownership interest to 23.4%. Prior to this acquisition, we held a 9.0% ownership interest in PTL. On September 7, 2017, we acquired an additional 5.5% ownership interest from GE Capital for approximately $239.1 million in cash. At the same time, affiliates of Mitsui & Co., Ltd. (“Mitsui”), our second largest shareholder, acquired an additional 10.0% ownership interest in PTL at the same valuation. PTL is currently owned 41.1% by Penske Corporation, 28.9% by us, and 30.0% by Mitsui. GE Capital no longer owns any ownership interests in PTL. We account for our investment in PTL under the equity method, and we therefore record our share of PTL’s earnings on our statements of income under the caption “Equity in earnings of affiliates,” which also includes the results of our other equity method investments.

2017 & 2018 Key Developments

Retail Automotive Franchised Dealership Acquisitions and Dispositions. In 2017, we acquired or were granted open points (new franchises awarded from the automotive manufacturer) representing thirteen automotive franchises, which represented approximately $500.0 million in annualized revenue. Of the retail automotive franchises acquired, two are located in New Jersey and represent the Jaguar and Land Rover brands, two are located in Arizona and represent the Mercedes-Benz and Sprinter brands, two are located in the U.K. and represent the BMW and MINI brands, and two are located in Germany and represent the Audi and Volkswagen brands. In 2017, we disposed of twenty-five retail automotive franchises, which represented approximately $270.0 million in annualized revenue. Of the franchises disposed of, nine represented franchises in Puerto Rico, five represented smart franchises in the U.S. and five represented BMW, MINI, and Lexus franchises in the U.K.

Acquisition of Stand-Alone Used Vehicle Dealerships. In the first quarter of 2017, we acquired CarSense in the U.S. and CarShop in the U.K., both businesses representing stand-alone used vehicle dealerships, which we believe complement our existing franchised retail automotive dealership operations and provide scalable opportunities across our market areas. Our CarSense operations consist of five locations operating in the Philadelphia and Pittsburgh, Pennsylvania market areas, including southern New Jersey. Our CarShop operations consist of five retail locations and a vehicle preparation center operating principally throughout Southern England. These businesses generated approximately $710.0 million in revenue in 2017.

In January 2018, we acquired The Car People, which has four large-scale retail locations operating across Northern England. Prior to our acquisition, The Car People sold approximately 18,000 vehicles per year and is expected to represent approximately $300.0 million in annualized revenue, which would bring our total projected annualized revenues from our fourteen stand-alone used vehicle locations to approximately $1.0 billion.

3

Investment in PTL. In September 2017, we acquired an additional 5.5% ownership interest in PTL, a leading provider of transportation services and supply chain management, from GE Capital for approximately $239.1 million in cash. Prior to this acquisition, we held a 23.4% ownership interest in PTL. PTL is currently owned 41.1% by Penske Corporation, 28.9% by us, and 30.0% by Mitsui. GE Capital no longer owns any ownership interests in PTL. We account for our investment in PTL under the equity method.

Issuance of 3.75% Senior Subordinated Notes. In August 2017, we issued $300.0 million of 3.75% senior subordinated notes due 2020. We used the proceeds of the 3.75% notes to repay amounts outstanding under our U.S. credit agreement and floor plan credit agreements, leaving us with additional flexibility to continue our acquisition strategy.

Shareholder Dividends and Stock Repurchases. We increased our quarterly stock dividend each quarter in 2017. Our latest declared dividend is $0.34 per share payable March 1, 2018, which represents a dividend yield of 2.6% using our January 31, 2018 closing stock price. We repurchased 302,000 shares of our common stock in 2017 for $12.7 million, which, together with quarterly dividends, represents a return to shareholders of approximately $121.1 million.

Company and Dealership Awards. Twenty of our dealerships in the U.S. were named by Automotive News as among the 100 “Best Dealerships to Work For” in 2017. In addition, our U.K. dealerships, collectively known as the Sytner Group, were ranked in the U.K. by the London Sunday Times as the “Best Big Company to Work For” in 2017. We believe these awards reflect our ongoing commitment to our valuable dealership employees, which enhances customer satisfaction and may result in improved sales over time. Additionally, in January 2018, PAG was named one of the “World’s Most Admired Companies” by Fortune Magazine.

Outlook

Retail Automotive Dealership. In 2017, U.S. light vehicle sales declined 1.8%, as compared to last year, to 17.2 million units, with passenger car sales declining 11.2%, while sales of trucks, crossovers and sport utility vehicles increased 4.4%. We believe the sales of trucks, crossovers and sport utility vehicles will continue to outperform passenger car sales, largely due to consumer preference. We believe the U.S. market for new light vehicle sales has plateaued and will be impacted by the level of OEM incentives, increasing lease returns, generally low interest rates, strong credit availability, low levels of unemployment, the age of vehicles on the road, vehicle innovation, and tax reform, although actual sales may differ materially. We also expect to see strength across the used vehicle market into 2018, as the number of lease returns increases providing customers with an additional supply of affordable late model, low mileage vehicles from which to choose.

In 2017, U.K. new vehicle registrations declined 5.7%, as compared to last year, to 2.5 million registrations. The U.K. market is represented 44% by the private market and 56% by business/fleet. Private market registrations decreased 6.8%, while business/fleet registrations decreased 4.7%. Although new vehicle sales declined in 2017, sales of the premium brands we represent outperformed these figures. U.K. sales are being negatively affected by the uncertainty of residual values and future tax rates on diesel powered vehicles, as the U.K. and Western European countries consider the ramifications of diesel engines on the environment. Sales of diesel powered vehicles experienced a 17% decline in sales in 2017. The March 2019 planned exit from the European Union (“Brexit”) may be causing and may continue to cause economic and political uncertainty, potentially impacting the economic environment, which may lead to further declines in new vehicle registrations in future periods. Since no country has previously left the European Union, the outcome of any future negotiations between the U.K. and the European Union is uncertain and may affect the timing, terms of trade, and the level of new vehicle registrations in those markets.

Retail Commercial Truck Dealership. In 2017, North American sales of Class 5-8 heavy and medium-duty trucks, the principal vehicles for our PTG business, were 499,932 units, an increase of 3.3% from 2016. The Class 5-7 medium-duty truck market increased 6.0% to 248,138 units from 234,163 units in 2016. The largest North American market, Class 8 heavy-duty trucks, increased 0.7% to 251,794 units from 249,952 units in 2016. According to ACT Research (“ACT”), retail sales of Class 8 heavy-duty trucks were generally expected to decline in 2017; however, generally strong economic conditions, the stabilization in the values of used trucks, improved freight metrics, and increased utilization pushed the

4

market to a stronger than expected performance in 2017. These conditions are expected to continue in 2018 with the market expected to increase with stronger Class 8 retail unit sales in North America.

