Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

[X]

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the fiscal year ended December 31, 2016

OR

|

|

|

[ ]

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the transition period from to

|

Commission file number 0-24960

COVENANT TRANSPORTATION GROUP, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

88-0320154

|

|

|

(State / other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

|

400 Birmingham Hwy.

|

||

|

Chattanooga, TN

|

37419

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

|

Registrant's telephone number, including area code:

|

423 - 821-1212

|

|

Securities registered pursuant to Section 12(b) of the Act:

|

$0.01 Par Value Class A Common Stock – The NASDAQ Global Select Market

|

|

(Title of class)

|

|

|

Securities registered pursuant to Section 12(g) of the Act:

|

None

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

[ ] Yes [X] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

[ ] Yes [X] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

[X] Yes [ ] No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S‑K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10‑K or any amendments to this Form 10‑K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "accelerated filer, "large accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

[ ]

|

Accelerated filer

|

[X]

|

|

Non-accelerated filer

|

[ ]

(Do not check if a smaller reporting company)

|

Smaller reporting company

|

[ ]

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

[ ] Yes [X] No

The aggregate market value of the common equity held by non-affiliates of the registrant as of June 30, 2016, was approximately $220.0 million (based upon the $18.07 per share closing price on that date as reported by NASDAQ). In making this calculation the registrant has assumed, without admitting for any purpose, that all executive officers, directors, and affiliated holders of more than 10% of a class of outstanding common stock, and no other persons, are affiliates.

As of March 10, 2017, the registrant had 15,902,290 shares of Class A common stock and 2,350,000 shares of Class B common stock outstanding.

Portions of the materials from the registrant's definitive proxy statement for the 2017 Annual Meeting of Stockholders to be held on May 16, 2017, have been incorporated by reference into Part III of this Form 10-K.

|

Part I

|

|||

|

Item 1.

|

4

|

||

|

Item 1A.

|

17

|

||

|

Item 1B.

|

30

|

||

|

Item 2.

|

30

|

||

|

Item 3.

|

30

|

||

|

Item 4.

|

31

|

||

|

Part II

|

|||

|

Item 5.

|

32

|

||

|

Item 6.

|

34

|

||

|

Item 7.

|

36

|

||

|

Item 7A.

|

57

|

||

|

Item 8.

|

58

|

||

|

Item 9.

|

58

|

||

|

Item 9A.

|

59

|

||

|

Item 9B.

|

59

|

||

|

Part III

|

|||

|

Item 10.

|

60

|

||

|

Item 11.

|

60

|

||

|

Item 12.

|

60

|

||

|

Item 13.

|

60

|

||

|

Item 14.

|

60

|

||

|

Part IV

|

|||

|

Item 15.

|

61

|

||

| Item 16. | Form 10-K Summary | 63 | |

|

64

|

||

|

65

|

||

|

Financial Data

|

||

|

66

|

||

|

67

|

||

|

68

|

||

|

69

|

||

|

70

|

||

|

71

|

||

PART I

This Annual Report on Form 10-K contains certain statements that may be considered forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended and such statements are subject to the safe harbor created by those sections and the Private Securities Litigation Reform Act of 1995, as amended. All statements, other than statements of historical or current fact, are statements that could be deemed forward-looking statements, including without limitation: any projections of earnings, revenues, or other financial items; any statement of plans, strategies, and objectives of management for future operations; any statements concerning proposed new services or developments; any statements regarding future economic conditions or performance; and any statements of belief and any statements of assumptions underlying any of the foregoing. In this Annual Report, statements relating to our ability to achieve our strategic plan, our ability to recruit and retain qualified independent contractors and qualified driver and non-driver employees, our ability to react to market conditions, our ability to gain market share, future demand for and supply of new and used tractors and trailers (including expected prices of such equipment), expected functioning and effectiveness of our information systems and other technology we implement, expected sources and adequacy of working capital and liquidity, future relationships, use, classification, compensation, and availability with respect to third-party service providers, future driver market conditions, future allocation of capital, expected settlement of operating lease obligations, future asset sales and acquisitions, future insurance, litigation, and claims levels and expenses, future tax expense and deductions, future fuel management, expense, and the future effectiveness of fuel surcharge programs and price hedges, future interest rates and effectiveness of interest rate swaps, expected capital expenditures (including the future mix of lease and purchase obligations), future asset utilization and efficiency, future trucking capacity, expected freight demand and volumes, future rates, future depreciation and amortization, future compliance with and impact of existing and proposed federal and state laws and regulations, future salaries, wages, and other employee benefit expenses, future earnings from and value of our investments, future customer relationships, future defaults under debt agreements, future unforeseen events such as strikes, work stoppages, and weather catastrophes, future acquisitions, future credit availability, future performance of our subsidiaries, and future operating and maintenance expenses, among others, are forward-looking statements. Such statements may be identified by their use of terms or phrases such as "believe," "may," "could," "expects," "estimates," "projects," "anticipates," "plans," "intends," and similar terms and phrases. Forward-looking statements are based on currently available operating, financial, and competitive information. Forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified, which could cause future events and actual results to differ materially from those set forth in, contemplated by, or underlying the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in the section entitled "Item 1A. Risk Factors," set forth below. Readers should review and consider the factors discussed in "Item 1A. Risk Factors," along with various disclosures in our press releases, stockholder reports, and other filings with the Securities and Exchange Commission.

All such forward-looking statements speak only as of the date of this Annual Report. You are cautioned not to place undue reliance on such forward-looking statements. We expressly disclaim any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in our expectations with regard thereto or any change in the events, conditions, or circumstances on which any such statement is based.

References in this Annual Report to "we," "us," "our," or the "Company" or similar terms refer to Covenant Transportation Group, Inc. and its subsidiaries.

GENERAL

Background and Strategy

We were founded in 1986 as a provider of expedited long haul freight transportation, primarily using two-person driver teams in transcontinental lanes. Since that time, we have grown from 25 tractors to approximately 2,550 tractors and expanded our services from predominantly long haul dry van to include refrigerated, dedicated, cross-border, regional, and brokerage. The expansion of our fleet and service offerings have placed us among the nation's twenty-five largest truckload transportation companies based on 2015 revenue.

Generally, we transport full trailer loads of freight from origin to destination without intermediate stops or handling. We provide truckload transportation services throughout the continental United States, into and out of Mexico, and into and out of portions of Canada. Our truckload freight services utilize equipment we own or lease or equipment owned by independent contractors for the pick-up and delivery of freight. In most of our truckload business, we transport freight over nonroutine routes. Our dedicated freight service offering provides similar transportation services, but does so pursuant to agreements whereby we make our equipment available to a specific customer for shipments over particular routes at specified times. To complement our truckload operations, we provide freight brokerage/logistics services and accounts receivable factoring services. Through our asset based and non-asset based capabilities, we transport many types of freight for a diverse customer base.

