Attached files

| file | filename |

|---|---|

| EX-31.1 - CERTIFICATION PURSUANT TO RULE 13A-14(A)/15D-14(A) CERTIFICATIONS SECTION 302 OF - VERSAR INC | exhibit31-1_otten.htm |

| EX-32.2 - CERTIFICATE PURSUANT TO SECTION 18 U.S.C. PURSUANT TO SECTION 906 OF THE SARBANE - VERSAR INC | exhibit32-2_downes.htm |

| EX-32.1 - CERTIFICATE PURSUANT TO SECTION 18 U.S.C. PURSUANT TO SECTION 906 OF THE SARBANE - VERSAR INC | exhibit32-1_otten.htm |

| EX-31.2 - CERTIFICATION PURSUANT TO RULE 13A-14(A)/15D-14(A) CERTIFICATIONS SECTION 302 OF - VERSAR INC | exhibit31-2_downes.htm |

| EX-23.2 - CONSENTS OF EXPERTS AND COUNSEL - VERSAR INC | gt_consentofindependentre.htm |

| EX-23.1 - CONSENTS OF EXPERTS AND COUNSEL - VERSAR INC | versarconsentofindependen.htm |

| EX-21 - SUBSIDIARIES OF THE REGISTRANT - VERSAR INC | exhibit21.htm |

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended

|

Commission File

|

|

July 1, 2016

|

No. 1-9309

|

Versar, Inc.

(Exact name of registrant as specified in its charter)

|

DELAWARE

|

54-0852979

|

|

(State or other jurisdiction

of Incorporation or organization)

|

(I.R.S. employer identification no.)

|

|

6850 Versar Center, Springfield, Virginia

|

22151

|

|

(Address of principal executive offices)

|

(Zip code)

|

(703) 750-3000

(Registrant’s telephone number, including area

code)

Securities registered pursuant to Section 12(b) of the

Act:

Common Stock, $.01 par value

(Title of Class)

NYSE MKT

(Name of each exchange on which registered)

Securities registered pursuant to Section 12(g) of Act:

NONE

Indicate by check mark if the registrant is a well-known seasoned

issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file

reports pursuant to Section 13 or Section 15(d) of the

Act.

Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all

reports required to be filed by Section 13 or 15(d) of the

Securities Exchange Act of 1934 during the preceding 12 months (or

for such shorter period that the registrant was required to file

such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Yes ☐ No ☑

Indicate by check mark whether the registrant has submitted

electronically and posted on its corporate web site, if any, every

Interactive Data File required to be submitted and posted pursuant

to Rule 405 of Regulation S-T during the preceding 12 months (or

for such shorter period that the registrant was required to submit

and post such files).

Yes ☑ No ☐

Indicate by check mark if disclosure of

delinquent filers pursuant to Item 405 of Regulation S-K is not

contained herein, and will not be contained, to the best of

registrant’s knowledge, in definitive proxy or information

statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large

accelerated filer, an accelerated filer, or a non-accelerated filer

(as defined in Rule 12b-2 of the Exchange Act).

|

Large accelerated filer ☐

|

Accelerated filer ☐

|

|

Non-accelerated filer ☐

(Do not check if a smaller reporting company)

|

Smaller reporting company

☑

|

Indicate by check mark whether the registrant is a shell company

(as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☑

The aggregate market value of the voting stock held by

non-affiliates of the registrant as of March 1, 2017 was

approximately $10,348,996.

The number of shares of Common Stock outstanding as of March 1,

2017 was 9,950,958.

PART I

Item 1. Business

Unless this report indicates otherwise the terms

”Versar,” the “Company,” “we,”

“us,” and “our” refer to Versar, Inc. and

consolidated subsidiaries. Versar’s fiscal year end is based

upon a 52 or 53 week year ending on the last Friday of the fiscal

period and therefore does not close on a calendar month end. The

Company’s fiscal year 2016 included 53 weeks and fiscal years

2015 and 2014 included 52 weeks.

Cautionary Statement Regarding Forward-Looking

Statements

This report contains

certain forward-looking statements that are based on current

expectations. Actual results may differ materially.

The forward-looking

statements include, without limitation, those regarding the

continued award of future work or task orders from government and

private clients, cost controls and reductions, the expected

resolution of delays in billing of certain projects, and the

possible impact of current and future claims against the Company

based upon negligence and other theories of liability.

Forward-looking statements involve numerous risks and uncertainties

that could cause actual results to differ materially, including,

but not limited to, the possibility that the demand for the

Company's services may decline as a result of possible changes in

general and industry specific economic conditions and the effects

of competitive services and pricing; the possibility that the

Company will not be able to perform work within budget or

contractual limitations; one or more current or future claims made

against the Company may result in substantial liabilities; the

possibility that the Company will not be able to attract and retain

key professional employees; failure to recover at-risk contract

costs; changes to or failure of the Federal, State, or local

governments to fund certain programs in which the Company

participates; changes in customer procurement policies and

practices; delays in project funding; effects of U.S. Government

conflict of interest policies; loss of anticipated new contract

vehicles either due to funding changes or competitive factors, and

such other risks and uncertainties set forth in this report and in

other reports and other documents filed by the Company from time to

time with the Securities and Exchange

Commission.

Business Overview

Versar, Inc. is a Delaware corporation incorporated in 1969. We are

a global project management company providing value-oriented

solutions to government and commercial clients in three business

segments: (1) Engineering and Construction Management (ECM); (2)

Environmental Services Group (ESG); and (3) Professional Services

Group (PSG). We also provide tailored and secure engineering

solutions in extreme environments and offer specialized abilities

in construction management, security system integration,

performance-based remediation, and hazardous materials

mangement.

Fiscal 2016 proved to be an eventful year for Versar. The year

began with the successful completion of the strategic acquisition

of a federal security integration business from Johnson Controls,

formerly known as Johnson Controls Security Systems, which is now

known as Versar Security Systems (VSS). VSS is a security systems

integrator that designs, installs and supports complex physical

security, network security, and facilities management systems

primarily for Federal Government clients such as Federal Aviation

Administration (FAA), the Food and Drug Administration (FDA),

Department of Justice (DOJ), the Federal Bureau of Investigation

(FBI) and the Federal Emergency Management Agency (FEMA). The

acquisition of VSS expanded Versar’s client base, technical

capabilities, and geographic scope.

As the year progressed, Versar faced significant challenges as

revised government procedures and other market factors resulted in

longer timelines for contract awards and project start dates than

the Company anticipated. This resulting impact on the

Company’s financial performance created constraints that

initiated covenant defaults with our lender and a related inability

to file our required securities filings in a timely manner,

resulting in additional oversight from the lender and the

Company’s related contracting of a Chief Restructuring

Officer (CRO) and exploration of financial and strategic

alternatives. The Company operated at a financial loss for fiscal

2016. In response, the Company initiated a wide range of deliberate

cost cutting measures during fiscal 2016, the results of which will

continue to be realized in future periods. We will continue to

manage our costs based on financial performance. As we adapted

internally to longer cycles in both contract award and project

start dates, we experienced a decrease in our backlog as compared

to fiscal 2015. To address this, we adjusted our bidding strategies

and teaming partnerships, diversified our capabilities, and made

strategic hires. As a service-based company, our revenue is

primarily derived from the provision of labor-based services,

rather than capital-intensive product offerings. Thus, our revenue

is driven by our ability to retain existing clients, attract new

clients, provide quality project and program management at

competitive rates, and identify and retain qualified

employees.

