Attached files

| file | filename |

|---|---|

| EX-10.15 - EXHIBIT 10.15 - DIRECTOR COMPENSATION POLICY - NxStage Medical, Inc. | nxtm20161231ex1015bodcomp.htm |

| EX-32.2 - EXHIBIT 32.2 - CERTIFICATION - NxStage Medical, Inc. | nxtm20161231ex322.htm |

| EX-32.1 - EXHIBIT 32.1 - CERTIFICATION - NxStage Medical, Inc. | nxtm20161231ex321.htm |

| EX-31.2 - EXHIBIT 31.2 - CERTIFICATION - NxStage Medical, Inc. | nxtm20161231ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - CERTIFICATION - NxStage Medical, Inc. | nxtm20161231ex311.htm |

| EX-23 - EXHIBIT 23 - CONSENT - NxStage Medical, Inc. | nxtm20161231ex23.htm |

| EX-21 - EXHIBIT 21 - SUBSIDIARY LISTING - NxStage Medical, Inc. | nxtm20161231ex21.htm |

| EX-10.7 - EXHIBIT 10.7 - PERFORMANCE SHARE AWARD AGREEMENT - NxStage Medical, Inc. | nxtm20161231ex107psa.htm |

| EX-10.6 - EXHIBIT 10.6 - RESTRICTED STOCK UNIT AGREEMENT - NxStage Medical, Inc. | nxtm20161231ex106rsu.htm |

| EX-10.5 - EXHIBIT 10.5 - STOCK OPTION AGREEMENT - NxStage Medical, Inc. | nxtm20161231ex105option.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2016 | ||

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from __________ to __________ | ||

Commission file number: 000-51567

NxStage Medical, Inc.

(Exact Name of Registrant as Specified in Its Charter)

Delaware | 04-3454702 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

350 Merrimack Street, Lawrence, MA | 01843 | |

(Address of Principal Executive Offices) | (Zip Code) | |

Registrant's Telephone Number, Including Area Code:

(978) 687-4700

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, $0.001 par value | Nasdaq Global Select Market | |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. þ Yes o No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes þ No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. þ Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). þ Yes o No

1

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer £ | Smaller reporting company £ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes þ No

The aggregate market value of common stock held by non-affiliates of the registrant was approximately $1.4 billion, as of June 30, 2016, based on the last reported sale price of the registrant's common stock on the NASDAQ Global Select Market on June 30, 2016.

There were 65,216,409 shares of the registrant's common stock outstanding as of the close of business on February 22, 2017.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive proxy statement for its 2017 Annual Meeting of Stockholders are incorporated by reference in response to Part III of this Annual Report.

2

NXSTAGE MEDICAL, INC.

2016 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

Page | ||

Mine Safety Disclosures | ||

Item 10. | Directors, Executive Officers and Corporate Governance | |

Item 11. | Executive Compensation | |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

Item 13. | Certain Relationships and Related Transactions, and Director Independence | |

Item 14. | Principal Accounting Fees and Services | |

3

CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report and certain information incorporated by reference herein contain forward-looking statements concerning our business, operations and financial condition, including statements with respect to:

•the growth of our business;

•our vision of enabling better clinical outcomes for patients at a lower cost to the healthcare system;

•the ability of our product pipeline to help us expand existing markets and enter new ones;

•achieving greater operating leverage and improved financial results in the future;

•expectations about achieving overall company profitability in 2017;

•our belief that the significant majority of our near-term revenues will come from sales of the System One in the U.S.;

•financial performance of our NxStage Kidney Care dialysis centers and our continued investments in them;

•estimates of the number of end-stage renal disease (ESRD) patients that could be treated at home with the System One;

•potential value and components of the global market for ESRD and critical care products;

• | our strategic initiatives to grow home hemodialysis adoption, expand globally, enhance our product offerings, expand into high growth adjacencies and enter peritoneal dialysis and their ability to unlock commercial opportunities and drive future growth; |

• | our belief that peritoneal dialysis is ripe for technology innovation and that we are well-positioned to launch into this market; |

• | access to home and more frequent hemodialysis; |

• | the potential for our nocturnal clearance and other initiatives to expand the home hemodialysis market and improve patient care; |

• | our plans for, and expected design and functionality of, our next-generation hemodialysis system, next-generation critical care system and peritoneal dialysis system; |

•the development and commercialization of new products and improvements to existing products;

•sales to our key customers, including DaVita HealthCare Partners and Fresenius Medical Care;

•the adequacy of our funding;

• | expectations with respect to future demand for our products and revenue growth, with components of such revenue growth including sales of disposable products; |

• | future financial results for our System One, In-Center and Services segments and total company; |

• | expectation of sustaining gross profit as a percentage of revenue in our System One segment above 50% and the underlying elements of such objective; |

• | future selling and marketing, research and development, distribution, and general and administrative expenses and the drivers for such expenses; |

• | our manufacturing operations and supply chain; |

•the scope and impact of our research and development efforts;

•availability of suitable facilities;

•expectations with respect to our working capital levels and requirements;

•availability of credit under our revolving credit facility;

•global economic conditions;

•expectations with respect to achieving positive operating margins and maintaining positive cash flows;

•volatility of our stock price;

•expectation to retain earnings and not issue dividends;

•legal proceedings;

•expectations with respect to product reliability;

•impact of the adoption of new accounting standards;

•future realization of our deferred tax assets;

• | anticipated benefits of manufacturing dialyzers for sale to Asahi Kasei Kuraray Medical Co. (Asahi) and future sales to Asahi; |

•our ability to withstand supply chain disruptions;

•the scope and adequacy of patent protection with respect to our products;

4

• | the availability of, and changes in, reimbursement for home and more frequent hemodialysis, including home nocturnal hemodialysis; and |

•the financial, commercial and operational impact of any of the above.

All statements other than statements of historical facts included in this Annual Report regarding our strategies, prospects, financial condition, costs, plans and objectives are forward-looking statements. When used in this Annual Report, the words “expect”, “anticipate”, “intend”, “plan”, “believe”, “seek”, “estimate”, “potential”, “continue”, “predict”, “may”, "will" and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. Because these forward-looking statements involve risks and uncertainties, actual results could differ materially from those expressed or implied by these forward-looking statements.

Readers should carefully review the Risk Factors and Management's Discussion and Analysis of Financial Condition and Results of Operations set forth in this Annual Report, as these sections describe important factors that could cause actual results to differ materially from those indicated by our forward-looking statements. We undertake no obligation to revise or update publicly any forward-looking statement.

NOTE REGARDING TRADEMARKS

NxStage®, Streamline®, ButtonHole®, MasterGuard®, Medisystems®, Nx2me Connected Health®, Nx2me®, LockSite® and OneSite® are registered trademarks of NxStage Medical, Inc. PureFlow SLTM and System OneTM are trademarks of NxStage Medical, Inc. iPad® is a registered trademark of Apple Inc.

5

PART I

For convenience, in this Annual Report “NxStage,” “we,” “us,” and “the Company” refer to NxStage Medical, Inc. and our consolidated subsidiaries, taken as a whole.

Item 1. | Business |

Our Company

NxStage Medical, Inc. is a medical technology company that develops, manufactures and markets innovative products and services for patients suffering from chronic or acute kidney failure. Since our initial public offering in 2005, we have built a strong business that we believe serves as a solid foundation for future growth. As a leader in home hemodialysis, we remain committed to not only growing this and our other existing areas, but also expanding to new markets where we believe our current and future technology has the ability to deliver value for both patients and our customers.

Our vision is to improve the standard of kidney care through technology leadership, therapy innovation and the efficient use of healthcare resources. By creating technology that is designed to have broad capability, be simple to use in a variety of settings, and incorporate greater automation with reduced equipment and supply costs, we believe we can ultimately enable better clinical outcomes for patients at a lower overall cost to the healthcare system. We work with our customers, patients, physicians, industry partners and government leaders to advance this vision.

