Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - DST SYSTEMS INC | dstex321231161.htm |

| EX-31.2 - EXHIBIT 31.2 - DST SYSTEMS INC | dstex3121231161.htm |

| EX-31.1 - EXHIBIT 31.1 - DST SYSTEMS INC | dstex3111231161.htm |

| EX-24 - EXHIBIT 24 - DST SYSTEMS INC | dstex241231161.htm |

| EX-23 - EXHIBIT 23 - DST SYSTEMS INC | dstex231231161.htm |

| EX-21 - EXHIBIT 21 - DST SYSTEMS INC | dstex211231161.htm |

| EX-12 - EXHIBIT 12 - DST SYSTEMS INC | dstex121231161.htm |

| EX-10.17.2 - EXHIBIT 10.17.2 - DST SYSTEMS INC | dstex10172123120161.htm |

| EX-10.17.1 - EXHIBIT 10.17.1 - DST SYSTEMS INC | dstex10171123121061.htm |

| EX-10.16.1 - EXHIBIT 10.16.1 - DST SYSTEMS INC | dstex10161123120161.htm |

Use these links to rapidly review the document

United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2016 | |

or | |

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from | to |

Commission file number 1-14036

DST Systems, Inc.

(Exact name of Registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 43-1581814 (I.R.S. Employer identification no.) | |

333 West 11th Street, Kansas City, Missouri (Address of principal executive offices) | 64105 (Zip code) | |

(816) 435-1000

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each Exchange on which registered | |

Common Stock, $0.01 Per Share Par Value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES x NO ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web-site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO x

Aggregate market value of the voting and non-voting stock held by non-affiliates of the Registrant as of June 30, 2016:

Common Stock, $0.01 par value—$3,824,656,457

Number of shares outstanding of the Registrant’s common stock as of January 31, 2017:

Common Stock, $0.01 par value—31,546,703

Documents incorporated by reference: Portions of our Proxy Statement to be filed on or about on March 28, 2017 are incorporated into Part III

DST Systems, Inc. 2016 Form 10-K Annual Report Table of Contents | ||

The brand, service or product names or marks referred to in this Annual Report are trademarks or services marks, registered or otherwise, of DST Systems, Inc. or its consolidated subsidiaries.

2

PART I

Item 1. Business

DST Systems, Inc. is a global provider of technology-based information processing and servicing solutions. References below to “DST,” “the Company,” “we,” “us” and “our” may refer to DST Systems, Inc. exclusively or to one or more of our consolidated subsidiaries. We provide business solutions through a unique blend of industry knowledge and experience, technological expertise and service excellence to clients in the asset management, brokerage, retirement, healthcare and other markets. The Company was formed in 1969. Through a reorganization in August 1995, we are a corporation organized in the State of Delaware.

NARRATIVE DESCRIPTION OF BUSINESS

DST uses our proprietary software applications to provide sophisticated information processing and servicing solutions through strategically unified data management and business processing solutions to clients globally within the asset management, brokerage, retirement, healthcare and other markets. Our wholly-owned data centers provide the secure technology infrastructure necessary to support our solutions.

We manage our business through two operating segments: Financial Services and Healthcare Services. Our investments in equity securities, private equity investments, real estate and certain financial interests have been aggregated into an Investments and Other segment.

In connection with the execution of our strategic plan, which includes focusing on the Financial Services and Healthcare markets, we sold our North American Customer Communications business on July 1, 2016. Additionally, during 2016, our Board of Directors approved a plan for management to divest of our United Kingdom (“U.K.”) Customer Communications business. As a result of this significant shift in the strategic direction of our operations, we have classified the results of the Customer Communications businesses sold and being sold as discontinued operations in our consolidated financial statements for all periods presented. The net after-tax proceeds from the sale are being used in accordance with the Company’s capital plan, including investments in the business, share repurchases, strategic acquisitions, debt repayments and other corporate purposes.

During 2016, we acquired all of the membership interests of Kaufman Rossin Fund Services LLC (“KRFS”), a full-service provider of specialized hedge fund administration services to the global financial community. KRFS’ hedge fund services include accounting and valuation, back-office outsourcing, investor services, treasury services, and customized reporting.

For the year ended December 31, 2016, DST’s operating revenues were $1,474.4 million. Segment operating revenues, as a percentage of consolidated operating revenues (excluding intersegment revenues), were 71.0%, 28.9%, and 0.1% contributed from the Financial Services, Healthcare Services, and Investments and Other segments, respectively.

FINANCIAL SERVICES SEGMENT

Through the Financial Services segment, we provide investor, investment, advisor/intermediary and asset distribution services to companies within the financial services industry. Utilizing our proprietary software applications, we offer our clients information processing solutions to support direct and intermediary sales of mutual funds, alternative investments, securities brokerage accounts and retirement plans. This includes transaction processing; account opening and maintenance; reconciliation of trades, positions and cash; corporate actions; regulatory reporting and compliance functions; and tax reporting. We also support full reporting to investors for confirmations, statements and tax forms, web access, and electronic delivery of documents.

Services are provided either under a remote processing (“Remote”) model or on a business process outsourcing (“BPO”) basis, either directly by DST or through Boston Financial Data Services, Inc. (“BFDS”), our domestic joint venture with State Street Corporation (“State Street”), utilizing our proprietary software applications, including our TA 2000® and TRAC® systems. Our BPO service offerings are enhanced by AWD®, our proprietary workflow software, which is also licensed separately to third parties.

In the United States (“U.S.”), we provide services to mutual funds, brokerage firms, retirement plans and alternative investment funds (such as real estate investment trusts “REITs”). In Australia and the U.K., we license our wealth management platform to provide solutions related to participant accounting and recordkeeping for wealth management, “wrap platforms” and retirement savings (“superannuation”) industries/markets. Our primary customers are funds and fund managers. We also offer investor services on a Remote and BPO basis internationally (U.K., Canada, Ireland and Luxembourg) solely through International

3

Financial Data Services, U.K. (“IFDS U.K.”) and International Financial Data Services, L.P. (“IFDS L.P.”), (collectively, “IFDS”), which are joint ventures with State Street.

Accounts serviced under shareowner recordkeeping arrangements with the mutual fund and alternative investment sponsors are referred to as “registered accounts.” Registered accounts include both tax-advantaged and non tax-advantaged accounts on the books of the transfer agent. We also contract directly with broker/dealers to manage brokerage subaccounts.

We deliver a comprehensive suite of asset servicing, distribution solutions and asset management for open-end mutual funds, closed-end funds, exchange-traded funds and alternative investment funds. Focusing on the needs of small- to medium-sized funds that require a broad set of customizable services, we provide compliance, creative services, medallion distribution, fund administration, fund accounting, legal, tax administration, transfer agency and asset management services.

Our distribution services range from consulting to active wholesaling and marketing, including closed-end funds IPO launch platform services. We also offer products designed to assist clients in meeting the expanding needs associated with distributing U.S. investment products through financial intermediaries.

