Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(mark one)

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2016

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 001-35007

Swift Transportation Company

(Exact name of registrant as specified in its charter)

Delaware | 20-5589597 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

2200 South 75th Avenue

Phoenix, AZ 85043

(Address of principal executive offices and Zip Code)

(602) 269-9700

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Class A Common Stock, par value $0.01 per share | New York Stock Exchange |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ý | Accelerated filer | ¨ | |||

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

As of June 30, 2016, the aggregate market value of our Class A common stock held by non-affiliates was $1,248,343,682, based on the closing price of our common stock as quoted on the NYSE as of such date.

There were 83,322,456 shares of the registrant's Class A Common Stock and 49,741,938 shares of the registrant's Class B Common Stock outstanding as of February 6, 2017.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive proxy statement for its 2017 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission (the "SEC") are incorporated by reference into Part III of this report.

SWIFT TRANSPORTATION COMPANY

2016 ANNUAL REPORT ON FORM 10-K |

TABLE OF CONTENTS | |

PAGE | |

1

2016 ANNUAL REPORT ON FORM 10-K | ||

GLOSSARY OF TERMS | ||

The following glossary provides definitions for certain acronyms and terms used in this Annual Report on Form 10-K. These acronyms and terms are specific to our company, commonly used in our industry, or are otherwise frequently used throughout our document. | ||

Term | Definition | |

Swift/the Company/Management/We/Us/Our | Unless otherwise indicated or the context otherwise requires, these terms represent Swift Transportation Company and its subsidiaries. Swift Transportation Company is the holding company for Swift Transportation Co., LLC (a Delaware limited liability company) and Interstate Equipment Leasing, LLC. | |

2007 Stock Plan | The Company's 2007 Omnibus Incentive Plan, as amended and restated. | |

2007 Transactions | In April 2007, Jerry Moyes and his wife contributed their ownership of all of the issued and outstanding shares of IEL to Swift Corporation in exchange for additional Swift Corporation shares. In May 2007, the Moyes Affiliates, contributed their shares of Swift Transportation Co., Inc. common stock to Swift Corporation in exchange for additional Swift Corporation shares. Swift Corporation then completed its acquisition of Swift Transportation Co., Inc. through a merger on May 10, 2007, thereby acquiring the remaining outstanding shares of Swift Transportation Co., Inc. common stock. Upon completion of the 2007 Transactions, Swift Transportation Co., Inc. became a wholly-owned subsidiary of Swift Corporation. At the close of the market on May 10, 2007, the common stock of Swift Transportation Co., Inc. ceased trading on NASDAQ. | |

2012 Agreement | The Company's previous credit agreement, replaced by the 2013 Agreement. | |

2012 ESPP | Employee Stock Purchase Plan, effective beginning in 2012. | |

2013 Agreement | The Company's Second Amended and Restated Credit Agreement, replaced by the 2014 Agreement. | |

2013 RSA | Second Amended and Restated Receivables Sale Agreement, entered into in 2013 by SRCII (defined below), with unrelated financial entities, "The Purchasers." The 2013 RSA was later replaced by the 2015 RSA. | |

2014 Agreement | The Company's Third Amended and Restated Credit Agreement, replaced by the 2015 Agreement. | |

2014 Stock Plan | The Company's 2014 Omnibus Incentive Plan. | |

2015 Agreement | The Company's Fourth Amended and Restated Credit Agreement. | |

2015 RSA | Third Amendment to Amended and Restated Receivables Sale Agreement, entered into in 2015 by SRCII (defined below), with unrelated financial entities, "The Purchasers." | |

AOCI | Accumulated Other Comprehensive Income (Loss) | |

ASC | Accounting Standards Codification | |

ASU | Accounting Standards Update | |

BASICs | Behavioral Analysis and Safety Improvement Categories - part of the new enforcement and compliance model introduced by the FMCSA (defined below) | |

Board | Swift's Board of Directors | |

C-TPAT | Customs-Trade Partnership Against Terrorism | |

CDL | Commercial Drivers' License | |

Central | Central Refrigerated Transportation, LLC (formerly Central Refrigerated Transportation, Inc.) | |

Central Acquisition | Swift's acquisition of all of the outstanding capital stock of Central | |

CEO | Chief Executive Officer, Richard Stocking | |

CFO | Chief Financial Officer, Virginia Henkels | |

CMV | Commercial Motor Vehicle | |

CODM | Chief Operating Decision Makers, which includes our CEO and CFO | |

COFC | Container on Flat Car | |

CSA | Compliance Safety Accountability | |

Deadhead | Tractor movement without hauling freight (unpaid miles driven) | |

DHS | United States Department of Homeland Security | |

DOE | United States Department of Energy | |

DOT | United States Department of Transportation | |

2

2016 ANNUAL REPORT ON FORM 10-K | ||

GLOSSARY OF TERMS — CONTINUED | ||

Term | Definition | |

EBITDA | Earnings Before Interest, Taxes, Depreciation, and Amortization (a non-GAAP measure) | |

ELD | Electronic Logging Device | |

EPA | United States Environmental Protection Agency | |

EPS | Earnings Per Share | |

FASB | Financial Accounting Standards Board | |

FLSA | Fair Labor Standards Act | |

FMCSA | Federal Motor Carrier Safety Administration | |

GAAP | United States Generally Accepted Accounting Principles | |

GHG | Green House Gas | |

IEL | Interstate Equipment Leasing, LLC (formerly Interstate Equipment Leasing, Inc.) | |

IPO | Initial Public Offering | |

LIBOR | London InterBank Offered Rate | |

LTL | Less-than-truckload | |

Mohave | Mohave Transportation Insurance Company, a Swift wholly-owned captive insurance subsidiary | |

Moyes Affiliates | Jerry Moyes, Vickie Moyes, The Jerry and Vickie Moyes Family Trust dated December 11, 1987, and various Moyes children's trusts | |

NASDAQ | National Association of Securities Dealers Automated Quotations | |

New Revolver | Revolving line of credit under the 2015 Agreement | |

New Term Loan A | The Company's first lien term loan A under the 2015 Agreement | |

NLRB | National Labor Relations Board | |

NYSE | New York Stock Exchange | |

OID | Original Issue Discount | |

Old Revolver | Revolving line of credit under the 2014 Agreement | |

Old Term Loan A | The Company's first lien term loan A under the 2014 Agreement | |

OTR | Over-the-road | |

Red Rock | Red Rock Risk Retention Group, Inc., a Swift captive insurance subsidiary | |

Revenue xFSR | Revenue, Excluding Fuel Surcharge Revenue | |

RSU | Restricted Stock Unit: represents a right to receive a share of Class A common stock, when it vests - awarded to employees of the Company | |

SafeStat | Safety Status measurement system | |

SEC | Securities and Exchange Commission | |

Senior Notes | The Company's senior secured second priority notes | |

SRCII | Swift Receivables Company II, LLC | |

Swift Refrigerated | Swift Refrigerated Service, LLC (formerly Central Refrigerated Transportation, LLC) | |

The Purchasers | Unrelated financial entities in the 2015 and 2013 RSA, which were accounts receivable securitization agreements entered into by SRCII | |

Term Loan B | The Company's first lien term loan B under the 2014 Agreement | |

TOFC | Trailer on Flat Car | |

TSA | United States Transportation Security Administration | |

VPF | Variable Prepaid Forward (contract) | |

3

PART I | ||||

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS |

This report contains "forward-looking statements" within the meaning of the federal securities laws that involve risks and uncertainties. Forward-looking statements include statements we make concerning:

• | our plans, objectives, goals, strategies (including our growth strategies and the benefits and advantages to us compared to others in the trucking industry), future events, future revenues or performance, and financing needs; |

• | our compliance with, and the impact on Swift of, proposed, established or new environmental, transportation, safety, tax, accounting, labor, and other laws and regulations; |

• | the benefits of our business model, operations, and strategies in light of changing trends in the trucking industry; |

• | the benefits of our driver academies and driver development programs; |

• | our opportunities in the temperature-controlled market; |

• | the benefits of our C-TPAT status; |

• | the benefits of utilizing owner-operators; |

• | future opportunities in our Dedicated and Swift Refrigerated segments, as well as our non-asset-based freight brokerage and logistics services; |

• | that we expect to reduce our participation in the spot market; |

• | that our elimination of our TOFC service will result in efficiencies in our COFC service; |

• | our expectations to pursue acquisitions and integrate such acquisitions quickly; |

• | our compliance with environmental, transportation, and other laws and regulations; |

• | the outcome of pending claims, litigation, and actions in respect thereof; |

• | trucking industry supply, demand, pricing, and cost trends; |

• | our expectation of increasing driver wages and hiring expenses, as well as the contracted pay rates for owner-operators; |

• | trends in the age of our tractor and trailer fleet, equipment costs, and depreciation expense; |

• | the amount of intangible asset amortization in future periods; |

• | our ability to grow Adjusted EPS and return on assets and generate free cash flow to reduce debt; |

• | the benefits of a shorter tractor trade-in cycle; |

• | the benefits of our fuel surcharge program and our ability to recover increasing fuel costs through surcharges; |

• | the impact of the lag effect relating to our fuel surcharges; |

• | the sources and sufficiency of our liquidity and financial resources to pay debt, make capital expenditures, and operate our business; |

• | the value of equipment under operating leases relating to our residual value guarantees; |

• | our intentions concerning the potential use of derivative financial instruments to hedge fuel price increases; |

• | our expectations regarding the use of the NYSE's "controlled company" exemption concerning certain corporate governance requirements; |

• | our ability to alter our trade cycle and purchase agreements; |

• | the sufficiency and condition of our facilities; |

• | our intention to reinvest foreign earnings outside the United States; |

• | our intentions concerning the payment of dividends; and |

• | the timing and amount of future acquisitions of trucking equipment and other capital expenditures, as well as the use and availability of cash, cash flow from operations, leases, and debt to finance such acquisitions. |

Such statements appear under the headings entitled Risk Factors, Management's Discussion and Analysis of Financial Condition and Results of Operations, and Business. When used in this report, the words "estimates," "expects," "anticipates," "projects," "forecasts," "plans," "intends," "believes," "foresees," "seeks," "likely," "may," "will," "could," "should," "goal," "target," and variations of these words or similar expressions (or the negative versions of any such words) are intended to identify forward-looking statements. In addition, we, through our senior management, from time to time make forward-looking public statements concerning our expected future operations and performance and other developments. These forward-looking statements are subject to risks and uncertainties that may change at any time, and therefore, our actual results may differ materially from those that we expected. Accordingly, undue reliance should not be placed on our forward-looking statements. We derive many of our forward-looking statements from our operating budgets and forecasts, which are based upon many detailed assumptions. While we believe that our assumptions are reasonable, we caution that it is very difficult to predict the impact of known factors, and of course, it is impossible for us to anticipate all factors that could affect our actual results. All forward-looking statements are based upon information available to us on the date of this report. We undertake no obligation to publicly update or revise forward-looking statements to reflect events or circumstances after the date made or to reflect the occurrence of unanticipated events, except as required by law.

Important factors that could cause actual results to differ materially from our expectations ("cautionary statements") are disclosed under "Risk Factors" and elsewhere in this report. All forward-looking statements in this report and subsequent written and oral forward-looking statements attributable to us, or persons acting on our behalf, are expressly qualified in their entirety by the cautionary statements.

4

ITEM 1. | BUSINESS |

Certain acronyms and terms used throughout this Annual Report on Form 10-K are specific to our company, commonly used in our industry, or are otherwise frequently used throughout our document. Definitions for these acronyms and terms are provided in the "Glossary of Terms," available in the front of this document.

Company Overview |

Swift is a multi-faceted transportation services company, operating one of the largest fleets of truckload equipment in North America from over 40 terminals near key freight centers and traffic lanes. We principally operate in short- to medium-haul traffic lanes around our terminals and dedicated customer locations. During 2016, our consolidated average operational truck count was 17,548, which along with our intermodal containers covered 2.2 billion miles for shippers throughout North America, contributing to consolidated operating revenue of $4.0 billion and consolidated operating income of $242.0 million. As of December 31, 2016, our fleet was comprised of 13,937 company tractors and 4,429 owner-operator tractors, as well as 64,066 trailers, and 9,131 intermodal containers. Our customers have the opportunity to "one-stop-shop" for their truckload transportation needs with our extensive suite of service offerings, which includes line-haul services, dedicated customer contracts, temperature-controlled units, intermodal freight solutions, cross-border United States/Mexico and United States/Canada freight, flatbed hauling, freight brokerage and logistics, and others.

Company Background |

The Company began operations in 1966 with only one truck, with Jerry Moyes, along with his father and brother as its founders. The founders originally conducted operations under the name of Common Market Distributing, later buying Swift Transportation Co., Inc. ("Swift Transportation"). In the 1980s, Jerry Moyes bought out his partners, becoming the sole owner of Swift Transportation. In 1990, Swift Transportation went public on the NASDAQ stock market.

• | The 2007 Transactions — In April 2007, Mr. Moyes and his wife contributed their ownership of all of the issued and outstanding shares of IEL to Swift Corporation in exchange for additional Swift Corporation shares. In May 2007, the Moyes Affiliates, contributed their shares of Swift Transportation common stock to Swift Corporation in exchange for additional Swift Corporation shares. Swift Corporation then completed its acquisition of Swift Transportation through a merger on May 10, 2007, thereby acquiring the remaining outstanding shares of Swift Transportation common stock. Upon completion of the 2007 Transactions, Swift Transportation became a wholly-owned subsidiary of Swift Corporation. At the close of market on May 10, 2007, the common stock of Swift Transportation ceased trading on NASDAQ. |

• | The IPO — On May 20, 2010, Swift Corporation formed Swift Transportation Company, a Delaware corporation. Swift Transportation Company did not engage in any business or other activities except in connection with its formation and the IPO and held no assets or subsidiaries prior to such offering. Immediately prior to the consummation of the IPO, Swift Corporation merged with and into Swift Transportation Company, with Swift Transportation Company surviving as a Delaware corporation. In the merger, all of the outstanding common stock of Swift Corporation was converted into shares of Swift Transportation Company Class B common stock on a one-for-one basis, and all outstanding stock options of Swift Corporation were converted into options to purchase shares of Class A common stock of Swift Transportation Company. All outstanding Class B shares are held by Mr. Moyes and the Moyes Affiliates. Swift Transportation Company went public on the NYSE in December 2010, at an initial trading price of $11.00 per share. |

• | Central Acquisition — On August 6, 2013, Swift acquired all of the outstanding capital stock of Central in a cash transaction. Jerry Moyes, our then-CEO and controlling stockholder, was the principal owner of Central. Given Mr. Moyes' interests in the temperature-controlled truckload industry, our Board established a special committee comprised solely of disinterested, independent directors in May of 2011 to evaluate Swift's expansion of its temperature-controlled operations. The special committee evaluated alternative business opportunities, including organic growth and various acquisition targets, and negotiated the transaction contemplated by the stock purchase agreement, with the assistance of its independent financial advisors. Upon the unanimous recommendation of the special committee, the Central Acquisition was approved by the Board (with Mr. Moyes not participating in the vote). |

5

Industry and Competition |

Truckload carriers represent the largest part of the transportation supply chain for most retail and manufactured goods in North America and typically transport a full trailer (or container) of freight for a single customer from origin to destination without intermediate sorting and handling. Generally, the truckload industry is compensated based on miles, whereas the LTL industry is compensated based on package size and/or weight. Overall, the United States trucking industry is large, fragmented, and highly competitive. We compete with thousands of truckload carriers, most of whom operate much smaller fleets than we do. To a lesser extent, our intermodal services, as well as our freight brokerage and logistics business, compete with railroads, LTL carriers, logistics providers, and other transportation companies.

