Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - Pzena Investment Management, Inc. | pzn201610kex311.htm |

| EX-32.2 - EXHIBIT 32.2 - Pzena Investment Management, Inc. | pzn201610kex322.htm |

| EX-32.1 - EXHIBIT 32.1 - Pzena Investment Management, Inc. | pzn201610kex321.htm |

| EX-31.2 - EXHIBIT 31.2 - Pzena Investment Management, Inc. | pzn201610kex312.htm |

| EX-23.1 - EXHIBIT 23.1 - Pzena Investment Management, Inc. | pzn201610kex231.htm |

| EX-21.1 - EXHIBIT 21.1 - Pzena Investment Management, Inc. | pzn201610kex211.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ý | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |

For the Fiscal Year Ended December 31, 2016

or

o | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |

For the transition period from to

Commission file number 001-33761

PZENA INVESTMENT MANAGEMENT, INC.

(Exact Name of Registrant as Specified in its Charter)

Delaware | 20-8999751 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

320 Park Avenue

New York, New York 10022

(Address of Principal Executive Offices)

Registrant’s telephone number, including area code: (212) 355-1600

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Class A Common Stock, par value $.01 per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Accelerated filer x | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes o No ý

The aggregate market value of the common equity held by non-affiliates of the registrant as of June 30, 2016, the last business day of its most recently completed second fiscal quarter, was approximately $120.2 million based on the closing sale price of $7.61 per share of Class A common stock of the registrant on such date on the New York Stock Exchange. For purposes of this calculation only, it is assumed that the affiliates of the registrant include only directors and executive officers of the registrant.

As of March 9, 2017, there were 17,365,024 outstanding shares of the registrant’s Class A common stock, par value $0.01 per share.

As of March 9, 2017, there were 51,164,689 outstanding shares of the registrant’s Class B common stock, par value $0.000001 per share.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

Page | ||

i

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, or Annual Report, contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 27E of the Securities and Exchange Act of 1934, as amended (the "Exchange Act"). Forward-looking statements provide our current views, expectations, or forecasts, of future events and performance and include statements about our expectations, beliefs, plans, objectives, intentions, assumptions and other statements that are not historical facts. Words or phrases such as “anticipate,” “believe,” “continue,” “ongoing,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project” or similar words or phrases, or the negatives of those words or phrases, may identify forward-looking statements, but the absence of these words does not necessarily mean that a statement is not forward-looking.

Forward-looking statements are subject to known and unknown risks and uncertainties, including but not limited to those noted below and described in Part I, Item 1A — "Risk Factors" of this Annual Report, and are based on assumptions and estimates. If one or more of these risks or uncertainties materialize, or if one or more of our assumptions or estimates prove incorrect, our actual results could differ materially from those expected or implied by the forward-looking statements. Accordingly, you should not unduly rely on any forward-looking statements. The forward-looking statements in this Annual Report, speak only as of the date of this Annual Report. There may be additional risks, uncertainties and factors that we do not currently view as material or that are not known. We undertake no obligation to publicly revise any forward-looking statements to reflect circumstances or events after the date of this Annual Report, or to reflect the occurrence of unanticipated events. You should, however, review the factors and risks we describe in the reports we will file from time to time with the Securities and Exchange Commission, or SEC, after the date of this Annual Report.

Forward-looking statements include, but are not limited to, statements about:

• | our ability to respond to global economic, market, business and geopolitical conditions; |

• | our anticipated future results of operations and operating cash flows; |

• | our successful formulation and execution of business strategies and investment policies; |

• | our financing plans and the availability of short- or long-term borrowing, or equity financing; |

• | our competitive position and the effects of competition on our business; |

• | our ability to identify and capture potential growth opportunities available to us; |

• | the recruitment and retention of our employees; |

• | our expected levels of compensation for our employees; |

• | our potential operating performance, achievements, efficiency and cost reduction efforts; |

• | our expected tax rate; |

• | changes in interest rates; |

• | our expectation with respect to the economy, capital markets, the market for asset management services and other industry trends; and |

• | the impact of future legislation and regulation, and changes in existing legislation and regulation, on our business. |

ii

Preliminary Notes

In this Annual Report, “we,” “our,” “us,” and "the Company" refer to Pzena Investment Management, Inc. and its consolidated subsidiaries.

Each Russell Index referred to in this Annual Report is a registered trademark or trade name of Frank Russell Company®. Frank Russell Company® is the owner of all copyrights relating to these indices and is the source of the performance statistics of these indices that are referred to herein.

Information with respect to Morgan Stanley Capital International, which we refer to as MSCI, requires a license from MSCI. All MSCI brands and product names are the trademarks, service marks, or registered trademarks of MSCI or its subsidiaries in the United States and other jurisdictions. MSCI is the owner of all copyrights relating to these indices and is the source of the performance statistics of these indices that are referred to in this Annual Report.

The S&P 500 Index is licensed from Standard & Poor's Financial Services LLC, which is the source of the performance statistics of this index.

iii

PART I.

ITEM 1. | BUSINESS |

Overview

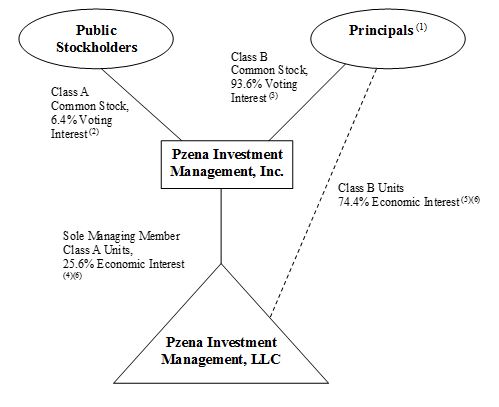

Pzena Investment Management, Inc. was formed in 2007 and is the sole managing member of Pzena Investment Management, LLC, which is our operating company. Founded in 1995, Pzena Investment Management, LLC is a value-oriented investment management company. We believe that we have established a positive, team-oriented culture that enables us to attract and retain highly qualified people. Since our inception, over twenty years ago, we have built a diverse, global client base of respected and sophisticated institutional investors, select third-party distributed mutual funds for which we act as sub-investment adviser, and funds for which we act as investment adviser.

Pzena Investment Management, LLC is comprised of Class A and Class B membership units, each of which have an identical economic interest in the operating company. As a holding company, we hold all the Class A membership units and recognize income generated from our economic interest in our operating company's net income. The Class B membership units of the operating company are held by employees and certain outside members. For each Class A membership unit held, we have issued one corresponding share of Class A common stock, par value $0.01 per share, which entitles the holder to one vote per share. For each Class B membership unit, we have issued one corresponding share of Class B common stock, par value $0.000001 per share, which entitles the holder to five votes per share without dividend rights, as described below in the graphic illustration. As of December 31, 2016, we owned approximately 25.6% of the economic interest in our operating company and our Class A shareholders hold approximately 6.4% of our voting interests.

Pzena Investment Management, Inc. also serves as the general partner of Pzena Investment Management, LP, a partnership formed with the objective of aggregating employee ownership in one entity.

The graphic below illustrates our holding company structure and ownership as of December 31, 2016.

