Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - ALNYLAM PHARMACEUTICALS, INC. | alny-ex322_8.htm |

| EX-32.1 - EX-32.1 - ALNYLAM PHARMACEUTICALS, INC. | alny-ex321_9.htm |

| EX-31.2 - EX-31.2 - ALNYLAM PHARMACEUTICALS, INC. | alny-ex312_10.htm |

| EX-31.1 - EX-31.1 - ALNYLAM PHARMACEUTICALS, INC. | alny-ex311_11.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

☒ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2017

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ___________

Commission File Number 001-36407

ALNYLAM PHARMACEUTICALS, INC.

(Exact Name of Registrant as Specified in Its Charter)

|

Delaware |

|

77-0602661 |

|

(State or Other Jurisdiction of Incorporation or Organization) |

|

(I.R.S. Employer Identification No.) |

|

300 Third Street, Cambridge, MA |

|

02142 |

|

(Address of Principal Executive Offices) |

|

(Zip Code) |

(617) 551-8200

(Registrant’s Telephone Number, Including Area Code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

|

☒ |

|

Accelerated filer |

|

☐ |

|

|

|

|

|

|||

|

Non-accelerated filer |

|

☐ (Do not check if a smaller reporting company) |

|

Smaller reporting company |

|

☐ |

|

|

|

|

|

|

|

|

|

Emerging growth company |

|

☐ |

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

At April 28, 2017, the registrant had 86,190,192 shares of Common Stock, $0.01 par value per share, outstanding.

|

|

|

PAGE NUMBER |

|

|

|

|

|

PART I. FINANCIAL INFORMATION |

|

|

|

|

|

|

|

ITEM 1. FINANCIAL STATEMENTS (Unaudited) |

|

|

|

|

|

|

|

CONDENSED CONSOLIDATED BALANCE SHEETS AS OF MARCH 31, 2017 AND DECEMBER 31, 2016 |

|

2 |

|

|

3 |

|

|

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS FOR THE THREE MONTHS ENDED MARCH 31, 2017 AND 2016 |

|

4 |

|

|

5 |

|

|

|

|

|

|

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

|

15 |

|

|

|

|

|

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

|

22 |

|

|

|

|

|

|

23 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

24 |

|

|

|

|

|

|

|

24 |

|

|

|

|

|

|

|

47 |

|

|

|

|

|

|

|

48 |

|

1

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands, except share and per share amounts)

(Unaudited)

|

|

|

March 31, 2017 |

|

|

December 31, 2016 |

|

||

|

ASSETS |

|

|

|

|

|

|

|

|

|

Current assets: |

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

171,079 |

|

|

$ |

193,617 |

|

|

Marketable securities |

|

|

385,843 |

|

|

|

424,185 |

|

|

Investment in equity securities of Regulus Therapeutics Inc. |

|

|

2,682 |

|

|

|

8,997 |

|

|

Billed and unbilled collaboration receivables |

|

|

19,457 |

|

|

|

23,334 |

|

|

Prepaid expenses and other current assets |

|

|

18,127 |

|

|

|

21,744 |

|

|

Total current assets |

|

|

597,188 |

|

|

|

671,877 |

|

|

Marketable securities |

|

|

255,305 |

|

|

|

324,799 |

|

|

Property, plant and equipment, net |

|

|

129,962 |

|

|

|

114,572 |

|

|

Restricted investments |

|

|

150,000 |

|

|

|

150,000 |

|

|

Other assets |

|

|

1,471 |

|

|

|

1,562 |

|

|

Total assets |

|

$ |

1,133,926 |

|

|

$ |

1,262,810 |

|

|

LIABILITIES AND STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

|

|

|

Accounts payable |

|

$ |

25,371 |

|

|

$ |

54,465 |

|

|

Accrued expenses |

|

|

31,842 |

|

|

|

42,118 |

|

|

Deferred rent |

|

|

1,818 |

|

|

|

1,576 |

|

|

Deferred revenue |

|

|

36,755 |

|

|

|

33,540 |

|

|

Total current liabilities |

|

|

95,786 |

|

|

|

131,699 |

|

|

Deferred rent, net of current portion |

|

|

8,006 |

|

|

|

8,431 |

|

|

Deferred revenue, net of current portion |

|

|

46,049 |

|

|

|

49,392 |

|

|

Long-term debt |

|

|

150,000 |

|

|

|

150,000 |

|

|

Other liabilities |

|

|

3,184 |

|

|

|

3,067 |

|

|

Total liabilities |

|

|

303,025 |

|

|

|

342,589 |

|

|

Commitments and contingencies (Note 5) |

|

|

|

|

|

|

|

|

|

Stockholders’ equity: |

|

|

|

|

|

|

|

|

|

Preferred stock, $0.01 par value per share, 5,000,000 shares authorized and no shares issued and outstanding at March 31, 2017 and December 31, 2016 |

|

|

— |

|

|

— |

|

|

|

Common stock, $0.01 par value per share, 125,000,000 shares authorized; 86,068,086 shares issued and outstanding at March 31, 2017; 85,941,344 shares issued and outstanding at December 31, 2016 |

|

|

861 |

|

|

|

859 |

|

|

Additional paid-in capital |

|

|

2,627,969 |

|

|

|

2,609,614 |

|

|

Accumulated other comprehensive loss |

|

|

(33,828 |

) |

|

|

(33,441 |

) |

|

Accumulated deficit |

|

|

(1,764,101 |

) |

|

|

(1,656,811 |

) |

|

Total stockholders’ equity |

|

|

830,901 |

|

|

|

920,221 |

|

|

Total liabilities and stockholders’ equity |

|

$ |

1,133,926 |

|

|

$ |

1,262,810 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

2

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

(In thousands, except per share amounts)

(Unaudited)

|

|

|

Three Months Ended March 31, |

|

|||||

|

|

|

2017 |

|

|

2016 |

|

||

|

Net revenues from collaborators |

|

$ |

18,960 |

|

|

$ |

7,345 |

|

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

Research and development (1) |

|

|

86,984 |

|

|

|

96,273 |

|

|

General and administrative (1) |

|

|

38,487 |

|

|

|

21,100 |

|

|

Total operating expenses |

|

|

125,471 |

|

|

|

117,373 |

|

|

Loss from operations |

|

|

(106,511 |

) |

|

|

(110,028 |

) |

|

Other income (expense): |

|

|

|

|

|

|

|

|

|

Interest income |

|

|

2,128 |

|

|

|

1,813 |

|

|

Other (expense) income |

|

|

(2,907 |

) |

|

|

5,241 |

|

|

Total other (expense) income |

|

|

(779 |

) |

|

|

7,054 |

|

|

Net loss |

|

$ |

(107,290 |

) |

|

$ |

(102,974 |

) |

|

Net loss per common share - basic and diluted |

|

$ |

(1.25 |

) |

|

$ |

(1.21 |

) |

|

Weighted-average common shares used to compute basic and diluted net loss per common share |

|

|

86,027 |

|

|

|

85,277 |

|

|

Comprehensive loss: |

|

|

|

|

|

|

|

|

|

Net loss |

|

$ |

(107,290 |

) |

|

$ |

(102,974 |

) |

|

Unrealized loss on marketable securities, net of tax |

|

|

(1,936 |

) |

|

|

(8,224 |

) |

|

Reclassification adjustment for realized loss (gain) on marketable securities included in net loss |

|

|

1,549 |

|

|

|

(5,156 |

) |

|

Comprehensive loss |

|

$ |

(107,677 |

) |

|

$ |

(116,354 |

) |

|

(1) |

Non-cash stock-based compensation expenses included in operating expenses are as follows: |

|

Research and development |

|

$ |

8,691 |

|

|

$ |

14,356 |

|

|

General and administrative |

|

|

7,026 |

|

|

|

9,124 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

3

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands)

