Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - APOGEE ENTERPRISES, INC. | apog-ex322_20173410k.htm |

| EX-32.1 - EXHIBIT 32.1 - APOGEE ENTERPRISES, INC. | apog-ex321_20173410k.htm |

| EX-31.2 - EXHIBIT 31.2 - APOGEE ENTERPRISES, INC. | apog-ex312_20173410k.htm |

| EX-31.1 - EXHIBIT 31.1 - APOGEE ENTERPRISES, INC. | apog-ex311_20173410k.htm |

| EX-23 - EXHIBIT 23 - APOGEE ENTERPRISES, INC. | apog-ex23_20173410k.htm |

| EX-21 - EXHIBIT 21 - APOGEE ENTERPRISES, INC. | apog-ex21_20173410k.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_________________________________

FORM 10-K

_________________________________

x | ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 4, 2017

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 0-6365

_________________________________

APOGEE ENTERPRISES, INC.

(Exact name of registrant as specified in its charter)

_________________________________

Minnesota | 41-0919654 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

4400 West 78th Street – Suite 520, Minneapolis, MN | 55435 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (952) 835-1874

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |||

Common Stock, $0.33 1/3 Par Value | The NASDAQ Stock Market LLC | |||

Securities registered pursuant to Section 12(g) of the Act: None

________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x | Accelerated filer | ¨ | |||

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Emerging growth company | ¨ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ¨ | |||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

As of August 27, 2016, the last business day of the registrant's most recently completed second fiscal quarter, the approximate aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant was $1,386,000,000 (based on the closing price of $47.97 per share as reported on the NASDAQ Stock Market LLC as of that date).

As of April 26, 2017, 28,679,636 shares of the registrant’s common stock, par value $0.33 1/3 per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required in Part III hereof is incorporated by reference to the Proxy Statement for the registrant's 2017 Annual Meeting of Shareholders to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after the end of the fiscal year covered by this Form 10-K.

APOGEE ENTERPRISES, INC.

Annual Report on Form 10-K

For the fiscal year ended March 4, 2017

TABLE OF CONTENTS

Page | ||

3

PART I

ITEM 1. BUSINESS

The Company

Apogee Enterprises, Inc. (Apogee, the Company or we) was incorporated under the laws of the State of Minnesota in 1949. We are a world leader in certain technologies involving the design and development of value-added glass products and services.

Our Company has four reporting segments, with three of the segments serving the commercial construction market:

• | The Architectural Glass segment fabricates coated, high-performance glass used globally in customized window and wall systems. For fiscal 2017, the Architectural Glass segment accounted for approximately 33 percent of our net sales. |

• | The Architectural Framing Systems segment designs, engineers, fabricates and finishes the aluminum frames used in customized window, curtainwall, storefront and entrance systems comprising the outside skin of buildings. For fiscal 2017, the Architectural Framing Systems segment accounted for approximately 35 percent of our net sales. |

• | The Architectural Services segment provides full-service installation of the walls of glass, windows and other curtainwall products making up the outside skin of buildings. For fiscal 2017, the Architectural Services segment accounted for approximately 24 percent of our net sales. |

• | The Large-Scale Optical Technologies (LSO) segment manufactures value-added glass and acrylic products for framing and display applications. For fiscal 2017, this segment accounted for approximately 8 percent of our net sales. |

On December 14, 2016, we acquired substantially all the assets of Sotawall, Inc. (now operating under the name Sotawall Limited or "Sotawall"), a privately-held designer and fabricator of high-performance, unitized curtainwall systems for commercial construction projects based in the Toronto, Canada area, for approximately $138 million. Sotawall's results of operations have been included in the consolidated financial statements and within the Architectural Framing Systems segment since the date of acquisition.

Strategy

Our overall strategy in the Architectural Glass and Architectural Framing Systems segments is to deliver growth faster than our commercial construction markets. We accomplish this through geographic and market segment expansion and new product offerings, while differentiating ourselves through superior service and lead times. In recent years, we have increased our focus on window and curtainwall retrofit and renovation of existing commercial buildings. We have seen increased interest from the non-residential and high-end multi-family residential building sectors in upgrading façades and improving energy efficiency. We consider this to be a significant opportunity for Apogee in the coming years.

In the Architectural Services segment, our emphasis is on improving margins through focused project selection, while continuing to deliver organic growth in line with our available project management capacity.

Within the LSO segment, our strategy is to grow domestically and internationally by continuing to convert the custom picture framing and fine art markets from clear uncoated glass and acrylic products to value-added products that protect art from UV damage and minimize reflection. Additionally, we have begun to enter new display markets that desire the value-added properties our glass and acrylic products provide in an effort to diversify LSO's product offerings.

We believe each of our segments has the ability to grow organically through entry into new geographies, further penetration in existing geographies and introduction of new products. We also regularly evaluate business development opportunities in adjacent sectors. Any of these strategies can also be executed by acquisition or strategic alliances.

Finally, we are constantly working to improve the efficiency and productivity of our operations by implementing lean manufacturing disciplines and automation. We expect these efforts to continue to deliver gross margin expansion into the foreseeable future.

Products and Services

Architectural Glass, Architectural Framing Systems and Architectural Services segments

These segments participate in various phases of the value chain to design, engineer, fabricate and install customized glass and aluminum window, curtainwall, storefront and entrance systems comprising the outside skin of buildings in the commercial, institutional and high-end multi-family residential construction sectors.

In our Architectural Glass segment, we add ultra-thin, high-performance coatings to uncoated glass to create a variety of aesthetic characteristics, unique designs and energy efficiency, including varying levels of solar energy management, aligned with the industry trend of increasingly energy-efficient buildings. We also laminate layers of glass and vinyl to protect against hurricanes and other severe impacts, and temper, or heat strengthen, glass to provide additional strength. Our high-performance glass is

4

custom made-to-order and is typically fabricated into insulating and/or laminated glass units for installation into window, curtainwall, storefront or entrance systems.

Within our Architectural Framing Systems segment, we design and fabricate window, curtainwall, storefront and entrance systems using our customized aluminum and glass, or glass supplied by others. We also provide finishing services for metal components used in windows and curtainwall, as well as plastic components for other products.

By integrating technical capabilities, project management skills and field installation services, our Architectural Services segment provides design, engineering, fabrication and installation expertise for the outside skin of buildings. Our ability to efficiently design high-quality window and curtainwall systems and effectively manage the installation of building façades allows our customers to meet or exceed the timing and cost requirements of their jobs.

Our product and service offerings allow architects to create distinctive looks for office towers, hotels, education facilities and dormitories, health care facilities, government buildings, retail centers and multi-family residential buildings, while meeting functional requirements such as energy efficiency, hurricane, blast and other impact resistance and/or sound control.

LSO segment

The LSO segment provides coated glass and acrylic primarily for use in framing and display applications. Products vary based on size and coatings applied to provide conservation-grade UV protection, anti-reflective and anti-static properties and/or security features.

Product Demand and Distribution Channels

Architectural Glass, Architectural Framing Systems and Architectural Services segments

Demand for the products and services offered by our Architectural segments is affected by changes in the North American commercial construction industries, as well as by changes in general economic conditions. Additionally, the Architectural Glass segment has an operation in Brazil and is, therefore, also impacted by Brazil's commercial construction industry and general economic conditions.

We look at several external indicators to analyze potential demand for our products and services, such as U.S. job growth, office space vacancy rates, credit and interest rates available for commercial construction projects, architectural billing statistics and material costs. We also rely on our own internal indicators to analyze demand. This includes our sales pipeline, made up of contracts in review, projects awarded or committed, and bidding activity. Our sales pipeline, together with ongoing feedback, analysis and data from our customers, architects and building owners, provide visibility into near- and medium-term future demand. Additionally, we evaluate data on U.S. non-residential construction market activity, industry analysis and longer-term trends provided by external data sources.

