Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - HAWKINS INC | hwkn10k2017exhibit322.htm |

| EX-32.1 - EXHIBIT 32.1 - HAWKINS INC | hwkn10k2017exhibit321.htm |

| EX-31.2 - EXHIBIT 31.2 - HAWKINS INC | hwkn10k2017exhibit312.htm |

| EX-31.1 - EXHIBIT 31.1 - HAWKINS INC | hwkn10k2017exhibit311.htm |

| EX-23.1 - EXHIBIT 23.1 - HAWKINS INC | hwkn10k2017exhibit231.htm |

| EX-21 - EXHIBIT 21 - HAWKINS INC | hwkn10k2017exhibit21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K | ||

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE | ||

SECURITIES EXCHANGE ACT OF 1934 | ||

For the Fiscal Year Ended April 2, 2017 | ||

Commission File No. 0-7647 | ||

HAWKINS, INC.

(Exact Name of Registrant as Specified in its Charter)

Minnesota | 41-0771293 | |

(State of Incorporation) | (I.R.S. Employer Identification No.) | |

2381 Rosegate, Roseville, Minnesota | 55113 | |

(Address of Principal Executive Offices) | (Zip Code) | |

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act: | Common Stock, par value $.05 per share | |||

Name of exchange on which registered: | NASDAQ Global Market | |||

Securities registered pursuant to Section 12(g) of the Act: | None | |||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding twelve months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ¨ | Non-accelerated filer | ¨ | Accelerated filer | þ | Smaller reporting company | o | |||

Emerging growth company | o | |||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of voting stock held by non-affiliates of the Registrant on October 2, 2016 (the last business day of the Registrant’s most recently completed second fiscal quarter) was approximately $409.3 million based upon the closing sale price for the Registrant’s common stock on that date as reported by The NASDAQ Stock Market, excluding all shares held by officers and directors of the Registrant and by the Trustees of the Registrant’s Employee Stock Ownership Plan and Trust.

As of May 26, 2017, the Registrant had 10,619,541 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of our definitive Proxy Statement for the annual meeting of shareholders to be held August 9, 2017, are incorporated by reference in Part III of this Annual Report on Form 10-K

FORWARD-LOOKING STATEMENTS

The information presented in this Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements have been made pursuant to the provisions of the Private Securities Litigation Reform Act of 1995. These statements are not historical facts, but rather are based on our current expectations, estimates and projections, and our beliefs and assumptions. Words such as “anticipate,” “expect,” “intend,” “plan,” “believe,” “seek,” “estimate,” “will” and similar expressions may identify forward-looking statements. These statements are not guarantees of future performance and are subject to certain risks, uncertainties and other factors, some of which are beyond our control and are difficult to predict. These factors could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements. These risks and uncertainties are described in the risk factors and elsewhere in this Annual Report on Form 10-K. We caution you not to place undue reliance on these forward-looking statements, which reflect our management’s view only as of the date of this Annual Report on Form 10-K. We are not obligated to update these statements or publicly release the result of any revisions to them to reflect events or circumstances after the date of this Annual Report on Form 10-K or to reflect the occurrence of unanticipated events.

As used in this Annual Report on Form 10-K, except where otherwise stated or indicated by the context, “Hawkins,” “we,” “us,” “the Company,” “our,” or “the Registrant” means Hawkins, Inc. References to “fiscal 2018” means our fiscal year ending April 1, 2018, “fiscal 2017” means our fiscal year ended April 2, 2017, “fiscal 2016” means our fiscal year ended April 3, 2016, and “fiscal 2015” means our fiscal year ended March 29, 2015.

ii

Hawkins, Inc.

Annual Report on Form 10-K

For the Fiscal Year Ended April 2, 2017

Page | ||

PART I | ||

ITEM 1. | ||

ITEM 1A. | ||

ITEM 1B. | ||

ITEM 2. | ||

ITEM 3. | ||

ITEM 4. | ||

PART II | ||

ITEM 5. | ||

ITEM 6. | ||

ITEM 7. | ||

ITEM 7A. | ||

ITEM 8. | ||

ITEM 9. | ||

ITEM 9A. | ||

ITEM 9B. | ||

PART III | ||

ITEM 10. | ||

ITEM 11. | ||

ITEM 12. | ||

ITEM 13. | ||

ITEM 14. | ||

PART IV | ||

ITEM 15. | ||

ITEM 16. | ||

iii

PART I

ITEM 1. BUSINESS

Hawkins, Inc. distributes, blends and manufactures chemicals and specialty ingredients for our customers in a wide variety of industries. We began our operations primarily as a distributor of bulk chemicals with a strong customer focus. Over the years, we have maintained our strong customer focus and have expanded our business by increasing our sales of value-added chemical products and specialty ingredients, including manufacturing, blending and repackaging certain products. We believe that we create value for our customers through superb service and support, quality products, personalized applications and trustworthy, creative employees.

We currently conduct our business in three segments: Industrial, Water Treatment, and Health and Nutrition. Our Health and Nutrition segment was established as a result of our acquisition of Stauber Performance Ingredients (“Stauber”) in December 2015. Financial information regarding these segments is reported in Item 7 and note 13 of Item 8 of this Annual Report on Form 10-K.

Industrial Segment. Our Industrial Group specializes in providing industrial chemicals, products and services to industries such as agriculture, chemical processing, electronics, energy, food, pharmaceutical and plating. This group’s principal products are acids, alkalis and industrial and food-grade salts.

The Industrial Group:

• | Receives, stores and distributes various chemicals in bulk quantities, including liquid caustic soda, sulfuric acid, hydrochloric acid, phosphoric acid, potassium hydroxide and aqua ammonia; |

• | Manufactures sodium hypochlorite (bleach), agricultural products and certain food-grade products, including liquid phosphates, lactates and other blended products; |

• | Repackages water treatment chemicals for our Water Treatment Group and bulk industrial chemicals to sell in smaller quantities to our customers; |

• | Performs custom blending of chemicals according to customer formulas and specifications; and |

• | Performs contract and private label bleach packaging. |

The group’s sales are concentrated primarily in Illinois, Iowa, Kentucky, Minnesota, Missouri, North Dakota, South Dakota, Tennessee and Wisconsin, while the group’s products sold into the food and pharmaceutical markets are sold nationally. The Industrial Group relies on a specially trained sales staff that works directly with customers on their specific needs. The group conducts its business primarily through distribution centers and terminal operations. Agricultural sales within this group tend to be seasonal, with higher sales due to the application of fertilizer during the planting season of March through June given the regions of the country where we are located.

Water Treatment Segment. Our Water Treatment Group specializes in providing chemicals, equipment and solutions for potable water, municipal and industrial wastewater, industrial process water and non-residential swimming pool water. This group has the resources and flexibility to treat systems ranging in size from a single small well to a multi-million-gallon-per-day facility.

The group utilizes delivery routes operated by our employees who typically serve as route driver, salesperson and trained technician to deliver our products and diagnose our customers’ water treatment needs. We believe that the high level of service provided by these individuals allows us to serve as the trusted water treatment expert for many of the municipalities and other customers that we serve. We also believe that there are significant synergies between our Water Treatment and Industrial Groups in that we are able to obtain a competitive cost position on many of the chemicals sold by the Water Treatment Group due to the volumes of these chemicals purchased by our Industrial Group. In addition, our Industrial and Water Treatment groups share certain of our facilities, which leverage fixed costs across both groups.

