Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - Terra Income Fund 6, Inc. | a93017exhibit32.htm |

| EX-31.2 - EXHIBIT 31.2 - Terra Income Fund 6, Inc. | a93017exhibit312.htm |

| EX-31.1 - EXHIBIT 31.1 - Terra Income Fund 6, Inc. | a93017exhibit311.htm |

| EX-10.3 - EXHIBIT 10.3 - Terra Income Fund 6, Inc. | a93017exhibit103.htm |

| EX-10.2 - EXHIBIT 10.2 - Terra Income Fund 6, Inc. | a93017exhibit102.htm |

| EX-10.1 - EXHIBIT 10.1 - Terra Income Fund 6, Inc. | a93017exhibit101.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended September 30, 2017

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 814-01136

Terra Income Fund 6, Inc.

(Exact name of registrant as specified in its charter)

Maryland | 46-2865244 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

805 Third Avenue, 8th Floor

New York, New York 10022

(Address of principal executive offices)

(212) 753-5100

(Registrant’s telephone number, including area code)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933.Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934.Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Accelerated filer o | |

Non-accelerated filer þ (Do not check if a smaller reporting company) | Smaller reporting company o | |

Emerging growth company þ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. þ

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).Yes o No þ

As of November 20, 2017, the registrant had 7,936,167 shares of common stock, $0.001 par value, outstanding.

TABLE OF CONTENTS

Page | |

PART I | |

PART II | |

PART III | |

PART IV | |

i

CERTAIN DEFINITIONS

Except as otherwise specified in this Annual Report on Form 10-K, the terms:

• | “we,” “us,” “our” and the “Company” refer to Terra Income Fund 6, Inc.; |

• | “Terra Income Advisors” refers to Terra Income Advisors, LLC; |

• | “Terra Capital Markets” refers to Terra Capital Markets, LLC: |

• | “Terra Capital Partners” refers to Terra Capital Partners, LLC; and |

• | “Terra Income Funds” refers collectively to Terra Secured Income Fund, LLC, Terra Secured Income Fund 2, LLC, Terra Secured Income Fund 3, LLC, Terra Secured Income Fund 4, LLC, Terra Secured Income Fund 5, LLC, Terra Secured Income Fund 5 International, Terra Income Fund International and Terra Secured Income Fund 7, LLC. |

FORWARD-LOOKING STATEMENTS

Some of the statements in this Annual Report on Form 10-K constitute forward-looking statements because they relate to future events or our future performance or financial condition. The forward-looking statements contained in this Annual Report on Form 10-K may include, but are not limited to, statements as to:

• | our future operating results; |

• | our business prospects and the prospects of our portfolio companies; |

• | the impact of the investments that we expect to make; |

• | the ability of our portfolio companies to achieve their objectives; |

• | our current and expected financings and investments; |

• | the adequacy of our cash resources, financing sources and working capital; |

• | the timing and amount of cash flows, distributions and dividends, if any, from our portfolio companies; |

• | our contractual arrangements and relationships with third parties; |

• | actual and potential conflicts of interest with any of the following affiliated entities: Terra Income Advisors, LLC, our investment adviser; Terra Capital Partners, LLC, our sponsor; Terra Secured Income Fund, LLC; Terra Secured Income Fund 2, LLC; Terra Secured Income Fund 3, LLC; Terra Secured Income Fund 4, LLC; Terra Secured Income Fund 5, LLC; Terra Secured Income Fund 5 International; Terra Income Fund International; Terra Secured Income Fund 7, LLC; Terra Property Trust, Inc., a subsidiary of Terra Secured Income Fund 5, LLC; Terra Property Trust 2, Inc., a subsidiary of Terra Secured Income Fund 7, LLC; Terra Capital Advisors, LLC; Terra Capital Advisors 2, LLC; Terra Income Advisors 2, LLC; or any of their affiliates; |

• | the dependence of our future success on the general economy and its effect on our investments; |

• | our use of financial leverage; |

• | the ability of Terra Income Advisors, LLC to locate suitable investments for us and to monitor and administer our investments; |

• | the ability of Terra Income Advisors, LLC or its affiliates to attract and retain highly talented professionals; |

• | our ability to elect to be taxed as, and maintain thereafter, our qualification as a regulated investment company under the Internal Revenue Code of 1986, as amended and as a business development company under the Investment Company Act of 1940; |

• | the impact on our business of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 and the rules and regulations issued thereunder; |

• | the effect of changes to tax legislation and our tax position; and |

• | the tax status of the enterprises in which we invest. |

ii

In addition, words such as “anticipate,” “believe,” “expect” and “intend” indicate a forward-looking statement, although not all forward-looking statements include these words. The forward-looking statements contained in this Annual Report on Form 10-K involve risks and uncertainties. Our actual results could differ materially from those implied or expressed in the forward-looking statements for any reason, including the factors set forth in “Part I — Item 1A. Risk Factors” in this Annual Report. Other factors that could cause actual results to differ materially include:

• | changes in the economy; |

• | risks associated with possible disruption in our operations or the economy generally due to terrorism or natural disasters; and |

• | future changes in laws or regulations and conditions in our operating areas. |

We have based the forward-looking statements included in this Annual Report on Form 10-K on information available to us on the date of this Annual Report on Form 10-K. Except as required by the federal securities laws, we undertake no obligation to revise or update any forward-looking statements, whether as a result of new information, future events or otherwise. Stockholders are advised to consult any additional disclosures that we may make directly to stockholders or through reports that we may file in the future with the SEC, including annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K. The forward-looking statements and projections contained in this Annual Report on Form 10-K are excluded from the safe harbor protection provided by Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

iii

PART I

Item 1. Business.

Formation of Our Company

We are a Maryland corporation, formed on May 15, 2013 and commenced operations on June 24, 2015. We have elected to be regulated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). We are an externally managed, non-diversified, closed-end management investment company that has elected to be taxed for federal income tax purposes beginning with our taxable year ended September 30, 2015, and to qualify annually thereafter, as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”).

We entered into a stock purchase agreement with Terra Capital Partners, LLC (“Terra Capital Partners”), our sponsor and an affiliate of our company. On September 19, 2014, pursuant to a private placement, Terra Capital Partners contributed cash consideration of $125,000 to purchase approximately 11,111 shares of our common stock at $11.25 per share. On October 20, 2014, pursuant to a private placement, Terra Capital Partners contributed an additional $50,000 in cash to purchase approximately 4,445 additional shares of our common stock at $11.25 per share.

On February 25, 2015, our board of directors (the “Board”) determined to change the initial offering price from $10.00 per share to $12.50 per share. As a result, on February 26, 2015, we effected a reverse stock split to account for the change in the offering price since the September and October, 2014 contributions from Terra Capital Partners. As such, all share references and equity transaction pricing elsewhere reflect this reverse stock split.

On March 2, 2015, we filed a public registration statement on Form N-2 (the “Registration Statement”) with the Securities and Exchange Commission (the “SEC”) to offer a minimum of $2.0 million of common stock and a maximum of $1.0 billion of common stock in a continuous, public offering (the “Offering”). The SEC declared the Registration Statement effective on April 20, 2015, and we retained Terra Capital Markets, LLC (“Terra Capital Markets”), an affiliate of Terra Income Advisors, to serve as the dealer manager of the Offering. As dealer manager, Terra Capital Markets is responsible for marketing our shares being offered pursuant to the Offering. We will file post-effective amendments to the Registration Statement that are subject to SEC review to allow us to continue the Offering for at least two years from the date of the effectiveness of the Registration Statement.

On May 1, 2015, Terra Capital Partners contributed cash of $275,000 to purchase approximately 24,444 additional shares from the Offering at a per share price of $11.25, which price represents the then-current public offering price of $12.50 per share, net of selling commissions, broker-dealer fees and dealer manager fees. This contribution, in addition to the initial capital contributions described above, fulfilled Terra Capital Partners’ commitment to contribute total seed capitalization of $450,000.

