Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - SENSIENT TECHNOLOGIES CORP | ex32.htm |

| EX-31 - EXHIBIT 31 - SENSIENT TECHNOLOGIES CORP | ex31.htm |

| EX-23.1 - EXHIBIT 23.1 - SENSIENT TECHNOLOGIES CORP | ex23_1.htm |

| EX-21 - EXHIBIT 21 - SENSIENT TECHNOLOGIES CORP | ex21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

☒

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Fiscal Year Ended December 31, 2016

OR

|

☐

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Commission File Number 1-7626

Sensient Technologies Corporation

|

WISCONSIN

|

39-0561070

|

|

|

(State of Incorporation)

|

(IRS Employer Identification Number)

|

777 EAST WISCONSIN AVENUE

MILWAUKEE, WISCONSIN 53202-5304

(414) 271-6755

(Address of Principal Executive Offices)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

|

TITLE OF EACH CLASS

Common Stock, $0.10 par value

|

NAME OF EACH EXCHANGE

ON WHICH REGISTERED

|

|

|

New York Stock Exchange, Inc.

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for at least the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer ☒

|

Accelerated filer ☐

|

Non-accelerated filer ☐

|

Smaller Reporting Company ☐

|

Indicate by check mark if the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting Common Stock held by non-affiliates of the Registrant as of June 30, 2016, was $3,147,125,310. For purposes of this computation only, the Registrant’s directors and executive officers were considered to be affiliates of the Registrant. Such characterization shall not be construed to be an admission or determination for any other purpose that such persons are affiliates of the Registrant.

There were 44,359,946 shares of Common Stock outstanding as of February 16, 2017.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s 2017 Annual Meeting Proxy Statement which will be filed with the Securities and Exchange Commission within 120 days after December 31, 2016 (see Part III of this Form 10-K).

|

3

|

|||

|

3

|

|||

|

3

|

|||

|

3

|

|||

|

4

|

|||

|

4

|

|||

|

5

|

|||

|

5

|

|||

|

5

|

|||

|

5

|

|||

|

5

|

|||

|

6

|

|||

|

6

|

|||

|

6

|

|||

|

6

|

|||

|

6

|

|||

|

6

|

|||

|

9

|

|||

|

9

|

|||

|

10

|

|||

|

10

|

|||

|

11

|

|||

|

12

|

|||

|

12

|

|||

|

14

|

|||

|

17

|

|||

|

30

|

|||

|

30

|

|||

|

30

|

|||

|

30

|

|||

|

31

|

|||

|

31

|

|||

|

31

|

|||

|

31

|

|||

|

31

|

|||

|

31

|

|||

|

31

|

|||

|

32

|

|||

|

32

|

|||

|

32

|

|||

|

32

|

|||

|

60

|

|||

|

32

|

|||

|

S-1

|

|||

|

E-1

|

|||

FORWARD-LOOKING STATEMENTS

This document contains forward-looking statements that reflect management’s current assumptions and estimates of future economic circumstances, industry conditions, Company performance and financial results. Forward-looking statements include statements in the future tense, statements referring to any period after December 31, 2016, and statements including the terms “expect,” believe,” “anticipate” and other similar terms that express expectations as to future events or conditions. The Private Securities Litigation Reform Act of 1995 provides a safe harbor for such forward-looking statements. Such forward-looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties and other factors that could cause actual events to differ materially from those expressed in those statements. A variety of factors could cause the Company’s actual results and experience to differ materially from the anticipated results. These factors and assumptions include the pace and nature of new product introductions by the Company and the Company’s customers; our ability to anticipate and respond to changing consumer preferences and changing technologies; the Company’s ability to successfully implement its growth strategies; the outcome of the Company’s various productivity-improvement and cost-reduction efforts and acquisition and divestiture activities; the effectiveness of the Company’s restructuring activities; changes in costs of raw materials, including energy; industry, regulatory and economic factors related to the Company’s domestic and international business; growth in markets for products in which the Company competes; industry and customer acceptance of price increases; actions by competitors; currency exchange rate fluctuations; and the matters discussed below under the heading “Risk Factors” and under Part II, including the critical accounting policies set forth under the heading “CRITICAL ACCOUNTING POLICIES” within “Management’s Discussion and Analysis of Financial Condition and Results of Operation.” Except to the extent required by applicable law, the Company does not undertake to publicly update or revise its forward-looking statements even if experience or future changes make it clear that any projected results expressed or implied therein will not be realized.

NON-GAAP FINANCIAL MEASURES

Within this document, the Company reports certain non-GAAP financial measures, including: (1) adjusted operating income, adjusted net earnings and adjusted diluted EPS from continuing operations (which exclude restructuring and other costs) and (2) percentage changes in revenue, operating income, diluted EPS, adjusted operating income and adjusted diluted EPS on a local currency basis (which eliminate the effects that result from translating its international operations into U.S. dollars). The Company has included each of these non-GAAP measures in order to provide additional information regarding our underlying operating results and comparable year-over-year performance. Such information is supplemental to information presented in accordance with GAAP and is not intended to represent a presentation in accordance with GAAP. These non-GAAP measures should not be considered in isolation. Rather, they should be considered together with GAAP measures and the rest of the information included in this report. Management internally reviews each of these non-GAAP measures to evaluate performance on a comparative period-to-period basis and to gain additional insight into underlying operating and performance trends, and the Company believes the information can be beneficial to investors for the same purposes. These non-GAAP measures may not be comparable to similarly titled measures used by other companies.

Additional information related to the Company’s use of non-GAAP financial measures and the restructuring and other costs excluded from the non-GAAP financial measures in 2016, 2015 and 2014 and reconciliations of non-GAAP financial measures to the most comparable GAAP financial measures are available below in Item 7 under the sections titled “NON-GAAP FINANCIAL MEASURES.”

Sensient Technologies Corporation (the “Company”) was incorporated in 1882 in Wisconsin. Its principal executive offices are located at 777 East Wisconsin Avenue, Suite 1100, Milwaukee, Wisconsin 53202-5304, telephone (414) 271-6755.

The Company is subject to the informational and reporting requirements of the Securities Exchange Act of 1934, as amended (the “Act”), and, in accordance with the Act, files annual, quarterly and current reports, proxy statements and other information with the Securities and Exchange Commission (the “Commission”). These reports and other information may be read and copied at the public reference facilities of the Commission at its principal offices at 100 F Street, N.E., Washington, D.C. 20549, and can also be accessed from the website maintained by the Commission at http://www.sec.gov. The public may obtain information on operations of the public reference room by calling the Commission at (800) SEC-0330.

The Company’s common stock is listed on the New York Stock Exchange under the ticker symbol “SXT.” Information about the Company may be obtained at the offices of the New York Stock Exchange, 20 Broad Street, New York, New York 10005.

The Company can also be reached at its website at www.sensient.com. The Company’s web address is provided as an inactive textual reference only, and the contents of that website are not incorporated in or otherwise to be regarded as part of this report. The Company makes available free of charge on its website its proxy statement, its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Act as soon as reasonably practicable after such documents are electronically filed with or furnished to the Commission. Charters for the Audit, Compensation and Development, Nominating and Corporate Governance, Finance and Executive Committees of the Company’s Board of Directors, as well as the Company’s Code of Conduct, Corporate Governance Guidelines, Policy on Recovery of Incentive Compensation From Executives and Directors and Officers Stock Ownership Guidelines are also available on the Company’s website, and are available in print to any shareholder, free of charge, upon request. If there are any amendments to the Code of Conduct or the Corporate Governance Guidelines, or if waivers from any of them are granted for executive officers or directors, those amendments or waivers also will be posted on the Company’s website.

