Attached files

| file | filename |

|---|---|

| EX-10.7 - FORM OF PERFORMANCE UNIT AGREEMENT - AMGEN INC | amgn-ex107_20161231x10k.htm |

| EX-32 - SECTION 1350 CERTIFICATIONS - AMGEN INC | amgn-ex32_20161231x10k.htm |

| EX-31 - RULE 13A-14(A) CERTIFICATIONS - AMGEN INC | amgn-ex31_20161231x10k.htm |

| EX-21 - SUBSIDIARIES OF THE COMPANY - AMGEN INC | amgn-ex21_20161231x10k.htm |

| EX-10.32 - AMENDMENT NO. 2 TO COLLABORATION AND LICENSE AGREEMENT - AMGEN INC | amgn-ex1032_20161231x10k.htm |

| EX-10.20 - AGREEMENT BETWEEN AMGEN INC. AND MS. LORI A. JOHNSTON - AMGEN INC | amgn-ex1020_20161231x10k.htm |

| EX-10.5 - FORM OF GLOBAL RSU AGREEMENT - AMGEN INC | amgn-ex105_20161231x10k.htm |

| EX-10.4 - FORM OF STOCK OPTION AGREEMENT - AMGEN INC | amgn-ex104_20161231x10k.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 001-37702

Amgen Inc.

(Exact name of registrant as specified in its charter)

Delaware | 95-3540776 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

One Amgen Center Drive, | 91320-1799 | |

Thousand Oaks, California | (Zip Code) | |

(Address of principal executive offices) | ||

(805) 447-1000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common stock, $0.0001 par value | The NASDAQ Global Select Market | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or Section 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

(Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes ¨ No ý

The approximate aggregate market value of voting and non-voting stock held by non-affiliates of the registrant was $101,183,706,509 as of June 30, 2016.(A)

(A) | Excludes 83,869,173 shares of common stock held by directors and executive officers, and any stockholders whose ownership exceeds ten percent of the shares outstanding, at June 30, 2016. Exclusion of shares held by any person should not be construed to indicate that such person possesses the power, directly or indirectly, to direct or cause the direction of the management or policies of the registrant, or that such person is controlled by or under common control with the registrant. |

736,452,791

(Number of shares of common stock outstanding as of February 9, 2017)

DOCUMENTS INCORPORATED BY REFERENCE

Specified portions of the registrant’s Proxy Statement with respect to the 2017 Annual Meeting of stockholders to be held May 19, 2017, are incorporated by reference into Part III of this annual report.

INDEX

Page No. | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

i

PART I

Item 1. | BUSINESS |

Amgen Inc. (including its subsidiaries, referred to as “Amgen,” “the Company,” “we,” “our” or “us”) is committed to unlocking the potential of biology for patients suffering from serious illnesses by discovering, developing, manufacturing and delivering innovative human therapeutics. This approach begins by using tools like advanced human genetics to unravel the complexities of disease and understand the fundamentals of human biology.

Amgen focuses on areas of high unmet medical need and leverages its expertise to strive for solutions that improve health outcomes and dramatically improve people’s lives. A biotechnology pioneer, Amgen has grown to be one of the world’s leading independent biotechnology companies, has reached millions of patients around the world and is developing a pipeline of medicines with breakaway potential.

Our strategy is to develop innovative medicines in six focused therapeutic areas that meet important unmet medical needs in addressing serious illness. We have a presence in approximately 100 countries worldwide focusing on: oncology/hematology, cardiovascular disease, inflammation, bone health, nephrology and neuroscience.

Amgen was incorporated in California in 1980 and became a Delaware corporation in 1987. Amgen operates in one business segment: human therapeutics.

Significant Developments

Following is a summary of significant developments affecting our business that have occurred and that we have reported since the filing of our Annual Report on Form 10-K for the year ended December 31, 2015, and in early 2017.

Products/Pipeline

Bone health

EVENITY™ (romosozumab)*

• | In February 2016, we and UCB, our global collaboration partner in the development of EVENITY™, announced that the phase 3 FRAME (FRActure study in postmenopausal woMen with ostEoporosis) study met its co-primary endpoints. |

• | In March 2016, we and UCB announced that the phase 3 BRIDGE (placeBo-contRolled study evaluatIng the efficacy anD safety of EVENITY™ in treatinG mEn with osteoporosis) study met its primary endpoint. |

• | In September 2016, we and UCB announced that the U.S. Food and Drug Administration (FDA) accepted for review the Biologics License Application (BLA) for EVENITY™ for the treatment of osteoporosis in postmenopausal women at increased risk for fracture. The FDA has set a Prescription Drug User Fee Act (PDUFA) target action date of July 19, 2017. |

• | In December 2016, we and UCB announced that we submitted an application to the Pharmaceuticals and Medical Devices Agency in Japan, together with our joint venture partner Astellas Pharma, Inc., seeking marketing approval for EVENITY™ for the treatment of osteoporosis for those at high risk of fracture. |

Prolia® (denosumab)

• | In August 2016, we announced that the phase 3 randomized, double-blind, double-dummy, active-controlled study evaluating the safety and efficacy of Prolia® compared with risedronate in patients receiving glucocorticoid treatment met all primary and secondary endpoints at 12 months. |

XGEVA® (denosumab)

• | In October 2016, we announced that the phase 3 study evaluating XGEVA® versus Zometa® (zoledronic acid) in the prevention of skeletal-related events (SREs) in patients with multiple myeloma met its primary endpoint of non-inferiority in delaying the time to first on-study SRE. The secondary endpoints of superiority in delaying time to first SRE and delaying time to first-and-subsequent SREs were not met. |

1

Cardiovascular

Repatha® (evolocumab)

• | In July 2016, we announced that the FDA approved the Repatha® Pushtronex™ system (on-body infusor with prefilled cartridge), a new, monthly single-dose administration option. The Pushtronex™ system is a hands-free device designed to provide 420 mg of Repatha® in a single dose. |

• | In September 2016, we announced that the phase 3 GLAGOV (GLobal Assessment of Plaque ReGression with a PCSK9 AntibOdy as Measured by IntraVascular Ultrasound) study evaluating the effect of Repatha® on coronary artery disease met its primary and secondary endpoints. |

• | In December 2016, we announced that the Committee for Medicinal Products for Human Use (CHMP) of the European Medicines Agency (EMA) adopted a positive opinion for an extension to the marketing authorization of a new 420 mg single-dose delivery option for Repatha®. |

• | In January 2017, the United States District Court in Delaware granted Amgen’s request for a permanent injunction prohibiting Sanofi, Sanofi-Aventis U.S. LLC, Aventisub LLC, formerly doing business as Aventis Pharmaceuticals Inc. (collectively, Sanofi) and Regeneron Pharmaceuticals, Inc. (Regeneron) from infringing two patents that Amgen holds for Repatha® by manufacturing, using, selling or offering alirocumab for sale in the United States. Sanofi and Regeneron subsequently appealed the case to the U.S. Court of Appeals for the Federal Circuit (the Federal Circuit Court), and following a motion by Sanofi and Regeneron, in February 2017 the Federal Circuit Court entered a stay of the permanent injunction during the pendency of the appeal. See Part IV—Note 18, Contingencies and commitments, to the Consolidated Financial Statements. |

• | In February 2017, we announced that the phase 3 FOURIER (Further Cardiovascular OUtcomes Research with PCSK9 Inhibition in Subjects with Elevated Risk) study evaluating the effects of Repatha® on cardiovascular outcomes met its primary composite endpoint (cardiovascular death, non-fatal myocardial infarction (MI), non-fatal stroke, hospitalization for unstable angina or coronary revascularization) and key secondary composite endpoint (cardiovascular death, non-fatal MI or non-fatal stroke). No new safety issues were observed. |

• | In February 2017, we announced that the phase 3 EBBINGHAUS (Evaluating PCSK9 Binding antiBody Influence oN coGnitive HeAlth in high cardiovascUlar risk Subjects) cognitive function study achieved its primary endpoint. |

Inflammation

Enbrel® (etanercept)

• | In November 2016, we announced that the FDA approved the supplemental Biologics License Application (sBLA) for the expanded use of ENBREL, making it the first and only systemic therapy to treat pediatric patients (ages 4-17) with chronic moderate-to-severe plaque psoriasis. |

Nephrology

Parsabiv™ (etelcalcetide)*

• | In November 2016, we announced that the European Commission (EC) granted marketing authorization for Parsabiv™ for the treatment of secondary hyperparathyroidism (sHPT) in adult patients with chronic kidney disease (CKD) who are on hemodialysis. |

