Attached files

| file | filename |

|---|---|

| EX-32 - EX-32 - PEGASYSTEMS INC | d344763dex32.htm |

| EX-31.2 - EX-31.2 - PEGASYSTEMS INC | d344763dex312.htm |

| EX-31.1 - EX-31.1 - PEGASYSTEMS INC | d344763dex311.htm |

| EX-10.4 - EX-10.4 - PEGASYSTEMS INC | d344763dex104.htm |

| EX-10.3 - EX-10.3 - PEGASYSTEMS INC | d344763dex103.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| ☒ | Quarterly Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the quarterly period ended March 31, 2017

or

| ☐ | Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File Number: 1-11859

PEGASYSTEMS INC.

(Exact name of Registrant as specified in its charter)

| Massachusetts | 04-2787865 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

| One Rogers Street, Cambridge, MA | 02142-1209 | |

| (Address of principal executive offices) | (Zip Code) |

(617) 374-9600

(Registrant’s telephone number including area code)

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company,” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☒ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ (Do not check if smaller reporting company) | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

There were 77,142,095 shares of the Registrant’s common stock, $.01 par value per share, outstanding on April 28, 2017.

Table of Contents

PEGASYSTEMS INC.

| Page | ||||||

| Part I - Financial Information | ||||||

| Item 1. |

||||||

| Unaudited Condensed Consolidated Balance Sheets as of March 31, 2017 and December 31, 2016 |

3 | |||||

| 4 | ||||||

| 5 | ||||||

| 6 | ||||||

| Notes to Unaudited Condensed Consolidated Financial Statements |

7 | |||||

| Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

17 | ||||

| Item 3. |

26 | |||||

| Item 4. |

26 | |||||

| Part II - Other Information | ||||||

| Item 1A. |

28 | |||||

| Item 2. |

28 | |||||

| Item 6. |

28 | |||||

| 29 | ||||||

2

Table of Contents

Item 1. Unaudited Condensed Financial Statements:

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands)

| March 31, 2017 |

December 31, 2016 |

|||||||

| ASSETS | ||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 83,838 | $ | 70,594 | ||||

| Marketable securities |

63,948 | 63,167 | ||||||

|

|

|

|

|

|||||

| Total cash, cash equivalents, and marketable securities |

147,786 | 133,761 | ||||||

| Trade accounts receivable, net of allowance of $4,780 and $4,126 |

263,310 | 265,028 | ||||||

| Income taxes receivable |

10,827 | 14,155 | ||||||

| Other current assets |

19,652 | 12,188 | ||||||

|

|

|

|

|

|||||

| Total current assets |

441,575 | 425,132 | ||||||

| Property and equipment, net |

39,947 | 38,281 | ||||||

| Deferred income taxes |

69,846 | 69,898 | ||||||

| Long-term other assets |

4,445 | 3,990 | ||||||

| Intangible assets, net |

40,998 | 44,191 | ||||||

| Goodwill |

72,828 | 73,164 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 669,639 | $ | 654,656 | ||||

|

|

|

|

|

|||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities: |

||||||||

| Accounts payable |

$ | 14,237 | $ | 14,414 | ||||

| Accrued expenses |

38,545 | 36,751 | ||||||

| Accrued compensation and related expenses |

39,958 | 60,660 | ||||||

| Deferred revenue |

186,824 | 175,647 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

279,564 | 287,472 | ||||||

| Income taxes payable |

4,307 | 4,263 | ||||||

| Long-term deferred revenue |

9,958 | 10,989 | ||||||

| Other long-term liabilities |

15,733 | 16,043 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

309,562 | 318,767 | ||||||

|

|

|

|

|

|||||

| Stockholders’ equity: |

||||||||

| Preferred stock, 1,000 shares authorized; no shares issued and outstanding |

— | — | ||||||

| Common stock, 200,000 shares authorized; 77,129 shares and 76,591 shares issued and outstanding |

771 | 766 | ||||||

| Additional paid-in capital |

142,472 | 143,903 | ||||||

| Retained earnings |

223,021 | 198,315 | ||||||

| Accumulated other comprehensive loss |

(6,187 | ) | (7,095 | ) | ||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

360,077 | 335,889 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 669,639 | $ | 654,656 | ||||

|

|

|

|

|

|||||

See notes to unaudited condensed consolidated financial statements.

3

Table of Contents

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share amounts)

| Three Months Ended March 31, |

||||||||

| 2017 | 2016 | |||||||

| Revenue: |

||||||||

| Software license |

$ | 92,390 | $ | 68,345 | ||||

| Maintenance |

58,965 | 52,975 | ||||||

| Services |

71,892 | 57,538 | ||||||

|

|

|

|

|

|||||

| Total revenue |

223,247 | 178,858 | ||||||

|

|

|

|

|

|||||

| Cost of revenue: |

||||||||

| Software license |

1,300 | 1,021 | ||||||

| Maintenance |

7,218 | 5,915 | ||||||

| Services |

59,572 | 49,574 | ||||||

|

|

|

|

|

|||||

| Total cost of revenue |

68,090 | 56,510 | ||||||

|

|

|

|

|

|||||

| Gross profit |

155,157 | 122,348 | ||||||

|

|

|

|

|

|||||

| Operating expenses: |

||||||||

| Selling and marketing |

71,288 | 61,078 | ||||||

| Research and development |

40,296 | 34,920 | ||||||

| General and administrative |

12,335 | 11,048 | ||||||

| Acquisition-related |

— | 919 | ||||||

| Restructuring |

— | 258 | ||||||

|

|

|

|

|

|||||

| Total operating expenses |

123,919 | 108,223 | ||||||

|

|

|

|

|

|||||

| Income from operations |

31,238 | 14,125 | ||||||

| Foreign currency transaction gain |

676 | 1,376 | ||||||

| Interest income, net |

165 | 290 | ||||||

| Other expense, net |

(279 | ) | (2,298 | ) | ||||

|

|

|

|

|

|||||

| Income before provision for income taxes |

31,800 | 13,493 | ||||||

| Provision for income taxes |

4,779 | 3,093 | ||||||

|

|

|

|

|

|||||

| Net income |

$ | 27,021 | $ | 10,400 | ||||

|

|

|

|

|

|||||

| Earnings per share: |

||||||||

| Basic |

$ | 0.35 | $ | 0.14 | ||||

|

|

|

|

|

|||||

| Diluted |

$ | 0.33 | $ | 0.13 | ||||

|

|

|

|

|

|||||

| Weighted-average number of common shares outstanding: |

| |||||||

| Basic |

76,761 | 76,375 | ||||||

| Diluted |

81,875 | 79,235 | ||||||

| Cash dividends declared per share |

$ | 0.03 | $ | 0.03 | ||||

|

|

|

|

|

|||||

See notes to unaudited condensed consolidated financial statements.

4

Table of Contents

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(in thousands)

| Three Months Ended March 31, |

||||||||

| 2017 | 2016 | |||||||

| Net income |

$ | 27,021 | $ | 10,400 | ||||

| Other comprehensive income, net: |

||||||||

| Unrealized gain on available-for-sale marketable securities, net of tax |

127 | 286 | ||||||

| Foreign currency translation adjustments |

781 | (7 | ) | |||||

|

|

|

|

|

|||||

| Total other comprehensive income, net |

908 | 279 | ||||||

|

|

|

|

|

|||||

| Comprehensive income |

$ | 27,929 | $ | 10,679 | ||||

|

|

|

|

|

|||||

See notes to unaudited condensed consolidated financial statements.