We serve as the asset manager to proprietary open-end mutual funds, closed-end funds and exchange-traded funds through active management and through the utilization of sub-advisors and index providers. Additionally, we offer data analytics and consulting services in both the U.S. and U.K. to help our clients gain actionable insights into the needs and preferences of their customers.

We typically have multi-year agreements with our clients. Financial Services’ fees are primarily charged to the client based on the number of accounts, participants or transactions processed. For subaccounts, broker/dealers provide a portion of the services directly. As a result, our revenue per account is generally higher for registered accounts than for subaccounts. On a more limited basis, we also generate revenue through asset-based fee arrangements, subscriptions and/or seat licensing and from investment earnings related to cash balances maintained in our full service transfer agency bank accounts.

The Financial Services segment’s largest customer accounted for 10.5% of the segment’s operating revenues in 2016 and the five largest Financial Services customers collectively accounted for 28.0% of the segment’s operating revenues in 2016. Financial Services’ customers in 2016 included our joint ventures with State Street, BFDS (which was the segment’s second largest customer) and IFDS U.K. (which was the segment’s third largest customer). Collectively, these joint ventures accounted for approximately 12.4% of the segment’s operating revenues in 2016.

Sources of new business for the Financial Services segment include: (i) existing clients, particularly with respect to complementary and new products and services, (ii) companies relying on their own in-house capabilities and not using outside vendors, (iii) companies using competitors’ systems, and (iv) new entrants into the markets served by Financial Services. We consider our existing client base to be one of our best sources of new business. We believe that competition in the markets in which the Financial Services segment operates is based largely on price, quality of service, features offered, the ability to handle rapidly changing volumes, response to security and compliance needs, product innovation, and responsiveness. Our competitors are primarily financial institutions and in-house systems. Our financial institution competitors may have an advantage because they can take into consideration the value of their clients’ funds on deposit or under management when pricing their services. We believe there is significant competition in our markets and our ability to compete effectively is dependent in part on access to capital.

HEALTHCARE SERVICES SEGMENT

The Healthcare Services segment uses our proprietary software applications to provide healthcare organizations with pharmacy, healthcare administration, and health outcomes optimization solutions to satisfy their information processing, quality of care, cost management and payment integrity needs. Our healthcare solutions include claims adjudication, benefit management, care management, business intelligence and other ancillary services. The Healthcare Services segment’s five largest customers accounted for 51.4% of segment operating revenues in 2016, including 17.8% from its largest customer. Effective January 2017, two of our Healthcare Services customers began transitioning off of our systems, which is expected to result in lower overall segment revenue growth during 2017 as compared to 2016.

Our healthcare services are marketed to health insurance companies, health plans and benefits administrators. Customers primarily consist of managed care organizations, preferred provider organizations, third-party administrators, dental, vision, and behavioral health organizations operating commercial and government sponsored programs such as the Health Insurance Exchanges that operate under the Patient Protection and Affordable Care Act, Medicare Advantage, Medicare Part D and Medicaid.

4

We compete with other third-party providers and companies that perform their services in-house with licensed or internally developed systems and processes. We believe that we compete effectively in the market due to our ongoing investment in our products and the development of new products to meet the evolving business requirements of our customers.

Our competitors’ healthcare administration and health outcomes optimization solutions are primarily based on complete replacement of a payer’s core system. We believe that a component application approach shifts the focus away from core application replacement to one in which clients have more alternatives for modernization of the business operation. With a component approach, health payer clients can still choose core application replacement if warranted, or adopt component applications that address only those areas of the business that offer the most opportunity of improvement for the customer, resulting in protection of the client’s current IT investment and reduced disruption to its business operation.

Pharmacy Solutions

We use our proprietary software applications, supporting technology and enhanced clinical expertise to provide pharmacy health management solutions supporting commercial, Medicaid and Medicare Part D plans. These services include pharmacy claims administration, pharmacy network solutions, government programs administration, formulary and rebate management, trend control and quality compliance programs, member services, and discount drug card programs. RxNova, our proprietary claims processing system, is a highly scalable and comprehensive system for the administration of pharmacy benefits, prescription claims adjudication, eligibility, pharmacy management, and related activities. This benefit management solution provides substantial flexibility to accommodate varying provider requirements, allows point-of-sale monitoring, and provides control of pharmacy plan benefits with online benefit authorization.

We generally derive revenue from our pharmacy-solutions business on a transactional fee basis. Fees are earned on pharmacy claims processing and payments services, pharmacy and member call center services, formulary and rebate administration, administration or management of clinical programs, pharmacy network management, member and plan web services and management information and reporting.

Healthcare Administration

We use our proprietary software applications to provide medical claim administration services and health plan compliance and revenue integrity services for payers and providers in the domestic healthcare industry. Healthcare administration services are offered on a software license, Remote and BPO basis. Our solutions, combined with our health outcomes optimization solutions described below, are offered as stand-alone component solutions to complement health plans, existing operations or systems, or as an integrated core administration package of solutions.

Claims administration services include claims processing, benefit plan management, eligibility and enrollment management, provider contract administration, mail receipt and processing, imaging/data capture and retention, fulfillment, utilization management, and customer service. Health plan compliance and revenue integrity services include a retrospective review of medical records to accurately capture members’ health status through proper hierarchical condition categories.

Healthcare administration revenues are generally derived from fees charged on a per member/per month basis or transactional basis. We also realize revenue from fixed-fee license agreements that include provisions for ongoing support and maintenance and for additional license payments in the event that usage or members increase.

Health Outcomes Optimization

We also provide health outcomes optimization solutions through the use of our integrated care management and population health analytics applications and professional services for health plans and providers in the domestic healthcare industry. Our Integrated Care Management solution is a real-time, intuitive, workflow-driven solution suite that assists customers to improve member outcomes and manage costs. Our population health technology provides organizations with the ability to measure and manage federal and state required quality management initiatives, provider network quality and efficiency, member health programs, and risk adjustment on an integrated system. In addition to our proprietary systems, we are the exclusive distributor of Johns Hopkins’ Adjusted Clinical Groups (“ACG”), a patient classification system developed by Johns Hopkins University. The ACG System is a software tool that provides health plans the ability to easily identify their at-risk population and stratify them into the optimal care management program for both the member’s needs and the health plan’s goals for that member.

Professional services include business and industry consulting, risk adjustment, compliance and regulatory consulting, behaviorally based interventions, healthcare quality incentive management, medical management (disease, care, and utilization), HEDIS, managed information technology, software engineering, operations process engineering and management consulting.

Health outcomes optimization revenues are generally derived from fees charged based on a per member/per month basis. We also realize revenue from fixed-fee license agreements that include provisions for ongoing support and maintenance and for

5

additional license payments in the event that usage or members increase. Additionally, we derive professional service revenues from fees for implementation services, custom programming and data center operations.

INVESTMENTS AND OTHER SEGMENT

The Investments and Other segment is comprised of our investments in equity securities, private equity investments, real estate and other financial interests. The assets held are primarily passive in nature.

At December 31, 2016, the Investments and Other segment held investments in available-for-sale equity securities with a market value of approximately $180.1 million, including approximately 2.2 million shares of State Street with a market value of $169.6 million based on closing exchange values at December 31, 2016.