The group operates out of warehouses in 29 cities supplying products and services to customers primarily in Arkansas, Florida, Illinois, Indiana, Iowa, Kansas, Minnesota, Missouri, Montana, Nebraska, North Dakota, Ohio, Oklahoma, South Dakota, Wisconsin and Wyoming. We added two new Water Treatment branches in fiscal 2016. We entered the Florida market in fiscal 2015 through our acquisition of substantially all the assets of The Dumont Company, Inc. (“Dumont”), with seven operating locations. We expect to continue to invest in existing and new branches to expand the group’s geographic coverage. Our Water

1

Treatment Group has historically experienced higher sales during April to September, primarily due to a seasonal increase in chemicals used by municipal water treatment facilities.

Health and Nutrition Segment. We established the Health and Nutrition segment of our business in December 2015 through our acquisition of Stauber. Our Health and Nutrition Group specializes in providing ingredient distribution, processing and formulation solutions to manufacturers of nutraceutical, functional food and beverage, personal care, dietary supplement and other nutritional food, health and wellness products. This group offers a diverse product portfolio including minerals, botanicals and herbs, vitamins and amino acids, excipients, joint products, sweeteners and enzymes.

The Health and Nutrition Group relies on a specially trained sales and product development staff that works directly with customers on their specific needs. The group’s extensive product portfolio combined with value-added services, including product formulation, sourcing and distribution, processing and blending and quality control and compliance, positions this group as a one-stop ingredient solutions provider to its customers. The group operates out of facilities in California and New York and its products are sold nationally and, in certain cases, internationally.

Raw Materials. We have numerous suppliers, including many of the major chemical producers in the United States. We source our health and nutrition ingredients from a wide array of domestic and international vendors. We typically have written distributorship agreements or supply contracts with our chemical suppliers that are periodically renewed. We believe that most of the products we purchase can be obtained from alternative sources should existing relationships be terminated. We are dependent upon the availability of our raw materials. While we believe that we have adequate sources of supply for our raw material and product requirements, we cannot be sure that supplies will be consistently available in the future. In the event that certain raw materials become generally unavailable, suppliers may extend lead times or limit or cut off the supply of materials to us. As a result, we may not be able to supply or manufacture products for our customers.

Intellectual Property. Our intellectual property portfolio is of economic importance to our business. When appropriate, we have pursued, and we will continue to pursue, patents covering our products. We also have obtained certain trademarks for our products to distinguish them from our competitors’ products. We regard much of the formulae, information and processes that we generate and use in the conduct of our business as proprietary and protectable under applicable copyright, patent, trademark, trade secret and unfair competition laws.

Customer Concentration. In fiscal 2017, none of our customers accounted for 10% or more of our total sales. Sales to our largest customer, which is in our Industrial segment, represented approximately 4% of our total sales in fiscal 2017, 5% of our total sales in fiscal 2016 and 6% of our total sales in fiscal 2015. Aggregate sales to our five largest customers, four of which are in our Industrial segment and one of which is in our Health and Nutrition segment, represented approximately 12% of our total sales in fiscal 2017, 14% of our total sales in fiscal 2016 and 18% of our total sales in fiscal 2015. No other customer represented more than 2% of our total sales in fiscal 2017. The loss of any of our largest customers, or a substantial portion of their business, could have a material adverse effect on our results of operations.

Competition. We operate in a competitive industry and compete with many producers, distributors and sales agents offering products equivalent to substantially all of the products we offer. Many of our competitors are larger than we are and may have greater financial resources, although no one competitor is dominant in the markets we serve. We compete by offering quality products at competitive prices coupled with outstanding customer service and value-added services or product formulation where needed. Because of our long-standing relationships with many of our suppliers, we are often able to leverage those relationships to obtain products when supplies are scarce or to obtain competitive pricing.

Geographic Information. Substantially all of our revenues are generated by sales to customers within, and long-lived assets are located in, the United States. Approximately 2% of our total revenues were from sales to customers outside of the U.S. in fiscal 2017, and approximately 1% of our revenues were from sales to customers outside of the U.S. in both fiscal 2016 and fiscal 2015.

Working Capital. Due to the nature of our operations, which includes purchases of large quantities of bulk chemicals, the timing of purchases can result in significant changes in working capital and the resulting operating cash flow. Historically, our cash requirements for working capital increase during the period from April through November as caustic soda inventory levels increase with most of the barges received during this period. Additionally, due to seasonality of the Water Treatment business, our accounts receivable balance is generally higher during the period of April through September.

Employees. We had 659 employees as of April 2, 2017, including 58 covered by collective bargaining agreements.

2

About Us. Hawkins, Inc. was founded in 1938 and incorporated in Minnesota in 1955. We became a publicly-traded company in 1972. Our principal executive offices are located at 2381 Rosegate, Roseville, Minnesota.

Available Information. We have made available, free of charge, through our Internet website (http://www.hawkinsinc.com), our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and, if applicable, amendments to those reports, as soon as reasonably practicable after we electronically file these materials with, or furnish them to, the Securities and Exchange Commission. Reports of beneficial ownership filed by our directors and executive officers pursuant to Section 16(a) of the Exchange Act are also available on our website. We are not including the information contained on our website as part of, or incorporating it by reference into, this Annual Report on Form 10-K.

3

ITEM 1A. RISK FACTORS

You should consider carefully the following risks when reading the information, including the financial information, contained in this Annual Report on Form 10-K.

We operate in a highly competitive environment and face significant competition and price pressure.

We operate in a highly competitive industry and compete with producers, manufacturers, distributors and sales agents offering products equivalent to substantially all of the products we offer. Competition is based on several key criteria, including product price, product performance, product quality, product availability and security of supply, breadth of product offerings, geographic reach, responsiveness of product development in cooperation with customers, technical expertise and customer service. Many of our competitors are larger than we are and may have greater financial resources, more product offerings and a broader geographic reach. As a result, these competitors may be able to offer a broader array of products to a larger geographic area and may be better able than us to withstand changes in conditions within our industry, changes in the prices and availability of raw materials and changes in general economic conditions as well as be able to introduce innovative products that reduce demand for or the profit of our products. Additionally, competitors’ pricing decisions could compel us to decrease our prices, which could adversely affect our margins and profitability. Our ability to maintain or increase our profitability would be dependent upon our ability to offset competitive decreases in the prices and margins of our products by improving production efficiency, investing in infrastructure to reduce freight costs, identifying and selling higher margin products, providing higher levels of technical expertise and customer service, and improving existing products through innovation and research and development. If we are unable to maintain our profitability or competitive position, we could lose market share to our competitors and experience reduced profitability.

Fluctuations in the prices and availability of our raw materials, which may be cyclical in nature, could have a material adverse effect on our operations and the margins we receive on sales of our products.

We experience regular and recurring fluctuations in the pricing of our raw materials. Those fluctuations can be significant and occur rapidly. The cyclicality of commodity markets, such as caustic soda, primarily results from changes in the balance between supply and demand and the level of general economic activity. We cannot predict whether the markets for our raw materials will favorably impact or negatively impact the margins we can realize.

Our principal chemical raw materials are generally purchased under supply contracts. The prices we pay under these contracts generally lag the market prices of the underlying raw material and the cost of inventory we have on hand, particularly inventories of our bulk commodity chemicals where we have significant volumes stored at our facilities, generally will lag the current market pricing of such inventory. The pricing within our supply contracts generally adjusts quarterly or monthly. While we attempt to maintain competitive pricing and stable margin dollars, the potential variance in our cost of inventory from the current market pricing can cause significant volatility in our margins realized. In periods of rapidly increasing market prices, our inventory cost position will tend to be favorable, possibly by material amounts, which may positively impact our margins. Conversely, in periods of rapidly decreasing market prices, our inventory cost position will tend to be unfavorable, possibly by material amounts, which may negatively impact our margins. We do not engage in futures or other derivatives contracts to hedge against fluctuations in future prices. We may enter into sales contracts where the selling prices for our products are fixed for a period of time, exposing us to volatility in raw materials prices that we acquire on a spot market or short-term contractual basis. We attempt to pass commodity pricing changes to our customers, but we may be unable to or be delayed in doing so. Our inability to pass through price increases or any limitation or delay in our passing through price increases could adversely affect our profit margins.

