Attached files

| file | filename |

|---|---|

| 10-K - 10-K - AUTOLIV INC | d302454d10k.htm |

| EX-32.2 - EX-32.2 - AUTOLIV INC | d302454dex322.htm |

| EX-32.1 - EX-32.1 - AUTOLIV INC | d302454dex321.htm |

| EX-31.2 - EX-31.2 - AUTOLIV INC | d302454dex312.htm |

| EX-31.1 - EX-31.1 - AUTOLIV INC | d302454dex311.htm |

| EX-23 - EX-23 - AUTOLIV INC | d302454dex23.htm |

| EX-21 - EX-21 - AUTOLIV INC | d302454dex21.htm |

| EX-12.1 - EX-12.1 - AUTOLIV INC | d302454dex121.htm |

| EX-10.48 - EX-10.48 - AUTOLIV INC | d302454dex1048.htm |

| EX-10.47 - EX-10.47 - AUTOLIV INC | d302454dex1047.htm |

Exhibit 13

Autoliv Annual Report 2016

Content1)

| 03 |

Global Presence | |

| 04 |

Who we are, What we do | |

| 05 |

2016 in Summary | |

| 06 |

President’s Letter | |

| 08 |

Segments | |

| 10 |

Real Life Safety | |

| 12 |

Financial Targets | |

| 13 |

Strategies | |

| 20 |

Market & Competitors | |

| 22 |

Customers | |

| 24 |

Our People | |

| 27 |

Sustainability | |

| 34 |

Shareholders | |

| 36 |

Share Performance | |

| 39 |

Management’s Discussion and Analysis | |

| 58 |

Consolidated Statements of Net Income | |

| 58 |

Consolidated Statements of Comprehensive Income | |

| 59 |

Consolidated Balance Sheets | |

| 60 |

Consolidated Statements of Cash Flows | |

| 61 |

Consolidated Statements of Total Equity | |

| 62 |

Notes to Consolidated Financial Statements | |

| 86 |

Auditor’s Reports | |

| 87 |

Glossary and Definitions | |

| 88 |

Corporate Governance | |

| 90 |

Board of Directors | |

| 91 |

Executive Management | |

| 92 |

Contact Information & Calendar | |

| 93 |

Selected Financial Data |

1) See page in Annual Report.

Reader’s Guide

Autoliv, Inc. is incorporated in Delaware, USA, and follows Generally Accepted Accounting Principles in the United States (U.S. GAAP). This annual report also contains certain non-U.S. GAAP measures, see page 41 and page 55 in the Annual Report. All amounts in this annual report are in U.S. dollars unless otherwise indicated. “We”, “the Company” and “Autoliv” refer to “Autoliv, Inc.” as defined in Note 1 “Principles of Consolidation” on page 62 in the Annual Report. For forward-looking information, refer to the “Safe Harbor Statement” on page 57 in the Annual Report. Data on markets and competitors are Autoliv’s estimates (unless otherwise indicated). The estimates are based on orders awarded to us or our competitors or other information put out by third parties as well as plans announced by vehicle manufacturers and regulatory agencies.

Financial Information

Every year, Autoliv publishes an annual report and a proxy statement prior to the Annual General Meeting of Shareholders, see page 36 in the Annual Report. The proxy statement provides information not only on the agenda for the meeting, but also on the work of the Board of Directors and its committees as well as on compensation paid to and presentation of directors and certain senior executive officers. For financial information, please also refer to the Form 10-K and Form 10-Q reports and Autoliv’s other filings with the Securities and Exchange Commission (SEC). These filings are available at www.autoliv.com under Investors/Filings. The annual and quarterly reports, the proxy statement and Autoliv’s filings with the SEC as well as the Company’s Corporate Governance Guidelines, Charters, Code of Conduct and other documents governing the Company can be downloaded from the Company’s corporate website. Hard copies of the above-mentioned documents can be obtained free of charge from the Company at the addresses on page 92 in the Annual Report.

Superior Global Presence

Autoliv has operations in 27 countries and one of the broadest customer bases of any automotive supplier. We have the largest global footprint in automotive safety.

SALES 2016

AMERICAS 34% OF SALES

EUROPE 30% OF SALES

JAPAN 9% OF SALES

CHINA 18% OF SALES

REST OF ASIA 9% OF SALES

FORD 11%

HYUNDAI/KIA 11%

NISSAN/RENAULT 11%

HONDA 10%

GM 10%

MERCEDES BENZ 8%

VW 7%

FCA 6%

TOYOTA 6%

BMW 4%

PSA 3%

LOCAL CHINESE OEM’S 3%

MAZDA 2%

MITSUBISHI 2%

LAND ROVER 2%

VOLVO 2%

OTHERS 2%

Autoliv’s vision of Saving More Lives is the guiding principle to more than 70,000 associates in 27 countries. Each year, our products save over 30,000 lives and prevent ten times as many severe injuries.

Who we are What we do

For over six decades, Autoliv has demonstrated the ability to be responsive in real life safety situations.

We are a Fortune 500 company and the world’s largest automotive safety supplier with sales to all the leading car manufacturers in the world. We develop, manufacture and market protective systems such as airbags, seatbelts, steering wheels, passive safety electronics and active safety systems including brake control systems, radar, night vision and camera vision systems. We also produce pedestrian protection systems.

Human errors cause more than 90% of all fatal crashes, and the introduction of active safety systems is expected to increase road safety further, either by avoiding or reducing the speed of impact.

Autoliv’s mission is to be the leading supplier of safety systems for the future car, well integrated with autonomous driving.

Our values One Autoliv, Transparent, Innovative and Agile are a reflection of our company’s DNA, as well as how we will succeed going forward. Not only do we strive to prevent serious accidents and injuries, we challenge ourselves to continuously focus on what is important – consistency and quality for our customers, confidence and security for our employees, stability and growth for our shareholders, as well as being sustainable and earning trust within our communities.

HEADQUARTERS

Stockholm, Sweden

INCORPORATED

Delaware, United States

SEGMENTS

Passive Safety and Electronics

ASSOCIATES > 70,000 worldwide

OPERATIONS IN 27 countries

TECH CENTER LOCATIONS 22 worldwide

CRASH TEST TRACKS 19 worldwide

LIVES SAVED > 30,000 per year

PREVENT/REDUCE SEVERE INJURIES > 300,000 annually

2016 in Summary

Solid growth and execution. Autoliv made significant investments for the future and executed on its M&A strategy.

16% organic growth in active safety1)

$203m in direct shareholder returns

39% market share in the global passive safety market

$868m in operational cash flow

10% total sales growth

$499m of CAPEX, supporting growth

1) Non-US GAAP measure see page 41 in the Annual Report for reconciliation

Strong Organic Sales Growth

In 2016, consolidated sales were $10,074 million. Excluding negative currency translation effects and positive M&A effects from our recent acquisition, Autoliv grew 7% organically, making it the seventh consecutive year with organic sales growth.

Dear Shareholder,

2016 was a year of solid execution and growth for Autoliv. It was also a year of high order intake and correspondingly high investments in the future growth of our company. The year was further characterized by significant changes in our industry, in both passive safety and electronics.

For the first time, Autoliv’s sales in 2016 exceeded 10 billion dollars, resulting in a total sales growth of around 10%, double the growth of the global light vehicle production. Organic sales grew by over 7%. The additional sales growth was a result of recent M&A and joint venture activities.

The double digit total sales growth shows that we are executing on our strategy of growing organically, through the solid execution of our on-going business and through the integration of assets coming from M&A activities.

It was also a year of continued high investments in preparation of strong anticipated future growth in both our business segments, Passive Safety and Electronics. These investments limit our short term earnings potential, but they will enable us to further strengthen our market leadership and earnings potential in the years to come.

The combination of growth and high investments resulted in an operating margin well within our long term target range of 8-9%. I am pleased that we were able to achieve this level of earnings while simultaneously making significant investments for the future.

