Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - Consolidated Water Co. Ltd. | v461442_ex31-1.htm |

| EX-32.2 - EXHIBIT 32.2 - Consolidated Water Co. Ltd. | v461442_ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Consolidated Water Co. Ltd. | v461442_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Consolidated Water Co. Ltd. | v461442_ex31-2.htm |

| EX-23.2 - EXHIBIT 23.2 - Consolidated Water Co. Ltd. | v461442_ex23-2.htm |

| EX-23.1 - EXHIBIT 23.1 - Consolidated Water Co. Ltd. | v461442_ex23-1.htm |

| EX-21.1 - EXHIBIT 21.1 - Consolidated Water Co. Ltd. | v461442_ex21-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transaction period from __________________ to __________________

Commission File Number: 0-25248

CONSOLIDATED WATER CO. LTD.

(Exact name of Registrant as specified in its charter)

| CAYMAN ISLANDS | 98-0619652 | |

| (State or other jurisdiction of | (I.R.S. Employer Identification No.) | |

| incorporation or organization) | ||

| Regatta Office Park | ||

| Windward Three, 4th Floor, West Bay Road | ||

| P.O. Box 1114 | ||

| Grand Cayman, KY1-1102, Cayman Islands | N/A | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s Telephone number, including area code: (345) 945-4277

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | Name of each exchange on which registered: | |

| Common Stock, $0.60 Par Value | The NASDAQ Stock Market LLC (NASDAQ Global Select Market) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Sec. 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this 10-K or any amendments to this Form 10-K. [Not Applicable]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

The aggregate market value of common stock held by non-affiliates of the registrant, based on the closing sales price for the registrant’s common shares, as reported on the NASDAQ Global Select Market on June 30, 2016, was $187,204,652.

As of March 10, 2017, 14,871,664 shares of the registrant’s common shares were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the registrant’s Proxy Statement related to its Annual Shareholders’ Meeting will be subsequently filed with the Securities and Exchange Commission as to Part III of this Form 10-K.

TABLE OF CONTENTS

2

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including but not limited to, statements regarding our future revenues, future plans, objectives, expectations and events, assumptions and estimates. Forward-looking statements can be identified by use of the words or phrases “will,” “will likely result,” “are expected to,” “will continue,” “estimate,” “project,” “potential,” “believe,” “plan,” “anticipate,” “expect,” “intend,” or similar expressions and variations of such words. Statements that are not historical facts are based on our current expectations, beliefs, assumptions, estimates, forecasts and projections for our business and the industry and markets related to our business.

The forward-looking statements contained in this report are not guarantees of future performance and involve certain risks, uncertainties and assumptions which are difficult to predict. Actual outcomes and results may differ materially from what is expressed in such forward-looking statements. Important factors which may affect these actual outcomes and results include, without limitation:

| · | tourism and weather conditions in the areas we serve; |

| · | the economies of the U.S. and other countries in which we conduct business; |

| · | our relationships with the governments we serve; |

| · | regulatory matters, including resolution of the negotiations for the renewal of our retail license on Grand Cayman; |

| · | our ability to successfully enter new markets, including Mexico and the United States; and |

| · | other factors, including those “Risk Factors” set forth under Part I, Item 1A. “Risk Factors” in this Annual Report. |

The forward-looking statements in this Annual Report speak as of its date. We expressly disclaim any obligation or undertaking to update or revise any forward-looking statement contained in this Annual Report to reflect any change in our expectations with regard thereto or any change in events, conditions or circumstances on which any forward-looking statement is based, except as may be required by law.

References herein to “we,” “our,” “ours” and “us” refer to Consolidated Water Co. Ltd. and its subsidiaries.

Note Regarding Currency and Exchange Rates

Unless otherwise indicated, all references to “$” or “US$” are to United States dollars.

The exchange rate for conversion of Cayman Island dollars (CI$) into US$, as determined by the Cayman Islands Monetary Authority, has been fixed since April 1974 at US$1.20 per CI$1.00.

The exchange rate for conversion of Belize dollars (BZE$) into US$, as determined by the Central Bank of Belize, has been fixed since 1976 at US $0.50 per BZE$1.00.

The exchange rate for conversion of Bahamas dollars (B$) into US$, as determined by the Central Bank of The Bahamas, has been fixed since 1973 at US$1.00 per B$1.00.

The official currency of the British Virgin Islands is the United States dollar.

Our Netherlands subsidiary conducts business in US$ and euros, our Indonesian subsidiary conducts business in US$ and Indonesian rupiahs, and our Mexico subsidiary conducts business in US$ and Mexican pesos. The exchange rates for conversion of euros, rupiahs and Mexican pesos into US$ vary based upon market conditions.

3

| ITEM 1. | BUSINESS |

Overview

We develop and operate seawater desalination plants (that utilize reverse osmosis technology) and water distribution systems in areas where naturally occurring supplies of potable water are scarce or nonexistent. Through our subsidiaries and affiliates, we provide the following services to our customers in the Cayman Islands, The Bahamas, Belize, the British Virgin Islands and Indonesia:

| · | Retail Water Operations. We produce and supply water to end-users, including residential, commercial and government customers in the Cayman Islands under an exclusive retail license issued by the Cayman Islands government to provide water in two of the three most populated and rapidly developing areas on Grand Cayman Island. We also have a desalination plant in Bali, Indonesia that sells water to resort and residential properties. In 2016, our retail water operations generated approximately 41% of our consolidated revenues. Substantially all of our retail revenues were generated by our Grand Cayman operations. |

| · | Bulk Water Operations. We produce and supply water to government-owned distributors in the Cayman Islands, Belize and the Bahamas. In 2016, our bulk water operations generated approximately 51% of our consolidated revenues. |

| · | Services Operations. We provide design, engineering, construction and management services for desalination plants and projects. We manufacture and service a wide range of water-related products and provide design, engineering, construction, management and other services for commercial and municipal water production, water supply and treatment, and industrial water and wastewater treatment. In 2016, our services operations generated approximately 8% of our consolidated revenues. |

| · | Affiliate Operations. We own 50% of the voting rights and 43.53% of the equity rights of Ocean Conversion (BVI) Ltd., which produces and supplies bulk water to the British Virgin Islands Water and Sewerage Department. |

As of December 31, 2016, the number of plants we, or our affiliates, operated in each country and the production capacities of these plants are as follows:

| (1) | In millions of gallons per day. |

| Location | Plants | Capacity(1) | ||||||

| Cayman Islands | 6 | 8.9 | ||||||

| Bahamas | 3 | 15.2 | ||||||

| Belize | 1 | 0.6 | ||||||

| British Virgin Islands | 2 | 0.8 | ||||||

| Bali | 1 | 0.8 | ||||||

| Total | 13 | 26.3 | ||||||

| (1) | In millions of gallons per day. |

Strategy

Our strategy is to provide water services in areas where (i) the supply of potable water is scarce and (ii) the production of potable water by reverse osmosis desalination is, or will be, economically viable for customers in those areas. We also seek to complement this primary strategy with other products and services relevant to desalination, water production and water treatment. We focus primarily on markets with the following characteristics:

| · | inadequate sources of potable water. |

| · | favorable regulatory and tax environments. |

| · | a large proportion of tourist properties (which historically have generated higher volume sales than residential properties). |

| · | growing populations and economies. |

4

We believe that our potential market includes any location with a demand for, but a limited supply of, potable water and that has access to seawater. The desalination of seawater is the most widely used process for producing potable water in areas with an insufficient natural supply. In addition, in many locations, desalination is the only commercially viable means to expand the existing water supply. We believe that our experience in the development and operation of reverse osmosis desalination plants provides us with the capabilities to successfully expand our operations beyond our existing markets and we expect to do so in the coming years.

