Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - VISTEON CORP | ex-322q3201710xq.htm |

| EX-32.1 - EXHIBIT 32.1 - VISTEON CORP | ex-321q3201710xq.htm |

| EX-31.2 - EXHIBIT 31.2 - VISTEON CORP | ex-312q3201710xq.htm |

| EX-31.1 - EXHIBIT 31.1 - VISTEON CORP | ex-311q3201710xq.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

________________

FORM 10-Q

(Mark One)

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) |

OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2017

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) |

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission file number 001-15827

VISTEON CORPORATION

(Exact name of registrant as specified in its charter)

State of Delaware | 38-3519512 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

One Village Center Drive, Van Buren Township, Michigan | 48111 |

(Address of principal executive offices) | (Zip code) |

Registrant’s telephone number, including area code: (800)-VISTEON

Not applicable

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ü No__

Indicate by check mark whether the registrant: has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ü No __

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer," "accelerated filer,” "smaller reporting company" and “emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ü Accelerated filer __ Non-accelerated filer __ Smaller reporting company __

Emerging growth company __

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. __

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes __ No ü

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ü No__

As of October 19, 2017, the registrant had outstanding 31,098,830 shares of common stock.

Exhibit index located on page number 49.

1

Visteon Corporation and Subsidiaries

Index

Page | ||

2

Part I

Financial Information

Item 1. | Consolidated Financial Statements |

VISTEON CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Dollars in Millions Except Per Share Amounts)

(Unaudited)

Three Months Ended September 30 | Nine Months Ended September 30 | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

Sales | $ | 765 | $ | 770 | $ | 2,349 | $ | 2,345 | |||||||

Cost of sales | 649 | 665 | 1,990 | 2,010 | |||||||||||

Gross margin | 116 | 105 | 359 | 335 | |||||||||||

Selling, general and administrative expenses | 54 | 53 | 158 | 163 | |||||||||||

Restructuring expense | 6 | 5 | 10 | 22 | |||||||||||

Interest expense | 4 | 6 | 15 | 14 | |||||||||||

Interest income | 1 | 1 | 3 | 4 | |||||||||||

Equity in net income of non-consolidated affiliates | 1 | — | 6 | 3 | |||||||||||

Other (income) expense, net | (1 | ) | 12 | (3 | ) | 16 | |||||||||

Income before income taxes | 55 | 30 | 188 | 127 | |||||||||||

Provision for income taxes | 8 | 5 | 34 | 27 | |||||||||||

Net income from continuing operations | 47 | 25 | 154 | 100 | |||||||||||

Income (loss) from discontinued operations, net of tax | — | 7 | 8 | (15 | ) | ||||||||||

Net income | 47 | 32 | 162 | 85 | |||||||||||

Net income attributable to non-controlling interests | 4 | 4 | 11 | 12 | |||||||||||

Net income attributable to Visteon Corporation | $ | 43 | $ | 28 | $ | 151 | $ | 73 | |||||||

Basic earnings (loss) per share: | |||||||||||||||

Continuing operations | $ | 1.38 | $ | 0.62 | $ | 4.50 | $ | 2.47 | |||||||

Discontinued operations | — | 0.21 | 0.25 | (0.42 | ) | ||||||||||

Basic earnings per share attributable to Visteon Corporation | $ | 1.38 | $ | 0.83 | $ | 4.75 | $ | 2.05 | |||||||

Diluted earnings (loss) per share: | |||||||||||||||

Continuing operations | $ | 1.35 | $ | 0.61 | $ | 4.43 | $ | 2.44 | |||||||

Discontinued operations | — | 0.20 | 0.25 | (0.41 | ) | ||||||||||

Diluted earnings per share attributable to Visteon Corporation | $ | 1.35 | $ | 0.81 | $ | 4.68 | $ | 2.03 | |||||||

Comprehensive income: | |||||||||||||||

Comprehensive income | $ | 59 | $ | 35 | $ | 205 | $ | 106 | |||||||

Comprehensive income attributable to Visteon Corporation | $ | 53 | $ | 31 | $ | 190 | $ | 96 | |||||||

See accompanying notes to the consolidated financial statements.

3

VISTEON CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(Dollars in Millions)

(Unaudited) | |||||||

September 30 | December 31 | ||||||

2017 | 2016 | ||||||

ASSETS | |||||||

Cash and equivalents | $ | 732 | $ | 878 | |||

Restricted cash | 3 | 4 | |||||

Accounts receivable, net | 506 | 505 | |||||

Inventories, net | 174 | 151 | |||||

Other current assets | 181 | 170 | |||||

Total current assets | 1,596 | 1,708 | |||||

Property and equipment, net | 361 | 345 | |||||

Intangible assets, net | 128 | 129 | |||||

Investments in non-consolidated affiliates | 40 | 45 | |||||

Other non-current assets | 154 | 146 | |||||

Total assets | $ | 2,279 | $ | 2,373 | |||

LIABILITIES AND EQUITY | |||||||

Short-term debt, including current portion of long-term debt | $ | 44 | $ | 36 | |||

Accounts payable | 429 | 463 | |||||

Accrued employee liabilities | 102 | 103 | |||||

Other current liabilities | 235 | 309 | |||||

Total current liabilities | 810 | 911 | |||||

Long-term debt | 347 | 346 | |||||

Employee benefits | 305 | 303 | |||||

Deferred tax liabilities | 22 | 20 | |||||

Other non-current liabilities | 62 | 69 | |||||

Stockholders’ equity: | |||||||

Preferred stock (par value $0.01, 50 million shares authorized, none outstanding as of September 30, 2017 and December 31, 2016) | — | — | |||||

Common stock (par value $0.01, 250 million shares authorized, 55 million shares issued, 31 and 33 million shares outstanding as of September 30, 2017 and December 31, 2016, respectively) | 1 | 1 | |||||

Additional paid-in capital | 1,333 | 1,327 | |||||

Retained earnings | 1,420 | 1,269 | |||||

Accumulated other comprehensive loss | (194 | ) | (233 | ) | |||

Treasury stock | (1,945 | ) | (1,778 | ) | |||

Total Visteon Corporation stockholders’ equity | 615 | 586 | |||||

Non-controlling interests | 118 | 138 | |||||

Total equity | 733 | 724 | |||||

Total liabilities and equity | $ | 2,279 | $ | 2,373 | |||

See accompanying notes to the consolidated financial statements.

4

VISTEON CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Dollars in Millions)

(Unaudited)

Nine Months Ended September 30 | |||||||

2017 | 2016 | ||||||

Operating Activities | |||||||

Net income | $ | 162 | $ | 85 | |||

Adjustments to reconcile net income to net cash provided from operating activities: | |||||||

Depreciation and amortization | 62 | 62 | |||||

Equity in net income of non-consolidated affiliates, net of dividends remitted | (6 | ) | (2 | ) | |||

Non-cash stock-based compensation | 9 | 6 | |||||

Gain on India operations repurchase | (7 | ) | — | ||||

(Gains) losses on divestitures and impairments | (4 | ) | 5 | ||||

Other non-cash items | 2 | 15 | |||||

Changes in assets and liabilities: | |||||||

Accounts receivable | 29 | 15 | |||||

Inventories | (15 | ) | 15 | ||||

Accounts payable | (39 | ) | (45 | ) | |||

Other assets and other liabilities | (62 | ) | (118 | ) | |||

Net cash provided from operating activities | 131 | 38 | |||||

Investing Activities | |||||||

Capital expenditures, including intangibles | (69 | ) | (56 | ) | |||

India operations repurchase | (47 | ) | — | ||||

Payments for acquisition and divestiture of businesses | (2 | ) | (15 | ) | |||

Settlement of net investment hedge | 5 | — | |||||

Proceeds from asset sales and business divestitures | 15 | 15 | |||||

Climate Transaction withholding tax refund | — | 356 | |||||

Short-term investments | — | 47 | |||||

Loans to non-consolidated affiliates, net of repayments | — | (8 | ) | ||||

Other | 1 | — | |||||

Net cash (used by) provided from investing activities | (97 | ) | 339 | ||||

Financing Activities | |||||||

Short-term debt, net | 8 | (11 | ) | ||||

Principal payments on debt | (2 | ) | (2 | ) | |||

Distribution payments | (1 | ) | (1,736 | ) | |||

Repurchase of common stock | (170 | ) | (500 | ) | |||

Dividends paid to non-controlling interests | (29 | ) | — | ||||

Stock based compensation tax withholding payments | (1 | ) | (11 | ) | |||

Other | (2 | ) | — | ||||

Net cash used by financing activities | (197 | ) | (2,260 | ) | |||

Effect of exchange rate changes on cash and equivalents | 17 | 6 | |||||

Net decrease in cash and equivalents | (146 | ) | (1,877 | ) | |||

Cash and equivalents at beginning of the period | 878 | 2,729 | |||||

Cash and equivalents at end of the period | $ | 732 | $ | 852 | |||

See accompanying notes to the consolidated financial statements.

