Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-4801

BARNES GROUP INC.

(Exact name of registrant as specified in its charter)

Delaware |  | 06-0247840 | ||

(State of incorporation) | (I.R.S. Employer Identification No.) | |||

123 Main Street, Bristol, Connecticut | 06010 | |||

(Address of Principal Executive Office) | (Zip Code) | |||

(860) 583-7070

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Stock, $0.01 Par Value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x | Accelerated filer o | |

Non-accelerated filer o | Smaller reporting company o | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting stock (Common Stock) held by non-affiliates of the registrant as of the close of business on June 30, 2016 was approximately $1,661,081,242 based on the closing price of the Common Stock on the New York Stock Exchange on that date. The registrant does not have any non-voting common equity.

The registrant had outstanding 53,823,313 shares of common stock as of February 16, 2017.

Documents Incorporated by Reference

Portions of the registrant’s definitive proxy statement to be delivered to stockholders in connection with the Annual Meeting of Stockholders to be held May 5, 2017 are incorporated by reference into Part III.

Barnes Group Inc.

Index to Form 10-K

Year Ended December 31, 2016

Page | ||

Part I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Part II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Part III | ||

Item 10. | ||

Items 11-14. | ||

Part IV | ||

Item 15. | ||

Item 16. | ||

FORWARD-LOOKING STATEMENTS

This Annual Report may contain forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements often address our expected future operating and financial performance and financial condition, and often contain words such as "anticipate," "believe," "expect," "plan," "estimate," "project," and similar terms. These forward-looking statements do not constitute guarantees of future performance and are subject to a variety of risks and uncertainties that may cause actual results to differ materially from those expressed in the forward-looking statements. These include, among others: difficulty maintaining relationships with employees, including unionized employees, customers, distributors, suppliers, business partners or governmental entities; failure to successfully negotiate collective bargaining agreements or potential strikes, work stoppages or other similar events; difficulties leveraging market opportunities; changes in market demand for our products and services; rapid technological and market change; the ability to protect intellectual property rights; introduction or development of new products or transfer of work; higher risks in global operations and markets; the impact of intense competition; acts of terrorism, cybersecurity attacks or intrusions that could adversely impact our businesses; uncertainties relating to conditions in financial markets; currency fluctuations and foreign currency exposure; future financial performance of the industries or customers that we serve; our dependence upon revenues and earnings from a small number of significant customers; a major loss of customers; inability to realize expected sales or profits from existing backlog due to a range of factors, including changes in customer sourcing decisions, material changes, production schedules and volumes of specific programs; the impact of government budget and funding decisions; changes in raw material or product prices and availability; integration of acquired businesses; restructuring costs or savings; the continuing impact of prior acquisitions and

divestitures; and any other future strategic actions, including acquisitions, divestitures, restructurings, or strategic business realignments, and our ability to achieve the financial and operational targets set in connection with any such actions; the outcome of pending and future legal, governmental, or regulatory proceedings and contingencies and uninsured claims; future repurchases of common stock; future levels of indebtedness; and numerous other matters of a global, regional or national scale, including those of a political, economic, business, competitive, environmental, regulatory and public health nature; and other risks and uncertainties described in this Annual Report. The Company assumes no obligation to update its forward-looking statements.

PART I

Item 1. Business

BARNES GROUP INC. (1)

Founded in 1857, Barnes Group Inc. (the “Company”) is a global industrial and aerospace manufacturer and service provider, serving a wide range of end markets and customers. The highly engineered products, differentiated industrial technologies, and innovative solutions delivered by Barnes Group are used in far-reaching applications that provide transportation, manufacturing, healthcare products, and technology to the world. Barnes Group’s approximately 5,000 skilled and dedicated employees around the globe are committed to achieving consistent and sustainable profitable growth.

Structure

The Company operates under two global business segments: Industrial and Aerospace. The Industrial segment includes the the Molding Solutions, Nitrogen Gas Products and Engineered Components business units. The Aerospace segment includes the original equipment manufacturer (“OEM”) business and the aftermarket business, which includes maintenance repair and overhaul (“MRO”) services and the manufacture and delivery of aerospace aftermarket spare parts.

In the third quarter of 2016, the Company, through three of its subsidiaries (collectively, the “Purchaser”), completed its acquisition of the molds business of Adval Tech Holding AG and Adval Tech Holdings (Asia) Pte. Ltd. ("FOBOHA"). FOBOHA is headquartered in Haslach, Germany and operates out of three manufacturing facilities located in Germany, Switzerland and China. The Company completed its purchase of the Germany and Switzerland businesses on August 31, 2016. The purchase of the China business required government approval which was granted on September 30, 2016. FOBOHA specializes in the development and manufacture of complex plastic injection molds for packaging, medical, consumer and automotive applications. The Company acquired FOBOHA for an aggregate cash purchase price of CHF 136.3 million ($138.6 million) which was financed using cash on hand and borrowings under the Company's revolving credit facility. The purchase price includes preliminary adjustments under the terms of the Share Purchase Agreement ("SPA"), including approximately CHF 11.3 million ($11.5 million) related to cash acquired, and is subject to post closing adjustments under the terms of the SPA. In connection with the acquisition, the Company recorded $39.8 million of intangible assets and $73.7 million of goodwill. FOBOHA is being integrated into the Industrial Segment, within our Molding Solutions business unit. See Note 2 and Note 5 to the Consolidated Financial Statements.

In the fourth quarter of 2015, the Company completed the acquisition of privately held Priamus System Technologies AG and two of its subsidiaries (collectively, "Priamus") from Growth Finance AG. Priamus, which has approximately 40 employees, is headquartered in Schaffhausen, Switzerland and has direct sales and service offices in the U.S. and Germany. Priamus is a technology leader in the development of advanced process control systems for the plastic injection molding industry and services many of the world's highest quality plastic injection molders in the medical, automotive, consumer goods, electronics and packaging markets. Priamus is being integrated into the Industrial Segment, within our Molding Solutions business unit. See Note 2 of the Consolidated Financial Statements.

In the third quarter of 2015, the Company completed the acquisition of the Thermoplay business ("Thermoplay") by acquiring all of the capital stock of privately held HPE S.p.A., the parent company through which Thermoplay operates. Thermoplay’s headquarters and manufacturing facility are located in Pont-Saint-Martin in Aosta, Italy, with technical service capabilities in China, India, France, Germany, United Kingdom, Portugal, and Brazil. Thermoplay specializes in the design, development, and manufacturing of hot runner systems for plastic injection molding, primarily in the packaging, automotive, and medical end markets. Thermoplay is being integrated into the Industrial Segment, within our Molding Solutions business unit. See Note 2 of the Consolidated Financial Statements.

