Attached files

| file | filename |

|---|---|

| 8-K - OND Q2 FY17 EARNINGS PRESENTATION - PROCTER & GAMBLE Co | ondq2fy17earningspp.htm |

Procter and Gamble Earnings Release:Q2 FY 2017 ResultsJanuary 20, 2017

Business ResultsQ2 FY 2017

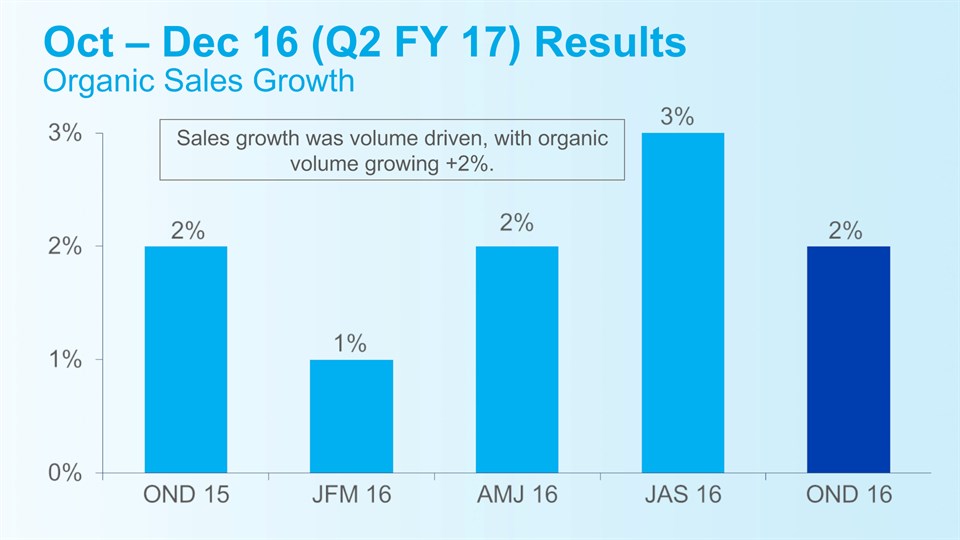

Oct – Dec 16 (Q2 FY 17) ResultsOrganic Sales Growth Sales growth was volume driven, with organic volume growing +2%.

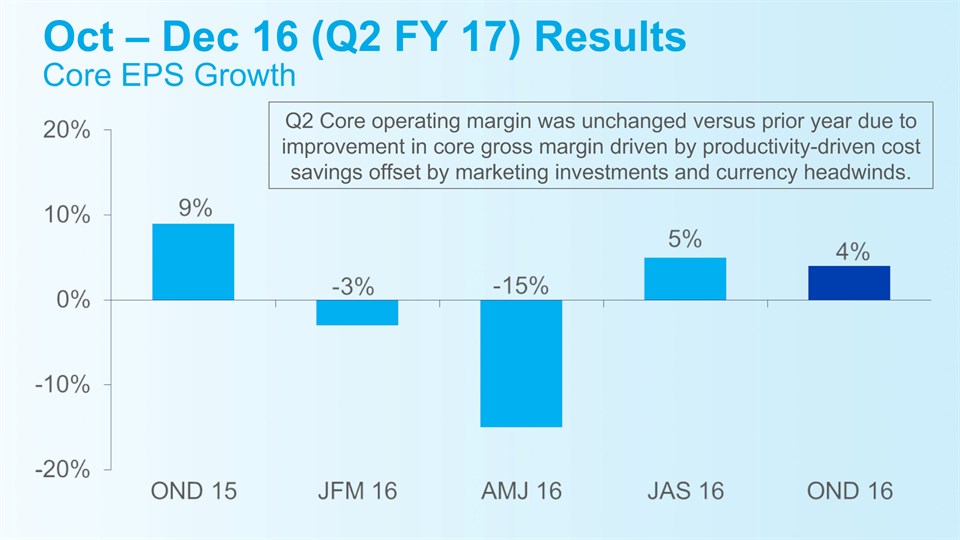

Oct – Dec 16 (Q2 FY 17) ResultsCore EPS Growth Q2 Core operating margin was unchanged versus prior year due to improvement in core gross margin driven by productivity-driven cost savings offset by marketing investments and currency headwinds.

