Attached files

| file | filename |

|---|---|

| EX-21.1 - SUBSIDIARIES OF QUMU CORPORATION - Qumu Corp | qumuexhibit21112312016.htm |

| EX-32 - CERTIFICATION OF CEO / CFO PURSUANT TO SECTION 906 - Qumu Corp | qumuexhibit3212312016.htm |

| EX-31.2 - CERTIFICATION OF CFO PURSUANT TO SECTION 302 - Qumu Corp | qumuexhibit31212312016.htm |

| EX-31.1 - CERTIFICATION OF CEO PURSUANT TO SECTION 302 - Qumu Corp | qumuexhibit31112312016.htm |

| EX-23.1 - CONSENT OF KPMG LLP - Qumu Corp | qumuexhibit23112312016.htm |

| EX-10.13 - AMENDMENT TO TERM LOAN CREDIT AGREEMENT - Qumu Corp | qumuexhibit101312312016.htm |

FORM 10-K

U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED December 31, 2016

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE

SECURITIES EXCHANGE ACT OF 1934

COMMISSION FILE NO. 000-20728

QUMU CORPORATION

(Exact name of registrant as specified in its charter)

Minnesota | 41-1577970 | |

State or other jurisdiction of incorporation or organization | (I.R.S. Employer Identification No.) | |

510 1st Avenue North, Suite 305, Minneapolis, MN 55403 | ||

(Address of principal executive offices) | ||

(612) 638 - 9100 | ||

(Registrant's telephone number, including area code) | ||

Securities registered pursuant to Section 12(b) of the Act: | Common Stock, $.01 par value | |

Preferred Stock Purchase Rights | ||

Securities registered pursuant to Section 12(g) of the Act: | None | |

Indicate by checkmark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by checkmark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by checkmark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by checkmark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company.

Large Accelerated Filer o Accelerated Filer o Non-Accelerated Filer o Smaller Reporting Company x

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes o No x

The aggregate market value of common stock held by non-affiliates of the registrant, computed by reference to the last quoted price at which such stock was sold on such date as reported by the Nasdaq Stock Market as of the last business day of the registrant’s most recently completed second fiscal quarter was approximately $37,187,000.

As of March 24, 2017, the registrant had 9,221,614 outstanding shares of common stock.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its 2017 Annual Meeting of Shareholders, to be filed within 120 days after the end of the fiscal year covered by this report, are incorporated by reference into Part III hereof.

1

TABLE OF CONTENTS

Page | ||

2

General Information

PART I

Cautionary Note Regarding Forward-Looking Statements

We make statements from time to time regarding our business and prospects, such as projections of future performance, statements of management's plans and objectives, forecasts of market trends, and other matters that are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Statements containing the words or phrases “will likely result,” “are expected to,” “will continue,” “is anticipated,” “estimates,” “projects,” “believes,” “expects,” “anticipates,” “intends,” “target,” “goal,” “plans,” “objective,” “should” or similar expressions identify forward-looking statements. Forward-looking statements may appear in documents, reports, filings with the Securities and Exchange Commission (SEC), news releases, written or oral presentations made by our authorized officers or other representatives. For such statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

Our future results, including results expressed in or implied by forward-looking statements, involve a number of risks and uncertainties. Forward-looking statements are not guarantees of future actions, outcomes, results or performance. Any forward-looking statement made by us or on our behalf speaks only as of the date on which such statement is made. We do not undertake any obligation to update or keep current any forward-looking statement to reflect events or circumstances arising after the date of such statement.

In addition to the factors identified or described by us from time to time in filings with the SEC, there are many important factors that could cause our future results to differ materially from historical results or trends, results anticipated or planned by us, or the results expressed in or implied by any forward-looking statements. These important factors are described below under Item 1A. Risk Factors.

ITEM 1. BUSINESS

Overview

Qumu Corporation ("Qumu" or the "Company") provides the software applications businesses use to create, manage, secure, deliver and measure the success of their videos. The Company's innovative solutions release the power in video to engage and empower employees, partners and clients, allowing organizations around the world to realize the greatest possible value from video they create and publish. Whatever the audience size, viewer device or network configuration, the Company's solutions are how business does video. Qumu markets its products to customers primarily in North America, Europe and Asia.

Qumu generates revenue through the sale of enterprise video content management software solutions, hardware, maintenance and support, and professional and other services. Software sales may take the form of a perpetual software license, a term software license or a cloud-hosted software as a service (SaaS). Software licenses and appliances revenue includes sales of perpetual software licenses and hardware. Service revenue includes term software licenses, SaaS, maintenance and support, and professional and other services. An individual sale can range from single year agreements for thousands of dollars to multi-year agreements for over a million dollars.

Year Ended December 31, | Increase (Decrease) | Percent Increase (Decrease) | |||||||||||||||||||||||

2016 | 2015 | 2014 | 2015 to 2016 | 2014 to 2015 | 2015 to 2016 | 2014 to 2015 | |||||||||||||||||||

Software licenses and appliances | $ | 5,839 | $ | 9,456 | $ | 11,363 | $ | (3,617 | ) | $ | (1,907 | ) | (38 | )% | (17 | )% | |||||||||

Service | 25,843 | 24,998 | 15,158 | 845 | 9,840 | 3 | % | 65 | % | ||||||||||||||||

Total revenues | $ | 31,682 | $ | 34,454 | $ | 26,521 | $ | (2,772 | ) | $ | 7,933 | (8 | )% | 30 | % | ||||||||||

History

The Company was founded in 1978, incorporated as IXI, Inc. in Minnesota in February 1987 and changed its name to Rimage Corporation in April 1988. From 1995 to 2011, the Company focused its business on the development and sale of its CD recordable publishing systems and DVD recordable publishing systems.

In response to declines in the disc publishing business due to technology substitutions and the rise of video as a communication and collaboration platform, in October 2011, the Company acquired Qumu, Inc., a leader in the enterprise video content management software market, and changed its name to Qumu Corporation in September 2013. Qumu completed the transition to an enterprise video content management software company in July 2014, when the Company closed on the sale of its disc publishing assets to Equus Holdings, Inc. and Redwood Acquisition, Inc. (now known as Rimage Corporation).

3

On October 3, 2014, the Company acquired Kulu Valley Ltd., a private limited company incorporated and operating in England and Wales, subsequently renamed Qumu Ltd (“Kulu Valley”). The acquisition was made to expand Qumu’s addressable market through the offering of Kulu Valley’s best-in-class video content creation capabilities and easy-to-deploy pure cloud solution, while providing customers with access to industry-leading video content management and delivery capability.

Enterprise Video Content Management and Delivery Software

To increase communication, engagement and collaboration between employees and stakeholders, organizations have and continue to be invested significantly in content and network infrastructure that connects these employees and stakeholders across offices, conference rooms, computers, tablets and smart phones. As part of this, enterprises are adopting video as a mainstream communication and collaboration tool because they understand its benefits over other mediums.