Key elements of our strategy include:

| · | Expanding our existing operations in the Cayman Islands, The Bahamas and Belize. We plan to continue to seek new water supply agreements and licenses, renewing our existing supply agreements, and increasing our production levels in our existing markets. |

| · | Penetrating new markets. We plan to continue to seek opportunities to profitably expand our operations into new markets that have significant unfulfilled demands for potable water. These markets include the rest of the Caribbean, Mexico, Asia, the United States and any other areas where we can provide water on a profitable basis and in favorable regulatory environments. We may pursue these opportunities either on our own or through joint ventures and strategic alliances. |

| · | Broadening our existing and future operations with complementary products and services. We consider opportunities to leverage our water-related expertise to enter complementary industries as viable complements to our existing business and will pursue such opportunities as they arise. We may pursue these opportunities either on our own or through joint ventures, strategic alliances and/or acquisitions. Consistent with this strategy, in February 2016, we acquired 51% of the ownership of Aerex Industries, Inc., a U.S. original equipment manufacturer and service provider of a wide range of products and services applicable to desalination as well as commercial and municipal water production, water supply and treatment, and industrial water and wastewater treatment. |

5

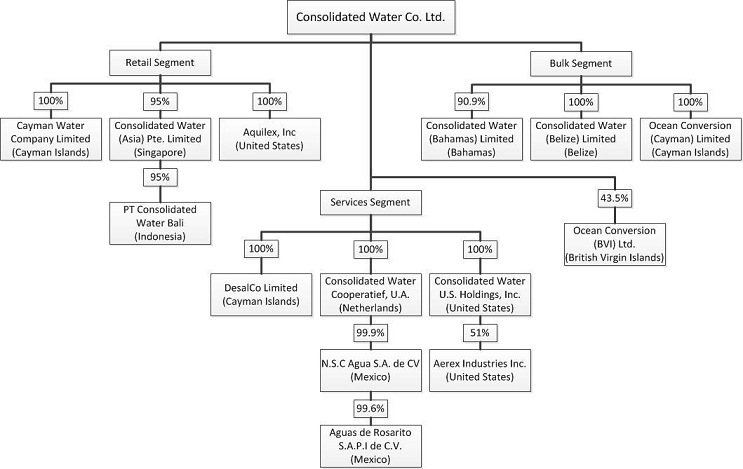

Our Company

We conduct our operations in the Cayman Islands, The Bahamas, Belize, the British Virgin Islands, Mexico, the United States and Indonesia through our subsidiaries and our affiliate, as detailed below.

Retail segment

Cayman Water Company Limited (“Cayman Water”). Cayman Water operates under an exclusive retail license granted by the Cayman Islands government to provide water to customers within a prescribed service area on Grand Cayman that includes the Seven Mile Beach and West Bay areas, two of the three most populated areas in the Cayman Islands. Cayman Water owns and operates three desalination plants and is the only non-government owned public water utility on Grand Cayman.

Consolidated Water (Asia) Pte. Limited (“CW-Asia”) and PT Consolidated Water Bali (“CW-Bali”). We own 95% of CW-Asia, a Singapore company, which owns 95% of CW-Bali, an Indonesian company. CW-Bali owns and operates a desalination plant with a capacity of 790,000 gallons per day that provides water to resort and residential properties in the Nusa Dua area of Bali, Indonesia.

Aquilex, Inc. (“Aquilex”). Aquilex, a United States company, provides financial, engineering, information technology, administrative and supply chain management support services to our subsidiaries and affiliate. We include Aquilex in our retail segment for financial reporting purposes; however it provides services to all three of our business segments.

Bulk segment

Consolidated Water (Bahamas) Limited (“CW-Bahamas”). We own approximately 90.9% equity interest in CW-Bahamas, which provides bulk water under long-term contracts to the Water and Sewerage Corporation of The Bahamas, a government agency. CW-Bahamas owns and operates our largest desalination plant and two other desalination plants.

Consolidated Water (Belize) Limited (“CW-Belize”). CW-Belize owns and operates one desalination plant and has an exclusive contract to provide bulk water to Belize Water Services Ltd., a water distributor that serves residential, commercial and tourist properties in Ambergris Caye, Belize.

Ocean Conversion (Cayman) Limited (“OC-Cayman”). OC-Cayman provides bulk water under licenses and agreements to the Water Authority-Cayman, a government-owned utility and regulatory agency, which distributes the water to properties located outside our exclusive retail license service area in Grand Cayman. OC-Cayman operates three desalination plants owned by the Water Authority-Cayman.

6

Services segment

DesalCo Limited (“DesalCo”). A Cayman Islands company, DesalCo provides management, engineering and construction services for desalination projects as well as management and engineering services relating to municipal water distribution and treatment.

Consolidated Water Cooperatief, U.A. (“CW-Cooperatief”), N.S.C. Agua, S.A. de C.V. (“NSC”) and Aguas de Rosarito S.A.P.I. de C.V. (“AdR”). CW-Cooperatief is a wholly-owned Netherlands subsidiary organized in 2010. CW-Cooperatief owns a 99.9% interest in NSC, a Mexican company. NSC was formed to pursue a project encompassing the design, construction, ownership and operation of a 100 million gallon per day seawater reverse osmosis desalination plant to be located in northern Baja California, Mexico and accompanying pipeline to deliver water to the Mexican potable water system. This project is currently in the development stage and NSC does not generate any operating revenues. In August 2016, NSC and another party incorporated AdR, a special purpose Mexican company that will ultimately own the Baja California project if it proceeds. NSC presently owns 99.6% of AdR.

Consolidated Water U.S. Holdings, Inc. (“CW-Holdings”) and Aerex Industries, Inc. (“Aerex”). On February 11, 2016, we purchased, through a newly formed wholly-owned U.S. subsidiary (CW-Holdings), a 51% interest in Aerex, a U.S. company located in Fort Pierce, Florida. Aerex is an original equipment manufacturer and service provider of a wide range of products and services applicable to desalination, municipal water treatment and industrial water and wastewater treatment. Its products include reverse osmosis desalination equipment, membrane separation equipment, filtration equipment, piping systems, vessels and custom fabricated components. Aerex also offers engineering, design, consulting, inspection, training and equipment maintenance services to its customers.

Affiliate

Ocean Conversion (BVI) Ltd. (“OC-BVI”). We own 50% of the voting stock of OC-BVI, a British Virgin Islands company, which sells bulk water to the Government of the British Virgin Islands Water and Sewerage Department. We own an overall 43.53% equity interest in OC-BVI’s profits and certain profit sharing rights that raise our effective interest in OC-BVI’s profits to approximately 45%. OC-BVI also pays our subsidiary, DesalCo Limited, fees for certain engineering and administrative services. We account for our investment in OC-BVI under the equity method of accounting.

Our Operations

For fiscal year 2016, our retail water, bulk water and services segments generated approximately 41%, 51% and 8%, respectively, of our consolidated revenues. For additional information about our business segments and geographical information about our operating revenues and long-lived assets, see Note 17 to our consolidated financial statements at ITEM 8 of this Annual Report.

Retail Water Operations

For fiscal years 2016, 2015 and 2014, our retail water operations accounted for approximately 41%, 41% and 37%, respectively, of our consolidated revenues. This business produces and supplies water to end-users, including residential, commercial and government customers in the Cayman Islands and Bali, Indonesia.

