Attached files

| file | filename |

|---|---|

| EX-32.1 - EX-32.1 - H&E Equipment Services, Inc. | hees-ex321_11.htm |

| EX-31.2 - EX-31.2 - H&E Equipment Services, Inc. | hees-ex312_9.htm |

| EX-31.1 - EX-31.1 - H&E Equipment Services, Inc. | hees-ex311_7.htm |

| EX-23.1 - EX-23.1 - H&E Equipment Services, Inc. | hees-ex231_10.htm |

| EX-21.1 - EX-21.1 - H&E Equipment Services, Inc. | hees-ex211_6.htm |

| EX-10.3 - EX-10.3 - H&E Equipment Services, Inc. | hees-ex103_16.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K

(Mark One)

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

or

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 000-51759

H&E EQUIPMENT SERVICES, INC.

(Exact Name of Registrant as Specified in Its Charter)

|

Delaware |

|

81-0553291 |

|

(State or Other Jurisdiction of |

|

(IRS Employer |

|

|

|

|

|

7500 Pecue Lane, Baton Rouge, Louisiana 70809 |

|

(225) 298-5200 |

|

(Address of Principal Executive Offices, including Zip Code) |

|

(Registrant’s Telephone Number, Including Area Code) |

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class |

|

Name of Each Exchange on Which Registered |

|

Common Stock, par value $0.01 per share |

|

Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

|

Large Accelerated Filer |

|

☒ |

|

Accelerated Filer |

|

☐ |

|

|

|

|

|

|||

|

Non-Accelerated Filer |

|

☐ |

|

Smaller Reporting Company |

|

☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the common stock held by non-affiliates of the registrant was approximately $593,698,073 (computed by reference to the closing sale price of the registrant’s common stock on the Nasdaq Global Market on June 30, 2016, the last business day of the registrant’s most recently completed second fiscal quarter).

As of February 16, 2017, there were 35,575,555 shares of common stock, par value $0.01 per share, of the registrant outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the document listed below have been incorporated by reference into the indicated parts of this Form 10-K, as specified in the responses to the item numbers involved.

|

|

Part III |

The registrant’s definitive proxy statement, for use in connection with the Annual Meeting of Stockholders, to be filed within 120 days after the registrant’s fiscal year ended December 31, 2016. |

|

|

|

|

|

|

|

Item 1. |

|

|

4 |

|

|

Item 1A. |

|

|

10 |

|

|

Item 1B. |

|

|

19 |

|

|

Item 2. |

|

|

20 |

|

|

Item 3. |

|

|

21 |

|

|

Item 4. |

|

|

21 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 5. |

|

|

22 |

|

|

Item 6. |

|

|

25 |

|

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

27 |

|

Item 7A. |

|

|

48 |

|

|

Item 8. |

|

|

49 |

|

|

Item 9. |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

83 |

|

Item 9A. |

|

|

84 |

|

|

Item 9B. |

|

|

87 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 10. |

|

|

88 |

|

|

Item 11. |

|

|

88 |

|

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

88 |

|

Item 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

|

88 |

|

Item 14. |

|

|

88 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 15. |

|

|

89 |

|

|

Item 16. |

|

|

89 |

|

|

|

91 |

|||

|

|

92 |

|||

2

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the federal securities laws. Statements that are not historical facts, including statements about our beliefs and expectations, are forward-looking statements. Forward-looking statements include statements preceded by, followed by or that include the words “may”, “could”, “would”, “should”, “believe”, “expect”, “anticipate”, “plan”, “estimate”, “target”, “project”, “intend”, “foresee” and similar expressions. These statements include, among others, statements regarding our expected business outlook, anticipated financial and operating results, our business strategy and means to implement the strategy, our objectives, the amount and timing of capital expenditures, the likelihood of our success in expanding our business, financing plans, budgets, working capital needs and sources of liquidity. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. We believe that these risks and uncertainties include, but are not limited to, those described in the “Risk Factors” section of this Annual Report on Form 10-K. These factors should not be construed as exhaustive and should be read with the other cautionary statements in this Annual Report on Form 10-K.

Forward-looking statements are only predictions and are not guarantees of performance. These statements are based on our management’s beliefs and assumptions, which in turn are based on currently available information. Important assumptions relating to the forward-looking statements include, among others, assumptions regarding demand for our products, the expansion of product offerings geographically or through new marketing applications, the timing and cost of planned capital expenditures, competitive conditions and general economic conditions. These assumptions could prove inaccurate. Forward-looking statements also involve known and unknown risks and uncertainties, which could cause actual results to differ materially from those contained in any forward-looking statement. In addition, even if our actual results are consistent with the forward-looking statements contained in this Annual Report on Form 10-K, those results may not be indicative of results or developments in subsequent periods. Many of these factors are beyond our ability to control or predict. Such factors include, but are not limited to, the following:

|

|

• |

general economic conditions and construction and industrial activity in the markets where we operate in North America; |

|

|

• |

our ability to forecast trends in our business accurately, and the impact of economic downturns and economic uncertainty on the markets we serve; |

|

|

• |

the impact of conditions in the global credit and commodity markets and their effect on construction spending and the economy in general; |

|

|

• |

relationships with equipment suppliers; |

|

|

• |

increased maintenance and repair costs as we age our fleet and decreases in our equipment’s residual value; |

|

|

• |

our indebtedness; |

|

|

• |

risks associated with the expansion of our business; |

|

|

• |

our possible inability to integrate any businesses we acquire; |

|

|

• |

competitive pressures; |

|

|

• |

security breaches and other disruptions in our information technology systems; |

|

|

• |

adverse weather events or natural disasters; |

|

|

• |

compliance with laws and regulations, including those relating to environmental matters and corporate governance matters; and |

|

|

• |

other factors discussed under Item 1A - Risk Factors or elsewhere in this Annual Report on Form 10-K. |

Except as required by applicable law, including the securities laws of the United States and the rules and regulations of the Securities and Exchange Commission (“SEC”), we are under no obligation to publicly update or revise any forward-looking statements after we file this Annual Report on Form 10-K, whether as a result of any new information, future events or otherwise. Investors, potential investors and other readers are urged to consider the above mentioned factors carefully in evaluating the forward-looking statements and are cautioned not to place undue reliance on such forward-looking statements. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results or performance.