(1) | As of December 31, 2016, the members of Pzena Investment Management, LLC, other than us, consisted of: |

• | Our named executive officers and their estate planning vehicles, who collectively held, through direct and indirect interests, approximately 54.2% of the economic interests in Pzena Investment Management, LLC. |

• | 32 of our other employee members and their estate planning vehicles, who collectively held, through direct and indirect interests, approximately 4.2% of the economic interests in Pzena Investment Management, LLC. |

• | Certain other members of our operating company, including one of our directors and his related entities, and former employees, who collectively held, through direct and indirect interests, approximately 16.0% of the economic interests in Pzena Investment Management, LLC. |

1

(2) | Each share of Class A common stock is entitled to one vote per share. |

(3) | Each share of Class B common stock is entitled to five votes per share for so long as the number of shares of Class B common stock outstanding represents at least 20% of all shares of common stock outstanding. Holders of Class B common stock have the right to receive the par value of the Class B common stock held by them upon our liquidation, dissolution or winding up, but do not share in dividends. |

(4) | As of December 31, 2016, we held 17,355,024 Class A units of Pzena Investment Management, LLC, which represented the right to receive 25.6% of the distributions made by Pzena Investment Management, LLC. |

(5) | As of December 31, 2016, the principals collectively held 50,502,655 Class B units of Pzena Investment Management, LLC, which represented the right to receive 74.4% of the distributions made by Pzena Investment Management, LLC. |

(6) | Pursuant to the operating agreement of our operating company, each vested Class B unit is exchangeable for a share of the Company's Class A common stock, subject to certain timing and volume restrictions. When a vested Class B unit is exchanged for a share of Class A common stock, or is forfeited, a corresponding share of the Company's Class B common stock will automatically be redeemed and cancelled. When a share of Class A common stock or Class B unit is repurchased and retired, a corresponding membership unit or share of Class B common stock is redeemed and cancelled, respectively. Conversely, to the extent that we issue shares of Class A common stock, or additional Class B units pursuant to our equity incentive plans, the corresponding Class A membership units or shares of Class B common stock will be issued, respectively. |

We utilize a classic value approach to investing and seek to make investments in good businesses at low prices, which requires:

• | willingness to invest in companies before their stock prices reflect signs of business improvement, and |

• | significant patience, based upon our understanding of the business’ fundamentals, and our long-term investment horizon. |

Our approach and process aim to achieve attractive returns over the long term. We manage assets in value-oriented investment strategies reflecting varying degrees of portfolio concentrations across a wide range of market capitalizations in both U.S. and non-U.S. capital markets.

Our assets under management, or AUM, was $30.0 billion at December 31, 2016, and we managed money on behalf of institutions, acted as sub-investment adviser to a variety of SEC-registered mutual funds and non-U.S. funds as well as investment adviser to certain Pzena SEC-registered mutual funds and non-U.S. funds.

Our operating company is led by a committee, consisting of our Chief Executive Officer (CEO), Mr. Richard S. Pzena; each of our Presidents, Messrs. John P. Goetz and William L. Lipsey; our Executive Vice President, Mr. Michael D. Peterson; and our Chief Operating Officer (COO), Mr. Gary J. Bachman (the "Executive Committee").

Our Competitive Strengths

We believe that the following are our competitive strengths:

• | Focus on Investment Excellence. We recognize that we must achieve investment excellence in order to attain long-term business success. All of our business decisions, including the design of our investment process and our willingness to limit AUM in our investment strategies, are focused on producing attractive long-term investment results. We believe that our long-term investment performance, together with our willingness to close our strategies to new investors in order to optimize the prospects for future performance, has contributed to our positive reputation among our clients and the institutional consultants who advise them. |

• | Consistency of Investment Process. Since our inception over twenty years ago, we have utilized a classic value investment approach and a systematic, disciplined investment process to construct portfolios for our investment strategies in U.S. and non-U.S. markets across all market capitalizations. The consistency of our process has allowed us to leverage the same investment team to launch new strategies. We believe that our consistent investment process has resulted in our strong brand recognition in the investment community. |

• | Diverse and High Quality Client Base. We believe that we have developed a favorable reputation in the institutional investment community. This is evidenced by our strong relationships with institutional investors, investment consultants, and mutual fund providers, as well as the diversity and sophistication of our investors. For more information concerning our client base, see “Our Client Relationships and Distribution Approach” below. |

2

• | Experienced Investment Professionals and a Team-Oriented Approach. We believe that our greatest asset is the experience of the individuals on our team. For more information on our investment team, see “Our Investment Team” below. |

• | Employee Retention. We have focused on building an environment that we believe is attractive to talented investment professionals. Important among our practices are our team-oriented approach to investment decisions, rotation of coverage areas among individuals, and our culture of employee ownership. |

• | Culture of Ownership. We believe the key contributors to our success should have significant ownership of our business. Since our inception, we have communicated to all our employees that they have the opportunity to become members of our operating company. As of December 31, 2016, we had 38 employee members positioned within all of our functional areas. We believe this ownership model results in a shared sense of purpose with our clients and their advisers. We intend to continue fostering a culture of ownership through our equity incentive plans, which are designed to align our team’s interests with those of our stockholders and clients. We believe this culture of ownership contributes to our team orientation and connection with clients. |

Our Business Strategy

The key to our success is continued long-term investment performance. In conjunction with this, we believe the following strategies will enable us to grow our business over time:

• | Unwavering Focus on Classic Value Investing. We view our unwavering focus on long-term classic value investment excellence to be the key driver of our business success. |

• | Capitalize on Growth Opportunities Created By Our Global Strategies. Among both institutional and retail investors industry-wide, over the past few years, there have been increasing levels of investments in portfolios including non-U.S. equities. As of December 31, 2016, the total AUM in our International (ex-U.S.) Value strategies, Global Value strategies, Emerging Markets Value strategy, European Value strategy, and other non-U.S. strategies was $14.4 billion, or 48.0% of our overall AUM. Our global capability provides opportunity for implementation of our strategies around the world. |

• | Work with Our Strong Consultant Relationships. We believe that we have built strong relationships with the leading investment consulting firms who advise potential institutional clients. Historically, new accounts sourced through consultant-led searches have been a large driver of our inflows and are expected to be a major component of our future inflows. We estimate that approximately 70% of all retirement plan assets are advised by investment consultants, with a relatively small number of these consultants representing a significant majority of these relationships. As a result of a consistent servicing effort over our history, we have built strong relationships with consulting firms that we believe are the most important. New accounts sourced through consultant-led searches have been a large driver of our historical growth and are expected to be a major component of our future growth. As of December 31, 2016, our largest consultant relationship represented approximately 10% of our AUM. |

• | Expand Our Non-U.S. Client Base. In recent years, we have increased our efforts to develop our non-U.S. client base. Through our strong relationships with global consultants, we have been able to accelerate the development of our relationships with their non-U.S. branches. Over time, we aim to achieve growth of this client base through these relationships and by directly calling on the world’s largest institutional investors. We have also sought to expand our non-U.S. base through our relationships with non-U.S. mutual funds and other investment fund advisers. During 2015, we expanded our physical presence to three continents with the launch of a business development and client service office in London, in addition to our headquarters in the United States and representative office in Melbourne. To date, our marketing efforts have resulted in client relationships in fifteen non-U.S. countries, including the United Kingdom, Luxembourg, Australia and Canada. As of December 31, 2016, we managed $8.9 billion on behalf of non-U.S. clients. |