Qumu video content management software solutions allow organizations to create, capture, organize and deliver content across the extended enterprise to a wide variety of end points, including mobile devices and thin clients. Qumu's video platform supports both live and on-demand streaming, and also secure download capabilities, a critical component for enterprise delivery. Qumu provides information technology administrators and corporate communication leaders a way to securely address the challenges of video that might otherwise overwhelm their data networks while utilizing their existing information technology infrastructures, thereby maximizing their investment and enabling the rapid adoption of video in their content, collaboration, communication and marketing infrastructures.

Qumu provides an end-to-end solution with an intuitive and rich user experience to create, manage and deliver live and on-demand video content both behind and beyond the secure firewall.

Capabilities and Products

Qumu Platform - Creating a Global Video Infrastructure for Organizations

The Qumu platform is a video content management software solution that can be deployed as a perpetual software license, a term software license or a cloud-hosted software as a service (SaaS). Qumu’s implementations can range in size from tens of thousands to millions of dollars, and they integrate with customers' existing video services (e.g., videoconferencing systems), business applications and broader IT infrastructures using Qumu's extensive application services or "APIs." Deployments also range from a single customer location to a global infrastructure serving over one hundred thousand corporate employees. Qumu’s platform solution components are deployed as needed to serve different capabilities of the enterprise video content lifecycle of creating, capturing, managing, delivering and experiencing video content.

Video Capture

• | Qumu Capture Studio is a portable software-enabled device that quickly and easily records, edits, and publishes video and presentation content. |

• | Qumu Quick Capture is a browser-based applet for the simple creation of videos captured from a user's computer screen and/or webcam. |

• | Qumu's encoder control facilitates live encoding and can leverage popular encoders from multiple vendors. |

• | Qumu also integrates with videoconferencing systems or Unified Communication software to enable their use as “studios” for the creation of live or on-demand video content. |

• | Qumu’s Creator provides ease of use for anyone to create slides and video at the desktop to produce their own rich content. |

Video Management

Qumu’s platform is an enterprise scalable solution that provides central control for all video applications, content and resources involved in the production and delivery of enterprise video. Video Control Center manages both live streamed video and video on-demand workflows. This comprehensive business video platform includes numerous industry-leading features:

• | Patent pending Qumu Pathfinder technology for intelligent routing to multiple device types with different bitrates, enabling more efficient use of the network and improved user experience. |

• | Qumu Speech Search for searching and indexing the spoken dialogue within video programs, greatly reducing time-to-knowledge. |

• | Live Broadcast Console for managing and deploying live streamed videos across an organization. |

• | Broad and deep security capabilities encompassing single-sign-on ("SSO"), Active Directory/LDAP integration, and Security Assertion Markup Language ("SAML") that make it easy to create a secure video application and network based on the enterprise's existing security standards. |

4

Video Delivery

• | The combination of Pathfinder with Qumu’s VideoNet Edge software creates a unique, highly secure, fault tolerant video delivery network with advanced streaming and caching features to provide outstanding performance for an unlimited number of users. By ensuring that only one stream crosses the WAN on its way to viewers in remote locations, VideoNet Edge minimizes the strain placed on the network by live webcasting or video on demand. VideoNet Edge can work as the sole distribution platform for video or in conjunction with other enterprise or Internet-based content distribution networks (“CDNs”). Qumu VideoNet Edge provides caching of H.264/MPEG-4, Windows Media & Flash video, Video on Demand and live broadcast content, reducing traffic from the centrally-located origin server. Importantly, Qumu offers VideoNet Edge software in a variety of form factors (Windows Software, virtual machine, appliance, and integrated with Citrix CloudBridge and Riverbed VSP) to provide customers with the most deployment options. |

• | Qumu VideoNet Edge software solutions can federate existing CDNs into a single system for intranet and Internet content distribution of video and related media assets. The federation capability includes Internet-based CDNs like Akamai and Amazon CloudFront as well as intranet-based devices like Riverbed Steelhead, Cisco ACNS/WaaS/CDS, and Blue Coat Director. This federation capability allows customers and partners to execute an “embrace and replace” strategy for upgrading their networks as opposed to “rip and replace” from other vendors. |

• | Qumu Secure Download allows video to be securely delivered to mobile devices, viewed offline, and managed/disposed automatically based on prescribed policies. |

Mobility and Integration

• | Qumu provides Mobile Apps for iOS, Android and Windows phones and tablets. The apps are complete out-of-the-box native video applications built using the Qumu Mobile SDKs. Customers can also work with Qumu Professional Services to create fully branded applications accessing Qumu's video infrastructure. Qumu’s HTML5-based video portal also provides native support for all device platforms. |

• | Qumu provides integration between its mobile apps and leading mobile device management/mobile application management ("MDM/MAM") platforms such as Good Technology and XenMobile to ensure that Qumu's solutions work within the environments its customers are investing in for mobile security. |

• | Qumu integrates with a variety of key business applications and infrastructure capabilities to enable organizations to employ video in any work context required. Qumu offers integration with Microsoft SharePoint and Lync as well as with Office365; IBM Connections and IBM WebSphere; Jive and other collaborative and social platforms. Qumu continues to work with partners and integrators to extend video functionality through the use of its REST APIs. Qumu also integrates with Citrix capabilities such as XenApp and XenDesktop, enabling Qumu video to be delivered to thick or thin clients managed within a Citrix virtual desktop infrastructure. |

Externalizing Video for Maximum Reach and Impact

The Qumu platform in a cloud deployment allows SaaS enabled customers to easily create video and rich media presentations and deliver video seamlessly to customers, partners, and employees. Cloud deployments allow organizations worldwide to rapidly and clearly present their messages and drive business opportunities through the integration of video with their web sites and their marketing and campaign automation platforms.

The Qumu platform in a cloud delivery brings the power of Qumu video to organizations that do not wish to make infrastructure investments to own and support their applications. Instead, Qumu provides the following capabilities that are easily purchased, implemented, and available through the web browser:

• | Create rich media with the Qumu platform in minutes - Qumu's customers can capture video and easily integrate it with PowerPoint slides to ensure that messages are delivered and understood; provide high quality sales enablement on a regular basis from the desktop; and broadcast news about products and services to partners and customers every week. |

• | Embed and share Qumu content easily with nearly any application - video “widgets” can be embedded, played, and tracked within any external application, ranging from web sites, to email offers, to campaigns managed and executed by platforms like Eloqua and Salesforce.com. Analytics on origin and viewership are easily captured and integrated back for targeted marketing and sales. |

• | Quickly create and deliver video for both live and on-demand - organizations purchase Qumu's cloud platform to support a variety of live broadcasts and on-demand scenarios, and the platform enables both to be executed and managed easily whenever desired. Video and content created and captured is managed within the cloud platform resident on IBM SoftLayer, thus providing market-leading security and compliance for users. |

5

• | Support an unlimited number of users - Qumu's cloud platform scales easily with a customer's needs, enabling organizations to create rich video presentations for 100's or to drive high performance video marketing campaigns to many thousands. Video is also transcoded automatically to support any user, format, or device for viewing. |

Marketing and Distribution

Qumu’s solutions serve a growing customer base of large enterprises across a wide range of vertical and horizontal markets. Qumu has primarily targeted enterprises with 10,000+ employees and a history of video use for corporate communications. Qumu's customers are some the largest corporations worldwide. Beginning in 2014, Qumu increased its efforts and ability in targeting mid-size businesses with less than 10,000 employees by promoting the new cloud deployment model.