(Unaudited)

|

|

|

Three Months Ended March 31, |

|

|||||

|

|

|

2017 |

|

|

2016 |

|

||

|

Cash flows from operating activities: |

|

|

|

|

|

|

|

|

|

Net loss |

|

$ |

(107,290 |

) |

|

$ |

(102,974 |

) |

|

Adjustments to reconcile net loss to net cash used in operating activities: |

|

|

|

|

|

|

|

|

|

Depreciation and amortization |

|

|

3,000 |

|

|

|

4,601 |

|

|

Non-cash stock-based compensation |

|

|

15,717 |

|

|

|

23,480 |

|

|

Charge for 401(k) company stock match |

|

|

551 |

|

|

|

331 |

|

|

Realized loss (gain) on sale of marketable equity securities |

|

|

1,549 |

|

|

|

(5,156 |

) |

|

Other |

|

|

608 |

|

|

|

— |

|

|

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

|

Billed and unbilled collaboration receivables |

|

|

3,877 |

|

|

|

(516 |

) |

|

Prepaid expenses and other assets |

|

|

3,708 |

|

|

|

(2,010 |

) |

|

Accounts payable |

|

|

(11,067 |

) |

|

|

347 |

|

|

Accrued expenses and other |

|

|

(10,855 |

) |

|

|

(4,305 |

) |

|

Deferred revenue |

|

|

(128 |

) |

|

|

2,579 |

|

|

Net cash used in operating activities |

|

|

(100,330 |

) |

|

|

(83,623 |

) |

|

Cash flows from investing activities: |

|

|

|

|

|

|

|

|

|

Purchases of property, plant and equipment |

|

|

(36,152 |

) |

|

|

(2,759 |

) |

|

Purchases of marketable securities |

|

|

(86,803 |

) |

|

|

(164,561 |

) |

|

Sales and maturities of marketable securities |

|

|

198,031 |

|

|

|

294,317 |

|

|

Deposit for manufacturing facility |

|

|

— |

|

|

|

(9,057 |

) |

|

Net cash provided by investing activities |

|

|

75,076 |

|

|

|

117,940 |

|

|

Cash flows from financing activities: |

|

|

|

|

|

|

|

|

|

Proceeds from exercise of stock options and other types of equity |

|

|

2,769 |

|

|

|

1,824 |

|

|

Proceeds from issuance of common stock to Sanofi Genzyme |

|

|

— |

|

|

|

14,301 |

|

|

Payments for repurchase of common stock for employee tax withholding |

|

|

(53 |

) |

|

|

(59 |

) |

|

Net cash provided by financing activities |

|

|

2,716 |

|

|

|

16,066 |

|

|

Net (decrease) increase in cash and cash equivalents |

|

|

(22,538 |

) |

|

|

50,383 |

|

|

Cash and cash equivalents, beginning of period |

|

|

193,617 |

|

|

|

180,895 |

|

|

Cash and cash equivalents, end of period |

|

$ |

171,079 |

|

|

$ |

231,278 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

4

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation and Principles of Consolidation

The accompanying condensed consolidated financial statements of Alnylam Pharmaceuticals, Inc. are unaudited and have been prepared in accordance with accounting principles generally accepted in the United States of America, or GAAP, applicable to interim periods and, in the opinion of management, include all normal and recurring adjustments that are necessary to state fairly the results of operations for the reported periods. Our condensed consolidated financial statements have also been prepared on a basis substantially consistent with, and should be read in conjunction with, our audited consolidated financial statements for the year ended December 31, 2016, which were included in our Annual Report on Form 10-K that was filed with the Securities and Exchange Commission, or SEC, on February 15, 2017. The year-end condensed consolidated balance sheet data was derived from our audited financial statements, but does not include all disclosures required by GAAP. The results of our operations for any interim period are not necessarily indicative of the results of our operations for any other interim period or for a full fiscal year.

The accompanying condensed consolidated financial statements reflect the operations of Alnylam and our wholly-owned subsidiaries. All intercompany accounts and transactions have been eliminated.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the condensed consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Liquidity

Based on our current operating plan, we believe that our cash, cash equivalents and fixed income marketable securities at March 31, 2017, together with the cash we expect to generate under our current alliances, will be sufficient to enable us to advance our Alnylam 2020 strategy for at least the next 12 months from the filing of this Quarterly Report on Form 10-Q.

Net Loss Per Common Share

We compute basic net loss per common share by dividing net loss by the weighted-average number of common shares outstanding. We compute diluted net loss per common share by dividing net loss by the weighted-average number of common shares and dilutive potential common share equivalents then outstanding. Potential common shares consist of shares issuable upon the exercise of stock options (the proceeds of which are then assumed to have been repurchased using the treasury stock method). Because the inclusion of potential common shares would be anti-dilutive for all periods presented, diluted net loss per common share is the same as basic net loss per common share.

The following table sets forth for the periods presented the potential common shares (prior to consideration of the treasury stock method) excluded from the calculation of net loss per common share because their inclusion would be anti-dilutive, in thousands:

|

|

|

At March 31, |

|

|||||

|

|

|

2017 |

|

|

2016 |

|

||

|

Options to purchase common stock |

|

|

12,048 |

|

|

|

10,183 |

|

|

Unvested restricted common stock |

|

|

163 |

|

|

|

185 |

|

|

|

|

|

12,211 |

|

|

|

10,368 |

|

Equity

Total stockholders’ equity at March 31, 2017 decreased $89.3 million compared to December 31, 2016. This decrease was related primarily to our net loss, partially offset during the three months ended March 31, 2017 by increases to additional paid-in capital due to stock-based compensation.

5

The fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. In general, fair values determined by Level 1 inputs utilize quoted prices (unadjusted) in active markets for identical assets or liabilities. Fair values determined by Level 2 inputs utilize data points that are observable, such as quoted prices (adjusted), interest rates and yield curves. Fair values determined by Level 3 inputs utilize unobservable data points for the asset or liability, and include situations where there is little, if any, market activity for the asset or liability. The fair value hierarchy level is determined by the lowest level of significant input.