5

VISTEON CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1. Description of Business

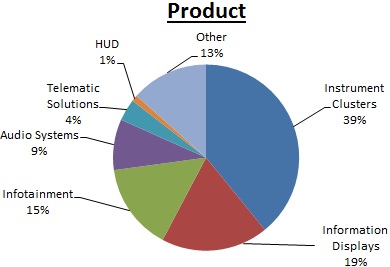

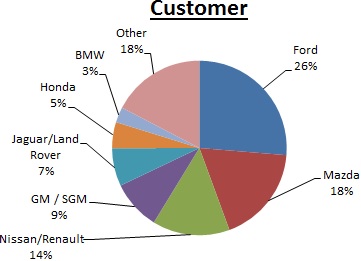

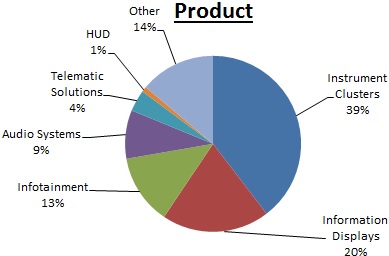

Visteon Corporation (the "Company" or "Visteon") is a global automotive supplier that designs, engineers and manufactures innovative electronics products for nearly every original equipment vehicle manufacturer ("OEM") worldwide including Ford, Mazda, Nissan/Renault, General Motors, Honda, BMW and Daimler. Visteon is headquartered in Van Buren Township, Michigan and has an international network of manufacturing operations, technical centers and joint venture operations, supported by approximately 10,000 employees, dedicated to the design, development, manufacture and support of its product offerings and its global customers. The Company's manufacturing and engineering footprint is principally located outside of the United States. Visteon delivers value for its customers and stockholders through its technology-focused core vehicle cockpit electronics business. The Company's cockpit electronics product portfolio includes instrument clusters, information displays, infotainment systems, audio systems, telematics solutions, and head up displays. The Company's vehicle cockpit electronics business is comprised of and reported under the Electronics segment. In addition to the Electronics segment, the Company had operations in South America and Europe associated with the former Climate business, not subject to discontinued operations classification, that comprised Other, and were exited by December 31, 2016.

NOTE 2. Summary of Significant Accounting Policies

The unaudited consolidated financial statements of the Company have been prepared in accordance with the rules and regulations of the U.S. Securities and Exchange Commission. Certain information and footnote disclosures normally included in financial statements prepared in accordance with accounting principles generally accepted in the United States ("U.S. GAAP") have been condensed or omitted pursuant to such rules and regulations. These interim consolidated financial statements include all adjustments (consisting of normal recurring adjustments, except as otherwise disclosed) that management believes are necessary for a fair presentation of the results of operations, financial position and cash flows of the Company for the interim periods presented. Interim results are not necessarily indicative of full-year results.

Reclassifications: Certain prior period amounts have been reclassified to conform to the current period presentation.

Other (Income) Expense, Net:

Three Months Ended September 30 | Nine Months Ended September 30 | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(Dollars in Millions) | |||||||||||||||

Transformation initiatives | $ | 1 | $ | — | $ | 1 | $ | 3 | |||||||

Gain on non-consolidated affiliate transactions, net | (2 | ) | (1 | ) | (4 | ) | (1 | ) | |||||||

Foreign currency translation charge | — | 11 | — | 11 | |||||||||||

Loss on asset contribution | — | 2 | — | 2 | |||||||||||

Transaction exchange losses | — | — | — | 1 | |||||||||||

$ | (1 | ) | $ | 12 | $ | (3 | ) | $ | 16 | ||||||

Transformation initiative costs include information technology separation costs, integration of acquired business, and financial and advisory services incurred in connection with the Company's transformation into a pure play cockpit electronics business. The gain on non-consolidated affiliate transactions represents the Company's sale of three cost method investments and an equity method investment during the nine months ended September 30, 2017 as further described in Note 5, "Non-Consolidated Affiliates."

During the three and nine months ended September 30, 2016, the Company recorded a charge of approximately $11 million related to foreign currency translation amounts recorded in accumulated other comprehensive loss associated with the agreement to sell the Company's South Africa climate operations. In connection with the closure of the Climate facility in Argentina, the Company entered into an agreement, during the third quarter of 2016, to contribute land and building with a net book value of $2 million to the local municipality.

Restricted Cash: Restricted cash represents amounts designated for uses other than current operations and includes $2 million related to the Letter of Credit Facility, and $1 million related to cash collateral for other corporate purposes as of September 30, 2017.

6

Recently Issued Accounting Pronouncements: In May 2014, the Financial Accounting Standards Board ("FASB") issued Accounting Standards Update ("ASU") No. 2014-9, "Revenue from Contracts with Customers," which is the new comprehensive revenue recognition standard that will supersede existing revenue recognition guidance under U.S. GAAP. The standard's core principle is that a company will recognize revenue when it transfers promised goods or services to a customer in an amount that reflects the consideration to which the company expects to be entitled in exchange for those goods and services. This ASU allows for both retrospective and prospective methods of adoption.

The Company has, with other industry leaders, interacted with the FASB on certain interpretation issues as well as interacted with non-authoritative industry groups with respect to the implementation of the standard and will continue to monitor the interactions between its industry group and the standard setters. The Company does not expect any changes to how it accounts for reimbursements of pre-production costs, currently accounted for as a cost reduction. In addition, the Company continues to evaluate its contracts with customers analyzing the impact, if any, on revenue from the sale of production parts, particularly in regards to material rights, variable consideration and the impact of termination clauses on the timing of revenue recognition. The Company will adopt this standard January 1, 2018 and has selected the modified retrospective transition method for any impacts that might arise. Under the modified retrospective method, the Company will recognize the cumulative effect of initially applying the standard as an adjustment to opening retained earnings at the date of initial application. While the Company continues to evaluate a significant number of contracts with customers, the Company does not expect the cumulative adjustment to be material. As policy elections, the Company plans to exclude from revenue all value added tax ("VAT"), a consumption tax placed on certain products in countries outside the U.S. In addition, the Company will elect not to identify shipping and handling as a separate performance obligation.

In February 2016, the FASB issued ASU 2016-02, "Leases (Topic 842)." The amendments in Topic 842 supersede current lease requirements in Topic 840 which require lessees to recognize most leases on their balance sheets as lease liabilities with corresponding right-of-use assets. The objective of Topic 842 is to establish the principles that lessees and lessors shall apply to report useful information to users of financial statements about the amount, timing, and uncertainty of cash flows arising from a lease. This new guidance is effective for interim and annual reporting periods beginning after December 15, 2018, with early adoption permitted. The Company is currently evaluating the impact of adopting this standard on its consolidated financial statements.

In March 2016, the FASB issued ASU 2016-09, "Compensation - Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting." The ASU includes multiple provisions intended to simplify various aspects of the accounting for share-based payments. While aimed at reducing the cost and complexity of the accounting for share-based payments, these amendments are not expected to significantly impact net income, earnings per share, and the statement of cash flows. This new guidance was effective for interim and annual reporting periods beginning after December 15, 2016, with early adoption permitted. The Company's adoption of this standard did not have a material impact on its consolidated financial statements. The Company has adopted an entity-wide accounting policy election to account for forfeitures in compensation cost when they occur.

In August 2016, the FASB issued ASU 2016-15, "Statement of Cash Flows (Topic 230): Classification of certain cash receipts and cash payments." The ASU addresses eight specific cash flow issues with the objective of reducing the existing diversity in practice in how certain transactions are classified in the statement of cash flows. The ASU will be applied using a retrospective transition method to each period presented. This new guidance is effective for interim and annual reporting periods beginning after December 15, 2017 with early adoption permitted. The Company is currently evaluating the impact of adopting this standard on its consolidated financial statements.