Qumu serves its customer base primarily via direct sales, and to a lesser extent via channel partners, offering a variety of deployment methodologies and business models to meet customer demand including software, software on server appliance, software-enabled devices, SaaS and managed services.

In 2016, Qumu was selected as a leader by multiple industry reports:

• | Gartner’s Critical Capabilities reports focus on a group of competing products or services based on a set of use cases that match typical client deployment scenarios. These use cases are based on the real-world problems that clients need to solve, as well as how they intend to use the technology or service within their enterprises. Qumu received the highest scores for video content management. |

• | Aragon Research named Qumu a leader in its Video Content Management report. |

• | Wainhouse Research positioned Qumu as the leader in Enterprise Streaming Market. |

These selections are visible proof points in the market that had a positive impact on Qumu’s market awareness and lead generation activities.

Qumu sells products and services internationally through its U.S. operation and its subsidiaries in the United Kingdom and Japan. International sales comprised approximately 27%, 27% and 15% of revenues for the years ended December 31, 2016, 2015 and 2014, respectively. During the years ended December 31, 2016 and 2015, the Company had one customer that accounted for more than 10% of its revenues; no customer accounted for more than 10% of revenues for the year ended December 31, 2014.

Competition

Major competitors of Qumu include Kaltura, Kontiki, Cisco, Polycom, vBrick, Brightcove and MediaPlatform. Due to Qumu's unique end to end solution for a complete video infrastructure that includes support for mobile devices and existing IT infrastructure, Qumu believes it is able to compete effectively with these competitors. Qumu also differentiates itself from its competitors through its video delivery technology and flexibility as to solution deployment and service options.

Research and Development

Qumu develops its software internally and licenses or purchases software from third parties. Research and development expense was $8.5 million, $10.7 million and $9.5 million for the years ended December 31, 2016, 2015 and 2014, respectively.

As of December 31, 2016, the Company employed 61 employees in research and development. This staff engages in research and development of new products and enhancements to existing products. In addition, Qumu partners with third parties to utilize their competencies in creating products to enhance its product offerings.

Backlog of Contracted Commitments

The Company's contracted commitment backlog was $22.9 million at December 31, 2016, compared to $33.4 million at December 31, 2015. The Company defines contracted commitments as the dollar value of signed non-cancellable customer purchase commitments. Of the total at December 31, 2016, the Company expects to recognize between $16.0 million and $17.0 million as revenue during the year ended December 31, 2017. Actual amounts could differ depending on timing of customer deployments and other factors.

Intellectual Property

Qumu currently maintains three U.S. patents and has two non-provisional utility patent applications pending in the U.S. Further, Qumu protects the proprietary nature of its software primarily through copyright and license agreements. It is Qumu's policy to protect the proprietary nature of its newly developed products whenever they are likely to become significant sources

6

of revenue. No assurance can be given that Qumu will be able to obtain patent or other protection for its products. In addition, Qumu has registered and may in the future register trademarks and other marks used in its business.

Qumu also licenses or purchases the intellectual property ownership rights of programs developed by others with license or technology transfer agreements that may obligate Qumu to pay a flat license fee or royalties, typically based on a dollar amount per unit shipped or a percentage of the revenue generated by those programs. Contractual obligations with respect to such licenses will require cash payments of $301,000 in 2017.

As the number of Qumu's products increases and the functionality of those products expand, Qumu believes that it may become increasingly subject to attempts by others to duplicate its proprietary technology and to the possibility of infringement of its intellectual property. In addition, although Qumu does not believe that any of its products infringe on the rights of others, third parties have claimed, and may in the future claim, Qumu's products infringe on their rights and these third parties may assert infringement claims against Qumu in the future. Qumu may litigate to enforce its intellectual property rights and to defend against claimed infringement of the rights of others or to determine the ownership, scope, or validity of Qumu's proprietary rights and the rights of others. Any claim of infringement against Qumu could involve significant liabilities to third parties, could require Qumu to seek licenses from third parties and could prevent Qumu from developing, selling or using its products.

The Company is the owner of various trademarks and trade names referenced in this Annual Report on Form 10-K including: "Qumu," "VideoNet Edge" and "Pathfinder." Solely for convenience, the trademarks and trade names in this Report are referred to without the ® and TM symbols, but such references should not be construed as any indicator that the Company or the other respective owners will not assert, to the fullest extent under applicable law, its or their rights thereto.

Employees

As of December 31, 2016, the Company had 150 employees, of which 61 were involved in research and development, 28 in service and support, 37 in sales and marketing, and 24 in administration and management. None of Qumu's employees are represented by a labor union or covered by a collective bargaining agreement.

Available Information

Qumu maintains a website at www.qumu.com. Qumu files reports with the Securities and Exchange Commission and its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and other reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, are available on its website, as soon as reasonably practicable after these documents are filed with the SEC. To obtain copies of these reports, go to www.qumu.com and click on “Company,” then click on “Investor Relations,” then "SEC Filings" and all current EDGAR reports are available for viewing. A copy of any report filed by the Company with the SEC will also be furnished without charge to any shareholder who requests it in writing to: Secretary, Qumu Corporation 510 1st Avenue North, Suite 305, Minneapolis, MN 55403.

ITEM 1A. RISK FACTORS

If any of the following risks actually occur, our results of operations, cash flows and the market price of our common stock could be negatively impacted. Although we believe that we have identified and discussed below the most significant risk factors affecting our business, there may be additional risks and uncertainties that are not presently known or that are not currently believed to be significant that may adversely affect our performance or financial condition. Any forecast regarding our future performance, including, but not limited to, forecasts regarding estimated bookings, revenue, or cash flow from our operating activities, are forward-looking statements. These forward-looking statements reflect various assumptions and are subject to significant uncertainties and risks that could cause the actual results to differ materially from those described in the forward-looking statement, including the risks reflected in the risk factors set forth below. Consequently, the future results expressed or implied by any forward-looking statement are not guaranteed and the variation of actual results or events from such statements may be material and adverse.

The markets for video content and software to manage video content are each in early stages of development. If this market does not develop or develops more slowly than we expect, our revenues may decline or fail to grow.

With the sale of the disc publishing business on July 1, 2014, we now derive all of our revenues from providing video content management software. The use of video as a mainstream communication and collaboration platform and the market for video content management software is in an early stage of development, and it is uncertain whether this use of video will achieve high levels of acceptance. Widespread acceptance and use of video in the enterprise is critical to our future growth and success. Likewise, it is uncertain whether video content management software will achieve high levels of demand and market acceptance. Our success will depend on enterprises adopting video as a platform and upon enterprise demand for software to help them capture, organize and distribute this content.