_________

(1) As used in this annual report, “Company,” “Barnes Group,” “we” and “ours” refer to the registrant and its consolidated subsidiaries except where the context requires otherwise, and “Industrial” and “Aerospace” refer to the registrant’s segments, not to separate corporate entities

1

INDUSTRIAL

Industrial is a global manufacturer of highly-engineered, high-quality precision parts, products and systems for critical applications serving a diverse customer base in end-markets such as transportation, industrial equipment, consumer products, packaging, electronics, medical devices, and energy. Focused on innovative custom solutions, Industrial participates in the design phase of components and assemblies whereby customers receive the benefits of application and systems engineering, new product development, testing and evaluation, and the manufacturing of final products. Products are sold primarily through its direct sales force and global distribution channels. Industrial’s Molding Solutions businesses design and manufacture customized hot runner systems, advanced mold cavity sensors and process control systems, and precision high cavitation and cube mold assemblies - collectively, the enabling technologies for many complex plastic injection molding applications. Industrial’s Nitrogen Gas Products business manufactures nitrogen gas springs and manifold systems used to precisely control stamping presses. Industrial’s Engineered Components businesses manufacture and supply precision mechanical products used in transportation and industrial applications, including mechanical springs, high-precision punched and fine-blanked components, and retaining rings. Engineered Components is equipped to produce many types of highly engineered precision springs, from fine hairsprings for electronics and instruments to large heavy-duty springs for machinery.

Industrial competes with a broad base of large and small companies engaged in the manufacture and sale of engineered products, precision molds, hot runner systems and precision components. Industrial competes on the basis of quality, service, reliability of supply, engineering and technical capability, geographic reach, product breadth, innovation, design, and price. Industrial has manufacturing, distribution and assembly operations in the United States, Brazil, China, Germany, Italy, Mexico, Singapore, Sweden and Switzerland. Industrial also has sales and service operations in the United States, Brazil, Canada, Czech Republic, China/Hong Kong, France, Germany, India, Italy, Japan, Mexico, the Netherlands, Portugal, Singapore, Slovakia, South Africa, South Korea, Spain, Switzerland, Thailand and the United Kingdom. Sales by Industrial to its three largest customers accounted for approximately 11% of its sales in 2016.

AEROSPACE

Aerospace is a global provider of complex fabricated and precision machined components and assemblies for OEM turbine engine, airframe and industrial gas turbine builders, and the military. The Aerospace aftermarket business provides jet engine component MRO services, including services performed under our Component Repair Programs (“CRPs”), for many of the world’s major turbine engine manufacturers, commercial airlines and the military. The Aerospace aftermarket activities also include the manufacture and delivery of aerospace aftermarket spare parts, including the revenue sharing programs (“RSPs”) under which the Company receives an exclusive right to supply designated aftermarket parts over the life of the related aircraft engine programs.

Aerospace’s OEM business supplements the leading jet engine OEM capabilities and competes with a large number of fabrication and machining companies. Competition is based mainly on quality, engineering and technical capability, product breadth, new product introduction, timeliness, service and price. Aerospace’s fabrication and machining operations, with facilities in Arizona, Connecticut, Michigan, Ohio, Utah and Singapore, produce critical engine and airframe components through technologically advanced manufacturing processes.

The Aerospace aftermarket business supplements jet engine OEMs’ maintenance, repair and overhaul capabilities, and competes with the service centers of major commercial airlines and other independent service companies for the repair and overhaul of turbine engine components. The manufacture and supply of aerospace aftermarket spare parts, including those related to the RSPs, are dependent upon the reliable and timely delivery of high-quality components. Aerospace’s aftermarket facilities, located in Connecticut, Ohio and Singapore, specialize in the repair and refurbishment of highly engineered components and assemblies such as cases, rotating life limited parts, rotating air seals, turbine shrouds, vanes and honeycomb air seals. Sales by Aerospace to its three largest customers, General Electric, Rolls-Royce and United Technologies Corporation, accounted for approximately 51%, 13% and 11% of its sales in 2016, respectively. Sales to its next four largest customers in 2016 collectively accounted for approximately 10% of its total sales.

FINANCIAL INFORMATION

The backlog of the Company’s orders believed to be firm at the end of 2016 was $886 million as compared with $764 million at the end of 2015. Of the 2016 year-end backlog, $636 million was attributable to Aerospace and $250 million was attributable to Industrial. Approximately 65% of the Company's year-end backlog is scheduled to be shipped during 2017. The remainder of the Company’s backlog is scheduled to be shipped after 2017.

2

We have a global manufacturing footprint and a technical service network to service our worldwide customer base. The global economies have a significant impact on the financial results of the business as we have significant operations outside of the United States. For an analysis of our revenue from sales to external customers, operating profit and assets by business segment, as well as revenues from sales to external customers and long-lived assets by geographic area, see Note 19 of the Consolidated Financial Statements. For a discussion of risks attendant to the global nature of our operations and assets, see Item 1A. Risk Factors.

RAW MATERIALS

The principal raw materials used to manufacture our products are various grades and forms of steel, from rolled steel bars, plates and sheets, to high-grade valve steel wires and sheets, various grades and forms (bars, sheets, forgings, castings and powders) of stainless steels, aluminum alloys, titanium alloys, copper alloys, graphite, and iron-based, nickel-based (Inconels) and cobalt-based (Hastelloys) superalloys for complex aerospace applications. Prices for steel, titanium, Inconel, Hastelloys, as well as other specialty materials, have periodically increased due to higher demand and, in some cases, reduction of the availability of materials. If this occurs, the availability of certain raw materials used by us or in products sold by us may be negatively impacted.

RESEARCH AND DEVELOPMENT

We conduct research and development activities in our effort to provide a continuous flow of innovative new products, processes and services to our customers. We also focus on continuing efforts aimed at discovering and implementing new knowledge that significantly improves existing products and services, and developing new applications for existing products and services. Our product development strategy is driven by product design teams and collaboration with our customers, particularly within Industrial’s Molding Solutions businesses, as well as within our Aerospace and our other Industrial businesses. Many of the products manufactured by us are custom parts made to customers’ specifications. Investments in research and development are important to our long-term growth, enabling us to stay ahead of changing customer and marketplace needs. We spent approximately $13 million, $13 million and $16 million in 2016, 2015 and 2014, respectively, on research and development activities.

PATENTS AND TRADEMARKS

Patents and other proprietary rights are critical to certain of our business units, however the Company also holds certain trade secrets and unpatented know-how. We are party to certain licenses of intellectual property and hold numerous patents, trademarks, and trade names that enhance our competitive position. The Company does not believe, however, that any of these licenses, patents, trademarks or trade names is individually significant to the Company or either of our segments. We maintain procedures to protect our intellectual property (including patents and trademarks) both domestically and internationally. Risk factors associated with our intellectual property are discussed in Item 1A. Risk Factors.

EXECUTIVE OFFICERS OF THE COMPANY

For information regarding the Executive Officers of the Company, see Part III, Item 10 of this Annual Report.

ENVIRONMENTAL

Compliance with federal, state, and local laws, as well as those of other countries, which have been enacted or adopted regulating the discharge of materials into the environment or otherwise relating to the protection of the environment has not had a material effect, and is not expected to have a material effect, upon our capital expenditures, earnings, or competitive position.

Our past and present business operations and past and present ownership and operations of real property and the use, sale, storage and handling of chemicals and hazardous products subject us to extensive and changing U.S. federal, state and local environmental laws and regulations, as well as those of other countries, pertaining to the discharge of materials into the environment, enforcement, disposition of wastes (including hazardous wastes), the use, shipping, labeling, and storage of chemicals and hazardous materials, building requirements, or otherwise relating to protection of the environment. We have experienced, and expect to continue to experience, costs to comply with environmental laws and regulations. In addition, new laws and regulations, stricter enforcement of existing laws and regulations, the discovery of previously unknown contamination or the imposition of new clean-up requirements could require us to incur costs or become subject to new or increased liabilities that could have a material adverse effect on our business, financial condition, results of operations and cash flows.

