Attached files

Exhibit 13

2016 Annual Report

SEABOARD CORPORATION

Description of Business

Seaboard Corporation and its subsidiaries (“Seaboard”) are a diverse global agribusiness and transportation company. In the United States (“U.S.”), Seaboard is primarily engaged in pork production and processing and ocean transportation. Overseas, Seaboard is primarily engaged in commodity merchandising, grain processing, sugar production and electric power generation. Seaboard also has an interest in a turkey operation in the U.S.

This report, including information included or incorporated by reference in this report, contains certain forward-looking statements with respect to the financial condition, results of operations, plans, objectives, future performance and business of Seaboard. Forward-looking statements generally may be identified as statements that are not historical in nature and statements preceded by, followed by or that include the words: “believes,” “expects,” “may,” “will,” “should,” “could,” “anticipates,” “estimates,” “intends,” or similar expressions. In more specific terms, forward-looking statements, include, without limitation: statements concerning the projection of revenues, income or loss, capital expenditures, capital structure or other financial items, including the impact of mark-to-market accounting on operating income; statements regarding the plans and objectives of management for future operations; statements of future economic performance; statements regarding the intent, belief or current expectations of Seaboard and its management with respect to: (i) Seaboard’s ability to obtain adequate financing and liquidity; (ii) the price of feed stocks and other materials used by Seaboard; (iii) the sales price or market conditions for pork, grains, sugar, turkey and other products and services; (iv) the recorded tax effects under certain circumstances and changes in tax laws; (v) the volume of business and working capital requirements associated with the competitive trading environment for the Commodity Trading and Milling (“CT&M”) segment; (vi) the charter hire rates and fuel prices for vessels; (vii) the fuel costs and spot market prices for electricity in the Dominican Republic; (viii) the effect of the fluctuation in foreign currency exchange rates; (ix) the profitability or sales volume of any of Seaboard’s segments; (x) the anticipated costs and completion timetables for Seaboard’s scheduled capital improvements, acquisitions and dispositions; (xi) the productive capacity of facilities that are planned or under construction, and the timing of the commencement of operations at such facilities; (xii) the increase in Seaboard's hog and other production capacity attributable to acquisitions; or (xiii) other trends affecting Seaboard’s financial condition or results of operations, and statements of the assumptions underlying or relating to any of the foregoing statements.

This list of forward-looking statements is not exclusive. Seaboard undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events, changes in assumptions or otherwise. Forward-looking statements are not guarantees of future performance or results. They involve risks, uncertainties and assumptions. Actual results may differ materially from those contemplated by the forward-looking statements due to a variety of factors. The information contained in this report, including, without limitation, the information under the captions “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Letter to Stockholders” identifies important factors which could cause such differences.

2016 Annual Report 1

Letter to Stockholders is intentionally omitted from Exhibit 13 and will be included in the printed Annual Report.

2 2016 Annual Report

SEABOARD CORPORATION

Letter to Stockholders

Letter to Stockholders is intentionally omitted from Exhibit 13 and will be included in the printed Annual Report.

2016 Annual Report 3

SEABOARD CORPORATION

|

|

|

|

|

|

|

Corporate Office Seaboard Corporation Merriam, Kansas Pork Seaboard Foods LLC Pork Division Office Merriam, Kansas Processing Plant Guymon, Oklahoma High Plains Bioenergy, LLC Guymon, Oklahoma HPB – St. Joe Biodiesel LLC St. Joseph, Missouri Seaboard de Mexico USA LLC Mexico Daily’s Premium Meats, LLC* Missoula, Montana Salt Lake City, Utah St. Joseph, Missouri Commodity Trading and Milling Commodity Trading Operations Atlanta, Georgia* Australia* Canada Chapel Hill, North Carolina Colombia Ecuador Greece Isle of Man Kenya Peru* Singapore South Africa Uruguay* Africa Poultry Development Limited* Kenya and Zambia Bag Yaglari Sanayi ve Ticaret T.A.S.* Turkey Beira Grain Terminal, S.A. Mozambique Belarina Alimentos S.A. Brazil Bolux Group Proprietary Limited* Botswana Compania Industrial de Productos Agropecuarios S.A.* Colombia Congo Poultry Limited* Democratic Republic of Congo Flour Mills of Ghana Limited Ghana Gambia Milling Corporation* Gambia |

National Milling Company of Guyana, Inc. Guyana Les Moulins d’Haiti S.E.M.* Haiti Lesotho Flour Mills Limited* Lesotho Life Flour Mill Ltd.* Nigeria LMM Farine, S.A. Madagascar Minoterie de Matadi, S.A.* Democratic Republic of Congo Minoterie du Congo, S.A. Republic of Congo Moderna Alimentos, S.A.* Molinos Champion, S.A.* Ecuador National Milling Corporation Limited Zambia Paramount Mills (Pty) Ltd.* South Africa Rafael del Castillo & Cia. S.A.* Colombia Societe Africaine de Developpement Industriel Alimentaire, S.P.R.L.* Democratic Republic of Congo Unga Holdings Limited* Kenya and Uganda Marine Seaboard Marine Ltd. Marine Division Office Miami, Florida Port Operations Brooklyn, New York Houston, Texas Miami, Florida New Orleans, Louisiana Philadelphia, Pennsylvania Agencia Maritima del Istmo, S.A. Costa Rica Cayman Freight Shipping Services, Ltd. Cayman Islands JacintoPort International LLC Houston, Texas Kingston Wharves Limited* Jamaica Lafito Logistics Holdings, Ltd.* Bahamas Representaciones Maritimas y Aereas, S.A. Guatemala Sea Cargo, S.A. Panama Seaboard de Colombia, S.A. Colombia |

Seaboard de Nicaragua, S.A. Nicaragua Seaboard del Peru, S.A. Peru Seaboard Freight & Shipping Jamaica Limited Jamaica Seaboard Honduras, S. de R.L. de C.V. Honduras Seaboard Marine (Trinidad) Ltd. Trinidad Seaboard Marine of Haiti, S.A. Haiti SEADOM, S.A. Dominican Republic SeaMaritima S.A. de C.V. Mexico Sugar Alconoa S.R.L. Ingenio y Refineria San Martin del Tabacal S.R.L. Argentina Power Transcontinental Capital Corp. (Bermuda) Ltd. La Compania de Electricidad de San Pedro de Macoris* Dominican Republic Turkey Butterball, LLC* Division Office Garner, North Carolina Processing Plants Carthage, Missouri Huntsville, Arkansas Mt. Olive, North Carolina Ozark, Arkansas Further Processing Plants Jonesboro, Arkansas Montgomery, Illinois Raeford, North Carolina Other Mount Dora Farms de Honduras, S.R.L. Honduras Mount Dora Farms Inc. Houston, Texas |

*Represents a non-controlled, non-consolidated affiliate

4 2016 Annual Report

SEABOARD CORPORATION

Division Summaries

Seaboard’s Pork Division is a vertically integrated pork producer and one of the largest producers and processors in the U.S. Seaboard is able to efficiently control pork production across the entire life cycle of a hog, beginning with research and development in nutrition and genetics and extending to the production of high quality meat products at our processing and further processing facilities.

Seaboard’s hog processing facility is located in Guymon, Oklahoma. The facility is a double shift operation that processes approximately 20,500 hogs per day and generally operates at capacity. Weekend shifts are added as market conditions dictate. Hogs processed at the plant are primarily Seaboard-raised hogs. The remaining hogs processed are raised by third parties and purchased under contract or occasionally in the open market. Seaboard produces and sells fresh and frozen pork products to further processors, food service operators, grocery stores, distributors and retail outlets throughout the U.S. Seaboard also sells to distributors, trading companies and further processors in Japan, Mexico, China and numerous other foreign markets.

Seaboard’s hog production facilities consist of genetic and commercial breeding, farrowing, nursery and finishing buildings located in the Central U.S. These facilities have a capacity to produce over five million hogs annually. Seaboard owns and operates seven centrally located feed mills to provide formulated feed to these hogs.

