Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SYNOVUS FINANCIAL CORP | d483599d8k.htm |

Exhibit 99.1

Synovus Financial Corp.

BancAnalysts Association of Boston

Kessel Stelling, Chairman and CEO

November 2, 2017

1

Forward Looking Statements

This slide presentation and certain of our filings with the Securities and Exchange Commission contain statements that constitute “forward-looking

statements” within the meaning of, and subject to the protections of, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements other than statements of

historical fact are forward- looking statements. You can identify these forward-looking statements through Synovus’ use of words such as “believes,” “anticipates,” “expects,” “may,” “will,”

“assumes,” “should,” “predicts,” “could,” “should,” “would,” “intends,” “targets,” “estimates,” “projects,” “plans,” “potential”

and other similar words and expressions of the future or otherwise regarding the outlook for Synovus’ future business and financial performance and/or the performance of the banking industry and economy in general. These forward-looking

statements include, among others, statements on (1) future loan growth; (2) future deposit growth; (3) future net interest income and net interest margin; (4) future adjusted non-interest

income; (5) future non-interest expense levels and efficiency ratios; (6) future credit trends and key metrics; (7) future effective tax rates; (8) our strategy and initiatives for future

growth, capital management, strategic transactions, our brand initiative and financial planning; (9) our expectations related to the anticipated benefits of certain transactions and initiatives, including those related to the Cabela’s

transaction and debt redemption; and (10) our assumptions underlying these expectations. Prospective investors are cautioned that any such forward-looking statements are not guarantees of future performance and involve known and unknown risks

and uncertainties which may cause the actual results, performance or achievements of Synovus to be materially different from the future results, performance or achievements expressed or implied by such forward-looking statements. Forward-looking

statements are based on the information known to, and current beliefs and expectations of, Synovus’ management and are subject to significant risks and uncertainties. Actual results may differ materially from those contemplated by such

forward-looking statements. A number of factors could cause actual results to differ materially from those contemplated by the forward-looking statements in this presentation. Many of these factors are beyond Synovus’ ability to control or

predict. These forward-looking statements are based upon information presently known to Synovus’ management and are inherently subjective, uncertain and subject to change due to any number of risks and uncertainties, including, without

limitation, the risks and other factors set forth in Synovus’ filings with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended December 31, 2016 under

the captions “Cautionary Notice Regarding Forward-Looking Statements” and “Risk Factors” and in Synovus’ quarterly reports on Form 10-Q and current reports on Form 8-K. We believe these forward-looking statements are reasonable; however, undue reliance should not be placed on any forward-looking statements, which are based on current expectations and speak only as of the date

that they are made. We do not assume any obligation to update any forward- looking statements as a result of new information, future developments or otherwise, except as otherwise may be required by law. Use of

Non-GAAP Financial Measures This slide presentation contains certain non-GAAP financial measures determined by methods other than in accordance with generally accepted

accounting principles. Such non-GAAP financial measures include the following: adjusted diluted earnings per share; adjusted return on average assets; adjusted return on average common equity; adjusted return

on average tangible common equity; loan growth excluding transfers to held-for-sale; net charge-off ratio excluding charge-offs

on loans transferred to held-for-sale; average deposit growth excluding WFB deposits; average core transaction deposits; cost of interest bearing core deposits; total

adjusted revenues; adjusted non-interest income; adjusted non-interest expense; adjusted efficiency ratio; tangible common equity ratio; and common equity Tier 1 (CET1)

ratio (fully phased-in). The most comparable GAAP measures to these measures are diluted earnings per share; return on average assets; return on average common equity; loan growth; net charge-off ratio; total average deposits; effective cost of funds; total non-interest income; total non-interest expense; efficiency

ratio; total shareholders’ equity to total assets ratio; and CET1 ratio, respectively. Management uses these non- GAAP financial measures to assess the performance of Synovus’ business and the

strength of its capital position. Management believes that these non-GAAP financial measures provide meaningful additional information about Synovus to assist management, investors, and bank regulators in

evaluating Synovus’ operating results, financial strength, the performance of its business and the strength of its capital position. However, these non-GAAP financial measures have inherent limitations as

analytical tools and should not be considered in isolation or as a substitute for analyses of operating results or capital position as reported under GAAP. The non-GAAP financial measures should be considered

as additional views of the way our financial measures are affected by significant items and other factors, and since they are not required to be uniformly applied, they may not be comparable to other similarly titled measures at other companies.

Adjusted diluted earnings per share, adjusted return on average assets, and adjusted return on average common equity are measures used by management to evaluate operating results exclusive of items that are not indicative of ongoing operations and

impact period-to-period comparisons. Adjusted return on average tangible common equity is a measure used by management to compare Synovus’ performance with other

financial institutions because it calculates the return available to common shareholders without the impact of intangible assets and their related amortization, thereby allowing management to evaluate the performance of the business consistently.

Loan growth excluding transfers to held-for-sale is a measure used by management to evaluate organic loan growth exclusive of loans transferred to held-for-sale and the net charge-off ratio excluding charge-offs on loans transferred to held-for- sale is a measure used by management to evaluate charge-offs exclusive of charge-offs on loans transferred to

held-for-sale. Average core transaction deposits is a measure used by management to evaluate organic growth of deposits and the quality of deposits as a funding source.

The cost of interest bearing core deposits is a measure used to evaluate the cost of deposits as a funding source exclusive of brokered deposits and non-interest bearing deposits. Total adjusted revenues and

adjusted non-interest income are measures used by management to evaluate total revenue and non-interest income exclusive of net investment securities gains/losses and

changes in fair value of private equity investments, net, and the Cabela’s transaction fee. Adjusted non-interest expense and the adjusted efficiency ratio are measures utilized by management to measure

the success of expense management initiatives focused on reducing recurring controllable operating costs. The tangible common equity ratio and common equity Tier 1 (CET1) ratio (fully phased-in) are used by

management and bank regulators to assess the strength of our capital position. The computations of the non- GAAP financial measures used in this slide presentation are set forth in the Appendix to this slide

presentation. 2

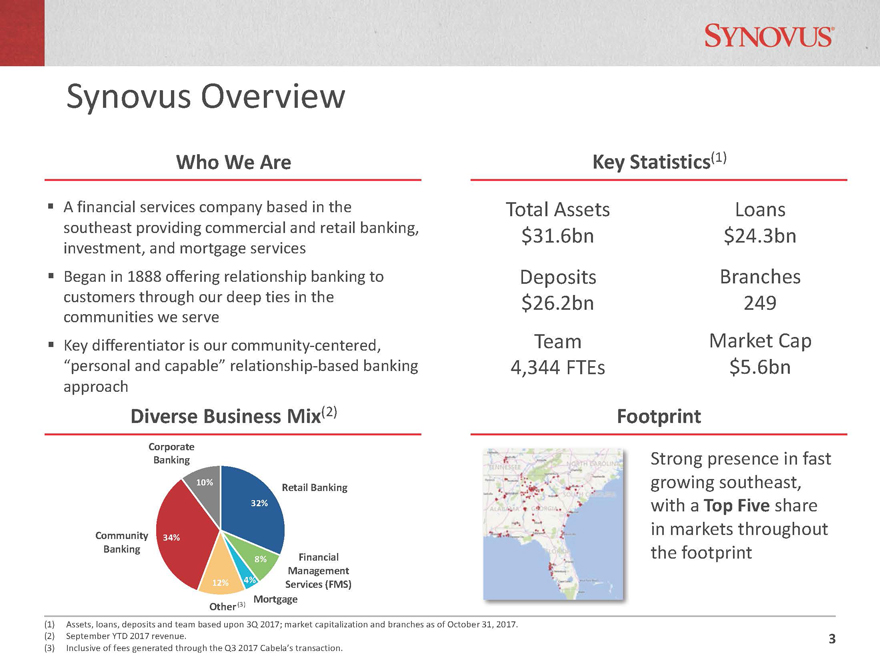

Retail Banking Financial Management Services (FMS)

Mortgage Other Community Banking Corporate Banking

32% 8% 12% 4% 34% 10%

Synovus Overview (1) Assets, loans, deposits and team based upon 3Q 2017; market capitalization and branches as of October 31, 2017. (2) September YTD 2017 revenue. (3)

Inclusive of fees generated through the Q3 2017 Cabela’s transaction.

A financial services company based in the southeast providing commercial and retail

banking, investment, and mortgage services

Began in 1888 offering relationship banking to customers through our deep ties in the communities we serve § Key

differentiator is our community-centered, “personal and capable” relationship-based banking approach Who We Are Key Statistics(1)

Total Assets $31.6bn

Loans $24.3bn Deposits $26.2bn Team 4,344 FTEs Branches 249 Market Cap $5.6bn

Diverse Business Mix(2) Footprint Strong presence in fast growing southeast, with a

Top Five share in markets throughout the footprint 3

Recent Recognition

2017

American Banker/ Reputation Institute named Synovus “Most Reputable

Bank.” Synovus ranked second in 2016.

Synovus won 28 Greenwich Excellence Awards for Small Business Banking and Middle Market Banking in 2016.

Only one bank won more awards than Synovus. Synovus named “Best Regional Bank, Southeast” in the November 2016 issue of MONEY Magazine. Financial Services Roundtable

named Synovus a 2017 Corporate Social Responsibility Leadership Award winner. Family Asset Management (FAM) ranked in the top 50 of Bloomberg Markets Magazine’s list four consecutive years.

