Attached files

| file | filename |

|---|---|

| EX-23.2 - CONSENT OF INDEPENDENT PETROLEUM ENGINEERS - California Resources Corp | a2016yeexhibit232ryderscot.htm |

| EX-99.1 - REPORT OF INDEPENDENT PETROLEUM ENGINEERS - California Resources Corp | a2016yeexhibit991ryderscott.htm |

| EX-32.1 - CERTIFICATIONS OF CEO AND CFO - California Resources Corp | a2016yeexhibit321.htm |

| EX-31.2 - CERTIFICATION OF CFO - California Resources Corp | a2016yeexhibit312.htm |

| EX-31.1 - CERTIFICATION OF CEO - California Resources Corp | a2016yeexhibit311.htm |

| EX-23.1 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - California Resources Corp | a2016yeexhibit231kpmgconse.htm |

| EX-21 - LIST OF SUBSIDIARIES - California Resources Corp | a2016yeexhibit21listofsubs.htm |

| EX-12 - RATIO OF EARNINGS TO FIXED CHARGES - California Resources Corp | a2016yeexhibit12.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-36478

California Resources Corporation

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 46-5670947 (I.R.S. Employer Identification No.) | |

9200 Oakdale Ave. Los Angeles, California (Address of principal executive offices) | 91311 (Zip Code) | |

(888) 848-4754

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock | New York Stock Exchange | |

5% Senior Notes due 2020 | ||

5½% Senior Notes due 2021 | ||

6% Senior Notes due 2024 | ||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act: | Yes ¨ No þ |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Date File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or such shorter period as the registrant was required to submit and post files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer | ¨ | Accelerated Filer | þ | |

Non-Accelerated Filer | ¨ | Smaller Reporting Company | ¨ | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes ¨ No þ

The aggregate market value of the voting common stock held by nonaffiliates of the registrant was approximately $496 million, computed by reference to the closing price on the New York Stock Exchange composite tape of $12.20 per share of Common Stock on June 30, 2016. Shares of Common Stock held by each executive officer and director have been excluded from this computation in that such persons may be deemed to be affiliates. This determination of potential affiliate status is not a conclusive determination for other purposes.

At January 31, 2017, there were 42,542,637 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement to be filed with the Securities and Exchange Commission in connection with the registrant's 2017 Annual Meeting of Stockholders, are incorporated by reference into Part III of this Form 10-K.

1

LIST OF OPERATING SUBSIDIARIES

The following is a list of our subsidiaries at December 31, 2016 other than certain subsidiaries that did not in the aggregate constitute a significant subsidiary.

Name | Jurisdiction of Formation | |

California Heavy Oil, Inc. | Delaware | |

California Resources Coles Levee, LLC | Delaware | |

California Resources Coles Levee, L.P. | Delaware | |

California Resources Elk Hills, LLC | Delaware | |

California Resources Long Beach, Inc. | Delaware | |

California Resources Petroleum Corporation | Delaware | |

California Resources Production Corporation | Delaware | |

California Resources Tidelands, Inc. | Delaware | |

California Resources Wilmington, LLC | Delaware | |

CRC Construction Services, LLC | Delaware | |

CRC Marketing, Inc. | Delaware | |

CRC Services, LLC | Delaware | |

Elk Hills Power, LLC | Delaware | |

Socal Holding, LLC | Delaware | |

Southern San Joaquin Production, Inc. | Delaware | |

Thums Long Beach Company | Delaware | |

Tidelands Oil Production Company | Texas | |

2

TABLE OF CONTENTS

Page | ||

Part I | ||

Items 1 | BUSINESS | |

General | ||

Business Operations | ||

Our Business Strategy | ||

Key Characteristics of our Operations | ||

Portfolio Management and 2017 Capital Budget | ||

Reserves and Production Information | ||

Marketing Arrangements | ||

Regulation of the Oil and Natural Gas Industry | ||

Employees | ||

Available Information | ||

Item 1A | RISK FACTORS | |

Item 1B | UNRESOLVED STAFF COMMENTS | |

Item 2 | PROPERTIES | |

Our Operations | ||

Our Reserves and Production Information | ||

Determination of Identified Drilling Locations | ||

Production, Price and Cost History | ||

Productive Wells | ||

Acreage | ||

Participation in Exploratory and Development Wells Being Drilled | ||

Delivery Commitments | ||

Our Infrastructure | ||

Item 3 | LEGAL PROCEEDINGS | |

Item 4 | MINE SAFETY DISCLOSURES | |

EXECUTIVE OFFICERS | ||

Part II | ||

Item 5 | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | |

Item 6 | SELECTED FINANCIAL DATA | |

Item 7 | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

The Separation and Spin-off | ||

Basis of Presentation and Certain Factors Affecting Comparability | ||

Business Environment and Industry Outlook | ||

Seasonality | ||

Income Taxes | ||

Operations | ||

Financial and Operating Results | ||

Balance Sheet Analysis | ||

Statement of Operations Analysis | ||

Liquidity and Capital Resources | ||

Cash Flow Analysis | ||

Acquisitions and Divestitures | ||

2016 Capital Program and 2017 Capital Budget | ||

Off-Balance-Sheet Arrangements | ||

Lawsuits, Claims, Contingencies and Commitments | ||

Critical Accounting Policies and Estimates | ||

Significant Accounting and Disclosure Changes | ||

Item 7A | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | |

FORWARD-LOOKING STATEMENTS | ||

Item 8 | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | |

Report of Independent Registered Public Accounting Firm on Consolidated and Combined Financial Statements | ||

Report of Independent Registered Public Accounting Firm on Internal Control Over Financial Reporting | ||

Consolidated Balance Sheets | ||

Consolidated and Combined Statements of Operations | ||

Consolidated and Combined Statements of Comprehensive Income | ||

Consolidated and Combined Statements of Equity | ||

3

Consolidated and Combined Statements of Cash Flows | ||

Notes to Consolidated and Combined Financial Statements | ||

Quarterly Financial Data (Unaudited) | ||

Supplemental Oil and Gas Information (Unaudited) | ||

SCHEDULE II - VALUATION AND QUALIFYING ACCOUNTS | ||

Item 9 | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | |

Item 9A | CONTROLS AND PROCEDURES | |

Item 9B | OTHER INFORMATION | |

Part III | ||

Item 10 | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | |

Item 11 | EXECUTIVE COMPENSATION | |

Item 12 | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | |

Item 13 | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS AND DIRECTOR INDEPENDENCE | |

Item 14 | PRINCIPAL ACCOUNTANT FEES AND SERVICES | |

Part IV | ||

Item 15 | EXHIBITS | |

4

PART I

Item 1 | BUSINESS |

In this report, except when the context otherwise requires or where otherwise indicated, (1) all references to ‘‘CRC,’’ the ‘‘Company,’’ ‘‘we,’’ ‘‘us’’ and ‘‘our’’ refer to California Resources Corporation and its subsidiaries or the California business, (2) all references to the ‘‘California business’’ refer to Occidental’s California oil and gas exploration and production operations and related assets, liabilities and obligations, which we assumed in connection with the spin-off from Occidental on November 30, 2014 (the Spin-off), and (3) all references to ‘‘Occidental’’ refer to Occidental Petroleum Corporation, our former parent, and its subsidiaries.

General

We are an independent oil and natural gas exploration and production company operating properties within the state of California. We were incorporated in Delaware as a wholly owned subsidiary of Occidental on April 23, 2014, and remained a wholly owned subsidiary of Occidental until November 30, 2014. As of November 30, 2014, all material existing assets, operations and liabilities of Occidental's California business were consolidated under us. On November 30, 2014, Occidental distributed shares of our common stock on a pro rata basis to Occidental stockholders and we became an independent, publicly traded company (the Spin-off). Occidental initially retained approximately 18.5% of our outstanding shares of common stock, which it distributed to Occidental stockholders on March 24, 2016. On May 31, 2016 we completed a reverse stock split using a ratio of one share of common stock for every ten shares then outstanding. Share and per share amounts included in this report have been restated to reflect this reverse stock split.