We are also dependent upon the availability of our raw materials. In the event that raw materials are in short supply or unavailable, raw material suppliers may extend lead times or limit or cut off supplies. As a result, we may not be able to supply or manufacture products for some or all of our customers. Constraints on the supply or delivery of critical raw materials could disrupt our operations and adversely affect the performance of our businesses.

Demand for our products is affected by general economic conditions and by the cyclical nature of many of the industries we serve, which could cause significant fluctuations in our sales volumes and results.

Demand for our products is affected by general economic conditions. A decline in general economic or business conditions in the industries served by our customers could have a material adverse effect on our businesses. Although we sell to areas traditionally considered non-cyclical, such as water treatment, food products and health and nutritional ingredients, many of our customers are in businesses that are cyclical in nature, such as the industrial manufacturing and energy industries which include the ethanol and agriculture industries. Downturns in these industries could adversely affect our sales and our financial results by affecting demand for and pricing of our products.

4

Changes in our customers’ needs or failure of our products to meet customers’ specifications could adversely affect our sales and profitability.

Our products are used for a broad range of applications by our customers. Changes in our customers’ product needs or processes may enable our customers to reduce or eliminate consumption of the products that we provide. Customers may also find alternative materials or processes that no longer require our products. Consequently, it is important that we develop new products to replace the sales of products that mature and decline in use.

Our products provide important performance attributes to our customers’ products. If our products fail to meet the customers’ specifications, perform in a manner inconsistent with the customers’ expectations or have a shorter useful life than required, a customer could seek replacement of the product or damages for costs incurred as a result of the product failure. A successful claim or series of claims against us could have a material adverse effect on our financial condition and results of operations and could result in a loss of one or more customers.

Our business is subject to hazards common to chemical businesses, any of which could interrupt our production and adversely affect our results of operations.

Our business is subject to hazards common to chemical manufacturing, blending, storage, handling and transportation, including explosions, fires, severe weather, natural disasters, mechanical failure, unscheduled downtime, transportation interruptions, traffic accidents involving our delivery vehicles, chemical spills, discharges or releases of toxic or hazardous substances or gases and other risks. These hazards could cause personal injury and loss of life, severe damage to or destruction of property and equipment, and environmental contamination. In addition, the occurrence of material operating problems at any of our facilities due to any of these hazards may make it impossible for us to make sales to our customers and may result in a negative public or political reaction. Many of our facilities are near significant residential populations which increases the risk of negative public or political reaction should an environmental issue occur and could lead to adverse zoning or other regulatory actions that could limit our ability to operate our business in those locations. Accordingly, these hazards and their consequences could have a material adverse effect on our operations as a whole, including our results of operations and cash flows, both during and after the period of operational difficulties.

We are highly dependent upon transportation infrastructure to ship and receive our products and delays in these shipments could adversely affect our results of operations.

Although we maintain a number of owned trucks and trailers, we rely heavily upon transportation provided by third parties (including common carriers, barge companies, rail companies and trans-ocean cargo companies) to deliver products to us and to our customers. Our access to third-party transportation is not guaranteed, and we may be unable to transport our products in a timely manner, or at all, in certain circumstances, or at economically attractive rates. Disruptions in transportation are common, are often out of our control, and can happen suddenly and without warning. Rail limitations, such as limitations in rail capacity, availability of railcars and adverse weather conditions have disrupted or delayed rail shipments in the past and we expect they will continue into the future. Barge shipments are delayed or impossible under certain circumstances, including during times of high or low water levels, when waterways are frozen and when locks and dams are inoperable. Truck transportation has been negatively impacted by a number of factors, including limited availability of qualified drivers and equipment, and limitations on drivers’ hours of service, and may be further impacted by the implementation of federally mandated electronic log books, and we expect these conditions will continue into the future. The volumes handled by, and operating challenges at, ocean ports have at times been volatile and can delay the receipt of goods, or cause the cost of shipping goods to be more expensive. Our failure to ship or receive products in a timely and efficient manner could have a material adverse effect on our financial condition and results of operations.

Environmental, health and safety, transportation and storage laws and regulations cause us to incur substantial costs and may subject us to future liabilities and risks.

We are subject to numerous federal, state and local environmental, health and safety laws and regulations in the jurisdictions in which we operate, including the management, storage, transportation and disposal of chemicals and wastes; product regulation; air water and soil contamination; and the investigation and cleanup of any spills or releases that may result from our management, handling, storage, sale, or transportation of chemicals and other products. The nature of our business exposes us to risks of liability under these laws and regulations. Ongoing compliance with such laws and regulations is an important consideration for us and we invest substantial capital and incur significant operating costs in our compliance efforts. In addition, societal concerns regarding the safety of chemicals in commerce and their potential impact on the environment have resulted in a growing trend towards increasing levels of product safety and environmental protection regulations. These concerns have led to, and could continue to result in, more stringent regulatory intervention by governmental authorities. In addition, these concerns could influence public

5

perceptions, impact the commercial viability of the products we sell and increase the costs to comply with increasingly complex regulations, which could have a negative impact on our business, financial condition and results of operations.

In addition, we operate a fleet of more than 150 vehicles, primarily in our Water Treatment Group, which are highly regulated, including by the U.S. Department of Transportation (“DOT”). The DOT governs transportation matters including authorization to engage in motor carrier service, including the necessary permits to conduct our businesses, equipment operation, and safety. We are audited periodically by the DOT to ensure that we are in compliance with various safety, hours-of-service, and other rules and regulations. If we were found to be out of compliance, the DOT could severely restrict or otherwise impact our operations, which could have a material adverse effect on our operations as a whole, including our results of operations and cash flows.

If we violate applicable laws or regulations, in addition to being required to correct such violations, we could be held liable in administrative, civil or criminal proceedings for substantial fines and other sanctions that could disrupt, limit or halt our operations, which could have a material adverse effect on our operations as a whole, including our results of operations and cash flows. Liabilities associated with the investigation and cleanup of releases of hazardous substances, as well as personal injury, property damages or natural resource damages arising out of such releases of hazardous substances, may be imposed in many situations without regard to violations of laws or regulations or other fault, and may also be imposed jointly and severally (so that a responsible party may be held liable for more than its share of the losses involved, or even the entire loss). Such liabilities can be difficult to identify and the extent of any such liabilities can be difficult to predict. We use, and in the past have used, hazardous substances at many of our facilities, and have generated, and continue to generate, hazardous wastes at a number of our facilities. We have in the past been, and may in the future be, subject to claims relating to exposure to hazardous materials and the associated liabilities may be material.

Our food, pharmaceutical and nutritional products are subject to government regulation, both in the United States and abroad, which could increase our costs significantly and limit or prevent the sale of such products.