3

The Company

We are one of the largest integrated equipment services companies in the United States focused on heavy construction and industrial equipment. We rent, sell and provide parts and services support for four core categories of specialized equipment: (1) hi-lift or aerial work platform equipment; (2) cranes; (3) earthmoving equipment; and (4) industrial lift trucks. We engage in five principal business activities in these equipment categories:

|

|

• |

equipment rentals; |

|

|

• |

new equipment sales; |

|

|

• |

used equipment sales; |

|

|

• |

parts sales; and |

|

|

• |

repair and maintenance services. |

By providing rental, sales, parts, repair and maintenance functions under one roof, we offer our customers a one-stop solution for their equipment needs. This full-service approach provides us with (1) multiple points of customer contact; (2) cross-selling opportunities among our rental, new and used equipment sales, parts sales and services operations; (3) an effective method to manage our rental fleet through efficient maintenance and profitable distribution of used equipment; and (4) a mix of business activities that enables us to operate effectively throughout economic cycles. We believe that the operating experience and extensive infrastructure we have developed throughout our history as an integrated services company provide us with a competitive advantage over rental-focused companies and equipment distributors. In addition, our focus on four core categories of heavy construction and industrial equipment enables us to offer specialized knowledge and support to our customers.

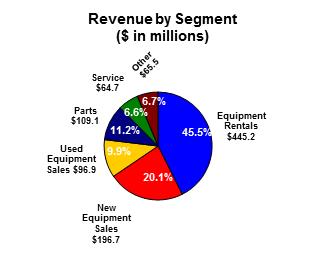

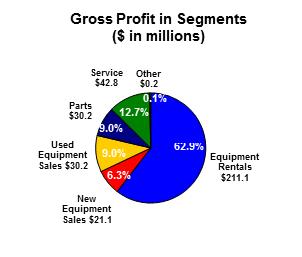

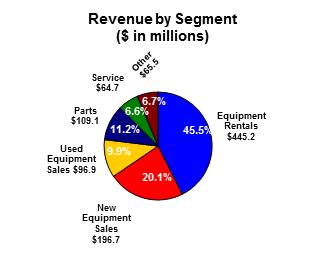

For the year ended December 31, 2016, we generated total revenues of approximately $978.1 million. The pie charts below illustrate a breakdown of our revenues and gross profit for the year ended December 31, 2016 by business segment (see note 17 to our consolidated financial statements for further information regarding our business segments):

We have operated, through our predecessor companies, as an integrated equipment services company for approximately 56 years and have built an extensive infrastructure that as of February 16, 2017 includes 78 full-service facilities located throughout the West Coast, Intermountain, Southwest, Gulf Coast, Southeast and Mid-Atlantic regions of the United States. Our management, from the corporate level down to the branch store level, has extensive industry experience. We focus our rental and sales activities on, and organize our personnel principally by, our four core equipment categories. We believe this allows us to provide specialized equipment knowledge, improve the effectiveness of our rental and sales forces and strengthen our customer relationships. In addition, we operate our day-to-day business on a branch basis, which we believe allows us to more closely service our customers, fosters management accountability at local levels and strengthens our local and regional relationships.

4

Equipment Rentals. We rent our heavy construction and industrial equipment to our customers on a daily, weekly and monthly basis. We have a well-maintained rental fleet that, at December 31, 2016, consisted of approximately 28,753 pieces of equipment having an original acquisition cost (which we define as the cost originally paid to manufacturers or the original amount financed under operating leases) of approximately $1.3 billion and an average age of approximately 33.0 months. Our rental business creates cross-selling opportunities for us in sales and service support activities.

New Equipment Sales. We sell new heavy construction and industrial equipment in all four core equipment categories, and are a leading U.S. distributor for nationally recognized suppliers including JLG Industries, Gehl, Genie Industries (Terex), Komatsu, and Doosan/Bobcat. In addition, we are the world’s largest distributor of Grove and Manitowoc crane equipment. Our new equipment sales operation is a source of new customers for our parts sales and service support activities, as well as for used equipment sales.

Used Equipment Sales. We sell used equipment primarily from our rental fleet, as well as inventoried equipment that we acquire through trade-ins from our customers and selective purchases of high-quality used equipment. For the year ended December 31, 2016, approximately 87.1% of our used equipment sales revenues were derived from sales of rental fleet equipment. Used equipment sales, like new equipment sales, generate parts and services business for us.

Parts Sales. We sell new and used parts to customers and also provide parts to our own rental fleet. We maintain an extensive in-house parts inventory in order to provide timely parts and service support to our customers as well as to our own rental fleet. In addition, our parts operations enable us to maintain a high-quality rental fleet and provide additional product support to our end users.

Service Support. We provide maintenance and repair services for our customers’ owned equipment and to our own rental fleet. In addition to repair and maintenance on an as-needed or scheduled basis, we provide ongoing preventative maintenance services and warranty repairs for our customers. We devote significant resources to training our technical service employees and over time, we have built a full-scale services infrastructure that we believe would be difficult for companies without the requisite resources and lead time to effectively replicate.

In addition to our principal business activities mentioned above, we provide ancillary equipment support activities including transportation, hauling, parts shipping and loss damage waivers.

Industry Background

Although there has been some consolidation within the industry, including the acquisition of Rental Services Corporation by United Rentals, Inc. (“URI”) in 2012 and the currently pending acquisition of NES Rentals by URI, the U.S. construction equipment distribution industry remains highly fragmented and consists mainly of a small number of multi-location regional or national operators and a large number of relatively small, independent businesses serving discrete local markets. The industry is driven by a broad range of economic factors including total U.S. non-residential construction trends, construction machinery demand, demand for rental equipment and additional, region-specific factors. Construction equipment is largely distributed to end users through two channels: equipment rental companies and equipment dealers. Examples of equipment rental companies include URI, Sunbelt Rentals, Neff Rentals and Hertz Equipment Rental. Examples of equipment dealers include Finning and Toromont. Unlike many of these companies, which principally focus on one channel of distribution, we operate substantially in both channels. As an integrated equipment services company, we rent, sell and provide parts and services support. Although many of the historically pure equipment rental companies also provide parts and service support to customers, their service offerings are typically limited and may prove difficult to expand due to the infrastructure, training and resources necessary to develop the breadth of offerings and depth of specialized equipment knowledge that our services and sales staff provides.

Our Competitive Strengths

Integrated Platform of Products and Services. We believe that our operating experience and the extensive infrastructure we have developed through years of operating as an integrated equipment services company provides us with a competitive advantage over rental-focused companies and equipment distributors. Key strengths of our integrated equipment services platform include:

|

|

• |

ability to strengthen customer relationships by providing a full-range of products and services; |

|

|

• |

purchasing power gained through purchases for our new equipment sales and rental operations; |

|

|

• |

high quality rental fleet supported by our strong product support capabilities; |

|

|

• |

established retail sales network resulting in profitable disposal of our used equipment; and |

|

|

• |

mix of business activities that enables us to effectively operate through economic cycles. |

5

Complementary, High Margin Parts and Services Operations. Our parts and services businesses allow us to maintain our rental fleet in excellent condition and to offer our customers high-quality rental equipment. Our after-market parts and services businesses together provide us with a high-margin revenue source that has proven to be relatively stable throughout a range of economic cycles.

