Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - UNITED INSURANCE HOLDINGS CORP. | exh32231dec16.htm |

| EX-32.1 - EXHIBIT 32.1 - UNITED INSURANCE HOLDINGS CORP. | exh32131dec16.htm |

| EX-31.2 - EXHIBIT 31.2 - UNITED INSURANCE HOLDINGS CORP. | exh31231dec16.htm |

| EX-31.1 - EXHIBIT 31.1 - UNITED INSURANCE HOLDINGS CORP. | exh31131dec16.htm |

| EX-12.1 - EXHIBIT 12.1 - UNITED INSURANCE HOLDINGS CORP. | exh12131dec16.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________________

FORM 10-K

___________________________________

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2016

Commission File Number 001-35761

United Insurance Holdings Corp.

Delaware | 75-3241967 | |||

(State of Incorporation) | (IRS Employer Identification Number) | |||

800 2nd Avenue S

St. Petersburg, Florida 33701

727-895-7737

Securities registered pursuant to Section 12(b) of the Act: | ||||

COMMON STOCK, $0.0001 PAR VALUE PER SHARE | NASDAQ Stock Market LLC | |||

Securities registered pursuant to Section 12(g) of the Act: | ||||

PREFERRED SHARE PURCHASE RIGHTS | ||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes £ No R

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes £ No R

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes R No £

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes R No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | £ | Accelerated filer | þ | |

Non-accelerated filer | £ | Smaller reporting company | £ | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes £ No R

Non-affiliates held common stock issued by the registrant with an aggregate market value of $277,928,371 as of June 30, 2016, calculated using the closing sales price reported for such date on the NASDAQ Stock Market. For purposes of this disclosure, shares of common stock held by persons who hold more than 10% of the outstanding shares of common stock and shares held by executive officers and directors of the registrant have been excluded because such persons may be deemed to be affiliates. This determination of executive officer or affiliate status is not necessarily a conclusive determination for other purposes.

As of March 15, 2017, 21,676,125 shares of common stock, par value $0.0001 per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Form 10-K incorporates by reference certain information from the Proxy Statement for the 2017 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission within 120 days after the end of our fiscal year ended December 31, 2016.

UNITED INSURANCE HOLDINGS CORP.

Forward-Looking Statements | ||

Item 1. Business | ||

Item 1A. Risk Factors | ||

Item 1B. Unresolved Staff Comments | ||

Item 2. Properties | ||

Item 3. Legal Proceedings | ||

Item 4. Mine Safety Disclosures | ||

Part II. | ||

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | ||

Item 6. Selected Financial Data | ||

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations | ||

Item 7A. Quantitative and Qualitative Disclosures about Market Risk | ||

Item 8. Financial Statements and Supplementary Data | ||

Auditor's Report | ||

Consolidated Balance Sheets | ||

Consolidated Statements of Comprehensive Income | ||

Consolidated Statements of Stockholders' Equity | ||

Consolidated Statements of Cash Flows | ||

Notes to Consolidated Financial Statements | ||

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | ||

Item 9A. Controls and Procedures | ||

Item 9B. Other Information | ||

Part III. | ||

Item 10. Directors, Executive Officers and Corporate Governance | ||

Item 11. Executive Compensation | ||

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||

Item 13. Certain Relationships and Related Transactions, and Director Independence | ||

Item 14. Principal Accounting Fees and Services | ||

Part IV. | ||

Item 15. Exhibits, Financial Statement Schedules | ||

Exhibit Index | ||

Item 16. Form 10-K Summary | ||

Signatures | ||

Throughout this Annual Report on Form 10-K (Annual Report), we present amounts in all tables in thousands, except for share amounts, per share amounts, policy counts or where more specific language or context indicates a different presentation. In the narrative sections of this Annual Report, we show full values rounded to the nearest thousand.

2

UNITED INSURANCE HOLDINGS CORP.

FORWARD-LOOKING STATEMENTS

Statements in this Form 10-K for the year ended December 31, 2016 or in documents incorporated by reference contains “forward-looking statements” within the meaning of the Private Securities Reform Litigation Act of 1995. These forward-looking statements include statements about anticipated growth in revenues, earnings per share, estimated unpaid losses on insurance policies, investment returns and expectations about our liquidity, and our ability to meet our investment objectives and to manage and mitigate market risk with respect to our investments. These statements are based on current expectations, estimates and projections about the industry and market in which we operate, and management’s beliefs and assumptions. Without limiting the generality of the foregoing, words such as “may,” “will,” “expect,” "endeavor," "project," “believe,” “anticipate,” “intend,” “could,” “would,” “estimate,” or “continue” or the negative variations thereof or comparable terminology are intended to identify forward-looking statements. Forward-looking statements are not guarantees of future performance and involve certain known and unknown risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such statements. The risks and uncertainties include, without limitation:

• | the regulatory, economic and weather conditions present in the states in which we operate; |

• | the impact of new federal or state regulations that affect the property and casualty insurance market; |

• | the cost, viability and availability of reinsurance; |

• | assessments charged by various governmental agencies; |

• | pricing competition and other initiatives by competitors; |

• | our ability to attract and retain the services of senior management; |

• | the outcome of litigation pending against us, including the terms of any settlements; |

• | dependence on investment income and the composition of our investment portfolio and related market risks; |

• | our exposure to catastrophic events and severe weather conditions; |

• | downgrades in our financial strength ratings; |

• | risks and uncertainties relating to our acquisitions including our ability to successfully integrate the acquired companies; and |

• | other risks and uncertainties described under "Risk Factors" below. |

We caution you to not place reliance on these forward-looking statements, which are valid only as of the date they were made. We undertake no obligation to update or revise any forward-looking statements to reflect new information or the occurrence of unanticipated events or otherwise. In addition, we prepare our financial statements in accordance with U.S. generally accepted accounting principles (GAAP), which prescribes when we may reserve for particular risks, including litigation exposures. Accordingly, our results for a given reporting period could be significantly affected if and when we establish a reserve for a major contingency. Therefore, the results we report in certain accounting periods may appear to be volatile and past results may not be indicative of results in future periods.

These forward-looking statements are subject to numerous risks, uncertainties and assumptions about us described in our filings with the Securities and Exchange Commission (SEC). The forward-looking events that we discuss in this Form 10-K are valid only as of the date of this Form 10-K and may not occur, or may have different consequences, in light of the risks, uncertainties and assumptions that we describe from time to time in our filings with the SEC. A detailed discussion of these and other risks and uncertainties that could cause actual results and events to differ materially from our forward-looking statements is included in the section entitled “RISK FACTORS” in Part I, Item 1A of this Form 10-K. Except as required by applicable law, we undertake no obligation and disclaim any obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

3

UNITED INSURANCE HOLDINGS CORP.