Our architectural products and services are used in subsets of the construction industry differentiated by building type, level of customization required, customers, geographic location and project size.

Building type - The construction industry is typically segmented into residential construction and non-residential construction, which includes commercial, industrial and institutional construction. Our products and services are primarily used in commercial buildings (office towers, hotels and retail centers) and institutional buildings (education facilities and dormitories, health care facilities and government buildings), as well as in high-end multi-family residential buildings (a subset of residential construction).

Level of customization - The large majority of our projects involve a high degree of customization, as the product or service is based on customer-specified requirements for aesthetics, performance and size, and is designed to satisfy local building codes.

Customers and distribution channels - Our customers are mainly glazing subcontractors and general contractors, with project design being influenced by architects and building owners. Our high-performance architectural glass is primarily sold using a direct sales force and independent sales representatives. Installation services are marketed by a direct sales force in certain metropolitan areas in the U.S. We also have the ability to provide remote project management throughout the U.S. We market our custom and standard windows, curtainwall, storefront and entrance systems using a combination of direct sales forces, independent sales representatives and distributors.

Geographic location - We primarily supply architectural glass products to customers in North America, with some international sales of our high-performance architectural glass. We estimate the U.S. demand for architectural glass fabrication in non-residential buildings is in excess of $1 billion annually. Our aluminum framing systems, including windows, curtainwall, storefront and entrances, are marketed in the U.S. and Canada, and we estimate demand to be in excess of $3 billion annually. In installation

5

services, we are one of only a few architectural glass installation companies in the U.S. to have a national presence, and we estimate the U.S. demand to be in the range of $10 to $15 billion.

Project size - Our Architectural Glass segment primarily serves mid-size to monumental high-profile projects. Architectural Framing Systems primarily targets small and mid-size projects, and Architectural Services primarily serves mid-size projects.

LSO segment

In our LSO segment, we have the largest domestically manufactured brand of value-added glass and acrylic used in the custom picture framing market. Under the Tru Vue brand, products are sold primarily in North America through national and regional retail chains using a direct sales force, as well as through local picture framing shops using an independent distribution network. We also supply our glass and acrylic products to museums and public and private galleries and collections worldwide through independent distributors.

Competitive Conditions

Architectural Glass, Architectural Framing Systems and Architectural Services segments

The North American commercial construction market is highly fragmented. Competitive factors include price, product quality, product attributes and performance, reliable service, on-time delivery, lead-time, warranty and the ability to provide technical engineering and design services. To protect and enhance our competitive position, we maintain strong relationships with architects, who influence the selection of products and services on a project, and with general contractors, who initiate projects and develop specifications.

In our Architectural Glass segment, we experience competition from regional glass fabricators who can provide certain products with attributes similar to our products. Within the market sector for large, complex projects, we encounter competition from international companies, which have products that may be equivalent to or have different characteristics than we provide. This international competition has strengthened in recent years due to the relative strength of the U.S. dollar.

The commercial window and storefront manufacturing industry is highly fragmented, and our Architectural Framing Systems segment competes against several national, regional and local aluminum window and storefront manufacturers, as well as regional paint and anodizing companies. When providing installation services, our Architectural Services segment competes against national, regional and local glass installation companies.

LSO segment

Product attributes, price, quality, marketing and service are the primary competitive factors in the LSO segment. Our competitive strengths include our excellent relationships with customers, innovative marketing programs and the performance of our value-added products. We compete with certain European valued-added glass and acrylic products for picture framing.

Warranties

We offer product and service warranties that we believe are competitive for the markets in which our products and services are sold. The nature and extent of these warranties depend upon the product or service, the market and, in some cases, the customer being served. Our standard warranties are generally from two to 10 years for our architectural glass, curtainwall and window system products, while we generally offer warranties of two years or less on our other products and services.

Sources and Availability of Raw Materials

Raw materials used within the Architectural Glass segment include flat glass, vinyl, silicone sealants and lumber. The Architectural Framing Systems segment's materials include aluminum billet and extrusions, fabricated glass, plastic extrusions, hardware, paint and chemicals. Within the Architectural Services segment, materials used include fabricated glass, aluminum extrusions and fabricated metal panels. The LSO segment mainly uses glass and acrylics. A majority of our raw materials are readily available from a variety of domestic and international sources.

Trademarks and Patents

We have several trademarks and trade names that we believe have significant value in the marketing of our products, including APOGEE®. Trademark registrations in the U.S. are generally for a term of 10 years, renewable every 10 years as long as the trademark is used in the regular course of trade.

Within the Architectural Glass segment, VIRACON®, DIGITALDISTINCTIONS®, ROOMSIDE®, EXTREMEDGE®, BUILDING DESIGN®, GLASS IS EVERYTHING®, CLEARPOINT®, CYBERSHIELD® and STORMGUARD® are registered trademarks. VIRASPAN™ is an unregistered trademark. In addition, GLASSEC®, INSULATTO® and BLINDATTO® are registered trademarks in Brazil. GLASSECVIRACON™ is an unregistered trademark in Brazil.

6

Within the Architectural Framing Systems segment, LINETEC®, WAUSAU WINDOW AND WALL SYSTEMS®, TUBELITE®, ADVANTAGE BY WAUSAU®, 300ES®, FINISHER OF CHOICE®, THERML=BLOCK®, MAXBLOCK®, DFG®, ECOLUMINUM®, ALUMINATE®, GET THE POINT!®, FORCEFRONT®, SOTAWALL®, SOTA® and HYBRID-WALL® are registered trademarks. CUSTOM WINDOW™, INVENT™, INVENT.PLUS™, INVENT RETRO™, INVISION™, CLEARSTORY™, EPIC™, HERITAGE™, VISULINE™, SEAL™, SUPERWALL™ and CROSSTRAK™ are unregistered trademarks. ALUMICOR™ and BUILDING EXCELLENCETM are unregistered trademarks in Canada.

Within the Architectural Services segment, HARMON®, H DESIGN®, HARMON GLASS®, HI-7000® and INNOVATIVE FAÇADE SOLUTIONS® are registered trademarks. UCW-8000™, HI-8500™, HI-9000™, SMU-6000™, HPW-250™ and BUILDING TRUST IN EVERYTHING WE DO™ are unregistered trademarks.

Within the LSO segment, TRU VUE®, CONSERVATION CLEAR®, CONSERVATION MASTERPIECE ACRYLIC®, CONSERVATION REFLECTION CONTROL®, ULTRAVUE®, MUSEUM GLASS®, OPTIUM®, PREMIUM CLEAN®, REFLECTION CONTROL®, AR REFLECTION-FREE®, TRU VUE AR®, OPTIUM ACRYLIC®, OPTIUM MUSEUM ACRYLIC®, CONSERVATION MASTERPIECE®, STATICSHIELD®, TRULIFE® and VISTA AR® are registered trademarks. TRULIFE INFINITY FRAMETM, THE DIFFERENCE IS CLEARTM and TRU FRAMEABLE MOMENTSTM are unregistered trademarks.

We have several patents pertaining to our glass coating methods and products, including our UV coating and etch processes for anti-reflective glass for the picture framing industry and fine art market, as well as a patent for an indirect daylighting device and patents for hybrid window wall/curtain wall systems and methods of installation. Despite being a point of differentiation from our competitors, no single patent is considered to be material.

Seasonality

We do not experience a significant seasonal effect in our Architectural segments. However, the construction industry is highly cyclical in nature and can be influenced differently by the effects of local economies.