The manufacture, packaging, labeling, advertising, promotion, distribution and sale of our food, pharmaceutical and nutritional products are subject to regulation by numerous national and local governmental agencies in the United States and other countries. The primary regulatory bodies in the United States are the Food and Drug Administration (the “FDA”), the United States Department of Agriculture and the Federal Trade Commission, and we are also subject to similar regulators in other countries. Failure to comply with these regulatory requirements may result in various types of penalties or fines. These include injunctions, product withdrawals, recalls, product seizures, fines and criminal prosecutions. Individual states also regulate dietary supplements. A state may interpret claims or products presumptively valid under federal law as illegal under that state’s regulations. Approvals or licensing may be conditioned on reformulation of products or may be unavailable with respect to certain products or product ingredients. Any of these government agencies, as well as legislative bodies, can change existing regulations, or impose new ones, or could take aggressive measures, causing or contributing to a variety of negative consequences, including:

• | requirements for the reformulation of certain or all products to meet new standards, |

• | the recall or discontinuance of certain or all products, |

• | additional record-keeping requirements, |

• | expanded documentation of the properties of certain or all products, |

• | expanded or different labeling, |

• | adverse event tracking and reporting, and |

• | additional scientific substantiation. |

In particular, the FDA’s current good manufacturing practices (“GMPs”) describe policies and procedures designed to ensure that nutraceuticals, pharmaceuticals and dietary supplements are produced in a quality manner, do not contain contaminants or impurities, and are accurately labeled and cover the manufacturing, packaging, labeling and storing of supplements, with requirements for quality control, design and construction of manufacturing plants, testing of ingredients and final products, record keeping, and complaints processes. Those who manufacture, package or store dietary supplements must comply with current GMPs. If we or our suppliers fail to comply with current GMPs, the FDA may take enforcement action against us or our suppliers.

Any or all of the potential negative consequences described above could have a material adverse effect on us or substantially increase the cost of doing business in this area. There can be no assurance that the regulatory environment in which we operate will not change or that such regulatory environment, or any specific action taken against us, will not result in a material adverse effect on us.

6

Our businesses expose us to potential product liability claims and recalls, which could adversely affect our financial condition and performance.

The repackaging, blending, mixing and distribution of products by us, including chemical products and products used in food or food ingredients or with medical, pharmaceutical or dietary supplement applications, involve an inherent risk of exposure to product liability claims, product recalls, product seizures and related adverse publicity, including, without limitation, claims for exposure to our products, spills or escape of our products, personal injuries, food-related claims and property damage or environmental claims. A product liability claim, judgment or recall against our customers could also result in substantial and unexpected expenditures for us, affect consumer confidence in our products and divert management’s attention from other responsibilities. Although we maintain product liability insurance, there can be no assurance that the type or level of coverage is adequate or that we will be able to continue to maintain our existing insurance or obtain comparable insurance at a reasonable cost, if at all. A product recall or a partially or completely uninsured judgment against us could have a material adverse effect on our business, financial condition and results of operations.

Demand for our food and nutritional products is highly dependent upon consumers’ perception of the safety and quality of our products, our customers’ products as well as similar products distributed by other companies, and adverse publicity and negative public perception regarding particular ingredients or products or the nutraceuticals industry in general could limit our ability to increase revenue and grow that portion of our business.

Purchasing decisions made by consumers of products that contain our ingredients may be affected by adverse publicity or negative public perception regarding particular ingredients or products or the nutraceuticals industry in general. This negative public perception may include publicity regarding the legality or quality of particular ingredients or products in general or of other companies or our products or ingredients specifically. Negative public perception may also arise from regulatory investigations, regardless of whether those investigations involve us. We are highly dependent upon consumers’ perception of the safety and quality of products that contain our ingredients as well as similar products distributed by other companies. Thus, the mere publication of reports asserting that such products may be harmful could have a material adverse effect on us, regardless of whether these reports are scientifically supported. Publicity related to dietary supplements may also result in increased regulatory scrutiny of our industry. Adverse publicity may have a material adverse effect on our business, financial condition, results of operations and cash flows. There can be no assurance of future favorable scientific results and media attention or of the absence of unfavorable or inconsistent findings.

Our Water Treatment Group and our agricultural product sales within our Industrial Group are subject to seasonality and weather conditions, which could adversely affect our results of operations.

Our Water Treatment Group has historically experienced higher sales during April to September, primarily due to a seasonal increase in chemicals used by municipal water treatment facilities. Our agricultural product sales are also seasonal, primarily corresponding with the planting and harvesting seasons. Demand in both of these areas is also affected by weather conditions, as either higher or lower than normal precipitation or temperatures may affect water usage and the timing and the amount of consumption of our products. We cannot assure you that seasonality or fluctuating weather conditions will not have a material adverse effect on our results of operations.

The insurance that we maintain may not fully cover all potential exposures.

We maintain property, business interruption and casualty insurance, but such insurance may not cover all risks associated with the hazards of our businesses and is subject to limitations, including deductibles and limits on the liabilities covered. We may incur losses beyond the limits or outside the coverage of our insurance policies, including liabilities for environmental remediation and product liability. In addition, from time to time, various types of insurance for companies in the chemical or food and nutritional products industry have not been available on commercially acceptable terms or, in some cases, have not been available at all. In the future, we may not be able to obtain coverage at current levels, and our premiums may increase significantly on coverage that we maintain.

We entered into a credit facility, and failure to comply with the covenants thereunder may have a material adverse effect.

In December 2015, we entered into a credit agreement (the “Credit Agreement”) with U.S. Bank National Association and other lenders from time to time party thereto (collectively, the “Lenders”), which included senior secured credit facilities (the “Credit Facility”) totaling $165.0 million, consisting of (i) a $100.0 million senior secured term loan credit facility (the “Term Loan Facility”) and (ii) a $65.0 million senior secured revolving loan credit facility (the “Revolving Loan Facility”). The Revolving Loan Facility includes a $5.0 million letter of credit subfacility and $8.0 million swingline subfacility. Loans under the Term Loan

7

Facility are to be repaid in quarterly installments on the last day of each fiscal quarter, with $5.0 million paid in year one, $7.5 million to be paid in year two, and $10.0 million to be paid in years three through five. As of April 2, 2017, we had $93.1 million outstanding under the Term Loan Facility and $10.0 million outstanding under the Revolving Loan Facility. The remaining outstanding balance on these credit facilities will be repaid in full after five years.

If we are unable to generate sufficient cash flow or otherwise obtain funds necessary to make required payments on the Credit Facility, we will be in default. We are also required to comply with several financial covenants under the Credit Agreement. Our ability to comply with such financial covenants may be affected by events beyond our control, which could result in a default under the Credit Agreement; such default may have a material adverse effect on our business, financial condition, operating results or cash flows.

The Credit Agreement also contains other customary affirmative and negative covenants, including covenants that restrict the ability of the Company and its subsidiaries to incur additional indebtedness, dispose of significant assets, make certain investments, including any acquisitions other than permitted acquisitions, make certain payments, enter into sale and leaseback transactions, grant liens on its assets or rate management transactions, subject to certain limitations. These restrictions may adversely affect our business.

Impairment to the carrying value of our goodwill or other intangible assets could adversely affect our financial condition and consolidated results of operations.

Goodwill represents the excess of the cost of acquired businesses over the fair value of identifiable tangible net assets and identifiable intangible assets purchased. Goodwill is tested at least annually for impairment, and is tested for impairment more frequently if events or changes in circumstances indicate that the asset might be impaired. Our annual test for impairment is as of the first day of our fourth fiscal quarter, or January 2, 2017 for fiscal 2017. Goodwill impairment testing is at the reporting unit level. For our Industrial and Water Treatment reporting units, we performed an analysis of qualitative factors to determine if it is more likely than not that the fair value of a reporting unit is less than its carrying amount. If that qualitative analysis indicates that an impairment may exist, then we would calculate the amount of the impairment by comparing the fair value of the assets and liabilities to the fair value of the reporting unit. For our Health and Nutrition reporting unit, we performed a quantitative goodwill impairment analysis, which required us to estimate the fair value of this reporting unit and compare the fair value to the reporting unit’s carrying value. The fair value of the reporting unit in excess of the value of the assets and liabilities is the implied fair value of the goodwill. If this amount is less than the carrying amount of goodwill, impairment is recognized for the difference. As of January 2, 2017, the excess fair value over the carrying value of our Health and Nutrition reporting unit was $7.4 million, or 4.8%. A significant amount of judgment is involved in determining if an indication of impairment exists. Factors may include, among others: a significant decline in our expected future cash flows; a sustained, significant decline in our stock price and market capitalization; a significant adverse change in the business climate; unanticipated competition; and slower growth rates. An adverse change in these factors may have a significant impact on the recoverability of the net assets recorded, and the resulting impairment charge could have a material adverse effect on our financial condition and consolidated results of operations.