• | In February 2017, we announced that the FDA approved Parsabiv™ for the treatment of sHPT in adult patients with CKD who are on hemodialysis. |

Neuroscience

Erenumab (formerly AMG 334)

• | In June 2016, we announced that the global phase 2 study evaluating the efficacy and safety of erenumab in chronic migraine prevention met its primary endpoint. Erenumab is being developed jointly with Novartis AG (Novartis). |

• | In September 2016, we announced that the phase 3 ARISE (A phase 3, RandomIzed, double-blind, placebo-controlled Study to Evaluate the efficacy and safety of erenumab in migraine prevention) study evaluating the efficacy of erenumab in episodic migraine prevention met its primary endpoint. |

• | In November 2016, we announced the positive top-line results of the global phase 3, randomized, double-blind, placebo-controlled STRIVE (STudy to evaluate the efficacy and safety of erenumab in migRaIne preVEntion) study. The study met its primary endpoint. |

2

Oncology/Hematology

BLINCYTO® (blinatumomab)

• | In September 2016, we announced that the FDA approved the sBLA for BLINCYTO® to include new data supporting the treatment of pediatric patients with Philadelphia chromosome-negative (Ph-) relapsed or refractory (R/R) B-cell precursor acute lymphoblastic leukemia (ALL). |

• | In February 2017, we announced the submission of a sBLA to the FDA to include overall survival data from the Phase 3 TOWER study, supporting the conversion of BLINCYTO®’s accelerated approval to full approval. The sBLA also includes new data supporting the treatment of patients with Philadelphia chromosome-positive (Ph+) R/R B-cell precursor ALL. |

KYPROLIS® (carfilzomib)

• | In June 2016, the EC approved a variation to the marketing authorization for KYPROLIS® to include use in combination with dexamethasone alone for adult patients with multiple myeloma who have received at least one prior therapy. The EC approved the extended indication for KYPROLIS® based on data from the phase 3 head-to-head ENDEAVOR (RandomizEd, OpeN Label, Phase 3 Study of Carfilzomib Plus DExamethAsone Vs Bortezomib Plus DexamethasOne in Patients With Relapsed Multiple Myeloma) study. |

• | In September 2016, we announced the top-line results of the phase 3 CLARION (Carfilzomib, Melphalan, Prednisone vs Bortezomib, Melphalan, Prednisone in Newly Diagnosed Multiple Myeloma) study, which evaluated an investigational regimen of KYPROLIS®, melphalan and prednisone versus VELCADE® (bortezomib), melphalan and prednisone for 54 weeks in patients with newly diagnosed multiple myeloma who were ineligible for hematopoietic stem-cell transplant. The study did not meet the primary endpoint of superiority in progression-free survival (PFS). |

Nplate® (romiplostim)

• | In April 2016, we announced that the phase 3 study of Nplate® in children with symptomatic immune thromobocytopenia met its primary endpoint. |

Biosimilars

AMJEVITA™ (adalimumab-atto) /ABP 501

• | In September 2016, we announced that the FDA approved AMJEVITA™ across all eligible indications of the reference product, HUMIRA® (adalimumab), including treatment of psoriatic arthritis, ankylosing spondylitis and moderate-to-severe rheumatoid arthritis, polyarticular juvenile idiopathic arthritis in patients four years of age or older, chronic plaque psoriasis, adult Crohn’s disease and ulcerative colitis. For discussion of ongoing, related litigation, see Part IV—Note 18, Contingencies and commitments, to the Consolidated Financial Statements. |

• | In January 2017, we announced that the CHMP of the EMA adopted a positive opinion for the marketing authorization of ABP 501, recommending approval for all available indications. |

ABP 215

• | In November 2016, we and Allergan plc (Allergan), our collaboration partner in the development and commercialization of certain biosimilar candidates, announced the submission of a BLA to the FDA for ABP 215, a biosimilar candidate to Avastin® (bevacizumab). The FDA has accepted the BLA and set the Biosimilar User Fee Act target action date of September 14, 2017. |

• | In December 2016, we and Allergan announced the submission of a Marketing Authorization Application (MAA) to the EMA for ABP 215. |

ABP 980

• | In July 2016, we and Allergan announced the results from a phase 3 study evaluating the efficacy and safety of ABP 980 compared with trastuzumab (Herceptin®) in patients with human epidermal growth factor receptor 2-positive early breast cancer. The results ruled out inferiority compared to trastuzumab but could not rule out superiority based on its primary efficacy endpoint of the difference of the percentage of patients with a pathologic complete response. |

* FDA provisionally approved trade name

3

Marketing, Distribution and Selected Marketed Products

The largest concentration of our sales and marketing forces is based in the United States and Europe. Additionally, we continue to expand the commercialization and marketing of our products into other geographic territories, including parts of Latin America, the Middle East and Asia. This expansion is occurring by either establishing our own affiliate, acquiring existing third- party businesses or product rights or in partnering with third parties. Use of our own sales and marketing forces versus a third-party’s varies across these markets. Such use typically depends on several factors including the nature of entry into the new market, the size of opportunity and the operational capabilities. Together with our partners, we market our products to healthcare providers, including physicians or their clinics, dialysis centers, hospitals and pharmacies.

In the United States, we sell primarily to pharmaceutical wholesale distributors that we utilize as the principal means of distributing our products to healthcare providers. We also market certain products directly to consumers through direct-to-consumer print and television advertising, as well as through multi-channel marketing. For further discussion, see Government Regulation—Regulation of Product Marketing and Promotion. Outside the United States, we sell principally to healthcare providers and/or pharmaceutical wholesale distributors depending on the distribution practice in each country.

Our product sales to three large wholesalers, AmerisourceBergen Corporation, McKesson Corporation and Cardinal Health, Inc., each accounted for more than 10% of total revenues for each of the years ended December 31, 2016, 2015 and 2014. On a combined basis, these wholesalers accounted for approximately 96%, 97% and 94% of our U.S. gross product sales, respectively, and approximately 81%, 81% and 77% of our worldwide gross revenues, respectively. We monitor the financial condition of our larger customers and limit our credit exposure by setting credit limits and, in certain circumstances, by requiring letters of credit.

For financial information related to our one business segment, see Part IV—Consolidated Statements of Income, Consolidated Balance Sheets, and Note 19, Segment information, to the Consolidated Financial Statements.

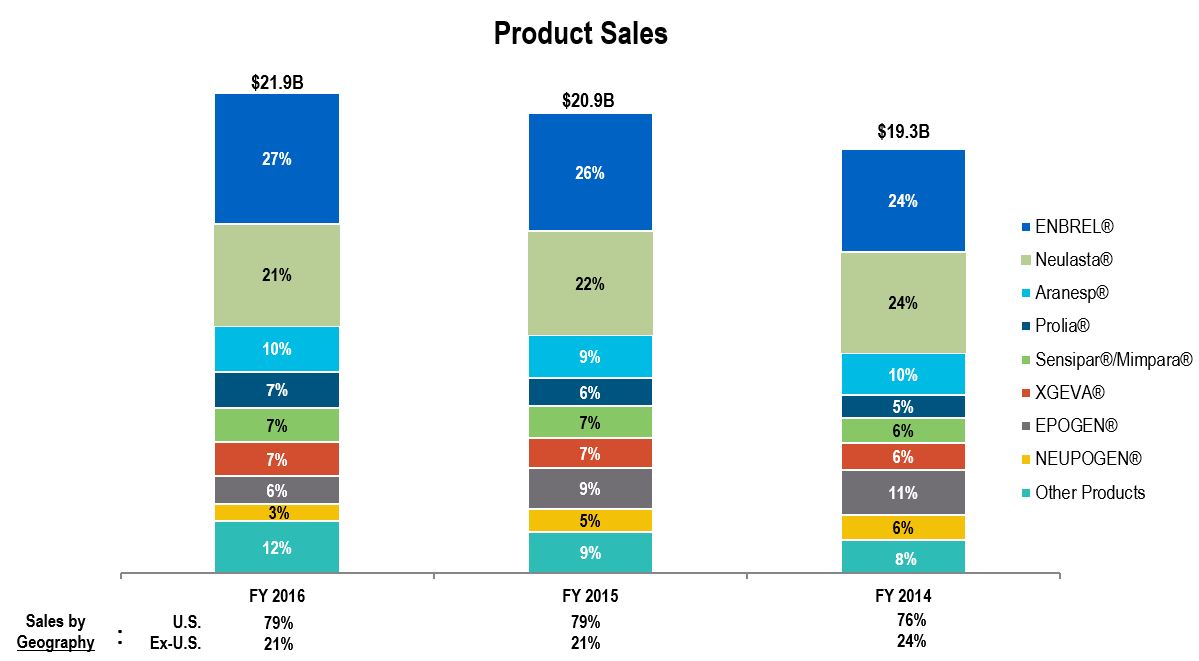

Our products are marketed around the world with the United States being our largest market. The following chart shows our product sales by principal product and by geography for the years ended December 31, 2016, 2015 and 2014.

