Attached files

| file | filename |

|---|---|

| EX-10.3 - EXHIBIT 10.3 - MOLINA HEALTHCARE, INC. | waiverrelease-drmolinafinal.htm |

| EX-32.1 - EXHIBIT 32.1 - MOLINA HEALTHCARE, INC. | a6302017-10qex321.htm |

| EX-31.1 - EXHIBIT 31.1 - MOLINA HEALTHCARE, INC. | a6302017-10qex311.htm |

| EX-10.5 - EXHIBIT 10.5 - MOLINA HEALTHCARE, INC. | mohpurchaseagreement052220.htm |

| EX-10.4 - EXHIBIT 10.4 - MOLINA HEALTHCARE, INC. | waiverrelease-johnmolinafi.htm |

| EX-10.2 - EXHIBIT 10.2 - MOLINA HEALTHCARE, INC. | a2017amendedrestatedemploy.htm |

| EX-10.1 - EXHIBIT 10.1 - MOLINA HEALTHCARE, INC. | mohthirdamendmentcreditagr.htm |

| EX-4.2 - EXHIBIT 4.2 - MOLINA HEALTHCARE, INC. | moh330mindenture.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2017

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-31719

MOLINA HEALTHCARE, INC.

(Exact name of registrant as specified in its charter)

Delaware | 13-4204626 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

200 Oceangate, Suite 100 Long Beach, California | 90802 | |

(Address of principal executive offices) | (Zip Code) | |

(562) 435-3666

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ý | Accelerated filer | ¨ |

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Emerging growth company | ¨ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section13(a) of the Exchange Act. | |

¨ | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No ý

The number of shares of the issuer’s Common Stock, $0.001 par value, outstanding as of July 28, 2017, was approximately 57,118,000.

MOLINA HEALTHCARE, INC. FORM 10-Q

FOR THE QUARTERLY PERIOD ENDED June 30, 2017

TABLE OF CONTENTS

CROSS-REFERENCE INDEX

ITEM NUMBER | Page | |

PART I - Financial Information | ||

1. | ||

2. | ||

3. | ||

4. | ||

Part II - Other Information | ||

1. | ||

1A. | ||

2. | ||

3. | Defaults Upon Senior Securities | Not Applicable. |

4. | Mine Safety Disclosures | Not Applicable. |

5. | Other Information | Not Applicable. |

6. | ||

FINANCIAL STATEMENTS

MOLINA HEALTHCARE, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(In millions, except per-share data) (Unaudited) | |||||||||||||||

Revenue: | |||||||||||||||

Premium revenue | $ | 4,740 | $ | 4,029 | $ | 9,388 | $ | 8,024 | |||||||

Service revenue | 129 | 135 | 260 | 275 | |||||||||||

Premium tax revenue | 114 | 109 | 225 | 218 | |||||||||||

Health insurer fee revenue | — | 76 | — | 166 | |||||||||||

Investment income and other revenue | 16 | 10 | 30 | 19 | |||||||||||

Total revenue | 4,999 | 4,359 | 9,903 | 8,702 | |||||||||||

Operating expenses: | |||||||||||||||

Medical care costs | 4,491 | 3,594 | 8,602 | 7,182 | |||||||||||

Cost of service revenue | 124 | 116 | 246 | 243 | |||||||||||

General and administrative expenses | 405 | 351 | 844 | 691 | |||||||||||

Premium tax expenses | 114 | 109 | 225 | 218 | |||||||||||

Health insurer fee expenses | — | 50 | — | 108 | |||||||||||

Depreciation and amortization | 37 | 34 | 76 | 66 | |||||||||||

Impairment losses | 72 | — | 72 | — | |||||||||||

Restructuring and separation costs | 43 | — | 43 | — | |||||||||||

Total operating expenses | 5,286 | 4,254 | 10,108 | 8,508 | |||||||||||

Operating (loss) income | (287 | ) | 105 | (205 | ) | 194 | |||||||||

Other expenses (income), net: | |||||||||||||||

Interest expense | 27 | 25 | 53 | 50 | |||||||||||

Other income, net | — | — | (75 | ) | — | ||||||||||

Total other expenses (income), net | 27 | 25 | (22 | ) | 50 | ||||||||||

(Loss) income before income tax (benefit) expense | (314 | ) | 80 | (183 | ) | 144 | |||||||||

Income tax (benefit) expense | (84 | ) | 47 | (30 | ) | 87 | |||||||||

Net (loss) income | $ | (230 | ) | $ | 33 | $ | (153 | ) | $ | 57 | |||||

Net (loss) income per share: | |||||||||||||||

Basic | $ | (4.10 | ) | $ | 0.58 | $ | (2.74 | ) | $ | 1.02 | |||||

Diluted | $ | (4.10 | ) | $ | 0.58 | $ | (2.74 | ) | $ | 1.01 | |||||

CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) INCOME

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(Amounts in millions) (Unaudited) | |||||||||||||||

Net (loss) income | $ | (230 | ) | $ | 33 | $ | (153 | ) | $ | 57 | |||||

Other comprehensive income: | |||||||||||||||

Unrealized investment gain | — | 4 | 1 | 13 | |||||||||||

Less: effect of income taxes | — | 2 | — | 5 | |||||||||||

Other comprehensive income, net of tax | — | 2 | 1 | 8 | |||||||||||

Comprehensive (loss) income | $ | (230 | ) | $ | 35 | $ | (152 | ) | $ | 65 | |||||

See accompanying notes.

Molina Healthcare, Inc. 2017 Form 10-Q | 3

MOLINA HEALTHCARE, INC.

CONSOLIDATED BALANCE SHEETS

See accompanying notes.

June 30, 2017 | December 31, 2016 | ||||||

(Amounts in millions, except per-share data) | |||||||

(Unaudited) | |||||||

ASSETS | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 2,979 | $ | 2,819 | |||

Investments | 2,192 | 1,758 | |||||

Restricted investments | 325 | — | |||||

Receivables | 1,006 | 974 | |||||

Income taxes refundable | 68 | 39 | |||||

Prepaid expenses and other current assets | 159 | 131 | |||||

Derivative asset | 440 | 267 | |||||

Total current assets | 7,169 | 5,988 | |||||

Property, equipment, and capitalized software, net | 449 | 454 | |||||

Deferred contract costs | 93 | 86 | |||||

Intangible assets, net | 112 | 140 | |||||

Goodwill | 559 | 620 | |||||

Restricted investments | 118 | 110 | |||||

Deferred income taxes | 36 | 10 | |||||

Other assets | 47 | 41 | |||||

$ | 8,583 | $ | 7,449 | ||||

LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||

Current liabilities: | |||||||

Medical claims and benefits payable | $ | 2,077 | $ | 1,929 | |||

Amounts due government agencies | 1,844 | 1,202 | |||||

Accounts payable and accrued liabilities | 375 | 385 | |||||

Deferred revenue | 284 | 315 | |||||

Current portion of long-term debt | 773 | 472 | |||||

Derivative liability | 440 | 267 | |||||

Total current liabilities | 5,793 | 4,570 | |||||

Senior notes | 1,017 | 975 | |||||

Lease financing obligations | 198 | 198 | |||||

Deferred income taxes | — | 15 | |||||

Other long-term liabilities | 54 | 42 | |||||

Total liabilities | 7,062 | 5,800 | |||||

Stockholders’ equity: | |||||||

Common stock, $0.001 par value; 150 shares authorized; outstanding: 57 shares at June 30, 2017 and at December 31, 2016 | — | — | |||||

Preferred stock, $0.001 par value; 20 shares authorized, no shares issued and outstanding | — | — | |||||

Additional paid-in capital | 865 | 841 | |||||

Accumulated other comprehensive loss | (1 | ) | (2 | ) | |||

Retained earnings | 657 | 810 | |||||

Total stockholders’ equity | 1,521 | 1,649 | |||||

$ | 8,583 | $ | 7,449 | ||||

Molina Healthcare, Inc. 2017 Form 10-Q | 4

MOLINA HEALTHCARE, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

Six Months Ended June 30, | |||||||

2017 | 2016 | ||||||

(Amounts in millions) (Unaudited) | |||||||

Operating activities: | |||||||

Net (loss) income | $ | (153 | ) | $ | 57 | ||

Adjustments to reconcile net (loss) income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 96 | 89 | |||||

Impairment losses | 72 | — | |||||

Deferred income taxes | (41 | ) | 39 | ||||

Share-based compensation, including accelerated share-based compensation | 35 | 16 | |||||