Investments for growth

Our expectations for high future growth are based on the high order intake we have experienced in 2015 and 2016. As indicated in our guidance for 2017 this “high order intake – high investment” scenario that started already in 2015 and continued throughout 2016 will also impact 2017. This period of high investments, particularly in research, development and engineering, has two main purposes: to prepare us for the anticipated high future delivery volumes in passive safety and to invest further in product development in active safety to secure continued technology leadership. Both are necessary for our future growth and earnings potential.

Firstly, in our Passive Safety segment we have had two full years of around 50% order intake, more than 10% higher than our current passive safety market share. This positive development is leading to high investments, in preparation for our customers start of production. For example, in just two years, we have more than doubled the number of customer development projects. These projects will only start to generate revenues for us when our customers start production, which occur one and a half to three years after they are initiated.

Secondly, within our Electronics segment we continued our high level of investment, mainly for product development in our active safety business. We fully believe in this strategy as active safety leading towards autonomous driving is one of the fastest growing business opportunities in the world. In this high growth area, we captured around 25% of the available business in 2016, which shows our customers’ confidence in our Active Safety products and Advanced Driver Assistance Systems (ADAS).

Quality first

Our vision of Saving More Lives and our three core strategies: Quality, One Product one Process and Innovation remain unchanged. As always Quality is our main focus. In 2016 we continued to make progress in terms of our quality metrics. One key metric, developed to further sharpen our quality efforts is measuring “zero defects”. A zero defect requires a production line to run absolutely flawlessly. This is a very tough metric that only a few years ago seemed more like a distant aspiration than a target. Today more than 10% of our production lines run with zero defects for at least 15 consecutive days, more than double the proportion of lines only one year ago.

Despite our relentless focus on quality, we experienced some quality related issues in 2016. Although relatively limited, these can never be tolerated and we are taking additional measures to further strengthen certain aspects of our quality initiatives.

Strategic M&A and joint ventures

In addition to our investments for future growth and the continued sharp focus on quality, we executed strategically important M&A and joint venture activities during the year.

At the end of the first quarter we finalized the agreement to form a joint venture in the area of brake control with the Japanese manufacturer Nissin Kogyo. The new company, Autoliv-Nissin Brake Systems (ANBS) is now operational. In the latter part of 2016 it recorded a significant new business win with a lifetime contract value of more than 1 billion dollars with a U.S. based car manufacturer.

In September we announced another strategic joint venture, this time with Volvo Car Corporation. This new company, subsequently named Zenuity, will represent a very important addition to our active safety strategy towards autonomous driving. The set-up is unique. All decision making and system level software development at Volvo Cars and Autoliv for Advanced Driver Assistance Systems (ADAS) and Highly Autonomous Driving (HAD) will be concentrated in this joint venture. No other car manufacturer and tier one supplier have formed this type of 50/50 joint venture in such a strategic area. In addition Autoliv will market and sell Zenuity’s software solutions to all car manufacturers globally. We strongly believe it will be a significant competitive advantage over the years to come as openness and collaboration become increasingly important for sharing the burden of high development costs and improving time to market in the area of autonomous driving. Zenuity is planning its start of operations for the first half of 2017.

This initiative fits perfectly with Autoliv’s stated mission of being the leading safety system supplier for the future car, well integrated with autonomous driving.

Focus on sustainability

During 2016 we have put increased focus on developing our sustainability strategy. We make contributions to society by staying at the forefront of technology, innovating and manufacturing high quality products that help our customers save more lives in real-life traffic. In 2017, we will also put more focus on developing targets to limit our impact on the environment, while continuing our on-going work to ensure ethical operations and being an employer of choice.

Shareholder returns

In 2016, the S&P 500 Index increased by about 10%, and the OMX All Shares Index in Stockholm where Autoliv’s SDR’s are listed, increased by 6%. The Autoliv share was down 9% on NYSE, while the OMX listed SDR’s closed down 4% compared to one year ago. In 2016 relevant automotive indexes (S&P and OMX) also underperformed the general market. Looking at the share over a three year period (a relevant cycle given Autoliv’s typical time from order to revenues) Autoliv’s share has outperformed the OMX All Share index by close to 50%, and also outperformed the S&P 500 index.

During the year Autoliv returned more than 200 million dollars, or 2.30 dollars per share, to its shareholders through regular dividends, a new record.

We exited the year with a net debt to EBITDA ratio of 0.4x. It is our target that over time, this ratio should be between 0.5x and 1.5x. We are continuing to monitor this measure, as we aim to be shareholder friendly and over time return excess cash to our shareholders.

Looking ahead

The automotive safety industry is in a period of great change. In Passive Safety one of our key competitors has encountered serious quality related issues and may be undergoing some form of restructuring. Meanwhile other main competitors have recently changed ownership.

In Electronics, particularly within active safety, rapid industry growth is expected to continue for many years and a group of companies both from the automotive and technology industries are positioning themselves to take part in this high growth environment.

In this transitionary environment we continue to work toward our end of decade targets outlined at our Capital Markets day in 2015. Over time it is inevitable that some changes will occur as the market continues to develop and change. Currently, we believe we will surpass our corporate sales target of 12 billion dollars by the end of the decade while our target of achieving more than one billion dollars in active safety sales is likely to be realized one year later than originally anticipated.

For 2017 Autoliv anticipates full-year organic growth of around 4%. The expectation for the full year adjusted operating margin is around 8.5%, excluding costs for capacity alignment and antitrust related matters.

In summary

Autoliv exists to save lives and create long term sustainable value for our stakeholders, particularly you the shareholder. To do this I believe we need to deliver in three areas.

| • | Quality, which leads to trust and security. This is the number one priority. |

| • | Robustness, providing the durability and functions our customers expects over time. |

| • | User experience, ensuring our products are easy to understand and use. |

We deal with the physical transportation of humans at very high speeds, which, should something go wrong, is a matter of life and death. If we deliver quality, robustness and a great user experience, we will create the trust needed to emerge as a winner in a transformed automotive industry.

With our vision of saving more lives and quality first as guiding lights we continue our journey to further strengthen our leadership in automotive safety.

Yours sincerely,

Jan Carlson

Chairman, President & CEO

Stockholm, February 23, 2017

Autoliv runs its business through two business segments: Passive Safety and Electronics.

Passive Safety

Passive Safety is Autoliv’s largest segment, and it includes Autoliv’s airbag, steering wheel and seatbelt businesses, accounting for 79% of Autoliv’s business in 2016.

The segment is organized in geographies: Europe, North America, South America, China, Korea, Japan & South East Asia and India. The segment has full responsibility for profit and loss account, technology development, applications engineering and purchasing.

2016 development

Consolidated segment sales grew by close to 4% to $7,919 million compared to $7,621 million in the full year 2015. Excluding negative currency translation effects of more than $161 million, the organic sales growth was 6%. The organic sales growth was mainly due to higher sales in Europe, China, Japan, North America and India.

The improvement in operating margin is primarily because costs relating to antitrust matters and capacity alignments (particularly European) were higher in 2015 than in 2016.

Sales of airbag products (including steering wheels) were favorably impacted by higher sales of inflatable curtains in Japan and Europe, and steering wheels, especially in Europe.

Sales of seatbelt products were particularly strong in Europe and China. The global trend towards more advanced and higher value-added seatbelt systems continued globally.

Headcount

The increase in Passive Safety headcount was driven by growth in both sales and order intake, although at a lower rate.

MIKAEL BRATT President Passive Safety

Looking back at 2016, what are you most proud of?

The ability to deliver quality and set the foundation for the unprecedented wave of new launches to be executed over the next few years. We have supported the industry need for replacement inflators, and see expansions of machine build, streamlining of processes and positive execution on existing contracts. It has been an exciting and eventful first year at Autoliv.

What are you looking forward to in 2017?

Execution on quality, delivery, and cost is the mantra for 2017. Quality is always at the forefront of all we do, and I look forward to continuing to embrace the zero defects culture in all dimensions of Q5. Our team is empowered as a stronger more autonomous segment to focus on our business situations and excel.