Commercial Vehicle Distribution. Our PCV Australia distribution business and the on-highway portion of our PPS business each operate principally in the Australian and New Zealand heavy and medium-duty truck markets. In 2017, the Australian heavy-duty truck market reported sales of 12,002 units, representing an increase of 21.5% from 2016. The New Zealand market reported sales of 3,294 units in 2017, representing an increase of 23.0% from 2016. The brands we represent in Australia hold an 8.3% market share in the Australian heavy-duty truck market, and a 5.3% market share in New Zealand. The Australian heavy-duty commercial vehicle market had lagged behind historical sales levels in recent years partly due to difficult macroeconomic conditions and the relative weak price of commodities in these markets. However, recent improvements in the heavy-duty truck market and overall market conditions, as well as a moderate strengthening of the Australian Dollar, have led to increasing industry sales which we expect to continue into 2018. We also expect continued new order growth from the off-highway engine distribution business as a result of improving market conditions.

Penske Truck Leasing. We expect PTL to benefit from continued strong demand for its full-service truck leasing, truck rental and contract maintenance, and logistics services resulting from continued positive economic conditions in the United States and customers’ desire to increase efficiency and lower costs by outsourcing non-core responsibilities such as fleet ownership. As a global logistics services provider, we also expect PTL to experience increased demand for its logistics supply chain solutions based primarily on optimizing the use of drivers, trucks, warehouses, and other services within the supply chain. As a result of recent improvements in the truck market, in 2017 we saw modest freight growth and improved conditions within PTL’s commercial truck rental business, an increase in the utilization rate of its fleet, and stabilization of used truck prices. We anticipate that these improvements will continue into 2018.

As discussed in “Item 1A. Risk Factors,” there are a number of factors that could cause actual results to differ materially from our expectations. For a detailed discussion of our financial and operating results, see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Long-Term Business Strategy

Our long-term business strategy focuses on several key areas in an effort to foster long-term relationships with our customers and our associates. The key areas of our long-term strategy follow:

|

· Attract, develop, and empower associates to grow our business; |

|

· Diversification; |

|

· Offer outstanding brands in premium facilities and superior customer service; |

|

· Expand revenues at existing locations and increase higher-margin businesses; |

|

· Grow through strategic acquisitions; |

|

· Enhance customer satisfaction; |

|

· Leverage scale and implement “best practices”; and |

|

· Embrace digital marketing. |

Attract, Develop, and Empower Associates to Grow our Business

We view our local managers and associates as one of our most important assets. We operate in a decentralized manner that fosters an entrepreneurial spirit where each dealership or business unit has independent operational and financial management responsible for day-to-day operations. We believe experienced local managers are better qualified to make day-to-day decisions concerning the successful operation of a business unit and can be more responsive to our customers’ needs. We seek local management that not only has relevant industry experience, but is also familiar with the local market. We also have regional management that oversees operations and supports the local unit operationally and administratively. We invest for future growth and offer outstanding brands and facilities which we believe attract outstanding talent. We believe attracting the best talent and allowing our associates to make business decisions at the local level helps to foster long-term growth through increased repeat and referral business.

5

Diversification

Our business benefits from our diversified revenue mix, including the multiple revenue streams in a traditional dealership (new vehicles, used vehicles, finance and insurance, and service and parts operations), revenues from our retail commercial truck dealership operations, our commercial vehicle distribution operations, and returns relating to our joint venture investments, which we believe helps to mitigate the cyclicality that has historically impacted some elements of the automotive sector. We are further diversified within our retail automotive operations due to revenues generated from franchised dealerships and stand-alone used vehicle dealerships, due to our brand mix where we represent more than 40 brands, and geographically where we operate across more than 15 states and internationally. One of the unique attributes of our operations versus our peers is our diversification outside the U.S., with operations across nine countries.

The following table shows our consolidated revenues by country, and by state in the U.S., as a percentage of our total revenue:

|

Country |

|

% of Total 2017 Revenue |

|||

|

United States |

|

|

|

58 |

% |

|

United States Revenue by State |

|

|

|

|

|

|

Arizona |

|

6 |

% |

|

|

|

Arkansas |

|

2 |

% |

|

|

|

California |

|

11 |

% |

|

|

|

Connecticut |

|

3 |

% |

|

|

|

Florida |

|

3 |

% |

|

|

|

Georgia |

|

4 |

% |

|

|

|

Indiana |

|

1 |

% |

|

|

|

Maryland |

|

1 |

% |

|

|

|

Minnesota |

|

1 |

% |

|

|

|

New Jersey |

|

8 |

% |

|

|

|

New York |

|

1 |

% |

|

|

|

Ohio |

|

2 |

% |

|

|

|

Oklahoma |

|

1 |

% |

|

|

|

Pennsylvania |

|

1 |

% |

|

|

|

Puerto Rico |

|

1 |

% |

|

|

|

Rhode Island |

|

2 |

% |

|

|

|

Tennessee |

|

1 |

% |

|

|

|

Texas |

|

6 |

% |

|

|

|

Virginia |

|

2 |

% |

|

|

|

Wisconsin |

|

1 |

% |

|

|

|

United Kingdom |

|

|

|

33 |

% |

|

Germany/Italy |

|

|

|

6 |

% |

|

Canada |

|

|

|

1 |

% |

|

Australia/New Zealand/Pacific |

|

|

|

2 |

% |

The U.K. is the second largest automotive retail market in Western Europe as measured by new units sold. We generated 88% of our revenue in the U.K. through the sale and service of premium brands in 2017. We believe we are among the largest Audi, Bentley, BMW, Ferrari, Jaguar, Land Rover, Maserati, Mercedes-Benz, MINI, and Porsche dealers in the U.K. based on new unit sales. Additionally, we operate a number of dealerships in Germany, Western Europe’s largest automotive retail market, including through joint ventures with experienced local partners, which sell and service Audi, Lexus, Porsche, Toyota, Volkswagen and other brands. We also operate BMW, MINI, Maserati, Porsche, Audi, Land Rover and Volvo dealerships in Northern Italy, as well as BMW and MINI dealerships in Spain, through joint ventures with local partners. Our non-consolidated joint venture in Japan operates BMW, MINI, Rolls-Royce, Ferrari, and ALPINA dealerships.

Diversification Through Stand-Alone Used Vehicle Dealerships. Our acquisitions of CarSense in the U.S. and CarShop and The Car People in the U.K., each representing stand-alone used vehicle dealerships, complement and

6

provide more diversification to our retail automotive operations and provide scalable opportunities across our market areas.

Diversification Through Retail Commercial Truck Dealership. Our PTG business provides more diversification to our overall business model and allows us to bring our automotive dealership expertise to the retail commercial truck market. Recently acquired operations in Canada, in addition to our U.S. locations, further diversifies our revenue stream.