Specialized, High-Quality Equipment Fleet. Our focus on four core types of heavy construction and industrial equipment allows us to better provide the specialized knowledge and support that our customers demand when renting and purchasing equipment. These four types of equipment are attractive because they have a long useful life, high residual value and generally strong industry demand.

Well-Developed Infrastructure. We have built an infrastructure that as of February 16, 2017 included a network of 78 full-service facilities in 22 states, and a workforce that included a highly-skilled group of approximately 459 service technicians and an aggregate of 260 sales people in our specialized rental and equipment sales forces. We believe that our well-developed infrastructure helps us to better serve large multi-regional customers than our historically rental-focused competitors and provides an advantage when competing for lucrative fleet and project management business as well as the ability to quickly capitalize on new opportunities.

Leading Distributor for Suppliers. We are a leading U.S. distributor for nationally-recognized equipment suppliers, including JLG Industries, Gehl, Genie Industries (Terex), Komatsu and Doosan/Bobcat. In addition, we are the world’s largest distributor of Grove and Manitowoc crane equipment. These relationships improve our ability to negotiate equipment acquisition pricing and allow us to purchase parts at wholesale costs.

Customized Information Technology Systems. Our information systems allow us to actively manage our business and our rental fleet. We have a customer relationship management system that provides our sales force with real-time access to customer and sales information. In addition, our enterprise resource planning system enhances our ability to provide more timely and meaningful information to manage our business.

Experienced Management Team. Our senior management team is led by John M. Engquist, our Chief Executive Officer, who has approximately 42 years of industry experience. Our senior and regional managers have an average of approximately 23 years of industry experience. Our branch managers have extensive knowledge and industry experience as well.

Our Business Strategy

Our business strategy includes, among other things, leveraging our integrated business model, managing the life cycle of our rental equipment, further developing our parts and services operations and selectively entering new markets and pursuing acquisitions. However, the timing and extent to which we implement these various aspects of our strategy depend on a variety of factors, many of which are outside our control, such as general economic conditions and construction activity in the United States.

Leverage Our Integrated Business Model. We intend to continue to actively leverage our integrated business model to offer a one-stop solution to our customers’ varied needs with respect to the four categories of heavy construction and industrial equipment on which we focus. We will continue to cross-sell our services to expand and deepen our customer relationships. We believe that our integrated equipment services model provides us with a strong platform for growth and enables us to effectively operate through economic cycles.

Managing the Life Cycle of Our Rental Equipment. We actively manage the size, quality, age and composition of our rental fleet, employing a “cradle through grave” approach. During the life of our rental equipment, we (1) aggressively negotiate on purchase price; (2) use our customized information technology systems to closely monitor and analyze, among other things, time utilization (equipment usage based on customer demand), rental rate trends and pricing optimization and equipment demand; (3) continuously adjust our fleet mix and pricing; (4) maintain fleet quality through regional quality control managers and our on-site parts and services support; and (5) dispose of rental equipment through our retail sales force. This allows us to purchase our rental equipment at competitive prices, optimally utilize our fleet, cost-effectively maintain our equipment quality and maximize the value of our equipment at the end of its useful life.

Grow Our Parts and Services Operations. Our strong parts and services operations are keystones of our integrated equipment services platform and together provide us with a relatively stable high-margin revenue source. Our parts and services operations help us develop strong, ongoing customer relationships, attract new customers and maintain a high quality rental fleet. We intend to further grow this product support side of our business and further penetrate our customer base.

Enter Carefully Selected New Markets. We intend to continue our strategy of selectively expanding our network to solidify our presence in attractive and contiguous regions where we operate. We look to add new locations in those markets that offer attractive growth opportunities, high or increasing levels of demand for construction and heavy equipment, and contiguity to our existing markets. Eleven of our current 78 locations have opened since January 1, 2014.

6

Make Selective Acquisitions. The equipment industry is fragmented and includes a large number of relatively small, independent businesses servicing discrete local markets. Some of these businesses may represent attractive acquisition candidates. We intend to evaluate and pursue, on an opportunistic basis, acquisitions which meet our selection criteria, including favorable financing terms, with the objective of increasing our revenues, improving our profitability, entering additional attractive markets and strengthening our competitive position.

History

Through our predecessor companies, we have been in the equipment services business for approximately 56 years. H&E Equipment Services L.L.C. was formed in June 2002 through the combination of Head & Engquist Equipment, LLC (“Head & Engquist”), a wholly-owned subsidiary of Gulf Wide Industries, L.L.C. (“Gulf Wide”), and ICM Equipment Company L.L.C. (“ICM”). Head & Engquist, founded in 1961, and ICM, founded in 1971, were two leading regional, integrated equipment service companies operating in contiguous geographic markets. In the June 2002 transaction, Head & Engquist and ICM were merged with and into Gulf Wide, which was renamed H&E Equipment Services L.L.C. (“H&E LLC”). Prior to the combination, Head & Engquist operated 25 facilities in the Gulf Coast region, and ICM operated 16 facilities in the Intermountain region of the United States.

Prior to our initial public offering in February 2006, our business was conducted through H&E LLC. In connection with our initial public offering, we converted H&E LLC into H&E Equipment Services, Inc. In order to have an operating Delaware corporation as the issuer for our initial public offering, H&E Equipment Services, Inc. was formed as a Delaware corporation and wholly-owned subsidiary of H&E Holdings, and immediately prior to the closing of our initial public offering, on February 3, 2006, H&E LLC and H&E Holdings merged with and into us (H&E Equipment Services, Inc.), with us surviving the reincorporation merger as the operating company. Effective February 3, 2006, H&E LLC and H&E Holdings no longer existed under operation of law pursuant to the reincorporation merger.

We completed, effective as of February 28, 2006, the acquisition of all the outstanding capital stock of Eagle High Reach Equipment, Inc. (now known as H&E California Holding, Inc.) and all of the outstanding equity interests of its subsidiary, Eagle High Reach Equipment, LLC (now known as H&E Equipment Services (California), LLC) (collectively, “Eagle” or the “Eagle Acquisition”). Prior to the acquisition, Eagle was a privately-held construction and industrial equipment rental company serving the southern California construction and industrial markets out of four branch locations.

We completed, effective as of September 1, 2007, the acquisition of all of the outstanding capital stock of J.W. Burress, Incorporated (now known as H&E Equipment Services (Mid-Atlantic), Inc.) (“Burress” or the “Burress Acquisition”). Prior to the acquisition, Burress was a privately-held company operating primarily as a distributor in the construction and industrial equipment markets out of 12 locations in four states in the Mid-Atlantic region of the United States.