Investments in Marketable Securities and Cash Equivalents

We invest our excess cash balances in short-term and long-term marketable debt and equity securities. We classify our investments in marketable debt securities as either held-to-maturity or available-for-sale based on facts and circumstances present at the time we purchased the securities. At each balance sheet date presented, we classified all of our investments in debt and equity securities as available-for-sale. We report available-for-sale investments at fair value at each balance sheet date and include any unrealized holding gains and losses (the adjustment to fair value) in accumulated other comprehensive income (loss), a component of stockholders’ equity. At March 31, 2017, the balance in our accumulated other comprehensive loss was composed solely of activity related to our available-for-sale marketable securities, including our investment in equity securities of Regulus Therapeutics Inc., or Regulus. Realized gains and losses are determined using the specific identification method and are included in other income (expense). We recognized $1.5 million of realized losses and $5.2 million of realized gains from sales of our Regulus available-for-sale securities as other income (expense) in our condensed consolidated statements of comprehensive loss during the three months ended March 31, 2017 and 2016, respectively. If any adjustment to arrive at fair value reflects a decline in the value of the investment, we consider all available evidence to evaluate the extent to which the decline is “other than temporary,” including our intention to sell and, if so, record a charge to our condensed consolidated statements of comprehensive loss. We did not record any impairment charges related to our fixed income marketable securities during the three months ended March 31, 2017 or 2016. Our marketable securities are classified as cash equivalents if the original maturity, from the date of purchase, is 90 days or less, and as marketable securities if the original maturity, from the date of purchase, is in excess of 90 days. Our cash equivalents are composed of commercial paper, corporate notes and money market funds.

We account for our investment in Regulus as an available-for-sale marketable security. Intraperiod tax allocation rules require us to allocate our provision for income taxes between continuing operations and other categories of earnings, such as other comprehensive income. In periods in which we have a year-to-date pre-tax loss from continuing operations and pre-tax income in other categories of earnings, such as other comprehensive income, we must allocate the tax provision to the other categories of earnings. We then record a related tax benefit in continuing operations. Upon sales of our available-for-sale marketable securities, we apply the aggregate portfolio approach to recognize the related tax provision or benefit into income (loss) from continuing operations. As a result, the disproportionate tax effect remains in accumulated other comprehensive income (loss) as long as we maintain an investment portfolio.

Recent Accounting Pronouncements

In May 2014, the Financial Accounting Standards Board, or FASB, issued a new revenue recognition standard which amends revenue recognition principles and provides a single, comprehensive set of criteria for revenue recognition within and across all industries. The new standard provides a five step framework whereby revenue is recognized when promised goods or services are transferred to a customer at an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The standard also requires enhanced disclosures pertaining to revenue recognition in both interim and annual periods. In August 2015, the FASB deferred the effective date of the new revenue standard from January 1, 2017 to January 1, 2018. In March 2016, the FASB issued amendments to clarify the implementation guidance on principal versus agent considerations. In April 2016, the FASB issued amendments to clarify the guidance on accounting for licenses of intellectual property and identifying performance obligations. In May 2016, the FASB issued amendments related to collectibility, non-cash consideration, the presentation of sales and other similar taxes collected from customers and transition. The standard allows for adoption using a full retrospective method or a modified retrospective method. We are currently evaluating the method of our adoption as well as the expected impact that the standard could have on our condensed consolidated financial statements and related disclosures.

In January 2016, the FASB issued new guidance on recognition and measurement of financial assets and financial liabilities. The new guidance will impact the accounting for equity investments, financial liabilities under the fair value option, and the presentation and disclosure requirements for financial instruments. All equity investments in unconsolidated entities (other than those accounted for under the equity method of accounting) will generally be measured at fair value with changes in fair value recognized through earnings. There will no longer be an available-for-sale classification (changes in fair value reported in other comprehensive income (loss)) for equity securities with readily determinable fair values. In addition, the FASB clarified the need for a valuation allowance on deferred tax assets resulting from unrealized losses on available-for-sale debt securities. In general, the new guidance

6

will require modified retrospective application to all outstanding instruments, with a cumulative effect adjustment recorded to opening retained earnings. This guidance will be effective for us on January 1, 2018. We are currently evaluating the expected impact that the standard could have on our condensed consolidated financial statements and related disclosures.

In February 2016, the FASB issued a new leasing standard that requires that all lessees recognize the assets and liabilities that arise from leases on the condensed consolidated balance sheet and disclose qualitative and quantitative information about its leasing arrangements. The new standard will be effective for us on January 1, 2019. Early adoption is permitted. We are currently evaluating the timing of our adoption and the expected impact that this standard could have on our consolidated financial statements and related disclosures.

In October 2016, the FASB issued guidance that an entity should recognize the income tax consequences of an intra-entity transfer of an asset other than inventory when the transfer occurs instead of deferring the income tax effects. The new standard will be effective for us on a modified retrospective basis on January 1, 2018. We are currently evaluating the expected impact that this standard could have on our condensed consolidated financial statements and related disclosures.

In November 2016, the FASB issued guidance that requires restricted cash and restricted cash equivalents be included with cash and cash equivalents when reconciling the total beginning and ending amounts for the periods shown on the statement of cash flows. The new standard will be effective for us on January 1, 2018 using a retrospective transition method to each period presented. Early adoption is permitted. We are currently evaluating the timing of our adoption and the expected impact that this standard could have on our condensed consolidated financial statements and related disclosures.

In March 2017, the FASB issued guidance that amends the amortization period for certain purchased callable debt securities held at a premium by shortening the amortization period for the premium to the earliest call date. The new standard will be effective for us on January 1, 2019. Early adoption is permitted. We are currently evaluating the timing of our adoption and the expected impact that this standard could have on our condensed consolidated financial statements and related disclosures.

2. COLLABORATION AGREEMENTS

The following table summarizes our total consolidated net revenues from collaborators, for the periods indicated, in thousands:

|

|

|

Three Months Ended March 31, |

|

|||||

|

Description |

|

2017 |

|

|

2016 |

|

||

|

Sanofi Genzyme |

|

$ |

12,277 |

|

|

$ |

4,415 |

|

|

The Medicines Company |

|

|

6,364 |

|

|

|

2,657 |

|

|

Other |

|

|

319 |

|

|

|

273 |

|

|

Total net revenues from collaborators |

|

$ |

18,960 |

|

|

$ |

7,345 |

|

Product Alliances

Sanofi Genzyme Collaboration

In January 2014, we entered into a global, strategic collaboration with Sanofi Genzyme, the specialty care global business unit of Sanofi, to discover, develop and commercialize RNA interference, or RNAi, therapeutics as Genetic Medicines to treat orphan diseases. The 2014 Sanofi Genzyme collaboration superseded and replaced the previous collaboration between us and Sanofi Genzyme entered into in October 2012 to develop and commercialize RNAi therapeutics targeting transthyretin, or TTR, for the treatment of hereditary ATTR amyloidosis, including patisiran and revusiran, in Japan and the Asia-Pacific region.

2012 Sanofi Genzyme Agreement

Under the 2012 Sanofi Genzyme agreement, Sanofi Genzyme paid us an upfront cash payment of $22.5 million. We were also entitled to receive certain milestone payments under the 2012 Sanofi Genzyme agreement. In the fourth quarter of 2013, we earned a milestone of $7.0 million based upon the completion of a successful patisiran Phase 2 clinical trial and a milestone of $4.0 million based upon the initiation of the APOLLO Phase 3 clinical trial for patisiran.

We determined that the deliverables under the 2012 Sanofi Genzyme agreement included the license, a joint steering committee and any additional TTR-specific RNAi therapeutic compounds that comprised the ALN-TTR program. We also determined that, pursuant to the accounting guidance governing revenue recognition on multiple element arrangements, the license and undelivered joint steering committee and any additional TTR-specific RNAi therapeutic compounds did not have standalone value due to the specialized nature of the services to be provided by us. In addition, while Sanofi Genzyme had the ability to grant sublicenses, it could not sublicense all or substantially all of its rights under the 2012 Sanofi Genzyme agreement. The uniqueness of our services and the

7

limited sublicense right were indicators that standalone value was not present in the arrangement. Therefore the deliverables were not separable and, accordingly, the license and undelivered services were treated as a single unit of accounting. We were unable to reasonably estimate the period of performance under the 2012 Sanofi Genzyme agreement, as we were unable to estimate the timeline of our deliverables related to the deliverable for any additional TTR-specific RNAi therapeutic compounds. Through December 31, 2013, we had deferred all revenue, or $33.5 million, under the 2012 Sanofi Genzyme agreement.

