Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Zoetis Inc. | ex322-20161231.htm |

| EX-32.1 - EXHIBIT 32.1 - Zoetis Inc. | ex321-20161231.htm |

| EX-31.2 - EXHIBIT 31.2 - Zoetis Inc. | ex312-20161231.htm |

| EX-31.1 - EXHIBIT 31.1 - Zoetis Inc. | ex31120161231.htm |

| EX-23 - EXHIBIT 23 - Zoetis Inc. | ex23-20161231.htm |

| EX-21.1 - EXHIBIT 21.1 - Zoetis Inc. | exhibit2112016.htm |

| EX-12 - EXHIBIT 12 - Zoetis Inc. | ex12zoetis-20161231.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2016 | ||

or | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from __________ to __________ | ||

Commission File Number: 001-35797

Zoetis Inc. |

(Exact name of registrant as specified in its charter) |

Delaware | 46-0696167 | |

(State or other jurisdiction of | (I.R.S. Employer Identification No.) | |

incorporation or organization) | ||

10 Sylvan Way, Parsippany, New Jersey | 07054 | |

(Address of principal executive offices) | (Zip Code) | |

(973) 822-7000 |

(Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | ||

Common Stock, $0.01 par value per share | New York Stock Exchange | ||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting stock held by nonaffiliates of the registrant as of July 3, 2016, the last business day of the registrant's most recently completed second fiscal quarter, was $23,506 million. The registrant has no non-voting common stock.

The number of shares outstanding of the registrant's common stock as of February 10, 2017 was 491,964,064 shares.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the registrant’s Proxy Statement for the 2017 Annual Meeting of Shareholders (hereinafter referred to as the “2017 Proxy Statement”) are incorporated into Part III of this Form 10-K.

TABLE OF CONTENTS

Page | ||||

Item 1. | ||||

Item 1A. | ||||

Item 1B. | ||||

Item 2. | ||||

Item 3. | ||||

Item 4. | ||||

Item 5. | ||||

Item 6. | ||||

Item 7. | ||||

Item 7A. | ||||

Item 8. | ||||

Item 9. | ||||

Item 9A. | ||||

Item 9B. | ||||

Item 10. | ||||

Item 11. | ||||

Item 12. | ||||

Item 13. | ||||

Item 14. | ||||

Item 15. | ||||

Item 16. | ||||

PART I

Item 1. Business.

Overview

Zoetis Inc. is a global leader in the discovery, development, manufacture and commercialization of animal health medicines and vaccines, with a focus on both livestock and companion animals. We have a diversified business, commercializing products across eight core species: cattle, swine, poultry, sheep and fish (collectively, livestock) and dogs, cats and horses (collectively, companion animals); and within five major product categories: anti-infectives, vaccines, parasiticides, medicated feed additives and other pharmaceuticals. For more than 60 years, as a business unit of Pfizer Inc. (Pfizer), and since 2013 as an independent public company, we have been committed to enhancing the health of animals and bringing solutions to our customers who raise and care for them.

We were incorporated in Delaware in July 2012. The address of our principal executive offices is 10 Sylvan Way, Parsippany, New Jersey 07054. Unless the context requires otherwise, references to “Zoetis,” “the company,” “we,” “us” or “our” in this Annual Report on Form 10-K for the fiscal year ended December 31, 2016 (2016 Annual Report) refer to Zoetis Inc., a Delaware corporation, and its subsidiaries. In addition, unless the context requires otherwise, references to “Pfizer” in this 2016 Annual Report refer to Pfizer Inc., a Delaware corporation, and its subsidiaries.

On February 1, 2013, our Class A common stock began trading on the New York Stock Exchange (NYSE) under the symbol “ZTS.” On February 6, 2013, an initial public offering (IPO) of our Class A common stock was completed, which represented approximately 19.8% of our total outstanding shares, with Pfizer owning the remaining outstanding shares. On June 24, 2013, an exchange offer was completed whereby Pfizer shareholders exchanged a portion of Pfizer common stock for Zoetis common stock, resulting in the full separation of Zoetis and the disposal of Pfizer's entire ownership and voting interest in Zoetis.

Operating Segments

The animal health medicines and vaccines market is characterized by meaningful differences in customer needs across different regions. This is due to a variety of factors, including:

• | economic differences, such as standards of living in developed markets as compared to emerging markets; |

• | cultural differences, such as dietary preferences for different animal proteins, pet ownership preferences and pet care standards; |

• | epidemiological differences, such as the prevalence of certain bacterial and viral strains and disease dynamics; |

• | treatment differences, such as utilization of different types of medicines and vaccines, as well as the pace of adoption of new technologies; |

• | environmental differences, such as seasonality, climate and the availability of arable land and fresh water; and |

• | regulatory differences, such as standards for product approval and manufacturing. |

As a result of these differences, among other things, we organize and operate our business in two segments: the United States and International. Within each of these operating segments, we offer a diversified product portfolio for both livestock and companion animal customers so that we can capitalize on local trends and customer needs. Our operating segments are:

• | United States with revenue of $2,447 million, or 50% of total revenue for the year ended December 31, 2016; and |

• | International with revenue of $2,390 million, or 49% of total revenue for the year ended December 31, 2016. |

In addition, our Client Supply Services (CSS) organization provides contract manufacturing services to third parties and represented 1% of our total revenue for the year ended December 31, 2016.

1 |

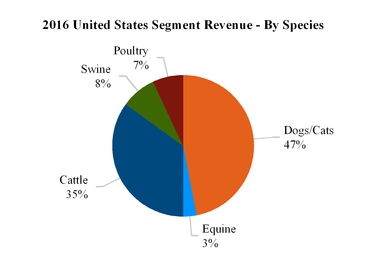

Our 2016 revenue for the United States and key international markets, together with the percentage of revenue attributable to livestock and companion animal products in those markets, is as follows:

(MILLIONS OF DOLLARS) | Revenue | Livestock | Companion Animal |

United States | $2,447 | 50% | 50% |

Australia | $157 | 62% | 38% |

Brazil | $245 | 82% | 18% |

Canada | $173 | 61% | 39% |

China | $145 | 73% | 27% |

France | $117 | 62% | 38% |

Germany | $125 | 53% | 47% |

Italy | $83 | 50% | 50% |

Japan | $127 | 47% | 53% |

Mexico | $76 | 85% | 15% |

Spain | $82 | 72% | 28% |

United Kingdom | $151 | 48% | 52% |

Other Developed | $302 | 66% | 34% |

Other Emerging | $607 | 84% | 16% |

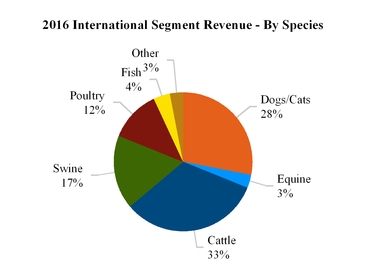

For additional information regarding our performance in each of these operating segments and the impact of foreign exchange rates, see Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations and Notes to Consolidated Financial Statements— Note 18A. Segment, Geographic and Other Revenue Information—Segment Information. Our 2016 reported revenue for each segment, by species, is as follows:

2 |

Products

Over the course of our history, we have focused on developing a diverse portfolio of animal health products, including medicines and vaccines, complemented by biodevices, diagnostics, and genetics. We refer to a single product in all brands, or its dosage forms for all species, as a product line. We have approximately 300 comprehensive product lines, including products for both livestock and companion animals across each of our major product categories.