• | Provide Access To Our Strategies Through a Range of Investment Vehicles and Distribution Channels. Our clients access our investment strategies through a range of investment vehicles and distribution channels, including separately managed accounts, mutual funds that we sub-advise, and certain private placement vehicles and non-U.S. funds that we offer to institutional investors. During 2014 we launched three SEC-registered Pzena mutual funds for which we act as investment adviser in an effort to expand the access investors have to our strategies. During 2016 we launched a fourth SEC-registered Pzena mutual fund and continue to develop intermediary relationships to grow retail distribution channels. For more information concerning access to our strategies and our distribution approach, see “Our Client Relationships and Distribution Approach” below. |

3

• | Employ Global Team to Serve Clients and Prospects. Our business development and client service professionals are critical to our business, as noted below under "Business Development and Client Service Teams," and are generally focused geographically. In addition to our headquarters in the United States and representative office in Melbourne, we have four dedicated professionals located in our London office. During 2015 we demonstrated our commitment to the retail market with an expanded two person leadership team focusing on the growth of our distribution capabilities and intermediary business across channels. In 2016, we added three sales professionals to this intermediary distribution team. |

Our Investment Team

We have built an investment team that is well-suited to implement our classic value investment strategy. The members of our investment team have a diverse set of backgrounds, including former corporate management, private equity, management consulting, accounting, and Wall Street professionals. Their diverse business backgrounds are instrumental in enabling us to make investments in companies where we would be comfortable owning the entire business for a three- to five-year period. We look beyond temporary earnings shortfalls that result in stock price declines, which may lead others to forego investment opportunities, if we believe the long-term fundamentals of a company remain attractive.

As of December 31, 2016, we had a 25-member investment team. Each member serves as a research analyst, and certain members of the team also have portfolio management responsibilities. There are generally three portfolio managers for each investment strategy. These three managers have joint decision-making responsibility, and each has “veto authority” over all decisions regarding the relevant portfolio. Research analysts have sector and company-level research responsibilities which span all of our investment strategies, including those with a non-U.S. focus. In order to facilitate the professional development of our team, and to keep a fresh perspective on the companies in our investment portfolios, our research analysts generally rotate industry coverage every three to four years.

We follow a collaborative, consensus-oriented approach to making investment decisions, such that all members of our investment team, irrespective of their seniority, can play a significant role in this decision making process. We hold weekly research review meetings attended by all portfolio managers and relevant research analysts, and that are open to other employees, at which we openly discuss and debate our findings regarding the normalized earnings power of potential portfolio companies. In addition, we hold daily morning meetings, attended by our portfolio managers, research analysts, portfolio implementation, and client service personnel, in order to review developments in our holdings and set a trading strategy for the day. These meetings are critical for sharing relevant developments and analysis of the companies in our portfolios. We believe that our collaborative culture is attractive to our investment professionals.

Our Investment Strategies

As of December 31, 2016, our approximately $30.0 billion in AUM was invested in a variety of value-oriented investment strategies, representing differing degrees of concentration, and capitalization segments of U.S. and non-U.S. markets. See "Item 7 — Management's Discussion and Analysis of Financial Condition & Results of Operations — Operating Results — Assets Under Management and Flows" for additional details about our strategies.

4

The following table identifies our current U.S. and non-U.S. investment strategies, and the allocation of our AUM among them, as of December 31, 2016, 2015, and 2014:

Strategy1 | As of December 31, | |||||||||||

2016 | 2015 | 2014 | ||||||||||

U.S. Strategies | (in billions) | |||||||||||

Large Cap Value | $ | 9.4 | $ | 9.9 | $ | 11.9 | ||||||

Mid Cap Value | 2.5 | 1.8 | 1.8 | |||||||||

Value | 2.0 | 1.6 | 1.8 | |||||||||

Small Cap Value | 1.6 | 1.1 | 1.3 | |||||||||

Other U.S. Strategies | 0.1 | 0.1 | — | |||||||||

Global and Non-U.S. Strategies | ||||||||||||

International (ex-U.S.)Value | 4.9 | 4.2 | 3.4 | |||||||||

Global Value | 4.6 | 4.2 | 5.6 | |||||||||

Emerging Markets Value | 2.6 | 1.8 | 1.1 | |||||||||

European Value | 2.1 | 1.1 | 0.7 | |||||||||

Other Global and Non-U.S. Strategies | 0.2 | 0.2 | 0.1 | |||||||||

Total | $ | 30.0 | $ | 26.0 | $ | 27.7 | ||||||

1 Inclusive of our Expanded Value, Focused Value and variations thereof.

We follow the same investment process for each of these strategies. Our investment strategies are distinguished by the market capitalization ranges from which we select securities for their portfolios, which we refer to as each strategy’s investment universe, as well as the regions in which we invest. In addition, the number of holdings typically found in the portfolios of each of our investment strategies may vary depending on the degree of concentration in the portfolio, with our Focused value strategies generally reflecting fewer holdings than our Expanded value strategies.

Our largest investment strategies as of December 31, 2016 are further described below. This strategy detail is representative of our Expanded and Focused value strategies, and variations thereof.

U.S. Strategies

Large Cap Value. This strategy reflects a portfolio composed of approximately 30 to 80 stocks drawn generally from a universe of 500 of the largest U.S. listed companies, based on market capitalization.

Mid Cap Value. This strategy reflects a portfolio composed of approximately 30 to 80 stocks drawn generally from a universe of U.S. listed companies ranked from the 201st to 1,200th largest, based on market capitalization.

Value. This strategy reflects a portfolio composed of a portfolio of approximately 30 to 40 stocks drawn generally from a universe of 1,000 of the largest U.S. listed companies, based on market capitalization.

Small Cap Value. This strategy reflects a portfolio composed of approximately 40 to 50 stocks drawn generally from a universe of U.S. listed companies ranked from the 1,001st to 3,000th largest, based on market capitalization.

Global and Non-U.S. Strategies

International (ex-U.S.) Value. This strategy reflects a portfolio composed of approximately 30 to 80 stocks drawn generally from a universe of 1,500 of the largest companies across the world, excluding the United States, based on market capitalization.

Global Value. This strategy reflects a portfolio composed of approximately 40 to 95 stocks drawn generally from a universe of 2,000 of the largest companies across the world, based on market capitalization.

Emerging Markets Value. This strategy reflects a portfolio composed of approximately 40 to 80 stocks drawn generally from a universe of 1,500 of the largest emerging market companies, based on market capitalization.

5

European Value. This strategy reflects a portfolio composed of approximately 40 to 50 stocks drawn generally from a universe of 750 of the largest European companies, based on market capitalization.

We believe that our ability to retain and grow assets has been, and will continue to be, driven primarily by delivering attractive long-term investment results to our clients. We have therefore prioritized, and will continue to prioritize, investment performance over asset accumulation. Where we have deemed it necessary, we have, at times, closed certain products to new investors in order to preserve capacity to effectively implement our concentrated investment strategies for the benefit of existing clients. Currently, all of our investment strategies are open to new investors.