Our industry has encountered the following major economic cycles since 2000:

Period | Economic Cycle |

2000 — 2001 | industry over-capacity and depressed freight volumes |

2002 — 2006 | economic expansion |

2007 — 2009 | freight slowdown, fuel price spike, economic recession, and credit crisis |

2010 — 2013 | moderate recovery. The industry freight data began to show positive trends for both volume and pricing. The slow, steady growth is a result of moderate increases in gross domestic product, coupled with a tighter supply of available tractors. Trends in supply of available tractors were lower due to several years of below average truck builds, an increase in truckload fleet bankruptcies in 2009 and 2010, increasing equipment prices due to stringent EPA requirements, less available credit, and less driver availability. |

2014 — present | return to pre-recession levels and relative stabilization. In 2014, total spending on transportation, which fell during the 2007 – 2009 recession, returned to pre-recession levels. Truck tonnage grew throughout 2014, followed by decelerating growth in 2015, and relative stabilization in 2016. Capacity became looser in 2015 and 2016, as inventory levels were high and large volumes of tractor purchases created a supply/demand imbalance, putting pressure on pricing. Fuel prices declined. |

The principal means of competition in our industry are customer service, capacity, and price. In times of strong freight demand, customer service, and capacity become increasingly important, and in times of weak freight demand, pricing becomes increasingly important. Most truckload contracts (other than dedicated contracts) do not guarantee truck availability or load levels. Pricing is influenced by supply and demand.

The trucking industry faces the following primary challenges, which we believe we are well-positioned to address, as discussed under "Our Competitive Strengths" and "Company Strategy," below:

• | cumulative impacts of regulatory initiatives, such as ELDs, hours-of service limitations for drivers, and the FMCSA's CSA; |

• | uncertainty in the economic environment, including changing supply chain and consumer spending patterns; |

• | pressures on volumes and pricing from excess industry capacity, excess customer inventories, and depressed shipping demand; |

• | driver shortages; |

• | driver distraction and other unfavorable safety trends; |

• | significant and rapid fluctuations in fuel prices; and |

• | increased prices for new revenue equipment, design changes of new engines, and volatility in the used equipment sales market. |

Our Mission and Vision |

O U R V I S I O N | We are an efficient and nimble world class service organization that is focused on the customer. |

We are aligned and working together at all levels to achieve our common goals. | |

Our team enjoys our work and co-workers and this enthusiasm resonates both internally and externally. | |

We are on the leading edge of service, always innovating to add value to our customers. | |

Our information and resources can easily be adapted to analyze and monitor what is most important in a changing environment. | |

Our financial health is strong, generating excess operating cash flows and growing profitability year-after-year with a culture that is cost- and environmentally-conscious. | |

We train, build, and develop our employees through perpetual learning opportunities to enhance their skill sets, allowing us to recognize our talented people. | |

6

Our Competitive Strengths |

We aspire to achieve the themes of our mission and vision and believe our competitive strengths and strategies will enable us to attain our desired level of service to customers and results for our shareholders. We believe the following competitive strengths provide a solid platform for pursuing our goals and strategies:

North American Truckload Leader with Broad Terminal Network and a Modern Fleet |

Our fleet size offers wide geographic coverage, while maintaining the efficiencies associated with significant traffic density within our operating regions. Our terminals are strategically located near key population centers, driver recruiting areas, and cross-border hubs, often in close proximity to our customers. This broad network offers benefits such as in-house maintenance, more frequent equipment inspections, localized driver recruiting, rapid customer response, and personalized marketing efforts. Our size allows us to achieve substantial economies of scale in purchasing items such as tractors, trailers, containers, fuel, and tires where pricing is volume-sensitive. We believe our scale also offers additional benefits in brand awareness and access to capital. Our OTR sleeper fleet has an average age of 2.4 years for our approximately 10,200 core operating units. By maintaining a newer fleet than many of our industry competitors, we believe that we have the following advantages: • Newer tractors typically have fewer repairs and lower operating costs. • Newer tractors are available for dispatch more often. • Drivers are typically more attracted to newer tractors, which helps with driver recruiting and retention. • Many competitors that allowed their fleets to age excessively will likely face a deferred capital expenditure spike, accompanied by difficulty in replacing their tractors because while new tractor prices have increased and the value received for the old tractors has decreased. |

High Quality Customer Service and Extensive Suite of Services |

Our intense focus on customer satisfaction has helped us establish a strong platform for cross-selling our other services to our strong and diversified customer base. We believe customers continue to search for ways to better streamline their transportation management functions. We respond to this need by providing our customers with solutions that include a wide variety of shipping services, including general and specialized truckload, cross-border services, regional distribution, high-service dedicated operations, intermodal service, and surge capacity through fleet flexibility and brokerage and logistics operations. This breadth of service helps diversify our customer base and provides us with a competitive advantage, especially for customers with multiple needs and cross-border United States/Mexico and United States/Canada shipments. |

Strong Owner-operator Business |

We supplement our company tractor fleet with owner-operators, who own and operate their own tractors and are responsible for ownership and operating expenses. We believe that owner-operators provide significant advantages that primarily arise from the entrepreneurial motivation of business ownership. The owner-operators we contract with tend to be more experienced, have fewer accidents per million miles, and on average, produce higher weekly revenue per tractor than our company drivers. |

Leader in Driver Development |

Historically, driver recruiting and retention have been significant challenges for truckload carriers. To address these challenges, we employ nationwide recruiting efforts through our terminal network, operate eleven driver academies, partner with third-party driver training facilities, provide drivers with modern tractors, and promote numerous driver satisfaction initiatives. |

Regional Operating Model |

Our short- and medium-haul regional operating model contributes to higher revenue per mile and takes advantage of shipping trends toward regional distribution. We also experience less competition in our short- and medium-haul regional business from railroads. In addition, our regional terminal network allows our drivers to be home more often, which assists with driver retention. |

Experienced Management, Aligned with Corporate Success |

Our management team has a proven track record of growth and cost control. Management focuses on disciplined execution and financial performance by measuring our progress through a combination of financial metrics. We align management's priorities with our stockholders' through equity incentive awards and an annual performance-based bonus plan. |

7

Company Strategy |

Our key financial goals include improving our asset utilization, controlling costs, growing Adjusted EPS (defined in "Non-GAAP Financial Measures" under Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations), improving return on net assets, as well as generating cash flow to reinvest in our business, repay debt, and return capital to our stockholders. We align our company focus to attain these goals by implementing the following strategies, which we believe also serve to minimize the impact of challenges currently faced in the trucking industry.