We concentrate on market sectors where we believe our capacity in relation to sector size and our operating proficiency can make a meaningful difference to customers. The primary sectors in which we operate are as follows:

● Expedited / Long haul: In our expedited / long haul business, we operate approximately 1,000 tractors, approximately 700 of which are driven by two-person driver teams. Our expedited operations primarily involve high service freight with delivery standards, such as 1,000 miles in 22 hours, or 15-minute delivery windows that are difficult for competitors to satisfy with solo-driven tractors or rail-intermodal service. Our expedited services often involve high value, high security, or time-definite loads for integrated global freight companies, less-than-truckload carriers, manufacturers, and retailers. We believe we are one of the five largest team expedited providers, and that growth in omni-channel, organic food, manufacturing, and e-commerce freight make this an attractive sector.

● Temperature-Controlled: In our temperature-controlled business, operated through our SRT subsidiary, we operate approximately 850 tractors, approximately 200 of which are driven by two-person driver teams, and also offer intermodal service in longer haul lanes. The temperature-controlled sector includes fresh and frozen foods, pharmaceuticals, cosmetics, and other freight where extreme heat or cold could cause damage. We believe we are among the ten largest temperature-controlled providers, and that factors such as United States population growth, increasing consumer preference for fresh and organic produce, and demographic trends requiring more pharmaceuticals make this an attractive sector. Improving results of operations at SRT is one of our primary goals for 2017.

● Dedicated: In our dedicated contract business, we operate approximately 700 tractors, approximately 150 of which are driven by two-person driver teams, primarily for manufacturers located in the southeastern United States. The dedicated sector typically involves longer-term contracts that allocate a specified number of tractors and trailers to a specific customer, with fixed and variable compensation. Many of our dedicated contract customers are automotive companies or shippers of produce, where the nature of the product we ship requires high service standards. We believe these sectors are growing because of an improved manufacturing environment in the United States, particularly in the Southeast, growth in organic produce, customer concerns about trucking capacity, and a need for dependable service.

● Capacity Provider Solutions and Logistics Services / Equipment Sales and Leasing: We primarily provide freight brokerage and logistics capacity to customers when the freight does not fit our network or profitability requirements. In addition, we participate in the market for used equipment sales and leasing through our 49% ownership of Transport Enterprise Leasing, LLC ("TEL"), and we assist current and potential capacity providers with improving their cash flows through secured invoice factoring services. We believe this suite of services links our interests with those of our customers and current and potential third party capacity providers. We intend to expand our presence in these sectors, which we believe offer attractive growth opportunities with lower capital investment than our truckload operations.

As our fleet has grown over three decades and our service platform matured, several important trends dramatically affected the truckload industry and our business. First, supply chain patterns became more fluid in response to dynamic changes in labor and transportation costs, ocean freight and rail-intermodal service standards, retail distribution center networks, governmental regulations, and other industry-wide factors. Second, the cost structure of the truckload business rose dramatically, particularly equipment, driver wages, and, at times, fuel prices, impacting us and our customers' freight decisions. Third, customers used technology to constantly optimize their supply chains, which necessitated expanding our own technological capability to optimize our asset allocation, manage yields, and drive operational efficiency. Fourth, a confluence of regulatory constraints, safety and security demands, and scarcity of qualified driver applicants, negatively impacted our asset productivity and reinforced what a precious resource professional truck drivers are (and we believe increasingly will be) in our industry.

While the results for 2016 were not as robust as those achieved in 2015, which provided the highest annual earnings in the Company’s 31-year history, we are proud of earning a profit for the fifth consecutive year after only producing a profit in one calendar year from 2006-2011. We believe our return to profitability on a consistent basis is the result of redefining and retooling our business model, and as the result of our strategic planning process, whereby we annually focus on five initiatives that fall under the following key tenets:

● Organizational Excellence and Entrepreneurial Spirit. We have re-aligned our management team, added talent, and implemented best practices in part through using Franklin Covey's Four Disciplines of Execution® to bring a new focus to metrics, accountability, and incentive compensation. Through multiple programs recognizing individual initiative, we have also been instilling an ownership culture throughout our company. We also implemented a single enterprise management system across all subsidiaries to improve visibility and coordination of customers, operations, and financial activities.

● Focus on the Driver. Drivers are the lifeblood of our company and our industry. We employ a broad range of safety, lifestyle, compensation, equipment technology, and personal recognition methods to convey our respect and appreciation for our drivers and to improve their careers. A portion of these techniques involve sophisticated analytics to identify likely candidates, match teams, evaluate recruiting spending, deliver training content to drivers, and design tractor specifications.

● Focus on the Customer Experience. Our mission statement begins: "CTG's mission is to be a problem solver for every customer…" We offer premium service in sectors where we can make a difference, and we use our brokerage subsidiary, Covenant Transport Solutions, Inc. ("Solutions"), to cover loads that cannot be as efficiently serviced through our Truckload segment. With each interaction, we seek to enhance the value we bring to the customer relationship.

● Rigorous Capital Allocation Process and Reduce Leverage. Our senior management annually ranks capital investment opportunities against available capital and acceptable leverage levels, and material investments must pass return on investment and capital investment committee approval processes. In addition, reducing our total leverage has been a primary strategic goal. Our leverage decreased in 2016 over 2015, as we remain focused on investing capital when we can obtain acceptable returns and reducing our leverage. We believe our disciplined investment review has contributed to our improved results by allocating capital to more profitable business units and downsizing other units into greater profitability.

● Risk Management—Assess and Mitigate. We consistently evaluate risk areas with significant volatility, as well as the costs and benefits associated with mitigating the volatility. Diesel fuel prices, insurance and claims cost, and used equipment prices are all areas where we identified significant risk and volatility for our business. To manage these risks, we have employed fuel hedging contracts on a portion of our fuel usage not covered by customer fuel surcharges, lowered our self-insured accident liability retention, and expanded our ability to sell our used equipment to increase bargaining power with the tractor and trailer manufacturers.

● Technology. We purchase and deploy technology that we believe will allow us to operate more safely, securely, and efficiently. Our information systems are integrated into a single platform that represents a multi-year investment to upgrade the hardware and software of our information systems. This technology was purchased off the shelf, which minimizes our fixed cost investment, and enables us to stay current with the latest developments.

We believe the ongoing execution of our strategic plan has contributed to the substantial improvement in operating results and profitability we have generated over the past several years. Some of the significant successes resulting from our strategic planning efforts include the completion of a follow-on stock offering in 2014 that helped significantly deleverage our balance sheet; enhancements to recruiting, retention, and business intelligence; upgraded information technology; focus on service and on time delivery; and enhanced cross-marketing opportunities between our subsidiaries. Each of these accomplishments positively impacted the success of the key initiatives identified above, our overarching financial goals, and ultimately, the Company. However, some of our key metrics and our profitability were negatively impacted in 2016 compared to 2015, and, accordingly, we still have significant work ahead to achieve our goals, deliver a strong and stable product for our customers, provide a bright future for our employees and owner-operators, and create meaningful value for our stockholders.

The Company

We operate a relatively new tractor fleet and employ sophisticated tractor technology that enhances our operational efficiencies and our drivers' safety. Our company-owned tractor fleet has an average age of approximately 1.8 years, which compares favorably to an average U.S. Class 8 tractor age of approximately 8 years in 2016. Some of the technologies we employ include the following: (1) freight optimization software that can perform sophisticated analyses of profitability and other measures on each customer, route, and load; (2) routing software that selects the best route, identifies fuel stops, and warns of deviations from routing instructions; (3) a tracking and communications system that permits direct communication between drivers and fleet managers, as well as constant location and delivery updates; (4) electronic logging devices in all of our tractors; (5) aerodynamics and other fuel efficiency systems that have significantly improved fuel mileage; and (6) safety technology, including rollover stability control, collision mitigation, and lane-change warning. We believe our modern fleet lowers maintenance costs, improves fuel mileage, improves safety, contributes to better customer service, and assists with driver retention.