On June 24, 2015, we successfully reached our minimum escrow requirement and officially commenced our operations by receiving gross proceeds of $2,000,000 (the “Minimum Offering Requirement”). Since commencing operations, and through November 20, 2017, we have sold a total of 7,679,894 shares of common stock for total gross proceeds of $90.6 million, excluding shares pursuant to our distribution reinvestment plan (“DRIP”). The proceeds from the issuance of common stock are presented in our statements of changes in net assets and statements of cash flows.

On January 13, 2017, we decreased the public offering price of our common stock from $12.50 per share to $10.90 per share. The decrease in the public offering price was effective as of our January 17, 2017 bi-monthly closing and first applied to subscriptions received from January 1, 2017 through January 16, 2017.

Overview of Our Business

We do not currently have any employees and do not expect to have any employees. Services necessary for our business are provided by individuals who are employees of our advisor, Terra Income Advisors, LLC (“Terra Income Advisors” or the “Adviser”), or by individuals who were contracted by us or by Terra Income Advisors to work on behalf of us pursuant to the terms of the investment advisory and administrative services agreement between us and Terra Income Advisors (the “Investment Advisory Agreement”). Terra Income Advisors is responsible for sourcing potential investments, conducting due diligence on prospective investments, analyzing investment opportunities, structuring investments and monitoring our portfolio on an ongoing basis according to asset allocation and other guidelines set by our Board. Terra Income Advisors is registered as investment adviser with the SEC. We have elected to be taxed for federal income tax purposes for our taxable year in which we commence operations, and intend to qualify annually thereafter, as a RIC under Subchapter M of the Code.

The level of our investment activity depends on many factors, including the amount of debt and equity capital available to prospective borrowers, the level of refinancing activity for such companies, the availability of credit to finance transactions, the general economic environment and the competitive environment for the types of investments we make. The timing of investing the proceeds from our Offering depends on the availability of investment opportunities that are consistent with our investment objective and strategies and any restrictions imposed by the RIC diversification requirements. Any distributions we make prior to

1

the time that all capital raised has been deployed may be substantially lower than the distributions that we expect to pay when our portfolio is fully invested.

Our Investment Adviser

Our investment activities are externally managed by Terra Income Advisors, a private investment firm affiliated with us, pursuant to the Investment Advisory Agreement, under the oversight of the Board, a majority of whom are independent. Terra Income Advisors is registered as an investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act”).

Under the Investment Advisory Agreement, we have agreed to pay Terra Income Advisors a base management fee as well as an incentive fee based on our investment performance. Also, we have agreed to pay selling commissions, broker-dealer fees, a dealer manager fee and a servicing fee, and to reimburse Terra Income Advisors for our organization and offering expenses up to a maximum amount equal to 1.5% of the gross proceeds from the Offering. Terra Income Advisors will bear all organization and offering expenses in excess of this amount.

The management of our investment portfolio is the responsibility of Terra Income Advisors and its executive officers. The investment committee of Terra Income Advisors will approve each new investment that we make. Our Board, including a majority of independent directors, oversees and monitors our investment performance and, beginning with the second anniversary of the date of the Investment Advisory Agreement, our Board will annually review the compensation we pay to our Adviser and its performance during the preceding 12 months to determine if the compensation paid to our Adviser is reasonable in relation to the nature and quality of the services performed, and that the provisions of the Investment Advisory Agreement are carried out.

About Terra Capital Partners

Terra Capital Partners, the parent company of Terra Income Advisors, is a real estate finance and investment firm based in New York City that focuses primarily on the origination and management of mezzanine loans, as well as first mortgage loans, bridge loans and preferred equity investments in all major property types. Since its formation in 2001 and its commencement of operations in 2002, Terra Capital Partners has been engaged in providing financing on commercial properties of all major property types throughout the U.S. In the lead up to the global financial crisis in 2007, believing that the risks associated with commercial real estate markets had grown out of proportion to the potential returns from such markets, Terra Capital Partners sold 100% of its interest in its portfolio. It was not until mid-2009, after its assessment that commercial mortgage markets would begin a period of stabilization and growth, that Terra Capital Partners began to sponsor new investment vehicles, which included the Terra Income Funds, to again provide debt capital to commercial real estate markets. The financings provided by vehicles managed by Terra Capital Partners have been secured by approximately 11.0 million square feet of office properties, 5.5 million square feet of land, 3.4 million square feet of retail properties, 3.8 million square feet of industrial properties, 3,828 hotel rooms and 23,674 apartment units. The value of the properties underlying this capital was approximately $6.3 billion based on appraised values as of the closing dates. None of the financings extended by Terra Capital Partners and its affiliates have required foreclosure or suffered any loss of principal. In addition to its extensive experience originating and managing debt financings, Terra Capital Partners and its affiliates have owned and operated over six million square feet of office and industrial space between 2005 and 2007, and this operational experience further informs its robust origination and underwriting standards and would be beneficial should our Adviser need to foreclose on a property underlying a financing. As of the date of this Form 10-K, Terra Capital Partners and its affiliates employed 33 persons.

Terra Capital Partners, led by its Chief Executive Officer, Bruce D. Batkin, and its Chairman, Simon J. Mildé, is owned and operated by highly experienced real estate, finance and securities professionals. Members of the Terra Capital Partners management team have broad based, long-term relationships with major financial institutions, property owners and commercial real estate service providers. They have worked together as a team for 15 years, building on their prior experience in commercial real estate investment, finance, development and asset management. They have held leadership roles at many of the top international real estate and investment banking firms, including Jones Lang Wootton (formerly Jones Lang LaSalle Incorporated and now JLL), Merrill Lynch, Donaldson, Lufkin and Jenrette Securities Corporation (now Credit Suisse (USA) Inc.) and ABN Amro Bank N.V. We believe that the active and substantial ongoing participation of Terra Capital Partners in the real estate finance market, and the depth of experience and disciplined investment approach of its management team will allow Terra Income Advisors to successfully execute our investment strategy.

Investment Objectives and Strategy

Our primary investment objectives are to pay attractive and stable cash distributions and to preserve, protect and return capital contributions to stockholders. Our investment strategy is to use substantially all of the proceeds of the Offering to originate and manage a diversified portfolio consisting of (i) commercial real estate loans to U.S. companies qualifying as “eligible portfolio companies” under the 1940 Act, including mezzanine loans, first and second lien mortgage loans, subordinated mortgage loans, bridge loans and other commercial real estate-related loans related to or secured by high quality commercial real estate in the United States and (ii) preferred equity real estate investments in U.S. companies qualifying as “eligible portfolio companies” under

2

the 1940 Act. We may also purchase select commercial real estate-related debt securities, such as commercial mortgage-backed securities or collateralized debt obligations; provided, however, that we will select all investments after considering its ability to qualify to be taxed as a RIC.

We seek to structure, acquire and maintain a portfolio of investments that generate a stable income stream to enable us to pay attractive and consistent cash distributions to our stockholders. We directly structure, underwrite and originate most of our investments, as we believe that doing so will provide us with the best opportunity to invest in loans that satisfy our standards, establish a direct relationship with the borrower and optimize the terms of our investments; however, we may acquire existing loans from the originating lender should our adviser determine such an investment is in our best interest. We may hold our investments until their scheduled maturity dates or may sell them if we are able to command favorable terms for their disposition. We may also seek to realize growth in the value of our investments by timing their sale to maximize value. We believe that our investment strategy allows us to pay attractive and stable cash distributions to our stockholders and to preserve, protect and return our stockholders’ capital contributions, consistent with our investment objectives.