PART I

Item 1. Business

INTRODUCTION

Company Overview

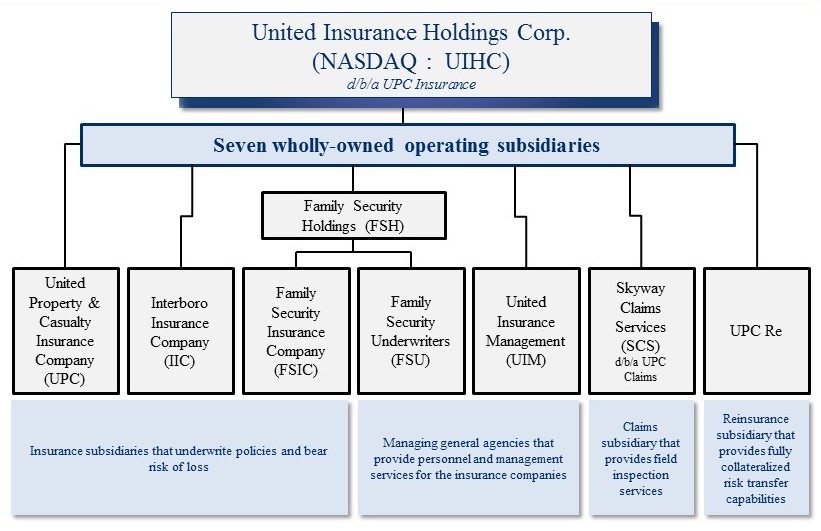

United Insurance Holdings Corp. serves as the holding company for United Property & Casualty Insurance Company and its affiliated companies (referred to in this document as we, our, us, the Company or UPC Insurance). We conduct our business principally through the seven wholly owned operating subsidiaries shown below. Collectively, including United Insurance Holdings Corp., we refer to these entities as “UPC Insurance,” which is the preferred brand identification we are establishing for our Company.

UPC Insurance is primarily engaged in the homeowners' property and casualty insurance business in the United States. We currently write in Connecticut, Florida, Georgia, Hawaii, Louisiana, Massachusetts, New Jersey, New York, North Carolina, Rhode Island, South Carolina, and Texas, and we are licensed to write in Alabama, Delaware, Maryland, Mississippi, New Hampshire, and Virginia. Our target market currently consists of areas where the perceived threat of natural catastrophe has caused large national insurance carriers to reduce their concentration of policies. In such areas we believe an opportunity exists for UPC Insurance to write profitable business. We manage our risk of catastrophic loss primarily through sophisticated pricing algorithms, avoidance of policy concentration, and the use of a comprehensive catastrophe reinsurance program. UPC Insurance has been operating continuously in Florida since 1999, and has successfully managed its business through various hurricanes, tropical storms, and other weather related events. We believe our record of successful risk management and experience in writing business in catastrophe-exposed areas provides us a competitive advantage as we grow our business in other states facing similar perceived threats.

We conduct our operations under one business segment.

4

UNITED INSURANCE HOLDINGS CORP.

Our Strategy

The Company's vision is: "to be the premier provider of property insurance in catastrophe exposed areas."

Our mission is to build a sustainable franchise that delivers quality insurance products in select markets in order to produce superior risk-adjusted returns for investors. Our strategy is to grow in our target markets by building a team of insurance professionals that can (i) provide agents and policyholders quality insurance products with world-class service and systems; (ii) raise and manage capital to support business growth; and (iii) build and maintain relationships with external partners. We believe the team of professionals we have assembled has proven its ability to do each of these things, thereby providing us a source of sustainable competitive advantage as we continue to grow our footprint.

Our emphasis on growing in areas with an ongoing threat of natural catastrophes exposes our company to risk and volatility. We manage the inherent volatility associated with our risk profile in three primary ways: 1) strategically, through geographic and product diversification; 2) financially, through the use of robust reinsurance programs, low financial and operating leverage, and a conservative investment approach; and 3) operationally, by insourcing key insurance functions and establishing strong external distribution partnerships.

To achieve our goals in 2017, UPC Insurance seeks to:

• | Grow our premium base in existing states; |

• | Complete our merger with AmCo Holding Company; |

• | Expand our product offerings in several states where we can leverage existing distribution capabilities; |

• | Utilize and add strategic partnerships to expand distribution and service capabilities in all states; |

• | Improve the efficiency of our catastrophe reinsurance programs; and |

• | Leverage investments in technology and analytics to manage exposure growth and improve profitability. |

Corporate Information

On December 11, 2012, in connection with an underwritten public offering of 5,000,000 shares of our common stock, we were approved to begin trading our common stock on The NASDAQ Capital Market (NASDAQ). On February 3, 2015, we successfully completed the acquisition of FSH and its two wholly owned subsidiaries in an all-stock transaction which resulted in the issuance of 503,857 shares of our common stock. On April 29, 2016, we completed the acquisition of IIC. The purchase price for IIC consisted of $48,450,000 in cash, $8,550,000 in a note payable, and an accrued liability for $3,471,000 which we paid during July 2016.

Our principal executive offices are located at 800 2nd Avenue S, St. Petersburg, FL 33701 and our telephone number at that location is (727) 895-7737.

Recent Events

On February 22, 2017, our Board of Directors declared a $0.06 per share quarterly cash dividend. For additional information regarding this declaration, see Part II, Item 5 of this report.

During the fourth quarter of 2016, we assumed more than 3,100 wind-only residential policies from Citizens Property Insurance Company (Citizens), representing approximately $4,600,000 of annualized premiums. We also assumed more than 3,900 wind-only policies from the Texas Windstorm Insurance Association (TWIA), representing approximately $6,600,000 of annualized premiums. The total amount of assumed premium may be reduced by additional opt outs and cancellations by policyholders.

During the fourth quarter of 2016, Hurricane Matthew impacted Florida and Georgia before making landfall in South Carolina and also impacting North Carolina. We write property insurance in all four states and are working diligently to provide claim service to our insureds who were impacted by the storm. We have received over 5,000 claims related to Hurricane Matthew and incurred approximately $30,000,000 of pre-tax catastrophe losses, net of reinsurance recoveries, during the fourth quarter of 2016 from this event.

On August 17, 2016, we entered into a Merger Agreement with AmCo Holding Company (AmCo), a North Carolina corporation and a wholly owned subsidiary of RDX Holding, LLC (RDX), to acquire AmCo and its two wholly owned

5

UNITED INSURANCE HOLDINGS CORP.

subsidiaries, American Coastal and BlueLine Cayman Holdings, through a series of mergers. American Coastal is engaged in the commercial residential property and casualty insurance business and writes coverage for Florida condominiums, homeowners' associations, apartments and townhomes through AmRisc, its managing general agent. BlueLine Cayman Holdings is a Cayman Islands holding company that holds an interest in BlueLine Re, a protected cell whose sole business is the entry into and performance of quota share agreements. At the effective time of the mergers, each issued and outstanding share of common stock of AmCo will be converted into shares of common stock of UIHC equal to 209,563.55 multiplied by the lesser of (a) one and (b) a fraction, the numerator of which is 130% of $14.81 and the denominator of which is the 30-day trailing volume-weighted average closing stock price of UIHC common stock as of the day of the closing of the mergers. Immediately following the completion of the mergers, current UIHC stockholders and RDX members will own approximately 51% and 49% of the outstanding shares of UIHC common stock, respectively.

PRODUCTS AND DISTRIBUTION

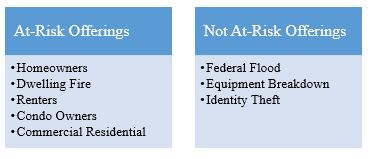

Homeowners policies and related coverage account for the vast majority of the business that we write, but we are diversifying by product as well as geography. We offer the following insurance products:

On our flood, equipment breakdown and identity theft policies, we earn a commission while retaining no risk of loss, since all such risk is ceded to other private companies and the federal government via the National Flood Insurance Program. Policies we issue under our homeowners' programs in the various states where we conduct business provide structure, content and liability coverage. We offer standardized policies for a broad range of exposures, and our policies include coverage options for standard single-family homeowners, renters, and condominium unit owners.

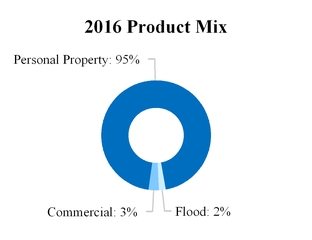

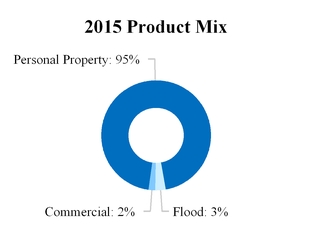

In 2016, personal property policies (by which we mean both standard homeowners', dwelling fire, renters and condo owners' policies) produced written premium of $669,007,000 and accounted for 95% of our total gross written premium. The remaining product mix is categorized between commercial residential and flood and has been distributed as seen below for 2016 and 2015.