Business Segments

The company is aligned into three reportable segments: ECM, ESG,

and PSG, all of which are described below.

ECM

ECM’s services include facility

planning and programming, engineering design, construction,

construction management and security systems installation and

support. ECM supports federal, state and local governments, as well

as commercial clients worldwide. Our

global network of engineering and construction resources

facilitates the effective mobilization of highly skilled

construction teams and advanced methodologies around the

world.

The primary markets for ECM’s services include a broad range

of infrastructure, master planning, and engineering design for

facilities, transportation, resource management, energy, and local,

regional and international development.

Our services include:

●

Facility Condition Assessments and Space Utilization Analysis

providing Architect-Engineer studies, master planning and area

development plans, sustainability and energy audits, full

Sustainment, Restoration and Modernization (SRM) and Military

Construction (MILCON) design capabilities

●

Construction Management Services providing quality assurance

services in Title II or as owner’s representatives, providing

a legally defensible record of the construction, earned value

project management to objectively measure construction progress,

engineering and schedule analysis and negotiation of change

orders

●

Construction Services includes integrated design-build solutions

for construction, horizontal and vertical SRM projects,

construction of design-bid-build projects including all building

trades, equipment installation and furnishings as

specified

●

Security Systems planning and analysis that includes developing and

updating physical security plans, site surveys and physical

security risk assessments. Engineering and design turnkey solutions

integrating physical and electronic security systems, full

program/project documentation, and configuration management and

design control expertise.

ECM’s key

projects that contributed to the revenue include integration and

maintenance of access control and security systems for the FAA,

construction management services for the U.S. Air Force (USAF) and

U.S. Army, construction management and personal services including

engineering, construction inspection, operations and maintenance

and administrative support to the U.S. Army Corps of Engineers

(USACE) and project and construction management services for the

District of Columbia Courts and commercial customers. The largest

ECM project during fiscal 2016 was the $109.5 million firm fixed

price Design/Bid/Build runway repair task order at Dover Air Force

Base (DAFB) awarded, on August 13, 2014 under Versar’s

S/R&M Acquisition Task Order Contract (SATOC) indefinite

delivery/indefinite quantity (IDIQ) with the Air Force Civil

Engineer Center (AFCEC), held with our joint venture partner,

Johnson Controls Federal Systems. The SATOC IDIQ primarily services

Air Force customers, providing a fast track, efficient method for

execution of all types of facility repairs, renovations and

construction. During the months of December 2016 through February

2017, the work on the task order was suspended due to normal

seasonal weather conditions. Work resumed in March 2017 and the

contract is anticipated to be completed by the end of June

2017.

ESG

ESG

supports federal, state and local governments, and commercial

clients worldwide. For over 40 years, our team of engineers,

scientists, archeologists, and unexploded ordnance staff has

performed thousands of investigations, assessments, and remediation

safely and effectively. Our client-focused approach, complemented

by our regulatory expertise, provides low risk with high value in

today’s complex regulatory climate.

Our

services include:

●

Compliance

services include hazardous waste and hazardous materials management

from permitting support to compliance with applicable federal laws,

emergency response training, hazardous waste facility

decommissioning, energy planning, energy audit and assessment,

commission and metering, Energy Savings Performance Contract (ESPC)

support and Executive Order 13514/sustainability services. We are a

greenhouse gas verification body in California, one of the few

companies certified to review greenhouse gas emissions data in that

state.

●

Cultural Resources

provides clients with reliable solutions from recognized experts,

quality products that are comprehensive yet focused on client

objectives, and large-business resources with small-business

responsiveness and flexibility. ESG’s staff has set the

standard for management, methodologies, and products. Our expertise

and experience in the design and management of innovative programs

that are responsive to client needs and satisfy regulatory

requirements.

●

Natural Resources

services include protected species assessments and management,

wetland delineations and Section 404 permitting, ecosystem and

habitat restoration, and water quality monitoring, ecological

modeling, and environmental planning. Our team has extensive

expertise in developing innovative means for mitigation, managing

the complex regulatory environment, and providing our clients with

the knowledge and experience needed to meet or exceed goals and

objectives.

●

Remediation

services provides on-going federal remediation and restoration

projects, including four Air Force Performance Based Remediation

(PBR) projects operating at more than ten different locations in

nine states. Our success is based in part on the understanding that

the goal of remedial action projects is to eliminate our

clients’ long-term liability and reduce the life cycle costs

of environmental restoration.

●

UXO/MMRP provides

range sustainment services at two of the world’s largest

ranges. Our highly experience staff provide range sustainment

services, range permitting, monitoring, and deconstruction,

surface, subsurface, and underwater investigations and removals,

geophysical surveys, and anomaly avoidance and construction

support.

ESG’s key

projects that contributed to the revenue are our New England, Great

Lakes, Tinker and Front Range PBRs, Range Sustainment Services at

Nellis AFB, hydrodynamic flow modeling and sedimentation study at

Naval Submarine Base Kings Bay, shoreline stabilization projects at

Possum and Cedar Point for the Navy, an Environmental Impact

Statement (EIS) for housing privatization for the USAF, fence to

fence programs at Cannon, Holloman, Barksdale, Columbus AFBs and

Joint Base McGuire-Dix-Lakehurst, large cultural resources efforts

at Avon Park, Tyndall AFB, and Joint Base McGuire-Dix-Lakehurst,

and numerous remedial actions for the U.S. Environmental Protection

Agency (EPA).

PSG

PSG provides onsite environmental, engineering, construction

management, and logistics services to the USAF, U.S. Army, U.S.

Army Reserve, National Guard Bureau, FAA, Bureau of Land Management

(BLM), and DOJ through the Drug Enforcement Agency (DEA). Versar

provides on-site services that enhance a customer’s mission

through the use of subject matter experts who are fully dedicated

to accomplish mission objectives. These services are particularly

attractive as the federal agencies and Department of Defense (DOD)

continue to be impacted by budgetary pressures. This segment

focuses on providing onsite support to government clients to

augment their capabilities and capacities.

Our services include:

●

Facilities and operational support by delivering comprehensive

facility maintenance, life cycle management plan minimizing

operating costs, space utilization, operational

planning/forecasting, and automated planning technical support

services ensuring operational readiness of reserve forces to the

U.S. Army Reserve.

●

Versar assists the U.S. Army Reserve with assessing, improving,

obtaining, maintaining, and sustaining environmental compliance, as

well as conservation requirements, performing hazardous waste

management, spill prevention and clean-up, biological assessments,

wetland sustainment, and environmental training.

●

Environmental quality program services, to include facility and

utilities integration, National Environmental Policy Act

considerations, water program management, wildlife program

management, archaeological and historical preservation to DOD Joint

Base communities.

●

Microbiological and chemical support to the U.S. Army’s

designated Major Range and Test Facility Base for Chemical and

Biological Testing and Training.