We also own partnership interests in certain real estate joint ventures that lease office space to us, certain of our unconsolidated affiliates and unrelated third parties. We also own various office and retail properties, undeveloped land and an underground storage facility.

SOFTWARE DEVELOPMENT AND MAINTENANCE

DST’s software development and maintenance efforts are focused on introducing new products and services, as well as enhancing our existing products and services. The software development, maintenance and enhancements costs, including capitalized software development costs, were $217.3 million, $205.5 million and $171.1 million for the years ended December 31, 2016, 2015 and 2014, respectively.

INTELLECTUAL PROPERTY

We hold U.S. patents, U.S. copyrights and trademarks covering various aspects of the information processing and computer software services and products provided by the Financial Services and Healthcare Services segments. The duration of the patent term is generally 20 years from its earliest application filing date. The patent term is not renewable. The durations of the copyrights depend on a number of factors, such as who created the work and whether he or she was employed by us at the time. The trademark rights generally will continue for as long as we maintain usage of the trademarks. We believe our copyrights are adequate to protect our original works of authorship. We believe that although the patents, trademarks and copyrights related to the segments are valuable, our success primarily depends upon our product and service quality, marketing and service skills. Despite patent, trademark and copyright protection, we may be vulnerable to competitors who attempt to imitate our systems or processes. In addition, other companies and inventors may receive patents that contain claims applicable to our systems and processes.

EMPLOYEES

We had approximately 5,700 employees in the U.S. and approximately 2,700 employees internationally within our continuing operations at December 31, 2016. Additionally, our joint ventures, BFDS, IFDS U.K. and IFDS L.P. had approximately 2,200 employees in the U.S. and 7,000 employees internationally at December 31, 2016. We also had approximately 1,400 employees internationally that are included within our discontinued operations. Except for certain employees of DST Output (Nottingham) Limited, a U.K. subsidiary included within our discontinued operations, none of our employees are represented by a labor union or covered by a collective bargaining agreement. We consider our employee relations to be good.

SEGMENT, GEOGRAPHIC AREA AND OTHER FINANCIAL INFORMATION

This discussion of the business of DST Systems, Inc. should be read in conjunction with, and is qualified by reference to, Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) under Item 7 herein. In addition, the information set forth in the first paragraph and under the headings “Introduction” and “Seasonality” in the MD&A and the segment and geographic information included in Item 8, Note 17 are incorporated herein by reference in partial response to this Item 1.

6

AVAILABLE INFORMATION

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports will be made available free of charge on or through our Internet website (www.dstsystems.com) as soon as reasonably practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission (“SEC”). In addition, our corporate governance guidelines and the charters of the Audit Committee, the Corporate Governance/Nominating Committee, and Compensation Committee of the DST Board of Directors are available at investors.dstsystems.com/govdocs. These guidelines and charters are available in print to any stockholder who requests them. Written requests may be made to the DST Corporate Secretary, 333 West 11th Street, Kansas City, Missouri 64105, and oral requests may be made by calling the DST Corporate Secretary’s Office at (816) 435-8655. An individual may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E. Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet site (http://www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

Item 1A. Risk Factors

In addition to the other information set forth in this report, you should carefully consider the following factors, which could materially affect our business, financial condition or results of operations in future periods. While we believe we have identified and discussed below the key risk factors affecting our business, there may be additional risks and uncertainties not currently known to us or that we currently deem to be immaterial that may adversely affect our business, financial condition, operating results or share price in the future.

Risks Related to Our Business

Trends or events affecting our clients or their industries could decrease the demand for our products and services and the loss of, reduction of business with, or less favorable terms with any of our significant customers could materially harm our business and results of operations.

We derive our revenues from the delivery of products and services to clients primarily in the mutual fund, brokerage, investment management, healthcare, and other financial service (e.g., insurance, banking and financial planning) industries. Demand for our products and services among companies in those industries could decline for many reasons. If demand for our products decreases or any of the industries we serve decline or fail or consolidate, reducing the number of potential clients, our business and our operating results could be adversely affected.

On a consolidated basis, for the year ended December 31, 2016, our five largest customers (excluding BFDS and IFDS, our 50%-owned joint ventures with State Street) accounted for approximately 22.0% of our consolidated operating revenues. For the same period, the Healthcare Services segment’s five largest customers accounted for approximately 51.4% of our revenue in that segment, including 17.8% from its largest customer. Because of our significant customer concentration, particularly in the Healthcare Services segment, our revenue could fluctuate significantly due to changes in economic conditions, the use of competitive products, or the loss of, reduction of business with, or less favorable terms with any of our significant customers, and a delay or default in payment by any significant customer could materially harm our business and results of operations.

Events that adversely affect our clients’ businesses, rates of growth or numbers of customers they serve could decrease demand for our products and services and the number of transactions we process. Events that could adversely affect our clients’ businesses include decreased demand for our customers’ products and services, adverse conditions in our customers’ markets or adverse economic conditions generally. We may be unsuccessful in predicting the needs of changing industries and whether potential customers will accept our products or services. We also may invest in technology or infrastructure for specific customers and not realize additional revenue from such investments. If trends or events do not occur as we expect, our business could be negatively impacted.

7

We depend on information technology, and any failures of or damage to, attack on or unauthorized access to our information technology systems could result in significant costs and reputational damage.

We have developed and maintained, and our businesses depend on, information technology, including elements both internal and external, to record and process a large volume of complex transactions and other data, including personally identifiable information regarding financial and health matters. In certain circumstances, vendors have access to such data in order to assist us with responsibilities, such as producing benefit plan identification cards, maintaining software we license on our own behalf or resell to others, or helping clients comply with anti-money laundering regulations. Any interruptions, delays, breakdowns, or breach, including as a result of cybersecurity breaches or breaches of our environments and procedures or those of our vendors, could result in significant data losses or theft of our or our customers’ intellectual property, proprietary business information or personally identifiable information. In recent years, several health care and financial services firms were victims of computer systems hacking attacks, resulting in the disruption of services to clients, loss or misappropriation of sensitive or private data, and reputational harm. Rapid advances in technology, and the limits and costs of technology, skills and manpower, may prevent us from anticipating, identifying, preventing or addressing all potential security threats and breaches. A cybersecurity breach could negatively affect our reputation as a trusted product and service provider by adversely affecting the market’s perception of the security or reliability of our products or services. In addition, a system breach could result in other negative consequences, including remediation costs, disruption of internal operations, increased cybersecurity protection costs, lost revenues, regulatory penalties, and litigation.

The demand for our products and services could decrease if we do not continually address our clients’ technology and capacity requirements.

Our clients use technology-based products and services in the complex and rapidly changing markets in which they operate. We may not have effective and efficient processes to support the design, set-up, quality assurance, and maintenance activities for the timely implementation of new client services, migration of existing clients onto new or different platforms, and ongoing servicing that meets the needs of the business and clients. We must substantially invest in technology and systems to meet customer requirements for technology and capacity. If we do not meet clients’ technology and capacity requirements in advance of our competitors or if the investments we make are not cost-effective or do not result in successful products or services, our business could be adversely affected.