Our primary product, the System One, was designed to satisfy an unmet clinical need for a system capable of delivering the therapeutic flexibility and clinical benefits of traditional dialysis machines in a smaller, portable, easy-to-use form that can be used by healthcare professionals and trained lay users alike in a variety of settings, including patient homes, as well as more traditional care settings such as hospitals and dialysis centers. Given its design, the System One is particularly well-suited for home hemodialysis and a range of dialysis therapies that are more practical to deliver in the home setting, including more frequent hemodialysis and nocturnal hemodialysis. Clinical literature suggests such therapies provide patients better clinical outcomes and improved quality of life.

We also operate a small number of NxStage Kidney Care dialysis centers, independently and in some instances as joint ventures, that treat end-stage renal disease patients directly. These centers provide us with valuable experience to better meet and anticipate the needs of both our customers and patients, while optimizing our product technology.

Our research and development efforts are important to our future success. Our product development organization is working to develop innovative technical approaches that address the limitations of current dialysis systems and disposable products. We are also working on enhancements to our product designs to improve ease of use, functionality, reliability and safety and to reduce product cost. We believe that our product pipeline will help us to both expand existing markets and enter new ones.

We report our operating results through three segments: System One, In-Center and Services. We sell our products in and provide our services in three markets: home, critical care and in-center. Our other business activities excluded from segment operating performance measures relate primarily to the manufacturing of dialyzers for sale to Asahi Kasei Kuraray Medical Co. (Asahi). Together with certain research and development and general and administrative expenses that are excluded from our business segment operating results, these business activities are reported in the Other category. The operating results of NxStage Kidney Care are included in our Services segment. For convenience, we use the term “products business” to refer collectively to our System One segment, In-Center segment, and Other category.

We are headquartered in Lawrence, Massachusetts, with manufacturing facilities in Mexico, Germany and Italy. Through our international network of affiliates and distribution partners, patients in over 21 countries have been treated with our products.

Our Financial Performance

The table below provides a three year history of revenues and income (loss) from operations summarized for the products business (which includes the results of our System One segment, In-Center segment and Other category), Services segment and in total. For detail below this summary level, please see further segment discussion under Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 8, Financial Statements and Supplementary Data.

6

(in thousands) | 2016 | 2015 | 2014 | ||||||||

Products Business (System One Segment, In-Center Segment & Other) | |||||||||||

Revenues | $ | 359,127 | $ | 332,845 | $ | 300,598 | |||||

Income (Loss) from operations | $ | 22,695 | $ | 9,197 | $ | (7,261 | ) | ||||

Services Segment | |||||||||||

Revenues | $ | 14,781 | $ | 6,412 | $ | 1,749 | |||||

Loss from operations | $ | (26,233 | ) | $ | (23,826 | ) | $ | (14,926 | ) | ||

Eliminations | |||||||||||

Elimination of intersegment revenues | $ | (7,530 | ) | $ | (3,134 | ) | $ | (846 | ) | ||

Elimination of intersegment gross profit | $ | (747 | ) | $ | — | $ | — | ||||

Total Company | |||||||||||

Revenues | $ | 366,378 | $ | 336,123 | $ | 301,501 | |||||

Loss from operations | $ | (4,285 | ) | $ | (14,629 | ) | $ | (22,187 | ) | ||

Since inception, we have focused on building a long-term sustainable business model based on innovative technologies and offerings. Although we have driven significant revenue growth, and have a robust product portfolio and product development pipeline, we have historically operated at a net loss. In recent years, we have started to achieve greater operating leverage and financial improvements, while still maintaining our focus on product development and topline growth. During 2016, we continued to generate operating income in our products business, and we expect to continue our focus on driving improvements in 2017 and beyond within this business, while we continue to invest in our existing NxStage Kidney Care dialysis centers. We expect to achieve positive net income for the full 2017 fiscal year as our products business continues to grow.

Our Market

Kidney Failure: Chronic and Acute

Chronic kidney disease is typically characterized by the progressive loss of kidney function due to damage caused by diabetes, high blood pressure and other causes. The final stage of chronic kidney disease is called end-stage renal disease (ESRD), which is an irreversible, life-threatening loss of kidney function that is treated predominantly with dialysis. Dialysis is a kidney replacement therapy that removes toxins and excess fluids from the bloodstream. Unless the patient receives a kidney transplant, dialysis is required for the remainder of the patient’s life. The primary types of dialysis are hemodialysis and peritoneal dialysis. Hemodialysis diverts the patient’s blood to an external dialyzer, where a filter and cleansing fluid (“dialysate”) remove toxins and excess fluids, and then returns the cleansed blood to the patient. Hemodialysis is traditionally performed by healthcare professionals in a dialysis clinic on a fixed schedule three times per week, referred to as “in-center” treatment, but can be performed by the patient, with the availability of a care partner, in the home three to seven times per week. Peritoneal dialysis is a home therapy in which toxins are removed through the peritoneum, a part of the patient’s abdomen, through multiple fluid exchanges each day.

Acute kidney failure happens suddenly, as a result of illness, injury or other conditions. Acute kidney failure is typically treated with renal replacement therapies, including hemodialysis, in a hospital or similar critical care setting.

Approximately 470,000 ESRD patients in the U.S. and 2.6 million ESRD patients worldwide rely on life-sustaining dialysis treatment.

7

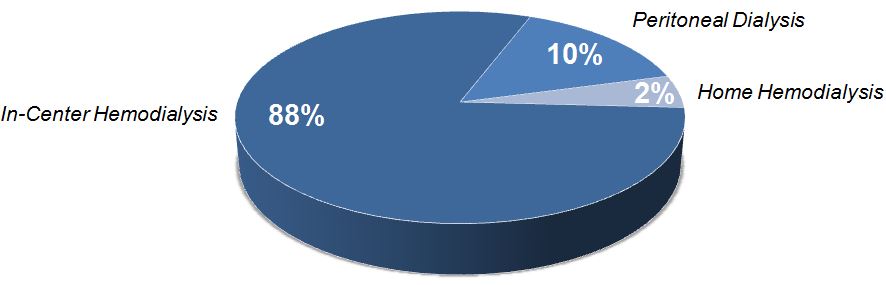

Dialysis Modality Prevalence (U.S.)

Although in-center hemodialysis is the most common ESRD therapy in the U.S., surveys of healthcare professionals suggest that a larger proportion of patients could take responsibility for their own care. In fact, more than 90% of surveyed U.S. nephrologists have said they would choose a home dialysis therapy for themselves if informed they needed renal replacement therapy, with home hemodialysis being the preferred option. With our current technology, we believe that approximately 10-15% of ESRD patients in the U.S. would be appropriate candidates for home hemodialysis with the System One.

Studies have consistently shown that home hemodialysis may be a viable alternative for ESRD patients to experience enhanced health, control and freedom. Home hemodialysis offers patients numerous benefits when compared with traditional in-center hemodialysis, including:

- improved survival;

- | independence and the ability to better understand and take control of one’s care; |

- | freedom from specific time constraints with greater ability to work and participate in “normal” life activities; |

- | greater freedom to travel; |

- | convenience of not driving to and from the dialysis center three times a week; and |

- | privacy and comfort of being at home. |

In addition, home hemodialysis presents the most practical setting for performing therapy at the frequency and duration that best suits a patient’s clinical needs. Traditional in-center hemodialysis treatment schedules are constrained by staffing and time slot availability, which presents practical and economic limitations on the ability to explore or implement innovative therapy delivery models that are more tailored to the unique clinical and lifestyle needs of patients, as well as responsive to the growing body of clinical literature reporting on the benefits of different therapy delivery models. Although the significant majority of ESRD patients are cared for in-center under a delivery model that provides for three treatments a week (Monday, Wednesday and Friday, or Tuesday, Thursday and Saturday), typically at 3 to 4 hours per session, there is mounting clinical evidence demonstrating the quality of life and clinical benefits of alternative therapy delivery schedules, including additional dialysis sessions (from four to seven sessions per week) as well as longer, nocturnal therapy sessions. More frequent therapy, in particular, has been shown to lead to better clinical outcomes such as:

- improved survival;

- | reduced risk of cardiovascular morbidity; |

- | improved regulation of blood pressure and phosphorus and reduced need for related medications; |

- | improved physical and mental quality of life; and |

- | better therapy tolerance. |

For more information about the clinical benefits of more frequent hemodialysis, please review the section below entitled “Clinical Evidence.”