Our livestock products primarily help prevent or treat diseases and conditions to enable the cost-effective production of safe, high-quality animal protein. Human population growth and increasing standards of living are important long-term growth drivers for our livestock products in three major ways. First, population growth and increasing standards of living drive increased demand for improved nutrition, particularly animal protein. Second, population growth leads to increased natural resource constraints driving a need for enhanced productivity. Finally, as standards of living improve, there is increased focus on food quality and safety. Livestock products represented approximately 59% of our revenue for the year ended December 31, 2016.

Our companion animal products help extend and improve the quality of life for pets; increase convenience and compliance for pet owners; and help veterinarians improve the quality of their care and the efficiency of their businesses. Growth in the companion animal medicines and vaccines sector is driven by economic development, related increases in disposable income and increases in pet ownership and spending on pet care. Companion animals are also living longer, receiving increased medical treatment and benefiting from advances in animal health medicines and vaccines. Companion animal products represented approximately 40% of our revenue for the year ended December 31, 2016.

In addition, our CSS organization provides contract manufacturing services to third parties and represented 1% of our total revenue for the year ended December 31, 2016.

Our major product categories are:

• | anti-infectives: products that prevent, kill or slow the growth of bacteria, fungi or protozoa; |

• | vaccines: biological preparations that help prevent diseases of the respiratory, gastrointestinal and reproductive tracts or induce a specific immune response; |

• | parasiticides: products that prevent or eliminate external and internal parasites such as fleas, ticks and worms; |

• | medicated feed additives: products added to animal feed that provide medicines to livestock; and |

• | other pharmaceutical products: pain and sedation, oncology, antiemetic, allergy and dermatology, and reproductive products. |

Our remaining revenue is derived from other product categories, such as nutritionals and agribusiness, as well as products and services in complementary areas, including biodevices, diagnostics, genetics.

As part of our growth strategy, through our research and development (R&D) group, we focus on the discovery and development of new chemical and biological entities, as well as product lifecycle innovation. Historically, a substantial portion of our products and revenue has been the result of product lifecycle innovation where we actively work to broaden the value of existing products by developing claims in additional species, more convenient formulations and combinations, and by expanding usage into more countries. For example, the first product in our ceftiofur line was an anti-infective approved for treating bovine respiratory disease (BRD) in cattle that was administered via intramuscular injection. Through follow-on studies and reformulations, we have expanded the product line into additional cattle claims and administration routes, as well as other species and regions. The ceftiofur product line currently includes the brands Excede®, Excenel® RTU, Excenel® RTU EZ, Excenel®, Naxcel® and Spectramast®.

Examples of our first-in-class and/or best-in-class products that we have launched in recent years and products that we believe may represent platforms for future product lifecycle innovation include (listed alphabetically):

• | Apoquel®, the first Janus kinase inhibitor for use in veterinary medicine, was approved for the control of pruritus associated with allergic dermatitis and the control of atopic dermatitis in dogs at least 12 months of age. Since January 2014, we launched Apoquel in all key markets including the United States, Europe, Japan, Brazil, and Australia and expect ongoing market launches throughout 2017; |

• | Cerenia®, the first and only product on the market to prevent vomiting due to motion sickness in dogs, was first launched in Europe in 2006, followed by the United States in 2007; it was approved to prevent vomiting in cats in 2012 in the United States and European countries. In January 2016, it was approved in the United States for intravenous administration in dogs and cats four months of age and older and for the prevention of vomiting caused by emetogenic or chemotherapeutic agents in dogs four months of age or older; |

• | CytopointTM, the first canine monoclonal antibody to help reduce the clinical signs such as itching of atopic dermatitis in dogs of any age, licensed in the United States in 2016. An injection given once every four to eight weeks, Cytopoint neutralizes interleukin - 31, a protein that has been demonstrated to trigger itching in dogs. This therapy is conditionally licensed in Canada and an application for approval in the European Union is under review; |

• | Fostera® PCV MH was introduced in November 2013 in the United States and approved in the European Union in 2015. It was developed to help protect pigs from PCVAD and enzootic pneumonia caused by M. hyopneumoniae. The one-bottle formulation of Fostera PCV MH allows the convenience of a one-dose program or the flexibility of a two-dose program; |

• | Improvac®/Improvest®/Vivax®, a protein product that works like an immunization, is currently the only product that provides a safe and effective alternative to physical castration to manage unpleasant aromas that can occur when cooking pork; launched in Australia and New Zealand in 2004, in Brazil in 2007, in certain European countries beginning in 2008, and in the United States in 2011; |

• | Inforce®3, the first vaccine for cattle that prevents respiratory disease caused by bovine respiratory syncytial virus (BRSV) while also aiding in the prevention of infectious bovine rhinotracheitis (IBR) and parainfluenza3 (PI3), launched in 2010; |

• | Palladia®, the first drug to be approved by the U.S. Food and Drug Administration (FDA) for treating cancer in dogs, launched in 2009; |

3 |

• | Simparica® (sarolaner) Chewables, a monthly chewable tablet for dogs to control fleas and ticks, was approved in the European Union and New Zealand in 2015, and in the United States, Canada, Australia, and Brazil (Simparic) in 2016; and |

• | Vanguard® and Versican Plus® are market leading vaccine lines for dogs intended to help prevent a range of diseases including those that are zoonotic. The Versican Plus line was launched in the European Union in 2014. Zoetis added new and innovative vaccines to its Vanguard line of canine vaccines with Vanguard crLyme, Vanguard Rapid Resp Intranasal, Vanguard B Oral, and Vanguard CIV H3N2. |

We pursue the development of new vaccines for emerging infectious diseases, with an operating philosophy of “first to know and fast to market.” Examples of the successful execution of this strategy include the first equine vaccine for West Nile virus in the United States and European Union; the first swine vaccine for pandemic H1N1 influenza virus in the United States; the first fully licensed vaccine to help reduce disease caused by the Georgia 08 variant of infectious bronchitis virus (IBV) in poultry; a conditionally licensed vaccine to help fight porcine epidemic diarrhea virus (PEDv) in the United States, and the first conditionally licensed vaccine to help prevent the H3N2 type of canine influenza that emerged in the United States. Examples also include the first and only vaccine to aid in the prevention of clinical symptoms of the disease caused by Hendra virus in horses, a serious zoonotic disease identified in Australia that can be fatal to horses and people; a conditionally licensed vaccine in the United States for use in poultry as an aid in the prevention of avian influenza virus H5N1; the first centrally-authorized vaccine in the European Union to reduce viremia associated with Schmallenberg virus infection in cattle and sheep; and the first live recombinant marker vaccine in the European Union and United States to prevent mortality and reduce infection caused by Classical Swine Fever in pigs. Additionally, the Pharmaq business of Zoetis is the global leader in vaccines and innovation for health products in aquaculture. In 2016, Pharmaq added to its leading Alpha Ject® vaccine line with Alpha Ject® LiVac® SRS vaccine, the first and only vaccine containing a live, attenuated version of P.salmonis to provide immunity against Salmonid Rickettsial Septicaemia (SRS), the leading cause of mortality in farmed fish in Chile.

Our diverse portfolio also includes diagnostics products such as the Witness® line of immunodiagnostic kits and, in August 2016, we expanded our diagnostic offerings into microfluidic “lab on a chip” diagnostic analyzers and tests with the acquisition of Scandinavian Micro BioDevices.