●

Biological, archaeological, and GIS support to plan restoration

projects for wildlife habitat improvements and also field

verification of GIS-generated disturbances and related mapping

data.

●

Engineering expertise and program oversight for civil engineering

activities related to various facilities services performed at the

Air National Guard Readiness Center and National Guard

Bureau.

●

Provides the DOJ’s DEA engineering and facilities planning

support for the implementation and completion of SRM

projects.

Revenue Earned by Geographic Location

Our consolidated gross revenue for fiscal 2016 was $167.9 million,

of which approximately $165.7 million was funded with U.S. currency

and approximately $2.2 million was derived from PPS, and funded in

Pounds sterling. Approximately 11% of our fiscal 2016 revenue was

generated in international locations.

Our consolidated gross revenue for fiscal 2015 was $159.9 million,

of which approximately $154.8 million was funded with U.S. currency

and approximately $5.1 million was derived from PPS, and funded in

Pounds sterling. Approximately 18% of our fiscal 2015 revenue was

generated in international locations.

Our consolidated gross revenue for fiscal 2014 was $110.3 million,

of which approximately $107.6 million was funded with U.S. currency

and approximately $2.7 million of the remainder was derived from

PPS, and funded in Pounds sterling. Approximately 30% of our fiscal

2014 business was conducted in international

locations.

Our Strategy

In addressing fiscal 2016’s challenges, Versar remains

committed to our customers, shareholders, employees and partners.

Versar will continue to provide technical expertise to our

primarily federal customers. We will focus on international

construction management in austere environments, security

solutions, ongoing investments in military base efficiencies and

renovation, compliance and environmental remediation. To reiterate

our long-term strategy to reflect our new reality, the following

elements are driving our strategy:

1.

Re-Establish Financial Stability and Grow Shareholder Value. In the

near term, Versar will become current with our financial reporting

requirements with the NYSE MKT LLC (the Exchange) and Securities

and Exchange Commission (SEC). While we continue to seek a

long-term financial solution, we are exploring all strategic

options. We are committed to conservatively managing our resources

to ensure shareholder value and re-establish our financial

stability.

2.

Profitably execute current backlog. Our front-line project managers

and employees will continue to control costs and streamline

processes to profitably execute our current backlog. In addition,

our back-office staff will redouble efforts to support our

front-line employees efficiently and effectively serve our

customers. We are committed to innovatively transform our business

processes to be as efficient and cost-effective as

possible.

3.

Grow our pipeline. We are aggressively mining existing Indefinite

Delivery Indefinite Quantity (IDIQ) contract vehicles to increase

win rates. While we reduced back-office staff in our Business

Development division, we remain committed to growing our pipeline

and backlog by carefully managing our proposal efforts from

identification through award to maximize our business development

investments.

4.

Retain and attract the best people. Our employees are critical to

the execution of our strategy and we are committed to attracting

and retaining the employees required to achieve all the elements of

our strategy.

Competition

Government Contracting is a highly competitive industry, where

price is often the deciding factor. In that environment, it is

critical for Versar to differentiate our capabilities and offerings

to ensure that our customers understand the value of our offerings.

Versar carefully targets our business development and sales efforts

and has developed strategic partnerships to enhance our competitive

advantage.

The acquisition of VSS in fiscal 2016 expanded our customer base to

include the FAA and FEMA, among others, as well as increased our

service offerings into higher margin classified construction.

During fiscal 2017, we will position the company to expand these

new capabilities to existing customers and existing capabilities to

new customers.

Backlog

We report “funded” backlog, which represents orders for

goods and services for which we have received firm contractual

commitments. Based on its history, the Company believes that

approximately 90% of funded backlog will be performed in the

succeeding twelve to eighteen-month period following the execution

of the relevant contract. However, there can be no assurance that

we will ultimately realize our full backlog. Additionally, other

companies with similar types of contracts may not calculate backlog

in the same manner we do, as their calculations may be based on

different subjective factors or because they use a different

methodology. Therefore, information presented by us regarding

funded backlog may not necessarily be comparable to similar

presentations by others.

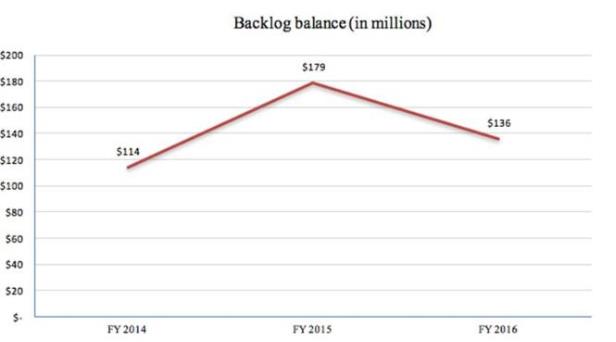

As of July 1, 2016, funded backlog was approximately $136 million,

a decrease of approximately 24% compared to approximately $179

million of funded backlog at the end of the fiscal year 2015.

Backlog for the DAFB project at the end of fiscal 2015 was $55.1

million compared to $8.6 million at the end of fiscal 2016. During

fiscal 2016, the DAFB revenue recognized was $50.2 million as

compared to $43.2 million in fiscal 2015. The Company’s

funded backlog value at fiscal 2015 was the largest in the

Company’s history primarily driven by the August 13, 2014

award of DAFB contract of $98.3 million.

Employees

At July 1, 2016, we had 529 employees, of which 75% are engineers,

scientists, and other professionals. 58% of our professional

employees have a bachelor’s degree, 38% have a master’s

degree, and 4% have a doctorate degree as their highest level of

education earned.

Item 1A. Risk Factors

Our line of credit contains, and our future

debt agreements may contain, covenants that may restrict our

ability to engage in activities that may be in our long-term best

interest, including financing future operations or capital needs or

engaging in other business activities, and that require us to

maintain specific financial ratios or levels.

Our

line of credit restricts, among other things, our ability

to:

●

incur additional

debt;

●

pay dividends or

distributions on our capital stock;

●

purchase, redeem

or retire capital stock;

●

make acquisitions

and investments;

●

create liens on

our assets;

●

enter into certain

transactions with affiliates;

●

merge or

consolidate with another company;

●

obtain or maintain

the appropriate bonding necessary to perform our work;

or

●

transfer or sell

assets outside the ordinary course of business.

In

addition, our line of credit requires that we comply with certain

consolidated Earnings Before Interest, Tax, Depreciation and

Amortization (EBITDA) financial ratios and levels,. These covenants

may adversely impact our ability to finance our future operations

or utilize the capital required to pursue available business

opportunities.

During fiscal 2016, we were in default under certain of our

financial maintenance covenants under our loan agreement, which

defaults were addressed by amendment of the loan agreement

subsequent to the end of the fiscal year; however, we are required

to repay or replace the existing facility. In the future, our

ability to fund our operations could be jeopardized if we cannot

obtain alternative sources of funding. If in the future we again

default under any future credit agreement, or if we are unable to

obtain a new facility or refinance our existing indebtedness, it

would have a material adverse impact on our financial position and

operations.