One of Consumer Reports’ “Best Banks for You” in the January 2016 issue. Georgia Trend named Synovus one of 17 “Best Places to Work In Georgia” in the

magazine’s 2016 ranking of the state’s top employers. 4

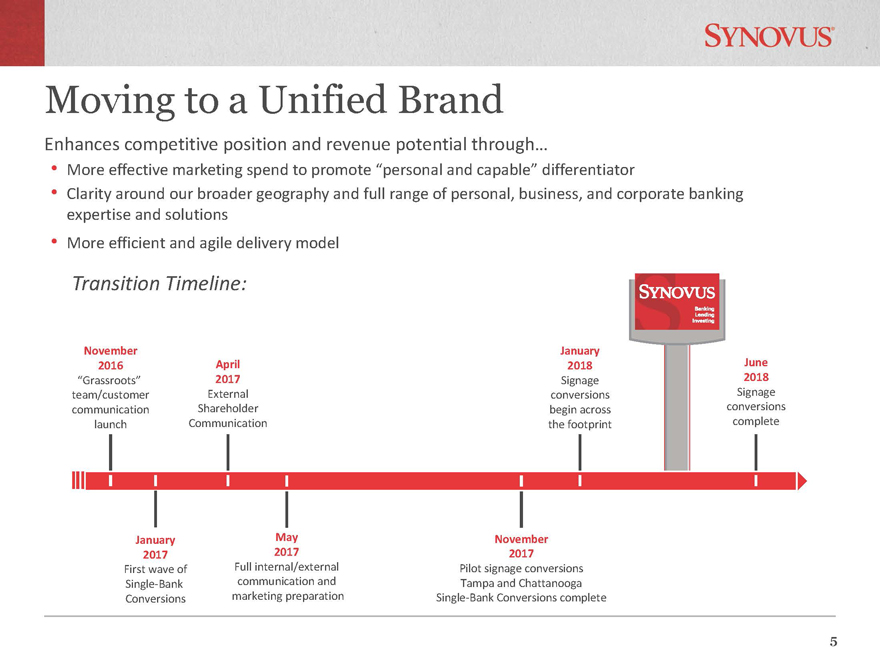

Transition Timeline:

November 2016

“Grassroots” team/customer Communication launch

April 2017 ExternalShareholder Communication May 2017

Full internal/external

communication and marketing preparation November 2017

Pilot signage conversions Tampa and Chattanooga Single-Bank Conversions complete January 2018 Signage

conversions begin across the footprint June 2018 Signage conversions complete Enhances competitive position and revenue potential through…

• More

effective marketing spend to promote “personal and capable” differentiator

• Clarity around our broader geography and full range of personal,

business, and corporate banking expertise and solutions

• More efficient and agile delivery model Moving to a Unified Brand January 2017

First wave of Single-Bank Conversions 5

0.88%

1.00%

1.27%

0.90%

1.01% 1.05%

3Q16 2Q17 3Q17

As Reported As Adjusted $0.51 $0.60 $0.78 $0.52 $0.61 $0.65 3Q16 2Q17 3Q17 As Reported As Adjusted

(1) Non-GAAP financial measure adjusted for one time charges and gains in Q3 2017; see appendix for applicable reconciliation.

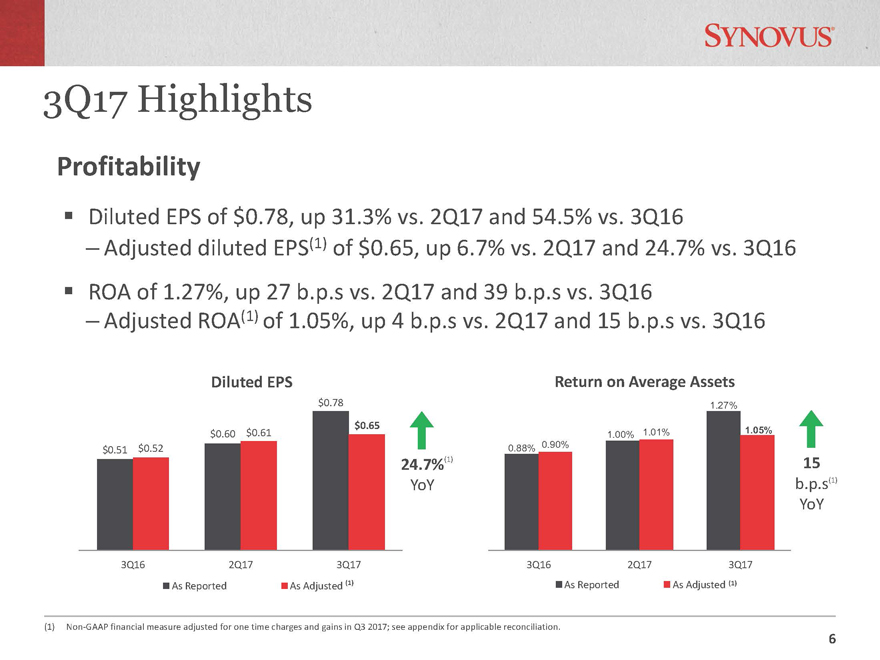

Return on Average Assets § Diluted EPS of $0.78, up 31.3% vs. 2Q17 and 54.5% vs. 3Q16

– Adjusted diluted EPS(1) of $0.65, up 6.7% vs. 2Q17 and 24.7% vs. 3Q16 § ROA of 1.27%, up 27 b.p.s vs. 2Q17 and 39 b.p.s vs. 3Q16 – Adjusted ROA(1)

of 1.05%, up 4 b.p.s vs. 2Q17 and 15 b.p.s vs. 3Q16 (1) (1)

Profitability 3Q17 Highlights Diluted EPS 24.7% YoY (1) 15 b.p.s YoY (1) 6

$24.03

$24.99

$25.29

3Q16 2Q17 3Q17

$23.14

$24.35 $24.50

3Q16 2Q17 3Q17

3Q17 Highlights

7

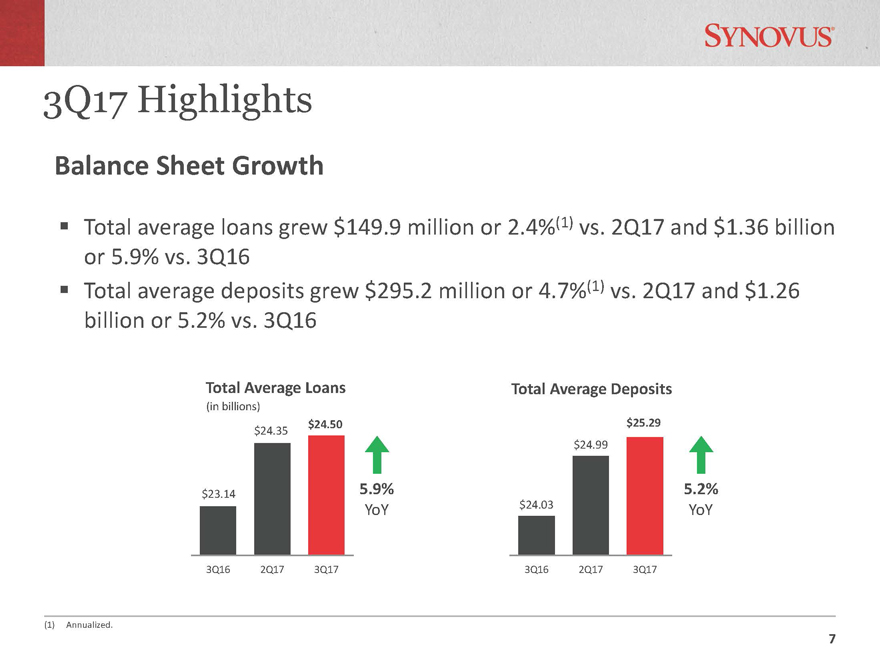

(1) Annualized.

Total average loans grew $149.9 million or 2.4%(1) vs. 2Q17 and $1.36 billion

or

5.9% vs. 3Q16

Total average deposits grew $295.2 million or 4.7%(1) vs. 2Q17 and $1.26

billion or 5.2% vs. 3Q16

Total Average Loans Total Average Deposits

(in billions)

Balance Sheet Growth

5.9%

YoY

5.2%

YoY

7

8.89% 10.34% 13.24% 9.08% 10.49% 10.92% 3Q16 2Q17 3Q17 As Reported As Adjusted 3Q17 Highlights 8

(1) Non-GAAP financial measure adjusted for one time charges and gains in Q3 2017; see appendix for applicable reconciliation.