Business Units

We have one reportable segment, our truckload services ("Truckload").

The Truckload segment consists of three operating fleets that are aggregated because they have similar economic characteristics and meet the aggregation criteria. The three operating fleets that comprise our Truckload segment are as follows: (i) Covenant Transport, Inc. ("Covenant Transport"), our historical flagship operation, which provides expedited long haul, dedicated, temperature-controlled, and regional solo-driver service; (ii) Southern Refrigerated Transport, Inc. ("SRT"), which provides primarily long haul, regional, dedicated, and intermodal temperature-controlled service; and (iii) Star Transportation, Inc. ("Star"), which provides regional solo-driver and dedicated services, primarily in the southeastern United States.

In addition, our Solutions subsidiary has service offerings ancillary to our Truckload operations, including: freight brokerage service directly and through freight brokerage agents, who are paid a commission for the freight they provide, and accounts receivable factoring. These operations consist of several operating segments, which neither individually nor in the aggregate meet the quantitative or qualitative reporting thresholds.

The following charts reflect the size of each of our operating subsidiaries measured by 2016 total revenue, net of fuel surcharge revenue, which we refer to as "freight revenue":

|

Distribution of Freight Revenue

Among Operating Subsidiaries

|

|

|

Covenant Transport

|

56%

|

|

SRT

|

25%

|

|

Solutions

|

11%

|

|

Star

|

8%

|

Our Truckload segment comprised approximately 89%, 89%, and 90% of our total freight revenue in 2016, 2015, and 2014, respectively.

In our Truckload segment, we primarily generate revenue by transporting freight for our customers. Generally, we are paid a predetermined rate per mile for our truckload services. We enhance our truckload revenue by charging for tractor and trailer detention, loading and unloading activities, and other specialized services, as well as through the collection of fuel surcharges to mitigate the impact of increases in the cost of fuel. The main factors that could affect our Truckload revenue are the revenue per mile we receive from our customers, the percentage of miles for which we are compensated, and the number of shipments and miles we generate. These factors relate, among other things, to the general level of economic activity in the United States, inventory levels, specific customer demand, the level of capacity in the trucking industry, and driver availability.

The main expenses that impact the profitability of our Truckload segment are the variable costs of transporting freight for our customers. These costs include fuel expenses, driver-related expenses, such as wages, benefits, training, and recruitment, and purchased transportation expenses, which primarily include compensating independent contractors. Expenses that have both fixed and variable components include maintenance and tire expense and our total cost of insurance and claims. These expenses generally vary with the miles we travel, but also have a controllable component based on safety, self-insured retention versus insurance premiums, fleet age, efficiency, and other factors. Historically, our main fixed costs include rentals and depreciation of long-term assets, such as revenue equipment and terminal facilities, and the compensation of non-driver personnel.

We measure the productivity of our Truckload segment with three key performance metrics: average freight revenue per total mile (excluding fuel surcharges), average miles per tractor, and average freight revenue per tractor per week (excluding fuel surcharges). A description of each follows:

|

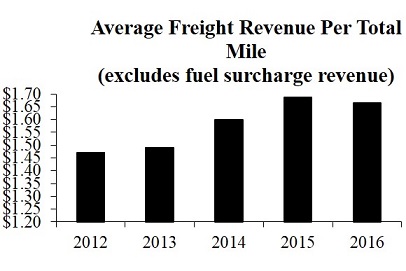

Average Freight Revenue Per Total Mile. Our average freight revenue per total mile is primarily a function of 1) the allocation of assets among our subsidiaries and 2) the macro U.S. economic environment including supply/demand of freight and carriers. The year-over-year increase from 2012 to 2015 is a result of allocating more tractors to our niche/specialized service offerings that provide higher rates (including expedited/critical freight, high-value/constant security, and temperature-controlled). A weaker pricing environment and condensed peak season during 2016 resulted in the slight decrease from the previous year.

|

|

|

Average Freight Revenue Per Total Mile (excludes fuel surcharge revenue)

|

2012

|

2013

|

2014

|

2015

|

2016

|

||

|

$1.47

|

$1.49

|

$1.60

|

$1.69

|

$1.67

|

|

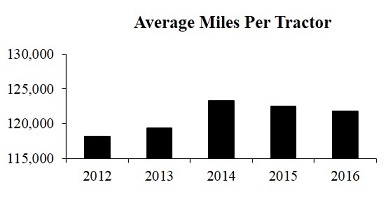

Average Miles Per Tractor. Average miles per tractor reflect economic demand, driver availability, regulatory constraints, and the allocation of tractors among the service offerings. Utilization in 2016 and 2015 declined from that of 2014 primarily due to a softer freight market and the increase in certain e-commerce freight that has a shorter length of haul, partially offset by the increase in the portion of tractors operated by teams.

|

|

|

Average Miles Per Tractor

|

2012

|

2013

|

2014

|

2015

|

2016

|

||

|

118,103

|

119,375

|

123,275

|

122,508

|

121,782

|

|

Average Freight Revenue Per Tractor Per Week. We use average freight revenue per tractor per week as our main measure of asset productivity. This operating metric takes into account the effects of freight rates, non-revenue miles, and miles per tractor. In addition, because we calculate average freight revenue per tractor using all of our tractors, it takes into account the percentage of our fleet that is unproductive due to lack of drivers, repairs, and other factors. The decrease in average freight revenue per tractor per week in 2016 is primarily due to an increase in our unseated tractors, specifically at SRT, and a softer freight market both in terms of utilization and rates.

|

|

|

Average Freight Revenue Per Tractor Per Week (excludes fuel surcharge revenue)

|

2012

|

2013

|

2014

|

2015

|

2016

|

||

|

$3,320

|

$3,411

|

$3,777

|

$3,967

|

$3,881

|

Our Solutions subsidiary comprised approximately 11%, 11%, and 10% of our total operating revenue in 2016, 2015, and 2014, respectively. Solutions derives revenue from providing brokerage and logistics services, particularly arranging transportation services for customers directly and through relationships with thousands of third-party carriers and integration with our Truckload segment. Solutions provides freight brokerage services directly and through freight brokerage agents, who are paid a commission for the freight brokerage service they provide and accounts receivable factoring. The main factors that impact profitability in terms of expenses are the variable costs of outsourcing the transportation freight for our customers and managing fixed costs, including salaries and selling, general, and administrative expenses. Our brokerage loads increased to 62,614 in 2016, from 36,217 in 2015, while average revenue per load decreased approximately 41% to $1,068 in 2016, from $1,820 in 2015, primarily due to the full year impact of a new customer added in 2015 and reduced peak-season freight opportunities during the fourth quarter of 2016. Additionally, revenue from Solutions' accounts receivable factoring improved by approximately 6% year-over-year to $2.6 million in 2016 from $2.4 million in 2015.