7

Some customers may be reluctant or unwilling to use video as a medium within the enterprise for a number of reasons, including lack of perceived benefit of this new method of communication and existing investments in other enterprise-wide communications tools. Further, even if customers are using video as a medium, these customers may choose to rely upon their own IT infrastructure and resources to manage their video content. Because many companies generally are predisposed to maintaining control of their IT systems and infrastructure, there may be resistance to using software as a service provided by a third party. Privacy concerns and transition costs are also factors that may affect a potential customer’s decision to subscribe to an external solution.

Additional factors that may limit market acceptance of our video content management software include:

• | competitive dynamics may cause pricing levels to change as the market matures and cause customers to seek out lower priced alternatives to our video content management software or force us to reduce the prices we charge for our products or services; or |

• | existing and new market participants may introduce new types of solutions and different approaches to enable enterprises to address their enterprise communications or video communications needs and these disruptive technologies may reduce demand for our video content management software. |

If customers do not perceive the benefits of our video content management software, or if customers are unwilling to accept video content as an alternative to other more traditional forms of enterprise communication, the market for our software might not continue to develop or might develop more slowly than we expect, either of which would significantly adversely affect our financial results and prospects.

To compete effectively, we must continually improve existing products and introduce new products that achieve market acceptance.

The software industry in general, and in particular, software targeted to a new and developing market like enterprise video content management, is characterized by rapid technological changes, evolving industry standards, changing customer requirements, and frequent new product and service introductions and enhancements. The introduction of products using new technologies or the adoption of new industry standards can make our existing products, or products under development, obsolete or unmarketable. If these technologies are patented or proprietary to our competitors, we may not be able to access these technologies. In order to remain competitive and increase sales, we must anticipate and adapt to these rapidly changing technologies, enhance our existing products and introduce new products to address the changing demands of our customers. If we fail to anticipate or respond to technological developments or customer requirements, or if we are significantly delayed in developing and introducing products, our revenues will decline.

The process of developing new technology is complex and uncertain, and if we fail to accurately predict customers’ changing needs and emerging technological trends, our business could be harmed. We must commit significant resources and may incur obligations (such as royalty obligations) to develop new products and features before knowing whether our investments will result in products the market will accept and without knowing the levels of revenue, if any, that may be derived from these products. Although we expect to continue to invest substantial resources in product development activities, our efforts to achieve and maintain profitability will require us to be selective and focused with our research and development expenditures. Some of our competitors have greater engineering and product development resources than we have, allowing them to develop a greater number of products or improvements or to develop them more quickly.

If we fail to anticipate or respond in a cost-effective and timely manner to technological developments, changes in industry standards or customer requirements, or if we experience any significant delays in the development or introduction of new products or improvements to existing products, our business, operating results and financial condition could be affected adversely.

If we do not generate sufficient cash flow to fund our operations, we may need additional capital and any additional capital we seek may not be available in the amount or at the time we need it.

In the year ended December 31, 2016, we had an operating loss of $11.4 million, used $9.4 million of net cash in continuing operating activities, and ended 2016 with $10.4 million in cash and cash equivalents. In the third quarter of 2015 through early 2016, we implemented a significant expense reduction program that, when combined with expected revenue growth in 2017, we believe will allow us to attain our goal of being cash flow breakeven for the second half of 2017.

On October 21, 2016, we entered into a credit agreement with HCP-FVD, LLC as lender and Hale Capital Partners, LP as administrative agent for an $8.0 million term loan secured by substantially all of our assets. The credit agreement was amended effective March 31, 2017 to modify certain covenants and certain prepayment terms. The term loan requires payment of interest monthly at the prime rate plus 6% and is due in full at its maturity date of October 21, 2019. As of December 31, 2016, interest was payable at 9.75%.

8

Our financing needs are based upon management estimates as to future revenue and expense. If we are not able to become cash flow breakeven for the second half of 2017 by increasing revenue and controlling expenses, we may need to raise funds in the future to execute our business plan and pursue our growth objectives. Our credit agreement also contains covenants requiring minimum cash in the U.S. of $4.0 million and requiring that our combined eligible accounts receivable and cash in the U.S. be no less than 118% of our obligations under the credit agreement. If we are not able to achieve our operating plan for 2017, we may need to raise funds in the future to achieve covenant compliance. In addition to these potential short-term capital needs, we will need to generate sufficient cash to repay the term loan at maturity or secure capital to refinance the term loan at maturity. If we are unable to maintain compliance with our covenants, we may have to negotiate with our lender and there can be no assurance the lender will not accelerate the repayment of such borrowings.

If we are able to raise funds in the future, we cannot assure you that additional financing will be available in the amount or at the time we need it, or that it will be available on acceptable terms or at all. We may obtain future additional financing by incurring indebtedness or from an offering of our equity securities or both.

If we raise additional equity financing, our shareholders may experience significant dilution of their ownership interests and the value of shares of our common stock could decline. Our efforts to raise additional funds from the sale of equity may be hampered by the currently depressed trading price of our common stock. If we raise additional equity financing, the provisions our credit agreement require us to use the proceeds from the equity financing to prepay our term loan. New investors may demand rights, preferences or privileges senior to those of existing holders of common stock. Our efforts to raise funds by incurring additional indebtedness may be hampered by the covenants and restrictions of our existing outstanding indebtedness and the fact that our assets are pledged to our lender to secure existing debt. The covenants of our credit agreement restrict our ability to make dividends, create liens, incur indebtedness, and sell our assets and properties, subject to certain exceptions. Likewise, any additional debt we incur would likely have covenants that would affect the manner in which we conduct our business, including by restricting our ability to incur additional indebtedness, preventing us from creating liens or requiring specified financial covenants. In addition, we may face challenges in securing additional debt financing if our future cash flow from operations is not sufficient to support debt service payments. If we raise capital through the sale of our investment in BriefCam, the credit agreement also requires us to use the proceeds to prepay our term loan. If we cannot timely raise any needed funds, we may be forced to make further substantial reductions in our operating expenses, which could limit our sales and marketing efforts, adversely affect our ability to attract and retain qualified personnel, limit our ability to develop and enhance our solutions, make it more difficult for us to respond to competitive pressures or unanticipated working capital requirements, and otherwise adversely affect our ability to pursue our growth objectives.

We have limited operating history with our video content software management business, which may make evaluating our business and prospects difficult.

With our acquisition of Qumu, Inc. in October 2011, we began our video content management business. Prior to the acquisition of Qumu, Inc. and through July 1, 2014, we also operated the disc publishing business. On October 3, 2014, we acquired Kulu Valley Ltd., a private limited company incorporated in England and Wales, subsequently renamed Qumu Ltd, to add its cloud-based video content creation capabilities and expanded market reach to include external use cases. As a result, we have a limited history with our video content software management business and an even more limited history with the standalone operation of our video content software management business. Accordingly, our historical financial results are not necessarily indicative of the future financial condition or results of operations of our video content management business. This limited history may make it difficult for shareholders, prospective investors, analysts and others to evaluate our business and prospects given the risks and uncertainties that we face as a relatively early stage, high technology company entering a new and rapidly evolving market.