In March 2017, the FASB issued ASU 2017-07, “Compensation - Retirement Benefits (Topic 715): Improving the presentation of net periodic pension cost and net periodic postretirement benefit cost." The ASU requires entities to present the service cost component of the net periodic benefit cost in the same income statement line item(s) as other employee compensation costs arising from services rendered during the period. In addition, only the service cost component will be eligible for capitalization in assets. Entities will present the other components separately from the line item(s) that includes the service cost and outside of any subtotal of operating income, and disclose the line(s) used to present the other components of net periodic benefit cost, if the components are not presented separately in the income statement. The standard will be applied retrospectively for the presentation of the service cost component and the other components of net periodic pension cost and net periodic postretirement benefit cost in the income statement and prospectively, for the guidance limiting the capitalization of net periodic benefit cost in assets to the service cost. This new guidance is effective for interim and annual reporting periods beginning after December 15, 2017 and interim periods, with early adoption permitted. The Company is currently evaluating the impact of adopting this standard on its consolidated financial statements.

In May 2017, the FASB issued ASU 2017-09, "Compensation - Stock Compensation (Topic 718): Scope of Modification Accounting." The ASU amends the scope of modification accounting for share-based payment arrangements, provides guidance

7

on the types of changes to the terms or conditions of share-based payment awards to which an entity would be required to apply modification accounting. The new guidance will allow companies to make certain changes to awards without accounting for them as modifications. It does not change the accounting for modifications. The new guidance will be applied prospectively to awards modified on or after the adoption date. This new guidance is effective for interim and annual reporting periods beginning after December 15, 2017 with early adoption permitted. The Company is currently evaluating the impact of adopting this standard on its consolidated financial statements.

In July 2017, the FASB issued ASU 2017-11, "Earnings Per Share (Topic 260): Distinguishing Liabilities from Equity (Topic 480); Derivatives and Hedging (Topic 815): (Part I) Accounting for certain financial instruments with down round features, (Part II)Replacement of the indefinite deferral for mandatory redeemable financial instruments of certain Nonpublic entities and certain mandatory Non-controlling interests with a scope exception." The amendments in Part I of this update change the classification analysis of certain equity-linked financial instruments (or embedded features) with down round features. When determining whether certain financial instruments should be classified as liabilities or equity instruments, a down round feature no longer precludes equity classification when assessing whether the instrument is indexed to an entity’s own stock. The amendments also clarify existing disclosure requirements for equity-classified instruments. This new guidance is effective for interim and annual reporting periods beginning after December 15, 2018 and interim periods, with early adoption permitted. The Company is currently evaluating the impact of adopting this standard on its consolidated financial statements.

In August 2017, the FASB issued ASU 2017-12, "Derivative and Hedging (Topic 815): Targeted improvements to accounting for hedging activities." The ASU was created to better align accounting rules with a company’s risk management activities to better reflect the economic results of hedging in the financial statements; and simplify hedge accounting treatment. This new guidance is effective for interim and annual reporting periods beginning after December 15, 2018 and interim periods, with early adoption permitted. The Company is currently evaluating the impact of adopting this standard on its consolidated financial statements.

NOTE 3. Business Acquisition

On July 8, 2016 Visteon acquired AllGo Embedded Systems Private Limited, a leading developer of embedded multimedia system solutions to global vehicle manufacturers, for a purchase price of $17 million ("AllGo Purchase") including $2 million of contingent consideration payable upon completion of certain technology milestones, achieved and paid on July 6, 2017. In addition, the purchase agreement includes contingent payments of $5 million if key employees remain employed through July 2019. The AllGo Purchase was a strategic acquisition to add greater scale and depth to the Company's infotainment software capabilities.

The AllGo Purchase was accounted for as a business combination, with the purchase price allocation reflecting the final valuation results, is shown below (dollars in millions):

Assets Acquired: | Liabilities Assumed: | |||||||

Accounts receivable | $ | 1 | Deferred tax liabilities | $ | 2 | |||

Intangible assets | 7 | Total liabilities assumed | 2 | |||||

Goodwill | 11 | |||||||

Total assets acquired | $ | 19 | Purchase price | $ | 17 | |||

Assets acquired and liabilities assumed were recorded at estimated fair values based on management's estimates, available information, and reasonable and supportable assumptions. Additionally, the Company utilized a third-party to assist with certain estimates of fair values. Fair values for intangible assets were based on the income approach including excess earnings and relief from royalty methods. These fair value measurements are classified within level 3 of the fair value hierarchy. The purchase price allocation resulted in goodwill of $11 million, which is not deductible for income tax purposes; however, purchase accounting requires the establishment of deferred tax liabilities on the fair value increments related primarily to intangible assets that will be recognized as a future income tax benefit as the related assets are amortized.

The pro forma effects of the AllGo acquisitions does not materially impact the Company's reported results for any period presented, and as a result no pro forma financial statements are presented.

NOTE 4. Discontinued Operations

During 2014 and 2015, the Company divested the majority of its global Interiors business (the "Interiors Divestiture") and completed the sale of its Argentina and Brazil interiors operations on December 1, 2016. Separately, the Company completed the sale of the majority of its global Climate business (the "Climate Transaction") during 2015. As the operations subject to the Interiors Divestiture and Climate Transaction met conditions required to qualify for discontinued operations reporting, the results of operations for the

8

Interiors and Climate businesses have been reclassified to income (loss) from discontinued operations, net of tax in the consolidated statements of comprehensive income for the three and nine month periods ended September 30, 2017 and 2016.

Discontinued operations are summarized as follows:

Three Months Ended September 30 | Nine Months Ended September 30 | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(Dollars in Millions) | |||||||||||||||

Sales | $ | — | $ | 14 | $ | — | $ | 34 | |||||||

Cost of sales | — | 20 | — | 48 | |||||||||||

Gross margin | — | (6 | ) | — | (14 | ) | |||||||||

Selling, general and administrative expenses | — | 2 | — | 4 | |||||||||||

(Gain) loss on Climate Transaction | — | — | (7 | ) | 2 | ||||||||||

Loss and impairment on Interiors Divestiture | — | — | — | 2 | |||||||||||

Other expense, net | — | 1 | — | 2 | |||||||||||

(Loss) income from discontinued operations before income taxes | — | (9 | ) | 7 | (24 | ) | |||||||||

Benefit for income taxes | — | (16 | ) | (1 | ) | (9 | ) | ||||||||

Net income (loss) from discontinued operations, net of tax, attributable to Visteon | $ | — | $ | 7 | $ | 8 | $ | (15 | ) | ||||||

In connection with the Climate Transaction, the Company completed the repurchase of the electronics operations located in India during the first quarter of 2017 for $47 million, recognizing a $7 million gain on settlement of purchase commitment contingencies. The Company had previously consolidated the India operations based on the Company's controlling financial interest as a result of the repurchase obligation, operating control, and the obligation to fund losses or benefit from earnings.

During the nine months ended September 30, 2016, the Company recorded currency impacts of $8 million in connection with the Korean capital gains withholding tax recovered during the first quarter of 2016. During the third quarter of 2016, the Company recorded a $17 million income tax benefit to reflect change in estimates associated with the filing of the Company’s U.S. tax returns that resulted in a reduction in U.S. income tax related to the 2015 Climate Transaction.

NOTE 5. Non-Consolidated Affiliates

Non-Consolidated Affiliate Transactions

Visteon and Yangfeng Automotive Trim Systems Co. Ltd. ("YF") each own 50% of a joint venture under the name of Yanfeng Visteon Investment Co., Ltd. ("YFVIC"). In October 2014, YFVIC completed the purchase of YF’s 49% direct ownership in Yanfeng Visteon Automotive Electronics Co., Ltd ("YFVE") a consolidated joint venture of the Company. The purchase by YFVIC was financed through a shareholder loan from YF and external borrowings which were guaranteed by Visteon, of which $15 million is outstanding as of September 30, 2017. The guarantee contains standard non-payment provisions to cover the borrowers in event of non-payment of principal, accrued interest, and other fees, and the loan is expected to be fully paid by September 2019.

During the first quarter of 2017, the Company completed the sale of its 50% interest in an equity method investment for proceeds of $7 million, consistent with its carrying value.

During 2017 the Company disposed of its remaining cost method investments. In the first half of of 2017, the Company sold two cost method investments for proceeds of approximately $6 million and recorded a net pretax gain of $2 million. On July 11, 2017, the Company sold a cost method investment for proceeds of approximately $2 million and recorded a pretax gain of $2 million. The gain on sale of the cost method investments are included in the Company's consolidated statements of comprehensive income as "Other (income) expense, net" for the three and nine months ended September 30, 2017.