Diversification Through Penske Truck Leasing. We currently hold a 28.9% ownership interest in PTL, a leading provider of transportation services and supply chain management, which further diversifies our total results of operations. In September 2017, we increased our ownership interest in PTL from 23.4% to 28.9% as a result of our acquisition of an additional 5.5% ownership interest, as discussed previously, which further diversifies our earnings potential. We also expect to realize significant cash tax savings as a result of our investment in PTL in addition to the diversification offered by earnings from PTL.

Offer Outstanding Brands in Premium Facilities and Superior Customer Service

We offer outstanding brands in premium facilities and believe offering our customers a superior customer service experience will generate repeat and referral business and will help to foster a loyal and dedicated customer base. Customer satisfaction is measured at each of our automotive dealerships on a monthly, quarterly, and/or yearly basis by the manufacturers we represent, and we compensate our employees, in part, based on their performance in such rankings.

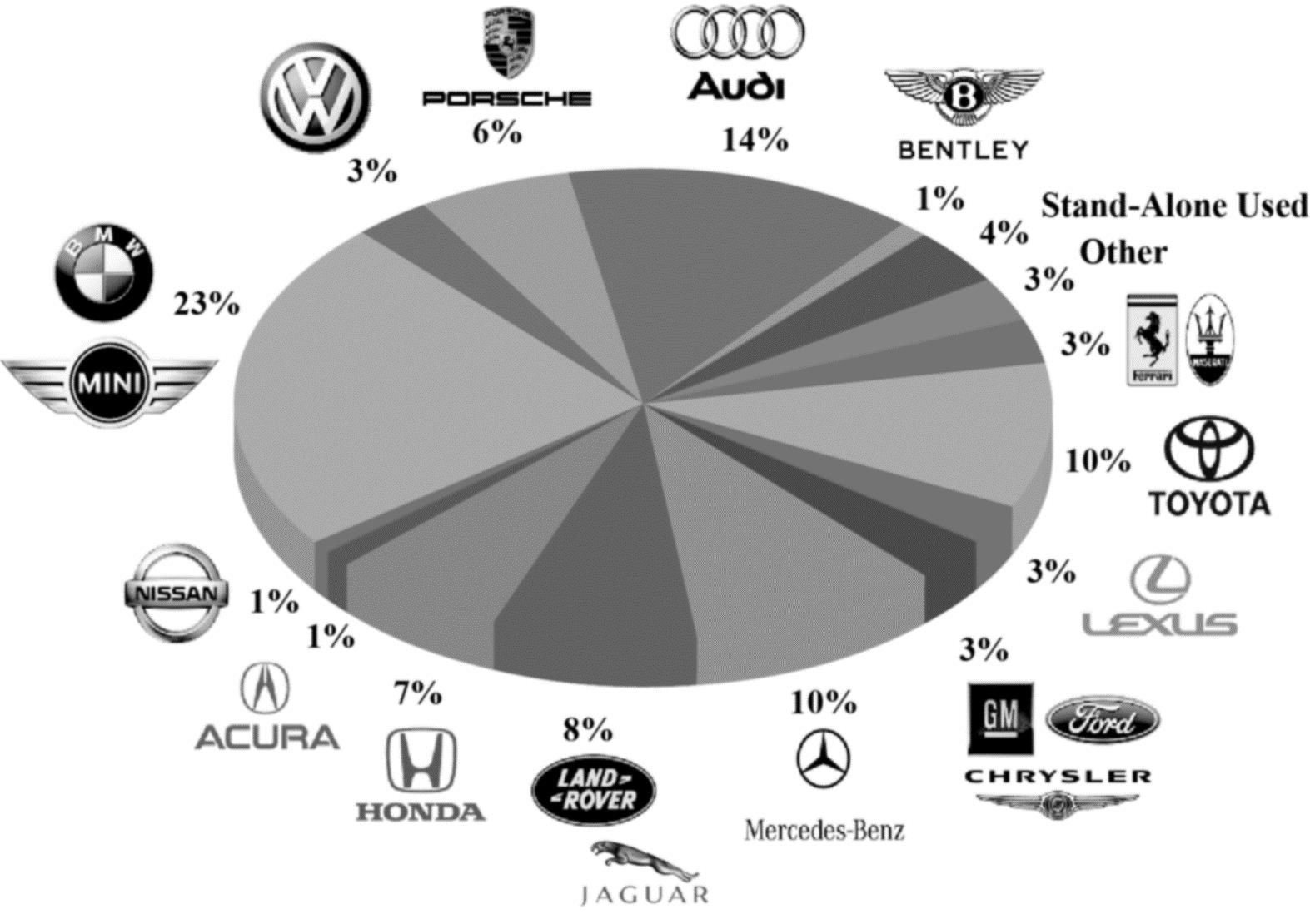

We sell over 40 brands in our markets and our automotive dealership revenue mix consists of 70% related to premium brands, 23% related to volume non-U.S. brands, 3% related to brands of U.S. based manufacturers, and 4% related to our stand-alone used vehicle dealerships. We believe our largely premium and non-U.S. brand mix will continue to offer us the opportunity to generate same-store growth, including higher margin service and parts sales. The following chart reflects our percentage of total retail automotive dealership revenue by brand:

We sell and service outstanding automotive brands in our premium facilities, in attractive geographic markets. Where advantageous, we aggregate our automotive dealerships in a campus setting in order to build a destination location for our customers, which we believe helps to drive increased customer traffic to each of the brands at the location. This strategy also creates an opportunity to reduce personnel expenses, consolidate advertising and administrative expenses and leverage operating expenses over a larger base of dealerships.

7

Our PTG dealerships provide a similar suite of services as our automotive dealerships, and similar to our retail automotive business, our retail commercial truck business is committed to providing outstanding brands and superior customer service in premium facilities. The necessity of repairing trucks for our customers is a key area of differentiation for our commercial truck dealerships, and we provide around-the-clock service in certain locations to get our customers’ commercial trucks back on the road so they can complete their routes.

Expand Revenues at Existing Locations and Increase Higher-Margin Businesses

Increase Same-Store Sales. We believe our emphasis on superior customer service and premium facilities will contribute to increases in same-store sales over time. We have added a significant number of incremental service bays in recent years in order to better accommodate our customers and further enhance our higher-margin service and parts revenues.

Grow Finance, Insurance, and Other Aftermarket Revenues. Each sale of a vehicle provides us the opportunity to assist in arranging financing for the sale of a vehicle, to sell the customer an extended service contract or other insurance product, and to sell aftermarket products, such as security systems and protective coatings. Where possible, we attempt to vertically integrate with the captive finance companies of the manufacturers we represent and to supplement these offerings with preferred lenders as necessary. In order to improve our finance and insurance business, we focus on enhancing training programs and implementing process improvements which we believe will improve our overall revenues.