3

We use and generate hazardous substances and wastes in our operations. In addition, many of our current and former properties are or have been used for industrial purposes. Accordingly, we monitor hazardous waste management and applicable environmental permitting and reporting for compliance with applicable laws at our locations in the ordinary course of our business. We may be subject to potential material liabilities relating to any investigation and clean-up of our locations or properties where we delivered hazardous waste for handling or disposal that may be contaminated or which may have been contaminated prior to our purchase, and to claims alleging personal injury.

AVAILABLE INFORMATION

Our Internet address is www.BGInc.com. Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports are available without charge on our website as soon as reasonably practicable after they are filed with, or furnished to, the U.S. Securities and Exchange Commission ("SEC"). In addition, we have posted on our website, and will make available in print to any stockholder who makes a request, our Corporate Governance Guidelines, our Code of Business Ethics and Conduct, and the charters of the Audit Committee, Compensation and Management Development Committee and Corporate Governance Committee (the responsibilities of which include serving as the nominating committee) of the Company’s Board of Directors. References to our website addressed in this Annual Report are provided as a convenience and do not constitute, and should not be viewed as, an incorporation by reference of the information contained on, or available through, the website. Therefore, such information should not be considered part of this Annual Report.

Item 1A. Risk Factors

Our business, financial condition or results of operations could be materially adversely affected by any of the following risks. Please note that additional risks not presently known to us may also materially impact our business and operations.

RISKS RELATED TO OUR BUSINESS

We depend on revenues and earnings from a small number of significant customers. Any bankruptcy of or loss of or, cancellation, reduction or delay in purchases by these customers could harm our business. In 2016, our net sales to General Electric and its subsidiaries accounted for 17% of our total sales and approximately 51% of Aerospace's net sales. Aerospace's second and third largest customers, Rolls-Royce and United Technologies Corporation and its subsidiaries, accounted for 13% and 11%, respectively, of Aerospace net sales in 2016. Approximately 10% of Aerospace's sales in 2016 were to its next four largest customers. Approximately 11% of Industrial's sales in 2016 were to its three largest customers. Some of our success will depend on the business strength and viability of those customers. We cannot assure you that we will be able to retain our largest customers. Some of our customers may in the future reduce their purchases due to economic conditions or shift their purchases from us to our competitors, in-house or to other sources. Some of our long-term sales agreements provide that until a firm order is placed by a customer for a particular product, the customer may unilaterally reduce or discontinue its projected purchases without penalty, or terminate for convenience. The loss of one or more of our largest customers, any reduction, cancellation or delay in sales to these customers (including a reduction in aftermarket volume in our RSPs), our inability to successfully develop relationships with new customers, or future price concessions we make to retain customers could significantly reduce our sales and profitability.

The global nature of our business exposes us to foreign currency fluctuations that may affect our future revenues, debt levels and profitability. We have manufacturing facilities and technical service, sales and distribution centers around the world, and the majority of our foreign operations use the local currency as their functional currency. These include, among others, the Brazilian real, British pound sterling, Canadian dollar, Chinese renminbi, Euro, Japanese yen, Korean won, Mexican peso, Singapore dollar, Swedish krona, Swiss franc and Thai baht. Since our financial statements are denominated in U.S. dollars, changes in currency exchange rates between the U.S. dollar and other currencies expose us to translation risk when the local currency financial statements are translated to U.S. dollars. Changes in currency exchange rates may also expose us to transaction risk. We may buy hedges in certain currencies to reduce or offset our exposure to currency exchange fluctuations; however, these transactions may not be adequate or effective to protect us from the exposure for which they are purchased. We have not engaged in any speculative hedging activities. Currency fluctuations may adversely impact our revenues and profitability in the future.

Our operations depend on our manufacturing, sales, and service facilities and information systems in various parts of the world which are subject to physical, financial, regulatory, environmental, operational and other risks that could disrupt our operations. We have a significant number of manufacturing facilities, technical service, and sales centers both within and outside the U.S. The global scope of our business subjects us to increased risks and uncertainties such as threats

4

of war, terrorism and instability of governments; and economic, regulatory and legal systems in countries in which we or our customers conduct business.

Customer, supplier and our facilities are located in areas that may be affected by natural disasters, including earthquakes, windstorms and floods, which could cause significant damage and disruption to the operations of those facilities and, in turn, could have a material adverse effect on our business, financial condition, results of operations and cash flows. Additionally, some of our manufacturing equipment and tooling is custom-made and is not readily replaceable. Loss of such equipment or tooling could have a negative impact on our manufacturing business, financial condition, results of operations and cash flows.

Although we have obtained property damage and business interruption insurance, a major catastrophe such as an earthquake, windstorm, flood or other natural disaster at any of our sites, or significant labor strikes, work stoppages, political unrest, or any of the events described above, in any of the areas where we conduct operations could result in a prolonged interruption of our business. Any disruption resulting from these events could cause significant delays in the manufacture or shipment of products or the provision of repair and other services that may result in our loss of sales and customers. Our insurance will not cover all potential risks, and we cannot assure you that we will have adequate insurance to compensate us for all losses that result from any insured risks. Any material loss not covered by insurance could have a material adverse effect on our financial condition, results of operations and cash flows. We cannot assure you that insurance will be available in the future at a cost acceptable to us or at a cost that will not have a material adverse effect on our profitability, net income and cash flows.

The global nature of our operations and assets subject us to additional financial and regulatory risks. We have operations and assets in various parts of the world. In addition, we sell or may in the future sell our products and services to the U.S. and foreign governments and in foreign countries. As a global business, we are subject to complex laws and regulations in the U.S. and other countries in which we operate, and associated risks, including: U.S. imposed embargoes of sales to specific countries; foreign import controls (which may be arbitrarily imposed or enforced); import regulations and duties; export regulations (which require us to comply with stringent licensing regimes); reporting requirements regarding the use of "conflict" minerals mined from certain countries; anti-dumping regulations; price and currency controls; exchange rate fluctuations; dividend remittance restrictions; expropriation of assets; war, civil uprisings and riots; government instability; government contracting requirements including cost accounting standards, including various procurement, security, and audit requirements, as well as requirements to certify to the government compliance with these requirements; the necessity of obtaining governmental approval for new and continuing products and operations; and legal systems or decrees, laws, taxes, regulations, interpretations and court decisions that are not always fully developed and that may be retroactively or arbitrarily applied. We have experienced inadvertent violations of some of these regulations, including export regulations, safety and environmental regulations, regulations prohibiting sales of certain products and product labeling regulations, in the past, none of which has had or, we believe, will have a material adverse effect on our business. However, any significant violations of these or other regulations in the future could result in civil or criminal sanctions, and the loss of export or other licenses which could have a material adverse effect on our business. We are subject to federal and state unclaimed property laws in the ordinary course of business, and are currently undergoing a multi-state unclaimed property audit, the timing and outcome of which cannot be predicted, and we may incur significant professional fees in conjunction with the audit. We may also be subject to unanticipated income taxes, excise duties, import taxes, export taxes, value added taxes, or other governmental assessments, and taxes may be impacted by changes in legislation in the tax jurisdictions in which we operate. In addition, our organizational and capital structure may limit our ability to transfer funds between countries, particularly into the U.S., without incurring adverse tax consequences. Any of these events could result in a loss of business or other unexpected costs that could reduce sales or profits and have a material adverse effect on our financial condition, results of operations and cash flows.

