Attached files

| file | filename |

|---|---|

| EX-10.3 - EXHIBIT 10.3 RESTRICTED STOCK UNIT AGREEMENT - Dine Brands Global, Inc. | din-2017930x10qxex103.htm |

| EX-32.2 - EXHIBIT 32.2 SECTION 906 CFO CERTIFICATION - Dine Brands Global, Inc. | din-2017930x10qxex322.htm |

| EX-32.1 - EXHIBIT 32.1 SECTION 906 CEO CERTIFICATION - Dine Brands Global, Inc. | din-2017930x10qxex321.htm |

| EX-31.2 - EXHIBIT 31.2 SECTION 302 CFO CERTIFICATION - Dine Brands Global, Inc. | din-2017930x10qxex312.htm |

| EX-31.1 - EXHIBIT 31.1 SECTION 302 CEO CERTIFICATION - Dine Brands Global, Inc. | din-2017930x10qxex311.htm |

| EX-12.1 - EXHIBIT 12.1 COMPUTATION OF RATIOS - Dine Brands Global, Inc. | din-2017930x10qxex121.htm |

| EX-10.4 - EXHIBIT 10.4 RESTRICTED STOCK UNIT AGREEMENT - Dine Brands Global, Inc. | din-2017930x10qxex104.htm |

| EX-10.2 - EXHIBIT 10.2 NONQUALIFIED STOCK OPTION AGREEMENT - Dine Brands Global, Inc. | din-2017930x10qxex102.htm |

| EX-10.1 - EXHIBIT 10.1 EMPLOYMENT AGREEMENT - Dine Brands Global, Inc. | din-2017930x10qxex101.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________________________

FORM 10-Q

(Mark One)

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2017

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number 001-15283

DineEquity, Inc.

DineEquity, Inc.

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 95-3038279 (I.R.S. Employer Identification No.) | |

450 North Brand Boulevard, Glendale, California (Address of principal executive offices) | 91203-1903 (Zip Code) | |

(818) 240-6055

(Registrant’s telephone number, including area code)

______________________________________________________________

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer o | |

Non-accelerated filer o (Do not check if a smaller reporting company) | ||

Smaller reporting company o | ||

Emerging growth company o | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

Class | Outstanding as of November 3, 2017 | |

Common Stock, $0.01 par value | 17,988,168 | |

DineEquity, Inc. and Subsidiaries

Index

Page | ||

Cautionary Statement Regarding Forward-Looking Statements

Statements contained in this report may constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements involve known and unknown risks, uncertainties and other factors, which may cause actual results to be materially different from those expressed or implied in such statements. You can identify these forward-looking statements by words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “believe,” “estimate,” “intend,” “plan” and other similar expressions. You should consider our forward-looking statements in light of the risks discussed under the heading “Risk Factors” in our most recent Annual Report on Form 10-K, as well as our consolidated financial statements, related notes, and the other financial information appearing elsewhere in this report and our other filings with the United States Securities and Exchange Commission. The forward-looking statements contained in this report are made as of the date hereof and the Company assumes no obligation to update or supplement any forward-looking statements.

Fiscal Quarter End

The Company’s fiscal quarters end on the Sunday closest to the last day of each calendar quarter. For convenience, the fiscal quarters of each year are referred to as ending on March 31, June 30, September 30 and December 31. The first fiscal quarter of 2017 began on January 2, 2017 and ended on April 2, 2017 and the second and third fiscal quarters of 2017 ended on July 2, 2017 and October 1, 2017, respectively. The first fiscal quarter of 2016 began on January 4, 2016 and ended on April 3, 2016 and the second and third fiscal quarters of 2016 ended on July 3, 2016 and October 2, 2016, respectively.

1

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements.

DineEquity, Inc. and Subsidiaries

Consolidated Balance Sheets

(In thousands, except share and per share amounts)

Assets | September 30, 2017 | December 31, 2016 | ||||||

(Unaudited) | ||||||||

Current assets: | ||||||||

Cash and cash equivalents | $ | 104,212 | $ | 140,535 | ||||

Receivables, net | 96,657 | 141,389 | ||||||

Restricted cash | 31,338 | 30,256 | ||||||

Prepaid gift card costs | 36,667 | 47,115 | ||||||

Prepaid income taxes | 8,749 | 2,483 | ||||||

Other current assets | 5,703 | 4,370 | ||||||

Total current assets | 283,326 | 366,148 | ||||||

Long-term receivables, net | 131,033 | 141,152 | ||||||

Property and equipment, net | 199,857 | 205,055 | ||||||

Goodwill | 339,236 | 697,470 | ||||||

Other intangible assets, net | 585,160 | 763,431 | ||||||

Deferred rent receivable | 84,071 | 86,981 | ||||||

Non-current restricted cash | 14,700 | 14,700 | ||||||

Other non-current assets, net | 3,825 | 3,646 | ||||||

Total assets | $ | 1,641,208 | $ | 2,278,583 | ||||

Liabilities and Stockholders’ (Deficit) Equity | ||||||||

Current liabilities: | ||||||||

Accounts payable | $ | 26,452 | $ | 50,503 | ||||

Gift card liability | 104,317 | 170,812 | ||||||

Dividends payable | 17,755 | 17,465 | ||||||

Accrued employee compensation and benefits | 13,527 | 14,609 | ||||||

Current maturities of long-term debt, capital lease and financing obligations | 16,202 | 13,144 | ||||||

Accrued advertising | 8,359 | 6,369 | ||||||

Other accrued expenses | 16,775 | 13,410 | ||||||

Total current liabilities | 203,387 | 286,312 | ||||||

Long-term debt, less current maturities | 1,281,950 | 1,282,691 | ||||||

Capital lease obligations, less current maturities | 64,923 | 74,665 | ||||||

Financing obligations, less current maturities | 39,292 | 39,499 | ||||||

Deferred income taxes, net | 178,848 | 253,898 | ||||||

Deferred rent payable | 65,449 | 69,572 | ||||||

Other non-current liabilities | 24,036 | 19,174 | ||||||

Total liabilities | 1,857,885 | 2,025,811 | ||||||

Commitments and contingencies | ||||||||

Stockholders’ (deficit) equity: | ||||||||

Common stock, $0.01 par value, shares: 40,000,000 authorized; September 30, 2017 - 25,033,220 issued, 17,996,223 outstanding; December 31, 2016 - 25,134,223 issued, 17,969,636 outstanding | 250 | 251 | ||||||

Additional paid-in-capital | 292,255 | 292,809 | ||||||

(Accumulated deficit) retained earnings | (86,634 | ) | 382,082 | |||||

Accumulated other comprehensive loss | (105 | ) | (107 | ) | ||||

Treasury stock, at cost; shares: September 30, 2017 - 7,036,997; December 31, 2016 - 7,164,587 | (422,443 | ) | (422,263 | ) | ||||

Total stockholders’ (deficit) equity | (216,677 | ) | 252,772 | |||||

Total liabilities and stockholders’ (deficit) equity | $ | 1,641,208 | $ | 2,278,583 | ||||

See the accompanying Notes to Consolidated Financial Statements.

2

DineEquity, Inc. and Subsidiaries

Consolidated Statements of Comprehensive (Loss) Income

(In thousands, except per share amounts)

(Unaudited)

Three Months Ended | Nine Months Ended | |||||||||||||||

September 30, | September 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Revenues: | ||||||||||||||||

Franchise and restaurant revenues | $ | 112,347 | $ | 123,259 | $ | 358,912 | $ | 380,034 | ||||||||

Rental revenues | 30,263 | 30,507 | 90,852 | 92,746 | ||||||||||||

Financing revenues | 2,061 | 2,251 | 6,280 | 7,019 | ||||||||||||

Total revenues | 144,671 | 156,017 | 456,044 | 479,799 | ||||||||||||

Cost of revenues: | ||||||||||||||||

Franchise and restaurant expenses | 41,800 | 41,553 | 123,476 | 122,129 | ||||||||||||

Rental expenses | 22,318 | 22,771 | 67,665 | 69,032 | ||||||||||||

Financing expenses | 449 | 9 | 449 | 155 | ||||||||||||

Total cost of revenues | 64,567 | 64,333 | 191,590 | 191,316 | ||||||||||||

Gross profit | 80,104 | 91,684 | 264,454 | 288,483 | ||||||||||||

General and administrative expenses | 38,030 | 36,002 | 125,701 | 111,937 | ||||||||||||

