Attached files

| file | filename |

|---|---|

| EX-10.67 - EXHIBIT 10.67 - Univar Solutions Inc. | unvr-12312016xex1067.htm |

| EX-32.2 - EXHIBIT 32.2 - Univar Solutions Inc. | unvr-12312016xex322.htm |

| EX-32.1 - EXHIBIT 32.1 - Univar Solutions Inc. | unvr-12312016xex321.htm |

| EX-31.2 - EXHIBIT 31.2 - Univar Solutions Inc. | unvr-12312016xex312.htm |

| EX-31.1 - EXHIBIT 31.1 - Univar Solutions Inc. | unvr-12312016xex311.htm |

| EX-23.1 - EXHIBIT 23.1 - Univar Solutions Inc. | unvr-12312016xex231.htm |

| EX-21.1 - EXHIBIT 21.1 - Univar Solutions Inc. | unvr-12312016xex211.htm |

| EX-10.68 - EXHIBIT 10.68 - Univar Solutions Inc. | unvr-12312016xex1068.htm |

| EX-10.66 - EXHIBIT 10.66 - Univar Solutions Inc. | unvr-12312016xex1066.htm |

| EX-10.65 - EXHIBIT 10.65 - Univar Solutions Inc. | unvr-12312016xex1065.htm |

| EX-10.25 - EXHIBIT 10.25 - Univar Solutions Inc. | unvr-12312016xex1025.htm |

| EX-10.24 - EXHIBIT 10.24 - Univar Solutions Inc. | unvr-12312016xex1024.htm |

| EX-10.18 - EXHIBIT 10.18 - Univar Solutions Inc. | unvr-12312016xex1018.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________________________________

Form 10-K

__________________________________________________________

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-37443

_________________________________________________________

Univar Inc.

(Exact name of registrant as specified in its charter)

__________________________________________________________

Delaware | 26-1251958 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

3075 Highland Parkway, Suite 200 Downers Grove, Illinois | 60515 |

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (331) 777-6000

__________________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock ($0.01 par value) | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ý | Accelerated filer | ¨ |

Non-accelerated filer | ¨ | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ý

Aggregate market value of common stock held by non-affiliates of registrant on June 30, 2016: $770.5 million (see Item 12, under Part III hereof), based on a closing price of registrant’s Common Stock of $18.91 per share.

At February 10, 2017, 139,846,144 shares of the registrant’s common stock, $0.01 par value, were outstanding.

Documents Incorporated by Reference

Certain portions of the registrant’s Proxy Statement for the Annual Meeting of Stockholders to be held May 4, 2017 and to be filed within 120 days after the registrant’s fiscal year ended December 31, 2016 (hereinafter referred to as “Proxy Statement”) are incorporated by reference into Part III.

Univar Inc.

Form 10-K

TABLE OF CONTENTS

Page | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

2

SUPPLEMENTAL INFORMATION

Unless the context otherwise indicates or requires, as used in this Annual Report on Form 10-K, (i) the terms “we,” “our,” “us,” “Univar” and the “Company,” refer to Univar Inc. and its consolidated subsidiaries, and (ii) the term “issuer” refers to Univar Inc. exclusive of its subsidiaries.

Our fiscal year ends on December 31, and references to “fiscal” when used in reference to any twelve month period ended December 31, refer to our fiscal years ended December 31.

The term “GAAP” refers to accounting principles generally accepted in the United States of America.

____________________________________

Forward-looking statements and information

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Private Securities litigation Reform Act of 1995. Some of the forward-looking statements can be identified by the use of forward-looking terms such as “believes,” “expects,” “may,” “will,” “should,” “could,” “seeks,” “intends,” “plans,” “estimates,” “anticipates” or other comparable terms. These forward-looking statements include all matters that are not historical facts. They appear in a number of places throughout this Annual Report on Form 10-K and include statements regarding our intentions, beliefs or current expectations concerning, among other things, our results of operations, financial condition, macro-economic conditions, liquidity, prospects, business trends, currency trends, competition, markets, growth strategies and the industries in which we operate and including, without limitation, statements relating to our estimated or anticipated financial performance or results. Forward-looking statements are subject to known and unknown risks and uncertainties, many of which may be beyond our control. We caution you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition and liquidity, and the development of the industries in which we operate may differ materially from those made in or suggested by the forward-looking statements contained in this Annual Report on Form 10-K. In addition, even if our results of operations, financial condition and liquidity, and the development of the industries in which we operate are consistent with the forward-looking statements contained in this Annual Report on Form 10-K, those results or developments may not be indicative of results, conditions or developments in subsequent periods. A number of important factors could cause actual results to differ materially from those contained in or implied by the forward-looking statements, including those reflected in forward-looking statements relating to our operations and business and the risks and uncertainties discussed in “Risk Factors.” Factors that could cause actual results to differ from those reflected in forward-looking statements relating to our operations and business include:

• | general economic conditions, particularly fluctuations in industrial production and the demands of our customers; |

• | disruptions in the supply of chemicals we distribute or our customers' or producers' operations; |

• | termination or change of contracts or relationships with customers or producers on short notice; |

• | the price and availability of chemicals, or a decline in the demand for chemicals; |

• | our ability to pass through cost increases to our customers; |

• | our ability to meet customer demand for a product; |

• | trends in oil and gas prices; |

• | our ability to execute strategic investments, including pursuing acquisitions and/or dispositions, and successfully integrating and operating acquired companies; |

• | challenges associated with international operations, including securing producers and personnel, import/export requirements, compliance with foreign laws and international business laws and changes in economic or political conditions; |

• | our ability to effectively implement our strategies or achieve our business goals; |

• | exposure to interest rate and currency fluctuations; |

• | competitive pressures in the chemical distribution industry; |

• | consolidation of our competitors; |

• | our ability to implement and efficiently operate the systems needed to manage our operations; |

• | the risks associated with security threats, including cybersecurity threats; |

• | increases in transportation costs and changes in our relationship with third party carriers; |

3

• | the risks associated with hazardous materials and related activities; |

• | accidents, safety failures, environmental damage, product quality issues, major or systemic delivery failures involving our distribution network or the products we carry or adverse health effects or other harm related to the materials we blend, manage, handle, store, sell or transport; |

• | evolving laws and regulations relating to hydraulic fracturing and risks associated with chemicals used in hydraulic fracturing; |

• | losses due to potential product liability claims and recalls and asbestos claims; |

• | compliance with extensive environmental, health and safety laws, including laws relating to our environmental services businesses and the investigation and remediation of contamination, that could require material expenditures or changes in our operations; |

• | general regulatory and tax requirements; |

• | operational risks for which we may not be adequately insured; |

• | ongoing litigation and other legal and regulatory actions and risks, including asbestos claims; |

• | potential impairment of goodwill; |

• | inability to generate sufficient working capital; |

• | loss of key personnel; |

• | labor disruptions and other costs associated with the unionized portion of our workforce; |

• | negative developments affecting our pension plans and multi-employer pensions; |

• | the impact of labeling regulations; and |

• | our substantial indebtedness and the restrictions imposed by our debt instruments and indenture. |

All forward-looking statements made in this Annual Report on Form 10-K are qualified by these cautionary statements. These forward-looking statements are made only as of the date of this Annual Report on Form 10-K and we do not undertake any obligation, other than as may be required by law, to update or revise any forward-looking or cautionary statements to reflect changes in assumptions, the occurrence of events, unanticipated or otherwise and changes in future operating results over time or otherwise.