Expand Service and Parts and Collision Repair Revenues. Today’s vehicles are increasingly complex and require sophisticated equipment and specially trained technicians to perform certain services. Additionally, many manufacturers today are offering maintenance programs packaged with the vehicle sale. These programs require customers to have the service work performed at a factory-authorized dealership. Unlike independent service shops, our dealerships are authorized to perform this work under warranties provided by manufacturers. Additionally, we offer maintenance programs for sale through our dealerships. We believe that our brand mix and the complexity of today’s vehicles, combined with our investment in expanded service facilities, including the addition of a significant number of incremental service bays in recent years, and our focus on customer service, will contribute to increases in our service and parts revenue. We also operate 38 automotive collision repair centers and six commercial truck collision centers which are integrated with local dealership operations. We offer rapid repair services such as paint-less dent repair, headlight reconditioning, wheel repairs, tire sales, seat sales for our retail commercial truck operations, and windshield replacement at most of our facilities in order to offer our customers the convenience of one-stop shopping for all of their vehicle requirements.

Grow Through Strategic Acquisitions

We believe that attractive retail automotive acquisition opportunities exist for well-capitalized dealership groups with experience in identifying, acquiring and integrating dealerships. The fragmented automotive retail market provides us with significant growth opportunities in our markets. We generally seek to acquire dealerships with high-growth automotive brands in highly concentrated or growing demographic areas that will benefit from our management expertise, manufacturer relations and scale of operations, as well as smaller, single location dealerships that can be effectively integrated into our existing operations. Over time, we have also been awarded new franchises from various manufacturers. In 2017, we acquired or were granted open points representing thirteen franchises, which generated approximately $500.0 million in annualized revenue.

In 2017, we acquired CarSense in the U.S. and CarShop in the U.K., both businesses representing stand-alone used vehicle dealerships, which we believe complement our retail automotive dealership operations and provide scalable opportunities across our market areas. These businesses generated approximately $710.0 million in revenue in 2017. We believe there are attractive acquisition opportunities to grow these operations in both the U.S. and the U.K., and in January 2018, we acquired The Car People in the U.K., as discussed previously, which is expected to represent approximately $300.0 million in annualized revenue.

8

We believe there are attractive retail commercial truck acquisition opportunities. We see continued growth in the brands we represent at our existing retail commercial truck dealerships and believe there are opportunities for us to continue to make strategic acquisitions over time.

Enhance Customer Satisfaction

We strive for superior customer satisfaction. By offering outstanding brands in premium facilities, “one-stop” shopping convenience in our aggregated facilities, and a well-trained and knowledgeable sales staff, we aim to forge lasting relationships with our customers, enhance our reputation in the community, and create the opportunity for significant repeat and referral business. We monitor customer satisfaction data to track the performance of operations, and incent our personnel to provide exceptional customer service, thereby driving increased customer loyalty and enhancing our reputation.

Reputation management is an extremely important and powerful business tool. Our reputation management strategy, which includes encouraging, monitoring, and responding to customer reviews, is crucial for generating and maintaining trust and customer loyalty in a competitive market. We proactively monitor online reputation management sites, including Google and Yelp, among others, to enhance our online presence, build loyalty, assess customer comments, ensure we are offering a superior customer service experience, and ultimately drive sales and profitability. We encourage customer reviews and have automated tools in place that make it easy for customers to review our business. Analysis of online reviews provides us valuable operational insights that we leverage to foster customer loyalty, stay ahead of the competition, and drive new sales.

Leverage Scale and Implement “Best Practices”

We seek to build scale in many of the markets where we have operations. Our desire is to reduce or eliminate redundant administrative costs such as accounting, payroll, information technology systems and other general administrative costs. In addition, we seek to leverage our industry knowledge and experience to foster communication and cooperation between like brand dealerships throughout our organization. Corporate management and local management meet regularly to review operating performance, examine industry trends, and implement operating improvements. Key financial information is discussed and compared across all markets. This frequent interaction facilitates implementation of successful strategies throughout the organization.

Embrace Digital Marketing

With consumers becoming increasingly immersed in the digital space, we have adopted a comprehensive digital marketing strategy that encompasses all avenues of customer engagement including websites, social media, video, mobile, email marketing, online advertising, search engine optimization, branding, and content. We strive to build and optimize our presence across all digital platforms to deliver a seamless and transparent experience for our customers.

To attract customers and enhance our customer service, each of our dealerships uses a custom content management system (CMS) to maintain its own website. All of our dealership websites have consistent functionality and responsive formats, except where otherwise required by original equipment manufacturers, which helps to minimize costs and provide a consistent image across dealerships.

To drive high quality traffic to our web properties, we primarily focus on search engine optimization and search engine marketing, and employ some third-party lead providers in key markets to augment our traffic. Most importantly, we have invested heavily in our own websites so we can retain traffic and deliver a quality experience. We operate with a “mobile first” mentality and have ensured that the content we serve our customers is tailored to their method of engagement with us, the device they are using, and their specific requests, where applicable. We believe the majority of our web traffic comes from mobile devices, making this approach important as a key driver of our success.

We promote our U.S. and U.K. automotive retail new and pre-owned vehicle inventory online through PenskeCars.com and Sytner.co.uk, respectively. The websites are designed to streamline the car-buying process and allow consumers to view and compare on average over 50,000 new, certified and pre-owned vehicles. These sites, together with our dealership websites, provide consumers a simple way to schedule service appointments online 24/7 and

9

view extensive vehicle information, including photos, prices, promotions, videos, and third-party vehicle history reports for pre-owned vehicles. Additionally, customers may download a PenskeCars.com app to access vehicle inventory, locate or contact a dealership, explore payments, and get instant trade offers at their convenience.

To help us continue to develop the online experience, we research consumer behavior and survey our customers to validate our approach and help guide our site design. Customers, now more than ever, are interested in a transparent and quick process, and use the web as a way to educate themselves about their potential purchase and save time during the purchase process. To further our digital strategy, and respond to changing consumer preferences, we created a digital retailing experience, called Preferred Purchase, for our U.S. dealerships that incorporates new online functionality to streamline the sales process in our traditional business model. Preferred Purchase allows customers to value trade-in vehicles, review pricing, leasing and financing options, manufacturer incentive programs, and pre-qualify for credit, all online without visiting the dealership. This functionality is integrated and automated on a single platform that resides on both our individual dealership sites as well as our corporate sites. Preferred Purchase promotes transparency and is intended to speed up customer transaction times and give our customers the flexibility to choose the path or sales process most comfortable to them. We continue to assess consumers’ purchasing habits, opinions, and preferences to ensure we are meeting consumer needs and making the right investments in new technology.

Social media is an optimal platform to proactively communicate with our customers and receive input on our service, branding, and online engagement. Our dealerships maintain social media pages, including Facebook, Instagram and Twitter, among others, to attract new customers, build stronger relationships with current customers, and help grow the business. Using a social media mobile app, our dealerships can easily capture customer photos, send review invitations, record videos, and submit content for their social media sites. Social media is an ever-increasing and critical part of our digital strategy, and one of the most powerful and cost-effective ways to engage with our customers, enhance brand visibility, and generate customer leads. By choosing a specific audience using a range of demographic tools, our dealerships are able to reach targeted potential customers effectively and efficiently.