Products Market

8

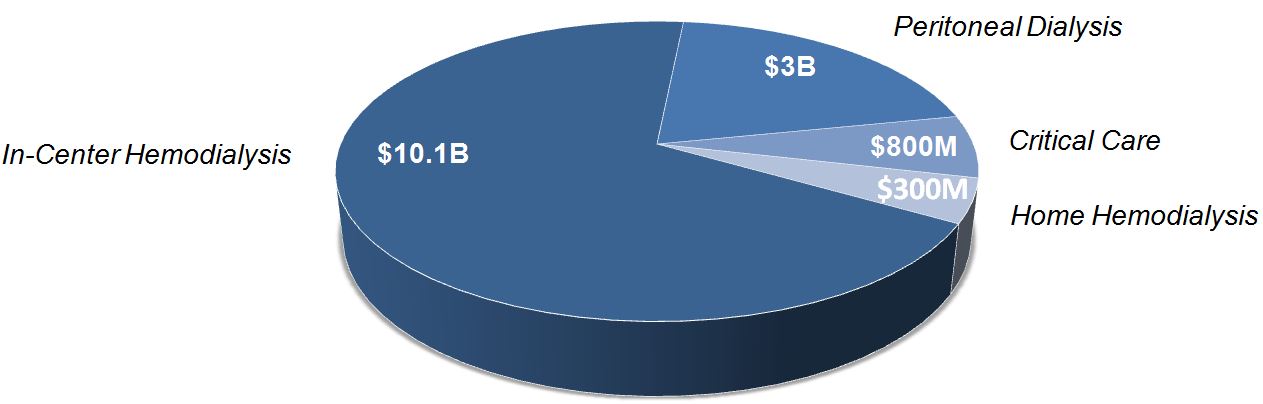

Based on the prevalence of kidney failure and related healthcare data, we estimate the potential value of the global market for ESRD and critical care products to be allocated among the following constituents:

Market Opportunity: Global ESRD & Critical Care Products

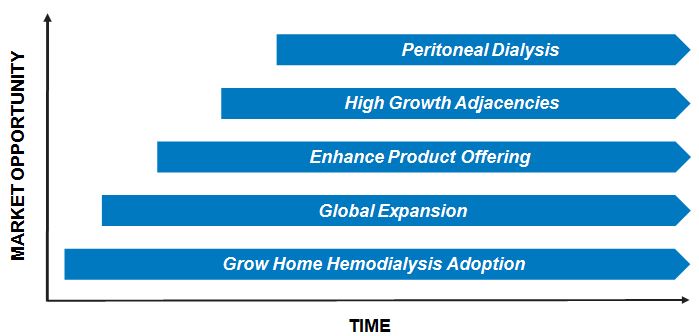

While we believe the significant majority of our near-term revenues will come from sales of the System One in the U.S., we are working on a number of strategic initiatives that we believe will unlock a greater market opportunity for us over the next few years.

Strategic Initiatives

Grow Adoption of Home Hemodialysis with the System One

To increase patient awareness and demand for home and more frequent hemodialysis, we conduct and sponsor local and national patient outreach and awareness campaigns, participate in preeminent nephrology conferences, organize educational programs for patients and clinicians in collaboration with local service providers, collaborate with local and national kidney patient organizations, utilize direct mail and Internet campaigns to provide product literature and clinically relevant information, employ patient advocates, advertise in trade publications and broader media outlets and conduct numerous other educational and promotional activities. In addition, our NxStage Kidney Care dialysis centers are working to expand access to home therapies and are helping us to devise best practices for successful home dialysis programs.

We also advocate for increased access to the life changing benefits of home hemodialysis and more frequent hemodialysis for medically suitable patients. Even though healthcare professionals would choose home hemodialysis for themselves more than any other modality, many of their patients do not have adequate access to this option. According to data from the Centers for Medicare & Medicaid Services (CMS), only 18% of U.S. dialysis clinics actively offer home hemodialysis to their patients, and only 27% are certified to offer the therapy. Although access to home and more frequent hemodialysis continues to grow,

9

we believe that current Medicare reimbursement policies lead to adoption rates lower than rates commensurate with the percentage of patients experts believe can perform and medically benefit from this therapy. We believe further improving Medicare reimbursement for home hemodialysis training, as well as more predictable Medicare reimbursement for more frequent dialysis with less administrative burden and payment for medical oversight equal to that provided for overseeing in-center patients would allow U.S. adoption of home hemodialysis at rates more consistent with what is deemed to be appropriate by the medical community. We continue to engage in regular dialogue with CMS, Medicare contractors, policymakers and industry experts on such issues to encourage broader adoption of home and more frequent hemodialysis.

Drive Global Expansion

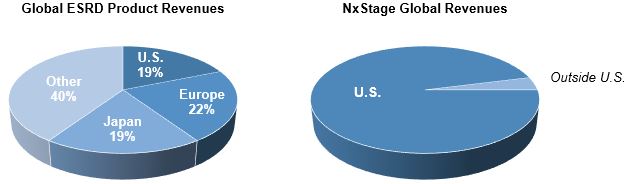

Historically, predominantly all of our revenues have come from sales of our products in the U.S. However, the U.S. represents a small portion of the global market for ESRD products. Accordingly, the international market represents a significant growth opportunity.

We commenced international sales in 2009 and have sold the System One in 21 countries. We seek to increase our product revenues by expanding our international presence within countries where we have an established footprint and entering new regions through third-party distributors who have an established presence in such regions. Furthermore, our product pipeline is expected to introduce features and enhancements that we believe will increase the appeal of our products to international customers.

Enhance the Ease of Use and Clinical Flexibility of our Product Offering

We promote our products’ ease of use and clinical flexibility. Accordingly, we continue to add new features and tools associated with our next-generation hemodialysis system to enhance usability and reduce the burden of therapy, and we continue work to expand the System One's applications.

In 2014, the System One became the first and only hemodialysis machine cleared in the U.S. to perform hemodialysis overnight while the patient and care partner sleep. The System One also is CE marked for home nocturnal hemodialysis in the EU. Home nocturnal hemodialysis is an important patient option associated with a number of lifestyle and clinical advantages. By doing therapy while sleeping, patients free up their day to pursue other activities thereby reducing the overall burden of therapy. A longer, overnight therapy also allows for greatly expanded flexibility in dialysis dose and schedule, better enabling physicians to match the dialysis prescription to individual patient needs. We believe that this nocturnal clearance will open home hemodialysis therapy to new segments of patients, and improve care for ESRD patients by expanding therapeutic options and flexibility.

We have also seen strong interest in Nx2me Connected Health, our telehealth platform for the collection and delivery of treatment and medical information for patients using the System One. By enhancing the ease of information collection and availability to the patient and care team, Nx2me may foster improved home patient retention and communication.

In addition, our research and development organization continues to work on enhancements to our product designs and is currently developing, among other things, our next-generation critical care system. Additional information about our innovative product pipeline is provided below in the sections entitled “Enter Peritoneal Dialysis,” “Next-Generation Hemodialysis System,” "Next-Generation Critical Care System" and “Product Development.”