The Company is a leading global manufacturer and marketer of colors, flavors and fragrances. The Company uses advanced technologies at facilities around the world to develop specialty food and beverage systems, cosmetic and pharmaceutical systems, specialty inks and colors, and other specialty and fine chemicals. The Company’s customers include major international manufacturers representing some of the world’s best-known brands.

The Company’s principal products include:

| ● |

flavors, flavor enhancers, ingredients and bionutrients;

|

| ● |

fragrances, aroma chemicals and essential oils;

|

| ● |

natural ingredients, including dehydrated vegetables and other food ingredients;

|

| ● |

natural and synthetic food and beverage colors;

|

| ● |

cosmetic colors and ingredients; pharmaceutical excipients and ingredients; and

|

| ● |

technical colors, specialty inks and colors, and specialty dyes and pigments.

|

The Company’s three reportable segments are the Flavors & Fragrances Group and the Color Group, which are managed on a product-and-services basis, and the Asia Pacific Group, which is managed on a geographic basis. The Company’s corporate expenses and restructuring and certain other costs are included in the “Corporate & Other” category as described in this report. Financial information regarding the Company’s three reportable segments and the operations included within Corporate & Other is set forth in Note 11, Segment and Geographic Information in the Notes to Consolidated Financial included in this report.

In 2014, the Company announced and began a restructuring plan related to eliminating underperforming operations, consolidating manufacturing facilities and improving efficiencies within the Company, with an emphasis on the Flavors & Fragrances Group. Additional information regarding the costs related to the implementation of restructuring plan is set forth below under the heading “Restructuring”.

The Company is a global developer, manufacturer and supplier of flavor and fragrance systems for the food, beverage, personal care and household-products industries. The Company’s flavor formulations are used in many of the world’s best-known consumer products. Under the unified brand names of Sensient Flavors, Sensient Natural Ingredients and Sensient Fragrances, the Group is a supplier to multinational companies.

The Flavors & Fragrances Group produces flavor and fragrance products that impart a desired taste, texture, aroma and/or other characteristics to a broad range of consumer and other products. This Group includes the Company’s natural ingredients business, which produces ingredients for food processors. The main products of the Group are systems products, including flavor-delivery systems, and compounded and blended products. In addition, the Group has strong positions in selected ingredient products such as essential oils, natural and synthetic flavors and aroma chemicals. The Group serves food and non-food industries. In food industries, markets include savory, beverage and sweet flavors. In non-food industries, the Group supplies fragrance products to the personal and home-care markets.

Operating through its Sensient Natural Ingredients business, the Company believes it is the second largest producer (by sales) of dehydrated onion and garlic products in the United States. The Company is also one of the largest producers and distributors of chili powder, paprika, chili pepper and dehydrated vegetables such as parsley, celery and spinach. Domestically, the Company sells dehydrated products to food manufacturers for use as ingredients and also for repackaging under private labels for sale to the retail market and to the food service industry. Advanced dehydration technologies utilized by Sensient Natural Ingredients permit fast and effective rehydration of ingredients used in many of today’s popular convenience foods.

The Flavors & Fragrances Group operates principally through the Company’s subsidiaries Sensient Flavors LLC and Sensient Natural Ingredients LLC. As of December 31, 2016, the Group’s principal manufacturing plants are located in California, Illinois, Michigan, Wisconsin, Belgium, China, Costa Rica, France, Mexico, the Netherlands, Spain and the United Kingdom.

The Company is a developer, manufacturer and supplier of colors for businesses worldwide. The Company provides natural and synthetic color systems for use in foods, beverages and pharmaceuticals; colors and other ingredients for cosmetics, such as active ingredients, solubilizers and surface treated pigments; pharmaceutical excipients, such as colors, flavors and coatings; specialty inks; and technical colors for industrial applications.

The Company believes that it is one of the world’s largest producers (by sales) of synthetic and natural colors, and that it is the world’s largest manufacturer (by sales) of certified food colors. The Company sells its synthetic and natural colors to domestic and international producers of beverages, bakery products, processed foods, confections, pet foods, cosmetics and pharmaceuticals. The Company also makes industrial colors, specialty inks and other dyes and pigments used in a variety of non-food applications.

The Color Group operates principally through the Company’s subsidiary Sensient Colors LLC. As of December 31, 2016, the Group’s principal manufacturing plants are located in Missouri, New Jersey, Brazil, Canada, China, France, Germany, Italy, Mexico, Switzerland and the United Kingdom.

The Color Group operates under the following trade names:

| ● |

Sensient Food Colors (food and beverage colors);

|

| ● |

Sensient Pharmaceutical Coating Systems (pharmaceutical colors and coatings);

|

| ● |

Sensient Cosmetic Technologies (cosmetic colors and ingredients and systems);

|

| ● |

Sensient Inks (specialty inks); and

|

| ● |

Sensient Industrial Colors (paper colors; and industrial colors for plastics, leather, wood stains, antifreeze and other uses).

|

The Company believes that its advanced process technology, state-of-the-art laboratory facilities and equipment, world class application chemists and a complete range of synthetic and natural color products constitute the basis for its market leadership position.

Beginning in the first quarter of 2016, the results of operations for the Company’s color business in China, South Korea and Japan, which were previously reported in the Asia Pacific segment, are now reported in the Color segment. All prior year results have been restated to reflect these changes.

The Asia Pacific Group focuses on marketing the Company’s diverse product line in the Pacific Rim under the Sensient name. Through these operations, the Company offers a full range of products from its Flavors & Fragrances Group and Color Group, as well as products developed by regional technical teams to appeal to local preferences.

Sales, marketing and technical functions are managed through the Asia Pacific Group’s headquarters in Australia. Manufacturing operations are located in Australia, China, Japan, New Zealand and the Philippines. The Asia Pacific Group maintains offices for local technical support, as well as sales, in China, India, Indonesia, Korea and Thailand, and for research and development in Singapore.

Corporate provides management, administrative and support services to the Company from its headquarters in Milwaukee, Wisconsin. The Company’s corporate expenses and restructuring and other costs are included in the “Corporate & Other” category.

The development of specialized products and services is a complex technical process calling upon the combined knowledge and talents of the Company’s research, development and quality assurance personnel. The Company believes that its competitive advantage lies in its ability to work with its customers to develop and deliver high-performance products that address the distinct needs of those customers.

The Company’s research, development and quality assurance personnel support the Company’s efforts to improve existing products and develop new products tailored to customer needs, while providing on-going technical support and know-how to the Company’s manufacturing activities. The Company employed 722 people in research and development, quality assurance, quality control and lab technician positions as of December 31, 2016.

Expenditures for research and development related to continuing operations in calendar year 2016 were $40.9 million, compared with $35.1 million in the year ended December 31, 2015, and $35.9 million in the year ended December 31, 2014. As part of its commitment to quality as a competitive advantage, the Company’s production facilities hold various certifications, such as those under the International Organization for Standardization (ISO) and those recognized by the Global Food Safety Initiative (GFSI), including the Safe Quality Food Program (SQF), British Retail Consortium (BRC), Food Safety System Certification (FSSC 22000) and International Featured Standards (IFS), for certifying the safety and quality of its products and production processes.