We have developed a unique and proprietary homeowners' product we refer to as "UPC 1.0". This new product uses a granular approach to pricing for catastrophe perils. Our objective is to create specific geographic areas such that within each territory or "catastrophe band" the expected losses are within a specified range of error or approximation from a central estimate. These areas may have millions of data points that help us create distance-to-coast factors that provide a sophisticated

6

UNITED INSURANCE HOLDINGS CORP.

market segmentation that is highly correlated to our risk exposure and reinsurance costs. UPC 1.0 has been filed and approved for use in Florida, Connecticut, Georgia, Louisiana, New Jersey, South Carolina and Texas and we plan to file it for use in all our states.

We currently market and distribute our policies to consumers through approximately 12,000 independent agents representing over 7,500 agencies. UPC Insurance has focused on the independent agency distribution channel since its inception, and we believe we have built significant credibility and loyalty with the independent agent communities in the states in which we operate. We recruit, train and appoint the full-service insurance agencies that distribute our products. Typically, a full-service agency is small to medium in size and represents several insurance companies for both personal and commercial product lines. We depend heavily upon our independent agents to produce new business for us. We compensate our independent agents primarily with fixed-rate commissions that we believe are consistent with those generally prevailing in the market. In addition to our relationships with individual agencies, we have important relationships with aggregators of underlying agency demand. The two most significant of these relationships are with Allstate in Florida, which, through its Ivantage program, refers homeowners to our company and other partner companies, and with the Florida Association of Insurance Agents (FAIA), which serves as a conduit between UPC Insurance and many smaller agencies in Florida with whom we do not have direct appointments.

Our sales representatives monitor and support our agents and also have the principal responsibility for recruiting and training our new agents. We manage our relationships with independent agents through periodic business reviews using established benchmarks and goals for premium volume and profitability.

7

UNITED INSURANCE HOLDINGS CORP.

GEOGRAPHIC MARKETS

UPC Insurance Company began operations in Florida in 1999, and has operated continuously there since that time. In 2010, we began writing business outside of Florida and we currently write business in twelve states. The table below shows the years in which we began to actively write in each state:

State | Year Became Active |

Florida | 1999 |

South Carolina | 2010 |

Massachusetts | 2011 |

Rhode Island | 2012 |

North Carolina | 2013 |

New Jersey | 2013 |

Texas | 2013 |

Louisiana | 2014 |

Georgia | 2015 |

Hawaii | 2015 |

Connecticut | 2016 |

New York | 2016 |

UPC Insurance is also licensed to write, but has not commenced writing business in Alabama, Delaware, Maryland, Mississippi, New Hampshire, and Virginia. It is a fundamental part of our strategy to diversify our operations outside of Florida and to write in multiple states where the perceived threat of natural catastrophes has caused large national insurance companies to reduce their concentration.

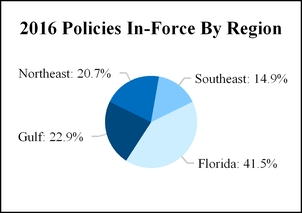

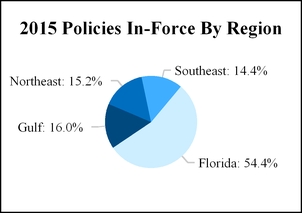

The table below shows the geographic distribution of our 451,155 policies in-force as of December 31, 2016, and 347,015 policies in-force as of December 31, 2015.

Policies In-Force By Region (1) | 2016 Policies | % | 2015 Policies | % | ||||||||

Florida | 187,414 | 41.5 | % | 188,748 | 54.4 | % | ||||||

Gulf | 103,207 | 22.9 | 55,555 | 16.0 | ||||||||

Northeast | 93,258 | 20.7 | 52,738 | 15.2 | ||||||||

Southeast | 67,276 | 14.9 | 49,974 | 14.4 | ||||||||

Total | 451,155 | 100.0 | % | 347,015 | 100.0 | % | ||||||

(1) Each region is comprised of the following states: Gulf includes Hawaii, Louisiana and Texas, Northeast includes Connecticut, Massachusetts, New Jersey, New York and Rhode Island, and Southeast includes Georgia, North Carolina and South Carolina.

8

UNITED INSURANCE HOLDINGS CORP.

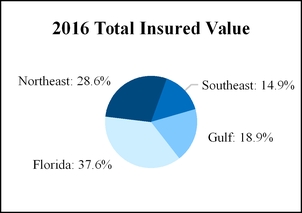

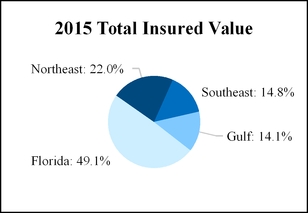

As of December 31, 2016, our total insured value of all polices in-force was approximately $214,114,964,000, an increase of $54,509,072,000, or 34.2%, from the same date in 2015. We have approximately 37.6% of our total insured value in Florida compared to roughly 49.1% as of December 31, 2015. The following table provides evidence of our improving geographic diversification by illustrating the breakdown of total insured value:

Total Insured Value By Region (1) | 2016 TIV | % | 2015 TIV | % | ||||||||||

Florida | $ | 80,444,296 | 37.6 | % | $ | 78,539,211 | 49.1 | % | ||||||

Northeast | 61,327,280 | 28.6 | 34,920,238 | 22.0 | ||||||||||

Gulf | 40,411,989 | 18.9 | 22,467,968 | 14.1 | ||||||||||

Southeast | 31,931,399 | 14.9 | 23,678,475 | 14.8 | ||||||||||

Total | $ | 214,114,964 | 100.0 | % | $ | 159,605,892 | 100.0 | % | ||||||

(1) Each region is comprised of the following states: Gulf includes Hawaii, Louisiana and Texas, Northeast includes Connecticut, Massachusetts, New Jersey, New York and Rhode Island, and Southeast includes Georgia, North Carolina and South Carolina.

9

UNITED INSURANCE HOLDINGS CORP.

COMPETITION

Our target market for homeowners' insurance, our primary product offering, includes the 18 states in which we are currently licensed plus the State of Maine where we plan to obtain a license at some point in the future. The following table summarizes the homeowners' insurance market countrywide for the year ending December 31, 2016, the date for which the most current data is available:

Countrywide Property Insurance Market - 2016 Homeowners DWP * | ||||||||

2016 Rank | Company Name | Direct Written Premium | Market Share | |||||

1 | State Farm Group | $ | 17,613,109 | 19.3 | % | |||

2 | Allstate Insurance Group | 7,903,530 | 8.7 | % | ||||

3 | Liberty Mutual Group | 6,164,379 | 6.8 | % | ||||

4 | Farmers Insurance Group | 5,515,277 | 6.0 | % | ||||

5 | USAA Group | 5,341,021 | 5.9 | % | ||||

6 | Travelers Group | 3,387,144 | 3.7 | % | ||||

7 | Nationwide Corp. Group | 3,299,236 | 3.6 | % | ||||

8 | American Family Insurance Group | 2,855,835 | 3.1 | % | ||||

9 | Chubb Ltd. Group | 2,697,841 | 3.0 | % | ||||

10 | Erie Insurance Group | 1,538,085 | 1.7 | % | ||||

11 | Auto Owners Group | 1,246,574 | 1.4 | % | ||||

12 | Metropolitan Group | 1,135,803 | 1.2 | % | ||||

13 | Hartford Fire & Casualty Group | 1,113,000 | 1.2 | % | ||||

14 | American International Group | 1,093,643 | 1.2 | % | ||||

15 | Progressive Group | 925,018 | 1.0 | % | ||||

16 | Universal Insurance Holdings Group | 880,902 | 1.0 | % | ||||

17 | CSAA Insurance Group | 874,444 | 1.0 | % | ||||

18 | Auto Club Enterprises Insurance Group | 857,774 | 0.9 | % | ||||

19 | Amica Mutual Group | 777,210 | 0.9 | % | ||||

20 | Country Insurance & Financial Services Group | 672,139 | 0.7 | % | ||||

21 | AmTrust, NGH Group | 668,332 | 0.7 | % | ||||

22 | United Insurance Holdings Group | 627,825 | 0.7 | % | ||||

23 | Tower Hill Insurance Group | 607,919 | 0.7 | % | ||||

24 | Assurant, Inc. Group | 558,206 | 0.6 | % | ||||

25 | The Hanover Insurance Group | 551,336 | 0.6 | % | ||||

Total - Top 25 Insurers | 68,905,582 | 75.6 | % | |||||

Total - All Insurers | $ | 91,276,900 | 100.0 | % | ||||

* The information displayed in the table above is compiled and published by the National Association of Insurance Commissioners (NAIC) as of December 31, 2016 based on information filings submitted annually by all licensed insurance companies. The information above is presented on a consolidated or aggregated basis for each insurance company group. The amounts shown in the table above are also on a statutory basis and exclude non-Homeowners lines of business that are included in the Company's total direct written premium for 2016.

We compete primarily on the basis of product features, the strength of our distribution network, high-quality service to our agents and policyholders, and our reputation for long-term financial stability and commitment. Our long and successful track record writing homeowners insurance in catastrophe-exposed areas has enabled us to develop sophisticated pricing techniques that endeavor to accurately reflect the risk of loss while allowing us to be competitive in our target markets. This pricing segmentation approach allows us to offer products in areas that have a high demand for property insurance yet are under-served by the national carriers.

10

UNITED INSURANCE HOLDINGS CORP.

We price our product at levels that we project will generate an acceptable underwriting profit. We try to be extremely granular in our approach, so that our price can accurately reflect the risk and profitability of each potential customer. In our pricing algorithm, we consider insurance credit scores (where allowable) and historical attritional loss costs for the rating territory in which the customer resides, as well as projected reinsurance costs based on the specific geographic and structural characteristics of the home. In addition to the specific characteristics of the policy being priced, we also evaluate the reinsurance cost of each incremental policy on our portfolio as a whole. In this regard, we seek to optimize our portfolio by diversifying our geographic exposure in order to limit our probable maximum loss, total insured value and average annual loss. We use the output from third-party modeling software to analyze our risk exposures, including wind exposures, by zip code or street address as part of the optimization process.

We have established underwriting guidelines designed to provide a uniform approach to our risk selection and designed to achieve underwriting profitability. Our underwriters review the property inspection report during their risk evaluation and if the policy does not meet our underwriting criteria, we have the right to cancel the policy within 90 days in Florida and within 60 days in other states.

We strive to provide excellent service to our independent agents and our policyholders. We continue to enhance our web-based systems which allow our agents to prepare and process new policies and policy changes online and deliver policy declarations quickly. We work with a select group of third party vendors to develop, manage and maintain our information technology systems. This allows us to obtain up-to-date technology at a reasonable cost and to achieve economies of scale without incurring significant fixed-overhead expenses. As agent and consumer behaviors evolve we continue to enhance our technology platforms to offer solutions that meet their needs.

REGULATION

We are subject to extensive regulation in the markets we serve, primarily at the state level. In general, these regulations are designed to protect the interests of insurance policyholders. They have a substantial effect on our business and relate to a wide variety of matters, including insurer solvency, reserve adequacy, insurance company licensing and examination, agent and adjuster licensing, policy forms, rate setting, the nature and amount of investments, claims practices, participation in shared markets and guaranty funds, transactions with affiliates, the payment of dividends, underwriting standards, statutory accounting methods, trade practices, and corporate governance. Some of these matters are discussed in more detail below. From time to time, individual states and/or the National Association of Insurance Commissioners (NAIC) propose new regulations and/or legislation that affect us. We can neither predict whether any of these proposals in the various jurisdictions might be adopted, nor what effect, if any, their adoption may have on our results of operations or financial condition. For a discussion of statutory financial information and regulatory contingencies, see Note 13 to our Notes to Consolidated Financial Statements which is incorporated in this Part I, Item 1 by reference.

Our insurance affiliates provide audited statutory financial statements to the various insurance regulatory authorities. With regard to periodic examinations of an insurance company's affairs, insurance regulatory authorities, in general, defer to the insurance regulatory authority in the state in which an insurer is domiciled; however, insurance regulatory authorities from any state in which we operate may conduct examinations at their discretion. UPC is domiciled in Florida, FSIC is domiciled in Hawaii, and IIC is domiciled in New York.

The ratio of gross and net premiums written to statutory surplus is a common measure of operating leverage used in the property-casualty insurance industry and serves as an indicator of a company’s premium growth capacity. Florida state law requires insurance companies to maintain premium-to-surplus ratios not in excess of 10:1 and 4:1 for gross premiums-to-surplus and net premiums-to-surplus, respectively. The table below shows the premium-to-surplus ratios for our Florida regulated entity at December 31, 2016 and 2015.

December 31, | ||||||

2016 | 2015 | |||||

UPC (1) | ||||||

Gross premiums-to-surplus ratio | 3.7 | 3.7 | ||||

Net premiums-to-surplus ratio | 2.2 | 2.5 | ||||

(1) Florida insurance statute §624.4095 requires property insurance premiums to be multiplied by a factor of 90%

for the purposes of this calculation

11

UNITED INSURANCE HOLDINGS CORP.

Risk-Based Capital Requirements

To enhance the regulation of insurer solvency, the NAIC has published risk-based capital (RBC) guidelines for insurance companies designed to assess capital adequacy and to raise the level of protection statutory surplus provides for policyholders. The guidelines measure three major areas of risk facing property and casualty insurers: (i) underwriting risks, which encompass the risk of adverse loss developments and inadequate pricing; (ii) declines in asset values arising from credit risk; and (iii) other business risks. Most states, including Florida, Hawaii and New York, have enacted the NAIC guidelines as statutory requirements, and insurers having less statutory surplus than required will be subject to varying degrees of regulatory action, depending on the level of capital inadequacy. Insurance regulatory authorities could require our insurance subsidiaries to cease operations in the event it fails to maintain the required statutory capital.

The level of required risk-based capital is calculated and reported annually. There are five outcomes to the RBC calculation set forth by the NAIC which are as follows:

1. | No Action Level - If RBC is greater than 200%, no further action is required. |

2. | Company Action Level - If RBC is between 150% -200%, the insurer must prepare a report to the regulator outlining a comprehensive financial plan that identifies conditions that contributed to the insurer's financial condition and proposes corrective actions. |

3. | Regulatory Action Level - If RBC is between 100% -150%, the state insurance commissioner is required to perform any examinations or analyses to the insurer's business and operations that he or she deems necessary as well as issuing appropriate corrective orders. |

4. | Authorized Control Level - If RBC is between 70% - 100%, this is the first point that the regulator may take control of the insurer even if the insurer is still technically solvent and is in addition to all the remedies available at the higher action levels. |

5. | Mandatory Control Level - If RBC is less than 70%, the regulator is required to take steps to place the insurer under its control regardless of the level of capital and surplus. |

At December 31, 2016, UPC's, FSIC's, and IIC's RBC ratios were 339%, 433%, and 867% respectively.