Amortization of convertible senior notes and lease financing obligations | 16 | 15 | |||||

Other, net | 7 | 11 | |||||

Changes in operating assets and liabilities: | |||||||

Receivables | (32 | ) | (415 | ) | |||

Prepaid expenses and other assets | (38 | ) | (143 | ) | |||

Medical claims and benefits payable | 148 | 82 | |||||

Amounts due government agencies | 642 | 509 | |||||

Accounts payable and accrued liabilities | (18 | ) | 147 | ||||

Deferred revenue | (32 | ) | (119 | ) | |||

Income taxes | (30 | ) | (10 | ) | |||

Net cash provided by operating activities | 672 | 278 | |||||

Investing activities: | |||||||

Purchases of investments | (1,636 | ) | (974 | ) | |||

Proceeds from sales and maturities of investments | 874 | 812 | |||||

Purchases of property, equipment and capitalized software | (60 | ) | (102 | ) | |||

(Increase) decrease in restricted investments held-to-maturity | (10 | ) | 5 | ||||

Net cash paid in business combinations | — | (8 | ) | ||||

Other, net | (13 | ) | (6 | ) | |||

Net cash used in investing activities | (845 | ) | (273 | ) | |||

Financing activities: | |||||||

Proceeds from senior notes offering, net of issuance costs | 325 | — | |||||

Proceeds from employee stock plans | 11 | 10 | |||||

Other, net | (3 | ) | 1 | ||||

Net cash provided by financing activities | 333 | 11 | |||||

Net increase in cash and cash equivalents | 160 | 16 | |||||

Cash and cash equivalents at beginning of period | 2,819 | 2,329 | |||||

Cash and cash equivalents at end of period | $ | 2,979 | $ | 2,345 | |||

Molina Healthcare, Inc. 2017 Form 10-Q | 5

MOLINA HEALTHCARE, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(continued)

Six Months Ended June 30, | |||||||

2017 | 2016 | ||||||

(Amounts in millions) (Unaudited) | |||||||

Supplemental cash flow information: | |||||||

Schedule of non-cash investing and financing activities: | |||||||

Common stock used for share-based compensation | $ | (21 | ) | $ | (7 | ) | |

Details of change in fair value of derivatives, net: | |||||||

Gain (loss) on 1.125% Call Option | $ | 173 | $ | (148 | ) | ||

(Loss) gain on 1.125% Conversion Option | (173 | ) | 148 | ||||

Change in fair value of derivatives, net | $ | — | $ | — | |||

Details of business combinations: | |||||||

Fair value of assets acquired | $ | — | $ | (131 | ) | ||

Purchase price amounts accrued/received | — | 21 | |||||

Reversal of amounts advanced to sellers in prior year | — | 102 | |||||

Net cash paid in business combinations | $ | — | $ | (8 | ) | ||

See accompanying notes.

Molina Healthcare, Inc. 2017 Form 10-Q | 6

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

June 30, 2017

1. Basis of Presentation

Organization and Operations

Molina Healthcare, Inc. provides quality managed health care to people receiving government assistance. We offer cost-effective Medicaid-related solutions to meet the health care needs of low-income families and individuals, and to assist government agencies in their administration of the Medicaid program. We have three reportable segments. These segments consist of our Health Plans segment, which constitutes the vast majority of our operations; our Molina Medicaid Solutions segment; and our Other segment.

The Health Plans segment consists of health plans operating in 12 states and the Commonwealth of Puerto Rico, and includes our direct delivery business. As of June 30, 2017, these health plans served approximately 4.7 million members eligible for Medicaid, Medicare, and other government-sponsored health care programs for low-income families and individuals. This membership includes Affordable Care Act Marketplace (Marketplace) members, most of whom receive government premium subsidies. The health plans are operated by our respective wholly owned subsidiaries in those states, each of which is licensed as a health maintenance organization (HMO). Our direct delivery business consists primarily of the operation of primary care clinics in several states in which we operate.

Our health plans’ state Medicaid contracts generally have terms of three to four years. These contracts typically contain renewal options exercisable by the state Medicaid agency, and allow either the state or the health plan to terminate the contract with or without cause. Our health plan subsidiaries have generally been successful in retaining their contracts, but such contracts are subject to risk of loss when a state issues a new request for proposal (RFP) open to competitive bidding by other health plans. If one of our health plans is not a successful responsive bidder to a state RFP, its contract may be subject to non-renewal.

In addition to contract renewal, our state Medicaid contracts may be periodically amended to include or exclude certain health benefits (such as pharmacy services, behavioral health services, or long-term care services); populations such as the aged, blind or disabled (ABD); and regions or service areas.

The Molina Medicaid Solutions segment provides support to state government agencies in the administration of their Medicaid programs, including business processing, information technology development and administrative services.

The Other segment includes primarily our Pathways behavioral health and social services provider, and corporate amounts not allocated to other reportable segments.

Restructuring Plan

We recorded $43 million in restructuring and separation costs in the second quarter of 2017 related primarily to contractually required termination benefits paid to our former chief executive officer (CEO) and chief financial officer (CFO). Also included in these costs are consulting fees incurred for the development and implementation of our corporate restructuring initiatives. See Note 11, “Restructuring and Separation Costs.”

Recent Developments — Health Plans Segment

Direct Delivery. On August 2, 2017, we announced plans to restructure our direct delivery operations.

Mississippi Health Plan. In June 2017, Molina Healthcare of Mississippi, Inc. was awarded a Medicaid Coordinated Care Contract for the statewide administration of the Mississippi Coordinated Access Network (MississippiCAN). The contract begins July 1, 2017, for three years with options to renew annually for up to two additional years. The operational start date for the program is currently scheduled for July 1, 2018, pending the completion of a readiness review.

Washington Health Plan. In May 2017, Molina Healthcare of Washington, Inc. was selected by the Washington State Health Care Authority to negotiate and enter into managed care contracts for the North Central region of the state’s Apple Health Integrated Managed Care Program. The start date for the new contract is scheduled for January 1, 2018.

Molina Healthcare, Inc. 2017 Form 10-Q | 7

Terminated Medicare Acquisition. In August 2016, we entered into agreements with each of Aetna Inc. and Humana Inc. to acquire certain assets related to their Medicare Advantage business. The transaction was subject to closing conditions including the completion of the proposed acquisition of Humana by Aetna (the Aetna-Humana Merger). In January 2017, the U.S. District Court for the District of Columbia granted the request for relief made by the U.S. Department of Justice in its civil antitrust lawsuit against Aetna and Humana, to prohibit the Aetna-Humana Merger. In February 2017, our agreements with each of Aetna and Humana were terminated by the parties pursuant to the terms of the agreements. Under the termination agreements, we received an aggregate termination fee of $75 million from Aetna and Humana in the first quarter of 2017, which is reported in “Other income, net.”

New York Health Plan. In August 2016, we closed on our acquisition of the outstanding equity interests of Today’s Options of New York, Inc., which now operates as Molina Healthcare of New York, Inc. The purchase price allocation was completed, and the final purchase price adjustments were recorded, in the first quarter of 2017. Such adjustments were insignificant, and the final purchase price was $38 million.

Recent Developments — Other Segment

Pathways subsidiary. In the second quarter of 2017, we recorded non-cash goodwill and intangible assets impairment losses of $72 million, related primarily to our Pathways subsidiary. See Note 10, “Impairment Losses.”

Consolidation and Interim Financial Information

The consolidated financial statements include the accounts of Molina Healthcare, Inc., its subsidiaries, and variable interest entities (VIEs) in which Molina Healthcare, Inc. is considered to be the primary beneficiary. Such VIEs are insignificant to our consolidated financial position and results of operations. In the opinion of management, all adjustments considered necessary for a fair presentation of the results as of the date and for the interim periods presented have been included; such adjustments consist of normal recurring adjustments. All significant intercompany balances and transactions have been eliminated. The consolidated results of operations for the current interim period are not necessarily indicative of the results for the entire year ending December 31, 2017.

The unaudited consolidated interim financial statements have been prepared under the assumption that users of the interim financial data have either read or have access to our audited consolidated financial statements for the fiscal year ended December 31, 2016. Accordingly, certain disclosures that would substantially duplicate the disclosures contained in the December 31, 2016 audited consolidated financial statements have been omitted. These unaudited consolidated interim financial statements should be read in conjunction with our December 31, 2016 audited consolidated financial statements.