Within the LSO segment, picture framing glass and acrylic sales tend to increase in the September-to-December timeframe, but the timing of customer promotional activities may offset some of this seasonal impact.

Working Capital Requirements

Trade accounts receivable is the largest component of working capital for the Company, including receivables relating to contractual retention amounts that can be outstanding throughout a project's duration within the Architectural Services segment. Inventory requirements are not significant in any of our segments, although the LSO segment requires greater inventory levels as it builds to stock to meet the demands of its customers.

Backlog

Backlog represents the dollar amount of signed contracts or firm orders, generally as a result of a competitive bidding process, which is expected to be recognized as revenue primarily in the near-term. Backlog is not a term defined under U.S. GAAP and is not a measure of contract profitability. Backlog should not be used as the sole indicator of our future revenue because we have a substantial amount of projects with short lead times that book-and-bill within the same reporting period that are not included in backlog. We have strong visibility beyond backlog as projects awarded, verbal commitments and bidding activities are monitored separately and not included in backlog.

Architectural Glass segment backlog as of year-end was $66.4 million, compared to $62.4 million in the prior year, net of intersegment eliminations. This segment has strategically shortened lead-times, with capability and productivity improvements, in order to serve mid-size projects where there is a higher level of book-and-bill activity within quarters. The backlog is all expected to be filled in fiscal 2018.

Architectural Framing Systems segment backlog has grown to $245.4 million at year-end, compared to $123.0 million at the end of the prior year, due to recent increased order activity, particularly of longer lead-time contracts. The acquisition of Sotawall contributed approximately $70 million to this segment's backlog. Approximately 75 percent of the backlog in this segment is expected to be filled in fiscal 2018, with the remainder expected to be filled in fiscal 2019 and beyond.

Backlog in the Architectural Services segment declined from $320.4 million at the end of the prior year to $255.1 million at March 4, 2017, due to timing of firm orders and signed contracts. Approximately 67 percent of the backlog in this segment is expected to be filled during fiscal 2018, with the remainder expected to be filled in fiscal 2019 and beyond.

Backlog is not a significant metric for the LSO segment, as orders are typically booked and billed within a short time frame.

7

Research and Development

The amount spent on research and development activities was $8.6 million, $8.0 million and $6.5 million in fiscal 2017, 2016 and 2015, respectively. Of this amount, $2.2 million, $2.4 million and $2.4 million, respectively, were focused primarily upon design of custom window and curtainwall systems in accordance with customer specifications and are included in cost of sales in the accompanying consolidated financial statements.

Environment

We use hazardous materials in our manufacturing operations, and have air and water emissions that require controls. As a result, we are subject to stringent federal, state and local regulations governing the storage and use of these materials and disposal of wastes. We contract with outside vendors to collect and dispose of waste at our production facilities in compliance with applicable environmental laws. In addition, we have procedures in place that we believe enable us to properly manage the regulated materials used in and wastes created by our manufacturing processes. We believe we are currently in material compliance with such laws and regulations. While we will continue to incur environmental compliance costs for our ongoing manufacturing operations, we do not expect these to be material to our consolidated financial statements.

In fiscal 2008, we acquired one manufacturing facility that had certain historical environmental conditions. We are working to remediate those conditions, and the remediation activities are being conducted without significant disruption to our operations.

Employees

The Company employed 5,511 and 4,614 persons on March 4, 2017 and February 27, 2016, respectively. At March 4, 2017, 624 of these employees were represented by U.S. labor unions.

International Sales

Information regarding export and international sales is included in Item 8, Financial Statements and Supplementary Data, within Note 16 of our Consolidated Financial Statements.

Available Information

The Company maintains a website at www.apog.com. Through a link to a third-party content provider, this corporate website provides free access to the Company's Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and, if applicable, amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the Exchange Act), as soon as reasonably practicable after electronic filing such material with, or furnishing it to, the Securities and Exchange Commission. Also available on our website are various corporate governance documents, including our Code of Business Ethics and Conduct, Corporate Governance Guidelines, and charters for the Audit, Compensation, and Nominating and Corporate Governance Committees of the Board of Directors.

EXECUTIVE OFFICERS OF THE REGISTRANT

Name | Age | Positions with Apogee Enterprises and Employment History | ||

Joseph F. Puishys | 58 | Chief Executive Officer and President of the Company since 2011. President of Honeywell's Environmental and Combustion Controls division from 2008 through 2011, President of Honeywell's Building Solutions from 2005 through 2008, and President of Honeywell Building Solutions, America from 2004 to 2005. | ||

James S. Porter | 56 | Chief Financial Officer since 2005 and Executive Vice President since 2015. Vice President of Strategy and Planning from 2002 through 2005. Various management positions within the Company since 1997. | ||

Patricia A. Beithon | 63 | General Counsel and Secretary since 1999. | ||

Gary R. Johnson | 55 | Vice President, Treasurer since 2001. Various management positions within the Company since 1995. | ||

John A. Klein | 60 | Senior Vice President, Operations and Supply Chain Management of the Company since 2012. Director of Operations at Cooper Industries' Power Systems Division from 2008 through 2012, and Vice President of Operations at Rexnord Industries' Bearing Division from 2005 through 2007. | ||

Executive officers are elected annually by the Board of Directors to serve for a one-year period. There are no family relationships between any of the executive officers or directors of the Company.

8

ITEM 1A. RISK FACTORS

Our business faces many risks. Any of the risks discussed below, or elsewhere in this Form 10-K or our other filings with the Securities and Exchange Commission, could have a material adverse impact on our business, financial condition or results of operations.

General global economic and business conditions

Our Architectural Glass, Architectural Framing Systems and Architectural Services segments are dependent on global economic conditions and the cyclical nature of the North American commercial construction industry. The commercial construction industry is impacted by global macroeconomic trends that, in turn, affect, among other things, availability of credit, employment levels, consumer confidence, interest rates and commodity prices. To the extent changes in these factors negatively impact the overall commercial construction industry, our revenue and profits could be significantly reduced.

Our Architectural Glass segment's operation located in Brazil is subject to the economic, political and tax conditions prevalent in the country. We cannot predict how changing economic conditions in Brazil will impact our financial results; however, our Brazilian operation makes up less than five percent of our net sales annually.

Our LSO segment depends on the strength of the retail custom picture framing industry. This industry is highly dependent on consumer confidence and the conditions of the U.S. economy. A decline in consumer confidence, whether as a result of an economic slowdown, uncertainty regarding the future or other factors, could result in a decrease in net sales and operating income of this segment.

Foreign currency exchange impacts

Our subsidiaries in Canada and Brazil report their results of operations and financial position in their relevant functional currencies (local country currency), which are then translated into U.S. dollars. This translated financial information is included in our consolidated financial statements. As the relationship between these currencies and the U.S. dollar changes, there could be a negative impact on our reported results and financial position.

In addition, as the U.S. dollar strengthens against foreign currencies, imports of products into the U.S. produced by international competitors have become more price competitive and exports of our U.S.-fabricated products have become less price competitive. If we are not able to counteract these price pressures through superior quality and service, our net sales and operating income could be negatively impacted.

New competitors or specific actions of our existing competitors

All of our operating segments operate in competitive industries where the actions of our existing competitors or new competitors could result in a loss of customers or share of customers' demand. Changes in our competitors' products, prices or services could negatively impact our share of demand, net sales or margins.

Our Architectural Glass and Architectural Framing Systems segments have seen an increase in imports of competitive products into the U.S. from international suppliers due to the relative strength of the U.S. dollar. If imports of competitive products were to occur at increased levels for extended periods of time, our net sales and margins could be negatively impacted.