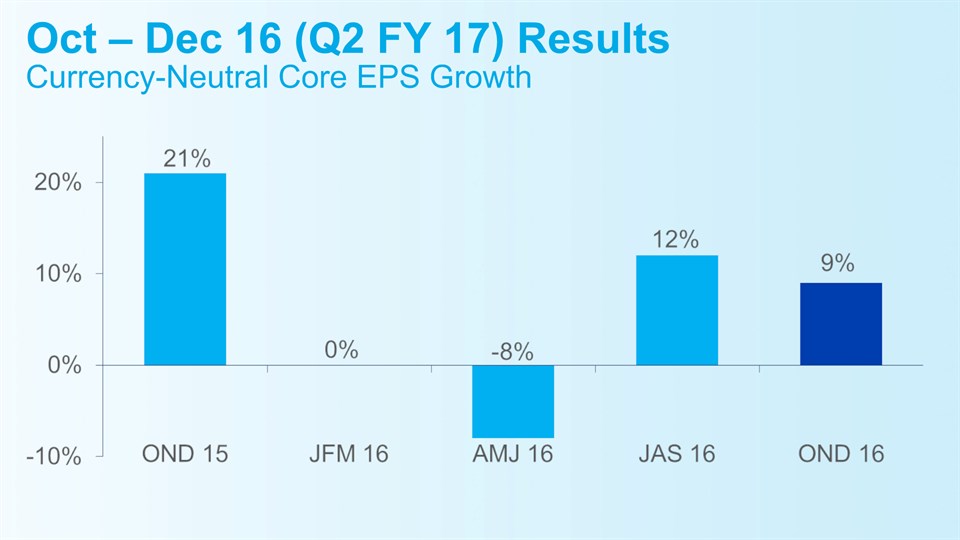

Oct – Dec 16 (Q2 FY 17) ResultsCurrency-Neutral Core EPS Growth

Business Segment Results and HighlightsQ2 FY 2017

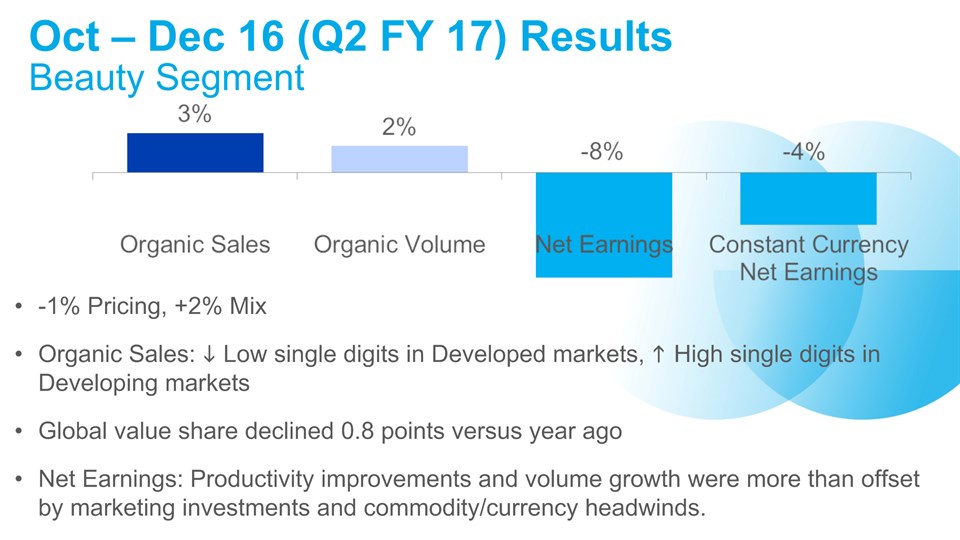

-1% Pricing, +2% MixOrganic Sales: i Low single digits in Developed markets, h High single digits in Developing marketsGlobal value share declined 0.8 points versus year agoNet Earnings: Productivity improvements and volume growth were more than offset by marketing investments and commodity/currency headwinds. Oct – Dec 16 (Q2 FY 17) ResultsBeauty Segment