5

Table of Contents

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

| Three Months Ended March 31, |

||||||||

| 2017 | 2016 | |||||||

| Operating activities: |

||||||||

| Net income |

$ | 27,021 | $ | 10,400 | ||||

| Adjustments to reconcile net income to cash provided by operating activities: |

||||||||

| Deferred income taxes |

727 | 650 | ||||||

| Depreciation and amortization |

6,088 | 5,466 | ||||||

| Stock-based compensation expense |

12,508 | 8,935 | ||||||

| Foreign currency transaction gain |

(676 | ) | (1,376 | ) | ||||

| Other non-cash |

(379 | ) | 2,712 | |||||

| Change in operating assets and liabilities: |

||||||||

| Trade accounts receivable |

3,383 | 6,697 | ||||||

| Income taxes receivable and other current assets |

(4,382 | ) | (201 | ) | ||||

| Accounts payable and accrued expenses |

(21,193 | ) | (24,822 | ) | ||||

| Deferred revenue |

9,412 | 1,129 | ||||||

| Other long-term assets and liabilities |

(65 | ) | 450 | |||||

|

|

|

|

|

|||||

| Cash provided by operating activities |

32,444 | 10,040 | ||||||

|

|

|

|

|

|||||

| Investing activities: |

||||||||

| Purchases of marketable securities |

(3,322 | ) | (8,193 | ) | ||||

| Proceeds from maturities and called marketable securities |

2,300 | 15,890 | ||||||

| Sales of marketable securities |

— | 6,179 | ||||||

| Payments for acquisitions, net of cash acquired |

(290 | ) | (255 | ) | ||||

| Investment in property and equipment |

(2,415 | ) | (4,251 | ) | ||||

|

|

|

|

|

|||||

| Cash (used in) provided by investing activities |

(3,727 | ) | 9,370 | |||||

|

|

|

|

|

|||||

| Financing activities: |

||||||||

| Issuance of common stock for share-based compensation plans |

68 | 44 | ||||||

| Dividend payments to shareholders |

(2,298 | ) | (2,297 | ) | ||||

| Common stock repurchases for tax withholdings for net settlement of equity awards and under share repurchase programs |

(13,764 | ) | (17,569 | ) | ||||

|

|

|

|

|

|||||

| Cash used in financing activities |

(15,994 | ) | (19,822 | ) | ||||

|

|

|

|

|

|||||

| Effect of exchange rates on cash and cash equivalents |

521 | (434 | ) | |||||

|

|

|

|

|

|||||

| Net increase (decrease) in cash and cash equivalents |

13,244 | (846 | ) | |||||

| Cash and cash equivalents, beginning of period |

70,594 | 93,026 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents, end of period |

$ | 83,838 | $ | 92,180 | ||||

|

|

|

|

|

|||||

See notes to unaudited condensed consolidated financial statements.

6

Table of Contents

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1. BASIS OF PRESENTATION

Pegasystems Inc. (together with its subsidiaries, “the Company”) has prepared the accompanying unaudited condensed consolidated financial statements pursuant to the rules and regulations of the U.S. Securities and Exchange Commission (“SEC”) regarding interim financial reporting. Accordingly, they do not include all of the information and footnotes required by accounting principles generally accepted in the United States of America (“U.S.”) for complete financial statements and should be read in conjunction with the Company’s audited financial statements included in the Annual Report on Form 10-K for the year ended December 31, 2016.

In the opinion of management, the Company has prepared the accompanying unaudited condensed consolidated financial statements on the same basis as its audited financial statements, and these financial statements include all adjustments, consisting only of normal recurring adjustments, necessary for a fair presentation of the results of the interim periods presented. The operating results for the interim periods presented are not necessarily indicative of the results expected for the full year 2017.

2. NEW ACCOUNTING PRONOUNCEMENTS

Financial Instruments: In June 2016, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2016-13, “Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments,” which requires measurement and recognition of expected credit losses for financial assets measured at amortized cost, including trade accounts receivable, upon initial recognition of that financial asset using a forward-looking expected loss model, rather than an incurred loss model for credit losses. Credit losses relating to available-for-sale debt securities should be recorded through an allowance for credit losses when the fair value is below the amortized cost of the asset, removing the concept of “other-than-temporary” impairments. The effective date for the Company will be January 1, 2020, with early adoption permitted. The Company is currently evaluating the effect this ASU will have on its consolidated financial statements and related disclosures.

Leases: In February 2016, the FASB issued ASU No. 2016-02, “Leases (Topic 842),” which requires lessees to record most leases on their balance sheets, recognizing a lease liability for the obligation to make lease payments and a right-of-use asset for the right to use the underlying asset for the lease term. The effective date for the Company will be January 1, 2019, with early adoption permitted. The Company currently expects that most of its operating lease commitments will be subject to this ASU and recognized as operating lease liabilities and right-of-use assets upon adoption with no material impact to its results of operations and cash flows.

Revenue: In May 2014, the FASB issued ASU No. 2014-09, “Revenue from Contracts with Customers (Topic 606)”. This ASU, including subsequently issued amendments, amends the guidance for revenue recognition, creating the new Accounting Standards Codification Topic 606 (“ASC 606”). ASC 606 requires entities to apportion consideration from contracts to performance obligations on a relative standalone selling price basis, based on a five-step model. Under ASC 606, revenue is recognized when a customer obtains control of a promised good or service and is recognized in an amount that reflects the consideration which the entity expects to receive in exchange for the good or service. ASC 606 also requires disclosure of the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers.

The Company has elected the full retrospective adoption model, effective January 1, 2018. The Company’s quarterly results beginning with the quarter ending March 31, 2018 and comparative prior periods will be compliant with ASC 606. The Company’s Annual Report on Form 10-K for the year ended December 31, 2018 will be the Company’s first Annual Report that will be issued in compliance with ASC 606.

7

Table of Contents

The Company is still in the process of quantifying the implications of the adoption of ASC 606. However the Company currently expects the following impacts:

| • | Currently, the Company recognizes revenue from term licenses and perpetual licenses with extended payment terms over the term of the agreement as payments become due or earlier if prepaid, provided all other criteria for revenue recognition have been met, and any corresponding maintenance over the maintenance term. The adoption of ASC 606 will result in revenue for performance obligations being recognized as they are satisfied. Therefore, revenue from the term license and perpetual performance obligation with extended payment terms is expected to be recognized when control is transferred to the customer and revenue from the maintenance performance obligation is expected to be recognized on a straight-line basis over the contractual maintenance term. This will result in revenue from term licenses and perpetual licenses with extended payment terms being recognized prior to amounts being billed to the customer, and in these cases the Company expects to recognize a net contract asset on the balance sheet. |

| • | Currently, the Company allocates revenue to licenses under the residual method when it has VSOE for the remaining undelivered elements which allocates any future credits or significant discounts entirely to the license. The adoption of ASC 606 will result in the future credits, significant discounts, and material rights under ASC 606, being allocated to all performance obligations based upon their relative selling price. Under ASC 606, additional license revenue from the reallocation of such arrangement considerations will be recognized when control is transferred to the customer. |

| • | Currently, the Company does not have VSOE for fixed price services, time and materials services in certain geographical areas, and unspecified future products, which results in revenue being deferred in such instances until such time as VSOE exists for all undelivered elements or recognized ratably over the longest performance period. The adoption of ASC 606 eliminates the requirement for VSOE and replaces it with the concept of a stand-alone selling price. Once the transaction price is allocated to each of the performance obligations the Company can recognize revenue as the performance obligations are delivered, either at a point in time or over time. Under ASC 606, license revenue will be recognized when control is transferred to the customer. |

| • | Sales commissions and other third party acquisition costs resulting directly from securing contracts with customers are currently expensed when incurred. ASC 606 will require these costs to be recognized as an asset when incurred and to be expensed over the associated contract term. As a practical expedient, if the term of the contract is one year or less, the Company will expense the costs resulting directly from securing the contracts with customers. The Company expects this to impact its multi-year cloud offerings and licenses with additional rights of use that extend beyond one year. |

| • | ASC 606 provides additional accounting guidance for contract modifications whereby changes must be accounted for either as a retrospective change (creating either a catch up or deferral of past revenues), prospectively with a reallocation of revenues amongst identified performance obligations, or prospectively as separate contracts which will not require any reallocation. This may result in a difference in the timing of the recognition of revenue as compared to how current contract modifications are recognized. |

| • | There will be a corresponding effect on tax liabilities in relation to all of the above impacts. |