2. Significant Accounting Policies

Certain of our significant accounting policies are discussed within the note to which they specifically relate.

Revenue Recognition – Health Plans Segment

Premium revenue is fixed in advance of the periods covered and, except as described below, is not generally subject to significant accounting estimates. Premium revenues are recognized in the month that members are entitled to receive health care services, and premiums collected in advance are deferred. Certain components of premium revenue are subject to accounting estimates and fall into two broad categories discussed in further detail below: 1) “Contractual Provisions That May Adjust or Limit Revenue or Profit;” and 2) “Quality Incentives.”

Contractual Provisions That May Adjust or Limit Revenue or Profit

Medicaid

Medical Cost Floors (Minimums), and Medical Cost Corridors: A portion of our premium revenue may be returned if certain minimum amounts are not spent on defined medical care costs. In the aggregate, we recorded a liability under the terms of such contract provisions of $136 million and $272 million at June 30, 2017 and December 31, 2016, respectively, to “Amounts due government agencies.” Approximately $114 million and $244 million of the liability accrued at June 30, 2017 and December 31, 2016, respectively, relates to our participation in Medicaid Expansion programs.

In certain circumstances, our health plans may receive additional premiums if amounts spent on medical care costs exceed a defined maximum threshold. Receivables relating to such provisions were insignificant at June 30, 2017 and December 31, 2016.

Molina Healthcare, Inc. 2017 Form 10-Q | 8

Profit Sharing and Profit Ceiling: Our contracts with certain states contain profit-sharing or profit ceiling provisions under which we refund amounts to the states if our health plans generate profit above a certain specified percentage. In some cases, we are limited in the amount of administrative costs that we may deduct in calculating the refund, if any. Liabilities for profits in excess of the amount we are allowed to retain under these provisions were insignificant at June 30, 2017 and December 31, 2016.

Retroactive Premium Adjustments: State Medicaid programs periodically adjust premium rates on a retroactive basis. In these cases, we must adjust our premium revenue in the period in which we learn of the adjustment, rather than in the months of service to which the retroactive adjustment applies.

Medicare

Risk Adjustment: Our Medicare premiums are subject to retroactive increase or decrease based on the health status of our Medicare members (measured as a member risk score). We estimate our members’ risk scores and the related amount of Medicare revenue that will ultimately be realized for the periods presented based on our knowledge of our members’ health status, risk scores and Centers for Medicare & Medicaid Services (CMS) practices. Consolidated balance sheet amounts related to anticipated Medicare risk adjustment premiums and Medicare Part D settlements were insignificant at June 30, 2017 and December 31, 2016.

Minimum MLR: Additionally, federal regulations have established a minimum annual medical loss ratio (Minimum MLR) of 85% for Medicare. The medical loss ratio represents medical costs as a percentage of premium revenue. Federal regulations define what constitutes medical costs and premium revenue. If the Minimum MLR is not met, we may be required to pay rebates to the federal government. We recognize estimated rebates under the Minimum MLR as an adjustment to premium revenue in our consolidated statements of operations.

Marketplace

Premium Stabilization Programs: The Affordable Care Act (ACA) established Marketplace premium stabilization programs effective January 1, 2014. These programs, commonly referred to as the “3R’s,” include a permanent risk adjustment program, a transitional reinsurance program, and a temporary risk corridor program. We record receivables or payables related to the 3R programs and the Minimum MLR when the amounts are reasonably estimable as described below, and, for receivables, when collection is reasonably assured. Our receivables (payables) for each of these programs, as of the dates indicated, were as follows:

June 30, 2017 | December 31, 2016 | ||||||||||||||

Current Benefit Year | Prior Benefit Years | Total | |||||||||||||

(In millions) | |||||||||||||||

Risk adjustment | $ | (502 | ) | $ | (546 | ) | $ | (1,048 | ) | $ | (522 | ) | |||

Reinsurance | — | 57 | 57 | 55 | |||||||||||

Risk corridor | — | (1 | ) | (1 | ) | (1 | ) | ||||||||

Minimum MLR | (3 | ) | (2 | ) | (5 | ) | (1 | ) | |||||||

• | Risk adjustment: Under this permanent program, our health plans’ composite risk scores are compared with the overall average risk score for the relevant state and market pool. Generally, our health plans will make a risk transfer payment into the pool if their composite risk scores are below the average risk score, and will receive a risk transfer payment from the pool if their composite risk scores are above the average risk score. We estimate our ultimate premium based on insurance policy year-to-date experience, and recognize estimated premiums relating to the risk adjustment program as an adjustment to premium revenue in our consolidated statements of operations. |

• | Reinsurance: This program was designed to provide reimbursement to insurers for high cost members and ended December 31, 2016; we expect to settle the outstanding receivable balance in 2017. |

• | Risk corridor: This program was intended to limit gains and losses of insurers by comparing allowable costs to a target amount as defined by CMS, and ended December 31, 2016; we expect to settle the outstanding payable balance in 2017. |

Additionally, the ACA established a Minimum MLR of 80% for the Marketplace. The medical loss ratio represents medical costs as a percentage of premium revenue. Federal regulations define what constitutes medical costs and premium revenue. If the Minimum MLR is not met, we may be required to pay rebates to our Marketplace policyholders. Each of the 3R programs is taken into consideration when computing the Minimum MLR. We

Molina Healthcare, Inc. 2017 Form 10-Q | 9

recognize estimated rebates under the Minimum MLR as an adjustment to premium revenue in our consolidated statements of operations.

Quality Incentives

At several of our health plans, revenue ranging from approximately 1% to 3% of certain health plan premiums is earned only if certain performance measures are met.

The following table quantifies the quality incentive premium revenue recognized for the periods presented, including the amounts earned in the periods presented and prior periods. Although the reasonably possible effects of a change in estimate related to quality incentive premium revenue as of June 30, 2017 are not known, we have no reason to believe that the adjustments to prior years noted below are not indicative of the potential future changes in our estimates as of June 30, 2017.

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(Dollars in millions) | |||||||||||||||

Maximum available quality incentive premium - current period | $ | 39 | $ | 41 | $ | 77 | $ | 81 | |||||||

Quality incentive premium revenue recognized in current period: | |||||||||||||||

Earned current period | $ | 29 | $ | 36 | $ | 48 | $ | 54 | |||||||

Earned prior periods | 1 | 49 | 6 | 54 | |||||||||||

Total | $ | 30 | $ | 85 | $ | 54 | 108 | ||||||||

Quality incentive premium revenue recognized as a percentage of total premium revenue | 0.6 | % | 2.1 | % | 0.6 | % | 1.3 | % | |||||||

Income Taxes

The provision for income taxes is determined using an estimated annual effective tax rate, which generally differs from the U.S. federal statutory rate primarily because of state taxes, nondeductible expenses such as the Health Insurer Fee (HIF), goodwill impairment, certain compensation, and other general and administrative expenses. The effective tax rate was not impacted by HIF in 2017 given the 2017 HIF moratorium.

The effective tax rate may be subject to fluctuations during the year, particularly as a result of the level of pretax earnings, and also as new information is obtained. Such information may affect the assumptions used to estimate the annual effective tax rate, including factors such as the mix of pretax earnings in the various tax jurisdictions in which we operate, valuation allowances against deferred tax assets, the recognition or the reversal of the recognition of tax benefits related to uncertain tax positions, and changes in or the interpretation of tax laws in jurisdictions where we conduct business. We recognize deferred tax assets and liabilities for temporary differences between the financial reporting basis and the tax basis of our assets and liabilities, along with net operating loss and tax credit carryovers.

Premium Deficiency Reserves on Loss Contracts

We assess the profitability of our medical care policies to identify groups of contracts where current operating results or forecasts indicate probable future losses. If anticipated future variable costs exceed anticipated future premiums and investment income, a premium deficiency reserve is recognized. We recorded a premium deficiency reserve to “Medical claims and benefits payable” on our accompanying consolidated balance sheets relating to our Marketplace program of $30 million as of December 31, 2016, which increased to $100 million as of June 30, 2017.

Recent Accounting Pronouncements

Goodwill Impairment. In January 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-04, Simplifying the Test for Goodwill Impairment, which eliminates the requirement to calculate the implied fair value of goodwill to measure a goodwill impairment loss. Instead, an impairment loss is measured as the excess of the carrying amount of the reporting unit, including goodwill, over the fair value of the reporting unit. ASU 2017-04 is effective beginning January 1, 2020; we have early adopted ASU 2017-04 as of June 30, 2017, in connection with the assessment of our Pathways subsidiary. See further discussion at Note 10, “Impairment Losses.”