Impairment and closure charges | 532,522 | 206 | 535,440 | 3,932 | ||||||||||||

Interest expense | 15,353 | 15,358 | 46,496 | 46,107 | ||||||||||||

Amortization of intangible assets | 2,507 | 2,500 | 7,507 | 7,480 | ||||||||||||

(Gain) loss on disposition of assets | (35 | ) | 113 | (6,387 | ) | 679 | ||||||||||

(Loss) income before income tax benefit (provision) | (508,273 | ) | 37,505 | (444,303 | ) | 118,348 | ||||||||||

Income tax benefit (provision) | 56,555 | (13,232 | ) | 28,228 | (41,703 | ) | ||||||||||

Net (loss) income | (451,718 | ) | 24,273 | (416,075 | ) | 76,645 | ||||||||||

Other comprehensive (loss) income, net of tax: | ||||||||||||||||

Foreign currency translation adjustment | (2 | ) | (1 | ) | (2 | ) | — | |||||||||

Total comprehensive (loss) income | $ | (451,720 | ) | $ | 24,272 | $ | (416,077 | ) | $ | 76,645 | ||||||

Net (loss) income available to common stockholders: | ||||||||||||||||

Net (loss) income | $ | (451,718 | ) | $ | 24,273 | $ | (416,075 | ) | $ | 76,645 | ||||||

Less: Net loss (income) allocated to unvested participating restricted stock | 8,496 | (338 | ) | 6,921 | (1,103 | ) | ||||||||||

Net (loss) income available to common stockholders | $ | (443,222 | ) | $ | 23,935 | $ | (409,154 | ) | $ | 75,542 | ||||||

Net (loss) income available to common stockholders per share: | ||||||||||||||||

Basic | $ | (24.98 | ) | $ | 1.33 | $ | (23.09 | ) | $ | 4.17 | ||||||

Diluted | $ | (24.98 | ) | $ | 1.33 | $ | (23.09 | ) | $ | 4.15 | ||||||

Weighted average shares outstanding: | ||||||||||||||||

Basic | 17,742 | 17,950 | 17,718 | 18,099 | ||||||||||||

Diluted | 17,742 | 18,041 | 17,718 | 18,201 | ||||||||||||

Dividends declared per common share | $ | 0.97 | $ | 0.92 | $ | 2.91 | $ | 2.76 | ||||||||

Dividends paid per common share | $ | 0.97 | $ | 0.92 | $ | 2.91 | $ | 2.76 | ||||||||

See the accompanying Notes to Consolidated Financial Statements.

3

DineEquity, Inc. and Subsidiaries

Consolidated Statements of Cash Flows

(In thousands)

(Unaudited)

Nine Months Ended | ||||||||

September 30, | ||||||||

2017 | 2016 | |||||||

Cash flows from operating activities: | ||||||||

Net (loss) income | $ | (416,075 | ) | $ | 76,645 | |||

Adjustments to reconcile net (loss) income to cash flows provided by operating activities: | ||||||||

Impairment and closure charges | 535,306 | 1,461 | ||||||

Depreciation and amortization | 23,053 | 22,924 | ||||||

Non-cash interest expense | 2,509 | 2,400 | ||||||

Deferred income taxes | (77,345 | ) | (14,852 | ) | ||||

Non-cash stock-based compensation expense | 8,826 | 8,215 | ||||||

Tax benefit from stock-based compensation | — | 1,153 | ||||||

Excess tax benefit from stock-based compensation | — | (966 | ) | |||||

(Gain) loss on disposition of assets | (6,422 | ) | 679 | |||||

Other | (2,791 | ) | 456 | |||||

Changes in operating assets and liabilities: | ||||||||

Accounts receivable, net | (1,569 | ) | 4,312 | |||||

Current income tax receivables and payables | (1,699 | ) | (1,138 | ) | ||||

Gift card receivables and payables | (26,387 | ) | (30,355 | ) | ||||

Other current assets | (1,336 | ) | (824 | ) | ||||

Accounts payable | (7,530 | ) | (1,397 | ) | ||||

Accrued employee compensation and benefits | (1,146 | ) | (9,293 | ) | ||||

Other current liabilities | 3,606 | 2,638 | ||||||

Cash flows provided by operating activities | 31,000 | 62,058 | ||||||

Cash flows from investing activities: | ||||||||

Additions to property and equipment | (9,608 | ) | (3,543 | ) | ||||

Proceeds from sale of property and equipment | 1,100 | — | ||||||

Principal receipts from notes, equipment contracts and other long-term receivables | 15,283 | 13,969 | ||||||

Other | (356 | ) | (393 | ) | ||||

Cash flows provided by investing activities | 6,419 | 10,033 | ||||||

Cash flows from financing activities: | ||||||||

Dividends paid on common stock | (52,326 | ) | (50,790 | ) | ||||

Repurchase of common stock | (10,003 | ) | (45,010 | ) | ||||

Principal payments on capital lease and financing obligations | (10,621 | ) | (10,391 | ) | ||||

Tax payments for restricted stock upon vesting | (2,345 | ) | (2,680 | ) | ||||

Proceeds from stock options exercised | 2,635 | 1,282 | ||||||

Excess tax benefit from stock-based compensation | — | 966 | ||||||

Cash flows used in financing activities | (72,660 | ) | (106,623 | ) | ||||

Net change in cash, cash equivalents and restricted cash | (35,241 | ) | (34,532 | ) | ||||

Cash, cash equivalents and restricted cash at beginning of period | 185,491 | 192,013 | ||||||

Cash, cash equivalents and restricted cash at end of period | $ | 150,250 | $ | 157,481 | ||||

Supplemental disclosures: | ||||||||

Interest paid in cash | $ | 50,808 | $ | 51,940 | ||||

Income taxes paid in cash | $ | 50,813 | $ | 56,734 | ||||

See the accompanying Notes to Consolidated Financial Statements.

4

DineEquity, Inc. and Subsidiaries

Notes to Consolidated Financial Statements

(Unaudited)

1. General

The accompanying unaudited consolidated financial statements of DineEquity, Inc. (the “Company” or “DineEquity”) have been prepared in accordance with United States generally accepted accounting principles (“U.S. GAAP”) for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. The operating results for the nine months ended September 30, 2017 are not necessarily indicative of the results that may be expected for the twelve months ending December 31, 2017.

The consolidated balance sheet at December 31, 2016 has been derived from the audited consolidated financial statements at that date, but does not include all of the information and footnotes required by U.S. GAAP for complete financial statements.

These consolidated financial statements should be read in conjunction with the consolidated financial statements and footnotes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2016.

2. Basis of Presentation

The Company’s fiscal quarters end on the Sunday closest to the last day of each calendar quarter. For convenience, the fiscal quarters of each year are referred to as ending on March 31, June 30, September 30 and December 31. The first fiscal quarter of 2017 began on January 2, 2017 and ended on April 2, 2017 and the second and third fiscal quarters of 2017 ended on July 2, 2017 and October 1, 2017, respectively. The first fiscal quarter of 2016 began on January 4, 2016 and ended on April 3, 2016 and the second and third fiscal quarters of 2016 ended on July 3, 2016 and October 2, 2016, respectively.

The accompanying consolidated financial statements include the accounts of the Company and its subsidiaries that are consolidated in accordance with U.S. GAAP. All intercompany balances and transactions have been eliminated.

The preparation of financial statements in conformity with U.S. GAAP requires the Company’s management to make assumptions and estimates that affect the reported amounts of assets and liabilities, disclosures of contingent assets and liabilities, if any, at the date of the consolidated financial statements, and the reported amounts of revenues and expenses during the reporting period. Significant estimates are made in the calculation and assessment of the following: impairment of goodwill, other intangible assets and tangible assets; income taxes; allowance for doubtful accounts and notes receivables; lease accounting estimates; contingencies; and stock-based compensation. On an ongoing basis, the Company evaluates its estimates based on historical experience, current conditions and various other assumptions that are believed to be reasonable under the circumstances. The Company adjusts such estimates and assumptions when facts and circumstances dictate. Actual results could differ from those estimates.

3. Accounting Policies

Accounting Standards Adopted Effective January 2, 2017

In March 2016, the Financial Accounting Standards Board (“FASB”) issued new guidance that addresses accounting for certain aspects of share-based payments, including excess tax benefits or deficiencies, forfeiture estimates, statutory tax withholding and cash flow classification of certain share-based payment activity. The Company applied the prospective transition method in adopting the new guidance and prior period amounts have not been restated. Because of the adoption, the Company recognized an excess tax deficiency from stock-based compensation as a discrete item, increasing the income tax provision for the three and nine months ended September 30, 2017 by $0.1 million and $1.8 million, respectively. Historically, excess tax benefits or deficiencies were recorded as additional paid-in capital. The Company applied the prospective transition method with respect to the cash flow classification of certain share-based payment activity; accordingly, the cash flows for the nine months ended September 30, 2016 have not been restated. The Company has elected to maintain its practice of estimating forfeitures when recognizing expense for share-based payment awards. Amendments to the accounting for minimum statutory withholding requirements had no impact on the Company's Consolidated Financial Statements.