Any disruption or failure in the operation of our information systems, including from conversions or integrations of information technology or reporting systems, could have a material adverse effect on our business, financial condition, results of operations and cash flows. Our information technology (IT) systems are an integral part of our business. We depend upon our IT systems to help process orders, manage inventory, make payments and collect accounts receivable. Our IT systems also allow us to purchase, sell and ship products efficiently and on a timely basis, to maintain cost-effective operations, and to help provide superior service to our customers. We are currently in the process of implementing enterprise resource planning (ERP) platforms across certain of our businesses, and we expect that we will need to continue to improve and further integrate our IT systems, on an ongoing basis in order to effectively run our business. If we fail to successfully manage and integrate our IT systems, including these ERP platforms, it could adversely affect our business or operating results.

Further, in the ordinary course of our business, we store sensitive data, including intellectual property, our proprietary business information and that of our customers, suppliers and business partners, and personally identifiable information of our employees, in our data centers and on our networks. The secure maintenance and transmission of this information is critical to our business operations. Despite our security measures, our information technology and infrastructure may be vulnerable to attacks by hackers

5

or breached due to employee error, malfeasance or other disruptions. Any such breach could compromise our networks and the information stored there could be accessed, publicly disclosed, lost or stolen. Any such access, disclosure or other loss of information could result in legal claims or proceedings, liability under laws that protect the privacy of personal information, and regulatory penalties, disrupt our operations, and damage our reputation, which could adversely affect our business, revenues and competitive position.

We have significant indebtedness that could affect our operations and financial condition, and our failure to meet certain financial covenants required by our debt agreements may materially and adversely affect our assets, financial position and cash flows. At December 31, 2016, we had consolidated debt obligations of $501.0 million, representing approximately 30% of our total capital (indebtedness plus stockholders’ equity) as of that date. Our level of indebtedness, proportion of variable rate debt obligations and the significant debt servicing costs associated with that indebtedness may adversely affect our operations and financial condition. For example, our indebtedness could require us to dedicate a substantial portion of our cash flows from operations to payments on our debt, thereby reducing the amount of our cash flows available for working capital, capital expenditures, investments in technology and research and development, acquisitions, dividends and other general corporate purposes; limit our flexibility in planning for, or reacting to, changes in the industries in which we compete; place us at a competitive disadvantage compared to our competitors, some of whom have lower debt service obligations and greater financial resources than we do; limit our ability to borrow additional funds; or increase our vulnerability to general adverse economic and industry conditions. In addition, a majority of our debt arrangements require us to maintain certain debt and interest coverage ratios and limit our ability to incur debt, make investments or undertake certain other business activities. These requirements could limit our ability to obtain future financing and may prevent us from taking advantage of attractive business opportunities. Our ability to meet the financial covenants or requirements in our debt arrangements may be affected by events beyond our control, and we cannot assure you that we will satisfy such covenants and requirements. A breach of these covenants or our inability to comply with the restrictions could result in an event of default under our debt arrangements which, in turn, could result in an event of default under the terms of our other indebtedness. Upon the occurrence of an event of default under our debt arrangements, after the expiration of any grace periods, our lenders could elect to declare all amounts outstanding under our debt arrangements, together with accrued interest, to be immediately due and payable. If this were to happen, we cannot assure you that our assets would be sufficient to repay in full the payments due under those arrangements or our other indebtedness or that we could find alternative financing to replace that indebtedness.

Conditions in the worldwide credit markets may limit our ability to expand our credit lines beyond current bank commitments. In addition, our profitability may be adversely affected as a result of increases in interest rates. At December 31, 2016, we and our subsidiaries had $501.0 million aggregate principal amount of consolidated debt obligations outstanding, of which approximately 59% had interest rates that float with the market (not hedged against interest rate fluctuations). A 100 basis point increase in the interest rate on the floating rate debt in effect at December 31, 2016 would result in an approximate $3.0 million annualized increase in interest expense.

Changes in the availability or price of materials, products and energy resources could adversely affect our costs and profitability. We may be adversely affected by the availability or price of raw materials, products and energy resources, particularly related to certain manufacturing operations that utilize steel, stainless steel, titanium, Inconel, Hastelloys and other specialty materials. The availability and price of raw materials and energy resources may be subject to curtailment or change due to, among other things, new laws or regulations, global economic or political events including strikes, terrorist attacks and war, suppliers’ allocations to other purchasers, interruptions in production by suppliers, changes in exchange rates and prevailing price levels. In some instances there are limited sources for raw materials and a limited number of primary suppliers for some of our products for resale. Although we are not dependent upon any single source for any of our principal raw materials or products for resale, and such materials and products have, historically, been readily available, we cannot assure you that such raw materials and products will continue to be readily available. Disruption in the supply of raw materials, products or energy resources or our inability to come to favorable agreements with our suppliers could impair our ability to manufacture, sell and deliver our products and require us to pay higher prices. Any increase in prices for such raw materials, products or energy resources could materially adversely affect our costs and our profitability.

We maintain pension and other postretirement benefit plans in the U.S. and certain international locations. Our costs of providing defined benefit plans are dependent upon a number of factors, such as the rates of return on the plans’ assets, exchange rate fluctuations, future governmental regulation, global fixed income and equity prices, and our required and/or voluntary contributions to the plans. Declines in the stock market, prevailing interest rates, declines in discount rates, improvements in mortality rates and rising medical costs may cause an increase in our pension and other postretirement benefit expenses in the future and result in reductions in our pension fund asset values and increases in our pension and other postretirement benefit obligations. These changes have caused and may continue to cause a significant reduction in our net worth and without sustained growth in the pension investments over time to increase the value of the plans’ assets, and

6

depending upon the other factors listed above, we could be required to increase funding for some or all of these pension and postretirement plans.

We carry significant inventories and a loss in net realizable value could cause a decline in our net worth. At December 31, 2016, our inventories totaled $227.8 million. Inventories are valued at the lower of cost or market based on management's judgments and estimates concerning future sales levels, quantities and prices at which such inventories will be sold in the normal course of business. Accelerating the disposal process or incorrect estimates of future sales potential may necessitate future reduction to inventory values. See “Part II - Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations - Critical Accounting Policies”.

We have significant goodwill and an impairment of our goodwill could cause a decline in our net worth. Our total assets include substantial goodwill. At December 31, 2016, our goodwill totaled $633.4 million. The goodwill results from our prior acquisitions, representing the excess of the purchase price we paid over the net assets of the companies acquired. We assess whether there has been an impairment in the value of our goodwill during each calendar year or sooner if triggering events warrant. If future operating performance at one or more of our reporting units does not meet expectations or fair values fall due to significant stock market declines, we may be required to reflect a non-cash charge to operating results for goodwill impairment. The recognition of an impairment of a significant portion of goodwill would negatively affect our results of operations and total capitalization, the effect of which could be material. See “Part II - Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations - Critical Accounting Policies”.