We face intense competition and such competition may result in price reductions, lower gross profits and loss of market share.

Our products face intense competition, both from other products and from other technologies, both in the U.S. and in international markets. We compete with others such as Kaltura, Kontiki, Cisco, Polycom, vBrick, Brightcove and MediaPlatform who deliver video content to businesses. Further, because some prospective customers may choose to rely upon their own IT infrastructure and resources to manage their video content, we compete with customer-created solutions for video content management. We expect the intensity of competition we face to increase in the future from other established and emerging companies.

Many of our competitors have greater resources than we do, including greater sales, product development, marketing, financial, technical or engineering resources. In addition, because our enterprise video content management software business is relatively new with a limited operating history, our target customers may prefer to purchase software products that are critical to their business from one of our larger, more established competitors.

9

To remain competitive, we believe that we must continue to provide:

• | technologically advanced products and solutions that anticipate and satisfy the demands of end-users; |

• | continuing advancements or innovations in our product offerings, including products with price-performance advantages or value-added features in security, reliability or other key areas of customer interest; |

• | innovations in video content creation, management, delivery and user experience; |

• | a responsive and effective sales force; |

• | a dependable and efficient sales distribution network; |

• | superior customer service; and |

• | high levels of quality and reliability. |

We cannot assure you that we will be able to compete successfully against our current or future competitors. Competition may result in price reductions, lower gross profit margins, increased discounts to customers and loss of market share, and could require increased spending by us on research and development, sales and marketing and customer support.

We encounter long sales cycles with our enterprise video solutions, which could adversely affect our operating results in a given period.

Our ability to increase revenues and achieve profitability depends, in large part, on widespread acceptance of our enterprise video content management software products by large businesses and other organizations. As we target our sales efforts at these customers, we face greater costs, longer sales cycles and less predictability in completing sales. In the large enterprise market, the customer’s decision to use our products may be an enterprise-wide decision and, therefore, these types of sales require us to provide greater levels of education regarding the use and benefits of our applications. Further, given the constant innovation with our industry and our products, customers may delay purchasing decisions until certain features or products in development are brought to market. Longer sales cycles could cause our operating and financial results to suffer in a given period.

Adverse economic conditions, particularly those affecting our customers have harmed and may continue to harm our business.

Unfavorable changes in economic conditions, including recession, inflation, lack of access to capital, lack of consumer confidence or other changes have resulted and may continue to result in lower spending among our customers and target customers.

Further, we sell our products throughout the United States, as well as in several international countries to commercial and government customers. Our business may be adversely affected by factors in the United States and other countries such as disruptions in financial markets, reductions in government spending, or downturns in economic activity in specific countries or regions, or in the various industries in which we operate; social, political or labor conditions in specific countries or regions; or adverse changes in the availability and cost of capital, interest rates, tax rates, or regulations. These factors are beyond our control, but may result in further decreases in spending among customers and softening demand for our products.

Further, challenging economic conditions also may impair the ability of our customers to pay for products and services they have purchased. As a result, our cash flow may be negatively impacted and our allowance for doubtful accounts and write-offs of accounts receivable may increase.

Our sales will decline, and our business will be materially harmed, if our sales and marketing efforts are not effective.

We will need to continue to optimize our sales infrastructure in order to grow our customer base and our business. Identifying and recruiting qualified personnel and training them in the use and functionality of our software requires significant time, expense and attention. It can take six months or longer before our sales representatives are fully-trained and productive. If we are unable to hire, develop and retain talented sales personnel or if new sales personnel are unable to achieve desired productivity levels in a reasonable period of time, we may not be able to realize the expected benefits of this investment or increase our revenues. We also intend to expand new sales models that focus on different sales strategies tailored to different customer types. Our business may be adversely affected if our efforts to train our internal sales force or execute our selling strategies do not generate a corresponding increase in revenues.

For sales that are made to customers through our channel partners, we depend on these businesses to provide effective sales and marketing support to our products. Our channel partners are independent businesses that we do not control. Our agreements with channel partners do not contain requirements that a certain percentage of such parties’ sales are of our products. These channel partners may choose to devote their efforts to other products in different markets or reduce or fail to devote the resources to provide effective sales and marketing support of our products, any of which could harm our business by reducing sales to customers.

10

We believe that our future growth and success will depend upon the success of our internal sales and marketing efforts as well as those of our channel partners.

Competition for highly skilled personnel is intense and if we fail to attract and retain talented employees, we may fail to compete effectively.

Our future success depends, in significant part, on our continuing ability to identify, hire, develop, motivate, and retain highly skilled personnel for all areas of our organization. Competition in our industry for qualified employees, particularly in senior management, product development and sales, is intense. In addition, our compensation arrangements, such as our equity award programs, may not always be successful in attracting new employees and retaining and motivating our existing employees given the high demand for these employees from other employers. Our ability to compete effectively depends on our ability to attract new employees and to retain and motivate our existing employees.

Our enterprise video content management software products must be successfully integrated into our customers’ information technology environments and workflows and changes to these environments, workflows or unforeseen combinations of technologies may harm our customers’ experience in using our software products.

A significant portion of our sales are made into applications that require our enterprise video content management software products to be integrated into other enterprise workflows, enterprise information technology environments or software functionalities. Any significant changes to enterprise workflows, IT environments or software programs may limit the use or functionality of or demand for our products. As our customers advance technologically, we must be able to effectively integrate our products to remain competitive. Further, current and potential customers may choose to use products offered by our competitors or may not purchase our products if our products would require changes in their existing enterprise workflows, IT environments or software.

The growth and functionality of our enterprise video content management software products depend upon the solution’s effective operation with mobile operating systems and computer networks.

Our products are currently compatible with various mobile operating systems including the iOS, Windows Mobile and Android operating systems. The functionality of our products depends upon the continued interoperability of these products with popular mobile operating systems. Any changes in these systems that degrade our products’ functionality or give preferential treatment to competitive offerings could adversely affect the operability and usage of our video management software products on mobile devices. Additionally, in order to deliver a high quality user experience, it is important that our products work well with a range of mobile technologies, systems, and networks. We may not be successful in keeping pace with changes in mobile technologies, operating systems, or networks or in developing products that operate effectively within existing or future technologies, systems, and networks. Further, any significant changes to mobile operating systems by their respective developers may prevent our products from working properly or at all on these systems. In the event that it is more difficult for users to access content delivered by our solutions to their mobile devices, if our products do not operate effectively within the most popular operating systems or if popular mobile devices do not offer a high quality user experience, sales of and customer demand for our software products could be harmed.

Any failure of major elements of our products could lead to significant disruptions in the ability to serve customers, which could damage our reputation, reduce our revenues or otherwise harm our business.