In November 2016, the FASB issued new guidance to reduce diversity in practice in the classification and presentation of changes in restricted cash in the statement of cash flows. The new guidance requires amounts generally described as restricted cash should be included with cash and cash equivalents when reconciling the beginning-of-period total amounts to the end-of-period total amounts shown on the statement of cash flows. Calendar year public entities will be required to adopt the new guidance beginning with the first fiscal quarter of 2018. The Company elected to adopt the new guidance retrospectively

5

DineEquity, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (Continued)

3. Accounting Policies (Continued)

effective January 2, 2017 and the cash flows for the nine months ended September 30, 2017 were restated. Adoption of the new guidance did not impact the Company's Consolidated Balance Sheets or Consolidated Statements of Comprehensive Income.

In January 2017, the FASB issued new guidance simplifying the test of goodwill for impairment. The new guidance requires a single-step quantitative test to measure potential impairment based on the excess of a reporting unit's carrying amount over its fair value. Calendar year public entities will be required to adopt the new guidance beginning with the first fiscal quarter of 2020. The Company has elected early adoption of the new guidance, as is permitted for interim or annual tests of goodwill performed after January 1, 2017.

Newly Issued Accounting Standards Not Yet Adopted

In August 2016, the FASB issued new guidance on the classification of certain cash receipts and payments in the statement of cash flows. The new guidance is intended to reduce diversity in practice in how certain transactions are classified in the statement of cash flows. The Company will be required to adopt the new guidance beginning with its first fiscal quarter of 2018. Early adoption is permitted. The Company is currently assessing the impact that the new guidance will have on its consolidated statements of cash flows.

In June 2016, the FASB issued new guidance on the measurement of credit losses on financial instruments. The new guidance will replace the incurred loss methodology of recognizing credit losses on financial instruments that is currently required with a methodology that estimates the expected credit loss on financial instruments and reflects the net amount expected to be collected on the financial instrument. Application of the new guidance may result in the earlier recognition of credit losses as the new methodology will require entities to consider forward-looking information in addition to historical and current information used in assessing incurred losses. The Company will be required to adopt the new guidance on a modified retrospective basis beginning with its first fiscal quarter of 2020, with early adoption permitted in its first fiscal quarter of 2019. The Company is currently evaluating the impact of the new guidance on its consolidated financial statements and related disclosures and whether early adoption will be elected.

In February 2016, the FASB issued new guidance with respect to the accounting for leases. The new guidance will require lessees to recognize a right-of-use asset and a lease liability for virtually all leases, other than leases with a term of 12 months or less, and to provide additional disclosures about leasing arrangements. Accounting by lessors is largely unchanged from existing accounting guidance. The Company will be required to adopt the new guidance on a modified retrospective basis beginning with its first fiscal quarter of 2019. Early adoption is permitted.

While the Company is still in the process of evaluating the impact of the new guidance on its consolidated financial statements and disclosures, the Company expects adoption of the new guidance will have a material impact on its Consolidated Balance Sheets due to recognition of the right-of-use asset and lease liability related to its operating leases. While the new guidance is also expected to impact the measurement and presentation of elements of expenses and cash flows related to leasing arrangements, the Company does not presently believe there will be a material impact on its Consolidated Statements of Comprehensive Income or Consolidated Statements of Cash Flows. Recognition of a lease liability related to operating leases will not impact any covenants related to the Company's long-term debt because the debt agreements specify that covenant ratios be calculated using U.S. GAAP in effect at the time the debt agreements were entered into.

In January 2016, the FASB issued guidance on the recognition and measurement of financial instruments. The guidance modifies how entities measure certain equity investments and present changes in the fair value of those investments, as well as changes how fair value of financial instruments is measured for disclosure purposes. The amendment is effective commencing with the Company's first fiscal quarter of 2018. The Company is currently evaluating the impact of the new guidance on its financial statements and disclosures.

In May 2014, the FASB issued new accounting guidance on revenue recognition, which provides for a single, five-step model to be applied to all revenue contracts with customers. The new standard also requires additional financial statement disclosures that will enable users to understand the nature, amount, timing and uncertainty of revenue and cash flows relating to customer contracts. Companies have an option to use either the full retrospective method or the modified retrospective method to implement the standard. In August 2015, the FASB deferred the effective date of the new revenue guidance by one year such that the Company will be required to adopt the new guidance beginning with its first fiscal quarter of 2018. The FASB has subsequently issued several clarifications on specific topics within the new revenue recognition guidance that did not change the core principles of the guidance originally issued in May 2014.

6

DineEquity, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (Continued)

3. Accounting Policies (Continued)

This new guidance supersedes nearly all the existing general revenue recognition guidance under U.S. GAAP as well as most industry-specific revenue recognition guidance, including guidance with respect to revenue recognition by franchisors. The Company believes the recognition of the majority of its revenues, including franchise royalty revenues and sales of IHOP pancake and waffle dry mix will not be affected by the new guidance. Additionally, lease rental revenues are not within the scope of the new guidance.

The Company believes the new guidance will impact the timing of recognition of franchise and development fees. Under existing guidance, these fees are typically recognized upon the opening of restaurants. Under the new guidance, the Company believes the fees will have to be deferred and recognized as revenue over the term of the individual franchise agreements. However, the effect of the required deferral of fees received in any given year will be mitigated by the recognition of revenue from fees retrospectively deferred from prior years. The Company has essentially completed reviewing most of its nearly 4,000 agreements to obtain the data elements necessary to implement the new guidance and is in the process of quantifying the impact of the new guidance on its consolidated financial statements and related disclosures.

The Company also believes the new guidance will impact the accounting for transactions related to the Applebee's national advertising fund. Currently, franchisee contributions to and expenditures of the Applebee's national advertising fund are not included in the Consolidated Statements of Comprehensive Income. Under the new guidance, the Company would include contributions to and expenditures from the Applebee's advertising fund within the Consolidated Statements of Comprehensive Income as is currently done with contributions to and expenditures from the IHOP national advertising fund and with international restaurants of both brands. While this change will materially impact the gross amount of reported franchise revenues and expenses, the impact would be an offsetting increase to both revenue and expense such that the impact on gross profit and net income, if any, would not be material.

The Company presently expects to use the full retrospective method of adoption when the new revenue guidance is adopted in the first fiscal quarter of 2018.

The Company reviewed all other newly issued accounting pronouncements and concluded that they either are not applicable to the Company's operations or that no material effect is expected on the Company's financial statements because of future adoption.

4. Goodwill and Intangible Assets

Changes in the carrying amount of goodwill for the nine months ended September 30, 2017 are as follows:

Applebee's Franchise Unit | IHOP Franchise Unit | Total | |||||||||

(In millions) | |||||||||||

Balance at December 31, 2016: | |||||||||||

Goodwill, gross | $ | 686.7 | $ | 10.8 | $ | 697.5 | |||||

Accumulated impairment loss | — | — | — | ||||||||

Goodwill | 686.7 | 10.8 | 697.5 | ||||||||

Impairment loss | (358.2 | ) | — | (358.2 | ) | ||||||

Balance at September 30, 2017: | |||||||||||

Goodwill, gross | 686.7 | 10.8 | 697.5 | ||||||||

Accumulated impairment loss | (358.2 | ) | — | (358.2 | ) | ||||||

Goodwill | $ | 328.5 | $ | 10.8 | $ | 339.2 | |||||

7

DineEquity, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (Continued)

4. Goodwill and Intangible Assets (Continued)

Changes in the carrying amount of intangible assets for the nine months ended September 30, 2017 are as follows:

Not Subject to Amortization | Subject to Amortization | ||||||||||||||||||

Applebee's Tradename | Other | Applebee's Franchising Rights | Leaseholds | Total | |||||||||||||||

(In millions) | |||||||||||||||||||

Balance at December 31, 2016 | $ | 652.4 | $ | 2.0 | $ | 109.0 | $ | — | $ | 763.4 | |||||||||

Impairment | (173.4 | ) | — | — | — | (173.4 | ) | ||||||||||||

Amortization expense | — | — | (7.5 | ) | (0.0 | ) | (7.5 | ) | |||||||||||

Additions | — | 0.4 | — | 2.3 | 2.7 | ||||||||||||||

Balance at September 30, 2017 | $ | 479.0 | $ | 2.4 | $ | 101.5 | $ | 2.3 | $ | 585.2 | |||||||||

The Company evaluates its goodwill and the indefinite-lived Applebee's tradename for impairment annually in the fourth quarter of each year. In addition to the annual evaluation for impairment, goodwill and indefinite-lived intangible assets are evaluated more frequently if the Company believes indicators of impairment exist.