2014 Sanofi Genzyme Collaboration

In January 2014, we entered into the 2014 Sanofi Genzyme collaboration. As noted above, the 2014 Sanofi Genzyme collaboration superseded and replaced the 2012 Sanofi Genzyme agreement.

The 2014 Sanofi Genzyme collaboration is structured as an exclusive relationship for the worldwide development and commercialization of RNAi therapeutics in the field of Genetic Medicines, which includes our current and future Genetic Medicine programs that reach Human Proof-of-Principle Study Completion (as defined in the Sanofi Genzyme master agreement), or Human POP, by the end of 2019, subject to extension to the end of 2021 in various circumstances. We will retain product rights in the United States, Canada and Western Europe, referred to as the Alnylam Territory, while Sanofi Genzyme will obtain exclusive rights to develop and commercialize collaboration products in the rest of the world, referred to as the Sanofi Genzyme Territory, together with certain broader co-development/co-commercialize or worldwide rights for certain products. Sanofi Genzyme’s rights, described in detail below, are structured as an opt-in that is triggered upon achievement of Human POP. We maintain development control for all programs prior to Sanofi Genzyme’s opt-in and maintain development and commercialization control after Sanofi Genzyme’s opt-in for all programs in the Alnylam Territory. We will retain global rights to any RNAi therapeutic Genetic Medicine program that does not reach Human POP by the end of 2019, subject to certain limited exceptions. We retain full rights to all current and future RNAi therapeutic programs outside of the field of Genetic Medicines, including the right to form new collaborations.

Under the 2014 Sanofi Genzyme collaboration, Sanofi Genzyme’s specific license rights and the programs into which Sanofi Genzyme has opted include the following:

|

|

• |

Regional license terms and programs — Upon opt-in, we will retain product rights in the Alnylam Territory, while Sanofi Genzyme will obtain exclusive rights to develop and commercialize the product in the Sanofi Genzyme Territory. Sanofi Genzyme can elect this license for any of our current and future Genetic Medicine programs that complete Human POP by the end of 2019, subject to limited extension. Development costs for products once Sanofi Genzyme exercises an option will be shared between Sanofi Genzyme and us, with Sanofi Genzyme responsible for twenty percent of the global development costs. Upon the effective date of the 2014 Sanofi Genzyme collaboration, Sanofi Genzyme expanded the scope of its regional license and collaboration for patisiran, an investigational RNAi therapeutic currently in Phase 3 clinical development, which was originally established under the 2012 Sanofi Genzyme agreement. In September 2015, Sanofi Genzyme elected to opt into our fitusiran clinical development program for the treatment of hemophilia and other rare bleeding disorders under the regional license terms. Cost-sharing for the fitusiran program began in January 2016 under the regional license terms. Sanofi Genzyme also had the right to elect to co-develop and co-commercialize fitusiran in the Alnylam Territory pursuant to the co-development/co-commercialize license terms described below. In November 2016, Sanofi Genzyme exercised this right and elected to co-develop and co-commercialize fitusiran in the Alnylam Territory. In addition, during 2016, Sanofi Genzyme elected not to opt into the development and commercialization of givosiran or ALN-CC5 in the Sanofi Genzyme Territory. Sanofi Genzyme will be required to make payments totaling up to $50.0 million upon the achievement of certain patisiran development milestones. We could potentially earn the next patisiran milestone payment, ranging between $5.0 million and $20.0 million based on the geographic region, upon the achievement of specified events in connection with a regulatory filing or approval. In addition, Sanofi Genzyme will be required to make payments totaling up to $75.0 million per regional product other than patisiran, consisting of up to $55.0 million in development milestones and $20.0 million in commercial milestones. Sanofi Genzyme will also be required to pay tiered double-digit royalties up to twenty percent for each regional product based on annual net sales, if any, of such regional product by Sanofi Genzyme, its affiliates and sublicensees. |

8

|

|

the exercise of its co-development/co-commercialize rights for fitusiran, Sanofi Genzyme paid us approximately $6.0 million in January 2017 for its incremental share of co-development costs incurred from January 2016 through September 2016. Sanofi Genzyme will be required to make payments totaling up to $75.0 million in development milestones for fitusiran, and, prior to the discontinuation of the revusiran program, was required to make certain milestone payments for revusiran. In December 2014, we earned a development milestone payment of $25.0 million based upon the initiation of the first global Phase 3 clinical trial for revusiran. We could potentially earn the first fitusiran milestone payment of $25.0 million upon the initiation of the first global Phase 3 clinical trial of fitusiran. Sanofi Genzyme will also be required to pay tiered double-digit royalties up to twenty percent for each co-development/co-commercialize product based on annual net sales, if any, in the Sanofi Genzyme Territory for such co-development/co-commercialize product by Sanofi Genzyme, its affiliates and sublicensees. The parties will share profits equally and we expect to book product sales in the Alnylam Territory. |

|

|

• |

Global license terms and programs — Upon opt-in, Sanofi Genzyme will obtain a worldwide license to develop and commercialize the product. Sanofi Genzyme had the right to elect a global license for givosiran, but instead elected a license to co-develop and co-commercialize fitusiran, as described above. Sanofi Genzyme continues to have one right to a global license through 2019, subject to limited extension, for a future Genetic Medicine program that was not one of our defined Genetic Medicine programs as of the effective date of the 2014 Sanofi Genzyme collaboration. Sanofi Genzyme shall be responsible for one hundred percent of global development costs. Sanofi Genzyme will be required to make payments totaling up to $200.0 million per global product, including up to $60.0 million in development milestones and $140.0 million in commercial milestones. Sanofi Genzyme will also be required to pay tiered double-digit royalties up to twenty percent for each global product based on annual net sales, if any, of each global product by Sanofi Genzyme, its affiliates and sublicensees. |

Due to the uncertainty of pharmaceutical development and the high historical failure rates generally associated with drug development, we may not receive any additional milestone payments or any royalty payments from Sanofi Genzyme under the 2014 Sanofi Genzyme collaboration.

Under the master agreement, the parties will collaborate in the development of option products, with us leading development for all programs prior to Sanofi Genzyme’s opt-in and also leading development and commercialization for all programs in the Alnylam Territory after Sanofi Genzyme’s opt-in. If Sanofi Genzyme does not exercise its option to license rights to a particular program, we will retain the exclusive right to develop and commercialize such program throughout the world, including the right to sublicense to third parties.

The 2014 Sanofi Genzyme collaboration is governed by an alliance joint steering committee that is comprised of an equal number of representatives from each party. There are additional committees to manage various aspects of each regional, co-developed/co-commercialized and global program. We and Sanofi Genzyme intend to enter into supply agreements to provide for supply of collaboration products to Sanofi Genzyme for clinical studies, and, at Sanofi Genzyme’s request, commercial sales. Sanofi Genzyme also has certain rights to manufacture collaboration products. Additionally, Sanofi Genzyme has certain limited opt-out rights, as specified in the master agreement, upon which products revert fully back to us with no further obligations to Sanofi Genzyme.