Profitable Revenue Growth | |

To increase freight volumes and yield, we intend to further penetrate our existing customer base, cross-sell our services, pursue new customer opportunities by leveraging our outstanding customer service and extensive suite of truckload services, and effectively price fuel surcharges. In our pursuit to be best in class, we survey our customers and identify areas where we can accelerate the capture of new freight opportunities, improve our customers' experience, and profit from enhancing the value our customers receive. We are continuously refining our freight management tools to allocate our equipment to more profitable loads and complementary shipping lanes. In addition to growth in our core OTR dry van truckload business, we are targeting expansion in the following areas: | |

Dedicated Services and Private Fleet Outsourcing | Dedicated contracts are often used by our customers with high-service and high-priority freight, sometimes to replace private fleets previously operated by them. The size and scale of our fleet and terminal network allows us to provide the equipment availability and high service levels required for dedicated contracts. We believe these opportunities will increase in times of scarce capacity in the truckload industry. |

Temperature-controlled | Beginning with the Central Acquisition, we compete in the over-the-road temperature-controlled business to complement our dedicated temperature-controlled and our OTR dry van service offerings. Growth in the temperature-controlled market has outpaced the dry van market over the past ten years, and many of our current customers have a need for this service. We believe the scale provided by the Central Acquisition and our ability to penetrate our existing customer base provides us with future opportunities in this growing market. |

Cross-border United States/Mexico and United States/Canada Freight | The combination of our United States, cross-border, customs brokerage, and Mexican operations enables us to provide efficient door-to-door service between the United States and Mexico, as well as Canada. We believe our sophisticated load security measures, as well as our DHS status as a C-TPAT carrier, allow us to offer more efficient service than most competitors and afford us substantial advantages with major cross-border United States/Mexico and United States/Canada shippers. |

Freight Brokerage and Logistics | We believe we have a substantial opportunity to continue to increase our non-asset-based freight brokerage and logistics services. We believe many customers increasingly seek transportation companies that offer both asset-based and non-asset-based services to ensure additional certainty that safe, secure, and timely truckload service will be available on demand. We intend to continue growing our transportation management and freight brokerage capability to build market share, earn marginal revenue on more loads, and preserve our assets for the most attractive lanes and loads. |

Intermodal | We have intermodal agreements with most major North American rail carriers, which have helped increase our volumes through more competitive pricing. Our intermodal presence, which expanded to service Mexico in 2013, complements our regional operating model and allows us to better serve customers in longer haul lanes and reduce our investment in fixed assets. Our intermodal fleet has more than doubled its size since its inception in 2005. Our capacity totaled 9,131 and 9,150 containers as of December 31, 2016 and 2015, respectively. |

8

Increase Asset Productivity and Return on Capital | |

Because of our size and operating leverage, even small improvements in our asset productivity and yield can have a significant impact on our operating results. We believe we have substantial opportunity to improve the productivity and yield of our existing assets as follows: | |

Disciplined Tractor Fleet Growth | We will continue to focus on maintaining discipline regarding the timing and extent of company tractor fleet growth, based on availability of high-quality freight. |

Process Improvement and System Integration | Successful implementation of process improvements and effective systems integration will achieve more efficient utilization of our tractors, trailers, and drivers' available hours-of-service. For example, our entire tractor fleet is retrofitted with ELDs, which we believe can help us more efficiently utilize our drivers' available hours-of-service. |

Tractor Utilization | We use equipment pools, relays, team drivers, and similar measures to improve company tractor utilization. |

Owner-operator Trucking Capacity | On average, owner-operators produce higher weekly revenue per tractor than company drivers. As such, we generally prefer to increase the percentage of our trucking capacity provided by owner-operators, when possible. |

Elimination of Unproductive Assets | Our return on capital improves as we successfully eliminate unproductive assets. |

Continue to Focus on Efficiency and Cost Control | |

To ensure that we respond appropriately to economic change, we closely manage our costs and capital resources and continually monitor the economic environment, as well as its potential impact on our customers and end-markets. We presently have ongoing efforts in the following areas that we expect will yield benefits in future periods: | |

Tractor Capacity | In order to balance freight flows and reduce deadhead miles, we manage the flow of our tractor capacity through our network. |

Driver Satisfaction | Improving driver satisfaction typically reduces turnover costs and improves performance. We believe our driver development programs, including our driver academies and nationwide recruiting, will become increasingly advantageous to us in countering attrition effects stemming from noncompliance with internal policies and procedures, as well as recent regulatory initiatives (discussed below). In addition, we believe that the negative impact of such regulations will be partially mitigated by our average length of haul, regional terminal network, and less mileage-intensive operations, such as intermodal, dedicated, brokerage, and cross-border operations. |

Waste Reduction | Reducing waste in shop methods and procedures and in other administrative processes remains important to us. |

Pursue Selected Acquisitions | |

From time to time, we take advantage of opportunities to add complementary operations to our company by pursuing acquisitions. Acquisitions can provide us an opportunity to expand our fleet with customer revenue and drivers already in place. In our history, we have completed 13 acquisitions, including Central in 2013, most of which were immediately integrated into our existing business. Given our size in relation to most competitors, we expect most future acquisitions to be integrated quickly. | |

We believe that by achieving profitable revenue growth, improving asset utilization, continuing to control costs, and streamlining our processes, we will be able to grow our Adjusted EPS and our return on net assets, while generating free cash flow to reinvest in our business, potentially acquire complementary businesses, repay debt, reduce our leverage ratio, and return capital to our stockholders. These goals are in part dependent on continued improvement in industry-wide truckload volumes and pricing. Although we expect the economic environment and capacity constraints in our industry to support achievement of our goals, we have limited ability to affect industry volumes and pricing and cannot provide assurance that this environment will sustain. Nevertheless, we believe our competitive strengths and the expected supply and demand environment in the truckload industry are aligned to support the achievement of our goals through the strategies outlined above.

9

Information by Segment and Geography |

• | Segments — Our four reportable segments are Truckload, Dedicated, Swift Refrigerated, and Intermodal. Segment information is provided in Notes 2 and 24 to the consolidated financial statements, including accounting and reporting policy, segment definitions, and financial information. Supplementary segment information is available in Part II, Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations. |

• | Geography — The required disclosures relating to revenue and long-lived assets by geography are included in Note 24 to the consolidated financial statements. Income tax information by geography is included in Note 11 to the consolidated financial statements. |

Customers and Marketing |

• | Customers — Our customers are typically large corporations in the retail (including discount and online retail), food and beverage, consumer products, paper products, transportation and logistics, housing and building, automotive, and manufacturing industries. Many of our customers have extensive operations, geographically distributed locations, and diverse shipping needs. Customer satisfaction is an important priority for us, which is demonstrated by the numerous "carrier of the year" or similar awards received from our customers over the past several years. Such achievements have helped us maintain a large and stable customer base featuring Fortune 500 and other leading companies from a number of different industries. Consistent with industry practice, our typical customer contracts (other than dedicated contracts) do not guarantee shipment volumes by our customers or truck availability by us. This affords us and our customers some flexibility to negotiate rates in response to changes in freight demand and industry-wide truck capacity. We believe our fleet capacity, terminal network, customer service and breadth of services offer a competitive advantage to major shippers, particularly in times of rising freight volumes when shippers must quickly access capacity across multiple facilities and regions. |

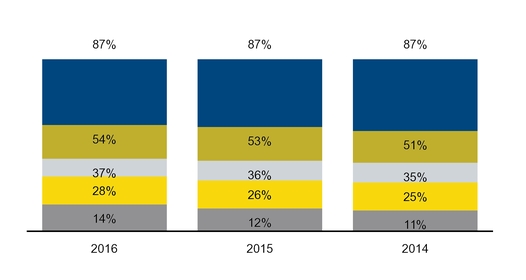

Customer Concentration | ||||||||||||||

(as a percentage of consolidated operating revenue) | ||||||||||||||

Largest (Wal-Mart) | Top 5 | Top 10 | Top 25 | Top 200 | ||||||||||

One customer, Wal-Mart, accounted for more than 10% of our operating revenue during 2016, 2015, and 2014.