On

December 9, 2016, Versar, together with certain of its domestic

subsidiaries acting as guarantors, entered into a First Amendment

and Waiver (the Amendment) to the loan agreement (the Loan

Agreement) dated September 30, 2015 with Bank of America, N.A. (the

Lender), as the lender and letter of credit issuer for a revolving

credit facility in the amount of $25,000,000 and a term facility in

the amount $5,000,000. Under the Amendment, the Lender waived all

existing events of default, and reduced the revolving facility to

$13,000,000 from $25,000,000. The Amendment amends the Loan

Agreement to remove the consolidated Total Leverage Ratio covenant,

consolidated Senior Leverage Ratio covenant, consolidated Fixed

Charge Coverage Ratio covenant, and the consolidated Asset

Coverage Ratio covenant, and adds a covenant requiring Versar to

maintain certain minimum quarterly consolidated EBITDA amounts and

requires the Company to pursue alternative sources of funding for

its ongoing business operations and to repay or replace the Loan

Agreement.

If the

Company is not able to repay or refinance the obligations under the

Loan Agreement in accordance with the Loan Agreement requirements

or meet certain other conditions, the Lender may exercise its

rights and remedies with respect to such defaults. In such event,

the Lender could demand immediate repayment of the outstanding

borrowings and terminate the facility. The Lender could also seek

to foreclose on its security interests in our assets and those of

our subsidiaries, which would materially and negatively impact our

ability to fund our business operations. We are currently seeking

alternative sources of funding for our ongoing business operations

as needed. There can be no assurance that we will be able to obtain

alternative financing on terms acceptable to the Company, or at

all. Failure to secure alternative financing would have a material

adverse effect on the Company and its financial

condition.

The Company is taking affirmative steps to modify operational plans

and its internal organization to ensure that it can continue to

operate with its existing cash resources. The actual amount of

funds that the Company will need will be determined by many

factors, some of which are beyond its control, and the Company may

need funds sooner than currently anticipated.

The accompanying Financial Statements have been prepared assuming

the Company will continue as a going concern. If the Company is

unable to identify alternative sources of funding and raise

additional capital as needed to fund operations, due to the

Company’s negative cash flow from operations and accumulated

deficit, there would be substantial doubt about its ability to

continue as a going concern. The Financial Statements do not

include any adjustments that might result from the outcome of this

uncertainty.

We are dependent on government contracts for the majority of our

revenue, and a reduction or delay in spending by government

agencies could adversely affect our business and operating

results.

Contracts with agencies of the United States government and various

state and local governments represented approximately 90% of our

revenue in fiscal 2016, with the remaining 10% of our revenue

coming from commercial sources. Therefore, the success of our

business is materially dependent on contracts with governmental

agencies. Companies engaged in government contracting are subject

to certain unique business risks not shared by those serving the

general commercial sector. Among these risks are:

●

a competitive procurement process with no firm schedule or

guarantee of contracts being awarded;

●

competitive pricing pressure that may require cost reductions in

order to realize revenue under contracts;

●

award of work to competitors due primarily to policy

reasons;

●

dependence on congressional and state appropriations and

administrative allotment of funds;

●

policies and regulations that can be readily changed by governing

bodies;

●

competing political priorities and changes in the political climate

regarding funding and operations of the services;

●

shifts in buying practices and policy changes regarding the use of

contractors;

●

changes in and delays or cancellations of government programs or

requirements;

●

government contracts that are usually awarded for relatively short

periods of time and are subject to renewal options in favor of the

government; and

●

many contracts with U.S. government agencies require annual funding

and may be terminated in the agency’s sole

discretion.

The U.S. government’s contracting laws provide that the U.S.

government can do business only with responsible contractors.

Accordingly, U.S. government agencies have the authority under

certain circumstances to suspend or debar a contractor from bidding

on government contracts.

A reduction or shift in spending priorities by U.S. government

agencies could limit or eliminate the continued funding of our

existing government contracts or awards of new contracts or new

task orders under existing contracts. Any such reductions or shifts

in spending, if significant, could have a material adverse effect

on our business.

Inability of the legislative and executive branches of the federal

government to agree on a budget for key agencies or to enact

appropriations in a timely manner has in the past delayed, and may

in the future delay, the award of contracts. These delays, if

significant, could have a material adverse effect on our

business.

Our government contracts are subject to audit and potential

reduction of costs and fees.

Contracts with the U.S. government and many other state and local

governmental agencies are subject to auditing by governmental

agencies, which could result in the disallowance of certain costs

and expenses. These audits can result in the disallowance of

significant costs and expenses if the auditing agency determines,

in its discretion, that certain costs and expenses were

unwarranted, allowable, or were excessive. Disallowance of costs

and expenses, if pervasive or significant, could have a material

adverse effect on our business.

As a government contractor, we are subject to a number of

procurement laws and regulations, violation of which could result

in sanctions, contract termination, forfeiture of profit, harm to

our reputation or loss of our status as an eligible government

contractor.

We must comply with federal, state and local laws and regulations

regarding the formation, administration and performance of

government contracts. These laws and regulations govern how we

transact business with our government clients and, in some

instances, impose additional costs and related obligations on our

business operations. Even though we take significant precautions to

identify, prevent and deter fraud, misconduct and non-compliance,

we face the risk that our personnel or outside partners may engage

in misconduct, fraud or improper activities. Government contract

violations could result in the imposition of civil and criminal

penalties or sanctions, contract termination, forfeiture of profit

and/or suspension of payment, any of which could make us lose our

status as an eligible government contractor and could cause our

reputation to suffer serious harm. Loss of our status as an

eligible government contractor would have a material adverse effect

on our business.

Actual or perceived conflicts of interest may prevent us from being

able to bid on or perform contracts.

U.S. government agencies have conflict of interest policies that

may prevent us from bidding on or performing certain contracts.

When dealing with U.S. government agencies that have such policies,

we must decide, at times with incomplete information, whether to

participate in a particular business opportunity when doing so

could preclude us from participating in a related procurement at a

future date. We have, on occasion, declined to bid on certain

projects because of actual or perceived conflicts of interest. We

will continue to encounter such conflicts of interest in the

future, which could cause us to be unable to secure key contracts

with U.S. government customers.

Robust enforcement of environmental regulations is important to our

financial success.

Our business is materially dependent on the continued enforcement

by local, state and federal governments of various environmental

regulations. From time to time, depending on changed enforcement

priorities, local, state and federal agencies modify environmental

clean-up standards to promote economic growth and to discourage

industrial businesses from relocating. Any relaxation in

environmental and compliance standards could impact our ability to

secure additional contracting work with such agencies or with other

federal agencies that operate or manage contaminated

property.

Many of our U.S. government customers procure goods and services

through IDIQ, government wide acquisition contract (GWAC) or GSA

Schedule contracts under which we must compete for post-award

orders.

Budgetary pressures and reforms in the procurement process have

caused many U.S. government customers to purchase goods and

services through ID/IQ, GSA Schedule contracts and other multiple

award and/or GWAC contract vehicles. These contract vehicles

increase competition and pricing pressures, requiring us to make

sustained efforts following the initial contract award to obtain

ongoing awards and realize revenue. There can be no assurance that

we will increase revenue or otherwise sell successfully under these

contract vehicles. Any failure by the Company to compete

effectively in this procurement environment could harm our

business, financial condition, operating results and cash flows and

our ability to meet our financial obligations.