Comparisons of results between current and prior periods are not intended to express any future trends, or indications of future performance, unless expressed as such, and should only be viewed as historical data.

4

PART I

ITEM 1. BUSINESS

Our Company

We are a leading global chemical and ingredients distributor and provider of specialty services. We purchase chemicals from thousands of chemical producers worldwide and warehouse, repackage, blend, dilute, transport and sell those chemicals to more than 100,000 customer locations across approximately 150 countries. Our specialized services include digital promotion or e-marketing of chemicals for our producers, chemical waste removal, and on-site storage of chemicals for our customers, support services for the agricultural and pest control industries and environmental maintenance and response services. We derive competitive advantage from our scale, broad product offering, technical expertise, specialized services, long-standing relationships with leading chemical producers and our industry-leading safety record.

The global chemical distribution industry is large and fragmented with thousands of distributors but represents a relatively small portion of the total chemical industry. While the total chemical industry is projected to grow at rates about equal to the growth of the gross national product of countries we operate in around the world, the distributed chemicals portion of the market is projected to grow faster as producers and customers increasingly realize the benefits of outsourcing. Chemical producers rely on us to warehouse, repackage, transport and sell their products as a way to expand their market access, enhance their geographic reach, lower their costs and grow their business. Customers who purchase products and services from us benefit from a lower total cost of ownership, as they are able to simplify their chemical sourcing process and outsource functions to us such as just-in-time availability of the right product, packaging, mixing, blending and technical expertise. They also rely on us for safe delivery and off-loading of chemicals in a manner that is fully compliant with increasing local and federal regulations.

In the year ended December 31, 2016, we generated $8.1 billion in net sales, a net loss of $68.4 million and $562.7 million in Adjusted EBITDA. For a reconciliation of Adjusted EBITDA to net income (loss), see “Selected Financial Data” in Item 6 of this Annual Report on Form 10-K.

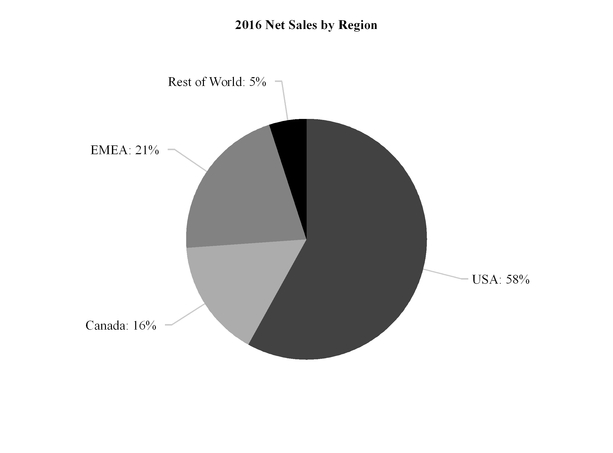

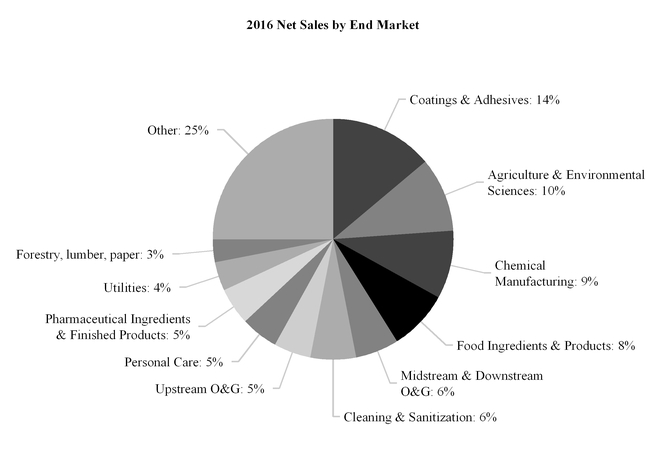

The following charts illustrate the geographical and end market diversity of our 2016 net sales:

5

We maintain strong, long-term relationships with our producers and our customers, many of which span multiple decades. We source materials from thousands of producers worldwide, including premier global leaders. For the year ended December 31, 2016, our 10 largest producers accounted for approximately 35 percent of our total chemical purchases and our 20 largest producers accounted for approximately 42 percent. Similarly, we sell products to thousands of customers globally, ranging from small and medium-sized businesses to large industrial customers. For the year ended December 31, 2016, our top 10 customers accounted for approximately 9 percent of our consolidated net sales and our top 20 customers accounted for 13 percent. Globally, we service our customers with on-time delivery rates greater than 96 percent.

Our Segments

Our business is organized and managed in four geographical segments: Univar USA (“USA”), Univar Canada (“Canada”), Univar Europe and the Middle East and Africa (“EMEA”), and Rest of World (“Rest of World”), which is predominantly in Latin America. For additional information on our geographical segments, see “Note 21: Segments” in Item 8 of this Annual Report on Form 10-K for additional information.

USA

We supply a broad offering of commodity and specialty chemicals, as well as specialized value-added services to a wide range of end markets, touching a majority of the manufacturing and industrial production sectors in the United States. Our close proximity to customers, combined with our deep product knowledge and end market expertise, serves as a competitive advantage.

In the United States, we service these multiple end markets with one-to-three day order lead times from nearby facilities. We repackage and blend bulk chemicals for shipment by our transportation fleet as well as common carriers. Our highly skilled salesforce is deployed by geographic sales district as well as by end-use market and industry, e.g., coatings & adhesives, food products and ingredients, pharmaceutical products and ingredients, water treatment, personal care, and energy.

Canada

Our Canadian operations are regionally focused, with a highly skilled salesforce supplying a broad offering of commodity and specialty chemicals to the local customer base. In Eastern Canada, we primarily focus on industrial markets such as food ingredients and products, pharmaceutical ingredients and finished products, coatings and adhesives, and chemical manufacturing.

6

We also service the cleaning and sanitation, personal care, mining, and oil and gas markets. In Western Canada, we focus on forestry, chemical manufacturing, mining, and oil and gas markets (e.g., midstream gas pipeline, oil sands processing and oil refining). Lastly, due to its size, we have dedicated resources and expertise serving the agriculture end market. In agriculture, we formulate and distribute crop protection and fertilizer products to independent retailers and specialty applicators servicing the agricultural end markets in both Western Canada and Eastern Canada and we provide support services to agricultural chemical producers throughout the country.

Europe, Middle East & Africa (EMEA)

We maintain a strong presence in the United Kingdom and Continental Europe with sales offices in 20 countries. We also have six sales offices in the Middle East and Africa.

We execute primarily on a pan-European basis, leveraging centralized or shared information technology systems, raw materials procurement, logistics, route operations and the management of producer relationships where possible to benefit from economies of scale and improve cost efficiency. We have strong end market expertise and key account management capability across Europe to better support sales representatives in each country and for serving our key customer end markets, namely pharmaceutical products and ingredients, food, coating and adhesives, and personal care.

Rest of World

We operate sales offices and distribution sites in Mexico, Brazil and to a lesser extent the Asia-Pacific region. We expanded our footprint in Latin America through strategic acquisitions, most recently through our 2014 acquisition of D’Altomare, a Brazilian distributor of specialty chemicals and ingredients.