8

Table of Contents

3. MARKETABLE SECURITIES

| March 31, 2017 | ||||||||||||||||

| (in thousands) | Amortized Cost |

Unrealized Gains |

Unrealized Losses |

Fair Value | ||||||||||||

| Municipal bonds |

$ | 36,944 | $ | 15 | $ | (38 | ) | $ | 36,921 | |||||||

| Corporate bonds |

27,057 | 2 | (32 | ) | 27,027 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | 64,001 | $ | 17 | $ | (70 | ) | $ | 63,948 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| December 31, 2016 | ||||||||||||||||

| (in thousands) | Amortized Cost |

Unrealized Gains |

Unrealized Losses |

Fair Value | ||||||||||||

| Municipal bonds |

$ | 36,746 | $ | — | $ | (139 | ) | $ | 36,607 | |||||||

| Corporate bonds |

26,610 | 1 | (51 | ) | 26,560 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | 63,356 | $ | 1 | $ | (190 | ) | $ | 63,167 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The Company considers debt securities with maturities of three months or less from the purchase date to be cash equivalents. Interest is recorded when earned. All of the Company’s investments are classified as available-for-sale and are carried at fair value. Unrealized gains and losses considered to be temporary in nature are recorded as a component of accumulated other comprehensive loss, net of related income taxes. The Company reviews all investments for reductions in fair value that are other-than-temporary. When such reductions occur, the cost of the investment is adjusted to fair value through recording a loss on investments in the unaudited condensed consolidated statements of operations. Gains and losses on investments are calculated on the basis of specific identification. As of March 31, 2017, the Company did not hold any investments with unrealized losses that are considered to be other-than-temporary.

As of March 31, 2017, remaining maturities of marketable debt securities ranged from April 2017 to August 2019, with a weighted-average remaining maturity of approximately 12 months.

4. DERIVATIVE INSTRUMENTS

The Company uses foreign currency forward contracts (“forward contracts”) to hedge its exposure to fluctuations in foreign currency exchange rates associated with its foreign currency denominated cash, accounts receivable, and intercompany receivables and payables held by its U.S. parent company and United Kingdom (“U.K.”) subsidiary.

The Company is primarily exposed to foreign currency exchange rate fluctuations in the U.S. dollar, the Euro and the Australian dollar relative to the British pound and the Euro and the Indian rupee relative to the U.S. dollar. At the end of June 2016, the U.K. held a referendum in which U.K. voters approved an exit from the European Union (the “E.U.”), commonly referred to as “Brexit”. Uncertainty continues to remain around the future effects of Brexit, resulting in continued volatility in the British pound relative to other currencies. This prolonged weakening of the British pound may continue to result in foreign currency transaction gains from the remeasurement of foreign currency denominated cash and accounts receivable held by the Company’s U.K. subsidiary with corresponding losses on the Company’s forward contracts included in other expense, net.

The forward contracts are not designated as hedging instruments. As a result, the Company records the fair value of these contracts at the end of each reporting period in the accompanying unaudited condensed consolidated balance sheets as other current assets for unrealized gains and accrued expenses for unrealized losses, with any fluctuations in the value of these contracts recognized in other expense, net, in the accompanying unaudited condensed consolidated statements of operations. The cash flows related to these forward contracts are classified as operating activities in the accompanying unaudited condensed consolidated statements of cash flows. The Company does not enter into any forward contracts for trading or speculative purposes.

As of March 31, 2017 and December 31, 2016, the total notional value of the Company’s outstanding forward contracts were $36.8 million and $128.4 million, respectively.

9

Table of Contents

The fair value of the Company’s outstanding forward contracts was as follows:

| (in thousands) | March 31, 2017 |

December 31, 2016 |

||||||||||

| Recorded In: |

Fair Value | Recorded In: |

Fair Value | |||||||||

| Asset Derivatives |

||||||||||||

| Foreign currency forward contracts |

Other current assets | $ | 90 | Other current assets | $ | 628 | ||||||

| Liability Derivatives |

||||||||||||

| Foreign currency forward contracts |

Accrued expenses | $ | 17 | Accrued expenses | $ | 883 | ||||||

The Company had forward contracts outstanding with total notional values as follows:

| As of March 31, 2017 | ||||||||

| Currency (in thousands) | 2017 | 2016 | ||||||

| Euro |

€ | 12,305 | € | 15,590 | ||||

| British pound |

£ | 855 | £ | 2,605 | ||||

| Australian dollar |

A$ | 10,160 | A$ | 16,025 | ||||

| Indian rupee |

Rs | — | Rs | 303,500 | ||||

| United States dollar |

$ | 14,705 | $ | 21,080 | ||||

| Three Months Ended March 31, |

||||||||

| (in thousands) | 2017 | 2016 | ||||||

| Loss from the change in the fair value of forward contracts included in other expense, net |

$ | (279 | ) | $ | (2,297 | ) | ||

| Foreign currency transaction gain from the remeasurement of foreign currency assets and liabilities |

$ | 676 | $ | 1,376 | ||||

|

|

|

|

|

|||||

| Net gain (loss) |

$ | 397 | $ | (921 | ) | |||

|

|

|

|

|

|||||

10

Table of Contents

5. FAIR VALUE MEASUREMENTS

Assets and Liabilities Measured at Fair Value on a Recurring Basis

The Company records its marketable securities and forward contracts at fair value on a recurring basis. Fair value is an exit price, representing the amount that would be received from the sale of an asset or paid to transfer a liability in an orderly transaction between market participants based on assumptions that market participants would use in pricing an asset or liability. As a basis for classifying the fair value measurements, a three-tier fair value hierarchy, which classifies the fair value measurements based on the inputs used in measuring fair value, was established as follows: (Level 1) observable inputs such as quoted prices in active markets for identical assets or liabilities; (Level 2) significant other inputs that are observable either directly or indirectly; and (Level 3) significant unobservable inputs on which there is little or no market data, which require the Company to develop its own assumptions. This hierarchy requires the Company to use observable market data, when available, and to minimize the use of unobservable inputs when determining fair value.

The Company’s money market funds are classified within Level 1 of the fair value hierarchy. The Company’s marketable securities classified within Level 2 of the fair value hierarchy are valued based on a market approach using quoted prices, when available, or matrix pricing compiled by third party pricing vendors, using observable market inputs such as interest rates, yield curves, and credit risk. The Company’s foreign currency forward contracts, which are all classified within Level 2 of the fair value hierarchy, are valued based on the notional amounts and rates under the contracts and observable market inputs such as currency exchange rates and credit risk. If applicable, the Company will recognize transfers into and out of levels within the fair value hierarchy at the end of the reporting period in which the actual event or change in circumstance occurs. There were no transfers between Level 1 and Level 2 during the three months ended March 31, 2017.