Restricted Cash. In November 2016, the FASB issued ASU 2016-18, Restricted Cash, which will require us to include in our consolidated statements of cash flows the balances of cash, cash equivalents, restricted cash and

Molina Healthcare, Inc. 2017 Form 10-Q | 10

restricted cash equivalents. When these items are presented in more than one line item on the balance sheet, the new guidance requires a reconciliation of the totals in the statement of cash flows to the related captions in the balance sheet. Transfers between cash and cash equivalents and restricted cash and restricted cash equivalents will no longer be presented in the statement of cash flows. ASU 2016-18 is effective beginning January 1, 2018; early adoption is permitted. We intend to early adopt ASU 2016-18 as of December 31, 2017, and are currently evaluating the effect to our consolidated statements of cash flows.

Stock Compensation. In March 2016, the FASB issued ASU 2016-09, Improvements to Employee Share-Based Payment Accounting, which amends ASC Topic 718, Compensation – Stock Compensation. ASU 2016-09 simplifies several aspects of accounting for employee share-based payment transactions, including the accounting for income taxes, forfeitures, statutory tax and classification in the statement of cash flows. We adopted ASU 2016-09 in the first quarter of 2017; such adoption did not significantly impact our consolidated financial statements. In addition, the prior period presentation in the statement of cash flows was not adjusted because such adjustments were insignificant.

Leases. In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842), as modified by ASU 2017-03, Transition and Open Effective Date Information. Under ASU 2016-02, an entity will be required to recognize assets and liabilities for the rights and obligations created by leases on the entity’s balance sheet for both finance and operating leases. For leases with a term of 12 months or less, an entity can elect to not recognize lease assets and lease liabilities and expense the lease over a straight-line basis for the term of the lease. ASU 2016-02 will require new disclosures that depict the amount, timing, and uncertainty of cash flows pertaining to an entity’s leases. ASU 2016-02 is effective for us beginning January 1, 2019, and must be adopted using a modified retrospective approach for annual and interim periods beginning after December 15, 2018. Early adoption is permitted. Under this guidance, we will record assets and liabilities relating primarily to our long-term office leases, and are currently evaluating the effect to our consolidated financial statements.

Revenue Recognition. In May 2014, the FASB issued ASU 2014-09, Revenue from Contracts with Customers (Topic 606). We intend to adopt this standard and the related modifications on January 1, 2018, using the modified retrospective approach. Under this approach, the cumulative effect of initially applying the guidance will be reflected as an adjustment to beginning retained earnings.

We have determined that the insurance contracts of our Health Plans segment, which comprises the majority of our operations, are excluded from the scope of ASU 2014-09 because the recognition of revenue under these contracts is dictated by other accounting standards governing insurance contracts.

For our Molina Medicaid Solutions segment, we have determined that certain service revenue and cost of service revenue will no longer be deferred and recognized over the service delivery period. Rather, service revenue will be recognized based on the expected cost plus gross margin method, and cost of service revenue will be recognized as incurred. As of June 30, 2017, we expect the cumulative adjustment for historical periods through June 30, 2017 to increase retained earnings by no more than $50 million. This estimate will be updated in each quarterly and annual report until adoption. We expect the cumulative adjustment, if any, relating to our Other segment to be insignificant.

Other recent accounting pronouncements issued by the FASB (including its Emerging Issues Task Force), the American Institute of Certified Public Accountants, and the Securities and Exchange Commission (SEC) did not have, or are not believed by management to have, a significant impact on our present or future consolidated financial statements.

Molina Healthcare, Inc. 2017 Form 10-Q | 11

3. Net (Loss) Income per Share

The following table sets forth the calculation of basic and diluted net (loss) income per share:

______________________________

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

(In millions, except net income per share) | |||||||||||||||

Numerator: | |||||||||||||||

Net (loss) income | $ | (230 | ) | $ | 33 | $ | (153 | ) | $ | 57 | |||||

Denominator: | |||||||||||||||

Denominator for basic net (loss) income per share | 56 | 55 | 56 | 55 | |||||||||||

Effect of dilutive securities: | |||||||||||||||

1.125% Warrants (1) | — | — | — | 1 | |||||||||||

Denominator for diluted net (loss) income per share | 56 | 55 | 56 | 56 | |||||||||||

Net (loss) income per share: (2) | |||||||||||||||

Basic | $ | (4.10 | ) | $ | 0.58 | $ | (2.74 | ) | $ | 1.02 | |||||

Diluted | $ | (4.10 | ) | $ | 0.58 | $ | (2.74 | ) | $ | 1.01 | |||||

Potentially dilutive common shares excluded from calculations: | |||||||||||||||

1.125% Warrants (1) | 2 | — | 1 | — | |||||||||||

(1) | For more information regarding the 1.125% Warrants, refer to Note 9, “Stockholders' Equity.” The dilutive effect of all potentially dilutive common shares is calculated using the treasury-stock method. Certain potentially dilutive common shares issuable are not included in the computation of diluted net (loss) income per share because to do so would be anti-dilutive. For the three and six months ended June 30, 2017, the 1.125% Warrants were excluded from diluted shares outstanding because to do so would have been anti-dilutive. |

(2) | Source data for calculations in thousands. |

4. Fair Value Measurements

We consider the carrying amounts of cash and cash equivalents and other current assets and current liabilities (not including derivatives and the current portion of long-term debt) to approximate their fair values because of the relatively short period of time between the origination of these instruments and their expected realization or payment. For our financial instruments measured at fair value on a recurring basis, we prioritize the inputs used in measuring fair value according to a three-tier fair value hierarchy defined by GAAP. For a description of the methods and assumptions that we use to a) estimate the fair value; and b) determine the classification according to the fair value hierarchy for each financial instrument, see Note 5, “Fair Value Measurements,” in our 2016 Annual Report on Form 10-K.

Derivative financial instruments include the 1.125% Call Option derivative asset and the 1.125% Conversion Option derivative liability. These derivatives are not actively traded and are valued based on an option pricing model that uses observable and unobservable market data for inputs. Significant market data inputs used to determine fair value as of June 30, 2017 included the price of our common stock, the time to maturity of the derivative instruments, the risk-free interest rate, and the implied volatility of our common stock. As described further in Note 8, “Derivatives,” the 1.125% Call Option asset and the 1.125% Conversion Option liability were designed such that changes in their fair values would offset, with minimal impact to the consolidated statements of operations. Therefore, the sensitivity of changes in the unobservable inputs to the option pricing model for such instruments is mitigated.

The net changes in fair value of Level 3 financial instruments were insignificant to our results of operations for the six months ended June 30, 2017.

Molina Healthcare, Inc. 2017 Form 10-Q | 12

Our financial instruments measured at fair value on a recurring basis at June 30, 2017, were as follows:

Total | Quoted Market Prices (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | ||||||||||||

(In millions) | |||||||||||||||

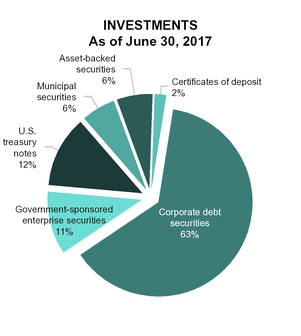

Corporate debt securities | $ | 1,386 | $ | — | $ | 1,386 | $ | — | |||||||

U.S. treasury notes | 263 | 263 | — | — | |||||||||||

Government-sponsored enterprise securities (GSEs) | 241 | 241 | — | — | |||||||||||

Municipal securities | 140 | — | 140 | — | |||||||||||

Asset-backed securities | 128 | — | 128 | — | |||||||||||

Certificates of deposit | 34 | — | 34 | — | |||||||||||

Subtotal - current investments | 2,192 | 504 | 1,688 | — | |||||||||||

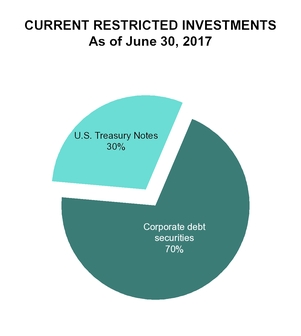

Corporate debt securities | 228 | — | 228 | — | |||||||||||

U.S. treasury notes | 97 | 97 | — | — | |||||||||||

Subtotal - current restricted investments | 325 | 97 | 228 | — | |||||||||||

1.125% Call Option derivative asset | 440 | — | — | 440 | |||||||||||

Total assets | $ | 2,957 | $ | 601 | $ | 1,916 | $ | 440 | |||||||

1.125% Conversion Option derivative liability | $ | 440 | $ | — | $ | — | $ | 440 | |||||||