We evaluate the useful lives of our intangible assets to determine if they are definite- or indefinite-lived. Reaching a determination on useful life requires significant judgments and assumptions regarding the future effects of obsolescence, demand, competition, other economic factors (such as the stability of the industry, legislative action that results in an uncertain or changing regulatory environment, and expected changes in distribution channels), and the expected lives of other related groups of assets.

We cannot accurately predict the amount and timing of any impairment of goodwill and other intangible assets. Should the value of these assets become impaired, there could be a material adverse effect on our financial condition and consolidated results of operations.

If we are unable to retain key personnel or attract new skilled personnel, it could have an adverse impact on our businesses.

Because of the specialized and technical nature of our businesses, our future performance is dependent on the continued service of, and on our ability to attract and retain, qualified management, scientific, technical and support personnel. The unanticipated departure of key members of our management team could have an adverse impact on our business.

We may not be able to successfully consummate future acquisitions or integrate acquisitions into our business, which could result in unanticipated expenses and losses.

As part of our business growth strategy, we have acquired businesses and may pursue acquisitions in the future. Our ability to pursue this strategy will be limited by our ability to identify appropriate acquisition candidates and our financial resources, including

8

available cash and borrowing capacity. The expense incurred in consummating acquisitions, the time it takes to integrate an acquisition or our failure to integrate businesses successfully could result in unanticipated expenses and losses. Furthermore, we may not be able to realize the anticipated benefits from acquisitions.

The process of integrating acquired operations into our existing operations may result in unforeseen operating difficulties and may require significant financial resources that would otherwise be available for the ongoing development or expansion of existing operations. The risks associated with the integration of acquisitions include potential disruption of our ongoing businesses and distraction of management, unforeseen claims, liabilities, adjustments, charges and write-offs, difficulty in conforming the acquired business’ standards, processes, procedures and controls with our operations, and challenges arising from the increased scope, geographic diversity and complexity of the expanded operations.

Our businesses are subject to risks stemming from natural disasters or other extraordinary events outside of our control, which could interrupt our production and adversely affect our results of operations.

Natural disasters have the potential of interrupting our operations and damaging our properties, which could adversely affect our businesses. Flooding of the Mississippi River has temporarily shifted the Company’s terminal operations out of its buildings three times since the spring of 2010. We can give no assurance that flooding or other natural disasters will not recur or that there will not be material damage or interruption to our operations in the future from such disasters.

Chemical-related assets may be at greater risk of future terrorist attacks than other possible targets in the United States. Federal law imposes site security requirements, specifically on chemical facilities, which have increased our overhead expenses. Federal regulations have also been adopted to increase the security of the transportation of hazardous chemicals in the United States. We ship and receive materials that are classified as hazardous and we believe we have met these requirements, but additional federal and local regulations that limit the distribution of hazardous materials are being considered. Bans on movement of hazardous materials through certain cities could adversely affect the efficiency of our logistical operations. Broader restrictions on hazardous material movements could lead to additional investment and could change where and what products we provide.

The occurrence of extraordinary events, including future terrorist attacks and the outbreak or escalation of hostilities, cannot be predicted, but their occurrence can be expected to negatively affect the economy in general, and specifically the markets for our products. The resulting damage from a direct attack on our assets, or assets used by us, could include loss of life and property damage. In addition, available insurance coverage may not be sufficient to cover all of the damage incurred or, if available, may be prohibitively expensive.

We may not be able to renew our leases of land where four of our operations facilities reside.

We lease the land where our three main terminals are located and where another significant manufacturing plant is located. We do not have guaranteed lease renewal options and may not be able to renew our leases in the future. Our current lease renewal periods extend out to 2023, 2028, 2029 and 2034. The failure to secure extended lease terms on any one of these facilities may have a material adverse impact on our business, as they are where a portion of our chemicals are manufactured and where the majority of our bulk chemicals are stored. While we can make no assurances, based on historical experience and anticipated future needs, we intend to extend these leases and believe that we will be able to renew our leases as the renewal periods expire. If we are unable to renew three of our leases (two relate to terminals and one to manufacturing) any property remaining on the land becomes the property of the lessor, and the lessor has the option to either maintain the property or remove the property at our expense. The fourth lease provides that we turn any property remaining on the land over to the lessor for them to maintain or remove at their expense. The cost to relocate our operations could have a material adverse effect on our results of operations and financial condition.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

9

ITEM 2. PROPERTIES

Our corporate office is located in Roseville, Minnesota, where we lease approximately 40,000 square feet under a lease with an initial term through December 31, 2021. We own our principal manufacturing, warehousing, and distribution location in Minneapolis, Minnesota, which consists of approximately 11 acres of land, with six buildings containing a total of 177,000 square feet of office and warehouse space primarily used by our Industrial Group. We have installed sprinkler systems in substantially all of our warehouse facilities for fire protection. We believe that we carry customary levels of insurance covering the replacement of damaged property.

In addition to the facilities described previously, our other facilities are described below. We believe that these facilities, together with those described above, are adequate and suitable for the purposes they serve. Unless noted, each facility is owned by us and is primarily used as office and warehouse.

Group | Location | Approx. Square Feet | ||

Industrial | Camanche, IA | 95,000 | ||

Centralia, IL (1) | 77,000 | |||

Dupo, IL (2) | 64,000 | |||

St. Paul, MN (3) | 32,000 | |||

Rosemount, MN (4) | 63,000 | |||

St Louis, MO | 6,000 | |||

Water Treatment | Ft. Smith, AR (5) | 17,000 | ||

Apopka, FL | 32,100 | |||

Big Pine Key, FL (5) | 4,200 | |||

Hollywood, FL (5) | 5,400 | |||

LaBelle, FL (5) | 8,200 | |||

Thomasville, GA (5) | 35,800 | |||

Brooker, FL | 4,640 | |||

Tarrytown, FL (5) | 6,500 | |||

Swainsboro, GA | 57,000 | |||

Eldridge, IA | 6,000 | |||

Slater, IA | 12,000 | |||

Centralia, IL | 39,000 | |||

Havana, IL | 16,000 | |||

Peotone, IL (5) | 18,000 | |||

Muncie, IN | 12,000 | |||

Garnett, KS | 18,000 | |||

Frankfort, KY | 20,000 | |||

Columbia, MO (5) | 14,000 | |||

Billings, MT | 9,000 | |||

Fargo, ND | 20,000 | |||

Washburn, ND | 14,000 | |||

Lincoln, NE (5) | 16,000 | |||

Tulsa, OK | 7,300 | |||

Sioux Falls, SD | 27,000 | |||

Rapid City, SD | 9,000 | |||

Fond du Lac, WI | 24,000 | |||

Superior, WI | 17,000 | |||

Industrial and Water Treatment | St. Paul, MN (6) | 59,000 | ||

Memphis, TN | 41,000 | |||

Health and Nutrition | Fullerton, CA (7) | 55,800 | ||

Florida, NY (8) | 107,000 | |||

10

(1) | This facility includes 10 acres of land located in Centralia, Illinois owned by the Company. The facility includes manufacturing capacity and primarily serves our food-grade products and agriculture businesses. |