The Company’s assets and liabilities measured at fair value on a recurring basis consisted of the following:

| Fair Value Measurements at Reporting Date Using |

||||||||||||

| (in thousands) | March 31, 2017 |

Level 1 | Level 2 | |||||||||

| Fair Value Assets: |

||||||||||||

| Money market funds |

$ | 85 | $ | 85 | $ | — | ||||||

| Marketable securities: |

||||||||||||

| Municipal bonds |

$ | 36,921 | $ | — | $ | 36,921 | ||||||

| Corporate bonds |

27,027 | — | 27,027 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total marketable securities |

$ | 63,948 | $ | — | $ | 63,948 | ||||||

|

|

|

|

|

|

|

|||||||

| Foreign currency forward contracts |

$ | 90 | $ | — | $ | 90 | ||||||

| Fair Value Liabilities: |

||||||||||||

| Foreign currency forward contracts |

$ | 17 | $ | — | $ | 17 | ||||||

|

|

|

|

|

|

|

|||||||

| Fair Value Measurements at Reporting Date Using |

||||||||||||

| (in thousands) | December 31, 2016 |

Level 1 | Level 2 | |||||||||

| Fair Value Assets: |

||||||||||||

| Money market funds |

$ | 458 | $ | 458 | $ | — | ||||||

| Marketable securities: |

||||||||||||

| Municipal bonds |

$ | 36,607 | $ | — | $ | 36,607 | ||||||

| Corporate bonds |

26,560 | — | 26,560 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total marketable securities |

$ | 63,167 | $ | — | $ | 63,167 | ||||||

|

|

|

|

|

|

|

|||||||

| Foreign currency forward contracts |

$ | 628 | $ | — | $ | 628 | ||||||

| Fair Value Liabilities: |

||||||||||||

| Foreign currency forward contracts |

$ | 883 | $ | — | $ | 883 | ||||||

|

|

|

|

|

|

|

|||||||

11

Table of Contents

For certain other financial instruments, including accounts receivable and accounts payable, the carrying value approximates their fair value due to the relatively short maturity of these items.

Assets Measured at Fair Value on a Nonrecurring Basis

Assets recorded at fair value on a nonrecurring basis, such as property and equipment, and intangible assets, are recognized at fair value if they become impaired. During the first three months of 2017 and 2016, the Company did not recognize any impairments of its assets recorded at fair value on a nonrecurring basis.

6. TRADE ACCOUNTS RECEIVABLE, NET OF ALLOWANCE

Unbilled trade accounts receivable primarily relate to services earned under time and materials arrangements and to license, maintenance, and cloud arrangements that have commenced or been delivered in excess of scheduled invoicing.

| (in thousands) | March 31, 2017 |

December 31, 2016 |

||||||

| Trade accounts receivable |

$ | 230,213 | $ | 234,473 | ||||

| Unbilled trade accounts receivable |

37,877 | 34,681 | ||||||

|

|

|

|

|

|||||

| Total accounts receivable |

268,090 | 269,154 | ||||||

|

|

|

|

|

|||||

| Allowance for sales credit memos |

(4,780 | ) | (4,126 | ) | ||||

|

|

|

|

|

|||||

| $ | 263,310 | $ | 265,028 | |||||

|

|

|

|

|

|||||

7. GOODWILL AND OTHER INTANGIBLE ASSETS

The following table presents the changes in the carrying amount of goodwill:

| (in thousands) | 2017 | |||

| Balance as of January 1, |

$ | 73,164 | ||

| Purchase price adjustments to goodwill |

(354 | ) | ||

| Currency translation adjustments |

18 | |||

|

|

|

|||

| Balance as of March 31, |

$ | 72,828 | ||

|

|

|

|||

Intangible assets are recorded at cost and are amortized using the straight-line method over their estimated useful lives.

| (in thousands) | Range of |

Cost | Accumulated Amortization |

Net Book Value |

||||||||||

| As of March 31, 2017 |

||||||||||||||

| Customer related intangibles |

4-10 years | $ | 63,100 | $ | (39,441 | ) | $ | 23,659 | ||||||

| Technology |

3-10 years | 58,942 | (41,603 | ) | 17,339 | |||||||||

| Other intangibles |

3 years | 5,361 | (5,361 | ) | — | |||||||||

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 127,403 | $ | (86,405 | ) | $ | 40,998 | |||||||

|

|

|

|

|

|

|

|||||||||

| As of December 31, 2016 |

||||||||||||||

| Customer related intangibles |

4-10 years | $ | 63,091 | $ | (37,573 | ) | $ | 25,518 | ||||||

| Technology |

3-10 years | 58,942 | (40,269 | ) | 18,673 | |||||||||

| Other intangibles |

3 years | 5,361 | (5,361 | ) | — | |||||||||

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 127,394 | $ | (83,203 | ) | $ | 44,191 | |||||||

|

|

|

|

|

|

|

|||||||||

12

Table of Contents

Amortization expense of acquired intangibles is reflected in the Company’s unaudited condensed consolidated statements of operations as follows:

| Three Months Ended March 31, |

||||||||

| (in thousands) | 2017 | 2016 | ||||||

| Cost of revenue |

$ | 1,334 | $ | 1,346 | ||||

| Selling and marketing |

1,866 | 1,530 | ||||||

| General and administrative |

— | 89 | ||||||

|

|

|

|

|

|||||

| Total amortization expense |

$ | 3,200 | $ | 2,965 | ||||

|

|

|

|

|

|||||

Amortization of intangibles is estimated to be recorded over their remaining useful lives as follows:

|

(in thousands) as of March 31, 2017 |

Future estimated amortization expense |

|||

| Remainder of 2017 |

$ | 9,129 | ||

| 2018 |

11,337 | |||

| 2019 |

5,545 | |||

| 2020 |

2,649 | |||

| 2021 |

2,626 | |||

| 2022 and thereafter |

9,712 | |||

|

|

|

|||

| $ | 40,998 | |||

|

|

|

|||

8. ACCRUED EXPENSES

| (in thousands) | March 31, 2017 |

December 31, 2016 |

||||||

| Partner commissions |

$ | 1,829 | $ | 2,199 | ||||

| Other taxes |

7,418 | 9,031 | ||||||

| Employee reimbursable expenses |

2,280 | 1,624 | ||||||

| Dividends payable |

2,315 | 2,298 | ||||||

| Professional services contractor fees |

6,581 | 6,550 | ||||||

| Self-insurance health and dental claims |

2,324 | 2,182 | ||||||

| Professional fees |

3,783 | 3,654 | ||||||

| Short-term deferred rent |

1,839 | 1,770 | ||||||

| Income taxes payable |

1,168 | 1,391 | ||||||

| Acquisition-related expenses and merger consideration |

— | 290 | ||||||

| Restructuring |

101 | 105 | ||||||

| Marketing and sales program expenses |

2,865 | 1,508 | ||||||

| Foreign currency forward contracts |

17 | 883 | ||||||

| Fixed assets in progress |

2,811 | 855 | ||||||

| Other |

3,214 | 2,411 | ||||||

|

|

|

|

|

|||||

| $ | 38,545 | $ | 36,751 | |||||

|

|

|

|

|

|||||

13

Table of Contents

9. DEFERRED REVENUE

| (in thousands) | March 31, 2017 |

December 31, 2016 |

||||||

| Term license |

$ | 10,056 | $ | 15,843 | ||||

| Perpetual license |

25,240 | 23,189 | ||||||

| Maintenance |

122,628 | 112,397 | ||||||

| Cloud |

17,928 | 13,604 | ||||||

| Services |

10,972 | 10,614 | ||||||

|

|

|

|

|

|||||

| Current deferred revenue |

186,824 | 175,647 | ||||||

|

|

|

|

|

|||||

| Perpetual license |

6,901 | 7,909 | ||||||

| Maintenance |

1,744 | 1,802 | ||||||

| Cloud |

1,313 | 1,278 | ||||||

|

|

|

|

|

|||||

| Long-term deferred revenue |

9,958 | 10,989 | ||||||

|

|

|

|

|

|||||

| $ | 196,782 | $ | 186,636 | |||||

|

|

|

|

|

|||||

10. STOCK-BASED COMPENSATION

The following table presents the stock-based compensation expense included in the Company’s unaudited condensed consolidated statements of operations:

| Three Months Ended March 31, |

||||||||

| (in thousands) | 2017 | 2016 | ||||||

| Cost of revenues |

$ | 3,622 | $ | 2,680 | ||||

| Operating expenses |

8,886 | 6,255 | ||||||

|

|

|

|

|

|||||

| Total stock-based compensation before tax |

$ | 12,508 | $ | 8,935 | ||||

| Income tax benefit |

$ | (3,815 | ) | $ | (2,605 | ) | ||

During the first three months of 2017, the Company issued approximately 564,000 shares of common stock to its employees and 9,000 shares of common stock to its non-employee directors under the Company’s share-based compensation plans.