4

Enbrel® (etanercept)

We market ENBREL primarily in the United States. It was launched in 1998 and is used primarily in indications for the treatment of adult patients with the following conditions:

• | moderately to severely active rheumatoid arthritis, |

• | chronic moderate-to-severe plaque psoriasis patients who are candidates for systemic therapy or phototherapy, and |

• | active psoriatic arthritis. |

Neulasta® (pegfilgrastim)

We market Neulasta®, a pegylated protein based on the filgrastim molecule, primarily in the United States and Europe. Neulasta® was launched in 2002, and is used primarily in the indication to help reduce the chance of infection due to a low white blood cell count, in people with certain types of cancer (non-myeloid) who receive anti-cancer medicines (chemotherapy) that can cause fever and a low blood cell count. In 2015, the Neulasta® Onpro® kit became available in the United States.

Aranesp® (darbepoetin alfa)

We market Aranesp® primarily in Europe and the United States. It was launched in 2001, and is indicated to treat a lower-than-normal number of red blood cells (anemia) caused by CKD (in both patients on dialysis and patients not on dialysis). Aranesp® is also indicated for the treatment of anemia due to concomitant myelosuppressive chemotherapy in patients with non-myeloid malignancies, and when chemotherapy will be used for at least two months after starting Aranesp®.

Aranesp® and EPOGEN® compete with each other in the United States, primarily in the dialysis setting.

Prolia® (denosumab)

We market Prolia® primarily in the United States and Europe. It contains the same active ingredient as XGEVA® but is approved for different indications, patient populations, doses and frequencies of administration. Prolia® was launched in the United States and Europe in 2010. In the United States, it is used primarily in the indication for the treatment of postmenopausal women with osteoporosis at high risk for fracture, defined as a history of osteoporotic fracture, or multiple risk factors for fracture, or patients who have failed or are intolerant to other available osteoporosis therapy. In Europe, Prolia® is used primarily for the treatment of osteoporosis in postmenopausal women at increased risk of fracture.

Sensipar®/Mimpara® (cinacalcet)

We market cinacalcet as Sensipar® primarily in the United States and as Mimpara® primarily in Europe. It was launched in 2004 and is used primarily in the indication for the treatment of sHPT in adult patients with CKD who are on dialysis.

XGEVA® (denosumab)

We market XGEVA® primarily in the United States and Europe. XGEVA® was launched in the United States in 2010, and is used primarily in the indication for the prevention of SREs (pathological fracture, radiation to bone, spinal cord compression or surgery to bone) in patients with bone metastases from solid tumors. It is not indicated for the prevention of SREs in patients with multiple myeloma. XGEVA® was launched in Europe in 2011, and is used primarily in the indication for the prevention of SREs in adults with bone metastases from solid tumors.

EPOGEN® (epoetin alfa)

We market EPOGEN® in the United States for dialysis patients. EPOGEN® was launched in 1989, and we market it for the indication to treat anemia caused by CKD in patients on dialysis to lessen the need for red blood cell transfusions. The majority of our sales are to two large dialysis providers.

NEUPOGEN® (filgrastim)

We market NEUPOGEN®, a recombinant-methionyl human granulocyte colony-stimulating factor (G-CSF), primarily in the United States, Canada and Europe. NEUPOGEN® was launched in 1991 and is used primarily in the indication to help reduce the chance of infection due to a low white blood cell count in people with certain types of cancer (non-myeloid) who receive anti-cancer medicines (chemotherapy) that can cause fever and a low blood cell count.

Other Marketed Products

We market several other products, including KYPROLIS® (carfilzomib), Vectibix® (panitumumab), Nplate® (romiplostim), Repatha® (evolocumab), BLINCYTO® (blinatumomab), IMLYGIC® (talimogene laherparepvec) and Corlanor® (ivabradine).

5

Patents

The following table describes our outstanding material patents for the indicated product by territory, general subject matter and latest expiry date. Certain of the European patents are the subject of supplemental protection certificates that provide additional protection for the product in certain European countries beyond the dates listed in the table (see footnotes).

One or more patents with the same or earlier expiry date may fall under the same “general subject matter” and are not listed separately.

Product | Territory | General Subject Matter | Expiration | |||

Enbrel® (etanercept) | U.S. | Methods of treating psoriasis | 8/13/2019 | |||

U.S. | Aqueous formulation and methods of treatment using the formulation | 6/8/2023 | ||||

U.S. | Fusion protein, and pharmaceutical compositions | 11/22/2028 | ||||

U.S. | DNA encoding fusion protein, and methods of making fusion protein | 4/24/2029 | ||||

Neulasta® (pegfilgrastim) | Europe | Pegylated G-CSF(1) | 2/8/2015 | |||

Aranesp® (darbepoetin alfa) | U.S. | Glycosylation analogs of erythropoietin proteins | 5/15/2024 | |||

Prolia®/ XGEVA® (denosumab) | U.S. | RANKL antibodies; and methods of use(2) | 12/22/2017 | |||

U.S. | Methods of treatment | 6/25/2022 | ||||

U.S. | Nucleic acids encoding RANKL antibodies, and methods of producing RANKL antibodies | 11/30/2023 | ||||

U.S. | RANKL antibodies including sequences | 2/19/2025 | ||||

Europe | RANKL antibodies(1) | 12/22/2017 | ||||

Europe | Medical use of RANKL antibodies(1) | 4/15/2018 | ||||

Europe | RANKL antibodies including epitope binding | 2/23/2021 | ||||

Europe | RANKL antibodies including sequences(1) | 6/25/2022 | ||||

Sensipar®/ Mimpara® (cinacalcet) | U.S. | Calcium receptor-active molecules | 3/8/2018 | |||

U.S. | Formulation | 9/22/2026 | ||||

Europe | Calcium receptor-active molecules(1) | 10/23/2015 | ||||

KYPROLIS® (carfilzomib) | U.S. | Compositions and compounds | 12/7/2027 | |||

U.S. | Methods of treatment | 4/14/2025 | ||||

Europe | Compositions, compounds and methods of treatment(1) | 8/8/2025 | ||||

Vectibix® (panitumumab) | U.S. | Human monoclonal antibodies to epidermal growth factor receptor (EGFr) | 4/8/2020 | |||

Europe | Human monoclonal antibodies to EGFr(1) | 5/5/2018 | ||||

Nplate® (romiplostim) | U.S. | Thrombopoietic compounds | 1/19/2022 | |||

U.S. | Formulation | 2/12/2028 | ||||

Europe | Thrombopoietic compounds(1) | 10/22/2019 | ||||

Europe | Formulation | 4/20/2027 | ||||

Repatha® (evolocumab) | U.S. | Antibodies(3) | 10/25/2029 | |||

U.S. | Methods of treatment | 10/8/2030 | ||||

Europe | Compositions and method of treatment | 8/22/2028 | ||||

BLINCYTO® (blinatumomab) | U.S. | Bifunctional polypeptides(3) | 4/21/2019 | |||

U.S. | Method of administration | 9/28/2027 | ||||

Europe | Bifunctional polypeptides | 11/26/2024 | ||||

Europe | Method of administration | 11/29/2026 | ||||

IMLYGIC® (talimogene laherparepvec) | U.S. | Compositions and method of treatment(3) | 1/22/2021 | |||

Europe | Composition and uses | 1/22/2021 | ||||

Parsabiv™ (etelcalcetide) | U.S. | Compound and pharmaceutical composition | 7/29/2030 | |||

Europe | Compound and pharmaceutical composition | 7/29/2030 | ||||

6

(1) | A European patent with this subject matter may also be entitled to supplemental protection in one or more countries in Europe, and the length of any such extension will vary by country. For example, supplementary protection certificates have been issued related to the indicated products for patents in at least the following countries: |

• | pegfilgrastim — France, Germany, Italy, Spain, and the United Kingdom, expiring in August 2017 |

• | denosumab — France, Italy, Spain and the United Kingdom, expiring in 2025 |

• | cinacalcet — France, Germany, Italy, Spain, and the United Kingdom, expiring in 2019 |

• | panitumumab — France, Germany, Italy, Spain, and the United Kingdom, expiring in 2022 |

• | romiplostim — France, Italy, Spain, and the United Kingdom, expiring in 2024 |

• | carfilzomib — France and Germany, expiring in 2028 |

(2) | The U.S. Patent and Trademark Office has issued a Notice of Final Determination that a patent with this subject matter is eligible for patent term extension with an expiry of September 17, 2021. |

(3) | A patent with this subject matter may be entitled to patent term extension in the United States. |

Competition

We operate in a highly competitive environment. Our products compete with other products or treatments for diseases for which our products may be indicated. Our competitors market products or are actively engaged in research and development (R&D) in areas in which we have products or in which we are developing product candidates or new indications for existing products. Our competitive positions may be based on, among other things, safety, efficacy, reliability, availability, patient convenience/delivery devices, price, reimbursement, access to and timing of market entry and patent position and expiration.