During the third quarter of 2016, the Company agreed to sell a 50% interest in an equity investment for approximately $7 million. The Company recorded a loss in the investment of $5 million during the three and nine months ended September 30, 2016 related to this transaction. Also in the third quarter 2016, the Company sold a cost method investment to a third party for proceeds of approximately $11 million. The Company recorded a pre-tax gain of $6 million during the three and nine months ended September 30, 2016 related to this transaction. The net $1 million gain on the sale of non-consolidated affiliates is included in the Company's consolidated statements of comprehensive income as "Other (income) expense, net" for the three and nine months ended September 30, 2016.

9

Investments in Affiliates

The Company recorded equity in net income of affiliates of $1 million for the three month period ended September 30, 2017. For the nine month periods ended September 30, 2017 and 2016, the Company recorded net income of affiliates of $6 million and $3 million, respectively.

Investments in affiliates were $40 million and $45 million as of September 30, 2017 and December 31, 2016, respectively. As of December 31, 2016, investments in affiliates accounted for under the cost method and equity method totaled $5 million and $40 million, respectively.

Variable Interest Entities

The Company determines whether joint ventures in which it has invested are Variable Interest Entities (“VIE”) at the start of each new venture and when a reconsideration event has occurred. An enterprise must consolidate a VIE if it is determined to be the primary beneficiary of the VIE. The primary beneficiary has both the power to direct the activities of the VIE that most significantly impact the entity’s economic performance and the obligation to absorb losses or the right to receive benefits from the VIE that could potentially be significant to the VIE.

The Company determined that YFVIC, is a VIE. The Company holds a variable interest in YFVIC primarily related to its ownership interests and subordinated financial support. The Company and YF each own 50% of YFVIC and neither entity has the power to control the operations of YFVIC, therefore the Company is not the primary beneficiary of YFVIC and does not consolidate the joint venture.

A summary of the Company's investments in YFVIC is provided below.

September 30 | December 31 | ||||||

2017 | 2016 | ||||||

(Dollars in Millions) | |||||||

Payables due to YFVIC | $ | 9 | $ | 14 | |||

Exposure to loss in YFVIC | |||||||

Investment in YFVIC | $ | 27 | $ | 22 | |||

Receivables due from YFVIC | 28 | 15 | |||||

Subordinated loan receivable | 22 | 22 | |||||

Loan guarantee | 15 | 22 | |||||

Maximum exposure to loss in YFVIC | $ | 92 | $ | 81 | |||

NOTE 6. Restructuring Activities

Given the economically-sensitive and highly competitive nature of the automotive electronics industry, the Company continues to closely monitor current market factors and industry trends, taking action as necessary which may include restructuring actions. However, there can be no assurance that any such actions will be sufficient to fully offset the impact of adverse factors on the Company or its results of operations, financial position and cash flows. During the three and nine months ended September 30, 2017, the Company recorded $6 million and $10 million of restructuring expenses, net of reversals, respectively.

Electronics

During the fourth quarter of 2016, the Company announced a restructuring program impacting engineering and administrative functions to further align the Company's engineering and related administrative footprint with its core product technologies and customers. Through September 30, 2017, the Company has recorded approximately $37 million of restructuring expenses, net of reversals, under this program, and expects to incur up to $45 million of restructuring costs associated with approximately 250 employees. During the three and nine months ended September 30, 2017, the Company has recorded approximately $6 million and $10 million, respectively, of restructuring expenses under this program, and $18 million remains accrued as of September 30, 2017. The Company expects to record additional restructuring costs related to this program as the underlying plan is finalized.

During the first quarter of 2016, the Company announced a restructuring program to transform the Company's engineering organization and supporting functional areas to focus on execution and technology. The organization will be comprised of regional engineering, product management and advanced technologies, and global centers of competence. For the three and nine month

10

periods ended September 30, 2016, the Company recorded $1 million and $13 million, respectively, of restructuring expenses under this program, associated with approximately 100 employees. As of September 30, 2017 the plan is considered substantially complete.

Other and Discontinued Operations

During the three and nine months ended September 30, 2016, the Company recorded $4 million and $11 million, respectively, of restructuring expenses, related to severance and termination benefits, in connection with the wind-down of certain operations in South America. As of September 30, 2017, the plan is considered substantially complete.

As of September 30, 2017, the Company retained approximately $6 million of restructuring reserves as part of the Interiors Divestiture associated with previously announced programs for the fundamental reorganization of operations at facilities in Brazil and France.

Restructuring Reserves

Restructuring reserve balances of $26 million and $40 million as of September 30, 2017 and December 31, 2016, respectively, are classified as "Other current liabilities" on the consolidated balance sheets. The Company anticipates that the activities associated with the current restructuring reserve balance will be substantially complete within one year. The Company’s consolidated restructuring reserves and related activity are summarized below, including amounts associated with discontinued operations.

Electronics | Other | Total | |||||||||

(Dollars in Millions) | |||||||||||

December 31, 2016 | $ | 31 | $ | 9 | $ | 40 | |||||

Expense | 1 | — | 1 | ||||||||

Utilization | (8 | ) | (1 | ) | (9 | ) | |||||

March 31, 2017 | 24 | 8 | 32 | ||||||||

Expense | 6 | — | 6 | ||||||||

Utilization | (6 | ) | (1 | ) | (7 | ) | |||||

Reversals | (2 | ) | (1 | ) | (3 | ) | |||||

Foreign currency | 2 | — | 2 | ||||||||

June 30, 2017 | 24 | 6 | 30 | ||||||||

Expense | 7 | — | 7 | ||||||||

Utilization | (11 | ) | — | (11 | ) | ||||||

Reversals | (1 | ) | — | (1 | ) | ||||||

Foreign currency | 1 | — | 1 | ||||||||

September 30, 2017 | $ | 20 | $ | 6 | $ | 26 | |||||

NOTE 7. Inventories

Inventories consist of the following components:

September 30 | December 31 | ||||||

2017 | 2016 | ||||||

(Dollars in Millions) | |||||||

Raw materials | $ | 109 | $ | 83 | |||

Work-in-process | 33 | 34 | |||||

Finished products | 32 | 34 | |||||

$ | 174 | $ | 151 | ||||

11

NOTE 8. Other Assets

Other current assets are comprised of the following components:

September 30 | December 31 | ||||||

2017 | 2016 | ||||||

(Dollars in Millions) | |||||||

Recoverable taxes | $ | 61 | $ | 60 | |||

Joint venture receivables | 37 | 39 | |||||

Prepaid assets and deposits | 36 | 35 | |||||

Notes receivable | 28 | 18 | |||||

Contractually reimbursable engineering costs | 15 | 7 | |||||

Foreign currency hedges | 1 | 6 | |||||

Other | 3 | 5 | |||||

$ | 181 | $ | 170 | ||||

The Company receives bank notes from certain of its customers in China to settle trade accounts receivable. The Company may hold such bank notes until maturity, exchange them with suppliers to settle liabilities, or sell them to third party financial institutions in exchange for cash. The Company has entered into arrangements with financial institutions to sell certain bank notes, generally maturing within nine months. Notes are sold with recourse, but qualify as a sale as all rights to the notes have passed to the financial institution. The Company sold $11 million during the nine months ended September 30, 2017 to financial institutions, $5 million of which occurred in the third quarter and will mature within the first half of 2018. The collection of such bank notes are included in operating cash flows based on the substance of the underlying transactions, which are operating in nature.

Other non-current assets are comprised of the following components:

September 30 | December 31 | ||||||

2017 | 2016 | ||||||

(Dollars in Millions) | |||||||

Deferred tax assets | $ | 49 | $ | 48 | |||

Recoverable taxes | 36 | 34 | |||||

Joint venture receivables | 26 | 25 | |||||

Contractually reimbursable engineering costs | 19 | 11 | |||||

Long term notes receivable | 10 | 10 | |||||

Other | 14 | 18 | |||||

$ | 154 | $ | 146 | ||||

In conjunction with the Interiors Divestiture, the Company entered into a three year term loan with the buyer for $10 million, which matures on December 1, 2019.

Current and non-current contractually reimbursable engineering costs of $15 million and $19 million, respectively, as of September 30, 2017 and $7 million and $11 million, respectively, as of December 31, 2016, are related to pre-production design and development costs incurred pursuant to long-term supply arrangements that are contractually guaranteed for reimbursement by customers. The Company expects to receive cash reimbursement payments of approximately $8 million during the remainder of 2017, $10 million in 2018, $9 million in 2019, $2 million in 2020 and $5 million in 2021.