In the third quarter of 2017, the Company noted that the decline in the market price of the Company's common stock since December 31, 2016, which the Company had believed to be temporary, persisted throughout the first eight months of 2017 and that the favorable trend in Applebee's domestic same-restaurant sales experienced in the second quarter of 2017 did not continue into the first two months of the third quarter. The Company also noted a continuing increase in Applebee's bad debt expense and in royalties not recognized in income until paid in cash. Additionally, the Company also determined an increasing shortfall in franchisee contributions to the Applebee's national advertising fund could require a larger amount of future subsidization in the form of additional franchisor contributions to the fund than previously estimated. Based on these unfavorable developments, primarily the decline in the market price of the Company's common stock, the Company determined that indicators of impairment existed and that an interim test of goodwill and indefinite-lived intangible assets for impairment should be performed.

The Company performed an interim quantitative test of impairment of Applebee's goodwill and tradename in the third quarter of 2017. In performing the quantitative test of goodwill, the Company used the income approach method of valuation that included the discounted cash flow method as well as other generally accepted valuation methodologies to determine the fair value of goodwill and intangible assets. Significant assumptions used to determine fair value under the discounted cash flow model included expected future trends in sales, operating expenses, overhead expenses, capital expenditures and changes in working capital, along with an appropriate discount rate based on the Company's estimated cost of equity capital and after-tax cost of debt.

In performing the impairment review of the tradename, the Company used the relief of royalty method under the income approach method of valuation. Significant assumptions used to determine fair value under the relief of royalty method include future trends in sales, a royalty rate and a discount rate to be applied to the forecast revenue stream.

As a result of performing the quantitative test of impairment, the Company recognized an impairment of Applebee's goodwill of $358.2 million and an impairment of Applebee's tradename of $173.4 million. The Company adopted the guidance in FASB Accounting Standards Update 2017-04 on January 1, 2017; accordingly, the amount of the goodwill impairment was determined as the amount by which the carrying amount of the goodwill exceeded the fair value of the Applebee's franchise reporting unit as estimated in the impairment test. These assets are at risk of additional impairment in the future in the event of sustained downward movement in the Company's stock price, downward revisions of long-term performance assumptions or increases in the assumed long-term discount rate.

8

DineEquity, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (Continued)

5. Stockholders' Equity

Dividends

During the nine months ended September 30, 2017, the Company paid dividends on common stock of $52.3 million, representing cash dividends of $0.97 per share declared in the fourth quarter of 2016 and the first and second quarters of 2017. On August 10, 2017, the Company's Board of Directors declared a third quarter 2017 cash dividend of $0.97 per share of common stock. This dividend was paid on October 6, 2017 to the Company's stockholders of record at the close of business on September 18, 2017. The Company reported dividends payable of $17.8 million at September 30, 2017.

Stock Repurchase Program

In October 2015, the Company's Board of Directors approved a stock repurchase program authorizing the Company to repurchase up to $150 million of DineEquity common stock (the “2015 Repurchase Program”) on an opportunistic basis from time to time in open market transactions and in privately negotiated transactions based on business, market, applicable legal requirements and other considerations. The 2015 Repurchase Program, as approved by the Board of Directors, does not require the repurchase of a specific number of shares and can be terminated at any time. A summary of shares repurchased under the 2015 Repurchase Program, during the nine months ended September 30, 2017 and cumulatively, is as follows:

2015 Repurchase Program | Shares | Cost of shares | ||||

(In millions) | ||||||

Repurchased during the three months ended September 30, 2017 | — | $ | — | |||

Repurchased during the nine months ended September 30, 2017 | 145,786 | $ | 10.0 | |||

Cumulative repurchases as of September 30, 2017 | 1,000,657 | $ | 82.9 | |||

Remaining dollar value of shares that may be repurchased | n/a | $ | 67.1 | |||

Treasury Stock

Repurchases of DineEquity common stock are included in treasury stock at the cost of shares repurchased plus any transaction costs. Treasury stock may be re-issued when stock options are exercised, when restricted stock awards are granted and when restricted stock units settle in stock upon vesting. The cost of treasury stock re-issued is determined using the first-in, first-out (“FIFO”) method. During the nine months ended September 30, 2017, the Company re-issued 273,376 shares of treasury stock at a total FIFO cost of $9.8 million.

6. Income Taxes

The Company's effective tax rate was 6.4% for the nine months ended September 30, 2017 as compared to 35.2% for the nine months ended September 30, 2016. The effective tax rate of 6.4% for the nine months ended September 30, 2017 (the tax benefit of $28.2 million on the pretax book loss of $444.3 million) was significantly different than the statutory federal tax rate of 35% because the $358.2 million impairment of goodwill (see Note 4) is not deductible for federal income tax purposes and therefore has no associated tax benefit. The Company did recognize a tax benefit of $65.1 million as a discrete item related to the $173.4 million impairment of Applebee's tradename.

The total gross unrecognized tax benefit as of September 30, 2017 and December 31, 2016 was $5.9 million and $3.9 million, respectively, excluding interest, penalties and related tax benefits. The Company estimates the unrecognized tax benefit may decrease over the upcoming 12 months by an amount up to $1.8 million related to settlements with taxing authorities and the lapse of statutes of limitations. For the remaining liability, due to the uncertainties related to these tax matters, the Company is unable to make a reasonably reliable estimate as to when cash settlement with a taxing authority will occur.

As of September 30, 2017, accrued interest was $1.0 million and accrued penalties were less than $0.1 million, excluding any related income tax benefits. As of December 31, 2016, accrued interest was $1.0 million and accrued penalties were less than $0.1 million, excluding any related income tax benefits. The Company recognizes interest accrued related to unrecognized tax benefits and penalties as a component of its income tax provision recognized in its Consolidated Statements of Comprehensive Income.

The Company files federal income tax returns and the Company or one of its subsidiaries files income tax returns in various state and foreign jurisdictions. With few exceptions, the Company is no longer subject to federal, state or non-United States tax examinations by tax authorities for years before 2011. The Internal Revenue Service commenced examination of the Company’s U.S. federal income tax return for the tax years 2011 to 2013 during the year. The examination is currently in process. The Company believes that adequate reserves have been provided relating to all matters contained in the tax periods open to examination.

9

DineEquity, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (Continued)

7. Stock-Based Compensation

The following table summarizes the components of stock-based compensation expense included in general and administrative expenses in the Consolidated Statements of Comprehensive Income:

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(In millions) | |||||||||||||||

Total stock-based compensation expense: | |||||||||||||||

Equity classified awards expense | $ | 1.3 | $ | 2.6 | $ | 9.0 | $ | 8.3 | |||||||

Liability classified awards expense | — | (0.5 | ) | (1.1 | ) | 0.6 | |||||||||

Total pre-tax stock-based compensation expense | 1.3 | 2.1 | 7.9 | 8.9 | |||||||||||

Book income tax benefit | (0.5 | ) | (0.7 | ) | (3.0 | ) | (3.3 | ) | |||||||

Total stock-based compensation expense, net of tax | $ | 0.8 | $ | 1.4 | $ | 4.9 | $ | 5.6 | |||||||

As of September 30, 2017, total unrecognized compensation expense of $17.6 million related to restricted stock and restricted stock units and $3.2 million related to stock options are expected to be recognized over a weighted average period of 2.1 years for restricted stock and restricted stock units and 1.9 years for stock options.