Retail Operations in the Cayman Islands

We sell water through our retail operations to a variety of residential and commercial customers through our wholly-owned subsidiary, Cayman Water, which operates under an exclusive license issued to us by the Cayman Islands government. Pursuant to the license, we have the exclusive right to produce potable water and distribute it by pipeline to our licensed service area which consists of two of the three most populated areas of Grand Cayman Island: Seven Mile Beach and West Bay.

Under our license, we pay a royalty to the government of 7.5% of our gross retail water sales revenues (excluding energy cost adjustments). The selling prices of water sold to our customers are determined by the license and vary depending upon the type and location of the customer and the monthly volume of water purchased. The license provides for an automatic adjustment for inflation or deflation on an annual basis, subject to temporary limited exceptions, and an automatic adjustment for the cost of electricity on a monthly basis. The Water Authority-Cayman (“WAC”), on behalf of the government, reviews and confirms the calculations of the price adjustments for inflation and electricity costs. If we wish to adjust our prices for any reason other than inflation or electricity costs, we must request prior approval of the Cabinet of the Cayman Islands government. Disputes regarding price adjustments would be referred to arbitration.

7

The license was originally scheduled to expire in July 2010 but has been extended several times by the Cayman Islands government in order to provide the parties with additional time to negotiate the terms of a new license agreement. The most recent extension of the license expired on June 30, 2016. We continue to provide water subsequent to June 30, 2016 on the assumption that the license has been further extended to allow the parties to continue negotiations without interruption to an essential service.

The Cayman Islands government could ultimately offer a third party a license to service some or all of Cayman Water’s present service area. However, as set forth in the existing license, “the Governor hereby agrees that upon the expiry of the term of this Licence or any extension thereof, he will not grant a licence or franchise to any other person or company for the processing, distribution, sale and supply of water within the Licence Area without having first offered such a licence or franchise to the Company on terms no less favourable than the terms offered to such other person or company.”

In February 2011, the Water (Production and Supply) Law, 2011 and the Water Authority (Amendment) Law, 2011 (the “New Laws”) were published and enacted. Under the New Laws, the WAC will issue any new license, and such new license could include a rate of return on invested capital model, as discussed in the following paragraph.

Following the enactment of the New Laws, we were advised in correspondence from the Cayman Islands government and the WAC that: (i) the WAC, and not the Cayman Islands government, is the principal negotiator in these license negotiations; and (ii) the WAC has determined that a rate of return on invested capital model (“RCAM”) for the retail license is in the best interest of the public and Cayman Water’s customers. RCAM is the rate model currently utilized in the electricity transmission and distribution license granted by the Cayman Islands government to the Caribbean Utilities Company, Ltd. We responded to the Cayman Islands government that we disagreed with the government’s position on these two matters and negotiations for a new license temporarily ceased.

In July 2012, in an effort to resolve several issues relating to our retail license renewal negotiations, we filed an Application for Leave to Apply for Judicial Review (the “Application”) with the Grand Court of the Cayman Islands (the “Court”), seeking declarations that: (i) certain provisions of the New Laws appear to be incompatible and a determination as to how those provisions should be interpreted; (ii) the WAC’s roles as the principal license negotiator, statutory regulator and our competitor put the WAC in a position of hopeless conflict; and (iii) the WAC’s decision to replace the rate structure under our current exclusive license with RCAM was predetermined and unreasonable. The hearing for this judicial review was held in April 2014 and in June 2014 the Court issued its ruling, which was limited to the determination that (i) the renewal of the license does not require a public bidding process; and (ii) the WAC is the proper entity to negotiate with us for the renewal of the license.

In November 2014, we wrote to the Minister of Works offering to recommence license negotiations on the basis of the RCAM model subject to the following conditions: (i) the Government would undertake to amend the current water legislation to provide for an independent regulator and a fair and balanced regulatory regime more consistent with that provided under the electrical utility regulatory regime, (ii) the Government and we would mutually appoint an independent referee and chairman of the negotiations, (iii) our new license would provide exclusivity for the production and provision of all piped water, both potable and non-potable, within our Cayman Islands license area, (iv) the Government would allow us to submit our counter proposal to the WAC’s RCAM license draft, and (v) the principle of subsidization of residential customer rates by commercial customer rates would continue under a new license. In March 2015, we received a letter from the Minister of Works with the following responses to the November 2014 letter: (1) while the Cayman government plans to create a new public utilities commission, the provision of the new retail license will not depend upon the formation of such a commission; (2) any consideration regarding inclusion of the exclusive right to sell non-potable water within the area covered by the retail license will not take place until after the draft license has proceeded through the review process of the negotiations; (3) rather than allow us to submit our counter proposal to the WAC’s RCAM license draft, the WAC will draft the license with the understanding that we will be allowed to propose amendments thereto; (4) the principle of subsidization of residential customer rates by commercial customer rates would continue under the new license; and (5) a request that we consider eliminating our monthly minimum volume charge in the new license.

We recommenced license negotiations with the WAC during the third quarter of 2015 based upon a draft RCAM license provided by the WAC.

In October 2016, the Government of the Cayman Islands passed legislation which created a new utilities regulation and competition office (“OFREG”). OFREG is an independent and accountable regulatory body with a view of protecting the rights of consumers, encouraging affordable utility services, and promoting competition. OFREG has the ability to supervise, monitor and regulate multiple utility undertakings and markets. Water utilities are not presently included in the scope of OFREG’s regulatory functions and remain under the regulatory control of the WAC. However, we were given the opportunity by the Cayman Islands government to comment on four draft legislative bills which are intended to transfer responsibility for economic regulation of the water utility sector from the WAC to OFREG. We have not been advised as to the final form and content of these legislative bills and are therefore presently unable to assess their ultimate impact on our retail license negotiations, however we believe that these bills will be enacted into law within the coming months. OFREG began operations in January 2017, and we have been advised by the WAC that they are presently coordinating with OFREG to transfer responsibility for our license negotiations from the WAC to OFREG. We cannot presently determine the impact of OFREG or the pending legislative bills on our retail license negotiations, when our retail license negotiations will be completed, or the outcome of such negotiations.

See also ITEM 1.A. RISK FACTORS and ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS - Material Commitments, Expenditures and Contingencies – Renewal of Retail License.

8

Our retail operations in the Cayman Islands produce potable water at three reverse osmosis seawater conversion plants in Grand Cayman located at our Abel Castillo Water Works (“ACWW”), Britannia and West Bay sites. We own the land for our ACWW and West Bay plants and have entered into a lease for the land for our Britannia plant that expires January 1, 2027. The current production capacity of the plant located at ACWW is 2.0 million gallons of water per day. The production capacity of the Britannia plant is 715,000 gallons of water per day. The production capacity of the West Bay plant is approximately 900,000 gallons of water per day.

Electricity to our plants is supplied by Caribbean Utilities Co. Ltd., a publicly traded utility company. We maintain diesel engine-driven standby generators at all three retail plant sites with sufficient capacity to operate our distribution pumps and other essential equipment during any temporary interruptions in electricity supply. Standby generation capacity is available at our West Bay plant and ACWW plants to operate a portion of the water production capacity as well.

In the event of an emergency, our distribution system is connected to the distribution system of the WAC. In prior years, we have purchased water from the WAC for brief periods of time and have also sold potable water to the WAC from our retail plants.

Our pipeline system on Grand Cayman covers the Seven Mile Beach and West Bay areas and consists of approximately 90 miles of potable water pipeline. We extend our distribution system periodically as demand warrants. We have a main pipe loop covering the Seven Mile Beach and West Bay areas. We place extensions of smaller diameter pipe off our main pipe to service new developments in our service area. This system of building branches from the main pipe keeps construction costs low and allows us to provide service to new areas in a timely manner. Developers are responsible for laying the pipeline within their developments at their own cost, but in accordance with our specifications. When a development is completed, the developer then transfers operation and maintenance of the pipeline to us.