Total liabilities | $ | 440 | $ | — | $ | — | $ | 440 | |||||||

Our financial instruments measured at fair value on a recurring basis at December 31, 2016, were as follows:

Total | Quoted Market Prices (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | ||||||||||||

(In millions) | |||||||||||||||

Corporate debt securities | $ | 1,179 | $ | — | $ | 1,179 | $ | — | |||||||

U.S. treasury notes | 84 | 84 | — | — | |||||||||||

GSEs | 231 | 231 | — | — | |||||||||||

Municipal securities | 142 | — | 142 | — | |||||||||||

Asset-backed securities | 69 | — | 69 | — | |||||||||||

Certificates of deposit | 53 | — | 53 | — | |||||||||||

Subtotal - current investments | 1,758 | 315 | 1,443 | — | |||||||||||

1.125% Call Option derivative asset | 267 | — | — | 267 | |||||||||||

Total assets | $ | 2,025 | $ | 315 | $ | 1,443 | $ | 267 | |||||||

1.125% Conversion Option derivative liability | $ | 267 | $ | — | $ | — | $ | 267 | |||||||

Total liabilities | $ | 267 | $ | — | $ | — | $ | 267 | |||||||

There were no current restricted investments as of December 31, 2016.

Molina Healthcare, Inc. 2017 Form 10-Q | 13

Fair Value Measurements – Disclosure Only

The carrying amounts and estimated fair values of our senior notes, which are classified as Level 2 financial instruments, are indicated in the following table.

June 30, 2017 | December 31, 2016 | ||||||||||||||

Carrying Value | Fair Value | Carrying Value | Fair Value | ||||||||||||

(In millions) | |||||||||||||||

5.375% Notes | $ | 692 | $ | 745 | $ | 691 | $ | 714 | |||||||

1.125% Convertible Notes | 483 | 976 | 471 | 792 | |||||||||||

4.875% Notes | 325 | 333 | — | — | |||||||||||

1.625% Convertible Notes | 289 | 386 | 284 | 344 | |||||||||||

$ | 1,789 | $ | 2,440 | $ | 1,446 | $ | 1,850 | ||||||||

5. Investments

Available-for-Sale Investments

We consider all of our investments classified as current assets (including restricted investments) to be available-for-sale. Certain of our senior notes, as further discussed in Note 7, “Debt,” contain a limitation on the use of proceeds which required us to deposit the net proceeds from their issuance into a segregated deposit account, a current asset reported as “Restricted investments” in the accompanying consolidated balance sheets. Such proceeds, while restricted as to their use and held in a segregated deposit account, are available-for-sale based upon our contractual liquidity requirements.

The following tables summarize our investments as of the dates indicated:

June 30, 2017 | |||||||||||||||

Amortized | Gross Unrealized | Estimated Fair | |||||||||||||

Cost | Gains | Losses | Value | ||||||||||||

(In millions) | |||||||||||||||

Corporate debt securities | $ | 1,387 | $ | 1 | $ | 2 | $ | 1,386 | |||||||

U.S. treasury notes | 263 | — | — | 263 | |||||||||||

GSEs | 242 | — | 1 | 241 | |||||||||||

Municipal securities | 140 | — | — | 140 | |||||||||||

Asset-backed securities | 128 | — | — | 128 | |||||||||||

Certificates of deposit | 34 | — | — | 34 | |||||||||||

Subtotal - current investments | 2,194 | 1 | 3 | 2,192 | |||||||||||

Corporate debt securities | 227 | 1 | — | 228 | |||||||||||

U.S. treasury notes | 97 | — | — | 97 | |||||||||||

Subtotal - current restricted investments | 324 | 1 | — | 325 | |||||||||||

Total | $ | 2,518 | $ | 2 | $ | 3 | $ | 2,517 | |||||||

December 31, 2016 | |||||||||||||||

Amortized | Gross Unrealized | Estimated Fair | |||||||||||||

Cost | Gains | Losses | Value | ||||||||||||

(In millions) | |||||||||||||||

Corporate debt securities | $ | 1,180 | $ | 1 | $ | 2 | $ | 1,179 | |||||||

U.S. treasury notes | 84 | — | — | 84 | |||||||||||

GSEs | 232 | — | 1 | 231 | |||||||||||

Municipal securities | 143 | — | 1 | 142 | |||||||||||

Asset-backed securities | 69 | — | — | 69 | |||||||||||

Certificates of deposit | 53 | — | — | 53 | |||||||||||

Total - current investments | $ | 1,761 | $ | 1 | $ | 4 | $ | 1,758 | |||||||

There were no current restricted investments as of December 31, 2016.

Molina Healthcare, Inc. 2017 Form 10-Q | 14

The contractual maturities of our available-for-sale investments as of June 30, 2017 are summarized below:

Amortized Cost | Estimated Fair Value | ||||||

(In millions) | |||||||

Due in one year or less | $ | 1,301 | $ | 1,301 | |||

Due after one year through five years | 1,194 | 1,193 | |||||

Due after five years through ten years | 23 | 23 | |||||

Total | $ | 2,518 | $ | 2,517 | |||

Gross realized gains and losses from sales of available-for-sale securities are calculated under the specific identification method and are included in investment income. Gross realized investment gains and losses for the three and six months ended June 30, 2017 and 2016 were insignificant.

We have determined that unrealized losses at June 30, 2017 and December 31, 2016, are temporary in nature, because the change in market value for these securities has resulted from fluctuating interest rates, rather than a deterioration of the credit worthiness of the issuers. So long as we maintain the intent and ability to hold these securities to maturity, we are unlikely to experience losses. In the event that we dispose of these securities before maturity, we expect that realized losses, if any, will be insignificant.

The following table segregates those available-for-sale investments that have been in a continuous loss position for less than 12 months, and those that have been in a loss position for 12 months or more as of June 30, 2017:

In a Continuous Loss Position for Less than 12 Months | In a Continuous Loss Position for 12 Months or More | ||||||||||||||||||||

Estimated Fair Value | Unrealized Losses | Total Number of Positions | Estimated Fair Value | Unrealized Losses | Total Number of Positions | ||||||||||||||||

(Dollars in millions) | |||||||||||||||||||||

Corporate debt securities | $ | 913 | $ | 2 | 418 | $ | — | $ | — | — | |||||||||||

GSEs | 247 | 1 | 101 | — | — | — | |||||||||||||||

Total - current investments | $ | 1,160 | $ | 3 | 519 | $ | — | $ | — | — | |||||||||||

The following table segregates those available-for-sale investments that have been in a continuous loss position for less than 12 months, and those that have been in a loss position for 12 months or more as of December 31, 2016:

In a Continuous Loss Position for Less than 12 Months | In a Continuous Loss Position for 12 Months or More | ||||||||||||||||||||

Estimated Fair Value | Unrealized Losses | Total Number of Positions | Estimated Fair Value | Unrealized Losses | Total Number of Positions | ||||||||||||||||

(Dollars in millions) | |||||||||||||||||||||

Corporate debt securities | $ | 542 | $ | 2 | 378 | $ | — | $ | — | — | |||||||||||

GSEs | 198 | 1 | 73 | — | — | — | |||||||||||||||

Municipal securities | 101 | 1 | 129 | — | — | — | |||||||||||||||

Total - current investments | $ | 841 | $ | 4 | 580 | $ | — | $ | — | — | |||||||||||

Held-to-Maturity Investments

Pursuant to the regulations governing our Health Plans segment subsidiaries, we maintain statutory deposits and deposits required by government authorities primarily in certificates of deposit and U.S. treasury securities. We also maintain restricted investments as protection against the insolvency of certain capitated providers. The use of these funds is limited as required by regulation in the various states in which we operate, or as needed in the event of insolvency of capitated providers. Therefore, such investments are reported as non-current “Restricted investments” in the accompanying consolidated balance sheet. We have the ability to hold these restricted investments until maturity, and as a result, we would not expect the value of these investments to decline significantly due to a sudden change in market interest rates.