10

Retail Automotive Dealership Operations

Retail Automotive Franchises. We routinely acquire and dispose of retail automotive franchises. Our financial statements include the results of operations of acquired dealerships from the date of acquisition. We expect to continue to pursue acquisitions and selected dispositions in the future. The following table exhibits our retail automotive franchises by location and manufacturer as of December 31, 2017:

|

Location |

|

Franchises |

|

Franchises |

|

U.S. |

|

Non-U.S. |

|

Total |

|

Arizona |

|

26 |

|

BMW/MINI |

|

22 |

|

44 |

|

66 |

|

Arkansas |

|

11 |

|

Toyota/Lexus |

|

24 |

|

1 |

|

25 |

|

California |

|

29 |

|

Mercedes-Benz/Sprinter/smart |

|

17 |

|

25 |

|

42 |

|

Connecticut |

|

9 |

|

Audi/Volkswagen/Bentley |

|

18 |

|

51 |

|

69 |

|

Florida |

|

6 |

|

Chrysler/Jeep/Dodge/Fiat/Alfa Romeo |

|

8 |

|

— |

|

8 |

|

Georgia |

|

4 |

|

Honda/Acura |

|

21 |

|

— |

|

21 |

|

Indiana |

|

2 |

|

Ferrari/Maserati |

|

4 |

|

12 |

|

16 |

|

Maryland |

|

2 |

|

Porsche |

|

8 |

|

11 |

|

19 |

|

Minnesota |

|

2 |

|

Jaguar/Land Rover |

|

12 |

|

20 |

|

32 |

|

New Jersey |

|

26 |

|

Lamborghini |

|

1 |

|

4 |

|

5 |

|

Ohio |

|

7 |

|

Nissan/Infiniti |

|

4 |

|

— |

|

4 |

|

Puerto Rico |

|

4 |

|

Cadillac/Chevrolet |

|

5 |

|

— |

|

5 |

|

Rhode Island |

|

9 |

|

Others |

|

11 |

|

20 |

|

31 |

|

Tennessee |

|

1 |

|

Total |

|

155 |

|

188 |

|

343 |

|

Texas |

|

9 |

|

|

|

|

|

|

|

|

|

Virginia |

|

6 |

|

|

|

|

|

|

|

|

|

Wisconsin |

|

2 |

|

|

|

|

|

|

|

|

|

Total U.S. |

|

155 |

|

|

|

|

|

|

|

|

|

U.K. |

|

143 |

|

|

|

|

|

|

|

|

|

Germany |

|

29 |

|

|

|

|

|

|

|

|

|

Italy |

|

16 |

|

|

|

|

|

|

|

|

|

Total Non-U.S. |

|

188 |

|

|

|

|

|

|

|

|

|

Total Worldwide |

|

343 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Retail Automotive Stand-Alone Used Vehicle Dealerships. The following table exhibits the stand-alone used vehicle dealerships we currently operate by geographic location:

|

Location |

|

Number of Dealerships |

|

U.S. |

|

|

|

Pennsylvania |

|

4 |

|

New Jersey |

|

1 |

|

Total U.S. |

|

5 |

|

U.K. |

|

|

|

CarShop |

|

5 |

|

The Car People (1) |

|

4 |

|

Total U.K. |

|

9 |

|

Total |

|

14 |

|

|

|

|

|

(1) Acquired in January 2018 |

||

New Vehicle Retail Sales. In 2017, we retailed 248,774 new vehicles which generated 48.8% of our retail automotive dealership revenue and 25.5% of our retail automotive dealership gross profit. New vehicles are typically acquired by dealerships directly from the manufacturer. We strive to maintain outstanding relationships with the automotive manufacturers, based in part on our long-term presence in the retail automotive market, our commitment to providing premium facilities, our commitment to drive customer satisfaction, the reputation of our management team and the

11

consistent sales volume at our dealerships. Our dealerships finance the purchase of most new vehicles from the manufacturers through floor plan financing provided primarily by various manufacturers’ captive finance companies.

Used Vehicle Retail Sales. In 2017, we retailed 252,922 used vehicles, which generated 32.2% of our retail automotive dealership revenue and 12.2% of our retail automotive dealership gross profit. We acquire used vehicles from various sources including auctions open only to authorized new vehicle dealers, public auctions, trade-ins from consumers in connection with their purchase of a new vehicle from us, and lease expirations or terminations. To improve customer confidence in our used vehicle inventory, we provide vehicle history reports for all used vehicles and virtually all of our franchised new vehicle dealerships participate in manufacturer certification processes for used vehicles. If certification is obtained, the used vehicle owner is typically provided benefits and warranties similar to those offered to new vehicle owners by the applicable manufacturer. Most of our dealerships have implemented software tools which assist in procuring and selling used vehicles. In the U.K., we offer used vehicles to wholesalers and other dealers via online auction.

We currently operate fourteen stand-alone used vehicle dealerships in the U.S. and U.K. While we operate these dealerships under separate names (CarSense, CarShop and The Car People), each of these dealerships are committed to offering high quality “like-new” used vehicles at “no-haggle” prices. These businesses typically sell low mileage, high quality vehicles in a friendly and transparent buying experience. We acquired these businesses in 2017 and 2018, but each has a long history of serving their local communities. We include the results of our stand-alone used vehicle dealerships within used vehicle retail sales.

Vehicle Finance, Extended Service and Insurance Sales. Finance, extended service and insurance sales represented 2.9% of our retail automotive dealership revenue and 19.9% of our retail automotive dealership gross profit in 2017. At our customers’ option, our dealerships can arrange third-party financing or leasing in connection with vehicle purchases. We typically receive a portion of the cost of the financing or leasing paid by the customer for each transaction as a fee. While these services are generally non-recourse to us, we are subject to chargebacks in certain circumstances, such as default under a financing arrangement or prepayment. These chargebacks vary by finance product, but typically are limited to the fee we receive.

We also offer our customers various vehicle warranty and extended protection products, including extended service contracts, maintenance programs, guaranteed auto protection (known as “GAP,” this protection covers the shortfall between a customer’s loan balance and insurance payoff in the event of a total loss), lease “wear and tear” insurance and theft protection products. The extended service contracts and other products that our dealerships currently offer to customers are underwritten by independent third parties, including the vehicle manufacturers’ captive finance companies. Similar to finance transactions, we are subject to chargebacks relating to fees earned in connection with the sale of certain extended protection products. We also offer for sale other aftermarket products, including security systems and protective coatings.

We offer finance and insurance products using a “menu” process, which is designed to ensure that we offer our customers a complete range of finance, insurance, protection, and other aftermarket products in a transparent manner. We provide training to our finance and insurance personnel to help ensure compliance with internal policies and procedures, as well as applicable state regulations.