Underwriting and Marketing Restrictions

During the past several years, various regulatory and legislative bodies have adopted or proposed new laws or regulations to address the cyclical nature of the insurance industry, catastrophic events and insurance capacity and pricing. These regulations (i) created “market assistance plans” under which insurers are induced to provide certain coverage; (ii) restrict the ability of insurers to reject insurance coverage applications, to rescind or otherwise cancel certain policies in mid-term, and to terminate agents; (iii) restrict certain policy non-renewals and require advance notice on certain policy non-renewals; and (iv) limit rate increases or decrease rates permitted to be charged.

Most states also have insurance laws requiring that rate schedules and other information be filed with the insurance regulatory authority, either directly or through a rating organization with which the insurer is affiliated. The insurance regulatory authority may disapprove a rate filing if it finds that the rates are inadequate, excessive or unfairly discriminatory.

Most states require licensure or insurance regulatory authority approval prior to the marketing of new insurance products. Typically, licensure review is comprehensive and includes a review of a company’s business plan, solvency, reinsurance, character of its officers and directors, rates, forms and other financial and non-financial aspects of a company. The insurance regulatory authorities may prohibit entry into a new market by not granting a license or by withholding approval.

Limitations on Dividends by Insurance Subsidiaries

As a holding company with no significant business operations of our own, we rely on payments from our insurance affiliates as one of the principal sources of cash to pay dividends and meet our obligations. Our insurance affiliates are regulated as property and casualty insurance companies and their ability to pay dividends is restricted by Florida, Hawaii and New York law.

12

UNITED INSURANCE HOLDINGS CORP.

The state laws of Florida, Hawaii, and New York permit an insurer to pay dividends or make distributions out of that part of statutory surplus derived from net operating profit and net realized capital gains or adjusted net investment income. The state laws further provide calculations to determine the amount of dividends or distributions that can be made without the prior approval of the insurance regulatory authorities and the amount of dividends or distributions that would require prior approval of the insurance regulatory authorities in those states. Statutory risk-based capital requirements may further restrict our insurance affiliates' ability to pay dividends or make distributions if the amount of the intended dividend or distribution would cause statutory surplus to fall below minimum risk-based capital requirements.

For additional information regarding those restrictions, see Part II, Item 5 of this report.

Insurance Holding Company Regulation

As a holding company of insurance subsidiaries, we are subject to laws governing insurance holding companies in Florida, Hawaii and New York. These laws, among other things, (i) require us to file periodic information with the insurance regulatory authority, including information concerning our capital structure, ownership, financial condition and general business operations, (ii) regulate certain transactions between our affiliates and us, including the amount of dividends and other distributions and the terms of surplus notes and (iii) restrict the ability of any one person to acquire certain levels of our voting securities without prior regulatory approval. Any purchaser of 5% or more of the outstanding shares of our common stock could be presumed to have acquired control of us unless the insurance regulatory authority, upon application, determines otherwise.

Insurance holding company regulations also govern the amount any affiliate of the holding company may charge our insurance affiliates for services (i.e., management fees and commissions). We have a long-term management agreement between UPC and UIM, which presently provides for monthly management fees. The Florida Office of Insurance Regulation must approve any changes to this agreement.

We also have a management agreement between FSIC and FSU, which presently provides for monthly management fees. The Hawaii Insurance Division must approve any changes to this agreement.

The New York Department of Financial Services does not permit the use of a managing general agent and therefore we do not have a management agreement between IIC and any other company. Instead, UPC Insurance allocates a portion of relevant expenses to IIC for statutory accounting purposes.

FINANCIAL STABILITY RATING

Financial stability ratings are important to insurance companies in establishing their competitive position and such ratings may impact an insurance company’s ability to write policies. Demotech maintains a letter-scale financial stability rating system ranging from A** (A double prime) to L (licensed by insurance regulatory authorities); they have assigned our insurance subsidiaries a financial stability rating of A, which is the third highest of six rating levels. According to Demotech, "Regardless of the severity of a general economic downturn or deterioration in the insurance cycle, insurers earning a Financial Stability Rating of A possess Exceptional financial stability related to maintaining surplus as regards policyholders at an acceptable level.” With a financial stability rating of A, we expect our property insurance policies will be acceptable to the secondary mortgage marketplace and mortgage lenders. This rating is intended to provide an independent opinion of an insurer’s financial strength and is not an evaluation directed at our investors. At least annually, based on year-to-date results as of the third quarter, Demotech reviews our rating and may revise it upward or downward or revoke it at their sole discretion.

EMPLOYEES

As of March 2017, we have 167 full time employees, which includes our executive officers. We are neither party to any collective bargaining agreements nor have we experienced any work stoppages or strikes as a result of labor disputes. We believe we have good working relationships with our employees.

AVAILABLE INFORMATION

We make available, free of charge through our website, www.upcinsurance.com, our Annual Report, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such materials with, or furnish them to, the SEC.

13

UNITED INSURANCE HOLDINGS CORP.

These reports may also be obtained at the SEC’s Public Reference Room at 100 F Street NE, Washington, D.C. 20549. Information on the operation of the Public Reference Room is available by calling the SEC at 1-800-SEC-0330. You may also access this information at the SEC’s website (www.sec.gov). This site contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

14

UNITED INSURANCE HOLDINGS CORP.

Item 1A. Risk Factors

Many factors affect our business and results of operations, some of which are beyond our control. Additional risks and uncertainties we are unaware of, or we currently deem immaterial, also may become important factors that affect us. If any of the following risks occur, our business, financial conditions or results of operations may be materially and adversely affected. In that event, the trading price of our securities could decline, and our stockholders could lose all or part of their investment in our securities. This discussion contains forward-looking statements. See the section entitled FORWARD-LOOKING STATEMENTS for a discussion of uncertainties, risks and assumptions associated with these statements.

RISKS RELATED TO OUR BUSINESS

As a property and casualty insurer, we may experience significant losses, and our financial results may vary from period to period, due to our exposure to catastrophic events and severe weather conditions, the incidence and severity of which could be affected by climate change.

Our property and casualty insurance operations expose us to risks arising from catastrophes. Catastrophes can be caused by various natural events, including hurricanes, windstorms, earthquakes, hail, severe winter weather and fires; they can also be man-made, such as terrorist attacks (including those involving nuclear, biological, chemical or radiological events) or consequences of war or political instability. We may incur catastrophe losses that exceed the amount of:

•catastrophe losses that we experienced in prior years;

•catastrophe losses that, using third-party catastrophe modeling software, we projected could be incurred;

•catastrophe loss estimates that we used to develop prices for our products; or

•our current reinsurance coverage (which would cause us to have to pay such excess losses).

The incidence and severity of weather conditions are largely unpredictable, but the frequency and severity of property claims generally increase when severe weather conditions occur. Climate change, to the extent that it may affect weather patterns, may cause an increase in the frequency and/or the severity of catastrophic events or severe weather conditions which, in addition to the attendant increase in claims-related costs, may also cause an increase in our reinsurance costs and/or negatively impact our ability to provide homeowners insurance to our policyholders in the future. Governmental entities may also respond to climate change by enacting laws and regulations that may increase our cost of providing homeowners insurance in the future, which could adversely affect demand.

Catastrophes may have a material adverse effect on our results of operations during any reporting period due to increases in our loss and loss adjustment expense. Catastrophes may also cause us to increase our reserve for unpaid losses and loss adjustment expenses, which could materially harm our financial condition and our liquidity and could impair our ability to raise capital on acceptable terms or at all. In addition to catastrophes, the accumulation of losses from several smaller weather-related events in any reporting period may have a similar impact to our results of operations and financial condition.