Our LSO segment competes with several international specialty glass manufacturers that have traditionally been less focused on the U.S. custom picture framing industry. Certain of these competitors have recently developed some value-added products that are able to compete more directly with some products in our existing portfolio. If these competitors are able to successfully increase their product attributes and production capacity and/or increase their sales and marketing focus to the U.S. custom picture framing market, this segment's net sales and margins could be negatively impacted.

Acquisitions and related integration activities

We have completed and may complete additional acquisitions in the future to accelerate the execution of our growth strategies, including new geographies, markets and new product introductions. While we have a disciplined approach to assessing potential acquisition targets, conducting due diligence activities, and negotiating appropriate acquisition terms, there are risks inherent in completing acquisitions, including:

• | diversion of management’s attention from existing business activities; |

• | difficulties or delays in integrating and assimilating information and financial systems, operations, and products of an acquired business or other business venture or in realizing projected efficiencies, growth prospects, cost savings, and synergies; |

9

• | potential loss of key employees and customers of the acquired businesses or adverse effects on relationships with existing customers and suppliers; |

• | adverse impact on overall profitability if the acquired business does not achieve the return on investment projected at the time of acquisition; and |

• | inaccurate assessment of additional post-acquisition capital investments, undisclosed, contingent or other liabilities, problems executing backlog of material supply or installation projects underway at time of acquisition, unanticipated costs, and an inability to recover or manage such liabilities and costs. |

If one or more of these risks arises in a material manner, our operating results could be negatively impacted.

Effective utilization and management of our manufacturing capacity

Near-term performance depends, to a significant degree, on our ability to provide sufficient available capacity and appropriately utilize existing production capacity. The failure to successfully maintain existing capacity, successfully implement planned capacity expansions, and make additional investments in additional physical capacity could adversely affect our operating results.

Loss of key personnel and inability to source sufficient labor

Our success depends on the skills of the Company's leadership, construction project managers and other key technical personnel, and our ability to secure sufficient manufacturing labor. Increased activity in residential and commercial construction has caused increased competition for experienced construction project managers. Additionally, some of our manufacturing facilities are located in regions that at times may experience low levels of unemployment. If we are unable to retain existing employees and/or recruit and train additional employees with the requisite skills and experience, our operating results could be adversely impacted.

Commodity price fluctuations and supply availability

Our Architectural Framing Systems and Architectural Services segments use aluminum as a significant input to their products. While we structure many of our supply agreements in a way to moderate the effects of fluctuations in the market for raw aluminum, and we are usually eventually able to pass aluminum cost increases on to our customers, short-term operating results could be negatively impacted by sudden price movements in the market for raw aluminum.

Our Architectural Glass segment uses raw glass as a significant input to its products. The supply of raw glass has become tighter due to several years of growth in automotive manufacturing and residential and non-residential construction. Although we have secured supply commitments from multiple suppliers that allow us to reach our near-term growth targets, a significant unplanned downtime at one or more of our key suppliers could negatively impact our operating results.

Product quality issues

We manufacture and/or install a significant portion of our products based on the specific requirements of each customer. We believe that future orders of our products or services will depend on our ability to maintain the performance, reliability and quality standards required by our customers. If our products have performance, reliability or quality problems, or products are installed using incompatible glazing materials or installed improperly (by us or a customer), we may experience: additional warranty expense; reduced or canceled orders; higher manufacturing or installation costs; or delays in the collection of accounts receivable. Additionally, performance, reliability or quality claims from our customers, with or without merit, could result in costly and time-consuming litigation that could require significant time and attention of management and involve significant monetary damages that could negatively impact our financial results.

Project management and installation issues

The Architectural Services segment and, occasionally, a portion of the Architectural Framing Systems segment are awarded fixed-price contracts for installation services. Often, bids are required before all aspects of a construction project are known. An underestimate in the amount of labor required and/or cost of materials for a project; a change in the timing of the delivery of product; system design errors, difficulties or errors in execution; or significant project delays, caused by us or other trades, could result in failure to achieve the expected results. Any one or more of such issues could result in losses on individual contracts that could negatively impact our operating results.

Changes in architectural trends, building codes or consumer preferences

Any change in commercial construction customer preference, architectural trends or building codes that reduce window-to-wall ratios in non-residential construction would negatively impact net sales and operating income in our architectural-related segments. The LSO segment depends on U.S. consumers framing art and other decorative items. Any shift in customer preference away from framed art to other forms of wall decor could negatively impact future net sales and operating income in the LSO segment.

Customer dependence in the LSO segment

The LSO segment is highly dependent on a relatively small number of customers for its sales, and we expect this to continue in the future. Accordingly, loss of a significant customer, a significant reduction in pricing, or a shift to a less favorable mix of value-

10

added picture framing glass or acrylic products for one of those customers, could materially reduce LSO net sales and operating results.

Results can differ significantly from our expectations and the expectations of analysts

Our sales and earnings guidance and external analyst estimates are largely based on our view of our business and the broader commercial construction market. Even though we have significant market intelligence through our contact with real estate developers, building owners and architects, and continually monitor micro- and macro-economic indicators of future performance of the commercial construction market, we are unable to precisely predict events that can significantly change market cycles. Failure to meet our guidance or analyst expectations for net sales and earnings would likely have an adverse impact on the market price of our common stock.

Significant risk retention through self-insurance programs

We obtain third-party insurance for potential losses from general liability, employment practices, workers' compensation and automobile liability risk, as well as medical insurance. However, a high amount of risk is retained on a self-insured basis, partially through our wholly-owned insurance subsidiary. Therefore, a material architectural product liability event could have a material adverse effect on our operating results.

Dependence on information technology systems and potential security threats

Our operations are dependent upon various information technology systems that are used to process, transmit and store electronic information, and to manage or support our manufacturing operations and a variety of other business processes and activities. We could encounter difficulties in maintaining our existing systems, and developing and implementing new systems. Such difficulties could lead to disruption in business operations and/or significant additional expenses that could adversely affect our results.

Additionally, information technology security threats are increasing in frequency and sophistication. These threats pose a risk to the security of our systems and networks, and the confidentiality, availability and integrity of our data. Should such an attack succeed, it could lead to the compromise of confidential information, manipulation and destruction of data and product specifications, production downtimes, disruption in the availability of financial data, or misrepresentation of information via digital media. The occurrence of any of these events could adversely affect our reputation and could result in litigation, regulatory action, project delay claims, and increased costs and operational consequences of implementing further data protection systems.

Use of hazardous chemicals and environmental compliance

We use hazardous chemicals in the production process of some of our products. One of our facilities has certain historical environmental conditions that are in the process of being remediated. Our inability to remediate the historical environmental conditions at the facility at or below the amounts reserved could have an adverse impact on future financial results. Additionally, we are subject to a variety of local, state and federal governmental regulations relating to storage, discharge, handling, emission, generation and disposal of toxic or other hazardous substances used to manufacture our products, compliance with which is expensive. Our failure to comply with current or future environmental regulations could result in the imposition of substantial fines, suspension of production, alteration of our manufacturing processes or increased costs.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

The following table lists, by segment, the Company's major properties as of March 4, 2017.