During the first three months of 2017, the Company granted approximately 919,000 restricted stock units (“RSUs”) and 1,414,000 non-qualified stock options to its employees with total fair values of approximately $40.3 million and $18.9 million, respectively. This includes approximately 175,000 RSUs which were granted in connection with the election by employees to receive 50% of their 2017 target incentive compensation under the Company’s Corporate Incentive Compensation Plan in the form of RSUs instead of cash. Stock-based compensation of approximately $7.7 million associated with this RSU grant will be recognized over a one-year period beginning on the grant date.

The Company recognizes stock based compensation on the accelerated recognition method, treating each vesting tranche as if it were an individual grant. As of March 31, 2017, the Company had approximately $76.2 million of unrecognized stock-based compensation expense, net of estimated forfeitures, related to all unvested RSUs and unvested stock options that is expected to be recognized over a weighted-average period of 2.2 years.

14

Table of Contents

11. EARNINGS PER SHARE

Basic earnings per share is computed using the weighted-average number of common shares outstanding during the applicable period. Diluted earnings per share is computed using the weighted-average number of common shares outstanding during the applicable period, plus the dilutive effect of outstanding options and RSUs, using the treasury stock method. Certain shares related to some of the Company’s outstanding stock options and RSUs were excluded from the computation of diluted earnings per share because they were anti-dilutive in the periods presented, but could be dilutive in the future.

| Three Months Ended March 31, |

||||||||

| (in thousands, except per share amounts) | 2017 | 2016 | ||||||

| Basic |

||||||||

| Net income |

$ | 27,021 | $ | 10,400 | ||||

|

|

|

|

|

|||||

| Weighted-average common shares outstanding |

76,761 | 76,375 | ||||||

|

|

|

|

|

|||||

| Earnings per share, basic |

$ | 0.35 | $ | 0.14 | ||||

|

|

|

|

|

|||||

| Diluted |

||||||||

| Net income |

$ | 27,021 | $ | 10,400 | ||||

|

|

|

|

|

|||||

| Weighted-average common shares outstanding, basic |

76,761 | 76,375 | ||||||

| Weighted-average effect of dilutive securities: |

||||||||

| Stock options |

3,184 | 1,692 | ||||||

| RSUs |

1,930 | 1,168 | ||||||

|

|

|

|

|

|||||

| Effect of assumed exercise of stock options and RSUs |

5,114 | 2,860 | ||||||

|

|

|

|

|

|||||

| Weighted-average common shares outstanding, assuming dilution |

81,875 | 79,235 | ||||||

|

|

|

|

|

|||||

| Earnings per share, diluted |

$ | 0.33 | $ | 0.13 | ||||

|

|

|

|

|

|||||

| Outstanding options and RSUs excluded as impact would be anti-dilutive |

314 | 492 | ||||||

15

Table of Contents

12. GEOGRAPHIC INFORMATION AND MAJOR CLIENTS

Geographic Information

Operating segments are defined as components of an enterprise, about which separate financial information is available that is evaluated regularly by the chief operating decision maker (“CODM”) in deciding how to allocate resources and in assessing performance.

The Company develops and licenses software applications for customer engagement and its Pega® Platform, and provides consulting services, maintenance, and training related to its offerings. The Company derives substantially all of its revenue from the sale and support of one group of similar products and services - software that provides case management, business process management, and real-time decisioning solutions to improve customer engagement and operational excellence in the enterprise applications market. To assess performance, the Company’s CODM, who is the chief executive officer, reviews financial information on a consolidated basis. Therefore, the Company determined it has one reportable segment - Customer Engagement Solutions and one reporting unit.

The Company’s international revenue is from clients based outside of the U.S. The Company derived its revenue from the following geographic areas:

| Three Months Ended March 31, |

||||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||

| U.S. |

$ | 137,609 | 61 | % | $ | 93,228 | 52 | % | ||||||||

| Other Americas |

9,491 | 4 | % | 25,559 | 14 | % | ||||||||||

| U.K. |

30,190 | 14 | % | 24,355 | 14 | % | ||||||||||

| Other EMEA(1) |

21,846 | 10 | % | 21,267 | 12 | % | ||||||||||

| Asia Pacific |

24,111 | 11 | % | 14,449 | 8 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | 223,247 | 100 | % | $ | 178,858 | 100 | % | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Includes Europe, the Middle East and Africa, but excludes the United Kingdom. |

Major Clients

Clients accounting for 10% or more of the Company’s total revenue were as follows:

| Three Months Ended March 31, |

||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||

| Total revenue |

223,247 | 178,858 | ||||||

| Client A |

— | % | 10 | % | ||||

No client accounted for 10% or more of the Company’s total outstanding trade receivables as of March 31, 2017 or December 31, 2016.

16

Table of Contents

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Forward-Looking Statements

This Quarterly Report on Form 10-Q contains or incorporates forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements include, but are not limited to, statements about our future financial performance and business plans, the adequacy of our liquidity and capital resources, the continued payment of quarterly dividends by the Company, and the timing of revenue recognition under existing license and cloud arrangements and are described more completely in Part I of our Annual Report on Form 10-K for the year ended December 31, 2016. These forward-looking statements are based on current expectations, estimates, forecasts, and projections about the industry and markets in which we operate, and management’s beliefs and assumptions. In addition, other written or oral statements that constitute forward-looking statements may be made by us or on our behalf. Words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “could,” “estimate,” “may,” “target,” “strategy,” “is intended to,” “project,” “guidance,” “likely,” “usually,” or variations of such words and similar expressions are intended to identify such forward-looking statements.

These statements are not guarantees of future performance and involve certain risks, uncertainties, and assumptions that are difficult to predict. Important factors that could cause actual future activities and results to differ materially from those expressed in such forward-looking statements include, among others, variation in demand for our products and services and the difficulty in predicting the completion of product acceptance and other factors affecting the timing of license revenue recognition; the ongoing consolidation in the financial services, insurance, healthcare, and communications markets; reliance on third party relationships; the potential loss of vendor specific objective evidence for our consulting services; the inherent risks associated with international operations and the continued uncertainties in international economies; foreign currency exchange rates; the financial impact of the Company’s past acquisitions and any future acquisitions; the potential legal and financial liabilities and reputation damage due to cyber-attacks and security breaches; and management of the Company’s growth. These risks, and other factors that could cause actual results to differ materially from those expressed in such forward-looking statements, are described more completely in Item 1A of Part I of our Annual Report on Form 10-K for the year ended December 31, 2016. We have no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or risks. New information, future events or risks may cause the forward-looking events we discuss in this report not to occur or to materially change.

Business overview

We develop, market, license, and support software applications for marketing, sales, service, and operations. In addition, we license our Pega® Platform for clients that wish to build and extend their own applications. The Pega Platform assists our clients in building, deploying, and evolving enterprise applications, creating an environment in which business and IT can collaborate to manage back office operations, front office sales, marketing, and/or customer service needs. We also provide consulting services, maintenance, and training for our software. Our software applications and Pega Platform can be deployed on Pega, partner, or customer-managed cloud architectures.

Our clients include Global 3000 companies and government agencies that seek to manage complex enterprise systems and customer service issues with greater agility and cost-effectiveness. Our strategy is to sell a client a series of licenses, each focused on a specific purpose or area of operations in support of longer term enterprise-wide digital transformation initiatives.

Our license revenue is primarily derived from sales of our applications and our Pega Platform. Our cloud revenue is derived from the licensing of our hosted Pega Platform and software application environments. Our consulting services revenue is primarily related to new license implementations.