Terra Income Advisors’ management team has extensive experience in originating, acquiring, structuring, managing and disposing of real estate-related loans similar to the types of loans in which we intend to invest. In order to meet our investment objectives, we generally seek to follow the following investment criteria:

• | focus primarily on the origination of new loans; |

• | focus on loans backed by properties in the United States; |

• | invest primarily in fixed rate rather than floating rate loans, but we reserve the right to make debt investments that bear interest at a floating rate; |

• | invest in loans expected to be repaid within one to five years; |

• | maximize current income; |

• | lend to creditworthy borrowers; |

• | lend on properties that are expected to generate sustainable cash flow; |

• | maximize diversification by property type, geographic location, tenancy and borrower; |

• | source off-market transactions; and |

• | hold investments until maturity unless, in our adviser’s judgment, market conditions warrant earlier disposition. |

While the size of each of our investments generally ranges between $3 million and $20 million, our investments ultimately be at the discretion Terra Income Advisors, subject to oversight by our Board. Prior to raising substantial capital, we may make smaller investments and invest a larger portion of our capital base in cash and cash items (including receivables) and U.S. government securities to enable us to acquire assets that meet our desired investment profile and to meet certain RIC qualification requirements under the Code.

To enhance our returns, we intend to employ leverage as market conditions permit and at the discretion of our Terra Income Advisors, but in no event will leverage employed exceed 50% of the value of our assets, as required by the 1940 Act. See Item 1A “Risk Factors — Risks Related to Debt Financing” for a discussion of the risks inherent in employing leverage.

Business Strategy

In executing our business strategy, we believe that we benefit from Terra Income Advisors’ affiliation with Terra Capital Partners, given its strong track record and extensive experience and capabilities as real estate investment manager and sponsor of the Terra Income Funds. We believe the following core strengths will enable us to realize our investment objectives and provide us with significant competitive advantages in the marketplace, and attractive risk-adjusted returns to our stockholders:

Significant Experience of Our Management Team

Terra Income Advisors has a highly experienced management team with extensive expertise in originating, underwriting, structuring, financing and managing commercial real estate loans and related investments through a variety of credit and interest rate environments and economic cycles. Terra Income Advisors’ senior management team is led by Bruce D. Batkin and Simon J. Mildé, the co-founders of Terra Capital Partners, each of whom has over 35 years in the commercial real estate finance industry, including over 15 years working together at Terra Capital Partners. Messrs. Batkin and Mildé are supported by a team of 15 highly experienced real estate, finance and securities professionals. This team has extensive relationships across the commercial real estate industry, including long-term relationships with major financial institutions, property owners and commercial real estate service providers. We believe that we benefit from Terra Income Advisors’ strong track record and extensive experience and

3

capabilities originating, structuring, financing and managing commercial real estate loans and will continue to do so as we grow our portfolio over time.

Significant Experience of Terra Capital Partners

Terra Capital Partners provides our Terra Income Advisers with all of its key investment personnel. Terra Capital Partners has developed a reputation within the commercial real estate finance industry as a leading sophisticated real estate investment and asset management company with a 15 year track record in originating, underwriting and managing commercial real estate and real estate-related loans, preferred equity investments and investments with similar characteristics to the assets that we acquire. We believe we benefit from the depth and the disciplined approach Terra Capital Partners brings to its underwriting and investment management processes to structure and manage investments prudently. In addition to its extensive experience originating and managing debt financings, Terra Capital Partners and its affiliates have owned and operated over six million square feet of office and industrial space between 2005 and 2007, and this operational experience has further informed its robust origination and underwriting standards.

Disciplined Investment Process

We follow a disciplined investment origination, underwriting and selection process. We follow an investment approach focused on long-term credit performance and capital protection. This investment approach involves a multi-phase evaluation, structuring and monitoring process for each potential investment opportunity. After investment, our management team focuses on a thorough review of our investments for potential credit quality deterioration and potential proactive steps, including making available significant managerial assistance as required by the 1940 Act, to mitigate any losses to our invested capital. We believe this approach maximize current income and minimize capital loss. None of the loans originated by our Adviser and its affiliates have suffered a foreclosure or loss of principal, which we believe is attributable to our Adviser’s rigorous origination, underwriting and selection process.

Portfolio Construction

We construct a portfolio that is diversified by property type, geographic location and borrower. Although we expect to hold our assets for the duration of the expected five-year term of our company, we may decide to sell assets prior to the end of the term in order to maximize stockholder returns.

We construct our portfolio based on our evaluation of the impact of each potential investment on the risk/reward mix in our existing portfolio. By selecting those assets that we believe will maximize stockholder returns while minimizing investment-specific risk, we believe we can build and manage an investment portfolio that provides superior value to stockholders over time, both in absolute terms and relative to other commercial real estate loan and real estate-related investment vehicles.

Superior Analytical Tools

We believe that our management team possesses the superior analytical tools to evaluate each potential investment through the balanced use of qualitative and quantitative analysis, which helps us manage risk on an individual investment and portfolio basis. We rely on a variety of analytical tools and models to assess our investments and risk management. We also conduct an extensive evaluation of the numerous factors that affect our potential investments. These factors include:

• | Top-down review of both the current macroeconomic environment generally and the real estate and commercial real estate loan market specifically; |

• | Detailed evaluation of the real estate industry and its sectors; |

• | Bottom-up review of each individual investment’s attributes and risk/reward profile relative to the macroeconomic environment; |

• | Quantitative cash flow analysis and impact of the potential investment on our portfolio; and |

• | Ongoing management and monitoring of all investments to assess changing conditions on our original investment assumptions. |

Extensive Strategic Relationships

Our management team maintains extensive relationships within the real estate industry, including real estate developers, institutional real estate sponsors and investors, real estate funds, investment and commercial banks, private equity funds, asset originators and broker-dealers, as well as the capital and financing markets generally. We believe these relationships enhance our ability to source and finance our investments as well as mitigate their credit and interest rate risk. We leverage the many years of experience and well-established contacts of our management team, and to use these relationships for the benefit of our stockholders.

4

Market Opportunities

The opportunity for alternative commercial real estate lenders is the direct result of (i) limited supply of commercial real estate debt from banks and securitized lenders due to regulations implemented since the last recession and (ii) strong demand for commercial real estate financing. New regulations, particularly those imposed by or Basel III and the Dodd-Frank Act, have reduced the availability of commercial real estate debt capital from regulated institutions and the commercial mortgage-backed securities (“CMBS”) market. At the same time, demand for commercial real estate debt in the U.S. has been supported by strong economic fundamentals, including employment gains, low inflation and positive gross domestic product growth, while new construction of commercial real estate has been limited relative to historical averages. These fundamentals, as well as abundant domestic and international commercial real estate equity capital available for U.S. commercial real estate, create an opportunity for providers of commercial real estate debt to finance property acquisition, refinancing and development.

Traditional Providers of Commercial Real Estate Debt Have Reduced Availability of Capital

The turmoil in the U.S. mortgage market that commenced with the onset of the global financial crisis in 2008 has diminished the availability of credit for commercial real estate from traditional providers of capital to commercial real estate borrowers. Although credit availability has increased over the past several years, there is an opportunity for alternative commercial real estate debt providers like us to capitalize on the lack of supply created by a more risk-averse credit culture, tighter underwriting standards, a tepid recovery in the CMBS market and changes in the regulatory environment that continue to constrain the lending capacity of large commercial banks and traditional providers of capital.

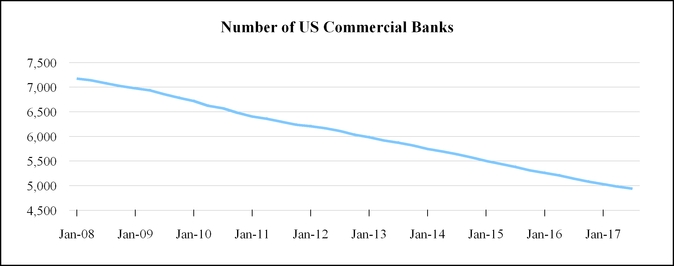

Stricter Underwriting from a Reduced Number of Banks

Fallout from the 2008 recession has reduced the number of U.S. commercial banks by approximately 25% through a combination of consolidation, failure or overall balance sheet reduction.