Business Operations

Our Business

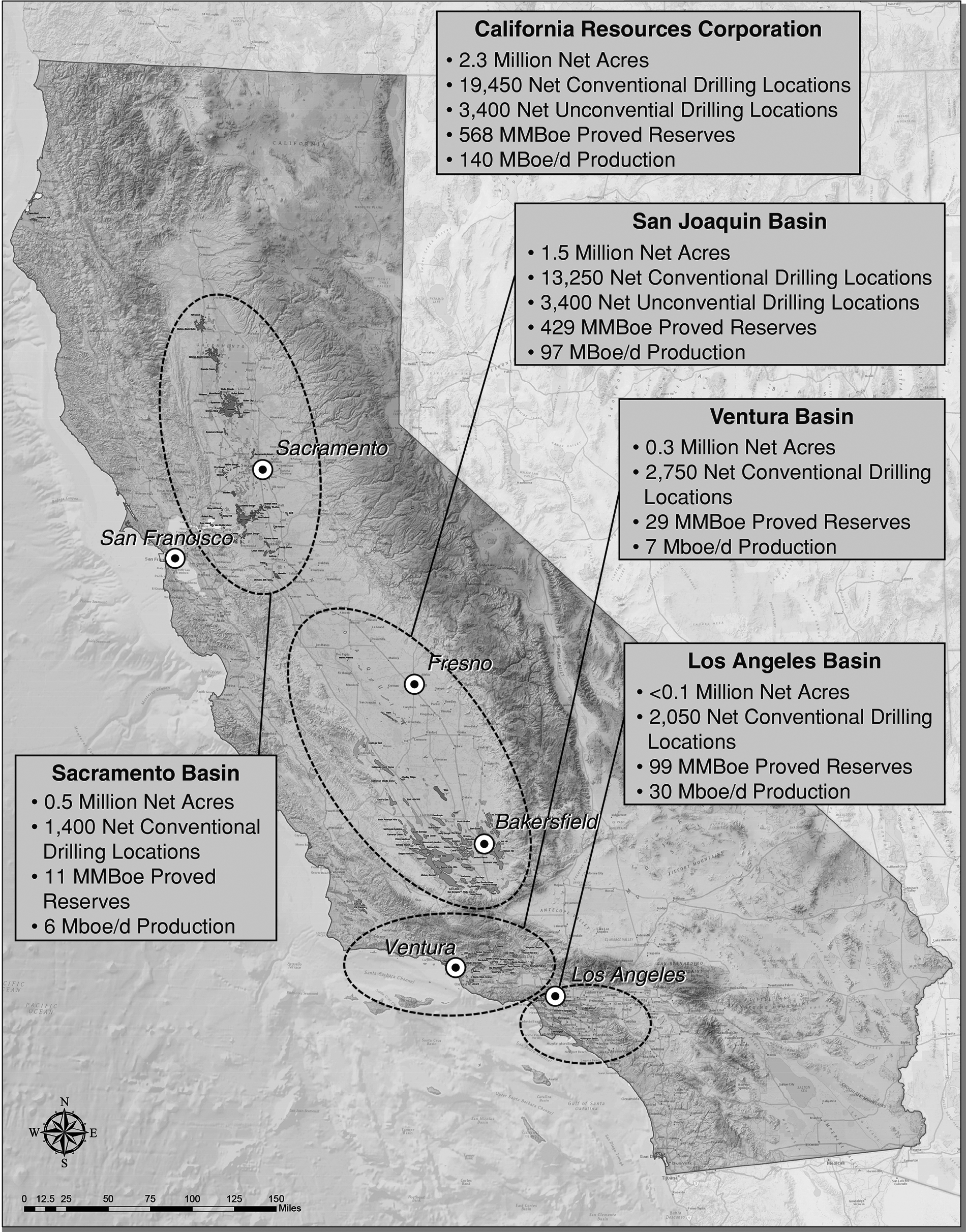

Our business is focused on conventional and unconventional assets in California. We are the largest oil and gas producer in California on a gross operated basis and we believe we have the largest privately held mineral acreage position in the state, consisting of approximately 2.3 million net acres spanning the state’s four major oil and gas basins. We produced approximately 140 thousand barrels of oil equivalent per day (MBoe/d) for the year ended December 31, 2016. As of December 31, 2016, we had net proved reserves of 568 million barrels of oil equivalent (MMBoe), of which approximately 71% was categorized as proved developed reserves. Oil represented 72% of our proved reserves.

Our large acreage position and extensive drilling inventory provide us a diversified portfolio of oil and natural gas locations that are economically viable in a variety of operating and commodity price conditions, including many which are high return projects throughout the price cycle. Our acreage position contains numerous development and growth opportunities due to its varied geologic characteristics and multiple stacked pay reservoirs which, in many cases, are thousands of feet thick. We have a large portfolio of low-risk and low-decline conventional opportunities in each of our major oil and gas basins with approximately 70% of our proved reserves associated with conventional opportunities. Conventional reservoirs are capable of natural flow using primary, steamflood and waterflood recovery methods. We also have a significant portfolio of unconventional growth opportunities in lower permeability reservoirs that typically utilize established well stimulation techniques. We have approximately 3,400 net identified drilling locations targeting unconventional reservoirs primarily in the San Joaquin basin. Prior to the severe price declines, we were focused on higher-value unconventional production from seven discrete stacked pay horizons within the Monterey formation, primarily within the upper Monterey. Over the longer term, as project economics improve, we will seek to duplicate our successful upper Monterey results to develop opportunities in the unconventional reservoirs of the lower Monterey, Kreyenhagen and Moreno formations, which have similar geological attributes.

5

The following table summarizes certain information concerning our acreage, wells and drilling activities (as of December 31, 2016, acres and dollars in millions, unless otherwise stated):

Acreage | Average Net Acreage Held in Fee (%) | Producing Wells, gross | Net Revenue Interest (%) | Identified Drilling Locations(1) | ||||||||||||||||

Gross | Net | Gross | Net | |||||||||||||||||

San Joaquin Basin | 1.8 | 1.5 | 64 | % | 6,246 | 79 | % | 23,900 | 16,650 | |||||||||||

Los Angeles Basin(2) | <0.1 | <0.1 | 52 | % | 1,315 | 78 | % | 2,150 | 2,050 | |||||||||||

Ventura Basin | 0.3 | 0.3 | 72 | % | 567 | 84 | % | 2,950 | 2,750 | |||||||||||

Sacramento Basin | 0.6 | 0.5 | 37 | % | 709 | 76 | % | 1,900 | 1,400 | |||||||||||

Total | 2.8 | 2.3 | 58 | % | 8,837 | 79 | % | 30,900 | 22,850 | |||||||||||

(1) | Our total identified drilling locations exclude approximately 6,400 gross (5,300 net) prospective resource drilling locations. Our total identified drilling locations include approximately 2,350 gross (2,150 net) locations associated with proved undeveloped reserves as of December 31, 2016. Our total identified drilling locations also include approximately 2,300 gross (2,100 net) injection well locations. Please see "Item 2 – Properties – Our Reserves and Production Information" for more information regarding the processes and criteria through which we identified our drilling locations. |

(2) | We currently hold approximately 42,600 gross (34,400 net) acres in the Los Angeles basin. Our Los Angeles basin operations are concentrated with pad drilling. |

We develop our capital investment programs by prioritizing life of project returns to grow our net asset value over the long term, while balancing the short- and long-term growth potential of each of our assets. We use a Value Creation Index (VCI) metric for project selection and capital allocation across our portfolio of opportunities. We calculate the VCI for each of our projects by dividing the net present value of the project's expected pre-tax cash flow over its life by the present value of the investments, each using a 10% discount rate. Projects are expected to meet a VCI of 1.3, meaning that 30% of expected value is created above our cost of capital for every dollar invested. Our technical teams are consistently working to enhance value by improving the economics of our inventory through detailed geologic studies as well as application of more effective and efficient drilling and completion techniques. As a result, we expect many projects that do not currently meet our investment hurdle today will do so by the time of development. We regularly monitor internal performance and external factors and adjust our capital investment program with the objective of creating the most value from our portfolio of drilling opportunities.