12

NOTE 9. Intangible Assets, net

Intangible assets, net as of September 30, 2017 and December 31, 2016, are comprised of the following:

September 30, 2017 | December 31, 2016 | ||||||||||||||||||||||||

Estimated Weighted Average Useful Life (years) | Gross Carrying Value | Accumulated Amortization | Net Carrying Value | Gross Carrying Value | Accumulated Amortization | Net Carrying Value | |||||||||||||||||||

(Dollars in Millions) | |||||||||||||||||||||||||

Definite-Lived: | |||||||||||||||||||||||||

Developed technology | 10 | $ | 41 | $ | 28 | $ | 13 | $ | 40 | $ | 25 | $ | 15 | ||||||||||||

Customer related | 9 | 85 | 31 | 54 | 83 | 25 | 58 | ||||||||||||||||||

Capitalized software development | 3 | 6 | — | 6 | 4 | — | 4 | ||||||||||||||||||

Other | 32 | 10 | 1 | 9 | 8 | 1 | 7 | ||||||||||||||||||

Subtotal | 142 | 60 | 82 | 135 | 51 | 84 | |||||||||||||||||||

Indefinite-Lived: | |||||||||||||||||||||||||

Goodwill | 46 | — | 46 | 45 | — | 45 | |||||||||||||||||||

Total | $ | 188 | $ | 60 | $ | 128 | $ | 180 | $ | 51 | $ | 129 | |||||||||||||

The Company recorded approximately $3 million and $9 million of amortization expense related to definite-lived intangible assets for the three and nine months ended September 30, 2017. The Company currently estimates annual amortization expense to be $13 million for 2017, $14 million for 2018 and 2019, $11 million for 2020, and $9 million for 2021. Indefinite-lived intangible assets are not amortized but are tested for impairment at least annually, or earlier when events and circumstances indicate that it is more likely than not that such assets have been impaired. There were no indicators of potential impairment during the nine months ended September 30, 2017.

During the three months ended September 30, 2017, the Company contributed $2 million to a non-profit corporation who is building a state of the art research and development facility. The contribution provides the Company certain rights regarding access to the facility for three years. The Company will use the facility for autonomous driving research and development activities for multiple products and therefore capitalized the contribution as an intangible asset. The Company expects to make a second contribution of $2 million during the first half of 2018 when the facility is substantially complete. The asset will be amortized over a 36 month period on a straight-line basis beginning in January 2018 when the term of the arrangement begins.

The Company capitalizes software development costs after the software product development reaches technological feasibility and until the software product becomes releasable to customers. During the nine months ended September 30, 2017, the Company capitalized $2 million related to software development cost intended for external use. The capitalized software development costs are amortized over the useful life of the technology on a straight-line basis.

A roll-forward of the carrying amounts of intangible assets is presented below:

Definite-lived intangibles | Indefinite-lived intangibles | ||||||||||||||||||||||

Developed Technology | Customer Related | Capitalized Software Development | Other | Goodwill | Total | ||||||||||||||||||

(Dollars in Millions) | |||||||||||||||||||||||

December 31, 2016 | $ | 15 | $ | 58 | $ | 4 | $ | 7 | $ | 45 | $ | 129 | |||||||||||

Additions | — | — | 2 | 2 | — | 4 | |||||||||||||||||

Foreign currency | 1 | 2 | — | — | 1 | 4 | |||||||||||||||||

Amortization | (3 | ) | (6 | ) | — | — | — | (9 | ) | ||||||||||||||

September 30, 2017 | $ | 13 | $ | 54 | $ | 6 | $ | 9 | $ | 46 | $ | 128 | |||||||||||

13

NOTE 10. Other Liabilities

Other current liabilities are summarized as follows:

September 30 | December 31 | ||||||

2017 | 2016 | ||||||

(Dollars in Millions) | |||||||

Product warranty and recall accruals | $ | 39 | $ | 43 | |||

Contribution payable | 35 | 31 | |||||

Restructuring reserves | 26 | 40 | |||||

Rent and royalties | 23 | 23 | |||||

Foreign currency hedges | 22 | 7 | |||||

Deferred income | 14 | 14 | |||||

Distribution payable | 14 | 15 | |||||

Dividends payable | 12 | 5 | |||||

Income taxes payable | 11 | 22 | |||||

Joint venture payables | 10 | 22 | |||||

Non-income taxes payable | 3 | 8 | |||||

Electronics operations repurchase commitment | — | 50 | |||||

Other | 26 | 29 | |||||

$ | 235 | $ | 309 | ||||

On December 1, 2015, Visteon completed the sale and transfer of its equity ownership in Visteon Deutschland GmbH, which operated the Berlin, Germany interiors plant ("Germany Interiors Divestiture"). The Company contributed cash, of approximately $141 million, assets of $27 million, and liabilities of $198 million including pension related liabilities. The Company will make a final contribution payment of approximately $35 million anticipated during 2017 upon fulfillment of buyer contractual commitments.

On January 22, 2016 the Company paid to shareholders a special distribution of $1.74 billion, an additional $14 million will be paid over a two-year period upon vesting and settlement of restricted stock units and performance-based share units previously granted to the Company's employees. The special cash distribution was funded from the Climate Transaction proceeds.

Following the initial sale as part of the Climate Transaction, the Company repurchased an Electronics operation located in India on March 27, 2017 as further described in Note 4, "Discontinued Operations."

Other non-current liabilities are summarized as follows:

September 30 | December 31 | ||||||

2017 | 2016 | ||||||

(Dollars in Millions) | |||||||

Deferred income | $ | 16 | $ | 18 | |||

Product warranty and recall accruals | 12 | 12 | |||||

Income tax reserves | 11 | 14 | |||||

Non-income tax reserves | 8 | 10 | |||||

Other | 15 | 15 | |||||

$ | 62 | $ | 69 | ||||

14

NOTE 11. Debt

The Company’s short and long-term debt consists of the following:

September 30 | December 31 | ||||||

2017 | 2016 | ||||||

(Dollars in Millions) | |||||||

Short-Term Debt: | |||||||

Current portion of long-term debt | $ | 1 | $ | 3 | |||

Short-term borrowings | 43 | 33 | |||||

$ | 44 | $ | 36 | ||||

Long-Term Debt: | |||||||

Term debt facility | $ | 347 | $ | 346 | |||

Short-Term Debt

Short-term borrowings are primarily related to the Company's non-U.S. consolidated joint ventures and are payable primarily in U.S. Dollars, Chinese Renminbi and India Rupee, or Russian Ruble. The Company had short-term borrowings of $43 million and $33 million as of September 30, 2017 and December 31, 2016, respectively. Short-term borrowings increased in the third quarter of 2017 primarily due to changes in working capital needs.

Available borrowings on outstanding affiliate credit facilities as of September 30, 2017 are approximately $24 million and certain of these facilities have pledged assets as security.

Long-Term Debt

As of December 31, 2016, the Company had an amended credit agreement (the “Credit Agreement”) which included a $350 million Term Facility maturing April 9, 2021 and a Revolving Credit Facility with capacity of $200 million maturing April 9, 2019. Borrowings under the Term Facility accrued interest at the greater of LIBOR or 0.75%, plus 2.75%, with an option by the Company to specify the LIBOR tenor of either 1, 2, 3, or 6 months. Loans drawn under the Revolving Credit Facility had an interest rate equal to LIBOR plus a margin ranging from 2.00% to 2.75% as specified by a ratings grid contained in the Credit Agreement. As of December 31, 2016, borrowings under the Revolving Credit Facility would accrue interest at LIBOR plus 2.50%. There were no outstanding borrowings at year-end.

On March 24, 2017, the Company entered into a second amendment to the Credit Agreement to, among other things, extend the maturity dates of both facilities by three years and increase the Revolving Credit Facility capacity to $300 million. The amended Revolving Credit Facility will mature on March 24, 2022 and the amended Term Facility will mature on March 24, 2024. The amendment reduced the LIBOR spread applicable to each of the Revolving Credit Facility and the Term Facility by 0.50% and reduced the LIBOR floor related to the Term Facility from 0.75% to 0.00%. The $350 million of borrowings under the amended Term Facility accrue interest at a rate of LIBOR plus 2.25%. In conjunction with the refinancing the Company received a credit rating upgrade from Standard & Poor's to BB from BB-. Pursuant to the ratings grid contained within the amended Revolving Credit Facility agreement, any borrowing thereunder shall accrue interest at LIBOR plus 1.75%. As of September 30, 2017, there were no outstanding borrowings under the amended Revolving Credit Facility.

