Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - NAVIENT CORP | d293261dex322.htm |

| EX-32.1 - EX-32.1 - NAVIENT CORP | d293261dex321.htm |

| EX-31.2 - EX-31.2 - NAVIENT CORP | d293261dex312.htm |

| EX-31.1 - EX-31.1 - NAVIENT CORP | d293261dex311.htm |

| EX-23.1 - EX-23.1 - NAVIENT CORP | d293261dex231.htm |

| EX-21.1 - EX-21.1 - NAVIENT CORP | d293261dex211.htm |

| EX-12.1 - EX-12.1 - NAVIENT CORP | d293261dex121.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| ☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

or

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file numbers 001-36228

Navient Corporation

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 46-4054283 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) | |

| 123 Justison Street, Wilmington, Delaware 19801 | (302) 283-8000 | |

| (Address of Principal Executive Offices) | (Telephone Number) | |

Securities registered pursuant to Section 12(b) of the Act

| Title of Each Class |

Name of Exchange on which Listed | |

| Common stock, par value $.01 per share | The NASDAQ Global Select Market | |

| Medium Term Notes, Series A, CPI-Linked Notes due 2017 | The NASDAQ Global Select Market | |

| Medium Term Notes, Series A, CPI-Linked Notes due 2018 | The NASDAQ Global Select Market | |

| 6% Senior Notes due December 15, 2043 | The NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☑ | Accelerated filer ☐ | |||||

| Non-accelerated filer ☐ | Smaller reporting company ☐ | |||||

| (Do not check if a smaller reporting company) | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

The aggregate market value of voting stock held by non-affiliates of the registrant as of June 30, 2016 was $3.8 billion (based on closing sale price of $11.95 per share as reported for the NASDAQ Global Select Market).

As of January 31, 2017, there were 291,008,528 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the proxy statement (the “2017 Proxy Statement”) relating to the Registrant’s 2017 Annual Meeting of Stockholders, currently scheduled to be held on May 25, 2017, are incorporated by reference into Part III of this Annual Report on Form 10-K.

Table of Contents

NAVIENT CORPORATION

Table of Contents

FORWARD-LOOKING AND CAUTIONARY STATEMENTS

This report contains “forward-looking” statements and other information that is based on management’s current expectations as of the date of this report. Statements that are not historical facts, including statements about our beliefs, opinions, or expectations and statements that assume or are dependent upon future events, are forward-looking statements and often contain words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “see,” “will,” “would,” or “target.” Forward-looking statements are subject to risks, uncertainties, assumptions and other factors that may cause actual results to be materially different from those reflected in such forward-looking statements.

For us, these factors include, among others, the risks and uncertainties associated with:

| • | increases in financing costs; |

| • | the availability of financing or limits on liquidity resulting from disruptions in the capital markets or other factors; |

| • | unanticipated increases in costs associated with compliance with federal, state or local laws and regulations; |

| • | changes in the marketplaces in which we compete (including changes in demand or changes resulting from new laws and regulations); |

| • | changes in accounting standards including but not limited to changes pertaining to loan loss reserves and estimates or other accounting standards that may impact our operations; |

| • | adverse outcomes in any significant litigation to which we are a party; |

| • | credit risk associated with our exposure to third parties, including counterparties to hedging or other derivative transactions; and |

| • | changes in the terms of education loans and the educational credit marketplace (including changes resulting from new laws and the implementation of existing laws). |

We could also be affected by, among other things:

| • | unanticipated deferrals in our FFELP securitization trusts that would delay repayment of the bonds beyond their legal final maturity date; |

| • | reductions to our credit ratings, the credit ratings of asset-backed securitizations we sponsor or the credit ratings of the United States of America; |

| • | failures of our operating systems or infrastructure, or those of third-party vendors; |

| • | risks related to cybersecurity including the potential disruption of our systems or potential disclosure of confidential customer information; |

| • | damage to our reputation resulting from cyber-breaches, litigation, the politicization of student loan servicing or other actions or factors; |

| • | failures to successfully implement cost-cutting initiatives and adverse effects of such initiatives on our business; |

| • | delays or errors in converting portfolio acquisitions to our servicing platform; |

| • | changes in law and regulations including but not limited to changes with respect to the student lending or servicing business and financial institutions generally, securitizations or derivatives; |

| • | increased competition from banks and other consumer lenders; |

| • | changes in the general interest rate environment, including the relationship between the relevant money-market index rate and the rate at which our assets are priced; |

1

Table of Contents

| • | our ability to successfully effectuate any acquisitions and other strategic initiatives; |

| • | changes in the demand for asset management and business processing services; |

| • | changes in general economic conditions; and |

| • | the other factors that are described in the “Risk Factors” section of this Annual Report on Form 10-K and in our other reports filed with the Securities and Exchange Commission (“SEC”). |

The preparation of our consolidated financial statements also requires management to make certain estimates and assumptions including estimates and assumptions about future events. These estimates or assumptions may prove to be incorrect and actual results could differ materially. All forward-looking statements contained in this report are qualified by these cautionary statements and are made only as of the date of this report. We do not undertake any obligation to update or revise these forward-looking statements except as required by law.

Definitions for certain capitalized terms used but not otherwise defined in this Annual Report on Form 10-K can be found in the “Glossary” at the end of this report.

Through this discussion and analysis, we intend to provide the reader with some narrative context for how our management views our consolidated financial statements, additional context within which to assess our operating results, and information on the quality and variability of our earnings, liquidity and cash flows.

2

Table of Contents

Our website address is www.navient.com. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to reports filed pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are filed with the Securities and Exchange Commission (the “SEC”). We are subject to the informational requirements of the Exchange Act and file or furnish reports, proxy statements and other information with the SEC. Copies of these reports, as well as any amendments to these reports, are available free of charge through our website at www.navient.com/about/investors/stockholderinfo/secfilings, as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. The public may also read and copy any materials filed by the Company with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Room 1580, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at www.sec.gov.

In addition, copies of our Board Governance Guidelines, Code of Business Conduct (which includes the code of ethics applicable to our Principal Executive Officer, Principal Financial Officer and Principal Accounting Officer) and the governing charters for each committee of our Board of Directors are available free of charge on our website at www.navient.com/about/investors/corp_governance, as well as in print to any stockholder upon request. We intend to disclose any amendments to or waivers from our Code of Business Conduct (to the extent applicable to our Principal Executive Officer or Principal Financial Officer) by posting such information on our website.

Information contained or referenced on the foregoing websites is not incorporated by reference into and does not form a part of this Annual Report on Form 10-K. Further, the Company’s references to the URLs for these websites are intended to be inactive textual references only.

3

Table of Contents

PART I.

| Item 1. | Business |

Overview

Navient is a Fortune 500 company that provides asset management and business processing services to education, health care and government clients at the federal, state, and local levels. We help our clients and millions of Americans achieve financial success through our services and support. Headquartered in Wilmington, Delaware, Navient employs team members in Western New York, Northeastern Pennsylvania, Indiana, Tennessee, Texas, Virginia, and other locations.

Navient holds the largest portfolio of education loans insured or federally guaranteed under the Federal Family Education Loan Program (“FFELP”). We also hold the largest portfolio of Private Education Loans. Navient services its own portfolio of education loans, as well as education loans owned by the United States Department of Education (“ED”), financial institutions and nonprofit education lenders. Navient is one of the largest servicers to ED under its Direct Student Loan Program (“DSLP”). Our data-driven insight, service and innovation support customers on the path to successful education loan repayment.