Fair Value Assumptions

The Company granted 537,030 stock options during the nine months ended September 30, 2017 for which the fair value was estimated using a Black-Scholes option pricing model. The following summarizes the assumptions used in the Black-Scholes model:

Risk-free interest rate | 1.9 | % |

Weighted average historical volatility | 22.9 | % |

Dividend yield | 7.3 | % |

Expected years until exercise | 4.5 | |

Weighted average fair value of options granted | $4.31 | |

The Company granted 350,000 performance-based stock options and 175,000 performance-based restricted stock units during the three months ended September 30, 2017 for which the fair value was estimated using a Monte Carlo simulation method. The following summarizes the assumptions used in estimating the fair values:

Risk-free interest rate | 1.6 | % |

Weighted average historical volatility | 30.0 | % |

Dividend yield | 9.6 | % |

Expected years until exercise | 3.4 | |

Weighted average fair value of options granted | $3.07 | |

Weighted average fair value of restricted stock units granted | $10.19 | |

10

DineEquity, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (Continued)

7. Stock-Based Compensation (Continued)

Equity Classified Awards - Stock Options

Stock option balances at September 30, 2017, and activity for the nine months ended September 30, 2017 were as follows:

Shares | Weighted Average Exercise Price | Weighted Average Remaining Contractual Term (in Years) | Aggregate Intrinsic Value (in Millions) | ||||||||||

Outstanding at December 31, 2016 | 701,134 | $ | 80.04 | ||||||||||

Granted | 887,030 | 48.35 | |||||||||||

Exercised | (64,916 | ) | 40.59 | ||||||||||

Expired | (58,217 | ) | 84.43 | ||||||||||

Forfeited | (171,847 | ) | 65.82 | ||||||||||

Outstanding at September 30, 2017 | 1,293,184 | 61.98 | 7.3 | $ | 0.9 | ||||||||

Vested at September 30, 2017 and Expected to Vest | 1,111,610 | 64.50 | 7.0 | $ | 0.6 | ||||||||

Exercisable at September 30, 2017 | 456,308 | $ | 81.35 | 3.3 | $ | 0.0 | |||||||

The aggregate intrinsic value in the table above represents the total pre-tax intrinsic value (the difference between the closing stock price of the Company’s common stock on the last trading day of the third quarter of 2017 and the exercise price, multiplied by the number of in-the-money options) that would have been received by the option holders had all option holders exercised their options on September 30, 2017. The aggregate intrinsic value will change based on the fair market value of the Company’s common stock and the number of in-the-money options.

Equity Classified Awards - Restricted Stock and Restricted Stock Units

Outstanding balances as of September 30, 2017, and activity related to restricted stock and restricted stock units for the nine months ended September 30, 2017 were as follows:

Restricted Stock | Weighted Average Grant Date Fair Value | Restricted Stock Units | Weighted Average Grant Date Fair Value | |||||||||||

Outstanding at December 31, 2016 | 235,472 | $ | 92.81 | 34,058 | $ | 93.95 | ||||||||

Granted | 208,460 | 52.08 | 275,578 | 22.37 | ||||||||||

Released | (89,911 | ) | 88.65 | (12,683 | ) | 81.63 | ||||||||

Forfeited | (73,409 | ) | 79.44 | — | — | |||||||||

Outstanding at September 30, 2017 | 280,612 | $ | 67.38 | 296,953 | $ | 28.39 | ||||||||

Liability Classified Awards - Long-Term Incentive Awards

The Company has granted cash long-term incentive awards (“LTIP awards”) to certain employees. Annual LTIP awards vest over a three-year period and are determined using a multiplier from 0% to 200% of the target award based on the total stockholder return of DineEquity common stock compared to the total stockholder returns of a peer group of companies. Although LTIP awards are only paid in cash, since the multiplier is based on the price of the Company's common stock, the awards are considered stock-based compensation in accordance with U.S. GAAP and are classified as liabilities. For the three months ended September 30, 2017, no expense was recognized. For the three months ended September 30, 2016, a credit of $0.5 million was included in total stock-based compensation expense related to LTIP awards. For the nine months ended September 30, 2017 and 2016, a credit of $1.0 million and an expense of $0.6 million, respectively, were included in total stock-based compensation expense related to LTIP awards. At September 30, 2017 and December 31, 2016, liabilities of less than $0.1 million and liabilities of $1.2 million, respectively, related to LTIP awards were included as part of accrued employee compensation and benefits in the Consolidated Balance Sheets.

11

DineEquity, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (Continued)

8. Segments

The Company currently has three operating segments: franchise operations (an aggregation of Applebee’s and IHOP franchise operations), rental operations and financing operations. Prior to June 2017, the Company operated 10 IHOP restaurants and those operations were considered to be a fourth operating segment. The Company views all operating segments as reportable segments regardless of whether an operating segment exceeds 10% of consolidated revenues, segment profit or total assets.

As of September 30, 2017, the franchise operations segment consisted of (i) 1,945 restaurants operated by Applebee’s franchisees in the United States, two U.S. territories and 14 countries outside the United States and (ii) 1,761 restaurants operated by IHOP franchisees and area licensees in the United States, three U.S. territories and 13 countries outside the United States. Franchise operations revenue consists primarily of franchise royalty revenues, sales of proprietary products to franchisees (primarily pancake and waffle dry mixes for the IHOP restaurants), franchise advertising fees from domestic IHOP restaurants and international restaurants of both brands and franchise fees. Franchise operations expenses include advertising expenses from domestic IHOP restaurants and international restaurants of both brands, the cost of IHOP proprietary products, bad debt expense, franchisor contributions to marketing funds, pre-opening training expenses and other franchise-related costs.

Rental operations revenue includes revenue from operating leases and interest income from direct financing leases. Rental operations expenses are costs of operating leases and interest expense from capital leases on franchisee-operated restaurants.

Company restaurant sales are retail sales at company-operated restaurants. Company restaurant expenses are operating expenses at company-operated restaurants and include food, labor, utilities, rent and other restaurant operating costs. In June 2017, the Company refranchised nine of ten company-operated restaurants in the Cincinnati, Ohio market area; the one restaurant not refranchised was permanently closed. As a result, the Company no longer operates any IHOP restaurants on a permanent basis. The Company has not presented these restaurants as discontinued operations as defined by U.S. GAAP because the refranchising of nine restaurants out of a total of over 3,700 restaurants did not represent a strategic shift that had a major effect on the Company's operations.

From time to time, the Company may operate IHOP restaurants reacquired from franchisees on a temporary basis until those restaurants are refranchised. There were no IHOP restaurants under temporary operation at September 30, 2017.

Financing operations revenue primarily consists of interest income from the financing of franchise fees and equipment leases and sales of equipment associated with refranchised IHOP restaurants. Financing expenses are primarily the cost of restaurant equipment associated with refranchised IHOP restaurants.

12

DineEquity, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (Continued)

8. Segments (Continued)

Information on segments is as follows:

Three months ended September 30, | Nine months ended September 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

(In millions) | ||||||||||||||||

Revenues from external customers: | ||||||||||||||||

Franchise operations | $ | 112.3 | $ | 119.2 | $ | 351.4 | $ | 366.7 | ||||||||

Rental operations | 30.3 | 30.5 | 90.9 | 92.7 | ||||||||||||

Company restaurants | — | 4.0 | 7.5 | 13.4 | ||||||||||||

Financing operations | 2.1 | 2.3 | 6.3 | 7.0 | ||||||||||||

Total | $ | 144.7 | $ | 156.0 | $ | 456.0 | $ | 479.8 | ||||||||

Interest expense: | ||||||||||||||||

Rental operations | $ | 2.6 | $ | 2.9 | $ | 8.0 | $ | 9.0 | ||||||||

Company restaurants | — | 0.1 | 0.2 | 0.3 | ||||||||||||

Corporate | 15.4 | 15.4 | 46.5 | 46.1 | ||||||||||||

Total | $ | 18.0 | $ | 18.4 | $ | 54.7 | $ | 55.4 | ||||||||

Depreciation and amortization: | ||||||||||||||||

Franchise operations | $ | 2.7 | $ | 2.7 | $ | 8.1 | $ | 7.9 | ||||||||

Rental operations | 3.0 | 3.1 | 9.1 | 9.4 | ||||||||||||

Company restaurants | — | 0.1 | 0.1 | 0.3 | ||||||||||||

Corporate | 1.9 | 1.5 | 5.8 | 5.3 | ||||||||||||

Total | $ | 7.6 | $ | 7.4 | $ | 23.1 | $ | 22.9 | ||||||||

Gross profit, by segment: | ||||||||||||||||

Franchise operations | $ | 70.5 | $ | 81.9 | $ | 235.7 | $ | 258.7 | ||||||||

Rental operations | 8.0 | 7.7 | 23.2 | 23.7 | ||||||||||||

Company restaurants | (0.0 | ) | (0.2 | ) | (0.3 | ) | (0.7 | ) | ||||||||

Financing operations | 1.6 | 2.3 | 5.9 | 6.8 | ||||||||||||

Total gross profit | 80.1 | 91.7 | 264.5 | 288.5 | ||||||||||||

Corporate and unallocated expenses, net | (588.4 | ) | (54.2 | ) | (708.8 | ) | (170.1 | ) | ||||||||