In addition, our NxStage Kidney Care dialysis centers are gaining valuable clinical insights that will help us to optimize our product technology.

We believe that technological improvements which make the administration of home hemodialysis less burdensome can help to expand the commercial potential of home hemodialysis.

Expand into High Growth Adjacencies

10

We focus on expanding into adjacent markets, including skilled nursing facilities where we believe our product technology offers a differentiated and compelling value proposition.

Nursing home residents represent approximately 8% of all ESRD patients. Nursing home patients are generally transported off-site to dialysis clinics, which may introduce several risks to their health and compromise their care. The System One can be used at skilled nursing facilities to offer residents on-site hemodialysis, which may eliminate patient discomfort from traveling to an outside facility and the accompanying disruptions in rehabilitation, medication schedules and social activities. Offering on-site hemodialysis also eliminates the high costs of transporting patients to dialysis clinics, which is not always covered by reimbursement.

Enter Peritoneal Dialysis

The commercial opportunity with peritoneal dialysis is significantly larger than that for home hemodialysis and is well established as it is generally favored by healthcare programs and payors. We believe, however, that peritoneal dialysis is ripe for technology innovation and that we are well-positioned to launch into this market based on our capabilities and decade long history of technological innovation and leadership within home hemodialysis. We are developing our peritoneal dialysis system to offer a differentiated therapy solution with on-site dialysate generation from concentrate without the need for premixed bagged fluids, with pre-connected, ready to use disposables that require fewer touch contamination points, and automation to improve setup, training and use.

Future Peritoneal Dialysis System

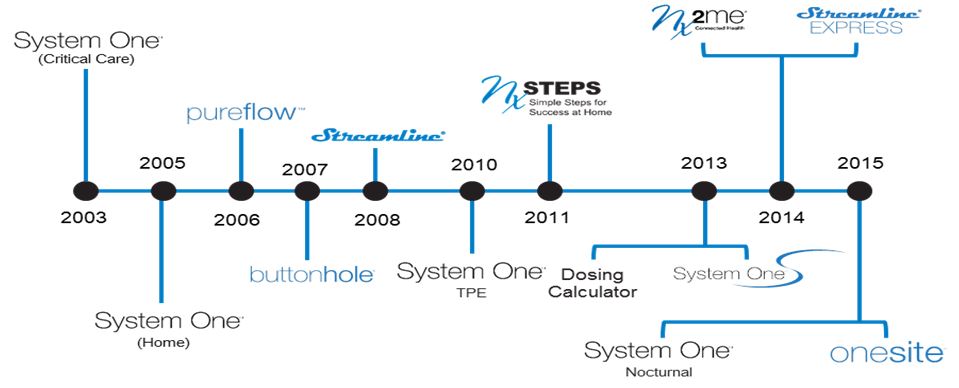

Our Products and Services

We have over a decade long history of product innovation. Our products and services currently target the home, critical care and in-center markets. The following timeline highlights some of our key product introductions since 2003:

11

The following section describes our product offerings.

Home Dialysis

Our home product offerings currently target the home hemodialysis market. The NxStage System One is a small, portable, easy-to-use hemodialysis system that is used to perform treatments during the day or at night, while sleeping. The System One is the only portable hemodialysis system that is cleared by the U.S. Food and Drug Administration (FDA) for in-center and hospital use (2002), for home hemodialysis (2005) and home nocturnal hemodialysis (2014). Its simplicity and compact size are intended to allow for easy use in patients’ homes or other home-like settings and give patients the opportunity to travel with their therapy.

System One - Home

In addition to our machine, we provide patients with the following proprietary consumables and services which are used for each treatment with the System One:

- | The NxStage Cartridge. A disposable, integrated treatment cartridge that loads simply and easily into the System One. The cartridge incorporates a proprietary volumetric fluid management system and includes a pre-attached dialyzer. |

- | PureFlow SL and Premixed Dialysate. Our PureFlow SL accessory prepares on-site premixed dialysate fluid in batches before treatment in the patient’s home using ordinary tap water and dialysate concentrate. The volume of fluids used varies with treatment options, prescription and setting. To accommodate patient travel with the System |

12

One or in other circumstances in which the PureFlow SL is not available, we also supply premixed dialysate in sterile five liter bags.

- | Nx2me Connected Health. Our Nx2me Connected Health platform leverages cloud-based computing and wireless communications by using an application we developed for the iPad. The Nx2me Connected Health application collects important System One cycler data, as well as patient information such as blood pressure and weight. Patients can review, confirm, and transmit this data to their dialysis centers after each treatment and dialysis center staff can access the transmitted data with their own clinician portal. This gives the staff enhanced capabilities to review and follow treatment adherence and progress as well as the ability to transfer this data directly into their electronic health records system. |

Unlike traditional dialysis systems, the System One does not require any special disinfection and its operation does not require specialized electrical or plumbing infrastructure or modifications to the home. Trained patients can bring the System One home, plug it into a conventional electrical outlet and operate it, thereby eliminating what can be expensive plumbing and electrical household modifications required by traditional dialysis systems.

Next-Generation Hemodialysis System

In 2016, we commenced a phased launch of our next-generation hemodialysis system. The first phase included software changes improving ease of use and set up time. In 2017, we expect to launch a second phase of enhancements, including a touch screen user interface and integrated blood pressure cuff, upon regulatory clearance. The third phase of our next-generation system includes a new on-site on-demand bicarbonate-based dialysis generation system. We have elected to develop a second generation of this system before investing in the regulatory process for its market clearance. We expect this development cycle to further enhance its capabilities as well as further optimize and reduce the cost of the system.

Next-Generation Hemodialysis System

Critical Care

The System One also delivers a range of renal replacement therapies within the critical care market. The System One sold to hospitals for critical care is based on the same technology platform used in the home market but offers a wider range of therapies, including therapeutic plasma exchange. We configure our critical care system with an intuitive touch screen display that provides real-time treatment information as well as easy troubleshooting capabilities for hospital staff and an ergonomic mobile stand for exceptional portability.

System One - Critical Care

13

We also supply related disposable cartridges and treatment fluids necessary to perform dialysis treatment in the critical care market.

The clinical flexibility of the System One, coupled with its ease of use and portability, make our system well suited for hospital critical care environments.

Next-Generation Critical Care System

In June 2013, we entered into a research and development program sponsored by the Defense Advanced Research Projects Agency of the U.S. Department of Defense to develop an innovative device for use in military applications under a government sponsored program. This program aligns well with our technology and we expect that we will continue to leverage this product development work in the advancement of our next-generation critical care system. We expect that the design of our next-generation critical care system will incorporate a small footprint, intuitive touch screen interface, multi-stream fluid management system, and the option of on-demand fluid generation.

In-Center

We sell extracorporeal disposable products under our Medisystems brand that are primarily used for in-center hemodialysis treatments for ESRD patients. These products include hemodialysis blood tubing sets, arteriovenous (AV) fistula needles, apheresis needles, safety accessories and access management disposables.

Our Streamline blood tubing sets feature an efficient and airless design intended to enable providers to optimize dose delivery, and includes our patented LockSite needleless access sites, eliminating the need for sharp needles or costlier guarded needles to be used with the tubing set in connection with dialysis therapy. In addition, our Streamline Express dialyzer features a pre-attached blood tubing set, which is designed to reduce the number of touch point contamination sites. Our AV fistula and apheresis needles have been designed to achieve a smooth blood flow throughout the treatment, intended to result in less clotting, fewer pressure drops, and less stress on the patient’s blood. We also offer ButtonHole needles for hemodialysis therapies, which are used by patients that employ the constant-site technique, whereby a fistula needle is inserted in the same place each treatment.