17

Table of Contents

Key Financial Metrics

In evaluating the financial condition and operating performance of our business, management focuses on the following key financial metrics:

| Three Months Ended March 31, |

Increase | |||||||||||||||

| (Dollars in thousands, except per share amounts) | 2017 | 2016 | ||||||||||||||

| Total revenue |

$ | 223,247 | $ | 178,858 | $ | 44,389 | 25 | % | ||||||||

| Recurring revenue (1) |

$ | 123,502 | $ | 115,805 | $ | 7,697 | 7 | % | ||||||||

| Operating Margin |

14 | % | 8 | % | ||||||||||||

| Diluted earnings per share |

$ | 0.33 | $ | 0.13 | $ | 0.20 | 154 | % | ||||||||

| Cash flow provided by operating activities |

$ | 32,444 | $ | 10,040 | $ | 22,404 | 223 | % | ||||||||

| (1) | See the table below for the composition of recurring revenue. |

| Three Months Ended | ||||||||||||||||||||

| (Dollars in thousands) | March 31, 2017 |

December 31, 2016 |

September 30, 2016 |

June 30, 2016 |

March 31, 2016 |

|||||||||||||||

| Recurring revenue: |

||||||||||||||||||||

| Term license |

$ | 53,710 | $ | 30,351 | $ | 28,919 | $ | 18,864 | $ | 54,332 | ||||||||||

| Cloud |

10,827 | 10,798 | 10,873 | 11,269 | 8,498 | |||||||||||||||

| Maintenance |

58,965 | 57,162 | 55,038 | 55,161 | 52,975 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total recurring revenue |

$ | 123,502 | $ | 98,311 | $ | 94,830 | $ | 85,294 | $ | 115,805 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Recurring revenue as a percent of total revenue |

55 | % | 49 | % | 52 | % | 45 | % | 65 | % | ||||||||||

Recurring revenue increased $7.7 million or 7% in the first three months of 2017 compared to the same period in 2016. Recurring revenue represented 65% of total revenue during the first three months of 2016 due to a large three year term license arrangement which was paid in advance and recognized in full in the first quarter of 2016. As recurring revenue grows in proportion to total revenue, gross profit, operating income, net income, and earnings per share may not grow as fast as historical trends due to more license revenue being recognized over longer periods.

18

Table of Contents

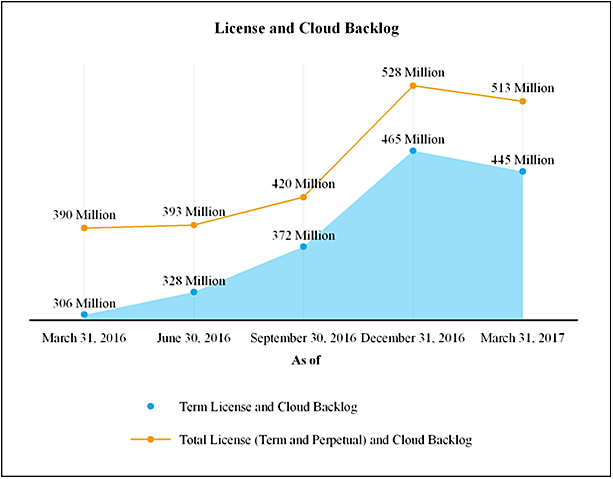

Another key performance factor is license and cloud backlog. It is computed by adding deferred license and cloud revenue recorded on the balance sheet (See Note 9 “Deferred Revenue”) and client license and cloud contractual commitments, which are not on our balance sheet because we have not yet invoiced our clients, nor have we recognized the associated revenues (See the table of future cash receipts in Liquidity and Capital Resources - Cash Provided by Operating Activities). License and cloud backlog may vary in any given period depending on the amount and timing of when the arrangements are executed, as well as the mix between perpetual, term, and cloud license arrangements, which may depend on our clients’ deployment preferences.

| As of March 31, | % Change |

|||||||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | 2017 vs. 2016 |

|||||||||||||||||

| Deferred license and cloud revenue on the balance sheet: |

||||||||||||||||||||

| Term license and cloud |

$ | 29,297 | 48 | % | $ | 18,409 | 32 | % | 59 | % | ||||||||||

| Perpetual license |

32,141 | 52 | % | 39,381 | 68 | % | (18 | )% | ||||||||||||

|

|

|

|

|

|||||||||||||||||

| Total deferred license and cloud revenue |

61,438 | 100 | % | 57,790 | 100 | % | 6 | % | ||||||||||||

|

|

|

|

|

|||||||||||||||||

| License and cloud contractual commitments not on the balance sheet: |

||||||||||||||||||||

| Term license and cloud |

416,088 | 92 | % | 287,926 | 87 | % | 45 | % | ||||||||||||

| Perpetual license |

35,532 | 8 | % | 43,944 | 13 | % | (19 | )% | ||||||||||||

|

|

|

|

|

|||||||||||||||||

| Total license and cloud commitments |

451,620 | 100 | % | 331,870 | 100 | % | 36 | % | ||||||||||||

|

|

|

|

|

|||||||||||||||||

| Total license (term and perpetual) and cloud backlog |

$ | 513,058 | $ | 389,660 | 32 | % | ||||||||||||||

|

|

|

|

|

|||||||||||||||||

| Total term license and cloud backlog |

$ | 445,385 | 87 | % | $ | 306,335 | 79 | % | 45 | % | ||||||||||

|

|

|

|

|

|||||||||||||||||

Critical accounting policies

Management’s Discussion and Analysis of Financial Condition and Results of Operations is based upon our unaudited condensed consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the U.S. and the rules and regulations of the SEC for interim financial reporting. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues, and expenses, and the related disclosure of contingent assets and liabilities. We base our estimates and judgments on historical experience, knowledge of current conditions, and beliefs of what could occur in the future given available information.

19

Table of Contents

There have been no changes in our critical accounting policies as disclosed in our Annual Report on Form 10-K for the year ended December 31, 2016. For more information regarding our critical accounting policies, we encourage you to read the discussion contained in Item 7 under the heading “Critical Accounting Estimates and Significant Judgments” and Note 2 “Significant Accounting Policies” included in the notes to the Consolidated Financial Statements contained in our Annual Report on Form 10-K for the year ended December 31, 2016.

Results of Operations

| Three Months Ended March 31, |

Increase | |||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||

| Total revenue |

$ | 223,247 | $ | 178,858 | $ | 44,389 | 25 | % | ||||||||

| Gross profit |

$ | 155,157 | $ | 122,348 | $ | 32,809 | 27 | % | ||||||||

| Total operating expenses |

$ | 123,919 | $ | 108,223 | $ | 15,696 | 15 | % | ||||||||

| Income from operations |

$ | 31,238 | $ | 14,125 | $ | 17,113 | 121 | % | ||||||||

| Operating margin |

14 | % | 8 | % | ||||||||||||

| Income before provision for income taxes |

$ | 31,800 | $ | 13,493 | $ | 18,307 | 136 | % | ||||||||

Revenue

Software license revenue

| Three Months Ended March 31, |

Increase (Decrease) | |||||||||||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||||||||||

| Perpetual licenses |

$ | 38,680 | 42 | % | $ | 14,013 | 21 | % | $ | 24,667 | 176 | % | ||||||||||||

| Term licenses |

53,710 | 58 | % | 54,332 | 79 | % | (622 | ) | (1 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total license revenue |

$ | 92,390 | 100 | % | $ | 68,345 | 100 | % | $ | 24,045 | 35 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

The mix between perpetual and term license arrangements executed in a particular period varies based on client needs. A change in the mix may cause our revenues to vary materially from period to period. A higher proportion of term license arrangements executed would generally result in more license revenue being recognized over longer periods. Additionally, some of our perpetual license arrangements include extended payment terms or additional rights of use, which may also result in the recognition of revenue over longer periods.