Seaboard produces biodiesel at facilities in Guymon, Oklahoma, and St. Joseph, Missouri. The biodiesel is produced from pork fat supplied by Seaboard’s Guymon pork processing plant and from other animal fat or vegetable oil supplied by non-Seaboard facilities. The biodiesel is sold to fuel blenders for distribution and in the retail markets.

Seaboard’s Pork Division has an agreement with a similarly-sized pork processor, Triumph Foods, LLC (“Triumph”), to market substantially all of the pork products produced at Triumph’s plant in St. Joseph, Missouri. The agreement enhances the efficiency of Seaboard’s sales and marketing efforts and expands Seaboard’s geographic footprint. Seaboard receives a fee on a per head basis on all Triumph products. According to the trade publications Successful Farming and Informa Economics Seaboard was ranked number three in pork production (based on sows in production) and number four (based on daily processing capacity, including Triumph’s capacity) in processing in the U.S. in 2016.

Seaboard’s Pork Division has a 50% noncontrolling interest in Daily’s Premium Meats, LLC (“Daily’s”). Daily’s produces and markets raw and pre-cooked bacon, ham and sausage primarily for the food service industry and, to a lesser extent, retail markets. Daily’s has three further processing plants located in Salt Lake City, Utah, Missoula, Montana, and St. Joseph, Missouri. Seaboard and Triumph each supply raw product to Daily’s.

In May 2015, Seaboard’s Pork Division and Triumph entered into a new joint venture, Seaboard Triumph Foods, LLC, which is constructing a new pork processing facility in Sioux City, Iowa. Construction is expected to be completed in mid-2017. The plant is designed to process about three million market hogs annually operating a single shift. As part of the operations, Seaboard’s Pork Division agreed to provide a portion of the hogs to be processed at the facility. During 2016, the Pork Division acquired hog inventory and related assets that increased Seaboard’s hog production capacity to meet the majority of such hog supply commitment for single shift processing at the new plant.

Commodity Trading and Milling Division

Seaboard’s Commodity Trading and Milling (“CT&M”) Division is an integrated agricultural commodity trading, processing and logistics operation. This Division sources, transports and markets approximately ten million metric tons per year of wheat, corn, soybeans, soybean meal and other commodities primarily to third-party customers and affiliated companies. These commodities are purchased worldwide, with primary destinations in Africa, South America, the Caribbean and Asia. Seaboard integrates the delivery of commodities to its customers through the use of owned or chartered bulk vessels.

2016 Annual Report 5

SEABOARD CORPORATION

Division Summaries

Seaboard’s CT&M Division operates facilities in 29 countries. The commodity trading business has 11 offices in 10 countries, in addition to four non-consolidated affiliates in three other countries. The grain processing businesses operate facilities at 41 locations in 22 countries, and include 7 consolidated and 18 non-consolidated affiliates primarily in Africa, South America, the Caribbean and Asia. Seaboard and its affiliates produce approximately five million metric tons of wheat flour, maize meal, manufactured feed and oilseed crush commodities per year in addition to other related grain-based products.

Marine Division

Seaboard’s Marine Division provides cargo shipping services between the U.S., the Caribbean and Central and South America. Seaboard’s primary operations, located in Miami, include an off-port warehouse for cargo consolidation and temporary storage and a terminal at PortMiami. At the Port of Houston, Seaboard operates a cargo terminal facility that includes on-dock warehouse space for temporary storage of bagged grains, resins and other cargoes. Seaboard also makes scheduled vessel calls to Brooklyn, New York, New Orleans, Louisiana, Philadelphia, Pennsylvania, and various foreign ports in the Caribbean and Central and South America.

This Division’s fleet consists of chartered and, to a lesser extent, owned vessels, and includes dry, refrigerated and specialized containers and other cargo related equipment. Seaboard is the largest shipper in terms of cargo volume in PortMiami. Seaboard provides extensive service between our domestic ports of call and multiple foreign destinations.

To maximize fleet utilization, Seaboard uses a network of offices and agents throughout the U.S., Canada, Latin America and the Caribbean to sell freight at multiple points. Seaboard’s full service capabilities allow transport by truck or rail of import and export cargo to and from various U.S. ports. Seaboard’s frequent sailings and fixed-day schedules allow customers to coordinate manufacturing schedules and maintain inventories at cost-efficient levels.

Sugar Division

In Argentina, Seaboard grows sugarcane, which it uses to produce refined sugar and alcohol. The sugar is primarily marketed locally, with some exports to the U.S. and other South American countries. Seaboard’s sugar processing plant, one of the largest in Argentina, has an annual capacity to produce approximately 250,000 metric tons of sugar and approximately 20 million gallons of alcohol per year. The mill is located in the Salta Province of Argentina, with administrative offices in Buenos Aires. Land owned by Seaboard in Argentina is planted primarily with sugarcane, which supplies the majority of the raw material processed. Depending on local market conditions, sugar may also be purchased from third parties for resale. In addition, this Division sells dehydrated alcohol to certain oil companies under the Argentine governmental bio-ethanol program, which requires alcohol to be blended with gasoline. This Division also owns a 51 megawatt cogeneration power plant, which is fueled by the burning of sugarcane by-products, natural gas and other biomass when available.

Power Division

In the Dominican Republic, Seaboard is an unregulated independent power producer generating electricity for the local power grid from an owned floating power generating facility with a capacity to generate 108 megawatts. Seaboard primarily sells power on the spot market and is not directly involved in the transmission or distribution of electricity. Principal buyers are government-owned distribution companies and partially government-owned generation companies.

Other Divisions

Seaboard has a 50% noncontrolling voting interest in Butterball, LLC (“Butterball”). Butterball is the largest vertically integrated producer, processor and marketer of branded and non-branded turkey and other products in the U.S. Butterball has four processing plants, three further processing plants and numerous live production and feed milling operations located in North Carolina, Arkansas, Missouri, Illinois and Kansas. Butterball produces over one billion pounds of turkey each year. Butterball is a national supplier to retail stores, foodservice outlets, and industrial entities but also exports products to Mexico and numerous other foreign markets.

Seaboard processes jalapeño peppers at its plant in Honduras, which are primarily shipped to and sold in the U.S.

6 2016 Annual Report

SEABOARD CORPORATION

Summary of Selected Financial Data

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Years ended December 31, |

|

|||||||||||||

|

(Millions of dollars except per share amounts) |

|

2016 |

|

2015 |

|

2014 |

|

2013 |

|

2012 |

|

|||||

|

Net sales |

|

$ |

5,379 |

|

$ |

5,594 |

|

$ |

6,473 |

|

$ |

6,670 |

|

$ |

6,189 |

|

|

Operating income |

|

$ |

222 |

|

$ |

126 |

|

$ |

424 |

|

$ |

204 |

|

$ |

310 |

|

|

Net earnings attributable to Seaboard |

|

$ |

312 |

|

$ |

171 |

|

$ |

367 |

|

$ |

212 |

|

$ |

287 |

|

|

Basic earnings per common share |

|

$ |

266.50 |

|

$ |

146.44 |

|

$ |

311.44 |

|

$ |

177.53 |

|

$ |

238.24 |

|

|

Total assets |

|

$ |

4,755 |

|

$ |

4,431 |

|

$ |

3,692 |

|

$ |

3,431 |

|

$ |

3,354 |

|

|

Long-term debt, less current maturities |

|

$ |

499 |

|

$ |

518 |

|

$ |

— |

|

$ |

80 |

|

$ |

121 |

|

|

Stockholders’ equity |

|

$ |

3,175 |

|

$ |

2,882 |

|

$ |

2,735 |

|

$ |

2,493 |

|

$ |

2,314 |

|

|

Dividends per common share |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

12.00 |

|

In the fourth quarter of 2015, Seaboard recorded interest income of $23 million, net of taxes ($31 million before taxes), or $19.49 per common share, for interest recognized on certain outstanding customer receivable balances in its Power segment. This interest income related to amounts determined to be collectible as of December 31, 2015, but previously had been considered uncollectable in prior years. This amount was fully collected by Seaboard in January 2016.