Navient also provides business processing services to education-related clients, such as guaranty agencies and colleges and universities.

Finally, the company leverages its scale and expertise to provide additional business processing services to a variety of other clients, including federal agencies, state and local governments, regional authorities, courts, hospitals, health care systems and other health care providers, financial service providers, and municipalities.

For all our clients, we aim to improve their financial performance, optimize their operations, and maintain compassionate, compliant service for their customers and constituents.

As of December 31, 2016, Navient’s principal assets consisted of:

| • | $87.7 billion in FFELP Loans, with a net interest margin of 0.85 percent for the year ended December 31, 2016 on a “Core Earnings” basis and a weighted average life of 7.1 years; |

| • | $23.3 billion in Private Education Loans, with a net interest margin of 3.41 percent for the year ended December 31, 2016 on a “Core Earnings” basis and a weighted average life of 6.4 years; |

| • | a leading education loan servicing platform that services loans for more than 12 million DSLP Loan, FFELP Loan and Private Education Loan customers (including cosigners), including 6.2 million customer accounts serviced under Navient’s contract with ED; and |

| • | a leading business processing platform through which we provide services for over 1,000 clients in the education, health care and public sectors. |

Strengths and Opportunities

Navient possesses a number of competitive advantages that distinguish it from its competitors, including:

Large, high quality asset base generating significant and predictable cash flows. At December 31, 2016, Navient’s $111 billion education loan portfolio is 77 percent funded to term and is expected to produce consistent and predictable cash flows over the remaining life of the portfolio. Navient’s $87.7 billion portfolio of FFELP Loans generally bears a maximum 3 percent loss exposure under the terms of the federal guaranty. Navient’s $23.3 billion portfolio of Private Education Loans bears the full credit risk of the borrower and any cosigner. Navient expects that cash flows from its FFELP Loan and Private Education Loan portfolios will significantly exceed future debt service obligations. Our interest earning assets are funded by both secured and unsecured debt. We reduced our unsecured debt outstanding by approximately 9 percent, from $15.1 billion at December 31, 2015 to $13.7 billion as of December 31, 2016.

4

Table of Contents

Efficient and large-scale operating platforms. Navient is the largest servicer of education loans, servicing over $300 billion in education loans for more than 12 million customers. Navient’s inventory of contingent asset recovery receivables is $20.0 billion as of December 31, 2016. We provide services to over 1,000 education, health care and public sector clients. Navient has demonstrated scalable infrastructure with capacity to add volume at a low cost. Our market share and tested infrastructure have enabled expansion to additional clients and asset types.

Superior performance. Navient has demonstrated superior default prevention performance and industry-leading services. The combined portfolio of federal loans serviced by Navient experienced a Cohort Default Rate (“CDR”) that is 31 percent lower than our peers, as calculated from the most recent CDR released by ED in September 2016. We are consistently a top performer in our asset recovery business and deliver superior service to our public and private sector clients. We continually leverage data-driven insights and customer service to identify new ways to add value to our clients.

Commitment to compliance and customer centricity. Navient fosters a robust compliance culture driven by a “customer first” approach. We invest in rigorous training programs, internal and external auditing, escalated service tracking and analysis, and customer research to enhance our compliance and customer service.

Strong capital return. As a result of our significant cash flow and capital generation, Navient expects to return excess capital to stockholders through dividends and share repurchases. In 2016, Navient repurchased 59.6 million shares of common stock (17 percent of common shares outstanding) for $755 million compared with 56.0 million shares of common shares repurchased in 2015 (14 percent of common shares outstanding) for $945 million, fully utilizing our existing share repurchase programs. In December 2016, Navient’s board of directors authorized a new $600 million share repurchase program effective January 1, 2017.

Navient has paid a quarterly dividend of $0.16 per share of common stock since the first quarter of 2015. For the years ended December 31, 2016 and 2015, Navient paid $201 million and $240 million, respectively, in dividends.

Meaningful growth opportunities. In the Asset Management business, Navient will continue pursuing opportunistic acquisitions of FFELP and Private Education Loan portfolios, including refinanced Private Education Loans, and other consumer loans. During the year ended December 31, 2016, Navient acquired $3.7 billion of education loans.

In the Business Processing Services business, Navient will pursue additional growth opportunities, including, among others:

| • | The continued expansion and growth of providing services to state and local governments through our Gila LLC subsidiary (commonly known as Municipal Services Bureau, or MSB). Gila provides receivables management services and account processing solutions for state governments, agencies, court systems, municipalities, toll authorities and financial services entities. Gila expands our customer base in the public sector and leverages our business processing services. |

| • | The continued expansion and growth of providing services to federal agencies. For example, on September 26, 2016, the Internal Revenue Service announced that it plans to begin private collection of certain overdue federal tax debts in the spring of 2017. A Navient subsidiary, Pioneer Credit Recovery, was selected along with three other contractors to implement the new program. |

| • | The continued expansion and growth of providing services to hospitals, health care systems and other health care providers through our Xtend Healthcare subsidiary, a health care revenue cycle management company. Xtend’s services include full revenue cycle outsourcing, accounts receivable management, extended business office support and consulting engagements. Xtend leverages Navient’s asset recovery and business processing capabilities into the health care payments sector. |

| • | The continued expansion and growth of providing services to education related clients. On April 4, 2016, ED published the first part of a two-part request for proposals (“RFP”) related to a new servicing platform |

5

Table of Contents

| for the Direct Student Loan Program. The first part of the RFP focused on screening candidates’ capabilities relative to certain published criteria. In July 2016, Navient was selected as one of three companies eligible to submit responses in the second part of the RFP process. On October 26, 2016, ED published the second part of the RFP for which we submitted our bid on January 9, 2017. |

Navient intends to leverage its large-scale operating platforms, superior and data-driven default prevention and asset recovery performance, operating efficiency and regulatory compliance and risk management infrastructure in growing these businesses and in pursuing other growth opportunities.

Navient’s Approach Helps Education Loan Borrowers Achieve Success

Navient services loans for more than 12 million DSLP Loan, FFELP Loan, and Private Education Loan customers, including 6.2 million customers whose accounts are serviced under Navient’s contract with ED. We help our customers navigate the path to financial success through proactive outreach and innovative, data-driven approaches.

Leveraging four decades of expertise: In our experience, customer success means making steady progress toward repayment and avoiding falling behind on or putting off payments. With customer success and default prevention as our top priorities, we apply data-driven outreach that draws from our more than 40 years of experience. Our strategists employ risk modeling to pinpoint struggling borrowers and deploy resources where needed. By tailoring our approach to each borrower’s unique situation — e.g., recent graduates, students re-entering school, those experiencing hardships or those with student debt but no degree — we help ensure industry-leading outcomes, as evidenced by a default rate that is 31 percent lower than other servicers. Nine times out of 10 when we can reach federal loan customers who have missed payments, we can identify a solution to help them avoid default.