Electronics

Electronics integrates resources and expertise in passive safety electronics, active safety products and brake control systems into one organization. The segment has full responsibility for profit and loss account, technology development, applications engineering and purchasing.

2016 Development

Consolidated sales increased by close to 40% compared to the full year 2015. Excluding acquisition effects from ANBS and MACOM of $426 million and negative currency translation effects of more than $11 million, the organic sales growth was more than 13%.

The lower operating margin was mainly a result of costs related to the formation of ANBS and higher costs for R,D&E, net, partially offset by higher organic sales.

Growth in organic sales for passive safety electronics products (mainly airbag control modules and remote sensing units) was due to growth across most regions, particularly in China.

The strong increase in sales of active safety products (automotive radars, night vision systems, cameras with driver assist systems and positioning systems) resulted from growth particularly for radar products in North America and camera and radar products in Europe.

Sales of brake control systems were in line with our expectations from the start of operations of ANBS in the beginning of the second quarter of 2016.

Headcount

The increase in Electronics headcount was mainly due to the integration of ANBS and hiring of R,D&E engineers in support of future growth.

JOHAN LÖFVENHOLM President Electronics

Looking back at 2016, what are you most proud of?

A successful launch of state-of-the-art active safety products for Daimler, a well-managed sales growth in passive safety electronics, and the integration of a completely new family member in brake systems are excellent examples of great accomplishments that make my team and me proud. Securing new business in all product areas shows that we are on the right path toward our long-term growth targets.

What are you looking forward to in 2017?

A continued focus on growth without compromising operational excellence. This includes the challenge of taking on the big wave of engineering work that is following successful business wins. With a winning mindset, I am confident that my team will succeed.

Industry Pioneer in Real Life Safety

We are an industry pioneer in automotive real life safety with more than 60 years of innovation, from mechanical seatbelts in the 1950s to our current state-of-the-art active safety electronics and systems.

Traffic Safety Research

Our road to saving more lives starts with our relentless innovation in vehicle safety technologies in combination with a deep understanding of traffic situations, human behavior and human-to-machine interaction. In order to better understand real life accidents as well as new risks associated with higher level automated driving, we research and study accident data in combination with our own field operational tests. The way we innovate to develop and engineer solutions is a key differentiator that we believe will continue to set us apart from our competitors.

Passive Technologies

Passive Technology for protection, from seatbelts and airbags to passive electronics, is our heritage and the foundation for Autoliv’s strong position in real life vehicle safety. We have pioneered innovation in passive safety since the 1950s and incrementally innovate our passive portfolio to improve protection, such as active seatbelts and complementary airbag solutions. We continue to drive passive safety innovation for autonomous vehicles.

Active Technologies

Active Technologies for the prevention and prediction of accidents are key enablers of Real Life Safety. No single technology – radar, vision, infrared, lidar or ultrasonic – is able to cover all sensing requirements. Leveraging our strong base in radar and vision technologies, we continuously expand our know-how by adding new building blocks, such as braking and GPS features, toward autonomous driving.

System integration

Fully mastering the sequence of traffic events, from prevention to prediction to protection, with the aim of bringing the driver back to normal driving state before an accident occurs, requires sensor fusion based on complex software algorithms integrated with precise actuation and advanced passive safety features. This increased responsibility for managing the entire safety chain toward autonomous driving is something we can now offer to our customers.

RADAR

Avoid Blind Spot Crashes

A radar system detects and warns of objects in the vehicle’s blind spots.

RADAR

Warn of Potential Collisions

A radar system provides an all-weather object detection and an advance warning of potential collisions, up to 120 meters ahead. Long-range radars are used for Adaptive Cruise Control systems (ACC) and Autonomous Emergency Braking (AEB).

CAMERAS

An Extra Pair of Eyes

Mono and stereo vision cameras can recognize vehicles, pedestrians, speed signs and lane markings, and are used in the Advanced Driver Assistance Systems (ADAS) to avoid collisions.

Seatbelts Prevent Fatalities

The combination of seatbelt, seatbelt pretensioners, load limiters, lap pretensioners and frontal airbags reduces the risk of life-threatening head or chest injuries in frontal crashes by 75%.

Airbags

In frontal crashes, driver airbags reduce fatalities by approximately 25% and reduce serious head injuries by over 60%. For front-seat passengers, fatalities are reduced by approximately 20%. Side-curtain airbags reduce the risk of life-threatening head injuries in side impacts by approximately 50% for passengers sitting on the side of the vehicle that is struck. Side airbags, rear side airbags, knee airbags and far-side airbags also help save lives and reduce serious injuries.

RADAR

Queue Assist

A radar controls stop-and-go functions in the queue.

BRAKE CONTROL

Optimum braking

Brake Actuation and Brake Control use sensors to apply the correct braking pressure for a given condition. They also offer electronic stability control, anti-locking brakes and traction control systems.

ADAS ECU

A Supporting Brain

The ADAS ECU ‘brain’ monitors the surroundings and fuses data from cameras, radars and sensors to interpret the situation and trigger ADAS features like emergency braking or automatic lane change. Satellite sensors – in the door beam, in the pillar between the doors, the rocker panel, and/or at the front of the vehicle – trigger seatbelt pretensioners and airbag systems.

NIGHT VISION

Night Driving Assist

In challenging lighting – at night, in fog, blinding headlight and sunlight glare – collisions can be avoided as far infrared technology shows a heat-generated image of animals, pedestrians and more.

Steering wheels alert

An integrated electrical motor can vibrate the steering wheel, alerting the driver to dangerous situations.

PEDESTRIAN PROTECTION

Protect Pedestrians

Thanks to a pyrotechnic hood-lifter and/or an outside pedestrian protection airbag, a pedestrian who is hit can avoid head injury caused by the hard area between the hood and the windscreen or one of the windshield pillars.

Autoliv’s long-term targets reflect the key performance measures through which we execute our key strategies. The targets cover the areas of sales growth, capital structure, sustainable margins and earnings growth.

Financial Targets

Organic Sales

Grow at least in line with our market. Definition on page 41 in the Annual Report. (Non-U.S. GAAP measure).

In 2016, Autoliv’s organic sales increased by 7%, compared to our underlying automotive safety market that grew by 8%. Sales growth was particularly strong in China and Europe, which grew by 14% and 10%, respectively, partly due to electronics.

Operating Margin

8–9% over the business cycles. (Non-U.S. GAAP excluding antitrust matters).

Autoliv achieved an adjusted operating margin, of 8.5% in 2016, within our long-term target range. This was achieved despite higher R,D&E, net, and other costs related to investments for capacity and growth as well as acquisition effects.

Earnings Per Share

Growth adjusted EPS faster than organic sales growth. (Non-U.S. GAAP excluding antitrust matters).

In 2016, adjusted EPS (excluding antitrust related costs) grew by 11%, which was approximately 4 percentage points better than the organic sales increase. The operating profit and the number of outstanding shares were higher than prior year. The increase in EPS was mainly driven by lower costs for capacity alignment.

Leverage Ratio

Around 1 time within the range of 0.5 to 1.5 times. Definition on page 87 in the Annual Report. (Non-U.S. GAAP measure).

Our target ratio is around one time, within a range of 0.5 to 1.5 times. By the end of 2016, Autoliv had net debt of $313 million. The leverage ratio was 0.4. There were no share repurchases made during 2016.

Our Strategies

In addition to our vision of Saving More Lives, Autoliv’s purpose is to create value for our main stake-holders: owners and creditors, customers, business partners, employees as well as family and society.

Quality

Zero defects by flawless execution

One Product

One Process

To improve cost effectiveness and robustness

Innovation

To create unique selling points

Quality

Paramount in Saving More Lives

Proactive Cycle

Lessons Learned /Standards /Global Yokoten(s)

Proactive Poka-Yoke Before Issue Occurs

Proactive Read-Across

Active Follow Up

Efficient Management of Risk, Resources, Timing & Financials

Quality always comes first. People’s lives depend on our safety products. We strive for zero defects and quality must always come first.