(2) | The land for this manufacturing and packaging facility is leased from a third party, with the lease expiring in May 2023. |

(3) | Our terminal operations, located at two sites on opposite sides of the Mississippi River, are made up of three buildings, outside storage tanks for the storage of liquid bulk chemicals, including caustic soda, as well as numerous smaller tanks for storing and mixing chemicals. The land is leased from the Port Authority of the City of St. Paul, Minnesota. One of the applicable leases runs through 2028, while the other one runs through 2034. |

(4) | This facility includes 28 acres of land owned by the Company. This manufacturing facility was constructed by us and has outside storage tanks for the storage of bulk chemicals, as well as numerous smaller tanks for storing and mixing chemicals. |

(5) | This facility is leased from a third party and is warehouse space. |

(6) | Our Red Rock facility, which consists of a 59,000 square-foot building located on approximately 10 acres of land, has outside storage capacity for liquid bulk chemicals, as well as numerous smaller tanks for storing and mixing chemicals. The land is leased from the Port Authority of the City of St. Paul, Minnesota and the lease runs until 2029. |

(7) | This is a leased facility comprising administrative offices and a distribution facility. The lease runs through January 2021. |

(8) | This is comprised of a 79,000 square foot manufacturing plant which sits on approximately 16 acres, as well as a leased 28,000 square foot warehouse located in close proximity. |

ITEM 3. LEGAL PROCEEDINGS

There are no material pending legal proceedings, other than ordinary routine litigation incidental to the business, to which we or any of our subsidiaries are a party or of which any of our property is the subject.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

11

PART II

ITEM 5. MARKET FOR THE COMPANY’S COMMON EQUITY, RELATED SHAREHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

Quarterly Stock Data | High | Low | |||||||

Fiscal 2017 | |||||||||

4th Quarter | $ | 54.80 | $ | 46.55 | |||||

3rd Quarter | 54.50 | 38.60 | |||||||

2nd Quarter | 45.50 | 40.62 | |||||||

1st Quarter | 45.65 | 35.44 | |||||||

Fiscal 2016 | |||||||||

4th Quarter | $ | 37.63 | $ | 30.53 | |||||

3rd Quarter | 43.17 | 34.74 | |||||||

2nd Quarter | 44.00 | 33.94 | |||||||

1st Quarter | 43.75 | 37.45 | |||||||

Cash Dividends | Declared | Paid | |||||||

Fiscal 2018 | |||||||||

1st Quarter | — | $ | 0.42 | ||||||

Fiscal 2017 | |||||||||

4th Quarter | $ | 0.42 | — | ||||||

3rd Quarter | — | $ | 0.42 | ||||||

2nd Quarter | $ | 0.42 | — | ||||||

1st Quarter | — | $ | 0.40 | ||||||

Fiscal 2016 | |||||||||

4th Quarter | $ | 0.40 | — | ||||||

3rd Quarter | — | $ | 0.40 | ||||||

2nd Quarter | $ | 0.40 | — | ||||||

1st Quarter | — | $ | 0.38 | ||||||

Our common shares are traded on The NASDAQ Global Market under the symbol “HWKN.” The price information represents sales prices as reported by The NASDAQ Global Market. As of May 26, 2017, shares of our common stock were held by approximately 422 shareholders of record.

We first started paying cash dividends in 1985 and have continued to do so since. Future dividend levels will be dependent upon our consolidated results of operations, financial position, cash flows and other factors, and are subject to approval by our Board of Directors.

We had the following share repurchase activity in the fourth quarter of fiscal 2017:

Period | Total Number of Shares Purchased | Average Price Paid Per Share | Total Number of Shares Purchased as Part of a Publicly Announced Plan or Program | Maximum Number of Shares that May Yet be Purchased under Plans or Programs (2) | |||||

1/2/2017-1/29/2017 | — | — | — | 112,546 | |||||

1/30/2017-2/26/2017 | — | — | — | 112,546 | |||||

2/26/2017-04/2/2017 | 13,015 | (1) | 48.45 | — | 112,546 | ||||

Total | 13,015 | — | — | ||||||

12

(1) The shares of common stock in this row represent shares that were surrendered to us by stock plan participants to satisfy minimum withholding tax obligations related to the vesting of restricted stock awards and are not shares purchased under the Board of Directors authorization described above.

(2) Our Board of Directors has authorized a share repurchase program of up to 300,000 shares of our outstanding common stock. The shares may be repurchased on the open market or in privately negotiated transactions subject to applicable securities laws and regulations. We did not sell or purchase any shares of our common stock during fiscal 2017. As of April 2, 2017, the maximum number of shares available to be repurchased under the share repurchase program was 112,546.

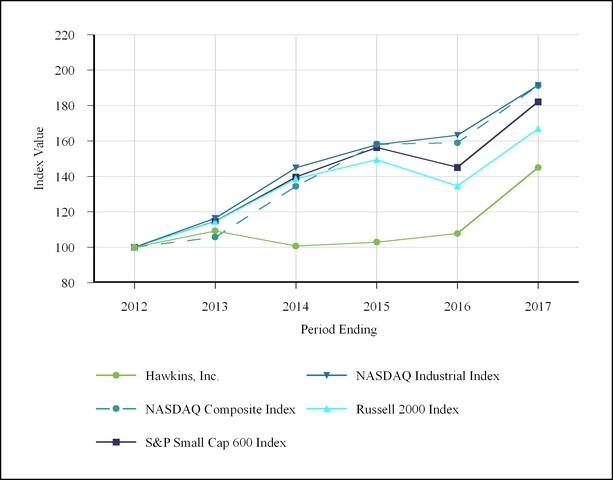

The following graph compares the cumulative total shareholder return on our common shares with the cumulative total returns of the NASDAQ Industrial Index, the NASDAQ Composite Index, the Russell 2000 Index and the Standard & Poor’s (“S&P”) Small Cap 600 Index for our last five completed fiscal years. The graph assumes the investment of $100 in our stock, the NASDAQ Industrial Index, the NASDAQ Composite Index, the Russell 2000 Index and the S&P Small Cap 600 Index on April 1, 2012, and reinvestment of all dividends.

13

ITEM 6. SELECTED FINANCIAL DATA

Selected financial data for the Company is presented in the table below and should be read in conjunction with Management’s Discussion and Analysis of Financial Condition and Results of Operations included in Item 7 and the Company’s Financial Statements and Notes to Financial Statements included in Item 8 of this Annual Report on Form 10-K. Total assets shown below are for the Company’s total operations.

Fiscal Year | |||||||||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||||

(In thousands, except per share data) | |||||||||||||||||||||

Sales | $ | 483,593 | $ | 413,976 | $ | 364,023 | $ | 348,263 | $ | 350,387 | |||||||||||

Gross profit | 98,073 | 80,257 | 65,791 | 61,600 | 56,936 | ||||||||||||||||

Net Income (1) | 22,555 | 18,143 | 19,214 | 18,094 | 17,108 | ||||||||||||||||

Basic earnings per common share | 2.14 | 1.72 | 1.82 | 1.72 | 1.64 | ||||||||||||||||

Diluted earnings per common share | 2.13 | 1.72 | 1.81 | 1.71 | 1.62 | ||||||||||||||||

Cash dividends declared per common share | 0.84 | 0.80 | 0.76 | 0.72 | 0.68 | ||||||||||||||||

Cash dividends paid per common share | 0.82 | 0.78 | 0.74 | 0.70 | 0.66 | ||||||||||||||||

Total assets | $ | 418,584 | $ | 436,491 | $ | 248,462 | $ | 237,193 | $ | 222,148 | |||||||||||

(1) - The reported number for fiscal 2013 is net income from continuing operations.