In May 2011, we acquired a 49.0% interest in TEL. TEL is a tractor and trailer equipment leasing company and used equipment reseller. We have accounted for our investment in TEL using the equity method of accounting and thus our financial results include our proportionate share of TEL's net income since May 2011, or $3.0 million in 2016, $4.6 million in 2015, and $3.7 million in 2014. As a result, TEL's results and growth are significant to our current year results and, in our estimation, to our longer-term vision.

Refer to Note 16, "Segment Information," of the accompanying consolidated financial statements for further information about our reporting segment's operating and financial results for 2016, 2015, and 2014.

Customers and Operations

We focus on targeted markets throughout the United States where we believe our service standards can provide a competitive advantage. We are a major carrier for transportation companies such as parcel freight forwarders, less-than-truckload carriers, and third-party logistics providers that require a high level of service to support their businesses, as well as for traditional truckload customers such as manufacturers, retailers, and food and beverage shippers. Our three operating fleets within the Truckload segment are truckload carriers and as such we generally dedicate an entire trailer to one customer from origin to destination. We also generate revenue through providing ancillary services, including freight brokerage services and accounts receivable factoring.

In 2016 and 2015, one customer accounted for more than 10% of our consolidated revenue. Wal-Mart accounted for $69.4 million of total revenue in 2016, while UPS accounted for $75.8 million and $82.6 million of revenue in 2015 and 2014, respectively. Both customers were serviced by both our Truckload segment and our Solutions subsidiary. Our top five customers accounted for approximately 39%, 34%, and 29% of our total revenue in 2016, 2015, and 2014, respectively.

We operate tractors driven by a single driver and also tractors assigned to two-person driver teams. Our single driver tractors generally operate in shorter lengths of haul, generate fewer miles per tractor, and experience more non-revenue miles, but the lower productive miles are expected to be offset by generally higher revenue per loaded mile and the reduced employee expense of compensating only one driver. In contrast, our two-person driver tractors generally operate in longer lengths of haul, generate greater miles per tractor, and experience fewer non-revenue miles, but we typically receive lower revenue per loaded mile and incur higher employee expenses of compensating both drivers. We expect operating statistics and expenses to shift with the mix of single and team operations.

We operate throughout the U.S. and in parts of Canada and Mexico, with substantially all of our revenue generated from within the U.S. All of our tractors are domiciled in the U.S., and we have generated less than two percent of our revenue in Canada and Mexico in 2016, 2015 and 2014. We do not separately track domestic and foreign revenue from customers, and providing such information would not be meaningful. Excluding a de minimus number of trailers, all of our long-lived assets are, and have been for the last three fiscal years, located within the United States.

In 2009, we began a multi-year project to upgrade the hardware and software of our information systems. The goal upon completion of the project was to have uniform operational and financial systems across the entire Company as we believe this provides improved customer service, utilization, and enhances our visibility into and across the organization. All of our operating subsidiaries are now operating on the new system. We implemented the new operating system at SRT in February 2014. As expected with any large conversion project, SRT experienced inefficiencies that resulted in a year-over-year reduction in first quarter 2014 profitability; however, by the second quarter of 2014 those inefficiencies were largely resolved and in 2015, we began realizing the efficiencies of having all subsidiaries on one operating platform. We expect to continue to evaluate where we can leverage the system to add further efficiencies across the Company.

Drivers and Other Personnel

Driver recruitment, retention, and satisfaction are essential to our success, and we have made each of these factors a primary element of our strategy. We recruit both experienced and student drivers as well as independent contractor drivers who own and drive their own tractor and provide their services to us under contract. We conduct recruiting and/or driver orientation efforts from five of our locations, and we offer ongoing training throughout our terminal network. We emphasize driver-friendly operations throughout our organization. We have implemented automated programs to signal when a driver is scheduled to be routed toward home, and we assign fleet managers specific tractor units, regardless of geographic region, to foster positive relationships between the drivers and their principal contact with us.

The truckload industry has periodically experienced difficulty in attracting and retaining enough qualified truck drivers. It is also common for the driver turnover rate of individual carriers to exceed 100% in a year. At times, there are driver shortages in the trucking industry. In past years, when there were driver shortages, the number of qualified drivers had not kept pace with freight growth because of (i) changes in the demographic composition of the workforce; (ii) alternative employment opportunities other than truck driving that became available in a growing economy; (iii) individual drivers' desire to be home more often; and (iv) regulatory requirements that limit the available pool of drivers.

Driver retention continued to be challenging in 2016, as economic growth provided more employment opportunities that attracted professional drivers. Despite these challenges our number of drivers decreased only slightly at December 31, 2016 as compared to the 2015 year. Despite having a similar number of drivers as of December 31, 2016, our average number of teams for 2016 increased as a percentage of our fleet to 38.7% compared to 35.3% in 2015 and our average tractor count for the year decreased as compared to December 31, 2015. Open tractors, including wrecked units, averaged approximately 5.4% for the year ended December 31, 2016, compared to approximately 4.6% for the year ended December 31, 2015, primarily as a result of an increase in turnover at SRT.

We believe having a happy, healthy, and safe driver is the key to our success, both in the short term and over a longer period. As a result, we are actively working to enhance our drivers' experience in an effort to recruit and retain more drivers.

Independent contractors provide a tractor and a driver and are responsible for all operating expenses in exchange for a fixed payment per mile. We do not have the capital outlay of purchasing the tractor. The payments to independent contractors are recorded in revenue equipment rentals and purchased transportation. When independent contractor tractors are utilized, we avoid expenses generally associated with company-owned equipment, such as driver compensation, fuel, interest, and depreciation. Obtaining equipment from independent contractors and under operating leases effectively shifts financing expenses from interest to "above the line" operating expenses.

We continue to educate our drivers and non-driver personnel regarding the Federal Motor Carrier Safety Administration ("FMCSA") Compliance Safety Accountability program ("CSA") to ensure we keep our top talent and challenge those drivers that need improvement. We believe CSA, in conjunction with other U.S. Department of Transportation ("DOT") regulations, including those related to hours-of-service, has reduced and will likely continue to impact effective capacity in our industry as well as negatively impact equipment utilization. Nevertheless, for carriers that are able to successfully manage this regulation-laden environment with driver-friendly equipment, compensation, and operations, we believe opportunities to increase market share may be available. Driver pay may increase as a result of regulation and economic expansion, which could provide more alternative employment opportunities. If economic growth is sustained, however, we expect the supply/demand environment to be favorable enough for us to offset expected compensation increases with better freight pricing.

We use driver teams in a substantial portion of our tractors. Driver teams permit us to provide expedited service on selected long haul lanes because teams are able to handle longer routes and drive more miles while remaining within DOT hours-of-service rules. The use of teams contributes to greater equipment utilization of the tractors they drive than obtained with single drivers. The use of teams, however, increases the accumulation of miles on tractors and trailers as well as personnel costs as a percentage of revenue and the number of drivers we must recruit.

We are not a party to any collective bargaining agreement. At December 31, 2016, we employed approximately 3,600 drivers and approximately 800 non-driver personnel. At December 31, 2016, we had active contracts with approximately 219 independent contractor drivers.