Our business is dependent upon providing customers with fast, efficient and reliable services. A reduction in the performance, reliability or availability of required network infrastructure may harm our ability to distribute content to our customers, as well as our reputation and ability to attract and retain customers. Our content management software solutions and operations are susceptible to, and could be damaged or interrupted by outages caused by fire, flood, power loss, telecommunications failure, Internet or mobile network breakdown, earthquake and similar events. Our solutions are also subject to human error, security breaches, power losses, computer viruses, break-ins, “denial of service” attacks, sabotage, intentional acts of vandalism and tampering designed to disrupt our computer systems and network communications. Our failure to protect our network against damage from any of these events could harm our business.

11

Our operations also depend on web browsers, ISPs (Internet service providers) and mobile networks to provide our customers’ end-users with access to websites, streaming and mobile content. Many of these providers have experienced outages in the past, and could experience outages, delays and other difficulties due to system failures unrelated to our solutions. Any such outage, delay or difficulty could adversely affect our ability to effectively provide our products and services, which would harm our business.

If we lose access to third-party licenses, our software product development and production may be delayed or we may incur additional expense to modify our products or products in development.

Some of our solutions contain software licensed from third parties. Third-party licensing arrangements are subject to a number of risks and uncertainties, including:

• | undetected errors or unauthorized use of another person’s code in the third-party’s software; |

• | disagreement over the scope of the license and other key terms, such as royalties payable; |

• | infringement actions brought by third-party licensees; |

• | that third parties will create solutions that directly compete with our products; and |

• | termination or expiration of the license. |

Because of these risks, some of these licenses may not be available to us in the future on terms that are acceptable to us or allow our products to remain competitive. The loss of these licenses or the inability to maintain any of them on commercially acceptable terms could delay development of future products or impair the functionality or enhancement of existing products, leading to increased expense associated with licenses of third-party software or development of alternative software to provide comparable functionality for our existing products and modification of our existing products. Further, if we lose or are unable to maintain any of these third-party licenses or are required to modify software obtained under third-party licenses, it could delay the release of new products, delay enhancements to our existing products or delay sales of our existing products. Any delays could result in loss of competitive position, loss of sales and loss of customer confidence, which could have a material adverse effect on our business, results of operations and financial condition.

If the limited amount of open source software that is incorporated into our products were to become unavailable or if we violate the terms of open source licenses, it could adversely affect sales of our products, which could disrupt our business and harm our financial results.

Our products incorporate a limited amount of “open source” software. Open source software is made available to us and to the public by its authors or other third parties under licenses that impose certain obligations on licensees that re-distribute or make derivative works of the open source software. We may not be able to replace the functionality provided by the open source software currently incorporated in our products if that software becomes unavailable, obsolete or incompatible with future versions of our products. In addition, we must carefully monitor our compliance with the licensing requirements applicable to that open source software. If we have failed or if in the future we fail to comply with the applicable license requirements, we might lose the right to use the subject open source software. The terms of some open source licenses would require us to give our customers significant rights to open source software that is subject to those licenses and is incorporated in our products. This would include the right to obtain from us the source code form of that open source software, and the right to use, modify and distribute that open source software to others. We may be required to provide these rights to customers on a royalty-free basis. Those rights might also extend to modifications and additions we make to the subject open source software. That open source software, and those modifications and additions, also might be obtained by our competitors and used in competing products.

The enforceability and interpretation of open source licenses remains uncertain under applicable law. Unfavorable court decisions could require us to replace open source software incorporated in our products. In some cases this might require us to obtain licenses to commercial software under terms that restrict our use of that commercial software and require us to pay royalties. In some cases we might need to redesign our software products, or to discontinue the sale of our software products if a redesign could not be accomplished on a timely basis. These same consequences result if our use of any open source software or commercial software is found to infringe any intellectual property right of another party. Any of these occurrences would harm our business, operating results and financial condition.

We sell a significant portion of our products internationally, which exposes us to risks associated with international operations.

We sell a significant amount of our products to customers outside the United States, particularly in Europe and Asia. International sales comprised approximately 27%, 27% and 15% of revenues for the years ended December 31, 2016, 2015 and 2014, respectively. We expect that sales to international customers, including customers in Europe and Asia, will continue to account for a significant portion of our net sales. Sales outside the United States involve the following risks, among others:

• | international governments may impose tariffs, quotas and taxes; |

12

• | the demand for our products will depend, in part, on local economic health; |

• | political and economic instability may reduce demand for our products; |

• | restrictions on the export or import of technology may reduce or eliminate our ability to sell in certain markets; |

• | potentially limited intellectual property protection in certain countries may limit our recourse against infringing products or cause us to refrain from selling in certain markets; |

• | potential difficulties in managing our international operations; |

• | the burden and cost of complying with a variety of international laws, including those relating to data security and privacy; |

• | we may decide to price our products in foreign currency denominations; |

• | our contracts with international channel partners cannot fully protect us against political and economic instability; |

• | potential difficulties in collecting receivables; and |

• | we may not be able to control our international channel partners’ efforts on our behalf. |

The financial results of our non-U.S. subsidiaries are translated into U.S. dollars for consolidation with our overall financial results. Currency translations and fluctuations may adversely affect the financial performance of our consolidated operations. Currency fluctuations may also increase the relative price of our product in international markets and thereby could also cause our products to become less affordable or less price competitive than those of international manufacturers. These risks associated with international operations may have a material adverse effect on our revenue from or costs associated with international sales.

If our domestic or international intellectual property rights are not adequately protected, others may offer products similar to ours or independently develop the same or similar technologies or otherwise obtain access to our technology and trade secrets which could depress our product selling prices and gross profit or result in loss of market share.

We believe that protecting our proprietary technology is important to our success and competitive positioning. In addition to common law intellectual property rights, we rely on patents, trade secrets, trademarks, copyrights, know-how, license agreements and contractual provisions to establish and protect our intellectual property rights. However, these legal means afford us only limited protection and may not adequately protect our rights or remedies to gain or keep any advantages we may have over our competitors.

Our competitors, who may have or could develop or acquire significant resources, may make substantial investments in competing technologies, or may apply for and obtain patents that will prevent, limit or interfere with our ability to develop or market our products. Further, although we do not believe that any of our products infringe on the rights of others, third parties have claimed, and may claim in the future, that our products infringe on their rights, and these third parties may assert infringement claims against us in the future.

Costly litigation may be necessary to enforce patents issued to us, to protect trade secrets or “know-how” we own, to defend us against claimed infringement of the rights of others or to determine the ownership, scope, or validity of our proprietary rights and the rights of others. Any claim of infringement against us may involve significant liabilities to third parties, could require us to seek licenses from third parties, and could prevent us from manufacturing, selling, or using our products. The occurrence of this litigation, or the effect of an adverse determination in any of this type of litigation, could have a material adverse effect on our business, financial condition and results of operations. Further, the laws of some of the countries in which our products are or may be sold may not protect our products and intellectual property to the same extent as the United States or at all. Our failure to protect or enforce our intellectual property rights could have a material adverse effect on our business, results of operations and financial condition.