We bill our customers on a monthly basis based on metered consumption and bills are typically collected within 30 to 35 days after the billing date. Receivables not collected within 45 days subject the customer to disconnection from water service. In 2016, 2015 and 2014, bad debts represented less than 1% of our total annual retail sales. In addition to their past due invoice balance, customers that have had their service disconnected must pay re-connection charges.

Historically, demand on our pipeline distribution has varied throughout the year. Demand depends upon various factors including the number of tourists visiting and the amount of rainfall during any particular time of the year and other cyclical climate conditions. In general, the majority of tourists come from the United States during the winter which is also our dry season.

Retail Operations in Bali, Indonesia

During the latter half of 2012, we commenced, through our subsidiary, CW-Bali, the construction of a seawater desalination plant with an initial capacity of 264,000 gallons per day in Nusa Dua, one of the primary tourist areas of Bali, Indonesia. Nusa Dua has a target customer profile consisting of tourist resorts and luxury/vacation residences comparable to our retail service area on Grand Cayman. We believe the water demands of these properties in Nusa Dua already exceed the supply capacity of the local public water utility, will soon exceed other local sources (such as wells), and that other areas of Bali will also eventually experience fresh water shortages. However, as desalination had not been employed to any meaningful extent in Bali, we concluded that to obtain customers in Bali we must first demonstrate the viability of desalination as well as our capabilities and expertise. Consequently, we elected to construct this plant before obtaining water supply agreements for its production. During 2014, we expanded the capacity of this plant to 790,000 gallons per day.

Since its inception, we have recorded operating losses for CW-Bali as the sales volumes for its plant have not been sufficient to cover its operating costs. In 2016, we determined, based upon probability-weighted scenarios for CW-Bali’s future undiscounted cash flows, that the carrying values of CW-Bali’s long-lived assets were not recoverable and recorded an impairment loss of $2.0 million for the three months ended September 30, 2016 to reduce the carrying values of these assets to their estimated fair values.

See further discussion of our Bali retail operations at ITEM 1.A. RISK FACTORS and ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS – Material Commitments, Expenditures and Contingencies – CW-Bali.

Bulk Water Operations

For fiscal years 2016, 2015 and 2014, our bulk water operations accounted for approximately 51%, 56% and 60%, respectively, of our consolidated revenues. These operations produce potable water from seawater and sells this water to governments in the Cayman Islands, Belize and The Bahamas.

9

Bulk Water Operations in the Cayman Islands

Through our wholly-owned subsidiary OC-Cayman we provide bulk water on a take-or-pay basis to the WAC, a government owned utility and regulatory agency, under various agreements. The WAC in turn distributes that water to properties in Grand Cayman outside of our retail license area.

The water we sell to the WAC is produced at three reverse osmosis seawater conversion plants in Grand Cayman owned by the WAC but designed, built and operated by OC-Cayman: the Red Gate, North Sound and North Side Water Works plants, which have production capacities of approximately 1.3 million, 1.6 million and 2.4 million gallons of water per day, respectively. The plants we operate for the WAC are located on land owned by the WAC.

The current operating agreement for the Red Gate plant expires in July 2017. The current operating agreement for the North Sound plant expires in April 2017. The current operating agreement for the North Side Water Works plant expires in June 2019.

Bulk Water Operations in Belize

In Belize, we sell bulk water through our wholly-owned subsidiary CW-Belize.

We own the reverse osmosis seawater conversion plant in Belize and lease the land on which our plant is located from the Belize government at an annual rent of BZE$1.00. The land lease expires in March 2026. The production capacity of the plant is 600,000 gallons of water per day.

Electricity to our plant is supplied by Belize Electricity Limited. At the plant site, we maintain a diesel engine-driven, standby generator with sufficient capacity to operate 100% of our water production equipment during any temporary interruption in the electricity supply.

In Ambergris Caye, Belize we are the exclusive provider of water to Belize Water Services Ltd. (“BWSL”), a government controlled entity which distributes the water through its own pipeline system to residential, commercial and tourist properties. BWSL distributes our water primarily to residential properties, small hotels, and businesses that serve the tourist market. The base price of water supplied, and adjustments thereto, are determined by the terms of the contract, which provides for annual adjustments based upon the movement in the government price indices specified in the contract, as well as monthly adjustments for changes in the cost of diesel fuel and electricity.

We have an exclusive contract with BWSL to supply a minimum of 2.03 million gallons of water per week or, upon demand, up to 2.94 million gallons per week, on a take-or-pay basis. This contract expires on March 23, 2026. BWSL has the right, with six months advance notice before the expiration date, to renew the contract for a further 25-year period on the same terms and conditions.

Bulk Water Operations in The Bahamas

We sell bulk water in The Bahamas through our majority-owned subsidiary, CW-Bahamas, to the Water and Sewerage Corporation of The Bahamas (“WSC”) and to a private resort on Bimini.

We supply bulk water in The Bahamas from our Windsor, Blue Hills and Bimini plants.

The water supply agreement for our Windsor plant, which has a capacity of 3.1 million gallons per day, was originally scheduled to expire in July 2013. Subsequent to July 2013, we continued to supply water from the Windsor plant on a month-to-month basis at the request of the government of The Bahamas. On December 28, 2016, we executed an amendment to the Windsor water supply agreement with the WSC, pursuant to which the agreement was extended for 15 years on a take-or-pay basis for a minimum of 16.8 million gallons per week. Pursuant to the amended agreement, CW Bahamas is required to complete capital improvements to the Windsor plant which we estimate will cost approximately $8.9 million to ensure that the plant can meet its performance guarantees during the extended agreement period. The per gallon price for the water supplied under the extended agreement, excluding the pass-through energy component, is approximately 18% less than the price in effect at December 31, 2016. The remaining terms of the amended agreement are substantially consistent with those of the original Windsor water supply agreement.

We supply water from the Blue Hills plant, our Company’s largest seawater conversion facility with a capacity of 12.0 million gallons per day, under the terms of a water supply agreement with the WSC that expires in March 2032 that requires us to deliver and requires the WSC to purchase a minimum of 63.0 million gallons of water each week.

The Bimini plant has a capacity of 115,000 gallons per day and supplies water to a private resort under a water supply agreement that expires in December 2020.

The high-pressure pumps at our Windsor and Blue Hills plants in the Bahamas are diesel engine-driven. Electricity for the remainder of our plant operations is supplied by Bahamas Electricity Corporation. We maintain a standby generator with sufficient capacity to operate essential equipment at our Windsor and Blue Hills plants and are able to produce 100% of the production capacity with these plants during temporary interruptions in the electricity supply.

10

We provide bulk water to the WSC, which distributes the water through its own pipeline system to residential, commercial and tourist properties on the Island of New Providence.

Services Operations

For fiscal years 2016, 2015 and 2014, our services operations accounted for approximately 8%, 3% and 3%, respectively, of our consolidated revenues and are comprised of businesses providing services in the Cayman Islands, The Bahamas, the British Virgin Islands and the United States. These businesses construct, manufacture and service a wide range of water-related products and provide design, engineering, management, and other services for desalination, commercial and municipal water production, water supply and treatment, and industrial water and wastewater treatment.

We provide design, engineering and construction services for desalination projects through DesalCo, which is recognized by suppliers as an original equipment manufacturer of reverse osmosis seawater desalination plants for our Company. DesalCo also provides management and procurement services for desalination plants and engineering services relating to municipal water production, distribution and treatment. DesalCo also conducts research and development. DesalCo frequently tests new components and technology offered by suppliers in our business and, at times, we collaborate with suppliers in the development of their products.