(Loss) income before income tax provision | $ | (508.3 | ) | $ | 37.5 | $ | (444.3 | ) | $ | 118.3 | ||||||

13

DineEquity, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (Continued)

9. Net (Loss) Income per Share

The computation of the Company's basic and diluted net (loss) income per share is as follows:

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(In thousands, except per share data) | |||||||||||||||

Numerator for basic and diluted (loss) income per common share: | |||||||||||||||

Net (loss) income | $ | (451,718 | ) | $ | 24,273 | $ | (416,075 | ) | $ | 76,645 | |||||

Less: Net loss (income) allocated to unvested participating restricted stock | 8,496 | (338 | ) | 6,921 | (1,103 | ) | |||||||||

Net (loss) income available to common stockholders - basic | (443,222 | ) | 23,935 | (409,154 | ) | 75,542 | |||||||||

Effect of unvested participating restricted stock in two-class calculation | — | 1 | 5 | 3 | |||||||||||

Net (loss) income available to common stockholders - diluted | $ | (443,222 | ) | $ | 23,936 | $ | (409,149 | ) | $ | 75,545 | |||||

Denominator: | |||||||||||||||

Weighted average outstanding shares of common stock - basic | 17,742 | 17,950 | 17,718 | 18,099 | |||||||||||

Dilutive effect of stock options | — | 91 | — | 102 | |||||||||||

Weighted average outstanding shares of common stock - diluted | 17,742 | 18,041 | 17,718 | 18,201 | |||||||||||

Net (loss) income per common share: | |||||||||||||||

Basic | $ | (24.98 | ) | $ | 1.33 | $ | (23.09 | ) | $ | 4.17 | |||||

Diluted | $ | (24.98 | ) | $ | 1.33 | $ | (23.09 | ) | $ | 4.15 | |||||

For the three and nine months ended September 30, 2017, diluted loss per common share was computed using the weighted average number of shares outstanding during each period as the 1,000 and 11,000 shares, respectively, from common stock equivalents would have been antidilutive.

10. Fair Value Measurements

The Company does not have a material amount of financial assets or liabilities that are required under U.S. GAAP to be measured on a recurring basis at fair value. The Company is not a party to any derivative financial instruments. The Company does not have a material amount of non-financial assets or non-financial liabilities that are required under U.S. GAAP to be measured at fair value on a recurring basis. The Company has not elected to use the fair value measurement option, as permitted under U.S. GAAP, for any assets or liabilities for which fair value measurement is not presently required.

The Company believes the fair values of cash equivalents, accounts receivable and accounts payable approximate their carrying amounts due to their short duration.

The fair values of the Company's Series 2014-1 Class A-2 Notes (the “Class A-2 Notes”) at September 30, 2017 and December 31, 2016 were as follows:

September 30, 2017 | December 31, 2016 | |||||||||||||||

Carrying Amount | Fair Value | Carrying Amount | Fair Value | |||||||||||||

(In millions) | ||||||||||||||||

Long-term debt, current and long-term | $ | 1,285.2 | $ | 1,274.0 | $ | 1,282.7 | $ | 1,286.2 | ||||||||

The fair values were determined based on Level 2 inputs, including information gathered from brokers who trade in the Company’s Class A-2 Notes and information on notes that are similar to those of the Company.

14

DineEquity, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (Continued)

11. Commitments and Contingencies

Litigation, Claims and Disputes

The Company is subject to various lawsuits, administrative proceedings, audits and claims arising in the ordinary course of business. Some of these lawsuits purport to be class actions and/or seek substantial damages. The Company is required under U.S. GAAP to record an accrual for litigation loss contingencies that are both probable and reasonably estimable. Legal fees and expenses associated with the defense of all of the Company's litigation are expensed as such fees and expenses are incurred. Management regularly assesses the Company's insurance coverage, analyzes litigation information with the Company's attorneys and evaluates the Company's loss experience in connection with pending legal proceedings. While the Company does not presently believe that any of the legal proceedings to which it is currently a party will ultimately have a material adverse impact on the Company, there can be no assurance that the Company will prevail in all the proceedings the Company is party to, or that the Company will not incur material losses from them.

Lease Guarantees

In connection with the sale of Applebee’s restaurants or previous brands to franchisees and other parties, the Company has, in certain cases, guaranteed or has potential continuing liability for lease payments totaling $325.2 million as of September 30, 2017. This amount represents the maximum potential liability for future payments under these leases. These leases have been assigned to the buyers and expire at the end of the respective lease terms, which range from 2017 through 2048. Excluding unexercised option periods, the Company's potential liability for future payments under these leases is $54.5 million. In the event of default, the indemnity and default clauses in the sale or assignment agreements govern the Company's ability to pursue and recover damages incurred. No material lease payment guarantee liabilities have been recorded as of September 30, 2017.

12. Allowance for Credit Losses

The Company's allowance for credit losses at September 30, 2017 and December 31, 2016 was $13.1 million and $3.1 million, respectively.

13. Restricted Cash

Current restricted cash of $31.3 million at September 30, 2017 primarily consisted of $23.9 million of funds required to be held in trust in connection with the Company's securitized debt and $7.0 million of funds from Applebee's franchisees pursuant to franchise agreements, usage of which was restricted to advertising activities. Current restricted cash of $30.3 million at December 31, 2016 primarily consisted of $25.7 million of funds required to be held in trust in connection with the Company's securitized debt and $4.3 million of funds from Applebee's franchisees pursuant to franchise agreements, usage of which was restricted to advertising activities. Non-current restricted cash of $14.7 million at September 30, 2017 and December 31, 2016 represents interest reserves required to be set aside for the duration of the Company's securitized debt.

14. Refranchising of Company-operated Restaurants

In June 2017, the Company completed the refranchising and sale of related restaurant assets of nine company-operated IHOP restaurants in the Cincinnati, Ohio market area. As part of the transaction, the Company entered into an asset purchase agreement, nine franchise agreements and nine sublease agreements for land and buildings. The Company compared the stated rent under the sublease agreements with comparable market rents and recorded net favorable lease assets of $2.3 million in connection with the transaction. The Company also received cash of $1.1 million and a note receivable for $4.8 million. After allocating a portion of the consideration to franchise fees and derecognition of the assets sold, the Company recognized a gain of $6.2 million on the refranchising and sale during the nine months ended September 30, 2017.

15

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Cautionary Statement Regarding Forward-Looking Statements

Statements contained in this report may constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements involve known and unknown risks, uncertainties and other factors, which may cause actual results to be materially different from those expressed or implied in such statements. You can identify these forward-looking statements by words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “believe,” “estimate,” “intend,” “plan” and other similar expressions. You should consider our forward-looking statements in light of the risks discussed under the heading “Risk Factors” in our most recent Annual Report on Form 10-K, as well as our consolidated financial statements, related notes, and the other financial information appearing elsewhere in this report and our other filings with the United States Securities and Exchange Commission. The forward-looking statements contained in this report are made as of the date hereof and the Company assumes no obligation to update or supplement any forward-looking statements.

You should read the following Management's Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) in conjunction with the consolidated financial statements and the related notes that appear elsewhere in this report.

Overview

The following discussion and analysis provides information which we believe is relevant to an assessment and understanding of our consolidated results of operations and financial condition. The discussion should be read in conjunction with the consolidated financial statements and the notes thereto included in Item 1 of Part I of this Quarterly Report and the audited consolidated financial statements and notes thereto and the MD&A contained in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2016. Except where the context indicates otherwise, the words “we,” “us,” “our,” “DineEquity” and the “Company” refer to DineEquity, Inc., together with its subsidiaries that are consolidated in accordance with United States generally accepted accounting principles (“U.S. GAAP”).

Through various subsidiaries, we own and franchise the Applebee's Neighborhood Grill & Bar® (“Applebee's”) concept in the bar and grill segment within the casual dining category of the restaurant industry and the International House of Pancakes® (“IHOP”) concept in the family dining category of the restaurant industry. References herein to Applebee's® and IHOP® restaurants are to these two restaurant concepts, whether operated by franchisees or area licensees and their sub-licensees (collectively, “area licensees”). With over 3,700 restaurants combined, all of which are franchised, we believe we are one of the largest full-service restaurant companies in the world. The June 19, 2017 issue of Nation's Restaurant News reported that IHOP and Applebee's were the largest restaurant systems in the family dining and casual dining categories, respectively, in terms of United States system-wide sales during 2016. This marks the tenth consecutive year our two brands have achieved the number one ranking in Nation's Restaurant News.