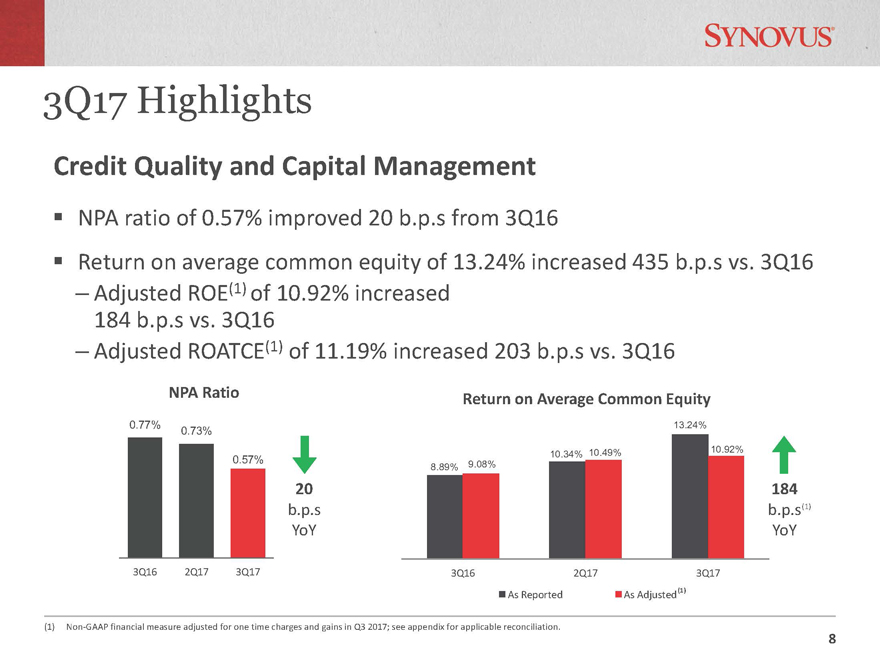

NPA ratio of 0.57% improved 20 b.p.s from 3Q16 Return on average common equity of 13.24% increased 435 b.p.s vs. 3Q16

– Adjusted ROE(1) of 10.92% increased 184 b.p.s vs. 3Q16 – Adjusted ROATCE(1) of 11.19% increased 203 b.p.s vs. 3Q16 NPA Ratio Return on Average Common Equity 0.77% 0.73%

0.57% 3Q16 2Q17 3Q17

(1) Credit Quality and Capital Management 20 b.p.s YoY 184 b.p.s YoY (1) 8

Transaction with World’s Foremost Bank and Capital One

On September 25, 2017, Synovus Bank completed the acquisition of certain assets and

assumption of certain liabilities of World’s Foremost Bank (WFB), a wholly-owned subsidiary

of Cabela’s Incorporated.

Simultaneous with the above transaction, Synovus Bank sold the

credit card assets and

related liabilities to Capital One Bank (Capital One), while retaining WFB’s $1.1 billion

brokered time deposit portfolio.

– The acquired deposits have a weighted average

remaining maturity of approximately 2.53

years and a weighted average rate of 1.83%, which represented a discount to market rates

of approximately 14 b.p.s as of September 25, 2017.

3Q17

non-interest income includes a $75.0 million fee received from Cabela’s and Capital

One as part of the

transaction.

During the third quarter, concurrent with the transaction, Synovus initiated various balance

sheet restructuring actions which will continue into the fourth quarter. These actions are

expected to result in over 5% EPS accretion in 2018 through increased net interest income,

lower provision expense, and lower non-interest expense growth.

9

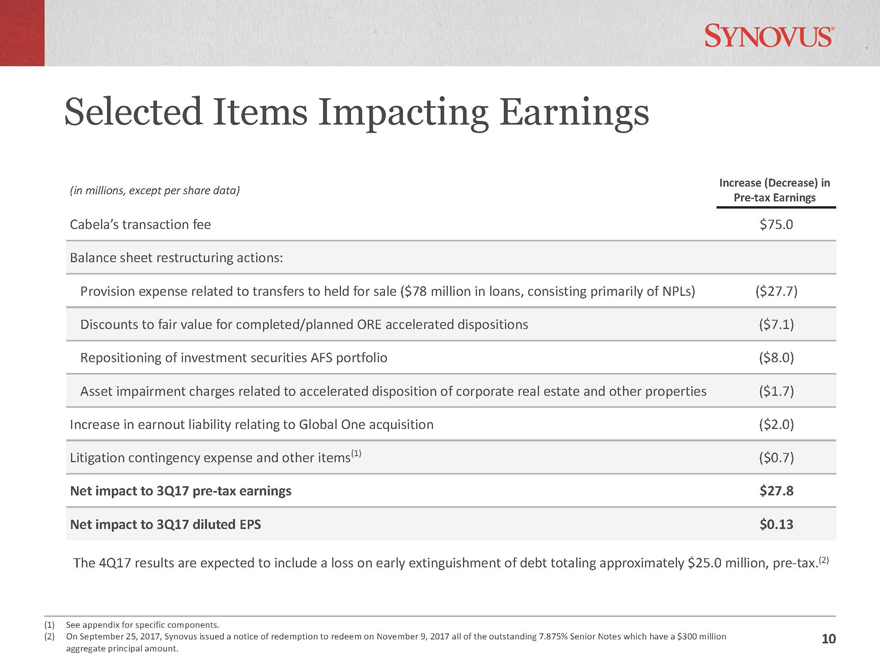

Selected Items Impacting Earnings

(1) See appendix for specific components.

(2) On September 25, 2017, Synovus issued a

notice of redemption to redeem on November 9, 2017 all of the outstanding 7.875% Senior Notes which have a $300 million aggregate principal amount.

(in

millions, except per share data) Increase (Decrease) in

Pre-tax Earnings

Cabela’s transaction fee $75.0

Balance sheet restructuring actions:

Provision expense related to transfers to held for sale ($78 million in loans, consisting primarily of NPLs) ($27.7)

Discounts to fair value for completed/planned ORE accelerated dispositions ($7.1)

Repositioning of investment securities AFS portfolio ($8.0)

Asset impairment

charges related to accelerated disposition of corporate real estate and other properties ($1.7)

Increase in earnout liability relating to Global One acquisition

($2.0)

Litigation contingency expense and other items(1) ($0.7)

Net impact to

3Q17 pre-tax earnings $27.8

Net impact to 3Q17 diluted EPS $0.13

The 4Q17 results are expected to include a loss on early extinguishment of debt totaling approximately $25.0 million, pre-tax.(2)

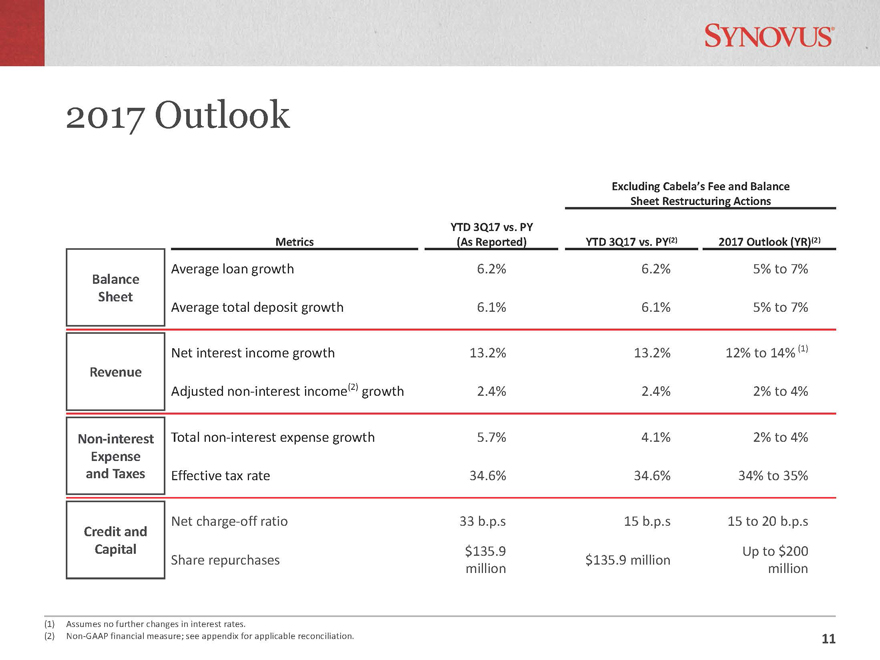

10

Excluding Cabela’s Fee and Balance

Sheet Restructuring Actions

Metrics

YTD 3Q17 vs. PY

(As Reported) YTD 3Q17 vs. PY(2) 2017 Outlook (YR)(2)

Balance

Sheet

Average loan growth 6.2% 6.2% 5% to 7%

Average total deposit growth 6.1% 6.1% 5% to 7%

Revenue

Net interest income growth 13.2% 13.2% 12% to 14% (1)

Adjusted non-interest income(2) growth 2.4% 2.4% 2% to 4%

Non-interest

Expense

and Taxes

Total non-interest expense growth 5.7% 4.1%

2% to 4%

Effective tax rate 34.6% 34.6% 34% to 35%

Credit and

Capital

Net charge-off ratio 33 b.p.s 15 b.p.s 15 to

20 b.p.s

Share repurchases $135.9

million $135.9 million Up to $200

million

2017 Outlook

(1) Assumes no further changes in interest rates.

(2)

Non-GAAP financial measure; see appendix for applicable reconciliation. 11

Financial and Strategic Objectives

69.8% 68.9%

65.6% 64.7%

58.6%

2013 2014 2015 2016 Q3

2017

$0.88

$1.33

$1.62

$1.89

$2.42

2013 2014 2015 2016

Broad Based Financial Improvement

(1) September YTD 2017 annualized.

(2) Non-GAAP

financial measure adjusted for one time charges and gains in Q3 2017; see appendix for applicable reconciliation.