Getting borrowers into the right payment plans: We help customers understand the complex array of federal loan repayment options so they can make informed choices about the plans that are aligned with their financial circumstances and goals. We promote awareness of federal repayment plan options, including Income-Driven Repayment (“IDR), through more than 170 million communications annually, including mail, email, phone calls, videos and text messages. For example, as of December 31, 2016, approximately one in four federal student borrowers and 49 percent of student loan balances serviced by Navient for the government were enrolled in an IDR plan (excluding loan types ineligible for the plans). We also help borrowers understand that options lengthening their repayment term may increase the total cost of their loans, while reminding them that they may pay extra or switch repayment plans at any time.

Leading the industry: Navient is a leader in recommending policy reforms aimed at improving upfront education and simplifying federal loan repayment options — reforms that we believe would make a meaningful difference for millions of Americans with student loans.

In 2009, we pioneered the creation of a loan modification program to help private education loan borrowers needing additional assistance. As of December 31, 2016, $2.6 billion of our Private Education Loans were enrolled in this interest rate reduction program, helping customers through more affordable monthly payments while making progress in repaying their principal loan balance.

We continually make enhancements designed to help our customers, drawing from a variety of inputs including customer surveys, analysis of customer inquiries and complaint data, regulator commentary and website activity. We regularly use customer and employee research panels to gather real-time feedback to inform enhancements underway.

Our Office of the Customer Advocate, established in 1997, offers escalated assistance to customers who request it. We are committed to working with customers and appreciate customer comments, which, combined with our own customer communication channels, help us improve the ways we assist our customers.

6

Table of Contents

We also continue to offer free resources to help customers and the general public build knowledge on personal finance topics, and we make recommendations for reforms to enhance student loan repayment success. We offer Path to Success, a series of interactive financial literacy videos. We also conduct a national research study, Money Under 35, that measures the financial health of Americans ages 22 to 35.

We take seriously our commitment to serve military customers and have developed a best-in-class approach to assist them. Navient was the first student loan servicer to launch a dedicated military benefits customer service team, website (Navient.com/military), and toll-free number. Navient’s military benefits team offers a single point of contact for all calls from service members and their families to help them learn about and access the benefits designed for them, including interest rate benefits, deferment and other options.

Business Segments

We have three primary reportable business segments: FFELP Loans, Private Education Loans and Business Services. A fourth segment — Other — primarily consists of financial results of our holding company, including activities related to repurchases of debt, our corporate liquidity portfolio, unallocated overhead and regulatory-related costs. Each of these business segments are discussed below.

FFELP Loans Segment

In the FFELP Loans segment, we acquire and finance FFELP Loans. Although FFELP Loans are no longer originated, we continue to pursue acquisitions of FFELP Loan portfolios. These acquisitions leverage our servicing scale and generate incremental earnings and cash flow. In this segment, we generate revenue primarily through net interest income on the FFELP Loan portfolio (after provision for loan losses). This segment is expected to generate significant amounts of earnings and cash flow as the portfolio amortizes.

We are currently the largest holder of FFELP Loans. Navient’s portfolio of FFELP Loans as of December 31, 2016 was $87.7 billion and we anticipate that this FFELP Loan portfolio will have an amortization period in excess of 20 years and a 7-year remaining weighted average life. Navient’s goal is to maximize and optimize the timing of the cash flows generated by its FFELP Loan portfolio. Navient also seeks to acquire FFELP Loan portfolios from third parties to add net interest income and servicing revenue. During the year ended December 31, 2016, Navient acquired $3.5 billion of FFELP Loans. FFELP Loans are insured or guaranteed by state or not-for-profit agencies and are protected by contractual rights to recovery from the United States pursuant to guaranty agreements among ED and these agencies. These guaranty agreements generally cover at least 97 percent of a FFELP Loan’s principal and accrued interest for loans disbursed. For more discussion of the FFELP and related credit support mechanisms, see Appendix A “Description of Federal Family Education Loan Program.”

As a result of the long-term funding strategy used for our FFELP Loan portfolio and the insurance and guarantees provided on these loans, the portfolio generates consistent and predictable cash flows. As of December 31, 2016, approximately 81 percent of the FFELP Loans held by Navient were funded to term with non-recourse, long-term securitization debt.

The Higher Education Act of 1965 (“HEA”) continues to regulate every aspect of FFELP Loans, including ongoing communications with borrowers and default aversion requirements. Failure to service FFELP Loans properly could jeopardize the insurance, guarantees and federal support on these loans. The insurance and guarantees on Navient’s existing FFELP Loans were not affected by the termination of FFELP originations.

Private Education Loans Segment

In this segment, we acquire, finance, and service our Private Education Loans. Private Education Loans primarily bridge the gap between the cost of higher education and the amount funded through financial aid, federal loans. or students’ and families’ resources. They also allow borrowers to refinance existing education

7

Table of Contents

loans at a lower rate. We pursue acquisitions of Private Education Loan portfolios. These acquisitions leverage our servicing scale and generate incremental earnings and cash flow. In this segment, we generate revenue primarily through net interest income on the Private Education Loan portfolio (after provision for loan losses). This segment is expected to generate significant amounts of earnings and cash flow as the portfolio amortizes.

We are currently the largest holder of Private Education Loans. Navient’s portfolio of Private Education Loans as of December 31, 2016 was $23.3 billion and we anticipate that this Private Education Loan portfolio will have an amortization period in excess of 20 years and a 6-year remaining weighted average life. Navient’s goal is to maximize and optimize the timing of the cash flows generated by its Private Education Loan portfolio. As of December 31, 2016, approximately 61 percent of the Private Education Loans held by Navient were funded to term with non-recourse, long-term securitization debt.

Unlike FFELP Loans, the holder of a Private Education Loan bears the full credit risk of the borrower and any cosigner. Navient believes the credit risk of the Private Education Loans it owns is well managed through the rigorous underwriting practices and risk-based pricing applied when the loans were originated, the continued high levels of qualified cosigners, our internal servicing and risk mitigation practices, and our careful use of forbearance and loan modification programs. Navient believes that these elements and practices reduce the risk of payment interruptions and defaults on its Private Education Loan portfolio.

Business Services Segment

Our Business Services segment generates revenue from business processing services related to servicing, asset recovery and other business processing activities. Within this segment, we generate revenue primarily through servicing our FFELP Loan portfolio as well as servicing education loans for Guarantors of FFELP Loans and other institutions, including ED. We provide asset recovery services for loans and receivables on behalf of Guarantors of FFELP Loans and higher education institutions. In addition, we provide asset recovery and other business processing services for federal, state, court, and municipal clients, public authorities, and health care organizations.

We provide business processing services for over 1,000 clients, working with a broad spectrum of services and asset classes. This market is highly fragmented and provides attractive organic growth opportunities. As of December 31, 2016, Navient had an outstanding inventory of asset recovery receivables of approximately $20.0 billion, of which $10.1 billion was attributable to asset classes unrelated to education loans. Non-education related asset recovery revenues increased 77 percent, from $99 million in 2015 to $174 million in 2016.

Federal Education Loan Related Revenues

In 2016, federal education loan (FFELP and ED) related revenues in the Business Services segment accounted for 80 percent of total Business Services segment revenues compared with 87 percent in 2015. Total Business Services segment revenues were $1.01 billion for the year ended December 31, 2016, compared to $1.02 billion for the year ended December 31, 2015.