Source: Federal Reserve Bank of St. Louis, October 2017

Those lenders that remain are subject to increased regulations (Dodd-Frank Act and Basel III, the latter of which imposes requirements for higher bank capital charges on certain types of real estate loans) and adhere to mortgage lending practices that are more conservative than prior to the economic crisis. Therefore, those financial institutions still willing to provide capital may not provide sufficient proceeds to meet borrowers’ needs, and many loans that previously would have been provided by a single lender often will require multiple lenders. This provides us, as an alternative lender, with an immediate opportunity to augment loans provided by traditional lenders with subordinated debt and preferred equity, often at higher property valuations, lower loan-to-value ratios and higher returns than prior to the economic crisis. In particular, due to the nature of the underlying assets, there has been less availability of debt capital on transitional properties, as a result of increased capital requirements, which significantly impact the profitability of such loans for financial institutions. We believe this opportunity will continue for the foreseeable future.

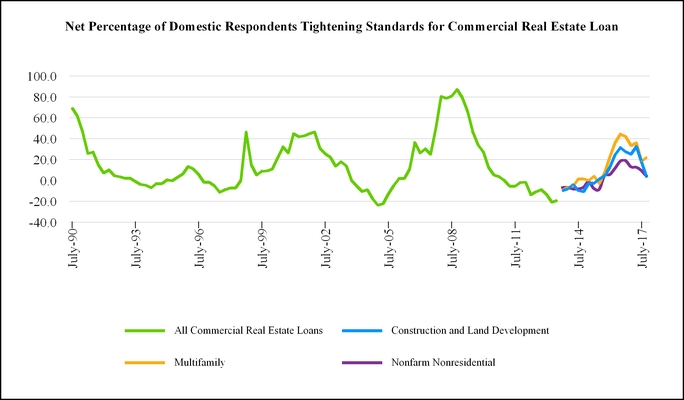

According to a survey conducted by the Federal Reserve, in January 2017, despite positive fundamentals in commercial real estate property, the net percentage of domestic respondents reporting tightening standards for commercial real estate loans was the highest since 2009, indicating that the opportunity for alternative providers of commercial real estate debt capital will likely increase.

5

(1) | Data is YTD through October 2017 |

Source: The Federal Reserve Board, October 2017.

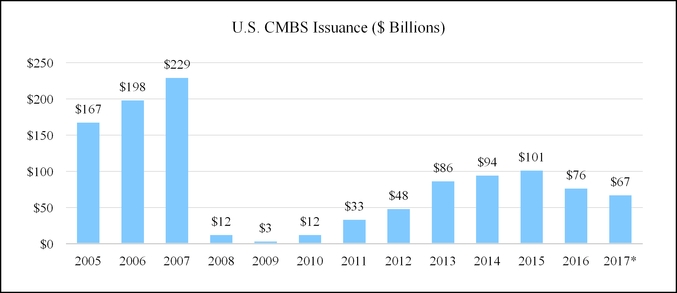

Overall CMBS Market Well Below Peak

In addition, enhanced risk-retention requirements for CMBS have increased securitization costs and limited competition from CMBS lenders. This has led to a decrease in CMBS securitizations and issuances that have failed to recover to previous levels, from a peak of $229 billion in 2007 to $76 billion in 2016. Risk retention requirements went into effect on December 24, 2016. A survey of industry professionals published in the market publication Commercial Mortgage Alert has predicted issuance of $75 billion for 2017, indicating an opportunity for additional providers of commercial real estate debt capital to continue to fill a supply gap.

(1) | Data is YTD through September 2017 |

6

(*) Only numbers from the first nine months of 2017 have been reported.

Source: Commercial Mortgage Alert, September 2017.

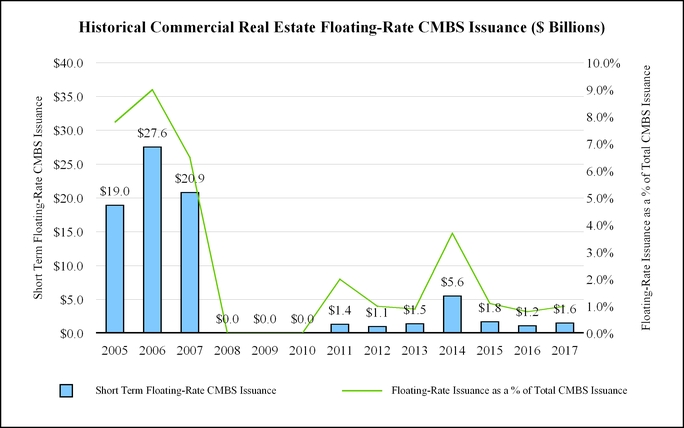

Lack of Supply of CMBS Debt for Transitional Properties

As a result of the same regulatory constraints impacting the entire CMBS market, floating-rate CMBS effectively disappeared from the marketplace from a peak of $27 billion in 2006. These transactions have historically been secured by transitional properties, similar to many of the loan opportunities that we intend to pursue. With floating-rate CMBS issuance failing to break $2 billion in more than one year (2014), as illustrated by the following table, we believe there is a meaningful void for alternative commercial real estate debt capital providers to fill, a trend we expect to continue.

(1) | Data is YTD through September 2017 |

Source: Commercial Mortgage Alert, September 2017.

Supply of Debt Capital Constrained by Regulatory Environment

The Dodd-Frank Act and Basel III have specific provisions targeting commercial real estate debt that have implemented risk-retention requirements for CMBS (in the case of the Dodd-Frank Act) and required higher bank capital charges on certain types of commercial real estate loans (in the case of Basel III). The two primary consequences of these regulations, the goals of which are to reduce the risk from commercial real estate in the banking system, have been to reduce the scope of lending from banks and other regulated financial institutions and to increase the costs for those institutions to provide commercial real estate debt.

In December 2016, the risk-retention rules of the Dodd-Frank Act became effective, requiring that a sponsor of a CMBS transaction retain, directly or indirectly, at least 5% of the credit risk of the securitized assets collateralizing the CMBS. This risk retention requirement can be satisfied through either ‘‘horizontal’’ risk retention where the risk retainer retains a 5% interest representing the most junior tranche in the CMBS securitization or through “vertical” risk retention where the risk retainer ends up retaining a 5% cross section of the entire CMBS securitization or through a combination of horizontal and vertical risk retention. Historically, bank sponsors of CMBS transactions had sold, or attempted to sell, 100% of the securitized assets collateralizing the CMBS. We expect that the impact of this requirement will be a reduction in CMBS volume as transaction costs (and ultimately borrowing costs) increase as a result of regulatory compliance and that some CMBS participants will exit the market.

Basel III increases bank capital requirements while tightening the definition of what can be included in the calculation of capital and revising the methodology of calculating risk-weighted assets, making them more risk sensitive. The effect is a revision

7

to the regulatory capital framework for U.S. banks, requiring banks to increase regulatory capital and decrease risk-weighted assets to achieve compliance with new (higher) risk-based capital ratios. With Basel III, risk-weightings are now higher on certain assets,

specifically certain acquisition, development and construction loans classified as HVCRE which are less profitable under the current framework, incentivizing banks to either adjust pricing on or abandon HVCRE loans entirely. The final Basel III rule requires that banking organizations to assign a higher risk weight of 150% (previously 100%) for HVCRE loans which, due to the breadth of the language and general uncertainty as to the interpretation of the rule, typically includes most transitional commercial real estate loans. This has reduced the availability of commercial real estate debt capital and increased financing costs for borrowers, creating an opportunity for alternative lenders.

Although the regulatory environment will continue to evolve over time, we believe that much of the substantive components of Dodd-Frank and Basel III will continue, and adjustments, if any, will be implemented only over a period of many years (much like the current regulations themselves). We expect that banks and CMBS lenders will continue to predominantly focus on stabilized properties at lower leverage points. As a result, we do not expect the size and breadth of the market opportunity to have significant near-term legislative risk.

Increased Market Share for Alternative Lenders

Non-bank lenders have historically had the advantage of flexibility and execution speed over competing bank and CMBS lenders. With the addition of increased regulatory scrutiny and tightening underwriting standards, the competitive advantage of alternative providers of commercial real estate debt capital has further increased, particularly for non-stabilized properties and new property development, here borrowers increasingly focus on speed and certainty of execution.