In 2016, our top selling product line, the ceftiofur line, contributed approximately 7% of our revenue. The ceftiofur line and our next three top selling products, Revolution®, Draxxin® and Apoquel®, contributed approximately 25% of our revenue. Our top ten product lines contributed 40% of our revenue.

4 |

Our product lines and products that represented approximately 1% or more of our revenue in 2016, which comprise 58% of our total revenue, are as follows (listed alphabetically):

Livestock products

Product line / product | Description | Primary species | ||

Anti-infectives | ||||

Ceftiofur injectable line | Broad-spectrum cephalosporin antibiotic active against gram-positive and gram-negative bacteria, including ß-lactamase-producing strains, with some formulations producing a single course of therapy in one injection | Cattle, sheep, swine | ||

Draxxin® | Single-dose low-volume antibiotic for the treatment and prevention of bovine and swine respiratory disease, infectious bovine keratoconjunctivitis and bovine foot rot | Cattle, swine, sheep | ||

Spectramast® | Treatment of subclinical or clinical mastitis in dry or lactating dairy cattle, delivered via intramammary infusion; same active ingredient as the ceftiofur line | Cattle | ||

Terramycin® line | Antibiotic for the treatment of susceptible infections | Cattle, poultry, sheep, swine | ||

Vaccines | ||||

Bovi-Shield® line | Aids in preventing diseases, including infectious bovine rhinotracheitis (IBR), bovine viral diarrhea (BVD) Types 1 and 2, parainfluenza3 (PI3), bovine respiratory syncytial virus (BRSV), and leptospirosis caused by Leptospira borgpetersenii, L.canicola, L grippotyphosa, L. hardjo, L. icterohaemorrhagiae, and L. pamona, depending on formulation | Cattle | ||

Rispoval® line | Aids in preventing three key viruses involved in cattle pneumonia-BRSV, PI3 virus and BVD-viruses as well as other respiratory diseases, depending on formulation | Cattle | ||

Suvaxyn® / Fostera® | Aids in preventing or controlling disease associated with major pathogens in swine such as porcine circovirus type 2 (PCV2), porcine reproductive and respiratory syndrome virus (PRRSv) and Mycoplasma hyopneumoniae, depending on formulation | Swine | ||

Parasiticides | ||||

Cydectin® | Injectable or pour-on endectocide to treat and control internal and external cattle parasites, including gastrointestinal roundworms, lungworms, cattle grubs, mites and lice | Cattle, sheep | ||

Dectomax® | Injectable or pour-on endectocide, characterized by extended duration of activity, for the treatment and control of internal and external parasite infections | Cattle, swine | ||

Medicated Feed Additives | ||||

Aureomycin® | Provides livestock producers control, treatment and convenience against a wide range of respiratory, enteric and reproductive diseases | Cattle, poultry, sheep, swine | ||

BMD® | Aids in preventing and controlling enteritis; and increases rate of weight gain and improves feed efficiency in poultry and swine | Poultry, swine | ||

Lasalocid line | Controls coccidiosis in poultry (Avatec®) and cattle (Bovatec®) and for increased rate of weight gain and improved feed efficiency in cattle | Poultry, cattle | ||

Lincomycin line | Controls necrotic enteritis; treatment of dysentery (bloody scours), control of ileitis and treatment/reduction in severity of mycoplasmal pneumonia | Swine, poultry | ||

Other | ||||

Eazi-BreedTM CIDR® | A vaginal insert that contains progesterone, used in reproductive management programs to synchronize estrus within a herd and help cows, heifers and ewes become pregnant | Cattle, sheep | ||

Embrex® devices | Devices for enhancing hatchery operations' efficiency through in ovo detection and vaccination | Poultry | ||

Lutalyse® | For estrus control or in the induction of parturition or abortion | Cattle, swine | ||

5 |

Companion animal products

Product line / product | Description | Primary species | ||

Anti-infectives | ||||

Clavamox® / Synulox® | A broad-spectrum antibiotic and the first and only potentiated penicillin approved for use in dogs and cats | Cats, dogs | ||

Convenia® | Anti-infective for the treatment of common bacterial skin infections that provides a course of treatment in a single injection | Cats, dogs | ||

Vaccines | ||||

Vanguard® L4 (4-way Lepto) | Compatible with the Vanguard line and helps protect against leptospirosis caused by Leptospira canicola, L. grippotyphosa, L. icterohaemorrhagiae and L. pomona | Dogs | ||

Vanguard® line | Aids in preventing canine distemper caused by canine distemper virus; infectious canine hepatitis caused by canine adenovirus type 1; respiratory disease caused by canine adenovirus type 2; canine parainfluenza caused by canine parainfluenza virus; canine parvoviral enteritis caused by canine parvovirus; Lyme disease and subclinical arthritis associated with Borrelia burgdorferi, the causative agent of Lyme disease; and Rapid Resp - a group of three vaccines combating infections in dogs caused by Bordetella bronchiseptica, canine parainfluenza and canine adenovirus; canine influenza vaccines; and an oral vaccine for Bordatella bronchiseptica | Dogs | ||

Parasiticides | ||||

ProHeart® | Prevents heartworm infestation; also for treatment of existing larval and adult hookworm infections | Dogs | ||

Revolution® / Stronghold® | An antiparasitic for protection against fleas, heartworm disease and ear mites in cats and dogs; sarcoptic mites and American dog tick in dogs and roundworms and hookworms for cats | Cats, dogs | ||

Other | ||||

Apoquel® | A selective inhibitor of the Janus Kinase 1 enzyme that controls pruritus associated with allergic dermatitis and control of atopic dermatitis in dogs at least 12 months of age | Dogs | ||

Cerenia® | A medication that prevents and treats acute vomiting in dogs, treats acute vomiting in cats and prevents vomiting due to motion sickness in dogs | Cats, dogs | ||

Rimadyl® | For the relief of pain and inflammation associated with osteoarthritis and for the control of postoperative pain associated with soft tissue and orthopedic surgeries | Dogs | ||

International Operations

We directly market our products in approximately 45 countries across North America, Europe, Africa, Asia, Australia and South America, and our products are sold in more than 100 countries. Operations outside the United States accounted for 49% of our total revenue for the year ended December 31, 2016. Through our efforts to establish an early and direct presence in many emerging markets, such as Brazil, China and Mexico, emerging markets contributed 22% of our revenue for the year ended December 31, 2016.

Our international businesses are subject, in varying degrees, to a number of risks inherent in carrying on business in other countries. These include, among other things, currency fluctuations, capital and exchange control regulations, expropriation and other restrictive government actions. See Item 1A. Risk Factors— Risks related to our international operations.

Sales and Marketing

Our sales organization includes sales representatives and technical and veterinary operations specialists. In markets where we do not have a direct commercial presence, we generally contract with distributors that provide logistics and sales and marketing support for our products.

Our sales representatives visit our customers, including veterinarians and livestock producers, to provide information and to promote and sell our products and services. Our technical and veterinary operations specialists, who generally have advanced veterinary medicine degrees, provide scientific consulting focused on disease management and herd management, training and education on diverse topics, including responsible product use. These direct relationships with customers allow us to understand the needs of our customers. Additionally, our sales representatives and technical and veterinary operations specialists partner with customers to provide training and support in areas of disease awareness and treatment protocols, including through the use of our products. As a result of these relationships, our sales and consulting visits are typically longer, more meaningful and provide us with better access to customer decision makers as compared to human health. As of December 31, 2016, our sales organization consisted of approximately 2,800 employees.