Quality is a top priority for Autoliv, but the Company does not maintain it through programs or by performing close inspections alone. It is very much about the quality mindset in the Autoliv culture and the people who make up the organization.

Our quality mindset drives a constant focus on delivering quality products, which motivates us to improve our processes and provide on-time delivery of quality products to our customers. This quality mindset also achieves greater cost effectiveness to satisfy our stakeholders. But more importantly, we are providing best-in-class safety systems and saving more lives,” says Svante Mogefors, Group VP Quality and Manufacturing.

Autoliv implements its quality strategy through the Q5 program, which shapes a proactive quality culture of zero defects. It is called Q5 because it addresses quality in five dimensions: customers, products, suppliers, growth and behavior.

“Thanks to our relentless focus on quality in all dimensions, we have successfully reduced the number of nonconforming events since 2011 by 49% despite the challenge of much higher sales volumes,” Svante Mogefors says.

The goal is to tie quality firmly together with value in all our processes and for all our employees, thereby leading to the best value for all our customers. “By developing the right skills and abilities of our people and continuously fostering a quality mindset – we create a proactive culture and behavior that promotes goal alignment,” says Svante Mogefors.

At the root of deeper engagement

At Autoliv we know that if we increase output we need to increase the input in people. We apply a long-term strategy on quality practices and promoting the meaning of our work. We have purpose alignment – saving more lives – we care about what we do and this makes for deep, not shallow, engagement. And we have role alignment, which means we challenge people to crowd source ideas for improvements and we celebrate the good and the bad findings.

‘We’re doing this because we want to save more lives,” Mogefors asserts. “That’s the common thread that runs all the way down from the top of the company to the shop floors.”

Autoliv has promoted this mindset through programs such as its “Zero Defect” initiative. “Rather than thinking about PPMs or defects per million, we hold ourselves to a standard of zero defects delivered through operations to our customers,” he explains. This is marked in days and is celebrated each time it reaches 15 consecutive days, thereby making it accountable, obtainable and measured.

In 2016, Autoliv extended its zero defects roll-out to suppliers and non-production, applying its methodology and learnings globally, resulting in a significant increase in lines achieving zero defects.

When quality deviations do occur, they rarely affect the protection provided by our products. Most deviations are due to other requirements, such as flawless labeling, precise delivery of the right parts at the right moment, color and texture nuance on steering wheels and other products where the look and feel is important to the car buyer.

Zero Defect culture

“We take a workshop approach with the production team responsible for each production line, to align the team’s focus on identifying the obstacles to zero defects and overcoming those obstacles.”

Surprisingly, this approach does not typically result in the need for large capital investment or the implementation of sophisticated new tools in production lines during this process. “It’s more about the behavior of the people who know the product best,” Mogefors says. “They know what physical barriers are involved in the production line on a daily basis. They are empowered to share their insights and ideas to address the root causes of defects once they are understood. And they are celebrated both for finding an error which can be addressed, and for hitting target days with no errors.”

“We aspire to the day when all our production lines produce zero defects on a daily basis,” he says, noting that this has required some retraining of employees to the zero defect mindset. “It’s really more about training in the concept and exposure to how applying a different way of thinking to our daily activities can be effective.”

Autoliv has seen strong results from the Zero Defects initiative. “We have many examples of production lines delivering zero defects in electronics, seatbelts and airbags,” he says.

“We are all united in the common vision of saving more lives. It is at the heart of everything we do and it means our operators don’t just sew airbags, but save lives. And it aligns our common goals across the globe.”

“You never stop improving if you identify things that can be improved,” Mogefors says.

Jidoka is Me – Automation with a human touch

Operator Anna was working on a seatbelt line when she noticed that a rail she was holding felt slightly lighter than normal. She stopped the line and initiated her team to check the rail dimensions. They detected that the part dimensions were different than the specs. The normal finished part weight is 292 grams and this finished part was 261 grams. A root cause analysis by the supplier showed the part had not been coated.

Traceability, stringent supplier quality and robust audits are part of Autoliv’s approach to flawless execution.

Autoliv’s strategy One Product One Process (1P1P) drives reduction of cost and complexity. Through effective standardization and by the application of lessons learned, we increase robustness and prevent incidents, creating increased customer satisfaction and value.

Day-to-day 1P1P is being executed with a global mindset in the areas of product design, manufacturing process, supplier management and knowledge transfer within Autoliv and to its partners. “With 1P1P, we drive standardization and cost reduction in our core products and customer features, without sacrificing the need for customer variations in product design,” says Mikael Bratt, President Passive Safety, Autoliv.

Global teams

Global cross-functional teams with the authority and responsibility to manage one or several product families drive the standardization process. During 2016, over 90% of Autoliv’s products were covered by 1P1P teams. “This ensures that best practices, lessons learned and other product-related knowledge are properly and efficiently collected, transferred and applied into production of existing products as well as for new customer developments,” says Mikael Bratt.

With 1P1P, we drive standardization and cost reduction in our core products and customer features, without sacrificing the need for customer variations in product designs.

Mikael Bratt President Passive Safety, Autoliv

One Product One Process

Improving cost effectiveness and robustness

Cost efficiency targets

The 1P1P strategy supports Autoliv’s annual cost efficiency targets:

| • | Consolidate the supply base to 1,000 supplier groups by 2016 through global sourcing to optimize cost without compromising service and knowledge. |

| • | Reduce direct material costs by at least 3%. |

| • | Complexity reduction by 6% less part numbers purchased in 2016 despite increased sales. |

| • | Improve labor productivity by at least 5%. |

Consolidate the supply base

Through 1P1P we can more efficiently focus on global sourcing to gain leverage and optimize our supplier footprint in order to improve quality, and reduce risk and cost. The ambition set in 2011 was to reduce the supply base to less than 1,000 direct material supplier groups by the end of 2016. This has basically been achieved (1,010), and the strategic work to optimize the supply base now continues by our global commodity purchasing teams.

Reduce direct material costs

Approximately half of our revenues are spent on direct materials from external suppliers. Autoliv mainly purchases manufactured components, and approximately 50% of the component costs are comprised of raw materials. We take several actions to mitigate higher commodity prices, such as re-design of products to reduce material content and weight, components standardization to reduce complexity and gain cost advantages.

Reduce labor costs

In 2016, wages, salaries and other labor costs corresponded to 22.4% of sales. Manufacturing in Best Cost Countries (BCC) could offer significant cost savings as average BCC headcount cost for direct personnel is only 20% of High Cost Country (HCC) headcount costs. Autoliv has more than 80% of its direct workers in BCC, and headcount in BCC is expected to increase further. To compensate for increasing labor and component costs, a higher degree of automation in BCC is foreseen. In HCC, automation and higher value added products (such as active safety) continue to make Autoliv competitive.

Innovate for Real Life Safety

We research, develop and engineer solutions in order to better understand real life accidents as well as new risks associated with higher level automatic driving.

“The way we innovate is a key differentiator that we believe will continue to set us apart from our competitors,” says Steve Fredin, Chief Technology Officer, Group VP, Business Development at Autoliv.

Customer technical centers

Autoliv has customer technical centers in all important markets. With almost 7,900 people in Research, Development and Application Engineering (R,D&E), our global footprint combined with the depth of our technical resources, enable Autoliv to serve all of the major customer development locations in the world. We support our customers by having manufacturing close to their assembly plants in North America, Western Europe and Japan. Our local teams support our corporate research efforts, and are responsible for all of our corporate development projects (both for passive safety and in electronics), as well as the application engineering for our customer projects.

No single customer project accounts for more than 2% of Autoliv’s total R,D&E spending. To fuel Autoliv’s product portfolio, additional expertise is brought in-house via technology partnerships, licensing agreements as well as mergers and acquisitions.