As of September 27, 2014, Seaboard’s Pork segment sold to Triumph Foods, LLC a 50% interest in Daily’s. Included in net earnings attributable to Seaboard for 2014 is a gain on sale of controlling interest in subsidiary of $40 million, net of taxes ($66 million gain before taxes), or $34.14 per common share.

On January 2, 2013, the American Taxpayer Relief Act of 2012 (the “Tax Act”) was signed into law. As the Tax Act was signed into law in 2013, the effects of the retroactive provisions in this law on current and deferred tax assets and liabilities for Seaboard were recorded in the first quarter of 2013. The total impact was a tax benefit of $8 million or $6.66 per common share, recorded in the first quarter of 2013 related to certain 2012 income tax credits. In addition to this amount was a credit of approximately $11 million, or $9.43 per common share, for 2012 Federal blender’s credits that was recognized as revenues in the first quarter of 2013. There was no tax expense on these transactions.

In December 2012, Seaboard declared and paid a dividend of $12.00 per common share. The increased amount of the dividend (which has historically been $0.75 per common share on a quarterly basis or $3.00 per common share on an annual basis) represented a prepayment of the annual 2013, 2014, 2015 and 2016 dividends ($3.00 per common share per year). Seaboard did not declare a dividend in 2016, 2015, 2014 or 2013. In 2010, Seaboard declared and paid dividends of $9.00 per common share, which included a prepayment of the annual 2011 and 2012 dividends ($3.00 per common share per year). See the Liquidity and Capital Resources section of Management’s Discussion and Analysis for 2017 dividend plans. Basic and diluted earnings per common share are the same for all periods presented.

2016 Annual Report 7

SEABOARD CORPORATION

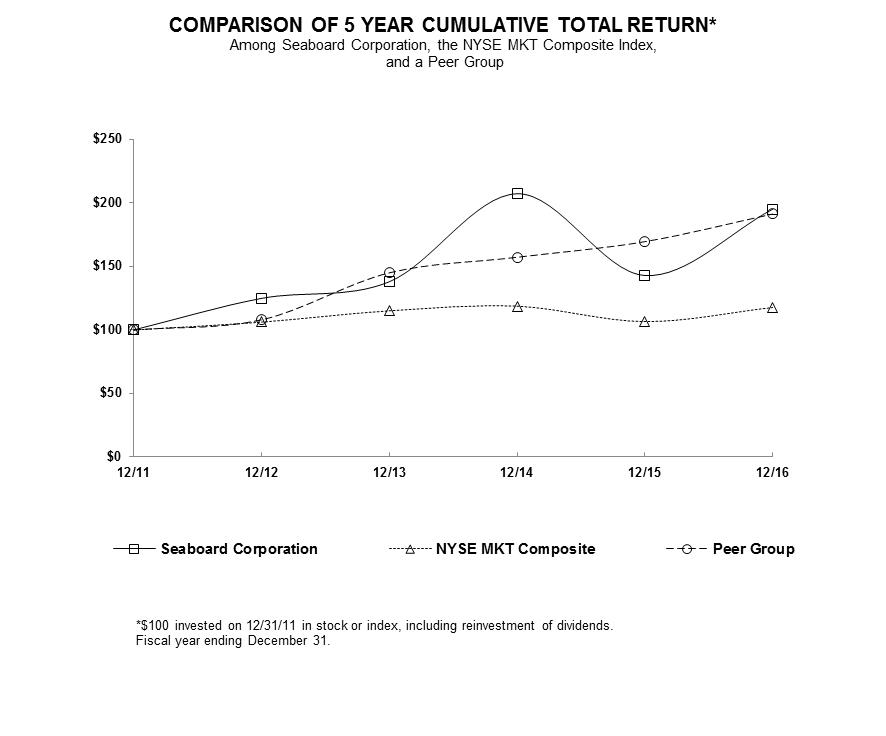

Company Performance Graph

The Securities and Exchange Commission requires a five-year comparison of stock performance for Seaboard with that of an appropriate broad equity market index and similar industry index. Seaboard’s common stock is traded on the NYSE MKT and provides an appropriate comparison for Seaboard’s stock performance. Because there is no single industry index to compare stock performance, the companies comprising the Dow Jones Food and Marine Transportation Industry indices (the “Peer Group”) were chosen as the second comparison.

The following graph shows a five-year comparison of cumulative total return for Seaboard Corporation, the NYSE MKT Index and the companies comprising the Dow Jones U.S. Food Products and the Dow Jones U.S. Marine Transportation indices, weighted by market capitalization for the five fiscal years commencing December 31, 2011 and ending December 31, 2016. The information presented in the performance graph is historical in nature and is not intended to represent or guarantee future returns.

The comparison of cumulative total returns presented in the above graph was plotted using the following index values and common stock price values:

|

|

|

12/31/11 |

|

12/31/12 |

|

12/31/13 |

|

12/31/14 |

|

12/31/15 |

|

12/31/16 |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Seaboard Corporation |

|

$ |

100.00 |

|

$ |

124.88 |

|

$ |

137.96 |

|

$ |

207.21 |

|

$ |

142.89 |

|

$ |

195.07 |

|

|

NYSE MKT Composite |

|

$ |

100.00 |

|

$ |

106.15 |

|

$ |

115.07 |

|

$ |

118.71 |

|

$ |

106.60 |

|

$ |

117.67 |

|

|

Peer Group |

|

$ |

100.00 |

|

$ |

107.99 |

|

$ |

144.96 |

|

$ |

157.25 |

|

$ |

169.52 |

|

$ |

191.29 |

|

8 2016 Annual Report

SEABOARD CORPORATION

Quarterly Financial Data (unaudited)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(UNAUDITED) |

|

1st |

|

2nd |

|

3rd |

|

4th |

|

Total for |

|

|||||

|

(Millions of dollars except per share amounts) |

|

Quarter |

|

Quarter |

|

Quarter |

|

Quarter |

|

the Year |

|

|||||

|

2016 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net sales |

|

$ |

1,319 |

|

$ |

1,357 |

|

$ |

1,330 |

|

$ |

1,373 |

|

$ |

5,379 |

|

|

|

$ |

36 |

|

$ |

76 |

|

$ |

42 |

|

$ |

68 |

|

$ |

222 |

|

|

|

Net earnings attributable to Seaboard |

|

$ |

54 |

|

$ |

80 |

|

$ |

75 |

|

$ |

103 |

|

$ |

312 |

|

|

Earnings per common share |

|

$ |

45.91 |

|

$ |

68.34 |

|

$ |

64.42 |

|

$ |

87.83 |

|

$ |

266.50 |

|

|

Dividends per common share |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

|

Closing market price range per common share: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

High |

|

$ |

3,054.00 |

|

$ |

3,125.00 |

|

$ |

3,440.00 |

|

$ |

4,444.14 |

|

|

|

|

|

Low |

|

$ |

2,483.00 |

|

$ |

2,726.50 |

|

$ |

2,782.92 |

|

$ |

3,201.95 |

|

|

|

|

|

2015 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net sales |

|

$ |

1,452 |

|

$ |

1,428 |

|

$ |

1,411 |

|

$ |

1,303 |

|

$ |

5,594 |

|

|

Operating income |

|

$ |

28 |

|

$ |

32 |

|

$ |

23 |

|

$ |

43 |

|

$ |

126 |

|

|

Net earnings attributable to Seaboard |

|

$ |

33 |

|

$ |

32 |

|

$ |

3 |

|

$ |

103 |

|

$ |

171 |

|

|

Earnings per common share |

|

$ |

28.11 |

|

$ |

27.04 |

|

$ |

2.59 |

|

$ |

88.70 |

|

$ |

146.44 |

|

|

Dividends per common share |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

|

Closing market price range per common share: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

High |

|

$ |

4,640.00 |

|

$ |

4,005.00 |

|

$ |

3,675.00 |

|

$ |

3,441.00 |

|

|

|

|

|

Low |

|

$ |

3,705.00 |

|

$ |

3,253.00 |

|

$ |

2,971.95 |

|

$ |

2,892.00 |

|

|

|

|

On December 18, 2015, the Protecting Americans from Tax Hikes Act of 2015 (the “2015 Tax Act”) was signed into law. The 2015 Tax Act reinstated and made permanent certain expired corporate income tax provisions that impact current and deferred taxes for financial reporting purposes. The annual effects of the provisions in this law on current and deferred tax assets and liabilities for Seaboard were recorded in the fourth quarter of 2015. The impact was a tax benefit of $13 million, or $10.92 per common share, primarily related to certain income tax credits. In addition to this amount was a credit of $17 million, or $14.88 per common share, for the 2015 Federal blender’s credits (extended by the 2015 Tax Act through December 31, 2016) that was recognized as revenues in the fourth quarter of 2015. There was no tax expense on these transactions. Since the 2015 Tax Act extended the provisions through December 31, 2016, revenue was recognized ratably throughout 2016. The Federal blender’s credits have not been renewed for 2017.