Our livestock and companion animal products are primarily available by prescription through a veterinarian. On a more limited basis, in certain markets, we sell certain products through local agricultural and farming retail outlets, pharmacies and pet stores. We also market our products by advertising to veterinarians, livestock producers and pet owners.

Customers

We sell our livestock products directly to a diverse set of livestock producers, including beef and dairy farmers as well as pork and poultry operations, and to veterinarians, third-party veterinary distributors and retail outlets that typically then sell the products to livestock producers. We

6 |

primarily sell our companion animal products to veterinarians or to third-party veterinary distributors that typically then sell our products to veterinarians, and in each case veterinarians then typically sell our products to pet owners. Our two largest customers, both distributors, represented approximately 13% and 7%, respectively, of our revenue for the year ended December 31, 2016, and no other customer represented more than 4% of our revenue for the same period.

Research and Development

Our research and development (R&D) operations are comprised of a dedicated veterinary medicine R&D organization, research alliances and other operations focused on the development, registration and regulatory maintenance of our products. We incurred R&D expense of $376 million in 2016, $364 million in 2015 and $396 million in 2014.

Our R&D efforts are comprised of more than 200 programs and reflect our commitment to develop better solutions. We create new insights for preventing and treating disease, and maximizing healthy performance, that result in the development of new platforms of knowledge which become the basis for continuous innovation. Leveraging internal discoveries, complemented by diverse external research collaborations, results in the delivery of novel vaccine, pharmaceutical and biopharmaceutical products to help our customers face their toughest challenges. While the development of new chemical and biological entities through new product R&D plays a critical role in our growth strategies, a significant share of our R&D investment (including regulatory functions) is focused on product lifecycle innovation. A commitment to continuous innovation, based on customer need, ensures we actively work to broaden the value of existing products by developing claims in additional species, more convenient formulations and combinations, and by expanding usage into more countries. We also create opportunities to optimize solutions through our extensive capabilities in diagnostics and genetics research, ensuring we can help our customers diagnose, predict, prevent and treat a variety of conditions.

We prioritize our R&D spending on an annual basis with the goal of aligning our research and business objectives, and do not disaggregate our R&D operations by research stage or by therapeutic area for purposes of managing our business. We make our strategic investments in R&D based on four criteria: strategic fit and importance to our current portfolio; technical feasibility of development and manufacture; return on investment; and the needs of customers and the market. A centralized portfolio management function links development plans with financial systems to build a comprehensive view of the status of project progression and spend. This view facilitates our ability to set targets for project timing and goals for investment efficiency. The allocation of our R&D investment between product lifecycle innovation and new product development, in addition to our ability to leverage the discoveries of our existing R&D and other industries, supports a cost-effective, efficient, sustainable and relatively predictable R&D process.

We regularly enter into agreements with external parties that enable us to collaborate on research programs or gain access to substrates and technologies. Some of our external partnerships involve funding from a non-governmental organization or a government grant. We are generally responsible for providing technical direction and supplemental expertise for, as well as investment in, such external partnerships. Depending on the nature of the agreement, we may act as the commercialization partner for discoveries that originate during the period of collaborative research, or we may own or have exclusive rights to any intellectual property that enables the development of proprietary products or models.

As of December 31, 2016, we employed approximately 1,000 employees in our global R&D operations. Our R&D headquarters is located in Kalamazoo, Michigan. We have R&D operations co-located with manufacturing sites in Louvain-la-Neuve, Belgium; Campinas, Brazil; Olot, Spain; Kalamazoo, Michigan; and Lincoln, Nebraska, United States. We co-locate R&D operations with manufacturing sites to facilitate the efficient transfer of production processes from our laboratories to manufacturing. In addition, we maintain R&D operations in Sydney, Australia; Zaventem, Belgium; São Paulo, Brazil; Beijing, China; Navi Mumbai, India; and Durham, North Carolina, United States. Since the acquisition of Pharmaq in 2015, we maintain R&D operations in Thanh Binh, Vietnam; Hong Ngu, Vietnam; and Oslo, Norway; and for recently acquired Scandinavian Micro Biodevices we operate a facility in Farum, Denmark. Each site is designed to meet the regulatory requirements for working with chemical or infectious disease agents.

Manufacturing and Supply Chain

Our products are manufactured at both sites operated by us and sites operated by third-party contract manufacturing organizations, which we refer to as CMOs. We have a global manufacturing network of 25 sites.

7 |

Our global manufacturing network is comprised of the following sites:

Site | Location | Site | Location | |||

Campinas | Brazil | Medolla | Italy | |||

Catania | Italy | Melbourne | Australia | |||

Charles City | Iowa, U.S. | Olot | Spain | |||

Chicago Heights | Illinois, U.S. | Oslo | Norway | |||

Durham | North Carolina, U.S. | Overhalla | Norway | |||

Eagle Grove | Iowa, U.S. | Salisbury | Maryland, U.S. | |||

Farum(a) | Denmark | San Diego | California, U.S. | |||

Guarulhos | Brazil | Suzhou | China | |||

Jilin(b) | China | Wellington | New Zealand | |||

Kalamazoo | Michigan, U.S. | White Hall | Illinois, U.S. | |||

Lincoln | Nebraska, U.S. | Willow Island | West Virginia, U.S. | |||

London | Ontario, Canada | Yantai | China | |||

Louvain-la-Neuve | Belgium | |||||

(a) | In August 2016, Zoetis acquired a veterinary diagnostics business in Denmark. |

(b) | This site is operated by our China joint venture, Jilin Zoetis Guoyuan Animal Health Company, Ltd. |

We own all of these sites, with the exception of our facilities in Medolla (Italy), Melbourne (Australia) and San Diego, California (U.S), which are leased sites.

In addition to our global manufacturing network and our CMOs, Pfizer continues to manufacture products for us at five Pfizer sites pursuant to a master manufacturing and supply agreement.

Our global manufacturing and supply chain is supported by a network of CMOs. As of December 31, 2016, this network was comprised of approximately 200 CMOs, including those centrally managed as well as local CMOs.

We select CMOs based on several factors: (i) their ability to reliably supply products or materials that meet our quality standards at an optimized cost; (ii) their access to niche products and technologies; (iii) capacity; and (iv) financial efficiency analyses. Our regional and global manufacturing teams seek to ensure that all of the CMOs we use adhere to our standards of manufacturing quality.

We purchase certain raw materials necessary for the commercial production of our products from a variety of third-party suppliers. We utilize logistics service providers as a part of our global supply chain, primarily for shipping and logistics support.

We intend to continue our efficiency improvement programs in our manufacturing and supply chain organization, including Six Sigma and Lean capabilities, which are processes intended to improve manufacturing efficiency. We have strong globally managed and coordinated quality control and quality assurance programs in place at our global manufacturing network sites, and we regularly inspect and audit our global manufacturing network and CMO sites. We recently conducted a review of our global manufacturing and supply network to improve efficiency and have announced plans to exit or sell certain sites. Over the last two years, we exited our manufacturing sites in Haridwar (India), Hsinchu (Taiwan), Laurinburg, North Carolina (U.S), Longmont, Colorado (U.S.), Shenzhou (China) and Van Buren, Arkansas (U.S.) as part of our operational efficiency program and supply network strategy. See Operational Efficiency Program and Supply Network Strategy.

Competition

Although our business is the largest based on revenue in the animal health medicines and vaccines industry, we face competition in the regions in which we compete. Principal drivers of competition vary depending on the particular region, species, product category and individual product, and include new product development, quality, price, service and promotion to veterinary professionals, pet owners and livestock producers.