This is evident in the fact that the market share of alternative lenders (financial and private/other companies, excluding banks, CMBS, insurance companies, and government agencies) has significantly increased. While alternative lenders made up approximately 5% of the market in 2009, that figure has doubled to approximately 10% in each of the last three years. With an estimated 2017 commercial real estate mortgage origination volume of $537 billion per the Mortgage Bankers Association, this would represent a market share of over $50 billion for alternative lenders.

(1) | Alternative includes both financial and private/other companies |

(2) | Based on independent reports of properties and portfolios $2.5 million and greater |

(3) | Data is through December 2016 |

Source: Real Capital Analytics, December 2016

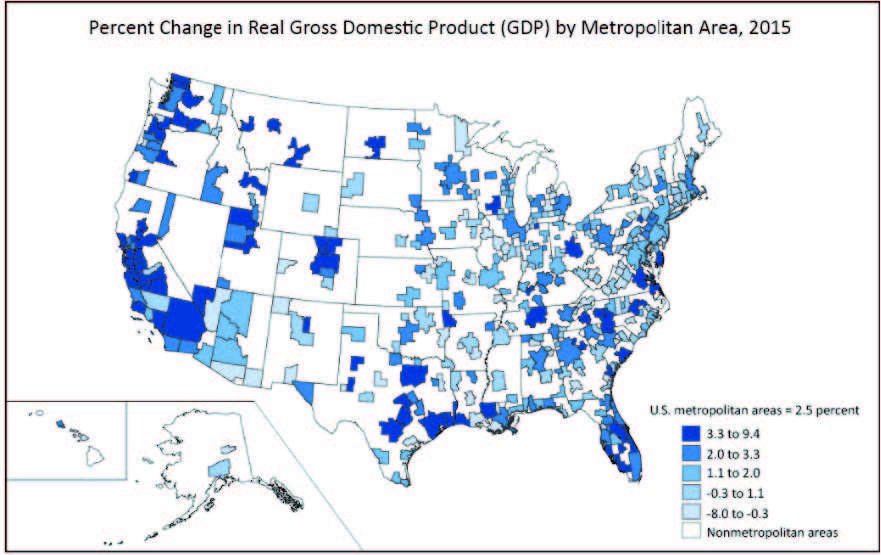

Stronger Real Estate Fundamentals Drive Transaction Volume

The post-crisis expansion of the economy is evident in most metropolitan areas across the county as shown in the chart below, with positive GDP growth and strong gains in employment driving demand for various asset classes within commercial real estate. The breadth of the recovery at this stage creates diverse opportunities for us across many different markets and various asset types. In addition to increases in demand driven by stronger economic growth, higher occupancy levels have been supported by a relative

8

lack of new supply of commercial real estate compared to historical averages, as measured by the amount of new completions as a percentage of existing stock. A relatively stable trend of supply additions allows the market to adjust to changes in demand with less volatility, which creates greater stability in property values over time.

Source: U.S. Bureau of Economic Analysis

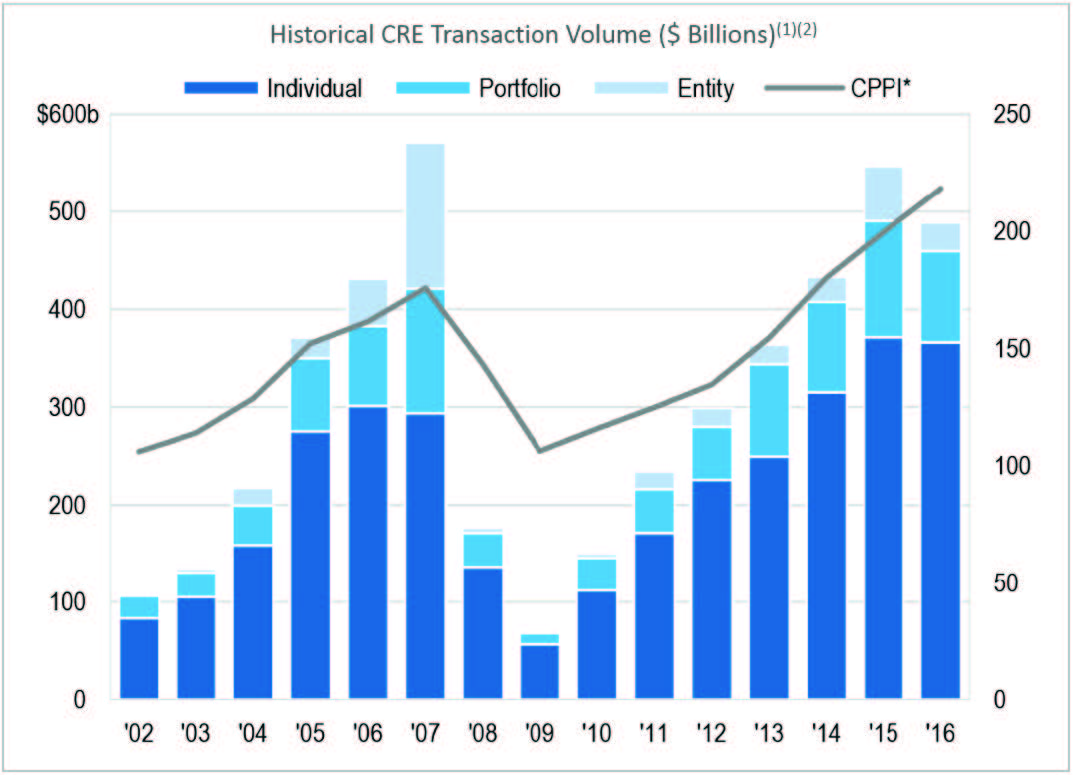

Historical commercial real estate transaction volume has increased to near pre-recession levels, driven by both the strength of commercial real estate fundamentals and the abundance of capital, particularly non-domestic, seeking commercial real estate investment opportunities. In fact, excluding entity purchases, the volume of portfolio and individual property transactions has already exceeded the pre-recession peak. Although the total volume decreased from 2015 to 2016, we believe this represents a return to equilibrium, and overall stability in property values, following several years of relative inactivity.

9

(1) | Based on independent reports of properties and portfolios $2.5 million and greater. Prior to 2005, Real Capital Analytics primarily captured sales valued at $5.0 million and above. |

(2) | Data is through December 2016. |

Source: Real Capital Analytics, December 2016

Unlike the years prior to the last recession, the abundant transaction volume has not eroded lender credit metrics. Comparing loan-to-value, debt yield, and debt service coverage ratio from 2008 to 2016 indicates stricter underwriting standards than at the peak of the previous cycle. This is a result of both increased conservatism on the part of regulated financial institutions and greater discipline on the part of non-bank alternative lenders.

Comparative Commercial Real Estate Loan Metrics (1) | ||||

Metric | 2008 Average | 2016 Average | ||

Loan-to-value | 67.0% | 63.0% | ||

Debt service coverage ratio | 1.29x | 1.66x | ||

Debt yield | 10.1% | 10.2% | ||

(1) | Based on independent reports of properties and portfolios $2.5 million and greater. Includes office, retail, industrial and hotel properties |

Source: Real Capital Analytics, December 2016

The combination of strong property fundamentals, stabilizing transaction volume, disciplined credit metrics and an overall lack of supply of commercial real estate debt should create significant opportunities for us to deploy capital.

10

Targeted Investments

Real Estate-Related Loans

We originate, acquire, fund and structure real estate-related loans, including first and second mortgage loans, mezzanine loans, bridge loans, convertible mortgages and other loans related to high-quality commercial real estate in the U.S. We also acquire some equity participations in the underlying collateral of such loans. We structure, underwrite and originate most if not all of our investments. We use what we consider to be conservative underwriting criteria, and our underwriting process involves comprehensive financial, structural, operational and legal due diligence to assess the risks of investments so that we can optimize pricing and structuring. By originating loans directly, we are able to structure and underwrite loans that satisfy our standards, establish a direct relationship with the borrower and utilize our own documentation. Described below are some of the types of loans we own and may originate.