Growth Profitability Efficiency

DILUTED EARNINGS

PER SHARE

RETURN ON

AVERAGE ASSETS

EFFICIENCY

RATIO

29%

CAGR

44

b.p.s

1116

b.p.s

As reported As Adjusted(2)

September

2017 YTD

(1)

0.61%

0.74%

0.80% 0.84%

1.05%

2013 2014 2015 2016 Q3

2017

13

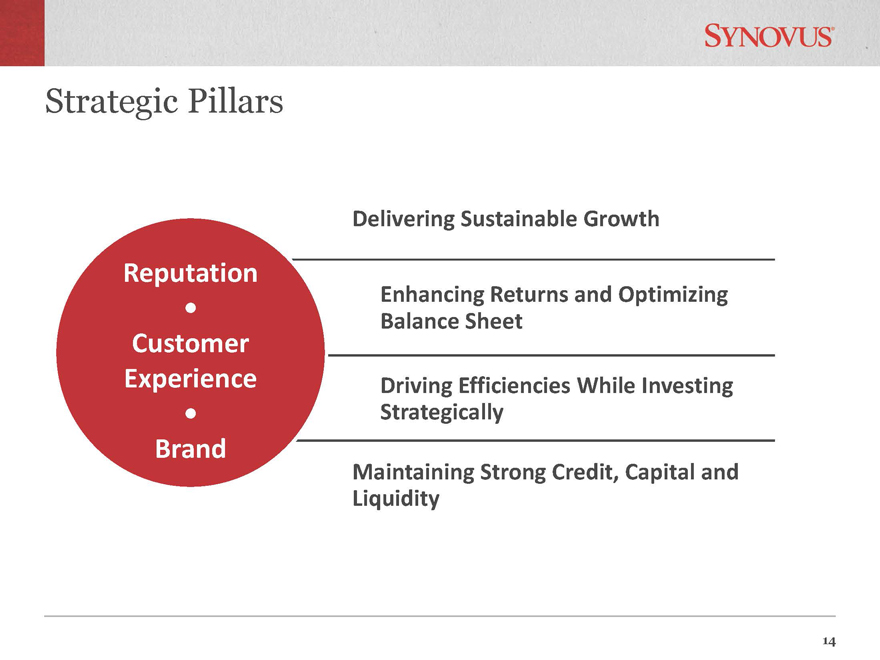

Strategic Pillars

Delivering Sustainable Growth

Enhancing Returns and Optimizing

Balance Sheet

Driving Efficiencies While Investing

Strategically

Maintaining Strong Credit, Capital and

Liquidity

Reputation

Customer

Experience

Brand

14

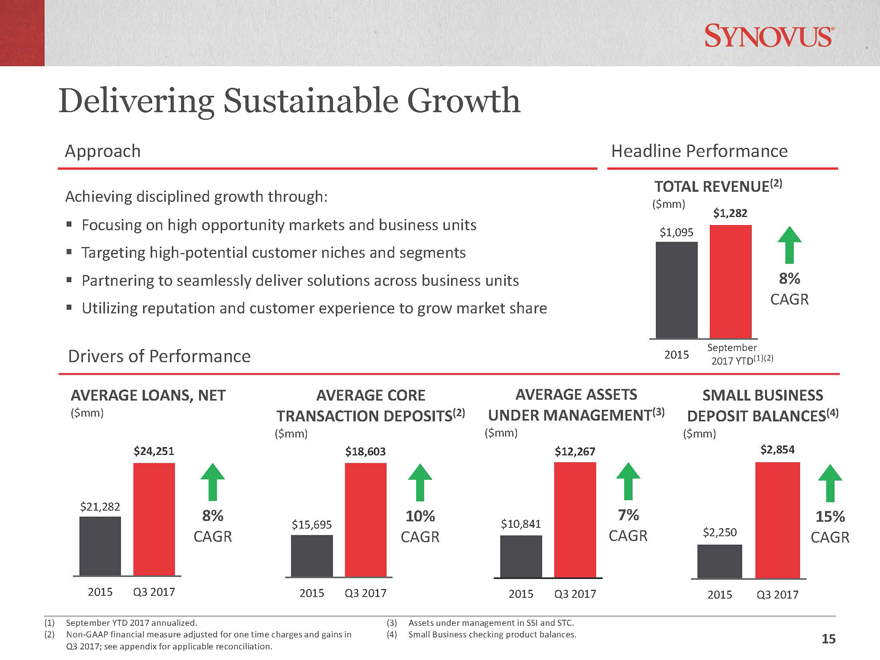

$1,095

$1,282

2015 September

2017 YTD Delivering Sustainable Growth

(1) September YTD 2017 annualized.

(2) Non-GAAP

financial measure adjusted for one time charges and gains in

Q3 2017; see appendix for applicable reconciliation.

AVERAGE LOANS, NET

($mm) AVERAGE CORE TRANSACTION DEPOSITS(2) ($mm)

(3) Assets under management in SSI and STC.

(4) Small Business checking product balances.

Approach Headline Performance Drivers of Performance

Achieving disciplined

growth through: Focusing on high opportunity markets and business units

Targeting high-potential customer niches and segments

Partnering to seamlessly deliver solutions across business units

Utilizing reputation and

customer experience to grow market share

8% CAGR AVERAGE ASSETS UNDER MANAGEMENT(3) ($mm) TOTAL REVENUE(2)

($mm) SMALL BUSINESS DEPOSIT BALANCES(4) ($mm) 8%

CAGR 10% CAGR 7% CAGR 15% CAGR

(1)(2) $21,282 $24,251 2015 Q3 2017 $15,695 $18,603 2015 Q3 2017 $10,841 $12,267

2015 Q3 2017

$2,250 $2,854 2015 Q3 2017 15

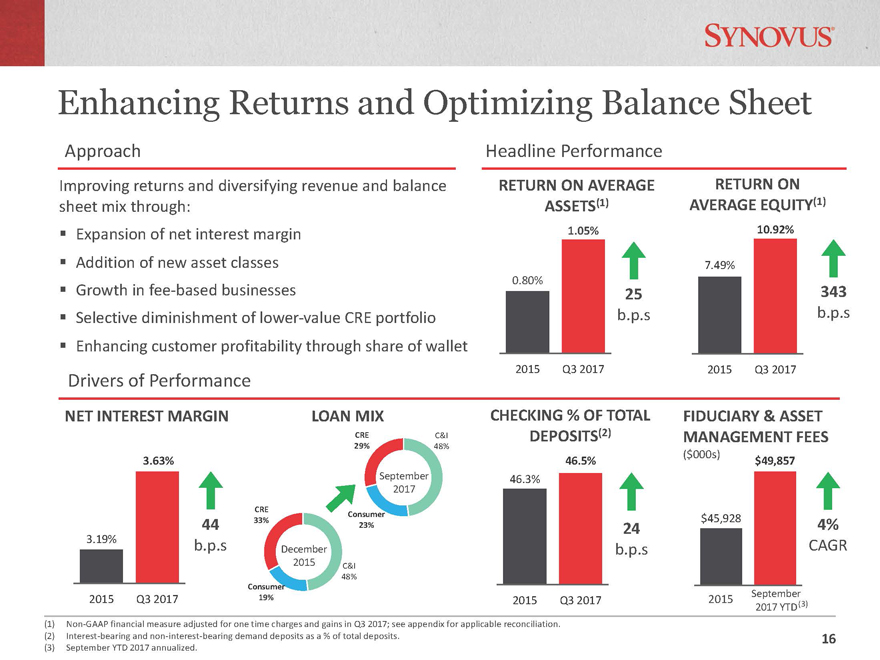

Enhancing Returns and Optimizing Balance Sheet 16

(1) Non-GAAP financial measure adjusted for one time charges and gains in Q3 2017; see appendix for applicable reconciliation.

(2) Interest-bearing and non-interest-bearing demand deposits as a % of total deposits.

(3) September YTD 2017 annualized.

NET INTEREST MARGIN LOAN MIX

Improving returns and diversifying revenue and balance sheet mix through:

§ Expansion of

net interest margin

§ Addition of new asset classes

§ Growth in fee-based businesses

§ Selective diminishment of lower-value CRE portfolio

§ Enhancing customer profitability through share of wallet

25 b.p.s 343 b.p.s

CHECKING % OF TOTAL DEPOSITS(2) FIDUCIARY & ASSET MANAGEMENT FEES ($000s)

RETURN ON

AVERAGE ASSETS(1)

24 b.p.s RETURN ON AVERAGE EQUITY(1) 44 b.p.s

4% CAGR

C&I 48% Consumer 19% CRE 33% C&I

48% Consumer 23% CRE 29% 0.80% 1.05% 2015 Q3 2017

7.49% 10.92% 2015 Q3 2017 3.19% 3.63% 2015 Q3 2017

46.3% 46.5% 2015 Q3 2017 $45,928 $49,857

Approach Headline Performance

Drivers of Performance December 2015 September 2017 YTD 2015 (3) September

2017 16

$22,803 $14,502 2015 September 2017 YTD 65.6% 58.6% 2015 Q3 2017

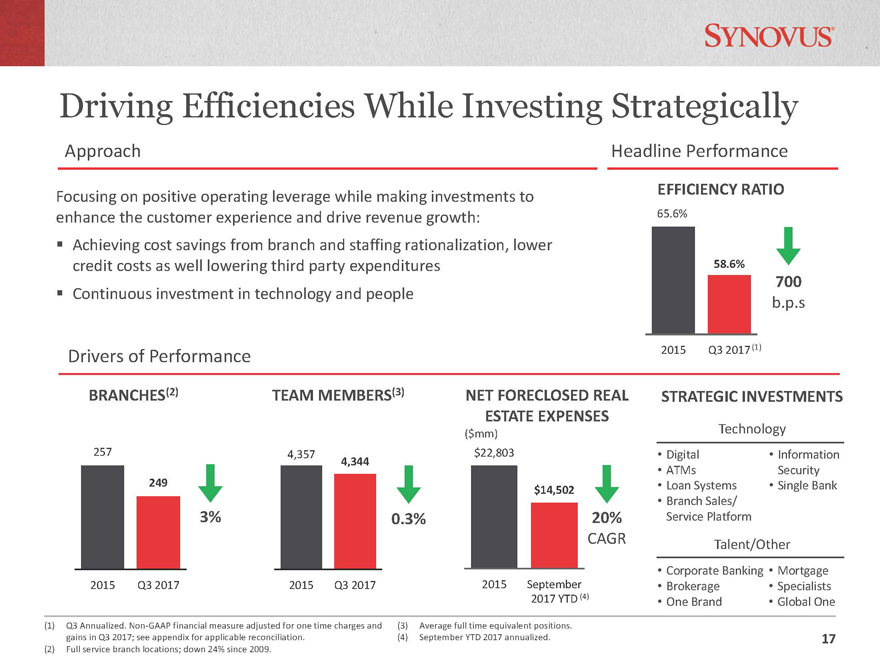

Driving Efficiencies While Investing Strategically

(1) Q3 Annualized. Non-GAAP financial measure adjusted for one time charges and gains in Q3 2017; see appendix for applicable reconciliation.