Changes in laws and regulations related to the Internet or changes in the Internet infrastructure itself may diminish the demand for our products, and could have a negative impact on our business.

The future success of our business depends in part upon the continued use of the Internet as a primary medium for commerce, communication and business applications. Federal, state or international government bodies or agencies have in the past adopted, and may in the future adopt, laws or regulations affecting the use of the Internet as a commercial medium. Changes in these laws or regulations could require us to modify our products in order to comply with these changes. In addition, government agencies or private organizations may begin to impose taxes, fees or other charges for accessing the Internet or commerce conducted via the Internet. These laws or charges could limit the growth of Internet-related commerce or communications generally, or result in reductions in the demand for Internet-based applications such as ours. The adoption of any laws or regulations that adversely affect the growth, popularity or use of the Internet could limit the growth of the video as a mainstream communication and collaboration tool, limit the market for video content management software generally, and limit the demand for our products.

13

In addition, the use of the Internet as a business tool could be adversely affected due to delays in the development or adoption of new standards and protocols to handle increased demands of Internet activity, security, reliability, cost, ease of use, accessibility, and quality of service. The performance of the Internet and its acceptance as a business tool has been adversely affected by “viruses,” “worms” and similar malicious programs and the Internet has experienced a variety of outages and other delays as a result of damage to portions of its infrastructure. If the use of the Internet is adversely affected by these issues, demand for our applications could suffer.

Expanding laws, regulations and customer requirements relating to data security and privacy may adversely affect sales of our products and result in increased compliance costs.

Our customers can use our products to collect, use and store personal or identifying information regarding their employees, customers and suppliers. Federal, state and international government bodies and agencies have adopted, are considering adopting, or may adopt laws and regulations regarding data security, privacy and the collection, use, storage and disclosure of personal information obtained from consumers and individuals. These laws and regulations could reduce the demand for our software products if we fail to design or enhance our products to enable our customers to comply with the privacy and security measures required by the legislation.

We also must comply with the policies, procedures and business requirements of our customers relating to data privacy and security, which can vary based upon the customer, the customer’s industry or location, and the product the customer selects, and which may be more restrictive than the privacy and security measures required by law or regulation. In particular, the European Union and many countries in Europe have stringent privacy laws and regulations, which may impact our ability to profitably operate in certain European countries or to offer products that meet the needs of customers subject to European Union privacy laws and regulations.

The costs of compliance with, and other burdens imposed by, our customers’ own requirements and the privacy and security laws and regulations that are applicable to our customers’ businesses may limit the use and adoption of our products and reduce overall demand. Non-compliance with our customers’ specific requirements may lead to termination of contracts with these customers or liabilities to the customers; non-compliance with applicable laws and regulations may lead to significant fines, penalties or liabilities.

Furthermore, privacy concerns may cause our customers’ workers to resist providing the personal data necessary to allow our customers to use our products effectively. If a customer experiences a significant data security breach involving our software products, our customers could lose confidence in our software’s ability to protect the personal information of their employees, customers and suppliers, which could cause our customers to discontinue use of our products. The loss of confidence from a significant data security breach involving our software products could hurt our reputation, cause sales and marketing challenges to existing and new customers, cause loss of market share or exacerbate competitive pressures, result in an increase in our development costs to address any potential vulnerabilities in our software products, and may result in reduced demand and revenue. Even the perception of privacy concerns, whether or not valid, may inhibit market adoption of our products in certain industries.

Domestic and international legislative and regulatory initiatives and our customers’ privacy policies and practices may adversely affect our customers’ ability to process, handle, store, use and transmit demographic and personal information from their employees, customers and suppliers, which could reduce demand for our products.

In addition to government activity, privacy advocacy groups and the technology and other industries are considering various new, additional or different self-regulatory standards that may place additional burdens on our software products. If the processing of personal information were to be curtailed in this manner, our software products would be less effective, which may reduce demand for our products and adversely affect our business.

A failure to maintain adequate internal control over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act of 2002 or to prevent or detect material misstatements in our annual or interim financial statements in the future could result in inaccurate financial reporting, or could otherwise harm our business.

Ensuring that we have internal financial and accounting controls and procedures adequate to produce accurate financial statements on a timely basis is a costly and time-consuming effort that needs to be re-evaluated frequently. The Sarbanes-Oxley Act requires, among other things, that we maintain effective internal control over financial reporting and disclosure controls and procedures. In particular, we are required to perform annual system and process evaluation and testing of our internal control over financial reporting to allow management to report on the effectiveness of our internal control over financial reporting. Furthermore, implementing any appropriate future changes to our internal control over financial reporting may entail substantial costs in order to modify our existing accounting systems, may take a significant period of time to complete and may distract our officers, directors and employees from the operation of our business. If we are not able to comply with the

14

requirements of Section 404 in the future, or if material weaknesses are identified, the market price of our common stock could decline.

We may face circumstances in the future that could result in impairment charges, including, but not limited to, significant goodwill impairment charges.

If the fair value of any of our long-lived assets decreases as a result of an economic slowdown, a downturn in the markets where we sell products and services or a downturn in our financial performance and/or future outlook, we may be required to record an impairment charge on such assets, including goodwill.

We are required to test intangible assets with indefinite life periods for potential impairment annually and on an interim basis if there are indicators of a potential impairment. We also are required to evaluate amortizable intangible assets and fixed assets for impairment if there are indicators of a possible impairment. One potential indicator of impairment is the value of our market capitalization, or enterprise value, as compared to our net book value.

As of December 31, 2016, the Company’s market capitalization, without a control premium, was greater than its book value and the Company concluded there was no goodwill impairment. Declines in the Company’s market capitalization or a downturn in our future financial performance and/or future outlook could require the Company to record goodwill and other impairment charges. While a goodwill impairment charge is a non-cash charge, it would have a negative impact on our results of operations.

We may experience significant quarterly and annual fluctuations in our results of operations due to a number of factors and these fluctuations may negatively impact the market price of our common stock.

Our quarterly and annual results of operations may fluctuate significantly due to a variety of factors, many of which are outside of our control. With the sale of the disc publishing business on July 1, 2014, there may be even wider fluctuations in our results of operations given the smaller size of our retained software business. This variability may lead to volatility in our stock price as research analysts and investors respond to quarterly fluctuations and this volatility may be exacerbated by the relatively illiquid nature of our common stock. In addition, comparing our results of operations on a period-to-period basis, particularly on a sequential quarterly basis, may not be meaningful. You should not rely on our past results as an indication of our future performance.