• | Marketing — We concentrate our marketing efforts on cross-selling our extensive suite of services we provide to existing customers, as well as on establishing new customers with shipment needs that complement our terminal network and existing routes. At December 31, 2016, we had a sales staff of approximately 40 individuals across the United States, Mexico, and Canada, who work closely with management to establish and expand accounts. |

10

Revenue Equipment |

We operate a modern company tractor fleet to help attract and retain drivers, promote safe operations, and reduce maintenance and repair costs. The following table shows the age of our owned and leased tractors and trailers as of December 31, 2016:

Model Year | Tractors (1) | Trailers | ||||

2017 | 1,225 | 6,696 | ||||

2016 | 3,856 | 4,521 | ||||

2015 | 3,142 | 6,664 | ||||

2014 | 4,011 | 4,593 | ||||

2013 | 675 | 4,551 | ||||

2012 | 343 | 3,753 | ||||

2011 | 83 | 3,189 | ||||

2010 | 13 | 111 | ||||

2009 | 78 | 4,392 | ||||

2008 | 150 | 1,857 | ||||

2007 | 99 | 129 | ||||

2006 and prior | 262 | 23,610 | ||||

Total | 13,937 | 64,066 | ||||

_______________

(1) Excludes 4,429 owner-operator tractors.

We typically purchase or lease tractors and trailers manufactured to our specifications. We follow a comprehensive maintenance program designed to reduce downtime and enhance the resale value of our equipment. We have major maintenance facilities in the following locations:

• | Phoenix, Arizona |

• | Memphis, Tennessee |

• | Greer, South Carolina |

• | West Valley City, Utah |

• | Columbus, Ohio |

• | Laredo, Texas |

• | Jurupa Valley, California |

In addition to these maintenance facilities, we perform routine servicing and maintenance of our revenue equipment at most of our regional terminal facilities, in an effort to avoid costly on-road repairs and deadhead miles. The contracts governing our equipment purchases typically contain specifications of equipment, projected delivery dates, warranty terms, and trade or return conditions, and are cancelable upon 60 to 90 days' notice without penalty.

Our tractor trade-in cycle range, depending on equipment type and usage, was 42 to 48 months and 36 to 48 months, during 2016 and 2015, respectively. Our newer equipment has enhanced features, which we believe tends to lower the overall life cycle costs by reducing safety-related expenses, lowering repair and maintenance expenses, improving fuel economy, and improving driver satisfaction. In 2017 and beyond, we will continue to monitor the appropriateness of this relatively short tractor trade-in cycle against the lower capital expenditure and financing costs of a longer tractor trade-in cycle, based on current and future business needs.

11

Technology |

Trucks — We equip virtually all of our trucks with certain OmniTRACStm technologies that enhance communication between the regional terminals and corporate headquarters, as well as the added benefits of ELDs, text-to-voice messaging, and turn-by-turn directions designed specifically for our industry. This allows us to alter driver routes rapidly, in case of urgent customer requests, adverse weather conditions, road closures, or other potential delays. It also enables our drivers to timely communicate route status or the need for emergency repairs. These technologies have afforded us additional productivity, improved safety, and increased customer and driver satisfaction.

We reduce costs through programs that manage equipment maintenance, select fuel purchasing locations in our nationwide network of terminals and approved truck stops, and inform us of inefficient or undesirable driving behaviors that are monitored and reported through electronic engine sensors and cameras. We believe our technologies and systems are superior to those employed by most of our smaller competitors.

Trailers and Containers — The majority of our trailers and containers are equipped with tracking devices that monitor locations of empty and loaded equipment via satellite. We also use geofencing, along with other on-site and off-site tracking capabilities to ensure we are alerted when our equipment is not located where we are expecting it to be located. These technological capabilities enable us to identify unused or stolen units, enhance our ability to charge for units detained by customers, and reduce theft.

Enterprise Resource Planning ("ERP") — In 2016, we began preliminary planning phases to replace our current ERP with a new solution, including identification of needs, request for proposal, evaluation of alternatives, and final selection of a new ERP. Beginning in 2017, the Company will be in the implementation phases of replacing its current ERP system with a new cloud-based solution. The core applications of the new ERP within finance, human resources, and payroll are expected to go live in 2018.

Employees |

The strength of our company is our people, working together with common goals. There were approximately 21,800 full-time employees in our total headcount of approximately 21,900 employees as of December 31, 2016, which was comprised of:

Company drivers (including driver trainees) | 16,600 | ||

Technicians and other equipment maintenance personnel | 1,300 | ||

Support personnel (such as corporate managers, sales, and administrative personnel) | 4,000 | ||

Total | 21,900 | ||

As of December 31, 2016, our 821 Trans-Mex drivers in Mexico were our only employees represented by a union.

Company Drivers — All of our drivers must meet specific guidelines relating primarily to safety records, driving experience, and personal evaluations, including a physical examination and mandatory drug and alcohol testing. Upon hire, drivers are trained in our policies, operations, safety techniques, and the fuel-efficient operation of the equipment. All new drivers must pass a safety test and have a current CDL. In addition, we have ongoing driver efficiency and safety programs to ensure that our drivers comply with our safety procedures.

We have established eleven driver academies across the United States. Our academies are strategically located in areas where external driver-training organizations were lacking. In other areas of the United States, we have contracted with driver-training schools, which are managed by third parties. There are certain minimum qualifications for candidates to be accepted into the academy, including passing the DOT physical examination and drug/alcohol screening. Students are required to complete three weeks of instructor-led study/training and then spend a minimum of 200 behind-the-wheel hours, driving with an experienced trainer.

In order to attract and retain qualified drivers and promote safe operations, we purchase high quality tractors equipped with optional comfort and safety features. We base our drivers at terminals and monitor each driver's location in order to schedule routing for our drivers so they can return home regularly. The majority of company drivers are compensated based on industry standard dispatched miles, loading/unloading, and number of stops or deliveries, plus bonuses. The driver's base pay per mile increases with the driver's length of experience. Our driver ranking system measures safety, compliance, customer service, and number of miles driven. Higher rankings provide drivers with additional benefits and/or privileges, such as special recognition, the ability to self-select freight, and the opportunity for increased pay.

Upon enrollment eligibility, drivers employed by us may participate in company-sponsored health, life and dental insurance plans and participate in our 401(k) and employee stock purchase plans.

Terminal Staff — Most of our large terminals are staffed with terminal leaders, fleet leaders, driver leaders, planners, safety coordinators, shop leaders, technicians, and customer service representatives. Our terminal leaders work with driver leaders, customer service representatives, and other operations personnel to coordinate the needs of both our customers and our drivers. Terminal leaders are also responsible for serving existing customers in their areas. Each fleet leader supervises approximately five

12

driver leaders at our larger terminals. Each driver leader is responsible for the general operation of approximately 40 to 50 trucks and their drivers, focusing on driver retention, productivity per truck, fuel consumption, fuel efficiency (with respect to driver-controllable idle time), safety, and scheduled maintenance. Customer service representatives are assigned specific customers to ensure specialized, high-quality service, and frequent customer contact.