Mezzanine Loans. These are loans secured by ownership interests in an entity that owns commercial real estate and generally finance the acquisition, refinancing, rehabilitation or construction of commercial real estate. Mezzanine loans may be either short-term (one-to-five year) or long-term (up to 10-year) and may be fixed or floating rate. We may originate mezzanine loans backed by high-quality properties in the U.S. that fit our investment strategy. We may own such mezzanine loans directly or we may hold a participation in a mezzanine loan or a sub-participation in a mezzanine loan. These loans are predominantly current-pay loans (although there may be a portion of the interest that accrues) and may provide for participation in the value or cash flow appreciation of the underlying property as described below. We invest in mezzanine loans with loan-to-value ratios ranging from 60% to 80%. With the credit market disruption and resulting dearth of capital available in this part of the capital structure, we believe that the opportunities to both directly originate and to buy mezzanine loans from third-parties on favorable terms will continue to be attractive.

Preferred Equity Investments. These are investments in preferred membership interests in an entity that owns commercial real estate and generally finance the acquisition, refinancing, rehabilitation or construction of commercial real estate. These investments are expected to have similar characteristics to and returns as mezzanine loans.

Subordinated Mortgage Loans (B-notes). B-notes include structurally subordinated first mortgage loans and junior participations in first mortgage loans or participations in these types of assets. Like first mortgage loans, these loans generally finance the acquisition, refinancing, rehabilitation or construction of commercial real estate. B-notes may be either short-term (one-to-five year) or long-term (up to 10-year), may be fixed or floating rate and are predominantly current-pay loans. We may originate current-pay B-notes backed by high-quality properties in the U.S. that fit our investment strategy. We may create B-notes by tranching our directly originated first mortgage loans generally through syndications of senior first mortgages, or buy such assets directly from third-party originators. Due to the current credit market disruption and resulting dearth of capital available in this part of the capital structure, we believe that the opportunities to both directly originate and to buy B-notes from third-parties on favorable terms will continue to be attractive.

Investors in B-notes are compensated for the increased risk of such assets from a pricing perspective but still benefit from a lien on the related property. Investors typically receive principal and interest payments at the same time as senior debt unless a default occurs, in which case these payments are made only after any senior debt is made whole. Rights of holders of B-notes are usually governed by participation and other agreements that, subject to certain limitations, typically provide the holders of subordinated positions of the mortgage loan with the ability to cure certain defaults and control certain decisions of holders of senior debt secured by the same properties (or otherwise exercise the right to purchase the senior debt), which provides for additional downside protection and higher recoveries.

Bridge Loans. We offer bridge financing products to borrowers who are typically seeking short-term capital to be used in an acquisition, development or refinancing of a given property. From the borrower’s perspective, shorter term bridge financing is advantageous because it allows time to improve the property value through repositioning without encumbering it with restrictive long-term debt. The terms of these loans generally do not exceed three years. Bridge loans may be structured as mezzanine loans, preferred equity or first mortgages.

First Mortgage Loans. These loans generally finance the acquisition, refinancing, rehabilitation or construction of commercial real estate. First mortgage loans may be either short-term (one-to-five year) or long-term (up to 10-year), may be fixed or floating rate and are predominantly current-pay loans. We originate current-pay first mortgage loans backed by high-quality properties in the U.S. that fit our investment strategy. We selectively syndicate portions of these loans, including senior or junior participations that will effectively provide permanent financing or optimize returns which may include retained origination fees.

First mortgages provide for a higher recovery rate and lower defaults than other debt positions due to the lender’s senior position. However, such loans typically generate lower returns than subordinate debt such as mezzanine loans or B-notes.

11

Convertible Mortgages. Convertible mortgages are similar to equity participations (as described below). We may invest in or originate a convertible mortgage if the Adviser concludes that we may benefit from the cash flow or any appreciation in the value of the subject property.

Equity Participations. In connection with our loan origination activities, we may pursue equity participation opportunities, or interests in the projects being financed, in instances when we believe that the risk-reward characteristics of the loan merit additional upside participation because of the possibility of appreciation in value of the underlying assets securing the loan. Equity participations can be paid in the form of additional interest, exit fees or warrants in the borrower. Equity participation can also take the form of a conversion feature, permitting the lender to convert a loan or preferred equity investment into equity in the borrower at a negotiated premium to the current net asset value of the borrower. We expect to be able to obtain equity participations in certain instances where the loan collateral consists of an asset that is being repositioned, expanded or improved in some fashion which is anticipated to improve future cash flow. In such case, the borrower may wish to defer some portion of the debt service or obtain higher leverage than might be merited by the pricing and leverage level based on historical performance of the underlying asset. We generate additional revenues from these equity participations as a result of excess cash flows being distributed or as appreciated properties are sold or refinanced.

Other Real Estate-Related Investments. The Adviser has the right to invest in other real estate-related investments, which may include CMBS or other real estate debt or equity securities, so long as such investments do not constitute more than 15% of our assets. Certain of our real estate-related loans require the borrower to make payments of principal on the fully committed principal amount of the loan regardless of whether the full loan amount is outstanding portfolio.

Regulation

We have elected to be regulated as a BDC under the 1940 Act. As with other companies regulated by the 1940 Act, a BDC must adhere to certain substantive regulatory requirements. The 1940 Act contains prohibitions and restrictions relating to transactions between BDCs and their affiliates (including any investment advisers or sub-advisers), principal underwriters and affiliates of those affiliates or underwriters and requires that a majority of the directors be persons other than “interested persons,” as that term is defined in the 1940 Act. In addition, the 1940 Act provides that we may not change the nature of our business so as to cease to be, or to withdraw our election as, a BDC unless approved by a majority of our outstanding voting securities.

“A majority of the outstanding voting securities” of a company is defined under the 1940 Act as the lesser of: (i) 67% or more of the voting securities of such company present at a meeting if the holders of more than 50% of the company’s outstanding voting securities are present or represented by proxy; or (ii) more than 50% of the outstanding voting securities of such company.

Qualifying Assets

Under the 1940 Act, a BDC may not acquire any asset other than assets of the type listed in Section 55(a) of the 1940 Act, which are referred to as qualifying assets, unless, at the time the acquisition is made, qualifying assets represent at least 70% of the company’s total assets. The principal categories of qualifying assets relevant to our business are the following:

1. | Securities purchased in transactions not involving any public offering from the issuer of such securities, which issuer (subject to certain limited exceptions) is an eligible portfolio company, or from any person who is, or has been during the preceding 13 months, an affiliated person of an eligible portfolio company, or from any other person, subject to such rules as may be prescribed by the SEC. An eligible portfolio company is defined in the 1940 Act as any issuer which: |

a. | is organized under the laws of, and has its principal place of business in, the United States; |

b. | is not an investment company (other than a small business investment company wholly owned by the BDC) or a company that would be an investment company but for certain exclusions under the 1940 Act; and |

c. | satisfies any of the following: |

i. | does not have any class of securities that is traded on a national securities exchange; |

ii. | has a class of securities listed on a national securities exchange, but has an aggregate market value of outstanding voting and non-voting common equity of less than $250 million; |

iii. | is controlled by a BDC or a group of companies including a BDC and the BDC has an affiliated person who is a director of the eligible portfolio company; |

iv. | is a small and solvent company having total assets of not more than $4 million and capital and surplus of not less than $2 million; or |

v. | meets such other criteria as may be established by the SEC. |

2. | Securities of any eligible portfolio company that we control. |

12

3. | Securities purchased in a private transaction from a U.S. issuer that is not an investment company or from an affiliated person of the issuer, or in transactions incident thereto, if the issuer is in bankruptcy and subject to reorganization or if the issuer, immediately prior to the purchase of its securities, was unable to meet its obligations as they came due without material assistance other than conventional lending or financing arrangements. |

4. | Securities of an eligible portfolio company purchased from any person in a private transaction if there is no ready market for such securities and we already own 60% of the outstanding equity of the eligible portfolio company. |

5. | Securities received in exchange for or distributed on or with respect to securities described in (1) through (4) above, or pursuant to the exercise of warrants or rights relating to such securities. |

6. | Cash, cash equivalents, U.S. government securities or high-quality debt securities maturing in one year or less from the time of investment. |

Control, as defined by the 1940 Act, is presumed to exist where a BDC beneficially owns more than 25% of the outstanding voting securities of the portfolio company.