If we fail to recover at-risk contract costs, we may have reduced

fees or losses.

We are at risk for any costs incurred before a contract is

executed, modified or renewed. A customer may choose not to pay us

for these costs. While such costs are typically associated with

specific anticipated contracts and funding modifications, we cannot

be certain that our customers will execute these contracts or

contract renewals, or that they will pay us for all our related

at-risk costs. If any such unrecovered at-risk costs are

significant, we may experience a decline in contract margins or

experience losses on certain contracts or in certain periods,

resulting in reduced profitability. We face increased pressure on

profit margins and may need to lower margins to price projects at a

more competitive rate to win awards.

We could face potential liability for failure to properly design

remediation.

Part of our business involves the design and implementation of

remediation at environmental clean-up sites. If we fail to properly

design and build a remediation system, or if a person claims that

we did, we could face expensive litigation or regulatory

enforcement efforts and potential settlement costs. If we fail to

successfully defend against such a lawsuit, it could have a

material adverse effect on our business.

Environmental laws and regulations and our use of hazardous

materials may subject us to significant liabilities.

Our operations are subject to U.S. federal, state and local

environmental laws and regulations, as well as environmental laws

and regulations in the various countries in which we operate. We

are also subject to environmental laws and regulations relating to

the discharge, storage, treatment, handling, disposal and

remediation of regulated substances and waste products, such as

radioactive, biochemical or other hazardous materials and

explosives. We may incur substantial costs in the future because of

modifications to current laws and regulations, new laws and

regulations, new guidance or new interpretation of existing laws or

regulations, violations of environmental laws or required operating

permits, or discovery of previously unknown contamination.

Incurring such additional costs could have a material adverse

effect on our business.

Our failure to properly manage projects may result in additional

costs or claims.

Our engagements regularly involve complex and lengthy projects. The

quality of our performance on such projects depends in large part

upon our ability to manage the relationship with our clients, and

to effectively manage the projects and deploy appropriate resources

in a timely manner. If we miscalculate the resources or time

required to complete those projects with capped or fixed fees, our

operating results could be adversely affected. Further, any defects

or errors, or failures to meet our client’s expectations,

could result in claims for damages against us.

Our services expose us to significant risks of liability and it may

be difficult to obtain or maintain adequate insurance

coverage.

Our services involve significant risks of professional and other

liabilities that may exceed the fees we derive from performance.

Our business activities could expose us to potential liability

under various laws and regulations and under federal and state

workplace health and safety regulations. In addition, we sometimes

may assume liability by contract under indemnification agreements.

Given the varied nature of our many agreements, we are not able to

predict the magnitude of any such liabilities.

We obtain insurance from third party carriers to cover our

potential risks and liabilities. However, it is possible that we

may not be able to obtain adequate insurance to meet our needs, may

have to pay an excessive amount for the insurance coverage we

require, or may not be able to acquire any insurance for certain

types of business risks.

We are exposed to risks associated with operating

internationally.

A certain portion of our business is conducted internationally.

Consequently, we are subject to a variety of risks that are

specific to international operations, including the

following:

●

export regulations that could erode profit margins or restrict

exports;

●

compliance with the U.S. Foreign Corrupt Practices

Act;

●

compliance with the U.K Anti Bribery Act;

●

compliance with the anti-corruption laws of other jurisdictions in

which we operate;

●

the burden and cost of compliance with foreign laws, treaties and

technical standards and changes in those regulations;

●

contract award and funding delays;

●

potential restrictions on transfers of funds;

●

foreign currency fluctuations;

●

import and export duties and value added taxes;

●

transportation delays and interruptions;

●

uncertainties arising from foreign local business practices and

cultural considerations; and

●

potential military conflicts, civil strife and political

risks.

While we have and will continue to adopt and implement aggressive

measures to reduce the potential impact of losses resulting from

the risks of our foreign business, we cannot ensure that such

measures will be adequate.

Political destabilization or insurgency in the regions in which we

operate may have a material adverse effect on our

business.

Certain regions in which we operate are highly politically

unstable. Insurgent activities in the areas in which we operate may

cause further destabilization in these regions. There can be no

assurance that the regions in which we operate will continue to be

stable enough to allow us to operate profitably or at all. We are

required to increase compensation to our personnel as an incentive

to deploy them to many of these regions. To date, we have been able

to recover such costs under our contracts, but we may not be able

to do so in the future. To the extent that we are unable to

transfer such increased costs to our customers, our operating

margins would be adversely impacted, which could adversely affect

our operating performance. In addition, increased insurgent

activities or destabilization, including civil unrest or a civil

war in Iraq or Afghanistan, may lead to a determination by the U.S.

government to halt our operations in a particular location, country

or region and to perform the services that we provide using

military personnel.

If our partners fail to perform their contractual obligations on a

project, we could be exposed to legal liability, loss of reputation

or reduced profits.

From time to time, we enter into joint venture and other

contractual arrangements with partners to jointly bid on and

execute certain projects. The success of these joint projects

depends in part on the satisfactory performance of the contractual

obligations by our partners. If any of our partners fail to satisfy

their contractual obligations, we may be required to make

additional investments and provide additional services to complete

projects, increasing our cost on such projects. If we are unable to

adequately address a partner’s performance issues, then our

client could terminate the joint project, exposing us to legal

liability, loss of reputation or reduced profits.

We operate in highly competitive industries.

The markets for many of our services are highly competitive. There

are numerous professional architectural, engineering, construction

management, and environmental consulting firms, and other

organizations that offer many of the same services offered by us.

We compete with many companies that have greater resources than us

and we cannot provide assurance that such competitors will not

substantially increase the resources they devote to those

businesses that compete directly with our services. Competitive

factors considered by clients include reputation, performance,

price, geographic location and availability of technically skilled

personnel. In addition, we face competition from the use by our

clients of in-house environmental, engineering and other

staff.

Our long-term growth strategy includes acquisitions of other

businesses, which may require us to incur costs and liabilities or

have other unexpected consequences which may adversely affect our

operating results and financial condition.

Like other companies with similar growth strategies, we may be

unable to successfully implement our growth strategy, as we may be

unable to identify suitable acquisition candidates, obtain

acceptable financing, or consummate any future acquisitions. We

frequently engage in evaluations of potential acquisitions and

negotiations for possible acquisitions, certain of which, if

consummated, could significantly enhance the Company’s

competitive position. Although it is our general objective only to

acquire those companies which will be accretive to both earnings

and cash flow, any potential acquisitions may result in material

transaction expenses, increased interest and amortization expense,

increased depreciation expense and increased operating expense, any

of which could have a material adverse effect on our operating

results. Acquisitions will require integration and management of

the acquired businesses to realize economies of scale and control

costs. In addition, acquisitions may involve other risks, including

diversion of management resources otherwise available for ongoing

development of our business and risks associated with entering new

markets. Future acquisitions may also result in potential dilution

of the Company’s securities. Consummation of acquisitions may

subject the Company to unanticipated business uncertainties or

legal liabilities relating to those acquired businesses for which

the sellers of the acquired businesses may not fully indemnify us.