Navient is currently the largest servicer and collector of loans made under the FFELP program, and the majority of our income has been derived, directly or indirectly, from our portfolio of FFELP Loans and the servicing and asset recovery we have provided for Guarantors and third-party owners of FFELP Loans. In 2010, Congress passed legislation ending the origination of education loans under FFELP. The terms and conditions of existing FFELP Loans were not affected by this legislation. We anticipate that the revenue we earn from providing servicing and asset recovery services on FFELP Loans will decline over time.

| • | Servicing revenues from the FFELP Loans we own represent intercompany charges to the FFELP Loans segment at rates paid to us by the securitization trusts which own the loans. These fees are contractually the first payment priority of the trusts after the payment of the trustee fees and exceed the actual cost of servicing the loans. Intercompany loan servicing revenues declined to $389 million in 2016 from $427 million in 2015. Intercompany loan servicing revenues will continue to decline as our FFELP Loan portfolio amortizes. |

8

Table of Contents

| • | In 2016, we earned account maintenance fees on FFELP Loans serviced for Guarantors of $21 million, down from $33 million in 2015. These fees will continue to decline as the underlying FFELP Loan portfolio serviced for Guarantors amortizes. |

| • | As of December 31, 2016, we provide asset recovery (default aversion, post-default collections and claims processing) to 11 of the 26 Guarantor agencies that serve as intermediaries between the U.S. federal government and FFELP lenders and are responsible for paying the claims made on defaulted loans. In 2016, asset recovery revenue from Guarantor clients totaled $194 million, compared to $209 million the prior year. As FFELP Loans are no longer originated, these revenues will decline over time unless we add additional Guarantor clients. The rate at which these revenues will decrease has also been affected by the Bipartisan Budget Act (the “Budget Act”) enacted on December 26, 2013 and effective on July 1, 2014, which reduced the amount to be paid to Guarantor agencies for assisting customers to rehabilitate their defaulted FFELP Loans under Section 428F of the HEA. This aspect of the Budget Act reduced our revenue by approximately $79 million in 2015 compared to 2014. |

Since 2009 when we were selected through a competitive bidding process, Navient has been one of four TIVAS that provides loan servicing for federal loans owned by ED. This contract has been extended through 2019. Under the terms of the contract extension, the allocation of new borrower volume is determined twice each year based on the relative performance of the servicers on five metrics: borrowers in current repayment status (30 percent), borrowers more than 90 but less than 271 days delinquent (15 percent), borrowers 271 days or more but less than 360 days delinquent (15 percent), a survey of borrowers (35 percent), and a survey of ED personnel (5 percent). Under this servicing contract as of December 31, 2016, we service approximately 6.2 million accounts or $197.0 billion in loans. We earned $151 million of revenue under the contract for the year ended December 31, 2016. We continually strive to help our customers succeed and seek to improve on the performance metrics that determine the allocation of new accounts under the servicing contract with ED.

On April 4, 2016, ED published the first part of a two-part RFP related to a new servicing platform for the Direct Student Loan Program. The first part of the RFP focused on screening candidates’ capabilities relative to certain published criteria. In July 2016, Navient was selected as one of three companies eligible to submit responses in the second part of the RFP process. On October 26, 2016, ED published the second part of the RFP. On January 9, 2017, Navient submitted its bid for ED’s single servicing solution contract. We have been informed that one of the two other bidders filed a bid protest in relation to this RFP on January 5, 2017.

Other Segment

Our Other segment primarily consists of activities of our holding company, including the repurchase of debt, our corporate liquidity portfolio, unallocated overhead and regulatory-related costs. We also include results from certain smaller wind-down operations within this segment.

Employees

At December 31, 2016, we had 6,773 employees. None of our employees are covered by collective bargaining agreements.

Spin-Off of Navient

On April 30, 2014, the spin-off of Navient from SLM Corporation (the “Spin-Off”) was completed and Navient became an independent, publicly traded company focused on asset management and business processing services. The separation was completed through the distribution of 100 percent of the outstanding shares of Navient common stock, on the basis of one share of Navient common stock for each share of SLM Corporation common stock. SLM Corporation continues operation as a separate publicly traded company and includes Sallie Mae Bank.

Due to the relative significance of Navient to SLM Corporation prior to the Spin-Off, for financial reporting purposes, Navient is treated as the “accounting spinnor” and therefore is the “accounting successor” to SLM

9

Table of Contents

Corporation as constituted prior to the Spin-Off, notwithstanding the legal form of the Spin-Off. Since Navient is the accounting successor, the historical financial statements of SLM Corporation prior to the Spin-Off are the historical financial statements of Navient. As a result, the GAAP financial results reported in this Annual Report on Form 10-K include the historical financial results of SLM Corporation prior to the Spin-Off on April 30, 2014 (i.e., such consolidated results include our asset management and business processing services business and the consumer banking business associated with Sallie Mae Bank (“SLM BankCo”)) and reflect the deemed distribution of SLM BankCo to SLM Corporation’s stockholders on April 30, 2014.

The following table shows the condensed balance sheet of SLM BankCo that the financial statements of Navient reflect as a shareholder distribution on April 30, 2014:

| (Dollars in millions) |

April 30, 2014 | |||

| Assets |

||||

| FFELP Loans, net |

$ | 1,380 | ||

| Private Education Loans, net |

7,204 | |||

| Investments |

139 | |||

| Cash and cash equivalents |

2,170 | |||

| Other assets |

883 | |||

|

|

|

|||

| Total assets |

$ | 11,776 | ||

|

|

|

|||

| Liabilities |

||||

| Short-term borrowings |

$ | 6,491 | ||

| Long-term borrowings |

2,750 | |||

| Other liabilities(1) |

825 | |||

|

|

|

|||

| Total liabilities |

10,066 | |||

|

|

|

|||

| Equity |

||||

| Preferred stock |

||||

| Series A |

165 | |||

| Series B |

400 | |||

| Common equity |

1,145 | |||

|

|

|

|||

| Total equity(2) |

1,710 | |||

|

|

|

|||

| Total liabilities and equity |

$ | 11,776 | ||

|

|

|

|||

| (1) | “Other liabilities” include net income tax liabilities of $383 million, which were presented as net income tax assets within “Other assets” on the consolidated financial statements of Navient. |

| (2) | In addition to the $1,710 million of consumer banking business net assets distributed, we also removed $41 million of goodwill from our balance sheet as required under Accounting Standards Codification (“ASC”) 350, “Intangibles – Goodwill and Other,” in connection with the distribution. This goodwill was allocated to the consumer banking business based on relative fair value. This total of $1,751 million is the amount that appears on our consolidated statement of changes in stockholders’ equity in connection with the deemed distribution of the consumer banking business. |

In connection with the Spin-Off, three public exchange-traded senior unsecured notes listed on NASDAQ Stock Market LLC and originally issued by SLM Corporation (and its predecessors in interest) remained obligations of Navient. These notes are referred to as (a) Medium Term Notes, Series A, CPI-Linked Notes due 2017, (NASDAQ: OSM / CUSIP: 63938C 207), (b) Medium Term Notes, Series A, CPI-Linked Notes due 2018 (NASDAQ: ISM / CUSIP: 63938C 306), and (c) 6% Senior Notes due December 15, 2043 (NASDAQ: JSM / CUSIP: 63938C 405). The notes are referred collectively as the “Exchange-traded Notes.” Navient’s status as the successor to the original issuer of these notes has been previously reported. On March 29, 2016, the Company filed Form 8-A with the SEC to reflect the transfer of the Nasdaq listing of the Exchange-traded Notes to the Company in connection with the Spin-Off and the Merger, pursuant to Section 12(b) of the Securities Exchange Act of 1934, as amended. In December of 2016, at the request of Nasdaq, the Company changed the CUSIP numbers on each of the Exchange-traded Notes, which change became effective on January 17, 2017. The new CUSIP numbers for each notes are reflected in the disclosure above.