The Company’s strategic focus is on the manufacture and marketing of high-performance components that bring life to products. Accordingly, the Company devotes considerable attention and resources to the development of product applications and processing improvements to support its customers’ numerous new and reformulated products. The majority of the proprietary processes and formulae developed by the Company are maintained as trade secrets and under confidentiality agreements with customers.

Within the Flavors & Fragrances Group, development activity is focused on ingredients, flavors and fragrances as well as flavor and fragrance systems that are responsive to consumer trends and the processing needs of our food and beverage customers. These activities include the development of functional ingredient systems for foods and beverages, savory flavors, and ingredient systems for prepared foods and flavors and ingredients for dairy, confectionery and other applications. The Company believes that the development of yeast derivatives and other specialty ingredients also provides growth opportunities in bionutrients and biotechnology markets, such as pharmaceuticals, vitamins, vaccines and bioremediation.

Within the Color Group, development activity for food and beverage product lines is focused on value-added products derived from synthetic dyes and pigments and natural food and beverage colors and on color systems. The Company also produces a diverse line of colors and ingredients for cosmetics and pharmaceutical applications and technical colors for industrial applications.

The Company uses a wide range of raw materials in producing its products. Chemicals used to produce certified colors are obtained from several domestic and foreign suppliers. Raw materials for natural colors, such as carmine, beta-carotene, annatto and turmeric, are purchased from overseas and U.S. sources.

In the production of flavors and fragrances, the principal raw materials include essential oils, aroma chemicals, botanicals, fruits and juices, and are obtained from domestic and foreign suppliers. Flavor enhancers and secondary flavors are produced from brewers’ yeast and vegetable materials such as corn and soybeans. Chili peppers, onion, garlic and other vegetables are acquired under annual contracts with numerous growers in the western United States and Europe. The Company has expanded its sources of vegetables to include growers in China.

The Company believes that its ability to reformulate its products and the general availability of alternate sources of materials would enable it to maintain its competitive position in the event of an interruption in the supply of raw materials from a single supplier.

All Company products are sold in highly competitive markets. While no single factor is determinative, the Company’s competitive position is based principally on process and applications expertise, quality, technological advances resulting from its research and development, and customer service and support. Because of its highly differentiated products, the Company competes with only a few companies across multiple product lines, and is more likely to encounter competition specific to a particular product line.

| · |

Flavors & Fragrances. Competition to supply the flavors and fragrances industries has taken on an increasingly global nature. Most of the Company’s customers do not buy their entire flavor and/or fragrance products from a single supplier and the Company does not compete with a single supplier in all product categories. Competition for the supply of flavors and fragrances is based on the development of customized ingredients for new and reformulated customer products, as well as on quality, customer service and price. Competition to supply dehydrated vegetable products is present through several large and small domestic competitors, as well as competitors in other countries. Competition for the supply of dehydrated vegetables is based principally on product quality, customer service and price.

|

| · |

Color. Competition in the color market is diverse, with the majority of the Company’s competitors specializing in either synthetic dyes and pigments or natural colors. The Company believes that it gains a competitive advantage as the only major basic manufacturer of a full range of color products, including synthetic dyes and pigments as well as natural colors. Competition in the supply of cosmetic colors and ingredients, specialty inks and pharmaceutical excipients is based on the development of customized products and solutions as well as quality, customer service and price. The Company believes that its reputation and capacity as a color producer as well as its product development give it a competitive advantage in these markets.

|

| · |

Asia Pacific. Because of the broad array of products available to customers of the Asia Pacific Group, the Company believes that it is able to offer a wider product base than many of its competitors. Competition is based upon reliability in product quality, service and price as well as technical support available to customers.

|

Additional information regarding the Company’s foreign operations is set forth in Note 11, Segment and Geographic Information in the Notes to Consolidated Financial Statements included in this report.

The Company owns or controls many patents, formulae and trademarks related to its businesses. The businesses are not materially dependent upon any particular patent or trademark; however, trademarks, patents and formulae are important to the business of the Company.

As of December 31, 2016, the Company employed 4,083 persons worldwide.

Compliance with government provisions regulating discharges into the environment, or otherwise relating to the protection of the environment, did not have a material adverse effect on the Company’s operations for the year covered by this report. Current compliance is not expected to have a material adverse effect in the next two years. The production, packaging, labeling and distribution of certain of the products of the Company in the U.S. are subject to the regulations of various federal, state and local governmental agencies, in particular the U.S. Food and Drug Administration. The Company is subject to similar regulations in many international markets.

As with any business, the Company’s business and operations involve risks and uncertainties. In addition to the other discussions in this report, particularly those under the headings “Management’s Discussion & Analysis of Operations & Financial Condition” and “Forward-Looking Statements” above, the following factors should be considered:

| · |

Our recent restructurings may not be as effective as we anticipate and we may fail to realize the expected cost savings.

|

During 2013, 2014, 2015 and 2016, we announced and engaged in various restructuring activities. These activities require the devotion of significant resources and management attention and may pose significant risks. Our ability to realize anticipated cost savings may be affected by a number of factors, including our ability to effectively reduce overhead, rationalize manufacturing capacity and shift production to more efficient facilities. Furthermore, our restructurings may not be as effective as we anticipate, and we may fail to realize the cost savings we expect from these restructurings. Actual charges, costs and adjustments due to restructuring activities may vary materially from our estimates and our restructuring activities may require cash and non-cash costs or charges in excess of budgeted amounts, which could reduce anticipated cost savings and could have an adverse effect on our margins and earnings.

| · |

The impact of currency exchange rate fluctuation may negatively affect our results.

|

We report the results of our foreign operations in the applicable local currency and then translate those results into U.S. dollars at applicable exchange rates. The applicable exchange rates between and among local currencies, foreign currencies and the U.S. dollar have fluctuated and will continue to do so in the future. These fluctuations have impacted our results of operations in recent periods as discussed in more detail in Management’s Discussion and Analysis of Financial Condition and Results of Operations in this annual report on Form 10-K. Such currency exchange rate volatility may also adversely impact our financial condition or liquidity. While we may use forward exchange contracts and foreign currency denominated debt to manage our exposure to foreign exchange risk, such risk management strategies may not be effective and our results of operations could be adversely affected.

| · |

In some product lines, most of our sales are made to a relatively small number of customers; if we lose any of those customers, sales and operating results could decline.

|

In some of our product lines, our sales are concentrated to a small number of customers. While we do not currently have any single customer that we consider to be significant to us as a whole, the loss of a significant customer of a product line could substantially affect the sales and profitability of that line, which may cause us to re-evaluate that line. Those developments could affect our results. In addition, the financial condition of our customers may adversely affect their ability to buy from us or to pay for products that they have already purchased.

| · |

Many of our products are used in items for human consumption and contact. We may be subject to product liability claims and product recalls, which could negatively impact our profitability and corporate image.

|

We sell flavors, fragrances and colors which are used in foods, beverages, pharmaceuticals, cosmetics and other items for human consumption or contact. These products involve risks such as product contamination or spoilage, product tampering and other adulteration. We may be subject to liability if the consumption or use of our flavors, fragrances and colors, or products which incorporate ingredients we manufacture, cause injury, illness or death. In addition, we or our customers may need to recall products in the event of contamination or damage.