The success of the information technology transformation initiative will depend on the timing, extent and cost of implementation; performance of third-parties; upgrade requirements; and availability and reliability of the various technologies required to provide such transformation.

We must continually invest in our information technology in order to continually meet our clients’ needs. We are implementing a multi-year information technology transformation initiative intended to reduce operating costs, increase information security, upgrade infrastructure, implement automation, provide access to emerging technologies and position us to take advantage of market opportunities. If we fail to provide an enhanced client experience, our ability to retain and attract clients and to maintain and grow revenues could be adversely affected. Using new and sophisticated technology on a very large scale entails risks. For example, deployment of new software may adversely affect the performance of existing services on our existing platforms and decrease the customer experience. If implementation of our information technology transformation initiative were delayed or costs exceed expected amounts, our margins could be adversely affected and such effects could be material. If the delivery of services expected to be deployed on modernized architecture were delayed due to technological constraints, performance of third-party suppliers, or other reasons, the cost of providing such services could become higher than expected, which could result in higher costs to clients, potentially resulting in decisions to purchase services from our competitors, which would adversely affect our revenues, profitability and cash flow from operations.

We have made and may continue to make acquisitions and divestitures that involve numerous risks and uncertainties.

Our business strategy anticipates that we will supplement internal growth by pursuing acquisitions of complementary businesses. We may be unable to identify suitable businesses to acquire. We compete with other potential buyers for the acquisition of other complementary businesses. Information we obtain about an acquisition target may be limited and there can be no assurance that an acquisition will perform as expected or positively impact our financial performance. Potential acquisitions involve risk, including the risk we would be unable to effectively integrate the acquired technologies, operations and personnel into our business, and the risk that management’s attention and our capital would be diverted from other areas of our business. The anticipated benefits of our acquisitions may not materialize. Future acquisitions or dispositions could result in the issuance of capital stock, incurrence of debt, contingent liabilities or expenses, or write-offs of goodwill and other intangible assets, any of which could harm our financial condition. If we cannot complete acquisitions, our growth may be limited and our financial condition may be adversely affected.

8

In addition, we have divested, and may in the future divest, businesses that are no longer a part of our ongoing strategic plan. These divestitures similarly require significant investment of time and resources, may disrupt our business, distract management from other responsibilities and may result in continued responsibility for the divested business, including through indemnification, for a period of time following the transaction, which could adversely affect our financial results.

If our new investments and business initiatives are not successful, our financial condition and prospects could be adversely affected.

We are investing heavily in our technology to improve existing products and services and add new products and services to address the needs of existing or new clients. Our investments may not lead to successful deployment or increases in the number of accounts or transactions. If we are not successful in creating value from our investments by increasing sales or reducing expenses, our financial condition and prospects could be harmed.

An increase in subaccounting services performed by brokerage firms has and will continue to adversely impact our revenues.

We service open-end and closed-end funds registered under the Investment Company Act of 1940, including mutual funds, exchange-traded funds, interval funds and exchange-listed closed-end funds, as well as private funds, collective investment trusts and other accounts under shareowner recordkeeping arrangements which we refer to as registered accounts. These arrangements are distinguished from broker subaccounts, which are serviced under contract with a broker/dealer. Our clients may adopt the broker subaccount structure. We offer subaccounting services to brokerage firms that perform shareowner subaccounting. As the recordkeeping functions in connection with subaccounting are more limited than traditional shareowner accounting, the fees charged are generally lower on a per unit basis. Brokerage firms that obtain agreements from our clients to use a broker subaccount structure cause accounts currently on our traditional recordkeeping system to convert to our subaccounting system, or to the subaccounting systems of other service providers, which generally results in lower revenues. While subaccounting conversions have generally been limited to our non tax-advantaged mutual fund accounts, such conversions have begun to extend to the tax-advantaged accounts (such as retirement and Section 529 accounts) we service, which could adversely affect our business and operating results.

Consolidation in or among our customers and potential customers could result in a reduction of customers or reduction in use of our services.

Mergers or acquisitions of or consolidations among our customers or between our customers and other entities could reduce the number of our customers and potential customers and result in the discontinuation or reduction in use of our services. This could adversely affect our revenues even if these events do not reduce the aggregate number of customers or the activities of the consolidated entities. Any of these developments could materially and adversely affect our business, financial condition, operating results and cash flows.

Our businesses are subject to substantial competition.

We are subject to intense competition from other established service providers in all industries we serve. Some of our competitors are able to bundle service offerings and offer more appealing pricing structures. Some of our clients, or the clients they serve, may develop, have developed or are developing the in-house capacity to perform the transaction processing and recordkeeping services they have paid us to perform. Additionally, some of our competitors and clients have greater financial and human resources and access to capital than we do.

In the financial and healthcare markets we serve, we compete based on a variety of factors, including investment performance, the range of products offered, brand recognition, business reputation, financial strength, stability and continuity of client and other intermediary relationships, quality of service, and level of fees charged for services. We continue to face market pressures regarding fee levels in certain products and services offered.

Our failure to successfully compete in any of our material operating businesses could have a material adverse effect on our operating results. Competition could also affect the revenue mix of services we provide, resulting in decreased revenues in lines of business with higher profit margins.

9

We may not be able to sustain critical operations and provide essential products and services during system failures or catastrophic events.

Damage to our facilities could impact our operations or financial condition. The performance of our services also depends upon facilities that house central computer operations or operating centers. Significant damage to any of our operating facilities could interrupt the operations at those facilities and interfere with our ability to serve customers. Moreover, in the event of a catastropic event we may not be able to execute our business resumption strategies for data processing and capabilities, and we may not have the ability to recover critical data, programs, applications, and data processing capabilities in a timely manner; any of these could impact our ability to serve our clients.

We operate internationally and are thus exposed to currency fluctuations and foreign political, economic and other conditions that could adversely affect our revenues from or support by foreign operations.

Inherent risks in our international business activities could decrease our international sales and also could adversely affect our ability to receive important support from our international operations, which could have a material adverse effect on our overall financial condition, operating results, and cash flow. These risks include potentially unfavorable foreign economic conditions, political conditions or national priorities, foreign government regulation, potential expropriation of assets by foreign governments, changes in intellectual property legal protections and remedies, the failure to bridge cultural differences, and limited or prohibited access to our foreign operations and the support they provide. We may also have difficulty repatriating any profits or be adversely affected by currency fluctuations in our international business.

Various events may cause our financial results to fluctuate from quarter-to-quarter or year-to-year. The nature of these events might inhibit our ability to anticipate and act in advance to counter them.

We may be unsuccessful in determining or controlling when and whether events occur that could cause varying financial results. Unfavorable results may occur that we did not anticipate or take advance action to address. We incur significant costs to develop products used to service our existing and potential client operations. The timing of these expenses may fluctuate as new client contracts are signed or existing client contracts are renewed, causing our results to vary accordingly. Factors contributing to the variability of our results include increased costs of supplies, increased costs relating to existing and potential client operations, and hiring staff to develop new and existing products. The timing of our fees associated with new and existing client contracts, including changes in recognition as a result of changes in accounting principles, may also cause results to vary from period to period.