Because we conduct a significant portion of our business in Florida, our financial results substantially depend on the regulatory, economic and weather conditions present in that state.

A significant portion of our policies in-force is concentrated in Florida. Moreover, if our proposed merger with AmCo Holding Company (“AmCo”) and its wholly owned subsidiaries (including American Coastal Insurance Company) is completed, our risk exposure in Florida will significantly increase because substantially all of AmCo’s business is conducted in respect of risk located in the State of Florida. Therefore, the prevailing regulatory, legal, economic, political, demographic, competitive, weather and other conditions in Florida will likely have a more significant impact on our revenues and profitability compared to such conditions in other jurisdictions in which we operate. Furthermore, changes in conditions could make doing business in Florida less attractive for us, which could have a more pronounced effect on us than it would on other insurance companies that are more geographically diversified.

In addition, due to Florida’s climate, we are subject to increased exposure to certain catastrophic events such as hurricanes, as well as an increased risk of losses. The occurrence of one or more catastrophic events or other conditions affecting losses in Florida may cause a material adverse effect on our results of operations and financial condition.

15

UNITED INSURANCE HOLDINGS CORP.

Our diversification strategy may not be effective.

Although we intend to continue focusing on Florida as a key market for our insurance products, we plan to take advantage of prudent opportunities to expand our core business into other states where we believe the potential for underwriting profit is strong. However, we may not be successful in this diversification strategy due to several factors, including the difficulties of finding appropriate expansion opportunities and the challenges of operating in new and unfamiliar markets.

Because we rely on insurance agents, the loss of these agent relationships or our ability to attract new agents could have an adverse impact on our business.

We currently market our policies to a broad range of prospective policyholders through approximately 12,000 independent agents representing over 7,000 agencies. Many of these agents are independent insurance agents that own their customer relationships, and our agency contracts with them limit our ability to directly solicit business from our existing policyholders. Independent agents commonly represent other insurance companies and we do not control their activities. Historically, we have used marketing relationships with two well-known national insurance companies that do not write new homeowners insurance policies in Florida and two associations of independent insurance agents in Florida to attract and retain agents and agency groups. The loss of these marketing relationships could adversely impact our ability to attract new agents or retain our agency network. Failure to grow or maintain our agency relationships or a failure to attract new agents could adversely affect sales of our insurance products.

Additionally, AmCo’s subsidiary, American Coastal Insurance Company (“American Coastal”), has an exclusive contract with AmRisc, pursuant to which AmRisc serves as American Coastal’s exclusive managing general agent for binding and writing commercial residential property lines for condominium, townhome and homeowners association insurance written in Florida. Under that contract, AmRisc must produce a certain volume of business for American Coastal. Therefore, if our proposed acquisition of AmCo (including American Coastal) is completed, failure of AmRisc to produce the required volume of business could cause the combined company to lose substantial premiums and could require us to seek one or more alternative managing general agents. If we were unable to find a replacement managing general agent or otherwise increase the production of premiums, our revenues could decrease, which could have a material adverse effect on our business, financial condition and results of operations.

Actual claims incurred may exceed our loss reserves for claims, which could adversely affect our results of operations and financial condition.

Loss reserves represent our estimate of ultimate unpaid losses for claims that have been reported and claims that have been incurred but not yet reported. Loss reserves do not represent an exact calculation of liability, but instead represent our best estimate, generally utilizing actuarial expertise, historical information and projection techniques at a given reporting date.

The process of estimating our loss reserves involves a high degree of judgment and is subject to a number of variables. These variables can be affected by both internal and external events, such as changes in claims handling procedures, economic inflation, legal trends, legislative changes, and varying judgments and viewpoints of the individuals involved in the estimation process, among others.

Because of the inherent uncertainty in estimating loss reserves, including reserves for catastrophes, additional liabilities resulting from one insured event, or an accumulation of insured events, may exceed our existing loss reserves. If our reserves are inadequate, it may cause us to overstate our earnings for the periods during which our reserves for expected losses was insufficient.

Our financial results may vary from period to period based on the timing of our collection of government-levied assessments from our policyholders.

Our insurance affiliates are subject to assessments levied by various governmental and quasi-governmental entities in the states in which we operate. While we may have the ability to recover these assessments from policyholders through policy surcharges in some states in which we operate, our payment of the assessments and our recoveries may not offset each other in the same reporting period in our financial statements and may cause a material adverse effect on our results of operations in a particular reporting period.

16

UNITED INSURANCE HOLDINGS CORP.

Our failure to implement and maintain adequate internal controls over financial reporting in our business could have a material adverse effect on our business, financial condition, results of operations and stock price.

“Internal controls over financial reporting” refer to those procedures within a company that are designed to reasonably ensure the accuracy of the company’s financial statements. Section 404 of the Sarbanes-Oxley Act of 2002 requires our management to annually assess the effectiveness of our internal controls over financial reporting. Based on its most recent assessment, management believes that our internal controls during 2016 and 2015 were effective.

If we fail to achieve and maintain adequate internal controls, or if we have material weaknesses in our internal controls, in each case in accordance with applicable standards, we may be unable to conclude on an ongoing basis that we have effective internal controls over financial reporting in accordance with Section 404. Because effective internal controls are necessary for us to produce reliable financial reports, our business, financial condition and results of operations could be harmed, investors could lose confidence in our reported financial information, and the market price for our stock could decline if our internal controls are ineffective or if material weaknesses in our internal controls are identified. Moreover, if we complete our merger with AmCo, any deficiencies or material weaknesses in AmCo’s internal controls over financial reporting could also have a material adverse impact on the combined company for the above-mentioned reasons.

If we experience difficulties with technology, data security and/or outsourcing relationships, our ability to conduct our business could be negatively impacted.

While technology can streamline many business processes and ultimately reduce the cost of operations, technology initiatives present certain risks. Our business is highly dependent upon our information technology systems and upon our contractors' and third-party administrators' ability to perform, in an efficient and uninterrupted fashion, necessary business functions such as the processing of policies and the adjusting of claims. Because our information technology and telecommunications systems interface with and often depend on these third-party systems, we could experience service denials if demand for such service exceeds capacity or a third-party system fails or experiences an interruption. If sustained or repeated, such a business interruption, system failure or service denial could result in a deterioration of our ability to write and process new and renewal business, provide customer service, pay claims in a timely manner or perform other necessary business functions.

Despite our implementation of security measures, our information technology systems are vulnerable to computer viruses, natural disasters, unauthorized access, cyber-attacks, system failures and similar disruptions. A material breach in the security of our information technology systems and data could include the theft of our confidential or proprietary information, including trade secrets and the personal information of our customers, claimants and employees. From time to time, we have experienced threats to our data and information technology systems, including malware and computer virus attacks, unauthorized access, system failures and disruptions. To the extent that any disruptions or security breaches result in a loss or damage to our data or inappropriate disclosure of proprietary or confidential information, it could cause significant damage to our reputation, adversely affect our relationships with our customers, result in litigation, increased costs and/or regulatory penalties, and ultimately harm our business. Third parties to whom we outsource certain of our functions are also subject to the risks outlined above, any one of which may result in our incurring substantial costs and other negative consequences, including a material adverse effect on our business, financial condition, results of operations and liquidity.

Loss of key vendor relationships or failure of a vendor to protect personal information of our customers, claimants or employees could affect our operations.