Certain of the existing patents on our principal products have expired, and we face new and increasing competition, including from biosimilars. We may also compete against biosimilar or generic versions of our competitors’ products. A biosimilar is another version of a biological product for which marketing approval is sought or has been obtained based on a demonstration that it is “highly similar” to the original reference product. See Government Regulation. We expect the adverse impact from biosimilars to be more like branded biologics than generic small molecules. Although we expect biosimilars to compete on price, we believe many patients, providers and payers will continue to place high value on the reputation, reliability and safety of our products. Zarxio®, a biosimilar version of NEUPOGEN® from Sandoz, a Novartis company (Sandoz), which launched in the United States in 2015, was the first biosimilar entrant into the U.S. market. Companies have pending applications with the FDA for biosimilar versions of EPOGEN® and Neulasta®, along with additional biosimilar versions of NEUPOGEN®. We are well positioned to compete and will leverage the experience we have had in the United States versus branded competition, as well as our considerable experience in competing against epoetin alfa and filgrastim biosimilars in Europe.

The introduction of new products, the development of new processes or technologies by competitors or the emergence of new information about existing products may result in increased competition for our marketed products, even for those protected by patents, or in reductions in the prices we receive from selling our products. In addition, the development of new treatment options or standards of care may reduce the use of our products or may limit the utility and application of ongoing clinical trials for our product candidates (as used in this document, clinical trials may include prospective clinical trials, observational studies, registries and other studies). See Item 1A. Risk Factors—Our products face substantial competition and Item 1A. Risk Factors—We currently face competition from biosimilars and expect to face increasing competition in the future.

7

The following table reflects our significant competitors and is not exhaustive.

Product | Territory | Competitor Marketed Product | Competitors | |||

ENBREL | U.S. & Canada | REMICADE®* | Janssen Biotech, Inc. (Janssen)(1)/Merck & Company, Inc. (Merck) | |||

U.S. & Canada | HUMIRA® | AbbVie Inc. | ||||

U.S. & Canada | STELARA®(2) | Janssen(1) | ||||

Neulasta® | Europe | Filgrastim biosimilars | Various | |||

Aranesp® | U.S. | PROCRIT®(3) | Janssen(1) | |||

U.S. | MIRCERA®(4) | Galenica Group (Galenica)/F. Hoffmann-La Roche Ltd. (Roche) | ||||

Europe | Epoetin alfa biosimilars | Various | ||||

Prolia® | U.S. & Europe | Alendronate, raloxifene and zoledronate generics | Various | |||

Sensipar®(5)/ Mimpara® | U.S. & Europe | Active Vitamin D analogs | Various | |||

XGEVA® | U.S. & Europe | Zoledronate generics | Various | |||

EPOGEN® | U.S. | MIRCERA®(4) | Galenica/Roche | |||

NEUPOGEN® | U.S. | Granix® | Teva Pharmacueticals Industries Ltd. (Teva) | |||

U.S. | Zarxio® | Sandoz | ||||

Europe | Filgrastim biosimilars | Various | ||||

KYPROLIS®(7) | U.S. | VELCADE® | Millennium Pharmaceuticals, Inc.(6) | |||

U.S. | REVLIMID® | Celgene Corporation (Celgene) | ||||

U.S. | POMALYST® | Celgene | ||||

Repatha® | U.S. & Europe | PRALUENT® | Regeneron Sanofi | |||

* | Approved biosimilar available |

(1) | A subsidiary of Johnson & Johnson (J&J). |

(2) | Dermatology only. |

(3) | PROCRIT® competes with Aranesp® in the supportive cancer care and pre-dialysis settings. |

(4) | MIRCERA® competes with Aranesp® in the nephrology segment only. |

(5) | Teva and Barr Pharmaceuticals have received tentative approval from the FDA for generic versions of Sensipar® that could compete with Sensipar® in the future. There is an injunction prohibiting them from commercializing in the United States until expiration of the Sensipar® patents. |

(6) | A wholly owned subsidiary of Takeda Pharmaceutical Company Limited. |

(7) | KYPROLIS® is facing increased competition from several recently approved products. |

8

Reimbursement

Sales of our principal products are dependent on the availability and extent of coverage and reimbursement from third-party payers. In many markets around the world, these payers, including government health systems, private health insurers and other organizations, continue to be focused on reducing the cost of healthcare. Their efforts have intensified as a result of rising healthcare costs and economic challenges. Drugs, and in particular specialty drugs such as our products, remain a focus for cost containment by these parties. As a result, payers around the world are being more restrictive regarding the use of biopharmaceutical products while requiring a higher level of clinical evidence to support the benefit such products bring to patients and the broader healthcare system.

The scrutiny of biopharmaceutical pricing in the United States remains intense and a point of focus in the discussion of rising healthcare costs. The pricing practices of certain companies have increased public media and government scrutiny of the biopharmaceutical industry, providing greater incentive for governments and private payers to limit or regulate the price of drug products and services. At the same time, value assessments of new technology, previously used predominantly outside the United States, are having an impact in the U.S. healthcare environment. Healthcare provider organizations and independent organizations are creating their own value assessments of biopharmaceutical drugs for comparison with manufacturer pricing. Although these organizations do not set drug prices, they seek to influence pricing as well as payer and provider decision making by publicly disclosing their assessments, often making assertions around what they believe to be the appropriate price to charge for a product. These developments put greater pressure on access to, pricing of and sales of our products.

In the United States, healthcare providers are reimbursed for covered services and products they deliver through Medicare, Medicaid and other government healthcare programs, as well as through private payers. Pharmacies are also reimbursed in a similar manner for drug products they dispense. We are required to provide specified rebates or discounts on the products we sell to certain government funded programs, including Medicare and Medicaid, and those rebates or discounts have increased over time. The Patient Protection and Affordable Care Act (ACA), enacted in 2010, increased many of the mandatory discounts and rebates required of us and imposed a new Branded Prescription Pharmaceutical Manufacturers and Importers fee payable each year by us and other manufacturers. The new U.S. presidential administration has identified repealing and replacing the ACA as a priority. The timing and method of repeal and replacement legislation is uncertain but changes could include the number of patient lives covered, the quality of the insurance, Medicaid eligibility and the level of patient protections provided.

Further efforts by government agencies and state legislatures in the United States could also affect us and our industry. For example, a recently enacted Vermont law requires manufacturers to submit price increase justifications to the state attorney general if certain price increase and state spending thresholds are met. Examples of other proposals that have been discussed and debated, but not yet enacted, include state ballot initiatives that would place a maximum price ceiling, or cap, on pharmaceutical products purchased by state agencies and state legislative efforts to cap pharmaceutical prices for commercial payers. Other legislative and regulatory actions that would have a significant impact on Amgen include: changes to how the Medicare program covers and reimburses current and future drugs, including for patients with End-Stage Renal Disease; changes in the Federal payment rate or new rebate requirements for covered drugs and policies for payment in Medicare or Medicaid; and changes to coverage and payment for biosimilars, including the current Medicare biosimilar coverage and payment policies intended to encourage biosimilar adoption, or other policies that provide easier substitution or reimbursement advantages.