Global research team

Autoliv has one Research Center in Sweden, one in China, and during 2016 our latest research center was opened in India. To identify types of accidents in which Autoliv’s safety expertise might apply, the researchers use databases of real traffic accidents and injuries (such as NASS-CDS in the U.S., GIDAS in Germany, CIDAS in China and RASSI in India). As the number of cars – and traffic accidents – is growing rapidly in Asia, Autoliv is now actively engaged in establishing and populating accident databases for Asia. “We also draw on our numerous crash tests and trials as well as on the vast expertise our specialists have gathered over many years,” says Ola Boström, Vice President Research.

In addition to having our own researchers, Autoliv provides funding for a number of scientists at universities and independent research institutes to work on special projects, such as researchers in the Advanced Vehicle Technologies Consortium led by MIT.

24% projects are for new innovations and improvements of existing products, standardization and cost reduction projects

76% project and programs related to customer orders (development of new vehicle models)

Corporate development projects in passive safety: China, France, Germany, Japan, South Korea, Sweden and the United States.

Electronic development projects: France, Germany, Japan, Romania, Sweden and the United States.

Investments

R,D&E expenditures increased by $127 million net, to be able to capture the future growth opportunities and maintain our focus on “quality first” in everything we do. Gross expenditures for R,D&E amounted to $817 million, 8.1% of sales.

Of these amounts, $166 million in 2016 and $153 million in 2015 related to engineering projects and crash tests that were paid by vehicle manufacturers, safety authorities, auto magazines and other external customers.

Net of this income, R,D&E expenditures amounted to $651 million in 2016 and $524 million in 2015, or 6.5% and 5.7% of sales respectively.

Of the gross R,D&E expense in 2016, 76% was for projects and programs for which we have customer orders, typically related to vehicle models in development. The remaining 24% was not only for completely new innovations but also for improvements of existing products, standardization and cost reduction projects. Our commitment to technological leadership is evidenced by our strong patent position.

Joint venture for autonomous driving

Autoliv Inc. and Volvo Cars signed a final agreement to form a new jointly-owned company to develop the next generation of autonomous driving software.

Jan Carlson, Chairman, President & Chief Executive Officer of Autoliv, says: “There are no two companies that can claim to have done more for automotive safety worldwide than Autoliv and Volvo. This new company, Zenuity, is a recognition of the fact that autonomous driving is the next step to transforming road safety.” The new company will develop ADAS and AD systems for use in Volvo Cars and for sale exclusively by Autoliv to all car makers globally, with revenues shared by both companies. Operations are expected to start during the first half of 2017.

Autoliv Research to Launch LIV, Learning Intelligent Vehicle

The system has been developed to facilitate collaboration and shared control between driver and vehicle. This is in order to attain trust and facilitate the required safety in autonomous driving.

The first version of LIV, the Learning Intelligent Vehicle, utilizes Artificial Intelligence (AI) technology, and coming versions will incorporate on-line and off-line machine learning, utilizing a wide array of data sources and developing an individual relationship with the driver.

Annika Larsson, Research Specialist Human Factors at Autoliv explains further: “As vehicles provide increasing levels of active as well as passive safeguards, we need to find ways for the drivers to feel this support and utilize the active safety systems available. With increasingly advanced machine learning and AI technology incorporated in LIV, we will not only be able to assist the driver in more situations than today. We will also be able to truly cooperate with the driver, allowing the driver-vehicle system to reach its full safety potential.”

Our Market & Competitors

Autoliv’s newly defined market of $39 billion, including Brake Control Systems is expected to grow with a CAGR of around 6% until 2019, assuming an underlying LVP CAGR of 2%.

Our market is driven by two primary factors: light vehicle production (LVP) and content per vehicle (CPV).

The first growth driver, LVP, has increased at an average annual growth rate of around 3% over the last two decades despite the cyclical nature of the automotive industry. LVP is expected to grow to around 96 million in 2019 from approximately 90 million in 2016, according to IHS. Almost all of this expansion will be in the Growth Markets, predominantly in China, India, Thailand, Indonesia and Eastern Europe.

Unlike LVP, where Autoliv can only aim to be on the best-selling platforms, Autoliv can influence CPV more directly by continuously developing and introducing new technologies with higher value-added features. Over the long term, this increases average safety content per vehicle and has caused the automotive safety market to grow faster than the LVP. A steady flow of new technologies has also enabled Autoliv to outpace the market and increase its market share. Since the start of Autoliv, Inc. in 1997, the Company’s sales CAGR has increased by 7%, excluding the recent ANBS JV, compared to the market of around 5% which includes an LVP of around 3%.

In Western Europe, North America and Japan, CPV growth has historically been driven by passive safety (mainly seatbelt, airbag and steering wheel products). Looking ahead, CPV growth in these regions will primarily be driven by active safety including software. New passive safety systems such as active seatbelts, knee airbags, far-side impact airbags along with improved protection for pedestrians and rear-seat occupants like bag-in-belt are expected to have a more modest effect on CPV.

In our Growth Markets, passive safety systems are still expected to dominate CPV growth. Average CPV in our Growth Markets is slightly more than $200, roughly one half of the average in the Developed Markets, which remains close to $400.

Consumer research clearly shows that people want safe cars, and several significant trends will have a positive influence on overall safety content per vehicle. These include:

1) Society becoming increasingly focused on Vision Zero, which includes reducing traffic fatalities and associated costs,

2) Demographic trends of increased urbanization, aging driver populations and increased safety focus in the Growth Markets,

3) Evolving government regulations and test rating systems to improve safety of vehicles in various markets, such as the new Euro NCAP,

4) Ongoing evolution of collision avoidance technologies and an industry focused on achieving advanced driver assistance (ADAS), highly automated driving (HAD) and, ultimately, some form of autonomous driving (AD).

Brake control systems1)

Autoliv entered the brake control market with a new product offering, the Safety Domain Controller during the first quarter of 2014. Through the JV (ANBS) we formed with Nissin Kogyo in March 2016, we expanded our product offering to brake control and brake apply systems, which we see as key building blocks, in the actuator area, towards highly automated driving. We estimate the total brake control market amounted to around $12 billion in 2016, with a projected CAGR of 3% through to 2019. We estimate that ANBS had a market share of close to 5% in 2016. Key competitors include Continental, Bosch, ZF-TRW and ADVICS.

1) The description and analysis of our addressable market henceforth excludes the brake control systems because it is a large market where our presence still is limited, hence an inclusion would make the description and analysis less meaningful.

Active Safety is one of the fastest growing areas of vehicle equipment and is expected to grow at a rate of 20-30% through 2019.

Market growth by region

Our global addressable automotive safety market of passive safety, including steering wheels and electronics, including active safety and passive safety electronics but excluding brake control systems, grew 8% in 2016, adjusted for currency. This can be compared to close to 5% increase in global LVP which was mainly due to a strong Chinese market driven by government incentives but also supported by an average LVP growth in the Developed Markets with high CPV of close to 2%.

From 2016 to 2019, LVP is expected to increase with an average rate of around 2%, according to IHS. The LVP growth is pre-dominantly expected to come from an annual average growth of around 3.5% in the Growth Markets, where it takes almost two vehicles to equal the same resulting sales as from one vehicle in the Developed Markets.

Despite this negative CPV mix effect, our addressable market is expected to grow at a CAGR of approximately 8% until 2019, to about $34 billion, based on the current macro-economic outlook and our internal market intelligence and estimates, including that the Active Safety market is a dynamic and rapidly changing market.

The growth rate of our addressable market is expected to be relatively similar in Developed Markets as in the Growth Markets in 2016-19, as the Growth markets are supported by a higher LPV growth while the Developed Markets are supported by increasing CPV resulting from higher penetration of active safety products.

Market growth by segment

The passive safety market (seat belts and airbags including steering wheels), is expected to grow at a CAGR of 4% until 2019 with the highest growth rate expected in steering wheels (where Autoliv has more than 30% global market share) as a result of the trend toward higher-value steering wheels with leather and additional features.

In seatbelts, Autoliv has reached a global market share of around 39%, primarily due to being the technology leader with several important innovations such as pretensioners and adaptive seatbelts. Our strong market position is also a reflection of our superior global footprint. Seatbelts are the primary life-saving safety product and are also an important requirement in low-end vehicles for the Growth Markets. This provides us with an excellent opportunity to benefit from the expected growth in this segment of the market.