Service and Parts Sales. Service and parts sales represented 10.4% of our retail automotive dealership revenue and 41.7% of our retail automotive dealership gross profit in 2017. We generate service and parts sales in connection with warranty and non-warranty work performed at each of our dealerships. We believe our service and parts revenues benefit from the increasingly complex technology used in vehicles that makes it difficult for independent repair facilities to maintain and repair today’s automobiles.

A goal of each of our dealerships is to make each vehicle purchaser a customer of our service and parts department. Our dealerships keep detailed records of our customers’ maintenance and service histories, and many dealerships send reminders to customers when vehicles are due for periodic maintenance or service. Many of our dealerships have extended evening and weekend service hours for the convenience of our customers. We also offer rapid repair services such as paint-less dent repair, headlight reconditioning, wheel repairs, tire sales and windshield replacement at most of our facilities in order to offer our customers the convenience of one-stop shopping for all of their automotive

12

requirements. We also operate 38 automotive collision repair centers, each of which is operated as an integral part of our dealership operations.

Fleet and Wholesale Sales. Fleet and wholesale sales represented 5.7% of our retail automotive dealership revenue and 0.7% of our retail automotive dealership gross profit in 2017. Fleet activities represent the sale of new units to customers that are deemed to not be retail customers such as cities, municipalities or rental car companies, and are generally sold at contracted amounts. Wholesale activities relate to the sale of used vehicles generally to other dealers and occur at auction. Vehicles sold through this channel generally include units acquired by trade-in that do not meet certain standards or aged units.

Retail Commercial Truck Dealership Operations

We operate a heavy and medium-duty truck dealership group known as Premier Truck Group (“PTG”) with locations in Texas, Oklahoma, Tennessee, Georgia, and Canada. As of December 31, 2017, PTG operated twenty locations, including fourteen full-service dealerships and six collision centers, offering primarily Freightliner and Western Star branded trucks. PTG also offers a full range of used trucks available for sale as well as service and parts departments, providing a full range of maintenance and repair services. This business generated $1,048.0 million of revenue in 2017.

PTG dealerships provide a similar suite of services as our automotive dealerships, offering new trucks and a large selection of used trucks for sale, a full range of parts, maintenance and repair services, and finance and insurance options for its customers by facilitating truck and trailer financing and leasing, extended maintenance plans, physical damage insurance, GAP insurance, roadside relief and other programs.

The necessity of repairing trucks for our customers is a key area of differentiation for our commercial truck dealerships, and we provide around-the-clock service in certain locations to get our customers’ commercial trucks back on the road so they can complete their routes. PTG also carries an extensive inventory of parts for the new and used trucks they sell and service, including Thomas Built Buses, and other makes of medium and heavy-duty trucks. The service and parts business of our PTG commercial truck dealerships represents approximately 73% of our retail commercial truck dealership gross profit.

Similar to our retail automotive business, PTG is committed to providing outstanding brands and superior customer service in premium facilities. For example, our Dallas Freightliner location offers a state-of-the-art facility of climate controlled office space, service shops, customer amenities, parts inventory storage, and a parts showroom. This facility is equipped with 80 full-service truck bays with a full suite of on-hand parts inventory. Guests of Dallas Freightliner enjoy a television lounge with HDTV theater seating, a large comfortable customer lounge with lockers, laundry and shower facilities, on-site trailer parking, and free recreational vehicle electrical hook-up.

Commercial Vehicle Distribution Operations

Penske Commercial Vehicles Australia. We are the exclusive importer and distributor of Western Star heavy-duty trucks (a Daimler brand), MAN heavy and medium-duty trucks and buses (a VW Group brand), and Dennis Eagle refuse collection vehicles, together with associated parts, across Australia, New Zealand and portions of the Pacific. This business, known as Penske Commercial Vehicles Australia (“PCV Australia”), distributes commercial vehicles and parts to a network of more than 70 dealership locations, including eight company-owned retail commercial vehicle dealerships. This business generated $250.3 million of revenue in 2017.

Our local headquarters is located in Brisbane, Australia, which is the country’s third largest city. Our headquarters includes administrative facilities as well as a parts distribution center and a production center. We also have a parts distribution center in Auckland, New Zealand.

Western Star trucks are manufactured by Daimler Trucks North America in Portland, Oregon. These technologically advanced, custom-built vehicles are ordered by customers to meet their particular needs for line haul, long distance road train, mining, logging and other heavy-duty applications. We are also the exclusive importer of MAN trucks and buses. MAN Truck and Bus, a VW Group company, is a leading producer of medium and heavy-duty trucks as well as city and coach buses. These cab-forward, fuel efficient vehicles are principally produced in several sites in Germany and are

13

ordered by customers for line haul, local distribution, mining and other off-road applications. Dennis Eagle refuse collection vehicles are manufactured by Ros Roca in Warwick, England. Together these brands represented 8.3% of heavy-duty truck units sold in Australia and 5.3% in New Zealand during 2017.

Our commercial vehicle distribution operations include six company-owned retail commercial vehicle dealerships in Australia and two company-owned retail commercial vehicle dealerships in New Zealand. Our dealership in Brisbane, Australia is the largest retailer of Western Star Trucks in Australia by volume. We finance our purchases of these vehicles under floor plan agreements with a local Daimler affiliate and a local Volkswagen affiliate with terms similar to our other floor plan agreements.

Penske Power Systems. We are also a leading distributor of diesel and gas engines and power systems, principally representing MTU, Detroit Diesel, Mercedes-Benz Industrial, Allison Transmission and MTU Onsite Energy. This business, known as Penske Power Systems (“PPS”), offers products across the on- and off-highway markets in Australia, New Zealand and portions of the Pacific, including trucking, mining, power generation, construction, industrial, rail, marine, agriculture, oil & gas, and defense, and supports full parts and aftersales service through a network of branches, remote field service locations, and dealers across the region. This business generated $260.7 million of revenue in 2017.

Penske Power Systems’ principal headquarters is located at its Melbourne workshop/office facility. In addition to sales, distribution and full product repair capability, this facility includes the offices for national sales, engineering and marketing, a regional training facility, and a regional engineering center. In addition, PPS operates a corporate office based at its Sydney (Chipping Norton) branch which is dedicated to corporate activities, distribution and product repair capability, and retail truck sales. PPS operates 14 branch facilities across Australia and in Auckland, New Zealand, and utilizes mobile remote field service units travelling directly to customer premises.

Penske Power Systems’ 79 dealers are strategically located throughout Australia, New Zealand and the Pacific. Most of the dealers (67) represent the Detroit Diesel brand, with the majority aligned to Western Star and/or Freightliner truck manufacturers. The remaining dealers represent the MTU (1) and Allison Transmission (11) brands. The “off-highway” business of PPS principally includes the sale of power systems by PPS directly to customers in the commercial, defense and maritime sectors, and to several dealers.