Upon the closing of the equity transaction in February 2014, we sold to Sanofi Genzyme 8,766,338 shares of our common stock and Sanofi Genzyme paid $700.0 million in aggregate cash consideration to us. As a condition to the closing of the equity transaction, Sanofi Genzyme entered into an investor agreement with us containing provisions regarding Sanofi Genzyme’s holding and “standstill” obligations, additional purchase, voting and registration rights, as well as certain other rights and obligations of the parties.

We recorded the issuance of 8,766,338 shares of our common stock under the stock purchase agreement using the price of our common stock on the date the shares were issued to Sanofi Genzyme. Based on the common stock price of $85.72, the fair value of the shares issued was $751.5 million, which was $51.5 million in excess of the proceeds received from Sanofi Genzyme for the issuance of our common stock. This $51.5 million is being amortized on a straight-line basis over the performance period. In addition, due to intraperiod tax allocation rules, upon closing of the equity transaction we recorded a benefit from income taxes of $15.2 million due to the Sanofi Genzyme equity purchase being recorded in additional paid-in capital, net of tax.

In accordance with the investor agreement, as a result of our issuance of shares in connection with our acquisition of Sirna Therapeutics, Inc., or Sirna, in March 2014, Sanofi Genzyme exercised its right to purchase an additional 344,448 shares of our common stock for $23.0 million. In addition, in January 2015, in connection with our public offering, Sanofi Genzyme exercised its right to purchase directly from us, in concurrent private placements, 744,566 shares of common stock at the public offering price resulting in $70.7 million in proceeds to us. The sales of common stock to Sanofi Genzyme were not registered as part of the public offering, though they were consummated simultaneously with the public offering.

9

Sanofi Genzyme also has the right at the beginning of each year to purchase a number of shares of our common stock based on the number of shares we issued during the previous year for compensation-related purposes. Sanofi Genzyme exercised this right to purchase directly from us 196,251 shares of our common stock on January 22, 2015 for $18.3 million and 205,030 shares of our common stock on February 1, 2016 for $14.3 million. In January 2017, Sanofi Genzyme elected not to exercise its compensation-related right for 2016. The sales of these shares to Sanofi Genzyme were consummated as private placements.

In each instance, the purchase by Sanofi Genzyme described above allowed Sanofi Genzyme to maintain its ownership level of our common stock of approximately 12 percent.

We determined that the deliverables for the programs on which Sanofi Genzyme was collaborating with us upon initiation of the 2014 Sanofi Genzyme collaboration included the licenses to our patisiran and revusiran clinical programs, which licenses were delivered to Sanofi Genzyme upon the closing date of the transaction, and the associated development activities, joint steering committee participation and information exchange for these clinical programs. We also determined that, pursuant to the accounting guidance governing revenue recognition on multiple element arrangements, the license and associated undelivered development activities, joint steering committee participation and information exchange activities did not have standalone value due to the specialized nature of the services to be provided by us. In addition, while Sanofi Genzyme has the ability to grant sublicenses, it cannot sublicense all or substantially all of its rights under the 2014 Sanofi Genzyme collaboration. The uniqueness of our services and the limited sublicense rights are indicators that standalone value is not present in the arrangement. Therefore the deliverables are not separable and, accordingly, the license and undelivered services were treated as a single unit of accounting. When multiple deliverables are accounted for as a single unit of accounting, we base our revenue recognition model on the final deliverable. Under the 2014 Sanofi Genzyme collaboration, the last deliverables for patisiran and revusiran were expected to be completed within approximately six years from the closing date of the transaction and the last deliverables for fitusiran are expected to be completed within approximately five years from the date Sanofi Genzyme elected to opt into our fitusiran clinical development program under the regional license terms. Our estimate regarding the performance period under the 2014 Sanofi Genzyme collaboration related to the license to our patisiran and revusiran clinical programs was adjusted in October 2016 due to our decision to discontinue development of revusiran. As a result, with respect to these programs, we currently expect the last deliverables to be completed within approximately five years from the closing date of the transaction.

We determined that the total cash received from Sanofi Genzyme under the now superseded 2012 Sanofi Genzyme agreement reflects consideration for certain of the performance obligations for ALN-TTR programs included in the 2014 Sanofi Genzyme collaboration. Therefore we are recognizing the $33.5 million of deferred revenue under the 2012 Sanofi Genzyme agreement on a straight-line basis over the period of performance of the ALN-TTR programs. As consideration is achieved, including any milestones or reimbursement for development activities, we recognize as revenue a portion of these payments equal to the percentage of the performance period completed when the milestone or activities have been satisfied, multiplied by the amount of the payment. We recognize the remaining portion of consideration received over the remaining performance period on a straight-line basis.

The following table presents information related to the 2014 Sanofi Genzyme collaboration, in thousands:

|

Excess of fair value of our common stock issued to Sanofi Genzyme in February 2014 |

|

$ |

(51,450 |

) |

|

Deferred revenue remaining under the 2012 Sanofi Genzyme agreement upon execution of the 2014 Sanofi Genzyme collaboration |

|

|

33,500 |

|

|

Milestone payment received: |

|

|

|

|

|

Year-ended December 31, 2014 |

|

|

25,000 |

|

|

Expense reimbursement from Sanofi Genzyme: |

|

|

|

|

|

Year-ended December 31, 2015 |

|

|

33,949 |

|

|

Year-ended December 31, 2016 |

|

|

54,337 |

|

|

Quarter-ended March 31, 2017 |

|

|

13,012 |

|

|

Total consideration at March 31, 2017 |

|

$ |

108,348 |

|

|

|

|

|

|

|

|

Cumulative revenue recognized at March 31, 2017 |

|

$ |

55,666 |

|

|

Deferred revenue at March 31, 2017 |

|

$ |

52,682 |

|

We determined that the opt-in rights that Sanofi Genzyme has for future Genetic Medicine programs represent separate and additional deliverables that Sanofi Genzyme may receive from us in future periods. Upon each initial opt-in by Sanofi Genzyme, we have determined that each program and the related activities will represent a single unit of accounting and, consistent with our accounting policies, we will base our revenue recognition period on the final deliverable associated with each future opt-in.