Our revenues may decrease due to declines in the levels of participation and activity in the securities markets.

We generate significant revenues from the transaction processing fees we earn for our services. These revenue sources are substantially dependent on the levels of participation and activity in the securities markets. The number of unique securities positions held by investors through our clients and our clients’ customer trading volumes reflect the levels of participation and activity in the markets, which are impacted by market prices and the liquidity of the securities markets, among other factors. We could continue to be negatively impacted by the volatile markets as certain of our fees are tied to the asset bases of our clients. The occurrence of significant market volatility or decreased levels of participation would likely result in reduced revenues and decreased profitability from our business operations. Additionally, we may be exposed to operational or other risks in connection with any systematic failures in the markets, or the default due to market-related failures of one or more counterparties with whom we transact.

We also derive significant revenues from asset management, administration and distribution contracts with clients. Under these contracts, the fees paid to us are based on a variety of factors, including the market value of assets under management (“AUM”), assets under administration (“AUA”) and number of transactions processed. AUM, AUA or the number of transactions processed may decline for various reasons, causing results to vary. Factors that could decrease AUM and AUA (and therefore revenues) include declines in the market value of the assets in the funds (and accounts as applicable) managed, administered and distributed, redemptions and other withdrawals from, or shifts among, the funds (and accounts as applicable) managed, administered and distributed, as well as market conditions generally.

Our revenues may decrease due to changes in asset management, administration and distribution fees and industry trends

The asset management, administration and distribution business is highly competitive and we compete for investors and clients on the basis of factors such as performance, reputation, service, and cost. Underperformance of any of our proprietary and client products, damage to our reputation, or service-related issues could lead to redemptions or terminations. Additionally, the asset management industry has generally been subject to fee compression and asset flows to lower cost products. Such a trend may result in fee compression in asset management, administration and distribution related contracts. The asset management, administration and distribution contracts may be terminated by the parties thereto, and the board of directors or trustees of

10

certain funds may terminate investment management, administration and distribution agreements for any reason and without penalty. The factors and trends described above could have a material adverse effect on revenues.

Investment decisions with respect to cash balances, market returns or losses on investments, and limits on insurance applicable to cash balances held in bank and brokerage accounts, including those held by us and as agent on behalf of our clients, could expose us to losses of such cash balances and adversely affect revenues attributable to cash balance deposit investments.

As part of our transaction processing and other services, we maintain and manage large bank and investment accounts containing client funds, which we hold as agent, as well as operational funds. Our revenues include investment earnings related to client fund cash balances. Our choices in selecting investments, or market conditions that affect the rate of return on or the availability of investments, could have an adverse effect on the level of such revenues. The amounts held in our operational and client deposit accounts could exceed the limits of government insurance programs of organizations such as the Federal Deposit Insurance Corporation and the Securities Investors Protection Corporation, exposing us to the risk of loss. Any substantial loss would have an adverse impact on our business and our financial condition.

Operational errors in the performance of our services or contractual obligations, as well as unknown or undetected defects, could lead to liability for claims, client loss and result in reputational damage.

The failure to properly perform our services or contractual obligations could result in our clients and/or certain of our subsidiaries being subjected to losses including censures, fines, or other sanctions by applicable regulatory authorities, and we could be liable to parties who are financially harmed by those errors. Despite testing, defects or errors may occur in our existing or new services, which could cause us to compromise customer data, lose revenues, lose clients, divert development resources, or damage our reputation, any of which could harm our business.

Our revenues could decrease if client contracts are terminated or fail to renew or if clients renegotiate contracts or utilize our services at lower than anticipated levels.

We derive most of our revenue by selling products and services under long-term contracts, many of which contain terms and conditions based on anticipated levels of utilization of our services. We cannot unilaterally extend the terms of our client contracts when they expire. Contracts can terminate during the term of agreement for various reasons, including through “termination for convenience” clauses in some contracts that enable clients to cancel by written notice. Our revenues could decrease as a result of terminations or non-renewals of client contracts; extensions of client contracts under, or contract re-negotiations resulting in, less favorable terms; or utilization of services at less than anticipated levels.

We are substantially dependent on our intellectual property rights, and a claim for infringement or a requirement to indemnify a client for infringement could adversely affect us.

We have made substantial investments in software and other intellectual property on which our business is highly dependent. Businesses we acquire also often depend on intellectual property portfolios, which increase the challenges we face in protecting our strategic advantage. Any disclosure, loss, invalidity of, or failure to protect our intellectual property could negatively impact our competitive position and, ultimately, our business. Our protection of our intellectual property rights in the U.S. or abroad may not be adequate and others, including our competitors, may use our proprietary technology without our consent. Furthermore, litigation may be necessary to enforce our intellectual property rights, to protect our trade secrets, or to determine the validity and scope of the proprietary rights of others. Such litigation could result in substantial costs and diversion of resources and could harm our business, financial condition, results of operations and cash flows.

To the extent available, we rely on patent, trade secret and copyright laws; however, significant portions of our proprietary intellectual property is not protected by patents. We also utilize nondisclosure and other contractual agreements and security measures to protect our proprietary technology. We cannot guarantee these measures will be effective. Our products and services rely on technology developed by others, including open source software, and we have no control over possible infringement of someone else’s intellectual property rights by the provider of this technology. The owner of the rights could seek damages from us rather than or in addition to the persons who provide the technology to us. We could be subject at any time to intellectual property infringement claims that are costly to evaluate and defend. Our clients may also face infringement claims, allege that such claims relate to our products and services, and seek indemnification from us. Any loss of our intellectual property rights, or any significant claim of infringement or indemnity for violation of the intellectual property rights, or any significant claim of infringement or indemnity for violation of the intellectual property rights of others, could have a material adverse effect on our financial condition, operating results, and cash flows.

11

Our investments in funds and other companies could decline in value.

We hold significant investments in available-for-sale equity securities of other companies, primarily State Street Corporation, and other financial interests that are subject to fluctuations in market prices. A significant decline in the value of our equity investments could have a material adverse effect on our financial condition or operating results. We may not always be able to sell those investments at higher prices than we paid for them or than the value of the consideration used to acquire them.

From time to time we add new investment strategies to our investment product offerings by providing the initial cash investments as “seed capital.” The seed capital investments may decline in value. A significant decline in their value could have a material adverse effect on our financial condition or operating results.

We are a limited partner in various private equity funds and have future capital commitments related to certain private equity fund investments. These investments are illiquid. Generally, private equity fund securities are non-transferable or are subject to long holding periods, and withdrawals from the private equity firm partnerships are typically not permitted. Even when transfer restrictions do not apply, there is generally no public market for the securities. Therefore, we may not be able to sell the securities at a time when we desire to do so. We may not always be able to sell those investments at the same or higher prices than we paid for them. We also participate in joint ventures with other companies. These joint venture investments could require further capital contributions.

We have restrictive covenants in our debt agreements, which may restrict our flexibility to operate our business. If we do not comply with these restrictive covenants, our failure could result in material and adverse effects on our operating results and our financial condition.