11

Property Location | Owned/ Leased | Function | ||

Architectural Glass segment | ||||

Owatonna, MN | Owned | Manufacturing/Administrative | ||

Owatonna, MN | Leased | Warehouse | ||

Statesboro, GA | Owned | Manufacturing/Warehouse | ||

St. George, UT | Owned | Manufacturing/Warehouse | ||

Nazaré Paulista, Brazil | Owned(1) | Manufacturing/Administrative | ||

Architectural Framing Systems segment | ||||

Wausau, WI | Owned | Manufacturing/Administrative | ||

Stratford, WI | Owned | Manufacturing | ||

Reed City, MI | Owned | Manufacturing | ||

Walker, MI | Leased | Manufacturing/Administrative | ||

Dallas, TX | Leased | Manufacturing | ||

Toronto, ON Canada | Leased | Manufacturing/Warehouse/Administrative | ||

Toronto, ON Canada | Owned | Manufacturing | ||

Brampton, ON Canada | Leased | Manufacturing/Warehouse/Administrative | ||

Architectural Services segment | ||||

Minneapolis, MN | Leased | Administrative | ||

West Chester, OH | Leased | Manufacturing | ||

Garland, TX | Leased | Manufacturing | ||

Glen Burnie, MD | Leased | Manufacturing | ||

Orlando, FL | Leased | Manufacturing | ||

LSO segment | ||||

McCook, IL | Owned | Manufacturing/Warehouse/Administrative | ||

Faribault, MN | Owned | Manufacturing/Administrative | ||

Other | ||||

Minneapolis, MN | Leased | Administrative | ||

(1) | This is an owned facility; however, the land is leased from the city. |

ITEM 3. LEGAL PROCEEDINGS

The Company has been a party to various legal proceedings incidental to its normal operating activities. In particular, like others in the construction supply and services industry, the Company's construction supply and services businesses are routinely involved in various disputes and claims arising out of construction projects, sometimes involving significant monetary damages or product replacement. The Company has also been subject to litigation arising out of general liability, employment practices, workers' compensation and automobile claims. Although it is very difficult to accurately predict the outcome of such proceedings, facts currently available indicate that no such claims will result in losses that would have a material adverse effect on the results of operations, cash flows or financial condition of the Company.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Apogee common stock is traded on the NASDAQ Stock Market LLC (Nasdaq) under the ticker symbol APOG.

As of April 8, 2017, there were 1,197 shareholders of record and 16,162 shareholders for whom securities firms acted as nominees.

12

The following chart shows the quarterly range and year-end closing price for one share of the Company's common stock over the past three fiscal years.

First | Second | Third | Fourth | Year-end | ||||||||||||||||||||||||||||

Low | High | Low | High | Low | High | Low | High | Close | ||||||||||||||||||||||||

2017 | $ | 39.93 | $ | 45.94 | $ | 41.50 | $ | 48.88 | $ | 39.96 | $ | 49.17 | $ | 47.64 | $ | 59.38 | $ | 58.19 | ||||||||||||||

2016 | 42.35 | 56.27 | 49.60 | 60.16 | 43.90 | 57.86 | 34.52 | 50.53 | 39.41 | |||||||||||||||||||||||

2015 | 28.28 | 35.64 | 29.21 | 36.68 | 35.07 | 47.02 | 37.83 | 48.03 | 45.85 | |||||||||||||||||||||||

Dividends

Quarterly, the Board of Directors evaluates declaring dividends based on operating results, available funds and the Company's financial condition. Cash dividends have been paid each quarter since 1974. The chart below shows quarterly and annual cumulative cash dividends per share for the past three fiscal years.

First | Second | Third | Fourth | Total | ||||||||||||||||

2017 | $ | 0.1250 | $ | 0.1250 | $ | 0.1250 | $ | 0.1400 | $ | 0.5150 | ||||||||||

2016 | 0.1100 | 0.1100 | 0.1100 | 0.1250 | 0.4550 | |||||||||||||||

2015 | 0.1000 | 0.1000 | 0.1000 | 0.1100 | 0.4100 | |||||||||||||||

Purchases of Equity Securities by the Company

The following table provides information with respect to purchases made by the Company of its own stock during the fourth quarter of fiscal 2017:

Period | Total Number of Shares Purchased (a) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs (b) | Maximum Number of Shares that May Yet Be Purchased under the Plans or Programs (b) | ||||||||

November 27, 2016 through December 31, 2016 | 180 | $ | 50.04 | — | 942,367 | |||||||

January 1, 2017 through January 28, 2017 | 3,185 | 55.55 | — | 942,367 | ||||||||

January 29, 2017 through March 4, 2017 | 1,625 | 57.98 | — | 942,367 | ||||||||

Total | 4,990 | $ | 56.15 | — | 942,367 | |||||||

(a) The shares in this column represent shares that were surrendered to us by plan participants in order to satisfy stock-for-stock option exercises or withholding tax obligations related to stock-based compensation.

(b) In fiscal 2004, the Board of Directors authorized the repurchase of 1,500,000 shares of Company stock, which was announced on April 10, 2003. Subsequently, the Board of Directors increased the authorization by 750,000 shares, which was announced on January 24, 2008; by 1,000,000 shares, which was announced on October 8, 2008; and by 1,000,000 shares, which was announced on January 13, 2016. The Company's repurchase program does not have an expiration date. No shares were repurchased in the fourth quarter of fiscal 2017.

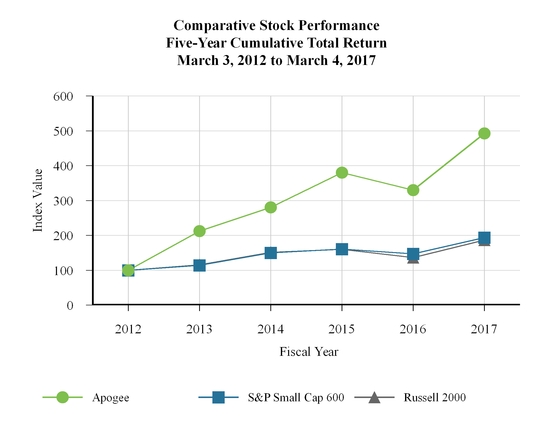

Comparative Stock Performance

The line graph below compares the cumulative total shareholder return on a $100 investment in our common stock for the last five fiscal years with the cumulative total return on a $100 investment in the Standard & Poor's Small Cap 600 Growth Index and the Russell 2000 Index. The graph assumes an investment at the close of trading on March 3, 2012, and also assumes the reinvestment of all dividends.

13

2012 | 2013 | 2014 | 2015 | 2016 | 2017 | ||||||||||||||||||

Apogee | $ | 100.00 | $ | 212.10 | $ | 280.52 | $ | 379.99 | $ | 329.79 | $ | 492.41 | |||||||||||

S&P Small Cap 600 Growth Index | 100.00 | 114.19 | 149.83 | 160.72 | 147.48 | 193.42 | |||||||||||||||||

Russell 2000 Index | 100.00 | 115.68 | 151.59 | 160.12 | 136.57 | 186.43 | |||||||||||||||||

We are not aware of any competitors, public or private, that are similar to us in size and scope of business activities. Most of our direct competitors are either privately owned or divisions of larger, publicly owned companies.

ITEM 6. SELECTED FINANCIAL DATA

The following information should be read in conjunction with Management's Discussion and Analysis of Financial Condition and Results of Operations, included in Item 7 of this Report, and our consolidated financial statements and related notes, included in Item 8 of this Report.