We may not realize the full anticipated benefit of any acquired

business that has operated as a small business (as determined by

the Small Business Administration based upon the North American

Industry Classification Systems) if following their acquisition by

us certain of their contracts are revoked or not renewed because

they fail to continue to maintain small business

status.

An economic

downturn may have a material

adverse effect on our business.

In an economic recession, or under other adverse macroeconomic

conditions that may arise from natural or man-made events,

customers and vendors may be less likely to meet contractual terms

and payment or delivery obligations. In particular, if the U.S.

government changes its operational priorities in Iraq and/or

Afghanistan, reduces the DOD Operations and Maintenance budget, or

reduces funding for Department of State initiatives in which we

participate, our business, financial condition and results of

operations could be severely affected.

Our quarterly and annual revenue, expenses and operating results

may fluctuate significantly, which could have a negative effect on

the price of our common stock.

Our quarterly and annual revenues, expenses and operating results

have and may continue to fluctuate significantly because of a

number of factors, including:

●

the seasonality of the spending cycle of our public sector clients,

notably the U.S. government, and the spending patterns of our

private sector clients;

●

the hiring and utilization rates of employees in the United States

and internationally;

●

the number and significance of client engagements commenced and

completed during the period;

●

the delays incurred in connection with an engagement because of

weather or other factors;

●

the ability to work within foreign countries’ regulations,

tax requirements and obligations;

●

the business, financial, and security risks related to working in

foreign countries;

●

the ability of clients to terminate engagements without

penalties;

●

the creditworthiness and solvency of clients;

●

the size and scope of engagements;

●

the delay in federal, state and local government

procurements;

●

the ability to perform contracts within budget or contractual

limitations;

●

the timing of expenses incurred for corporate

initiatives;

●

any threatened or pending litigation or other regulatory

enforcement matters;

●

periodic reductions in the prices of services offered by our

competitors;

●

the likelihood of winning the re-bids of our existing large

government contracts;

●

the general economic and political conditions;

●

the loss of a major contract or the shutdown of a major

program;

●

the volatility of currencies in foreign countries; and

●

our ability to integrate any acquisition or the ability of an

acquired business to continue to perform as expected.

Variations in any of these factors could cause significant

fluctuations in our operating results from quarter to quarter and

could result in net losses and have a material adverse effect on

our stock price.

We are highly dependent on key personnel and our business could

suffer if we fail to continue to attract, train and retain skilled

employees.

Our business is managed by a number of key management and operating

professional personnel. The loss of key personnel could have a

material adverse effect on our business.

Availability of highly trained and skilled professional,

administrative and technical personnel is critical to our future

growth and profitability. Even in the current economic climate,

competition in our industry for scientists, engineers, technicians,

management and professional personnel is intense and competitors

aggressively recruit key employees. Competition for experienced

personnel, particularly in highly specialized areas, has

occasionally made it more difficult for us to timely meet all our

staffing needs. We cannot be certain that we will be able to

continue to attract and retain required staff. Any failure to do so

could have a material adverse effect on our business, financial

condition, operating results and our ability to meet our financial

obligations. Failure to recruit and retain a sufficient number of

such employees could adversely affect our ability to maintain or

grow our business. Some of our contracts require us to staff a

program with personnel that the customer considers key to

successful performance. If we cannot provide such personnel or

acceptable substitutes, the customer may terminate the contract,

and we may be unable to recover our costs.

In order to succeed, we will have to keep up with a variety of

rapidly changing technologies. Various factors could affect our

ability to keep pace with these changes.

Our success will largely depend on our ability to keep pace with

changing technologies that can occur rapidly in our core business

segments. We may incur significant expenses updating our

technologies, which could have a material adverse effect on our

margins and results of operations. Even if we keep up with the

latest developments and available technology, newer services or

technologies could negatively affect our business.

Our employees may engage in misconduct or other improper

activities, which could harm our business.

Like all companies, we face the risk of employee fraud or other

misconduct. Employee misconduct could include intentional failures

to comply with U.S. government procurement regulations,

unauthorized activities, attempts to obtain reimbursement for

improper expenses, or submission of falsified time records.

Employee misconduct could also involve improper use of our

customers’ sensitive or classified information, which could

result in regulatory sanctions against us. Negative press reports

regarding employee misconduct could harm our reputation with the

government agencies for which we work. If our reputation with these

agencies is negatively affected, or if we are suspended or debarred

from contracting with government agencies for any reason, our

future revenues and growth prospects would be adversely affected.

It is not always possible to deter employee misconduct, and the

precautions we take to prevent and detect this activity may not be

effective in controlling unknown or unmanaged risks or losses,

which could harm our business, financial condition, operating

results and our ability to meet our financial

obligations.

Internal system or service failures could disrupt our business and

impair our ability to effectively provide our services and products

to our customers, which could damage our reputation and adversely

affect our revenue, profitability and operating

results.

Our information technology systems are

subject to systems failures, including network, software or

hardware failures, whether caused by us, third-party service

providers, cyber intruders or hackers, computer viruses, attacks on

our computers systems, phishing attacks, natural disasters, power

shortages or terrorist attacks. Any such failures or cyber-threat

could cause loss of data and interruptions or delays in our

business processes, cause us to incur remediation costs, subject us

to claims and damage our reputation. Failure or disruption of our

communications or utilities could cause us to interrupt or suspend

our operations or otherwise adversely affect our business. Any

system or service disruptions if not anticipated and appropriately

mitigated could have a material adverse effect on our business

including, among other things, an adverse effect on our ability to

bill our customers for work performed on our contracts, collect the

amounts that have been billed and produce accurate financial

statements in a timely manner. Our property and business

interruption insurance may be inadequate to compensate us for all

losses that may occur as a result of any system or operational

failure or disruption and, as a result, our results of operations

could be materially and adversely affected. Versar has invested in and implemented

systems that will allow it to achieve and remain in compliance with

the regulations governing its business; however, there can be no

assurance that such systems will be effective at achieving and

maintaining compliance or that we will not incur additional costs

in order to make such systems effective.

We have submitted claims to clients for work we performed beyond

the initial scope of some of our contracts. If these clients do not

approve these claims, our results of operations could be adversely

impacted.

We typically have pending claims submitted under some of our

contracts for payment of work performed beyond the initial

contractual requirements for which we have already recorded

revenue. In general, we cannot guarantee that such claims will be

approved in whole, in part, or at all. If these claims are not

approved, our revenue may be reduced in future

periods.

An impairment charge of goodwill could have a material adverse

impact on our financial condition and results of

operations.

Because we have grown in part through acquisitions, goodwill

and intangible assets-net represent a substantial portion of our

assets. Goodwill and intangible assets-net were $7.2 million as of

July 1, 2016. Under accounting principles generally accepted in the

United States, we are required to test goodwill carried in our

Consolidated Balance Sheets for possible impairment on an annual

basis based upon a fair value approach and whenever events occur

that indicate impairment could exist. These events or circumstances

could include a significant change in the business climate,

including a significant sustained decline in a reporting unit's

market value, legal factors, operating performance indicators,

competition, sale or disposition of a significant portion of our

business, a significant sustained decline in our market

capitalization and other factors. In connection with our annual

goodwill impairment testing for fiscal 2016, we recorded impairment

charges of $20.3 million related to goodwill and $3.8 million

related to intangible assets due to market conditions and business

trends within the ECM, ESG, and PSG reporting units.