Our Competitive Strengths

We derive strength and competitive advantage from our scale, broad product offering, high service level, long-standing relationships with producers, and our industry leading safety record.

Scale

We operate one of the most extensive chemical distribution networks in the world, comprised of more than 600 distribution facilities, approximately 90 million gallons of chemical storage tank capacity with hundreds of tractors, railcars, tankers and trailers operating daily through our facilities. We purchase thousands of different chemicals from thousands of producers in large quantities. Our purchasing power and global procurement relationships provide us with advantages over local and regional competitors due to economies of scale and our ability to manage our working capital.

Product breadth and market reach

We offer a wide range of chemical products and services across nearly all end-use markets. This enables us to present to customers a “one-stop shop” approach that simplifies their procurement process and lowers their total cost of ownership, and provides customers with the opportunity to achieve growth by accessing new end markets through us.

Service

Globally, we provide our customers with one-to-three day order lead times and greater than 96 percent on-time delivery from our nearby facilities. This highly responsive service level enables our customers to lower their inventory levels and avoid production interruptions from lack of chemical ingredients.

To complement our extensive product portfolio, we offer to our customers several specialized, value-added services, such as our unique distribution business focused on the marketing and sale of specialty and fine chemicals (ChemPoint.com), automated tank monitoring and refill of less than truckload quantities (MiniBulk), chemical waste management (ChemCare), technical support, and specialty product blending and formulation, particularly in agriculture. These services provide efficiency gains to our customers and deepen our relationship with them.

We also provide, through our highly skilled sales force, in-depth product technical knowledge and end market expertise to our customers, as well as valuable market and customer insights to our producers about how their products are performing in the market.

Long-standing producer and customer relationships

We have developed strong, long-term relationships, many spanning several decades, with the world's premier global chemical producers and distribute products to more than 100,000 customer locations around the globe, from small- and medium-sized businesses to global industrial customers. The strength of our relationships has provided opportunities for us to integrate our service

7

and logistics capabilities into our customers’ and producers’ business processes and to promote collaboration on supply chain optimization, marketing and other revenue enhancement strategies.

Safety and regulatory compliance

Our commitment to safety, strong safety record and compliance with federal, state and local environmental regulatory requirements is an increasingly important consideration for producers and customers when choosing a chemical distributor.

Our Growth Strategy

We believe that we are well positioned to drive profitability growth, increase our market share, and capitalize on industry outsourcing trends by focusing on our key initiatives of Commercial Greatness, Operational Excellence and One Univar.

Drive Profitable Growth

Commercial Greatness. We seek to increase the value we provide our customers and our producers by improving our customers’ experience and driving additional growth for our producers. We seek to:

• | continue to develop a highly skilled and well-equipped sales force utilizing a value-based consultative sales approach that is aligned to customer and end market needs by geography, product and service, and industry specialization; |

• | continue to increase our technical and industry-specific product and market expertise; |

• | develop a world-class marketing capability to dynamically identify and align resources with high-growth, high value opportunities; |

• | cultivate and maintain long-term producer relationships by bringing deep market and product knowledge, value-based selling, reducing complexity in producer distribution channels, and offering complementary products and services as a total solution for our customers; and |

• | strengthen our specialized service offerings such as ChemPoint.com, MiniBulk, and ChemCare by providing more growth for our producers and lower total cost of ownership for customers, while enhancing our profitability. We will also continue to work with customers and producers to develop tailored solutions to meet their specific requirements. |

Operational Excellence. We are committed to continuously improving our operating performance and lowering our costs per transaction. We seek to:

• | better align our USA business teams with identified growth opportunities in customer end markets, product markets, services, and industries in a way that narrows focus and increases accountability; |

• | increase our use of digital tools to simplify tasks, lower costs and improve customer experience; |

• | continue to use Lean Six Sigma methodologies to deliver project-by-project productivity gains; |

• | increase the cost efficiency of our warehouses, terminals, tank farms and logistics, and improve our net working capital efficiency; |

• | deliver a compelling customer value proposition by providing simplified sourcing, cost effective just-in-time delivery and managed inventory along with value-added services; and |

• | continue to build on our industry leading safety performance as a differentiator with both customers and producers. |

One Univar. We are committed to developing a healthy, high-performance culture through the selection, recognition and development of engaged employees. We aspire to build an environment where the best people want to work and add value for our customers, producers and shareholders. We will strengthen the overall governance and efficiency of our global business operations with integrated, disciplined operating processes and by leveraging best practices.

Expand our market share

We believe our Commercial Greatness and Operational Excellence initiatives will allow us to outperform competitors and obtain additional product authorizations from producers, leading to market share gains. We are also pursuing selective acquisitions to increase our presence in attractive end markets and whose products and service capabilities can benefit from our scale advantages.

Capitalize on industry outsourcing trends

We believe we are well positioned to benefit from the growing trend of chemical producers and customers to outsource key tasks to chemical distributors. As a leader in chemical distribution, we believe we can accelerate this trend by increasing the attractiveness of our total value proposition to both customers and our producers.

8

Through our Commercial Greatness, Operational Excellence and One Univar initiatives and by reinforcing “one-stop shop” provider capability, we will build on and increase the economic value we create in the global supply chain.

Company History

Our history dates back to 1924 when we were founded as a brokerage business. In 1986, we acquired McKesson Chemical Corporation, then the third largest US chemical distributor, solidifying our presence throughout the United States and making us the largest chemical distributor in North America. In 2001, we continued our expansion into Europe through the acquisition of Ellis & Everard, which specialized in the distribution of chemicals in the United Kingdom and Ireland and had additional facilities in Europe and the Eastern United States. In 2007, we acquired ChemCentral, which enabled us to improve our market share and operational efficiencies in North America.

In 2007, we were acquired by investment funds advised by CVC Capital Partners Advisory (US), Inc. (“CVC”) as well as investment funds associated with Goldman, Sachs & Co. and Parcom. On November 30, 2010, investment funds associated with Clayton, Dubilier & Rice, LLC (“CD&R”) acquired a 42.5 percent ownership interest in us. In December 2010, we acquired Basic Chemicals Solutions, a global distributor and trader of commodity chemicals, which further strengthened our ability to provide value in the supply chain between chemical producers and end-users and reinforced our global sourcing capabilities. In January 2011, we completed our acquisition of Quaron, a chemical distributor operating in Belgium and the Netherlands, which complemented our strong European foothold in specialty chemicals with expanded product portfolio and increased logistical capability. We continued our expansion into the emerging markets in 2011 through our acquisition of Eral-Protek, a leading chemical distributor in Turkey, and the acquisition of Arinos, a leading chemical distributor of specialty and commodity chemicals and high-value services in Brazil. In December 2012, we acquired Magnablend, whose specialty chemical and manufactured products broadened our oil and gas offerings. In May 2013, we expanded our Mexican presence with the acquisition of Quimicompuestos, making us a leading chemical distributor in the Mexican market, which is increasingly connected to the North American market. In November 2014, we acquired D’Altomare Quimica Ltda, or D’Altomare, a Brazilian distributor of specialty chemicals and ingredients, which expanded our geographic footprint and market presence in Brazil. On April 10, 2015, we acquired Key Chemical, Inc., or Key, one of the largest distributors of fluoride to municipalities in the United States, which we expect to help us expand our offerings into the municipal and other industrial markets.