In the U.S. private sector, healthcare providers and payers continue to institute cost reduction and containment measures that lower drug spending altogether or shift a greater portion of the costs to patients. Such measures include more limited benefit plan designs, higher tier formulary placement that increases the level of patient out of pocket costs and stricter utilization criteria before a patient may get access to a drug. In the retail pharmacy sector, in which the majority of our sales for ENBREL, Sensipar® and Repatha® occur, the use of such measures by Pharmacy Benefit Managers (PBMs) and insurers has continued to intensify which have limited Amgen product usage and revenues. PBMs are third-party organizations tasked with administrating prescription drug programs for large employers, health plans and government programs. Consolidation has resulted in a smaller number of PBMs and insurers overseeing a large portion of total covered lives in the United States; for example three PBMs oversee approximately 75% of covered lives in the United States. As a result, PBMs and insurers have greater market power and negotiating leverage to exclude drugs from their formularies in favor of competitor drugs or alternative treatments, and/or to mandate stricter utilization criteria. Formulary exclusion effectively encourages patients and providers to seek alternative treatments or pay 100% of the cost of a drug. Recent experience with Repatha® underscores that utilization management requirements continue to be onerous for patients and physicians, limiting access to appropriate usage. In highly competitive treatment markets such as with ENBREL, PBMs are also able to exert negotiating leverage by requiring incremental rebates from manufacturers in order to maintain their formulary position. A drug’s favorable position on formulary is essential to ensure patients have access.

In general, in countries outside the United States, government-sponsored healthcare systems are the primary payers for drugs and biologics. With increased budgetary constraints, payers in many countries apply a variety of measures to exert downward price pressure. These measures can include mandatory price controls, price referencing, therapeutic reference pricing, increases in mandates or incentives for generic substitution and biosimilar usage, and government-mandated price cuts. We expect that

9

countries will continue to take aggressive actions to reduce expenditures on drugs and biologics. Similarly, fiscal constraints may also impact the extent to which countries are willing to approve new and innovative therapies and/or allow access to new technologies. For example, many Health Technology Assessment (HTA) organizations use formal economic metrics such as cost-effectiveness to determine coverage and reimbursement of new therapies, and these organizations are proliferating in established and emerging markets.

The dynamics and developments discussed above serve to create pressure on the pricing and potential usage of our products, and the industry as a whole. We remain focused on delivering breakthrough treatments for unmet medical needs. Amgen is committed to working with the entire healthcare community to ensure continued innovation and to enable patient access to needed medicines. We do this by:

•investing billions of dollars annually in research and development;

•developing more affordable therapeutic choices in the form of high-quality and reliably-supplied biosimilars;

•pricing our medicines to reflect the value they provide;

•partnering with payers to share risk and accountability for health outcomes;

•providing patient support and education programs and helping patients in financial need access our medicines; and

• | working with policymakers, patients and other stakeholders to establish a sustainable healthcare system with access to affordable care and where patients and their healthcare professionals are the primary decision makers. |

See Item 1A. Risk Factors—Our sales depend on coverage and reimbursement from third-party payers, and pricing and reimbursement pressures may affect our profitability and Item 1A. Risk Factors—Guidelines and recommendations published by various organizations can reduce the use of our products.

Manufacturing, Distribution and Raw Materials

Manufacturing

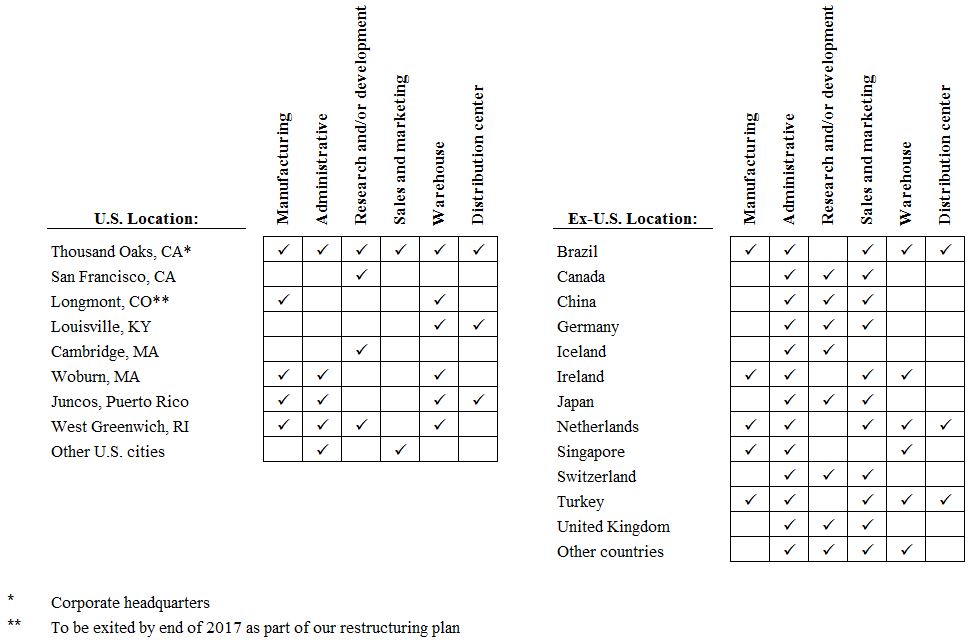

We believe we are a leader in the manufacturing of biologics and that our manufacturing capabilities represent a competitive advantage. The products we manufacture consist of both biologics and small molecule drugs. The majority of our products are biologics that are produced in living cells and that are inherently complex due to naturally-occurring molecular variations. Highly specialized knowledge and extensive process and product characterization are required to transform laboratory-scale processes into reproducible commercial manufacturing processes. For additional information regarding manufacturing facilities, see Item 2. Properties.

We perform most of our bulk manufacturing, formulation, and/or fill and finish activities in our Puerto Rico, Rhode Island, California and Ireland facilities and also conduct finish activities in the Netherlands. In addition, we utilize third-party contract manufacturers to supplement our commercial manufacturing requirements.

We manufacture products to support our clinical trials primarily in our California and Rhode Island locations. We also utilize third-party contract manufacturers for certain clinical products.

See Item 1A. Risk Factors for a discussion of the factors that could adversely impact our manufacturing operations and the global supply of our products.

Distribution

We operate distribution centers in Kentucky, California and the Netherlands for worldwide distribution of the majority of our commercial and clinical products. We also use third-party distributors to supplement distribution of our products worldwide.

Other

In addition to the manufacturing and distribution activities noted above, our operations in the United States, the U.S. territory of Puerto Rico and the Netherlands include key manufacturing support functions, including quality control, process development, procurement, production scheduling and warehousing. Certain of those manufacturing and distribution activities are highly regulated by the FDA as well as other international regulatory agencies. See Government Regulation—Regulation in the United States—Regulation of Manufacturing Standards.

10

Manufacturing Initiatives

We have multiple ongoing initiatives that are designed to extend our manufacturing advantage by optimizing our manufacturing network and/or mitigating manufacturing risks while continuing to ensure adequate supply of our products. We have initiated the bulk process qualification campaign to facilitate licensure at our biologics manufacturing facility in Singapore. Upon licensure, this facility will expand our capability to manufacture cell culture products utilizing new technology and innovation. The facility will be fully reconfigurable, providing efficient manufacturing capabilities to help ensure supply of our products worldwide. Our first product to be manufactured in the facility will be denosumab. We are also constructing an additional new facility at the site in Singapore to enable the manufacture of the active pharmaceutical ingredient for KYPROLIS®.

In addition to these initiatives, we have projects designed to optimize manufacturing asset utilization, to continue our use of third-party contract manufacturers and to maintain a state of regulatory compliance. This includes manufacturing network consolidation initiatives as well as process improvements surrounding manufacturing. See Item 1A. Risk Factors—Manufacturing difficulties, disruptions or delays could limit supply of our products and limit our product sales.

Raw Materials and Medical Devices

Certain raw materials, medical devices, including companion diagnostics, and components necessary for the commercial and/or clinical manufacturing of our products are provided by and are the proprietary products of unaffiliated third-party suppliers, certain of which may be our only sources for such materials. We currently attempt to manage the risk associated with such suppliers by inventory management, relationship management and evaluation of alternative sources when feasible. We also monitor the financial condition of certain suppliers and their ability to supply our needs. See Item 1A. Risk Factors—We rely on third-party suppliers for certain of our raw materials, medical devices and components.

We perform various procedures to assist us in authenticating the source of raw materials, including intermediary materials used in the manufacture of our products, which include verification of the country of origin. The procedures are incorporated into the manufacturing processes we and our third-party contract manufacturers perform.

Government Regulation

Regulation by government authorities in the United States and other countries is a significant factor in the production and marketing of our products and our ongoing R&D activities. In order to clinically test, manufacture and market products for therapeutic use, we must satisfy mandatory procedures and safety and effectiveness standards established by various regulatory bodies. Compliance with these standards is complex and failure to comply with any of these standards can result in significant implications. See Item 1A. Risk Factors for a discussion of factors that can adversely impact our development and marketing of commercial products including global regulatory implications.