Maintaining adequate bonding capacity is necessary for us to

successfully bid on and win fixed-price contracts. Failing to

maintain adequate bonding capacity could have a material adverse

impact on our ability to pursue new construction services

contracts.

In line with industry practice, we are often required to provide

bid, performance or payment bonds to clients under certain

fixed-price contracts. These bonds indemnify the

customer should we fail to perform our obligations under the

relevant contract. If a bond is required for a

particular project and we are unable to obtain an appropriate bond,

we cannot pursue that project. We have bonding capacity

but, as is typically the case, the issuance of a bond is at the

surety’s sole discretion. Moreover, due to events

that affect the insurance and bonding markets generally, bonding

may be more difficult to obtain in the future or may only be

available at significantly higher costs. There can be no

assurance that our bonding capacity will continue to be available

to us on reasonable terms. Our inability to obtain

adequate bonding and, as a result, to bid on new fixed-price

contracts could have a material adverse effect on our business,

financial condition, results of operations and cash

flows.

Our operating margins may decline under our fixed-price contracts

if we fail to estimate accurately the time and resources necessary

to satisfy our obligations.

Some of our contracts are fixed-price contracts, under which we

bear the risk of any cost overruns. Our profits are adversely

affected if our costs under these contracts exceed the assumptions

that we used in bidding for the contract. Often, we are required to

fix the price for a contract before we finalize the project

specifications, increasing the risk that we may misprice these

contracts. The complexity of many of our engagements makes

accurately estimating our time and resources more difficult. In the

event we fail to estimate our time and resources accurately, our

expenses will increase and our profitability, if any, under such

contracts will decrease.

Item 2. Properties

Our corporate executive office is located in Springfield, Virginia,

which is a suburb of Washington, D.C. Versar currently leases

40,507 square feet from Springfield Realty Investors, LLC. The rent

is subject to a two percent escalation per year through December

31, 2021.

As of July 1, 2016, we had under lease an

aggregate of approximately 213,000 square feet of office and manufacturing

space in the following locations (parenthetical reference of

business segments using space): Dulles (ECM), Springfield (all

segments), Hampton, VA (ESG); Chandler, AZ (ESG); Westminster, CO

(all segments); Atlanta, GA (ESG and PSG); Aiea, HI (ECM); Boise,

ID (ESG); Columbia (ESG), and Germantown, MD (ECM and ESG);

Charleston, SC (ESG); San Antonio and El Paso, TX (ESG); Clark Air

Force Base, the Republic of Philippines (ECM); Milton Keynes, U.K.

(ECM); and Abu Dhabi (ECM and ESG), United Arab Emirates. The lease

terms primarily range from two to six years.

Item 3. Legal Proceedings

Versar and its subsidiaries are parties from time to time to

various legal actions arising in the normal course of business. We

believe that any ultimate unfavorable resolution of any current

ongoing legal actions will not have a material adverse effect on

its consolidated financial condition and results of

operations.

PART II

Item 5. Market for Registrant’s Common Equity, Related

Stockholder Matters and Issuer Purchases of Equity Securities

Common Stock

Our common stock is traded on the NYSE MKT under the symbol VSR. At

March 1, 2017, the Company had 825 stockholders of record,

excluding stockholders whose shares were held in nominee name. The

quarterly high and low sales prices as reported on the NYSE MKT

during fiscal years 2016 and 2015 are presented below.

|

Fiscal Year 2017

|

High

|

Low

|

|

2nd Quarter

|

1.56

|

1.19

|

|

1st Quarter

|

1.87

|

1.15

|

|

|

|

|

|

Fiscal Year 2016

|

High

|

Low

|

|

4th Quarter

|

3.25

|

1.01

|

|

3rd Quarter

|

3.07

|

1.93

|

|

2nd Quarter

|

3.55

|

2.67

|

|

1st Quarter

|

4.38

|

2.86

|

|

|

|

|

|

Fiscal Year 2015

|

High

|

Low

|

|

4th Quarter

|

4.45

|

3.06

|

|

3rd Quarter

|

3.60

|

2.96

|

|

2nd Quarter

|

7.84

|

2.69

|

|

1st Quarter

|

4.10

|

3.06

|

No cash dividends have been paid by Versar since it began public

trading of its stock in 1986. The Board of Directors intends to

retain any future earnings for use in our business and does not

anticipate paying cash dividends in the foreseeable future. Under

the terms of our revolving line of credit, approval would be

required from our Lender for the payment of any dividends. We have

established equity compensation plans to attract, motivate and

reward good performance of high caliber employees, directors and

service providers serving Versar and its affiliates. Currently,

there is one stock incentive plan, which was previously approved by

the stockholders: the 2010 Stock Incentive Plan. We do not maintain

any equity compensation plans not approved by our stockholders.

Through July 1, 2016, 551,369 restricted stock units have been

granted under this plan.

Equity Compensation Plan Information

|

|

|

|

|

|

|

Number of securities

|

|

|

|

|

|

|

|

remaining available for

|

|

|

|

Number of Securities

|

|

|

|

future issuance under

|

|

|

|

to be issued upon

|

|

Weighted-average

|

|

equity compensation

|

|

|

|

exercise of

|

|

exercise price of

|

|

plans, excluding

|

|

|

|

outstanding options,

|

|

outstanding options,

|

|

securities reflected in

|

|

|

|

warrants and rights

|

|

warrants and rights

|

|

column (a)

|

|

Plan Category

|

|

(a)

|

|

(b)

|

|

(c)

|

|

Equity compensation plans approved by security holders

|

|

-

|

|

-

|

|

539,935

|

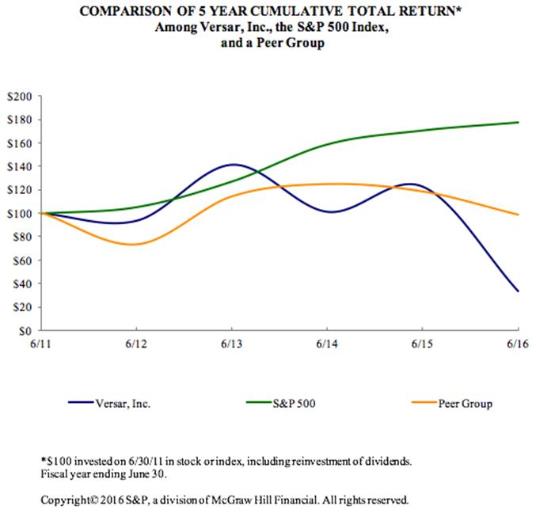

The graph below matches Versar, Inc.'s cumulative 5-Year total

shareholder return on common stock with the cumulative total

returns of (i) the S&P 500 index and (ii) a customized peer

group of five companies comprised of AECOM Technology Corp.,

Arcadis, NV, Ecology & Environment Inc., TRC Companies Inc. and

URS Corp. The graph tracks the performance of a $100 investment in

our common stock, in each of the peer groups, and the index (with

the reinvestment of all dividends) from 6/30/2011 to

6/30/2016.