On June 23, 2015, we closed our initial public offering (“IPO”) in which we issued and sold 20.0 million shares of common stock at a public offering price of $22.00 per share. In addition, we completed a concurrent private placement of $350.0 million for shares of common stock (17.6 million shares) to Dahlia Investments Pte. Ltd., an indirect wholly owned subsidiary of Temasek Holdings (Private) Limited (“Temasek”). We received total net proceeds of approximately $760.0 million from the IPO and the private placement after deducting underwriting discounts and commissions and other offering expenses of approximately $30.0 million. These expenses were recorded against the proceeds received from the IPO. Certain selling stockholders sold an additional 25.3 million shares of common stock in the IPO and concurrent private placement. We did not receive any proceeds from the sale of these shares.

In July 2015, we acquired the assets of Chemical Associates, Inc., a marketer, manufacturer, and distributor of oleochemicals, many of which are based on renewable and sustainable resources, which we believe will help increase the value Univar can bring in a number of our key markets such as personal care, food, cleaning and sanitization, lubricants, and coatings and adhesives. On October 2, 2015, we entered into the agrochemical formulation market and expanded our capabilities in the third-party agriculture logistics market in Canada with the acquisition of the Future Group. On November 3, 2015, we acquired Arrow Chemical, Inc., expanding our existing offering with a complementary portfolio of active pharmaceutical ingredients (“APIs”) and other specialty ingredients essential to the formulation of generic and over-the-counter pharmaceuticals. On December 1, 2015, we acquired Weaver Town Oil Services, Inc., and Weavertown Transport Leasing, Inc., operating as the Weavertown Environmental Group, or WEG, which strengthens our ChemCareSM waste management service offering with a broad range of complementary services, including industrial cleaning, waste management and transportation, site remediation, and 24/7 emergency response services. On December 17, 2015, we acquired Polymer Technologies Ltd., a U.K.-based developer and distributor of unique ultraviolet/electron beam curable chemistries used to formulate environmentally responsible paints, inks, and adhesives.

In March 2016, we acquired Bodine Services of the Midwest, further strengthening our ChemCareSM waste management, environmental maintenance and response service offering in key geographic markets. That same month, we acquired the assets of Nexus Ag Business, Inc., enhancing our existing macronutrient and crop protection inputs through a proprietary line of micronutrients, macronutrients and specialty fertilizers. Together with our leading distribution and services network in the region, this acquisition further strengthens our agriculture group’s ability to provide customers in Canada with a complete product service offering that covers the entire growing cycle from start to finish.

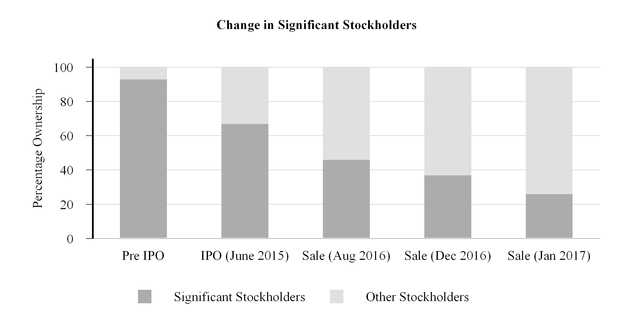

Also in 2016 and 2017, we engaged in a series of secondary registrations of our stock. As a result, CVC divested its remaining ownership in our company and both CD&R and Temasek reduced their ownership stakes in our company to 15.4% and 10.1%, respectively.

9

The below chart illustrates the change in our Significant Stockholders since the IPO date.

Products and End Markets

The main focus of our marketing approach is to identify attractive end-user markets and provide customers in those markets all of their commodity and specialty chemical needs. We also offer value-added services as well as procurement solutions that leverage our chemical, supply chain and logistics expertise, networked inventory sourcing and producer relationships. We provide our customers with a “one-stop shop” for their commodity and specialty chemical needs and offer a reliable and stable source of quality products and services.

We buy and inventory chemicals in large quantities such as barge loads, railcars or full truck loads from chemical producers and we sell and distribute smaller quantities to our customers. Approximately 40 percent of the chemicals we purchase are in bulk form, and we repackage them into various size containers for sale and distribution.

Commodity chemicals currently represent and have historically represented the largest portion of our business by sales and volume. Our commodity chemicals portfolio includes acids and bases, surfactants, glycols, inorganic compounds, alcohols and general chemicals used extensively throughout most end markets. Our specialty chemicals sales represent an important, high-value, higher-growth portion of the chemical distribution market. We typically sell specialty chemicals in lower volumes but at a higher profit than commodity chemicals. While many chemical producers supply these products directly to customers, there is an increasing trend toward outsourcing the distribution of these specialized, lower volume products. We believe that customers and producers value Univar’s ability to supply both commodity and specialty products, particularly as the markets continue to consolidate.

We focus on sourcing certain high volume products that we distribute to our customers. We buy products globally at attractive pricing. We largely sell chemicals sourced through our industry focused salesforce. However, a small proportion of the chemicals that we source are sold directly to certain high volume customers through our Basic Chemicals group. Our global sourcing capabilities help us enhance our global market presence and our product expertise across all market segments.

We serve a diverse set of end markets and regions, with no end market accounting for more than 20 percent of our net sales over the past year.

Our key global end markets include:

• | Agricultural and Environmental Sciences. We are a leading wholesale distributor of crop protection products to independent retailers and specialty applicators in Canada. To support this end market, we distribute herbicides, fungicides, insecticides, seed, micronutrients, macronutrients, horticultural products, fertilizers and feed, among other products. In addition, we provide storage, packaging and logistics services for major crop protection companies, storing chemicals, feed-grade materials, seed and equipment. We supply pest control products and equipment to the public health, vegetation management, turf and ornamental, food processing and post-harvest storage, animal health |

10

and hay production markets. We operate a network of over 70 Univar ProCenter distribution centers in North America to serve this end market.

• | Chemical Manufacturing. We distribute a full suite of chemical products in support of the chemical manufacturing industry (organic, inorganic, polymer chemistries and to a lesser extent oil refining). Our broad warehousing and delivery resources permit us to assure our chemical manufacturing customers efficient inventory management, just-in-time delivery, and custom blends and packages. Our industry expertise also assists our customers in making product selections which best suit the customers' objectives and with chemical waste and wastewater issues. |

• | Cleaning and Sanitization. The cleaning and sanitization industry is made up of thousands of large and small formulators that require a multitude of chemical ingredients to make cleaning products and detergents for home and industrial use. We believe that we distribute chemicals manufactured by many of the industry’s leading producers of enzymes, surfactants, solvents, dispersants, thickeners, bleaching aides, builders, sealants, acids, alkalis and other chemicals that are used as processing aids in the manufacturing of cleaning products. |

• | Coatings and Adhesives. The coatings and adhesives industry is one of our largest customer end markets. We sell resins, pigments, solvents, thickeners, dispersants and other additives used to make paints, inks, and coatings. We have a large team of industry and product specialists with the market expertise that enables us to work closely with formulators and producers to offer new technologies, formulations and scale-up support. Our product line includes epoxy resins, polyurethanes, titanium dioxide, fumed silica, esters, plasticizers, silicones and specialty amines. |