Customers

We serve approximately 38,800 customers in the United States, primarily in the West Coast, Intermountain, Southwest, Gulf Coast, Southeast and Mid-Atlantic regions. Our customers include a wide range of industrial and commercial companies, construction contractors, manufacturers, public utilities, municipalities, maintenance contractors and numerous and diverse other large industrial accounts. They vary from small, single machine owners to large contractors and industrial and commercial companies who typically operate under equipment and maintenance budgets. Our branches enable us to closely service local and regional customers, while our well-developed full-service infrastructure enables us to effectively service multi-regional and national accounts. Our integrated strategy enables us to satisfy customer requirements and increase revenues from customers through cross-selling opportunities presented by the various products and services that we offer. As a result, our five reporting segments generally derive their revenue from the same customer base. In 2016, no single customer accounted for more than 1.0% of our total revenues, and no single customer accounted for more than 10% of our revenue on a segmented basis. Our top ten customers combined accounted for approximately 6.4% of our total revenues in 2016.

Sales and Marketing

We have two distinct, focused sales forces; one specializing in equipment rentals and one focused specifically on new and used equipment sales. We believe maintaining separate sales forces for equipment rental and equipment sales is important to our customer service, allowing us to effectively meet the demands of different types of customers.

7

Both our rental sales force and equipment sales force are divided into smaller, product focused teams which enhances the development of in-depth product application and technical expertise. To further develop knowledge and experience, we provide our sales forces with extensive training, including frequent factory and in-house training by manufacturer representatives regarding the operational features, operator safety training and maintenance of new equipment. This training is essential, as our sales personnel regularly call on customers’ job sites, often assisting customers in assessing their immediate and ongoing equipment needs. In addition, we have a commission-based compensation program for our sales forces.

We maintain a company-wide customer relationship management system. We believe that this comprehensive customer and sales management tool enhances our territory management program by increasing the productivity and efficiency of our sales representatives and branch managers as they are provided real-time access to sales and customer information.

We have developed strategies to identify target customers for our equipment services in all markets. These strategies allow our sales force to identify frequent rental users, function as advisors and problem solvers for our customers and accelerate the sales process in new operations.

While our specialized, well-trained sales force strengthens our customer relationships and fosters customer loyalty, we also promote our business through marketing and advertising, including industry publications, direct mail campaigns, television, the Yellow Pages and our Company website at www.he-equipment.com.

Suppliers

We purchase a significant amount of equipment from the same manufacturers with whom we have distribution agreements. We purchased approximately 46% of our new equipment and rental fleet from three manufacturers (Grove/Manitowoc, Komatsu, and Genie Industries (Terex)) during the year ended December 31, 2016. These relationships improve our ability to negotiate equipment acquisition pricing. We are also a leading U.S. distributor for nationally-recognized equipment suppliers including JLG Industries, Gehl, Genie Industries (Terex), Komatsu, Doosan/Bobcat and Grove/Manitowoc. As an authorized distributor for a wide range of suppliers, we are also able to provide our customers parts and services that in many cases are covered under the manufacturer’s warranty. While we believe that we have alternative sources of supply for the equipment we purchase in each of our principal product categories, termination of one or more of our relationships with any of our major suppliers of equipment could have a material adverse effect on our business, financial condition or results of operations if we were unable to obtain adequate or timely rental and sales equipment.

Information Technology Systems

We have specialized information systems that track (1) rental inventory utilization statistics; (2) maintenance and repair costs; (3) returns on investment for specific equipment types; and (4) detailed operational and financial information for each piece of equipment. These systems enable us to closely monitor our performance and actively manage our business, and include features that were custom designed to support our integrated services platform. The point-of-sale aspect of our systems enables us to link all of our facilities, permitting universal access to real-time data concerning equipment located at the individual facility locations and the rental status and maintenance history for each piece of equipment. In addition, our systems include, among other features, on-line contract generation, automated billing, applicable sales tax computation and automated rental purchase option calculation. We customized our customer relationship management system to enable us to more effectively manage our sales territories and sales representatives’ activity. This customer relationship management system provides sales and customer information, available rental fleet and inventory information, a quote system and other organizational tools to assist our sales forces. We maintain an extensive customer database which allows us to monitor the status and maintenance history of our customers’ owned-equipment and enables us to more effectively provide parts and services to meet their needs. All of our critical systems run on servers and other equipment that is current technology and available from major suppliers and serviceable through existing maintenance agreements.

Seasonality

Although our business is not significantly impacted by seasonality, the demand for our rental equipment tends to be lower in the winter months. The level of equipment rental activities is directly related to commercial and industrial construction and maintenance activities. Therefore, equipment rental performance will be correlated to the levels of current construction activities. The severity of weather conditions can have a temporary impact on the level of construction activities.

Equipment sales cycles are also subject to some seasonality with the peak selling period occurring during the spring season and extending through the summer. Parts and services activities are less affected by changes in demand caused by seasonality.

8

The equipment industry is generally comprised of either pure rental equipment companies or manufacturer dealer/distributorship companies. We are an integrated equipment services company and rent, sell and provide parts and services support. Although there has been some consolidation within the equipment industry, including United Rentals’ acquisition of Rental Services Corporation in 2012 and United Rentals’ pending acquisition of NES Rentals, the equipment industry remains highly fragmented and consists mainly of a small number of multi-location regional or national operators and a large number of relatively small, independent businesses serving discrete local markets. Many of the markets in which we operate are served by numerous competitors, ranging from national and multi-regional equipment rental companies (for example, United Rentals, Sunbelt Rentals, Neff Rentals and Hertz Equipment Rental) or equipment dealers (for example, Finning and Toromont) to small, independent businesses with a limited number of locations.

We believe that participants in the equipment rental industry generally compete on the basis of availability, quality, reliability, delivery and price. In general, large operators enjoy substantial competitive advantages over small, independent rental businesses due to a distinct price advantage. Many rental equipment companies’ parts and services offerings are limited and may prove difficult to expand due to the training, infrastructure and management resources necessary to develop the breadth of service offerings and depth of knowledge our service technicians are able to provide. Some of our competitors have significantly greater financial, marketing and other resources than we do.

Traditionally, equipment manufacturers distributed their equipment and parts through a network of independent dealers with distribution agreements. As a result of consolidation and competition, both manufacturers and distributors sought to streamline their operations, improve their costs and gain market share. Our established, integrated infrastructure enables us to compete directly with our competitors on either a local, regional or national basis. We believe customers place greater emphasis on value-added services, teaming with equipment rental and sales companies who can meet all of their equipment, parts and services needs.

Environmental and Safety Regulations

Our facilities and operations are subject to comprehensive and frequently changing federal, state and local environmental and occupational health and safety laws. These laws regulate (1) the handling, storage, use and disposal of hazardous materials and wastes and, if any, the associated cleanup of properties affected by pollutants; (2) air quality (emissions); and (3) wastewater. We do not currently anticipate any material adverse effect on our business or financial condition or competitive position as a result of our efforts to comply with such requirements. Although we have made and will continue to make capital and other expenditures to comply with environmental requirements, we do not expect to incur material capital expenditures for environmental controls or compliance.