The market for airbags, where Autoliv has a market share of around 40%, is expected to grow slightly slower than the total passive safety market. This is related to the dilutive effect from new low-end vehicles in the Growth Markets, with relatively low installation rates for airbags.

The market for electronics (active safety and passive safety electronics) is expected to grow by a CAGR of around 15-20% between 2016 and 2019, with the highest growth rate for active safety products. The passive safety electronics market (electronic control units and related satellite sensors) is expected to grow close to 2% annually. We are the market leader with around 25% share.

Active Safety (radar, night vision, front-view mono and stereo vision cameras and ADAS ECU’s) is one of the fastest growing areas of vehicle equipment and is expected to grow at an annual rate of 20-30% between 2016 and 2019. Through acquisitions, technology partnerships with customers, and licensing agreements, Autoliv continuously adds key building blocks and has developed a leading market position with a market share of 15-20%. Our new state-of-the-art ADAS-ECU integrates many active and passive safety features.

During 2016 Autoliv signed a definitive agreement with Volvo Car Corporation to form a software Joint Venture (JV) named “Zenuity”. This JV is an industry first where an OEM and Tier 1 supplier both recognized as pioneers in automotive safety come together to form such a company to develop ADAS software towards HAD and AD.

Our competitors

In passive safety, Autoliv’s major competitors are Takata and ZF-TRW, where we estimate that they account for roughly one fifth and one sixth of the market respectively, while Autoliv leads the market with a share of around 39%.

Takata is a family-controlled Japanese company whose shares are listed on the Tokyo Stock Exchange. Its strongest market position is in Japan and North America. In recent years Takata has experienced severe problems related to malfunctioning airbag inflators, leading to a large number of recalls, significant costs and a weakened market position. The accumulation of recall costs and liabilities led Takata in 2016 to enter a process to find an equity sponsor to support the company through their crisis.

ZF-TRW is a global leader in driveline and chassis technology, as well as in passive safety technologies and is the second largest global automotive supplier as a result of their merger.

In Japan, South Korea and China there are a number of local suppliers that have close ties with the domestic vehicle manufacturers. For example, Toyota uses “keiretsu” (in-house) suppliers Tokai Rika for seatbelts, Denso for electronics and Toyoda Gosei for airbags and steering wheels. These suppliers generally receive the majority of the Toyota business in Japan for these products, in the same way as Mobis, a major supplier to Hyundai-Kia, in South Korea.

Other passive safety system competitors include KSS who during 2016 was acquired by Chinese based Ningbo Joyson Electric Corporation, Nihon Plast and Ashimori of Japan, Jinheng of China, Samsung in South Korea and Chris in South America. Collectively, these competitors account for the majority of the remaining 10% global market share in passive safety.

In the electronics market, (active safety and passive safety electronics), our market share is around 20-25%. It remains relatively fragmented with more and larger competitors than in the passive safety market. In active safety, key competitors includes Continental, Bosch, Denso, ZF-TRW, and Delphi, of which we believe Continental and Bosch have strong positions. Continental and Bosch are the largest competitors in passive safety electronics.

Mobileye currently has a leading market position in camera based mono vision algorithms. Mobileye is both a supplier to and competitor of Autoliv. In addition, new potential industry entrants like Nvidia, Qualcom, Intel, Apple, Uber and Google are testing solutions to enter the field of autonomous driving.

Our Customers

Due to our technological leadership and superior global footprint, our diversified customer base includes virtually every vehicle manufacturer in the world. This has also allowed Autoliv to gain market share with growing customers.

In 2016 our top five customers represented 48% of sales and the ten largest represented 79%. This reflects the concentration in the automotive industry. The five largest vehicle manufacturers (OEMs) in 2016 accounted for 52% of global light vehicle production (LVP) and the ten largest for 76%. A delivery contract is typically for the lifetime of a vehicle model, which is normally between 4 and 6 years depending on customer platform sourcing preferences and strategies.

RENAULT/NISSAN, FORD, HONDA

Renault/Nissan is our largest customer, accounting for 11% of our sales in 2016, followed by Ford with 11%. Honda accounts for 10%. We have cooperated with these OEMs for many years and even acquired assets of the Visteon Restraint Electronics, a Ford spin-off and recently formed the ANBS JV where our partner Nissin Kogyo (NK) is a keiretsu of Honda who has a 35% ownership stake in NK.

Autoliv’s strong global presence and our broad product offering also fits these global OEMs very well where we have historically benefited from global sourcing initiatives with these customers.

HYUNDAI/KIA, GM

Hyundai/Kia (HKMC) is one of our fastest-growing customers. HKMC now represents 11% of our sales versus 4% ten years ago. Our business with GM has declined since 2015 to 10% of our sales due the lingering effects of new business hold back in 2011 and 2012. Our sales with GM had increased substantially since 2010 in-part due to Delphi asset acquisition during the financial crisis.

The reason for this strong growth with HKMC is a combination of their success in the global LVP market along with our long-term investments in their home markets South Korea again related to the Delphi acquisition where HKMC was their 2nd largest customer.

BMW, MERCEDES, VOLVO

BMW, Mercedes and Volvo accounted for 14% of our sales in 2016, despite the fact that they only accounted for 6% of global LVP. Our high dependence on premium brand OEMs reflects the higher safety content in their vehicles along with our well-established position as technology leader in the automotive safety industry.

VOLKSWAGEN, TOYOTA

In 2016 Volkswagen and Toyota accounted for 12% and 11% of the global LVP, while they accounted for roughly 7% and 6% of our sales. Historically, TRW has had close relationships with Volkswagen, and Toyota uses in-house (“keiretsu”) suppliers such as Toyoda Gosei, Tokai Rika and Denso for at least 50% of Toyota’s safety business.

FCA, PSA

Fiat Chrysler are important for both our active and passive safety systems. At Fiat we have historically been under-represented; however the situation has improved in recent years. We have a strong position with PSA, especially with passive safety systems.

CHINESE DOMESTIC OEMS

Domestic Chinese OEMs account for 44% of the Chinese LVP. Their share of Autoliv’s sales has grown rapidly from close to 2%, five years ago, to 3% globally, and to 18% of our sales in China. They continued to improve in 2016, due to our strong position with large Chinese OEMs in combination with a large number of customer launches.

Great Wall Motors is our largest Chinese domestic customer. The locally manufactured cars have a lower than average CPV, explaining the high share of LVP compared to the lower share of our sales. With our strong position with local OEM’s and an increasing awareness of automotive safety in China, we remain optimistic about our long-term growth in the largest vehicle producing country.

CUSTOMER SALES TRENDS

Asian vehicle producers have steadily become increasingly important to Autoliv, and now represent 44% of global sales compared to 28% ten years ago. Of the Asian OEMs, the Japanese today represent 28% of our sales compared to 22% in 2006. This reflects both their increasing share of the global LVP and our increasing share with them.

The D3 (General Motors, Ford and Chrysler) now account for 24% of our global sales after a temporary decline to 19% in 2009. All D3 customers managed to recover after the financial crisis, also supported by our acquisition of the Delphi global occupant safety business in 2009-2010.

Our high dependence on European & Other customers has decreased significantly from around 44% of sales in 2006 to 31% in 2016.

Significant Launches during 2016

MERCEDES E-Class

Driver airbag with steering wheel, passenger airbag, knee airbag, seatbelt with pretensioner and bag-in belt, ADAS control unit, radar system and camera system.

Volvo S90/V90

Driver airbag with steering wheel, inflatable curtain, active seatbelt with pretensioner, safety electronics and cable cutter.

Honda Freed

Driver airbag with steering wheel, seatbelt with pretensioner and brake control system.

Mazda 3 /Axela

Driver airbag with steering wheel, passenger airbag, side airbag, inflatable curtain and safety electronics.

Honda CR-V

Radar system, brake control system and seatbelt with pretensioner.