Molina Healthcare, Inc. 2017 Form 10-Q | 15

The contractual maturities of our held-to-maturity restricted investments, which are carried at amortized cost, which approximates fair value, as of June 30, 2017 are summarized below:

Amortized Cost | Estimated Fair Value | ||||||

(In millions) | |||||||

Due in one year or less | $ | 100 | $ | 100 | |||

Due after one year through five years | 18 | 17 | |||||

$ | 118 | $ | 117 | ||||

6. Medical Claims and Benefits Payable

The following table provides the details of our medical claims and benefits payable (including amounts payable for the provision of long-term services and supports, or LTSS) as of the dates indicated.

June 30, 2017 | December 31, 2016 | ||||||

(In millions) | |||||||

Fee-for-service claims incurred but not paid (IBNP) | $ | 1,478 | $ | 1,352 | |||

Pharmacy payable | 121 | 112 | |||||

Capitation payable | 45 | 37 | |||||

Other | 433 | 428 | |||||

$ | 2,077 | $ | 1,929 | ||||

“Other” medical claims and benefits payable include amounts payable to certain providers for which we act as an intermediary on behalf of various government agencies without assuming financial risk. Such receipts and payments do not impact our consolidated statements of operations. Non-risk provider payables amounted to $111 million and $225 million as of June 30, 2017 and December 31, 2016, respectively.

Reinsurance recoverables of $65 million and $83 million as of June 30, 2017 and 2016, respectively, are included in “Receivables” in the accompanying consolidated balance sheets.

The following table presents the components of the change in our medical claims and benefits payable for the periods indicated. The amounts presented for “Components of medical care costs related to: Prior periods” represent the amount by which our original estimate of medical claims and benefits payable at the beginning of the period were more than the actual amount of the liability based on information (principally the payment of claims) developed since that liability was first reported.

Molina Healthcare, Inc. 2017 Form 10-Q | 16

Six Months Ended June 30, | |||||||

2017 | 2016 | ||||||

(Dollars in millions) | |||||||

Medical claims and benefits payable, beginning balance | $ | 1,929 | $ | 1,685 | |||

Components of medical care costs related to: | |||||||

Current period | 8,633 | 7,371 | |||||

Prior periods | (31 | ) | (189 | ) | |||

Total medical care costs | 8,602 | 7,182 | |||||

Change in non-risk provider payables | (114 | ) | 24 | ||||

Payments for medical care costs related to: | |||||||

Current period | 6,883 | 5,885 | |||||

Prior periods | 1,457 | 1,240 | |||||

Total paid | 8,340 | 7,125 | |||||

Medical claims and benefits payable, ending balance | $ | 2,077 | $ | 1,766 | |||

Benefit from prior period as a percentage of: | |||||||

Balance at beginning of period | 1.6 | % | 11.3 | % | |||

Premium revenue, trailing twelve months | 0.2 | % | 1.3 | % | |||

Medical care costs, trailing twelve months | 0.2 | % | 1.4 | % | |||

Assuming that our initial estimate of IBNP is accurate, we believe that amounts ultimately paid would generally be between 8% and 10% less than the IBNP liability recorded at the end of the period as a result of the inclusion in that liability of the provision for adverse claims deviation and the accrued cost of settling those claims. Because the amount of our initial liability is merely an estimate (and therefore not perfectly accurate), we will always experience variability in that estimate as new information becomes available with the passage of time. Therefore, there can be no assurance that amounts ultimately paid out will fall within the range of 8% to 10% lower than the liability that was initially recorded. Furthermore, because our initial estimate of IBNP is derived from many factors, some of which are qualitative in nature rather than quantitative, we are seldom able to assign specific values to the reasons for a change in estimate—we only know when the circumstances for any one or more factors are out of the ordinary.

As indicated in the table above, the amounts ultimately paid out on our medical claims and benefits payable liabilities in fiscal years 2017 and 2016 were less than what we had expected when we had established those liabilities. The differences between our original estimates and the amounts ultimately paid out (or now expected to be ultimately paid out) for the most part related to IBNP. While many related factors working in conjunction with one another serve to determine the accuracy of our estimates, we are seldom able to quantify the impact that any single factor has on a change in estimate. In addition, given the variability inherent in the reserving process, we will only be able to identify specific factors if they represent a significant departure from expectations. As a result, we do not expect to be able to fully quantify the impact of individual factors on changes in estimates.

While prior period development of our estimate as of December 31, 2016, through June 30, 2017, was favorable by $31 million, that amount is substantially less than the favorable prior period development of $189 million we recognized for the same period in the prior year. Further, favorable development through June 30, 2017, was less than the 8% to 10% we typically expect.

We believe that the most significant uncertainties surrounding our IBNP estimates at June 30, 2017 are as follows:

• | In the first half of 2017, our Marketplace enrollment across all health plans increased by over 400,000 members. Due to limited insight into the cost patterns associated with this large number of new Marketplace members, our liability estimates for these members are subject to more than the usual amount of uncertainty. |

• | At our Florida health plan, claims receipts increased significantly over the last few months due to an increase in the receipt of secondary claims, many of which are not our liability. These claims will either be denied or will have very small paid amounts. For this reason, claims denial rates, amounts paid per claim and other claims indicators will be impacted, making our liability estimates subject to more than the usual amount of uncertainty. |

Molina Healthcare, Inc. 2017 Form 10-Q | 17

• | At our Illinois health plan, we paid a large number of claims in the first half of 2017 that had previously been denied and were subsequently disputed by providers. This has created some distortion in the claims payment patterns, making our liability estimates subject to more than the usual amount of uncertainty. |

• | At our California health plan, we adjusted our inpatient authorization process. As a result, due to the expected increase in authorized inpatient stays, our liability estimates are subject to more than the usual amount of uncertainty. |

• | At our New Mexico health plan, a fee schedule reduction for a large provider has created some distortion in the claims payment patterns, making our liability estimates subject to more than the usual amount of uncertainty. |

7. Debt

Substantially all of our debt is held at the parent, which is reported in the Other segment. The following table summarizes our outstanding debt obligations and their classification in the accompanying consolidated balance sheets (in millions):

June 30, 2017 | December 31, 2016 | ||||||

Current portion of long-term debt: | |||||||

1.125% Convertible Notes, net of unamortized discount | $ | 488 | $ | 477 | |||

1.625% Convertible Notes, net of unamortized premium and discount | 291 | — | |||||

Lease financing obligations | 1 | 1 | |||||

Debt issuance costs | (7 | ) | (6 | ) | |||

773 | 472 | ||||||

Non-current portion of long-term debt, reported as “Senior notes”: | |||||||

5.375% Notes | 700 | 700 | |||||

4.875% Notes | 330 | — | |||||

1.625% Convertible Notes, net of unamortized premium and discount | — | 286 | |||||

Debt issuance costs | (13 | ) | (11 | ) | |||

1,017 | 975 | ||||||

Lease financing obligations | 198 | 198 | |||||

$ | 1,988 | $ | 1,645 | ||||

4.875% Notes due 2025

On June 6, 2017, we completed the private offering of $330 million aggregate principal amount of senior notes (4.875% Notes) due June 15, 2025, unless earlier redeemed. Interest on the 4.875% Notes is payable semiannually in arrears on June 15 and December 15. According to their terms, the guarantees under the 4.875% Notes mirror those of the Credit Facility, defined and described below. See Note 16, “Supplemental Condensed Consolidating Financial Information,” for more information on the guarantors. The 4.875% Notes contain customary non-financial covenants and change of control provisions.

The 4.875% Notes contain a limitation on the use of proceeds which required us to deposit the net proceeds from their issuance into a segregated deposit account, a current asset reported as “Restricted investments” in our consolidated balance sheets. These funds may be used by us as follows:

• | On or prior to August 20, 2018, to: |

◦ | Redeem, repurchase, repay, tender for, or acquire for value all or any portion of our 1.625% Convertible Notes, defined and discussed further below, or to satisfy the cash portion of any consideration due upon any conversion of the 1.625% Convertible Notes; and/or |

◦ | Pay any interest due on all or any portion of the 4.875% Notes. |

• | On or after August 20, 2018, to repurchase all or any portion of the 1.625% Convertible Notes that we are obligated to repurchase; and |

Molina Healthcare, Inc. 2017 Form 10-Q | 18

• | Subsequent to August 20, 2018 (or such earlier date in the event that there are no longer any 1.625% Convertible Notes outstanding), in any other manner not otherwise prohibited in the indenture governing the 4.875% Notes. |

5.375% Notes due 2022

We have outstanding $700 million aggregate principal amount of senior notes (5.375% Notes) due November 15, 2022, unless earlier redeemed. According to their terms, the guarantees under the 5.375% Notes mirror those of the Credit Facility, defined and described below. See Note 16, “Supplemental Condensed Consolidating Financial Information,” for more information on the guarantors.