Over the past decade, we have also built a 3D seismic library that covers approximately 4,800 square miles, representing over 90% of the 3D seismic data available in California. We have developed unique, proprietary stratigraphic and structural models of the subsurface geology and hydrocarbon potential in each of the four basins in which we operate. In recent years we have tested and successfully implemented various exploration, drilling, completion and enhanced recovery technologies to increase recoveries, growth and value from our portfolio. We continue working to build depth in our exploration inventory and identify new prospects based on the competitive advantage provided by this proprietary data set and our experience.

Business Environment

Much of the global exploration and production industry has been challenged at recent price levels, putting pressure on the industry's ability to generate positive cash flow and access capital. The decline in average oil prices that began in the last half of 2014 continued into the first quarter of 2016. While global oil prices improved modestly through the end of 2016 and began to trade in a narrower range, daily average prices were still lower for the full year of 2016 compared to 2015.

Consistent with our strategy to invest within our cash flow, we initially budgeted $50 million for our 2016 capital program, primarily to maintain the mechanical integrity of our facilities and systems and operate them safely. In the first half of the year, we further reduced the pace of our capital program to below our initial budget. In response to commodity price improvements in the second half of the year, we gradually increased our capital investment to $75 million for the full year. Our slowdown of drilling activity from late 2015 through the first half of 2016, coupled with the selective deferral of expense and capital workover activity, led to a decline in our production in 2016. However, we accomplished our operational tenet of minimizing our base decline with nominal capital investment.

6

At the time of our Spin-off, we had over 2,000 employees. In the third quarter of 2015 and early 2016, we implemented a voluntary retirement program and other employee actions to align our workforce with our view of the commodity price environment. We ended 2016 with approximately 1,450 employees, representing a nearly 30% reduction mainly through attrition and the 2015 and 2016 employee actions. We have also taken a number of other steps which better align our cost structure with the current environment. As a result of these steps, our 2016 production costs and general and administrative expenses were below 2015 levels. These measures helped offset some of the cash flow effects of the low commodity prices. We also pursued a number of alternatives to strengthen our balance sheet and better align our capital structure with the recent market conditions as described in more detail in “Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operation – Liquidity and Capital Resources.”

With significant operating control of our properties, we have the ability to adjust our drilling and workover rig count based on commodity prices and monitor market conditions to increase or decrease our program accordingly. We reactivated our drilling program in the third quarter of 2016 with one drilling rig located in the San Joaquin basin primarily targeting steamflood activities. By the end of the year, we operated two drilling rigs, one each in the San Joaquin and Los Angeles basins. We drilled 42 development wells with 37 wells in the San Joaquin basin and 5 in the Los Angeles basin. These included 34 steamflood and 8 waterflood wells. In 2016, we also increased our workover rig count from 26 at the beginning of the year to 41 at the end of the year to focus on projects that meet our investment criteria. In total, we performed 133 capital workover projects during 2016.

Compared to 2015, our 2016 production declined 12.5%, with only $31 million of drilling and workover capital employed for the year. Excluding the effect of our production-sharing contracts (PSCs) in Long Beach, our decline rate would have been under 12%. This performance reflects the resilience of our asset base and the better than expected flattening of our base production decline. We expect to direct virtually all of our capital investments toward oil-weighted opportunities in 2017 to the extent the oil-to-gas price relationship remains favorable, which should improve our overall margins. For example, our steamflood projects provide some of the highest returns in our portfolio when the oil-to-gas price ratio exceeds five to one. As of December 31, 2016, the ratio was approximately 19 to one.

The flattening of our production decline rate that started in the second half of 2016 as a result of higher activity levels has continued into the first quarter of 2017. We believe that the actions we have taken since the Spin-off to streamline our business and reduce costs, together with recent price increases, have brought us to an inflection point where we can increase our activity level. We intend to fund our capital investment program by reinvesting substantially all of our operating cash flow, while considering additional potential deleveraging opportunities. We expect to drive organic deleveraging by drilling our extensive inventory of oil-heavy, low-decline assets. Our high level of operational control provides flexibility to adjust the level of our capital investments as circumstances warrant. As a result, we have created dynamic budgets that can be adjusted to align investments with projected cash flows. In the event of improved and more consistent prices and cash flow, we may choose to deploy additional capital based on our VCI investment metric, while abiding by our financial covenants.

Prior to the Spin-off, while we were a subsidiary of Occidental, we did not have a hedging program. Given the volatile oil price environment, we instituted a program immediately after the Spin-off to protect our cash flows, margins and capital investment programs and to improve our ability to comply with our credit facility covenants in case of price deterioration.

7

Our Business Strategy

Near-Term Strategy

In mid-2016, global oil prices began to recover from the apparent low point of this commodity cycle. The recovery further strengthened following the production cuts announced at the November 2016 meeting of the Organization of the Petroleum Exporting Countries (OPEC). In light of these developments, we began to increase our activity level in the second half of 2016 and have continued to do so in early 2017. While we began 2017 with two rigs running, by the end of the first quarter of 2017, we anticipate having four rigs running (three in the San Joaquin basin and one in the Los Angeles basin). We also plan to add an additional rig in the Ventura basin by the third quarter of 2017. Our 2017 development program will focus primarily on our core fields: Elk Hills; Wilmington; Kern Front; Buena Vista; and the delineation of Kettleman North Dome. Based on then-current market conditions, we increased our 2017 planned capital program to $300 million from the $75 million invested in 2016. We have developed a dynamic plan which can be scaled up or down depending on the price environment. For 2017, we have action plans that can reduce our capital investment plan to under $100 million or increase it to as high as $500 million based on conditions during the year. For highlights of our 2017 program, see "Portfolio Management and 2017 Capital Budget" section below.

Our approach to our 2017 drilling program is consistent with our stated strategy to remain financially disciplined and fund projects through internally generated cash flow. This approach is intended to maintain our liquidity and further strengthen our balance sheet. We are prepared to significantly increase our drilling activity if prices continue to improve during 2017. We will also evaluate the use of excess cash for other opportunities to further strengthen our capital structure. Our plan is to deploy capital to projects that help stabilize our production and return to a growth profile in the second half of the year. Our current drilling inventory comprises a diversified portfolio of oil and natural gas locations that are economically viable in a variety of operating and commodity price conditions.