Revenue Equipment

At December 31, 2016, we operated 2,535 tractors and 7,389 trailers. Of these tractors, 2,181 were owned, 135 were financed under operating leases, and 219 were provided by independent contractors, who own and drive their own tractors. Of these trailers, 4,759 were owned, 1,695 were financed under operating leases, and 935 were financed under capital leases. Furthermore, at December 31, 2016, approximately 61.4% of our trailers were dry vans and the remaining trailers were refrigerated vans.

We believe that operating high quality, late-model equipment contributes to operating efficiency, helps us recruit and retain drivers, and is an important part of providing excellent service to customers. We operate a modern fleet of tractors, with the majority of units under warranty, to minimize repair and maintenance costs and reduce service interruptions caused by breakdowns. We also order most of our equipment with uniform specifications to reduce our parts inventory and facilitate maintenance. At December 31, 2016, our tractor fleet had an average age of approximately 1.8 years, and our trailer fleet had an average age of approximately 4.3 years. As of December 31, 2016, 100% of our tractor fleet had engines compliant with stricter regulations regarding emissions that became effective in 2007 and 99.8% of our tractor fleet had engines compliant with stricter regulations regarding emissions that became effective in 2010. We equip our tractors with a satellite-based tracking and communications system that permits direct communication between drivers and fleet managers. We believe that this system enhances our operating efficiency and improves customer service and fleet management. This system also updates the tractor's position approximately every fifteen minutes, which allows us and our customers to locate freight and accurately estimate pick-up and delivery times. We also use the system to monitor engine idling time, speed, performance, and other factors that affect operating efficiency. At December 31, 2016, 100% of our fleet was equipped with electronic on board recorders ("EOBRs," now referred to as electronic logging devices, or "ELDs"), which electronically monitor tractor miles and facilitate enforcement of hours-of-service regulations.

Over the past decade, the price of new tractors has risen dramatically and there has been significant volatility in the used equipment market. This has substantially increased our costs of operation.

Industry and Competition

Truckload is the largest segment of the for-hire ground freight transportation market based on revenue, surpassing the combined market size of less-than-truckload, railroad, intermodal, and parcel delivery combined. The truckload market is further segmented into sectors such as regional dry van, temperature-controlled van, flatbed, dedicated contract, expedited, and irregular route.

The U.S. trucking industry is highly competitive and includes thousands of "for-hire" motor carriers, none of which dominate the market. Service and price are the principal means of competition in the trucking industry. We compete to some extent with railroads and rail-truck intermodal service but attempt to differentiate ourselves from our competition on the basis of service. Rail and rail-truck intermodal movements are more often subject to delays and disruptions arising from rail yard congestion, which reduce the effectiveness of such service to customers with time-definite pick-up and delivery schedules. Historically, in times of high fuel prices or decreased consumer demand, however, rail-intermodal competition has been more significant.

Our industry is subject to dynamic factors that significantly affect our operating results. These factors include the availability of qualified truck drivers, the volume of freight in the sectors we serve, the price of diesel fuel, and government regulations that impact productivity and costs. Recently, our industry has experienced softened freight demand, scarcity of qualified truck drivers, decreased fuel costs, a depressed used tractor market, and regulations that limit productivity. In 2016, these factors contributed to an environment of challenging freight volumes, rate pressure, and increased costs, particularly around tractor depreciation expense and gains and losses on used tractors, for many trucking companies, including us. Based on our assessment of future regulatory changes, driver demographics, and expected growth rates of our major customers and sectors, we expect the pricing environment to improve in the latter half of 2017 and into 2018 and 2019, offset in part by higher driver pay and other inflationary costs. We believe large and diversified companies, like ourselves, are best positioned to capitalize on the current industry environment, because we can offer significant capacity commitments to major customers, safe and comfortable new equipment to drivers, and optimized routing and other business analytics to make the most of our drivers' federally limited operating hours.

We believe that the cost and complexity of operating trucking fleets are increasing and that economic and competitive pressures are likely to force many smaller competitors and private fleets to consolidate or exit the industry. As a result, we believe that larger, better-capitalized companies, like us, will have opportunities to increase profit margins and gain market share. In the market for dedicated services, we believe that truckload carriers, like us, have a competitive advantage over truck lessors, which are the other major participants in the market, because we expect to be able to offer lower prices by utilizing back-haul freight within our network that traditional lessors may not have.

Regulation

Our operations are regulated and licensed by various U.S. agencies. Our limited Canadian business activities are subject to similar requirements imposed by the laws and regulations of Canada, as well as its provincial laws and regulations. We operate within Mexico by utilizing third-party carriers within that country. Our company drivers and independent contractors also must comply with the safety and fitness regulations of the DOT, including those relating to drug and alcohol testing and hours-of-service. Such matters as weight and equipment dimensions are also subject to U.S. regulations. We also may become subject to new or more restrictive regulations relating to fuel emissions, drivers' hours-of-service, ergonomics, or other matters affecting safety or operating methods. Other agencies, such as the Environmental Protection Agency ("EPA") and the Department of Homeland Security ("DHS") also regulate our equipment, operations, and drivers.

The DOT, through the FMCSA, imposes safety and fitness regulations on us and our drivers, including rules that restrict driver hours-of-service. In December 2011, the FMCSA published its 2011 Hours-of-Service Final Rule (the "2011 Rule"). The 2011 Rule requires drivers to take 30-minute breaks after eight hours of consecutive driving and reduces the total number of hours a driver is permitted to work during each week from 82 hours to 70 hours. The 2011 Rule also provides that the 34-hour restart may only be used once per week and must include two rest periods between one a.m. and five a.m. (together, the "2011 Restart Restrictions"). These rule changes became effective in July 2013. We believe the 2011 Rule led to decreased productivity and caused some loss of efficiency, as drivers and shippers have needed supplemental training, computer programming has required modifications, additional drivers have been employed or engaged, additional equipment has been acquired, and shipping lanes have been reconfigured.

In December 2014, the 2015 Omnibus Appropriations bill was signed into law. Among other things, the legislation provided temporary relief from the 2011 Restart Restrictions while the FMCSA conducted a study to determine whether such restrictions had a positive result on driver safety (the "Study"), and essentially reverted to the more straightforward 34-hour restart rule that was in effect before the 2011 Rule became effective. In December 2016, a short-term funding bill was signed into law that directly tied the reinstatement of the 2011 Restart Restrictions to the outcome of the Study and requires the Study to demonstrate that the 2011 Restart Restrictions offer a "statistically significant improvement" in safety related matters in order for the 2011 Restart Restrictions to be reinstated. In March 2017, the results of the Study were released, and they did not show the necessary improvement needed to reinstate the 2011 Restart Restrictions. Based on these results, the FMCSA is expected to issue a formal notice permanently removing the 2011 Restart Restrictions from the hours-of-service regulations.