(2)

Full service branch locations; down 24% since 2009. BRANCHES(2) TEAM MEMBERS(3)

(3) Average full time equivalent positions.

(4) September YTD 2017 annualized. Focusing on positive operating leverage while making investments to

enhance the customer experience and drive revenue growth: Achieving cost savings from branch and staffing rationalization, lower credit costs as well lowering third party

expenditures Continuous investment in technology and people

700 b.p.s NET FORECLOSED REAL ESTATE EXPENSES ($mm) EFFICIENCY RATIO

3% 0.3% 20% CAGR

(1) STRATEGIC INVESTMENTS Technology Talent/Other • Digital • ATMs

• Loan Systems • Branch Sales/ Service Platform

• Information Security • Single Bank • Corporate Banking • Brokerage • One Brand

• Mortgage • Specialists (4) • Global One

257 249 2015 Q3 2017 4,357 4,344 2015 Q3 2017 Approach Headline Performance Drivers of Performance

17

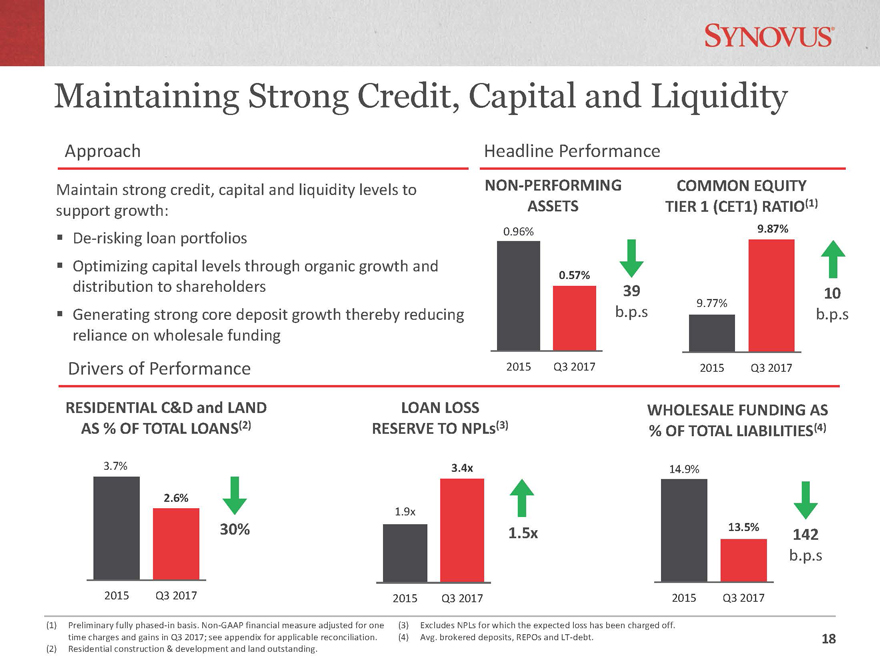

Maintaining Strong Credit, Capital and Liquidity

(1) Preliminary fully phased-in basis. Non-GAAP financial measure adjusted for one time charges and

gains in Q3 2017; see appendix for applicable reconciliation.

(2) Residential construction & development and land outstanding. Maintain strong credit,

capital and liquidity levels to support growth: De-risking loan portfolios Optimizing capital levels through organic growth and distribution to shareholders § Generating strong core deposit growth thereby

reducing reliance on wholesale funding 39

b.p.s

NON-PERFORMING ASSETS RESIDENTIAL C&D and LAND AS % OF TOTAL LOANS(2)

LOAN LOSS RESERVE TO NPLs(3) COMMON EQUITY TIER 1

(CET1) RATIO(1) WHOLESALE FUNDING AS % OF TOTAL LIABILITIES(4) 30% 1.5x 10 b.p.s 142 b.p.s (3) Excludes NPLs for which the expected loss has been charged off.

(4)

Avg. brokered deposits, REPOs and LT-debt. 0.96% 0.57% 2015 Q3 2017 9.77% 9.87% 2015 Q3 2017 3.7% 2.6%

2015 Q3 2017 1.9x

3.4x 2015 Q3 2017 14.9% 13.5% 2015 Q3 2017 Approach Headline Performance Drivers of Performance

18

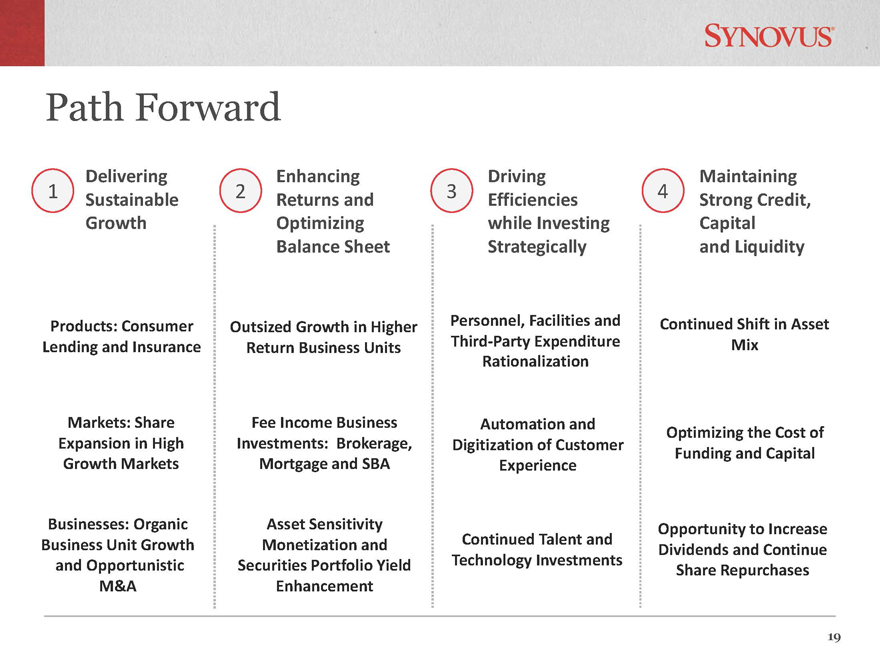

Path Forward 1 2 3 4 Products: Consumer Lending and Insurance

Markets: Share Expansion in High Growth Markets Businesses: Organic Business Unit Growth and Opportunistic M&A

Outsized Growth in Higher Return Business Units Fee Income Business Investments: Brokerage, Mortgage and SBA

Asset Sensitivity Monetization and Securities Portfolio Yield Enhancement Personnel, Facilities and Third-Party Expenditure Rationalization Automation and Digitization of Customer

Experience Continued Talent and Technology Investments

Continued Shift in Asset Mix Optimizing the Cost of Funding and Capital Opportunity to Increase Dividends

and Continue Share Repurchases

19 Enhancing Returns and Optimizing Balance Sheet Delivering Sustainable Growth Driving

Efficiencies while Investing Strategically Maintaining Strong Credit, Capital and Liquidity 19

Appendx

20

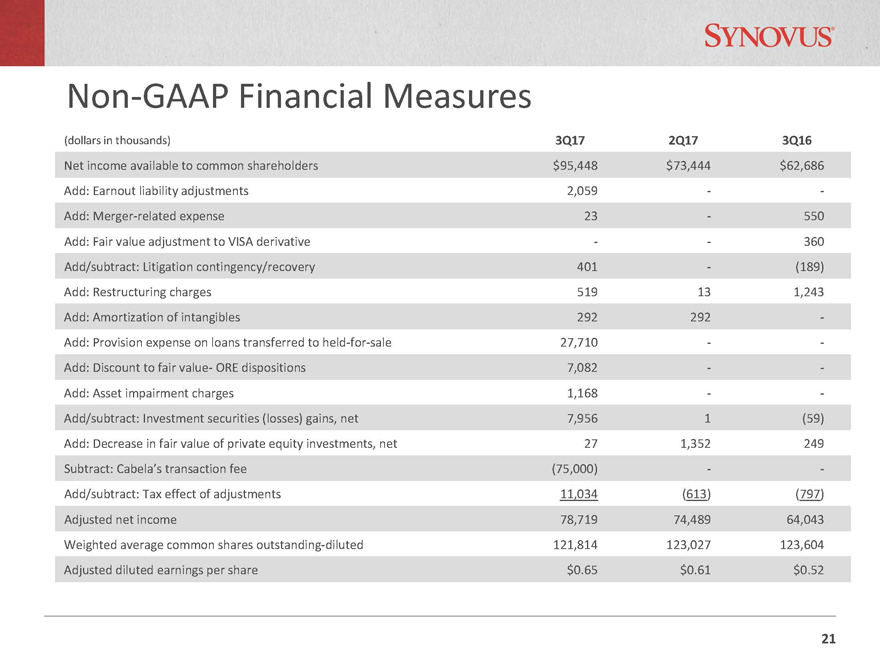

Non-GAAP Financial Measures

(dollars in thousands) 3Q17 2Q17 3Q16

Net income available to common shareholders $95,448

$73,444 $62,686

Add: Earnout liability adjustments 2,059 —

Add:

Merger-related expense 23—550

Add: Fair value adjustment to VISA derivative — 360

Add/subtract: Litigation contingency/recovery 401—(189)

Add: Restructuring charges 519 13

1,243

Add: Amortization of intangibles 292 292 -

Add: Provision expense on

loans transferred to held-for-sale 27,710 —

Add: Discount to fair value- ORE

dispositions 7,082 —

Add: Asset impairment charges 1,168 —

Add/subtract: Investment securities (losses) gains, net 7,956 1 (59)

Add:

Decrease in fair value of private equity investments, net 27 1,352 249

Subtract: Cabela’s transaction fee (75,000) —

Add/subtract: Tax effect of adjustments 11,034 (613) (797)

Adjusted net income 78,719 74,489

64,043

Weighted average common shares outstanding-diluted 121,814 123,027 123,604

Adjusted diluted earnings per share $0.65 $0.61 $0.52

21

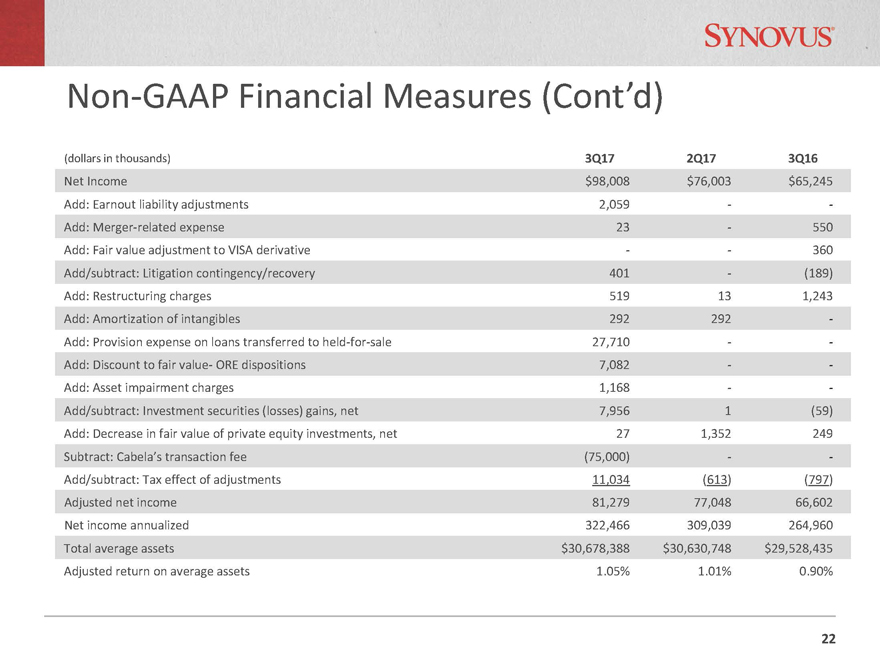

(dollars in thousands) 3Q17 2Q17 3Q16

Net Income $98,008 $76,003 $65,245

Add: Earnout liability adjustments 2,059 —

Add: Merger-related expense 23—550

Add: Fair value adjustment to VISA derivative —

360

Add/subtract: Litigation contingency/recovery 401—(189)

Add:

Restructuring charges 519 13 1,243

Add: Amortization of intangibles 292 292 -

Add: Provision expense on loans transferred to held-for-sale 27,710 —

Add: Discount to fair value- ORE dispositions 7,082 —

Add: Asset

impairment charges 1,168 —

Add/subtract: Investment securities (losses) gains, net 7,956 1 (59)

Add: Decrease in fair value of private equity investments, net 27 1,352 249

Subtract:

Cabela’s transaction fee (75,000) —

Add/subtract: Tax effect of adjustments 11,034 (613) (797)

Adjusted net income 81,279 77,048 66,602

Net income annualized 322,466 309,039 264,960

Total average assets $30,678,388 $30,630,748 $29,528,435

Adjusted return on

average assets 1.05% 1.01% 0.90%

Non-GAAP Financial Measures (Cont’d)

22

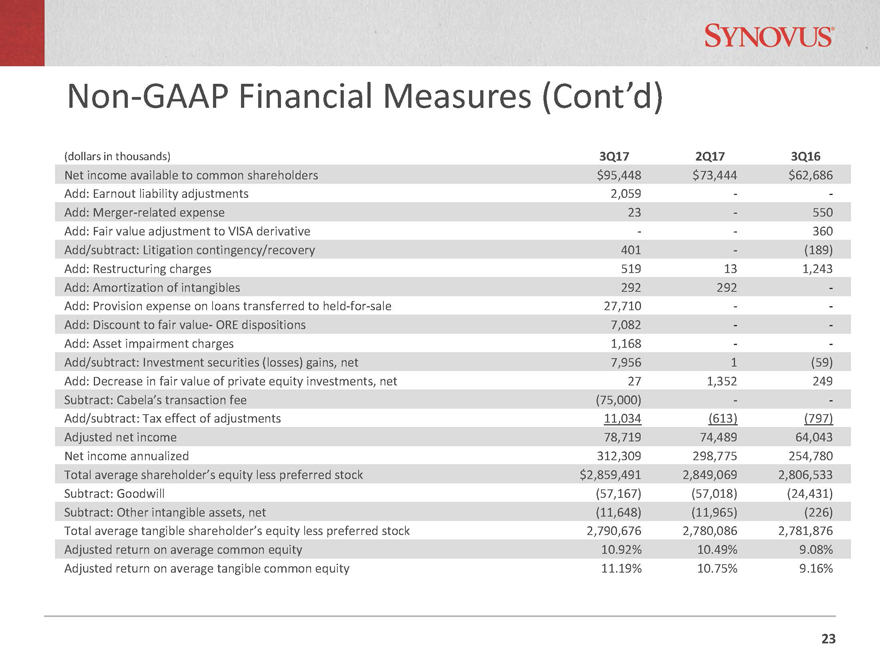

(dollars in thousands) 3Q17 2Q17 3Q16

Net income available to common shareholders $95,448 $73,444 $62,686

Add: Earnout liability

adjustments 2,059 —

Add: Merger-related expense 23—550

Add: Fair

value adjustment to VISA derivative — 360

Add/subtract: Litigation contingency/recovery 401—(189)

Add: Restructuring charges 519 13 1,243

Add: Amortization of intangibles 292 292 -

Add: Provision expense on loans transferred to held-for-sale 27,710 —

Add: Discount to fair value- ORE dispositions 7,082 —

Add: Asset impairment charges 1,168

—

Add/subtract: Investment securities (losses) gains, net 7,956 1 (59)

Add: Decrease in fair value of private equity investments, net 27 1,352 249

Subtract: Cabela’s transaction fee (75,000) —

Add/subtract: Tax

effect of adjustments 11,034 (613) (797)

Adjusted net income 78,719 74,489 64,043

Net income annualized 312,309 298,775 254,780

Total average shareholder’s equity less

preferred stock $2,859,491 2,849,069 2,806,533

Subtract: Goodwill (57,167) (57,018) (24,431)

Subtract: Other intangible assets, net (11,648) (11,965) (226)

Total average tangible

shareholder’s equity less preferred stock 2,790,676 2,780,086 2,781,876

Adjusted return on average common equity 10.92% 10.49% 9.08%

Adjusted return on average tangible common equity 11.19% 10.75% 9.16%

Non-GAAP Financial Measures (Cont’d)

23

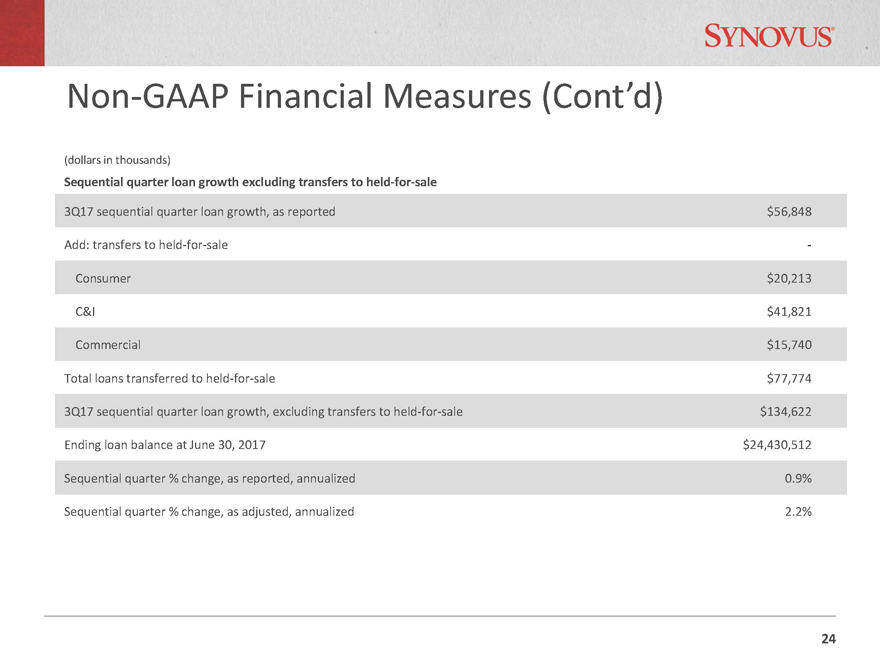

(dollars in thousands)