On February 11, 2016, we purchased, through a newly formed wholly-owned U.S. subsidiary (CW-Holdings), a 51% interest in Aerex, a U.S. company located in Fort Pierce, Florida. Aerex is an original equipment manufacturer and service provider of a wide range of products and services applicable to desalination, municipal water treatment and industrial water and wastewater treatment. Its products include reverse osmosis desalination equipment, membrane separation equipment, filtration equipment, piping systems, vessels and custom fabricated components. Aerex also offers engineering, design, consulting, inspection, training and equipment maintenance services to its customers.

Affiliate Operations

Our affiliate, OC-BVI, sells water to the Government of the British Virgin Islands Water and Sewerage Department (“BVIW&S”). We own 50% of the voting shares of OC-BVI and have an overall 43.53% equity interest in the profits of OC-BVI. We also own separate profit sharing rights in OC-BVI that raise our effective interest in OC-BVI’s profits from 43.53% to approximately 45%. Sage Water Holdings (BVI) Limited (“Sage”) owns the remaining 50% of the voting shares of OC-BVI and the remaining 55% interest in its profits. Under the Articles of Association of OC-BVI, we have the right to appoint three of the six directors of OC-BVI. Sage is entitled to appoint the remaining three directors. In the event of a tied vote of the directors, the President of the Caribbean Water and Wastewater Association, a regional trade association comprised primarily of government representatives, is entitled to appoint a junior director to cast a deciding vote.

We provide certain engineering and administrative services to OC-BVI for a monthly fee and a bonus arrangement which provides for payment of 4% of the net operating income of OC-BVI.

We account for our investment in OC-BVI using the equity method of accounting.

OC-BVI sells bulk water to BVIW&S, which distributes the water through its own pipeline system to residential, commercial and tourist properties on the islands of Tortola and Jost Van Dyke in the British Virgin Islands. OC-BVI provides operating, engineering and procurement services for another plant under a short-term agreement with Sage.

OC-BVI owns and operates a desalination plant located at Bar Bay, Tortola with a capacity of 720,000 gallons per day. Pursuant to a water supply agreement with the BVI government, OC-BVI is required to supply up to 600,000 gallons per day to the BVI government on a take-or-pay basis. This water supply agreement was schedule to expire in March 2017, but was extended in February 2017 to March 2031. The per gallon price for the water supplied under the extended agreement, excluding the pass-through energy component, is approximately 31% less than the price in effect at December 31, 2016. The remaining terms of the extended agreement are substantially consistent with those of the original Bar Bay water supply agreement.

OC-BVI purchases electrical power to operate this plant from BVI Electric Co. and operates diesel engine driven emergency power generators which can produce 100% of the plant’s production capacity when BVI Electric Co. is unable to provide power to the plant.

OC-BVI’s plant on the island of Jost Van Dyke has a capacity of 60,000 gallons per day. This plant operates under a 10-year contract with the BVI government that expired July 8, 2013. Pursuant to the contract, OC-BVI is operating the plant on a year-to-year basis until the BVI government informs OC-BVI of its intention to extend the existing, or enter into a new agreement. We purchase electrical power to operate this plant from BVI Electric Co.

11

Reverse Osmosis Technology

The conversion of seawater to potable water is called desalination. The two primary forms of desalination are distillation and reverse osmosis. Both methods are used throughout the world and technologies are improving to lower the costs of production. Reverse osmosis is a fluid separation process in which the saline water (i.e. seawater) is pressurized and the fresh water is separated from the saline water by passing through a semi-permeable membrane which rejects the salts. The saline water is first passed through a pretreatment system, which generally consists of fine filtration and treatment chemicals, if required. Pre-treatment removes suspended solids and organics which could cause fouling of the membrane surface. Next, a high-pressure pump pressurizes the saline water thus enabling approximately 40% conversion of the saline water to fresh water as it passes through the membrane, while more than 99% of the dissolved salts are rejected and remain in the now concentrated saline water. This concentrate is discharged without passing through the membrane; however, the remaining hydraulic energy in the concentrate is transferred to the initial saline feed water with an energy recovery device thus reducing the total energy requirement for the reverse osmosis system. The final step is post-treatment, which consists of stabilizing the produced fresh water (thereby removing undesirable dissolved gases), adjusting the pH and providing chlorination to prepare it for distribution.

We use reverse osmosis technology to convert seawater to potable water at all of the plants we construct and operate. We believe that this technology is the most effective and efficient conversion process for our markets. However, we are always seeking ways to maximize efficiencies in our current processes and investigating new, more efficient processes to convert seawater to potable water. The equipment at our plants is among the most energy efficient available and we monitor and maintain the equipment in an efficient manner. As a result of our decades of experience in seawater desalination, we believe our expertise and experience with respect to the development and operation of desalination plants and similar facilities is easily transferable to locations outside of our current operating areas.

Raw Materials and Sources of Supply

All materials, parts and supplies essential to our business operations are obtained from multiple sources and we use the latest industry technology. Prior to our acquisition of Aerex, we did not manufacture any parts or components for equipment essential to our business. Aerex has manufactured some of the key components for some of our plants in the past and we expect Aerex to do so in the future. Our access to seawater for processing into potable water is granted through our licenses and contracts with governments of the various jurisdictions in which we have our operations.

Seasonal Variations in Our Business

Our retail and bulk operations are affected by the levels of tourism and are subject to seasonal variations in our service areas. Demand for our water in the Cayman Islands, Belize, and the Bahamas is affected by variations in the level of tourism and local weather, primarily rainfall. Tourism in our service areas is affected by the economies of the tourists’ home countries, primarily the United States and Europe, terrorist activity and perceived threats thereof, and increased costs of fuel and airfares. We normally sell more water during the first and second quarters, when the number of tourists is greater and local rainfall is less in our markets, than in the third and fourth quarters.

Government Regulations, Custom Duties and Taxes

Our operations and activities are subject to the governmental regulations and taxes of the countries in which we operate. The following summary of regulatory developments and legislation does not purport to describe all present and proposed regulation and legislation that may affect our businesses. Legislative or regulatory requirements currently applicable to our businesses may change in the future. Any such changes could impose new obligations on us that may adversely affect our businesses and operating results. The following paragraphs set forth some of the key governmental regulations in the jurisdictions in which we operate outside of the United States.

The Cayman Islands

The Cayman Islands are a British Overseas Territory and have had a stable political climate since 1670, when the Treaty of Madrid ceded the Cayman Islands to England. The Queen of England appoints the Governor of the Cayman Islands to make laws with the advice and consent of the legislative assembly. The legislative assembly consists of 18 elected members and two members appointed by the Governor from the Civil Service. The Cabinet is responsible for day-to-day government operations. The Cabinet consists of seven ministers who are chosen by the Premier from its 18 popularly elected members, and the two Civil Service members. The elected members choose from among themselves a leader, who is designated the Premier, and is in effect the leader of the elected government. The Governor has reserved powers and the United Kingdom retains full control over foreign affairs and defense. The Cayman Islands are a common law jurisdiction and have adopted a legal system similar to that of the United Kingdom.

The Cayman Islands have no taxes on profits, income, distributions, capital gains or appreciation. We have exemptions from, or receive concessionary rates of customs duties on capital expenditures for plant and major consumable spare parts and supplies imported into the Cayman Islands under our retail water license. We do not pay import duty or taxes on reverse osmosis membranes, electric pumps and motors, and chemicals, but we do pay duty at the rate of 10% of the cost, including insurance and transportation to the Cayman Islands, of other plant and associated materials and equipment to manufacture or supply water in the Seven Mile Beach or West Bay areas. We have been advised by the Government of the Cayman Islands that we will not receive any duty concessions in our new retail water license.