Penske Truck Leasing

We currently hold a 28.9% ownership interest in PTL, a leading provider of transportation services and supply chain management. PTL is capable of meeting customers’ needs across the supply chain with a broad product offering that includes full-service truck leasing, truck rental and contract maintenance, along with logistics services such as dedicated contract carriage, distribution center management, transportation management and lead logistics provider. PTL has a highly diversified customer base that includes multi-national corporations across industries such as food and beverage, transportation, manufacturing, automotive, retail and healthcare, with whom they have long-term contracts, as well as individual consumers renting a single truck on a daily basis.

PTL operates one of the leading full-service truck leasing, truck rental and contract maintenance businesses in North America, and an international logistics business in North America, South America, Europe and Asia. PTL also operates its truck leasing and truck rental business in Australia through a joint venture with us.

Full-service truck leasing, truck rental and contract maintenance. Full-service truck leasing, truck rental and contract maintenance of commercial trucks, tractors and trailers is PTL’s largest business. PTL manages a fleet of approximately 269,000 trucks, tractors and trailers, consisting of approximately 185,500 vehicles owned by PTL and leased to customers under full-service lease or rental agreements and approximately 83,500 customer-owned and -operated vehicles for which they provided contract maintenance services. Terms under its full-service leases generally range from four to seven years for tractors and trucks and six to ten years for trailers. Its commercial and consumer rental fleet as of December 31, 2017 consisted of approximately 66,400 vehicles for use by its full-service truck leasing, small business and consumer customers for periods generally ranging from less than a day to 12 months. Most of its leased vehicles are configured according to customer specifications, including custom painting and lettering, while its rental trucks bear Penske branding.

14

Commercial customers often outsource to PTL in order to reduce the complexity, cost and total capital associated with vehicle ownership. Under a full-service lease, PTL provides and fully maintains the vehicle, which is generally specifically configured for the customer. The services provided under full-service lease and contract maintenance agreements generally include preventive and regular maintenance, advanced diagnostics, emergency road service, fleet services, safety programs, and nationwide fuel services through its network of company-operated facilities and a nationwide network of independent truck stops. In addition, PTL makes available to its full-service leasing and contract maintenance customers additional vehicles on a rental basis. This short-term availability of tractors, trucks and trailers typically accommodates seasonal, emergency and other temporary needs. A significant portion of these rentals are to existing full-service leasing and contract maintenance customers who are seeking flexibility in their fleet management. PTL has established a network of approximately 700 locations to provide full-service truck leasing, truck rental and contract maintenance services to customers. This network enables PTL to meet multi-location customer requirements. PTL’s commercial rental business generated 20% of its operating revenue for 2017 and its full-service lease and contract maintenance business generated 50% of its operating revenue in 2017.

For consumer customers, PTL provides short-term rental of light and medium-duty vehicles on a one-way and local basis, typically to transport household goods. Customers typically include local small businesses and individuals seeking a do-it-yourself solution to their moving needs. PTL’s fleet consists of late model vehicles ranging in size from small vans to 26-foot trucks, and its consumer rentals are conducted through approximately 1,860 independent rental agents and approximately 360 of its company-operated leasing and rental facilities. PTL’s consumer business generated 7% of its operating revenue for 2017.

Logistics. PTL’s logistics business offers a broad variety of services, such as dedicated contract carriage, distribution center management, transportation management, freight brokerage and lead logistics provider. PTL coordinates and provides services for its customers across the supply chain, including: inbound material flow, handling and packaging, inventory management, distribution and technologies, and sourcing of third-party carriers. These offerings are available individually or on a combined basis and often involve its associates performing services at the customer’s location. By offering a scalable series of services to its customers, PTL can manage the customer’s entire supply chain or any stand-alone service. PTL also utilizes specialized software that enables real-time fleet visibility and provides reporting metrics, giving customers detailed information on fuel economy and other critical supply chain costs. PTL’s international logistics business has approximately 380 locations in North America, South America, Europe and Asia. PTL’s logistics business generated 23% of its operating revenue for 2017.

Industry Information

Retail Automotive Dealership. Approximately 59% of our retail automotive dealership revenues are generated in the U.S., which in 2017 was the world’s second largest automotive retail market as measured by units sold. In 2017, sales of new cars and light trucks were approximately 17.2 million units, a decrease of 1.8% from 2016, and were generated at approximately 18,200 franchised new-car dealerships. According to the latest available data from the National Automobile Dealers Association, dealership revenue is derived as follows: 58% from new vehicle sales, 30% from used vehicle sales, and 12% from service and parts sales. Dealerships also offer a wide range of higher-margin products and services, including extended service contracts, financing arrangements and credit insurance. The National Automobile Dealers Association figures noted above include finance and insurance revenues within either new or used vehicle sales, as sales of these products are usually incremental to the sale of a vehicle.

In the U.S., the franchised automotive dealer industry is the largest retail business by revenue, with virtually all new cars and light trucks bought in the U.S. through franchised dealers in a market in excess of $1.0 trillion. Publicly held automotive retail groups account for less than 10% of total industry revenue. Although significant consolidation has already taken place, the industry remains highly fragmented, with more than 90% of the U.S. industry’s market share remaining in the hands of smaller regional and independent players. Our other markets are similarly fragmented. We believe that further consolidation in these markets is probable due to the significant capital requirements of maintaining manufacturer facility standards and the limited number of viable alternative exit strategies for dealership owners.

Our European markets consist of Germany, the U.K., Italy, and Spain, which represented the first, second, fourth, and fifth largest automotive retail markets, respectively, in Western Europe in 2017, and accounted for approximately 64% of the total vehicle sales in Western Europe. Unit sales of automobiles in Western Europe were approximately 14.3

15

million in 2017, a 2.5% increase compared to 2016. In Germany, the U.K., Italy, and Spain, new car sales were approximately 3.4 million, 2.5 million, 2.0 million and 1.2 million units, respectively, in 2017.

We also own a 49% interest in a Japanese joint venture. Unit sales in Japan were 5.2 million in 2017, an increase of 5.6% from 2016.

We also operate fourteen stand-alone used vehicle dealerships in the U.S. and the U.K. Used vehicle sales are even more fragmented than new vehicle sales and are generated by new car dealerships, used vehicle “superstores,” individual small lot sellers, as well as individual to individual sales. Used vehicle sales were approximately 40 million units in the U.S. and approximately 8 million units in the U.K. in 2017.

Retail Commercial Truck Dealership. In 2017, North America sales of Class 5-8 medium and heavy-duty trucks, the principal vehicles for our PTG business, were approximately 499,932 units, an increase of 3.3% from 2016. The Class 5-7 medium-duty truck market increased 6.0% to 248,138 units from 234,163 units in the same period in 2016. The largest market, Class 8 heavy-duty trucks, increased 0.7% to approximately 251,794 units from approximately 249,952 units in 2016. In this market, our principal brands, Freightliner and Western Star, represent approximately 39.7% of that market.