Our primary competitors include animal health medicines and vaccines companies such as Boehringer Ingelheim Vetmedica Inc., the animal health division of Boehringer Ingelheim GmbH, which acquired Merial, former animal health division of Sanofi S.A., in January 2017; Merck Animal Health, the animal health division of Merck & Co., Inc.; Elanco, the animal health division of Eli Lilly and Company; and Bayer Animal Health, the animal health division of Bayer AG. There are also several new start-up companies working in the animal health area. In addition, we compete with hundreds of other producers of animal health products throughout the world.

The level of competition from generic products varies from market to market. For example, the level of generic competition is higher in Europe and certain emerging markets than in the United States. Unlike in the human health market, there is no large, well-capitalized company focused on generic animal health products that exists as a global competitor in the industry. The reasons for this include the relatively smaller average market size of each product opportunity, the importance of direct distribution and education to veterinarians and livestock producers and the primarily self-pay nature of the business. In addition, companion animal health products are often directly prescribed and dispensed by veterinarians.

The importance of quality and safety concerns to pet owners, veterinarians and livestock producers also contributes to animal health brand loyalty. As a result, we believe that significant brand loyalty to products often continues after the loss of patent-based and regulatory exclusivity.

8 |

Intellectual Property

Our technology, brands and other intellectual property are important elements of our business. We rely on patent, trademark, copyright and trade secret laws, as well as regulatory exclusivity periods and non-disclosure agreements to protect our intellectual property rights. Our policy is to vigorously protect, enforce and defend our rights to our intellectual property, as appropriate.

Our product portfolio enjoys the protection of approximately 4,800 granted patents and 1,700 pending patent applications, filed in more than 60 countries, with a focus on our major markets, including Australia, Brazil, Canada, China, Europe, Japan and the United States, as well as other countries with strong patent systems. Many of the patents and patent applications in our portfolio are the result of our in-house research and development, while other patents and patent applications in our portfolio were wholly or partially developed by third parties and are licensed to Zoetis.

Patents for individual products expire at different times based on the date of the patent filing (or sometimes the date of patent grant) and the legal term of patents in the countries where such patents are obtained. The active ingredient of Draxxin, tulathromycin, is covered by both compound and formulation patents in the United States, Europe, Canada, Australia and other key markets, with terms that expire between May 2019 and January 2021 in the United States, between November 2018 and November 2020 in Europe, and between May 2018 and November 2020 in Canada and Australia. Several patents covering the ceftiofur antibiotic product line (Excede) began expiring in the United States in 2015. However, various formulation and use patents relevant to the product line extend through to 2024. The compound patent for the selamectin, the active ingredient in our parasiticide Revolution, expired in 2014. Again, we have process and formulation patents covering this product which expire in important markets in 2018 and 2019, respectively. The patent for the active ingredient of Convenia has expired, however, there are formulation patents relevant to the product line which expire between November 2022 and January 2024. The patent relating to the formulation of Orbeseal expires in December 2017. Zoetis typically enforces all of its patents.

Additionally, many of our vaccine products are based on proprietary master seeds and proprietary or patented adjuvant formulations. We actively seek to protect our proprietary information, including our trade secrets and proprietary know-how, including by seeking to require our employees, consultants, advisors and partners to enter into confidentiality agreements and other arrangements upon the commencement of their employment or engagement.

As a result of our separation from Pfizer, where necessary Pfizer has licensed to us the right to use certain intellectual property rights in the animal health field. We license to Pfizer the right to use certain of our trademarks and substantially all of our other intellectual property rights in the human health field and all other fields outside of animal health. In addition, Pfizer granted us a perpetual license to use certain of Pfizer's product name trademarks.

We seek to file and maintain trademarks around the world based on commercial activities in most regions where we have, or desire to have, a business presence for a particular product or service. We currently maintain more than 10,000 trademark applications and registrations in major regions, identifying goods and services dedicated to the care of livestock and companion animals.

Operational Efficiency Program and Supply Network Strategy

During 2015, we launched a comprehensive operational efficiency program, which was incremental to the supply network strategy that was previously announced. These initiatives have focused on reducing complexity in our product portfolios, changing our selling approach in certain markets and reducing our presence in certain countries, and planning to sell or exit 10 manufacturing sites over the long term. As of December 31, 2016, we divested or exited three U.S. manufacturing sites, two international manufacturing sites, and our 55 percent ownership share of a Taiwan joint venture, inclusive of its related manufacturing site. We are also continuing to optimize our resource allocation and efficiency by reducing resources associated with non-customer facing activities and operating more efficiently as a result of less internal complexity and more standardization of processes.

As part of this initiative, we expect to reduce certain positions through divestitures, normal attrition and involuntary terminations by approximately 2,000 to 2,500, subject to consultations with works councils and unions in certain countries. As of December 31, 2016, approximately 1,800 positions have been eliminated and additional reductions are expected primarily over the next six months.

Regulatory

The sale of animal health products is governed by the laws and regulations specific to each country in which we sell our products. To maintain compliance with these regulatory requirements, we have established processes, systems and dedicated resources with end-to-end involvement from product concept to launch and maintenance in the market. Our regulatory function actively seeks to engage in dialogue with various global agencies regarding their policies that relate to animal health products. In the majority of our markets, the relevant animal health authority is separate from those governing human medicinal products.

United States

United States Food and Drug Administration (FDA). The regulatory body that is responsible for the regulation of animal health pharmaceuticals in the United States is the Center for Veterinary Medicine (CVM), housed within the FDA. All manufacturers of animal health pharmaceuticals must show their products to be safe, effective and produced by a consistent method of manufacture as defined under the Federal Food, Drug and Cosmetic Act. The FDA's basis for approving a drug application is documented in a Freedom of Information Summary. Post-approval monitoring of products is required by law, with reports being provided to the CVM's Surveillance and Compliance group. Reports of product quality defects, adverse events or unexpected results are produced in accordance with the law. Additionally, we are required to submit all new information for a product, regardless of the source.

9 |

United States Department of Agriculture (USDA). The regulatory body in the United States for veterinary vaccines is the USDA. The USDA's Center for Veterinary Biologics is responsible for the regulation of animal health vaccines, including immunotherapeutics. All manufacturers of animal health biologicals must show their products to be pure, safe, effective and produced by a consistent method of manufacture as defined under the Virus Serum Toxin Act. Post-approval monitoring of products is required. Reports of product quality defects, adverse events or unexpected results are produced in accordance with the agency requirements.

Environmental Protection Agency (EPA). The main regulatory body in the United States for veterinary pesticides is the EPA. The EPA's Office of Pesticide Programs is responsible for the regulation of pesticide products applied to animals. All manufacturers of animal health pesticides must show their products will not cause “unreasonable adverse effects to man or the environment” as stated in the Federal Insecticide, Fungicide, and Rodenticide Act. Within the United States, pesticide products that are approved by the EPA must also be approved by individual state pesticide authorities before distribution in that state. Post-approval monitoring of products is required, with reports provided to the EPA and some state regulatory agencies.

In addition, the U.S. Foreign Corrupt Practices Act (FCPA) prohibits U.S. corporations and their representatives from offering, promising, authorizing or making payments to any foreign government official, government staff member, political party or political candidate in an attempt to obtain or retain business abroad. The scope of the FCPA includes interactions with certain healthcare professionals in many countries. Other countries have enacted similar anti-corruption laws and/or regulations.