A significant product defect, product liability judgment or product recall may negatively impact our profitability for a period of time depending on publicity, product availability, scope, competitive reaction and consumer attitudes. Even if a product liability claim is unsuccessful or is not fully pursued, the negative publicity surrounding any assertion that our products caused illness, injury or death could adversely affect our reputation with existing and potential customers and our corporate image.

| · |

Consolidation has resulted in customers with increased buying power, which can affect our profitability.

|

Many of our customers have consolidated in recent years and we expect the combination trend to continue. These consolidations have often produced large, sophisticated customers with increased buying power who are more capable of resisting price increases. If the larger size or greater buying power of those customers results in additional negotiating strength, the prices we are able to charge could be negatively affected and our profitability could decline.

| · |

Intense competition may result in reduced sales and profitability.

|

The industries and markets in which we operate are highly competitive. That competition can reduce both our sales and the prices at which we are able to sell our products, which can negatively affect our profitability.

| · |

Our sales and profitability are affected by changing consumer preferences and changing technologies.

|

Although we do not generally make or sell proprietary consumer products, many of our products are sold to companies which develop and market consumer products. Sales of flavors, fragrances, colors and inks depend in part upon our customers’ ability to identify and meet consumer preferences and their sales and marketing efforts, all of which are beyond our control. Our sales could also be affected by changing technologies that could impact consumer demand for products that contain our flavors, fragrances, colors and inks. Therefore, we depend upon our customers’ ability to create markets for the consumer products which incorporate many of the flavors, fragrances, colors and inks which we manufacture. In addition, if we cannot adequately anticipate and respond to the needs of our customers as they evolve in response to changing consumer preferences and technologies, our results of operations could be adversely affected.

| · |

If we do not maintain an efficient cost structure, our profitability could decrease.

|

Our success depends in part on our ability to maintain an efficient cost structure. We regularly initiate cost-reduction measures that could impact our manufacturing, sales, operations and information systems functions. If we do not continue to manage costs and achieve additional efficiencies, or we do not successfully implement related strategies, our competitiveness and our profits could decrease.

|

·

|

Commodity, energy and transportation price volatility and increases or material shortages may reduce our profits.

|

We use many different commodities as raw ingredients. We also use raw materials whose production is energy intensive. In addition, various energy sources are used in our production and distribution processes. Commodity and energy prices are subject to significant volatility caused by market fluctuations, supply and demand, currency fluctuation, production and transportation disruption, world events and changes in governmental programs. Commodity and energy price increases will raise both our raw material costs and operating costs. We may not be able to increase our product prices enough to offset these increased costs. Increasing our prices also may reduce sales volume and related profitability.

In addition, we obtain some of the raw materials that we use from a single supplier or a limited number of suppliers, and problems with those suppliers could affect the availability of those materials. Even if there are multiple suppliers of a particular raw material, there are occasional shortages. An unavailability or shortage of a raw material could negatively affect our operations using that raw material and thus our results.

| · |

There are many laws and regulations applicable to our industries. Compliance with those requirements is costly to us and can affect our operations. Failure to comply could also be costly and disruptive.

|

Our facilities and products are subject to many laws and regulations relating to the environment, health, safety and the content, processing, packaging, storage, distribution, quality and safety of food, drugs, cosmetics, other consumer products, specialty inks and industrial colors. These laws and regulations are administered in the United States by the Department of Agriculture, the Food and Drug Administration, the Environmental Protection Agency, the Department of Labor and other federal and state governmental agencies. We are subject to similar governmental regulation and oversight abroad. Compliance with these laws and regulations can be costly and affect our operations. Also, if we fail to comply with applicable laws and regulations, we could be subject to administrative penalties and injunctive relief, civil and criminal remedies, fines and recalls of our products. Our customers, particularly those in the pharmaceutical industry, are also subject to laws and regulations that may impose costs on or create risk for us.

| · |

Environmental compliance may be costly to us.

|

Our operations are subject to extensive and stringent laws and regulations which pertain to the discharge of materials into the environment, the handling and disposition of wastes and air emissions. These rules operate or will operate at both the federal and state levels in the United States, and there are analogous laws at many of our overseas locations. Environmental regulations, and the potential failure to comply with them, can have serious consequences, including the costs of compliance and defense, interference with our operations or the ability to obtain required permits, civil, criminal and administrative penalties and negative publicity.

| · |

Operating in foreign countries and emerging markets exposes us to increased risks, including economic, political and international operation risks.

|

We operate, manufacture and sell our products in many foreign countries and emerging markets. The international aspects of our business subject us to risks that could materially impact our operating results, including: difficulties in staffing and managing foreign personnel in diverse cultures; transportation delays or interruptions; and the effects of international political developments and political and economic instability. In addition, changes in policies by the United States or foreign governments could negatively affect our operating results due to changes in duties, tariffs, trade regulations, taxes or limitations on currency or fund transfers.

On June 23, 2016, the United Kingdom (U.K) held a referendum in which voters approved an exit from the European Union, commonly referred to as “Brexit”. As a result of the referendum, it is expected that the British government will begin negotiating the terms of the U.K.’s future relationship with the European Union. Although it is unknown what the terms will be, it is possible that there will be greater restrictions on imports and exports between the U.K. and European Union countries, increased regulatory complexities and economic uncertainties in the region. These changes may adversely affect our operations and financial results.

| · |

We depend on certain key personnel, and the loss of these persons may harm our business.

|

Our success depends in large part on the continued service and availability of our key management and technical personnel, and on our ability to attract and retain qualified new personnel. The competition for these individuals can be significant, and the loss of key employees could harm our business. In addition, we need to provide for smooth transitions when replacing key management and technical personnel positions, and our operations and results may be negatively affected if we are not able to do so.

| · |

We may not successfully complete and integrate past and future acquisitions, which could adversely affect our operating results.

|

We have acquired many companies and operations in the past and may continue growth by acquisition in the future. Our future growth through acquisitions could involve significant risks that may have a material adverse effect on us. We may also be at risk for factors associated with acquisitions that the Company has made in the past. Acquired companies may also have significant latent liabilities which may not be discovered before an acquisition or fully reflected in the price we pay.

We may also need to finance future acquisitions, and the terms of any financing, and the need to ultimately repay or refinance any indebtedness, may have negative effects on us. Acquisitions also could have a dilutive effect on our financial results. Acquisitions also generally result in goodwill, which would need to be written off against earnings in the future if it becomes impaired.

| · |

Our ability to successfully maintain and upgrade our information technology systems, and to effectively respond to failures, disruptions or breaches of our information technology systems, may affect our competitiveness and our profits could decrease.

|

Our success depends in part on our ability to maintain a current information technology platform for our business to operate. We routinely review and upgrade our information technology systems in order to better manage and report the sales, manufacturing and other operations of our business. If we do not continue to maintain our information technology platforms and successfully implement upgrades to systems, our competitiveness and profits could decrease. Furthermore, our information technology systems may be susceptible to failures, disruptions, breaches, theft and other similar cyber-security events. The impact of any such event and the effectiveness of our response thereto may adversely affect our operations and subject us to increased operating costs.

| · |

World events and natural disasters are beyond our control and could affect our results.

|

World events can adversely affect national, international and local economies. Economies can also be affected by natural disasters or by epidemics. Such events and conditions, as well as uncertainty or impairment of financial markets, have adversely affected and could continue to affect our revenues and profitability, particularly if they occur in locations in which we or our customers have significant operations. In addition, while we have manufacturing facilities throughout the world, certain of our facilities are the sole manufacturer of a specific product and a disruption in manufacturing could lead to increased costs of relocating or replacing the production of a product, or reformulating a product, which could have an adverse effect on our results.