We may not realize all of the sales expected from our existing backlog or anticipated orders. At December 31, 2016, we had $885.5 million of order backlog, the majority of which related to aerospace OEM customers. There can be no assurances that the revenues projected in our backlog will be realized or, if realized, will result in profits. We consider backlog to be firm customer orders for future delivery. OEM customers may provide projections of components and assemblies that they anticipate purchasing in the future under new and existing programs. Such projections are included in our backlog when they are supported by a long term agreement. Our customers may have the right under certain circumstances or with certain penalties or consequences to terminate, reduce or defer firm orders that we have in backlog. If our customers terminate, reduce or defer firm orders, we may be protected from certain costs and losses, but our sales will nevertheless be adversely affected. Although we strive to maintain ongoing relationships with our customers, there is an ongoing risk that orders may be canceled or rescheduled due to fluctuations in our customers’ business needs or purchasing budgets.

Also, our realization of sales from new and existing programs is inherently subject to a number of important risks and uncertainties, including whether our customers execute the launch of product programs on time, or at all, the number of units that our customers actually produce, the timing of production and manufacturing insourcing decisions made by our customers. In addition, until firm orders are placed, our customers may have the right to discontinue a program or replace us with another supplier at any time without penalty. Our failure to realize sales from new and existing programs could have a material adverse effect on our net sales, results of operations and cash flows.

We may not recover all of our up-front costs related to new or existing programs. New programs may require significant up-front investments for capital equipment, engineering, inventory, design and tooling. As OEMs in the transportation and aerospace industries have looked to suppliers to bear increasing responsibility for the design, engineering and manufacture of systems and components, they have increasingly shifted the financial risk associated with those responsibilities to the suppliers as well. This trend may continue and is most evident in the area of engineering cost reimbursement. We cannot assure you that we will have adequate funds to make such up-front investments or to recover such costs from our customers as part of our product pricing. In the event that we are unable to make such investments, or to recover them through sales or direct reimbursement from our customers, our profitability, liquidity and cash flows may be adversely affected. In addition, we incur costs and make capital expenditures for new program awards based upon certain estimates of production volumes and production complexity. While we attempt to recover such costs and capital expenditures by appropriately pricing our products, the prices of our products are based in part upon planned production volumes. If the actual production is significantly less than planned or significantly more complex than anticipated, we may be unable to recover such costs. In addition, because a significant portion of our overall costs is fixed, declines in our customers’ production levels can adversely affect the level of our reported profits even if our up-front investments are recovered.

We may not realize all of the intangible assets related to the Aerospace aftermarket businesses. We participate in aftermarket Revenue Sharing Programs ("RSPs") under which we receive an exclusive right to supply designated aftermarket parts over the life of the related aircraft engine program to our customer, General Electric. As consideration, we pay participation fees, which are recorded as intangible assets and are recognized as a reduction of sales over the estimated life of the related engine programs which range up to 30 years. Our total investments in participation fees under our RSPs as of

7

December 31, 2016 equaled $293.7 million, all of which have been paid. At December 31, 2016, the remaining unamortized balance of these participation fees was $198.0 million.

We entered into Component Repair Programs ("CRPs"), also with General Electric ("GE"), during the fourth quarter of 2013 ("CRP 1"), the second quarter of 2014 ("CRP 2") and the fourth quarter of 2015 ("CRP 3" and, collectively with CRP 1 and CRP 2, the "CRPs"). The CRPs provide for, among other items, the right to sell certain aftermarket component repair services for CFM56, CF6, CF34 and LM engines directly to other customers as one of a few GE licensed suppliers. In addition, the CRPs extend certain existing contracts under which the Company currently provides these services directly to GE.

We agreed to pay $26.6 million as consideration for the rights related to CRP 1. Of this balance, we paid $16.6 million in the fourth quarter of 2013, $9.1 million in the fourth quarter of 2014 and $0.9 million in the first quarter of 2016. We agreed to pay $80.0 million as consideration for the rights related to CRP 2. We paid $41.0 million in the second quarter of 2014, $20.0 million in the fourth quarter of 2014 and $19.0 million in the second quarter of 2015. We agreed to pay $5.2 million as consideration for the rights related to CRP 3. We paid $2.0 million in the fourth quarter of 2015 and $3.2 million was paid in December 2016. We recorded the CRP payments as an intangible asset which is recognized as a reduction of sales over the remaining useful life of these engine programs.

The realizability of each asset is dependent upon future revenues related to the programs' aftermarket parts and services and is subject to impairment testing if circumstances indicate that its carrying amount may not be recoverable. The potential exists that actual revenues will not meet expectations due to a change in market conditions, including, for example, the replacement of older engines with new, more fuel-efficient engines or our ability to maintain market share within the aftermarket business. A shortfall in future revenues may result in the failure to realize the net amount of the investments, which could adversely affect our financial condition and results of operations. In addition, profitability could be impacted by the amortization of the participation fees and licenses, and the expiration of the international tax incentives on these programs. See “Part II - Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations - Critical Accounting Policies”.

We face risks of cost overruns and losses on fixed-price contracts. We sell certain of our products under firm, fixed-price contracts providing for a fixed price for the products regardless of the production or purchase costs incurred by us. The cost of producing products may be adversely affected by increases in the cost of labor, materials, fuel, outside processing, overhead and other factors, including manufacturing inefficiencies. Increased production costs may result in cost overruns and losses on contracts.

The departure of existing management and key personnel, a shortage of skilled employees or a lack of qualified sales professionals could materially affect our business, operations and prospects. Our executive officers are important to the management and direction of our business. Our future success depends, in large part, on our ability to retain or replace these officers and other capable management personnel. Although we believe we will be able to attract and retain talented personnel and replace key personnel should the need arise, our inability to do so could have a material adverse effect on our business, financial condition, results of operations or cash flows. Because of the complex nature of many of our products and services, we are generally dependent on an educated and highly skilled workforce, including, for example, our engineering talent. In addition, there are significant costs associated with the hiring and training of sales professionals. We could be adversely affected by a shortage of available skilled employees or the loss of a significant number of our sales professionals.

If we are unable to protect our intellectual property rights effectively, our financial condition and results of operations could be adversely affected. We own or are licensed under various intellectual property rights, including patents, trademarks and trade secrets. Our intellectual property rights may not be sufficiently broad or otherwise may not provide us a significant competitive advantage, and patents may not be issued for pending or future patent applications owned by or licensed to us. In addition, the steps that we have taken to maintain and protect our intellectual property may not prevent it from being challenged, invalidated, circumvented or designed-around, particularly in countries where intellectual property rights are not highly developed or protected. In some circumstances, enforcement may not be available to us because an infringer has a dominant intellectual property position or for other business reasons, or countries may require compulsory licensing of our intellectual property. We also rely on nondisclosure and noncompetition agreements with employees, consultants and other parties to protect, in part, confidential information, trade secrets and other proprietary rights. There can be no assurance that these agreements will adequately protect these intangible assets and will not be breached, that we will have adequate remedies for any breach, or that others will not independently develop substantially equivalent proprietary information. Our failure to obtain or maintain intellectual property rights that convey competitive advantage, adequately protect our intellectual property or detect or prevent circumvention or unauthorized use of such property and the cost of enforcing our intellectual property rights could adversely impact our competitive position, financial condition and results of operations.