Owner-Operators |

In addition to Swift-employed company drivers, we enter into contractor agreements with third parties who own and operate tractors (or hire their own drivers to operate the tractors) that service our customers. We pay these owner-operators for their services, based on a contracted rate per mile. By operating safely and productively, owner-operators can improve their own profitability and ours. Owner-operators are responsible for most costs incurred for owning and operating their tractors. For convenience, we offer owner-operators maintenance services at our in-house shops and fuel at our terminals at competitive and attractive prices. As of December 31, 2016, owner-operators comprised 24.1% of our total fleet, as measured by tractor count.

We offer tractor financing to independent owner-operators through our financing subsidiaries. Our financing subsidiaries generally lease premium equipment from the original equipment manufacturers and sublease the equipment to owner-operators. The owner-operators are qualified for financing, based on their driving and safety records. In the event of default, our financing subsidiaries have the option to repossess the tractor and sublease it to a replacement owner-operator.

Safety and Insurance |

We take pride in our safety-oriented culture and maintain an active safety and loss-prevention program, which is led by regional safety management personnel at each of our terminals. We also equip our tractors with many safety features, such as roll-over stability devices and critical-event recorders, to help prevent or reduce the severity of accidents. We self-insure for a significant portion of our claims exposure and related expenses. We currently carry seven main types of insurance, which generally have the following self-insured retention amounts, maximum benefits per claim, and other limitations:

Insurance | Limits |

Automobile Liability, General Liability, and Excess Liability | $250.0 million of coverage per occurrence ($350.0 million aggregated limits through October 31, 2016), subject to a $10.0 million self-insured retention per-occurrence. |

Cargo Damage and Loss | $2.0 million limit per truck or trailer with a $10.0 million limit per occurrence; provided that there is a $1.0 million limit for tobacco loads and a $250 thousand deductible |

Property and Catastrophic Physical Damage | $150.0 million limit for property and $100.0 million limit for vehicle damage, excluding over the road exposures, subject to a $1.0 million deductible |

Workers' Compensation/Employers' Liability | Statutory coverage limits; employers' liability of $1.0 million bodily injury by accident and disease, subject to a $5.0 million self-insured retention for each accident or disease |

Employment Practices Liability | Primary policy with a $10.0 million limit subject to a $2.5 million self-insured retention |

Health Care | As of January 1, 2015, we are fully insured on our medical benefits, subject to contributed premiums. Prior to January 1, 2015, we had a $500 thousand specific deductible with an aggregating individual deductible of $150 thousand of each employee health care claim, as well as commercial insurance for the balance. |

Director and Officer Insurance | We maintain insurance that covers our directors and officers for losses and expenses arising out of claims, based on acts or omissions in their capacities as directors or officers. |

We insure certain casualty risks through our wholly-owned captive insurance subsidiaries, Mohave and Red Rock. Mohave and Red Rock provide reinsurance associated with a share of our automobile liability risk. In addition to insuring a proportionate share of our corporate casualty risk, Mohave provides reinsurance coverage to third-party insurance companies associated with our affiliated companies' owner-operators.

While under dispatch and our operating authority, the owner-operators we contract with are covered by our liability coverage and self-insurance retention limits. However, each is responsible for physical damage to his or her own equipment, occupational accident coverage, and liability exposure while the truck is used for non-company purposes. Additionally, fleet operators are responsible for any applicable workers' compensation requirements for their employees.

For safety, we electronically govern the speed of substantially all of our company tractors to a maximum of 62 miles per hour. Additionally, our owner-operator contracts include statements that owner-operators must comply with the Company's speed policy, which indicates that they must limit their speed to 67 miles per hour. These adopted speed limits are below the limits established by statute in many states. We believe our adopted speed limits for drivers reduce the frequency and severity of accidents, enhance fuel efficiency, and reduce maintenance expense, when compared to operating without our imposed speed limits.

13

Fuel |

We actively manage our fuel purchasing network in an effort to maintain adequate fuel supplies and reduce our fuel costs. Additionally, we utilize a fuel surcharge program to pass a majority of increases in fuel costs to our customers. In 2016, we purchased 16.9% of our fuel in bulk at 56 Swift and dedicated customer locations across the United States and Mexico. We purchased substantially all of the remainder through a network of retail truck stops with which we have negotiated volume purchasing discounts. The volumes we purchase at terminals and through the fuel network vary based on procurement costs and other factors. We seek to reduce our fuel costs by routing our drivers to truck stops when fuel prices at such stops are cheaper than the bulk rate paid for fuel at our terminals. We store fuel in underground storage tanks at two of our bulk fueling terminals and in above-ground storage tanks at our other bulk fueling terminals. We believe that we are sufficiently in compliance with applicable environmental laws and regulations relating to the storage and dispensing of fuel.

Seasonality |

In the truckload industry, results of operations generally show a seasonal pattern. As customers ramp up for the year-end holiday season, the late third and fourth quarters have historically been our strongest volume quarters. As customers reduce shipments after the winter holiday season, the first quarter has historically been a lower volume quarter for us than the other three quarters. In recent years, the macro consumer buying patterns combined with shippers' supply chain management, which historically contributed to the fourth quarter "peak" season, continued to evolve. As a result, our fourth quarter 2016, 2015, and 2014 volumes did not peak early in the quarter. Instead, volumes during the fourth quarter were more evenly disbursed throughout the quarter, with a brief decrease the week of the U.S. Thanksgiving holiday and then tapering off the last week of the year. In the eastern and mid-western United States, and to a lesser extent in the western United States, during the winter season our equipment utilization typically declines and operating expenses generally increase, with fuel efficiency declining because of engine idling and severe weather sometimes creating higher accident frequency, increased claims, and more equipment repairs. Revenue may also be affected by holidays as a result of curtailed operations or vacation shutdowns, because our revenue is directly related to available working days of shippers. From time to time, we also suffer short-term impacts from severe weather and similar events, such as tornadoes, hurricanes, blizzards, ice storms, floods, fires, earthquakes, and explosions that could harm our results of operations or make our results of operations more volatile.

Environmental Regulation |

General — We have bulk fuel storage and fuel islands at many of our terminals, as well as vehicle maintenance, repair, and washing operations at some of our facilities, which exposes us to certain environmental risks. Soil and groundwater contamination have occurred at some of our facilities in prior years, for which we have been responsible for remediating the environmental contamination. Also, less than one percent of our total shipments contain hazardous materials, which are generally rated as low- to medium-risk. In the past, we have been responsible for the costs of clean-up of cargo and diesel fuel spills caused by traffic accidents or other events.

We have instituted programs to monitor and mitigate environmental risks and maintain compliance with applicable environmental laws dealing with the hauling, handling, and disposal of hazardous materials, fuel spillage or seepage, emissions from our vehicles and facilities, engine-idling, discharge and retention of storm water, and other environmental matters. As part of our safety and risk management program, we periodically perform internal environmental reviews. We are a Charter Partner in the EPA's SmartWay Transport Partnership, a voluntary program promoting energy efficiency and air quality. We believe that our operations are sufficiently in compliance with current laws and regulations and do not know of any existing environmental condition that would reasonably be expected to have a material adverse effect on our business or operating results.

If we are held responsible for the cleanup of any environmental incidents caused by our operations or business, or if we are found to be in violation of applicable laws or regulations, we could be subject to liabilities, including substantial fines or penalties or civil and criminal liability. We have paid penalties for spills and violations in the past; however, they have not been material to our financial results or position.

Greenhouse Gas Emissions and Fuel Efficiency Standards — In 2008 the State of California's Air Resources Board ("ARB") approved the Heavy-Duty Vehicle GHG Emission Reduction Regulation in efforts to reduce GHG emissions from certain long-haul tractor-trailers that operate in California by requiring them to utilize technologies that improve fuel efficiency (regardless of where the vehicle is registered). The regulation required owners of long-haul tractors and 53-foot trailers to replace or retrofit their vehicles with aerodynamic technologies and low rolling resistance tires. The regulation also contained certain emissions and registration standards for refrigerated trailers.