Hair Care organic sales grew low single digits versus year ago. Developing markets were up mid-single digits driven by growth in GC and LA partially offset by competitive activity. Developed markets were flat with strong growth in Pantene and Head and Shoulders offset by competitive promotion activity.Skin & Personal Care organic sales grew low single digits versus year ago. Developing markets were up high single digits driven by double-digit growth on SKII in China and APDO in LA. Developed markets declined low single digits with growth in APDO and Personal Cleansing offset by Skin Care softness due to promotional activity spending. By Category Organic Sales Growth IYA Organic Sales Growth IYA Organic Sales Growth IYA By Category Global Developed Developing Hair Care + ~= + Skin & Personal Care + - + + represents growth above 1%, ~= represents growth of 1% to decline of 1%; - represents decline greater than 1%. Oct – Dec 16 (Q2 FY 17) ResultsBeauty Highlights

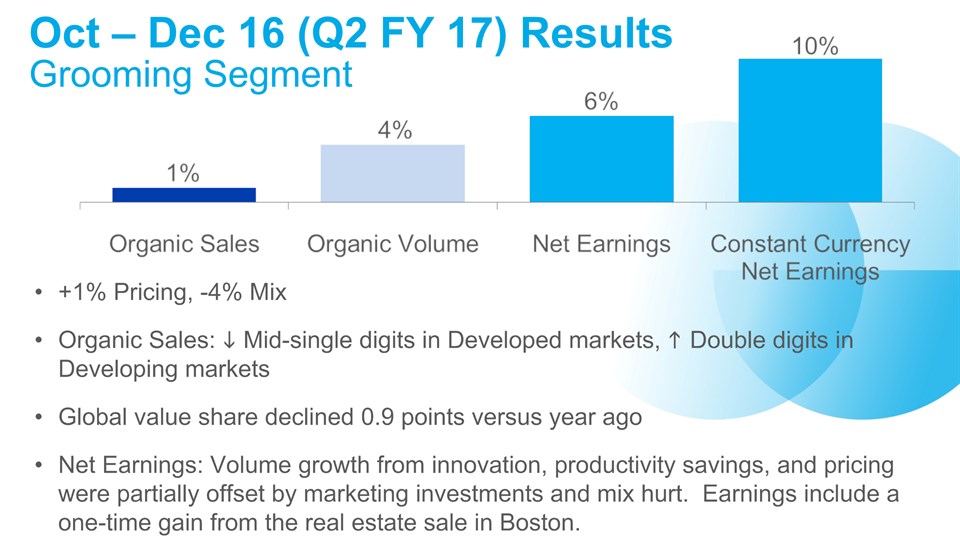

+1% Pricing, -4% Mix Organic Sales: i Mid-single digits in Developed markets, h Double digits in Developing marketsGlobal value share declined 0.9 points versus year agoNet Earnings: Volume growth from innovation, productivity savings, and pricing were partially offset by marketing investments and mix hurt. Earnings include a one-time gain from the real estate sale in Boston. Oct – Dec 16 (Q2 FY 17) ResultsGrooming Segment