Our Strategy Development Approach

Historically, a major component of our growth has been the development of new strategies. Prior to incubating a new strategy, we perform in-depth research on the potential market for the product, as well as its overall compatibility with our investment expertise. This process involves analysis by our client team, as well as by our investment professionals. We will only launch a new product if we believe that it can add value to a client’s investment portfolio. Prior to marketing a new strategy, we generally incubate the product for a period of one to five years, so that we can test and refine our investment strategy and process before actively marketing the product to our clients.

Our Investment Performance

Since we are long-term fundamental investors, we believe that our investment strategies yield the most benefits and are best evaluated, over a long-term timeframe. For more information on our performance, see “Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations — Operating Results — Assets Under Management and Flows.”

Our Client Relationships and Distribution Approach

We believe that strong relationships with our clients are critical to our ability to succeed and to grow our AUM. In building these relationships, we have focused our efforts where we can efficiently access and service large pools of sophisticated clients with our team of dedicated business development and client service professionals.

We distribute our products to institutional and retail clients primarily through the efforts of our business development and client service team, who communicate directly with our clients and with the consultants who serve them, as well as through the marketing programs of our sub-investment advisory partners and intermediary distribution partners. Since our objective is to attract long-term investors with an investment horizon in excess of three years, our business development and client service efforts focus on educating our investors and intermediary distribution partners regarding our disciplined classic value investment process and philosophy.

Our business development and client service team is responsible for:

• | identifying, developing relationships with, and marketing to prospective institutional clients; |

• | providing ongoing service to existing institutional accounts; |

• | responding to requests for investment management proposals; |

• | developing and maintaining relationships with independent consultants; |

• | developing and maintaining relationships with intermediary partners to grow retail distribution capabilities; |

• | addressing all ongoing client needs, including periodic updates and reporting requirements; and |

• | developing direct relationships with clients sourced through consultant-led searches. |

Our business development and client service team is actively engaged with our research team to ensure our clients receive content-based information. We introduce members of our research and portfolio management team into client portfolio reviews to ensure that our clients are exposed to the full breadth of our investment resources. We also provide quarterly reports to our

6

clients in order to share our investment perspectives. We additionally meet and hold conference calls regularly with clients to share perspectives on the portfolio and the current investment environment.

Distribution Channels

We manage assets in two principal distribution channels. A summary of selected financial data attributable to our operations for each distribution channel is included in “Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The following table provides information regarding the composition of our total assets under management by distribution channel:

As of December 31, | ||||||||||||

Assets Under Management | 2016 | 2015 | 2014 | |||||||||

(in billions) | ||||||||||||

Institutional Accounts | $ | 16.9 | $ | 14.9 | $ | 15.6 | ||||||

Retail Accounts | 13.1 | 11.1 | 12.1 | |||||||||

Total | $ | 30.0 | $ | 26.0 | $ | 27.7 | ||||||

Institutional Distribution Channel

Since our inception, we have directly offered institutional investment products to public and corporate pension funds, endowments, foundations, and certain commingled vehicles geared toward institutional investors. We continue to develop direct relationships with the largest institutional investors and consultants around the world.

Retail Distribution Channel

We have established relationships with mutual fund and fund providers globally, that offer us opportunities to efficiently access market segments geared primarily toward retail investors through sub-investment advisory roles. The funds that we sub-advise are generally either multi-manager funds, in which we manage only a portion of the fund's portfolio, or funds for which we are the sole sub-adviser.

We currently sub-advise five funds that are advised by The Vanguard Group. We manage a portion of each of the Vanguard Windsor Fund, Vanguard Selected Value Fund, Vanguard Emerging Markets Select Stock Fund and Vanguard Global Emerging Markets Fund, and are the sole sub-adviser of the Vanguard U.S. Fundamental Value Fund. As of December 31, 2016, these five funds represented $7.4 billion, or 24.8%, of our AUM. For the years ended December 31, 2016, 2015, and 2014, approximately 10.1%, 10.8%, and 9.4%, respectively, of our total revenue was generated from our sub-investment advisory agreements with The Vanguard Group.

We sub-advise a mutual fund that is advised by John Hancock Advisers, namely the John Hancock Classic Value Fund. As of December 31, 2016, this fund represented $1.7 billion, or 5.8%, of our AUM. For the years ended December 31, 2016, 2015, and 2014 approximately 4.8%, 5.9%, and 7.6%, respectively, of our total revenue was generated from our sub-investment advisory agreement with John Hancock Advisers.

Pzena Funds

U.S. investors that do not meet our minimum account size for a separate account, or who otherwise prefer to invest through a mutual fund, can invest in certain of our strategies through our Pzena mutual funds, which were launched during 2014 and are included in our retail distribution category. In 2016, we launched a fourth Pzena mutual fund. We act as the investment adviser to four Pzena mutual funds that offer no-load, open-end share classes designed to meet the needs of a range of investor types.

In addition, we serve as investment manager and promoter of Pzena Value Funds plc and its respective sub-funds, a family of Irish-based UCITS funds primarily reflecting institutional investors. Pzena Value Funds plc began operations in 2005 and offers shares to non-U.S. investors. We currently offer a sub-fund corresponding to our Emerging Markets Focused Value, Global Expanded Value, Global Focused Value, and Large Cap Expanded Value strategies.

We also offer access to certain of our global and non-U.S. strategies through private placement vehicles and collective investment trusts.

7

Advisory Fees

We earn advisory fees on the accounts that we manage for institutional clients and for retail clients which are primarily sub-advised mutual funds.

On our institutional accounts, we are paid fees according to a schedule which varies by investment strategy. The substantial majority of these accounts pay us management fees pursuant to a schedule in which the rate we earn on the AUM declines as the amount of AUM increases.

With respect to our retail accounts, as of December 31, 2016, we sub-advised fifteen SEC-registered mutual funds that each have an initial two-year term and are thereafter subject to annual renewal by each fund’s board of directors pursuant to the Investment Company Act of 1940, as amended (the “Investment Company Act”). Twelve of these fifteen sub-investment advisory agreements are beyond their initial two-year terms as of December 31, 2016. In addition, we sub-advise twenty-one non-U.S. funds. Under these agreements, we are generally paid a management fee according to a schedule, pursuant to which the rate we earn on the AUM declines as the amount of AUM increases. Certain of these funds pay us fixed-rate management fees. Due to the substantially larger account size of certain of these accounts, the average advisory fees we earn on them, as a percentage of AUM, are lower than the advisory fees we earn on our institutional accounts.

Advisory fees we earn on institutional accounts are generally based on the value of AUM at a specific date on a quarterly basis. Certain of our institutional accounts, and all of the mutual funds that we sub-advise, are calculated based on the average of the monthly or daily market value of the account. Advisory fees are also generally adjusted for any cash flows into or out of a portfolio, where the cash flow represents greater than 10% of the value of the portfolio. While a specific group of accounts may use the same fee rate, the calculation methodology may differ, as described above.