Credit Facility

In January 2017, we entered into an amended unsecured $500 million revolving credit facility (Credit Facility), referred to as the First Amendment. As of June 30, 2017, outstanding letters of credit amounting to $6 million reduced our borrowing capacity under the Credit Facility to $494 million. The Credit Facility has a term of five years and all amounts outstanding will be due and payable on January 31, 2022. As of June 30, 2017, no amounts were outstanding under the Credit Facility.

In addition to increasing amounts available to borrow under the Credit Facility and extending its term, the First Amendment provided that all guarantors immediately prior to January 3, 2017, other than Molina Information Systems, LLC, d/b/a Molina Medicaid Solutions, Molina Pathways, LLC, and Pathways Health and Community Support LLC, were automatically and unconditionally released from their obligations as guarantors of the Credit Facility and the 5.375% Notes.

The Credit Facility contains customary non-financial and financial covenants, including a net leverage ratio and an interest coverage ratio. In February 2017, we entered into a second amendment to the Credit Facility (the Second Amendment) which modified the Credit Facility’s definition of the earnings measure used in the financial covenant computations to a) allow us to receive credit for risk corridor payments owed to, but not received or accrued by us during 2016; and b) account for the difference between the amount of actual risk transfer payments made or accrued by us during 2016, and the amount of risk transfer payments that would have been due under the federal government’s proposed 2018 risk adjustment payment transfer formula.

In May 2017, we entered into a third amendment to the Credit Facility (the Third Amendment) which modified the Credit Facility’s definition of specified cash, to permit cash that is either subject to customary escrow arrangements or held in a segregated account to be netted from the Credit Facility’s consolidated net leverage ratio if the use of the cash is limited to the repayment of other indebtedness. The Third Amendment also adds a carve-out to the Credit Facility’s negative pledge covenant to allow for the escrow arrangements and segregated accounts. At June 30, 2017, we were in compliance with all financial and non-financial covenants under the Credit Facility.

Convertible Senior Notes

We have outstanding $550 million aggregate principal amount of 1.125% cash convertible senior notes due January 15, 2020, unless earlier repurchased or converted. We refer to these notes as our 1.125% Convertible Notes. We also have outstanding $302 million aggregate principal amount of 1.625% convertible senior notes due August 14, 2044, unless earlier repurchased, redeemed, or converted. We refer to these notes as our 1.625% Convertible Notes. The 1.125% Convertible Notes are convertible entirely to cash, and the 1.625% Convertible Notes are convertible partially to cash, each prior to their respective maturity dates under certain circumstances, one of which relates to the closing price of our common stock over a specified period. We refer to this conversion trigger as the stock price trigger.

The stock price trigger for the 1.125% Convertible Notes is $53.00 per share. The 1.125% Convertible Notes met this trigger in the quarter ended June 30, 2017; therefore, they are convertible into cash and are reported in current portion of long-term debt as of June 30, 2017.

The stock price trigger for the 1.625% Convertible Notes is $75.51 per share. The 1.625% Convertible Notes did not meet this stock price trigger in the quarter ended June 30, 2017. On contractually specified dates beginning in 2018, holders of the 1.625% Convertible Notes may require us to repurchase some or all of such notes. In addition, beginning May 15, 2018 until August 19, 2018, holders may convert some or all of the 1.625% Convertible Notes. Because of this conversion feature, the 1.625% Convertible Notes are reported in current portion of long-term debt as of June 30, 2017. As noted above, because the proceeds from the 4.875% Notes are initially restricted to payments upon conversion or redemption of the 1.625% Convertible Notes, such restricted investments are also classified as current in the accompanying consolidated balance sheets.

Molina Healthcare, Inc. 2017 Form 10-Q | 19

Cross-Default Provisions

The terms of our 4.875% Notes, 5.375% Notes and each of the 1.125% and 1.625% Convertible Notes contain cross-default provisions with the Credit Facility that are triggered upon an event of default under the Credit Facility, and when borrowings under the Credit Facility equal or exceed certain amounts as defined in the related indentures.

Debt Commitment Letter

In connection with the Terminated Medicare Acquisition, we entered into a debt commitment letter with Barclays Bank PLC (Barclays) in August 2016. Under this debt commitment letter, Barclays agreed to lend us up to $400 million, subject to satisfaction of certain conditions, including consummation of the Terminated Medicare Acquisition. The debt commitment letter automatically terminated in February 2017 as a result of the termination of this transaction. The costs associated with the debt commitment letter and its termination were reimbursed as described in Note 1, “Basis of Presentation–Health Plans Segment Recent Developments.”

8. Derivatives

The following table summarizes the fair values and the presentation of our derivative financial instruments (defined and discussed individually below) in the accompanying consolidated balance sheets:

Balance Sheet Location | June 30, 2017 | December 31, 2016 | |||||||

(In millions) | |||||||||

Derivative asset: | |||||||||

1.125% Call Option | Current assets: Derivative asset | $ | 440 | $ | 267 | ||||

Derivative liability: | |||||||||

1.125% Conversion Option | Current liabilities: Derivative liability | $ | 440 | $ | 267 | ||||

Our derivative financial instruments do not qualify for hedge treatment; therefore the change in fair value of these instruments is recognized immediately in our consolidated statements of operations, and reported in “Other income, net.” Gains and losses for our derivative financial instruments are presented individually in the accompanying consolidated statements of cash flows, “Supplemental cash flow information.”

1.125% Notes Call Spread Overlay. Concurrent with the issuance of the 1.125% Convertible Notes in 2013, we entered into privately negotiated hedge transactions (collectively, the 1.125% Call Option) and warrant transactions (collectively, the 1.125% Warrants), with certain of the initial purchasers of the 1.125% Convertible Notes (the Counterparties). We refer to these transactions collectively as the Call Spread Overlay. Under the Call Spread Overlay, the cost of the 1.125% Call Option we purchased to cover the cash outlay upon conversion of the 1.125% Convertible Notes was reduced by proceeds from the sale of the 1.125% Warrants. Assuming full performance by the Counterparties (and 1.125% Warrants strike prices in excess of the conversion price of the 1.125% Convertible Notes), these transactions are intended to offset cash payments in excess of the principal amount of the 1.125% Convertible Notes due upon any conversion of such Notes.

1.125% Call Option. The 1.125% Call Option, which is indexed to our common stock, is a derivative asset that requires mark-to-market accounting treatment due to cash settlement features until the 1.125% Call Option settles or expires. For further discussion of the inputs used to determine the fair value of the 1.125% Call Option, refer to Note 4, “Fair Value Measurements.”

1.125% Conversion Option. The embedded cash conversion option within the 1.125% Convertible Notes is accounted for separately as a derivative liability, with changes in fair value reported in our consolidated statements of operations until the cash conversion option settles or expires. For further discussion of the inputs used to determine the fair value of the 1.125% Conversion Option, refer to Note 4, “Fair Value Measurements.”

As of June 30, 2017, the 1.125% Call Option and the 1.125% Conversion Option were classified as a current asset and current liability, respectively, because the 1.125% Convertible Notes may be converted within 12 months of June 30, 2017, as described in Note 7, “Debt.”

Molina Healthcare, Inc. 2017 Form 10-Q | 20

9. Stockholders' Equity

Stockholders’ equity decreased $128 million during the six months ended June 30, 2017 compared with stockholders’ equity at December 31, 2016. The decrease was due primarily to the net loss of $153 million, partially offset by $24 million related to employee stock transactions in the six months ended June 30, 2017, which are described further below.

1.125% Warrants

In connection with the Call Spread Overlay transaction described in Note 8, “Derivatives,” in 2013, we issued 13,490,236 warrants with a strike price of $53.8475 per share. Under certain circumstances, beginning in April 2020, when the price of our common stock exceeds the strike price of the 1.125% Warrants, we will be obligated to issue shares of our common stock subject to a share delivery cap. The 1.125% Warrants could separately have a dilutive effect to the extent that the market value per share of our common stock exceeds the applicable strike price of the 1.125% Warrants. Refer to Note 3, “Net (Loss) Income per Share,” for dilution information for the periods presented. We will not receive any additional proceeds if the 1.125% Warrants are exercised.

Stock Incentive Plans

In connection with our equity incentive plans and employee stock purchase plan, approximately 692,000 shares of common stock vested or were purchased, net of shares used to settle employees’ income tax obligations, during the six months ended June 30, 2017.