The Company received comment letters from the staff of the Securities and Exchange Commission's Division of Corporation Finance dated June 24, 2015 and August 6, 2015 regarding its Annual Report on Form 10-K for the fiscal year ended December 31, 2014 and 2014 Annual Report to Shareholders. The Company responded to the staff comments on July 8, 2015 and August 18, 2015, respectively, with supplemental information and analyses. The staff comments related to various matters, including the Company’s disclosures of its restructuring activities, its treatment of long-lived assets, and its use of non-GAAP financial measures. The comment letters and the Company’s response letters are available on the Securities and Exchange Commission’s website.

As of the date of this annual report on Form 10-K, the Company has not received confirmation from the staff of the Division of Corporation Finance of the Securities and Exchange Commission that their review process relating to the comment letters had been completed. If the Company receives additional comments from the staff, the Company intends to attempt to resolve such additional comments promptly.

Refer to Item 3 for information about the informal inquiry the Company received from the staff of Securities and Exchange Commission’s Division of Enforcement on October 22, 2015.

We lease our corporate headquarters offices, which are located at 777 East Wisconsin Avenue, Milwaukee, Wisconsin. We own our Color Group headquarters offices located in St. Louis, Missouri. We lease our Asia Pacific Group headquarters offices located in Dandenong South, Australia. We own a part, and lease a part, of our Flavors & Fragrances Group headquarters offices located in Hoffman Estates, Illinois. As of December 31, 2016, the locations of our production properties by reportable segment are as follows:

Color Group:

U.S. – St. Louis, Missouri; and South Plainfield, New Jersey*.

International – Jundiai, Brazil*; Kingston, Ontario, Canada; Saint Ouen L’Aumone, France*; Geesthacht, Germany; Reggio Emilia, Italy; Lerma, Mexico; Johannesburg, South Africa; Morges, Switzerland; and Kings Lynn, United Kingdom*.

Flavors & Fragrances Group:

U.S. – Livingston and Turlock, California; Amboy, Illinois; Indianapolis, Indiana; Harbor Beach, Michigan; and Juneau, Wisconsin.

International – Heverlee, Belgium; Qingdao, China*; San Jose, Costa Rica*; Marchais and Strasbourg, France; Celaya and Tlalnepantla, Mexico; Elburg, Netherlands; Granada, Spain; and Wales and Milton Keynes, United Kingdom.

Asia Pacific:

U.S. – None.

International – Keysborough, Australia; Guangzhou, China*; Hitachi, Japan; Auckland, New Zealand; Manila, Philippines*; and Bangkok, Thailand*.

* Indicates a leased property at the location.

All properties are owned except as otherwise indicated above. All facilities are considered to be in good condition (ordinary wear and tear excepted) and suitable and adequate for the Company’s requirements.

Commercial Litigation

U.S. Equal Employment Opportunity Commission Civil Complaint

On September 21, 2015, the U.S. Equal Employment Opportunity Commission (EEOC) filed a civil complaint against Sensient Natural Ingredients LLC (SNI) in the U.S. District Court for the Eastern District of California. SNI is a wholly owned subsidiary of the Company. The EEOC’s complaint alleges that SNI failed to comply with the Americans with Disabilities Act (ADA), as amended, when it terminated five employees in 2011. The EEOC seeks to enjoin SNI from engaging in employment practices that discriminate on the basis of disability; asks the Court to order SNI to implement policies, practices, and programs to ensure it does not violate the ADA; and requests back pay with prejudgment interest, reinstatement, front pay, compensation for past and future pecuniary and non-pecuniary losses, and punitive damages on behalf of the five named former employees and any similarly aggrieved individuals. Recoverable compensatory and punitive damages are subject to statutory caps. The complaint does not request a specific damages amount. To date, the EEOC has provided the Company with a list of 13 additional potentially aggrieved former employees not listed in the complaint who may have been terminated in violation of the ADA during the relevant time period. In its discovery responses, the EEOC has identified 3 of those 13 former employees as additional claimants for whom the Agency seeks relief.

On September 20, 2016, the Company and the EEOC engaged in a mediation session in which the parties worked to settle this matter. As of December 31, 2016 and the date of this annual report on Form 10-K, the parties are still negotiating and attempting to finalize the terms of a settlement agreement, but the Company accrued $0.6 million for the settlement of this matter during 2016.

SEC Inquiry

On October 22, 2015, the Company received an informal inquiry from the staff of the Securities and Exchange Commission’s Division of Enforcement requesting the voluntary provision of documents and information generally related to the Company’s disclosures of its restructuring activities, its treatment of long-lived assets, and its use of non-GAAP financial measures in its SEC filings and 2014 Annual Report to Shareholders. The Company is fully cooperating with the inquiry and is unable to predict the outcome of the inquiry or its potential impact.

Other Claims and Litigation

The Company is involved in various other claims and litigation arising in the normal course of business. In the judgment of management, which relies in part on information from Company counsel, the ultimate resolution of these actions will not materially affect the consolidated financial statements of the Company.

Not applicable.

The executive officers of the Company and their ages as of February 20, 2017, are as follows:

|

Name

|

Age

|

Position

|

|

Paul Manning

|

42

|

Chairman, President and Chief Executive Officer

|

|

Kimberly Chase

|

48

|

Vice President and Treasurer

|

|

Michael C. Geraghty

|

55

|

President, Color Group

|

|

Gautam Grover

|

47

|

President, Flavors & Fragrances Group

|

|

Jeffrey T. Makal

|

53

|

Vice President, Controller and Chief Accounting Officer

|

|

John J. Manning

|

48

|

Vice President, General Counsel and Secretary

|

|

Kimberly A. Morin

|

54

|

Vice President, Human Resources

|

|

Stephen J. Rolfs

|

52

|

Senior Vice President and Chief Financial Officer

|

|

Robert J. Wilkins

|

60

|

President, Asia Pacific Group

|

The Company has employed all of the individuals named above, in substantively their current positions, for at least the past five years except as follows. Mr. Paul Manning has held his present office since April 21, 2016, and previously served as President and Chief Executive Officer (February 2014 – April 2016), President and Chief Operating Officer (October 2012 – February 2014) and President, Color Group (2010 – October 2012). Ms. Chase has held present office since October 20, 2016, and previously served as Assistant Treasurer (March 2015 – October 2016), Treasury Consultant (December 2013 – March 2015) and Treasury Director (August 2010 – December 2013). Mr. Geraghty has held his present office since October 18, 2012, and previously served as General Manager, Food Colors USA (April 2011 – October 2012). Mr. Grover has held his present office since December 3, 2015. Prior to joining the Company, Mr. Grover served as Vice President, Strategy (September 2012 – November 2015) and Vice President, Logistics Services (January 2013 – November 2015) for US Foods, Inc. and as Director, Strategy and Business Development and Business Director – Asia for Brady Corporation (2009 to September 2012). Mr. John Manning has held his present office since April 21, 2016, and previously served as Vice President and Assistant General Counsel (January 2013 – April 2016). Prior to joining the Company, Mr. John Manning served as an Assistant U.S. Attorney (2004 – December 2012) and Deputy Criminal Chief (2006 – December 2012) for the United States Attorney’s Office – Eastern District of Wisconsin. Ms. Morin has held her present office since October 20, 2015, and previously served as Human Resources Director, Flavors & Fragrances Group (August 2013 – October 2015). Prior to joining the Company, Ms. Morin served as Vice President Human Resources for Harbor Light Hospice, Inc., from April 2012 to August 2013, and as Senior Human Resources Director of Exel from 2005 to April 2012. Mr. Rolfs has held his present position since February 7, 2015, and previously served as Senior Vice President, Administration (July 2013 – February 2015) and Vice President, Administration (2010 – July 2013).