Regulation in the United States

In the United States, the Public Health Service Act, the Federal Food, Drug, and Cosmetic Act (FDCA) and the regulations promulgated thereunder, as well as other federal and state statutes and regulations govern, among other things, the production, research, development, testing, manufacture, quality control, labeling, storage, record keeping, approval, advertising and promotion, and distribution of our products, as well as the reporting of certain payments and other transfers of value to healthcare professionals and teaching hospitals.

Clinical Development and Product Approval. Drug development in our industry is complex, challenging and risky; and failure rates are high. Product development cycles are typically very long—approximately 10 to 15 years from discovery to market. A potential new medicine must undergo many years of preclinical and clinical testing to establish its safety and efficacy for use in humans at appropriate dosing levels and with an acceptable risk-benefit profile.

After laboratory analysis and preclinical testing in animals, we file an Investigational New Drug Application (IND) with the FDA to begin human testing. Typically, we undertake an FDA-designated three-phase human clinical testing program.

• | In phase 1, we conduct small clinical trials to investigate the safety and proper dose ranges of our product candidates in a small number of human subjects. |

• | In phase 2, we conduct clinical trials to investigate side effect profiles and the efficacy of our product candidates in a large number of patients who have the disease or condition under study. |

• | In phase 3, we conduct clinical trials to investigate the safety and efficacy of our product candidates in a large number of patients who have the disease or condition under study. |

The FDA monitors the progress of each trial conducted under an IND and may, at its discretion, re-evaluate, alter, suspend or terminate the testing based on the data accumulated to that point and the FDA’s risk-benefit assessment with regard to the

11

patients enrolled in the trial. The results of preclinical and clinical trials are submitted to the FDA in the form of a BLA for biologic products or an NDA for small molecule products. We are not permitted to market or promote a new product until the FDA has approved our marketing application.

Approval of Biosimilars. The ACA authorized the FDA to approve biosimilars via a separate, abbreviated pathway. The pathway allows sponsors of a biosimilar to seek and obtain regulatory approval based in part on the non-clinical and clinical trial data of an originator product to which the biosimilar has been demonstrated to be “highly similar” and to have no clinically meaningful differences in terms of safety, purity, and potency. The relevance of demonstrating “similarity” is that in many cases, biosimilars can be brought to market without conducting the full suite of clinical trials typically required of originators, as risk-benefit has previously been established. In order to preserve incentives for future innovation, the law establishes a period of exclusivity for originators’ products, which in general prohibits biosimilars from gaining FDA approval based in part on reliance on or reference to the originator’s data in their application to the FDA for 12 years after FDA approval of the originator product. The law does not change the duration of patents granted on biologic products. The FDA has released a number of guidance documents as part of the implementation of the abbreviated approval pathway for biosimilars, some of which remain in draft form. As of the end of 2016, four biosimilar applications have been approved by the FDA, including AMJEVITA™. A number of manufacturers have announced the filing of marketing applications to the FDA under the biosimilar pathway, some of which are for biosimilars of our products.

Regulation of Product Marketing and Promotion. The FDA regulates the marketing and promotion of products. Our product promotion for approved product indications must comply with the statutory standards of the FDCA, and the FDA’s implementing regulations and standards. The FDA’s review of marketing and promotional activities encompasses, but is not limited to, direct-to-consumer advertising, healthcare provider-directed advertising and promotion, sales representative communications to healthcare professionals, promotional programming and promotional activities involving electronic media. The FDA may also review industry-sponsored scientific and educational activities that make representations regarding product safety or efficacy in a promotional context. The FDA may take enforcement action against a company for promoting unapproved uses of a product or for other violations of its advertising and labeling laws and regulations. Enforcement action may include product seizures, injunctions, civil or criminal penalties or regulatory letters, which may require corrective advertising or other corrective communications to healthcare professionals. Failure to comply with the FDA’s regulations also can result in adverse publicity or increased scrutiny of company activities by the U.S. Congress or other legislators. Additionally, as described below, such failure may lead to additional liability under U.S. health care fraud and abuse laws.

Regulation of Manufacturing Standards. The FDA regulates and inspects equipment, facilities, laboratories and processes used in the manufacturing and testing of products prior to providing approval to market products. If after receiving approval from the FDA, we make a material change in manufacturing equipment, location or process, additional regulatory review may be required. We also must adhere to current Good Manufacturing Practice regulations and product-specific regulations enforced by the FDA through its facilities inspection program. The FDA conducts regular, periodic visits to re-inspect our equipment, facilities, laboratories and processes following an initial approval.

Regulation of Combination Products. Combination products are defined by the FDA to include products composed of two or more regulated components (e.g., a biologic and/or drug and a device). Biologics/Drugs and devices each have their own regulatory requirements, and combination products may have additional requirements. A number of our marketed products meet this definition and are regulated under this framework, and we expect that a number of our pipeline product candidates will be evaluated for regulatory approval under this framework as well.

Regulation Outside the United States

In the European Union (EU) countries as well as Switzerland, Canada, Australia and Japan, regulatory requirements and approval processes are similar in principle to those in the United States.

In the EU, there are currently two potential tracks for seeking marketing approval for a product which is not authorized in any Member State; a decentralized procedure; and a centralized procedure. In the decentralized procedure, identical applications for marketing authorization are submitted simultaneously to the national regulatory agencies. Regulatory review is led by one Member State (the Reference Member State) and its assessment—based on safety, quality and efficacy—is reviewed and approved (assuming there are no concerns that the product poses a serious risk to public health) by the other Member States from which the applicant is seeking approval (the Concerned Member States). The decentralized procedure leads to a series of single national approvals in all relevant countries. In the centralized procedure, which is required of all products derived from biotechnology, a company submits a single MAA to the EMA, which conducts an evaluation of the dossier, drawing upon its scientific resources across Europe. If the drug product is proven to fulfill the requirements for quality, safety and efficacy, the EMA’s CHMP adopts a positive opinion, which is transmitted to the EC for final decision on grant of the marketing authorization. While the EC generally follows the CHMP’s opinion, it is not bound to do so. Subsequent commercialization is enabled by country-by-country reimbursement approval.

12

In the EU, biosimilars are approved under a specialized pathway of the centralized procedure. As with the U.S. pathway, applicants seek and obtain regulatory approval for a biosimilar once the data exclusivity period for the original reference product has expired relying in part on the data submitted for the originator product together with data evidencing that the biosimilar is “highly similar” in terms of quality, safety and efficacy to the original reference product authorized in the European Economic Area.

Other countries such as Russia, Turkey and those in Latin America and the Middle East have review processes and data requirements similar to those of the EU, and in some cases rely on prior marketing approval from U.S. or EU regulatory authorities. The regulatory process in these countries may include manufacturing/testing facility inspections, testing of drug product upon importation and other domestic requirements.

In Asia Pacific, a number of countries such as China, Japan, South Korea and Taiwan may require local clinical trial data for bridging purposes as part of the drug registration process in addition to global clinical trials, which can add to overall drug development and registration timelines. In most of the Asian markets, registration timelines depend on marketing approval in the United States or the EU. In some markets in Asia, such as China, Thailand, and Indonesia, the regulatory timelines can be less predictable. The regulatory process may also include manufacturing/testing facility inspections, testing of drug product upon importation and other domestic requirements. Countries such as Australia and Japan have more mature systems that would allow for submissions in more competitive timeframes. Regarding biosimilars, several of these countries have pathways to register biosimilars (e.g., South Korea, India, Australia, Singapore and Taiwan) and biosimilar products are already present on the markets (e.g., Australia and South Korea).

In some countries, such as Japan and those in the EU, medical devices may be subject to regulatory regimes whereby the manufacturer must establish that its medical device conforms to essential requirements set out in the law for the particular device category. For example, in the EU, with limited exceptions, medical devices placed on the market must bear the Conformité Européenne marking to indicate their conformity with legal requirements.

Post-approval Phase

After approval, we continue to monitor adverse events reported following the use of our products through post marketing routine pharmacovigilance surveillance and studies when applicable. We report such events to the appropriate regulatory agencies, as required per local regulations for individual cases and aggregate reports. We proactively monitor (according to good pharmacovigilance practices) and ensure implementation of signal detection, assessment and the communication of adverse events that may be associated with the use of our products. We may also be required by regulatory agencies to conduct further clinical trials on our marketed products as a condition of their approval or to provide additional information on safety and efficacy. Health authorities, including the FDA, have authority to mandate labeling changes to products at any point in a product’s lifecycle based on new safety information or as part of an evolving label change to a particular class of products.