10

Table of Contents

Supervision and Regulation

The Dodd-Frank Act

The Dodd-Frank Act was adopted to reform and strengthen regulation and supervision of the U.S. financial services industry. The Dodd-Frank Act contains comprehensive provisions that govern the practices and oversight of financial institutions (including large non-bank financial institutions) and other participants in the financial markets. It imposed significant regulations, additional requirements and oversight on almost every aspect of the U.S. financial services industry, including increased capital and liquidity requirements, limits on leverage and enhanced supervisory authority. Some of these provisions apply to Navient and its various businesses and securitization vehicles.

The Consumer Financial Protection Act established the Consumer Financial Protection Bureau (“CFPB”), which has broad authority to write regulations under federal consumer financial protection laws and to directly or indirectly enforce those laws and examine financial institutions for compliance. The CFPB is authorized to impose fines and provide consumer restitution in the event of violations, engage in consumer financial education, track consumer complaints, request data and promote the availability of financial services to underserved consumers and communities. It has authority to prevent unfair, deceptive or abusive practices by issuing regulations that define the same or by using its enforcement authority without first issuing regulations. Since its creation, the CFPB has been active in its supervision, examination and enforcement of financial services companies, most notably bringing enforcement actions, imposing fines and mandating large refunds to customers of several large banking institutions, auto financing companies and debt collection companies. The CFPB has filed a lawsuit against Navient alleging several unfair, deceptive or abusive practices, and other violations of consumer protection statutes.

The Dodd-Frank Act also authorizes state officials to enforce regulations issued by the CFPB and to enforce the Dodd-Frank Act’s general prohibition against unfair, deceptive and abusive practices. The Attorneys General of the State of Illinois and the State of Washington also filed lawsuits against Navient and some of its subsidiaries containing similar alleged violations of consumer protection laws as the CFPB lawsuit.

Regulatory Outlook

In general, the number and scope of regulatory and enforcement actions in 2015 and 2016, as well as the amounts of fines and penalties levied against financial institutions, were significant. The types and numbers of class and stockholder derivative actions arising from allegations of violations of consumer protection and regulatory provisions also continued to increase. A number of prominent themes appear to be emerging from these actions:

| • | The number and configuration of regulators bringing actions often adds to the complexity, cost and unpredictability of timing for resolution of particular regulatory issues. |

| • | The regulatory compliance and risk control structures of financial institutions subject to enforcement actions are frequently cited, regardless of whether past practices have been changed, and enforcement orders have often included detailed demands for increased compliance, audit and board supervision, as well as the use of third-party consultants or monitors to recommend further changes or monitor remediation efforts. |

| • | Issues first identified with respect to one consumer product class or distribution channel are often applied to other product classes or channels. |

Navient is subject to oversight from several regulatory entities. We expect that the regulators overseeing our businesses will continue to be active and that consumer protection regulations, standards, supervision, examination and enforcement practices will continue to evolve in both detail and scope. This evolution has added and may continue to significantly add to Navient’s compliance, servicing and operating costs. We have invested

11

Table of Contents

in compliance through multiple steps including realignment of Navient’s compliance management system to a servicing, collections and business services business model rather than a loan originations business model; dedicated compliance resources for certain topics (such as the Servicemembers Civil Relief Act (“SCRA”); the Telephone Consumer Protection Act (“TCPA”); unfair, deceptive, or abusive acts and practices (“UDAAP”); and third-party vendor management) to focus on regulator and consumer expectations; formation of business support operations to enhance risk, control and compliance functions in each business area; additional regulatory training for front-line employees to ensure obligations are understood and followed during interactions with customers as well as additional regulatory training for our board of directors to enhance their ability to oversee the Company’s risk framework and compliance as it and the regulatory environment changes; expanded oversight of our incentive compensation programs; and expanded oversight and analysis of complaint trends to identify and remediate if necessary, areas of potential consumer harm.

While current operations and compliance processes may or may not satisfy evolving regulatory standards, they cannot provide assurance that past practices or products will not be the focus of examinations, inquiries or lawsuits.

As described in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Risk Management,” Navient has implemented a coordinated, formal enterprise risk management system aimed at reducing business and regulatory risks.

Listed below are some of the most significant recent and pending regulatory changes that have the potential to affect Navient.

Consumer Financial Protection Bureau. The CFPB has oversight of the private education loan industry as well as education loan servicers. The CFPB has been active in the education loan industry and undertook a number of initiatives in recent years relative to the private education loan market and education loan servicing, including:

| • | In February 2013, the CFPB published a notice soliciting information on potential options to offer more affordable repayment options to borrowers having difficulty repaying their private education loans. Based on the more than 28,000 comments received, on May 8, 2013, the CFPB published a report highlighting the ways in which private education loan debt can be a roadblock to financial soundness for consumers. The report analyzes the impact of private education loan burdens on the broader economy, assesses recent actions of policymakers in the education loan market and discusses policy options put forth by the public regarding private education loans. The report proposes a number of considerations for policymakers and market participants, such as refinancing relief and monthly payments more closely correlated with a borrower’s debt-to-income ratio. For a discussion on Navient’s approach to helping its customers, see “— Navient’s Approach to Helping Education Loan Borrowers Achieve Success” above. |

| • | On December 3, 2013, the CFPB issued a final rule defining larger participants of the education loan servicing market. The rule, which became effective on March 1, 2014, allows the CFPB to federally supervise certain nonbank education loan servicers for the first time. Under the final rule, the CFPB has supervisory authority over any nonbank education loan servicer that services more than one million borrower accounts, including accounts for both private and federal education loans. Our education loan servicing subsidiaries are subject to this oversight. The CFPB’s supervision includes gathering reports, conducting examinations for compliance with federal consumer financial laws and taking enforcement actions as appropriate. |

| • | On October 16, 2014, the Student Loan Ombudsman within the CFPB submitted his annual report based on private education loan inquiries and complaints received through the CFPB portal from October 1, 2013 through September 30, 2014. The CFPB does not seek to resolve or substantiate the inquiry or complaint but merely provides a gateway between the consumer and the lender or servicer to attempt to address consumer concerns. The Dodd-Frank Act created the Student Loan Ombudsman within the CFPB to receive and attempt to informally resolve inquiries about private education loans. The Student Loan |