Long-Term Strategy

We plan to drive long-term stockholder value by applying modern technology to develop our resource base and increase production. We have significant conventional opportunities to pursue, which we develop through their life-cycles to increase recovery factors by transitioning them from primary production to steamfloods, waterfloods and other enhanced recovery mechanisms. In the recent price and constrained capital environment, we have remained financially disciplined and prudent with our capital investments to maintain liquidity. We are cautiously optimistic that the prices at the end of 2016 are at a turning point and moving towards a more stabilized and relatively higher commodity price environment. In a sustained higher price environment, we intend to direct any additional available capital to oil projects that provide long-term value, high returns, growing cash flows and low production declines. Higher activity should ultimately lead to more production which further increases our cash flows, allowing us to strengthen our balance sheet through growth. The principal elements of our long-term business strategy include the following:

• | Focus on high-margin crude oil projects to generate sufficient cash flows to internally fund our growth capital needs. We expect the percentage of our oil production to continue to increase over time and favorably impact our overall margins as we anticipate directing virtually all of our capital investments towards oil-weighted opportunities to the extent the oil-to-gas price relationship remains favorable and capital is available. Approximately 95% of our identified drilling inventory is associated with oil-rich projects. Currently, 65% of our production is oil while 72% of our reserves are oil. Over time, we expect our share of oil production to approach the share of oil reserves. |

• | Maintain an appropriate share of conventional projects in our production mix to manage production declines and lower base maintenance capital requirements. Our portfolio of assets includes a large number of steamflood and waterflood projects that have much lower decline rates than many unconventional projects. At current price levels, we intend to focus a greater portion of our capital investments on such projects, which we expect will lower our production decline rates. Over time, we expect that this strategy will reduce the capital required to maintain flat crude oil production. We have significant additional lower-risk conventional opportunities with approximately 27,150 gross (19,450 net) identified drilling locations, 54% of which are associated with Improved Oil Recovery (IOR) and Enhanced Oil Recovery (EOR) projects. The remaining 46% are associated with primary recovery methods, many of which we expect will develop into IOR and EOR projects in the future. |

8

• | Proactive and collaborative approach to safety, environmental protection, and community relations. We are committed to managing our assets in a manner that safeguards people and protects the environment, and we seek to proactively engage with regulatory agencies, communities and other stakeholders to pursue mutually beneficial outcomes. As a California company, helping our state meet its water needs is a key strategic focus. Through our investments in water conservation and in recycling of produced water from oil and gas reservoirs, we are a net water supplier to agriculture. In 2016, our operations supplied more than 3.9 billion gallons of reclaimed water to agricultural water districts, a 49% increase from 2015. This water supply to agriculture set a company record and again exceeded the volume of fresh water we purchased for our operations statewide. We continue to evaluate measures to further decrease our fresh water use and to expand the beneficial use of our produced water over the coming years. |

• | Continue to pursue joint venture development opportunities. We continuously evaluate opportunities to accelerate future development through joint ventures. We would pursue these projects to the extent we believe they would increase stockholder value. We are actively discussing both development and exploration project opportunities. In addition to pursuing growth through joint ventures, we expect substantially all our cash flow to be directed to our capital program while considering other deleveraging opportunities as appropriate. |

• | Continue to identify high-growth unconventional drilling opportunities. Over the longer term and in a higher oil-price environment, we believe we can generate significant production growth from unconventional reservoirs such as tight sandstones and shales. In such an environment, we would expect to generate sufficient cash flow from our conventional projects to fund numerous unconventional opportunities in our portfolio. We hold mineral interests in approximately 1.3 million net acres with unconventional potential and have identified approximately 3,750 gross (3,400 net) drilling locations on this acreage. A meaningful portion of our production already comes from unconventional assets. While we have not yet developed sufficient information to reliably predict success rates across our entire portfolio, our continued technical reviews of these unconventional projects are allowing us to better understand performance of these reservoirs in addition to improving our overall cycle time from project identification to development. As a result of our increased understanding of these reservoirs, we believe we will be able to direct future available capital more precisely to higher value projects, allowing us to strategically increase our investment levels in unconventional drilling over time. |

• | Apply proven modern technologies to enhance production growth and cost efficiency. Over the last several decades, the oil and gas industry has focused significantly less effort on utilizing modern development and exploration processes and technologies in California relative to other prolific U.S. basins. We believe this is largely due to other oil companies’ limited capital investments in California, concentration on shallow zone thermal projects, or investments in other assets within their global portfolios. As an independent company focused on California, we intend to use proven modern technologies in drilling and completing wells, as well as production methods, which we expect will substantially increase both our production and cost efficiency over time. We have developed an extensive 3D seismic library covering almost 4,800 square miles in all four of our basins, representing over 90% of the 3D seismic data available for California, and have tested and successfully implemented various exploration, drilling, completion, IOR and EOR technologies in the state. |

• | Continued focus on our successful exploration program. As prices improve and sufficient additional capital becomes available, we intend to significantly increase our investment in exploration, focusing on both unconventional and conventional opportunities, primarily in areas that we believe can be quickly developed, such as those adjacent to our existing properties. In addition, we plan to explore and test new unconventional resource areas, which, if successful, could result in significant longer-term production growth. In addition, we are also actively pursuing joint venture partnership opportunities, which may give us the opportunity to implement some of our exploration projects even in the current environment. |

9

Key Characteristics of our Operations

The following are among the key characteristics of our operations:

• | Operational control of our diverse asset base provides flexibility over various commodity price ranges and preserves future value and growth potential in a higher price environment. Our near 100% operational control of 135 fields in California provides us flexibility to adapt our investments to various market environments through our ability to select drilling locations, the timing of our development and the drilling and completion techniques we use. Our large and diverse mineral acreage position, of which approximately 60% is held in fee, 15% is held by production and 25% are term leases, allows us to choose among multiple recovery mechanisms, including primary conventional, steamflood, waterflood and unconventional, and to develop various products, including oil, natural gas and natural gas liquids (NGLs). A majority of our interests are in producing properties located in reservoirs characterized by what we believe have long-lived production profiles with repeatable development opportunities. Approximately 95% of our identified drilling inventory is associated with oil-rich projects, primarily located in the San Joaquin, Los Angeles and Ventura basins, and the remaining inventory is associated with natural gas properties in the Sacramento, San Joaquin and Ventura basins. The variety of recovery mechanisms and product types available to us, together with our operating control, allows us to allocate capital in a manner designed to optimize cash flow over a wide range of commodity prices. The low base decline of our conventional assets allows us to limit production declines with minimal investment. We believe our low base decline positions us well to achieve oil production growth in the current price environment while living within our means. |

• | Relatively favorable margins driven by California's deficit energy market. We currently sell all of our crude oil into the California refining markets, which we believe have offered favorable pricing for comparable grades relative to other U.S. regions. California is heavily reliant on imported sources of energy, with approximately 65% of oil and 90% of natural gas consumed in recent years imported from outside the state. A vast majority of the imported oil arrives via supertanker, mostly from foreign locations. As a result, California refiners have typically purchased crude oil at international waterborne-based prices. We believe that the limited crude transportation infrastructure from other parts of the country to California will continue contributing to higher realizations than most other United States oil markets for comparable grades. In addition, we own fee mineral interests on approximately 60% of our net acreage position. The returns on fee mineral acreage are enhanced because we do not pay royalties and other lease payments. To further improve our margins, we are opportunistically pursuing newly opened export markets for our crude oil production. |

• | Largest acreage position in a world-class oil and natural gas province. We believe we are the largest private oil and natural gas mineral acreage holder in California, with interests in approximately 2.3 million net acres. California is one of the most prolific oil and natural gas producing regions in the world and is the third largest oil producing state in the nation. It has four of the 12 largest fields in the lower 48 states based on proved reserves as of 2013, and our portfolio includes interests in each of these four fields. California is also the nation’s largest state economy, and the world's sixth largest, with significant energy demands that exceed local supply. Our large acreage position with a diverse development portfolio enables us to pursue the appropriate production strategy for the relevant commodity price environment without the need to acquire new acreage. For example, in a high natural gas price environment we can rapidly increase our investments in the Sacramento basin to generate significant production growth. Our large acreage position also allows us to quickly deploy the knowledge we gain in our existing operations, together with our seismic data, in other areas within our portfolio. |

10

• | Opportunity rich drilling and workover portfolio. Our drilling inventory at December 31, 2016 consisted of approximately 30,900 gross identified well locations, including approximately 27,150 gross (19,450 net) conventional drilling locations and approximately 3,750 gross (3,400 net) unconventional drilling locations. Our drilling inventory count increased by about 30% from the prior year as a result of our technical teams' continued efforts. We also have approximately 1,000 workover projects that can deliver high returns. At about $55 Brent, we estimate that we have been able to increase investment opportunities that meet our 1.3 VCI hurdle sufficiently to double the drilling and workover capital we could deploy. In the process, our inventory of lower-risk conventional development opportunities with attractive returns has increased, even more than our unconventional opportunities. In a more favorable, sustained price environment, we believe we can also achieve further long-term production growth through the development of unconventional reservoirs. In addition, our rich conventional and unconventional portfolio can provide attractive joint venture partnership opportunities. |

• | Proven operational management and technical teams with extensive experience operating in California. The members of our operational management and technical teams have an average of over 25 years’ experience in the oil and natural gas industry, with an average of over 15 years focused on our California oil and gas operations through multiple pricing cycles. Our operational management team and technical staff have a proven track record of applying modern technologies and operating methods to develop our assets and improve their operating efficiencies. For example, our teams have successfully reduced field operating costs on a per unit basis by approximately 22% since the Spin-off. |

Portfolio Management and 2017 Capital Budget

We develop our capital investment programs by prioritizing life of project returns to grow our net asset value over the long term, while balancing the short- and long-term growth potential of each of our assets. We use the VCI metric for project selection and capital allocation across our portfolio of opportunities.