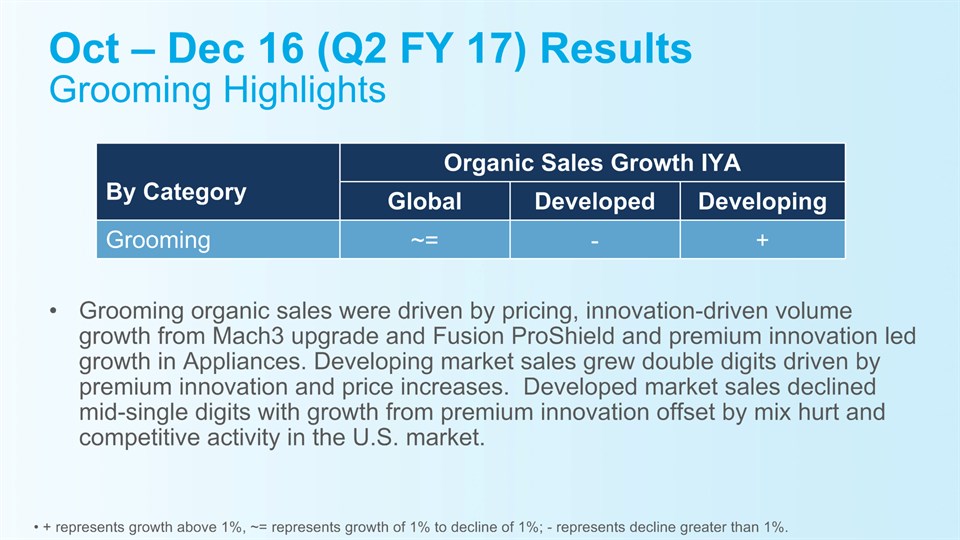

Grooming organic sales were driven by pricing, innovation-driven volume growth from Mach3 upgrade and Fusion ProShield and premium innovation led growth in Appliances. Developing market sales grew double digits driven by premium innovation and price increases. Developed market sales declined mid-single digits with growth from premium innovation offset by mix hurt and competitive activity in the U.S. market. By Category Organic Sales Growth IYA Organic Sales Growth IYA Organic Sales Growth IYA By Category Global Developed Developing Grooming ~= - + Oct – Dec 16 (Q2 FY 17) ResultsGrooming Highlights + represents growth above 1%, ~= represents growth of 1% to decline of 1%; - represents decline greater than 1%.

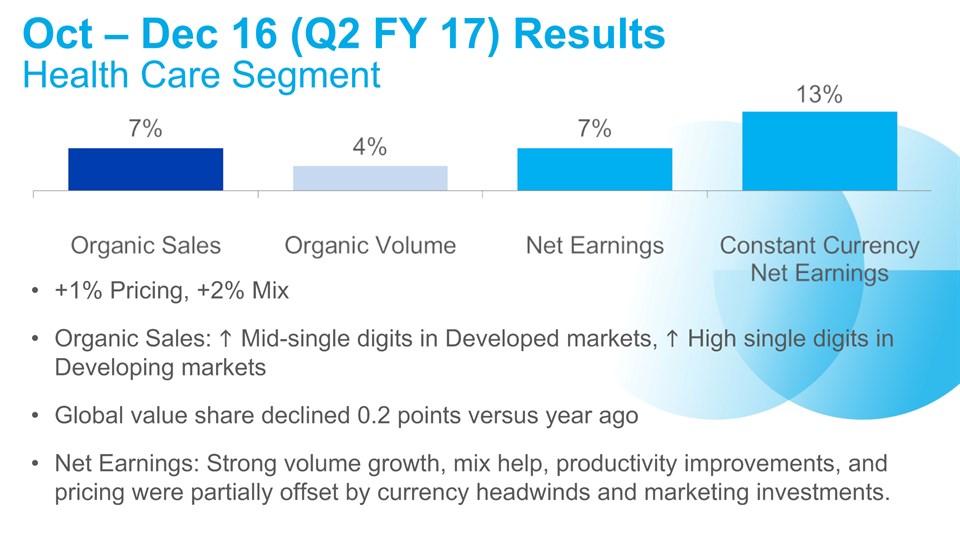

+1% Pricing, +2% MixOrganic Sales: h Mid-single digits in Developed markets, h High single digits in Developing marketsGlobal value share declined 0.2 points versus year agoNet Earnings: Strong volume growth, mix help, productivity improvements, and pricing were partially offset by currency headwinds and marketing investments. Oct – Dec 16 (Q2 FY 17) ResultsHealth Care Segment

Oral Care organic sales were up high single digits versus year ago. Developed market sales increased high single digits driven by strong volume growth in Paste and Power as well as favorable form mix. Developing markets increased double digits driven by strong volume growth and mix help across Power, Paste and Manual brush especially in China and LA. Personal Health Care organic sales increased low single digits due to increased volume and favorable product mix. By Category Organic Sales Growth IYA Organic Sales Growth IYA Organic Sales Growth IYA By Category Global Developed Developing Oral Care + + + Personal Health Care + + - + represents growth above 1%, ~= represents growth of 1% to decline of 1%; - represents decline greater than 1%. Oct – Dec 16 (Q2 FY 17) ResultsHealth Care Highlights