12

Table of Contents

| Ombudsman reports to Congress annually on the trends and issues that he identifies through this process. The report offers analysis, commentary and recommendations to address issues reported by consumers. |

| • | On May 14, 2015, the CFPB issued a Request for Information (“RFI”) about student loan servicing practices. The RFI identified a number of potential systemic problems with student loan servicing, and sought public comment from market participants regarding issues that the CFPB believe were identified through consumer complaints including: (1) delays in payment posting, which can result in increased accrued interest; (2) application of overpayments across all loans, instead of to the loans with the highest interest rates; (3) application of partial payments in a manner that maximizes late fees; (4) failure to correct payment processing or other errors in a timely fashion; (5) lost paperwork submitted to process applications for forbearance or alternative payments plans; and (6) issues related to servicing transfers, including failure to notify borrowers of servicing transfers, interruptions in receiving billing statements and other communications, and imposition of late fees when borrowers send payments to their prior servicers. |

| • | In October 2015, the Student Loan Ombudsman within the CFPB issued its annual report analyzing complaints submitted by consumers with student loans from October 1, 2014 through September 30, 2015. This report highlighted problems experienced by student loan borrowers with older federal student loans made by private lenders. Borrowers continued to submit complaints describing servicing and debt collection practices that create barriers to enroll in alternative repayment plans, including income-driven repayment plans for borrowers with federal loans. The Ombudsman noted that private student loan borrowers report that they encounter servicing problems, including lack of access to timely and accurate information on availability or eligibility criteria to enroll in alternative repayment programs. Additionally, the Ombudsman discussed analysis from a voluntary request sent by the Bureau’s Student Loan Ombudsman to certain market participants, asking for data about loans originated under FFELP and held by private investors. |

| • | In April 2016, the CFPB released a set of prototype disclosures (“Payback Playbook”) in conjunction with an RFI seeking information about how to best provide borrowers with information about their repayment options. The proposal, if implemented, would require servicers to provide personalized repayment options to borrowers. The submissions to this request were intended to assist policymakers and market participants when considering potential options to supplement or revise written communications in such a way to reduce defaults, improve borrower outcomes, and spur innovation. As a result of this RFI, the CFPB released a revised prototype Payback Playbook that was provided to ED in January 2017. This revised proposal would provide borrowers in good standing with personalized information about their current repayment plan and two alternatives. Struggling borrowers would receive information about their current plan and one alternative option that offers the lowest available monthly payment and customized instructions on how to enroll in that option. |

| • | On October 17, 2016, the Student Loan Ombudsman issued his 2016 Annual Report analyzing complaints submitted by consumers from September 1, 2015 through August 31, 2016. This report highlighted debt collection and servicing issues experienced by borrowers who had defaulted in the federal loan program. Borrowers are able to regain good standing (or “rehabilitate”) by making nine payments within a 10-month period. However, the Ombudsman estimates that 1 in 3 of these rehabilitated borrowers will re-default within two years due to problems accessing and obtaining income-driven repayment plans. This report also stated that defaulted borrowers reported complaints about debt collectors setting incorrect monthly payment amounts and failing to apply payments toward the loan rehabilitation process, and both collectors and servicers failing to communicate when a borrower’s loan is transferred out of default, or failing to communicate consistent information. In coordination with the release of this report, the CFPB also sent a voluntary information request to student loan servicers seeking information about how previously-defaulted borrowers perform over time. |

| • | In October 2016, the CFPB also revised the education loan examination procedures, incorporating information it gathered from its three years of supervisory and enforcement work, reflecting its revised supervisory priorities. |

13

Table of Contents

Debt Collection Supervision. Consistent with the authority granted to it under the Dodd-Frank Act, the CFPB also maintains supervisory authority over larger consumer debt collectors. On October 24, 2012, the CFPB issued its Larger Participant rule and examination procedures that allow the agency to federally supervise larger consumer debt collectors. The rule, which became effective January 2, 2013, defines larger participants as third-party debt collectors, debt buyers and collection attorneys with more than $10 million in annual receipts resulting from consumer debt collection. Under the rule, Navient’s collection subsidiaries are considered larger participants and are subject to supervision. In July 2016, the CFPB proposed new rules that would impose drastic changes to the debt collection industry generally. Under the proposals currently under consideration, debt collectors would, among other things, be required to limit communications attempts with borrowers, provide enhanced disclosure of debt details, and make it easier to dispute the debt. When responding to disputes, collectors would be prohibited from continuing to pursue debt without sufficient evidence. These requirements and restrictions would follow the debt if it were sold or transferred. The issuance of the CFPB’s rules does not preempt the various and varied levels of state consumer and collection regulations to which the activities of Navient’s subsidiaries are currently subject. Navient also utilizes third-party debt collectors to collect defaulted and charged-off education loans and will continue to be responsible for oversight of their procedures and controls.

Oversight of Derivatives. The Dodd-Frank Act created a comprehensive new regulatory framework for derivatives transactions, to be implemented by the Commodity Futures Trading Commission (“CFTC”), other prudential regulators and the SEC. This framework, among other things, subjects certain swap participants to new capital and margin requirements, recordkeeping and business conduct standards and imposes registration and regulation of swap dealers and major swap participants. The scope of potential exemptions continues to be defined through agency rulemakings. Even where Navient or a securitization trust sponsored by Navient qualifies for an exemption, many of its derivatives counterparties are subject to the new capital, margin and business conduct requirements and therefore Navient’s business may be impacted. Where Navient or the securitization trusts it sponsors do not qualify for an exemption, Navient or an existing or future securitization trust sponsored by Navient may be unable to enter into new swaps to hedge interest rate or currency risk or the costs associated with such swaps may increase. With respect to existing securitization trusts, an inability to amend, novate or otherwise materially modify existing swap contracts could result in a downgrade of its outstanding asset-backed securities. As a result, Navient’s business, ability to access the capital markets for financing and costs may be impacted by new regulations for derivatives transactions.

Other Significant Sources of Regulation

Many aspects of Navient’s businesses are subject to federal and state regulation and administrative oversight. Some of the most significant of these are described below.

Higher Education Act. Navient is subject to the HEA and its education loan operations are periodically reviewed by ED and Guarantors. As a servicer of federal education loans, Navient is subject to ED regulations regarding financial responsibility and administrative capability that govern all third-party servicers of insured education loans. In connection with its servicing operations on behalf of Guarantor clients, Navient must comply with ED regulations that govern Guarantor activities as well as agreements for reimbursement between ED and our Guarantor clients.

Federal Financial Institutions Examination Council. As a third-party service provider to financial institutions, Navient is also subject to periodic examination by the Federal Financial Institutions Examination Council (“FFIEC”). FFIEC is a formal interagency body of the U.S. government empowered to prescribe uniform principles, standards, and report forms for the federal examination of financial institutions by the Federal Reserve Banks (the “FRB”), the Federal Deposit Insurance Corporation (the “FDIC”), the National Credit Union Administration, the Office of the Comptroller of the Currency and the CFPB and to make recommendations to promote uniformity in the supervision of financial institutions.

14

Table of Contents

Consumer Protection and Privacy. Navient’s business servicing education loans is subject to federal and state consumer protection, privacy and related laws and regulations and is subject to examination by the CFPB. Some of the more significant federal laws and regulations include:

| • | various laws governing unfair, deceptive or abusive acts or practices; |

| • | the Truth-In-Lending Act and Regulation Z issued by the FRB, which governs disclosures of credit terms to consumer borrowers; |

| • | the Fair Credit Reporting Act and Regulation V issued by the CFPB, which governs the use and provision of information to consumer reporting agencies; |

| • | the Equal Credit Opportunity Act and Regulation B issued by the CFPB, which prohibit discrimination on the basis of race, creed or other prohibited factors in extending credit; |

| • | the SCRA, which applies to all debts incurred prior to commencement of active military service (including education loans) and limits the amount of interest, including certain fees or charges that are related to the obligation or liability; and |

| • | the TCPA, which governs communication methods that may be used to contact customers. |

Several states have passed or proposed student loan bills of rights or licensing requirements that may also apply to Navient’s education loan servicing business. It is possible that more states will propose or pass similar or different requirements on either holders of education loans or their servicers. These laws or rules may impose additional or different requirements than Navient faces at the federal level.