We acquired Stauber Performance Ingredients near the end of the third quarter of fiscal 2016, and we acquired substantially all the assets of Davis Supply, Inc. near the end of the second quarter of fiscal 2016 and The Dumont Company, Inc. in the third quarter of fiscal 2015. The results of these operations since the acquisition dates are included in our consolidated results of operations.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following is a discussion and analysis of our financial condition and results of operations for fiscal 2017, 2016 and 2015. Fiscal 2016 was a 53-week year, whereas fiscal 2017 and 2015 were 52-week years. This discussion should be read in conjunction with the consolidated Financial Statements and Notes to Consolidated Financial Statements included in Item 8 of this Annual Report on Form 10-K.

Overview

We derive substantially all of our revenues from the sale of chemicals and specialty ingredients to our customers in a wide variety of industries. We began our operations primarily as a distributor of bulk chemicals with a strong customer focus. Over the years, we have maintained the strong customer focus and have expanded our business by increasing our sales of value-added chemical products and specialty ingredients, including manufacturing, blending and repackaging certain products.

Acquisitions and Business Expansion

Near the end of the third quarter of fiscal 2016, we acquired Stauber Performance Ingredients (“Stauber”) for $157.0 million on a cash-free, debt-free basis, subject to a customary working capital adjustment. The total consideration for the acquisition was $158.2 million ($156.7 million net of cash acquired). Stauber operates out of facilities in New York and California and blends and distributes specialty products and ingredients to manufacturers of nutraceutical, functional food and beverage, personal care, dietary supplement, and other nutritional food, health and wellness products. The acquisition expanded our portfolio of value-added specialty products within new markets. The results of operations since the acquisition date, and the assets, including the goodwill associated with the acquisition, are reported in our Health and Nutrition operating segment, starting with our results for the fourth quarter of fiscal 2016. Direct costs of $3.3 million related to this acquisition, consisting mainly of professional and consulting fees, were expensed as incurred during the fiscal year, and are classified as selling, general and administrative expenses in our consolidated statement of income.

14

In the second quarter of fiscal 2016, we acquired substantially all the assets of Davis Supply, Inc. (“Davis”) for $4.5 million under the terms of an asset purchase agreement with Davis and its shareholders. Davis was a water treatment chemical distribution company operating in Florida, and upon acquisition we integrated this business into our existing Florida locations. The results of operations after the date of acquisition and the acquired assets are included in our Water Treatment Segment.

In the third quarter of fiscal 2015, we acquired substantially all the assets of The Dumont Company, Inc. (“Dumont”) for $10.1 million under the terms of an asset purchase agreement with Dumont and its shareholders. Dumont was a water treatment chemical distribution company serving municipal water and wastewater treatment, private utilities, commercial swimming pools, irrigation water treatment and food processing chemical markets. Through this acquisition we added seven operating locations across Florida. The results of operations since the acquisition date are included in our Water Treatment Segment.

In addition to the acquisitions discussed above, we opened two new branches for our Water Treatment Group in fiscal 2016. We expect to continue to invest in existing and new branches to expand our Water Treatment Group’s geographic coverage. The cost of any one of these expansion branches is not expected to be material. In addition, over the past three years, we have proactively added route sales and other support personnel to Water Treatment Group branch offices within our existing geographic coverage area. While these additions add costs in the near term, we expect these investments to better position us for future growth.

New Operating Segment

In connection with the Stauber acquisition in fiscal 2016, we established our Health and Nutrition operating segment. This segment specializes in providing ingredient distribution, processing and formulation solutions to manufacturers of nutraceutical, functional food and beverage, personal care, dietary supplement and other nutritional food, health and wellness products. This group offers a diverse product portfolio including minerals, botanicals and herbs, vitamins and amino acids, excipients, joint products, sweeteners and enzymes.

Because this segment began in the fourth quarter of fiscal 2016, there is no comparison to the prior year in the fiscal 2016 to fiscal 2015 year-over-year discussion below.

Share Repurchase Program

In fiscal 2015, our Board of Directors authorized a share repurchase program of up to 300,000 shares of our outstanding common stock. The shares may be repurchased on the open market or in privately negotiated transactions subject to applicable securities laws and regulations. The primary objective of the share repurchase program is to offset the impact of dilution from issuances relating to employee and director equity grants and our employee stock purchase program. No shares were repurchased during fiscal 2017. During fiscal 2016, we repurchased 127,852 shares of common stock with an aggregate purchase price of $4.8 million, and during fiscal 2015 we repurchased 59,602 shares of common stock with an aggregate purchase price of $2.2 million. The remaining balance of shares available to be purchased under the share repurchase program is 112,546 shares.

Financial Overview

An overview of our financial performance in fiscal 2017 is provided below:

• | Sales of $483.6 million, a 16.8% increase from fiscal 2016; |

• | Gross profit of $98.1 million, a $17.8 million, or 22.2%, increase from fiscal 2016; and |

• | Net cash provided by operating activities of $44.9 million. |

We seek to maintain relatively constant gross profit dollars per unit sold on each of our products as the cost of our raw materials increase or decrease, subject to competitive pricing pressures that may negatively impact our gross profit dollars per unit sold. Since we expect that we will continue to experience fluctuations in our raw material costs and resulting prices in the future, we believe that gross profit dollars is the best measure of our profitability from the sale of our products, as opposed to gross profit as a percentage of sales.

We use the last in, first out (“LIFO”) method of valuing the majority of our inventory, which causes the most recent product costs to be recognized in our income statement. The valuation of LIFO inventory for interim periods is based on our estimates of fiscal year-end inventory levels and costs. The LIFO inventory valuation method and the resulting cost of sales are consistent with our business practices of pricing to current chemical raw material prices. Our LIFO reserve decreased by $2.7 million in fiscal 2017 due to a reduction in inventory costs per unit over a wide variety of products and lower volumes of certain inventory on hand,

15

resulting in an increase to our reported gross profit for the year. Our LIFO reserve decreased by $1.4 million in fiscal 2016 due to a decrease in certain inventory volumes on hand, along with lower commodity prices, resulting in an increase to our reported gross profit for the year.

We disclose the sales of our bulk commodity products as a percentage of total sales dollars for our Industrial and Water Treatment segments. Our definition of bulk commodity products includes products that we do not modify in any way, but receive, store, and ship from our facilities, or direct ship to our customers in large quantities. We review our sales reporting on a periodic basis to ensure we are including all products that meet this definition. The disclosures in this document referring to sales of bulk commodity products have been updated for all periods presented based on the most recent review.

Results of Operations

The following table sets forth certain items from our statement of income as a percentage of sales from period to period:

Fiscal 2017 | Fiscal 2016 | Fiscal 2015 | |||||||

Sales | 100.0 | % | 100.0 | % | 100.0 | % | |||

Cost of sales | (79.7 | )% | (80.6 | )% | (81.9 | )% | |||

Gross profit | 20.3 | % | 19.4 | % | 18.1 | % | |||

Selling, general and administrative expenses | (12.3 | )% | (11.9 | )% | (9.7 | )% | |||

Operating income | 8.0 | % | 7.5 | % | 8.4 | % | |||

Interest (expense) income, net | (0.5 | )% | (0.2 | )% | — | % | |||

Income before income taxes | 7.5 | % | 7.3 | % | 8.4 | % | |||

Income tax provision | (2.8 | )% | (3.0 | )% | (3.1 | )% | |||

Net income | 4.7 | % | 4.4 | % | 5.3 | % | |||

Fiscal 2017 Compared to Fiscal 2016

Sales

Sales increased $69.6 million, or 16.8%, to $483.6 million for fiscal 2017, as compared to sales of $414.0 million for fiscal 2016. Fiscal 2017 includes a full year of operating results for our Health and Nutrition segment whereas fiscal 2016 included only one quarter of Health and Nutrition segment results due to the timing of the Stauber acquisition.