The Company currently has three operating segments: franchise operations (an aggregation of Applebee’s and IHOP franchise operations), rental operations and financing operations. Prior to June 2017, the Company operated 10 IHOP restaurants and those operations were considered to be a fourth operating segment. The Company views all operating segments as reportable segments regardless of whether an operating segment exceeds 10% of consolidated revenues, segment profit or total assets.

16

Key Financial Results

Three months ended September 30, | Favorable (Unfavorable) Variance | Nine months ended September 30, | Favorable (Unfavorable) Variance | |||||||||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||||||||||

(In millions, except per share data) | ||||||||||||||||||||||||

(Loss) income before income taxes | $ | (508.3 | ) | $ | 37.5 | $ | (545.8 | ) | $ | (444.3 | ) | $ | 118.3 | $ | (562.7 | ) | ||||||||

Income tax benefit (provision) | 56.6 | (13.2 | ) | 69.8 | 28.2 | (41.7 | ) | 69.9 | ||||||||||||||||

Net (loss) income | $ | (451.7 | ) | $ | 24.3 | $ | (476.0 | ) | $ | (416.1 | ) | $ | 76.6 | $ | (492.7 | ) | ||||||||

Effective tax rate | 11.1 | % | 35.3 | % | (24.2 | )% | 6.4 | % | 35.2 | % | (28.8 | )% | ||||||||||||

% increase (decrease) | % increase (decrease) | |||||||||||||||||||||||

Net (loss) income per diluted share | $ | (24.98 | ) | $ | 1.33 | n.m | $ | (23.09 | ) | $ | 4.15 | n.m. | ||||||||||||

Weighted average shares | 17.7 | 18.0 | (1.7 | )% | 17.7 | 18.2 | (2.7 | )% | ||||||||||||||||

n.m. - percentage change is not meaningful

The following sets forth the significant reasons for the decreases in our income before income taxes between each of the three and nine months ended September 30, 2017 and the respective comparable periods of 2016:

Three months ended September 30, 2017 | Nine months ended September 30, 2017 | ||||||||||

(In millions) | |||||||||||

Impairment of Applebee's goodwill and tradename | $ | (531.6 | ) | $ | (531.6 | ) | |||||

Decrease in gross profit: | |||||||||||

Applebee's franchise operations | (10.8 | ) | (23.4 | ) | |||||||

All other operations | (0.8 | ) | (0.6 | ) | |||||||

Total gross profit decrease | (11.6 | ) | (24.0 | ) | |||||||

Increase in General and Administrative (“G&A”) expenses: | |||||||||||

Executive separation costs | — | (8.8 | ) | ||||||||

All other G&A | (2.0 | ) | (5.0 | ) | |||||||

Total G&A increase | (2.0 | ) | (13.8 | ) | |||||||

Gain on disposition of assets | 0.1 | 7.1 | |||||||||

Other | (0.7 | ) | (0.4 | ) | |||||||

Decrease in income before income taxes | $ | (545.8 | ) | $ | (562.7 | ) | |||||

We performed an interim quantitative test of impairment of Applebee's goodwill and tradename during the three months ended September 30, 2017. As a result of performing this test, we recognized an impairment of Applebee's goodwill of $358.2 million and an impairment of Applebee's tradename of $173.4 million. See below under the heading “Significant Known Events, Trends or Uncertainties Impacting or Expecting to Impact Comparisons of Reported or Future Results - Impairment of Applebee's Goodwill and Tradename” for additional discussion of these impairments.

Our effective tax rate (“ETR”) was significantly different than the federal statutory rate of 35% for the three and nine months ended September 30, 2017, as compared to the respective periods of the prior year. The primary reason for the difference is the impairment of Applebee's goodwill noted above is not a deductible expense for federal income tax purposes so we received no tax benefit from this expense. We did recognize a deferred tax benefit of approximately $65 million related to the impairment of Applebee's tradename.

Key Performance Indicators

In evaluating the performance of each restaurant concept, we consider the key performance indicators to be the system-wide sales percentage change, the percentage change in domestic system-wide same-restaurant sales (“comp sales”) and net franchise restaurant development. Changes in both comp sales and in the number of Applebee's and IHOP franchise restaurants will impact our system-wide retail sales that drive franchise royalty revenues. Restaurant development also impacts franchise revenues in the form of initial franchise fees and, in the case of IHOP restaurants, sales of proprietary pancake and waffle dry mix.

17

An overview of these key performance indicators for the three and nine months ended September 30, 2017 is as follows:

Three months ended September 30, 2017 | Nine months ended September 30, 2017 | ||||||||||

Applebee's | IHOP | Applebee's | IHOP | ||||||||

Sales percentage decrease | (9.7 | )% | (0.7 | )% | (8.6 | )% | (0.1 | )% | |||

% decrease in domestic system-wide same-restaurant sales | (7.7 | )% | (3.2 | )% | (7.3 | )% | (2.5 | )% | |||

Net franchise restaurant (reduction) development (1) | (23 | ) | 9 | (71 | ) | 29 | |||||

(1) Franchise and area license restaurant openings, net of closings

The Applebee's sales percentage decrease for the three and nine months ended September 30, 2017 was due to the combined effects of declines in comp sales and restaurant closures. The smaller IHOP sales percentage decrease for the three and nine months ended September 30, 2017 was due to declines in comp sales that were partially offset by net restaurant development.

Detailed information on each of these key performance indicators is presented under the captions “Restaurant Data,” “Domestic Same-Restaurant Sales” and “Restaurant Development Activity” that follow.

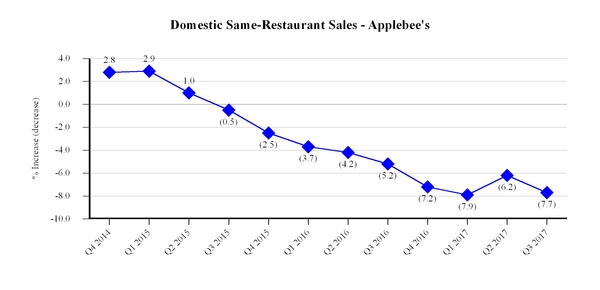

Domestic Same-Restaurant Sales

Applebee’s domestic system-wide same-restaurant sales decreased 7.7% for the three months ended September 30, 2017 from the same period in 2016. Most of the decrease resulted from a decline in customer traffic, as well as a small decrease in average customer check. For the nine months ended September 30, 2017, Applebee’s domestic system-wide same-restaurant sales decreased 7.3% from the same period in 2016. This decrease also resulted primarily from a decline in customer traffic as well as a small decrease in average customer check.

Based on data from Black Box Intelligence, a restaurant sales reporting firm (“Black Box”), the casual dining segment of the restaurant industry also experienced an overall decrease in same-restaurant sales during both the three and nine months ended September 30, 2017. The casual dining decreases in both periods were due to declines in customer traffic that were partially offset by an increase in average customer check. For both the three and nine months ended September 30, 2017, Applebee's declines in traffic and same-restaurant sales were substantially larger than those experienced by the overall casual dining segment. However, the 150 basis point decline in Applebee's same-restaurant sales from the second to the third quarter of 2017 was the same as that of the overall casual dining segment.

We believe the differential between Applebee's performance and that of the casual dining segment is due in large part to tactical initiatives previously implemented by Applebee's that did not generate desired results and to the inconsistent quality of operations across the Applebee's system. We engaged third-party consultants during the first half of 2017 to assess the continued decline in Applebee's traffic and same-restaurant sales and to provide actionable recommendations to stabilize the decline. We expect to incur approximately $10 million of costs related to these stabilization initiatives in 2017, of which approximately $8 million was incurred during the nine months ended September 30, 2017. We also contributed $4 million to

18

the Applebee's National Advertising Fund (the “Applebee's NAF”) in the third quarter of 2017 to help mitigate the decline in franchisee contributions to the Applebee's NAF that are based on a percentage of restaurant sales. We expect to contribute an additional $4 million to the Applebee's NAF in the fourth quarter of 2017. We may consider additional contributions in future periods as well.

Some of the stabilization actions we are implementing relate to brand repositioning and operational improvements that will take place over the next 12 to 18 months. Shorter-term actions, such as improving the quality of the customer experience across the Applebee's system, have shown improvement as the number of restaurants receiving the lowest of our internal ratings has declined since the end of 2016.