In the future, federal, state or local governments could enact new or more stringent laws or issue new or more stringent regulations concerning environmental and worker health and safety matters, or effect a change in their enforcement of existing laws or regulations, that could affect our operations. Also, in the future, contamination may be found to exist at our facilities or off-site locations where we have sent wastes. There can be no assurance that we, or various environmental regulatory agencies, will not discover previously unknown environmental non-compliance or contamination. We could be held liable for such newly-discovered non-compliance or contamination. It is possible that changes in environmental and worker health and safety laws or liabilities from newly-discovered non-compliance or contamination could have a material adverse effect on our business, financial condition and results of operations.

Employees

As of December 31, 2016, we had approximately 1,996 employees. Of these employees, 824 are salaried personnel and 1,172 are hourly personnel. Our employees perform the following functions: sales operations, parts operations, rental operations, technical services and office and administrative support. A collective bargaining agreement relating to two branch locations covers approximately 65 of our employees. We believe our relations with our employees are good, and we have never experienced a work stoppage.

Generally, the total number of employees does not significantly fluctuate throughout the year. However, acquisition activity or the opening of new branches may increase the number of our employees or fluctuations in the level of our business activity could require some staffing level adjustments in response to actual or anticipated customer demand.

Available Information

We file electronically with the SEC annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. The public may read and copy any materials we have filed with or furnished to the SEC at the SEC’s Public Reference Room at 100 F Street,

9

N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. Copies of our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, ownership reports for insiders and any amendments to these reports filed with or furnished to the SEC are available free of charge through our internet website (www.he-equipment.com) as soon as reasonably practicable after filing with the SEC. We use the Investor Relations section of our website as a means of disclosing material non-public information and for complying with our disclosure obligations under Regulation FD. Accordingly, investors should monitor the Investor Relations section of our website, in addition to following press releases, SEC filings and public conference calls and webcasts.

Additionally, we make available free of charge on our internet website:

|

|

• |

our Code of Conduct and Ethics; |

|

|

• |

the charter of our Corporate Governance and Nominating Committee; |

|

|

• |

the charter of our Compensation Committee; and |

|

|

• |

the charter of our Audit Committee. |

Investing in our securities involves a high degree of risk. You should consider carefully the following risk factors and the other information in this Annual Report on Form 10-K, including our consolidated financial statements and related notes, before making any investment decisions regarding our securities. If any of the following risks actually occur, our business, financial condition and operating results could be adversely affected. As a result, the trading price of our securities could decline and you may lose part or all of your investment.

Our business could be adversely affected by declines in construction and industrial activities, or a downturn in the economy in general, which could lead to decreased demand for equipment, depressed equipment rental rates and lower sales prices, resulting in a decline in our revenues, gross margins and operating results.

Our equipment is principally used in connection with construction and industrial activities. Consequently, a downturn in construction or industrial activities, or the economy in general, may lead to a decrease in the demand for equipment or depress rental rates and the sales prices for our equipment. Our business may also be negatively impacted, either temporarily or long-term, by:

|

|

• |

a reduction in spending levels by customers; |

|

|

• |

unfavorable credit markets affecting end-user access to capital; |

|

|

• |

adverse changes in federal, state and local government infrastructure spending; |

|

|

• |

an increase in the cost of construction materials; |

|

|

• |

adverse weather conditions which may affect a particular region; |

|

|

• |

an increase in interest rates; or |

|

|

• |

terrorism or hostilities involving the United States. |

Weakness or deterioration in the non-residential construction and industrial sectors caused by these or other factors could have a material adverse effect on our financial position, results of operations and cash flows in the future and may also have a material adverse effect on residual values realized on the disposition of our rental fleet. For example, during fiscal years 2009 and 2010, the economic downturn and related economic uncertainty, combined with weakness in the construction industry and a decrease in industrial activity, resulted in a significant decrease in the demand for our new and used equipment and depressed equipment rental rates, which resulted in decreased revenues and lower gross margins realized on our equipment rentals and on the sale of our new and used inventory during those periods. More recently, the decline in oil prices and the related downturn in oil industry activities during fiscal years 2014, 2015 and 2016 have resulted in a significant decrease in our new equipment sales, primarily the sale of new cranes, due to lower demand.

The inability to forecast trends accurately may have an adverse impact on our business and financial condition.

An economic downturn or economic uncertainty makes it difficult for us to forecast trends, which may have an adverse impact on our business and financial condition. For example, the economic downturn of 2009 and 2010 — which included, among other things,

10

significant reductions in available capital and liquidity from banks and other providers of credit, substantial reductions and/or fluctuations in equity and currency values worldwide and concerns that the worldwide economy may enter into a prolonged recessionary period — limited our ability, as well as the ability of our customers and our suppliers, to accurately forecast future product demand trends. More recently, declines in oil and natural gas prices, and uncertainty regarding future price levels, have negatively impacted the exploration, production and construction activity of our customers in those markets. Uncertainty regarding future equipment product demand could cause us to maintain excess equipment inventory and increase our equipment inventory carrying costs. Alternatively, this forecasting difficulty could cause a shortage of equipment for sale or rental that could result in an inability to satisfy demand for our products and a loss of market shares.

Unfavorable conditions or disruptions in the capital and credit markets may adversely impact business conditions and the availability of credit.

Disruptions in the global capital and credit markets as a result of an economic downturn, economic uncertainty, changing or increased regulation, reduced alternatives or failures of significant financial institutions could adversely affect our customers’ ability to access capital and could adversely affect our access to liquidity needed for business in the future. Additionally, unfavorable market conditions may depress demand for our products and services or make it difficult for our customers to obtain financing and credit on reasonable terms. Unfavorable market conditions also may cause more of our customers to be unable to meet their payment obligations to us, increasing delinquencies and credit losses. If we are unable to manage credit risk adequately, or if a large number of customers should have financial difficulties at the same time, our credit losses could increase above historical levels and our operating results would be adversely affected. Delinquencies and credit losses generally can be expected to increase during economic slowdowns or recessions. Moreover, our suppliers may be adversely impacted by unfavorable capital and credit markets, causing disruption or delay of product availability. These events could negatively impact our business, financial position, results of operations and cash flows.

In addition, if the financial institutions that have extended line of credit commitments to us are adversely affected by the conditions of the capital and credit markets, they may be unable to fund borrowings under those credit commitments, which could have an adverse impact on our financial condition and our ability to borrow funds, if needed, for working capital, acquisitions, capital expenditures and other corporate purposes.

Our significant indebtedness could adversely affect our financial condition.