Navient’s business processing services businesses are subject to federal and state consumer protection, privacy and related laws and regulations, including supervision by the CFPB of larger consumer debt collectors as discussed above. Some of the more significant federal statutes are the Fair Debt Collection Practices Act and additional provisions of the acts listed above, as well as the HEA and the various laws and regulations that govern government contractors. These activities are also subject to state laws and regulations similar to the federal laws and regulations listed above.

Recent Developments

The Company announced on February 21, 2017, that Christian Lown will join the Company as executive vice president and chief financial officer, effective March 27, 2017. Somsak Chivavibul, the current CFO, will remain as CFO until that date after which he will spearhead the launch of the Company’s new enterprise-wide decision management center, where he will be the Company’s executive vice president and chief decision management officer. The Company filed a Form 8-K announcing these appointments on February 21, 2017.

| Item 1A. | Risk Factors |

Navient employs a Risk Appetite Framework which defines the most significant risks impacting our business and provides a process for evaluating and quantifying such risks. Our Enterprise Risk Committee monitors approved risk limits and thresholds to ensure our businesses are operating within approved risk parameters. Through ongoing monitoring of risk exposures, management endeavors to identify potential risks and develop appropriate responses and mitigation strategies. Our Risk Appetite Framework segments Navient’s risks across nine domains: (1) credit; (2) market; (3) funding and liquidity; (4) compliance; (5) legal; (6) operational; (7) reputational/political; (8) governance; and (9) strategy. The risk factors enumerated in this section are presented in a manner that is consistent with our overall risk framework.

These are not the only risks facing our Company. Additional risks not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial conditions or results of operations in future periods. In addition, our reaction to material future developments as well as our competitors’ and regulators’ reactions to these developments will affect our future results.

15

Table of Contents

In addition to the other information set forth in this report including any forward-looking statements, you should carefully consider the following factors because these factors could cause our business, actual results of operations or financial condition to be materially different from our historic results or from our anticipated results of operations, cash flows or financial condition for future periods.

CREDIT RISK. Credit risk is the risk to earnings or capital resulting from an obligor’s failure to meet the terms of any contract with us or otherwise fail to perform as agreed. Credit risk is found in all activities where success depends on counterparty, issuer or borrower performance.

Economic conditions and the creditworthiness of third parties could have a material adverse effect on Navient’s business, results of operations, financial condition and stock price.

We anticipate that, for a period of time, Navient’s earnings will be largely dependent on the expected future creditworthiness of its education loan customers, especially with respect to its Private Education Loan portfolio. Our research consistently indicates that borrower unemployment rates and the failure of in-school borrowers to graduate or otherwise complete their education are two of the most significant macroeconomic factors that increase loan delinquencies and defaults. Additionally, modifications to the original repayment terms in the form of loan forbearance, deferment, grace periods and the use of payment modification programs, including income-based repayment programs can individually and cumulatively impact the performance of the Company’s FFELP Loan and Private Education Loan portfolios. Modifications to private loans may lower the potential return on investment and may have the related effect of delaying defaults which would otherwise have become apparent in the performance of our portfolios. Therefore, deterioration in the economy could adversely affect the credit quality of our borrowers requiring more frequent use of these loan modification tools. Higher credit-related losses and weaker credit quality could negatively affect Navient’s business, financial condition and results of operations and limit its funding options, including Navient’s access to the capital markets, which could also adversely impact its liquidity position.

Defaults on education loans held by Navient, particularly Private Education Loans, could adversely affect Navient’s earnings.

FFELP Loans are insured or guaranteed by state or not-for-profit agencies and are also protected by contractual rights to recovery from the United States pursuant to guaranty agreements among ED and these agencies. These guarantees generally cover at least 97 percent of a FFELP Loan’s principal and accrued interest and, in limited circumstances, 100 percent of the loan’s principal and accrued interest. Nevertheless, Navient is exposed to credit risk on the non-guaranteed portion of the FFELP Loans in its portfolio. Under certain circumstances, if we fail to service FFELP Loans in compliance with HEA regulations that relate to our ongoing communications with borrowers and default aversion requirements, we may jeopardize the insurance, guarantees and federal support we receive on these loans. A small percentage of our FFELP Loan portfolio has become permanently uninsured as a result of these regulations and we anticipate this will continue to a limited extent in the future. Under such circumstances, Navient bears the full credit exposure on such previously insured loans.

Navient bears the full credit exposure on all its Private Education Loans. Navient believes that delinquencies are an important indicator of the potential future credit performance for Private Education Loans. Navient’s delinquencies as a percentage of Private Education Loans in repayment were 7.4 percent at December 31, 2016. For a complete discussion of Navient’s loan delinquencies, see Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Private Education Loan Portfolio Performance.”

The evaluation of Navient’s allowance for loan losses is inherently subjective and it requires estimates that may be subject to significant changes. Future defaults could be higher than anticipated due to a variety of factors outside of Navient’s control, such as downturns in the economy, regulatory or operational changes and other unforeseen future trends. According to Company-sponsored independent research, young adults who stopped attending college before earning a degree or certificate are among those most likely to have trouble making payments. Losses on Private Education Loans are also impacted by various risk characteristics that may be

16

Table of Contents

specific to individual loans. Loan status (in-school, grace, forbearance, repayment and delinquency), loan seasoning (number of months in which a payment has been made by a customer), underwriting criteria (e.g., credit scores), existence of a cosigner are all factors that can impact the likelihood of default. The type of school may also play a significant role in loan performance. Additionally, general economic and employment conditions, including employment rates for recent college graduates can have a significant impact on loan delinquency and default rates. If actual loan performance is worse than currently estimated, it could materially affect Navient’s estimate of the allowance for loan losses and the related provision for loan losses in Navient’s statements of income and as a result adversely affect Navient’s results of operations.

MARKET, FUNDING & LIQUIDITY RISK. Market risk is the risk to earnings or capital resulting from changes in market conditions. Navient is exposed to various types of market risk, in particular the risk of loss resulting in a mismatch between the maturity/duration of assets and liabilities, interest rate risk, foreign currency exchange rates and other risks that arise through the management of our investment, debt and education loan portfolios. Funding and liquidity risk is the risk to earnings, capital or the conduct of our business arising from the inability to meet our obligations when they become due, such as the ability to access the unsecured or asset backed securities credit markets to fund liability maturities or invest in future asset growth and business operations at reasonable market rates.

Navient’s business is affected by the cost and availability of funding in the capital markets.