Thereafter, the EPA and the National Highway Traffic Safety Administration ("NHTSA") began taking coordinated steps in support of a new generation of clean vehicles and engines through reduced GHG emissions and improved fuel efficiency at a national level.

14

• | Phase 1: In September 2011, the EPA finalized federal regulations for controlling GHG emissions, beginning with model-year 2014 medium- and heavy-duty engines and vehicles and increasing in stringency through model-year 2018. The federal regulations relate to efficient engines, use of auxiliary power units, mass reduction, low rolling resistance tires, improved aerodynamics, improved transmissions, and reduced accessory loads. |

In December 2013, California's ARB approved regulations to align its GHG emission standards and test procedures, as well as its tractor-trailer GHG regulation, with the federal Phase 1 GHG regulation.

• | Phase 2: In June 2015, the EPA and NHTSA, working in concert with California's ARB, formally announced a proposed national program establishing Phase 2 of the GHG emissions and fuel efficiency standards for medium- and heavy-duty vehicles for model-year 2018 and beyond. In August 2016, the EPA and NHTSA announced the final rule regarding Phase 2, which builds upon Phase 1, and would apply to certain trailer types beginning with model-year 2018 for EPA standards (voluntary for NHTSA standards through model-year 2020). Tractors and certain trailer types would be subject to the Phase 2 standards beginning with model-year 2021, increasing in stringency through model-year 2024, and phasing in completely by model-year 2027. This rule marks the first time federal mandates will be applied to trailers, with respect to aerodynamics and low-rolling resistance tires. The final rule was effective December 27, 2016. |

Current and proposed GHG regulations could impact us by increasing the cost of new tractors and trailers, impairing productivity, and increasing our operating expenses.

Climate-change Proposals — Federal and state lawmakers are considering a variety of climate-change proposals related to carbon emissions and GHG emissions. The proposals could potentially limit carbon emissions for certain states and municipalities, which continue to restrict the location and amount of time that diesel-powered tractors (like ours) may idle.

Industry Regulation |

Our operations are regulated and licensed by various federal, state, and local government agencies in North America, including the DOT, the FMCSA, and the DHS, among others. Our company, as well as our drivers and contracted owner-operators, must comply with enacted governmental regulations regarding safety, equipment, and operating methods. Examples include regulation of equipment weight, equipment dimensions, driver hours-of-service, driver eligibility requirements, on-board reporting of operations, and ergonomics. The following discussion presents recently enacted federal, state, and local regulations that have an impact on our operations.

• | Hours-of-service — In December 2011, the FMCSA released its final rule on hours-of-service, which was effective on July 1, 2013. The key provisions included: |

◦ | retaining the current 11-hour daily driving time limit; |

◦ | reducing the maximum number of hours a truck driver can work within a week from 82 hours to 70 hours; and |

◦ | limiting the number of consecutive driving hours a truck driver can work to eight hours before requiring the driver to take a 30 minute break. |

Since 2004 the hours-of-service rules allowed drivers to restart their duty-cycle clocks every 34 hours to begin a new work week. From July 2013 through December 2014, the FMCSA required that drivers include 1:00 a.m. to 5:00 a.m. on consecutive days for applying the restart, which was also capped at once per week, or 168 hours. On December 13, 2014, Congress passed the fiscal year 2015 Omnibus Appropriations bill, which temporarily suspended enforcement of the 1:00 to 5:00 am provision and the 168-hour rule until September 30, 2015. The restart provision was again suspended in December 2015, pending completion of a study regarding driver restarts, when Congress passed the fiscal year 2016 Omnibus Appropriations bill. All other provisions of the hours-of-service rules that went into effect on July 1, 2013 remained unchanged.

In December 2016, a short-term funding bill was passed by Congress, which clarified the hours-of-service rule. The provision in the bill requires the DOT to proceed with the existing 34-hour restart provision in the hours-of-service rule to ensure continuity in federal rest regulations, should the report on the study (noted above) not meet the criteria set by Congress. If the report, which was completed in December 2015, successfully addresses fatigue, then the rules would go back into effect. We are not aware of any further developments related to the hours-of-service rules.

• | BASICs — In December 2010, the FMCSA introduced a new enforcement and compliance model that ranks both fleets and individual drivers on seven categories of safety-related data, eventually replacing the current SafeStat model. The seven categories of safety-related data, known as BASICs, currently include Unsafe Driving, Fatigued Driving (hours-of-service), Driver Fitness, Controlled Substances/Alcohol, Vehicle Maintenance, Hazardous Materials Compliance, and Crash Indicator. |

Certain BASICs information was initially published and made available to carriers, as well as the general public. However, in December 2015, as part of the Fixing America's Surface Transportation ("FAST") Act, Congress mandated that the FMCSA remove all CSA scores from public view until a more comprehensive study regarding the effectiveness of BASICs improving

15

truck safety could be completed. The study is currently underway and a report to Congress is expected to be published in June 2017.

Implementation and effective dates are unclear. In October 2016, the FMCSA outlined proposed changes to its safety measurement system and sought public feedback through December 2016 before deciding whether to adopt the proposed changes. SafeStat is currently the authoritative safety measurement system in effect. We currently have a satisfactory SafeStat DOT rating, which is the best available rating under the current safety rating scale.

• | Safety Fitness Determination — In January 2016, the FMCSA published a Notice of Proposed Rulemaking ("NPRM") in the Federal Register, regarding carrier safety fitness determination. The NPRM proposes new methodologies that would determine when a motor carrier is not fit to operate a commercial motor vehicle. Key proposed changes included in the NPRM are as follows: |

◦ | There would be only one safety rating of "unfit," as compared to the current rules, which have three safety ratings (satisfactory, conditional, and unsatisfactory). |

◦ | Carriers could be determined "unfit" by failing two or more BASICs, investigation results, or a combination of the two. |

◦ | Stricter standards would be used for BASICs with a higher correlation to crash risk (Unsafe Driving and Hours-of-Service Compliance). |

◦ | All investigation results would be used, not just results from comprehensive on-site reviews. |

◦ | Violations of a revised list of "critical" and "acute" safety regulations would result in failing a BASIC. |

◦ | Carriers would be assessed monthly. |

Public comments on the proposed rule were due in June 2016.

• | Moving Ahead for Progress in the 21st Century Bill — In July 2012, Congress passed the Moving Ahead for Progress in the 21st Century bill into law. Included in the highway bill was a provision that mandates electronic logging devices in commercial motor vehicles to record hours-of-service. Additionally, in response to the bill, a final rule related to entry-level driver training was passed in 2016, as well as amendments to the Drug and Alcohol Clearinghouse rules. |

◦ | Electronic Logging Devices ("ELD") — During 2012, the FMCSA published a Supplemental NPRM, announcing its plan to proceed with the ELDs and hours-of-service supporting documents rulemaking. The ELD rule became final in December 2015, as published in the Federal Register, with an effective date of February 16, 2016. The ELD rule phases in over a four-year period: |

▪ | Phase 1 (February 16, 2016 through December 18, 2017): Carriers and drivers subject to the rule may voluntarily use ELDs or use other forms of logging devices. |

▪ | Phase 2 (December 18, 2017 through December 16, 2019): Carriers and drivers subject to the rule can use Automatic On-board Recording Devices ("AOBRD") that were installed prior to December 18, 2017 or ELDs certified and registered after December 16, 2015. |

▪ | Phase 3 (after December 16, 2019): All drivers and carriers subject to the rule must use certified and registered ELDs that comply with the requirements of the ELD regulations. |

Although the final ELD rule may have a large impact on the industry as a whole, we do not expect a significant impact on Swift, as we previously installed ELDs in our operational trucks in conjunction with our efforts to improve efficiency and communications with drivers and owner-operators.