Industrial Segment. Industrial segment sales decreased $13.2 million, or 5.2%, to $238.6 million for fiscal 2017. Sales of bulk commodity products in the Industrial segment were approximately 19% of sales in fiscal 2017 compared to 20% in fiscal 2016. Sales volumes were down year over year, largely driven by the 53rd week in the prior year. These lower volumes, together with lower raw material costs on certain products which drove lower selling prices, resulted in the decrease in sales dollars.

Water Treatment Segment. Water Treatment segment sales increased $0.6 million, or 0.5%, to $129.0 million for fiscal 2017. Sales of bulk commodity products in the Water Treatment segment were approximately 15% of sales in fiscal 2017 compared to 16% in fiscal 2016. Sales dollars increased slightly, despite the inclusion of the 53rd week in the prior year, due to the business we acquired late in the second quarter of fiscal 2016 and increased volumes of specialized products.

Health and Nutrition Segment. Sales for our Health and Nutrition segment were $116.1 million in fiscal 2017, compared to $33.9 million for fiscal 2016, as the prior year included only one quarter of activity due to the timing of the Stauber acquisition. This compares to pro forma sales of $121.6 million for the comparable prior full-year period, which included the 53rd week.

Gross Profit

Gross profit was $98.1 million, or 20.3% of sales, for fiscal 2017, an increase of $17.8 million from $80.3 million, or 19.4% of sales, for fiscal 2016. The current year includes a full year of operating results for our Health and Nutrition segment as opposed to just one quarter of Health and Nutrition segment results in the prior year due to the timing of the Stauber acquisition. We estimated the total gross profit impact of the 53rd week in fiscal 2016 year to be approximately $2.1 million of additional gross profit in that year. The LIFO method of valuing inventory increased gross profit by $2.7 million for fiscal 2017, and increased gross profit by $1.4 million for fiscal 2016.

16

Industrial Segment. Gross profit for the Industrial segment was $38.9 million, or 16.3% of sales, for fiscal 2017, an increase of $0.9 million from $38.0 million, or 15.1% of sales, for fiscal 2016. The LIFO method of valuing inventory increased gross profit by $2.0 million in the current year and $1.0 million in the prior year. We estimated the gross profit impact of the 53rd week in our Industrial segment in fiscal 2016 to be approximately $1.0 million of additional gross profit in that year. Despite lower sales volumes, driven largely by the 53rd week in the prior year, gross profit dollars increased due to improved per-unit margins from certain of our specialized products, and the year-over-year impact from LIFO. Gross profit as a percentage of sales improved over the prior year because of the same drivers noted above in addition to lower selling prices in the current year driven by lower raw material costs on certain products.

Water Treatment Segment. Gross profit for the Water Treatment segment increased $0.5 million to $36.0 million, or 27.9% of sales, for fiscal 2017, as compared to $35.5 million, or 27.6% of sales, for fiscal 2016. The LIFO method of valuing inventory increased gross profit by $0.7 million in the current and $0.4 million in the prior year. We estimated the gross profit impact of the 53rd week in fiscal 2016 to be approximately $0.6 million of additional gross profit in that year. Gross profit increased due to increased sales volumes of specialized products that have higher per-unit margins as well as profits from the business we acquired late in the second quarter of fiscal 2016.

Health and Nutrition Segment. Gross profit for our Health and Nutrition segment was $23.2 million, or 20.0% of sales, in fiscal 2017, compared to $6.8 million, or 20.1% of sales, for fiscal 2016, as the prior year included only one quarter of activity due to the timing of the Stauber acquisition. Inventories in this segment are valued using the first-in, first-out (“FIFO”) method. We estimated the gross profit impact of the 53rd week in fiscal 2016 to be approximately $0.5 million of additional gross profit in that year.

Selling, General and Administrative Expenses

Selling, general and administrative (“SG&A”) expenses increased $10.3 million to $59.4 million, or 12.3% of sales, for fiscal 2017, as compared to $49.1 million, or 11.9% of sales, for fiscal 2016. We estimated the total impact to SG&A expenses of the 53rd week in fiscal 2016 to be approximately $0.9 million of additional expense in that year. We allocate certain corporate expenses to our operating segments, and we began allocating a portion of these costs to the Health and Nutrition segment in fiscal 2017. Corporate costs allocated to Health and Nutrition were $1.9 million for fiscal 2017; these costs would have been allocated to Industrial (approximately $1.2 million) and Water Treatment (approximately $0.7 million) in past years. Excluding the impact of corporate allocations, SG&A expenses in our Health and Nutrition segment increased by $8.1 million in fiscal 2017 as compared to fiscal 2016. Fiscal 2016 included only one quarter of activity due to the timing of the Stauber acquisition, and included $3.3 million of non-recurring costs directly related to the Stauber acquisition. SG&A expenses in our Health and Nutrition segment include $4.8 million of amortization expense on acquired intangible assets in fiscal 2017 and $1.2 million in fiscal 2016. SG&A expenses incurred elsewhere in the company increased by $2.2 million compared to the prior year, largely due to the addition of sales and support personnel in our Industrial and Water Treatment segments.

Operating Income

Operating income was $38.7 million, or 8.0% of sales, for fiscal 2017, as compared to $31.2 million, or 7.5% of sales, for fiscal 2016. Operating income reported in our segments is impacted by corporate allocations of certain SG&A costs. After corporate allocations, operating income in our Health and Nutrition segment was $5.5 million for fiscal 2017, compared to a loss of $0.9 million for fiscal 2016, which included only one quarter of operations and included $3.3 million of expenses related to our acquisition of Stauber. Operating income in our Industrial segment increased by $1.2 million primarily as a result of the gross profit improvement discussed above. Operating income for the Water Treatment segment was flat compared to the prior year as the increase in gross profit was offset by increased SG&A expenses.

Interest (Expense) Income, Net

Interest expense increased by $1.8 million for fiscal 2017 due to the interest costs on the debt added at the end of the third quarter of fiscal 2016 to partially fund the Stauber acquisition.

Income Tax Provision

Our effective income tax rate was 37.4% for fiscal 2017 compared to 40.2% for fiscal 2016. Our effective tax rate for fiscal 2016 was negatively impacted by income tax expense of approximately $0.5 million associated with $1.4 million of Stauber acquisition related expenditures which were not deductible for tax purposes and were recorded as discrete items during fiscal 2016. Our effective tax rate for 2016 was also negatively impacted by $0.2 million related to a preliminary audit finding by a state income

17

tax jurisdiction covering multiple years. The effective tax rate is generally impacted by projected levels of taxable income, permanent items, and state taxes.

Fiscal 2016 Compared to Fiscal 2015

Sales

Sales increased $50.0 million, or 13.7%, to $414.0 million for fiscal 2016, as compared to sales of $364.0 million for fiscal 2015. Our newly-established Health and Nutrition segment accounted for $33.9 million of the year-over-year increase and water treatment locations acquired in fiscal 2015 and 2016 accounted for $12.6 million of the increase.

Industrial Segment. Industrial segment sales increased $2.7 million, or 1.1%, to $251.7 million for fiscal 2016. Sales of bulk commodity products in the Industrial segment were approximately 20% of sales in fiscal 2016 compared to 23% in fiscal 2015. An overall increase in sales volumes, driven in part by the 53rd week in fiscal 2016, along with a shift in product mix to more sales of products that carry higher per-unit selling prices, more than offset the impact of lower selling prices due to lower product costs and lower volumes sold on certain bulk commodity products.