The capital markets have from time to time experienced periods of significant volatility. This volatility can dramatically and adversely affect financing costs when compared to historical norms or make funding unavailable at any costs. Additional factors that could make financing more expensive or unavailable to Navient include, but are not limited to, financial losses, events that have an adverse impact on Navient’s reputation, changes in the activities of Navient’s business partners, events that have an adverse impact on the financial services industry generally, counterparty availability, negative credit rating actions with respect to Navient, asset-backed securities sponsored by Navient or the U.S. federal government, changes affecting Navient’s assets, the ability of existing or future Navient-sponsored securitization trusts to hedge interest rate and currency risk, corporate and regulatory actions, absolute and comparative interest rate changes, general economic conditions and the legal, regulatory and tax environments governing funding transactions, including existing or future securitization and derivatives transactions. If financing is difficult, expensive or unavailable, Navient’s results of operations, cash flow or financial condition could be materially and adversely affected.

Higher or lower than expected prepayments of loans could change the expected net interest income the Company receives as the holder of the Residual Interests of securitization trusts holding education loans or cause the bonds issued by the securitization trust to be paid at a different speed than originally anticipated. These factors could materially alter our net interest margin or the value of our Residual Interests.

The rate at which borrowers prepay their loans can have a material impact on our net interest margin or the value of our Residual Interests. Prepayment rates and levels are subject to a variety of economic, social, competitive and other factors, including changes in interest rates, availability of alternative financings, regulatory changes affecting the education loan market and the general economy.

FFELP Loans and Private Education Loans may be voluntarily prepaid without penalty by the borrower or consolidated with the borrower’s other education loans through refinancing.

FFELP Loans may also be repaid after default by the Guarantors of FFELP Loans. Conversely, borrowers might not choose to prepay their education loans or the terms of the education loans may be extended as a result of grace periods, deferment periods, income-driven repayment plans or other repayment terms or monthly payment amount modifications agreed to by the servicer, for example. FFELP Loan borrowers may be eligible for various existing income-based repayment programs under which borrowers can qualify for reduced or zero monthly payment or even debt forgiveness after a certain number of years of repayment.

17

Table of Contents

Future initiatives by ED or by Congress to encourage or force consolidation, create additional income-based repayment or debt forgiveness programs or establish other policies and programs that influence the rate at which borrowers repay their loans, could also affect prepayments on education loans. Additionally, several recent entrants into the student loan refinancing market may increase borrower prepayments. These companies specialize in consolidating and refinancing student loans and may have certain advantages including lower cost structures, fewer regulatory constraints and the ability to be highly selective in choosing borrowers who are eligible to refinance. Their ability to selectively market to borrowers with high incomes, high credit scores or other credit determinants may adversely impact the performance of our remaining portfolio.

While we anticipate some variability in prepayment levels, extraordinary or extended increases or decreases in prepayment rates could materially affect our liquidity, interest income, net interest margin and the value of our Residual Interests. Additionally, a prolonged introduction of significant amounts of subsidized funding into the Private Education Loan market at below market interest rates — whether from Federal or private sources —could increase the prepayment rates of our existing Private Education Loans and have a material adverse effect on our business, results of operations and cash flows When, as a result of unanticipated prepayment levels, education loans within a securitization trust amortize faster than originally contracted, the trust’s pool balance may decline at a rate faster than the prepayment rate assumed when the trust’s bonds were originally issued. If the trust’s pool balance declines faster than originally anticipated, in most of our securitization structures, the bonds issued by that trust will also be repaid faster than originally anticipated. In such cases, the Company’s net interest income may decrease and the value of any retained Residual Interest in the trust may similarly decline.

Conversely, when education loans within a securitization trust amortize more slowly than originally contracted, the trust’s pool balance may decline more slowly than the prepayment rate assumed when the trust’s bonds were originally issued and the bonds may be repaid more slowly than originally anticipated. In these cases, the Company’s net interest income increases and the value of any retained Residual Interest in the trust may increase. In addition, if the prepayment rate is especially slow and certain rights of the sellers or the servicer are not exercised or are insufficient or other action is not taken to counter the slower prepayment rate, the trust’s bonds may not be repaid by their legal final maturity date(s), which could result in an event of default under the underlying securitization agreements. Since June 30, 2016, Moody’s and Fitch have taken final ratings action on $52.4 billion and $38.8 billion, respectively, of non-recourse FFELP ABS sponsored by our affiliates due to concerns that trust cash flows may not be sufficient to pay all bonds by the legal final maturity date. As of January 31, 2017, these actions have resulted in downgrades to non-investment grade rating on $4.1 billion and $6.6 billion in FFELP ABS by Moody’s and Fitch, respectively. Subsequent to the initial downgrade action, Fitch has upgraded $0.5 billion of FFELP ABS to investment grade after the Company successfully extended the legal final maturity dates of these bonds. As of January 31, 2017, $11.3 billion of non-recourse FFELP ABS sponsored by our affiliates remains on credit watch by Fitch. Moody’s has completed its ratings actions. For a discussion of the rating agencies actions and the Company’s efforts to mitigate the “legal final maturity” risk, see Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources — Funding and Liquidity Risk Management.”

Finally, rating agencies may place bonds on watch or change their ratings on (or their ratings methodology for) the bonds issued by a securitization trust, possibly raising or lowering their ratings, based upon these prepayment rates and their perception of the risk posed by those rates to the timing of the trust cash flows. Placing bonds on watch, or changing ratings negatively or proposing or making changes to ratings methodology could: (i) affect our liquidity; (ii) impede our access to the securitization markets; (iii) require changes to our securitization structures; (iv) impact our net interest margins; and/or (v) raise or lower the value of our Residual Interests of our future securitization transactions.

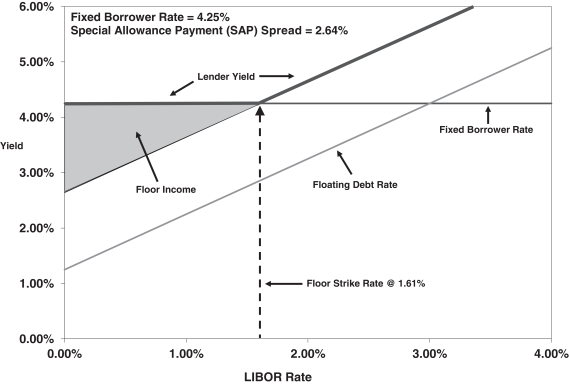

High or increasing interest rate environments may cause Navient’s Floor Income to decline, which may adversely affect its earnings.

FFELP Loans disbursed before April 1, 2006 generally earn interest at the higher of either the borrower rate, which is fixed over a period of time, or a floating rate based on a Special Allowance Payment or SAP formula set

18

Table of Contents

by ED. Navient has generally financed its FFELP Loans with floating rate debt whose interest is matched closely to the floating nature of the applicable SAP formula. Historically, these loans have been indexed to either the Treasury bill, commercial paper or one-month LIBOR rates. If a decline in interest rates causes the borrower rate to exceed the SAP formula rate, Navient will continue to earn interest on the loan at the fixed borrower rate while the floating rate interest on Navient debt will continue to decline. The additional spread earned between the fixed borrower rate and the SAP formula rate is referred to as “Floor Income.”

Depending on the type of FFELP Loan and when it was originated, the borrower rate is either fixed to term or is reset to a market rate on July 1 of each year. For loans where the borrower rate is fixed to term, Navient may earn Floor Income for an extended period of time; for those loans where the borrower interest rate is reset annually on July 1, Navient may earn Floor Income to the next reset date. In accordance with legislation enacted in 2006, holders of FFELP Loans are required to rebate Floor Income to ED for all FFELP Loans disbursed on or after April 1, 2006.