14

Fiscal Year | |||||||||||||||||||

(In thousands, except per share data and percentages) | 2017(1, 2) | 2016 | 2015 | 2014(3) | 2013 | ||||||||||||||

Results of Operations Data | |||||||||||||||||||

Net sales | $ | 1,114,533 | $ | 981,189 | $ | 933,936 | $ | 771,445 | $ | 700,224 | |||||||||

Gross profit | 292,023 | 243,570 | 208,544 | 165,252 | 145,733 | ||||||||||||||

Operating income | 122,225 | 97,393 | 63,585 | 40,285 | 27,419 | ||||||||||||||

Net earnings | 85,790 | 65,342 | 50,516 | 27,986 | 19,111 | ||||||||||||||

Earnings per share - basic | 2.98 | 2.25 | 1.76 | 0.98 | 0.68 | ||||||||||||||

Earnings per share - diluted | 2.97 | 2.22 | 1.72 | 0.95 | 0.67 | ||||||||||||||

Cash dividends per share | 0.515 | 0.455 | 0.410 | 0.370 | 0.360 | ||||||||||||||

Balance Sheet Data | |||||||||||||||||||

Total assets | 784,658 | 657,440 | 612,057 | 569,995 | 524,779 | ||||||||||||||

Long-term debt | 65,400 | 20,400 | 20,587 | 20,659 | 20,756 | ||||||||||||||

Shareholders' equity | 470,577 | 406,195 | 382,476 | 356,104 | 336,792 | ||||||||||||||

Other Data | |||||||||||||||||||

Gross profit as a percentage of sales | 26.2 | % | 24.8 | % | 22.3 | % | 21.4 | % | 20.8 | % | |||||||||

Operating income as a percentage of sales | 11.0 | % | 9.9 | % | 6.8 | % | 5.2 | % | 3.9 | % | |||||||||

Return on average invested capital(4) | 14.3 | % | 12.7 | % | 8.8 | % | 6.0 | % | 4.3 | % | |||||||||

(1) | Fiscal 2017 included 53 weeks. Each of the other periods presented included 52 weeks. |

(2) | Includes the acquisition of Sotawall in December 2016. |

(3) | Includes the acquisition of Alumicor in November 2013. |

(4) | Return on average invested capital is a non-GAAP measure that we define as [operating income x .65]/average invested capital. We believe this measure is useful in understanding operational performance over time. This non-GAAP measure should be viewed in addition to, and not as an alternative to, the reported financial results of the company prepared in accordance with GAAP. Other companies may calculate this measure differently from us, limiting the usefulness of the measure for comparison with others. |

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Forward-Looking Statements

This discussion contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements reflect our current views with respect to future events and financial performance. The words “believe,” “expect,” “anticipate,” “intend,” “estimate,” “forecast,” “project,” “should” and similar expressions are intended to identify “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. All forecasts and projections in this document are “forward-looking statements,” and are based on management's current expectations or beliefs of the Company's near-term results, based on current information available pertaining to the Company, including the risk factors noted under Item 1A in this Form 10-K. From time to time, we also may provide oral and written forward-looking statements in other materials we release to the public, such as press releases, presentations to securities analysts or investors, or other communications by the Company. Any or all of our forward-looking statements in this report and in any public statements we make could be materially different from actual results.

Accordingly, we wish to caution investors that any forward-looking statements made by or on behalf of the Company are subject to uncertainties and other factors that could cause actual results to differ materially from such statements. These uncertainties and other risk factors include, but are not limited to, the risks and uncertainties set forth under Item 1A in this Form 10-K.

We wish to caution investors that other factors might in the future prove to be important in affecting the Company's results of operations. New factors emerge from time to time; it is not possible for management to predict all such factors, nor can it assess the impact of each such factor on the business or the extent to which any factor, or a combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We undertake no obligation to update publicly or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Overview

We are a world leader in certain technologies involving the design and development of value-added glass products and services. Our four reporting segments are: Architectural Glass, Architectural Framing Systems, Architectural Services and Large-Scale Optical Technologies (LSO).

Highlights for fiscal 2017:

• | Consolidated net sales increased to $1.1 billion, or 14 percent over fiscal 2016. |

• | Operating income increased to $122 million, or 25 percent over the prior year. |

15

• | Diluted EPS was $2.97, compared to $2.22 in the prior year, for growth of 34 percent. |

• | We acquired the assets of Sotawall, Inc., a Canadian privately-held designer and fabricator of high-performance, unitized curtainwall systems for commercial construction projects, for approximately $138 million on December 14, 2016. Sotawall's results since the date of acquisition have been included in the consolidated financial statements and within the Architectural Framing Systems segment. |

Results of Operations

Net Sales

(Dollars in thousands) | 2017 | 2016 | 2015 | 2017 vs. 2016 | 2016 vs. 2015 | ||||||||||||

Net sales | $ | 1,114,533 | $ | 981,189 | $ | 933,936 | 13.6 | % | 5.1 | % | |||||||

Fiscal 2017 Compared to Fiscal 2016

Net sales in fiscal 2017 increased by 13.6 percent compared to fiscal 2016, due to gains in volume across all three architectural segments. Volume growth was driven by continued strength in non-residential construction end-markets and success in our strategies to expand geographically and introduce new products. The Architectural Framing Systems segment drove nearly 60 percent of our growth this year. The acquisition of Sotawall in the fourth quarter, included in this segment, contributed 13 percent of our overall growth. The Architectural Glass segment drove approximately 22 percent of our growth and the Architectural Services segment contributed nearly all of the remainder. Currency did not have a meaningful impact on our consolidated sales as compared to the prior year.

Fiscal 2016 Compared to Fiscal 2015

Net sales increased by 5.1 percent, or 7.0 percent on a constant currency basis, over fiscal 2015. This was mainly due to pricing and volume growth resulting from strong commercial construction activity in the U.S, partially offset by declines in the commercial construction markets in Brazil and Canada. The Architectural Glass segment accounted for approximately 44 percent of the growth, and the Architectural Services segment drove approximately 32 percent of the growth, with nearly all of the remainder coming from the domestic Architectural Framing segment businesses.

Constant currency revenue excludes the impact of fluctuations in foreign currency on our international operations. Constant currency percentages are calculated by converting prior-period local currency results using the average monthly exchange rate and comparing the adjusted amount to current period reported results. We believe constant currency information provides valuable supplemental information regarding our core operating results, consistent with how we evaluate our performance. We also refer to constant currency measures elsewhere in this report. This non-GAAP measure should be viewed in addition to, and not as an alternative to, the reported results prepared in accordance with U.S. GAAP.

Performance

The relationship between various components of operations, as a percentage of net sales, is provided below.

(Percentage of net sales) | 2017 | 2016 | 2015 | |||||

Net sales | 100.0 | % | 100.0 | % | 100.0 | % | ||

Cost of sales | 73.8 | 75.2 | 77.7 | |||||

Gross profit | 26.2 | 24.8 | 22.3 | |||||

Selling, general and administrative expenses | 15.2 | 14.9 | 15.5 | |||||

Operating income | 11.0 | 9.9 | 6.8 | |||||

Other income, net | — | — | 0.2 | |||||

Earnings before income taxes | 11.0 | 9.9 | 7.0 | |||||

Income tax expense | 3.3 | 3.3 | 1.6 | |||||

Net earnings | 7.7 | % | 6.7 | % | 5.4 | % | ||

Effective income tax rate | 30.1 | % | 32.9 | % | 22.3 | % | ||

Fiscal 2017 Compared to Fiscal 2016

Gross profit was 26.2 percent in fiscal 2017, an improvement of 140 basis points from fiscal 2016, driven by operating leverage on increased volume and improved productivity in our three architectural segments.

Selling, general and administrative (SG&A) expense for fiscal 2017 was 15.2 percent, an increase of 30 basis points, or $23.6 million, from fiscal 2016, mainly as a result of increased incentive-related compensation and intangible asset amortization expenses.

16

The effective tax rate for fiscal 2017 was 30.1 percent, compared to 32.9 percent in fiscal 2016. The decline of 280 basis points was a result of benefits from various tax planning strategies, including recognition of a foreign tax credit contributing 160 basis points, and increased income in foreign jurisdictions with lower tax rates.

Fiscal 2016 Compared to Fiscal 2015

Gross profit improved 250 basis points from fiscal 2015 to fiscal 2016, primarily due to improved pricing and mix, as well as productivity and volume leverage across all architectural segments.