We have a significant amount of indebtedness outstanding. As of December 31, 2016, we had total indebtedness of approximately $794.3 million, consisting of the $630.0 million aggregate amounts outstanding under our senior unsecured notes, $162.6 million of outstanding borrowing under our senior secured credit facility (the “Credit Facility”) and $1.7 million of capital lease obligations. As of February 16, 2017, we had borrowing availability under the Credit Facility of $469.7 million, net of a $7.7 million outstanding letter of credit.

Our indebtedness could have important consequences. For example, it could:

|

|

• |

increase our vulnerability to general adverse economic and industry conditions; |

|

|

• |

require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures and other general corporate purposes; |

|

|

• |

limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

|

|

• |

place us at a competitive disadvantage compared to our competitors that have less debt; and |

|

|

• |

limit our ability to obtain additional financing for working capital, capital expenditures, acquisitions or general corporate purposes. |

We expect to use cash flow from operations and borrowings under our Credit Facility to meet our current and future financial obligations, including funding our operations, debt service and capital expenditures. Our ability to make these payments depends on our future performance, which will be affected by financial, business, economic and other factors, many of which we cannot control. Our business may not generate sufficient cash flow from operations in the future, which could result in our being unable to repay indebtedness, or to fund other liquidity needs. If we do not have enough capital, we may be forced to reduce or delay our business activities and capital expenditures, sell assets, obtain additional debt or equity capital or restructure or refinance all or a portion of our debt, including the senior unsecured notes and our Credit Facility, on or before maturity. We cannot make any assurances that we will be able to accomplish any of these alternatives on terms acceptable to us, or at all. In addition, the terms of existing or future indebtedness, including the agreements governing the senior unsecured notes and the Credit Facility may limit our ability to pursue any of these alternatives.

11

We may not be able to generate sufficient cash to service all of our indebtedness and may be forced to take other actions to satisfy our obligations under our indebtedness, which may not be successful.

Our ability to make scheduled payments or to refinance our debt obligations depends on our financial and operating performance, which is subject to prevailing economic and competitive conditions and to certain financial, business and other factors beyond our control. We cannot make assurances that we will maintain a level of cash flows from operating activities sufficient to permit us to pay the principal, premium, if any, and interest on our indebtedness. In the absence of such operating results and resources, we could face substantial liquidity problems and might be required to dispose of material assets or operations to meet our debt service and other obligations. The Credit Facility and the indenture governing the senior unsecured notes restrict our ability to dispose of assets and use the proceeds from the disposition. We may not be able to consummate those dispositions or to obtain the proceeds which we could realize from such dispositions. Any proceeds we do receive from a disposition may not be adequate to meet any debt service obligations then due.

If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, seek additional capital or restructure or refinance our indebtedness. We cannot assure you that we would be able to take any of these actions, that these actions would be successful and permit us to meet our scheduled debt service obligations or that these actions would be permitted under the terms of our existing or future debt agreements, including the Credit Facility or the indenture governing the senior unsecured notes.

If we cannot make scheduled payments on our debt, we will be in default and, as a result:

|

|

• |

our debt holders could declare all outstanding principal and interest to be due and payable; |

|

|

• |

the lenders under the Credit Facility could terminate their commitments to lend us money and foreclose against the assets securing our borrowings; and |

|

|

• |

we could be forced into bankruptcy or liquidation. |

Despite current indebtedness levels, we may still be able to incur more indebtedness, which could further exacerbate the risks described above.

Under the terms of the agreements governing the Credit Facility and the senior unsecured notes, we and our subsidiaries may be able to incur substantial indebtedness in the future.

Additionally, our Credit Facility provides revolving commitments of up to $602.5 million in the aggregate. As of February 16, 2017, we had $469.7 million of availability under the Credit Facility, net of a $7.7 million outstanding letter of credit. If new debt is added to our current debt levels, the risks that we now face relating to our substantial indebtedness could intensify.

The agreements governing the Credit Facility and our senior unsecured notes restrict our ability to engage in certain corporate and financial transactions.

The agreements governing the Credit Facility and the senior unsecured notes contain certain covenants that, among other things, restrict or limit our and our restricted subsidiaries’ ability to:

|

|

• |

incur more debt; |

|

|

• |

pay dividends and make distributions; |

|

|

• |

issue preferred stock of subsidiaries; |

|

|

• |

make investments; |

|

|

• |

repurchase stock; |

|

|

• |

create liens; |

|

|

• |

enter into transactions with affiliates; |

|

|

• |

enter into sale and lease-back transactions; |

|

|

• |

merge or consolidate; and |

|

|

• |

transfer and sell assets. |

Our ability to borrow under the Credit Facility depends upon compliance with the restrictions contained in the Credit Facility. Events beyond our control could affect our ability to meet these covenants.

12

In addition, the Credit Facility requires us to meet certain financial conditions tests. Events beyond our control can affect our ability to meet these financial conditions tests and to comply with other provisions governing the Credit Facility and the senior unsecured notes. Our failure to comply with obligations under the agreements governing the Credit Facility and the senior unsecured notes may result in an event of default under the agreements governing the Credit Facility and the senior unsecured notes, respectively. A default, if not cured or waived, may permit acceleration of this indebtedness and our other indebtedness. We may not be able to remedy these defaults. If our indebtedness is accelerated, we may not have sufficient funds available to pay the accelerated indebtedness and may not have the ability to refinance the accelerated indebtedness on terms favorable to us or at all.

Variable rate indebtedness subjects us to interest rate risk, which could cause our debt service obligations to increase significantly.

Borrowings under the Credit Facility are at variable rates of interest and expose us to interest rate risk. As such, our results of operations are sensitive to movements in interest rates. There are many economic factors outside our control that have in the past and may, in the future, impact rates of interest including publicly announced indices that underlie the interest obligations related to a certain portion of our debt. Factors that impact interest rates include governmental monetary policies, inflation, recession, changes in unemployment, the money supply, international disorder and instability in domestic and foreign financial markets. If interest rates increase, our debt service obligations on the variable rate indebtedness would increase even though the amount borrowed remained the same, and our results of operations would be adversely impacted. Such increases in interest rates could have a material adverse effect on our financial conditions and results of operations.

Our business could be hurt if we are unable to obtain additional capital as required, resulting in a decrease in our revenues and profitability.

The cash that we generate from our business, together with cash that we may borrow under our Credit Facility, may not be sufficient to fund our capital requirements. We may require additional financing to obtain capital for, among other purposes, purchasing equipment, completing acquisitions, establishing new locations and refinancing existing indebtedness. Any additional indebtedness that we incur will make us more vulnerable to economic downturns and limit our ability to withstand competitive pressures. Moreover, we may not be able to obtain additional capital on acceptable terms, if at all. If we are unable to obtain sufficient additional financing in the future, our business could be adversely affected by reducing our ability to increase revenues and profitability.

Our revenue and operating results may fluctuate, which could result in a decline in our profitability and make it more difficult for us to grow our business.