Certain of our clients pay us performance fees according to the performance of their accounts relative to certain agreed-upon benchmarks, which results in a lower base fee, but allows for us to earn higher fees if the relevant investment strategy outperforms the agreed-upon benchmark. Some performance-based fee arrangements include high-water mark provisions, which generally provide that if a client account underperforms relative to its performance target, it must gain back such underperformance before we can collect future performance-based fees. Fulcrum fee arrangements related to one client relationship require a reduction in the base fee, or allow for a performance fee if the relevant investment strategy underperforms or outperforms, respectively, the agreed-upon benchmark.

Competition

We compete in all aspects of our business with a large number of investment management firms, commercial banks, broker-dealers, insurance companies, and other financial institutions.

In order to grow our business, we must be able to compete effectively to maintain existing AUM and attract additional AUM. Historically, we have competed for AUM principally on the basis of:

• | the performance of our investment strategies; |

• | our clients’ perceptions of our drive, focus, and alignment of our interests with theirs; |

• | the quality of the service we provide to our clients and the duration of our relationships with them; |

• | our brand recognition and reputation within the investing community; |

• | the range of strategies and investment vehicles we offer; and |

• | the level of advisory fees we charge for our investment management services. |

Our ability to continue to compete effectively will also depend upon our ability to attract highly qualified investment professionals and retain our existing employees.

Employees

At December 31, 2016, we had 100 full-time employees, including 25 investment professionals and 23 business development and client service professionals.

8

Regulatory Environment and Compliance

Our business is subject to extensive regulation in the United States at both the federal and state level, as well as by self-regulatory organizations. Under these laws and regulations, agencies that regulate investment advisers have broad administrative powers, including the power to limit, restrict, or prohibit an investment adviser from carrying on its business in the event that it fails to comply with such laws and regulations. Possible sanctions that may be imposed include the suspension of individual employees, limitations on engaging in certain lines of business for specified periods of time, revocation of investment adviser and other registrations, censures and fines. Our business is also subject to foreign regulation, as discussed below.

SEC Regulation

Our operating company, Pzena Investment Management, LLC, is registered as an investment adviser with the SEC. As a registered investment adviser, it is subject to the requirements of the Investment Advisers Act of 1940, as amended, which we refer to as the Investment Advisers Act, and the SEC’s regulations thereunder, as well as to examination by the SEC’s staff. The Investment Advisers Act imposes substantive regulation on virtually all aspects of Pzena Investment Management, LLC's business and its relationships with its clients. As an investment adviser, Pzena Investment Management, LLC owes fiduciary duties to its clients, which relate to conflicts of interest, client recommendations and other fundamental matters. Applicable requirements relate to, among other things, engaging in transactions with clients, maintaining an effective compliance program, performance fees, solicitation arrangements, advertising, recordkeeping, reporting, and disclosure requirements.

The U.S. funds for which Pzena Investment Management, LLC acts as the sub-investment adviser and four of the U.S. funds for which Pzena Investment Management, LLC acts as investment adviser, are registered with the SEC under the Investment Company Act. The Investment Company Act imposes additional obligations, including detailed operational requirements for both the funds and their advisers. Moreover, the Investment Company Act requires that an investment adviser’s contract with a registered fund may be terminated by the fund on not more than 60 days’ notice, and is subject to annual renewal by the fund’s board after an initial two-year term.

Both the Investment Advisers Act and the Investment Company Act regulate the “assignment” of advisory contracts by the investment adviser. The SEC is authorized to institute proceedings and impose sanctions for violations of the Investment Advisers Act and the Investment Company Act, ranging from fines and censures to termination of an investment adviser’s registration.

Pzena Financial Services, LLC, our SEC registered broker-dealer subsidiary, is subject to the SEC's Uniform Net Capital Rule, which requires that at least a minimum part of a registered broker-dealer's assets be kept in relatively liquid form. At December 31, 2016, Pzena Financial Services, LLC had net capital of $253,633, which was $246,011 in excess of its net capital requirement of $7,622.

ERISA-Related Regulation

With respect to our benefit plan clients, Pzena Investment Management, LLC is a “fiduciary” under the Employment Retirement Act of 1974, or ERISA, and is therefore subject to ERISA, and to regulations promulgated thereunder. ERISA and applicable provisions of the Internal Revenue Code impose certain duties on persons who are fiduciaries under ERISA, prohibit certain transactions involving ERISA plan clients, and provide monetary penalties for violations of these prohibitions.

Foreign Regulation

Pzena Investment Management, LLC maintains a representative office in Melbourne, Australia, and maintains an exemption from the Australian Financial Services license requirement under the Corporations Act 2001 of the Commonwealth of Australia.

Pzena Investment Management, Ltd, our United Kingdom subsidiary, is an appointed representative of Mirabella Advisers LLP which is authorized and regulated by the Financial Conduct Authority ("FCA") in the United Kingdom.

9

Pzena Investment Management, LLC currently avails itself of the international adviser exemption in Ontario, Canada. In addition, Pzena Investment Management, LLC is registered as an exempt market dealer in Ontario, Canada. As an exempt adviser, Pzena Investment Management, LLC is only permitted to provide advice in Ontario to certain institutional and high net worth individual clients. As an exempt market dealer, Pzena Investment Management, LLC is permitted to act as a market intermediary for only certain types of trades, and is permitted to market, sell and distribute prospectus-exempt securities to accredited investors. An exempt adviser and market dealer must, upon the request of the Ontario Securities Commission, or OSC, produce all books, papers, documents, records and correspondence relating to its activities in Ontario, and inform the OSC if it becomes the subject of an investigation or disciplinary action by any financial services or securities regulatory authority or self-regulatory authority.

We operate in various other foreign jurisdictions without registration in reliance upon applicable exemptions under the laws of those jurisdictions.

Our Executive Officers

Richard S. Pzena was appointed our Chairman, Chief Executive Officer and Co-Chief Investment Officer in May 2007. Prior to forming Pzena Investment Management, LLC in 1995, Mr. Pzena was the Director of U.S. Equity Investments and Chief Research Officer for Sanford C. Bernstein & Company. Mr. Pzena joined Sanford C. Bernstein & Company in 1986 as an oil industry analyst. During 1990 and 1991, Mr. Pzena served as Chief Investment Officer, Small Cap Equities, and assumed his broader domestic equity role in 1991. Prior to joining Bernstein, Mr. Pzena worked for the Amoco Corporation in various financial and planning roles. He earned a B.S. summa cum laude and an M.B.A. from the Wharton School of the University of Pennsylvania in 1979 and 1980, respectively.

John P. Goetz was appointed our President, and Co-Chief Investment Officer in June 2007, and became a member of our Board of Directors in May 2011. Mr. Goetz joined us in 1996 as Director of Research and has been Co-Chief Investment Officer since 2005. Previously, Mr. Goetz held a range of key positions at Amoco Corporation for over 14 years, most recently as the Global Business Manager for Amoco’s $1 billion polypropylene business, where he had bottom-line responsibility for operations and development worldwide. Prior positions at Amoco included strategic planning, joint venture investments and project financing in various oil and chemical businesses. Prior to joining Amoco, Mr. Goetz had been employed by The Northern Trust Company and Bank of America. He earned a B.A. summa cum laude in Mathematics and Economics from Wheaton College in 1979 and an M.B.A. from the Kellogg School at Northwestern University in 1982.