| Item 5. |

Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

|

The only market in which the common stock of the Company is listed is the New York Stock Exchange. The range of the high and low sales prices as quoted in the New York Stock Exchange – Composite Transaction tape for the common stock of the Company and the amount of dividends declared for the fiscal years 2016 and 2015 are set forth below:

|

Market Price

|

Dividends

Declared

|

|||||||||||

|

High

|

Low

|

Per Share

|

||||||||||

|

2016

|

||||||||||||

|

First Quarter

|

$

|

65.75

|

$

|

52.69

|

$

|

0.27

|

||||||

|

Second Quarter

|

72.53

|

62.63

|

0.27

|

|||||||||

|

Third Quarter

|

76.15

|

68.64

|

0.27

|

|||||||||

|

Fourth Quarter

|

83.38

|

68.51

|

0.30

|

|||||||||

|

2015

|

||||||||||||

|

First Quarter

|

$

|

68.99

|

$

|

56.71

|

$

|

0.25

|

||||||

|

Second Quarter

|

70.53

|

64.04

|

0.25

|

|||||||||

|

Third Quarter

|

69.87

|

59.34

|

0.27

|

|||||||||

|

Fourth Quarter

|

67.47

|

59.54

|

0.27

|

|||||||||

In 2016 and 2015, common stock dividends were paid on a quarterly basis, and it is expected that quarterly dividends will continue to be paid in the future. On October 20, 2016, the Company announced an increase in its cash dividend on its common stock from an annual rate of $1.08 per share to an annual rate of $1.20 per share, commencing with the quarterly dividend paid on December 1, 2016, to shareholders of record on November 7, 2016.

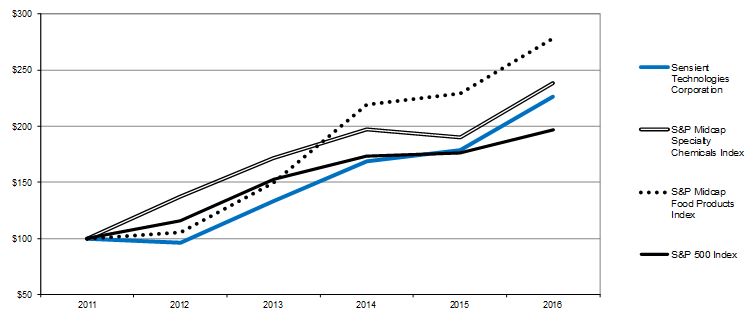

This graph compares the cumulative total shareholder return for the Company’s common stock over the last five years to the total returns on the Standard & Poor’s Midcap Specialty Chemicals Index (the “S&P Midcap Specialty Chemicals Index”), the Standard & Poor’s Midcap Food Products Index (the “S&P Midcap Food Products Index”) and the Standard & Poor’s 500 Stock Index (the “S&P 500 Index”). The graph assumes a $100 investment made on December 31, 2011, and reinvestment of dividends. The stock performance shown on the graph is not necessarily indicative of future price performance.

|

2011

|

2012

|

2013

|

2014

|

2015

|

2016

|

|||||||||||||||||||

|

Sensient Technologies Corporation

|

$

|

100

|

$

|

96

|

$

|

134

|

$

|

169

|

$

|

179

|

$

|

227

|

||||||||||||

|

S&P Midcap Specialty Chemicals Index

|

100

|

137

|

171

|

197

|

190

|

238

|

||||||||||||||||||

|

S&P Midcap Food Products Index

|

100

|

106

|

150

|

219

|

229

|

278

|

||||||||||||||||||

|

S&P 500 Index

|

100

|

106

|

153

|

174

|

176

|

197

|

||||||||||||||||||

Standard & Poor’s and S&P are registered trademarks of Standard & Poor’s Financial Services, LLC.

On August 21, 2014, the Board of Directors authorized the repurchase of up to five million shares. As of February 16, 2017, 3,605,840 shares had been repurchased under this authorization. The Company repurchased 302,221 shares during the fourth quarter of 2016 and a total of 702,698 shares during 2016.

The following table provides the specified information about the repurchases of shares by the Company during the fourth quarter of 2016. All shares were purchased under the authorization described above. There is no expiration date for this authorization.

|

Period

|

Total number of

shares purchased

|

Average price

paid per share

|

Total number of shares purchased as

part of a publicly announced plan

|

Maximum number of shares that may be

purchased under publicly announced plans

|

||||||||||||

|

October 1 to 31, 2016

|

134,727

|

$

|

73.90

|

134,727

|

1,592,254

|

|||||||||||

|

November 1 to 30, 2016

|

161,994

|

74.03

|

161,994

|

1,430,260

|

||||||||||||

|

December 1 to 31, 2016

|

5,500

|

76.95

|

5,500

|

1,424,760

|

||||||||||||

|

Total

|

302,221

|

$

|

74.02

|

302,221

|

||||||||||||

The number of shareholders of record on February 16, 2017, was 2,425.

Information regarding the Company’s equity compensation plans is incorporated by reference into Item 11 of Part III of this report.

The following selected financial data is derived from our consolidated financial statements. This data should be read in conjunction with the consolidated financial statements and notes thereto, and with Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Quarterly Data

|

(in thousands except per share amounts) (unaudited)

|

||||||||||||||||||||

|

First

Quarter

|

Second

Quarter

|

Third

Quarter

|

Fourth

Quarter

|

Full

Year

|

||||||||||||||||

|

2016

|

||||||||||||||||||||

|

Revenue

|

$

|

342,468

|

$

|

360,836

|

$

|

349,662

|

$

|

330,244

|

$

|

1,383,210

|

||||||||||

|

Gross profit

|

115,843

|

124,434

|

122,563

|

112,587

|

475,427

|

|||||||||||||||

|

Earnings from continuing operations

|

31,193

|

24,751

|

35,619

|

31,350

|

122,913

|

|||||||||||||||

|

(Loss) Gain from discontinued operations, net of tax

|

(22

|

)

|

3,365

|

—

|

—

|

3,343

|

||||||||||||||

|

Net earnings

|

31,171

|

28,116

|

35,619

|

31,350

|

126,256

|

|||||||||||||||

|

Earnings per basic share:

|

||||||||||||||||||||

|

Continuing operations

|

0.70

|

0.56

|

0.80

|

0.71

|

2.76

|

|||||||||||||||

|

Discontinued operations

|

—

|

0.08

|

—

|

—

|

0.08

|

|||||||||||||||

|

Earnings per basic share

|

0.70

|

0.63

|

0.80

|

0.71

|

2.84

|

|||||||||||||||

|

Earnings per diluted share:

|

||||||||||||||||||||

|

Continuing operations

|

0.69

|

0.55

|

0.79

|

0.70

|

2.74

|

|||||||||||||||

|

Discontinued operations

|

—

|

0.08

|

—

|

—

|

0.07

|

|||||||||||||||

|

Earnings per diluted share

|

0.69

|

0.63

|

0.79

|

0.70

|

2.82

|

|||||||||||||||

|

2015

|

||||||||||||||||||||

|

Revenue

|

$

|

346,226

|

$

|

346,009

|

$

|

344,533

|

$

|

339,196

|

$

|

1,375,964

|

||||||||||

|

Gross profit

|

117,433

|

118,155

|

112,772

|

106,073

|

454,433

|

|||||||||||||||

|

Earnings from continuing operations

|

30,735

|

29,542

|

27,638

|

19,332

|

107,247

|

|||||||||||||||

|

Loss from discontinued operations, net of tax

|

(209

|

)

|

(92

|

)

|

(47

|

)

|

(114

|

)

|

(462

|

)

|

||||||||||

|

Net earnings

|

30,526

|

29,450

|

27,591

|

19,218

|

106,785

|

|||||||||||||||

|

Earnings per basic share:

|

||||||||||||||||||||

|

Continuing operations

|

0.65

|

0.64

|

0.61

|

0.43

|

2.34

|

|||||||||||||||

|

Discontinued operations

|

—

|

—

|

—

|

—

|

(0.01

|

)

|

||||||||||||||

|

Earnings per basic share

|

0.65

|

0.64

|

0.61

|

0.43

|

2.33

|

|||||||||||||||

|

Earnings per diluted share:

|

||||||||||||||||||||

|

Continuing operations

|

0.65

|

0.64

|

0.61

|

0.43

|

2.32

|

|||||||||||||||

|

Discontinued operations

|

—

|

—

|

—

|

—

|

(0.01

|

)

|

||||||||||||||

|

Earnings per diluted share

|

0.64

|

0.63

|

0.60

|

0.43

|

2.31

|

|||||||||||||||

Five Year Review

|

(in thousands except percentages, employee and per share data)

|

||||||||||||||||||||||||||||||||||||||||

|

Years ended December 31,

|

2016

|

2015

|

2014

|

2013

|

2012

|

|||||||||||||||||||||||||||||||||||

|

Summary of Operations

|

||||||||||||||||||||||||||||||||||||||||

|

Revenue

|

$

|

1,383,210

|

100.0

|

%

|

$

|

1,375,964

|

100.0

|

%

|

$

|

1,447,821

|

100.0

|

%

|

$

|

1,462,126

|

100.0

|

%

|

$

|

1,453,555

|

100.0

|

%

|

||||||||||||||||||||

|

Cost of products sold

|

907,783

|

65.6

|

921,531

|

67.0

|

959,311

|

66.3

|

987,080

|

67.5

|

990,911

|

68.2

|

||||||||||||||||||||||||||||||

|

Selling and administrative expenses

|

289,818

|

21.0

|

288,092

|

20.9

|

357,845

|

24.7

|

301,266

|

20.6

|

269,765

|

18.6

|

||||||||||||||||||||||||||||||

|

Operating income

|

185,609

|

13.5

|

166,341

|

12.1

|

130,665

|

9.0

|

173,780

|

11.9

|

192,879

|

13.3

|

||||||||||||||||||||||||||||||

|

Interest expense

|

18,324

|

1.3

|

16,945

|

1.2

|

16,067

|

1.1

|

16,147

|

1.1

|

16,901

|

1.2

|

||||||||||||||||||||||||||||||

|

Earnings before income taxes

|

167,285

|

12.1

|

149,396

|

10.9

|

114,598

|

7.9

|

157,633

|

10.8

|

175,978

|

12.1

|

||||||||||||||||||||||||||||||

|

Income taxes

|

44,372

|

3.2

|

42,149

|

3.1

|

32,827

|

2.3

|

43,335

|

3.0

|

50,896

|

3.5

|

||||||||||||||||||||||||||||||

|

Earnings from continuing operations

|

122,913

|

8.9

|

107,247

|

7.8

|

81,771

|

5.6

|

114,298

|

7.8

|

125,082

|

8.6

|

||||||||||||||||||||||||||||||

|

Gain (loss) from discontinued operations, net of tax

|

3,343

|

0.2

|

(462

|

)

|

-

|

(8,125

|

)

|

(0.6

|

)

|

(1,003

|

)

|

(0.1

|

)

|

(1,174

|

)

|

(0.1

|

)

|

|||||||||||||||||||||||

|

Net earnings

|

$

|

126,256

|

9.2

|

%

|

$

|

106,785

|

7.8

|

%

|

$

|

73,646

|

5.1

|

%

|

$

|

113,295

|

7.7

|

%

|

$

|

123,908

|

8.5

|

%

|

||||||||||||||||||||

|

Earnings per basic share:

|

||||||||||||||||||||||||||||||||||||||||

|

Continuing operations

|

$

|

2.76

|

$

|

2.34

|

$

|

1.69

|

$

|

2.30

|

$

|

2.52

|

||||||||||||||||||||||||||||||

|

Discontinued operations

|

0.08

|

(0.01

|

)

|

(0.17

|

)

|

(0.02

|

)

|

(0.02

|

)

|

|||||||||||||||||||||||||||||||

|

Earnings per basic share

|

$

|

2.84

|

$

|

2.33

|

$

|

1.52

|

$

|

2.28

|

$

|

2.50

|

||||||||||||||||||||||||||||||

|

Earnings per diluted share:

|

||||||||||||||||||||||||||||||||||||||||

|

Continuing operations

|

$

|

2.74

|

$

|

2.32

|

$

|

1.67

|

$

|

2.29

|

$

|

2.51

|

||||||||||||||||||||||||||||||

|

Discontinued operations

|

0.07

|

(0.01

|

)

|

(0.17

|

)

|

(0.02

|

)

|

(0.02

|

)

|

|||||||||||||||||||||||||||||||

|

Earnings per diluted share

|

$

|

2.82

|

$

|

2.31

|

$

|

1.51

|

$

|

2.27

|

$

|

2.49

|

||||||||||||||||||||||||||||||

|

Other Related Data

|

||||||||||||||||||||||||||||||||||||||||

|

Dividends per share, declared and paid

|

$

|

1.11

|

$

|

1.04

|

$

|

0.98

|

$

|

0.91

|

$

|

0.87

|

||||||||||||||||||||||||||||||

|

Average common shares outstanding:

|

||||||||||||||||||||||||||||||||||||||||

|

Basic

|

44,523

|

45,910

|

48,525

|

49,755

|

49,596

|

|||||||||||||||||||||||||||||||||||

|

Diluted

|

44,843

|

46,204

|

48,819

|

49,934

|

49,822

|

|||||||||||||||||||||||||||||||||||

|

Book value per common share

|

$

|

18.83

|

$

|

18.78

|

$

|

21.94

|

$

|

24.72

|

$

|

23.09

|

||||||||||||||||||||||||||||||

|

Price range per common share

|

52.69 -

83.38

|

56.71 -

70.53

|

46.08 -

63.35

|

35.54 -

53.35

|

33.13 -

41.08

|

|||||||||||||||||||||||||||||||||||

|

Share price at December 31

|

78.58

|

62.82

|

60.34

|

48.52

|

35.56

|

|||||||||||||||||||||||||||||||||||

|

Capital expenditures

|

81,216

|

79,941

|

79,398

|

104,246

|

103,806

|

|||||||||||||||||||||||||||||||||||

|

Depreciation

|

45,714

|

46,694

|

50,225

|

50,716

|

46,992

|

|||||||||||||||||||||||||||||||||||

|

Amortization

|

1,305

|

1,245

|

1,231

|

1,300

|

1,360

|

|||||||||||||||||||||||||||||||||||

|

Total assets

|

1,667,860

|

1,703,732

|

1,772,039

|

1,870,813

|

1,781,821

|

|||||||||||||||||||||||||||||||||||

|

Long-term debt

|

582,780

|

613,502

|

450,548

|

347,529

|

333,479

|

|||||||||||||||||||||||||||||||||||

|

Total debt

|

603,358

|

634,157

|

466,436

|

354,579

|

353,527

|

|||||||||||||||||||||||||||||||||||

|

Shareholders’ equity

|

835,741

|

845,127

|

1,046,935

|

1,242,684

|

1,153,898

|

|||||||||||||||||||||||||||||||||||

|

Return on average shareholders’ equity

|

14.7

|

%

|

11.6

|

%

|

6.4

|

%

|

9.5

|

%

|

11.3

|

%

|

||||||||||||||||||||||||||||||

|

Total debt to total capital

|

41.9

|

%

|

42.9

|

%

|

30.8

|

%

|

22.2

|

%

|

23.5

|

%

|

||||||||||||||||||||||||||||||

|

Employees

|

4,083

|

4,032

|

4,053

|

4,130

|

3,983

|

|||||||||||||||||||||||||||||||||||

The 2016 results include charges of $26.1 million ($21.1 million after tax, or $0.47 per share) related to the restructuring and other divestiture costs. The restructuring costs pertain to the Company’s 2014 Restructuring Plan related to eliminating underperforming operations, consolidating manufacturing facilities and improving efficiencies within the Company, and the other costs pertain to the Company’s divestiture.

The 2015 results include charges of $43.6 million ($33.6 million after tax, or $0.73 per share) related to the restructuring and other acquisition related costs. The restructuring costs pertain to the Company’s 2014 Restructuring Plan related to eliminating underperforming operations, consolidating manufacturing facilities and improving efficiencies within the Company, and the other costs pertain to acquisition related costs.

The 2014 results include charges of $90.6 million ($65.5 million after tax, or $1.34 per share) related to the restructuring and other proxy contest costs. The restructuring costs pertain to the Company’s 2014 Restructuring Plan related to eliminating underperforming operations, consolidating manufacturing facilities and improving efficiencies within the Company, and the other costs pertain to proxy contest costs.

The 2013 results include a charge of $31.7 million ($22.0 million after tax, or $0.44 per share) related to the 2013 restructuring program related to the relocation of the Flavors & Fragrances Group headquarters to Chicago, as well as a profit improvement plan across all segments of the Company.

OVERVIEW

Sensient Technologies Corporation (the “Company”) is a global developer, manufacturer and supplier of flavor and fragrance systems for the food, beverage, personal care and household-products industries. In addition, the Company is a developer, manufacturer and supplier of colors for businesses worldwide. The Company provides natural and synthetic color systems for use in foods, beverages and pharmaceuticals; colors and other ingredients for cosmetics, pharmaceuticals and specialty inks; and technical colors for industrial applications. The Company’s three reportable segments are the Flavors & Fragrances Group and the Color Group, which are managed on a product-and-services basis, and the Asia Pacific Group, which is managed on a geographic basis. The Company’s corporate expenses and restructuring and other costs are included in the “Corporate & Other” category.

The Company’s 2016 diluted earnings per share from continuing operations were $2.74 in 2016 and $2.32 in 2015. Included in the 2016 and 2015 results, were $26.1 million and $43.6 million, respectively, of restructuring and other costs, or 47 cents per share and 73 cents per share, respectively. Adjusted diluted earnings per share, which exclude these restructuring and other costs, were $3.21 in 2016 and $3.05 in 2015 (see discussion below regarding Non-GAAP Financial Measures and the Company’s Restructuring Activities and Divestiture).

The Company’s net cash provided by operating activities was $222.5 million in 2016, an increase from the $128.0 million reported in 2015. The Company’s total debt decreased to $603 million as of December 31, 2016, from $634.2 million as of December 31, 2015. Since 1962, the Company has continued without interruption to pay a quarterly cash dividend. In 2016, the Company increased the quarterly dividend by 3 cents per share from 27 cents to 30 cents per share, or $1.20 per share on an annualized basis. In addition, the Company repurchased $50.1 million of Company stock in 2016, which is in addition to the $176.6 million repurchased in 2015.

Additional information on the results is included below.

RESULTS OF CONTINUING OPERATIONS

2016 vs. 2015

Revenue

Sensient’s revenue was approximately $1.4 billion in both 2016 and 2015. The impact of foreign exchange rates reduced consolidated revenue by 2% in 2016.

Gross Profit

The Company’s gross margin was 34.4% in 2016 and 33.0% in 2015. Included in the cost of products sold are $2.1 million and $6.1 million of restructuring costs for 2016 and 2015, respectively. The increase in the gross margin is primarily a result of higher selling prices and volumes, mainly in the Color segment, savings associated with the 2014 Restructuring Plan ($7.9 million) and reduced restructuring costs, partially offset by higher raw material costs and manufacturing costs. Restructuring costs reduced gross margin by 10 basis points and 50 basis points in 2016 and 2015, respectively.

Selling and Administrative Expenses

Selling and administrative expense as a percent of revenue was 21.0% in 2016 and 20.9% in 2015. Restructuring and other costs of $24.0 million and $37.5 million for 2016 and 2015, respectively, were included in selling and administrative expense. Selling and administrative expense as a percent of revenue in 2016 were comparable to 2015 as a result of higher performance based executive compensation ($7.6 million) and professional fees ($6.2 million), partially offset by lower restructuring and other costs ($13.5 million). Restructuring and other costs increased selling and administrative expense as a percent of revenue by 180 basis points and 270 basis points in 2016 and 2015, respectively.

Operating Income

Operating income was $185.6 million in 2016 and $166.3 million in 2015. Operating margins increased to 13.4% in 2016 from 12.1% in 2015. Restructuring and other costs reduced operating margins by 190 basis points and 320 basis points in 2016 and 2015, respectively.

Additional information on segment results can be found in the Segment Information section.

Interest Expense

Interest expense was $18.3 million in 2016 and $16.9 million in 2015. The increase in expense was primarily due to the increase in average debt outstanding, which was partially offset by lower average interest rates.

Income Taxes

The effective income tax rate was 26.5% in 2016 and 28.2% in 2015. The effective tax rates in both 2016 and 2015 were impacted by audit settlements, mix of foreign earnings and restructuring and other costs. The effective tax rate in 2015 was also impacted by changes in estimates associated with the finalization of prior year tax items. In total, the net impact of these discrete items and restructuring and other costs reduced the effective income tax rate by 1.2% for 2016 and 2.4% for 2015.

|

2016

|

2015

|

|||||||

|