The DOT uses two methods of evaluating the safety and fitness of carriers. The first method is the application of a safety rating that is based on an onsite investigation and affects a carrier’s ability to operate in interstate commerce. We currently have a satisfactory DOT safety rating under this method, which is the highest available rating under the current safety rating scale. If we received a conditional or unsatisfactory DOT safety rating, it could adversely affect our business, as some of our existing customer contracts require a satisfactory DOT safety rating. In January 2016, the FMCSA published a Notice of Proposed Rulemaking outlining a revised safety rating measurement system which would replace the current methodology. Under the proposed rule, the current three safety ratings of "satisfactory," "conditional," and "unsatisfactory" would be replaced with a single safety rating of "unfit." Thus, a carrier with no rating would be deemed fit. Moreover, data from roadside inspections and the results of all investigations would be used to determine a carrier’s fitness on a monthly basis. This would replace the current methodology of determining a carrier’s fitness based solely on infrequent comprehensive onsite reviews. The proposed rule underwent a public comment period that ended in June 2016 and several industry groups and lawmakers expressed their disagreement with the proposed rule, arguing that it violates the requirements of the FAST Act and that the FMCSA must first finalize its review of the CSA scoring system, described in further detail below. Based on this feedback, in January 2017, the FMCSA announced that a Supplemental Notice of Proposed Rulemaking outlining certain changes to the proposed rule would be released in the future. Therefore, it is uncertain if, when, or under what form this proposed rule could take effect. However, if this rule or a similar rule was enacted, and we received a rating of "unfit," it could materially adversely affect our operations.

In addition to the safety rating system, the FMCSA has adopted the CSA program as an additional safety enforcement and compliance model that evaluates and ranks fleets on certain safety-related standards. The CSA program analyzes data from roadside inspections, moving violations, crash reports from the last two years, and investigation results. The data is organized into seven categories. Carriers are grouped by category with other carriers that have a similar number of safety events (e.g., crashes, inspections, or violations) and carriers are ranked and assigned a rating percentile to prioritize them for interventions if they are above a certain threshold. Currently, these scores do not have a direct impact on a carrier’s safety rating. However, the occurrence of unfavorable scores in one or more categories may (i) affect driver recruiting and retention by causing high-quality drivers to seek employment with other carriers, (ii) cause our customers to direct their business away from us and to carriers with higher fleet safety rankings, (iii) subject us to an increase in compliance reviews and roadside inspections, or (iv) cause us to incur greater than expected expenses in our attempts to improve unfavorable scores, any of which could adversely affect our results of operations and profitability.

Under CSA, these scores were initially made available to the public in five of the seven categories. However, pursuant to the FAST Act, which was signed into law in December 2015, the FMCSA is required to remove from public view the previously available CSA scores while it reviews the reliability of the scoring system. During this period of review by the FMCSA, we will continue to have access to our own scores and will still be subject to intervention by the FMCSA when such scores are above the intervention thresholds. Currently, certain of our subsidiaries are exceeding the established intervention thresholds in one or more of the seven categories of CSA, in comparison to their peer groups; however, they all continue to maintain a satisfactory rating with the DOT. We will continue to promote improvement of these scores in all seven categories with ongoing reviews of all safety-related policies, programs, and procedures for their effectiveness.

In 2011, the FMCSA issued new rules that would require nearly all carriers, including us, to install and use ELDs in their tractors to electronically monitor truck miles and facilitate enforcement of hours-of-service regulations. These rules, however, were vacated by the Seventh Circuit Court of Appeals in August 2011. In response, Congress passed legislation in July 2012 renewing the mandate, subject to new regulations to be promulgated by the DOT. Pursuant to its rulemaking authority, the FMCSA published a new final rule in December 2015 which requires the use of ELDs by nearly all carriers by December 2017 (the "2015 ELD Rule"). We have proactively installed ELDs on 100% of our tractor fleet, so we don’t believe the 2015 ELD Rule will impact our operations or profitability or our use of ELDs. Furthermore, we believe that more effective hours-of-service enforcement after the 2015 ELD Rule takes effect may improve our competitive position by causing all carriers to adhere more closely to hours-of-service requirements.

In the aftermath of the September 11, 2001 terrorist attacks, the DHS and other federal, state, and municipal authorities implemented and continue to implement various security measures, including checkpoints and travel restrictions on large trucks. The U.S. Transportation Security Administration ("TSA") adopted regulations that require a determination by the TSA that each driver who applies for or renews his or her license for carrying hazardous materials is not a security threat. This could reduce the pool of qualified drivers who are permitted to transport hazardous waste, which could require us to increase driver compensation, limit our fleet growth, or allow trucks to sit idle. These regulations also could complicate the matching of available equipment with hazardous material shipments, thereby increasing our response time on customer orders and our non-revenue miles. As a result, it is possible we could fail to meet the needs of our customers or could incur increased expenses to do so.

In November 2015, the FMCSA published its final rule related to driver coercion, which took effect in January 2016. Under this rule, carriers, shippers, receivers, or transportation intermediaries that are found to have coerced drivers to violate certain FMCSA regulations (including hours-of-service rules) may be fined up to $16,000 for each offense. In addition, other rules have been recently proposed or made final by the FMCSA, including (i) a rule requiring the use of speed limiting devices on heavy duty trucks to restrict maximum speeds, which was proposed in 2016 but not yet made final, (ii) a rule mandating the creation of a national clearinghouse that employers and prospective employers must query to determine if current or prospective drivers have had any drug/alcohol positives or refusals, which was made final in December 2016, with a compliance date in January 2020, and (iii) a rule setting forth minimum driver-training standards for new drivers applying for commercial driver licenses for the first time and to experienced drivers upgrading their licenses or seeking a hazmat endorsement, which was made final in December 2016, with a compliance date in February 2020. The effect of these recently proposed or finalized rules could result in a decrease in fleet production and driver availability, either of which could adversely affect our business or operations.

In March 2014, the Ninth Circuit Court of Appeals held that California state wage and hour laws are not preempted by federal law. The case was appealed to the Supreme Court of the United States, which in May 2015 refused to review the case, and accordingly, the Ninth Circuit Court of Appeals decision stands. Current and future state and local wage and hour laws, including laws related to employee meal breaks and rest periods, may vary significantly from federal law. As a result, we, along with other companies in the industry, could become subject to an uneven patchwork of wage and hour laws throughout the United States. There is proposed federal legislation to preempt state and local wage and hour laws; however, passage of such legislation is uncertain. If federal legislation is not passed, we will either need to comply with the most restrictive state and local laws across our entire network, or overhaul our management systems to comply with varying state and local laws. Either solution could result in increased compliance and labor costs, driver turnover, and decreased efficiency.

Tax and other regulatory authorities, as well as independent contractors themselves, have increasingly asserted that independent contractor drivers in the trucking industry are employees rather than independent contractors, for a variety of purposes, including income tax withholding, workers' compensation, wage and hour compensation, unemployment, and other issues. Federal legislators have introduced legislation in the past to make it easier for tax and other authorities to reclassify independent contractor drivers as employees, including legislation to increase the recordkeeping requirements for those that engage independent contractor drivers and to heighten the penalties of companies who misclassify their employees and are found to have violated employees' overtime and/or wage requirements. Additionally, federal legislators have sought to abolish the current safe harbor allowing taxpayers meeting certain criteria to treat individuals as independent contractors if they are following a long-standing, recognized practice, extend the Fair Labor Standards Act to independent contractors, and impose notice requirements based upon employment or independent contractor status and fines for failure to comply. Some states have put initiatives in place to increase their revenues from items such as unemployment, workers' compensation, and income taxes, and a reclassification of independent contractor drivers as employees would help states with this initiative. Further, class actions and other lawsuits have been filed against certain members of our industry seeking to reclassify independent contractors as employees for a variety of purposes, including workers' compensation and health care coverage. Taxing and other regulatory authorities and courts apply a variety of standards in their determination of independent contractor status. Our classification of independent contractors has been the subject of audits by such authorities from time to time. While we have been successful in continuing to classify our independent contractor drivers as independent contractors and not employees, we may be unsuccessful in defending that position in the future. If our independent contractor drivers are determined to be our employees, we would incur additional exposure under federal and state tax, workers' compensation, unemployment benefits, labor, employment, and tort laws, including for prior periods, as well as potential liability for employee benefits and tax withholdings.