Our debt agreements contain customary restrictive covenants, including limitations on consolidated indebtedness, liens, investments, subsidiary investments, and asset dispositions, and require us to maintain certain leverage and interest coverage ratios. Failure to comply with these covenants could result in an event of default that, if not cured or waived, could result in reduced liquidity for the Company and could have a material adverse effect on our operating results and financial condition. In addition, an event of default or declaration of acceleration under one of our debt agreements could result in a cross default under one or more of our other debt agreements, including our financing agreements. This would have a material adverse impact on our liquidity, financial position and results of operation.

Regulatory and Litigation Risks

We and our unconsolidated affiliates are subject to regulation. Any regulatory violations, changes or uncertainties could adversely affect our business.

A number of our businesses are subject to U.S. or foreign regulation, including privacy, licensing, processing, recordkeeping, investment adviser, broker/dealer, retirement, reporting and related regulations. New products and services we plan to offer may also be subject to regulation, either directly or as a downstream provider to customers or clients. Such regulations cover all aspects of our businesses including, but not limited to, sales and trading methods, trade practices among broker/dealers, use and safekeeping of customers’ funds and securities, capital structure of securities firms, net capital, anti-money laundering efforts, healthcare, recordkeeping and the conduct of directors, officers and employees. Any violation of applicable regulations could expose us or those businesses to civil or criminal liability, significant fines or sanctions, damage our reputation, the revocation of licenses, censures, or a temporary suspension or permanent bar from conducting business, which could adversely affect our business or our financial results. Governmental changes, changing interpretation of regulations, and uncertainties surrounding services we provide could increase our costs of business, result in penalties, or diminish business, which could materially and adversely affect our financial results.

The SEC or other regulatory agencies may issue regulations impacting mutual fund service providers, which could adversely affect our business. The Department of Labor (“DOL”) recently issued fiduciary regulations that, if not delayed, repealed or substantially altered in the near future, are likely to impact our business.

The SEC or other regulatory agencies may issue regulations impacting third-party service providers of mutual funds and other fund-types products, such as distributors, administrators, or custodians, (collectively referred to as “mutual funds”), which could adversely affect our business. The SEC may issue additional regulations under the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (“Dodd-Frank Act”) or other legislative authority that would require brokers and financial intermediaries that distribute mutual funds to make more detailed fee disclosures at the point-of-sale. Additionally, brokers and financial intermediaries may become, in some instances, subject to a new DOL-imposed fiduciary standard-of-care that, if applicable, could cause them to alter their methods of distribution, share class structure, and/or wholesaling activities. It is not yet clear what impact they may have on such activities. It is also unclear whether the regulations will be delayed, repealed or substantially altered in the near future. We cannot predict all of the requirements the SEC or FINRA may impose. Regulations that would cause current distribution channels or interest in mutual fund investing to change could decrease the number of

12

accounts on our systems as a result of changes in client offerings or the attractiveness of offerings to customers of our clients. The biggest impact of the fiduciary regulations is expected to fall on brokers and registered investment advisers who give individualized non-discretionary advice in the “retail” marketplace, but discretionary investment managers in the “institutional” space are also expected to be affected, primarily in connection with sales of investment products and services. To the extent that our business units, clients, unaffiliated intermediary partners and retirement plan service providers fit into these categories, this could adversely affect our business and operating results. Additionally, to the extent the Dodd- Frank Act and/or DOL regulations impact the operations, financial condition, liquidity and capital requirements of unaffiliated financial institutions with whom we transact business, those institutions may seek to pass on increased costs, reduce their capacity to transact, or otherwise present inefficiencies in their interactions with us.

Our clients are subject to regulation that could affect our business.

Our clients are subject to extensive regulation, including investment adviser, broker/dealer and privacy regulations applicable to services we provide to the financial services industry and insurance, privacy and other regulations applicable to services we provide to the healthcare industry. Changes in, and any violation by our clients of, applicable laws and regulations (whether related to the services we provide or otherwise) could diminish their business or financial condition and thus their demand for our products and services or could increase our cost of continuing to provide services to such industries. Demand could also decrease if we do not continue to offer products and services that help our clients comply with regulations. For example, our accounts in our Healthcare Services segment are impacted by the Affordable Care Act, including the Health Insurance Marketplace. Changes to the Affordable Care Act may be enacted by Congress in response to the new administration’s stated agenda, and we cannot predict the impact that will have on our customers and their demand for our services.

Our businesses expose us to risks of claims and losses that could be significant and damage our reputation and business prospects.

Our proprietary applications and related consulting and other services include the processing or clearing of financial and healthcare transactions for our clients and their customers and the design of benefit plans and compliance programs. The dollar amount of transactions processed or cleared is vastly higher than the revenues we derive from providing these services. In the event we make transaction processing or operational errors, or mismanage any process, we could be exposed to claims for any resulting processing delays, disclosure of protected information, miscalculations, mishandling of pass-through disbursements or other processes, and failure to follow a client’s instructions or meet specifications. Additionally, we may be subject to claims or liability resulting from a failure of third parties (including regulatory authorities) to recognize the limitations of our role as our clients’ agent or consultant, and we may be subject to claims or liability resulting from fraud committed by third parties. We may be exposed to the risk of counterparty breaches or failure to perform. We may be subject to claims, including class actions, for reimbursements, losses or damages arising from any transaction processing or operational error, or from process mismanagement. Because of the sensitive nature of the financial and healthcare transactions we process, our liability and any alleged damages may significantly exceed the fees we receive for performing the service at issue. Litigation could include class action claims based upon, among other theories, various regulatory requirements and consumer protection and privacy laws that class action plaintiffs may attempt to use to assert private rights of action. Any of these claims and related settlements or judgments could affect our operating results, damage our reputation, decrease demand for our services, or cause us to make costly operating changes.

Risks Related to Corporate Governance or our Equity Securities

We do not control certain businesses in which we have significant ownership.

We invest in joint ventures and other unconsolidated affiliates as part of our business strategy, and part of our net income is derived from our pro rata share of the earnings of those businesses. Despite owning significant equity interests in those companies and having directors on their boards, we do not control their operations, strategies or financial decisions. The other owners may have economic, business or legal interests or goals that are inconsistent with our goals or the goals of the businesses we co-own. Our pro rata share of any losses due to unfavorable performance of those companies could negatively impact our financial results.

13

Some of our joint venture investments are subject to buy-sell agreements, which could, among other things, restrict us from selling our interests even if we were to determine it would be prudent to do so.

We own interests in unconsolidated entities, including Boston Financial Data Services, International Financial Data Services Limited Partnership, International Financial Data Services Limited, and various real estate joint ventures. Our interests in such unconsolidated entities are subject to buy/sell arrangements, which could restrict our ability to sell our interests even if we were to determine it would be prudent to do so. These arrangements could also allow us to purchase the other owners’ interests to prevent someone else from acquiring them and we cannot control the timing of occasions to do so. The businesses or other owners may encourage us to increase our investment in or make contributions to the businesses at an inopportune time.