In the fourth quarter of 2015, Seaboard recorded interest income of $23 million, net of taxes ($31 million before taxes), or $19.49 per common share, for interest recognized on certain outstanding customer receivable balances in its Power segment. This interest income related to amounts determined to be collectible as of December 31, 2015, but previously had been considered uncollectable in prior years. This amount was fully collected by Seaboard in January 2016.

No dividends were paid during 2016 and 2015 as they were declared and prepaid in December 2012. During 2016 and 2015, Seaboard did not repurchase any common shares. See the Liquidity and Capital Resources section of Management’s Discussion and Analysis for 2017 dividend plans.

2016 Annual Report 9

SEABOARD CORPORATION

Management’s Discussion & Analysis

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

OVERVIEW

Seaboard is a diverse global agribusiness and transportation company, with operations in several industries. Most of the sales and costs of Seaboard’s segments are significantly influenced by worldwide fluctuations in commodity prices and changes in foreign political and economic conditions. Accordingly, sales, operating income and cash flows can fluctuate significantly from year to year. As each segment operates in distinct industries and different geographical locations, management evaluates their operations separately. Seaboard’s reporting segments are based on information used by Seaboard’s Chief Executive Officer in his capacity as chief operating decision maker to determine allocation of resources and assess performance.

Pork Segment

The Pork segment is primarily a U.S. business with some export sales to Japan, Mexico, China and numerous other foreign markets. Revenues from the sale of pork products are primarily generated from a single hog processing plant in Guymon, Oklahoma, which generally operates at daily double shift processing capacity of approximately 20,500 hogs, and a ham boning and processing plant in Mexico. In 2016, Seaboard raised approximately 81% of the hogs processed at the Guymon plant, with the remaining hog requirements purchased primarily under contracts from independent producers. This segment is Seaboard’s most capital intensive segment, representing approximately 57% of Seaboard’s total fixed assets, in addition to 40% of total inventories.

Within the portfolio of Seaboard’s businesses, management believes profitability of the Pork segment is most susceptible to commodity price fluctuations. As a result, this segment’s operating income and cash flows can materially fluctuate from year to year, significantly affecting Seaboard’s consolidated operating income and cash flows. Sales prices are directly affected by both domestic and worldwide supply and demand for pork products and other proteins. Feed accounts for the largest input cost in raising hogs and is materially affected by price changes for corn and soybean meal. Market prices for hogs purchased from third parties for processing at the plant also represent a major cost factor. With the Guymon plant generally operating at capacity, Seaboard is constantly looking for ways to enhance the facility’s operational efficiency, while also looking to increase margins by introducing new, higher value products.

The Pork segment also produces biodiesel, which is sold to third parties. Biodiesel is produced from pork fat from Seaboard’s pork processing plant and from other animal fat or vegetable oil purchased from third parties.

The Pork segment has an agreement with Triumph Foods, LLC (“Triumph”) to market substantially all of the pork products produced at Triumph’s plant in St. Joseph, Missouri. The Pork segment markets the pork products for a fee primarily based on the number of head processed by Triumph. Triumph has processing capacity similar to that of Seaboard’s Guymon plant and operates with an integrated model similar to Seaboard’s model. Seaboard’s sales prices for its pork products are primarily based on a margin sharing arrangement that considers the average sales price and mix of products sold from both Seaboard’s and Triumph’s hog processing plants.

The Pork segment has a 50% noncontrolling interest in Daily’s Premium Meats, LLC (“Daily’s”). Daily’s produces and markets raw and pre-cooked bacon, ham and sausage primarily for the food service industry and, to a lesser extent, retail markets. Daily’s has three further processing plants located in Salt Lake City, Utah, Missoula, Montana, and St. Joseph, Missouri.

In May 2015, Seaboard’s Pork segment and Triumph entered into a new joint venture, Seaboard Triumph Foods, LLC (“STF”), which is constructing a new pork processing facility in Sioux City, Iowa. Construction is expected to be completed in mid-2017. The plant is designed to process about three million market hogs annually operating a single shift. As part of the operations, Seaboard’s Pork segment agreed to provide a portion of the hogs to be processed at the facility. During 2016, the Pork segment acquired hog inventory and related assets in the Central U.S. that increased Seaboard’s hog production capacity to meet the majority of such hog supply commitment for single shift processing at the new plant.

Commodity Trading and Milling Segment

The Commodity Trading and Milling (“CT&M”) segment, which is managed under the name of Seaboard Overseas and Trading Group, primarily operates overseas and is an integrated agricultural commodity trading, processing and logistics operation with locations in Africa, South America, the Caribbean, Europe and Asia. These foreign operations can be significantly impacted by changes in local crop production, political instability and local government policies, as well as

10 2016 Annual Report

SEABOARD CORPORATION

Management’s Discussion & Analysis

fluctuations in economic and industry conditions and foreign currency exchange rates. This segment’s sales are also significantly affected by fluctuating prices of various commodities, such as wheat, corn, soybeans and soybean meal. Although this segment owns three vessels, the majority of the trading business is transacted with chartered ships. Freight rates, influenced by available charter capacity for worldwide trade in bulk cargoes, and related fuel costs affect business volumes and margins. Consolidated and non-consolidated affiliates operate the grain processing businesses in foreign countries that are in most cases lesser developed. Flour exports of various countries can exacerbate volatile market conditions that may have a significant impact on both the trading and milling businesses’ sales and operating income. This segment represents approximately 51% of Seaboard’s total inventories at December 31, 2016.

The majority of CT&M segment’s sales are derived from its commodity trading business in which agricultural commodities are sourced from multiple origins and delivered to third-party and affiliate customers in various international locations. The execution of these purchase and delivery transactions have long cycles of completion, which may extend for several months with a high degree of price volatility. As a result, these factors can significantly affect sales volumes, operating income, working capital and related cash flows from quarter to quarter. Profit margins are sometimes protected by using commodity derivatives and other risk management practices. Seaboard invested in several entities in recent years and continues to seek opportunities to expand its trading, milling and agro-processing business.

Marine Segment

The Marine segment provides cargo shipping services primarily between the U.S. and 26 countries in the Caribbean and Central and South America. Fluctuations in economic conditions and political instability in the regions or countries in which Seaboard operates may affect trade volumes and operating profits. In addition, cargo rates can fluctuate depending on local supply and demand for shipping services. This segment time-charters the majority of its ocean cargo vessels and is therefore affected by fluctuations in charter hire rates, as well as fuel costs. Seaboard continues to explore ways to increase volumes on existing routes, while seeking opportunities to broaden its route structure in the regions it serves.

Sugar Segment

The Sugar segment operates a vertically integrated sugar and alcohol production facility in Argentina. This segment’s sales and operating income are significantly affected by local and worldwide sugar prices. Domestic sugar production levels in Argentina affect the local price. Global sugar price fluctuations, to a lesser extent, have an impact in Argentina as well. Depending on local market conditions, this business purchases sugar from third parties for resale. This segment sells dehydrated alcohol to certain oil companies under an Argentine government bio-ethanol program, which mandates that alcohol be blended with gasoline. This segment also owns a 51 megawatt cogeneration power plant, which is fueled by the burning of sugarcane by-products, natural gas and other biomass when available. The functional currency of the Sugar segment is the Argentine peso. The currency exchange rate can have an impact on reported U.S. dollar sales, operating income and cash flows. Seaboard continues to explore various ways to improve and expand this segment, investing in efficiency improvements and production capacity increases.