In addition, a BDC must have been organized and have its principal place of business in the U.S. and must be operated for the purpose of making investments in the types of securities in eligible portfolio companies, or in other securities that are consistent with its purpose as a BDC.

Managerial Assistance to Portfolio Companies

In order to count portfolio securities as qualifying assets for the purpose of the 70% test, we must either control the issuer of the securities or must offer to make available to the issuer of the securities (other than small and solvent companies described above) significant managerial assistance; except that, where we purchase such securities in conjunction with one or more other persons acting together, one of the other persons in the group may make available such managerial assistance. Making available significant managerial assistance means, among other things, any arrangement whereby the BDC, through its directors, officers or employees, offers to provide, and, if accepted, does so provide, significant guidance and counsel concerning the management, operations or business objectives and policies of a portfolio company.

Terra Income Advisors or its affiliates may provide such managerial assistance on our behalf to portfolio companies that request this assistance, recognizing that our involvement with each investment will vary based on factors including the size of the company, the nature of our investment, the company’s overall stage of development and our relative position in the capital structure. We may receive fees for these services.

Temporary Investments

Pending investment in other types of “qualifying assets,” as described above, our investments may consist of cash, cash equivalents, U.S. government securities or high-quality debt securities maturing in one year or less from the time of investment, which we refer to, collectively, as temporary investments, so that 70% of our assets are qualifying assets. Typically, we will invest in U.S. Treasury bills or in repurchase agreements, provided that such agreements are fully collateralized by cash or securities issued by the U.S. government or its agencies. A repurchase agreement involves the purchase by an investor, such as us, of a specified security and the simultaneous agreement by the seller to repurchase it at an agreed-upon future date and at a price that is greater than the purchase price by an amount that reflects an agreed-upon interest rate. There is no percentage restriction on the proportion of our assets that may be invested in such repurchase agreements. However, if more than 25% of our total assets constitute repurchase agreements from a single counterparty, we would not meet the asset diversification requirements in order to qualify as a RIC for U.S. income tax purposes. Thus, we do not intend to enter into repurchase agreements with a single counterparty in excess of this limit. Terra Income Advisors will monitor the creditworthiness of the counterparties with which we enter into repurchase agreement transactions.

Indebtedness and Senior Securities

As a BDC, we are permitted, under specified conditions, to issue multiple classes of indebtedness and one class of stock senior to our common stock if our asset coverage, as defined in the 1940 Act, is at least equal to 200% immediately after each such issuance. In addition, while any senior securities remain outstanding, we must generally make provisions to prohibit any distribution to our stockholders or the repurchase of such securities or stock unless we meet the applicable asset coverage ratios at the time of the distribution or repurchase. We may also borrow amounts up to 5% of the value of our total assets for temporary or emergency purposes without regard to asset coverage. For a discussion of the risks associated with leverage, see Item 1A “Risk Factors — Risks Related to Debt Financing” and Item 1A “Risk Factors — Risks Related to Business Development Companies.”

Common Stock

We will generally not be able to issue and sell our common stock at a price per share, after deducting selling commissions, broker-dealer fees, and dealer manager fees, that is below our net asset value (“NAV”) per share. See Item 1A “Risk Factors — Risk

13

Related to Business Development Companies — Regulations governing our operation as a BDC and RIC will affect our ability to raise, and the way in which we raise, additional capital or borrow for investment purposes, which may have a negative effect on our growth.” We may, however, sell our common stock, or warrants, options or rights to acquire our common stock, at a price below the then-current NAV of our common stock if our Board determines that such sale is in our best interests and that of our stockholders, and our stockholders approve such sale. In any such case, the price at which our securities are to be issued and sold may not be less than a price which, in the determination of our Board, closely approximates the market value of such securities (less any distributing commission or discount). We may generally issue new shares of our common stock at a price below NAV per share in rights offerings to existing stockholders, in payment of dividends and in certain other limited circumstances, subject to applicable requirements of the 1940 Act.

Co-Investments

As a BDC, we are subject to certain regulatory restrictions in making our investments. For example, we may be prohibited under the 1940 Act from knowingly participating in certain transactions with our affiliates without the prior approval of our Board who are not interested persons and, in some cases, prior approval by the SEC. The SEC has granted us exemptive relief permitting us, subject to satisfaction of certain conditions, to co-invest in certain privately negotiated investment transactions with certain affiliates of Terra Income Advisors, including the Terra Income Funds, Terra Property Trust, Inc. (“TPT”), Terra Property Trust 2, Inc. (“TPT2”), and any future BDC or closed-end management investment company that is registered under the 1940 Act and is advised by Terra Income Advisors or its affiliated investment advisers (the “Co-Investment Affiliates”). However, we will be prohibited from engaging in certain transactions with our affiliates even under the terms of this exemptive order. We believe this relief will not only enhance our ability to further our investment objectives and strategy, but may also increase favorable investment opportunities for us, in part by allowing us to participate in larger investments, together with our Co-Investment Affiliates, than would be available to us if we had not obtained such relief.

Compliance Policies and Procedures

As a BDC, we and Terra Income Advisors have each adopted and implemented written policies and procedures reasonably designed to prevent violation of the federal securities laws and are required to review these compliance policies and procedures annually for their adequacy and the effectiveness of their implementation. Our chief compliance officer and the chief compliance officer of Terra Income Advisors are responsible for administering these policies and procedures.

Proxy Voting Policies and Procedures

We have delegated our proxy voting responsibility to Terra Income Advisors. The proxy voting policies and procedures of Terra Income Advisors are set forth below. The guidelines are reviewed periodically by Terra Income Advisors and our disinterested directors, and, accordingly, are subject to change. For purposes of these Proxy Voting Policies and Procedures described below, “we” “our” and “us” refers to Terra Income Advisors.

Proxy Policies

As an investment adviser registered under the Advisers Act, we have a fiduciary duty to act solely in the best interests of our clients. As part of this duty, we recognize that we must vote client securities in a timely manner free of conflicts of interest and in the best interests of our clients.

These policies and procedures for voting proxies for our investment advisory clients are intended to comply with Section 206 of, and Rule 206(4)-6 under, the Advisers Act.

We vote proxies relating to our portfolio securities in the best interests of our clients’ stockholders. We review on a case-by-case basis each proposal submitted to a stockholder vote to determine its impact on the portfolio securities held by our clients. Although we generally vote against proposals that may have a negative impact on our clients’ portfolio securities, we may vote for such a proposal if there exist compelling long-term reasons to do so.

Our proxy voting decisions are made by the senior officers who are responsible for monitoring each of our client’s investments. To ensure that our vote is not the product of a conflict of interest, we require that: (i) anyone involved in the decision making process disclose to our Chief Compliance Officer any potential conflict that he or she is aware of and any contact that he or she has had with any interested party regarding a proxy vote; and (ii) employees involved in the decision making process or vote administration are prohibited from revealing how we intend to vote on a proposal in order to reduce any attempted influence from interested parties.

Proxy Voting Records

Investors may obtain information, without charge, regarding how Terra Income Advisors voted proxies with respect to our portfolio securities by making a written request for proxy voting information to: Chief Compliance Officer, Michael S. Cardello.

14

Other

As a BDC, we will be periodically examined by the SEC for compliance with applicable securities laws and related regulations.