We are subject to various environmental laws and regulations dealing with the hauling and handling of hazardous materials, fuel storage tanks, air emissions from our vehicles and facilities, engine idling, and discharge and retention of storm water. Our truck terminals often are located in industrial areas where groundwater or other forms of environmental contamination could occur. Our operations involve the risks of fuel spillage or seepage, environmental damage, and hazardous waste disposal, among others. Certain of our facilities have waste oil or fuel storage tanks, and fueling islands. A small percentage of our freight consists of low-grade hazardous substances, which subjects us to a wide array of regulations. Additionally, increasing efforts to control emissions of greenhouse gases may have an adverse effect on us. Although we have instituted programs to monitor and control environmental risks and promote compliance with applicable environmental laws and regulations, if we are involved in a spill or other accident involving hazardous substances, if there are releases of hazardous substances we transport, if soil or groundwater contamination is found at our facilities or results from our operations, or if we are found to be in violation of applicable laws or regulations, we could be subject to cleanup costs and liabilities, including substantial fines or penalties or civil and criminal liability, any of which could have a materially adverse effect on our business and operating results.

EPA regulations limiting exhaust emissions became more restrictive in 2010. In 2010, an executive memorandum was signed directing the National Highway Traffic Safety Administration ("NHTSA") and the EPA to develop new, stricter fuel efficiency standards for heavy trucks. In August 2011, the NHTSA and the EPA adopted final rules that established the first-ever fuel economy and greenhouse gas standards for medium-and heavy-duty vehicles (the "Phase 1 Standards"). The Phase 1 Standards apply to tractor model years 2014 to 2018 and require the achievement of an approximate 20 percent reduction in fuel consumption by the 2018 model year, which equates to approximately four gallons of fuel for every 100 miles traveled. In addition, in February 2014, President Obama announced that his administration would begin developing the next phase of tighter fuel efficiency and greenhouse gas standards for medium-and heavy-duty trucks and trailers (the "Phase 2 Standards"). In October 2016, the EPA and NHTSA published the final rule mandating that the Phase 2 Standards will apply to trailers beginning with model year 2018 and tractors beginning with model year 2021. The Phase 2 Standards require nine percent and 25 percent reductions in emissions and fuel consumption for trailers and tractors, respectively, by 2027. We believe these requirements will result in additional increases in new tractor and trailer prices and additional parts and maintenance costs incurred to retrofit our tractors and trailers with technology to achieve compliance with such standards, which could adversely affect our operating results and profitability, particularly if such costs are not offset by potential fuel savings. We cannot predict, however, the extent to which our operations and productivity will be impacted.

The California Air Resources Board ("CARB") also adopted emission control regulations that will be applicable to all heavy-duty tractors that pull 53-foot or longer box-type trailers within the state of California. The tractors and trailers subject to these CARB regulations must be either EPA SmartWay certified or equipped with low-rolling, resistance tires and retrofitted with SmartWay-approved aerodynamic technologies. Enforcement of these CARB regulations for model year 2011 equipment began in January 2010 and will be phased in over several years for older equipment. We currently purchase Smart Way certified equipment in our new tractor and trailer acquisitions. In addition, in February 2017 CARB proposed California Phase 2 standards that generally align with the federal Phase 2 Standards, with some minor additional requirements, and as proposed would stay in place even if the federal Phase 2 Standards are affected by action from the Trump administration. Federal and state lawmakers also have proposed a variety of other regulatory limits on carbon emissions and fuel consumption. Compliance with these regulations could increase the cost of new tractors and trailers, impair equipment productivity, and increase operating expenses. These effects, combined with the uncertainty as to the operating results that will be produced by the newly designed diesel engines and the residual values of these vehicles, could increase our costs or otherwise adversely affect our business or operations.

In order to reduce exhaust emissions, some states and municipalities have begun to restrict the locations and amount of time where diesel-powered tractors may idle. These restrictions could force us to purchase on-board power units that do not require the engine to idle or to alter our drivers' behavior, which could result in a decrease in productivity or increase in driver turnover.

In April 2016, the Food and Drug Administration published a final rule establishing requirements for shippers, loaders, carriers by motor vehicle and rail vehicle, and receivers engaged in the transportation of food, to use sanitary transportation practices to ensure the safety of the food they transport as part of the Food Safety Modernization Act of 2011 (the "FSMA"). This rule sets forth requirements related to (i) the design and maintenance of equipment used to transport food, (ii) the measures taken during food transportation to ensure food safety, (iii) the training of carrier personnel in sanitary food transportation practices, and (iv) maintenance and retention of records of written procedures, agreements, and training related to the foregoing items. These requirements will take effect for larger carriers such as us in April 2017 and are applicable when we perform as a carrier or as a broker. We believe that our current food shipping practices are already in compliance with the majority of these requirements and we do not expect any issues with compliance. If we are found to be in violation of applicable laws or regulations related to the FSMA, we could be subject to substantial fines, penalties and/or criminal liability, any of which could have a material adverse effect on our business, financial condition, and results of operations.

The regulatory environment has recently changed under the administration of President Trump. In January 2017, the President’s office issued a temporary moratorium on proposed and recently published regulations, which will delay the effectiveness of such regulations for at least 60 days. Additionally, in January 2017, the President signed an executive order requiring federal agencies to repeal two regulations for each new one they propose and imposing a regulatory budget, which would limit the amount of new regulatory costs federal agencies can impose on individuals and businesses each year. The impact of these actions by the Trump administration may inhibit future new regulations and/or lead to the repeal or delayed effectiveness of existing regulations. Therefore, it is uncertain how we may be impacted in the future by existing or proposed regulations.

Fuel Availability and Cost

The cost of fuel trended lower in 2016, compared to 2015 and 2014, as demonstrated by a decrease in the Department of Energy ("DOE") national average for diesel to approximately $2.30 per gallon for 2016 compared to $2.71 per gallon for 2015. Our fuel cost was further decreased in 2016 due to an increase in our average fuel miles per gallon during 2016 as a result of purchasing equipment with more fuel-efficient engines.