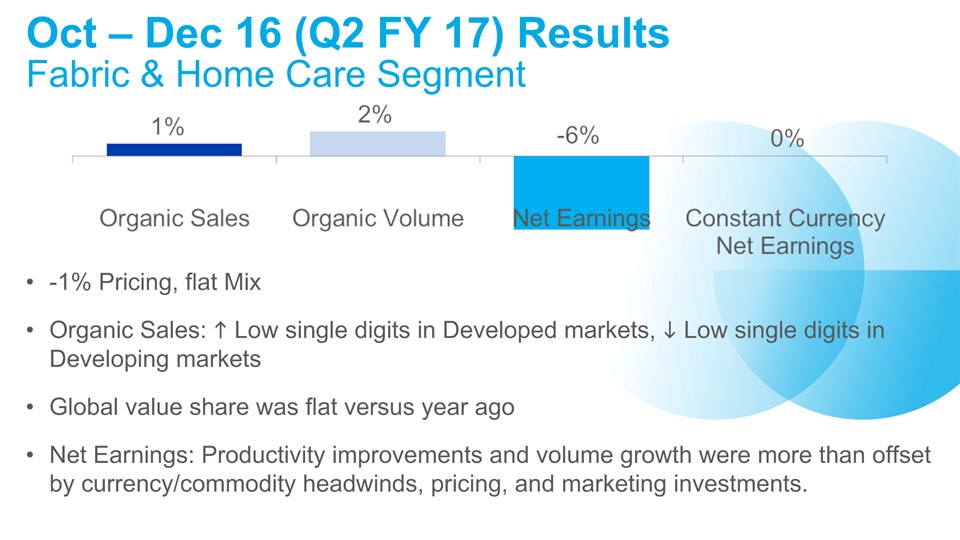

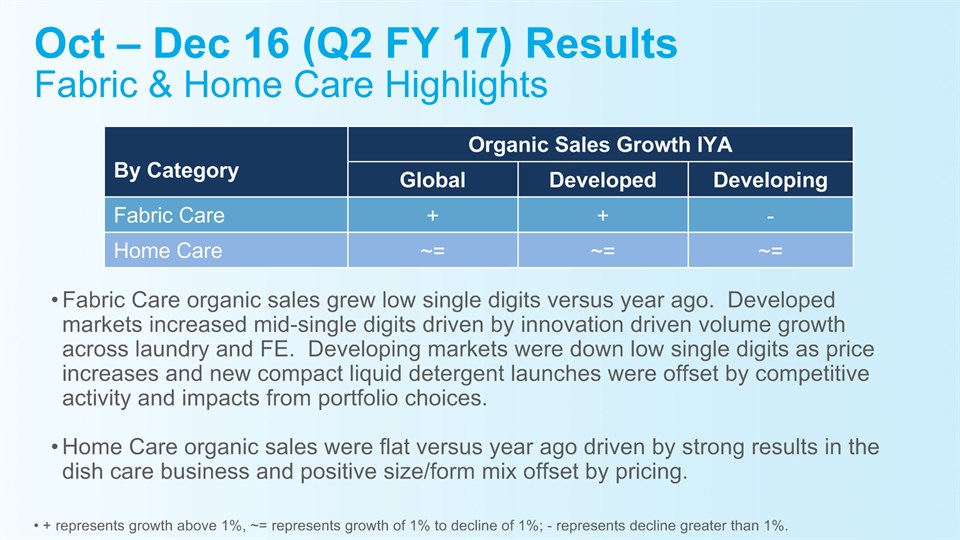

-1% Pricing, flat MixOrganic Sales: h Low single digits in Developed markets, i Low single digits in Developing marketsGlobal value share was flat versus year agoNet Earnings: Productivity improvements and volume growth were more than offset by currency/commodity headwinds, pricing, and marketing investments. Oct – Dec 16 (Q2 FY 17) ResultsFabric & Home Care Segment

Fabric Care organic sales grew low single digits versus year ago. Developed markets increased mid-single digits driven by innovation driven volume growth across laundry and FE. Developing markets were down low single digits as price increases and new compact liquid detergent launches were offset by competitive activity and impacts from portfolio choices.Home Care organic sales were flat versus year ago driven by strong results in the dish care business and positive size/form mix offset by pricing. + represents growth above 1%, ~= represents growth of 1% to decline of 1%; - represents decline greater than 1%. By Category Organic Sales Growth IYA Organic Sales Growth IYA Organic Sales Growth IYA By Category Global Developed Developing Fabric Care + + - Home Care ~= ~= ~= Oct – Dec 16 (Q2 FY 17) ResultsFabric & Home Care Highlights