Power Segment

The Power segment is an unregulated independent power producer in the Dominican Republic generating electricity from a system of diesel engines mounted on a floating power generating facility for the local power grid. Seaboard sells power on the spot market primarily to government-owned distribution companies and partially government-owned generation companies. This segment is subject to delays in obtaining timely collections from sales to these government-related entities. Supply of power in the Dominican Republic is determined by a government body and is subject to fluctuations based on governmental budgetary constraints. While fuel is this segment’s largest cost component and is subject to price swings, higher fuel costs generally have been passed on to customers. In 2015, Seaboard invested an additional $10 million in a business operating a 300 megawatt electricity generating facility in the Dominican Republic, increasing Seaboard’s ownership interest to 29.9%. See Note 4 to the consolidated financial statements for further discussion. Seaboard may pursue further power industry investments in the future.

Turkey Segment

Seaboard has a 50% noncontrolling voting interest in Butterball, LLC (“Butterball”). Butterball is a vertically integrated producer, processor and marketer of branded and non-branded turkey and other products. Butterball has four processing plants, three further processing plants and numerous live production and feed milling operations located in North Carolina, Arkansas, Missouri, Illinois and Kansas. Sales prices are directly affected by both domestic and worldwide supply and demand for turkey products and other proteins. Feed accounts for the largest input cost in raising turkeys and is materially affected by price changes for corn and soybean meal. As a result, commodity price fluctuations can

2016 Annual Report 11

SEABOARD CORPORATION

Management’s Discussion & Analysis

significantly affect the profitability and cash flows of Butterball. The turkey business is seasonal only on the whole bird side, with the Thanksgiving and Christmas holidays driving the majority of those sales.

LIQUIDITY AND CAPITAL RESOURCES

Summary of Sources and Uses of Cash

Cash and short-term investments as of December 31, 2016 increased $50 million from December 31, 2015. The increase was primarily the result of net cash from operating activities of $427 million, net proceeds from short-term investments of $53 million and proceeds from sale of fixed assets of $47 million. Partially offsetting the increase was cash used for acquisition of businesses of $219 million, capital expenditures of $158 million, investments in affiliates of $71 million and purchase of long-term investments of $31 million. Cash from operating activities increased $11 million for 2016 primarily as a result of higher net earnings, partially offset by working capital changes.

Cash and short-term investments as of December 31, 2015 increased $777 million from December 31, 2014. The increase was primarily the result of net cash from proceeds related to issuance of long-term debt of $522 million, operating activities of $416 million, notes payable borrowings of $83 million and proceeds from sale of fixed assets of $48 million. Partially offsetting the increase was cash used for capital expenditures of $139 million, investments in affiliates of $119 million and purchase of long-term investments of $28 million. Cash from operating activities increased $42 million for 2015 primarily as a result of decreases in accounts receivable and increases in current liabilities, principally in the CT&M segment, partially offset by lower net earnings.

Capital Expenditures, Acquisitions and Other Investing Activities

During 2016, Seaboard invested $158 million in property, plant and equipment, of which $69 million was in the Pork segment, $35 million in the CT&M segment, $19 million in the Marine segment and $34 million in the Sugar Segment. The Pork segment expenditures were primarily for improvements to existing facilities and related equipment, additional hog finishing barns and the June 2016 purchase and improvement of a biodiesel plant in St. Joseph, Missouri, for $6 million that became operational in the third quarter. Of the CT&M segment expenditures, $29 million was for the construction of two dry bulk vessels, which were delivered and then sold and leased back by Seaboard at book value of $44 million during the first quarter of 2016. The Marine segment expenditures were primarily for purchases of cargo carrying and handling equipment. The Sugar segment expenditures were primarily for milling capacity increase and fermentation and distillery equipment upgrades. All other capital expenditures were primarily of a normal recurring nature and included replacements of machinery and equipment, and general facility modernizations and upgrades.

The total 2017 capital expenditures budget is $231 million. The Pork segment plans to spend $75 million primarily for improvements to existing facilities and related equipment and additional hog finishing barns. The CT&M segment plans to spend $72 million primarily for milling assets, a pulse and grain elevator, and other improvements to existing facilities and related equipment. The Marine segment has budgeted $59 million primarily for additional cargo carrying and handling equipment and port improvements. The Sugar segment plans to spend $24 million primarily for increasing the milling capacity, enhancing energy production installations, and improving logistics infrastructure. The balance of $1 million is planned to be spent in all other businesses primarily for normal upgrades to existing operations. Management anticipates paying for these capital expenditures from a combination of available cash, the use of available short-term investments and Seaboard’s available borrowing capacity.

During 2015, Seaboard invested $139 million in property, plant and equipment, of which $40 million was in the Pork segment, $40 million in the CT&M segment and $43 million in the Marine segment. The Pork segment expenditures were primarily for improvements to existing facilities and related equipment and additional hog finishing barns. Of the CT&M segment expenditures, $30 million was for the construction of dry bulk vessels, two of which were delivered and then sold and leased back by Seaboard at book value of $44 million in 2015. The Marine segment expenditures were primarily for purchases of cargo carrying and handling equipment and $8 million for the purchase of a containerized cargo vessel. All other capital expenditures were of a normal recurring nature and primarily included replacements of machinery and equipment, and general facility modernizations and upgrades.

During 2014, Seaboard invested $121 million in property, plant and equipment, of which $54 million was in the Pork segment, $21 million in the CT&M segment and $29 million in the Marine segment. The Pork segment expenditures were primarily for improvements to existing facilities and related equipment, additional finishing barns and compressed natural gas semi-tractors and related refueling stations. The CT&M segment expenditures were primarily for payments related to building four vessels. The Marine segment expenditures were primarily for purchases of cargo carrying and

12 2016 Annual Report

SEABOARD CORPORATION

Management’s Discussion & Analysis

handling equipment. All other capital expenditures were of a normal recurring nature and primarily included replacements of machinery and equipment, and general facility modernizations.

During 2016 and 2015, Seaboard contributed $51 million and $26 million, respectively, to STF, its newly formed 50% joint venture, for construction of a pork processing facility in Sioux City, Iowa. As the joint venture obtained third-party financing in March 2016, the original subscription agreement was amended to modify the total contribution amount and timing of payments. Seaboard’s remaining commitment of approximately $73 million is expected to be contributed in 2017. In addition to capital contributions, Seaboard also agreed to provide a portion of the hogs to be processed at the facility. During 2016, Seaboard acquired hog inventory and related assets through acquisitions of existing farm operations for a total investment of $219 million. These assets increased Seaboard’s hog production capacity to meet the majority of such hog supply commitment for single shift processing at the new plant. Seaboard anticipates buying additional hog inventory and related assets during 2017 to further increase its hog supply capacity. See Note 12 to the consolidated financial statements for further discussion of the significant acquisitions. The new pork processing facility is expected to begin operations in mid-2017. During the first quarter of 2017, STF announced plans to expand the pork processing plant to be capable of processing an additional three million market hogs annually by operating a second shift. The expansion is estimated to cost approximately $47 million, of which Seaboard could be required to commit up to 50% of the amount.

Also during 2016, Seaboard invested $7 million of cash and converted its $8 million note receivable to equity for a 36% noncontrolling interest in a holding company that owns a controlling interest in two Haitian start-up projects consisting of a marine terminal operation and a free trade zone development, which includes a planned power plant. The investment is accounted for in the Marine segment using the equity method and reported on a three-month lag. Seaboard’s first proportionate share of income (loss) from affiliates was recognized in the second quarter of 2016. The note receivable, which included $4 million loaned in 2014 and $4 million loaned in 2015, was converted into equity by Seaboard once certain business operating conditions were met in Haiti.