William L. Lipsey was appointed our President, and Head of Business Development and Client Service in June 2007, and became a member of our Board of Directors in May 2011. Before joining Pzena Investment Management in 1997, Mr. Lipsey was an Investment Advisory Consultant and a Senior Vice President at Oppenheimer & Company, Inc. Prior to joining Oppenheimer & Company, Inc., Mr. Lipsey’s career included positions at Morgan Stanley, Kidder Peabody and Hewitt Associates. At Morgan Stanley and Kidder Peabody, Mr. Lipsey managed assets for institutional and private clients. He earned a B.S. in Economics from the Wharton School of the University of Pennsylvania in 1980 and an M.B.A. in Finance from the University of Chicago in 1986.

Michael D. Peterson was appointed Executive Vice President in February 2011. Prior to joining Pzena Investment Management in 1998, Mr. Peterson was an engagement manager at McKinsey & Company. At McKinsey & Company, he was a member of the Financial Institutions Group, as well as the Pricing Practice. Prior to joining McKinsey & Company, he was an Assistant Professor at the Indiana University School of Public and Environmental Affairs, where he taught operations research and operations management. He holds a PhD in Management (Operations Research) from the M.I.T. Sloan School of Management, where he was a National Science Foundation fellow from 1989 to 1992. Prior to that, he received an M.A. in Mathematics from the University of Cambridge in 1988 and an A.B. summa cum laude in Economics from Princeton University.

Jessica R. Doran was appointed to the position of Chief Financial Officer and Treasurer in July 2016. Ms. Doran has spent over ten years with Pzena working across various functions including operations, internal audit and most recently as the Manager of Financial Reporting. Ms. Doran received her B.A. in Economics and Management from Gettysburg College in 2003 and an M.S. in Accounting from Fordham Graduate School of Business in 2014. Ms. Doran is a Certified Public Accountant.

Gary J. Bachman was appointed to the position of Chief Operating Officer in July 2016. Mr. Bachman joined Pzena Investment Management in 2012 and served as Chief Financial Officer before his role as Chief Operating Officer. Prior to joining Pzena Investment Management, Mr. Bachman served as Executive Director of the Investment Bank Finance Department at JP Morgan Chase, from 2008 to 2012. Prior to this, Mr. Bachman worked in the Strategic Transaction and

10

Accounting Policy and External Reporting groups at Lehman Brothers, from 2000 to 2008. Mr. Bachman received his B.S. in Accounting from Binghamton University in 1990 and an M.B.A. in Finance from Fordham University in 1998. Mr. Bachman is a Certified Public Accountant.

Available Information

We make available free of charge through our website, www.pzena.com, our annual reports on Form 10-K, our quarterly reports on Form 10-Q and our current reports on Form 8-K, as well as amendments to those reports, and other filings required under the Securities Act or the Exchange Act as soon as reasonably practicable after they are electronically filed with the Securities and Exchange Commission ("SEC"). To retrieve these reports, and any amendments thereto, visit the Investor Relations section of our website. The SEC maintains a website at www.sec.gov. All of the materials we filed with the SEC may be accessed free of charge on the SEC's website through its EDGAR page. The SEC also has a Public Reference Room at 100 F Street, NE Washington, D.C., where our materials may be read and/or copied. Information about the operation of the Public Reference Room can be obtained by calling 1-800-SEC-0330.

Our Corporate Governance Guidelines, Code of Business Conduct and Ethics, Code of Ethics for Senior Financial Officers, and Board of Directors committee charters (including the charters of the Audit Committee, Compensation Committee, and Nominating and Corporate Governance Committee) are also available free of charge through our website under "Investor Relations — Corporate Governance."

The information on the Company's website is not part of, or incorporated by reference into, this Annual Report, or any other report we file with, or furnish to the SEC.

ITEM 1A. | RISK FACTORS |

We face a variety of significant and diverse risks, many of which are inherent in our business. Described below are the risks we currently believe could materially and adversely affect our business, financial condition, results of operations or cash flow.

Risks Related to Our Business

Our primary source of revenue is derived from management fees, which are directly tied to our assets under management. Fluctuations in AUM therefore will directly impact our revenue.

Substantially all of our revenue is derived from management fees paid by our clients, based on a percentage of the market value of our AUM. Any decline and/or significant impairment in AUM would greatly affect our revenue, and could occur due to a variety of factors, including:

• | Poor performance of our strategies: Poor performance of our investment strategies may result in decreased market value of AUM. In addition, underperformance could impact our ability to maintain our existing client base and develop new relationships, both of which could negatively impact AUM. |

• | Poor market environment: We expect our business may generate lower revenue in a depressed equities market or general economic downturn as a result of depreciation of our AUM. Any decline in the market value of securities held in client portfolios due to such adverse conditions would reduce AUM and lead to a decrease in revenue. Investor sentiment in a poor equities market environment could also decrease inflows and increase outflows from our investment strategies in favor of investments perceived as more attractive. |

• | Global market, economic, geo-political and other conditions: As a company that invests in both U.S. and non-U.S. markets, and with a global client base, our business is subject to changing conditions in the global financial markets, and may also be affected by domestic and international political, social and economic conditions, any of which could negatively impact our investment performance, growth strategy and AUM. See "Our global and non-U.S. strategies consist primarily of investments in the securities of issuers located outside of the United States, which may involve foreign currency exchange, political, social and economic uncertainties and risks" below. |

• | Termination of significant relationships: Our clients can generally terminate our advisory agreements or reduce assets under management upon short notice and for any reason. Investors in the pooled funds that we manage may also redeem their investments in the funds at any time without prior notice. As of December 31, 2016, three client relationships represented 37% and 20% of our AUM and revenue, respectively, including one client relationship which |

11

represents approximately 25% and 10% of our AUM and revenue respectively. The termination of any of these relationships and outflow of money from our pooled funds could significantly reduce our revenue, and we may not be able to establish relationships with other clients in order to replace the lost revenue. There can also be no assurance that our agreements with respect to these relationships will remain in place going forward.

• | Defined benefit plans are declining: Defined benefit plans are declining as corporate plan sponsors are decreasing their liabilities and shifting employee enrollment to defined contribution plans. We currently do not have significant exposure to the defined contribution market but continue to try to gain new assets in this market. Given the reduction in funding and shift to defined contribution plans there is no guarantee that we will be successful in increasing our penetration of the defined contribution market, which could limit our ability to grow our AUM. |

• | Intermediary dependence: New accounts sourced through consultant-led searches have been a large driver of our inflows in the past, and are expected to be a major component of our inflows going forward. We have also established relationships with certain mutual fund providers who have offered us opportunities to access certain market segments through sub-investment advisory roles. Such consultants and mutual fund providers routinely review and evaluate our organization and the services we offer, and poor evaluations may result in client outflows and impact our ability to attract new assets through such intermediaries. See "Item 1 — Our Business Strategy — Work with Our Strong Consultant Relationships" and "Item 1 — Our Client Relationships and Distribution Approach — Distribution Channels — Retail Distribution Channel". |

• | Passive strategies, such as index and exchange-traded funds have grown substantially in relation to active strategies: During the past decade investors have exhibited a desire for passive investment products given their relative performance and lower fee structure compared to active strategies managed by investment managers such as ourselves. If this market preference continues, existing and prospective clients may choose to invest in passive investment products, our growth strategy may be impaired and our AUM may be negatively impacted. |

We may face capacity constraints in certain of our strategies which may prevent us from accepting new investors in those strategies.