Outside the United States

European Union (EU). The European Medicines Agency (EMA) is the centralized regulatory agency of the EU, located in London. The agency is responsible for the scientific evaluation of medicines developed by healthcare companies seeking centralized approval for use in the EU. The agency has a veterinary review section distinct from the medical review section. The Committee for Veterinary Medicinal Products (CVMP) is responsible for scientific and technical review of the submissions for innovative pharmaceuticals, biopharmaceuticals and vaccines. After the CVMP issues a positive opinion on the approvability of a product, the EU commission reviews the opinion and, if they agree with the CVMP, they grant the product market authorization. Once granted by the European Commission, a centralized marketing authorization is valid in all EU and European Economic Area-European Free Trade Association states. Products can also be registered in the EU via a decentralized route under the supervision of the Co-ordination Group for Mutual Recognition and Decentralized Procedures - Veterinary (CMDv). This co-ordination group is composed of one representative per member state from each national regulatory agency, including Norway, Iceland and Liechtenstein. The CMDv reviews submissions of pharmaceuticals and vaccines for authorization of a veterinary product in two or more member states in accordance with the mutual recognition or the decentralized procedure. A series of Regulations, Directives, Guidelines and EU Pharmacopeia Monographs provide the requirements for product approval in the EU. In general, these requirements are similar to those in the United States, requiring demonstrated evidence of, safety, efficacy, and quality/consistency of manufacturing processes.

Brazil. The Ministry of Agriculture, Livestock Production and Supply (MAPA) is the regulatory body in Brazil that is responsible for the regulation and control of pharmaceuticals, biologicals and medicated feed additives for animal use. MAPA's regulatory activities are conducted through the Secretary of Agricultural Defense and its Livestock Products Inspection Department. In addition, regulatory activities are conducted at a local level through the Federal Agriculture Superintendence. These activities include the inspection and licensing of both manufacturing and commercial establishments for veterinary products, as well as the submission, review and approval of pharmaceuticals, biologicals and medicated feed additives. MAPA is one of the most active regulatory agencies in Latin America, having permanent seats at several international animal health forums, such as Codex Alimentarius, World Organization for Animal Health and Committee of Veterinary Medicines for the Americas. MAPA was also invited to be a Latin American representative at meetings of the International Cooperation on Harmonisation of Technical Requirements for Registration of Veterinary Medicinal Products (VICH). Several normative instructions issued by MAPA have set regulatory trends in Latin America.

Australia. The Australian Pesticides and Veterinary Medicines Authority (APVMA) is an Australian government statutory authority established in 1993 to centralize the registration of all agricultural and veterinary products into the Australian marketplace. Previously each State and Territory government had its own system of registration. The APVMA assesses applications from companies and individuals seeking registration so they can supply their product to the marketplace. Applications undergo rigorous assessment using the expertise of the APVMA's scientific staff and drawing on the technical knowledge of other relevant scientific organizations, Commonwealth government departments and state agriculture departments. If the product works as intended and the scientific data confirms that when used as directed on the product label it will have no harmful or unintended effects on people, animals, the environment or international trade, the APVMA will register the product. As well as registering new agricultural and veterinary products, the APVMA reviews older products that have been on the market for a substantial period of time to ensure they still do the job users expect and are safe to use. The APVMA also reviews registered products when particular concerns are raised about their safety and effectiveness. The review of a product may result in confirmation of its registration, or it may see registration continue with some changes to the way the product can be used. In some cases the review may result in the registration of a product being canceled and the product taken off the market.

Rest of world. Country-specific regulatory laws have provisions that include requirements for certain labeling, safety, efficacy and manufacturers' quality control procedures (to assure the consistency of the products), as well as company records and reports. With the exception of the EU, most other countries' regulatory agencies will generally refer to the FDA, USDA, EU and other international animal health entities, including the World Organization for Animal Health, Codex Alimentarius, in establishing standards and regulations for veterinary pharmaceuticals and vaccines.

Global policy and guidance

Joint FAO/WHO Expert Committee on Food Additives. The Joint FAO/WHO Expert Committee on Food Additives is an international expert scientific committee that is administered jointly by the Food and Agriculture Organization of the United Nations (FAO) and the World Health Organization (WHO). They provide a risk assessment/safety evaluation of residues of veterinary drugs in animal products, exposure and residue definition and maximum residue limit proposals for veterinary drugs. We work with them to establish acceptable safe levels of residual product in food-producing animals after treatment. This in turn enables the calculation of appropriate withdrawal times for our products prior to an animal entering the food chain.

10 |

Advertising and promotion review. Promotion of prescription animal health products is controlled by regulations in many countries. These rules generally restrict advertising and promotion to those claims and uses that have been reviewed and endorsed by the applicable agency. We conduct a review of promotion materials for compliance with the local and regional requirements in the markets where we sell animal health products.

Food Safety Inspection Service/generally recognized as safe. The FDA is authorized to determine the safety of substances (including “generally recognized as safe” substances, food additives and color additives), as well as prescribing safe conditions of use. However, although the FDA has the responsibility for determining the safety of substances, the Food Safety and Inspection Service, the public health agency in the USDA, still retains, under the tenets of the Federal Meat Inspection Act and the Poultry Products Inspection Act and their implementing regulations, the authority to determine that new substances and new uses of previously approved substances are suitable for use in meat and poultry products.

International Cooperation on Harmonisation of Technical Requirements for Registration of Veterinary Medicinal Products (VICH). VICH is a trilateral (EU-Japan-USA) program aimed at harmonizing technical requirements for veterinary product registration. The objectives of the VICH are as follows:

• | Establish and implement harmonized technical requirements for the registration of veterinary medicinal products in the VICH regions, which meet high quality, safety and efficacy standards and minimize the use of test animals and costs of product development. |

• | Provide a basis for wider international harmonization of registration requirements through the VICH Outreach Forum. |

• | Monitor and maintain existing VICH guidelines, taking particular note of the ICH work program and, where necessary, update these VICH guidelines. |

• | Ensure efficient processes for maintaining and monitoring consistent interpretation of data requirements following the implementation of VICH guidelines. |

• | By means of a constructive dialogue between regulatory authorities and industry, provide technical guidance enabling response to significant emerging global issues and science that impact on regulatory requirements within the VICH regions. |

Employees

As of December 31, 2016, we had approximately 9,000 employees worldwide, which included approximately 4,000 employees in the United States and approximately 5,000 in other jurisdictions. Some of these employees are members of unions, works councils, trade associations or are otherwise subject to collective bargaining agreements, including approximately 50 union employees in the United States.

Environmental, Health and Safety

We are subject to various federal, state, local and foreign environmental, health and safety laws and regulations. These laws and regulations govern matters such as the emission and discharge of hazardous materials into the ground, air or water; the generation, use, storage, handling, treatment, packaging, transportation, exposure to, and disposal of hazardous and biological materials, including recordkeeping, reporting and registration requirements; and the health and safety of our employees. Due to our operations, these laws and regulations also require us to obtain, and comply with, permits, registrations or other authorizations issued by governmental authorities. These authorities can modify or revoke our permits, registrations or other authorizations and can enforce compliance through fines and injunctions.

Certain environmental laws, such as the U.S. Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended (CERCLA), impose joint and several liability, without regard to fault, for cleanup costs on persons who disposed of or released hazardous substances into the environment, including at third-party sites or offsite disposal locations, or that currently own or operate (or formerly owned or operated) sites where such a release occurred. In addition to clean-up actions brought by federal, state, local and foreign governmental entities, private parties could raise personal injury or other claims against us due to the presence of, or exposure to, hazardous materials on, from or otherwise relating to such a property.