We are required to provide and maintain a bond issued by a reputable fidelity insurance company to protect us against larceny and embezzlement. Furthermore, as a BDC, we are prohibited from protecting any director or officer against any liability to us or our stockholders arising from willful misfeasance, bad faith, gross negligence or reckless disregard of the duties involved in the conduct of such person’s office.

Available Information

We are required to file with or submit to the SEC annual, quarterly and current reports, proxy statements and other information meeting the informational requirements of the Exchange Act. We maintain a website at http://www.terrafund6.com, on which we make available, free of charge, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. Information contained on our website is not incorporated by reference into this annual report on Form 10-K and investors should not consider information contained on our website to be part of this annual report on Form 10-K or any other report we file with the SEC. Investors may also inspect and copy these reports, proxy statements and other information, as well as our registration statement and related exhibits and schedules, at the Public Reference Room of the SEC at 100 F Street, N.E., Washington, D.C. 20549. Investors may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-732-0330. The SEC maintains an Internet site that contains reports, proxy and information statements and other information filed electronically by us with the SEC, which are available on the SEC’s website at www.sec.gov. Copies of these reports, proxy and information statements and other information may be obtained, after paying a duplicating fee, by electronic request at the following e-mail address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Section, 100 F Street, N.E., Washington, D.C. 20549.

15

Item 1A. Risk Factors.

Investing in our common stock involves a number of significant risks. In addition to the other information contained in this Form 10-K, investors should consider carefully the following information before making an investment in our common stock. If any of the following events occur, our business, financial condition and results of operations could be materially and adversely affected. In such case, the NAV of our common stock could decline, and investors may lose all or part of their investment.

Risks Related to an Investment in Our Common Stock

Investors do not know the purchase price per share at the time they submit their subscription agreements and could receive fewer shares of common stock than anticipated if our Board determines to increase the offering price to comply with the requirement that we avoid selling shares below NAV per share.

The purchase price for our shares is determined at each semi-monthly closing date to ensure that the sales price, after deducting selling commissions, broker-dealer fees, and dealer manager fees, is equal to or greater than the NAV of our shares. As a result, in the event of an increase in our NAV per share, the purchase price may be higher than the prior semi-monthly closing price per share, and therefore an investor may receive a smaller number of shares than if he or she had subscribed at the prior semi-monthly closing price.

The Offering may be deemed to be a “blind pool” offering. An investor may not have the opportunity to evaluate historical data or assess future investments prior to purchasing our shares.

Investors are not able to evaluate the economic merits, transaction terms or other financial or operational data concerning future investments we make using the proceeds from the Offering prior to making a decision to purchase our shares. Investors must rely on Terra Income Advisors to implement our investment policies, to evaluate our investment opportunities and to structure the terms of our investments rather than evaluating our investments in advance of purchasing shares of our common stock. Because investors are not able to evaluate all of our investments in advance of purchasing our shares, the Offering may entail more risk than other types of offerings. This additional risk may hinder investors’ ability to achieve their own personal investment objectives related to portfolio diversification, risk-adjusted investment returns and other objectives.

The Offering is a “best efforts” offering, and if we are unable to raise substantial funds, we will be limited in the number and type of investments we may make, and the value of investors’ investment in us may be reduced in the event our assets under-perform.

The Offering is being made on a best efforts basis, whereby the dealer manager and broker-dealers participating in the Offering are only required to use their best efforts to sell our shares and have no firm commitment or obligation to purchase any of the shares. To the extent that less than the maximum number of shares is subscribed for, the opportunity for the allocation of our investments among various issuers may be decreased, and the returns achieved on those investments may be reduced as a result of allocating all of our expenses over a smaller capital base.

Our shares are not listed on an exchange or quoted through a quotation system, and will not be for the foreseeable future, if ever. Therefore, it is unlikely that investors will be able to sell them and, if they are able to do so, it is unlikely that they will receive a full return of their invested capital.

Our shares are illiquid, and as such there is no secondary market and it is not expected that any will develop in the foreseeable future. Our offering period may extend for an indefinite period, and during that time investors will have limited ability to sell their shares. Therefore, an investment in our shares is not suitable for investors who expect to require short-term liquidity from their investments.

Prior to the return of our stockholders’ capital contributions following repayment of our investments or, in the alternative, the completion of a liquidity event, our share repurchase program may provide a limited opportunity for investors, the return of our stockholders’ capital contributions, subject to certain restrictions and limitations, at a price which may reflect a discount from the purchase price paid for the shares being repurchased.

We are not obligated to provide liquidity to our stockholders by a finite date, either from the repayment to us of our debt investments within a reasonable period of time subsequent to the termination of the Offering or from a liquidity event; therefore, it will be difficult for an investor to sell his or her shares.

We are not obligated to provide liquidity to our stockholders by a finite date, either from the repayment to us of our debt investments within a reasonable period of time subsequent to the termination of the Offering, or from a liquidity event. A liquidity event could include (i) a listing of our shares on a national securities exchange, (ii) the sale of all or substantially all of our assets either on a complete portfolio basis or individually followed by a liquidation or (iii) a merger or another transaction approved by our Board in which our stockholders receive cash or shares of a publicly traded company. However, there can be no assurance that we will return our stockholders’ capital contributions by a specified date following either the repayment to us of our debt investments

16

or the completion of a liquidity event. In such event, the liquidity for an investor’s shares will be limited to our share repurchase program, which we have no obligation to maintain.

The dealer manager in the Offering may be unable to sell a sufficient number of shares for us to achieve our investment objectives.

The dealer manager for the Offering is Terra Capital Markets. There is no assurance that it will be able to sell a sufficient number of shares to allow us to have adequate funds to originate a portfolio of investments and generate income sufficient to cover our expenses. As a result, we may be unable to achieve our investment objectives and investors could lose some or all of the value of their investment.

Because the dealer manager is one of our affiliates, investors will not have the benefit of an independent due diligence review of us by our dealer manager, which is customarily performed in firm commitment offerings; the absence of an independent due diligence review increases the risks and uncertainty investors face as a stockholder.

The dealer manager is one of our affiliates. As a result, its due diligence review and investigation of us and this Form 10-K cannot be considered to be an independent review. Therefore, investors do not have the benefit of an independent review and investigation of the Offering of the type normally performed by an unaffiliated, independent underwriter in a firm commitment public securities offering.

Our ability to conduct the Offering successfully depends, in part, on the ability of the dealer manager to establish, operate and maintain a network of broker-dealers.

The success of the Offering, and correspondingly our ability to implement our business strategy, depends upon the ability of the dealer manager to establish, operate and maintain a network of licensed securities broker-dealers and other agents to sell our shares. If the dealer manager fails to perform, we may not be able to raise adequate proceeds through the Offering to implement our investment strategy. If we are unsuccessful in implementing our investment strategy, investors could lose all or a part of their investment.

The U.S. Department of Labor’s regulation expanding the definition of fiduciary investment advice under ERISA could adversely affect our financial condition and results of operations.

On April 6, 2016, the U.S. Department of Labor (the “DOL”) issued its final regulation redefining “investment advice fiduciary” under the Employee Retirement Income Security Act (“ERISA”) and the Internal Revenue Code. The final regulation significantly expands the class of advisers and the scope of investment advice that are subject to fiduciary standards, imposing the same fiduciary standards on advisers to individual retirement accounts that have historically only applied to plans covered by ERISA. The DOL also finalized certain prohibited transaction exemptions that allow investment advisers to receive compensation for providing investment advice under arrangements that would otherwise be prohibited due to conflicts of interest. The DOL regulations became effective on April 10, 2017, but financial institutions relying on the “Best Interest Contract Exemption” will be permitted to comply with only a limited set of requirements through July 1, 2019, and that deadline may be revised or extended further. Because the changes required by the DOL regulations are triggering significant changes in the operations of financial advisors and broker-dealers, the implementation of the regulations may impact our ability to raise funds and thereby may impact our financial condition and results of operations.

The implementation of changes to investor account statements described in Financial Industry Regulatory Authority Regulatory Notice 15-02 may impact our ability to raise funds.