10

The following tables present information about our assets that are measured at fair value on a recurring basis at March 31, 2017 and December 31, 2016, and indicate the fair value hierarchy of the valuation techniques we utilized to determine such fair value, in thousands:

|

Description |

|

At March 31, 2017 |

|

|

Quoted Prices in Active Markets (Level 1) |

|

|

Significant Observable Inputs (Level 2) |

|

|

Significant Unobservable Inputs (Level 3) |

|

||||

|

Cash equivalents: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial paper |

|

$ |

4,990 |

|

|

$ |

— |

|

|

$ |

4,990 |

|

|

$ |

— |

|

|

Corporate notes |

|

|

625 |

|

|

|

— |

|

|

|

625 |

|

|

|

— |

|

|

Money market funds |

|

|

88,835 |

|

|

|

88,835 |

|

|

|

— |

|

|

|

— |

|

|

Marketable securities (fixed income): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Certificates of deposit |

|

|

16,900 |

|

|

|

— |

|

|

|

16,900 |

|

|

|

— |

|

|

Commercial paper |

|

|

92,791 |

|

|

|

— |

|

|

|

92,791 |

|

|

|

— |

|

|

Corporate notes |

|

|

210,119 |

|

|

|

— |

|

|

|

210,119 |

|

|

|

— |

|

|

U.S. government-sponsored enterprise securities |

|

|

281,359 |

|

|

|

— |

|

|

|

281,359 |

|

|

|

— |

|

|

U.S. treasury securities |

|

|

39,979 |

|

|

|

— |

|

|

|

39,979 |

|

|

|

— |

|

|

Marketable securities (Regulus equity holdings) |

|

|

2,682 |

|

|

|

2,682 |

|

|

|

— |

|

|

|

— |

|

|

Restricted cash (money market funds) |

|

|

1,471 |

|

|

|

1,471 |

|

|

|

— |

|

|

|

— |

|

|

Total |

|

$ |

739,751 |

|

|

$ |

92,988 |

|

|

$ |

646,763 |

|

|

$ |

— |

|

|

Description |

|

At December 31, 2016 |

|

|

Quoted Prices in Active Markets (Level 1) |

|

|

Significant Observable Inputs (Level 2) |

|

|

Significant Unobservable Inputs (Level 3) |

|

||||

|

Cash equivalents: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial paper |

|

$ |

17,199 |

|

|

$ |

— |

|

|

$ |

17,199 |

|

|

$ |

— |

|

|

Money market funds |

|

|

151,479 |

|

|

|

151,479 |

|

|

|

— |

|

|

|

— |

|

|

Marketable securities (fixed income): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Certificates of deposit |

|

|

17,999 |

|

|

|

— |

|

|

|

17,999 |

|

|

|

— |

|

|

Commercial paper |

|

|

59,340 |

|

|

|

— |

|

|

|

59,340 |

|

|

|

— |

|

|

Corporate notes |

|

|

333,872 |

|

|

|

— |

|

|

|

333,872 |

|

|

|

— |

|

|

U.S. government-sponsored enterprise securities |

|

|

297,773 |

|

|

|

— |

|

|

|

297,773 |

|

|

|

— |

|

|

U.S. treasury securities |

|

|

40,000 |

|

|

|

— |

|

|

|

40,000 |

|

|

|

— |

|

|

Marketable securities (Regulus equity holdings) |

|

|

8,997 |

|

|

|

8,997 |

|

|

|

— |

|

|

|

— |

|

|

Restricted cash (money market funds) |

|

|

1,471 |

|

|

|

1,471 |

|

|

|

— |

|

|

|

— |

|

|

Total |

|

$ |

928,130 |

|

|

$ |

161,947 |

|

|

$ |

766,183 |

|

|

$ |

— |

|

During the three months ended March 31, 2017, there were no transfers between Level 1 and Level 2 financial assets. The carrying amounts reflected in our condensed consolidated balance sheets for cash, billed and unbilled collaboration receivables, other current assets, accounts payable and accrued expenses approximate fair value due to their short-term maturities. The fair value of our long-term debt at March 31, 2017, computed pursuant to a discounted cash flow technique using a market interest rate, was $150.2 million and is considered a Level 3 fair value measurement. The effective interest rate reflects the current market rate.

11

The following tables summarize the fair value, accumulated other comprehensive income (loss) and intraperiod tax allocation regarding our investment in Regulus available-for-sale marketable securities at March 31, 2017 and 2016, and for the activity recorded for the three months ended March 31, 2017 and 2016, in thousands:

|

Description |

|

At December 31, 2016 |

|

|

Sales of Regulus Shares During Three Months Ended March 31, 2017 |

|

|

All Other Activity During Three Months Ended March 31, 2017 |

|

|

Balance at March 31, 2017 |

|

||||

|

Carrying value |

|

$ |

8,093 |

|

|

$ |

(4,803 |

) |

|

$ |

(608 |

) |

|

$ |

2,682 |

|

|

Accumulated other comprehensive income (loss), before tax |

|

|

904 |

|

|

|

1,549 |

|

|

|

(2,453 |

) |

|

|

— |

|

|

Investment in equity securities of Regulus, as reported |

|

$ |

8,997 |

|

|

$ |

(3,254 |

) |

|

$ |

(3,061 |

) |

|

$ |

2,682 |

|

|

Accumulated other comprehensive income (loss), before tax |

|

$ |

904 |

|

|

$ |

1,549 |

|

|

$ |

(2,453 |

) |

|

$ |

— |

|

|

Intraperiod tax allocation recorded as a benefit from income taxes |

|

|

(32,792 |

) |

|

|

— |

|

|

|

— |

|

|

|

(32,792 |

) |

|

Accumulated other comprehensive income (loss), net of tax |

|

$ |

(31,888 |

) |

|

$ |

1,549 |

|

|

$ |

(2,453 |

) |

|

$ |

(32,792 |

) |

|

Description |

|

At December 31, 2015 |

|

|

Sales of Regulus Shares During Three Months Ended March 31, 2016 |

|

|

All Other Activity During Three Months Ended March 31, 2016 |

|

|

Balance at March 31, 2016 |

|

||||

|

Carrying value |

|

$ |

11,935 |

|

|

$ |

(2,024 |

) |

|

$ |

— |

|

|

$ |

9,911 |

|

|

Accumulated other comprehensive income (loss), before tax |

|

|

39,484 |

|

|

|

(5,156 |

) |

|

|

(10,305 |

) |

|

|

24,023 |

|

|

Investment in equity securities of Regulus, as reported |

|

$ |

51,419 |

|

|

$ |

(7,180 |

) |

|

$ |

(10,305 |

) |

|

$ |

33,934 |

|

|

Accumulated other comprehensive income (loss), before tax |

|

$ |

39,484 |

|

|

$ |

(5,156 |

) |

|

$ |

(10,305 |

) |

|

$ |

24,023 |

|

|

Intraperiod tax allocation recorded as a benefit from income taxes |

|

|

(32,792 |

) |

|

|

— |

|

|

|

— |

|

|

|

(32,792 |

) |

|

Accumulated other comprehensive income (loss), net of tax |

|

$ |

6,692 |

|

|

$ |

(5,156 |

) |

|

$ |

(10,305 |

) |

|

$ |

(8,769 |

) |

We obtain fair value measurement data for our marketable securities from independent pricing services. We perform validation procedures to ensure the reasonableness of this data. This includes meeting with the independent pricing services to understand the methods and data sources used. Additionally, we perform our own review of prices received from the independent pricing services by comparing these prices to other sources and confirming those securities are trading in active markets.