Our ability to retain and grow assets as a firm has been, and will be, driven primarily by delivering attractive investment results to our clients. As a consequence, we have prioritized, and will continue to prioritize, investment performance over asset accumulation. Where we deemed it necessary, we have, at times, closed certain strategies to new investors in order to preserve capacity to effectively implement our concentrated investment strategies for the benefit of existing clients. We may in the future close certain of our strategies to new investors or to new inflows from existing investors. Any such closures may limit our future AUM growth and hence our revenue growth.

Market and competitive pressures to lower our advisory fees could lead to a decline in our profit and earnings.

Market and competitive pressures in recent years have created a trend towards lower management fees in the asset management industry and there can be no assurance that we will be able to maintain our current fee structure going forward. As a result, a shift in the composition of our AUM from higher to lower fee-generating client relationships would result in a decrease in revenue, even if our aggregate level of AUM remains unchanged or increases.

A portion of our investment advisory revenue is also derived from performance fees. We generally earn performance fees under certain client agreements according to the performance relative to an agreed-upon benchmark. This fee structure results in a lower base fee but allows for us to earn higher fees if the investment strategy outperforms the benchmark. Some performance-based fee arrangements include high-water mark provisions, which generally provide that if a client account underperforms relative to its performance target, it must gain back such underperformance before we can collect future performance-based fees. Therefore, if we fail to achieve the performance target for a particular period, we may not earn a performance fee for that period and for accounts with a high-water mark provision, our ability to earn future performance fees may be impaired. During fiscal years 2016 and 2015, we earned $0.2 million and $4.5 million in performance fees, respectively. An increase in performance-based fee arrangements with clients could create greater fluctuations in our revenue and earnings.

In addition, certain accounts related to one retail client relationship have fulcrum fee arrangements. These fee arrangements require a reduction in the base fee, or allow for a performance fee if the relevant investment strategy underperforms or outperforms, respectively, the agreed-upon benchmark over the contract's measurement period, which extends to three years. We recognized a $1.0 million reduction in base fees related to these fee arrangements for the year ended

12

December 31, 2016, which does not reflect the minimum base fees of accounts with fulcrum fee arrangements. For the year ended December 31, 2015, we did not recognize a reduction in base fees related to fulcrum fee arrangements. To the extent the three-year performance records of these accounts fluctuate relative to their relevant benchmarks, the amount of base fees recognized may vary.

Increases in our expenses could lead to a decline in our profit margin and increase the volatility of our earnings.

Our expenses are subject to increase based on a variety of factors such as higher operating expenses resulting from business expansion, product development and increased marketing efforts; higher compensation expense due to increased competition for talent, headcount and seniority level; and related expenses to meet business and regulatory needs. Some or all of these expenses may remain at higher levels for the foreseeable future, leading to higher costs for our business. Fluctuations in expenses could impact our profit margins and contribute to earnings volatility.

Loss of key employees, and difficulties in attracting qualified investment professionals, could have a material adverse effect on our business.

The success of our business largely depends on the participation of Richard S. Pzena and the other members of our Executive Committee. Their professional reputations, expertise in investing, and relationships with our clients and within the investing community in the U.S. and abroad are critical to executing our business strategy and attracting and retaining clients. The retention of these individuals is crucial to our future success. There is no guarantee that they will not resign, join our competitors or form a competing company. The terms of the current operating agreement of our operating company restrict each of these individuals from competing with us or soliciting our clients or employees during the term of their employment with us and, in certain circumstances, for a certain period thereafter. The penalty for breach of these restrictive covenants may be the forfeiture of a number of Class B units held by the individual, and his permitted transferees, as of the earlier of the date of his breach or the termination of his employment. Although we may seek specific performance of these restrictive covenants, there can be no assurance that we would be successful in obtaining this relief. After this post-employment restrictive period, we may not be able to prohibit them from competing with us or soliciting our clients or employees. Furthermore, we do not carry any "key man" insurance that would provide us with proceeds in the event of the death or disability of any of the above mentioned employees.

In addition to the participants mentioned above, our success also depends on our ability to retain the senior members of our investment team and to recruit additional qualified investment professionals. We may not be successful in our efforts to retain and recruit such individuals as the market for investment professionals is extremely competitive. Our portfolio managers possess substantial experience and expertise in classic value investing and maintain significant relationships with our clients. The loss of any of our senior investment professionals could limit our ability to successfully execute our investment approach and to sustain the performance of our investment strategies, which, in turn, could have a material adverse effect on our reputation, client relationships and our revenue and earnings.

Future growth of our business may place significant demands on our resources and employees and may increase our expenses, risks and regulatory oversight.

Future growth of our business may place significant demands on our infrastructure, our investment team and other employees, which may increase our expenses. In addition, we are required to continuously develop our infrastructure in response to the increasing sophistication of the investment management market, as well as compliance with legal and regulatory developments. We may face significant challenges in: maintaining and developing adequate financial and operational controls; implementing new or updated information and financial systems, and procedures and training; and managing and appropriately sizing our work force, and other components of our business on a timely and cost-effective basis. There can be no assurance that we will be able to manage the growth of our business effectively, or that we will be able to continue to grow, and any failure to do so could adversely affect our ability to generate revenue and control expenses.

The potential inability of our systems to accommodate an increasing volume of transactions could also constrain our ability to expand our businesses and potentially raise regulatory issues. In recent years, we have substantially upgraded and expanded the capabilities of our data processing systems and other operating technology, and we expect that we may need to continue to upgrade and expand these capabilities in the future to avoid disruption of, or constraints on, our operations.

13

We face risks, and corresponding potential costs and expenses, associated with conducting operations and growing our business in numerous countries.

We offer investment management services in different regulatory jurisdictions around the world, and intend to continue to expand our operations internationally. In order to remain competitive, we must be proactive and prepared to deploy necessary resources when and where growth opportunities present themselves. If we lack the necessary resources and/or personnel, we may be unable to take full advantage of strategic opportunities when they appear and our strategic decisions may not be efficiently implemented. Meeting local requirements and complying with local industry standards may also place additional demands on sales and compliance personnel and resources that we may not be able to meet. Finding and hiring additional, well-qualified personnel and crafting and adopting policies, procedures and controls to address local or regional requirements remain a challenge as we expand our operations internationally. Moreover, regulators could also change their policies or laws in a manner that might restrict or otherwise impede our ability to offer our investment products in their respective markets. Any of these requirements, activities, or needs could increase the costs and expenses we incur in a specific jurisdiction without any corresponding increase in revenue and income from operating in such jurisdiction.

The investment management business is intensely competitive.

Competition in the investment management business is based on a variety of factors, including investment performance; investor perception of an investment manager’s drive, focus and alignment of interests; quality of service provided to clients and duration of client relationships; business reputation; and level of fees charged for services. We compete in all aspects of our business with a large number of investment management firms, commercial banks, broker-dealers, insurance companies and other financial institutions. Our competitive risks are heightened by the fact that some of our competitors may implement investment styles that are viewed more favorably than ours or they may invest in alternative asset classes which the markets may perceive as more attractive than the public equity markets. If we are unable to compete effectively, our revenue could be reduced, and our business could be materially affected.