8

Any product liability, warranty, contractual or other claims in excess of insurance may adversely affect our financial condition. Our operations expose us to potential product liability risks that are inherent in the design, manufacture and sale of our products and the products we buy from third parties and sell to our customers, or to potential warranty, contractual or other claims. For example, we may be exposed to potential liability for personal injury, property damage or death as a result of the failure of an aircraft component designed, manufactured or sold by us, or the failure of an aircraft component that has been serviced by us or of the components themselves. While we have liability insurance for certain risks, our insurance may not cover all liabilities. Additionally, insurance coverage may not be available in the future at a cost acceptable to us. Any material liability not covered by insurance or for which third-party indemnification is not available for the full amount of the loss could have a material adverse effect on our financial condition, results of operations and cash flows.

From time to time, we receive product warranty claims, under which we may be required to bear costs of repair or replacement of certain of our products. Warranty claims may range from individual customer claims to full recalls of all products in the field. We vigorously defend ourselves in connection with these matters. We cannot, however, assure you that the costs, charges and liabilities associated with these matters will not be material, or that those costs, charges and liabilities will not exceed any amounts reserved for them in our consolidated financial statements.

Our business, financial condition, results of operations and cash flows could be adversely impacted by strikes or work stoppages. Approximately 16% of our U.S. employees are covered by collective bargaining agreements and more than 37% of our non-U.S. employees are covered by collective bargaining agreements or statutory trade union agreements. The Company has a national collective bargaining agreement (“CBA”) with certain unionized employees at the Bristol, Connecticut and Corry, Pennsylvania facilities of the Associated Spring business unit, covering approximately 250 employees. The current CBA will expire in August 2017, at which time we will negotiate a successor agreement. The local collective bargaining agreement for the Milwaukee, Wisconsin facility of the Associated Spring business unit will expire on June 30, 2017, at which time we will negotiate a successor agreement. In addition, we have annual negotiations in Brazil and Mexico and, collectively, these negotiations cover approximately 300 employees in those two countries. In 2016, we also completed negotiations resulting in wage increases at four locations in our Industrial segment and one location in our Aerospace segment, collectively covering a total of approximately 900 employees.

Although we believe that our relations with our employees are good, we cannot assure you that we will be successful in negotiating new collective bargaining agreements or that such negotiations will not result in significant increases in the cost of labor, including healthcare, pensions or other benefits. Any potential strikes or work stoppages, and the resulting adverse impact on our relationships with customers, could have a material adverse effect on our business, financial condition, results of operations or cash flows. Similarly, a protracted strike or work stoppage at any of our major customers, suppliers or other vendors could materially adversely affect our business.

Changes in taxation requirements could affect our financial results. Our products are subject to import and excise duties and/or sales or value-added taxes in many jurisdictions in which we operate. Increases in indirect taxes could affect our products’ affordability and therefore reduce our sales. We are also subject to income tax in numerous jurisdictions in which we generate revenues. Changes in tax laws, tax rates or tax rulings may have a significant adverse impact on our effective tax rate. Among other things, our tax liabilities are affected by the mix of pretax income or loss among the tax jurisdictions in which we operate and the repatriation of foreign earnings to the U.S. Further, during the ordinary course of business, we are subject to examination by the various tax authorities of the jurisdictions in which we operate which could result in an unanticipated increase in taxes. Potential tax reform discussed by the new U.S. administration, such as reducing the corporate income tax rate or changing the repatriation and taxation of foreign earnings, may impact income tax expenses, deferred tax assets in the U.S. and tax liability balances.

Changes in accounting guidance could affect our financial results. New accounting guidance that may become applicable to us from time to time, or changes in the interpretations of existing guidance, could have a significant effect on our reported results for the affected periods. For example, the Financial Accounting Standards Board issued a new accounting standard for revenue recognition in May 2014 - Accounting Standards Update (ASU) 2014-09, "Revenue from Contracts with Customers (Topic 606)". Although we are currently in the process of evaluating the impact of ASU 2014-09 on our consolidated financial statements, it is expected to change the way we account for certain of our sales transactions and reported backlog. Adoption of the standard could have a material impact on our financial statements and may retroactively affect the accounting treatment of transactions completed before adoption. See “Part II - Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations - Other Matters” for additional disclosure related to the Company's planned adoption of Topic 606.

9

RISKS RELATED TO THE INDUSTRIES IN WHICH WE OPERATE

We operate in highly competitive markets. We may not be able to compete effectively with our competitors, and competitive pressures could adversely affect our business, financial condition and results of operations. Our two global business segments compete with a number of larger and smaller companies in the markets we serve. Some of our competitors have greater financial, production, research and development, or other resources than we do. Within Aerospace, certain of our OEM customers compete with our repair and overhaul business. Some of our OEM customers in the aerospace industry also compete with us where they have the ability to manufacture the components and assemblies that we supply to them but have chosen, for capacity limitations, cost considerations or other reasons, to outsource the manufacturing to us. Our customers award business based on, among other things, price, quality, reliability of supply, service, technology and design. Our competitors’ efforts to grow market share could exert downward pressure on our product pricing and margins. Our competitors may also develop products or services, or methods of delivering those products or services that are superior to our products, services or methods. Our competitors may adapt more quickly than us to new technologies or evolving customer requirements. We cannot assure you that we will be able to compete successfully with our existing or future competitors. Our ability to compete successfully will depend, in part, on our ability to continue make investments to innovate and manufacture the types of products demanded by our customers, and to reduce costs by such means as reducing excess capacity, leveraging global purchasing, improving productivity, eliminating redundancies and increasing production in low-cost countries. We have invested, and expect to continue to invest, in increasing our manufacturing footprint in low-cost countries. We cannot assure you that we will have sufficient resources to continue to make such investments or that we will be successful in maintaining our competitive position. If we are unable to differentiate our products or maintain a low-cost footprint, we may lose market share or be forced to reduce prices, thereby lowering our margins. Any such occurrences could adversely affect our financial condition, results of operations and cash flows.

The industries in which we operate have been experiencing consolidation, both in our suppliers and the customers we serve. Supplier consolidation is in part attributable to OEMs more frequently awarding long-term sole source or preferred supplier contracts to the most capable suppliers in an effort to reduce the total number of suppliers from whom components and systems are purchased. If consolidation of our existing competitors occurs, we would expect the competitive pressures we face to increase, and we cannot assure you that our business, financial condition, results of operations or cash flows will not be adversely impacted as a result of consolidation by our competitors or customers.

Original equipment manufacturers in the aerospace and transportation industries have significant pricing leverage over suppliers and may be able to achieve price reductions over time. Additionally, we may not be successful in our efforts to raise prices on our customers. There is substantial and continuing pressure from OEMs in the transportation industries, including automotive and aerospace, to reduce the prices they pay to suppliers. We attempt to manage such downward pricing pressure, while trying to preserve our business relationships with our customers, by seeking to reduce our production costs through various measures, including purchasing raw materials and components at lower prices and implementing cost-effective process improvements. Our suppliers have periodically resisted, and in the future may resist, pressure to lower their prices and may seek to impose price increases. If we are unable to offset OEM price reductions, our profitability and cash flows could be adversely affected. In addition, OEMs have substantial leverage in setting purchasing and payment terms, including the terms of accelerated payment programs under which payments are made prior to the account due date in return for an early payment discount. OEMs can unexpectedly change their purchasing policies or payment practices, which could have a negative impact on our short-term working capital.