Ford F-Series Super Duty

Side airbag, inflatable curtain, positioning system and safety electronics.

Toyota CH-R

Driver airbag with steering wheel, side airbag, inflatable curtain and seatbelt with pretensioner.

BMW 5 Series

Driver airbag with steering wheel, passenger airbag, seatbelt with pretensioner, night vision system and cable cutter.

Chrysler Pacifica

Driver airbag, inflatable curtain, knee airbag, seatbelt with pretensioner and radar system.

The success of Autoliv depends on the success of our people

“The development of future leaders, experts, and specialists is a top priority at Autoliv.”

In a highly competitive and rapidly changing environment we rely on the skills of our people to be able to adapt quickly and find ways to meet our customers’ needs and create shareholder value.

With 70,300 associates in 27 countries, Autoliv provides an international work environment with varied work assignments and career paths. “To support the growth and development of our employees we have a multitude of development channels including technical and specialist career paths, international assignments, and a number of Autoliv Group common development programs,” says Per Tillman, VP Talent Management.

Development is key

“The development efforts at Autoliv focus on supporting our employees in building the skills and competencies needed,” Per says. During 2016, Autoliv has aligned our development programs with the business strategy and increased focus on our core competencies.

Several additional programs are planned for 2017. In addition to the Group common programs, numerous technical and functional training programs are available locally.

An important cornerstone of the development of each employee is the on-going development dialog between team member and manager, which is summarized in the annual Performance & Development Dialog (PDD). In the PDD, the employee and manager identify and agree on individual targets, development plans and activities. During 2016, 97% of targeted employees conducted a PDD with their managers.

Strong corporate culture

Working at Autoliv means doing work that makes a difference: Saving More Lives. Our strong corporate culture – guided by our values of Innovative, Transparent, Agile and supporting One Autoliv – is a cornerstone for Autoliv to extend its position as the leading supplier of automotive safety systems. Our people are entrusted with ensuring that their actions reflect responsible business practices and support the ethical standards while seeking the highest quality, safety and performance at all times. Autoliv has a long tradition of providing opportunities for employees to work in other countries. Job rotation and mobility across functions, facilities and regions are encouraged, not only to increase the employees’ understanding but also to strengthen leadership skills, global networks, knowledge sharing and the corporate culture. During 2016, 145 employees worked on international assignments in 16 countries.

Our workforce

During 2016, 68% of the 70,300 associates were direct workers in manufacturing, of whom 75% in Best Cost Countries, and 12.5% were temporary personnel. “Getting the right people in the right position is one of our highest priorities, and during the past year Autoliv has focused on making the talent acquisition process robust and efficient,” says Per Tillman. During the year, Autoliv continued to hire engineers in our Passive Safety and Electronics segments, giving Autoliv close to 8,000 engineers working in Research, Development and Engineering.

NO. OF ASSOCIATES PER REGION

Asia 21,265

Americas 19,138

Europe (incl. Africa, Russia & Turkey) 29,890

Total 70,293

Autoliv commits to diversity and we acknowledge, accept and value differences among our people and the contributions they make. At the end of 2016, 56% of the total workforce were men and 44% were women, and 13% of senior management positions were held by women.

Health & Safety management system

In both the marketplace and workplace, the health, safety and well-being of our employees is more than an element of our business – it is our business. During 2016, the Health and Safety Management System (HSMS) was implemented globally and continues to be instrumental in identifying and controlling significant hazards and risks. While we continue to strive for zero injuries and illness, the organization has performed well in reducing injuries and illnesses and has met 2016 objectives for both Incident Rate and Severity Rate. The foundation for our success is the persistence to achieve excellence through leadership and the engagement of our workforce to recognize and report hazards/risks and to implement programs or processes necessary to eliminate occupational injuries and illnesses.

The H&S targets for 2017 will be to continue to improve Autoliv’s Incident Rate and Severity Rate year over year and to strengthen our ergonomics program.

The global Health and Safety Teams continue to successfully communicate and share safety alerts, best practices and lessons learned.

An example of this communication is reflected in the Steering Wheels Chemical Storage & Handling Workshop, held in Turkey in 2016. The Workshop was well attended as more than 20 Autoliv Health & Safety professionals met to review current conditions and identify opportunities for improvement. As a result, more than 55 opportunities for improvement were identified and corrected. More importantly, these items were communicated to all other facilities around the world for review and implementation.

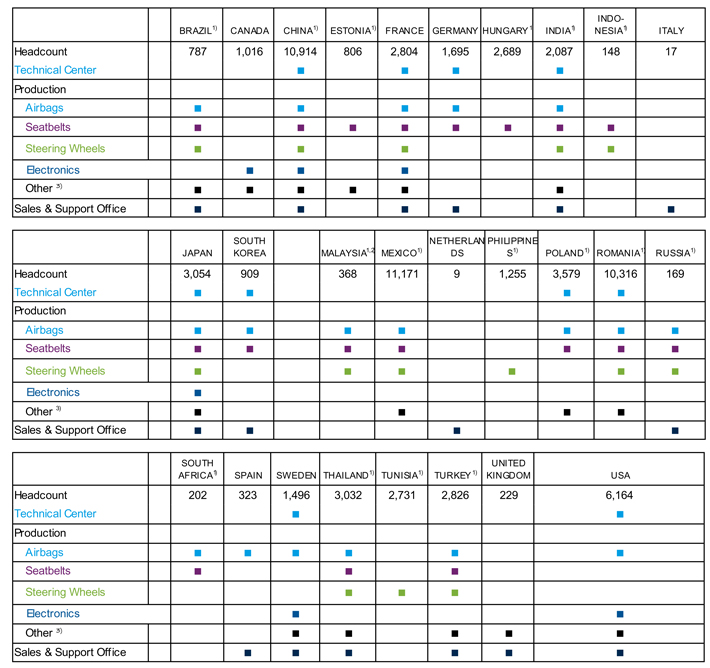

LOCATIONS AND CAPABILITIES

1) Defined as Best Cost Country. 2) Includes headcount in non-consolidated joint ventures. 3) Includes weaving and sewing of textile cushions, seatbelt webbing, inflators, components for airbag and seatbelt products.

Creating Sustainable Value

The foundation for our Sustainability is our Vision of Saving More Lives. This is the most significant impact we can make as a Company on our society. Of equal consequence is how we operate our Company. We understand that how we do business is as important as the business we do. We are passionate about contributing positively to society. As One Autoliv, our Sustainability strategy is to reduce our impact on the environment, develop sustainable products, operate ethically, and be an employer of choice for our employees.

Commit to our Employees

All over the world, we are committed on behalf of our employees to respecting human rights, diversity, health and safety at work.

Act Ethically Towards Society

Our responsibility is based on strict observance of ethical standards, including our suppliers, as well as engaging with the communities where we operate.

Limit our Impact on the Environment

Our commitment is to limit our environmental impact, particularly through reducing waste, energy use and water consumption.

Develop Sustainable Products for Consumers

Every day we innovate so that we can offer sustainable solutions and save more lives with our products.

Our strategy to reduce our impact on the environment, develop sustainable products, operate ethically, and be an employer of choice for our employees is best shown in our achievements and actions.

We are proud of what we have achieved thus far in our journey. We will continue to further develop our targets together with input from our stakeholders and have high expectations for future accomplishments.

International frameworks

Autoliv business practices follow international frameworks, including the UN Global Compact’s ten principles on human rights, labor, environment and anti-corruption.

Autoliv’s business is to save more lives through improving vehicle safety and reducing traffic accidents. This philosophy directly supports the UN Sustainable Development Goal #3, Good Health and Well-being. In 2013, 1.25 million people died as a result of traffic accidents. The UN has set an ambitious goal of halving vehicle deaths and injuries by 2020. Autoliv supports this goal. Our road to saving more lives starts with our relentless innovation in vehicle safety technologies in combination with deep insight of traffic situations, human behavior and human-to-machine interaction. The company’s own goal is to increase the number of lives saved, from more than 30,000 to 150,000 a year.