• | Food Ingredients and Products. For the food and beverage industry, we distribute a diverse portfolio of commodity and specialty products that are sold as processing aids or food additives. We sell food ingredients such as thickeners, emulsifiers, sweeteners, preservatives, leavening agents and humectants, as well as texturizer and fat replacement products that include xanthan gum, locust bean gum, cellulosics and guar gum. We distribute acidulants such as citric acid, lactic acid and malic acid, as well as alkalis. Additional offerings include supplements and products such as proteins, vitamins and minerals. The major food and beverage markets we serve are meat processing, baked goods, dairy, grain mill products, processed foods, carbonated soft drinks, fruit drinks and alcoholic beverages. We manage our product portfolio to ensure quality standards, security of supply and cost competitiveness. We refresh our product offering with products that meet the key trends impacting the food industry. Our industry experts have developed marketing tools that simplify the ingredient selection process for our customers and provide product performance information and solutions. |

• | Energy. We provide chemicals and service to midstream pipeline and downstream refinery operators primarily in the US and Canada. We offer an expansive product line with a team of highly skilled and uniquely dedicated specialists to stay on top of the latest trends, regulations and technologies. We also service the upstream oil and gas production market, including the US shale hydraulic fracturing sector, by providing a variety of bulk chemicals to the drill sites and also specialty blended products used to fracture rock and stimulate oil and gas production from the well. Other markets include Canada, Mexico, Europe’s North Sea and parts of Africa. In recent years, the number of operating hydraulic fracturing rigs in the US dropped significantly with the fall in oil prices, as has the size of this end market for us. |

• | Personal Care. We are a full-line distributor in the personal care industry providing a wide variety of specialty and basic chemicals used in skin care products, shampoos, conditioners, styling, hair color, body washes, sun care, color cosmetics, and pet care products. The chemicals that we distribute include surfactants, emollients, emulsifiers, rheology modifiers, active ingredients, color, preservatives and processing aids. Our dedicated team of industry experts and technical marketers work with our customers to formulate traditional and cutting-edge personal care products. |

• | Pharmaceutical Ingredients and Finished Products. We are uniquely positioned in the pharmaceutical ingredients industry due to the combination of our product portfolio, logistics footprint and customized solutions to meet the needs of a highly regulated industry. We represent some of the world’s leading excipient, process, solvent and active pharmaceutical ingredient producers, as well as producers of chemicals used to support water treatment, filtering and purification systems, thus offering our customers a broad product offering in the pharmaceutical industry. We sell active ingredients such as aspirin, ascorbic acid, caffeine and ibuprofen, and excipients that include phosphates, polyethylene glycols, polysorbates, methylcellulose, stearyl alcohol and stearates. We also make and sell certain finished pharmaceutical products. |

In some geographic regions we target other markets in addition to the end-user markets described above. Our water treatment products and services are utilized by customers in many of our end markets, and the municipal markets, and we believe that this will continue to be a growth area for our business.

11

Services

In addition to selling and distributing chemicals, we use our transportation and warehousing infrastructure and broad knowledge of chemicals and hazardous materials handling to provide important distribution and value-added services for producers and our customers. This intermediary role is increasingly important, in particular due to the recent trend of increased outsourcing of distribution by chemical producers to satisfy their need for supply chain efficiency. These services include:

Distribution Services

• | Inventory management. We manage our inventory in order to meet customer demands on short notice whenever possible. Our key role in the supply chain to chemical producers also enables us to obtain access to chemicals in times of short supply, when smaller chemical distributors may not able to obtain or maintain stock. Further, our global distribution network permits us to stock products locally to enhance “just-in-time” delivery, providing outsourced inventory management to our customers in a variety of end markets. |

• | Product knowledge and technical expertise. We partner with our customers in their production processes. For example, we employ a team of food technologists and chemicals and petroleum engineers who have the technical expertise to assist in the formulation of chemicals to meet specific customer performance requirements as well as provide customers with after-market support and consultation. |

• | Mixing, blending and repackaging. We provide our customers with a full suite of blending and repackaging services for our customers and in the agriculture industry for producers. Additionally, we can fulfill small orders through our repackaging services, enabling customers to maintain smaller inventories. |

Value-Added Services

• | MiniBulk and Remote Monitoring. MiniBulk is a complete storage and delivery system that improves plant safety and productivity. MiniBulk is a safe and efficient handling and use system for customers receiving less than full truckload quantities of chemicals. Our trained specialists deliver products that minimize employee exposure to hazardous chemicals. In addition drum storage and disposal are eliminated and access to products is improved. Similarly, our remote telemetry systems permit around-the-clock access to inventory information. The result is better inventory management, elimination of manual measurement and better assurance of timely/automatic replenishment. |

• | Specialized Blending. Leveraging our technical expertise, we are able to utilize our blending and mixing capabilities to create specialty chemical formulations to meet specific customer performance demands for agriculture and oil and gas products through our Future Group and Magnablend blending services. |

• | ChemCare and Environmental Response Services. Our ChemCare waste management service collects both hazardous and non-hazardous waste products at customer locations in the United States and Canada, and then works with select vendors in the waste disposal business to safely transport these materials to licensed third party treatment, storage and disposal facilities. ChemCare reviews each waste profile, recommends disposal alternatives to the customer and offers transportation of the waste to the appropriate waste disposal company. Hazardous and non-hazardous waste management technologies provided from our approved treatment storage and disposal facility vendors include recycling, incineration, fuels blending, lab packing, landfill, deep well injection and waste-to-energy. We have also expanded our environmental services capabilities through our recent acquisitions of Bodine and Weavertown Environmental Group. Among other things, we are able to provide our customers with industrial cleaning, site remediation and emergency environmental response services. |

• | ChemPoint. ChemPoint is our unique distribution business that facilitates the marketing and sales of specialty and fine chemicals, operating principally in North America and EMEA. ChemPoint is primarily focused on connecting producers to customers on relatively small volumes of high-value and highly-specialized chemicals. We offer an integrated, digital marketing and sales process that is powered by leading-edge technologies. |

Producers

We source chemicals from many of the premier global chemical manufacturers. Among our largest producers worldwide are the world’s largest general chemical and petrochemical producers, with many of the relationships with these producers having been in place for decades. We typically maintain relationships with multiple producers of commodity chemicals to protect against disruption in supply and distribution logistics as well as to maintain pricing discipline in our supply. Maintaining strong relationships with producers is important to our overall success. Our scale, geographic reach, diversified distribution channels and industry expertise enable us to develop strong, long-term relationships with producers, allowing us to integrate our service and logistics capabilities into their business processes, promoting collaboration on supply chain optimization, marketing and other revenue

12

enhancement strategies. The producers we work with also benefit from the insight we provide into customer buying patterns and trends. More and more, chemical producers are depending on the sales forces and infrastructure of large chemical distributors to efficiently market, warehouse and deliver their chemicals to end users.

Our base of thousands of chemical producers is highly diversified, with our largest producer representing approximately 12% of our 2016 chemicals expenditures, and no other chemical producer accounting for more than 10% of the total. Our 10 largest producers accounted for approximately 35% of our total chemical purchases in 2016. Our 20 largest producers accounted for approximately 42% of our total chemical purchases in 2016.

We typically purchase our chemicals through purchase orders rather than long-term contracts, although we have exclusive supply arrangements for certain chemicals. We normally enter into framework supply contracts with key producers. These framework agreements generally operate on an annual basis either with pricing items fixed to an index or without fixed pricing terms, although they often include financial incentives if we meet or exceed specified purchase volumes. We also have a limited number of longer term agreements with certain producers of commodity chemicals. For all of these chemicals, once we purchase the products, we ship them either directly to a customer or, more commonly, to one of our distribution centers.