NxStage Kidney Care

We operate a small number of NxStage Kidney Care dialysis centers, independently and in some instances as joint ventures, that treat ESRD patients directly. These centers provide us with valuable experience to better meet and anticipate the needs of both our customers and patients, while optimizing our product technology. In addition, these centers provide us with the opportunity to innovate and foster new care delivery models to advance the standard of renal care across other settings. More specifically, at NxStage Kidney Care we offer a range of treatment options, including home hemodialysis, peritoneal dialysis and flexible in-center hemodialysis. These centers also help us to devise best practices for successful home dialysis programs and provide sites for future clinical trials of our products.

Our Reporting Segments

We report our operating results through three segments: System One, In-Center and Services. Our other business activities relate primarily to the manufacturing of dialyzers for sale to Asahi Kasei Kuraray Medical Co. (Asahi). Together with certain

14

research and development and general and administrative expenses that are excluded from our business segment operating results, these business activities are reported in the Other category. We refer to our System One segment, In-Center segment and Other category as our products business. Additional financial information regarding our business segments and geographic data about our assets are contained in Note 9, Business Segment and Geographic Information to our consolidated financial statements and Management’s Discussion and Analysis of Financial Condition and Results of Operations included in this Annual Report. A discussion of the risks attendant to our operations is set forth in the Risk Factors section of this Annual Report.

System One

Our System One segment includes worldwide revenues from the sale and rental of the System One and PureFlow SL dialysate preparation equipment and the sale of disposable products in the home and critical care markets. Some of our largest customers in the home market provide outsourced renal dialysis services to some of our customers in critical care. Sales of products to both markets are made primarily through dedicated sales forces to dialysis centers and hospitals and delivered directly to the customer, or their patients, with certain products sold through distributors. In addition to specialized sales representatives, we also employ nurses in our sales force as clinical educators to support our sales efforts. We have a staff of customer support specialists to assist patients, clinics and hospitals with product orders and deliveries. We also provide technical support 24 hours a day, seven days a week through a dedicated staff of technical support representatives, to respond to questions raised by patients, clinics and hospitals concerning the System One.

Home. We market and sell the System One to dialysis clinics in the U.S. and other markets, which in turn provide the System One to their ESRD patients for chronic home hemodialysis treatment. In the U.S., Medicare regulations require that all chronic ESRD patients be under the care of a dialysis clinic, whether they are treated at home or in clinic. As a result, we do not sell the System One directly to Medicare patients. A significant majority of System One equipment in the home is purchased rather than rented by our customers. Purchased equipment pricing includes service for an initial contractual period after which the customer pays a standard service fee. We use a depot service model for equipment servicing and repair. If a device requires repair, we arrange for a replacement device to be shipped to the site of care, whether it is a patient’s home or a clinic, and for pick up and return to us of the system requiring service. This shipment is done by common carrier and, as there are no special installation requirements, the patient or clinic can quickly and easily set up the new machine.

After selling or renting a System One to a new clinic customer, our clinical educators train the clinic’s nurses and dialysis technicians on the proper use of the System One using our proprietary training materials. We then rely on our customers’ trained technicians and nurses to train home patients, their care partners and other technicians and nurses using the System One. In general, we are not responsible for, and do not provide, patient training except for NxStage Kidney Care patients. Patient training takes place at the clinic primarily during the patient’s prescribed treatment sessions. Training typically takes three to four weeks and consists of (1) basic education about ESRD, (2) training patients and care partners on inserting needles into the patient’s vascular access site and (3) instruction on the use and operation of the System One. Reimbursement for training sessions is provided by Medicare, at a fixed rate, and private insurance.

For each month that a patient is treated with the System One, we bill the clinic for the purchase of the related disposable cartridges and treatment fluids necessary to perform treatment, and other related services, where applicable.

Our customers for products used in the home are highly consolidated. DaVita HealthCare Partners (DaVita) and Fresenius Medical Care (Fresenius) own and operate the two largest chains of dialysis clinics in the U.S. and are our two largest customers for products used in the home. Collectively, they provide treatment to more than two-thirds of U.S. dialysis patients and a similar portion of our home patients, and account for the majority of our System One segment revenues. Increased sales to DaVita and Fresenius have driven a large portion of our historical revenue growth and will be important to future growth. Our home agreements with DaVita and Fresenius are intended to support the continued expansion of patient access to home hemodialysis with the System One, but like all our agreements with home market customers, these agreements are not requirements contracts and contain no minimum purchase volumes. Our home agreement with DaVita extends through December 31, 2018, with monthly renewals thereafter unless terminated by either party with 30 days' prior notice. Our home agreement with Fresenius continues to renew on a monthly basis unless we and Fresenius choose to modify the terms with an amendment or new agreement.

Critical Care. We market the System One directly to hospitals for treatment of acute kidney failure and fluid overload in the U.S. and other geographies. Most of our customers in the critical care market use the System One to perform prolonged or continuous renal replacement therapy for their acute kidney failure or fluid overload patients. We position the System One as a differentiated platform for the delivery of renal care in acute settings because of its technologically innovative features, ease of use and portability. The System One’s continuous volumetric balancing offers a simple effluent drainage capacity. It also uses a disposable, integrated treatment cartridge to minimize maintenance and disinfection requirements, and pre-mixed dialysate to free it from cumbersome water processing systems.

15

A significant majority of System One equipment in the critical care market is purchased rather than rented by our customers. Purchased equipment pricing includes service during our standard one-year warranty period, and we sell one- and two-year service contracts for post-warranty periods. We also offer a bio-medical training program, whereby we train bio-medical engineers on how to service and repair certain aspects of the System One in the critical care setting. Unlike the home market, we do not use a depot service model for equipment servicing and repair, but instead generally service critical care equipment in the field. The nature of the hospital critical care setting, coupled with the practices of other intensive care unit dialysis equipment suppliers, requires that we offer on-site support for our systems in this environment, or for the use of a trained bio-medical engineer.

After selling or renting a System One to a new hospital customer, our clinical educators generally train the hospital’s intensive care unit and acute dialysis nurses on the proper use of the System One using our proprietary training materials. We then rely on the trained nurses to train other nurses. By adopting this “train the trainer” approach, our sales nurses do not need to return to the hospital each time a new nurse requires training.

We also supply hospitals using the System One with related disposable cartridges and treatment fluids necessary to perform treatment.

International. We sell the System One and certain other products internationally, through a combination of direct sales to dialysis clinics and hospitals in the United Kingdom and Canada, and sales through distributors in Europe and other select markets. Products sold to distributors are shipped directly to distributor warehouses and the distributors sell or rent our products to dialysis providers or hospitals and are responsible for marketing, clinic training and equipment servicing and repair.

We entered the international market in 2009 and to date our international sales have been limited and focused primarily on the home market. While we are still early in our international commercialization efforts, we believe that there is a large opportunity for us to expand outside the U.S. Several of our product development initiatives, including our peritoneal dialysis system and next-generation critical care system, will be important to these efforts.

In-Center

Our In-Center segment includes revenues from the sale of blood tubing sets and needles for hemodialysis, primarily for the treatment of ESRD patients at dialysis clinics, and needles for apheresis. In this market, our customers are independent dialysis clinics as well as dialysis clinics that are part of national or regional chains. Although in many instances we have direct contractual relationships with our customers, nearly all of our sales in this segment are made through national distributors in order to leverage national networks, shipping efficiencies and existing customer relationships. We plan our manufacturing and distribution activities based on distributor purchase orders. Finished goods are shipped directly to distributor warehouses. We support distributor selling and marketing efforts with brand marketing support and a team of clinical educators who assist with clinical in-service activities.

We market our extracorporeal disposable products under the Medisystems brand, which we acquired in 2007. Medisystems branded products have an established reputation for quality, ease of use and innovation, and have been in the in-center market since 1981. In our marketing efforts, we emphasize our Medisystems products’ strong clinical performance and cost-effectiveness.