In 2016, we invested approximately $13 million for drilling wells, $18 million for capital workovers, $23 million for facilities and compression expansion (including $19 million for a major turnaround of our power plant), $15 million for maintenance and occupational health, safety and environmental projects and the rest for other items. Virtually all of our 2016 development capital was directed towards oil-weighted production consistent with 2015 and 2014.

In mid-2016, global oil prices began to recover from the apparent low point of this commodity cycle. The recovery further strengthened following the production cuts announced at the November 2016 meeting of the OPEC. In light of these developments, we began to increase our activity level in the second half of 2016 and have continued to do so in early 2017. While we began 2017 with two rigs running, by the end of the first quarter 2017, we anticipate having four rigs running (three in the San Joaquin and one in the Los Angeles basin). We also plan to add an additional rig in the Ventura basin by the third quarter of 2017. Our 2017 development program will focus primarily on our core fields: Elk Hills; Wilmington; Kern Front; Buena Vista; and the delineation of Kettleman North Dome. Based on the current market conditions, we increased our 2017 planned capital program to $300 million from the $75 million invested in 2016. We have developed a dynamic plan which can be scaled up or down depending on the price environment. For 2017, we have action plans that can reduce the capital program to below $100 million or increase it as high as $500 million based on conditions during the year while remaining within our operating cash flows.

Based on our current 2017 plan, we expect to use approximately half of our capital to drill over 100 wells. Our drilling program utilizes all four of our recovery mechanisms: primary conventional, steamflood, waterflood and unconventional. The depth of our primary conventional wells is expected to range from 2,000-14,000 feet.

With the significant reduction in our drilling costs since the Spin-off, many of our deep conventional and unconventional programs have become more competitive. We intend to drill approximately 20 unconventional wells in the Elk Hills, Buena Vista and Kettleman areas. We expect to focus our conventional program of approximately 90 wells primarily on Mount Poso, Elk Hills, Pleito Ranch, Kern Front and Wilmington, which will largely consist of steam and waterfloods. We recently entered into a joint venture that will invest up to $250 million in the development of certain of our properties. The joint venture will allow us to change the mix and nature of our drilling program as the year progresses.

11

We also plan to use over 15% of our capital for capital workovers on existing well bores. Capital workovers are some of the highest VCI projects in our portfolio and generally include well deepenings, recompletions, changes of lift methods and other activities designed to add incremental productive intervals and reserves.

Further, over 15% of our 2017 program is intended for development facilities at our newer projects, including pipeline and gathering line interconnections, gas compression and water management systems, and about 10% each is intended to be used for exploration and to maintain the mechanical integrity, safety and environmental performance of our operations.

As a result of higher activity levels, our production decline rate began to flatten in the second half of 2016 and continues to improve in 2017. We believe that the actions we have taken since the Spin-off to streamline our business and reduce costs, together with recent price increases, have brought us to an inflection point where we can increase our activity level.

In addition, we will continue to build our inventory of available projects, which will position us to take advantage of future higher prices.

Reserves and Production Information

The table below summarizes our proved reserves and average net daily production as of and for the year ended December 31, 2016 in each of California's four major oil and gas basins:

Proved Reserves as of December 31, 2016 | Average Net Daily Production for the Year Ended December 31, 2016 | ||||||||||||||||||||||||

Oil (MMBbl) | NGLs (MMBbl) | Natural Gas (Bcf) | Total (MMBoe) | Oil (%) | Proved Developed (%) | (MBoe/d) | Oil (%) | R/P Ratio (Years)(1) | |||||||||||||||||

San Joaquin Basin | 287 | 53 | 536 | 429 | 67 | % | 67 | % | 97 | 59 | % | 12.1 | |||||||||||||

Los Angeles Basin | 98 | — | 7 | 99 | 99 | % | 84 | % | 30 | 97 | % | 9.0 | |||||||||||||

Ventura Basin | 24 | 2 | 15 | 29 | 83 | % | 86 | % | 7 | 71 | % | 11.3 | |||||||||||||

Sacramento Basin | — | — | 68 | 11 | — | 100 | % | 6 | — | % | 5.0 | ||||||||||||||

Total operations | 409 | 55 | 626 | 568 | 72 | % | 71 | % | 140 | 65 | % | 11.1 | |||||||||||||

Note: MMBbl refers to millions of barrels; Bcf refers to billion cubic feet of natural gas; MMBoe refers to million barrels of oil equivalent; and MBoe/d refers to thousands of barrels of oil equivalent per day. Natural gas volumes have been converted to Boe based on the equivalence of energy content between six Mcf of natural gas and one Bbl of oil.

(1) | Calculated as total proved reserves as of December 31, 2016 divided by annualized Average Net Daily Production for the year ended December 31, 2016. |

Marketing Arrangements

We market our crude oil, natural gas, NGLs and electricity in accordance with standard energy industry practices.

Crude Oil. Substantially all of our crude oil production is connected to California markets via our crude oil gathering pipelines, which are used almost entirely for our production. We generally do not transport, refine or process the crude oil we produce and do not have any significant long-term crude oil transportation arrangements in place. California is heavily reliant on imported sources of energy, with approximately 65% of the oil consumed in recent years imported from outside the state. A vast majority of the imported oil arrives via supertanker, mostly from foreign locations. We currently sell all of our crude oil into the California refining markets, which we believe have offered relatively favorable pricing compared to other U.S. regions for similar grades. A vast majority of the imported oil arrives via supertanker, with a minor amount arriving by rail. As a result, California refiners have typically purchased crude oil at international waterborne-based prices. Currently, none of our index-based crude oil sales contracts have terms extending past one year and a substantial majority have 60- or 90-day terms. Beginning in late 2015, the U.S. federal government allowed the export of crude oil.

Prior to the Spin-off, while we were a subsidiary of Occidental, we did not have a hedging program. Given the volatile oil price environment, as well as our leverage, we began a hedging program immediately after the Spin-off to protect our cash flows, margins and capital investment program and improve our ability to comply with the covenants under our credit facilities in case of further price deterioration. We will continue to be strategic and opportunistic in implementing our hedging program.