Our ability to earn volume-based incentives from producers is an important factor in achieving our financial results. We receive these volume-based incentives in the form of rebates that are payable only when our sales equal or exceed the relevant target. In order to record these incentives throughout the year, we estimate the amount of incentives we expect to receive in order to properly record our cost of sales during the period. Because our right to receive these incentives will depend on our purchases for the entire year, our accounting estimates depend on our ability to forecast our annual purchases accurately which ultimately will vary depending on our customers’ demand and consumption patterns which may be independent of our performance as a distributor.

Sales and Marketing

We organize our business to align with our customers and end markets needs by geography, product and service, and industry specialization, including high-focus industries such as coatings and adhesives, food products and ingredients, pharmaceutical products and ingredients, personal care, agricultural and environmental sciences, energy and water treatment. We train our sales personnel so that they develop expertise in the industries that they serve. Our sales force leverages our strong producer relationships to provide superior product insight and expertise to deliver critical-use specialty, organic and inorganic chemicals to customers. We believe that aligning our business to customer and end markets enables our sales force and supply chain to deliver more valuable market insights to both our customers and producers.

Distribution Channels

We continue to refine our distribution business model to provide producers and our customers with the highest level of service, reliability and timeliness of deliveries while offering cost competitive products. We have multiple channels to market, including warehouse delivery, and direct-to-consumer delivery. The principal determinants of the way a customer is serviced include the size, scale and level of customization of a particular order, the nature of the product and the customer, and the location of the product inventories. For the year ended December 31, 2016, warehouse distribution accounted for approximately 80% of our net sales while direct distribution accounted for approximately 17% of our net sales, with the remaining approximate 3% of net sales derived primarily from our waste management services.

Warehouse Distribution

Our warehouse distribution business is the core of our operations. In our warehouse business, we purchase chemicals in truck load or larger quantities from chemical producers based on contracted demands of our customers or our estimates of anticipated customer purchases. Once received, chemicals are stored in one or more of our distribution facilities, depending on customer location, for sale and distribution in smaller, less-than-truckload quantities to our customers. Our warehouses have various facilities for services such as repackaging, blending and mixing to create specialized chemical solutions needed by our customers in ready-to-use formulations.

Our warehouse business connects large chemical producers with smaller volume customers whose consumption patterns tend to make them uneconomical to be served directly by producers. Thus, the core customer for our warehouse business model is a small or medium volume consumer of commodity and specialty chemicals. Since chemicals comprise only a fraction of the input costs for many of our customers’ products, our warehouse customers typically value quality, reliability of supply and ease of service. Our breadth of chemical product offerings also allows us to provide customers with complete management solutions for their chemical needs as they are able to obtain small volumes of many different products from us more efficiently and economically than if they dealt directly with multiple chemical producers. Our network of warehouses allows us to service most customers from multiple locations and also enables us to move products efficiently and economically throughout our own warehouse system to service customers on a real-time basis. Further, by leveraging our geographic footprint and state-of-the-art logistics

13

platform, we are able to combine multiple customer orders along the same distribution routes to reduce delivery costs and facilitate customer inventory management. For example, we combine multiple less-than-truckload deliveries for different customers along the same route to better utilize our delivery assets while at the same time minimizing our customers’ inventories.

With the leading market position in North America, our operations are capable of serving customers throughout the United States, including Hawaii and Alaska, and all major provinces and major manufacturing centers within Canada including remote areas such as the oil sands regions of Northern Canada. Our close proximity to major transportation arteries allows us to service customers in the most remote locations throughout the United States, particularly those markets that chemical producers are not able to serve profitably. In the USA, we rely mainly on our own fleet of distribution vehicles, while we primarily use third parties for the transportation of chemicals in Canada, EMEA and Rest of World.

Direct Distribution

Our direct distribution business provides point-to-point logistics for full truckloads or larger quantities of chemicals between producers and customers. In direct distribution, we sell and service large quantity purchases that are shipped directly from producers through our logistics infrastructure, which provides customers with sourcing and logistics support services for inventory management and delivery, in many cases far more economically than the producer might provide. We believe that producers view us not as competitors, but as providers of a valuable service, brokering these large orders through the utilization of our broad distribution network. We typically do not maintain inventory for direct distribution, but rather use our existing producer relationships and marketing expertise, ordering and logistics infrastructure to serve this demand, resulting in limited working capital investment for these sales. Our direct distribution service is valuable to major chemical producers as it allows them to deliver larger orders to customers utilizing our existing ordering, delivery and payment systems.

Insurance

The nature of our business exposes us to the possible risk of liabilities arising out of our operations, including damages to the environment, property, employees or the general public. Although we focus on operating safely and prudently, we occasionally receive claims, alleging damages, negligence or other wrongdoing in the planning or performance of work, which resulted in harm to the environment, property, employees or the general public. These liabilities can be significant. Accruals for deductibles are based on claims and actuarial estimates of claims development and claims incurred but not recorded.

We maintain policies of insurance that, subject to limitations, exclusions, or deductibles, provide coverage for these types of claims for our worldwide facilities and activities. To mitigate its aggregate loss potential above these retentions and deductibles, the company purchases insurance coverage from highly rated insurance companies. The company does not currently operate or participate in any captive insurance companies or other non-traditional risk transfer alternatives.

In the normal course of business, we also purchase surety bonds or letters of credit in connection with municipal contracts, import and export activities, environmental remediation, and environmental permits as a financial guarantee of our performance.

Competition

The chemical production, distribution and sales markets are highly competitive. Most of the products that we distribute are made to industry standard specifications and are either produced by, or available from, multiple sources or the producers with which we work may also sell their products through a direct sales force or through multiple chemical distributors.

Chemical distribution itself is a fragmented market in which only a small number of competitors have substantial international operations. Our principal large international competitor is Brenntag, which has a particularly strong position in Europe.

Many other chemical distributors operate on a regional, national or local basis and may have a strong relationship with local producers and customers that may give them a competitive advantage in their local market. Some of our competitors are either local or regional distributors with a broad product portfolio, while others are niche players which focus on a specific end market, either industry or product-based.

Chemical producers may also choose to limit their use of third party distributors, particularly with respect to higher margin products, or to partner with other chemical producers for distribution, each of which could increase competition.

We compete on the basis of price, diversification and flexibility in product offerings and supply availability, market insight and the ability to provide value-added services.

North America

The independent chemical distribution market in North America is fragmented. Our principal competitors in North America include Brenntag, Helm America, Hydrite Chemical, Prinova and Nexeo Solutions. We also compete with a number of smaller companies in certain niche markets.

14

EMEA

The independent chemical distribution market in Europe historically has been highly fragmented. Consolidation among chemical distributors has increased, mirroring developments within the chemical sector as a whole.

Brenntag is our leading competitor in Europe due to its strong market position in Germany, which is the largest European chemical distribution market. Other regional competitors in Europe include Azelis, Helm and IMCD. We believe that we are the leading chemical distributor in the United Kingdom and Ireland.

Rest of World

In Rest of World, the markets for chemical distribution are much more fragmented and credible competitive information for smaller companies is not available. Our relative competitive position in the Rest of World markets is smaller than in North America or EMEA.