Factors that may affect our results of operations include:

• | the number and mix of products and solutions sold in the period; |

• | the timing and amount of our recorded revenue, which will depend upon the mix of products and solutions selected by our customers with revenue from paid-up perpetual software licenses being recognized upon delivery, revenue from term software licenses recognized over the term of the contract, and revenue from cloud-hosted services recognized over the term of the subscription agreement; |

• | timing of customer purchase commitments, including the impact of long sales cycles and seasonal buying patterns; |

• | variability in the size of customer purchases and the impact of large customer orders on a particular period; |

• | the timing of major development projects and market launch of new products or improvements to existing products; |

• | reductions in our customers’ budgets for information technology purchases and delays in their purchasing cycles, due to changing global economic or market conditions; |

• | the impact to the marketplace of competitive products and pricing; |

• | the timing and level of operating expenses; |

• | the impact on revenue and expenses of acquisitions by us or by our competitors; |

• | future accounting pronouncements or changes in our accounting policies; and |

• | the impact of a recession or any other adverse global economic conditions on our business, including uncertainties that may cause a delay in entering into or a failure to enter into significant customer agreements. |

The foregoing factors are difficult to forecast, and these, as well as other factors, could adversely affect our quarterly and annual results of operations. Failure to achieve our quarterly or annual forecasts or to meet or exceed the expectations of research analysts or investors may cause our stock price to decline abruptly and significantly.

The limited liquidity for our common stock could affect your ability to sell your shares at a satisfactory price.

Our common stock is relatively illiquid. As of December 31, 2016, we had 9,227,247 shares of common stock outstanding. The average daily trading volume in our common stock, as reported by the Nasdaq Stock Market, for the 63 trading days beginning October 1, 2016 and ending December 31, 2016 was approximately 28,900 shares. A more active public market for our

15

common stock may not develop, which could adversely affect the trading price and liquidity of our common stock. Moreover, a thin trading market for our stock could cause the market price for our common stock to fluctuate significantly more than the stock market as a whole. Without a larger float, our common stock is less liquid than the stock of companies with broader public ownership. As a result, the trading prices of our common stock have been and may continue to be more volatile. In addition, in the absence of an active public trading market, shareholders may be unable to liquidate their shares of our common stock at a satisfactory price.

Provisions of Minnesota law, our bylaws and other agreements may deter a change of control of our company and may have a possible negative effect on our stock price.

Certain provisions of Minnesota law, our bylaws and other agreements may make it more difficult for a third-party to acquire, or discourage a third-party from attempting to acquire, control of our company, including:

• | the provisions of Minnesota law relating to business combinations and control share acquisitions; |

• | the provisions of our bylaws regarding the business properly brought before shareholders; |

• | the right of our board of directors to establish more than one class or series of shares and to fix the relative rights and preferences of any such different classes or series; |

• | the provisions of our stock incentive plans allowing for the acceleration of vesting or payments of awards granted under the plans in the event of specified events that result in a “change in control”; |

• | the provisions of our agreements provide for severance payments to our executive officers in the event of certain terminations following a “change in control”; and |

• | the provisions of our credit agreement requiring prepayment in full of our term loan upon a change in control. |

These measures could discourage or prevent a takeover of our company or changes in our management, even if an acquisition or such changes would be beneficial to our shareholders. This may have a negative effect on the price of our common stock.

Compliance with changing regulation of corporate governance and public disclosure may result in additional expenses and will constitute a larger percentage of our annual revenue than prior to the sale of the disc publishing business.

Keeping abreast of, and in compliance with, changing laws, regulations and standards relating to corporate governance and public company disclosure requirements, including the Sarbanes-Oxley Act of 2002 and in particular Section 404 of that Act relating to management certification of internal controls, the regulations of the Securities and Exchange Commission and the rules of the Nasdaq Stock Market have required an increased amount of management attention and external resources. We intend to invest all reasonably necessary resources to comply with evolving corporate governance and public disclosure standards, and this investment may result in increased general and administrative expenses and a diversion of management time and attention from revenue-generating activities to compliance activities. While all public companies face the costs and burdens associated with being public companies, the costs and burden of being a public company will be a significant portion of our annual revenues, which have been reduced following the sale of the disc publishing business on July 1, 2014.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Location of Property | Use of Property | Approximate Monthly Rent (USD) | Approximate Leased Square Footage | Lease Expiration Date | |||||

Minneapolis, Minnesota (Headquarters) | Engineering, service, sales, marketing and administration | $ | 23,000 | (1) | 16,500 | January 2023 | |||

San Bruno, California | Engineering, service, sales, marketing and administration | $ | 36,000 | (2) | 13,900 | June 2018 | |||

London, England | Engineering, service, sales, marketing and administration | $ | 36,500 | 5,500 | September 2019 | ||||

Hyderabad, India | Software development and testing | $ | 7,500 | 4,800 | September 2018 | ||||

_________________________________________________

(1) | The agreement has escalating lease payments ranging from approximately $23,000 to $26,000 per month during the course of the lease. |

(2) | The agreement has escalating lease payments ranging from approximately $33,000 to $38,000 per month during the course of the lease. |

16

ITEM 3. LEGAL PROCEEDINGS

The Company is exposed to a number of asserted and unasserted legal claims encountered in the ordinary course of its business. Although the outcome of any such legal actions cannot be predicted, management believes that there are no pending legal proceedings against or involving the Company for which the outcome is likely to have a material adverse effect upon its financial position or results of operations.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

17

PART II

ITEM 5. MARKET FOR COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Qumu's common stock is traded on the Nasdaq Global Market under the symbol “QUMU.” The following table sets forth, for the periods indicated, the range of low and high sales prices for Qumu's common stock as reported on The Nasdaq Stock Market.

Year Ended December 31, | ||||||||||||||||

2016 | 2015 | |||||||||||||||

Low | High | Low | High | |||||||||||||

First Quarter | $ | 2.10 | $ | 5.48 | $ | 12.31 | $ | 15.87 | ||||||||

Second Quarter | $ | 3.53 | $ | 5.50 | $ | 6.80 | $ | 14.99 | ||||||||

Third Quarter | $ | 2.19 | $ | 4.84 | $ | 1.58 | $ | 8.59 | ||||||||

Fourth Quarter | $ | 2.20 | $ | 3.77 | $ | 2.40 | $ | 4.94 | ||||||||

Shareholders

As of March 24, 2017, there were 107 shareholders of record of Qumu's common stock.

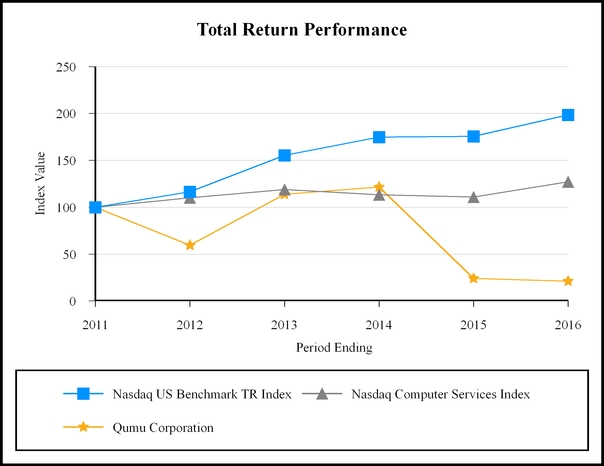

Dividends