The Revolving Credit Facility also provides $75 million availability for the issuance of letters of credit and a maximum of $20 million for swing line borrowing. Any amount of the facility utilized for letters of credit or swing line loans outstanding will reduce the amount available under the amended Revolving Credit Facility. The Company may request increases in the limits under the amended Term Facility and the amended Revolving Credit Facility and may request the addition of one or more term loan facilities under the Credit Agreement. Outstanding borrowings may be prepaid without penalty (other than borrowings made for the purpose of reducing the effective interest rate margin or weighted average yield of the loans). There are mandatory prepayments of principal in connection with: (i) excess cash flow sweeps above certain leverage thresholds, (ii) certain asset sales or other dispositions, (iii) certain refinancing of indebtedness and (iv) over-advances under the Revolving Credit Facility. There are no excess cash flow sweeps required at the Company’s current leverage level.

The Credit Agreement requires the Company and its subsidiaries to comply with customary affirmative and negative covenants, and contains customary events of default. The Revolving Credit Facility also requires that the Company maintain a total net leverage ratio no greater than 3.00:1.00. During any period when the Company’s corporate and family ratings meet investment

15

grade ratings, certain of the negative covenants shall be suspended. As of September 30, 2017, the Company was in compliance with all its debt covenants.

All obligations under the Credit Agreement and obligations in respect of certain cash management services and swap agreements with the lenders and their affiliates are unconditionally guaranteed by certain of the Company’s subsidiaries. Under the terms of the Credit Agreement, all obligations under the Credit Agreement are secured by a first-priority perfected lien (subject to certain exceptions) on substantially all property of the Company and the subsidiaries party to the Security Agreement, subject to certain limitations.

In connection with amending both the Term Facility and Revolving Credit Facility, the Company recorded $1 million of interest expense and deferred $2 million of costs as a non-current asset. The deferred costs will be amortized over the term of the debt facilities. As of September 30, 2017, the amended Term Facility remains at $350 million of aggregate principal and there were no outstanding borrowings under the amended Revolving Credit Facility.

Other

On September 29, 2017 the Company amended certain terms of its letter of credit facility. The amended agreement reduced the facility amount from $15 million to $5 million and extended the expiration date by three years to September 30, 2020. Under the agreement the Company is required to maintain a collateral account equal to 103% of the aggregate stated amount of issued letters of credit (or 110% for non-U.S. currencies) and must reimburse any amounts drawn under issued letters of credit. The Company had $2 million of outstanding letters of credit issued under this facility secured by restricted cash, as of September 30, 2017.

Additionally, the Company had $18 million of locally issued letters of credit with $1 million of collateral as of September 30, 2017, to support various tax appeals, customs arrangements and other obligations at its local affiliates.

NOTE 12. Employee Benefit Plans

Defined Benefit Plans

The Company's net periodic benefit costs for all defined benefit plans for the three month periods ended September 30, 2017 and 2016 were as follows:

U.S. Plans | Non-U.S. Plans | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(Dollars in Millions) | |||||||||||||||

Costs Recognized in Income: | |||||||||||||||

Service cost | $ | — | $ | — | $ | 1 | $ | 1 | |||||||

Interest cost | 7 | 7 | 2 | 3 | |||||||||||

Expected return on plan assets | (10 | ) | (10 | ) | (2 | ) | (3 | ) | |||||||

Net pension (income) expense | $ | (3 | ) | $ | (3 | ) | $ | 1 | $ | 1 | |||||

The Company's net periodic benefit costs for all defined benefit plans for the nine month periods ended September 30, 2017 and 2016 were as follows:

U.S. Plans | Non-U.S. Plans | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(Dollars in Millions) | |||||||||||||||

Costs Recognized in Income: | |||||||||||||||

Service cost | $ | — | $ | — | $ | 2 | $ | 2 | |||||||

Interest cost | 21 | 21 | 7 | 9 | |||||||||||

Expected return on plan assets | (30 | ) | (31 | ) | (7 | ) | (9 | ) | |||||||

Settlements and curtailments | — | — | — | 1 | |||||||||||

Amortization of losses and other | — | — | 1 | — | |||||||||||

Net pension (income) expense | $ | (9 | ) | $ | (10 | ) | $ | 3 | $ | 3 | |||||

16

During the nine months ended September 30, 2017, cash contributions to the Company's defined benefit plans were less than a million for the U.S. plans and $5 million for the non-U.S. plans. The Company expects to make cash contributions to its defined benefit pension plans of $7 million in 2017.

On April 28, 2016, the Company purchased a non-participating annuity contract for all participants of the Canada non-represented plan. The annuity purchase covered 52 participants and resulted in the use of $5 million of plan assets for pension benefit obligation settlements of approximately $5 million. In connection with the annuity purchase, the Company recorded a settlement loss of approximately $1 million during the the three months ended September 30, 2016.

NOTE 13. Income Taxes

During the three and nine month periods ended September 30, 2017, the Company recorded a provision for income tax on continuing operations of $8 million and $34 million, respectively, which reflects income tax expense in countries where the Company is profitable; withholding taxes; changes in uncertain tax benefits; and the inability to record a tax benefit for pretax losses and/or recognize expense for pretax income in certain jurisdictions (including the U.S.) due to valuation allowances. Pretax losses from continuing operations in jurisdictions where valuation allowances are maintained and no income tax benefits are recognized totaled

$13 million and $38 million for the nine months ended September 30, 2017 and September 30, 2016, respectively, resulting in an increase in the Company's effective tax rate in those years.

The Company provides for U.S. and non-U.S. income taxes and non-U.S. withholding taxes on the projected future repatriations of the earnings from its non-U.S. operations that are not considered permanently reinvested at each tier of the legal entity structure.

During the nine month periods ended September 30, 2017 and 2016, the Company recognized expense primarily related to non-U.S. withholding taxes of $6 million and $3 million, respectively, reflecting the Company's forecasts which contemplate numerous financial and operational considerations that impact future repatriations.

The Company's provision for income taxes in interim periods is computed by applying an estimated annual effective tax rate against income before income taxes, excluding equity in net income of non-consolidated affiliates for the period. Effective tax rates vary from period to period as separate calculations are performed for those countries where the Company's operations are profitable and whose results continue to be tax-effected and for those countries where full deferred tax valuation allowances exist and are maintained. In determining the estimated annual effective tax rate, the Company analyzes various factors, including but not limited to, forecasts of projected annual earnings, taxing jurisdictions in which the pretax income and/or pretax losses will be generated and available tax planning strategies. The Company’s estimated annual effective tax rate is updated each quarter and may be significantly impacted by changes to the mix of forecasted earnings by tax jurisdiction. The tax impact of adjustments to the estimated annual effective tax rate are recorded in the period such estimates are revised. The Company is also required to record the tax impact of certain other non-recurring tax items, including changes in judgment about valuation allowances and uncertain tax positions, and changes in tax laws or rates, in the interim period in which they occur, rather than include them in the estimated annual effective tax rate.

The need to maintain valuation allowances against deferred tax assets in the U.S. and other affected countries will cause variability in the Company’s quarterly and annual effective tax rates. Full valuation allowances against deferred tax assets in the U.S. and applicable foreign countries will be maintained until sufficient positive evidence exists to reduce or eliminate them. The factors considered by management in its determination of the probability of the realization of the deferred tax assets include, but are not limited to, recent historical financial results, historical taxable income, projected future taxable income, the expected timing of the reversals of existing temporary differences and tax planning strategies. If, based upon the weight of available evidence, it is more likely than not the deferred tax assets will not be realized, a valuation allowance is recorded. The weight given to the positive and negative evidence is commensurate with the extent to which the evidence may be objectively verified. As such, it is generally difficult for positive evidence regarding projected future taxable income exclusive of reversing taxable temporary differences to outweigh objective negative evidence of recent financial reporting losses, in particular, when there is a cumulative loss incurred over a three-year period. In regards to the full valuation allowance recorded against the U.S. net deferred tax assets, the cumulative U.S. pretax book loss adjusted for significant permanent items incurred over the three-year period ended December 31, 2016 limits the ability to consider other subjective evidence such as the Company’s plans to improve U.S. profits, and as such, the Company continues to maintain a full valuation allowance against the U.S. net deferred tax assets. Based on the Company’s current assessment, it is possible that within the next 12 to 24 months, the existing valuation allowance against the U.S. net deferred tax assets could be partially released. Any such release is dependent upon the sustained improvement in U.S. operating results, and, if such a release of the valuation allowance were to occur, it could have a significant impact on net income in the quarter in which it is deemed appropriate to partially release the reserve.