Regulatory Matters

Our business is subject to a wide range of regulatory requirements in the jurisdictions in which we operate. Among other things, these laws and regulations relate to environmental protection, economic sanctions, product regulation, anti-terrorism concerns, management, storage, transport and disposal of hazardous chemicals and other dangerous goods, and occupational health and safety issues. Changes in and introductions of regulations have in the past caused us to devote significant management and capital resources to compliance programs and measures. New laws, regulations, or changing interpretations of existing laws or regulations, or a failure to comply with current laws, regulations or interpretations, may have a material adverse effect on our business, financial condition and results of operations. The following summary illustrates some of the significant regulatory and legal requirements applicable to our business.

Environmental, Health and Safety Matters

We operate in a number of jurisdictions and are subject to various foreign, federal, state and local laws and regulations related to the protection of the environment, human health and safety, including laws regulating discharges of hazardous substances into the soil, air and water, blending, managing, handling, storing, selling, transporting and disposing of hazardous substances, investigation and remediation of contaminated properties and protecting the safety of our employees and others. Some of our operations are required to hold environmental permits and licenses and certain of our services businesses are also impacted by these laws. The cost of complying with these environmental, health and safety laws, permits and licenses has, in some instances, been substantial.

Some of our historic operations, including those of companies we acquired, have resulted in contamination at a number of currently and formerly owned or operated sites. We are required to investigate and remediate at many of such sites. Contamination at these sites generally resulted from releases of chemicals and other hazardous substances. We have spent substantial sums on such investigation and remediation and expect to continue to incur such expenditures, or discover additional sites in need of investigation and remediation, until such investigation and remediation is deemed complete. Information on our environmental reserves is included in “Note 19: Commitments and contingencies” to our consolidated financial statements for the year ended December 31, 2016 which are included in Item 8 of this Annual Report on Form 10-K.

CERCLA. The US Comprehensive Environmental Response, Compensation, and Liability Act, or CERCLA, also known as Superfund, as well as similar laws in other jurisdictions, governs the remediation of contaminated sites and establishes liability for the release of hazardous substances at such sites. A party that transported waste, or arranged for the shipment of waste, to a waste disposal facility or other third party site that requires remediation can be liable for the cost of cleanup regardless of fault, the lawfulness of the disposal or the actions of other parties. Under CERCLA, the EPA or a delegated state agency can oversee or require remediation of such sites and seek cost recovery from any party whose wastes were disposed at, or who otherwise contributed to the contamination of, such sites. We are party to consent agreements with the EPA and state regulatory authorities with respect to environmental remediation at a number of such sites. We may be identified as a Potentially Responsible Party at additional third party sites or waste disposal facilities.

RCRA. The EPA regulates the generation, transport, treatment, storage and disposal of hazardous waste under the US Resource Conservation and Recovery Act, or RCRA. RCRA also sets forth a framework for managing non-hazardous waste. Most owners and operators of hazardous waste treatment, storage and disposal facilities must obtain a RCRA permit. RCRA also mandates certain operating, recordkeeping and reporting obligations for owners and operators of hazardous waste facilities. Our facilities generate various hazardous and non-hazardous wastes and we are a hazardous waste transporter and temporary storage facility. As a result of such activities, we are required to comply with RCRA requirements, including the maintenance of financial resources and security to address forced closures or accidental releases.

Clean Air Act. The US Clean Air Act and similar laws in other jurisdictions establish a variety of air pollution control measures, including limits for a number of airborne pollutants. These laws also establish controls for emissions from automobiles

15

and trucks, regulate hazardous air pollutants emitted from industrial sources and address the production of substances that deplete stratospheric ozone. Under the Clean Air Act, we are required to obtain permits for, and report on emissions of, certain air pollutants, or qualify for and maintain records substantiating that we qualify for an exemption. Owners and operators of facilities that handle certain quantities of flammable and toxic substances must implement and regularly update detailed risk management plans filed with and approved by the EPA. Failure to comply with the Clean Air Act may subject us to fines, penalties and other governmental and private actions.

Clean Water Act. Many of the jurisdictions in which we operate regulate water quality and contamination of water. In the United States, the EPA regulates discharges of pollutants into US waters, sets wastewater standards for industry and establishes water quality standards for surface waters, such as streams, rivers and lakes, under the US Clean Water Act. The discharge of any regulated pollutant from point sources (such as pipes and manmade ditches) into navigable waters requires a permit from the EPA or a delegated state agency. Several of our facilities have obtained permits for discharges of treated process wastewater directly to surface waters. In addition, several of our facilities discharge to municipal wastewater treatment facilities and therefore are required to obtain pretreatment discharge permits from local agencies. A number of our facilities also have storm water discharge permits.

Oil Pollution Prevention Regulations. The Oil Pollution Prevention regulations promulgated by the EPA under the authority of the Clean Water Act require that facilities storing oil in excess of threshold quantities or which have the ability to reach navigable water have a spill prevention, control and countermeasure, or SPCC, plan. Many of our facilities have SPCC plans or similar oil storage plans required in non-US jurisdictions.

Storage Requirements. Our warehouse facilities are required to comply with applicable permits and zoning requirements from local regulatory authorities and pursuant to leases. These requirements, which differ based on type of facility and location, define structural specifications and establish limits on building usage. Regulators typically have the authority to address non-compliance with storage requirements through fines, penalties and other administrative sanctions.

EPCRA. The US Emergency Planning and Community Right-To-Know Act, or EPCRA, establishes reporting rules for facilities that store or manage chemicals and requires such facilities to maintain certain safety data. EPCRA is intended to facilitate state and local planning for chemical emergencies. EPCRA requires state and local emergency planning and emergency response authorities to be informed of the presence of specified quantities of “extremely hazardous substances” at a facility and the release of listed hazardous substances above threshold quantities. Facilities that store or use significant amounts of toxic chemicals must also submit annual toxic chemical release reports containing information about the types and amounts of toxic chemicals that are released into the air, water and soil, as well as information on the quantities of toxic chemicals sent to other facilities. We store and handle a number of chemicals subject to EPCRA reporting and recordkeeping requirements.

TSCA and the Lautenberg Act. The US Toxic Substances Control Act, the recently enacted Lautenberg Act (collectively TSCA) and similar laws in other jurisdictions, are intended to ensure that chemicals do not pose unreasonable risks to human health or the environment. TSCA requires the EPA to maintain the TSCA registry listing chemicals manufactured or processed in the United States. Chemicals not listed on the TSCA registry cannot be imported into or sold in the United States until registered with the EPA. TSCA also sets forth specific reporting, recordkeeping and testing rules for chemicals, including requirements for the import and export of certain chemicals, as well as other restrictions relevant to our business. Pursuant to these laws, the EPA from time to time issues Significant New Use Rules, or SNURs, when it identifies new uses of chemicals that could pose risks to human health or the environment and also requires pre-manufacture notification of new chemical substances that do not appear on the TSCA registry. When we import chemicals into the United States, we must ensure that chemicals appear on the TSCA registry prior to import, participate in the SNUR process when a chemical we import requires testing data and report to the EPA information relating to quantities, identities and uses of imported chemicals.

FIFRA and Other Pesticide and Biocide Regulations. We have a significant operation in the distribution and sale of pesticides and biocides. These products are regulated in many jurisdictions. In the United States, the Federal Insecticide, Fungicide, and Rodenticide Act, or FIFRA, authorizes the EPA to oversee and regulate the manufacture, distribution, sale and use of pesticides and biocides. We are required to register with the EPA and certain state regulatory authorities as a seller and repackager of pesticides and biocides. The EPA may cancel registration of any pesticide or biocide that does not comply with FIFRA, effectively prohibiting the manufacture, sale, distribution or use of such product in the United States.