The stock price performance included in this graph is not

necessarily indicative of future stock price

performance.

Item 7. Management’s Discussion and Analysis of Financial

Condition and Results of Operations

The following discussion and analysis of our financial condition

and results of operations is provided to enhance the understanding

of, and should be read together with, our consolidated financial

statements and the notes to those statements that appear elsewhere

in this Annual Report on Form 10-K. This discussion contains

forward-looking statements that involve risks and uncertainties.

Unless otherwise specifically noted, all years refer to our fiscal

years which ended on July 1, 2016, June 26, 2015 and June 27,

2014.

Financial Trends

Our business performance is affected by the overall level of U.S.

Government spending and the alignment of our offerings and

capabilities with the budget priorities of the U.S. Government.

Adverse changes in fiscal and economic conditions, such as the

manner in which spending reductions are implemented, including

sequestration, future government shutdowns, and issues related to

the nation’s debt ceiling, could have a material adverse

effect on our business.

In this challenging economic environment, our focus is on those

opportunities where the U.S. Government continues funding and which

clearly align with Versar’s capabilities. These opportunities

include construction management, security system integration,

performance-based remediation, and hazardous materials management.

We also continue to focus on areas that we believe offer attractive

enough returns to our clients, such as construction type services

both in the U. S. and internationally, improvements in energy

efficiency, and assisting with facility upgrades. We continue to

see a decline in some of our PSG contract positions largely due to

the continued shift to more contract solicitations being targeted

to small business and similar such programs. If we are unable to

seek new ways to develop our relationships with firms qualified for

these programs to increase our ability to capture more of this work

and maintain current projects this may result in a material impact

of future periods. Overall, our pipeline remains robust, but longer

timelines for contract awards and project start dates have slowed

the transition from pipeline to backlog and then to revenue

generating projects.

We believe that Versar has the expertise to identify and respond to

the challenges raised by the issues we face and that we are

positioned in the coming year to address these concerns. Our

business operates through the following three business segments:

ECM, ESG, and PSG. These segments are segregated based on the

nature of the work, business processes, customer bases and the

business environment in which each of the segments

operates.

The initial award for the DAFB project was $98.3 million. Seven

modifications have raised the contract ceiling to $109.5 million.

DAFB project contributed $50.2 million of revenue for fiscal 2016

as compared to $43.2 million for fiscal 2015, an increase of $6.9

million. Versar is the prime contractor on the DAFB project, with a

significant portion of the work performed by sub-contractors,

resulting in positive smaller gross margin on the project than our

self-performing projects. During January 2017, the DAFB customer,

issued the Company a Notice of Forbearance stating we had not met

our contractual obligation to complete the DAFB project by December

31, 2016. We submitted several change order requests to the DAFB

customer during fiscal 2016, which are still pending resolution.

The requested change orders impacted our timeline for completion of

the project, and were outside the original scope of services to be

performed, but did not impact the project’s profitability. We

continue to work and perform tasks on the DAFB project, while under

the Notice of Forbearance, in order to deliver the completed runway

project as soon as possible. We anticipate the acceptance of the

change orders and resolution of the construction related issues by

the DAFB customer that will resolve the current Notice of

Forbearance and allow the Company to complete the construction

project by June 28, 2017.

There are risk factors or uncertainties that could significantly

impact our future financial performance. A sample of these risks is

listed below. For a complete discussion of these risk factors and

uncertainties, refer to Item 1A. Risk Factors, herein.

Factors

Affecting Fiscal 2016 Performance

During fiscal 2016, the Company recognized many onetime project

losses and charges to our Income Statement and Balance Sheet as

follows:

Loss Contingency Accruals in the ESG Segment

In June 2016, a class action lawsuit was filed against the Company

by former employees alleging violations of several provisions of

California’s labor law relating to paid lunch time and breaks

for the years 2012 through 2015. The Company has reviewed the

supporting files and documentation regarding this notice and has

engaged outside counsel with experience with these matters to

assist the Company in the defense of this matter. Given that this

matter is in a very early stage it is difficult to predict the

likely outcome; however, management has determined a reasonably

possible loss in a range of $0.5 to $1.0 million, including the

expenses of outside counsel. The Company performed an initial

financial review of the number of employees, days worked, and hours

per day worked by employees on this project over the course of the

years noted in the lawsuit. As a result of this analysis, the

Company has recorded a loss contingency accrual of $0.5 million

related to this event. On October 11, 2016, the mediation resulted

in a Confidential Memorandum Of Understanding (MOU) for settlement

of this claim. The estimated contingency accrual of $0.5 million

remains consistent with this MOU.

In May 2016, during a routine audit by the General Services

Administration (“GSA”) concerning authorized GSA

schedule rates compared to the invoicing of a federal customer, the

GSA discovered that the Company had been charging its customer

several billing rates that were not supported by the contractual

listed billing rates for the fiscal 2015 and 2016. The outcome of

this audit finding has not yet been resolved. The Company has

performed a preliminary financial analysis of the number of

employees working, labor categories billed to the customer, the

contractual billing rates that should have been billed, days

worked, and hours per day worked on this project over the course of

the years noted in the audit finding. This preliminary analysis is

the basis for the Company’s probable loss and provided the

basis for the accrual made. Therefore, the Company determined the

audit finding to be estimateable and recorded a loss contingency

accrual of $0.3 million related to this event during the fiscal

year ended July 1, 2016. Subsequently, the outstanding audit

issues were resolved and the Company made a payment of $0.3 million

to the GSA in November 2016.

During April 2016, a project under one of

the Company’s PBR Task Orders involving a ground water

extraction well system at a site in Ohio failing

to meet minimum performance

requirements required rehabilitation/replacement. This work was

completed under the Company’s 2009 United States Air Force

Worldwide Environmental Restoration and Construction contract with

the Air Force Civil Engineer Center (“AFCEC”). This

extraction well system failure was not included in the

Company’s original budget for the performance of this

work. In accordance with the performance basis of our

contract with the customer, the Company must repair and or replace

all equipment located on the site that fails to meet performance

requirements. The Company has performed a review of the materials

and labor required to rehabilitate or replace the extraction well

system and used this review as the basis of the estimate for the

accrual. The Company recorded a loss contingency accrual of $0.3

million to rehabilitate or replace the extraction well system. The

corrective action will occur during the first three quarters of

fiscal 2017.

Lease Loss Accruals

In March 2016, the Company abandoned its field office facilities in

Charleston, SC and Lynchburg, VA, both within the ESG segment.

Although the Company remains obligated under the terms of these

leases for the rent and other costs associated with these leases,

the Company decided to cease using these spaces effective April 1,

2016, and does not plan to occupy them in the future. Therefore,

the Company recorded a charge to selling, general and

administrative expenses of approximately $0.4 million to recognize

the costs of exiting these spaces. This liability is equal to the

total amount of rent and other direct costs for the period of time

that the space is expected to remain unoccupied. In addition, this

liability includes, the present value of the amount by which the

rent paid by the Company to the landlord exceeds any rent paid to