12

The Bahamas

The Commonwealth of The Bahamas is an independent nation and a constitutional parliamentary democracy with the Queen of England as the constitutional head of state. The basis of the Bahamian law and legal system is the English common law tradition with a Supreme Court, Court of Appeals, and a Magistrates court.

Under the current laws of the Commonwealth of The Bahamas, no income, corporation, capital gains or other taxes are payable by us. We are required to pay an annual business license fee (the calculation of which is based on our preceding year’s financial statements) which to date has not been material to the results of our Bahamas operations.

Belize

Belize achieved full independence from the United Kingdom in 1981. Today, Belize is a constitutional monarchy with the adoption of a constitution in 1981. Based on the British model with three independent branches, the Queen of England is the constitutional head of state, represented by a Governor General. A Prime Minister and cabinet make up the executive branch, while a 31 member elected House of Representatives and a 13 member appointed Senate form a bicameral legislature. The cabinet consists of a prime minister, other ministers and ministers of state who are appointed by the Governor-General on the advice of the Prime Minister, who has the support of the majority party in the House of Representatives. Belize is an English common law jurisdiction with a Supreme Court, Court of Appeals and local Magistrate Courts.

The Government of Belize has exempted CW-Belize from certain customs duties and all revenue replacement duties until April 18, 2026, and had exempted CW-Belize from company taxes until January 28, 2006. Belize levies a gross receipts tax on corporations at a rate varying between 0.75% and 25%, depending on the type of business, and a corporate income tax at a rate of 25% of chargeable income. Gross receipts tax payable amounts are credited towards corporate income tax. The Government of Belize also implemented certain environmental taxes and a general sales tax effective July 1, 2006 and increased certain business and personal taxes and created new taxes effective March 1, 2005. Belize levies import duty on most imported items at rates varying between 0% and 45%, with most items attracting a rate of 20%. Under the terms of our water supply agreement with BWSL we are reimbursed by BWSL for all taxes and customs duties that we are required to pay and we record this reimbursement as an offset to our tax expense.

The British Virgin Islands

The British Virgin Islands (the “BVI”) is a British Overseas Territory, with the Queen as the Head of State and Her Majesty’s representative, the Governor, responsible for external affairs, defense and internal security, the Civil Service and administration of the courts. Since 1967, the BVI has held responsibility for its own internal affairs.

The BVI Constitution provides for the people of the BVI to be represented by a ministerial system of government, led by an elected Premier, a Cabinet of Ministers and the House of Assembly. The House of Assembly consists of 13 elected representatives, the Attorney General, and the Speaker.

The judicial system, based on English law, is under the direction of the Eastern Caribbean Supreme Court, which includes the High Court of Justice and the Court of Appeal. The ultimate appellate court is the Privy Council in London.

Market and Service Area

Although we currently operate in the Cayman Islands, Belize, the British Virgin Islands, The Commonwealth of The Bahamas, the United States and Indonesia we believe that our potential market consists of any location where a need exists for potable water and with access to seawater or brackish water. The desalination of seawater, either through distillation or reverse osmosis, is the most widely used process for producing potable water in areas with an insufficient natural supply. We believe our experience in the development and operation of reverse osmosis desalination plants will provide us with significant opportunities to successfully expand our operations beyond the markets in which we currently operate.

Cayman Islands. The Cayman Islands government, through the WAC, supplies water to parts of Grand Cayman, which are not within our licensed area, as well as to Cayman Brac. We operate all but one of the reverse osmosis desalination plants owned by the WAC on Grand Cayman and supply water under licenses and supply agreements held by OC-Cayman with the WAC.

According to the most recent information published by the Economics and Statistics Office of the Cayman Islands Government, the population of the Cayman Islands was estimated in December 2015 to be 60,413. According to the figures published by the Department of Tourism Statistics Information Center, during the year ended December 31, 2016, tourist air arrivals increased by less than 1% and tourist cruise ship arrivals fell by less than 1% compared to 2015.

13

Total visitors for the year were approximately 2.1 million in 2016 and 2015. We believe that our water sales in the Cayman Islands are more positively impacted by stay-over tourists that arrive by air than by those arriving by cruise ship, since cruise ship tourists generally only visit the island for one day or less and do not remain on the island overnight.

The Bahamas. On South Bimini Island in The Bahamas, we supply water to a private developer and do not have competitors. GE Water operates a seawater desalination plant on North Bimini Island and other small family islands. We competed with companies such as GE Water, Veolia, IDE Technologies, GS Inima and Biwater for the contract with the Bahamian government to build and operate a seawater desalination plant at Blue Hills, New Providence, Bahamas. We expect to compete with these companies and others for any future water supply contracts in The Bahamas.

Belize. Our current operations in Belize are located on Ambergris Caye, which consists of residential, commercial and tourist properties in the town of San Pedro. This town is located on the southern end of Ambergris Caye, one of many islands located east of the Belize mainland and off the southeastern tip of the Yucatan Peninsula. Ambergris Caye is approximately 25 miles long and, according to the Central Statistical Office “Belize: 2010 National Census Overview”, has a population of about 11,500 residents. We provide bulk potable water to BWSL, which distributes this water to this market. BWSL currently has no other source of potable water on Ambergris Caye. Our contract with BWSL makes us their exclusive producer of desalinated water on Ambergris Caye through 2026.

A 185 mile long barrier reef, which is the largest barrier reef in the Western Hemisphere, is situated just offshore of Ambergris Caye. This natural attraction is a choice destination for scuba divers and tourists. According to information published by the Belize Trade and Investment Development Service, tourism is Belize’s second largest source of foreign income, next to agriculture.

British Virgin Islands. The British Virgin Islands are a British Overseas Territory and are situated east of Puerto Rico. They consist of 16 inhabited and more than 20 uninhabited islands, of which Tortola is the largest and most populated. The British Virgin Islands serve as a hub for many large yacht-chartering businesses.

Competition

Cayman Islands. Pursuant to our license granted by the Cayman Islands government, we have the exclusive right to provide potable, piped water within our licensed service area on Grand Cayman. We are the only non-government-owned public water utility on Grand Cayman. The Cayman Islands government, through the WAC, supplies water to parts of Grand Cayman located outside of our licensed service area. Although we have no competition within our exclusive retail license service area for potable water, our ability to expand our service area is at the discretion of the Cayman Island government. Private residences and commercial multi-unit dwellings up to four units may install potable water making equipment for their own use. Water plants on premises within our license area and serving only their premises in existence prior to 1991 can be maintained but not replaced or expanded. We are aware of only one such plant currently in operation. The Cayman Islands government, through the WAC, supplies water to parts of Grand Cayman outside of our licensed service area. We have competed with such companies as GE Water, Veolia, and IDE Technologies for bulk water supply contracts with the WAC.

The Bahamas. On South Bimini Island in The Bahamas, we supply water to a private developer and do not have competitors. GE Water operates a seawater desalination plant on North Bimini Island and other small islands. We competed with companies such as GE Water, Veolia, IDE Technologies, GS Inima and Biwater for the contract with the Bahamian government to build and operate a seawater desalination plant at Blue Hills, New Providence, Bahamas. We expect to compete with these companies and others for any future water supply contracts in The Bahamas.

Belize. On Ambergris Caye in Belize, our water supply contract with Belize Water Services Limited is exclusive, and Belize Water Services Limited cannot seek contracts with other water suppliers, or produce water itself, to meet their future needs in San Pedro, Ambergris Caye, Belize.