We may not be successful in expanding into new investment strategies, markets and businesses.

We actively consider the opportunistic expansion of our businesses, but we may not be successful in any such attempted expansion. Attempts to expand our businesses involve a number of risks, including entry into markets in which we may have limited or no experience, increasing the demands on our operational systems, the broadening of our geographic footprint, increasing the risks associated with conducting operations in non-U.S. jurisdictions and the diversion of management’s attention from our core businesses.

We also may not be successful in identifying new investment strategies or geographic markets that increase our profitability. Because we have not yet identified all of these potential new investment strategies, geographic markets or

businesses, we cannot identify all the risks we may face and the potential adverse consequences. We also do not know how long it may take for us to expand, if we do so at all.

A change of control could result in termination of our investment advisory or sub-investment advisory agreements.

Pursuant to the Investment Company Act, each of the investment advisory or sub-investment advisory agreements for the SEC-registered mutual funds that we advise will automatically terminate upon their deemed “assignment,” and a fund’s board and shareholders must approve a new agreement in order for us to continue to act as its investment adviser or sub-investment adviser. In addition, pursuant to the Investment Advisers Act, each of our investment advisory agreements for the separate accounts we manage contains a provision that states that the agreement may not be “assigned” without the consent of the client. An "assignment," pursuant to both the Investment Company Act and the Investment Advisers Act, could be deemed to occur upon a sale or transfer of a controlling block of our voting securities. Such an assignment may be deemed to occur in the event that the holders of the Class B units of our operating company exchange enough of their Class B units for shares of our Class A common stock such that they no longer own a controlling interest in us. If such a deemed assignment occurs, there can be no assurance that we will be able to obtain the necessary consents from clients whose assets are managed pursuant to separate accounts, or the necessary approvals from the boards and shareholders of the SEC-registered funds that we sub-advise. An assignment, actual or constructive, would trigger these termination and consent provisions and, unless the necessary approvals and consents are obtained, could adversely affect our ability to continue managing client accounts, resulting in the loss of AUM and a corresponding loss of revenue.

14

Extensive regulation of our business has been and will be expensive and time consuming, and exposes us to the potential for significant penalties, including fines or limitations on our ability to conduct our business.

We are subject to extensive regulation of our investment management business and operations. As a registered investment adviser, the SEC oversees our activities pursuant to its regulatory authority under the Investment Advisers Act. In addition, we must comply with certain requirements under the Investment Company Act with respect to the SEC-registered funds for which we act as investment adviser or sub-investment adviser. Pzena Financial Services, LLC, our SEC registered broker dealer subsidiary is regulated by the Financial Industry Regulatory Authority ("FINRA"). Each of the regulatory bodies with jurisdiction over us has the authority to regulate various aspects of financial services, including the authority to grant, and, in specific circumstances to cancel, permissions to carry on particular businesses. Our failure to comply with applicable laws or regulations could result in fines, censure, suspensions of personnel or other sanctions, including revocation of our registration as an investment adviser. Even if a sanction imposed against us is small in monetary amount, the adverse publicity arising from the imposition of such sanctions by regulators could harm our reputation, result in withdrawal by our clients and/or impede our ability to retain clients and develop new client relationships. As we continue to expand into the international market, we may also be under the regulatory scope of local regulatory authorities and non-compliance with any of these authorities may result in fines, sanctions and inability to operate in that local market.

The SEC and its staff continue to engage in various initiatives and reviews that seek to improve and modernize the regulatory structure governing the asset management industry, and registered investment companies in particular. During the past few years, the SEC proposed, among other things, enhanced reporting by investment advisors, enhanced reporting on registered mutual funds and cyber security and new vendor concerns. While these proposals have yet to be finalized into new rules, any new rules, guidance or regulatory initiatives resulting from these efforts could expose us to additional compliance and reporting costs and may require us to change how we operate our business or manages funds.

The United Kingdom (U.K.) and other European jurisdictions in which we operate have implemented the Markets in Financial Instruments Directive (MiFID) rules into national legislation and have begun to implement MiFID II. MiFID II builds upon many initiatives introduced through MiFID which primarily focused on equity trading activity to migrate onto open and transparent markets. MiFID II, which will come into full effect in January 2018, will be implemented through a number of more detailed directives, regulations and standards to be made by the European Commission and by the European Securities Markets Authority (ESMA). It is expected that MiFID II will have significant and wide-ranging impacts on the European Union (EU) securities market, including (i) enhanced investor protection and governance standards, (ii) rules regarding the ability of portfolio management firms to receive and pay for investment research relating to all asset classes, (iii) an enhanced role for ESMA in supervising EU securities, (iv) new requirements regarding non-EU investment firms’ access to EU financial markets, as well as many other requirements for derivatives and trading activities. Each of these proposals, if adopted as stated may impose additional technological and compliance costs. We continue to monitor developments of these rules and the impact they may have on business activities.

In June 2016, the U.K. held a referendum in which voters approved an exit from the EU, commonly referred to as “Brexit.” As a result of the referendum, it is expected that the British government will begin negotiating the terms of the U.K.’s future relationship with the EU. The referendum is non-binding, however if passed into law, negotiations would commence to determine future terms of the U.K.’s relationship with the EU, including the terms of trade between the U.K. and the EU. The effects of Brexit will depend on any agreements the U.K. makes to retain access to EU markets either during a transitional period or more permanently. The measure could lead to regulatory changes and uncertainty and result in additional legal and compliance costs. We are actively working to ensure our operations are structured effectively and efficiently to service U.K. and European clients.

We also face the risk of significant intervention by regulatory authorities, including extended investigation and surveillance activity, adoption of costly or restrictive new regulations, and judicial or administrative proceedings that may result in substantial penalties. The requirements imposed by our regulators are designed to ensure the integrity of the financial markets and to protect customers and other third parties who deal with us, and are not designed to protect our stockholders. Any regulatory and legislative actions and reforms affecting the investment advisory industry may negatively impact earnings by increasing our costs of operations.

In addition, the regulatory environment in which we operate is subject to ongoing modification and further regulation. The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (“the Dodd-Frank Act”), and regulations to be promulgated pursuant to it, is one such example. Certain provisions of the Dodd-Frank Act may have unintended consequences on the financial market as a whole that could negatively affect our business.

15

Specific regulatory changes also may have a direct impact on the revenue of our business. In addition to regulatory scrutiny and potential fines and sanctions, regulators continue to examine different aspects of the asset management industry. For example, the use of “soft dollars,” where a portion of commissions paid to broker-dealers in connection with the execution of trades also pays for research and other services provided to advisors, has been reexamined by different regulatory bodies and may in the future be limited or modified. Although a substantial portion of the research relied on by our business in the investment decision-making process is generated internally by our investment analysts, external research, including external research paid for with soft dollars, is important to the process. This external research generally is used for information gathering or verification purposes, and includes broker-provided research, as well as third-party provided databases and research services. If the use of soft dollars were to be limited, we would have to bear additional costs.

The U.S. Department of Labor’s fiduciary rule could adversely affect our financial condition and results of operations.