Various plans, agreements, laws and organizational documents may have anti-takeover effects.

Provisions in our Certificate of Incorporation, Bylaws, certain plans and agreements, and applicable laws could make it more difficult for a party to make a tender offer for our shares or complete a takeover that is not approved by our Board of Directors. The provisions include:

• | super-majority stockholder approval required for certain actions; |

• | specific procedures for stockholders to nominate new directors; |

• | the Board’s authority to issue and set the terms of preferred stock; |

• | various rights of joint venture co-owners, lenders and certain customers and executives in the event of a change in control; |

• | public reporting of ownership and of changes in ownership by stockholders with at least a 5% interest in us; and |

• | legal restrictions on business combinations with certain stockholders. |

Because of contractual commitments, a change in control could affect our operating results and weaken our management retention and incentive tools.

A change in control of the Company could trigger various rights and obligations in service agreements with certain customers and in agreements governing our joint ventures. A change in control could also allow some clients to terminate their agreements with us or to obtain rights to use our processing software. We are parties to joint venture agreements that allow other co-owners to buy our equity interests if we undergo a change in control. Under certain executive equity-based and other incentive compensation awards, benefit programs and employment agreements with our management, a change in control by itself, or an individual’s termination of employment without “cause” or resignation for “good reason” (each as defined in applicable agreements) after a change in control could accelerate funding, payment or vesting of equity grants, as applicable, under such agreements and programs. This accelerated funding, vesting or payment may decrease an employee’s incentive to continue employment with us. We have adopted an executive severance plan which, among other things, provides benefits to participating senior officers and executives who are terminated in connection with a change of control. Certain other executive officers have agreements with us that require us to continue to employ them for three years after a change in control or to pay certain amounts if we terminate their employment without cause or they resign for good reason following a change in control. The executives might not be incented to achieve desired results for the new owners of our business, and the cost of keeping the executives on the payroll might deter potential new owners from acquiring us or hinder new owners from hiring replacement management.

We may not pay cash dividends on our common stock in the future.

Future cash dividends will depend upon our financial condition, earnings and other factors deemed relevant by our Board of Directors. Payment of dividends is subject to applicable laws and to restrictions in applicable debt agreements.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

Our main operating facilities, including our corporate headquarters, are located in Kansas City, Missouri and consist of 1.1 million square feet of office space, of which 54% is owned and 46% is leased, and 162,000 square feet of owned data center space. Additionally, we own an aggregate 222,000 square feet of space consisting primarily of a back-up data center in St. Louis, Missouri and office space in California and the United Kingdom. We lease an aggregate of 697,000 square feet of other office space and production space in North America, India, Thailand, Australia and Canada. Of the 2.2 million square feet of space identified above, the Company leases and subleases approximately 153,000 square feet to third-parties. Approximately 81%, 16% and 3% of the remaining square footage is utilized by the Financial Services, Healthcare Services and Investments and Other segments, respectively. In addition, we also lease approximately 556,000 square feet of other office space and

14

production space in the United Kingdom for operations that are included within our discontinued operations. We also own undeveloped land in Kansas City, Missouri and California and an underground facility with approximately 538,000 square feet in Kansas City, Missouri, of which 497,000 square feet is leased to third parties. Our real estate joint ventures own 2.7 million square feet of real estate, of which 2.2 million square feet is occupied by third parties or is vacant. We believe our facilities are currently adequate for their intended purposes and are adequately maintained.

The following table summarizes the square footage of U.S. real estate facilities wholly-owned by DST or owned through unconsolidated affiliates of DST as of December 31, 2016 (in millions):

DST wholly-owned (1) | Joint venture-owned (2) | ||||

Occupied by DST or unconsolidated affiliates | 0.5 | 0.5 | |||

Occupied by third parties or vacant | 0.2 | 2.2 | |||

Total | 0.7 | 2.7 | |||

_______________________________________________________________________

(1) | Amounts exclude square footage of wholly-owned data centers and an underground facility located below our Kansas City, Missouri data center |

(2) | Amounts exclude a joint venture-owned 1,000 room convention hotel and facilities owned and occupied by BFDS and IFDS |

Item 3. Legal Proceedings

We are involved in various legal proceedings arising in the normal course of our businesses. While the ultimate outcome of such legal proceedings cannot be predicted with certainty, management believes, after consultation with legal counsel, that the final outcome in such proceedings, in the aggregate, would not have a material adverse effect on our consolidated financial condition, results of operations or cash flows.

Item 4. Mine Safety Disclosures

None.

15

Executive Officers of the Registrant

The following list presents certain information with respect to each of our executive officers as of February 28, 2017.

Jonathan J. Boehm, age 56, is our Executive Vice President and Head of our Healthcare businesses. He re‑joined the Company in 1997 after prior service in the early 1980s. Prior to becoming an Executive Vice President managing our Healthcare businesses in 2009, he served as Group Vice President - Mutual Funds Full Service. He is responsible for our Healthcare Services segment, including DST HealthCare Holdings, Inc. and its subsidiaries DST Health Solutions and Argus Health Systems.

Edmund J. Burke, age 56, is our Executive Vice President and President of ALPS. ALPS includes the Corporation’s investment management and asset servicing businesses. ALPS Holdings, Inc. became a wholly‑owned subsidiary of the Company during 2011. Mr. Burke joined ALPS in 1991 and has served as President since 2000. As part of his responsibilities for the ALPS group of companies, Mr. Burke is President and Trustee of Clough Global Long/Short Fund, Clough Global Allocation Fund, Clough Global Equity Fund and Clough Global Opportunities Fund; Trustee of Liberty All‑Star Equity Fund; Director of Liberty All‑Star Growth Fund, Inc., and Chairman of the Board and President of Financial Investors Trust. Each of these funds operates as a registered investment company pursuant to the Investment Company Act of 1940.

Gregg Wm. Givens, age 56, is our Senior Vice President, Chief Financial Officer and Treasurer. He assumed the roles of Chief Financial Officer and Treasurer in January of 2014. He joined the Company in 1996 as an officer and served as Vice President and Chief Accounting Officer from 1999 through 2013.

Stephen C. Hooley, age 53, is our Chairman of the Board, Chief Executive Officer and President. He became Chief Executive Officer on September 12, 2012 and Chairman of the Board in July 2014. He joined the Company in mid‑2009 as President and Chief Operating Officer. He served from 2004 through mid‑2009 as President and Chief Executive Officer of BFDS. He served from 2009 through April 2013 as non‑executive Chairman of BFDS. From 2007 through March 2013, he served as Chief Executive Officer of IFDS L.P.

Vercie L. Lark, age 54, is our Executive Vice President and Head of our Financial Services businesses. He joined the Company as Vice President and Chief Information Officer in June 2010 and assumed his current title in April 2016. Mr. Lark previously served since July 2009 as Vice President and Chief Information Officer of CenturyLink, Inc., a provider of voice, broadband and video services. He had served since 2008 as the Chief Information Officer of Embarq Corporation, which was acquired in 2009 by CenturyLink.