Our In-Center segment revenues are highly concentrated in several significant purchasers. Henry Schein, Inc., accounted for 28% of our 2016 In-Center segment revenues. Gambro AB (a subsidiary of Baxter International, Inc.) accounted for 20% of our 2016 In-Center segment revenues, with all of Gambro's sales of our products being to DaVita.

Services

Our Services segment includes revenues from dialysis services provided to patients at our NxStage Kidney Care dialysis centers. As of February 3, 2017, we had 20 centers accepting patients in13 states, of which 19 have received Medicare certification. We continue to explore innovative service delivery models with our NxStage Kidney Care dialysis centers to advance the standard of renal care. Some of our service models vary on the number of treatment stations within a center, the configuration of the center and hours of operation. However, at all of our centers, we provide patients with a range of therapy options to address their clinical and lifestyle needs. For appropriate patients, such therapies may include home hemodialysis, flexible in-center hemodialysis and peritoneal dialysis.

Clinical Evidence

The vast majority of ESRD patients in the U.S. are prescribed traditional in-center hemodialysis, which consists of three dialysis sessions per week, typically at 3 to 4 hours per session, in a clinical setting. Despite falling mortality rates in hemodialysis patients during the past decade, rates remain much higher than in age-matched U.S. residents. Notably, among patients under age 50, mortality rates are 25 to 55 times higher than in general U.S. residents. Significant clinical literature strongly supports that home and more frequent hemodialysis therapy can lead to improved clinical outcomes.

16

Home Hemodialysis

Studies have consistently shown that home hemodialysis may offer enhanced health, control and freedom to ESRD patients. Several observational studies have found home hemodialysis to be associated with a lower mortality risk compared to in-center hemodialysis. Home therapy may also be an effective way by which to increase patient engagement in the delivery of dialysis, with accumulating health services research suggesting improved outcomes with higher patient activation. In addition, home patients are afforded a newfound independence and control over their care that can result in an improved quality of life.

More Frequent Hemodialysis

The traditional thrice weekly hemodialysis schedule is a clear departure from normal physiology in which the kidneys continuously filter blood. Accompanying each interval between consecutive dialysis sessions, changes in serum biochemistry and volume status may increase risks of both acute (e.g., cardiac arrhythmia) and chronic (e.g., end organ damage) complications. The roughly 72-hour interval between consecutive sessions on Friday and Monday or Saturday and Tuesday appears to be especially problematic. Multiple studies have suggested that this interval is associated with increased risks of mortality and morbidity.

More frequent hemodialysis, defined as the range of schedules that eliminates multiple-day intervals between consecutive sessions, mitigates the “unphysiology” of the usual hemodialysis schedule. Regimens range from every-other-day dialysis to daily dialysis. Accumulating evidence, including randomized clinical trials and large observational studies, indicates that more frequent hemodialysis confers multiple benefits, including reduced risk of cardiovascular morbidity, improved regulation of blood pressure and phosphorus and reduced need for related medications, better tolerability of hemodialysis and improved physical and mental quality of life.

Cardiovascular Disease. Cardiovascular disease is the leading cause of death in hemodialysis patients. An important predictor of cardiovascular mortality and morbidity in dialysis patients is left ventricular hypertrophy (LVH), a condition marked by enlargement and thickening of the walls of the left ventricle. LVH is an adaptive response to increased cardiac work, typically caused by combined pressure and volume overload. Multiple studies show that more frequent hemodialysis reduces left ventricular mass and is associated with significantly lower risk of cardiovascular mortality and morbidity, particularly due to heart failure and hypertensive disease.

Blood Pressure and Antihypertensive Medications. Hypertension is a cardinal feature of ESRD, with the prevalence of hypertension exceeding 85% in new ESRD patients. Highly elevated blood pressure is associated with poor outcomes in dialysis patients. With three hemodialysis sessions per week, blood pressure climbs during the interdialytic interval, in step with interdialytic weight gain, particularly among elderly patients and those with higher dry weight. Multiple randomized clinical trials show that frequent hemodialysis reduces blood pressure and the need for oral medications indicated for hypertension.

Serum Phosphorus and Phosphate Binders. ESRD patients commonly have elevated levels of serum phosphorus (“hyperphosphatemia”). Hyperphosphatemia is associated with higher risk of cardiovascular death. The treatment of hyperphosphatemia is burdensome. Dialysis patients consume on average 19 pills per day and 9 are phosphate binders. Moreover, Medicare Part D expenditures on binders for dialysis patients exceeded $840 million in 2014. Meanwhile, adherence to phosphate binders is poor, especially in younger patients and those with high pill burden. Multiple randomized clinical trials show that frequent hemodialysis reduces serum phosphorus. In observational research, frequent hemodialysis is also associated with a lower percentage of patients using binders.

Dialysis Tolerability. Dialysis treatment can be difficult to tolerate. Recurrent complications during and after the hemodialysis session may limit treatment persistence and engender withdrawal, which is the primary cause of death in 10% to 15% of patients. Long recovery time after treatment is common with the thrice-weekly hemodialysis schedule. In one study, recovery time was between two and six hours for 41% of hemodialysis patients and greater than six hours for 27%; recovery time greater than six hours was associated with substantially higher risks of death and hospitalization. In our prospective, observational FREEDOM (Following Rehabilitation, Economics, and Everyday Dialysis Outcome Measurements) study of daily home hemodialysis, recovery time was sharply reduced after 12 months of treatment, from roughly eight hours at baseline to merely one hour in per-protocol analysis. Meanwhile, recovery time after nocturnal hemodialysis may be only minutes in duration. In matched cohort studies, daily home hemodialysis was associated with almost 40% lower risk of death due to withdrawal or cachexia, relative to each of thrice-weekly in-center hemodialysis and peritoneal dialysis. By decreasing recovery time after treatment, frequent hemodialysis can improve the tolerability of dialysis treatment and may reduce the incidence of withdrawal from dialysis.

Quality of Life: Physical Health. Characteristics of poor physical health-related quality of life (HRQoL) include limitations in physical, self-care and social activities; severe bodily pain; frequent tiredness; and low self-rating of physical health. Mean physical HRQoL in hemodialysis patients is much lower than the U.S. general population norm. In both randomized clinical trials and prospective cohort studies, more frequent hemodialysis improves physical HRQoL. More

17

frequent hemodialysis is also associated with improvements in restless legs, especially in patients with severe symptoms, and sleep disturbances, including daytime somnolence.

Quality of Life: Mental Health. Characteristics of poor mental HRQoL include frequent psychological distress, social disability due to emotional problems and low self-rating of mental health. Poorer mental health, as measured by the Kidney Disease Quality of Life Short Form, has been associated with increased risks of both death and hospitalization in hemodialysis patients. Frequent hemodialysis can address depressive symptoms, as shown in our FREEDOM study. More frequent hemodialysis also has led to improvement in overall mental health, including large improvements in vitality and social functioning.

Potential Risks

In spite of the benefits of more frequent hemodialysis on cardiovascular function, health-related quality of life, and treatment tolerability, more frequent hemodialysis, including more frequent hemodialysis performed at home, may introduce specific risks pertaining to vascular access complications, infections, loss of residual renal function and increased burden on caregivers. All forms of hemodialysis, including treatments performed in-center and at home, involve some risks. In addition, there are certain risks unique to treatment in the home environment. Patients differ and not everyone will experience the reported benefits of home or more frequent hemodialysis. Certain risks associated with hemodialysis treatment are increased when performing nocturnal therapy due to the length of treatment time and because therapy is performed while the patient and care partner are sleeping.

Our Competition

The dialysis therapy market is mature, and we face competition from many sources. We believe that our competitive strengths include the quality and ease of use of our products and our history of leveraging innovative technology to deliver high value, clinically flexible solutions.