The increase in perpetual license revenue was primarily due to the higher value of perpetual arrangements executed and higher percentage of perpetual arrangements recognized in revenue during the first three months of 2017 compared to the same period in 2016. The aggregate value of future revenue expected to be recognized under all noncancellable perpetual licenses was $35.5 million as of March 31, 2017 compared to $43.9 million as of March 31, 2016. We expect to recognize $16.0 million of the $35.5 million as revenue during the remainder of 2017. See the table of future cash receipts in Liquidity and Capital Resources - Cash Provided by Operating Activities

The slight decrease in term license revenue was primarily due to a large three year term license arrangement which was paid in advance and recognized in full in the first quarter of 2016. If just the first year of this term license arrangement was paid in advance in the first three months of 2016, term license revenue for the first three months of 2017 would have increased by approximately 25%. The aggregate value of future revenue expected to be recognized under noncancellable term licenses and our cloud arrangements grew to $416.1 million as of March 31, 2017 compared to $287.9 million as of March 31, 2016. We expect to recognize $78.2 million of the $416.1 million as revenue during the remainder of 2017 in addition to new term license and Pega Cloud arrangements we may complete or prepayments we may receive from existing term license agreements. See the table of future cash receipts in Liquidity and Capital Resources - Cash Provided by Operating Activities.

20

Table of Contents

Maintenance revenue

| Three Months Ended March 31, |

Increase | |||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||

| Maintenance |

$ | 58,965 | $ | 52,975 | $ | 5,990 | 11 | % | ||||||||

The increase in maintenance revenue was primarily due to the continued growth in the aggregate value of the installed base of our software and continued strong renewal rates well in excess of 90%.

Services revenue

| Three Months Ended March 31, |

Increase (Decrease) | |||||||||||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||||||||||

| Consulting services |

$ | 59,252 | 82 | % | $ | 47,176 | 82 | % | $ | 12,076 | 26 | % | ||||||||||||

| Cloud |

10,827 | 15 | % | 8,498 | 15 | % | 2,329 | 27 | % | |||||||||||||||

| Training |

1,813 | 3 | % | 1,864 | 3 | % | (51 | ) | (3 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total services |

$ | 71,892 | 100 | % | $ | 57,538 | 100 | % | $ | 14,354 | 25 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

Consulting services revenue represents revenue primarily from new license implementations. Our consulting services revenue may fluctuate in future periods depending on the mix of new implementation projects we perform as compared to those performed by our enabled clients or led by our partners. The increase in consulting services revenue was primarily due to higher billable hours during the first three months of 2017 compared to the same period in 2016 driven by a large project which began in the second half of 2016.

Cloud revenue represents revenue from our Pega Cloud offerings. The increase in cloud revenue was primarily due to growth of our cloud client base.

Gross profit

| Three Months Ended March 31, |

Increase | |||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||

| Software license |

$ | 91,090 | $ | 67,324 | $ | 23,766 | 35 | % | ||||||||

| Maintenance |

51,747 | 47,060 | 4,687 | 10 | % | |||||||||||

| Services |

12,320 | 7,964 | 4,356 | 55 | % | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total gross profit |

$ | 155,157 | $ | 122,348 | $ | 32,809 | 27 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||

| Total gross profit % |

70 | % | 68 | % | ||||||||||||

| Software license gross profit % |

99 | % | 99 | % | ||||||||||||

| Maintenance gross profit % |

88 | % | 89 | % | ||||||||||||

| Services gross profit % |

17 | % | 14 | % | ||||||||||||

The increase in total gross profit was primarily due to the increase in software license revenue.

The increase in services gross profit percent was primarily due to the recognition of revenue in the first quarter of 2017 related to a large project which had been delayed from prior periods, for which the associated costs had already been recognized in 2016.

21

Table of Contents

Operating expenses

Amortization of intangibles

| Three Months Ended March 31, |

Increase (Decrease) | |||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||

| Cost of revenue |

$ | 1,334 | $ | 1,346 | $ | (12 | ) | (1 | )% | |||||||

| Selling and marketing |

1,866 | 1,530 | 336 | 22 | % | |||||||||||

| General and administrative |

— | 89 | (89 | ) | (100 | )% | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| $ | 3,200 | $ | 2,965 | $ | 235 | 8 | % | |||||||||

|

|

|

|

|

|

|

|||||||||||

The increase was primarily due to the amortization associated with $24.3 million of intangible assets acquired from OpenSpan in April 2016, partially offset by the full amortization in 2016 of certain technology and other intangibles acquired from Antenna Software, Inc. in October 2013.

Selling and marketing

| Three Months Ended March 31, |

Increase | |||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||

| Selling and marketing |

$ | 71,288 | $ | 61,078 | $ | 10,210 | 17 | % | ||||||||

| As a percent of total revenue |

32 | % | 34 | % | ||||||||||||

| Selling and marketing headcount at March 31, |

900 | 775 | ||||||||||||||

Selling and marketing expenses include compensation, benefits, and other headcount-related expenses associated with our selling and marketing personnel as well as advertising, promotions, trade shows, seminars, and other programs. Selling and marketing expenses also include the amortization of customer related intangibles.

The increase was primarily due to a $5.7 million increase in compensation and benefits associated with higher headcount and a $2 million increase in sales commissions associated with the higher value of new license arrangements executed during the first three months of 2017 compared to the same period in 2016.

The increase in headcount reflects our efforts to increase our sales capacity to target new accounts in existing industries, as well as to expand coverage in new industries and geographies and to increase the number of our sales opportunities.

Research and development

| Three Months Ended March 31, |

Increase | |||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||

| Research and development |

$ | 40,296 | $ | 34,920 | $ | 5,376 | 15 | % | ||||||||

| As a percent of total revenue |

18 | % | 20 | % | ||||||||||||

| Research and development headcount at March 31, |

1,441 | 1,277 | ||||||||||||||

Research and development expenses include compensation, benefits, contracted services, and other headcount-related expenses associated with the creation and development of our products, as well as enhancements and design changes to existing products and integration of acquired technologies.

The increase was primarily due to a $5.5 million increase in compensation and benefit expenses associated with higher headcount.

The increase in headcount primarily reflects the growth in our India research facility, which usually lowers our average compensation expense per employee, and the acquisition of OpenSpan.

22

Table of Contents

General and administrative

| Three Months Ended March 31, |

Increase | |||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||

| General and administrative |

$ | 12,335 | $ | 11,048 | $ | 1,287 | 12 | % | ||||||||

| As a percent of total revenue |

6 | % | 6 | % | ||||||||||||

| General and administrative headcount at March 31, |

384 | 356 | ||||||||||||||

General and administrative expenses include compensation, benefits, and other headcount-related expenses associated with finance, legal, corporate governance, and other administrative headcount. They also include accounting, legal, and other professional consulting and administrative fees. The general and administrative headcount includes employees in human resources, information technology, and corporate services departments whose costs are allocated to our other functional departments.

The increase was primarily due to a $2.1 million increase in compensation and benefits expenses associated with higher headcount, partially offset by a decrease of $1 million in legal fees.

Stock-based compensation

The following table summarizes stock-based compensation expense included in our unaudited condensed consolidated statements of operations:

| Three Months Ended March 31, |

Increase | |||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||

| Cost of revenues |

$ | 3,622 | $ | 2,680 | $ | 942 | 35 | % | ||||||||

| Operating expenses |

8,886 | 6,255 | 2,631 | 42 | % | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total stock-based compensation before tax |

$ | 12,508 | $ | 8,935 | $ | 3,573 | 40 | % | ||||||||

| Income tax benefit |

$ | (3,815 | ) | $ | (2,605 | ) | ||||||||||

The increase was primarily due to the increased value of our annual periodic equity awards granted in March 2016 and 2017. These awards generally have a five-year vesting schedule.