Health authorities, including the FDA, also have the authority, before or after approval, to require companies to implement a risk management program for a product to ensure that the benefits of the drug outweigh the risks. Each risk management program is unique and varies depending on the specific factors required. In the United States, a risk management program is known as a risk evaluation and mitigation strategy (REMS) and we currently have REMS for Prolia®, Nplate® and BLINCYTO®, as well as for our erythropoiesis-stimulating agents (ESAs), which includes EPOGEN® and Aranesp®.

Other Regulation

We are also subject to various laws pertaining to healthcare “fraud and abuse,” including anti-kickback laws and false claims laws. Anti-kickback laws make it illegal to solicit, offer, receive or pay any remuneration in exchange for or to induce the referral of business, including the purchase or prescription of a particular drug that is reimbursed by a state or federal program. False claims laws prohibit knowingly and willingly presenting, or causing to be presented for payment to third-party payers (including Medicare and Medicaid) any claims for reimbursed drugs or services that are false or fraudulent, claims for items or services not provided as claimed or claims for medically unnecessary items or services. Violations of fraud and abuse laws may be punishable by criminal and/or civil sanctions, including fines and civil monetary penalties, as well as by the possibility of exclusion from federal healthcare programs (including Medicare and Medicaid). Liability under the false claims laws may also arise when a violation of certain laws or regulations related to the underlying products (e.g., violations regarding improper promotional activity or unlawful payments) contributes to the submission of a false claim.

In 2012, Amgen announced it had finalized a settlement agreement with the U.S. government and various other parties regarding allegations that Amgen’s promotional, contracting, sales and marketing activities and arrangements caused the submission of various false claims under the Federal Civil False Claims Act and various State False Claims Acts. In connection with entering into the settlement agreement, Amgen also entered into a corporate integrity agreement with the Office of Inspector General (OIG) of the U.S. Department of Health and Human Services that requires Amgen to maintain its corporate compliance program and to undertake a set of defined corporate integrity obligations for a period of five years. Due to the breadth of the

13

statutory provisions and the absence of guidance in the form of regulations or court decisions addressing some of our practices, it is possible that in the future our practices might be further challenged under anti-kickback or similar laws.

Additionally, the U.S. Foreign Corrupt Practices Act (FCPA) prohibits U.S. corporations and their representatives from offering, promising, authorizing or making payments to any foreign government official, government staff member, political party or political candidate in an attempt to obtain or retain business abroad. The scope of the FCPA includes interactions with certain healthcare professionals in many countries. Other countries have enacted similar anti-corruption laws and/or regulations.

Our business has been and will continue to be subject to various other U.S. and foreign laws, rules and/or regulations.

Research and Development and Selected Product Candidates

We focus our R&D on novel human therapeutics for the treatment of serious illness in the areas of oncology/hematology, cardiovascular disease, inflammation, bone health, nephrology and neuroscience. We take a modality-independent approach to R&D with a focus on biologics. We use cutting-edge science and technology to study the subtle biological mechanisms in search of therapies that will improve the lives of those who suffer from diseases. Our discovery research programs may therefore yield targets that lead to the development of human therapeutics delivered as large molecules, small molecules, or other combination or new modalities. Human genetic validation is used whenever possible to enhance the likelihood of success. For the years ended December 31, 2016, 2015 and 2014, our R&D expenses were $3.8 billion, $4.1 billion and $4.3 billion, respectively.

We have major R&D centers in several locations throughout the United States (including Thousand Oaks and San Francisco, California and Cambridge, Massachusetts), in Iceland and in the United Kingdom, as well as smaller research centers and development facilities globally. See Item 2. Properties.

We conduct clinical trial activities by using both our internal staff and third-party contract clinical trial service providers. To increase the number of patients available for enrollment in our clinical trials, we have opened clinical sites and will continue opening clinical sites and enrolling patients in a number of geographic locations. See Government Regulation—Clinical Development and Product Approval for a discussion of government regulation over clinical development. Also see Item 1A. Risk Factors—We must conduct clinical trials in humans before we can commercialize and sell any of our product candidates or existing products for new indications.

Some of our competitors are actively engaged in R&D in areas where we have products or where we are developing product candidates or new indications for existing products. For example, we compete with other clinical trials for eligible patients, which may limit the number of available patients who meet the criteria for certain clinical trials. The competitive marketplace for our product candidates is significantly dependent on the timing of entry into the market. Early entry may have important advantages in gaining product acceptance, thereby contributing to a product’s eventual success and profitability. Accordingly, we expect that in some cases, the relative speed with which we can develop products, complete clinical testing, receive regulatory approval and supply commercial quantities of a product to the market will be important to our competitive position.

In addition to product candidates and marketed products generated from our internal R&D efforts, we acquire companies, acquire and license certain product and R&D technology rights and establish R&D arrangements with third parties to enhance our strategic position within our industry by strengthening and diversifying our R&D capabilities, product pipeline and marketed product base. In pursuing these R&D arrangements and licensing or acquisition activities, we face competition from other pharmaceutical and biotechnology companies that also seek to license or acquire technologies, product candidates or marketed products from those entities performing the R&D.

The following table is a selection of certain of our product candidates by phase of development in our therapeutic areas of focus as of February 13, 2017, unless otherwise indicated. Additional product candidate information can be found on our website at www.amgen.com. The website address is not intended to function as a hyperlink, and the information contained on our website is not intended to be a part of this filing. The information in this section does not include other, non-registrational clinical trials that we may conduct for purposes other than for submission to regulatory agencies for their approval of a new product indication. We may conduct non-registrational clinical trials for various reasons including to evaluate real-world outcomes or to collect additional safety information with the use of our products. In addition, the table does not include the biosimilar products we are developing, which are discussed later in this section.

14

Molecule | Disease/Condition | |

Phase 3 Programs | ||

Aranesp® | Myelodysplastic syndromes | |

BLINCYTO® | ALL | |

ENBREL | Psoriatic arthritis; Rheumatoid arthritis remission | |

Erenumab | Episodic migraine | |

EVENITY™ | Postmenopausal osteoporosis; Male osteoporosis | |

IMLYGIC® | Metastatic melanoma | |

KYPROLIS® | Multiple myeloma | |

Omecamtiv mecarbil | Chronic heart failure | |

Prolia® | Glucocorticoid-induced osteoporosis | |

Repatha® | Hyperlipidemia | |

Vectibix® | Metastatic colorectal cancer (mCRC) | |

XGEVA® | Delay or prevention of bone metastases in breast cancer; Cancer-related bone damage in patients with multiple myeloma | |

Phase 2 Programs | ||

BLINCYTO® | Diffuse Large B-Cell Lymphoma (DLBCL); R/R Ph+ and minimal residual disease of ALL | |

Erenumab | Chronic migraine | |

AMG 157 | Asthma; Atopic dermatitis | |

AMG 520 | Alzheimer’s disease | |

AMG 899 | Dyslipidemia | |

Phase 1 Programs | ||

IMLYGIC® | Various cancer types | |

KYPROLIS® | Small-cell lung cancer | |

Oprozomib | Multiple myeloma | |

AMG 176 | Various cancer types | |

AMG 211 | Various cancer types | |

AMG 224 | Multiple myeloma | |

AMG 301 | Migraine | |

AMG 330 | Acute myeloid leukemia | |

AMG 420 | Multiple myeloma | |

AMG 557 | Systemic lupus erythematosus | |

AMG 570 | Systemic lupus erythematosus | |

AMG 592 | Inflammatory diseases | |

AMG 820 | Various cancer types | |

AMG 986 | Heart failure | |

Phase 3 | clinical trials investigate the safety and efficacy of product candidates in a large number of patients who have the disease or condition under study; typically performed with registrational intent. |

Phase 2 | clinical trials investigate side effect profiles and efficacy of product candidates in a large number of patients who have the disease or condition under study. |

Phase 1 | clinical trials investigate safety and proper dose ranges of product candidates in a small number of human subjects. |

15

Phase 3 Product Candidate Program Changes

As of February 15, 2016, we had 15 phase 3 programs. As of February 13, 2017, we also had 15 phase 3 programs, as omecamtiv mecarbil for the treatment of chronic heart failure advanced from phase 2 trials to phase 3 trials and Parsabiv™ was approved by the EC and FDA for the treatment of sHPT in patients with CKD on hemodialysis.

Phase 3 Product Candidate Patent Information

The following table describes our outstanding composition of matter patents that have issued thus far for our product candidates in phase 3 development that have yet to be approved for any indication. Patents for products already approved for one or more indications but currently undergoing phase 3 clinical trials for additional indications are previously described. See Marketing, Distribution and Selected Marketed Products—Patents.