As discussed under the heading “Financial Results - Franchise Operations,” Applebee's has experienced a decrease in royalty revenue because of the decline in same-restaurant sales that is primarily due to a decline in customer traffic. The decline in same-restaurant sales has adversely impacted some of our franchisees' financial health, resulting in increases in our bad debt expense and in our royalties not recognized as revenue until paid in cash (“cash-basis royalties”). A franchisee that represents approximately 5% of Applebee's domestic system-wide sales is exhibiting a higher level of financial difficulty than other franchisees. We are addressing all franchisees' financial health through a collaborative effort between ourselves, a third-party advisor and franchisee representatives. We are considering various forms of assistance to franchisees, such as restaurant closures, assessing franchisee debt arrangements, temporary forbearance on payment obligations, extensions of credit and other support programs. To date, the assistance provided primarily has been the approved closures of non-viable restaurants. Any additional assistance to franchisees may entail incremental costs.

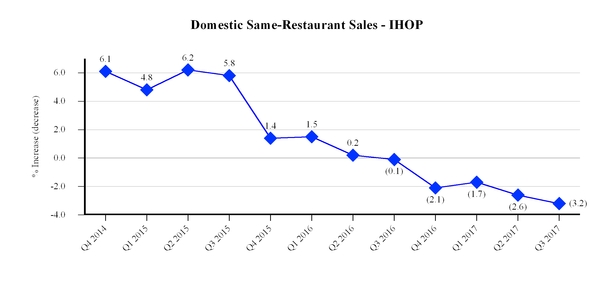

IHOP’s domestic system-wide same-restaurant sales decreased 3.2% for the three months ended September 30, 2017 from the same period in 2016. The decrease resulted from a decline in customer traffic that was partially offset by an increase in average customer check. The decline in IHOP's quarter-over-quarter customer traffic has grown progressively larger during the first three quarters of 2017. The decline in traffic peaked in the middle of the third quarter and lessened towards the end of the third quarter. For the nine months ended September 30, 2017, IHOP’s domestic system-wide same-restaurant sales decreased 2.5% from the same period in 2016. That decrease was also due to a decline in customer traffic that was partially offset by an increase in average customer check. We believe the decrease in customer traffic during the three and nine months ended September 30, 2017 was due in part to softness in our dinner daypart as the result of advertising promotions that did not drive sales and traffic as anticipated.

Based on data from Black Box, the family dining segment of the restaurant industry experienced a decrease in same-restaurant sales during the three and nine months ended September 30, 2017, compared to the same periods of the prior year, due to a decrease in customer traffic that was partially offset by an increase in average customer check. The IHOP declines in customer traffic and same-restaurant sales were larger than those experienced by the overall family dining segment for the three and nine months ended September 30, 2017. IHOP's increase in average customer check was smaller than that of the overall family dining segment for the three months ended September 30, 2017, whereas IHOP's increase in average customer check was larger than that of the overall family dining segment for the nine months ended September 30, 2017.

19

Restaurant Data

The following table sets forth the number of “Effective Restaurants” in the Applebee’s and IHOP systems and information regarding the percentage change in sales at those restaurants compared to the same periods in the prior year. Sales at restaurants that are owned by franchisees and area licensees are not attributable to the Company and, as such, the percentage change in sales at Effective Restaurants is based on non-GAAP sales data. However, we believe that presentation of this information is useful in analyzing our revenues because franchisees and area licensees pay us royalties and advertising fees that are based on a percentage of their sales, and, where applicable, rental payments under leases that partially may be based on a percentage of their sales. Management also uses this information to make decisions about plans for future development of additional restaurants as well as evaluation of current operations.

— | Three months ended September 30, | Nine months ended September 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||||

Applebee's Restaurant Data | (Unaudited) | ||||||||||||||||

Effective Restaurants(a) | |||||||||||||||||

Franchise | 1,953 | 2,028 | 1,981 | 2,029 | |||||||||||||

System-wide(b) | |||||||||||||||||

Sales percentage change(c) | (9.7 | )% | (5.1 | )% | (8.6 | )% | (4.5 | )% | |||||||||

Domestic same-restaurant sales percentage change(d) | (7.7 | )% | (5.2 | )% | (7.3 | )% | (4.4 | )% | |||||||||

Franchise(b) | |||||||||||||||||

Sales percentage change(c) | (9.7 | )% | (4.9 | )% | (8.6 | )% | (3.7 | )% | |||||||||

Domestic same-restaurant sales percentage change(d) | (7.7 | )% | (5.2 | )% | (7.3 | )% | (4.4 | )% | |||||||||

Average weekly domestic unit sales (in thousands) | $ | 40.9 | $ | 43.5 | $ | 43.5 | $ | 46.2 | |||||||||

IHOP Restaurant Data | |||||||||||||||||

Effective Restaurants(a) | |||||||||||||||||

Franchise | 1,586 | 1,521 | 1,568 | 1,512 | |||||||||||||

Area license | 162 | 167 | 165 | 165 | |||||||||||||

Company | — | 10 | 6 | 11 | |||||||||||||

Total | 1,748 | 1,698 | 1,739 | 1,688 | |||||||||||||

System-wide(b) | |||||||||||||||||

Sales percentage change(c) | (0.7 | )% | 1.3 | % | (0.1 | )% | 2.0 | % | |||||||||

Domestic same-restaurant sales percentage change(d) | (3.2 | )% | (0.1 | )% | (2.5 | )% | 0.5 | % | |||||||||

Franchise(b) | |||||||||||||||||

Sales percentage change(c) | 0.3 | % | 1.4 | % | 0.5 | % | 2.2 | % | |||||||||

Domestic same-restaurant sales percentage change(d) | (3.2 | )% | (0.1 | )% | (2.5 | )% | 0.5 | % | |||||||||

Average weekly domestic unit sales (in thousands) | $ | 35.7 | $ | 37.1 | $ | 36.3 | $ | 37.5 | |||||||||

Area License(b) | |||||||||||||||||

Sales percentage change(c) | (5.7 | )% | 2.4 | % | (3.6 | )% | 1.1 | % | |||||||||

(a) “Effective Restaurants” are the weighted average number of restaurants open in each fiscal period, adjusted to account for restaurants open for only a portion of the period. Information is presented for all Effective Restaurants in the Applebee’s and IHOP systems, which consist of restaurants owned by franchisees and area licensees as well as those owned by the Company.

(b) “System-wide sales” are retail sales at Applebee’s restaurants operated by franchisees and IHOP restaurants operated by franchisees and area licensees, as reported to the Company, in addition to retail sales at company-operated restaurants. Sales at restaurants that are owned by franchisees and area licensees are not attributable to the Company. An increase in franchisees' reported sales will result in a corresponding increase in our royalty revenue, while a decrease in franchisees' reported sales will result in a corresponding decrease in our royalty revenue. Unaudited reported sales for Applebee's domestic franchise restaurants, IHOP franchise restaurants and IHOP area license restaurants were as follows:

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

Reported sales (In millions) | (Unaudited) | ||||||||||||||

Applebee's domestic franchise restaurant sales | $ | 956.5 | $ | 1,058.9 | $ | 3,092.3 | $ | 3,382.1 | |||||||

IHOP franchise restaurant sales | 736.9 | 734.3 | 2,220.3 | 2,208.6 | |||||||||||

IHOP area license restaurant sales | 67.0 | 71.0 | 208.7 | 216.5 | |||||||||||

Total | $ | 1,760.4 | $ | 1,864.2 | $ | 5,521.3 | $ | 5,807.2 | |||||||

20

(c) “Sales percentage change” reflects, for each category of restaurants, the percentage change in sales in any given fiscal period compared to the prior fiscal period for all restaurants in that category.

(d) “Domestic same-restaurant sales percentage change” reflects the percentage change in sales in any given fiscal period, compared to the same weeks in the prior fiscal period, for domestic restaurants that have been operated throughout both fiscal periods that are being compared and have been open for at least 18 months. Because of new restaurant openings and restaurant closures, the domestic restaurants open throughout both fiscal periods being compared may be different from period to period. Domestic same-restaurant sales percentage change does not include data on IHOP area license restaurants.

Restaurant Development Activity | Three months ended September 30, | Nine months ended September 30, | |||||||||

2017 | 2016 | 2017 | 2016 | ||||||||

Applebee's | (Unaudited) | ||||||||||

Beginning of period | 1,968 | 2,027 | 2,016 | 2,033 | |||||||

Franchise restaurants opened: | |||||||||||

Domestic | 2 | 6 | 7 | 13 | |||||||

International | 2 | 3 | 6 | 7 | |||||||

Total franchise restaurants opened | 4 | 9 | 13 | 20 | |||||||

Franchise restaurants closed: | |||||||||||

Domestic | (22 | ) | (8 | ) | (74 | ) | (20 | ) | |||

International | (5 | ) | (1 | ) | (10 | ) | (6 | ) | |||