17

Unrecognized Tax Benefits

Gross unrecognized tax benefits as of September 30, 2017 and December 31, 2016, including amounts attributable to discontinued operations, were $17 million and $35 million, respectively. Of these amounts approximately $8 million and $12 million as of September 30, 2017 and December 31, 2016, respectively, represent the amount of unrecognized benefits that, if recognized, would impact the effective tax rate. The gross unrecognized tax benefit differs from that which would impact the effective tax rate due to uncertain tax positions embedded in other deferred tax attributes carrying a full valuation allowance. If the uncertainty is resolved while a full valuation allowance is maintained, these uncertain tax positions should not impact the effective tax rate in current or future periods. The Company records interest and penalties related to uncertain tax positions as a component of income tax expense and related amounts accrued at September 30, 2017 and December 31, 2016 were $3 million and $4 million, respectively.

During the first quarter of 2017, the IRS completed the audit of the Company's U.S. tax returns for the 2012 and 2013 tax years. The closing of the audit did not have a material impact on the Company's effective tax rate due to the valuation allowances maintained against the Company's U.S. tax attributes resulting in a decrease in unrecognized tax benefits of $16 million. Also during the first quarter of 2017, the Company settled tax assessments from the Mexican tax authorities in the amount of $2 million related to certain transfer pricing-related issues. During the third quarter of 2017, the Company settled tax assessments in connection with the Company’s former operations in Spain and France in the amount of $1 million.

With few exceptions, the Company is no longer subject to U.S. federal tax examinations for years before 2014, or state, local or non-U.S. income tax examinations for years before 2003, although U.S. net operating losses carried forward into open tax years technically remain open to adjustment. During the second quarter of 2017, the IRS contacted the Company to begin the examination process of the Company’s U.S. tax returns for 2014 and 2015. Although it is not possible to predict the timing of the resolution of all ongoing tax audits with accuracy, it is reasonably possible that certain tax proceedings in Europe, Asia and Mexico could conclude within the next twelve months and result in a significant increase or decrease in the balance of gross unrecognized tax benefits. Given the number of years, jurisdictions and positions subject to examination, the Company is unable to estimate the full range of possible adjustments to the balance of unrecognized tax benefits. The long-term portion of uncertain income tax positions (including interest) in the amount of $11 million is included in Other non-current liabilities on the consolidated balance sheet.

A reconciliation of the beginning and ending amount of unrecognized tax benefits including amounts attributable to discontinued operations is as follows:

Nine Months Ended September 30, 2017 | |||

(Dollars in Millions) | |||

Beginning balance | $ | 35 | |

Tax positions related to current period: | |||

Additions | 2 | ||

Tax positions related to prior periods: | |||

Reductions | (21 | ) | |

Effect of exchange rate changes | 1 | ||

Ending balance | $ | 17 | |

During 2012, Brazil tax authorities issued tax assessment notices to Visteon Sistemas Automotivos (“Sistemas”) related to the sale of its chassis business to a third party, which required a deposit in the amount of $15 million during 2013 necessary to open a judicial proceeding against the government in order to suspend the debt and allow Sistemas to operate regularly before the tax authorities after attempts to reopen an appeal of the administrative decision failed. Adjusted for currency impacts and accrued interest, the deposit amount is approximately $16 million, as of September 30, 2017. The Company believes that the risk of a negative outcome is remote once the matter is fully litigated at the highest judicial level. These appeal payments, as well as income tax refund claims associated with other jurisdictions, total $19 million as of September 30, 2017, and are included in "Other non-current assets" on the consolidated balance sheet.

18

NOTE 14. Stockholders’ Equity and Non-controlling Interests

Changes in equity for the three and nine months ended September 30, 2017 and 2016 are as follows:

2017 | 2016 | ||||||||||||||||||||||

Visteon | NCI | Total | Visteon | NCI | Total | ||||||||||||||||||

(Dollars in Millions) | |||||||||||||||||||||||

Three Months Ended September 30 | |||||||||||||||||||||||

Beginning balance | $ | 569 | $ | 136 | $ | 705 | $ | 616 | $ | 148 | $ | 764 | |||||||||||

Net income from continuing operations | 43 | 4 | 47 | 21 | 4 | 25 | |||||||||||||||||

Net income from discontinued operations | — | — | — | 7 | — | 7 | |||||||||||||||||

Net income | 43 | 4 | 47 | 28 | 4 | 32 | |||||||||||||||||

Other comprehensive income (loss) | |||||||||||||||||||||||

Foreign currency translation adjustments | 17 | 2 | 19 | 7 | — | 7 | |||||||||||||||||

Net investment hedge | (7 | ) | — | (7 | ) | (4 | ) | — | (4 | ) | |||||||||||||

Benefit plans | (1 | ) | — | (1 | ) | — | — | — | |||||||||||||||

Unrealized hedging gain | 1 | — | 1 | — | — | — | |||||||||||||||||

Total other comprehensive income | 10 | 2 | 12 | 3 | — | 3 | |||||||||||||||||

Stock-based compensation, net | 3 | — | 3 | 1 | — | 1 | |||||||||||||||||

Share repurchase | (10 | ) | — | (10 | ) | — | — | — | |||||||||||||||

Dividends to non-controlling interests | — | (24 | ) | (24 | ) | — | (6 | ) | (6 | ) | |||||||||||||

Ending balance | $ | 615 | $ | 118 | $ | 733 | $ | 648 | $ | 146 | $ | 794 | |||||||||||

2017 | 2016 | ||||||||||||||||||||||

Visteon | NCI | Total | Visteon | NCI | Total | ||||||||||||||||||

(Dollars in Millions) | |||||||||||||||||||||||

Nine Months Ended September 30 | |||||||||||||||||||||||

Beginning balance | $ | 586 | $ | 138 | $ | 724 | $ | 1,057 | $ | 142 | $ | 1,199 | |||||||||||

Net income from continuing operations | 143 | 11 | 154 | 88 | 12 | 100 | |||||||||||||||||

Net income (loss) from discontinued operations | 8 | — | 8 | (15 | ) | — | (15 | ) | |||||||||||||||

Net income | 151 | 11 | 162 | 73 | 12 | 85 | |||||||||||||||||

Other comprehensive income (loss) | |||||||||||||||||||||||

Foreign currency translation adjustments | 57 | 4 | 61 | 32 | (2 | ) | 30 | ||||||||||||||||

Net investment hedge | (20 | ) | — | (20 | ) | (6 | ) | — | (6 | ) | |||||||||||||

Benefit plans | (2 | ) | — | (2 | ) | 1 | — | 1 | |||||||||||||||

Unrealized hedging gain (loss) | 4 | — | 4 | (4 | ) | — | (4 | ) | |||||||||||||||

Total other comprehensive income (loss) | 39 | 4 | 43 | 23 | (2 | ) | 21 | ||||||||||||||||

Stock-based compensation, net | 9 | — | 9 | (5 | ) | — | (5 | ) | |||||||||||||||

Share repurchase | (170 | ) | — | (170 | ) | (500 | ) | — | (500 | ) | |||||||||||||

Dividends to non-controlling interests | — | (35 | ) | (35 | ) | — | (6 | ) | (6 | ) | |||||||||||||

Ending balance | $ | 615 | $ | 118 | $ | 733 | $ | 648 | $ | 146 | $ | 794 | |||||||||||

Share Repurchase Program

During 2016, Visteon completed two stock buyback programs with a third-party financial institution to purchase shares of common stock for an aggregate purchase price of $500 million. Under these programs, Visteon purchased 7,190,506 shares at an average price of $69.48.

On January 10, 2017, the Company's board of directors authorized $400 million of share repurchase of its shares of common stock through. On February 27, 2017 the Company entered into an accelerated share buyback ("ASB") program with a third-party financial institution to purchase shares of Visteon common stock for an aggregate purchase price of $125 million. On March 2, 2017, the Company received an initial delivery of 1,062,022 shares of common stock using a reference price of $94.16. The

19

program was concluded in May 2017 and the Company received an additional 238,344 shares. In total, the Company purchased 1,300,366 shares at an average price of $96.13 under this ASB program.

During the second quarter of 2017, the Company entered into a brokerage agreement with a third party financial institution to execute open market share purchases of the Company's common stock. The Company paid approximately $35 million to repurchase 359,100 shares at an average price of $97.44.