We rely on services and products provided by many third-party vendors. These include, for example, vendors of computer hardware and software and vendors of services such as claim adjustment services and human resource benefits management services. In the event that one or more of our vendors suffers a bankruptcy or otherwise becomes unable to continue to provide products or services, or fails to protect personal information of our customers, claimants or employees, we may suffer operational impairments and financial losses. Moreover, in the event of a data breach involving any of our third-party vendors, our customers’ data and personal information could also be put at risk. For example, many of the recent significant data breaches were a result of security breaches of third-party vendors. Any such data breach involving our third-party vendors could result in significant mitigation or legal expenses for us, which could materially and adversely affect our results of operations and financial condition.

17

UNITED INSURANCE HOLDINGS CORP.

Our success has been and will continue to be greatly influenced by our ability to attract and retain the services of senior management.

Our senior executive officers play an integral role in the development and management of our business. We cannot guarantee that any such officers will continue their employment with us. Additionally, we do not maintain any key person life insurance policies on any of our officers or employees. The loss of the services of any of our senior executive officers could have an adverse effect on our business, financial condition, results of operations, cash flows and/or future prospects.

Our acquisitions and other strategic transactions may be difficult to integrate, divert management resources, result in unanticipated costs or dilute our stockholders.

Part of our continuing business strategy is to evaluate opportunities to merge with and acquire companies that complement our business model or make other strategic transactions that facilitate or expedite the accomplishment of our business goals. Even if we enter into an agreement in respect of a merger with or acquisition of another business, we may not be able to finalize a transaction after significant investment of time and resources, including our proposed merger with AmCo. Further, we may not have the ability to finalize a transaction due to a lack of regulatory approval or imposition of a burdensome condition by the regulator.

In connection with an acquisition or merger, we could incur debt, amortization expenses related to intangible assets, large and immediate write-offs, assume liabilities or issue stock that would dilute our current stockholders' percentage of ownership. As a result, there is a risk of transaction related litigation. Such transactions could pose numerous risks to our operations, including:

• | incurring substantial unanticipated integration costs; |

• | assimilating the acquired businesses may divert significant management attention and financial resources from our other operations and could disrupt our ongoing business; |

• | acquisitions and mergers could result in the loss of key employees, particularly those of the acquired operations; |

• | difficulty retaining the acquired business' customers; |

• | failing to realize the strategic benefits or the potential cost savings or other financial benefits of the acquisitions or mergers; and |

• | incurring unanticipated liabilities or claims from the acquired businesses and contractually-based time and monetary limitations on the seller's obligation to indemnify us for such liabilities or claims. |

We are also subject to a certain level of risk regarding the actual condition of the businesses that we acquire. Until we actually assume operating control of such businesses and their assets and operations, we may not be able to ascertain the actual value or understand the potential liabilities of the acquired entities and their operations. As a result, we may not be able to complete acquisitions or mergers or integrate the operations, products or personnel gained through any such acquisition or merger without a material adverse effect on our business, financial condition and results of operations, including our proposed merger with AmCo, which has not yet been consummated.

RISKS RELATED TO THE INSURANCE INDUSTRY

Because we are operating in a highly competitive market, we may lack the resources to increase or maintain our market share.

The property and casualty insurance industry is highly competitive, and we believe it will remain highly competitive for the foreseeable future. The principal competitive factors in our industry are price, service, commission structure and financial condition. We compete with other property and casualty insurers that write coverage in the same geographic areas in which we write coverage and some of those insurers have greater financial resources and have a longer operating history than we do. In addition, our competitors may offer products for alternative forms of risk protection that we presently do not offer, which could adversely affect the sales of our products. Competition could limit our ability to retain existing business or to write new business at adequate rates, and such limitation may cause a material adverse effect on our results of operations and financial position.

18

UNITED INSURANCE HOLDINGS CORP.

Changes in state regulation may adversely affect our results of operation and financial condition.

As an insurance company, we are subject to the laws and regulations of the various states in which we operate. From time to time, states have passed legislation, and regulators have taken action, that has the effect of limiting the ability of insurers to manage catastrophe risk, such as legislation prohibiting insurers from reducing exposures or withdrawing from catastrophe-prone areas, or mandating that insurers participate in residual markets. In addition, following catastrophes, legislative initiatives and court decisions can seek to expand insurance coverage for catastrophe claims beyond the original intent of the policies, which could cause our actual loss and loss adjustment expense to exceed our estimates. Further, our ability to increase pricing to the extent necessary to offset rising costs of catastrophes requires approval of insurance regulatory authorities.

One example of such legislation occurred following the 2004 and 2005 hurricane seasons, when the Florida legislature required all insurers issuing replacement cost policies to pay the full replacement cost of damaged properties without depreciation, whether or not the insureds repaired or replaced the damaged property. Under prior law, insurers paid the depreciated amount of damaged property on covered losses until an insured commenced repairs or replacement. Under the current law, there is an increase in disputes over the amount of loss, since full payment is made before actual repairs begin and without documentation supporting the actual cost of repair. Despite our efforts to promptly calculate and pay meritorious amounts, our operating results have been affected by the change in law, coupled with a claims environment in Florida that creates opportunities for fraudulent or overstated claims.

Our ability or willingness to manage our catastrophe exposure by raising prices, modifying underwriting terms or reducing exposure to certain geographies may be limited due to considerations of public policy, the evolving political environment and our ability to penetrate other geographic markets, which may cause a material adverse effect on our results of operations, financial condition and cash flows. We cannot predict whether and to what extent the adoption of new legislation and regulations would affect our ability to manage our exposure to catastrophic events.

The insurance industry is heavily regulated and further restrictive regulation may reduce our profitability and limit our growth.

The insurance industry is extensively regulated and supervised. Insurance regulatory authorities generally design insurance rules and regulations to protect the interests of policyholders, and not necessarily the interests of insurers, their stockholders, and other investors. We are subject to comprehensive regulation and supervision by state insurance departments in all states in which our insurance subsidiaries are domiciled, as well as all states in which they are licensed, sell insurance products, issue policies, or handle claims. The regulations of each state are unique and complex and subject to change, and certain states may have regulations that conflict with the regulations of other states in which we operate. As a result, we are subject to the risk that compliance with the regulations in one state may not result in compliance with the regulations in another state.

State statutes and administrative rules generally require each insurance company to register with the department of insurance in its state of domicile and to furnish information concerning the operations of the companies within the holding company system which may materially affect the operations, management or financial condition of the insurers. As part of its registration, each insurance company must identify material agreements, relationships and transactions with affiliates, including loans, investments, asset transfers, transactions outside of the ordinary course of business, certain management, service, and cost sharing agreements, reinsurance transactions, dividends, and other financial and non-financial components of an insurer’s business. Some states impose restrictions or require prior regulatory approval of specific corporate actions, which may adversely affect our ability to operate, innovate, obtain necessary rate adjustments in a timely manner or grow our business profitably. Our ability to comply with these laws and regulations, and to obtain necessary regulatory action in a timely manner is, and will continue to be, critical to our success.

Currently, the federal government's role in regulating or dictating the policies of insurance companies is limited. However, from time to time Congress has considered and may in the future consider proposals that would increase the role of the federal government in insurance regulation, either in addition to or in lieu of state regulation.

In recent years, the state insurance regulatory framework has come under increased federal scrutiny. Changes in federal legislation, regulation and/or administrative policies in several areas, including changes in financial services regulation and federal taxation, could negatively affect the insurance industry and us. In addition, Congress and some federal agencies from time to time investigate the current condition of insurance regulation in the United States to determine whether to impose federal or national regulation or to allow an optional federal charter, similar to the option available to most banks. Further, the NAIC and state insurance regulators continually reexamine existing laws and regulations, specifically focusing on modifications to holding company regulations, interpretations of existing laws and the development of new laws and

19

UNITED INSURANCE HOLDINGS CORP.

regulations. We cannot predict what effect, if any, proposed or future legislation or NAIC initiatives may have on the manner in which we conduct our business.