Maria Mann, age 54, is Senior Vice President and Chief Information Officer. She joined the Company in April 2016. From 2011 through April 2016, she served as Chief Technology Officer at JP Morgan Chase and Co., a multinational banking and financial services holding company. She is responsible for our global information technology infrastructure and architecture functions, global information privacy and security, and global information technology sourcing as well as risk and corporate applications.

William Slattery, age 61, is Chief Executive Officer of DSTi Holdings Limited and Chairman of IFDS Ltd. He joined the Company in January 2017. Prior to joining DST, Mr. Slattery was Head of the Investment Servicing business for State Street Europe and held various executive positions at State Street since 2003. Before joining State Street, Mr. Slattery was Managing Director and Head of Global Risk Management at Deutsche Asset Management and Member of the Group Risk Board of Deutsche Bank AG. His earlier career included 23 years at the Central Bank of Ireland, including senior leadership roles with responsibility of Ireland’s International Financial Services Centre and as Deputy Head of Banking Supervision. Mr. Slattery, who has over 30 years in the financial services industry, was a former Chairman of Financial Services Ireland and was a member of the Public Expenditure Review Group.

Mary E. Sweetman, age 53, is Senior Vice President and Chief Human Resources Officer. She joined the Company in June 2013 as a vice president and assumed her current title in March 2014. Prior to joining the Company, she had served since 2007 as Senior Vice President, Human Resources for Furniture Brands International, a home furnishings designer and manufacturer that, following her departure from that company, filed for bankruptcy in September 2013.

Randall D. Young, age 60, became Senior Vice President, General Counsel and Secretary in mid‑2013. Since 2002, he had served as Vice President, General Counsel and Secretary. He joined the Company as a Vice President in 1995.

16

PART II

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The Company’s common stock trades under the symbol “DST” on the New York Stock Exchange (“NYSE”). As of February 13, 2017, there were approximately 35,600 beneficial owners of our common stock.

The following table provides the quarterly prices of, and quarterly cash dividends paid on, the Company’s common stock for the two-year period ended December 31, 2016. Future cash dividends will depend upon financial condition, earnings and other factors deemed relevant by DST’s Board of Directors. Payment of dividends is subject to applicable laws and to restrictions in applicable debt agreements. On January 25, 2017, the DST Board of Directors declared a quarterly cash dividend of $0.35 per share on DST’s common stock. The dividend will be payable on March 10, 2017, to stockholders of record at the close of business on February 24, 2017.

Dividend | High | Low | |||||||||

2015 | |||||||||||

1st Quarter | $ | 0.30 | $ | 109.81 | $ | 91.95 | |||||

2nd Quarter | 0.30 | 125.70 | 109.68 | ||||||||

3rd Quarter | 0.30 | 133.42 | 95.03 | ||||||||

4th Quarter | 0.30 | 124.52 | 105.08 | ||||||||

2016 | |||||||||||

1st Quarter | $ | 0.33 | $ | 111.80 | $ | 97.92 | |||||

2nd Quarter | 0.33 | 120.79 | 106.15 | ||||||||

3rd Quarter | 0.33 | 125.07 | 115.73 | ||||||||

4th Quarter | 0.33 | 117.08 | 94.63 | ||||||||

The prices set forth above do not include commissions and do not necessarily represent actual transactions. The closing price of our common stock on the NYSE on December 31, 2016 was $107.15.

Stock Repurchases

The following table sets forth information with respect to shares of our common stock purchased by us during the quarter ended December 31, 2016.

Period | Total Number of Shares Purchased | Average Price Paid Per Share | Total $ Amount of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Amount That May Yet Be Purchased Under the Plans or Programs | ||||||||||||

October 1 - October 31 | 675,677 | (1) | $ | 111.09 | $ | 74,999,936 | $ | 150,000,077 | ||||||||

November 1 - November 30 | 567 | (1) | 103.47 | — | 150,000,077 | |||||||||||

December 1 - December 31 | 234 | (1) | 107.65 | — | 150,000,077 | |||||||||||

Total | 676,478 | $ | 111.31 | $ | 74,999,936 | $ | 150,000,077 | (2) | ||||||||

_______________________________________________________________________

(1) | For the three months ended December 31, 2016, we purchased, in accordance with the 2015 Equity and Incentive Plan, 1,383 shares of our common stock for participant income tax withholding in conjunction with stock option exercises or from the vesting of restricted stock shares, as requested by the participants or from shares surrendered in satisfaction of option exercise price. These purchases were not made under the publicly-announced repurchase plans or programs, but were allowed by the rules of the Compensation Committee of our Board of Directors. Of these shares, 582 shares were purchased in October 2016, 567 shares were purchased in November 2016, and 234 shares were purchased in December 2016. |

(2) | On June 13, 2016 our Board of Directors authorized a new $300.0 million share repurchase plan. The plan allows, but does not require, the repurchase of common stock in open market and private transactions. The plan does not have an expiration date. We have entered and may enter into one or more plans with our brokers or banks for pre-authorized purchases within defined limits pursuant to Rule 10b5-1 to affect all or a portion of such share repurchases. |

17

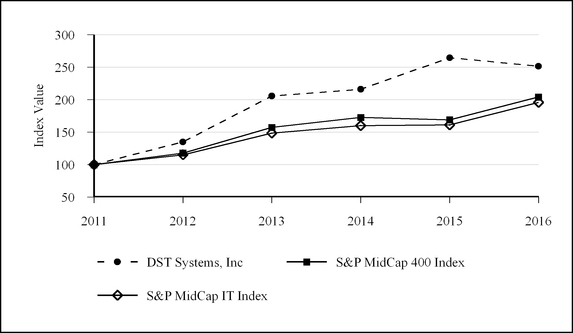

Stock Performance Graph

The following graph shows the changes in value since December 31, 2011 of an assumed investment of $100 in: (i) DST Common Stock; (ii) the stocks that comprise the S&P 400 MidCap index(1); and (iii) the stocks that comprise the S&P 400 MidCap Index - Information Technology Sector(1) (“S&P MidCap IT Index”). The table following the graph shows the dollar value of those investments as of December 31, 2016 and as of December 31 for each of the five preceding years. The value for the assumed investments depicted on the graph and in the table has been calculated assuming that cash dividends, if any, are reinvested at the end of each quarter in which they are paid.

Comparison of Cumulative Five Year Total Return

As of December 31, | |||||||||||||||||||||||

2011 | 2012 | 2013 | 2014 | 2015 | 2016 | ||||||||||||||||||

DST Systems, Inc | $ | 100.00 | $ | 135.05 | $ | 205.56 | $ | 216.01 | $ | 264.52 | $ | 251.44 | |||||||||||

S&P MidCap 400 Index | 100.00 | 117.88 | 157.37 | 172.74 | 168.98 | 204.03 | |||||||||||||||||

S&P MidCap IT Index | 100.00 | 115.21 | 148.38 | 160.13 | 161.11 | 195.70 | |||||||||||||||||

_______________________________________________________________________

(1) | Standard & Poor’s Corporation, an independent company, prepares the S&P 400 MidCap Index and the S&P Midcap IT Index. |

18

Item 6. Selected Financial Data