During the third quarter of 2017, the Company paid approximately $10 million to repurchase 82,513 shares on the open market at an average price of $121.25.

The Company anticipates that additional repurchases of common stock, if any, would occur from time to time in open market transactions or in privately negotiated transactions depending on market and economic conditions, share price, trading volume, alternative uses of capital and other factors.

Non-Controlling Interests

Non-controlling interests in the Visteon Corporation economic entity are as follows:

September 30 | December 31 | ||||||

2017 | 2016 | ||||||

(Dollars in Millions) | |||||||

Yanfeng Visteon Automotive Electronics Co., Ltd. | $ | 73 | $ | 97 | |||

Shanghai Visteon Automotive Electronics, Co., Ltd. | 43 | 39 | |||||

Other | 2 | 2 | |||||

$ | 118 | $ | 138 | ||||

20

Accumulated Other Comprehensive (Loss) Income

Changes in Accumulated other comprehensive (loss) income (“AOCI”) and reclassifications out of AOCI by component include:

Three Months Ended September 30 | Nine Months Ended September 30 | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(Dollars in Millions) | |||||||||||||||

Changes in AOCI: | |||||||||||||||

Beginning balance | $ | (204 | ) | $ | (170 | ) | $ | (233 | ) | $ | (190 | ) | |||

Other comprehensive income (loss) before reclassification, net of tax | 8 | 2 | 34 | 24 | |||||||||||

Amounts reclassified from AOCI | 2 | 1 | 5 | (1 | ) | ||||||||||

Ending balance | $ | (194 | ) | $ | (167 | ) | $ | (194 | ) | $ | (167 | ) | |||

Changes in AOCI by Component: | |||||||||||||||

Foreign currency translation adjustments | |||||||||||||||

Beginning balance | $ | (123 | ) | $ | (134 | ) | $ | (163 | ) | $ | (159 | ) | |||

Other comprehensive income before reclassification, net of tax (a) | 17 | 7 | 57 | 32 | |||||||||||

Ending balance | (106 | ) | (127 | ) | (106 | ) | (127 | ) | |||||||

Net investment hedge | |||||||||||||||

Beginning balance | (3 | ) | 2 | 10 | 4 | ||||||||||

Other comprehensive loss before reclassification, net of tax (a) | (7 | ) | (4 | ) | (20 | ) | (6 | ) | |||||||

Ending balance | (10 | ) | (2) | (10 | ) | (2) | |||||||||

Benefit plans | |||||||||||||||

Beginning balance | (76 | ) | (35) | (75 | ) | (36) | |||||||||

Other comprehensive income before reclassification, net of tax (a) | (1 | ) | — | (2 | ) | — | |||||||||

Amounts reclassified from AOCI | — | — | — | 1 | |||||||||||

Ending balance | (77 | ) | (35 | ) | (77 | ) | (35 | ) | |||||||

Unrealized hedging (loss) gain | |||||||||||||||

Beginning balance | (2 | ) | (3 | ) | (5 | ) | 1 | ||||||||

Other comprehensive income (loss) before reclassification, net of tax (b) | (1 | ) | (1 | ) | (1 | ) | (2 | ) | |||||||

Amounts reclassified from AOCI | 2 | 1 | 5 | (2 | ) | ||||||||||

Ending balance | (1 | ) | (3 | ) | (1 | ) | (3 | ) | |||||||

Total AOCI | $ | (194 | ) | $ | (167 | ) | $ | (194 | ) | $ | (167 | ) | |||

(a) Net tax expense was less than $1 million for the nine month period ending September 30, 2017. Income tax effects are zero for all other periods due to the recording of the valuation allowance.

(b) Net tax expense of less than $1 million and $1 million are related to unrealized hedging gain for the three and nine month periods ended September 30, 2017, respectively. Net tax benefits of $1 million and less than $1 million are related to unrealized hedging gain for the three and nine month periods ended September 30, 2016, respectively.

NOTE 15. Earnings Per Share

Basic earnings per share is calculated by dividing net income attributable to Visteon by the weighted average number of shares of common stock outstanding. Diluted earnings per share is computed by dividing net income by the weighted average number of common and potentially dilutive common shares outstanding. Performance based share units are considered contingently issuable shares, and are included in the computation of diluted earnings per share based on the number of shares that would be issuable if the reporting date were the end of the contingency period and if the result would be dilutive.

21

The table below provides details underlying the calculations of basic and diluted earnings (loss) per share:

Three Months Ended September 30 | Nine Months Ended September 30 | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(In Millions, Except Per Share Amounts) | |||||||||||||||

Numerator: | |||||||||||||||

Net income from continuing operations attributable to Visteon | $ | 43 | $ | 21 | $ | 143 | $ | 88 | |||||||

Income (loss) from discontinued operations, net of tax | — | 7 | 8 | (15 | ) | ||||||||||

Net income attributable to Visteon | $ | 43 | $ | 28 | $ | 151 | $ | 73 | |||||||

Denominator: | |||||||||||||||

Average common stock outstanding - basic | 31.2 | 34.0 | 31.8 | 35.6 | |||||||||||

Dilutive effect of performance based share units and other | 0.6 | 0.4 | 0.5 | 0.4 | |||||||||||

Diluted shares | 31.8 | 34.4 | 32.3 | 36.0 | |||||||||||

Basic and Diluted Per Share Data: | |||||||||||||||

Basic earnings (loss) per share attributable to Visteon: | |||||||||||||||

Continuing operations | $ | 1.38 | $ | 0.62 | $ | 4.50 | $ | 2.47 | |||||||

Discontinued operations | — | 0.21 | 0.25 | (0.42 | ) | ||||||||||

$ | 1.38 | $ | 0.83 | $ | 4.75 | $ | 2.05 | ||||||||

Diluted earnings (loss) per share attributable to Visteon: | |||||||||||||||

Continuing operations | $ | 1.35 | $ | 0.61 | $ | 4.43 | $ | 2.44 | |||||||

Discontinued operations | — | 0.20 | 0.25 | (0.41 | ) | ||||||||||

$ | 1.35 | $ | 0.81 | $ | 4.68 | $ | 2.03 | ||||||||

NOTE 16. Fair Value Measurements and Financial Instruments

Fair Value Measurements

The Company uses a three-level fair value hierarchy that categorizes assets and liabilities measured at fair value based on the observability of the inputs utilized in the valuation. The fair value hierarchy gives the highest priority to the quoted prices in active markets for identical assets and liabilities and lowest priority to unobservable inputs.

• | Level 1 – Financial assets and liabilities whose values are based on unadjusted quoted market prices for identical assets and liabilities in an active market that the Company has the ability to access. |

• | Level 2 – Financial assets and liabilities whose values are based on quoted prices in markets that are not active or model inputs that are observable for substantially the full term of the asset or liability. |

• | Level 3 – Financial assets and liabilities whose values are based on prices or valuation techniques that require inputs that are both unobservable and significant to the overall fair value measurement. |

Items Measured at Fair Value on a Nonrecurring Basis

Certain assets and liabilities are measured at fair value on a nonrecurring basis. The fair value measurements are generally determined using unobservable inputs and are classified within Level 3 of the fair value hierarchy. These assets include long-lived assets, intangible assets and investments in affiliates, which may be written down to fair value as a result of impairment. During the third quarter there were no items measured at fair value on a nonrecurring basis.

Items Not Carried at Fair Value

The Company's fair value of debt was approximately $397 million and $389 million as of September 30, 2017 and December 31, 2016, respectively. Fair value estimates were based on the current rates offered to the Company for debt of the same remaining maturities. Accordingly, the Company's debt fair value disclosures are classified as Level 2, "Other Observable Inputs" in the fair value hierarchy.

22

The Company is exposed to various market risks including, but not limited to, changes in currency exchange rates and market interest rates. The Company manages these risks, in part, through the use of derivative financial instruments. The maximum length of time over which the Company hedges the variability in the future cash flows related to transactions, excluding those transactions as related to the payment of variable interest on existing debt, is eighteen months. The maximum length of time over which the Company hedges forecasted transactions related to variable interest payments is the term of the underlying debt. The use of financial derivative instruments may pose risk of loss in the event of nonperformance by the transaction counter-party.

The Company presents its derivative positions and any related material collateral under master netting arrangements that provide for the net settlement of contracts, by counterparty, in the event of default or termination. Derivative financial instruments designated and non-designated as hedging instruments are included in the Company’s consolidated balance sheets. There is no cash collateral on any of these derivatives.

Items Measured at Fair Value on a Recurring Basis