Seaboard continued to invest in a flour production business in Brazil, of which Seaboard now holds a 98% noncontrolling interest. During 2016, 2015 and 2014, Seaboard invested an additional $14 million, $28 million and $4 million, respectively, in equity and long-term advances. See Note 4 to the consolidated financial statements for further discussion of this investment.

Seaboard invested in two limited liability companies that operate refined coal processing plants, one in Oklahoma during 2015 and one in Nebraska during 2016. Production of refined coal generates federal income tax credits. Seaboard’s funding commitment for these companies varies depending on production and, based on current production estimates, is anticipated to each be between $7 million and $9 million per year until 2021, for a total estimate of approximately $73 million as of December 31, 2016. Seaboard invested $14 million and $9 million during 2016 and 2015, respectively.

During 2015, the CT&M and Power segments invested in several businesses. Seaboard contributed $13 million in cash, a small amount of other assets, certain employees and rights to sell certain agricultural commodities that Seaboard had previously sold through its subsidiary, PS International, LLC, for a 40% noncontrolling interest in a commodity trading business in Atlanta, Georgia. Also, Seaboard invested $8 million in a flour milling business in Botswana for a 49% noncontrolling interest, $10 million for a 45% noncontrolling interest in a commodity trading and flour milling business in Uruguay, $10 million in an oilseed crushing business in the Republic of Turkey for a 25% noncontrolling interest, and $18 million for a 12% noncontrolling interest in a grain trading and poultry business in Morocco, which is accounted for using the cost method. During 2015, the Power segment invested $10 million in a business operating a 300 megawatt electricity generating facility in the Dominican Republic, increasing Seaboard’s ownership interest to 29.9%. See Note 4 to the consolidated financial statements for further discussion.

During 2014, the Pork segment sold a business, and the Marine segment invested in a business. In September 2014, the Pork segment sold to Triumph Foods, LLC a 50% interest in its Daily’s Premium Meats division for $74 million. Also in that month, Seaboard’s Marine segment invested $17 million in a cargo terminal business in Jamaica for a 21% noncontrolling interest. See Note 4 to the consolidated financial statements for further discussion.

2016 Annual Report 13

SEABOARD CORPORATION

Management’s Discussion & Analysis

Financing Activities, Debt and Related Covenants

The following table presents a summary of Seaboard’s available borrowing capacity as of December 31, 2016. At December 31, 2016, borrowings under the uncommitted lines of credit totaled $121 million, with all such borrowings related to foreign subsidiaries. See Note 7 to the consolidated financial statements for further discussion.

|

|

|

|

|

|

|

|

|

Total amount |

|

|

|

(Millions of dollars) |

|

available |

|

|

|

Short-term uncommitted and committed lines |

|

$ |

480 |

|

|

Amounts drawn against lines |

|

|

(121) |

|

|

Letters of credit reducing borrowing availability |

|

|

(4) |

|

|

Available borrowing capacity at December 31, 2016 |

|

$ |

355 |

|

On September 30, 2016, Seaboard entered into a $100 million committed line of credit with Wells Fargo Bank, National Association (“Wells Fargo”) that matures on September 29, 2017. Interest is computed at LIBOR plus 0.50%, and Seaboard incurs an unused commitment fee of 0.09% per annum. This line of credit is secured by certain short-term investments. The line of credit is subject to standard representations and covenants. There was no outstanding balance as of December 31, 2016.

At December 31, 2016, Seaboard had an unsecured term loan, which matures in 2022, with a balance of $497 million and $20 million of foreign subsidiary debt, primarily denominated in Argentine pesos. Seaboard was in compliance with all restrictive covenants related to these loans and facilities as of December 31, 2016. Seaboard has capacity under existing loan covenants to undertake additional debt financings of approximately $1,605 million at December 31, 2016. See Note 7 to the consolidated financial statements for further discussion of notes payable and long-term debt.

As of December 31, 2016, Seaboard had cash and short-term investments of $1,354 million and additional total working capital of $709 million. Accordingly, management believes Seaboard’s combination of internally generated cash, liquidity, capital resources and borrowing capabilities will be adequate for its existing operations and any currently known potential plans for expansion of existing operations or business segments for 2017. Management intends to continue seeking opportunities for expansion in the industries in which Seaboard operates, utilizing existing liquidity, available borrowing capacity and other financing alternatives.

As of December 31, 2016, $441 million of the $1,354 million of cash and short-term investments were held by Seaboard’s foreign subsidiaries, and Seaboard could be required to accrue and pay taxes to repatriate these funds if needed for Seaboard’s operations in the U.S. However, Seaboard’s intent is to permanently reinvest these funds outside the U.S., and current plans do not demonstrate a need to repatriate them to fund Seaboard’s U.S. operations.

Seaboard used cash to repurchase 18,405 shares of common stock at a total price of $53 million in 2014. No common stock was repurchased in 2016 or 2015. There were no dividends paid in 2016, 2015 or 2014. On February 2, 2017, Seaboard declared a quarterly dividend of $1.50 per share of common stock payable on February 23, 2017. Seaboard’s Board of Directors intends that Seaboard will continue to pay quarterly dividends for the reasonably foreseeable future, with the amount of any dividends being dependent upon such factors as Seaboard’s financial condition, results of operations and current and anticipated cash needs, including capital requirements. See Note 11 to the consolidated financial statements for further discussion on stockholders’ equity.

14 2016 Annual Report

SEABOARD CORPORATION

Management’s Discussion & Analysis

Contractual Obligations and Off-Balance Sheet Arrangements

The following table provides a summary of Seaboard’s contractual obligations as of December 31, 2016.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Payments due by period |

|

|||||||||||||

|

|

|

|

|

|

Less than |

|

1-3 |

|

3-5 |

|

More than |

|

||||

|

(Millions of dollars) |

|

Total |

1 year |

|

years |

|

years |

|

5 years |

|

||||||

|

Vessel, time and voyage-charter commitments |

|

$ |

198 |

|

$ |

47 |

|

$ |

53 |

|

$ |

52 |

|

$ |

46 |

|

|

Contract grower agreements |

|

|

100 |

|

|

29 |

|

|

40 |

|

|

22 |

|

|

9 |

|

|

Other operating lease payments |

|

|

307 |

|

|

31 |

|

|

54 |

|

|

46 |

|

|

176 |

|

|

Total lease obligations |

|

|

605 |

|

|

107 |

|

|

147 |

|

|

120 |

|

|

231 |

|

|

Short-term notes payable |

|

|

121 |

|

|

121 |

|

|

— |

|

|

— |

|

|

— |

|

|

Long-term debt |

|

|

517 |

|

|

17 |

|

|

54 |

|

|

80 |

|

|

366 |

|

|

Interest payments (1) |

|

|

77 |

|

|

17 |

|

|

30 |

|

|

21 |

|

|

9 |

|

|

Retirement benefit payments (2) |

|

|

96 |

|

|

8 |

|

|

18 |

|

|

16 |

|

|

54 |

|

|

Investment in affiliates (3) |

|

|

150 |

|

|

91 |

|

|

31 |

|

|

28 |

|

|

— |

|

|

Other purchase commitments |

|

|

947 |

|

|

638 |

|

|

105 |

|

|

86 |

|

|

118 |

|

|

Total contractual cash obligations and commitments |

|

$ |

2,513 |

|

$ |

999 |

|

$ |

385 |

|

$ |

351 |

|

$ |

778 |

|

(1) Interest payments in the table above include cash payments for interest on variable rate long-term debt based on interest rates as of December 31, 2016. Interest payments also include the net payments for interest rate exchange agreements based on the fixed amounts paid and the variable amount received, which is estimated using the projected yield as of December 31, 2016.

(2) Retirement benefit payments in the table above represent expected benefit payments for various non-qualified pension plans and supplemental retirement arrangements as discussed in Note 9 to the consolidated financial statements, which are unfunded obligations that are deemed to be employer contributions. No contributions are planned at this time to the two qualified pension plans. Effective January 1, 2017, the assets and liabilities of the two plans were merged, so that only one qualified defined benefit pension plan remains.