12

Unless otherwise indicated, we use the term "hedge" to describe derivative instruments that are designed to achieve our hedging program goals, even though they are not necessarily accounted for as cash flow or fair value hedges. As part of our hedging program, we currently have the following Brent-based crude oil contracts as of December 31, 2016:

Q1 2017 | Q2 2017 | Q3 2017 | Q4 2017 | Q1 2018 | Q2-Q4 2018 | ||||||||||||||||||

Crude Oil | |||||||||||||||||||||||

Calls: | |||||||||||||||||||||||

Barrels per day | 12,100 | 5,000 | 10,000 | 15,000 | 15,600 | 15,000 | |||||||||||||||||

Weighted-average price per barrel | $ | 56.37 | $ | 55.05 | $ | 56.15 | $ | 56.12 | $ | 58.77 | $ | 58.83 | |||||||||||

Puts: | |||||||||||||||||||||||

Barrels per day | 22,100 | 20,000 | 17,000 | 10,000 | — | — | |||||||||||||||||

Weighted-average price per barrel | $ | 49.10 | $ | 50.25 | $ | 50.88 | $ | 48.00 | $ | — | $ | — | |||||||||||

Swaps: | |||||||||||||||||||||||

Barrels per day | 20,000 | 20,000 | 20,000 | 20,000 | — | — | |||||||||||||||||

Weighted-average price per barrel | $ | 53.98 | $ | 53.98 | $ | 53.98 | $ | 53.98 | $ | — | $ | — | |||||||||||

The second through fourth quarter 2017 crude oil swaps grant our counterparty a quarterly option to increase volumes by up to 10,000 barrels per day for that quarter at a weighted-average Brent price of $55.46. Our counterparty also has an option to increase volumes by up to 5,000 barrels per day for the second half of the year at a weighted-average Brent price of $61.43.

Natural Gas. California imports approximately 90% of the natural gas consumed in the state. We have firm transportation capacity contracts to access markets where necessary. These contracts are required to facilitate deliveries. We sell virtually all of our natural gas production under individually negotiated contracts using market-based pricing on a monthly or shorter basis.

NGLs. We process substantially all of our NGLs through our processing plants, which facilitates access to third-party delivery points near the Elk Hills field. We currently have pipeline capacity contracts to transport 20,000 barrels per day of NGLs to market. We sell virtually all of our NGLs using index-based pricing. Our NGLs are generally sold pursuant to one-year contracts that are renewed annually.

Electricity. We provide part of the electrical output of our Elk Hills power plant to reduce Elk Hills field operating costs and increase reliability. We sell the excess to the grid and to others under contract.

Our Principal Customers

We sell our crude oil, natural gas and NGLs production to marketers, California refineries and other purchasers that have access to transportation and storage facilities. Our marketing of crude oil, natural gas and NGLs can be affected by factors that are beyond our control, and which cannot be accurately predicted.

For the year ended December 31, 2016, Phillips 66 Company, Tesoro Refining & Marketing Company LLC, Valero Marketing & Supply Company and Shell Trading (US) Company each accounted for at least 10%, and, collectively, 67% of our revenue. For the year ended December 31, 2015, Phillips 66 Company, Tesoro Refining & Marketing Company LLC and Valero Marketing & Supply Company each accounted for more than 10%, and collectively, 64% of our revenue. For the year ended December 31, 2014, ConocoPhillips/Phillips 66 Company and Tesoro Refining & Marketing Company LLC each accounted for at least 10%, and, collectively, 45% of our revenue.

13

Title to Properties

As is customary in the oil and natural gas industry, we initially conduct a high-level review of the title to our properties at the time of acquisition. Individual properties may be subject to ordinary course burdens that we believe do not materially interfere with the use or affect the value of our properties. Such burdens on properties may include customary royalty interests, liens incident to operating agreements and for current taxes, obligations or duties under applicable laws, development obligations, or net profits interests, among others. Prior to the commencement of drilling operations on those properties, we conduct a more thorough title examination and perform curative work with respect to significant defects. We generally will not commence drilling operations on a property until we have cured known title defects that are material to the project. In addition, our properties have been pledged as collateral to secure a portion of our debt.

Competition

We have many competitors (including international competitors exporting to California), some of which are larger and better funded, may be willing to accept greater risks or have special competencies. We compete for services to profitably develop our assets, to find or acquire additional reserves, to sell our production and to find and retain qualified personnel. Historically higher commodity prices intensify competition for drilling and workover rigs, pipe, other oil field equipment and personnel. Over the longer term, competition for reserves can increase costs for, or delay, reserves replacement. We compete on the basis of costs, our inventory of drilling opportunities, access to capital, efficiency of capital allocation and other factors.

Regulation of the Oil and Natural Gas Industry

Our operations are subject to complex and stringent federal, state, local and other laws and regulations relating to the exploration and development of our properties, the production, transportation, marketing and sale of our products, and the services we provide.

Regulation of Exploration and Production

Federal, state and local laws and regulations govern most aspects of exploration and production in California, including:

• | oil and natural gas production including well spacing or density on private and state lands; |

• | methods of constructing, drilling, completing, stimulating, operating, maintaining and abandoning wells; |

• | design, construction, operation, maintenance and decommissioning of facilities, such as natural gas processing plants, power plants, compressors and liquid and natural gas pipelines or gathering lines; |

• | improved or enhanced recovery techniques such as fluid injection for pressure management, waterflooding or steamflooding; |

• | sourcing and disposal of water used in the drilling, completion, stimulation, maintenance and enhanced recovery processes; |

• | imposition of taxes and fees with respect to our properties and operations; |

• | the conservation of oil and natural gas, including provisions for the unitization or pooling of oil and natural gas properties; |

• | posting of bonds or other financial assurance to drill, operate and abandon or decommission wells and facilities; and |

• | occupational health, safety and environmental matters and the transportation, marketing and sale of our products as described below. |

The Division of Oil, Gas, and Geothermal Resources (DOGGR) of the Department of Conservation is the state’s primary regulator of the oil and natural gas industry on private and state lands, with additional oversight from the State Lands Commission’s administration of state surface and mineral interests. The Bureau of Land Management (BLM) of the U.S. Department of the Interior exercises similar jurisdiction on federal lands in California. In addition, specific aspects of our operations, such as occupational health, safety, air and water quality, labor, marketing and taxation, are regulated by other federal, state or local agencies. Collectively, the effect of these regulations is to potentially limit the number and location of our wells and the amount of oil and natural gas that we can produce from our wells compared to what we otherwise would be able to do.

14

In 2013 California adopted Senate Bill 4 (SB 4), which increased regulation of certain well stimulation techniques, including, as defined, acid matrix stimulation and hydraulic fracturing, which involves the injection of fluid under pressure into underground rock formations to create or enlarge fractures to allow oil and gas to flow more freely. Among other things, SB 4 requires operators to obtain specific well stimulation permits, make disclosures and implement groundwater monitoring and water management plans. The U.S. Environmental Protection Agency (EPA) and the BLM also regulate certain well stimulation activities, though their regulations are currently being challenged in court. The implementation of federal and state well stimulation regulations has delayed, and increased the cost of, certain operations.

In addition, certain local governments have proposed or adopted ordinances that would regulate certain drilling activities in general and well stimulation or completion activities in particular, or ban such activities outright. The most onerous of these local measures was adopted by Monterey County in November 2016, where we own mineral interests but do not have production. The measure, which is currently stayed during a legal challenge, would prohibit drilling of new oil and gas wells, hydraulic fracturing and other well stimulation and phase out water injection.