The following tables summarize our marketable securities, other than our holdings in Regulus noted above, at March 31, 2017 and December 31, 2016, in thousands:

|

|

|

At March 31, 2017 |

|

|||||||||||||

|

|

|

Amortized Cost |

|

|

Gross Unrealized Gains |

|

|

Gross Unrealized Losses |

|

|

Fair Value |

|

||||

|

Certificates of deposit |

|

$ |

16,900 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

16,900 |

|

|

Commercial paper |

|

|

92,791 |

|

|

|

— |

|

|

|

— |

|

|

|

92,791 |

|

|

Corporate notes |

|

|

210,363 |

|

|

|

42 |

|

|

|

(286 |

) |

|

|

210,119 |

|

|

U.S. government-sponsored enterprise securities |

|

|

282,117 |

|

|

|

— |

|

|

|

(758 |

) |

|

|

281,359 |

|

|

U.S. treasury securities |

|

|

40,013 |

|

|

|

— |

|

|

|

(34 |

) |

|

|

39,979 |

|

|

Total |

|

$ |

642,184 |

|

|

$ |

42 |

|

|

$ |

(1,078 |

) |

|

$ |

641,148 |

|

12

|

|

|

At December 31, 2016 |

|

|||||||||||||

|

|

|

Amortized Cost |

|

|

Gross Unrealized Gains |

|

|

Gross Unrealized Losses |

|

|

Fair Value |

|

||||

|

Certificates of deposit |

|

$ |

17,999 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

17,999 |

|

|

Commercial paper |

|

|

59,340 |

|

|

|

— |

|

|

|

— |

|

|

|

59,340 |

|

|

Corporate notes |

|

|

334,266 |

|

|

|

47 |

|

|

|

(441 |

) |

|

|

333,872 |

|

|

U.S. government-sponsored enterprise securities |

|

|

298,910 |

|

|

|

9 |

|

|

|

(1,146 |

) |

|

|

297,773 |

|

|

U.S. treasury securities |

|

|

40,022 |

|

|

|

1 |

|

|

|

(23 |

) |

|

|

40,000 |

|

|

Total |

|

$ |

750,537 |

|

|

$ |

57 |

|

|

$ |

(1,610 |

) |

|

$ |

748,984 |

|

We classify our debt security investments based on their contractual maturity dates. The following table summarizes our available-for-sale debt securities by contractual maturity, at March 31, 2017, in thousands:

|

|

|

At March 31, 2017 |

|

|||||

|

|

|

Amortized Cost |

|

|

Fair Value |

|

||

|

Less than one year |

|

$ |

386,115 |

|

|

$ |

385,843 |

|

|

Greater than one year but less than two years |

|

|

256,069 |

|

|

|

255,305 |

|

|

Total |

|

$ |

642,184 |

|

|

$ |

641,148 |

|

5. COMMITMENTS AND CONTINGENCIES

Manufacturing Facility

In February 2016, we entered into an agreement with 20 Commerce LLC to purchase 12 acres of undeveloped land in Norton, Massachusetts. We completed the purchase and closed this transaction on April 4, 2016. We are constructing a manufacturing facility at this site for drug substance, including small interfering RNAs, or siRNAs, and siRNA conjugates, for clinical and commercial use. At March 31, 2017 and December 31, 2016, property, plant and equipment, net, on our condensed consolidated balance sheets reflects $88.6 million and $73.2 million, respectively, of land and associated costs related to the construction of our drug substance manufacturing facility.

Credit Agreements

On April 29, 2016, we entered into (i) a Credit Agreement, or the BOA Credit Agreement, with Alnylam U.S., Inc., our wholly-owned subsidiary, as the borrower, us, as a guarantor, and Bank of America N.A., or BOA, as the lender and (ii) a Credit Agreement, or the Wells Credit Agreement, together with the BOA Credit Agreement, the Credit Agreements, by and among Alnylam U.S., Inc., as the borrower, us, as a guarantor, and Wells Fargo Bank, National Association, or Wells, as the lender. The Credit Agreements were entered into in connection with the planned build out of our new drug substance manufacturing facility.

The BOA Credit Agreement and the Wells Credit Agreement provide for a $120.0 million and a $30.0 million term loan facility, respectively, and mature on April 29, 2021. The proceeds of the borrowing under each of the BOA Credit Agreement and the Wells Credit Agreement are to be used for working capital and general corporate purposes. Interest on borrowings under the Credit Agreements is calculated based on LIBOR plus 0.45 percent, except in the event of default. The borrower may prepay loans under each of the BOA Credit Agreement and the Wells Credit Agreement at any time, without premium or penalty, subject to certain notice requirements and LIBOR breakage costs.

The obligations of the borrower under each Credit Agreement are guaranteed by us. The obligations of the borrower and us under each Credit Agreement are secured by cash collateral in an amount equal to, at any given time, at least 100 percent of the principal amount of all term loans outstanding under such Credit Agreement at such time. At each of March 31, 2017 and December 31, 2016, we have recorded $150.0 million of cash collateral in connection with the Credit Agreements as restricted investments on our condensed consolidated balance sheets.

Each Credit Agreement contains limited representations and warranties and limited affirmative and negative covenants, including quarterly reporting obligations, as well as certain customary events of default.

During the three months ended March 31, 2017, we recorded $0.4 million of interest expense related to the Credit Agreements that is reflected in other income (expense) on our condensed consolidated statements of comprehensive loss.

13

University of Utah Litigation

On March 22, 2011, The University of Utah, or Utah, filed a civil complaint in the United States District Court for the District of Massachusetts, or the MA District Court, against us, Max Planck Gesellschaft Zur Foerderung Der Wissenschaften e.V. and Max Planck Innovation GmbH, together, Max Planck, the Whitehead Institute for Biomedical Research, or Whitehead, the Massachusetts Institute of Technology, or MIT, and the University of Massachusetts, or UMass, claiming a professor at Utah is the sole inventor or, in the alternative, a joint inventor, of the Tuschl patents. Utah was seeking changes to the inventorship of the Tuschl patents, unspecified damages and other relief. After several years of court proceedings and discovery, on September 28, 2015, the MA District Court granted both of our motions for summary judgment, finding that there was no collaboration between Dr. Bass and Dr. Tuschl, which is a pre-requisite for co-inventorship, and dismissing Utah’s state law damages claims as well.

On October 28, 2015, Utah filed a notice of appeal to the United States Court of Appeals for the Federal Circuit, or the CAFC. On December 18, 2015, the CAFC entered an order dismissing Utah’s appeal following a joint motion filed by us and Utah seeking dismissal of the appeal with prejudice. This disposed of Utah’s inventorship claims and its state law claims for damages. On October 14, 2015, we filed a motion with the MA District Court seeking reimbursement of costs and fees associated with defending this action in the amount of approximately $8.0 million. On November 30, 2015, the MA District Court denied our motion and on December 15, 2015, we filed a notice of appeal of this ruling with the CAFC. Oral arguments on our appeal were heard at the CAFC on January 12, 2017. On March 23, 2017, the CAFC denied our appeal and we have decided not to appeal this ruling any further.

Dicerna Litigation

On June 10, 2015, we filed a trade secret misappropriation lawsuit against Dicerna Pharmaceuticals, Inc., or Dicerna, in the Superior Court of Middlesex County, Massachusetts, seeking to stop misappropriation by Dicerna of our confidential, proprietary and trade secret information related to the RNAi assets we purchased from Merck, including certain GalNAc conjugate technology. In addition to permanent injunctive relief, we are also seeking monetary damages from Dicerna. On July 10, 2015, Dicerna filed its answer to our complaint, in which it denied our claims, along with initial discovery requests, to which we responded in a timely fashion. On July 27, 2015, Dicerna filed a motion seeking removal of the case to the Business Litigation Session of the Superior Court of Suffolk County, which we opposed. On August 31, 2015, the Court denied Dicerna’s motion. We and Dicerna agreed to a protective order, which was entered by the Court on November 12, 2015. Discovery is ongoing and we now expect fact discovery to close in June 2017.