Commercial Vehicle Distribution. Our commercial vehicle distribution business operates principally in Australia and New Zealand. In 2017, heavy-duty truck sales in Australia and New Zealand combined were 15,296 units, representing an increase of 21.8% from 2016. The brands we represent in Australia hold an 8.3% market share in the Australian heavy-duty truck market, and a 5.3% market share in New Zealand.

Penske Truck Leasing. PTL participates broadly in the global supply chain, estimated at $8.2 trillion annually, and particularly in the U.S. supply chain, estimated at $1.5 trillion annually. Only 11% of the total U.S. supply chain function is outsourced to third parties, such as PTL. We estimate, based on R. L. Polk registration data, that there are approximately 8.1 million commercial trucks operating in the United States, of which up to 4.0 million could be potential opportunities for PTL’s full-service leasing and contract maintenance offerings.

Dealership. Generally, new vehicle unit sales are cyclical and, historically, fluctuations have been influenced by factors such as manufacturer incentives, interest rates, fuel prices, unemployment, inflation, weather, the level of personal discretionary spending, credit availability, consumer confidence and other general economic factors. However, from a profitability perspective, automotive and truck retailers have historically been less vulnerable than manufacturers and parts suppliers to declines in new vehicle sales. We believe this is due to the retailers’ more flexible expense structure (a significant portion of the retail industry’s costs are variable) and their diversified revenue streams such as used vehicle sales and service and parts sales. In addition, manufacturers may offer various dealer incentives when sales are slow, which further increases the volatility in profitability for manufacturers and may help to decrease volatility for franchised automotive retailers.

Business Description

Information Technology and Customer Privacy

We consolidate financial, accounting and operational data received from our local operations through private data communications networks. Local operating data is gathered and processed through individual systems utilizing common centralized management systems predominately licensed from, and in many cases operated by, third parties. Our local systems follow our standardized accounting procedures and are compliant with any guidelines established by our vehicle manufacturers. Our database technology allows us to extract and aggregate data from the systems in a consistent format to generate consolidated financial and operational analysis. These systems also allow us to access detailed information for each individual location, as a group, or on a consolidated basis. Information we can access includes, among other things, inventory, cash, unit sales, the mix of new and used vehicle sales and sales of aftermarket products and services. Our ability to access this data allows us to continually analyze our local results of operations and financial position so as to identify areas for improvement.

We utilize common customer relationship management systems that assist us in identifying customer opportunities and responding to customer inquiries. We utilize compliance systems that assist us with our regulatory obligations and

16

assist us in maintaining the privacy of the information we receive from customers that we collect, process, and retain in the normal course of our business. We have adopted rigorous customer information safeguard programs and “red flag” policies to assist us in maintaining customer privacy.

As part of our business model, we receive personal information regarding customers, associates and vendors, from various online and offline channels. Our internal and third-party systems are under a moderate level of risk from hackers or other individuals with malicious intent to gain unauthorized access to our systems. Cyber-attacks are growing in number and sophistication thus presenting an ongoing threat to systems, whether internal or external, used to operate the business on a day to day basis. We perform periodic control testing and audits on our systems. Despite these measures, our facilities and systems, and those of our third-party service providers, could be vulnerable to security breaches, computer viruses, or other events. Any security breach or event resulting in the unauthorized disclosure of confidential information, or degradation of services provided by critical business systems, whether by us directly or our third-party service providers, could adversely affect our business operations, sales, reputation with current and potential customers, associates or vendors, as well as other operational and financial impacts derived from investigations, litigation, imposition of penalties, or other means.

Marketing

Retail Automotive Dealership. Our marketing strategy focuses on our individual businesses to capitalize on local branding, as well as corporate programs and web presence, which allows us to leverage scale and our parent brand recognition. We align ourselves with the marketing implemented by our OEM partners for their respective brands and integrate those initiatives and resources across the brands we represent.

The central core of our marketing strategy revolves around a data-driven approach that combines key metrics and trends from industry and consumer studies, our customer relationship management systems, and performance data from our businesses. This approach emphasizes objectivity and transparency in our marketing efforts and allows us to measure and gauge our success.

Our dealerships have strong local brand and name recognition and are respected in their communities. As such, we focus our efforts on our individual businesses to capitalize on their strong local reputation. To supplement local marketing, we implement corporate initiatives that link our local businesses to leverage scale and our parent brand recognition.

We leverage scale by using consistent performance metrics across the group to identify best practices and opportunities to negotiate enterprise arrangements for key marketing partners. A single, unified, customer relationship management tool is used by our new vehicle dealerships in the U.S. to enhance and streamline customer communication, provide visibility into our sales pipeline, and measure return on investment across the organization.

To attract customers and enhance customer service, each of our dealerships maintains its own website platform. All dealership websites have consistent functionality and responsive formats, except where otherwise required by vehicle manufacturers, which helps to minimize costs and provides a consistent image across dealerships. In addition to the dealership websites, we advertise most of our U.S. and U.K. automotive retail new and pre-owned vehicle inventory online through PenskeCars.com and Sytner.co.uk, as discussed previously under “Embrace Digital Marketing” above.

Consistent with our data-driven approach, as consumer activity continues to move toward digital, our marketing strategy places a strong emphasis on all forms of digital marketing. We strive to build and optimize our online presence across multiple platforms in order to drive high quality traffic to our business and maintain consistent and professional messaging. By focusing on social media, video, mobile, email marketing, online advertising, search engine optimization, branding, and content, we proactively optimize all avenues of digital customer engagement.

We monitor customer satisfaction data to track the performance of operations, and incent our personnel to provide exceptional customer service, thereby driving increased customer loyalty. Social media is a highly-valued element of our marketing strategy that allows us to engage with customers, build dealership awareness and enhance repeat and referral business. Additionally, we leverage corporate social media efforts and partners to benefit our dealerships and create a

17

strong sense of community. Online reputation management sites, such as Google and Yelp, are proactively monitored to ensure we are offering a superior customer experience.

Through our marketing strategy, we aim to forge lasting relationships with our customers, enhance our reputation, and create the opportunity for significant repeat and referral business.

Retail Commercial Truck Dealership and Commercial Vehicle Distribution. We market commercial trucks in the U.S. and Canada and commercial vehicles and other products in Australia and New Zealand principally through a network of dealership and service locations, supported by corporate level marketing efforts. Our digital marketing leverages manufacturer websites supplemented by brand specific websites to promote our brands. We also employ local sponsorships to generate brand awareness in our markets and market to customers at various trade shows and other industry events. While we rely on our dealerships and service locations to market to local customers, we typically assign a regional sales manager to oversee local dealer marketing efforts.

Agreements with Vehicle Manufacturers