Regulation of Health, Safety and Environmental Matters

Numerous federal, state, local, and other laws and regulations that govern health and safety, the release or discharge of materials, land use or environmental protection may restrict the use of our properties and operations, increase our costs or lower demand for or restrict the use of our products and services. Applicable federal health, safety and environmental laws include, but are not limited to, the Occupational Safety and Health Act, Clean Air Act, Clean Water Act, Safe Drinking Water Act, Oil Pollution Act, Natural Gas Pipeline Safety Act, Pipeline Safety Improvement Act, Pipeline Safety, Regulatory Certainty, and Job Creation Act, Endangered Species Act, Migratory Bird Treaty Act, Comprehensive Environmental Response, Compensation, and Liability Act, Resource Conservation and Recovery Act and National Environmental Policy Act. California imposes additional laws that are analogous to, and often more stringent than, such federal laws. The foregoing laws and regulations:

• | establish air, soil and water quality standards for a given region, such as the San Joaquin Valley, and attainment plans to meet those regional standards, which may include significant restrictions on development, economic activity and transportation in such region; |

• | require various permits and approvals before drilling, workover, production, underground fluid injection or waste disposal commences, or before facilities are constructed or put into operation; |

• | require the installation of sophisticated safety and pollution control equipment, such as leak detection, monitoring and shutdown systems, to prevent or reduce releases or discharges of regulated materials to air, land, surface water or ground water; |

• | restrict the use, types or sources of water, energy, land surface, habitat or other natural resources, require conservation and reclamation measures, and impose energy efficiency or renewable energy standards; |

• | restrict the types, quantities and concentrations of regulated materials, including oil, natural gas, produced water or wastes, that can be released or discharged into the environment, or any other uses of those materials resulting from drilling, production, processing, power generation or transportation activities; |

• | limit or prohibit operations on lands lying within coastal, wilderness, wetlands, groundwater recharge, endangered species habitat and other protected areas, and require the dedication of surface acreage for habitat conservation; |

• | establish standards for the closure, abandonment, cleanup or restoration of former operations, such as plugging and abandonment of wells and decommissioning of facilities; |

• | impose substantial liabilities for unauthorized releases or discharges of regulated materials into the environment with respect to our current or former properties and operations and other locations where such materials generated by us or our predecessors were released or discharged; |

• | require comprehensive environmental analyses, recordkeeping and reports with respect to operations affecting federal, state and private lands or leases; |

• | impose taxes or fees with respect to the foregoing matters; |

• | may expose us to litigation with government authorities, counterparties, special interest groups or others; and |

• | may restrict our rate of oil, NGLs, natural gas and electricity production. |

15

Due to the severe drought in California over the last several years, water districts and the state government are implementing regulations and policies that may restrict groundwater extraction and water usage and increase the cost of water. Water management is an essential component of our operations. We treat and re–use water that is co-produced with oil and natural gas for a substantial portion of our needs in activities such as pressure management, waterflooding, steamflooding and well drilling, completion and stimulation, and we provide reclaimed produced water to certain agricultural water districts. We also use supplied water from various local and regional sources, particularly for power plants and to support operations like steam injection in certain fields.

In 2014, at the request of the EPA, DOGGR commenced a detailed review of the multi-decade practice of permitting underground injection wells and associated aquifer exemptions under the Safe Drinking Water Act (SDWA). In 2015, the state set deadlines to obtain the EPA’s confirmation of aquifer exemptions under the SDWA in certain formations in certain fields, and those deadlines are currently being challenged in court. Since the state and the EPA did not complete their review before the state's deadlines, the state has announced that it will not rescind permits or enforce the deadlines with respect to many of the formations pending completion of the review, but plans to apply the deadlines to others. During the review, the state has restricted injection in certain formations or wells in several fields, including some operated by us. To date, such restrictions have not affected our oil and natural gas production in any material way. Separately, the state began a review in 2015 of permitted surface discharge of produced water and the use of reclaimed water for agricultural irrigation. Government authorities may ultimately restrict injection of produced water or other fluids in additional formations or certain wells, restrict the surface discharge or use of produced water or take other administrative actions. The foregoing reviews could also give rise to litigation with government authorities and third parties.

Federal, state and local agencies may assert overlapping authority to regulate in these areas. In addition, certain of these laws and regulations may apply retroactively and may impose strict or joint and several liability on us for events or conditions over which we and our predecessors had no control, without regard to fault, legality of the original activities, or ownership or control by third parties.

Regulation of Climate Change and Greenhouse Gas (GHG) Emissions

A number of international, federal, state and regional efforts seek to prevent or mitigate the effects of climate change or to track or reduce GHG emissions associated with energy use and industrial activity, including operations of the oil and natural gas production sector and those who use our products as a source of energy. The EPA has adopted federal regulations to:

• | require reporting of annual GHG emissions from power plants and gas processing plants; gathering and boosting compression and pipeline facilities; and certain completions and workovers; |

• | incorporate measures to reduce GHG emissions in permits for certain facilities; and |

• | restrict GHG emissions from certain mobile sources. |

California has adopted the most stringent such laws and regulations. These state laws and regulations:

• | established a “cap-and-trade” program for GHG emissions that sets a statewide maximum limit on total GHG emissions, and this cap declines annually to reach 1990 levels by 2020, the year that the cap-and-trade program currently expires; |

• | require allowances or qualifying offsets for GHGs emitted from California operations and for the volume of propane and liquid transportation fuels sold for use in California, for which allowances we incurred costs of approximately $33 million in 2016; |

• | require refiners to reduce the carbon content of transportation fuels they market in California by 10% by 2020; |

• | impose a more stringent state goal of reducing GHG emissions to 40% below 1990 levels by 2030 by reducing industrial source emissions, even if the cap-and-trade program is not extended; |

• | impose state goals to derive 50% of California’s electricity from renewable sources and to double the energy efficiency of buildings in the state by 2030; and |

• | impose state goals of reducing emissions of methane and fluorocarbon gases by 40% and black carbon by 50% below 2013 levels by 2030. |

16

The EPA and the California Air Resources Board (CARB) have also expanded direct regulation of methane emissions. In 2016, the EPA adopted regulations to require additional emission controls for methane, volatile organic compounds and certain other substances for new or modified oil and natural gas facilities and announced its intent to propose controls on methane emissions from existing sources. CARB has also proposed regulations to require monitoring, leak detection, repair and reporting of methane emissions from oil and gas production operations beginning in 2018 and additional controls such as vapor recovery to capture methane emissions in subsequent years.

Regulation of Transportation, Marketing and Sale of Our Products

Our sales prices of oil, NGLs and natural gas in the U.S. are set by the market and are not presently regulated. In late 2015, the U.S. federal government lifted restrictions on the export of domestically produced oil that allows for the sale of U.S. oil production, including ours, in additional markets, which may affect the prices we realize.

Federal and state laws regulate transportation rates for, and marketing and sale of, petroleum products and electricity with respect to certain of our operations and those of certain of our customers, suppliers and counterparties. Such regulations also govern:

• | interstate and intrastate pipeline transportation rates for oil, natural gas and NGLs in regulated pipeline systems; |

• | prevention of market manipulation in the oil, natural gas, NGL and power markets; |

• | market transparency rules with respect to natural gas and power markets; |

• | the physical and futures energy commodities market, including financial derivative and hedging activity; and |

• | prevention of discrimination in natural gas gathering operations in favor of producers or sources of supply. |

The federal and state agencies overseeing these regulations have substantial rate-setting and enforcement authority, and violation of the foregoing regulations could expose us to litigation with other government authorities, counterparties, special interest groups and others.

Employees

Our future success will depend partially on our ability to attract, retain and motivate qualified employees. We also utilize the services of independent contractors to perform drilling, well work, operations, construction and other services, including construction contractors whose workforce is often represented by labor unions. Approximately 75 of our employees are represented by labor unions. We have not experienced any strikes or work stoppages by our employees in the past 36 years or longer.

At the time of our Spin-off, we had over 2,000 employees. In the third quarter of 2015 and early 2016, we implemented a voluntary retirement program and other employee actions to align our workforce with our view of the commodity price environment. We ended 2016 with approximately 1,450 employees, representing a nearly 30% reduction mainly through attrition and the 2015 and 2016 employee actions.

Effective January 1, 2015, we adopted the California Resources Corporation 2014 Employee Stock Purchase Plan (ESPP). The ESPP provides our employees the ability to purchase shares of our common stock at a price equal to 85% of the closing price of a share of our common stock as of the first or last day of each fiscal quarter, whichever amount is less. At January 1, 2017, over one quarter of our employees had elected to participate in the plan.

17

Available Information

We make the following information available free of charge on our website at www.crc.com:

• | Forms 10-K, 10-Q, 8-K and amendments to these forms as soon as reasonably practicable after they are electronically filed with, or furnished to, the Securities and Exchange Commission (SEC); |

• | Other SEC filings including Forms 3, 4 and 5; and |

• | Corporate governance information, including our corporate governance guidelines, board-committee charters and code of business conduct (see Part III, Item 10, of this report for further information). |

Information contained on our website is not part of this report.