We actively manage our fuel costs by routing our drivers through fuel centers with which we have negotiated volume discounts and through jurisdictions with lower fuel taxes, where possible. We have also reduced the maximum speed of many of our trucks, implemented strict idling guidelines for our drivers, purchased technology to enhance our management and monitoring of out-of-route miles, encouraged the use of shore power units in truck stops, and imposed standards for accepting broker freight that includes minimum rates and fuel surcharges. These initiatives have contributed to significant improvements in fleet wide average fuel mileage. Moreover, we have a fuel surcharge program in place with the majority of our customers, which has historically enabled us to recover some of the higher fuel costs. However, even with the fuel surcharges, the price of fuel can affect our profitability. Our fuel surcharges are billed on a lagging basis, meaning we typically bill customers in the current week based on a previous week's applicable index. Therefore, in times of increasing fuel prices, we do not recover as much as we are currently paying for fuel. In periods of declining prices, the opposite is true. In addition, we incur additional costs when fuel prices rise that cannot be fully recovered due to our engines being idled during cold or warm weather, empty or out-of-route miles, and for fuel used by refrigerated trailer units that generally is not billed to customers. In addition, from time-to-time customers attempt to modify their surcharge programs, some successfully, which can result in recovery of a smaller portion of fuel price increases. Rapid increases in fuel costs or shortages of fuel could have a materially adverse effect on our operations or future profitability.

To reduce the variability of the ultimate cash flows associated with fluctuations in diesel fuel prices, we periodically enter into various derivative instruments, including forward futures swap contracts. Historically diesel fuel has not been a traded commodity on the futures market so heating oil has been used as a substitute, as prices for both generally move in similar directions. Recently, however, we have been able to enter into hedging contracts with respect to both heating oil and ultra-low sulfur diesel ("ULSD"). Under these contracts, we pay a fixed rate per gallon of heating oil or ULSD and receive the monthly average price of New York heating oil per the New York Mercantile Exchange ("NYMEX") and Gulf Coast ULSD, respectively. Because the fixed price is determined based on market prices at the time we enter into the hedge, in times of increasing fuel prices the hedge contracts become more valuable, whereas in times of decreasing fuel prices the opposite is true. At December 31, 2016, we had forward futures swap contracts on approximately 12.1 million and 7.6 million gallons of diesel to be purchased in 2017 and 2018, respectively, or approximately 27% and 17% of our projected annual 2017 and 2018 fuel requirements, respectively. Due to the relative stability of petroleum prices in 2016, and the completion of multiple contracts that were entered into during periods of higher heating oil and ULSD prices, the fair value of our fuel hedging contracts at December 31, 2016, represented a $3.6 million liability compared to a $27.3 million liability at December 31, 2015.

Seasonality

In the trucking industry, revenue has historically decreased as customers reduce shipments following the winter holiday season and as inclement weather impedes operations. At the same time, operating expenses have generally increased, with fuel efficiency declining because of engine idling and weather, causing more equipment repairs resulting from physical damage. For the reasons stated, first quarter results historically have been lower than results in each of the other three quarters of the year, excluding charges. Over the past several years, we have seen increases in demand at varying times, primarily related to restocking required to replenish inventories that have been held significantly lower than historical averages. Additionally, we have seen surges between Thanksgiving and Christmas resulting from holiday shopping trends toward delivery of gifts purchased over the internet. In recent years, we have seen the duration of this holiday "peak" season become compressed as consumers have come to expect shorter and shorter shipping times and our customers’ networks have adjusted accordingly.

Additional Information

At December 31, 2016, our corporate structure included Covenant Transportation Group, Inc., a Nevada holding company organized in May 1994, and its wholly owned subsidiaries: Covenant Transport, Inc., a Tennessee corporation; Southern Refrigerated Transport, Inc., an Arkansas corporation; Star Transportation, Inc., a Tennessee corporation; Covenant Transport Solutions, Inc., a Nevada corporation; Covenant Logistics, Inc., a Nevada corporation; Covenant Asset Management, LLC, a Nevada limited liability company; CTG Leasing Company, a Nevada corporation; Driven Analytic Solutions, LLC, a Nevada limited liability company, Heritage Insurance, Inc., a Tennessee corporation, and IQS Insurance Retention Group, Inc., a Vermont corporation.

Our headquarters is located at 400 Birmingham Highway, Chattanooga, Tennessee 37419, and our website address is www.ctgcompanies.com. Our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all other reports we file or furnish with the SEC pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the "Exchange Act") are available free of charge through our website. Information contained in or available through our website is not incorporated by reference into, and you should not consider such information to be part of, this Annual Report on Form 10-K.

Additionally, you may read all of the materials that we file with the SEC by visiting the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. If you would like information about the operation of the Public Reference Room, you may call the SEC at 1-800-SEC-0330. You may also visit the SEC's website at www.sec.gov. This site contains reports, proxy and information statements and other information regarding the Company and other companies that file electronically with the SEC.

Our future results may be affected by a number of factors over which we have little or no control. The following discussion of risk factors contains forward-looking statements as discussed in Item 1 above. The following issues, uncertainties, and risks, among others, should be considered in evaluating our business and growth outlook.

Our business is subject to general economic, credit, business, and regulatory factors affecting the truckload industry that are largely beyond our control, any of which could have a materially adverse effect on our operating results.

The truckload industry is highly cyclical, and our business is dependent on a number of factors that may have a materially adverse effect on our results of operations, many of which are beyond our control. We believe that some of the most significant of these factors include (i) excess tractor and trailer capacity in the trucking industry in comparison with shipping demand; (ii) declines in the resale value of used equipment; (iii) strikes, work stoppages, or work slowdowns at our facilities or at customer, port, border crossing, or other shipping-related facilities; (iv) increases in interest rates, fuel taxes, tolls, and license and registration fees; (v) rising costs of healthcare; and (vi) fluctuations in foreign exchange rates.

We are also affected by (i) recessionary economic cycles, such as the period from 2007 through 2009 freight environment, which was characterized by weak demand and downward pressure on rates; (ii) changes in customers’ inventory levels and in the availability of funding for their working capital; (iii) changes in the way our customers choose to utilize our services; and (iv) downturns in our customers’ business cycles, particularly in market segments and industries, such as retail and manufacturing, where we have significant customer concentration. Economic conditions may adversely affect our customers and their demand for and ability to pay for our services.

Economic conditions that decrease shipping demand and increase the supply of available tractors and trailers can exert downward pressure on rates and equipment utilization, thereby decreasing asset productivity. The risks associated with these factors are heightened when the United States economy is weakened. Some of the principal risks during such times, which risks we have experienced during prior recessionary periods, are as follows:

|

●

|

we may experience a reduction in overall freight levels, which may impair our asset utilization;

|

|

●

|

certain of our customers may face credit issues and could experience cash flow problems that may lead to payment delays, increased credit risk, bankruptcies, and other financial hardships that could result in even lower freight demand and may require us to increase our allowance for doubtful accounts;

|

|

●

|

freight patterns may change as supply chains are redesigned, resulting in an imbalance between our capacity and our customers' freight demand;

|

|

●

|

customers may solicit bids for freight from multiple trucking companies or select competitors that offer lower rates from among existing choices in an attempt to lower their costs, and we might be forced to lower our rates or lose freight;

|

|

●

|

we may be forced to accept more freight from freight brokers, where freight rates are typically lower, or may be forced to incur more non-revenue miles to obtain loads; and

|

|

●

|

lack of access to current sources of credit or lack of lender access to capital, leading to an inability to secure credit financing on satisfactory terms, or at all.

|