(3) Investment in affiliates represents obligations made to equity method investments of Seaboard, primarily $73 million committed to STF for construction of its Sioux City pork processing facility and $73 million of expected funding commitments based on production levels for two limited liability companies that operate refined coal processing plants.

Several of Seaboard’s segments have long-term contractual obligations, including non-cancelable operating lease agreements for facilities and equipment. The Marine and CT&M segments enter into contracts to time-charter vessels for use in operations. The Pork segment has contract grower agreements in place with farmers to raise a portion of Seaboard’s hogs to support its operations. The Pork segment has also entered into grain and feed ingredient purchase contracts to support the segment’s live hog operations, and has contracted for the purchase of additional hogs from third parties. The CT&M segment enters into commodity purchase contracts, primarily to support sales commitments. See Note 10 to the consolidated financial statements for further discussion on Seaboard’s contractual obligations and for a more detailed listing of other purchase commitments.

Non-current deferred income taxes and certain other long-term liabilities on the consolidated balance sheets are not included in the table above as management is unable to reliably estimate the timing of the payments for these items. In addition, deferred revenues and other deferred credits included in other long-term liabilities on the consolidated balance sheets have been excluded from the table above because they do not represent contractual obligations.

RESULTS OF OPERATIONS

Net sales for the years ended December 31, 2016, 2015 and 2014 were $5,379 million, $5,594 million and $6,473 million, respectively. The decrease for 2016 compared to 2015 primarily reflected lower commodity prices and the mix of products sold for the CT&M segment, lower volumes of sugar sold in the Sugar segment, and lower cargo rates in the Marine segment, partially offset by higher sales volume of market hogs from 2016 acquisitions of live operations and higher biodiesel volumes from the acquisition of a second biodiesel plant in the Pork segment. The decrease for 2015 compared to 2014 primarily reflected lower prices for pork products sold and the deconsolidation of Daily’s in the Pork

2016 Annual Report 15

SEABOARD CORPORATION

Management’s Discussion & Analysis

segment, lower sales prices for almost all commodities sold and lower sales volume of corn for the CT&M segment, and lower spot market rates and sales volume for the Power segment. The decreases were partially offset by higher cargo volumes for the Marine segment.

Operating income for the years ended December 31, 2016, 2015 and 2014 were $222 million, $126 million and $424 million, respectively. The increase for 2016 compared to 2015 primarily reflected lower feed costs for hogs internally grown in the Pork segment and higher margins on commodity trades to third parties in the CT&M segment, partially offset by higher production costs for sugar in the Sugar segment. The decrease for 2015 compared to 2014 primarily reflected lower prices for pork products sold, lower margins on commodity trades to third parties, and higher production costs for sugar and alcohol.

Pork Segment

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Millions of dollars) |

|

|

|

2016 |

|

2015 |

|

2014 |

|

|||

|

Net sales |

|

|

|

$ |

1,443 |

|

$ |

1,332 |

|

$ |

1,717 |

|

|

Operating income |

|

|

|

$ |

175 |

|

$ |

116 |

|

$ |

349 |

|

|

Income from affiliates |

|

|

|

$ |

11 |

|

$ |

11 |

|

$ |

4 |

|

Net sales for the Pork segment increased $111 million for the year ended December 31, 2016 compared to 2015. The increase was primarily the result of higher sales volume of market hogs related to acquisitions as discussed in Note 9 to the consolidated financial statements, higher prices for pork products sold and increased volume and sales prices for biodiesel resulting from increased output from the Guymon plant and the acquisition of a second biodiesel plant in St. Joseph, Missouri. The increase was partially offset by lower volume of pork products sold.

Operating income for the Pork segment increased $59 million for the year ended December 31, 2016 compared to 2015. The increase was primarily the result of lower feed costs for hogs internally grown and improved overall margins from higher meat prices. Management is unable to predict future market prices for pork products, the cost of feed or cost of third-party hogs; however, management anticipates positive operating income for this segment in 2017. The Federal blender’s credits have not been renewed for 2017.

Net sales for the Pork segment decreased $385 million for the year ended December 31, 2015 compared to 2014. The decrease was primarily the result of lower prices for pork products sold and the deconsolidation of Daily’s. The decrease was partially offset by an increase in related sales volume.

Operating income for the Pork segment decreased $233 million for the year ended December 31, 2015 compared to 2014. The decrease was primarily the result of lower prices for pork products and, to a lesser degree, the deconsolidation of Daily’s. Partially offsetting the decrease was lower costs for third-party hogs and lower feed costs for hogs internally grown. In December 2015, the Federal blender’s credit that Seaboard is entitled to receive for biodiesel it blends was reinstated for 2015 and 2016, retroactive to January 1, 2015. As a result, the 2015 Federal blender’s credit of $17 million was recorded as revenues in the fourth quarter of 2015. See Note 13 to the consolidated financial statements for further discussion of the Federal blender’s credit.

Income from affiliates for the Pork segment was primarily from Seaboard’s 50% ownership interest in Daily’s, accounted for using the equity method. Seaboard’s first proportionate share of earnings for Daily’s was recognized in the fourth quarter of 2014.

Commodity Trading and Milling Segment

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Millions of dollars) |

|

|

2016 |

|

2015 |

|

2014 |

|

|||

|

Net sales |

|

|

$ |

2,778 |

|

$ |

3,022 |

|

$ |

3,499 |

|

|

Operating income as reported |

|

|

$ |

38 |

|

$ |

2 |

|

$ |

54 |

|

|

Mark-to-market adjustments |

|

|

|

— |

|

|

(5) |

|

|

(13) |

|

|

Operating income (loss) excluding mark-to-market adjustments |

|

|

$ |

38 |

|

$ |

(3) |

|

$ |

41 |

|

|

Loss from affiliates |

|

|

$ |

(10) |

|

$ |

(50) |

|

$ |

(24) |

|

Net sales for the CT&M segment decreased $244 million for the year ended December 31, 2016 compared to 2015. The decrease primarily reflected lower sales prices, resulting from lower commodity prices and the mix of products sold, partially offset by higher volumes in corn and soybeans.

16 2016 Annual Report

SEABOARD CORPORATION

Management’s Discussion & Analysis

Operating income for the CT&M segment increased $36 million for the year ended December 31, 2016, compared to 2015. The increase primarily reflected higher margins on commodity trades to third parties and affiliates and fluctuations of $5 million of mark-to-market derivative contracts as discussed below. Excluding the effects of the mark-to-market adjustments for derivatives contracts, operating income increased $41 million.

Due to worldwide commodity price fluctuations, the uncertain political and economic conditions in the countries in which Seaboard operates, and the current volatility in the commodity markets, management is unable to predict future sales and operating results for this segment. However, management anticipates positive operating income for this segment in 2017, excluding the effects of marking to market derivative contracts.

Had Seaboard not applied mark-to-market accounting to its derivative instruments, operating income for this segment would have remained the same in 2016 and been lower by $5 million and $13 million in 2015 and 2014, respectively. While management believes its commodity futures, options and foreign exchange contracts are primarily economic hedges of its firm purchase and sales contracts or anticipated sales contracts, Seaboard does not perform the extensive record-keeping required to account for these transactions as hedges for accounting purposes. Accordingly, while the changes in value of the derivative instruments were marked to market, the changes in value of the firm purchase or sales contracts were not. As products are delivered to customers, these existing mark-to-market adjustments should be primarily offset by realized margins or losses as revenue is recognized over time and therefore, these mark-to-market adjustments could reverse in fiscal 2017. Management believes eliminating these mark-to-market adjustments provides a more reasonable presentation to compare and evaluate period-to-period financial results for this segment.