In our opinion it is not enough to help people survive a collision – we want to help them avoid accidents altogether. This means taking action before accidents occur. Autoliv is currently developing products such as the vehicle-to-vehicle communication safety technology that recognizes potentially dangerous situations before they happen and engages preventive measures, like our autonomous braking, to react quickly and intelligently to avoid an accident. Current active safety technologies make it possible to avoid an estimated 80% of all traffic accidents. Integrating these technologies in all newly produced vehicles supports achieving the UN global goal of reducing traffic fatalities.

Materiality and stakeholder expectations

Understanding stakeholder expectations is critical to developing a resilient, long-term business. In 2016, we conducted a materiality analysis, aligned with the GRI Principles for Defining Report Content, of the Autoliv sustainability pillars accounting for the importance to Autoliv and the importance to our stakeholders, including the known perspectives of our shareholders, customers, employees and communities. The objective of this analysis was to identify and prioritize relevant sustainability topics, to gain an enterprise-level perspective of the current Autoliv sustainability initiatives and on our current maturity level, determine our future ambition levels, identify potential sustainability gaps, and develop a future state sustainability strategy around key focus areas. The performance measurement and management criteria were developed to align with GRI reporting practices for disclosing management approaches to sustainability, and for measuring and reporting sustainability progress.

Autoliv combined the most material aspects of the analysis into the four sustainability pillars:

| • | Commit to our Employees, |

| • | Limit our Impact on the Environment, |

| • | Develop Sustainable Products for Consumers, and |

| • | Act Ethically toward Society. |

The most important conclusion of the analysis was that Autoliv is succeeding or in the leading stages in the majority of the key focus areas from a maturity perspective, however we can improve through setting progressive goals in the future.

Based on the results of the materiality assessment and the analysis, the Autoliv Executive Management Team has decided that Autoliv will establish key focus areas supporting each of our four sustainability pillars. In 2017, we will develop progressive goals supporting these focus areas that will reduce our global carbon footprint and increase our standing as an engaged and dynamic corporate citizen.

Sustainability Objectives and Key Achievements 2016

Commit to our Employees

We commit to creating a respectful and diverse working environment. To attract, develop, and retain highly skilled employees is a top priority, and we commit to the development of our employees. We support creativity, entrepreneurial behavior, and result-oriented actions to encourage our people to live our values: One Autoliv, Agile, Transparent, and Innovative. By respecting each other and working together, we achieve better results.

Human Rights

We commit to fair treatment of our employees including fair and equitable employment conditions in accordance with applicable laws. We recognize and respect employees’ right to freedom of association and collective bargaining, we provide humane and safe working conditions, prohibit forced or child labor, and promote a workplace free of discrimination and harassment.

Health & Safety

We commit to securing the well-being of our employees. Health and safety is more than an element of our business – it is our business – and we work diligently to reduce and eliminate occupational hazards. We also commit to adhering to required standards for the safe operation of facilities and the protection of our employees. We seek continuous improvement on health and safety performance, maintaining a culture that encourages the reporting, analysis and effective management of health and safety issues.

Diversity

We commit to diversity and acknowledge, accept and value differences among our people and the contributions they make. Our workforce reflects the diversity of the countries and cultures in which we operate. We work hard to create an inclusive environment where all people can contribute regardless of differentiating factors by encouraging individuals’ unique viewpoints and contributions. We believe each person should be able to work in a professional atmosphere which promotes equal employment opportunity and prohibits illegal, discriminatory practices.

KEY ACHIEVEMENTS

Autoliv commits to improve diversity on all levels. At the end of 2016, 44% of our workforce and 13% of our senior management positions were filled by women and we are striving to improve this even more in the future.

Health and Safety protocols continue to be vigorous at Autoliv as we continuously strive for excellence. We regularly educate, monitor, evaluate and refresh our Health and Safety policies and procedures to ensure that we are delivering on our commitment to our employees: to protect human health, the safe operation of our facilities and adhere to applicable regulations. We continue to strive for zero injuries in every facility. For 2016, we were better than our goals; injury incident rate of 2.25% and injury severity rate of 25%.

Supporting human rights in Turkey

Women at our Autoliv Turkey facility are taking a stand against violence towards women by participating in a community awareness campaign. For more than 5 years, the facility has participated in an all-female soccer tournament. The event attracts employees from our facility and the local community in growing numbers each year and has been a successful platform.

Limit our Impact on the Environment

We believe our operations have a modest environmental impact. Savings from more efficient energy and water usage and waste reduction can have a positive benefit for the environment and decrease our impact on climate change.

Energy reduction

Our facilities are improving energy efficiency and reducing water usage through continuous process improvement. Autoliv is making strides in energy reduction using various methods, including upgrading lighting to LED, automatic light power controls, and air conditioning temperature and time controls. These energy reductions will continue to reduce Autoliv’s impact on climate change for years to come.

Waste and scrap reduction

Our facilities reduce waste and scrap through annual policy deployment targets. Our employees look for ways to reduce waste and scrap, primarily through recycling scrap materials. Other methods include donating scrap tools, finding new uses for waste products and introducing reusable packaging where possible.

Water usage reduction

Taking steps to reduce and improve water usage, particularly in countries already experiencing water stress, is of key concern to Autoliv. We look not only to reduce the amount of water that we use in our production processes, but for innovative ways to capture wastewater and invest it productively back into each facility.

KEY ACHIEVEMENTS

Our facilities are certified in accordance with ISO 14001 (83%) or in compliance with the principles of ISO 14001 through our internal standard (15%), ANBS excluded. Our total energy consumption corresponds to 391,533 metric tons CO2e (using the Greenhouse Gas Protocol), an increase of 16% from 2015 due to new facilities, primarily the ANBS joint venture, and increased production overall.

Energy saving locally

In the U.S., Korea, India, Thailand, Brazil, China, France and Mexico, our facilities reduced their energy use by more than 17% on average through the installation of LED lighting, air compressor usage improvements and automatic power controls.

In 2016, Autoliv’s UK textile facility installed a natural gas-fired Combined Heat and Power (CHP) plant on site that will provide 70% of the electricity needs of the plant.

Reducing landfill locally

In Michigan, the United States, a team found a recycler that accepted Lexan plastics, keeping 6,000 pounds (2,720 kg) of plastics from becoming landfill every year.

By selling damaged wood pallets to a local furniture manufacturer, our team in Brazil saved 19,000 wood pallets from becoming landfill. These wood pallets became sofas, tables and chairs instead. Our Brazil team also eliminated one-time use cardboard packaging and replaced it with reusable bins, avoiding more than 10 tons of cardboard from going to a landfill annually.

Water saving initiatives

Two of our facilities in India designed and implemented several processes to reduce and reuse water. Through rainwater harvesting, the facilities collected 660,000 gallons (2.5 million liters) of rainwater. In addition, by treating wastewater, over 3.5 million gallons (13.3 million liters) of water were recaptured, treated and used for landscaping. Finally, over 4.7 million gallons (17.8 million liters) of effluent water is treated and reused in our seatbelt webbing production.

Our project team in China reduced wastewater by 64% through the implementation of proactive measures and employee education.

Develop Sustainable Products for Consumers

Our goal is to develop products that protect people in accidents without having a negative impact on our environment. Our products work at the heart of the vehicle, constantly looking ahead and around, assisting drivers to reach their destinations safely and sustainably.

Design for sustainability

From innovation to disposal, we consider the potential environmental impact when we design our products and processes. Raw materials, components, manufacturing, use and end-of-life considerations impact our thinking and final product specifications in various ways. These include our advancements in autonomous driving, low-weight safety systems, use of alternative energy in our products, and improved fuel efficiency.

Autoliv standard AS005 defines the requirements for reporting the material composition of our supplied parts and the restrictions that certain substances are subject to. This standard includes mandatory corporate protocols for the safe and appropriate use of chemicals in our products, lists declarable, restricted and forbidden substances, and sets specific procedures for following customer requirements and regulations, including REACH and Conflict Minerals.

KEY ACHIEVEMENTS