Demand for our defense-related products depends on government spending. A portion of Aerospace's sales is derived from the military market, including single-sourced and dual-sourced sales. The military market is largely dependent upon government budgets and is subject to governmental appropriations. Although multi-year contracts may be authorized in connection with major procurements, funds are generally appropriated on a fiscal year basis even though a program may be expected to continue for several years. Consequently, programs are often only partially funded and additional funds are committed only as further appropriations are made. We cannot assure you that maintenance of or increases in defense spending will be allocated to programs that would benefit our business. Moreover, we cannot assure you that new military aircraft programs in which we participate will enter full-scale production as expected. A decrease in levels of defense spending or the government’s termination of, or failure to fully fund, one or more of the contracts for the programs in which we participate could have a material adverse effect on our financial position and results of operations.

The aerospace industry is highly regulated. Complications related to aerospace regulations may adversely affect the Company. A substantial portion of our income is derived from our aerospace businesses. The aerospace industry is highly regulated in the U.S. by the Federal Aviation Administration, or FAA, and in other countries by similar regulatory agencies. We must be certified by these agencies and, in some cases, by individual OEMs in order to engineer and service systems and components used in specific aircraft models. If material authorizations or approvals were delayed, revoked or suspended, our

10

business could be adversely affected. New or more stringent governmental regulations may be adopted, or industry oversight heightened, in the future, and we may incur significant expenses to comply with any new regulations or any heightened industry oversight.

Fluctuations in jet fuel and other energy prices may impact our operating results. Fuel costs constitute a significant portion of operating expenses for companies in the aerospace industry. Fluctuations in fuel costs could impact levels and frequency of aircraft maintenance and overhaul activities, and airlines' decisions on maintaining, deferring or canceling new aircraft purchases, in part based on the value associated with new fuel efficient technologies. Widespread disruption to oil production, refinery operations and pipeline capacity in certain areas of the U.S. can impact the price of jet fuel significantly. Conflicts in the Middle East, an important source of oil for the U.S. and other countries where we do business, cause prices for fuel to be volatile. Because we and many of our customers are in the aerospace industry, these fluctuations could have a material adverse effect on our financial condition or results of operations.

Our products and services may be rendered obsolete by new products, technologies and processes. Our manufacturing operations focus on highly engineered components which require extensive engineering and research and development time. Our competitive advantage may be adversely impacted if we cannot continue to introduce new products ahead of our competition, or if our products are rendered obsolete by other products or by new, different technologies and processes. The success of our new products will depend on a number of factors, including innovation, customer acceptance, the efficiency of our suppliers in providing materials and component parts, and the performance and quality of our products relative to those of our competitors. We cannot predict the level of market acceptance or the amount of market share our new products will achieve. Additionally, we may face increased or unexpected costs associated with new product introduction including the use of additional resources such as personnel. We cannot assure that we will not experience new product introduction delays in the future.

RISKS RELATED TO RESTRUCTURING, ACQUISITIONS, JOINT VENTURES AND DIVESTITURES

Our restructuring actions could have long-term adverse effects on our business. From time to time, we have implemented restructuring activities across our businesses to adjust our cost structure, and we may engage in similar restructuring activities in the future. We may not achieve expected cost savings from workforce reductions or restructuring activities and actual charges, costs and adjustments due to these actions may vary materially from our estimates. Our ability to realize anticipated cost savings, synergies and revenue enhancements may be affected by a number of factors, including the following: our ability to effectively eliminate duplicative back office overhead and overlapping sales personnel, rationalize manufacturing capacity, synchronize information technology systems, consolidate warehousing and other facilities and shift production to more economical facilities; significant cash and non-cash integration and implementation costs or charges in order to achieve those cost savings, which could offset any such savings and other synergies resulting from our acquisitions or divestitures; and our ability to avoid labor disruption in connection with these activities. In addition, delays in implementing planned restructuring activities or other productivity improvements may diminish the expected operational or financial benefits.

Our acquisition and other strategic initiatives may not be successful. We have made a number of acquisitions in the past, including most recently the acquisition of the FOBOHA business, and we anticipate that we may, from time to time, acquire additional businesses, assets or securities of companies, and enter into joint ventures and other strategic relationships that we believe would provide a strategic fit with our businesses. These activities expose the Company to a number of risks and uncertainties, the occurrence of any of which could materially adversely affect our business, cash flows, financial condition and results of operations. A portion of the industries that we serve are mature industries. As a result, our future growth may depend in part on the successful acquisition and integration of acquired businesses into our existing operations. We may not be able to identify and successfully negotiate suitable acquisitions, obtain financing for future acquisitions on satisfactory terms, obtain regulatory approvals or otherwise complete acquisitions in the future.

We could have difficulties integrating acquired businesses with our existing operations. Difficulties of integration can include coordinating and consolidating separate systems, integrating the management of the acquired business, retaining market acceptance of acquired products and services, maintaining employee morale and retaining key employees, and implementing our enterprise resource planning systems and operational procedures and disciplines. Any such difficulties may make it more difficult to maintain relationships with employees, customers, business partners and suppliers. In addition, even if integration is successful, the financial performance of acquired business may not be as expected and there can be no assurance we will realize anticipated benefits from our acquisitions. We cannot assure you that we will effectively assimilate the business or product offerings of acquired companies into our business or product offerings or realize anticipated operational synergies. In connection with the integration of acquired operations or the conduct of our overall business strategies, we may periodically restructure our businesses and/or sell assets or portions of our business. Integrating the operations and personnel of acquired

11

companies into our existing operations may result in difficulties, significant expense and accounting charges, disrupt our business or divert management’s time and attention.

Acquisitions involve numerous other risks, including potential exposure to unknown liabilities of acquired companies and the possible loss of key employees and customers of the acquired business. Certain of the acquisition agreements by which we have acquired businesses require the former owners to indemnify us against certain liabilities related to the business operations before we acquired it. However, the liability of the former owners is limited and certain former owners may be unable to meet their indemnification responsibilities. We cannot assure you that these indemnification provisions will protect us fully or at all, and as a result we may face unexpected liabilities that adversely affect our financial condition. In connection with acquisitions or joint venture investments outside the U.S., we may enter into derivative contracts to purchase foreign currency in order to hedge against the risk of foreign currency fluctuations in connection with such acquisitions or joint venture investments, which subjects us to the risk of foreign currency fluctuations associated with such derivative contracts. Additionally, our final determinations and appraisals of the fair value of assets acquired and liabilities assumed in our acquisitions may vary materially from earlier estimates. We cannot assure you that the fair value of acquired businesses will remain constant.