We have made, and intend to continue to make, necessary expenditures for compliance with applicable environmental, health and safety laws and regulations. We are also a party to proceedings in which the primary relief sought is the cost of past and/or future remediation, or remedial measures to mitigate or remediate pollution. In connection with such proceedings, and otherwise, we are investigating and cleaning up environmental contamination from past industrial activity at certain sites, or financing other parties' completion of such activities. As a result, we incurred capital and operational expenditures in 2016 for environmental compliance purposes and for the clean-up of certain past industrial activities as follows:

• | environmental-related capital expenditures - $4 million; and |

• | other environmental-related expenditures - $16 million. |

However, we may not have identified all of the potential environmental liabilities relating to our current and former properties, or those liabilities associated with off-site disposal locations. Such liability could materially adversely affect our operating results and financial condition. Furthermore, regulatory agencies are showing increasing concern over the impact of animal health products and livestock operations on the environment. This increased regulatory scrutiny may necessitate that additional time and resources be spent to address these concerns in both new and existing products.

In connection with past acquisitions and divestitures, we have undertaken certain indemnification obligations that require us, or may require us in the future, to conduct or finance environmental cleanups at sites that we no longer own or operate. We have also entered into indemnification agreements in which we are being indemnified for various environmental cleanups; however, such indemnities are limited in both time and scope and may be further limited in the presence of new information, or may not be available at all.

11 |

While we cannot predict with certainty our future capital expenditures or operating costs for environmental compliance or remediation of contaminated sites, we have no reason to believe that they will have a material adverse effect on our operating results or financial condition.

Available Information

The company's Internet website address is www.zoetis.com. On our website, the company makes available, free of charge, its annual, quarterly and current reports, including amendments to such reports, as soon as reasonably practicable after the company electronically files such material with, or furnishes such material to, the Securities and Exchange Commission (SEC).

Also available on our website is information relating to corporate governance at Zoetis and our Board of Directors, including as follows: our Corporate Governance Principles; Director Qualification Standards; Zoetis Policies on Business Conduct (for all of our employees, including our Chief Executive Officer, Chief Financial Officer, Principal Accounting Officer, and Controller); Code of Business Conduct and Ethics for our Directors; Board Committees and Committee Charters; and ways to communicate by email with our Directors. We will provide any of the foregoing information without charge upon written request to our Corporate Secretary, Zoetis Inc., 10 Sylvan Way, Parsippany, New Jersey 07054. Information relating to shareholder services is also available on our website. We will disclose any future amendments to, or waivers from, provisions of these ethics policies and standards affecting our Chief Executive Officer, Chief Financial Officer, Principal Accounting Officer, and Controller on our website as promptly as practicable, as may be required under applicable SEC and NYSE rules.

We use our website (www.zoetis.com) as a means of disclosing material non-public information and for complying with our disclosure obligations under Regulation Fair Disclosure promulgated by the SEC. These disclosures are included in the “Investors” and “News & Media” sections of our website. Accordingly, investors should monitor these portions of our website, in addition to following our press releases, SEC filings and public conference calls and webcasts.

The information contained on our website does not constitute, and shall not be deemed to constitute, a part of this 2016 Annual Report, or any other report we file with, or furnish to, the SEC. Our references to the URLs for websites are intended to be inactive textual references only.

Item 1A. Risk Factors.

In addition to the other information set forth in this 2016 Annual Report, any of the factors described below could materially adversely affect our operating results, financial condition and liquidity, which could cause the trading price of our securities to decline.

This report contains “forward-looking” statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements reflect our current views with respect to, among other things, future events and performance. We generally identify forward-looking statements by words such as “anticipate,” “estimate,” “could,” “expect,” “intend,” “project,” “plan,” “predict,” “believe,” “seek,” “continue,” “outlook,” "objective," "target," “may,” “might,” “will,” “should,” “can have,” “likely” or the negative version of these words or comparable words or by using future dates in connection with any discussion of future performance, actions or events. Forward-looking statements are based on beliefs and assumptions made by management using currently available information. These statements are not guarantees of future performance, actions or events.

In particular, forward-looking statements include statements relating to our indebtedness, our ability to make interest and principal payments on our indebtedness, our ability to satisfy the covenants contained in our indebtedness, the redemption of our senior notes, expectations regarding indebtedness, the repurchase of shares, future use of cash and dividend payments, future actions, business plans or prospects, prospective products, product approvals or products under development, R&D costs, timing and likelihood of success, future operating or financial performance, future results of current and anticipated products and services, strategies, sales efforts, expenses, production efficiencies, production margins, interest rates, tax rates, changes in tax regimes and laws, foreign exchange rates, growth in emerging markets, the outcome of contingencies, such as legal proceedings, our agreements with Pfizer, the expected timing and content of regulatory actions, government regulation and financial results. Forward-looking statements are subject to risks and uncertainties, many of which are beyond our control, and are potentially inaccurate assumptions. However, there may also be other risks that we are unable to predict at this time. If one or more of these risks or uncertainties materialize, or if management's underlying beliefs and assumptions prove to be incorrect, actual results may differ materially from those contemplated by a forward-looking statement. You should not put undue reliance on forward-looking statements. Forward-looking statements speak only as of the date on which they are made.

We undertake no obligation to publicly update forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law or by the rules and regulations of the SEC. You are advised, however, to consult any further disclosures we make on related subjects in our Form 10-Q and 8-K reports and our other filings with the SEC. We note these factors for investors as permitted by the Private Securities Litigation Reform Act of 1995. You should understand that it is not possible to predict or identify all such factors. Consequently, you should not consider the following to be a complete discussion of all potential risks or uncertainties.

Risks related to our business and industry

Restrictions and bans on the use of antibacterials in food-producing animals may become more prevalent.

The issue of the potential transfer of increased antibacterial resistance in bacteria from food-producing animals to human pathogens, and the causality of that transfer, continue to be the subject of global scientific and regulatory discussion. Antibacterials refer to small molecules that can be used to treat or prevent bacterial infections and are a sub-categorization of the products that make up our anti-infectives and medicated feed additives portfolios. In some countries, this issue has led to government restrictions and bans on the use of specific antibacterials in some food-producing animals, regardless of the route of administration (in feed or injectable). These restrictions are more prevalent in countries where animal protein is plentiful and governments are willing to take action even when there is scientific uncertainty. Our total revenue attributable to antibacterials for livestock was approximately $1.3 billion for the year ended December 31, 2016.

12 |

For example, in December 2013, the FDA announced final guidance establishing procedures for the voluntary phase-out in the United States over a three-year period of the use of medically important antibacterials in animal feed for growth promotion in food production animals (medically important antibacterials include classes that are prescribed in animal and human health). The guidance provides for continued use of antibacterials in food producing animals for treatment, control and under certain circumstances for prevention of disease, all under the supervision of a veterinarian. The FDA indicated that it took this action to help preserve the efficacy of medically important antibacterials to treat infections in humans. As part of those efforts, stricter regulations governing the administration of medically important antibiotics have recently come into effect. As of January 1, 2017, the use of medically important antibiotics in the water or feed of food production animals now requires written authorization by a licensed veterinarian. Zoetis supports the FDA's efforts to voluntarily phase out growth promotion indications for medically important antibiotics in food producing animals and is complying with procedures outlined in the December 2013 FDA guidance. In addition, in October 2014, the French Parliament passed a law that prohibits rebates and discounts on antibiotics and requires the reporting of antibiotics sold to and agreements entered into with certain animal healthcare providers (including veterinarians, veterinary schools, pharmacists and students). The Parliament indicated that the law is in response to a government initiative aimed at fighting antimicrobial resistance in animals and reducing the use of certain categories of antibiotics by 25% (compared to 2013) by December 31, 2016.