Home Hemodialysis

The System One is the first portable system indicated for home hemodialysis and is also indicated for home nocturnal hemodialysis in the U.S. We believe the System One's design is unique in terms of product quality and ease of use compared to other products cleared for home use in the U.S. because of its design, portability and avoidance of home modifications. Multiple competitors provide more traditional systems, against which the System One competes in the home hemodialysis market.

Critical Care

The System One is also used in the critical care market. Other providers of products for hemodialysis in the critical care market include Gambro (a subsidiary of Baxter), Fresenius, Nikkiso Co. Ltd., B. Braun Medical, Inc. (B. Braun) and several smaller companies. In addition, multiple competitors provide more traditional systems used in intensive care units.

We believe we compete favorably in terms of product quality and ease of use due to our System One design, portability, drop-in cartridge and use of premixed fluids.

In-Center

Our Medisystems branded bloodlines, needles and other consumables are sold to U.S. in-center providers and compete against products produced by Fresenius, Nipro Medical Corporation, JMS Co. Ltd. and others. Outside the U.S., we face competition from several firms, including B. Braun and Baxter, together with its subsidiary Gambro.

We believe that we compete favorably with a strong Medisystems brand and with respect to product quality, ease of use, cost effectiveness, clinical flexibility and performance.

Services

The U.S. dialysis services industry is highly competitive. A majority of U.S. dialysis centers are operated by the two largest dialysis organizations, DaVita and Fresenius, with the remaining facilities allocated among several mid-sized dialysis organizations and a number of small dialysis organizations and local hospitals.

Intellectual Property

We seek to protect our investment in the research, development, manufacturing and marketing of our products through the use of patent, trademark, copyright and trade secret law. We own rights to a number of patents, trademarks, copyrights, trade secrets and other intellectual property directly related and important to our business both in the U.S. and abroad. We also have domestic and foreign pending patent applications. Any of our trade secrets, know-how or other technology not protected by a patent could be misappropriated, or independently developed by, a competitor and could, under some circumstances, be used to

18

prevent us from further use of such information, know-how or technology. We require our employees, consultants and advisors to execute confidentiality agreements with us. We also require our employees to agree to disclose and assign to us inventions conceived by them during their employment. Similar obligations are imposed upon consultants and advisors performing work for us relating to the design or manufacture of our products. Despite efforts to protect our intellectual property, unauthorized parties may attempt to copy aspects of our products or obtain and use information that we regard as proprietary.

Patents. Our strategy is to develop patent portfolios for our research and development projects. Patents for individual products extend for varying periods of time according to the date a patent application is filed or a patent is granted and the term of the patent protection available in the jurisdiction granting the patent. The scope of protection provided by a patent can vary significantly from country to country.

As of December 31, 2016, we had 137 U.S. and foreign counterpart patents and 52 U.S. and foreign counterpart patents pending. The issued patents and pending patent applications cover, among other things:

•safety technology for automated blood treatments;

• | control and mechanical features aimed at set-up including priming of blood circuits and preparation of fluids including dialysate for hemodialysis and peritoneal dialysis; |

•blood circuit improvements aimed at safety, cost effectiveness and convenience;

•control technology aimed at reliability and safety of blood treatment machines;

•sensor technology including temperature and pressure sensors; and

•administration of peritoneal dialysis.

The approximate expiration periods for our issued patents are as follows:

Expiration | Portion of Patent Portfolio |

Within the next 5 years | 29% |

6-10 years | 26% |

11-15 years | 12% |

16-20 years | 33% |

Hemodialysis technologies have been in existence for over fifty years, and there are thousands of patents held by third parties that relate to dialytic technologies. Collectively, our patents and other intellectual property are important to us, although there is no single patent that is solely responsible for protecting our products. We believe that the duration of our patents is adequate relative to the expected lives of our products.

Product Development

Our product development organization is working to develop innovative technical approaches that address the limitations of current dialysis systems and disposable products. We focus our development innovation on new hardware and disposables that allow for lower cost and higher capability. This includes developing new sensors, software, disposable designs, pump designs, manufacturing techniques, assembly automation, plastic processing technologies, and user interfaces, to name a few of our important development areas. Our development team has skills across the range of technologies required to develop and maintain dialysis systems and products, including filters, tubing sets, mechanical systems, fluids, software and electronics.

We are continually working on enhancements to our product designs to improve ease of use, functionality, reliability and safety and to reduce product cost. We also seek to develop new products that supplement our existing product offerings, such as our peritoneal dialysis system and next-generation critical care system, and intend to continue to actively pursue research and development opportunities for complementary products.

We believe our research and development efforts are critical to our success and continue to make significant investments in our product pipeline. Our research and development expenses were $31.0 million (8% of total revenues), $26.2 million (8% of total revenues) and $22.6 million (8% of total revenues) during 2016, 2015 and 2014, respectively.

Manufacturing

We have significant manufacturing infrastructure dedicated to high-volume plastics disposables production. We have manufacturing facilities in Mexico, Germany and Italy. Manufacturing innovation of process and automation is a critical capability that has contributed to our ability to manufacture high quality, low-cost products. We have designed most of our production automation ourselves. At our facility in Tijuana, Mexico, we perform a number of manufacturing operations relating to our System One equipment and disposables and in-center bloodlines, and we service System One equipment. We manufacture our dialyzer filters at a facility in Germany owned by Asahi and operated by us, and we perform molding activities

19

at our facility in Italy. We complement our internal production capabilities by outsourcing the manufacture of premixed dialysate, needles and some components.

We depend upon a number of single-source suppliers for certain of our raw materials, components and finished goods, including the fiber used in our System One filters, our needles and sterile bags, as well as sterilization services. Finding alternative sources for these raw materials, components, finished goods and sterilization services would be difficult and in many cases entail a significant amount of time, disruption and cost. Where obtaining a second source is more difficult, we have tried to establish supply agreements that better protect our continuity of supply, although we do not have supply agreements with all of our single-source suppliers. Where we have no agreements in place, we work, to the extent economically feasible, to maintain enough inventory of the single-sourced component to allow us to, if needed, satisfy our requirements for the component while we secure an alternative source of supply.

Some of our most critical supply relationships are with Membrana GmbH and Laboratorios PiSA S.A. de C.V.

Membrana is our only supplier of the fiber used in our filters for System One products under an agreement that expires in December 2023, and contractually we cannot obtain an alternative source of fiber for our System One products. While our relationship with Asahi could afford us back-up supply in the event of supply disruptions at Membrana, we do not have the regulatory approvals necessary to use Asahi fiber in our System One cartridge.

Laboratorios PiSA supplies substantially all of our premixed dialysate. Our supply agreement with Laboratorios PiSA extends through December 2019. We have committed to purchase from Laboratorios PiSA a minimum quantity of premixed dialysate over the term of the agreement. While we purchase premixed dialysate from another qualified supplier, any significant disruption in Laboratorios PiSA’s ability to supply premixed dialysate to us would impair our business, at least in the near term.

Government Regulation

In the U.S., numerous laws and regulations govern all the processes by which medical devices are brought to market and, for our NxStage Kidney Care dialysis centers, the manner in which we administer and submit claims for patient care. In the foreign countries in which we market and sell our products, we are subject to local regulations affecting, among other things, design and product standards, packaging and labeling and promotion requirements.

Food and Drug Administration

In the U.S., our products are subject to regulation by the FDA as medical devices. The FDA regulates the design, development, clinical testing, manufacture, labeling, distribution, import and export, sale and promotion of medical devices. Noncompliance with applicable FDA requirements can result in, among other things:

- violation letters;

- fines, injunctions, and civil penalties;

- recall or seizure of products;

- | administrative detention, which is the detention by the FDA of medical devices believed to be adulterated or misbranded; |

- operating restrictions, partial suspension or total shutdown of production;

- failure of the government to grant pre-market clearance or pre-market approval for devices;

- withdrawal of marketing clearances or approvals; and

- criminal prosecution.