Molecule | Territory | General Subject Matter | Estimated Expiration* | |||

Erenumab | U.S. | Polypeptides | 2031 | |||

EVENITY™ | U.S. | Polypeptides | 2026 | |||

Europe | Polypeptides | 2026 | ||||

Omecamtiv mecarbil | U.S. | Compound | 2027 | |||

* Patent expiration estimates are based on issued patents, which may be challenged, invalidated, or circumvented by competitors. The patent expiration estimates do not include any term adjustments, extensions or supplemental protection certificates that may be obtained in the future and extend these dates. Corresponding patent applications are pending in other jurisdictions. Additional patents may be filed or issued and may provide additional exclusivity for the product candidate or its use.

Phase 3 and 2 Program Descriptions

The following text provides additional information about selected product candidates that have advanced into human clinical trials.

Aranesp®

Aranesp® is a recombinant human protein agonist of the erythropoietin receptor.

In February 2016, we announced that the randomized, double-bind, placebo controlled phase 3 ARCADE trial met its primary endpoint of reducing the incidence of red blood cell transfusions in anemic patients with low and intermediate-1 risk myelodysplastic syndromes.

BLINCYTO®

BLINCYTO® is an anti-CD19 x anti-CD3 (BiTE®) bispecific antibody construct.

A phase 3 study in pediatric patients with high-risk first relapse B-precursor ALL is ongoing. Phase 2 studies in adult patients with R/R Ph+ and minimal residual disease of ALL are ongoing. A phase 2/3 study in patients with R/R DLBCL is ongoing.

In February 2017, we announced the submission of a sBLA to the FDA to include overall survival data from the Phase 3 TOWER study, supporting the conversion of BLINCYTO®’s accelerated approval to full approval. The sBLA also includes new data supporting the treatment of patients with Ph+ R/R B-cell precursor ALL.

Denosumab

Denosumab is a human monoclonal antibody that inhibits RANKL.

Prolia®

In August 2016, we announced that the phase 3 randomized, double-blind, double-dummy, active controlled study evaluating the safety and efficacy of Prolia® compared with risedronate in patients receiving glucocorticoid treatment met all primary and secondary endpoints at 12 months.

XGEVA®

In October 2016, we announced that a phase 3 study evaluating XGEVA® versus Zometa® in the prevention of SRE in patients with multiple myeloma met its primary endpoint of non-inferiority in delaying the time to first on-study SRE. The secondary endpoints of superiority in delaying time to first SRE and delaying time to first-and-subsequent SRE were not met.

16

A phase 3 study for the delay or prevention of bone metastases in patients with adjuvant breast cancer is ongoing.

ENBREL

ENBREL is a fusion protein that inhibits tumor necrosis factor.

A phase 3 study to evaluate ENBREL as a monotherapy for psoriatic arthritis treatment is ongoing. A phase 3 study to evaluate ENBREL as a monotherapy in maintaining remission in rheumatoid arthritis is ongoing.

Erenumab (formerly AMG 334)

Erenumab is a human monoclonal antibody that inhibits the receptor for calcitonin gene-related peptide. It is being evaluated for the prophylaxis of migraine. Erenumab is being developed jointly with Novartis.

In June 2016, we announced that the global phase 2 study evaluating the efficacy and safety of erenumab in chronic migraine prevention met its primary endpoint.

In September 2016, we announced that the phase 3 ARISE study evaluating the efficacy of erenumab in episodic migraine prevention, met its primary endpoint. Patients enrolled in ARISE study were randomized to receive either placebo, or erenumab 70 mg subcutaneously, once monthly for three months.

In November 2016, we announced that the global phase 3 STRIVE study evaluating the efficacy of erenumab in episodic migraine prevention, met its primary endpoint. Patients enrolled in STRIVE were randomized to receive either placebo, or one of two erenumab doses—70 mg or 140 mg—subcutaneously, once monthly for six months.

EVENITY™

EVENITY™ is a humanized monoclonal antibody that inhibits the action of sclerostin. It is being evaluated as a treatment for osteoporosis. EVENITY™ is being developed in collaboration with UCB.

In February 2016, we and UCB announced that the phase 3 FRAME study met its co-primary endpoints.

In March 2016, we and UCB announced that the phase 3 BRIDGE study met its primary endpoint.

In September 2016, we and UCB announced that the FDA accepted for review the BLA for EVENITY™ for the treatment of osteoporosis in postmenopausal women at increased risk for fracture. The FDA has set a PDUFA target action date of July 19, 2017. Phase 3 studies for the treatment of postmenopausal women with osteoporosis are ongoing.

IMLYGIC®

IMLYGIC® is an oncolytic immunotherapy derived from HSV-1.

A phase 1b/3 study to evaluate IMLYGIC® in combination with Merck’s anti-PD-1 therapy, KEYTRUDA® (pembrolizumab), in patients with mid- to late-stage metastatic melanoma is ongoing.

KYPROLIS®

KYPROLIS® is a proteasome inhibitor.

A phase 3 study, ARROW (RAndomized, Open-label, Phase 3 Study in Subjects with Relapsed and Refractory Multiple Myeloma Receiving Carfilzomib in Combination with Dexamethasone, Comparing Once-Weekly versus Twice-weekly Carfilzomib Dosing), with weekly dosing in relapsed and refractory multiple myeloma is ongoing.

Omecamtiv mecarbil

Omecamtiv mecarbil is a small molecule activator of cardiac myosin. It is being evaluated for the treatment of chronic heart failure. Omecamtiv mecarbil is being developed by Amgen in collaboration with Cytokinetics, Inc. and in an alliance with Servier for certain territories.

A phase 3 cardiovascular outcomes study for the treatment of chronic heart failure is ongoing.

Repatha®

Repatha® is a human monoclonal antibody that inhibits PCSK9.

In September 2016, we announced that the phase 3 GLAGOV study evaluating the effect of Repatha® on coronary artery disease met its primary and secondary endpoints.

17

In February 2017, we announced that the phase 3 FOURIER study evaluating the effects of Repatha® on cardiovascular outcomes met its primary composite endpoint and key secondary composite endpoint. No new safety issues were observed.

In February 2017, we announced that the phase 3 EBBINGHAUS cognitive function study achieved its primary endpoint.

Additional phase 3 studies to evaluate Repatha® in diabetes, statin intolerant subjects, with coronary imaging, and to reduce the need for future apheresis are ongoing.

Vectibix®

Vectibix® is a human monoclonal antibody antagonist of the EGFr.

In June 2015, we announced that results of a phase 3 study evaluating Vectibix® and best supportive care (BSC) met its primary endpoint, demonstrating a statistically significant improvement in overall survival in patients with chemorefractory wild-type KRAS (exon2) mCRC compared to those patients treated with BSC alone.

AMG 157

AMG 157 is a human monoclonal antibody that inhibits the action of TSLP. It is being evaluated as a treatment for asthma and atopic dermatitis, with phase 2 studies ongoing. AMG 157 is being jointly developed in collaboration with AstraZeneca plc (AstraZeneca).

AMG 520

AMG 520 is a small molecule inhibitor of BACE. It is being evaluated for the prevention of Alzheimer’s disease, with phase 2 studies ongoing. AMG 520 is being jointly developed in collaboration with Novartis.

AMG 899

AMG 899 is a small molecule CETP inhibitor. It is being evaluated for the treatment of dyslipidemia and has completed certain phase 2 studies. Development of AMG 899 is delayed pending competitor clinical trials in the class.

Amgen Development of Biosimilars

We continue to develop and commercialize biosimilar medicines. Our biosimilar product candidates are in varying stages of commercialization and clinical development as described in the following table:

Program | Reference product | Status | |

AMJEVITA™ / ABP 501 | adalimumab (HUMIRA®) | Approved by FDA across all eligible indications of reference product and MAA submitted to EMA | |

ABP 215* | bevacizumab (Avastin®) | BLA and MAA submitted to FDA and EMA, respectively | |

ABP 710 | infliximab (REMICADE®) | Phase 3 rheumatoid arthritis study ongoing | |

ABP 798* | rituximab (Rituxan® / Mabthera®) | Phase 3 rheumatoid arthritis study ongoing Phase 3 non-Hodgkin’s lymphoma study ongoing | |

ABP 959 | eculizumab (Soliris®) | Phase 1 ongoing | |

ABP 980* | trastuzumab (Herceptin®) | Phase 3 breast cancer study completed | |

* Developed in collaboration with Allergan

Business Relationships