We continually assess the strategic fit of our existing businesses and may divest or otherwise dispose of businesses that are deemed not to fit with our strategic plan or are not achieving the desired return on investment, and we cannot be certain that our business, operating results and financial condition will not be materially and adversely affected. A successful divestiture depends on various factors, including our ability to effectively transfer liabilities, contracts, facilities and employees to any purchaser, identify and separate the intellectual property to be divested from the intellectual property that we wish to retain, reduce fixed costs previously associated with the divested assets or business, and collect the proceeds from any divestitures. In addition, if customers of the divested business do not receive the same level of service from the new owners, this may adversely affect our other businesses to the extent that these customers also purchase other products offered by us. All of these efforts require varying levels of management resources, which may divert our attention from other business operations. If we do not realize the expected benefits or synergies of any divestiture transaction, our consolidated financial position, results of operations and cash flows could be negatively impacted. In addition, divestitures of businesses involve a number of risks, including significant costs and expenses, the loss of customer relationships, and a decrease in revenues and earnings associated with the divested business. Furthermore, divestitures potentially involve significant post-closing separation activities, which could involve the expenditure of material financial resources and significant employee resources. Any divestiture may result in a dilutive impact to our future earnings if we are unable to offset the dilutive impact from the loss of revenue associated with the divestiture, as well as significant write-offs, including those related to goodwill and other intangible assets, which could have a material adverse effect on our results of operations and financial condition.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

Number of Facilities - Owned | ||||||||

Location | Industrial | Aerospace | Other | Total | ||||

Manufacturing: | ||||||||

North America | 6 | 5 | 0 | 11 | ||||

Europe | 9 | 0 | 0 | 9 | ||||

Asia | 1 | 0 | 0 | 1 | ||||

Central and Latin America | 2 | 0 | 0 | 2 | ||||

18 | 5 | 0 | 23 | |||||

Non-Manufacturing: | ||||||||

North America | 0 | 0 | 1* | 1 | ||||

Europe | 2 | 0 | 0 | 2 | ||||

2 | 0 | 1 | 3 | |||||

* The Company's Corporate office

12

Number of Facilities - Leased | ||||||||

Location | Industrial | Aerospace | Other | Total | ||||

Manufacturing: | ||||||||

North America | 2 | 2 | 0 | 4 | ||||

Europe | 3 | 0 | 0 | 3 | ||||

Asia | 5 | 5 | 0 | 10 | ||||

10 | 7 | 0 | 17 | |||||

Non-Manufacturing: | ||||||||

North America | 8 | 2 | 1** | 11 | ||||

Europe | 13 | 1 | 0 | 14 | ||||

Asia | 22 | 0 | 0 | 22 | ||||

Central and Latin America | 4 | 0 | 0 | 4 | ||||

47 | 3 | 1 | 51 | |||||

** Industrial segment headquarters and certain Shared Services groups.

13

Item 3. Legal Proceedings

In November 2016, the Company’s previously disclosed arbitration with Triumph Actuation Systems - Yakima, LLC ("Triumph") was concluded. The Company was awarded $9.2 million, plus interest on the judgment of $1.4 million, which amounts were received on January 3, 2017. The outcome did not have a material impact on the Company's consolidated financial position, liquidity or consolidated results of operations.

In addition, we are subject to litigation from time to time in the ordinary course of business and various other suits, proceedings and claims are pending against us and our subsidiaries. While it is not possible to determine the ultimate disposition of each of these proceedings and whether they will be resolved consistent with our beliefs, we expect that the outcome of such proceedings, individually or in the aggregate, will not have a material adverse effect on our financial condition or results of operations.

Item 4. Mine Safety Disclosures

Not applicable.

14

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

(a) | Market Information |

The Company’s common stock is traded on the New York Stock Exchange under the symbol “B”. The following table sets forth, for the periods indicated, the low and high sales intra-day trading price per share, as reported by the New York Stock Exchange, and dividends declared and paid.

2016 | ||||||||||||

Low | High | Dividends | ||||||||||

Quarter ended March 31 | $ | 30.07 | $ | 35.81 | $ | 0.12 | ||||||

Quarter ended June 30 | 31.13 | 37.75 | 0.13 | |||||||||

Quarter ended September 30 | 32.55 | 41.86 | 0.13 | |||||||||

Quarter ended December 31 | 37.88 | 49.90 | 0.13 | |||||||||

2015 | ||||||||||||

Low | High | Dividends | ||||||||||

Quarter ended March 31 | $ | 33.75 | $ | 41.00 | $ | 0.12 | ||||||

Quarter ended June 30 | 38.75 | 41.74 | 0.12 | |||||||||

Quarter ended September 30 | 35.33 | 41.78 | 0.12 | |||||||||

Quarter ended December 31 | 33.00 | 39.74 | 0.12 | |||||||||

Stockholders

As of February 14, 2017, there were approximately 3,239 holders of record of the Company’s common stock. A significant number of the outstanding shares of common stock which are beneficially owned by individuals or entities are registered in the name of a nominee of The Depository Trust Company, a securities depository for banks and brokerage firms. The Company believes that there are approximately 18,774 beneficial owners of its common stock.

Dividends

Payment of future dividends will depend upon the Company’s financial condition, results of operations and other factors deemed relevant by the Company’s Board of Directors, as well as any limitations resulting from financial covenants under the Company’s credit facilities or debt indentures. See the table above for dividend information for 2016 and 2015.

Securities Authorized for Issuance Under Equity Compensation Plans

For information regarding Securities Authorized for Issuance Under Equity Compensation Plans, see Part III, Item 12 of this Annual Report.

15

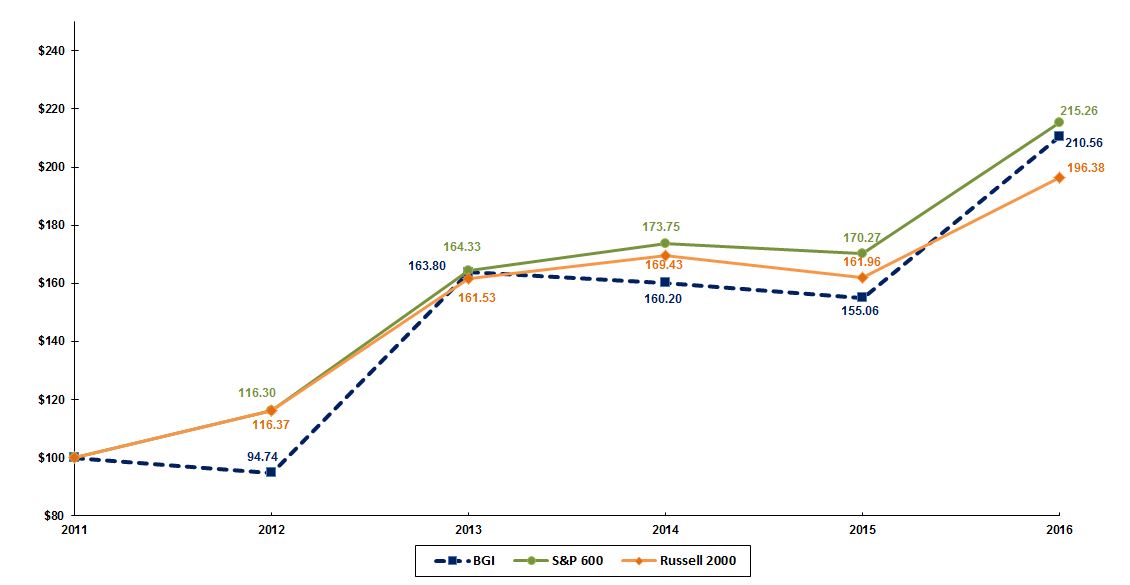

Performance Graph

A stock performance graph based on cumulative total returns (price change plus reinvested dividends) for $100 invested in Barnes Group, Inc. ("BGI") on December 31, 2011 is set forth below.

2011 | 2012 | 2013 | 2014 | 2015 | 2016 | |||||||

BGI | $100.00 | $94.74 | $163.80 | $160.20 | $155.06 | $210.56 | ||||||

S&P 600 | $100.00 | $116.30 | $164.33 | $173.75 | $170.27 | $215.26 | ||||||