Although we believe we have meritorious claims in this matter, litigation is subject to inherent uncertainty and a court could ultimately rule against us. In addition, litigation and related matters are costly and may divert the attention of our management and other resources that would otherwise be engaged in other activities.

Our accounting policy for accrual of legal costs is to recognize such expenses as incurred.

14

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

This Quarterly Report on Form 10-Q contains forward-looking statements that involve risks and uncertainties. The statements contained in this Quarterly Report on Form 10-Q that are not purely historical are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. Without limiting the foregoing, the words “may,” “will,” “should,” “could,” “expects,” “plans,” “intends,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue,” “target,” “goal” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these words. All forward-looking statements included in this Quarterly Report on Form 10-Q are based on information available to us up to, and including, the date of this document, and we expressly disclaim any obligation to update any such forward-looking statements to reflect events or circumstances that arise after the date hereof. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain important factors, including those set forth in this Item 2 — “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” as well as under Part II, Item 1A — “Risk Factors” and elsewhere in this Quarterly Report on Form 10-Q. You should carefully review those factors and also carefully review the risks outlined in other documents that we file from time to time with the Securities and Exchange Commission, or SEC.

Overview

We are a biopharmaceutical company developing novel therapeutics based on RNA interference, or RNAi. RNAi is a naturally occurring biological pathway within cells for selectively silencing and regulating the expression of specific genes. Since many diseases are caused by the inappropriate activity of specific genes, the ability to silence genes selectively through RNAi could provide a new way to treat a wide range of human diseases. We believe that drugs that work through RNAi have the potential to become a broad new class of innovative medicines, and that this potential new drug class is similar to the opportunity created with other major biological discoveries such as recombinant DNA and monoclonal antibodies. Using our intellectual property and expertise, we are developing what we believe to be a reproducible and modular platform to develop RNAi therapeutics for a variety of human diseases.

Our research and development strategy is focused primarily on the use of our proprietary N-acetylgalactosamine, or GalNAc-conjugate platform for delivery of small interfering RNAs, or “siRNAs” — the molecules that mediate RNAi — toward genetically validated, liver-expressed target genes involved in the cause or pathway of human diseases. We are also focused on clinical indications where there are high unmet needs, early biomarkers for the assessment of clinical activity in Phase 1 clinical studies, and a definable path for drug development, regulatory approval, patient access and commercialization.

Specifically, our broad pipeline of investigational RNAi therapeutics is focused in three Strategic Therapeutic Areas, or “STArs:” Genetic Medicines, with multiple product candidates for the treatment of rare diseases; Cardio-Metabolic Diseases, with product candidates directed toward genetically validated, liver-expressed disease targets for unmet needs in cardiovascular and metabolic diseases; and Hepatic Infectious Diseases, with product candidates designed to address the major global health challenges of hepatic infectious diseases, beginning with hepatitis B and hepatitis D viral infections. We are focused on advancement of our Alnylam 2020 strategy for the development and commercialization of RNAi therapeutics as a potential new class of innovative medicines. Specifically, our goal is to achieve, by the end of 2020, a company profile with three marketed products and ten RNAi therapeutic clinical programs, including four in late stages of development, across our three STArs. Our most advanced investigational RNAi therapeutic in development, patisiran, targets the transthyretin, or TTR, gene for the treatment of patients with polyneuropathy due to hereditary TTR-mediated amyloidosis, or hATTR amyloidosis. We expect to report top-line data from our ongoing APOLLO Phase 3 study of patisiran in mid-2017. Assuming that the APOLLO data are positive, we plan to submit our first new drug application, or NDA, and marketing authorization application, or MAA, for patisiran by the end of 2017. We expect to advance additional investigational RNAi therapeutics into Phase 3 development during 2017, including fitusiran, for the treatment of hemophilia and rare bleeding disorders, and givosiran, for the treatment of acute hepatic porphyrias.

Based on our expertise in RNAi therapeutics and broad intellectual property estate, we have formed alliances with leading pharmaceutical and life sciences companies to support our development and commercialization efforts, including Sanofi Genzyme, the specialty care global business unit of Sanofi, and The Medicines Company, or MDCO. We have incurred significant losses since we commenced operations in 2002 and expect such losses to continue for the foreseeable future. At March 31, 2017, we had an accumulated deficit of $1.76 billion. Historically, we have generated losses principally from costs associated with research and development activities, acquiring, filing and expanding intellectual property rights and general administrative costs. As a result of planned expenditures for research and development activities relating to our research platform, our drug development programs, including clinical trial and manufacturing costs, the establishment of late stage clinical and commercial capabilities, including European operations, the construction of our drug substance manufacturing facility, continued management and growth of our patent portfolio, collaborations and general corporate activities, we expect to incur additional operating losses for the foreseeable future. We also anticipate that our operating results will fluctuate for the foreseeable future. Therefore, period-to-period comparisons should not be relied upon as predictive of the results in future periods.

15

Although we currently have multiple clinical development programs, we are unable to predict when, if ever, we will successfully develop or be able to commence sales of any product. A substantial portion of our total net revenues in recent years has been derived from collaboration revenues from strategic alliances with Takeda, Monsanto, Sanofi Genzyme and MDCO. We expect our sources of potential funding for the next several years to be derived primarily from existing and new strategic alliances, which may include license and other fees, funded research and development and milestone payments, and proceeds from the sale of equity or debt.

Research and Development

Since our inception, we have focused on drug discovery and development programs. Research and development expenses represent a substantial percentage of our total operating expenses, as reflected by our broad pipeline of product development programs.

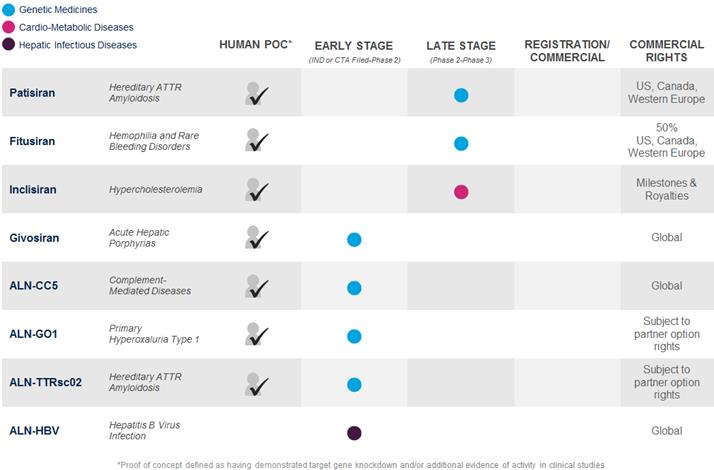

The following is a summary of our product development programs as of April 30, 2017, that identifies those programs in which we have achieved human proof of concept, or POC, by demonstrating target gene knockdown and/or additional evidence of activity in clinical studies, the development stage of our programs and our commercial rights to such programs:

During the first quarter of 2017 and recent period, we reported the following updates from our late-stage clinical programs:

|

|

• |

We continued to advance patisiran, presenting final 24-month data from our Phase 2 open-label extension, or OLE, study in April 2017. We expect to report top-line results from our APOLLO Phase 3 clinical study of patisiran in mid-2017. |

|

|

• |

We continued to advance fitusiran, presenting positive new data from our Phase 1 clinical trial in February 2017. |

16

|

|