Sequential quarter loan growth excluding transfers to held-for-sale

3Q17 sequential quarter loan growth, as reported $56,848

Add: transfers to held-for-sale -

Consumer $20,213

C&I $41,821

Commercial $15,740

Total loans transferred to held-for-sale $77,774

3Q17 sequential quarter loan growth, excluding transfers to held-for-sale $134,622

Ending loan balance at June 30, 2017 $24,430,512

Sequential quarter % change, as

reported, annualized 0.9%

Sequential quarter % change, as adjusted, annualized 2.2%

Non-GAAP Financial Measures (Cont’d)

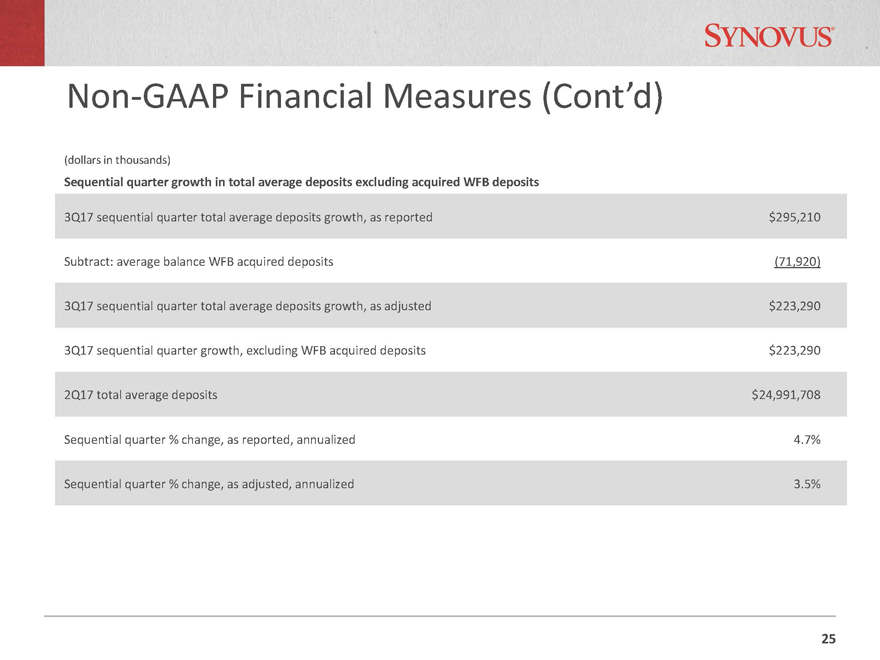

24

(dollars in thousands)

Sequential quarter growth in total average deposits excluding acquired WFB deposits

3Q17 sequential quarter total average deposits growth, as reported $295,210

Subtract: average

balance WFB acquired deposits (71,920)

3Q17 sequential quarter total average deposits growth, as adjusted $223,290

3Q17 sequential quarter growth, excluding WFB acquired deposits $223,290

2Q17 total average

deposits $24,991,708

Sequential quarter % change, as reported, annualized 4.7%

Sequential quarter % change, as adjusted, annualized 3.5%

Non-GAAP Financial Measures (Cont’d)

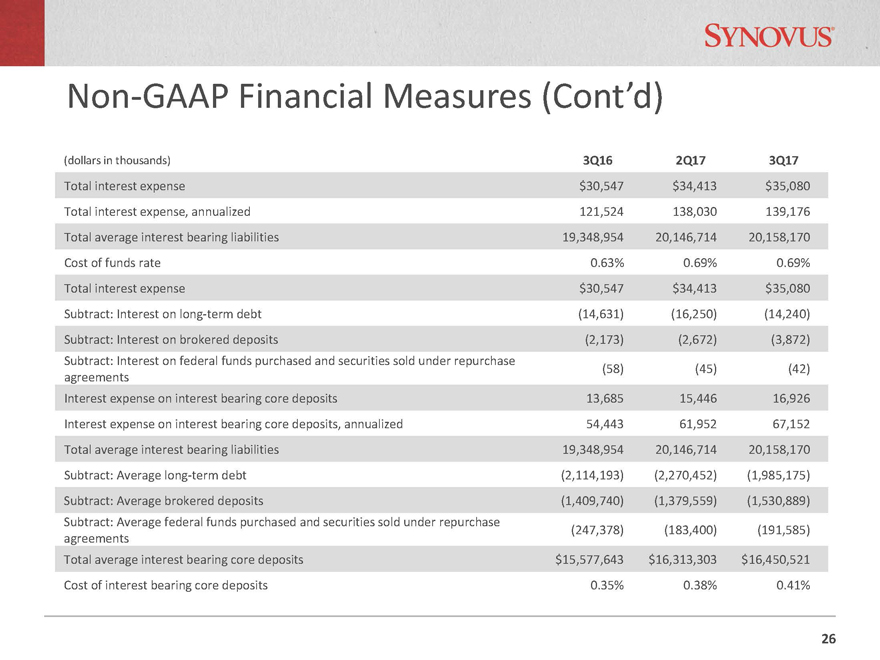

25

(dollars in thousands) 3Q16 2Q17 3Q17

Total interest expense $30,547 $34,413 $35,080

Total interest expense, annualized 121,524

138,030 139,176

Total average interest bearing liabilities 19,348,954 20,146,714 20,158,170

Cost of funds rate 0.63% 0.69% 0.69%

Total interest expense $30,547 $34,413 $35,080

Subtract: Interest on long-term debt (14,631) (16,250) (14,240)

Subtract:

Interest on brokered deposits (2,173) (2,672) (3,872)

Subtract: Interest on federal funds purchased and securities sold under repurchase

agreements (58) (45) (42)

Interest expense on interest bearing core deposits 13,685 15,446

16,926

Interest expense on interest bearing core deposits, annualized 54,443 61,952 67,152

Total average interest bearing liabilities 19,348,954 20,146,714 20,158,170

Subtract: Average

long-term debt (2,114,193) (2,270,452) (1,985,175)

Subtract: Average brokered deposits (1,409,740) (1,379,559) (1,530,889)

Subtract: Average federal funds purchased and securities sold under repurchase

agreements

(247,378) (183,400) (191,585)

Total average interest bearing core deposits $15,577,643 $16,313,303 $16,450,521

Cost of interest bearing core deposits 0.35% 0.38% 0.41%

Non-GAAP Financial Measures (Cont’d)

26

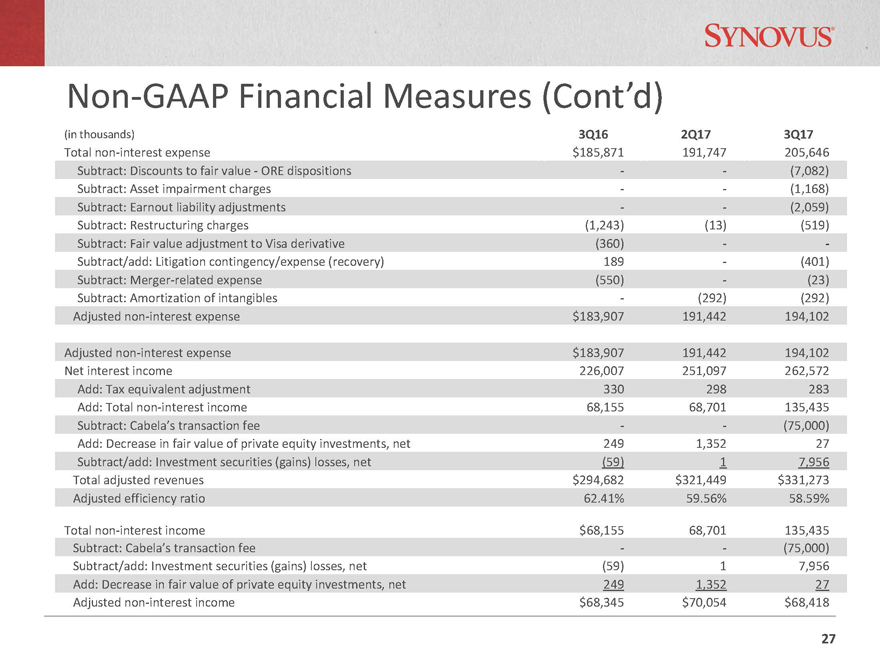

(in thousands) 3Q16 2Q17 3Q17

Total non-interest expense $185,871 191,747 205,646

Subtract: Discounts to fair value—ORE dispositions — (7,082)

Subtract: Asset impairment charges — (1,168)

Subtract: Earnout liability

adjustments — (2,059)

Subtract: Restructuring charges (1,243) (13) (519)

Subtract: Fair value adjustment to Visa derivative (360) —

Subtract/add:

Litigation contingency/expense (recovery) 189—(401)

Subtract: Merger-related expense (550)—(23)

Subtract: Amortization of intangibles—(292) (292)

Adjusted

non-interest expense $183,907 191,442 194,102

Adjusted non-interest expense

$183,907 191,442 194,102

Net interest income 226,007 251,097 262,572

Add: Tax

equivalent adjustment 330 298 283

Add: Total non-interest income 68,155 68,701 135,435

Subtract: Cabela’s transaction fee — (75,000)