◦ | Entry-Level Driver Training ("ELDT") — In December 2016, the FMCSA established new minimum training standards for certain individuals applying for (or upgrading) a Class A or Class B commercial driver's license, or obtaining a hazardous materials, passenger, or school bus endorsement on their commercial driver's license for the first time. These individuals are subject to the ELDT requirements and must complete a prescribed program of theory and behind-the wheel instruction. The final rule requires that behind-the-wheel proficiency of an entry-level truck driver be determined solely by the instructor's evaluation of how well the driver-trainee performs the fundamental vehicle controls skills and driving procedures set forth in the curricula, but does not have a minimum training hours requirement, as proposed by the FMCSA earlier in 2016. The final rule went into effect on February 6, 2017, with a compliance date of February 7, 2020. Upon the compliance date, training schools will be required to register with the FMCSA's Training Provider Registry and certify that their program meets the classroom and driving standards. |

◦ | Commercial Driver's License Drug and Alcohol Clearinghouse — In December 2016, the FMCSA amended the Federal Motor Carrier Safety Regulations to establish requirements of the Commercial Driver's License Drug and Alcohol Clearinghouse, a database under its administration that will contain information about violations of the FMCSA's drug and alcohol testing program for holders of commercial driver's licenses. In addition to requiring employers to check the database for driver applicant drug and alcohol test failures, the final rule requires employers to check the database to determine |

16

whether current employees have incurred a drug or alcohol violation that would prohibit them from performing safety-sensitive functions. The final rule is effective January 4, 2017, with a compliance date of January 6, 2020.

• | Prohibiting Coercion of Commercial Motor Vehicle Drivers — In November 2015, the Prohibiting Coercion of Commercial Motor Vehicle Drivers rule became final, as published in the Federal Register and adopted by the FMCSA. The rule explicitly prohibits motor carriers from coercing drivers to violate certain FMCSA regulations, including driver hours-of-service limits, CDL regulations, drug and alcohol testing rules, and hazardous materials regulations, among others. Under the rule, drivers can report incidents of coercion to the FMCSA, who is authorized to issue penalties against the motor carrier. |

• | Speed Limiting Devices — In September 2016, the NHTSA and FMCSA proposed regulations that would require speed limiting devices on vehicles with a gross vehicle weight rating of more than 26,000 pounds for the service life of the vehicle. The speed is expected to be limited to 62, 65, or 68, but would ultimately be set by the final rule. Based on the agencies' review of the available data, limiting the speed of these heavy vehicles would reduce the severity of crashes involving these vehicles and reduce the resulting injuries and fatalities. Public comments on the proposed rule were due in November 2016. |

For safety, we electronically govern the speed of substantially all of our company tractors to a maximum of 62 miles per hour. Additionally, our owner-operator contracts include statements that owner-operators must comply with the Company's speed policy, which indicates that they must limit their speed to 67 miles per hour.

Other Regulation |

• | The TSA — In the aftermath of the September 11, 2001 terrorist attacks, federal, state, and municipal authorities implemented and continue to implement various security measures on large trucks, including checkpoints and travel restrictions. The TSA adopted regulations that require drivers applying for or renewing a license for carrying hazardous materials to obtain a TSA determination that they are not a security threat. |

• | WOTC — In December 2014, United States President, Barack Obama, signed the Tax Increase Prevention Act of 2014 ("TIPA"). Among other things, TIPA extended 50% bonus depreciation and the Work Opportunity Tax Credit ("WOTC"). In December 2015, President Obama signed the Protecting Americans from Tax Hikes ("PATH") Act of 2015. Among other things, PATH further extended 50% bonus depreciation and WOTC. The financial impact of these regulations is discussed in Note 11 in Part II, Item 8. |

Available Information |

General information about Swift is provided, free of charge, on our website, www.swifttrans.com. This website also includes our annual reports on Form 10-K with accompanying XBRL documents, quarterly reports on Form 10-Q with accompanying XBRL documents, current reports on Form 8-K, and amendments to those reports that are filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as soon as reasonably practicable once the material is electronically filed or furnished to the SEC.

ITEM 1A. | RISK FACTORS |

When evaluating our company, the following risks should be considered in conjunction with the other information contained in this annual report on Form 10-K. If we are unable to mitigate and/or are exposed to any of the following risks in the future, then there could be a material, adverse effect on our business, results of operations, or financial condition.

Strategic Risk |

The truckload industry is affected by economic and business risks that are largely beyond our control.

The truckload industry is highly cyclical, and our business is dependent on a number of factors that may have a negative impact on our results of operations, many of which are beyond our control. We believe that some of the most significant of these factors are economic changes that affect supply and demand in transportation markets, such as:

• | recessionary economic cycles, such as the period from 2007 to 2009; |

• | changes in customers' inventory levels, including shrinking product/package sizes, and in the availability of funding for their working capital; |

• | excess tractor capacity in comparison with shipping demand; and |

• | downturns in customers' business cycles. |

17

The risks associated with these factors are heightened when the United States economy is weakened. Some of the principal risks during such times, which we experienced during the most recent recession, are as follows:

• | low overall freight levels, which typically impair our asset utilization; |

• | customers with credit issues and cash flow problems; |

• | changing freight patterns from redesigned supply chains, resulting in imbalance between our capacity and customer demand; |

• | customers bidding out freight or selecting competitors that offer lower rates, in an attempt to lower their costs, forcing us to lower our rates or lose freight; and |

• | more deadhead miles incurred to obtain loads. |

We are also subject to cost increases outside our control (for example fuel and diesel prices) that could materially reduce our profitability if we are unable to increase our rates sufficiently.

In addition, events outside our control, such as strikes or other work stoppages at our facilities or at customer, port, border, or other shipping locations, actual or threatened armed conflicts or terrorist attacks, efforts to combat terrorism, military action against a foreign state or group located in a foreign state, or heightened security requirements could lead to reduced economic demand, reduced availability of credit, or temporary closing of shipping locations or United States borders.

The truckload industry is highly competitive and fragmented, which subjects us to competitive pressures pertaining to pricing, capacity, and service.

Our operating segments compete with many truckload carriers, and some LTL carriers, railroads, logistics, brokerage, freight forwarding, and other transportation companies. Additionally, some of our customers may utilize their own private fleets rather than outsourcing loads to us. Some of our competitors may have greater access to equipment, a wider range of services, greater capital resources, less indebtedness, or other competitive advantages. Numerous competitive factors could impair our ability to maintain or improve our profitability. These factors include the following:

• | Many of our competitors periodically reduce their freight rates to gain business, especially during times of reduced growth in the economy. This may make it difficult for us to maintain or increase freight rates, or may require us to reduce our freight rates, or lose freight. Additionally, it may limit our ability to maintain or expand our business. |

• | Since some of our customers also operate their own private trucking fleets, they may decide to transport more of their own freight. |

• | Some shippers have selected core carriers for their shipping needs, for which we may not be selected. |

• | Many customers periodically solicit bids from multiple carriers for their shipping needs, which may depress freight rates or result in a loss of business to competitors. |

• | The continuing trend toward consolidation in the trucking industry may result in more large carriers with greater financial resources and other competitive advantages, with which we may have difficulty competing. |