Restricted stock awards (RSAs), performance stock awards (PSAs) and performance stock units (PSUs) activity for the six months ended June 30, 2017 is summarized below:

Restricted Stock Awards | Performance Stock Awards | Performance Stock Units | Total | Weighted Average Grant Date Fair Value | |||||||||||

Unvested balance, December 31, 2016 | 577,244 | 345,656 | — | 922,900 | $ | 58.15 | |||||||||

Granted | 377,076 | — | 231,100 | 608,176 | 56.98 | ||||||||||

Vested | (380,812 | ) | (260,894 | ) | (139,272 | ) | (780,978 | ) | 57.63 | ||||||

Forfeited | (58,643 | ) | — | — | (58,643 | ) | 54.48 | ||||||||

Unvested balance, June 30, 2017 | 514,865 | 84,762 | 91,828 | 691,455 | 57.57 | ||||||||||

The total fair value of RSAs granted during the six months ended June 30, 2017 and 2016 was $19 million and $17 million, respectively. The total fair value of RSAs which vested during the six months ended June 30, 2017 and 2016 was $20 million and $21 million, respectively.

No PSAs were granted during the six months ended June 30, 2017. The total fair value of PSAs granted during the six months ended June 30, 2016 was $15 million. The total fair value of PSAs which vested during the six months ended June 30, 2017 was $15 million. No PSAs vested during the six months ended June 30, 2016.

The total fair value of PSUs granted during the six months ended June 30, 2017 was $16 million. The total fair value of PSUs which vested during the six months ended June 30, 2017 was $9 million. There were no PSUs granted or vested in 2016.

During the six months ended June 30, 2017, the vesting of 133,957 RSAs, 153,574 PSAs and 139,272 PSUs was accelerated in connection with the termination of our former Chief Executive Officer (CEO) and former Chief Financial Officer (CFO) in May 2017. Share-based compensation expense of $35 million was recorded during the six months ended June 30, 2017, of which $23 million was recorded to “Restructuring and separation costs” in the accompanying consolidated statements of operations. See Note 11, “Restructuring and Separation Costs” for further discussion. Share-based compensation expense of $16 million was recorded to “General and administrative expenses” in the six months ended June 30, 2016.

As of June 30, 2017, there was $32 million of total unrecognized compensation expense related to unvested RSAs, including those with market and performance conditions, and unvested PSUs, which we expect to recognize over a remaining weighted-average period of 2.5 years and 2.1 years, respectively. This unrecognized compensation cost assumes an estimated forfeiture rate of 3.3% for non-executive employees as of June 30, 2017.

Molina Healthcare, Inc. 2017 Form 10-Q | 21

10. Impairment Losses

Goodwill represents the excess of the purchase price over the fair value of net assets acquired in business combinations. Goodwill is not amortized, but is subject to an annual impairment test. Refer to Note 2, “Significant Accounting Policies,” for a discussion of our adoption of ASU 2017-04, Simplifying the Test for Goodwill Impairment. We are required to test at least annually for impairment, or more frequently if adverse events or changes in circumstances indicate that the asset may be impaired. When testing goodwill for impairment, we may first assess qualitative factors, such as industry and market factors, cost factors, and changes in overall performance, to determine if it is more likely than not that the carrying value of a reporting unit exceeds its estimated fair value. If our qualitative assessment indicates that goodwill impairment is more likely than not, we perform additional quantitative analysis. We may also elect to skip the qualitative testing and proceed directly to the quantitative testing.

An impairment loss is measured as the excess of the carrying amount of the reporting unit, including goodwill, over the fair value of the reporting unit. We estimate the fair values of our reporting units using discounted cash flows. In the discounted cash flow analyses, we must make assumptions about a wide variety of internal and external factors, and consider the price that would be received to sell the reporting unit as a whole in an orderly transaction between market participants at the measurement date. Significant assumptions include financial projections of free cash flow (including significant assumptions about operations, capital requirements and income taxes), long-term growth rates for determining terminal value beyond the discretely forecasted periods, and discount rates.

In the course of developing our restructuring and profitability improvement plan, discussed further in Note 11, “Restructuring and Separation Costs,” we determined that future benefits to be derived from Pathways, including integration with our health plans, would be less than previously anticipated. In addition, poorer than expected year-to-date operating results and lower projections of operating results for periods in the near term led us to conclude that a triggering event for an interim impairment analysis had occurred in the second quarter of 2017.

Intangible Assets. We first evaluated Pathways’ finite-lived intangible assets (customer relationships and contract licenses) for impairment, using undiscounted cash flows expected over the longest remaining useful life of the assets tested. See below for a description of the estimates and assumptions used in the cash flow model. Because the undiscounted cash flows over the remaining useful life were less than Pathways’ carrying amount, the intangible assets were impaired. We recorded an impairment loss for the carrying amount of the intangible assets, or $11 million, in the second quarter of 2017.

Goodwill. We next tested Pathways’ goodwill for impairment. As described above, we estimated Pathways’ fair value using discounted cash flows, incorporating significant estimates and assumptions related to future periods. Such estimates included anticipated client census which drives service revenue; management’s determination that future benefits to be derived from Pathways (including integration with our health plans) will be less than previously anticipated; current prospects relating to the behavioral services labor market which drives cost of service revenue; and anticipated capital expenditures. In addition, we applied our weighted average cost of capital (WACC) as the best estimate to discount future estimated cash flows to present value. The WACC was based on externally available data considering market participants’ cost of equity and debt, and capital structure. We applied a terminal growth rate that corresponds to Pathways’ long-term growth prospects. The test resulted in a fair value less than Pathways’ carrying amount; therefore, we recorded an impairment loss for the difference, or $59 million, in the second quarter of 2017. In addition to the Pathways impairment loss, we recorded an impairment loss of $2 million for a separate subsidiary’s goodwill that did not pass the impairment test. Both impairment losses were recorded to the Other segment, and reported as “Impairment losses” in the accompanying consolidated statements of operations.

There were no impairments of intangible assets or goodwill during 2016.

Molina Healthcare, Inc. 2017 Form 10-Q | 22

The following table presents the balances of goodwill as of June 30, 2017 and December 31, 2016:

Health Plans | Molina Medicaid Solutions | Other | Total | ||||||||||||

(In millions) | |||||||||||||||

Historical goodwill | $ | 445 | $ | 71 | $ | 162 | $ | 678 | |||||||

Accumulated impairment losses at December 31, 2016 | (58 | ) | — | — | (58 | ) | |||||||||

Balance, December 31, 2016 | 387 | 71 | 162 | 620 | |||||||||||

Impairment losses | — | — | (61 | ) | (61 | ) | |||||||||

Balance, June 30, 2017 | $ | 387 | $ | 71 | $ | 101 | $ | 559 | |||||||

Accumulated impairment losses at June 30, 2017 | $ | (58 | ) | $ | — | $ | (61 | ) | $ | (119 | ) | ||||

11. Restructuring and Separation Costs

Following a management-initiated, broad operational assessment in early 2017, designed to improve our profitability and expand our core Medicaid business, in June 2017, we accelerated the implementation of a comprehensive restructuring and profitability improvement plan (the Restructuring Plan). Under the Restructuring Plan, we are taking the following actions:

1. | We are streamlining our organizational structure, including the elimination of redundant layers of management, the consolidation of regional support services, and other reductions to our workforce, to improve efficiency as well as the speed and quality of our decision-making. |

2. | We are re-designing core operating processes such as provider payment, utilization management, quality monitoring and improvement, and information technology to achieve more effective and cost efficient outcomes. |

3. | We are remediating high cost provider contracts and building around high quality, cost-effective networks. |

4. | We are restructuring our existing direct delivery operations. |

5. | We are reviewing our vendor base to ensure that we are partnering with the lowest-cost, most-effective vendors. |

6. | Throughout this process, we are taking precautions to ensure that our actions do not impede our ability to continue to deliver quality health care, retain existing managed care contracts, and to secure new managed care contracts. |

In addition to costs incurred under the Restructuring Plan, in the second quarter of 2017 we recorded costs associated with the separation of our former CEO and former CFO, described in further detail below.

All restructuring and separation costs incurred in the six months ended June 30, 2017, are reported in “Restructuring and separation costs” in the accompanying consolidated statements of operations, and are included in the Other segment because they represent corporate costs not allocated to the other reportable segments.

Separation Costs