ITEM 1A | RISK FACTORS |

RISK FACTORS

We are subject to certain risks and hazards due to the nature of our business activities. The risks discussed below, any of which could materially and adversely affect our business, financial condition, cash flows and results of operations, are not the only risks we face. We may experience additional risks and uncertainties not currently known to us or, as a result of developments occurring in the future, conditions that we currently deem to be immaterial may ultimately materially and adversely affect our business, financial condition, cash flows and results of operations.

Risks Related to Our Business and Industry

Commodity pricing can fluctuate widely and strongly affects our results of operations, financial condition, cash flow and ability to grow.

Our financial results, financial condition, cash flow and ability to grow correlate closely to the prices we obtain for our products. Compared to the 2014 average, global energy commodity prices have declined significantly. For example, Brent crude prices declined from over $110 per barrel in June 2014 to below $30 per barrel in January 2016. While prices remain lower than the 2014 and 2015 averages, they have improved modestly since early 2016. However, such improvements may not continue or may be reversed. Continued low prices for our products or further price decreases could have several adverse effects including:

• | reduced cash flow and decreased funds available for capital investments, interest payments and operational expenses; |

• | reduced proved oil and gas reserves over time and related cash flows; |

• | impairments of our oil and gas properties such as we experienced in 2014 and 2015; |

• | reduced borrowing base capacity under our first-out revolving credit facility as proved oil and gas reserves values fall; |

• | the potential for a reduction of our liquidity, mandatory loan repayments and default and foreclosure by our banks and bondholders against our secured assets; |

• | inability to attract counterparties to our transactions, including hedging transactions; and |

• | inability to access funds through the capital markets and the price we could obtain for, or our ability to conduct, asset sales or other monetization transactions. |

Commodity pricing can fluctuate widely and is affected by a variety of factors, including changes in consumption patterns; inventory levels; global and local economic conditions; the actions of OPEC and other significant producers and governments; actual or threatened production, refining and processing disruptions; worldwide drilling and exploration activities; the effects of conservation; weather, geophysical and technical limitations; currency exchange rates; technological advances and regional market conditions; transportation capacity, bottlenecks and costs in producing areas; alternative energy sources; other matters affecting the supply and demand dynamics for our products; and the effect of changes in these variables on market perceptions. These and other factors make it impossible to predict realized prices reliably. While our hedging activities provide some protection for a significant portion of our 2017 production, they may not adequately protect us from commodity price reductions and we may be unable to enter into acceptable additional hedges.

18

Our lenders require us to comply with covenants and can limit our borrowing capabilities, which may materially limit our ability to use or access capital and our business activities.

Our ability to borrow funds under our reserves-based first-lien first-out credit facilities is limited by the size of our lenders' commitments, our ability to comply with their covenants, our borrowing base and a minimum monthly liquidity requirement. At January 31, 2017, the lenders' commitments under our first-out facilities were $2.05 billion, and we had approximately $486 million in availability, subject to the minimum liquidity requirement. We may need to depend on our revolving credit facility for a portion of our future capital or operating needs.

The financial covenants that we must satisfy under our first-out facilities include quarterly first-out leverage and interest expense coverage ratios, as well as a semi-annual first-lien asset coverage ratio. The first-out facilities also restrict our ability to monetize assets and issue or purchase debt as a means of complying with our financial covenants. Our borrowing base under our first-out facilities, which currently exceeds lender commitments, is redetermined each May 1 and November 1. The borrowing base is determined with reference to a number of factors, including commodity prices and reserves. Restrictions under our first-out credit facilities are further described in "Management's Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources – Credit Facilities."

If we were to breach any of the covenants under our first-out facilities, our lenders would be permitted to accelerate the principal amount due under the first-out facilities and foreclose against the assets securing them. If payment were accelerated, or we failed to make certain payments, under our first-out facilities, it would result in a default under our second-out credit facility and outstanding notes and permit acceleration and foreclosure against the assets securing the second-out credit facility and the secured notes.

Low commodity prices, coupled with substantial interest payments, could constrain our liquidity. A significant reduction in our liquidity may force us to take actions which could have significant adverse effects.

The primary source of liquidity and resources to fund our capital program and other obligations is cash flow from operations and borrowings under our revolving credit facility. As noted above, our borrowing capacity is limited.

Further price declines would reduce our cash flows from operations and may limit our access to borrowing capacity or cause default under our credit facilities or notes. Under these conditions, if we were unable to achieve improved liquidity through additional financing, asset monetizations, restructuring of our debt obligations, equity issuances or otherwise, cash flow from operations and expected available credit capacity could be insufficient to meet our commitments. Successfully completing these actions could have significant adverse effects such as higher operating and financing costs, loss of certain tax attributes or dilution of equity. For example, our repurchases of unsecured notes in 2016 resulted in the elimination of federal net operating losses. In 2016, we incurred debt under a second-out credit facility that, together with our 2015 exchange, increased our annual interest expense.

We have significant indebtedness and may incur more debt. Higher levels of indebtedness could make us more vulnerable to economic downturns and adverse developments in our business or otherwise limit our operational flexibility.

As of December 31, 2016, we had $5.3 billion of consolidated indebtedness comprised of senior unsecured notes, second lien secured notes and first-out and second-out secured credit facility borrowings.

Our credit facilities and the indentures governing our outstanding notes permit us to incur significant additional indebtedness as well as certain defined obligations unrestricted by debt incurrence or lien covenants, or that do not constitute indebtedness. To the extent we need to incur indebtedness above amounts permitted by our credit facilities, we may seek amendments or waivers.

Indebtedness outstanding under our first-out and second-out facilities bears interest at variable rates, therefore a rise in interest rates will generate greater interest expense to the extent we do not purchase interest rate hedges.

19

Our level of indebtedness may have several important consequences, including, without limitation:

• | jeopardizing our ability to execute our business plans; |

• | increasing our vulnerability to adverse changes in our business and in economic and industry conditions generally, and putting us at a disadvantage against competitors that have lower fixed obligations and more cash flow to devote to their businesses; |

• | limiting our ability to obtain additional financing for working capital, capital investments and general corporate and other purposes or increasing the cost of that capital; and |

• | limiting our flexibility to operate our business, compete for capital, react to competitive pressures, address adverse regulatory changes and engage in certain transactions that might otherwise be beneficial to us. |

The terms of the credit facilities and note indentures may limit, among other things:

• | incurrence of additional indebtedness; |

• | investments; |

• | amounts and types of joint ventures; |

• | restricted payments; |

• | creation of liens on our assets; |

• | sales of assets that constitute collateral; |

• | application of the full proceeds of asset sales other than to pay down debt; |

• | mergers or acquisitions; and |

• | release of collateral. |

These limitations are further described in "Management's Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources – Credit Facilities; Senior Notes" and the documents governing our indebtedness that are filed with the Securities and Exchange Commission (SEC).

Our ability to meet our debt obligations and other financial needs will depend on our future performance or our ability to further reduce our debt, which will be affected by market, financial, business, economic, regulatory and other factors. If our cash flow is not sufficient to service our debt, we may be required to refinance debt, sell assets or sell additional equity on terms that may be unattractive, if it can be done at all. Further, our failure to comply with the financial and other restrictive covenants relating to our indebtedness could result in a default. Any of these factors could result in a material adverse effect on our business, financial condition, cash flows or results of operations and a default on our indebtedness could result in acceleration of all of our debt and foreclosure against assets constituting collateral for our secured credit facilities and secured notes.

Our business requires substantial capital investments, which may include acquisitions. We may be unable to fund these investments through operating cash flow or obtain any needed additional capital on satisfactory terms or at all, which could lead to a decline in our oil and gas reserves or production. Our capital investment program is also susceptible to risks that could materially affect its implementation.