British Virgin Islands. In the British Virgin Islands, GE Water operates seawater desalination plants in West End, Tortola, and on Virgin Gorda and generally bids against OC-BVI for projects. In 2010, Biwater PLC negotiated a 16 year contract on a sole sourced basis, pursuant to which it has constructed and is operating a 2.75 million gallon per day desalination plant in Parakeeta Bay, Tortola for the British Virgin Islands government. In August 2015, this plant was acquired from Biwater by Seven Seas Water, a division of AquaVenture Holdings.

United States. Aerex competes in the highly fragmented industry for manufactured water production and treatment equipment, systems and services against a large number of manufacturers, fabricators and service providers, many of which have greater resources than Aerex.

Bali, Indonesia. In Bali, we compete against local water treatment equipment suppliers who provide equipment and services to individual resort properties.

To implement our growth strategy for our desalination businesses outside our existing operating areas, we will have to compete with some of the same companies we competed with for the Blue Hills project in Nassau, Bahamas such as GE Water, Veolia, IDE Technologies, GS Inima, and Biwater as well as other companies. Some of these companies currently operate in areas in which we would like to expand our operations and already maintain worldwide operations having greater financial, managerial and other resources than our company. We believe that our low overhead costs, knowledge of local markets and conditions and our efficient manner of operating desalinated water production and distribution equipment provide us with the capabilities to effectively compete for new projects in the Caribbean basin and other select markets.

14

Environmental and Health Regulatory Matters

Cayman Islands. With respect to our Cayman Islands operations, we operate our water plants in accordance with guidelines of the Cayman Islands Department of Environmental Health. We are licensed by the WAC to discharge concentrated seawater, which is a byproduct of our desalination process, into deep disposal wells.

Our Cayman Islands license requires that our potable water quality meet the World Health Organization’s Guidelines for Drinking Water Quality and contain less than 200 mg/l of total dissolved solids.

The Bahamas, Belize, and British Virgin Islands. With respect to our Bahamas and Belize operations and OC-BVI’s British Virgin Islands operations, we and OC-BVI are required by our water supply contracts to take all reasonable measures to prevent pollution of the environment. We are licensed by the Belize and Bahamian governments to discharge concentrated seawater, which is a by-product of our desalination process, into deep disposal wells. OC-BVI is licensed by the British Virgin Islands government to discharge concentrated seawater into the sea. At several of our locations hydrogen sulfide gas is present in the seawater and we operate our plants in a manner so as to minimize the emission of airborne gas into the environment.

United States. Consistent with other U.S. manufacturers, Aerex must comply with laws and regulations administered by the U.S. Environmental Protection Agency.

We are not aware of any existing or pending environmental legislation which may affect our operations. To date, we have not received any complaints from any regulatory authorities.

Employees

As of March 10, 2017, we employed a total of 117 persons, 63 in the Cayman Islands, 19 in The Bahamas, 22 in the United States, seven in Belize and six in Asia. We also leased 18 employees for Aerex’s manufacturing activities in the United States and managed the six employees of OC-BVI in the British Virgin Islands. We have 10 management employees and 34 administrative and clerical employees. The remaining employees are engaged in engineering, purchasing, plant maintenance and operations, pipe laying and repair, leak detection, new customer connections, meter reading and laboratory analysis of water quality. None of our employees is a party to a collective bargaining agreement. We consider our relationships with our employees to be good.

Available Information

Our website address is http://www.cwco.com. Information contained on our website is not incorporated by reference into this Annual Report, and you should not consider information contained on our website as part of this Annual Report.

We have adopted a written code of conduct and ethics that applies to all of our employees and directors, including, but not limited to, our principal executive officer, principal financial officer, and principal accounting officer or controller, or persons performing similar functions. The Code of Business Conduct and Ethics, the charters of the Audit Committee, Compensation Committee, Nominations and Corporate Governance Committee and the Consolidated Water Co. Ltd. Corporate Governance Guidelines of our Board of Directors are available at the Investors portion of our website.

You may access, free of charge, our annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, plus amendments to such reports as filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, on our website and on the website of the Securities and Exchange Commission (the “SEC”) as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. In addition, paper copies of these documents may be obtained free of charge by writing us at the following address: Consolidated Water Co. Ltd., Regatta Office Park, Windward Three, 4th Floor, West Bay Road, P.O. Box 1114, Grand Cayman, KY1-1102, Cayman Islands, Attention: Investor Relations; or by calling us at (345) 945-4277.

15

| ITEM 1A. | RISK FACTORS |

Investing in our common shares involves risks. Prior to making a decision about investing in our common shares, you should consider carefully the factors discussed below and the information contained in this Annual Report. Each of these risks, as well as other risks and uncertainties not presently known to us or that we currently deem immaterial, could adversely affect our business, results of operations, cash flows and financial condition, and cause the value of our common shares to decline, which may result in the loss of part or all of your investment.

Our exclusive license to provide water to retail customers in the Cayman Islands may not be renewed in the future.

In the Cayman Islands, we provide water to retail customers under a license issued in July 1990 by the Cayman Islands government that grants our subsidiary, Cayman Water, the exclusive right to provide water to retail customers within our licensed service area. Pursuant to the license, we have the exclusive right to produce potable water and distribute it by pipeline to our licensed service area, which consists of two of the three most populated areas of Grand Cayman, the Seven Mile Beach and West Bay areas. For the years ended December 31, 2016, 2015 and 2014, the Company generated approximately 40%, 40% and 36%, respectively, of its consolidated revenues and 56%, 56% and 54%, respectively, of its consolidated gross profit from the retail water operations conducted pursuant to Cayman Water’s exclusive license.

The license was originally scheduled to expire in July 2010 but has been extended several times by the Cayman Islands government in order to provide the parties with additional time to negotiate the terms of a new license agreement. The most recent extension of the license expired on June 30, 2016. We continue to provide water subsequent to June 30, 2016 on the assumption that the license has been further extended to allow the parties to continue negotiations without interruption to an essential service.

The Cayman Islands government could ultimately offer a third party a license to service some or all of Cayman Water’s present service area. However, as set forth in the existing license, “the Governor hereby agrees that upon the expiry of the term of this Licence or any extension thereof, he will not grant a licence or franchise to any other person or company for the processing, distribution, sale and supply of water within the Licence Area without having first offered such a licence or franchise to the Company on terms no less favourable than the terms offered to such other person or company.”

In February 2011, the Water (Production and Supply) Law, 2011 and the Water Authority (Amendment) Law, 2011 (the “New Laws”) were published and enacted. Under the New Laws, the WAC will issue any new license, and such new license could include a rate of return on invested capital model, as discussed in the following paragraph.

Following the enactment of the New Laws, we were advised in correspondence from the Cayman Islands government and the WAC that: (i) the WAC, and not the Cayman Islands government, is the principal negotiator in these license negotiations; and (ii) the WAC has determined that a rate of return on invested capital model (“RCAM”) for the retail license is in the best interest of the public and Cayman Water’s customers. RCAM is the rate model currently utilized in the electricity transmission and distribution license granted by the Cayman Islands government to the Caribbean Utilities Company, Ltd. We responded to the Cayman Islands government that we disagreed with the government’s position on these two matters and negotiations for a new license temporarily ceased.