As part of potential, or future, industry-wide investigations, we may from time to time receive requests for information from government agencies and authorities at the state or federal level. If we are subpoenaed for information by government agencies and authorities, potential outcomes could include law enforcement proceedings or settlements resulting in fines, penalties and/or changes in business practices that could cause a material adverse effect on our results of operations. In addition, these investigations may result in changes to laws and regulations affecting the industry.

Changes to insurance laws or regulations, or new insurance laws and regulations, may be more restrictive than current laws or regulations and could significantly increase our compliance costs, which could have a material adverse effect on our results of operations and our prospects for future growth. Additionally, our failure to comply with certain provisions of applicable insurance laws and regulations could result in significant fines or penalties being levied against us and may cause a material adverse effect on our results of operations or financial condition.

Our inability to obtain reinsurance on acceptable terms would increase our loss exposure or limit our ability to underwrite policies.

We use, and we expect to continue to use, reinsurance to help manage our exposure to property risks. Reinsurance is insurance for insurers and is fundamentally a promise by the reinsurer to pay possible future claims in exchange for the payment of a premium by the insurance company seeking reinsurance. The availability and cost of reinsurance are each subject to prevailing market conditions beyond our control, which can affect business volume and profitability. We may be unable to maintain our current reinsurance coverage, to obtain additional reinsurance coverage in the event our current reinsurance coverage is exhausted by a catastrophic event, or to obtain other reinsurance coverage in adequate amounts or at acceptable rates. Similar risks exist whether we are seeking to replace coverage terminated during the applicable coverage period or to renew or replace coverage upon its expiration. We provide no assurance that we can obtain sufficient reinsurance to cover losses resulting from one or more storms or other events in the future, or that we can obtain such reinsurance in a timely or cost-effective manner. If we are unable to renew our expiring coverage or to obtain new reinsurance coverage, either our net exposure to risk would increase or, if we are unwilling to accept an increase in net risk exposures, we would have to reduce the amount of risk we underwrite. Either increasing our net exposure to risk or reducing the amount of risk we underwrite may cause a material adverse effect on our results of operations and our financial condition.

Our inability to collect from our reinsurers on our reinsurance claims could cause a material adverse effect on our results of operation and financial condition.

We use reinsurance as a tool to manage risks associated with our business. However, we remain primarily liable as the direct insurer on all risks that we obtain reinsurance for. Our reinsurance agreements do not eliminate our obligation to pay claims to insured. As a result, we are subject to counterparty risk with respect to our ability to recover amounts due from reinsurers. The risk could arise in two situations: (i) our reinsurers may dispute some of our reinsurance claims based on contract terms, and we may ultimately receive partial or no payment, or (ii) the amount of losses that reinsurers incur related to worldwide catastrophes may materially harm the financial condition of our reinsurers and cause them to default on their obligations.

While we will attempt to manage these risks through underwriting guidelines, collateral requirements and other oversight mechanisms, our efforts may not be successful. As a result, our exposure to counterparty risk under our reinsurance agreements may cause a material adverse effect on our results of operations, financial condition and cash flow.

Our investments are subject to market risks that may result in reduced returns or losses.

We invest a portion of the premiums we collect in various securities and expect returns from our investments in these securities to contribute to our overall profitability. Accordingly, fluctuations in interest rates or in the fixed-maturity, equity or alternative-investment markets may cause a material adverse effect on our results of operations.

Changes in the general interest rate environment will affect our returns on, and the fair value of, our fixed-maturity and short-term investments. A decline in interest rates reduces the interest rate payable on new fixed income investments, thereby negatively impacting our net investment income. Conversely, rising interest rates reduce the fair value of existing fixed maturities. In addition, defaults under, or impairments of, any of these investments as a result of financial problems with the issuer and, where applicable, its guarantor could reduce our net investment income and net realized investment gains or result in investment losses.

20

UNITED INSURANCE HOLDINGS CORP.

We are subject to risks associated with potential declines in credit quality related to specific issuers and a general weakening in the economy. While we have put in place procedures designed to monitor the credit risk of our invested assets, it is possible that we may experience credit or default losses in our portfolio, which could adversely affect our results of operations and financial condition.

We may decide to invest an additional portion of our assets in equity securities or other investments, which are subject to greater volatility than fixed maturities. General economic conditions, stock market conditions and many other factors beyond our control can adversely affect the fair value of our equity securities or other investments, and could adversely affect our realization of net investment income. As a result of these factors, we may not realize an adequate return on our investments, we may incur losses on sales of our investments and we may be required to write down the value of our investments, which could reduce our net investment income and net realized investment gains or result in investment losses.

The fair value of our investment portfolio is also subject to valuation uncertainties. The valuation of investments is more subjective when the markets for these investments are illiquid and may increase the risk that the estimated fair value of our investment portfolio is not reflective of prices at which actual transactions would occur.

Our determination of the amount of other-than-temporary impairment to record varies by investment type and is based upon our periodic evaluation and assessment of known and inherent risks associated with the respective investment type. We revise our evaluations and assessments as conditions change and new information becomes available, and we reflect changes in other-than-temporary impairments in our Consolidated Statements of Comprehensive Income. We base our assessment of whether other-than-temporary impairments have occurred on our case-by-case evaluation of the underlying reasons for the decline in fair value. However, we may not accurately assess whether the impairment of one or more of our investments is temporary or other-than-temporary and the recorded amounts for other-than-temporary impairments in our financial statements may be inadequate. Furthermore, historical trends may not be indicative of future impairments and additional impairments may need to be recorded in the future.

Our portfolio may benefit from certain tax laws, including those governing dividends-received deductions and tax credits. Federal and/or state tax legislation could be enacted that would lessen or eliminate some or all of these tax advantages and could adversely affect the value of our investment portfolio. This result could occur in the context of deficit reduction or various types of fundamental tax reform.

The property and casualty insurance and reinsurance industry is historically cyclical and the pricing and terms for our products may decline, which would adversely affect our profitability.

Historically, the financial performance of the property and casualty insurance and reinsurance industry has been cyclical, characterized by periods of severe price competition and excess underwriting capacity, or soft markets, followed by periods of high premium rates and shortages of underwriting capacity, or hard markets. We cannot predict when such a period may occur or how long any given hard or soft market will last. Downturns in the property and casualty market may cause a material adverse effect on our results of operations and our financial condition.

Losses from legal actions may be material to our operating results, cash flows and financial condition.

Trends in the insurance industry regarding claims and coverage issues, such as increased litigation, the willingness of courts to expand covered causes of loss, and the escalation of loss severity may contribute to increased litigation costs and increase our loss exposure under the policies that we underwrite.

As industry practices and legal, judicial, social and other environmental conditions change, unexpected and unintended issues related to claims and coverage may emerge. Examples of emerging claims and coverage issues include, but are not limited to:

• | judicial expansion of policy coverage and the impact of new theories of liability; |

• | plaintiffs targeting property and casualty insurers in purported class-action litigation relating to claims-handling and other practices; and |

• | adverse changes in loss cost trends, including inflationary pressures in home repair costs. |

Loss severity in the property and casualty insurance industry may increase and may be driven by the effects of these and other unforeseen emerging claims and coverage issues. Multiparty or class action claims may present additional exposure to substantial economic, non-economic or punitive damage awards. The loss of even one of these claims, if it resulted in a

21

UNITED INSURANCE HOLDINGS CORP.

significant award or a judicial ruling that was otherwise detrimental, could create a precedent in our industry that could have a material adverse effect on our results of operations and financial condition. This risk of potential liability may make reasonable settlements of claims more difficult to obtain.