The EPA has established procedures and standards for the design of pesticide and biocide containers, as well as the removal of pesticides and biocides from such containers prior to disposal. Applicable regulations also prescribe specific labeling requirements and establish standards to prevent leaks and spills of pesticides and biocides from containment structures at bulk storage sites and dispensing operations. These standards apply to dealers who repackage pesticides, commercial applicators and custom blenders.

REACH. In Europe, our business is affected by legislation dealing with the Registration, Evaluation, Authorization and Restriction of Chemicals, or REACH. REACH requires manufacturers and importers of chemical substances to register such substances with the European Chemicals Agency, or the ECHA, and enables European and national authorities to track such

16

substances. Depending on the amount of chemical substances to be manufactured or imported, and the specific risks of each substance, REACH requires different sets of data to be included in the registration submitted to the ECHA. Registration of substances with the ECHA imposes significant recordkeeping requirements that can result in significant financial obligations for chemical distributors, such as us, to import products into Europe. REACH is accompanied by legislation regulating the classification, labeling and packaging of chemical substances and mixtures.

GHG Emissions. In the US, various legislative and regulatory measures to address greenhouse gas, or GHG, emissions are in various phases of discussion or implementation. At the federal legislative level, Congress has previously considered legislation requiring a mandatory reduction of GHG emissions. Although Congressional passage of such legislation does not appear likely at this time, it could be adopted at a future date. It is also possible that Congress may pass alternative climate change bills that do not mandate a nationwide cap-and-trade program and instead focus on promoting renewable energy and energy efficiency. In the absence of congressional legislation curbing GHG emissions, the EPA is moving ahead administratively under its Clean Air Act authority.

The implementation of additional EPA regulations and/or the passage of federal or state climate change legislation will likely result in increased costs to operate and maintain our facilities. Increased costs associated with compliance with any future legislation or regulation of GHG emissions, if it occurs, may have a material adverse effect on our results of operations, financial condition and ability to make cash distributions.

Internationally, many of the countries in which we do business (but not the US) have ratified the Kyoto Protocol to the United Nations Framework Convention on Climate Change, or the Kyoto Protocol, and we have been subject to its requirements, particularly in the European Union. Many nations entered into the Copenhagen Accord, which may result in a new international climate change treaty in the future. If so, we may become subject to different and more restrictive regulation on climate change to the extent the countries in which we do business implement such a new treaty.

OSHA. We are subject to workplace safety laws in many jurisdictions, including the United States. The US Occupational Safety and Health Act, or OSHA, which addresses safety and health in workplace environments and establishes maximum workplace chemical exposure levels for indoor air quality. Chemical manufacturers and importers must employ a hazard communication program utilizing labels and other forms of warnings, as well as Material Safety Data Sheets, setting forth safety and hazardous materials information to employees and customers. Employers must provide training to ensure that relevant employees are equipped to properly handle chemicals.

We train employees and visitors who have access to chemical handling areas. OSHA requires the use of personal protective equipment when other controls are not feasible or effective in reducing the risk of exposure to serious workplace injuries or illnesses resulting from contact with hazardous substances or other workplace hazards. Employers must conduct workplace assessments to determine what hazards require personal protective equipment, and must provide appropriate equipment to workers.

OSHA operates a process safety management rule, or PSM Rule, that requires employers to compile written process safety information, operating procedures and facility management plans, conduct hazard analyses, develop written action plans for employee participation in safety management and certify every three years that they have evaluated their compliance with process safety requirements. Employees must have access to safety analyses and related information, and employers must maintain and provide process-specific training to relevant employees. We handle several chemicals that are hazardous and listed under the PSM Rule, which imposes extensive obligations on our handling of these chemicals and results in significant costs on our operations.

OSHA’s Hazardous Waste Operations and Emergency Response rules require employers and employees to comply with certain safety standards when conducting operations involving the exposure or potential exposure to hazardous substances and wastes. These standards require hazardous substances preparedness training for employees and generally apply to individuals engaged in cleanup operations, facility operations entailing the treatment, storage and disposal of hazardous wastes, and emergency responses to uncontrolled releases of hazardous substances.

OSHA regulations require employers to develop and maintain an emergency action plan to direct employer and employee actions in the event of a workplace emergency. Under most circumstances, the plan must be maintained in writing, remain accessible at the workplace and be made available to employees for review.

Chemical Facility Anti-Terrorism Standards. The US Department of Homeland Security, or DHS, regulates certain high-risk chemical facilities through its Chemical Facility Anti-Terrorism Standards. These standards establish a Chemical Security Assessment Tool comprised of four elements, including facility user registration, top-screen evaluation, security vulnerability assessment and site security planning. The site security plan must address any vulnerabilities identified in the security vulnerability assessment, including access control, personnel credentialing, recordkeeping, employee training, emergency response, testing of security equipment, reporting of security incidents and suspicious activity, and deterring, detecting and delaying potential attacks. DHS must approve all security vulnerability assessments and site security plans. We handle a number of chemicals regulated by DHS.

17

FDA. The U.S. Food & Drug Administration (FDA) Food Safety Modernization Act, or FSMA, directs FDA to build an integrated national food safety system in partnership with state and local authorities. Univar facilities that handle FDA regulated products are required to implement a written preventive controls plan. This involves evaluating the hazards that could affect food safety and specifying what preventive steps, or controls, will be put in place to significantly minimize or prevent the hazards. Also, when we import FDA regulated products into the United States, we have an explicit responsibility to verify that our foreign suppliers have adequate preventive controls in place. Finally, the rule establishes requirements for companies involved in transporting FDA regulated products to use sanitary practices to ensure the safety of those products.

Other Regulations

We are subject to other foreign, federal, state and local regulations. For example, many of the products we repackage, blend and distribute are subject to Food and Drug Administration regulations governing the handling of chemicals used in food, food processing or pharmaceutical applications. Compliance with these regulations requires testing, additional policies, procedures and documentation and segregation of products. In addition, we are subject to a variety of state and local regulations, including those relating to the fire protection standards, and local licensing and permitting of various aspects of our operations and facilities.

Legal Proceedings

In the ordinary course of our business, we are subject to periodic lawsuits, investigations and claims. Although we cannot predict with certainty the ultimate resolution of pending or future lawsuits, investigations and claims asserted against us, we do not believe that any currently pending legal proceeding to which we are a party is likely to have a material adverse effect on our business, results of operations, cash flows or financial condition. See “Note 19: Commitments and Contingencies” in Item 8 of this Annual Report on Form 10-K for additional information.

Asbestos Claims

In its 1986 purchase of McKesson Chemical Company from McKesson Corporation, or McKesson, our wholly owned subsidiary, Univar USA Inc., entered into an indemnification agreement with McKesson. Univar USA has an obligation to defend and indemnify McKesson for claims alleging injury from exposure to asbestos-containing products sold by McKesson Chemical Company, or the asbestos claims. Univar USA’s obligation to indemnify McKesson for settlements and judgments arising from asbestos claims is the amount which is in excess of applicable insurance coverage, if any, which may be available under McKesson’s historical insurance coverage. In addition, we are currently defending a small number of claims which name Univar USA as a defendant.