We cannot predict whether antibacterial resistance concerns will result in additional restrictions or bans, expanded regulations or public pressure to discontinue or reduce use of antibacterials in food-producing animals, which could materially adversely affect our operating results and financial condition.

Perceived adverse effects on human health linked to the consumption of food derived from animals that utilize our products could cause a decline in the sales of such products.

Our livestock business depends heavily on a healthy and growing livestock industry. If the public perceives a risk to human health from the consumption of the food derived from animals that utilize our products, there may be a decline in the production of such food products and, in turn, demand for our products. For example, livestock producers may experience decreased demand for their products or reputational harm as a result of evolving consumer views of animal rights, nutrition, health-related or other concerns. Any reputational harm to the livestock industry may also extend to companies in related industries, including our company. Adverse consumer views related to the use of one or more of our products in livestock also may result in a decrease in the use of such products and could have a material adverse effect on our operating results and financial condition.

Increased regulation or decreased governmental financial support relating to the raising, processing or consumption of food-producing animals could reduce demand for our livestock products.

Companies in the livestock industries are subject to extensive and increasingly stringent regulations. If livestock producers are adversely affected by new regulations or changes to existing regulations, they may reduce herd sizes or become less profitable and, as a result, they may reduce their use of our products, which may materially adversely affect our operating results and financial condition. Furthermore, new or more stringent regulations could, directly or indirectly, impact the use of one or more of our products. More stringent regulation of the livestock industry or our products could have a material adverse effect on our operating results and financial condition. Also, many food-producing companies, including livestock producers, benefit from governmental subsidies, and if such subsidies were to be reduced or eliminated, these companies may become less profitable and, as a result, may reduce their use of our products.

An outbreak of infectious disease carried by animals could negatively affect the sale and production of our products.

Sales of our livestock products could be materially adversely affected by the outbreak of disease carried by animals, which could lead to the widespread death or precautionary destruction of animals as well as the reduced consumption and demand for animal protein. In addition, outbreaks of disease carried by animals may reduce regional or global sales of particular animal-derived food products or result in reduced exports of such products, either due to heightened export restrictions or import prohibitions, which may reduce demand for our products due to reduced herd or flock sizes. In recent years, outbreaks of various diseases, including avian influenza, foot-and-mouth disease, bovine spongiform encephalopathy (otherwise known as BSE or mad cow disease) or porcine epidemic diarrhea virus (otherwise known as PEDv), have impacted the animal health business. For example, incidences of BSE in the United States and Brazil in 2012 led certain countries to implement additional inspections of, or suspend the importation of, U.S. and Brazilian beef. Similarly, outbreaks of highly pathogenic H5 avian flu affected (infected or exposed) 48 million birds in the United States in 2014 and 2015, and significantly impacted the egg and turkey industry. The discovery of additional cases of any of these, or new, diseases may result in additional restrictions on animal proteins, reduced herd sizes, or reduced demand for, animal protein, which may have a material adverse effect on our operating results and financial condition. Also, the outbreak of any highly contagious disease near our main production sites could require us to immediately halt production of our products at such sites or force us to incur substantial expenses in procuring raw materials or products elsewhere.

Consolidation of our customers and distributors could negatively affect the pricing of our products.

Veterinarians and livestock producers are our primary customers. In recent years, there has been a trend towards the concentration of veterinarians in large clinics and hospitals. In addition, livestock producers, particularly swine and poultry producers, and our distributors, have seen recent consolidation in their industries. Furthermore, we have seen the expansion of larger cross-border corporate customers and an increase in the consolidation of buying groups (cooperatives of veterinary practices that leverage volume to pursue discounts from manufacturers). The pace of consolidation and structure of markets varies greatly across geographies. If these trends towards consolidation continue, these customers and distributors could attempt to improve their profitability by leveraging their buying power to obtain favorable pricing. The resulting decrease in our prices could have a material adverse effect on our operating results and financial condition.

Our business may be negatively affected by weather conditions and the availability of natural resources.

The animal health industry and demand for many of our animal health products in particular regions are affected by weather conditions, as usage of our products follows varying weather patterns and weather-related pressures from pests, such as ticks. As a result, we may experience regional and seasonal fluctuations in our results of operations.

13 |

In addition, veterinary hospitals and practitioners depend on visits from and access to animals under their care. Veterinarians’ patient volume and ability to operate could be adversely affected if they experience prolonged snow, ice or other weather conditions, particularly in regions not accustomed to sustained inclement weather. Furthermore, livestock producers depend on the availability of natural resources, including large supplies of fresh water. Their animals' health and their ability to operate could be adversely affected if they experience a shortage of fresh water due to human population growth or floods, droughts or other weather conditions. In the event of adverse weather conditions or a shortage of fresh water, veterinarians or livestock producers may purchase less of our products.

For example, the widespread drought that impacted the United States in 2011, 2012 and in some regions in 2013 was considered the worst in many years, resulting in a reduction in the total cow herd in 2013. Droughts such as this one can lead to a decrease in harvested corn and higher corn prices, which may impact the profitability of livestock producers of cattle, pork and poultry. Higher corn prices may contribute to reductions in herd or flock sizes that may result in reduced spending on animal health products. In addition, droughts can lead to reduced availability of grazing pastures, forcing cattle producers to cull their herds. Fewer heads of cattle could result in reduced demand for our products. A prolonged drought could have a material adverse effect on our operating results and financial condition.

Our business is subject to risk based on global economic conditions.

Macroeconomic, business and financial disruptions could have a material adverse effect on our operating results, financial condition and liquidity. Certain of our customers and suppliers could be affected directly by an economic downturn and could face credit issues or cash flow problems that could give rise to payment delays, increased credit risk, bankruptcies and other financial hardships that could decrease the demand for our products or hinder our ability to collect amounts due from customers. For example, the economic downturns experienced in many markets across the globe have had an impact on certain of our customers and, as a result, on our operating results in those affected markets. If one or more of our large customers, including distributors, discontinue their relationship with us as a result of economic conditions or otherwise, our operating results and financial condition may be materially adversely affected. In addition, economic concerns may cause some pet owners to forgo or defer visits to veterinary practices or could reduce their willingness to treat pet health conditions or even to continue to own a pet. Furthermore, our exposure to credit and collectability risk is higher in certain international markets and our ability to mitigate such risks may be limited. While we have procedures to monitor and limit exposure to credit and collectability risk, there can be no assurances such procedures will effectively limit such risk and avoid losses.

Our business is subject to risk based on customer exposure to rising costs and reduced customer income.

Feed, fuel and transportation and other key costs for livestock producers may increase or animal protein prices or sales may decrease. Either of these trends could cause deterioration in the financial condition of our livestock product customers, potentially inhibiting their ability to purchase our products or pay us for products delivered. Our livestock product customers may offset rising costs by reducing spending on our products, including by switching to lower-cost alternatives to our products. In addition, concerns about the financial resources of pet owners also could cause veterinarians to alter their treatment recommendations in favor of lower-cost alternatives to our products. These shifts could result in a decrease in sales of our companion animal products, especially in developed countries where there is a higher rate of pet ownership.

Changes in distribution channels for companion animal products could negatively impact our market share, margins and distribution of our products.