Loss from affiliates for the CT&M segment decreased by $40 million for the year ended December 31, 2016 compared to 2015. The decrease primarily reflected lower operating and currency losses recorded against the investment and lower reserves for notes receivable and advances from an affiliate in Brazil. Seaboard’s loss from this Brazilian affiliate totaled $60 million in 2015 compared to $10 million in 2016. This Brazilian affiliate was consolidated in the fourth quarter of 2016. See Note 4 to the consolidated financial statements for further discussion of this affiliate. Based on the uncertainty of local political and economic environments in the countries in which Seaboard’s affiliates operate, management cannot predict future results.

Net sales for the CT&M segment decreased $477 million for the year ended December 31, 2015 compared to 2014. The decrease primarily reflected lower sales prices for almost all commodities sold and, to a lesser extent, lower sales volume primarily for corn.

Operating income for the CT&M segment decreased $52 million for the year ended December 31, 2015 compared to 2014. The decrease primarily reflected certain unfavorable market conditions, which resulted in lower margins on commodity trades to third parties. The decrease also reflected an increase in bad debt expense primarily attributable to trade receivables with an affiliate in Brazil (see Note 4 to the consolidated financial statements for further discussion) and fluctuations of $8 million of mark-to-market derivative contracts. Excluding the effects of mark-to-market adjustments for derivatives contracts, operating income decreased $44 million.

Loss from affiliates for the CT&M segment increased by $26 million for the year ended December 31, 2015 compared to 2014. The increase primarily reflected operating and currency losses recorded against the investment and reserves for notes receivable and advances from an affiliate in Brazil totaling $60 million. Partially offsetting the increase was an $11 million write down in a Democratic Republic of Congo (“DRC”) bakery business investment recorded in 2014 as further discussed in Note 4 to the consolidated financial statements and a decrease in losses in 2015 compared to 2014 in this same business.

Marine Segment

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Millions of dollars) |

|

|

2016 |

|

2015 |

|

2014 |

|

|||

|

Net sales |

|

|

$ |

916 |

|

$ |

940 |

|

$ |

853 |

|

|

Operating income (loss) |

|

|

$ |

33 |

|

$ |

19 |

|

$ |

(3) |

|

|

Income from affiliate |

|

|

$ |

1 |

|

$ |

2 |

|

$ |

— |

|

Net sales for the Marine segment decreased $24 million for the year ended December 31, 2016 compared to 2015. The decrease was primarily the result of lower cargo rates in certain markets during 2016 compared to 2015, partially offset by higher volumes.

2016 Annual Report 17

SEABOARD CORPORATION

Management’s Discussion & Analysis

Operating income for the Marine segment increased $14 million for the year ended December 31, 2016 compared to 2015. The increase was primarily the result of lower voyage costs, principally fuel costs, on a per unit shipped basis, partially offset by lower cargo rates. Management cannot predict changes in future cargo volumes, cargo rates and fuel costs, or to what extent changes in economic conditions in markets served will affect net sales or operating income during 2017. However, management anticipates this segment will have positive operating income for 2017.

Net sales for the Marine segment increased $87 million for the year ended December 31, 2015 compared to 2014. The increase was primarily the result of higher cargo volumes, partially offset by lower cargo rates in certain markets during 2015 compared to 2014.

Operating income for the Marine segment increased $22 million for the year ended December 31, 2015 compared to 2014. The increase was primarily the result of lower voyage costs, principally fuel costs, on a per unit shipped basis, partially offset by lower cargo rates.

Sugar Segment

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Millions of dollars) |

|

|

2016 |

|

2015 |

|

2014 |

|

|||

|

Net sales |

|

|

$ |

147 |

|

$ |

188 |

|

$ |

200 |

|

|

Operating income (loss) |

|

|

$ |

(12) |

|

$ |

2 |

|

$ |

27 |

|

|

Income from affiliates |

|

|

$ |

2 |

|

$ |

1 |

|

$ |

1 |

|

Net sales for the Sugar segment decreased $41 million for the year ended December 31, 2016 compared to 2015. The decrease primarily reflected lower volumes and lower selling prices of sugar sold. During the third and fourth quarters of 2016, labor strikes and inclement weather negatively impacted volumes and resulted in a $12 million inventory charge to cost of sales for fixed manufacturing costs associated with the revised production forecasts. Sugar and alcohol sales are denominated in Argentine pesos, and an increase in local sales prices in terms of U.S. dollars was principally offset by exchange rate changes as the Argentine peso continued to weaken against the U.S. dollar in 2016. Management cannot predict local sugar and alcohol prices for 2017, but management anticipates that the Argentine peso will continue to be weaker against the U.S. dollar, which should result in lower sale prices in terms of U.S. dollars in 2017.

Operating income for the Sugar segment decreased $14 million for the year ended December 31, 2016 compared to 2015. The decrease primarily reflected lower sales prices, lower volumes and the $12 million inventory charge. The decrease in operating income was partially offset by reduced selling, general and administrative expenses from decreased personnel-related costs. Based on recent market conditions, management currently cannot predict if this segment will be profitable in 2017.

Net sales for the Sugar segment decreased $12 million for the year ended December 31, 2015 compared to 2014. The decrease primarily reflected lower volumes for sugar sold. Sugar and alcohol sales are denominated in Argentine pesos, and an increase in local sales prices in terms of U.S. dollars was principally offset by exchange rate changes as the Argentine peso weakened against the U.S. dollar in 2015.

Operating income for the Sugar segment decreased $25 million for the year ended December 31, 2015 compared to 2014. The decrease primarily reflected higher production costs for sugar and alcohol. To a lesser extent, the decrease in operating income was also the result of higher selling, general and administrative expenses principally from increased personnel-related costs and lower volume of sugar sold. Also, operating income in 2014 included a $4 million gain related to a final insurance settlement for property damage and business interruption claims related to prior years.

Power Segment

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Millions of dollars) |

|

|

2016 |

|

2015 |

|

2014 |

|

|||

|

Net sales |

|

|

$ |

79 |

|

$ |

97 |

|

$ |

189 |

|

|

Operating income |

|

|

$ |

7 |

|

$ |

7 |

|

$ |

19 |

|

|

Income from affiliate |

|

|

$ |

4 |

|

$ |

3 |

|

$ |

2 |

|

Net sales for the Power segment decreased $18 million for the year ended December 31, 2016 compared to 2015. The decrease primarily reflected lower spot market rates, which were attributable primarily to lower fuel costs, a component of pricing.

18 2016 Annual Report

SEABOARD CORPORATION

Management’s Discussion & Analysis

Operating income for the Power segment remained flat for the year ended December 31, 2016 compared to 2015 primarily due to the lower spot market rates being offset by lower fuel costs per kilowatt hour generated and other lower production costs. Management cannot predict future fuel costs or the extent that spot market rates will fluctuate compared to fuel costs; however, management anticipates positive operating income for this segment in 2017.

Net sales for the Power segment decreased $92 million for the year ended December 31, 2015 compared to 2014. The decrease primarily reflected lower spot market rates and lower volumes. The lower spot market rates were attributable primarily to lower fuel costs, a component of pricing. The lower volumes were a result of cancelling the short-term leasing of a power generating facility on September 3, 2014 as discussed in Note 13 to the consolidated financial statements.

Operating income for the Power segment decreased $12 million for the year ended December 31, 2015 compared to 2014. The decrease primarily reflected lower spot market rates and lower volumes, partially offset by lower fuel costs per kilowatt hour generated and other lower production costs. Also, operating income in 2014 included a gain on sale of assets of $5 million as discussed in Note 13 to the consolidated financial statements.

Turkey Segment

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Millions of dollars) |

|

|

2016 |

|

2015 |

|

2014 |

|

|||

|

Income from affiliate |

|

|

$ |

73 |

|

$ |

103 |

|

$ |

54 |

|

The Turkey segment, accounted for using the equity method, represents Seaboard’s investment in Butterball. The decrease in income from affiliate for 2016 compared to 2015 was primarily the result of lower volume and prices for turkey products sold. Management is unable to predict future market prices for turkey products, the cost of feed or the impact from avian influenza; however, management anticipates positive income for this segment in 2017.

The increase in income from affiliate for 2015 compared to 2014 was primarily the result of lower feed costs and higher prices of turkey products sold.

Selling, General and Administrative Expenses