SG&A expense declined by 60 basis points from 2015 to 2016, but increased $1.2 million, as a result of expense discipline relative to sales growth across our segments.

Our effective tax rate for fiscal 2015 was 22.3 percent, including a $6.4 million tax benefit from an energy-efficient investment credit. Excluding this credit, our effective tax rate would have been 32.2%, compared to 32.9% in fiscal 2016. This increase of 70 basis points was due to changes in state income tax laws, combined with a higher percentage of earnings in the U.S., where the tax rate is higher than in the foreign jurisdictions in which we operate.

Segment Analysis

Architectural Glass

(In thousands) | 2017 | 2016 | 2015 | ||||||||

Net sales | $ | 411,881 | $ | 377,713 | $ | 346,471 | |||||

Operating income | 44,656 | 35,504 | 16,431 | ||||||||

Operating margin | 10.8 | % | 9.4 | % | 4.7 | % | |||||

Fiscal 2017 Compared to Fiscal 2016. Fiscal 2017 net sales increased $34.2 million, or 9.0 percent, over the prior year. This was primarily due to volume growth and improved pricing and mix in our U.S.-based business, as a result of our focus on growth in the mid-size building sector, as well as the effects of a positive U.S. construction market. Currency did not have a meaningful impact on segment sales as compared to the prior year.

Operating margin improved 140 basis points, driven by leverage on volume growth, pricing, mix and productivity.

Fiscal 2016 Compared to Fiscal 2015. Fiscal 2016 net sales improved 9.0 percent over the prior year, or 12.2 percent on a constant currency basis, primarily due to improved pricing, mix and volume growth in the U.S. as a result of the strong U.S. construction market, partially offset by declines in volume and mix in our Brazilian operation and lower export sales from the U.S.

Operating margin improved 470 basis points, doubling the fiscal 2015 operating margin, with improvement driven by pricing and mix, as well as strong operational performance and volume leverage in the U.S., partially offset by the impact of ongoing challenging Brazilian economic conditions.

Architectural Framing Systems

(In thousands) | 2017 | 2016 | 2015 | ||||||||

Net sales | $ | 385,978 | $ | 308,593 | $ | 298,395 | |||||

Operating income | 44,768 | 31,911 | 21,808 | ||||||||

Operating margin | 11.6 | % | 10.3 | % | 7.3 | % | |||||

Fiscal 2017 Compared to Fiscal 2016. Net sales improved 25.1 percent, or $77.4 million, over fiscal 2016 due to volume growth across our businesses. Our volume growth resulted from strong U.S. construction market conditions, increased penetration into certain geographies and new product introductions. In addition, Sotawall, acquired in the fourth quarter of fiscal 2017, contributed net sales of $17.8 million in fiscal 2017, or approximately six percentage points of growth. Currency did not have a meaningful impact on segment sales as compared to the prior year.

Operating margin improved 130 basis points over fiscal 2016, driven by leverage on volume growth and productivity.

Fiscal 2016 Compared to Fiscal 2015. Net sales improved 3.4 percent over fiscal 2015, or 6.0 percent on a constant currency basis, on volume growth from strong U.S. construction markets, and improved pricing and mix in our U.S. businesses, partially offset by volume weakness in our Canadian business.

17

Operating margin improved 300 basis points over fiscal 2015, driven by improved pricing and mix, lower raw material costs and volume leverage in the U.S., partially offset by the volume weakness in our Canadian business.

Architectural Services

(In thousands) | 2017 | 2016 | 2015 | ||||||||

Net sales | $ | 270,937 | $ | 245,935 | $ | 230,650 | |||||

Operating income | 18,494 | 11,687 | 7,442 | ||||||||

Operating margin | 6.8 | % | 4.8 | % | 3.2 | % | |||||

Fiscal 2017 Compared to Fiscal 2016. Net sales improved 10.2 percent, or $25.0 million, over the prior year, driven by volume growth due to year-on-year timing of project activity, as we have continued to experience strong commercial construction activity in the U.S. Operating margin improved 200 basis points over the prior year, as a result of leveraging volume growth and continued good execution on projects with better margins.

Fiscal 2016 Compared to Fiscal 2015. Net sales improved 6.6 percent over the prior year, driven by volume growth due to increased commercial construction activity in the U.S. Operating margin improved 160 basis points over the prior year, as a result of continued focus on project selection, improved project margins and good execution.

Large-Scale Optical Technologies (LSO)

(In thousands) | 2017 | 2016 | 2015 | ||||||||

Net sales | $ | 89,710 | $ | 88,541 | $ | 87,693 | |||||

Operating income | 22,467 | 22,963 | 21,954 | ||||||||

Operating margin | 25.0 | % | 25.9 | % | 25.0 | % | |||||

Fiscal 2017 Compared to Fiscal 2016. Net sales in our LSO segment increased 1.3 percent over the prior year. Operating margin declined 90 basis points over the prior year as a result of increased investments in new market opportunities.

Fiscal 2016 Compared to Fiscal 2015. Net sales in this segment increased 1.0 percent over the prior year as a result of an improved mix of value-added products and stable demand. Operating margin improved 90 basis points over the prior year as a result of improved product mix and strong operational performance.

Liquidity and Capital Resources

(In thousands) | 2017 | 2016 | 2015 | ||||||||

Operating Activities | |||||||||||

Net cash provided by operating activities | $ | 124,001 | $ | 128,943 | $ | 71,799 | |||||

Investing Activities | |||||||||||

Capital expenditures | (68,061 | ) | (42,037 | ) | (27,220 | ) | |||||

Net sales (purchases) of marketable securities | 32,728 | (31,767 | ) | 804 | |||||||

Acquisition of business and intangibles | (137,932 | ) | — | — | |||||||

Financing Activities | |||||||||||

Borrowings on line of credit, net | 44,988 | — | — | ||||||||

Repurchase and retirement of common stock | (10,817 | ) | (24,911 | ) | (6,894 | ) | |||||

Dividends paid | (14,667 | ) | (13,184 | ) | (12,071 | ) | |||||

Operating Activities. Cash provided by operating activities was $124.0 million in fiscal 2017, a decrease of $5.0 million from fiscal 2016. In all years presented, operating cash flows benefited by increased income as compared to the respective prior-year period. In addition, in fiscal 2017, cash from operations was negatively impacted by timing of working capital payments.

Investing Activities. Net cash used in investing activities was $183.8 million in the current year, mainly due to the acquisition of substantially all the assets of Sotawall, Inc. for approximately $138 million. We also made capital expenditures focused primarily on increasing our product capabilities, in particular related to the oversized glass fabrication project. Additional capital investments

18

were made to increase our manufacturing productivity across all reporting segments. In fiscal 2016 and 2015, capital investments were primarily focused on increasing manufacturing productivity and capacity.

We estimate fiscal 2018 capital expenditures to be $50 to $60 million, as we continue to invest in capabilities and productivity.

We continue to review our portfolio of businesses and their assets in comparison to our internal strategic and performance objectives. As part of this review, we may acquire other businesses, pursue geographic expansion, take actions to manage capacity and further invest in, fully divest and/or sell parts of our current businesses.

Financing Activities. We paid dividends totaling $14.7 million in fiscal 2017. Additionally, we repurchased 250,001 shares under our authorized share repurchase program during fiscal 2017, for a total cost of $10.8 million. We repurchased 575,000 shares under the program in fiscal 2016 and 203,509 shares under the program during fiscal 2015. We have repurchased a total of 3,307,633 shares, at a total cost of $72.3 million, since the inception of this program during fiscal 2004. We have remaining authority to repurchase 942,367 shares under this program, which has no expiration date.