Our revenue and operating results have historically varied from quarter to quarter. Periods of decline could result in an overall decline in profitability and make it more difficult for us to make payments on our indebtedness and grow our business. We expect our quarterly results to continue to fluctuate in the future due to a number of factors, including:

|

|

• |

general economic conditions in the markets where we operate; |

|

|

• |

the cyclical nature of our customers’ business, particularly our construction customers and customers in the oil and gas industry; |

|

|

• |

seasonal sales and rental patterns of our construction customers, with sales and rental activity tending to be lower in the winter months; |

|

|

• |

changes in the size of our rental fleet and/or in the rate at which we sell our used equipment from the fleet; |

|

|

• |

an overcapacity of fleet in the equipment rental industry; |

|

|

• |

severe weather and seismic conditions temporarily affecting the regions where we operate; |

|

|

• |

changes in corporate spending for plants and facilities or changes in government spending for infrastructure projects; |

|

|

• |

the effectiveness of integrating acquired businesses and new start-up locations; and |

|

|

• |

timing of acquisitions and new location openings and related costs. |

In addition, we incur various costs when integrating newly acquired businesses or opening new start-up locations, and the profitability of a new location is generally expected to be lower in the initial months of operation.

13

Fluctuations in the stock market, as well as general economic and market conditions, may impact the market price of our common stock.

The market price of our common stock has been and may continue to be subject to significant fluctuations in response to general economic changes and other factors including, but not limited to:

|

|

• |

variations in our quarterly operating results or results that vary from investor expectations; |

|

|

• |

changes in the strategy and actions taken by our competitors, including pricing changes; |

|

|

• |

securities analysts’ elections to discontinue coverage of our common stock, changes in financial estimates by analysts or a downgrade of our common stock or of our sector by analysts; |

|

|

• |

announcements by us or our competitors of significant contracts, acquisitions, strategic partnerships, joint ventures or capital commitments; |

|

|

• |

changes in the price of oil and other commodities; |

|

|

• |

investor perceptions of us and the equipment rental and distribution industry; and |

|

|

• |

national or regional catastrophes or circumstances and natural disasters, hostilities and acts of terrorism. |

Broad market and industry factors may materially reduce the market price of our common stock, regardless of or in a manner that is disproportionate to any related impact on our operating performance. As an example, in the latter half of 2014 the price of oil fell significantly and the price further declined and remained depressed throughout 2015 and 2016, compared to pre-2014 price levels, although the price rebounded somewhat in the latter half of 2016. We believe that this prolonged decline in oil prices and its impact on oil related economic activities is a significant factor in the price decline of our stock during the same period, even though other industrial and construction activities that are also primary drivers of our business generally remained at or above historic levels. In addition, the stock market historically has experienced price and volume fluctuations that often have been unrelated or disproportionate to the operating performance of companies. These fluctuations, as well as general economic and market conditions, including those listed above and others, may harm the market price of our common stock.

We are subject to competition, which may have a material adverse effect on our business by reducing our ability to increase or maintain revenues or profitability.

The equipment rental and retail distribution industries are highly competitive and the equipment rental industry is highly fragmented. Many of the markets in which we operate are served by numerous competitors, ranging from national and multi-regional equipment rental companies to small, independent businesses with a limited number of locations. We generally compete on the basis of availability, quality, reliability, delivery and price. Some of our competitors have significantly greater financial, marketing and other resources than we do, and may be able to reduce rental rates or sales prices. The market downturn and increased competitive pressures in 2009 and 2010 caused us to significantly reduce our rates to maintain market share, resulting in lower operating margins and profitability. We may encounter increased competition from existing competitors or new market entrants in the future, which could have a material adverse effect on our business, financial condition and results of operations.

We may not be able to facilitate our growth strategy by identifying or completing transactions with attractive acquisition candidates, which could limit our revenues and profitability. Future acquisitions may result in significant transaction expenses and we may involve significant costs. We may experience integration and consolidation risks associated with future acquisitions.

An element of our growth strategy is to selectively pursue on an opportunistic basis acquisitions of additional businesses. The success of this element of our growth strategy depends, in part, on selecting strategic acquisition candidates at attractive prices. We cannot assure you that we will be able to identify attractive acquisition candidates or complete the acquisition of any identified candidates at favorable prices and upon advantageous terms and conditions, including financing alternatives. We expect to face competition for acquisition candidates, which may limit the number of acquisition opportunities and lead to higher acquisition costs. We may not have the financial resources necessary to consummate any acquisitions or the ability to obtain the necessary funds on satisfactory terms. Any future acquisitions may result in significant transaction expenses and risks associated with entering new markets. We may also be subject to claims by third parties related to the operations of these businesses prior to our acquisition and by sellers under the terms of our acquisition agreements.

We may not have sufficient management, financial and other resources to integrate and consolidate any future acquisitions. Any significant diversion of management’s attention or any major difficulties encountered in the integration of the businesses we acquire could have a material adverse effect on our business, financial condition or results of operations, which could decrease our profitability and make it more difficult for us to grow our business. Furthermore, general economic conditions or unfavorable global

14

capital and credit markets could affect the timing and extent to which we successfully acquire new businesses, which could limit our revenues and profitability.

We may not be able to facilitate our growth strategy by identifying and opening attractive start-up locations, which could limit our revenues and profitability.

An element of our growth strategy is to selectively identify and implement start-up locations in order to add new customers. The success of this element of our growth strategy depends, in part, on identifying strategic start-up locations.

We also cannot assure you that we will be able to identify attractive start-up locations. Opening start-up locations may involve significant costs and limit our ability to expand our operations. Start-up locations may involve risks associated with entering new markets and we may face significant competition.

We may not have sufficient management, financial and other resources to successfully operate new locations. Any significant diversion of management’s attention or any major difficulties encountered in the locations that we open in the future could have a material adverse effect on our business, financial condition or results of operations, which could decrease our profitability and make it more difficult for us to grow our business. Furthermore, general economic conditions or unfavorable global capital and credit markets could affect the timing and extent to which we open new start-up locations, which could limit our revenues and profitability.

The continued payment of our quarterly dividend is subject to, among other things, the availability of funds and the discretion of our board of directors.

The payment of future dividends and the amount thereof is uncertain, at the sole discretion of our board of directors and considered by the board of directors each quarter. The payment of dividends is dependent upon, among other things, operating cash flow generated by our business, financial requirements for our operations, the execution of our growth strategy, the restrictions and covenants pursuant to our Credit Facility and senior unsecured notes, and the satisfaction of solvency tests imposed by the Delaware General Corporation Law and other applicable law for the declaration and payment of dividends.

We purchase a significant amount of our equipment from a limited number of manufacturers. Termination of one or more of our relationships with any of those manufacturers could have a material adverse effect on our business, as we may be unable to obtain adequate or timely rental and sales equipment.