Add: Decrease in fair value of private

equity investments, net 249 1,352 27

Subtract/add: Investment securities (gains) losses, net (59) 1 7,956

Total adjusted revenues $294,682 $321,449 $331,273

Adjusted efficiency ratio 62.41% 59.56%

58.59%

Total non-interest income $68,155 68,701 135,435

Subtract: Cabela’s transaction fee — (75,000)

Subtract/add: Investment securities

(gains) losses, net (59) 1 7,956

Add: Decrease in fair value of private equity investments, net 249 1,352 27

Adjusted non-interest income $68,345 $70,054 $68,418

Non-GAAP Financial Measures (Cont’d)

27

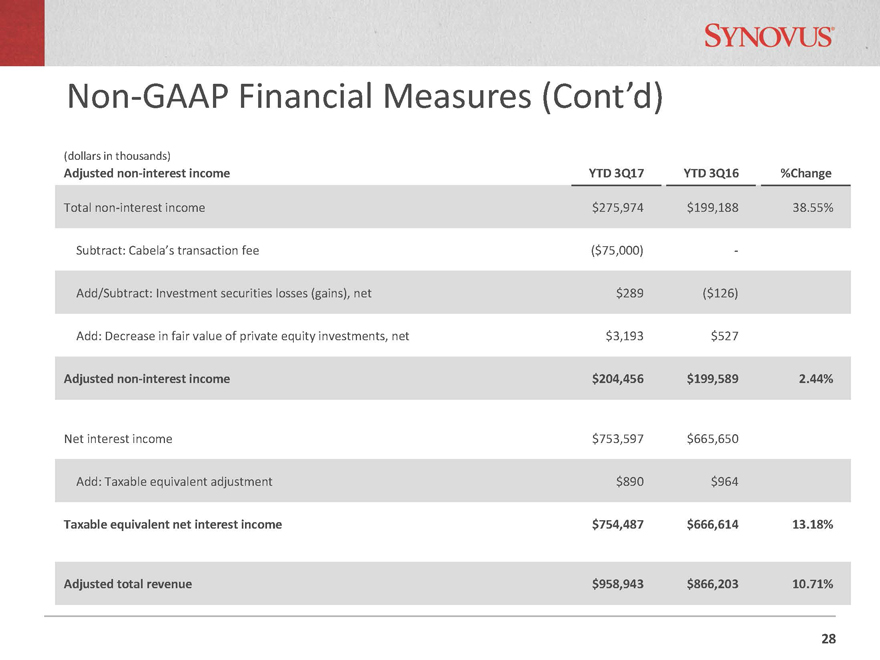

(dollars in thousands)

Adjusted non-interest income YTD 3Q17 YTD 3Q16 %Change

Total non-interest income $275,974 $199,188 38.55%

Subtract: Cabela’s transaction fee ($75,000) -

Add/Subtract: Investment

securities losses (gains), net $289 ($126)

Add: Decrease in fair value of private equity investments, net $3,193 $527

Adjusted non-interest income $204,456 $199,589 2.44%

Net interest income $753,597 $665,650

Add: Taxable equivalent adjustment $890

$964

Taxable equivalent net interest income $754,487 $666,614 13.18%

Adjusted

total revenue $958,943 $866,203 10.71%

Non-GAAP Financial Measures (Cont’d)

28

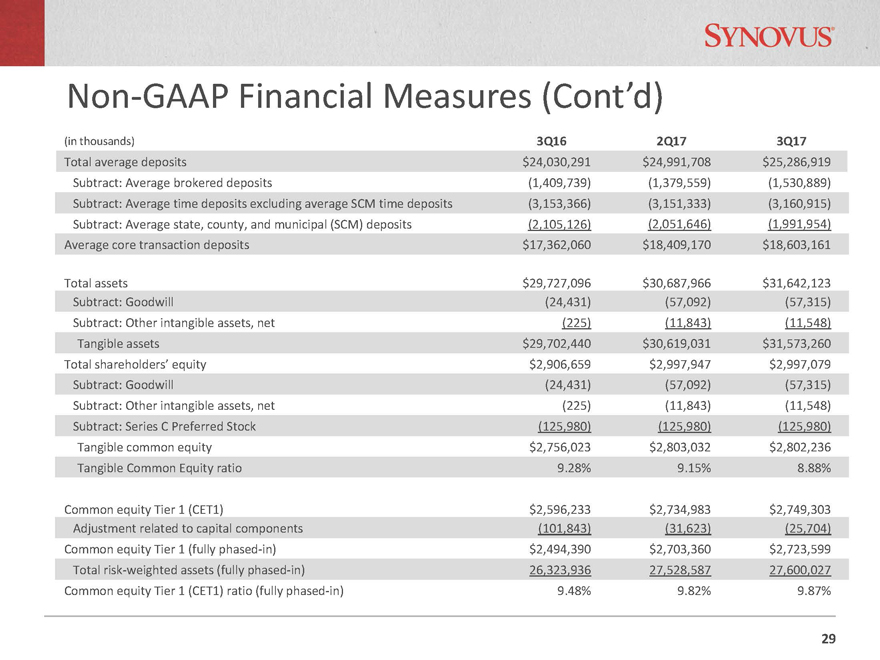

(in thousands) 3Q16 2Q17 3Q17

Total average deposits $24,030,291 $24,991,708 $25,286,919

Subtract: Average brokered deposits

(1,409,739) (1,379,559) (1,530,889)

Subtract: Average time deposits excluding average SCM time deposits (3,153,366) (3,151,333) (3,160,915)

Subtract: Average state, county, and municipal (SCM) deposits (2,105,126) (2,051,646) (1,991,954)

Average core transaction deposits $17,362,060 $18,409,170 $18,603,161

Total assets $29,727,096

$30,687,966 $31,642,123

Subtract: Goodwill (24,431) (57,092) (57,315)

Subtract: Other intangible assets, net (225) (11,843) (11,548)

Tangible

assets $29,702,440 $30,619,031 $31,573,260

Total shareholders’ equity $2,906,659 $2,997,947 $2,997,079

Subtract: Goodwill (24,431) (57,092) (57,315)

Subtract: Other intangible assets, net (225)

(11,843) (11,548)

Subtract: Series C Preferred Stock (125,980) (125,980) (125,980)

Tangible common equity $2,756,023 $2,803,032 $2,802,236

Tangible Common Equity ratio 9.28%

9.15% 8.88%

Common equity Tier 1 (CET1) $2,596,233 $2,734,983 $2,749,303

Adjustment related to capital components (101,843) (31,623) (25,704)

Common

equity Tier 1 (fully phased-in) $2,494,390 $2,703,360 $2,723,599

Total risk-weighted assets (fully phased-in) 26,323,936 27,528,587 27,600,027

Common equity Tier 1 (CET1) ratio (fully

phased-in) 9.48% 9.82% 9.87%

Non-GAAP Financial Measures (Cont’d)

29

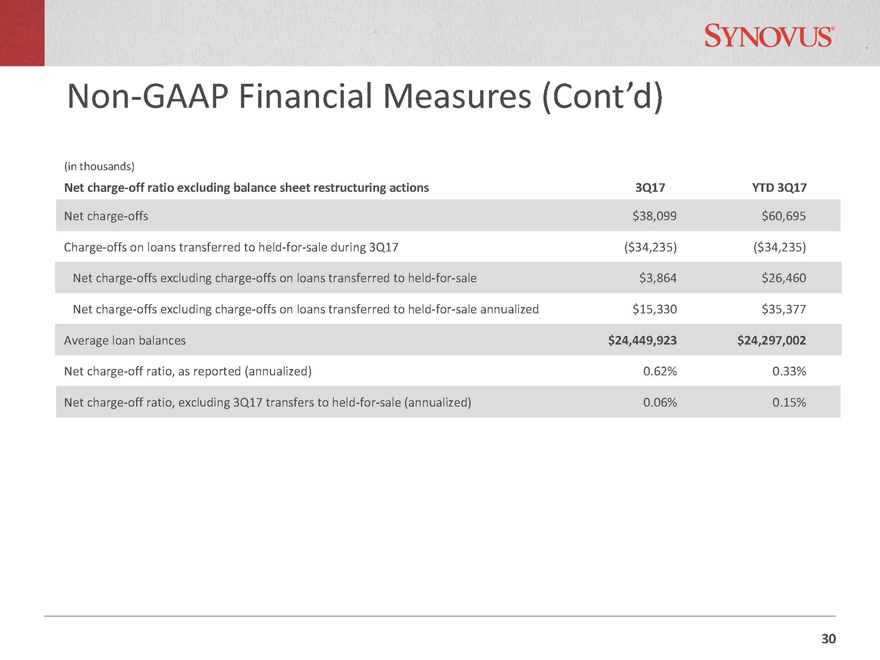

(in thousands)

Net charge-off ratio excluding balance sheet restructuring actions 3Q17 YTD 3Q17

Net charge-offs $38,099 $60,695

Charge-offs on loans transferred to held-for-sale during 3Q17 ($34,235) ($34,235)

Net charge-offs excluding charge-offs on loans transferred to held-for-sale $3,864 $26,460

Net charge-offs excluding charge-offs on loans transferred to held-for-sale

annualized $15,330 $35,377

Average loan balances $24,449,923 $24,297,002

Net charge-off ratio, as reported (annualized) 0.62% 0.33%

Net charge-off ratio, excluding

3Q17 transfers to held-for-sale (annualized) 0.06% 0.15%

Non-GAAP Financial Measures (Cont’d)

30