We maintain a $175.0 million committed revolving credit facility that expires in November 2021 as further described in Note 8 of the Notes to Consolidated Financial Statements. $45.0 million was outstanding under this credit facility as of March 4, 2017, as we used this facility to partially finance the Sotawall acquisition. Nothing was outstanding under this credit facility at the end of either of the two prior years. As defined within this credit facility, we have two financial covenants which require us to stay below a maximum leverage ratio and to maintain a minimum interest expense-to-EBITDA ratio. At March 4, 2017, we were in compliance with both financial covenants.

Other Financing Activities. The following summarizes our significant contractual obligations that impact our liquidity as of March 4, 2017:

Payments Due by Fiscal Period | |||||||||||||||||||||||||||

(In thousands) | 2018 | 2019 | 2020 | 2021 | 2022 | Thereafter | Total | ||||||||||||||||||||

Long-term debt obligations | $ | — | $ | — | $ | — | $ | 5,400 | $ | 47,000 | $ | 13,000 | $ | 65,400 | |||||||||||||

Operating leases (undiscounted) | 11,419 | 10,796 | 9,286 | 6,342 | 5,605 | 9,002 | 52,450 | ||||||||||||||||||||

Purchase obligations | 106,839 | 4,693 | 1,800 | 1,230 | 1,230 | — | 115,792 | ||||||||||||||||||||

Total cash obligations | $ | 118,258 | $ | 15,489 | $ | 11,086 | $ | 12,972 | $ | 53,835 | $ | 22,002 | $ | 233,642 | |||||||||||||

In addition to the committed revolving credit facility discussed above, we also have industrial revenue bond obligations of $20.4 million that mature in fiscal years 2021 through 2043.

From time to time, we acquire the use of certain assets through operating leases, such as warehouses, vehicles, forklifts, office equipment, hardware, software and some manufacturing equipment. Many of these operating leases have termination penalties. However, because the assets are used in the conduct of our business operations, it is unlikely that any significant portion of these operating leases would be terminated prior to the normal expiration of their lease terms. Therefore, we consider the risk related to termination penalties to be minimal.

Purchase obligations in the table above relate to raw material commitments and capital expenditures.

We expect to make contributions of approximately $1.0 million to our defined-benefit pension plans in fiscal 2018, which will equal or exceed our minimum funding requirements.

As of March 4, 2017, we had reserves of $4.0 million and $1.4 million for long-term unrecognized tax benefits and environmental liabilities, respectively. We expect approximately $0.4 million of the unrecognized tax benefits to lapse during the next 12 months. We are unable to reasonably estimate in which future periods the remaining unrecognized tax benefits and environmental liabilities will ultimately be settled.

At March 4, 2017, we had ongoing letters of credit of $23.5 million related to industrial revenue bonds and construction contracts that expire in fiscal 2018 and that reduce availability of funds under our committed credit facility.

In addition to the above standby letters of credit, we are required, in the ordinary course of business, to provide surety or performance bonds that commit payments to our customers for any non-performance by us. At March 4, 2017, $96.2 million of our backlog was bonded by performance bonds with a face value of $343.7 million. Performance bonds do not have stated expiration dates,

19

as we are released from the bonds upon completion of the contracts. We have never been required to make any payments related to these performance bonds with respect to any of our current portfolio of businesses.

We had total cash and short-term marketable securities of $20.0 million, and $106.5 million available under our committed revolving credit facility, at March 4, 2017. Due to our ability to generate strong cash from operations and borrowing capability under our committed revolving credit facility, we believe that our sources of liquidity will continue to be adequate to fund our working capital requirements, planned capital expenditures and dividend payments for at least the next 12 months.

Off-balance Sheet Arrangements. With the exception of operating leases, we had no off-balance sheet financing arrangements at March 4, 2017 or February 27, 2016.

Outlook

The following statements are based on our current expectations for fiscal 2018 results. These statements are forward-looking, and actual results may differ materially.

• | Revenue growth of approximately 10 percent over fiscal 2017. |

• | Gross margin of approximately 28 percent and operating margin of approximately 12.5 percent. |

• | Earnings per diluted share of $3.35 to $3.55. |

• | Capital expenditures of approximately $50 to $60 million. |

Recently Issued Accounting Pronouncements

See Note 1 of the Notes to Consolidated Financial Statements within Item 8 of this Form 10-K for information pertaining to recently issued accounting pronouncements, incorporated herein by reference.

Critical Accounting Policies

Our analysis of operations and financial condition is based on our consolidated financial statements prepared in accordance with U.S. GAAP. Preparation of these consolidated financial statements requires us to make estimates and assumptions affecting the reported amounts of assets and liabilities at the date of the consolidated financial statements, reported amounts of revenues and expenses during the reporting period and related disclosures of contingent assets and liabilities. In developing these estimates and assumptions, a collaborative effort is undertaken involving management across the organization including finance, sales, project management, quality, risk, legal and tax, as well as outside advisors such as consultants, engineers, lawyers and actuaries. Our estimates are evaluated on an ongoing basis and are drawn from historical experience and other assumptions that we believe to be reasonable under the circumstances. Actual results could differ under other assumptions or circumstances.

The following items in our consolidated financial statements require significant estimation or judgment:

Revenue recognition. We recognize revenue when title has transferred, except within our Architectural Services segment and for one business within our Architectural Framing Systems segment, which enter into fixed-price contracts for projects typically performed over a 12- to 24-month timeframe. The contracts clearly specify the enforceable rights of the parties, the consideration and the terms of settlement, and both parties can be expected to satisfy all obligations under the contract. We record revenue for these contracts on a percentage-of-completion basis as we are able to reasonably estimate total contract revenue and total contract costs. We compare the total costs incurred to date to the total estimated costs for the contract, and record that proportion of the total contract revenue in the period. Contract costs include materials, labor and other direct costs related to contract performance. We believe utilizing the cost-to-cost method for revenue recognition provides the greatest degree of accuracy in measuring revenue throughout the contract period. Provisions are established for estimated losses, if any, on uncompleted contracts in the period in which such losses are determined. Amounts representing contract change orders, claims or other items are included in contract revenue only upon customer approval. Recognizing revenue under the percentage-of-completion method of accounting requires significant estimates, including total costs and the percentage complete on the contract, as well as any potential losses or contract overruns. During fiscal 2017, approximately 26 percent of our consolidated sales were recorded on a percentage-of-completion basis.

Goodwill impairment. We evaluate goodwill for impairment annually at our year-end, or more frequently if impairment indicators exist. This year we elected to first perform a qualitative assessment to determine whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount (commonly referred to as “step 0”). If, after assessing all events and circumstances, it is determined that it is not more likely than not that the fair value of a reporting unit is less than its carrying amount, then the two-step goodwill impairment assessment is unnecessary. If we proceed in the goodwill analysis, step 1 of the process compares the fair value of each of our reporting units to carrying value, including goodwill. If the fair value exceeds the carrying value, goodwill impairment is not indicated. Each of our business units represents a reporting unit for the goodwill

20

impairment analysis. Based on our assessment process, we determined that it was not more likely than not that the fair value of any of our reporting units was less than its carrying amount.

When we perform step 1 of the goodwill impairment assessment, we base our determination of fair value on a discounted cash flow methodology that involves significant judgment about projections of future performance. Assumptions about future revenues and expenses, capital expenditures and changes in working capital are based on the annual operating plan and long-term business plan for each business unit. These plans take into consideration numerous factors, including historical experience, anticipated future economic conditions and growth expectations for the industries and end markets in which we participate. Growth rates for revenues and operating profits vary for each reporting unit. The discount rate assumption for each reporting unit takes into consideration our assessment of risks inherent in the future cash flows of our business and an estimated weighted-average cost of capital.