Non-operating income and expenses, net

| Three Months Ended March 31, |

Increase (Decrease) | |||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||

| Foreign currency transaction gain |

$ | 676 | $ | 1,376 | $ | (700 | ) | (51 | )% | |||||||

| Interest income, net |

165 | 290 | (125 | ) | (43 | )% | ||||||||||

| Other expense, net |

(279 | ) | (2,298 | ) | 2,019 | (88 | )% | |||||||||

|

|

|

|

|

|

|

|||||||||||

| Non-operating income (loss) |

$ | 562 | $ | (632 | ) | $ | 1,194 | n/m | ||||||||

|

|

|

|

|

|

|

|||||||||||

n/m - not meaningful

We use foreign currency forward contracts (“forward contracts”) to partially mitigate our exposure to fluctuations in foreign currency exchange rates associated with our foreign currency denominated cash, accounts receivable, and intercompany receivables and payables held by our U.S. parent company in currencies other than the U.S. dollar and by our U.K. subsidiary in currencies other than the British pound.

These forward contracts are not designated as hedging instruments. As a result, we record the fair value of the outstanding contracts at the end of the reporting period in our consolidated balance sheet, with any fluctuations in the value of these contracts recognized in other expense, net.

23

Table of Contents

The total change in the fair value of our foreign currency forward contracts recorded in other expense, net, during the first three months of 2017 and 2016 was a loss of $0.3 million and $2.3 million respectively.

See Note 4 “Derivative Instruments” of this Quarterly Report on Form 10-Q for discussion of our use of forward contracts.

Provision for income taxes

| Three Months Ended March 31, |

Increase | |||||||||||||||

| (Dollars in thousands) | 2017 | 2016 | ||||||||||||||

| Provision for income taxes |

$ | 4,779 | $ | 3,093 | $ | 1,686 | 55 | % | ||||||||

| Effective income tax rate |

15.0 | % | 22.9 | % | ||||||||||||

The provision for income taxes represents current and future amounts owed for federal, state, and foreign taxes. The decrease in the effective income tax rate in the first three months of 2017 compared to the same period in 2016 is primarily due to an increase in excess tax benefits generated by our stock compensation plans and a more favorable tax jurisdictional mix of earnings. The inclusion of excess tax benefits as a component of the provision for income taxes may increase volatility in future effective tax rates as the amount of excess tax benefits from share-based compensation awards is dependent upon our future stock price in relation to the fair value of awards, the timing of RSU vesting and exercise behavior of our stock option holders, and future grants of share-based compensation awards.

Liquidity and capital resources

| Three Months Ended | ||||||||

| March 31, | ||||||||

| (in thousands) | 2017 | 2016 | ||||||

| Cash provided by (used in): |

||||||||

| Operating activities |

$ | 32,444 | $ | 10,040 | ||||

| Investing activities |

(3,727 | ) | 9,370 | |||||

| Financing activities |

(15,994 | ) | (19,822 | ) | ||||

| Effect of exchange rate on cash |

521 | (434 | ) | |||||

|

|

|

|

|

|||||

| Net increase (decrease) in cash and cash equivalents |

$ | 13,244 | $ | (846 | ) | |||

|

|

|

|

|

|||||

| As of | As of | |||||||

| March 31, 2017 |

December 31, 2016 |

|||||||

| Total cash, cash equivalents, and marketable securities |

$ | 147,786 | $ | 133,761 | ||||

|

|

|

|

|

|||||

The increase in cash and cash equivalents during the first three months of 2017 compared to the same period in 2016 was primarily due to the $22.4 million increase in cash provided by operating activities as a result of the $16.6 million increase in net income and the $10.6 million decrease in share repurchases under share repurchase programs, partially offset by the $14.9 million decrease in cash provided by the maturities, calls, and sales of marketable debt securities, net of purchases and the $6.8 million increase in cash used for net settlement of stock compensation awards. We believe that our current cash, cash equivalents, marketable securities, and cash flow from operations will be sufficient to fund our operations, our dividend payments, and our share repurchase program for at least the next 12 months.

We evaluate acquisition opportunities from time to time, which if pursued, could require use of our funds. On April 11, 2016, we acquired OpenSpan for $48.8 million in cash, net of cash acquired. As of March 31, 2017, $7.4 million of the cash consideration remained in escrow and will act as security for the indemnification obligations of the selling shareholders through October 2017. We paid $0.3 million during both the first three months of 2017 and 2016, representing additional cash consideration to the selling shareholders of one of the three companies acquired in 2014 based on the achievement of certain performance milestones.

As of March 31, 2017, approximately $40.2 million of our cash and cash equivalents was held in our foreign subsidiaries. If it becomes necessary to repatriate these funds, we may be required to pay U.S. tax, net of any applicable foreign tax credits, upon repatriation. We consider the earnings of our foreign subsidiaries to be permanently reinvested and, as a result, U.S. taxes on

24

Table of Contents

such earnings are not provided. It is impractical to estimate the amount of U.S. tax we could have to pay upon repatriation due to the complexity of the foreign tax credit calculations. There can be no assurance that changes in our plans or other events affecting our operations will not result in materially accelerated or unexpected expenditures.

Cash provided by operating activities

The primary drivers during the first three months of 2017 and 2016 were net income of $27 million and $10.4 million, respectively.

Future Cash Receipts from Committed License and Cloud Arrangements

As of March 31, 2017, none of the amounts shown in the table below had been billed and no revenue had been recognized. The timing of cash receipts may not coincide with the timing of future expected revenue recognition.

|

(in thousands) as of March 31, 2017 |

Term and cloud contracts |

Perpetual contracts (1) |

Total | |||||||||

| Remainder of 2017 |

$ | 78,151 | $ | 16,016 | $ | 94,167 | ||||||

| 2018 |

129,907 | 15,525 | 145,432 | |||||||||

| 2019 |

103,110 | 3,245 | 106,355 | |||||||||

| 2020 |

70,467 | 746 | 71,213 | |||||||||

| 2021 |

28,665 | — | 28,665 | |||||||||

| 2022 and thereafter |

5,788 | — | 5,788 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

$ | 416,088 | $ | 35,532 | $ | 451,620 | ||||||

|

|

|

|

|

|

|

|||||||

| (1) | These amounts are for perpetual licenses with extended payment terms and/or additional rights of use. |

Total contractual future cash receipts due from our existing license and cloud arrangements were approximately $331.9 million as of March 31, 2016.

Cash (used in) provided by investing activities

During the first three months of 2017, purchases of marketable debt securities were $3.3 million, partially offset by proceeds received from maturities and called marketable debt securities of $2.3 million. We also invested $2.4 million primarily for leasehold improvements for the build out of additional office space at our Hyderabad, India location.

During the first three months of 2016, proceeds received from sales and maturities of marketable debt securities were $22.1 million, partially offset by purchases of marketable debt securities of $8.2 million. We also invested $4.3 million primarily for internally developed software and leasehold improvements for the build out of additional office space at our corporate headquarters in Cambridge, Massachusetts.

Cash used in financing activities

We used cash primarily for repurchases of our common stock, share repurchases for tax withholdings for the net settlement of our equity awards, and the payment of our quarterly dividend.

Since 2004, our Board of Directors has approved annual stock repurchase programs that have authorized the repurchase in the aggregate of up to $195 million of our common stock. Purchases under these programs have been made on the open market.

25

Table of Contents

The following table is a summary of our repurchase activity under all of our repurchase programs during the first three months of 2017 and 2016:

| Three Months Ended March 31, |

||||||||||||||||

| 2017 | 2016 | |||||||||||||||

| (Dollars in thousands) | Shares | Amount | Shares | Amount | ||||||||||||

| Prior year authorization as of January 1, |

$ | 39,385 | $ | 40,534 | ||||||||||||

| Repurchases paid |

29,250 | (1,260 | ) | 501,104 | (11,667 | ) | ||||||||||

| Repurchases unsettled |

5,450 | (238 | ) | 17,160 | (429 | ) | ||||||||||

|

|

|

|

|

|||||||||||||

| Authorization remaining as of March 31, |

$ | 37,887 | $ | 28,438 | ||||||||||||

|

|

|

|

|

|||||||||||||

In addition to the share repurchases made under our repurchase programs, we net settled the majority of our employee stock option exercises and RSU vestings, which resulted in the withholding of shares to cover the option exercise price and the minimum statutory tax withholding obligations.