Unless an exemption applies, all medical devices must receive either 510(k) clearance or an approved pre-market application (PMA) from the FDA before they may be commercially distributed in the U.S. To obtain a 510(k) clearance for a device, a pre-market notification to the FDA must be submitted demonstrating that the device is substantially equivalent to a legally marketed predicate device. The FDA attempts to respond to a 510(k) pre-market notification within 90 days of submission, but as a practical matter, pre-market clearance can take significantly longer, potentially up to one year or more. The PMA process is much more demanding and uncertain than the 510(k) pre-market notification process and must be supported by extensive clinical, technical and other information, including at least one adequate and well-controlled clinical investigation. The FDA has 180 days from the date of filing to review an accepted PMA, although the review generally occurs over a significantly longer period of time, and can take up to several years.

FDA Regulatory Clearance Status

We currently have all of the regulatory clearances required to market the System One in the U.S. in both the home and critical care markets, all of which have thus far been granted as 510(k) clearances. The FDA has cleared the System One for the treatment, under a physician’s prescription, of renal failure or fluid overload using hemofiltration, hemodialysis and/or

20

ultrafiltration. The FDA has also specifically cleared the System One for both home hemodialysis and home nocturnal hemodialysis use under a physician’s prescription.

We continue to seek opportunities for product improvements and feature enhancements, which will, from time to time, require FDA clearance before market launch. In total, we have received from the FDA 41 product clearances for the System One and related products and 25 product clearances for our Medisystems branded extracorporeal disposable products.

Continuing FDA Regulation

After a device is placed on the market, numerous regulatory requirements apply, including:

- | Quality System Regulations, which require manufacturers to have a quality system for the design, testing, manufacture, packaging, labeling, storage, installation, and servicing of finished medical devices; |

- | labeling regulations, which govern product labels and labeling, prohibit the promotion of products for unapproved, or off-label, uses and impose other restrictions on labeling and promotional activities; |

- | clearance of product modifications that could significantly affect safety or effectiveness or that would constitute a major change in intended use of one of our cleared devices; |

- | medical device reporting (MDR) regulations, which require that manufacturers evaluate and investigate potential adverse events and malfunctions, and report to the FDA if their device may have caused or contributed to a death or serious injury or malfunctioned in a way that would likely cause or contribute to a death or serious injury if it were to recur; |

- | the FDA’s recall authority, whereby it can ask, or under certain conditions order, device manufacturers to recall from the market a product that is in violation of governing laws and regulations; |

- | regulations pertaining to voluntary recalls; |

- | notices of corrections or removals; and |

- | product listing and establishment registration, which helps facilitate FDA inspections and other regulatory action. |

We are registered with the FDA as a medical device manufacturer. The FDA seeks to ensure compliance with regulatory requirements through periodic facility inspections and these inspections may include the manufacturing facilities of our subcontractors.

Foreign Regulation of Medical Devices

We are also subject to regulations in the foreign countries in which we market and sell our products. We currently have limited sales outside of the U.S. Foreign regulations, which may vary substantially from country to country, relate to, among other things, product standards, packaging, labeling and promotion requirements, import restrictions, tariff regulations, duties and tax requirements.

Clearance or approval of our products by regulatory authorities comparable to the FDA, or in the case of the EU the affixing of the CE mark, may be necessary in foreign countries prior to marketing the product in those countries, whether or not FDA clearance has been obtained. The regulatory requirements for medical devices vary significantly from country to country. They can involve requirements for additional testing and may be time consuming and expensive. We cannot provide assurance that we will be able to obtain regulatory approvals in any other markets or be able to affix the CE mark to new products in the EU.

In the specific case of the EU, manufacturers of medical devices are required to conduct an assessment of the conformity of the devices with the Essential Requirements found in Annex I to Council Directive 93/42/EEC of 14 June 1993 concerning medical devices, commonly known as the Medical Devices Directive, and to affix a CE mark to these devices prior to marketing these within the EU. The Essential Requirements govern the quality, safety and performance of the medical devices. The classification of individual medical devices will determine whether the participation by a notified body in the conformity assessment process will be necessary. Notified bodies are private organizations that are licensed by the competent authorities of individual EU Member States to conduct conformity assessment procedures and to verify the conformity of manufacturers and their medical devices with the Essential Requirements. If, where the participation by a notified body is necessary, the outcome of the conformity assessment procedure is positive the notified body will issue a related CE Certificate of Conformity. The manufacturer of the device will then complete the technical file for the medical device and, after having prepared and signed a related Declaration of Conformity, affix the CE mark to the product.

CE Certificates of Conformity have been issued in relation to all of our products that require such certificates and we have affixed a CE mark to these products. However, if we introduce any substantial change to any of our CE marked medical devices in the EU this may require an additional conformity assessment process in relation to the substantial changes and modification or preparation of new CE Certificates of Conformity and Declarations of Conformity.

21

In the EU we must comply with a number of regulatory requirements for products that have been CE marked and placed on the market relating to:

- | registration of medical devices; |

- | pricing and reimbursement of medical devices; |

- | establishment of post-marketing surveillance and adverse event reporting procedures; |

- | field safety corrective actions, including product recalls and withdrawals; |

- | marketing and promotion of medical devices; and |

- | interactions with physicians. |

Failure to comply with these requirements may result in enforcement measures being taken by the competent authorities of the EU Member States. These can include fines, administrative penalties, compulsory product withdrawals, injunctions and criminal prosecution. Such enforcement measures would have an adverse effect on the marketing of our products in the EU and, consequently, on our business and financial position.

Licensure and Certification

Our NxStage Kidney Care dialysis centers must be certified by CMS to receive Medicare payments. In some states, these centers must also secure additional state licenses, permits or certificates of needs. Governmental authorities, primarily state departments of health, periodically inspect our centers to determine if we satisfy applicable federal and state standards and requirements, including the conditions of coverage by the Medicare ESRD program.

Fraud and Abuse Laws

U.S. federal healthcare laws apply when our customers and NxStage Kidney Care dialysis centers submit claims for items or services that are reimbursed under Medicare, Medicaid, or other federally-funded healthcare programs. The principal federal fraud and abuse laws include:

• | the Anti-Kickback Statute, which among other things prohibits the offer or payment of any remuneration for the purpose of inducing or rewarding patient referrals or the order, purchase or recommendation of items or services reimbursable by a federal healthcare program; |

• | the False Claims Act, which prohibits the submission of false or otherwise improper claims for payment to a federally-funded healthcare program or causing such claims to be submitted; and |

• | criminal healthcare fraud statutes that prohibit false statements and improper claims to any third-party payors. |

There are often similar state anti-kickback and false claims laws that apply to state-funded Medicaid and other healthcare programs, as well as to private third-party payors. In addition, the U.S. Foreign Corrupt Practices Act can be used to prosecute companies in the U.S. for arrangements with physicians or other parties outside the U.S. if the physician or party is a government official of another country and the arrangement violates the laws of that country. Sanctions under these federal and state laws may include civil monetary penalties, exclusion of a manufacturer’s products or of a provider’s services from reimbursement under government programs, criminal fines and imprisonment.

Similar laws are increasingly being introduced in the individual European states. The provision of benefits or advantages to physicians to induce or encourage the prescription, recommendation, endorsement, purchase, supply, order or use of medical devices is prohibited. The provision of benefits or advantages to physicians is also governed by the national anti-bribery laws of European states. One such example is the UK Bribery Act. Payments made to physicians in certain EU Member States must also be publicly disclosed. Moreover, agreements with physicians must often be the subject of prior notification and approval by the physician’s employer or competent professional organization or the competent authorities of the individual European states. These requirements are provided in the national laws, industry codes or professional codes of conduct applicable in the European states. Failure to comply with these requirements could result in reputational harm, public reprimands, administrative penalties, fines or imprisonment.

Anti-Kickback and Related Statutes