We purchase most of our rental and sales equipment from leading, nationally-known original equipment manufacturers (“OEMs”). For the year ended December 31, 2016, we purchased approximately 46% of our rental and sales equipment from three manufacturers (Grove/Manitowoc, Komatsu, and Genie Industries (Terex)). Although we believe that we have alternative sources of supply for the rental and sales equipment we purchase in each of our core product categories, termination of one or more of our relationships with any of these major suppliers could have a material adverse effect on our business, financial condition or results of operations if we were unable to obtain adequate or timely rental and sales equipment.

Our suppliers of new equipment may appoint additional distributors, sell directly or unilaterally terminate our distribution agreements, which could have a material adverse effect on our business due to a reduction of, or inability to increase, our revenues.

We are a distributor of new equipment and parts supplied by leading, nationally-known OEMs. Under our distribution agreements with these OEMs, manufacturers retain the right to appoint additional dealers and sell directly to national accounts and government agencies. We have both written and oral distribution agreements with our new equipment suppliers. Under our oral agreements with the OEMs, we operate under our established course of dealing with the supplier and are subject to the applicable state law regarding such relationship. In most instances, the OEMs may appoint additional distributors, elect to sell to customers directly or unilaterally terminate their distribution agreements with us at any time without cause. Any such actions could have a material adverse effect on our business, financial condition and results of operations due to a reduction of, or an inability to increase, our revenues.

The cost of new equipment that we sell or purchase for use in our rental fleet may increase and therefore we may spend more for such equipment. In some cases, we may not be able to procure new equipment on a timely basis due to supplier constraints.

The cost of new equipment from manufacturers that we sell or purchase for use in our rental fleet may increase as a result of increased raw material costs, including increases in the cost of steel, which is a primary material used in most of the equipment we use, or due to increased regulatory requirements, such as those related to emissions. These increases could materially impact our financial condition or results of operations in future periods if we are not able to pass such cost increases through to our customers.

15

Our rental fleet is subject to residual value risk upon disposition.

The market value of any given piece of rental equipment could be less than its depreciated value at the time it is sold. The market value of used rental equipment depends on several factors, including:

|

|

• |

the market price for new equipment of a like kind; |

|

|

• |

wear and tear on the equipment relative to its age; |

|

|

• |

the time of year that it is sold (prices are generally higher during the construction season); |

|

|

• |

worldwide and domestic demands for used equipment; |

|

|

• |

the supply of used equipment on the market; and |

|

|

• |

general economic conditions. |

We include in operating income the difference between the sales price and the depreciated value of an item of equipment sold. Although for the year ended December 31, 2016, we sold used equipment from our rental fleet at an average selling price of approximately 152.3% of net book value, we cannot assure you that used equipment selling prices will not decline. Any significant decline in the selling prices for used equipment could have a material adverse effect on our business, financial condition, results of operations or cash flows.

We incur maintenance and repair costs associated with our rental fleet equipment that could have a material adverse effect on our business in the event these costs are greater than anticipated.

As our fleet of rental equipment ages, the cost of maintaining such equipment, if not replaced within a certain period of time, generally increases. Determining the optimal age for our rental fleet equipment is subjective and requires considerable estimates by management. We have made estimates regarding the relationship between the age of our rental fleet equipment, and the maintenance and repair costs, and the market value of used equipment. Our future operating results could be adversely affected because our maintenance and repair costs may be higher than estimated and market values of used equipment may fluctuate.

Security breaches and other disruptions in our information technology systems, including our customer relationship management system, could limit our capacity to effectively monitor and control our operations, compromise our or our customers’ and suppliers’ confidential information or otherwise adversely affect our operating results or business reputation.

Our information technology systems, some of which are managed by third parties, facilitate our ability to monitor and control our operations and adjust to changing market conditions, including processing, transmitting, storing, managing and supporting a variety of business processes, activities and information. Any disruption in any of these systems, including our customer management system, or the failure of any of these systems to operate as expected could, depending on the magnitude of the problem, adversely affect our operating results by limiting our capacity to effectively monitor and control our operations and adjust to changing market conditions.

Additionally, we collect and store sensitive data, including proprietary business information and the proprietary business information of our customers and suppliers, in data centers and on information technology networks. The secure operation of these information technology networks and the processing and maintenance of this information is critical to our business operations and strategy. Despite security measures and business continuity plans, our information technology networks and infrastructure may be vulnerable to damage, disruptions or shutdowns due to attacks by cyber criminals or breaches due to employee error or malfeasance or other disruptions during the process of upgrading or replacing computer software or hardware, power outages, computer viruses, telecommunication or utility failures, terrorist acts or natural disasters or other catastrophic events. The occurrence of any of these events could compromise our networks, and the information stored there could be accessed, publicly disclosed, lost or stolen. Any such access, disclosure or other loss of information could result in legal claims or proceedings, liability or regulatory penalties under laws protecting the privacy of personal information, disrupt operations, and damage our reputation, which could adversely affect our business. In addition, as security threats continue to evolve we may need to invest additional resources to protect the security of our systems.

Fluctuations in fuel costs or reduced supplies of fuel could harm our business.

We could be adversely affected by limitations on fuel supplies or significant increases in fuel prices that result in higher costs to us for transporting equipment from one branch to another branch or one region to another region. A significant or protracted disruption of fuel supplies could have an adverse effect on our financial condition and results of operations.

16

Hurricanes, other adverse weather events, national or regional catastrophes or natural disasters could negatively affect our local economies or disrupt our operations, which could have an adverse effect on our business or results of operations.

Our market areas in the Gulf Coast and Mid-Atlantic regions of the United States are susceptible to hurricanes. Such weather events can disrupt our operations, result in damage to our properties and negatively affect the local economies in which we operate. Future hurricanes could result in damage to certain of our facilities and the equipment located at such facilities, or equipment on rent with customers in those areas. In addition, climate change could lead to an increase in intensity or occurrence of hurricanes or other adverse weather events, including severe winter storms. Future occurrences of these events, as well as regional or national catastrophes or natural disasters, and their effects may adversely impact our business or results of operations.

We are dependent on key personnel. A loss of key personnel could have a material adverse effect on our business, which could result in a decline in our revenues and profitability.

Our senior and regional managers have an average of approximately 23 years of industry experience. Our branch managers have extensive knowledge and industry experience as well. Our success is dependent, in part, on the experience and skills of our management team. Competition for top management talent within our industry is generally significant. If we are unable to fill and keep filled all of our senior management positions, or if we lose the services of any key member of our senior management team and are unable to find a suitable replacement in a timely manner, we may be challenged to effectively manage our business and execute our strategy.

If the Company fails to maintain an effective system of internal controls, the Company may not be able to accurately report financial results or prevent fraud.