In July 2012, in an effort to resolve several issues relating to our retail license renewal negotiations, we filed an Application for Leave to Apply for Judicial Review (the “Application”) with the Grand Court of the Cayman Islands (the “Court”), seeking declarations that: (i) certain provisions of the New Laws appear to be incompatible and a determination as to how those provisions should be interpreted; (ii) the WAC’s roles as the principal license negotiator, statutory regulator and our competitor put the WAC in a position of hopeless conflict; and (iii) the WAC’s decision to replace the rate structure under our current exclusive license with RCAM was predetermined and unreasonable. The hearing for this judicial review was held in April 2014 and in June 2014 the Court issued its ruling, which was limited to the determination that (i) the renewal of the license does not require a public bidding process; and (ii) the WAC is the proper entity to negotiate with us for the renewal of the license.

In November 2014 we wrote to the Minister of Works offering to recommence license negotiations on the basis of the RCAM model subject to the following conditions: (i) the Government would undertake to amend the current water legislation to provide for an independent regulator and a fair and balanced regulatory regime more consistent with that provided under the electrical utility regulatory regime, (ii) the Government and we would mutually appoint an independent referee and chairman of the negotiations, (iii) our new license would provide exclusivity for the production and provision of all piped water, both potable and non-potable, within our Cayman Islands license area, (iv) the Government would allow us to submit our counter proposal to the WAC’s RCAM license draft, and (v) the principle of subsidization of residential customer rates by commercial customer rates would continue under a new license. We received a letter from the Minister of Works in March 2015 with the following responses to the November 2014 letter: (1) while the Cayman government plans to create a new public utilities commission, the provision of the new retail license will not depend upon the formation of such a commission; (2) any consideration regarding inclusion of the exclusive right to sell non-potable water within the area covered by the retail license will not take place until after the draft license has proceeded through the review process of the negotiations; (3) rather than allow us to submit our counter proposal to the WAC’s RCAM license draft, the WAC will draft the license with the understanding that we will be allowed to propose amendments thereto; (4) the principle of subsidization of residential customer rates by commercial customer rates would continue under the new license; and (5) a request that we consider eliminating our monthly minimum volume charge in the new license.

16

We recommenced license negotiations with the WAC during the third quarter of 2015 based upon a draft RCAM license provided by the WAC.

In October 2016, the Government of the Cayman Islands passed legislation which created a new utilities regulation and competition office (“OFREG”). OFREG is an independent and accountable regulatory body with a view of protecting the rights of consumers, encouraging affordable utility services, and promoting competition. OFREG has the ability to supervise, monitor and regulate multiple utility undertakings and markets. Water utilities are not presently included in the scope of OFREG’s regulatory functions and remain under the regulatory control of the WAC. However, we were given the opportunity by the Cayman Islands government to comment on four draft legislative bills which are intended to transfer responsibility for economic regulation of the water utility sector from the WAC to OFREG. We have not been advised as to the final form and content of these legislative bills and are therefore presently unable to assess their ultimate impact on our retail license negotiations, however we believe that these bills will be enacted into law within the coming months. OFREG began operations in January 2017, and we have been advised by the WAC that they are presently coordinating with OFREG to transfer responsibility for our license negotiations from the WAC to OFREG. We cannot presently determine the impact of OFREG or the pending legislative bills on our retail license negotiations.

The resolution of these license negotiations could result in a material reduction of the operating income and cash flows we have historically generated from our retail license and could require us to record an impairment loss to reduce the carrying value of our goodwill. Such impairment loss could have a material adverse impact on our results of operations.

Our bulk water supply agreements in the Cayman Islands may not be renewed or may be renewed on terms less favorable to us.

All of our bulk water supply agreements are for fixed terms, and such agreements for plants that we operate but are owned by our customers provide for our customers to take over the operations of the plant upon expiration of the agreements.

Our bulk water supply agreements with the WAC for their North Sound and Red Gate plants expire in April 2017 and July 2017 respectively. Our bulk water supply agreement with the WAC for their North Side Water Works plant expires in June 2019. We generated $3.2 million, $2.2 million, and $2.1 million in revenues from the North Sound, Red Gate, and North Side Water Works plants, respectively, during the year ended December 31, 2016. We generated $3.0 million, $3.0 million, and $2.4 million in revenues from the North Sound, Red Gate, and North Side Water Works plants, respectively, during the year ended December 31, 2015. We generated $4.0 million, $3.0 million, and $2.9 million in revenues from the North Sound, Red Gate, and North Side Water Works plants, respectively, during the year ended December 31, 2014.

If our bulk water supply agreements are not renewed or are renewed on terms less favorable to us, our results of operations and cash flows will be adversely affected and we could be required to record an impairment charge to reduce the carrying value of our goodwill. Such impairment charge could have a material adverse impact on our results of operations.

We have paid $20.7 million for land and equipment and incurred development expenses of approximately $20.5 million to date for a possible project in Mexico. We expect to expend significant additional funds in 2017 to continue to pursue this project. However, we may not be successful in completing this project.

We own a 99.9% interest in N.S.C. Agua, S.A. de C.V. (“NSC”), a development stage Mexico company formed to pursue a project encompassing the construction, operation and minority ownership of a 100 million gallon per day seawater reverse osmosis desalination plant to be located in northern Baja California, Mexico and an accompanying pipeline to deliver water to the Mexican potable water system (the “Project”). As of December 31, 2016, our consolidated balance sheet includes purchases for the Project of approximately $20.6 million in land and $91,000 in equipment. The project development activities we have conducted, which include conducting an equipment piloting plant and water data collection program at the proposed feed water source, completing various engineering studies and obtaining various governmental permits, have resulted in additional developmental expenses totaling $20.5 million from 2010 through December 31, 2016.

In August 2014, the State of Baja California (the “State”) enacted new legislation to regulate Public-Private Association projects which involve the type of long-term contract between a public sector authority and a private party that NSC is seeking to complete the Project. Pursuant to this new legislation, in January 2015, NSC submitted an expression of interest for its project to the Secretary of Infrastructure and Urban Development of the State of Baja California (“SIDUE”). SIDUE accepted NSC’s expression of interest and requested that NSC submit a detailed proposal for the Project that complied with requirements of the new legislation. NSC submitted this detailed proposal (the “APP Proposal”) to SIDUE in late March 2015. The new legislation required that such proposal be evaluated by SIDUE and submitted to the Public-Private Association Projects State Committee (the “APP Committee”) for review and authorization. If the Project was authorized the State would be required to conduct a public tender for the Project.

In response to our APP Proposal, in September 2015 NSC received a letter dated June 30, 2015 from the Director General of the Comisión Estatal de Agua de Baja California (“CEA”), the State agency with responsibility for the Project that stated (i) the Project is in the public interest with high social benefits and is consistent with the objectives of the State development plan and (ii) that the Project and accompanying required public tender process should be conducted. In November 2015, the State officially commenced the tender for the Project, the scope of which the State defined as a first phase to be operational in 2019 consisting of a 50 million gallons per day plant and a pipeline that connects to the Mexican potable water infrastructure and a second phase to be operational in 2024 consisting of an additional 50 million gallons per day of production capacity. A consortium comprised of NSC, NuWater S.A.P.I. de C.V. and Degremont S.A. de C.V. (the “Consortium”) submitted its tender for the Project on the April 21, 2016 tender submission deadline date set by the State.

17

We have acknowledged since the inception of the Project that, due to the amount of capital the Project requires, NSC will ultimately need an equity partner or partners for the Project. Consequently, NSC’s tender to the State for the Project was based upon the following: (i) NSC will sell or otherwise transfer the land and other Project assets to a new company (“Newco”) that would build and own the Project; (ii) NSC’s potential partners would provide the majority of the equity for the Project and thereby would own the majority interest in Newco; (iii) NSC would maintain a minority ownership position in Newco; and (iv) Newco would enter into a long-term management and technical services contract for the Project with an entity partially owned by NSC or another Company subsidiary.