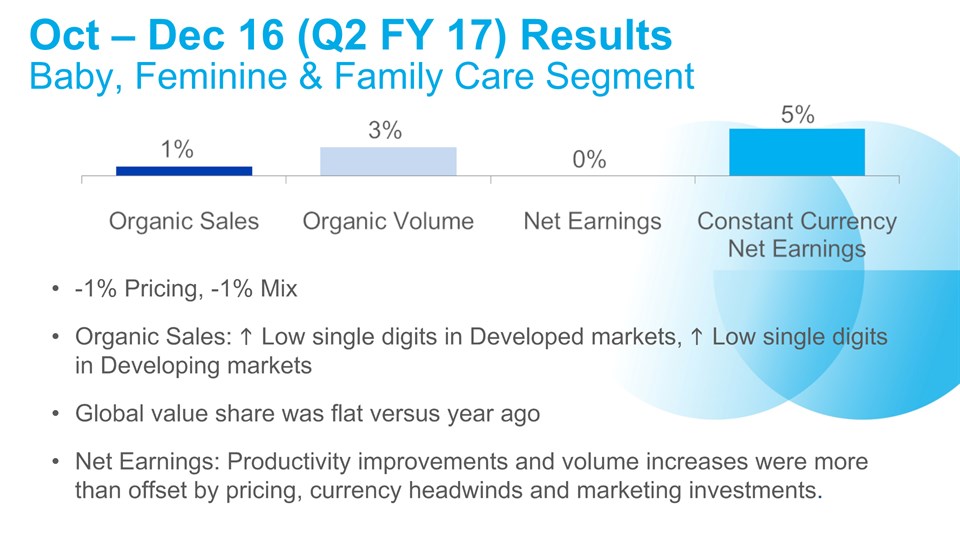

-1% Pricing, -1% MixOrganic Sales: h Low single digits in Developed markets, h Low single digits in Developing marketsGlobal value share was flat versus year agoNet Earnings: Productivity improvements and volume increases were more than offset by pricing, currency headwinds and marketing investments. Oct – Dec 16 (Q2 FY 17) ResultsBaby, Feminine & Family Care Segment

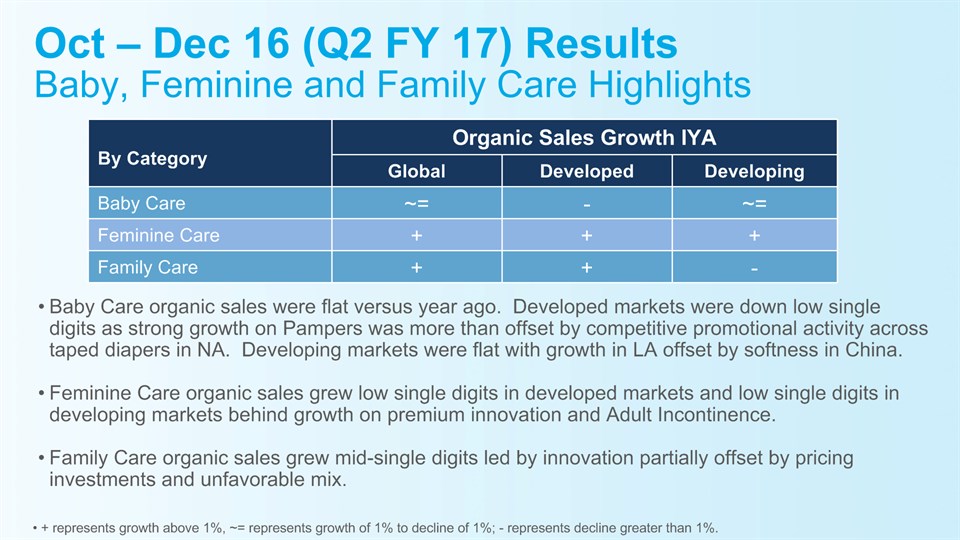

Baby Care organic sales were flat versus year ago. Developed markets were down low single digits as strong growth on Pampers was more than offset by competitive promotional activity across taped diapers in NA. Developing markets were flat with growth in LA offset by softness in China.Feminine Care organic sales grew low single digits in developed markets and low single digits in developing markets behind growth on premium innovation and Adult Incontinence.Family Care organic sales grew mid-single digits led by innovation partially offset by pricing investments and unfavorable mix. By Category Organic Sales Growth IYA Organic Sales Growth IYA Organic Sales Growth IYA By Category Global Developed Developing Baby Care ~= - ~= Feminine Care + + + Family Care + + - + represents growth above 1%, ~= represents growth of 1% to decline of 1%; - represents decline greater than 1%. Oct – Dec 16 (Q2 FY 17) ResultsBaby, Feminine and Family Care Highlights

FY 2017 Guidance

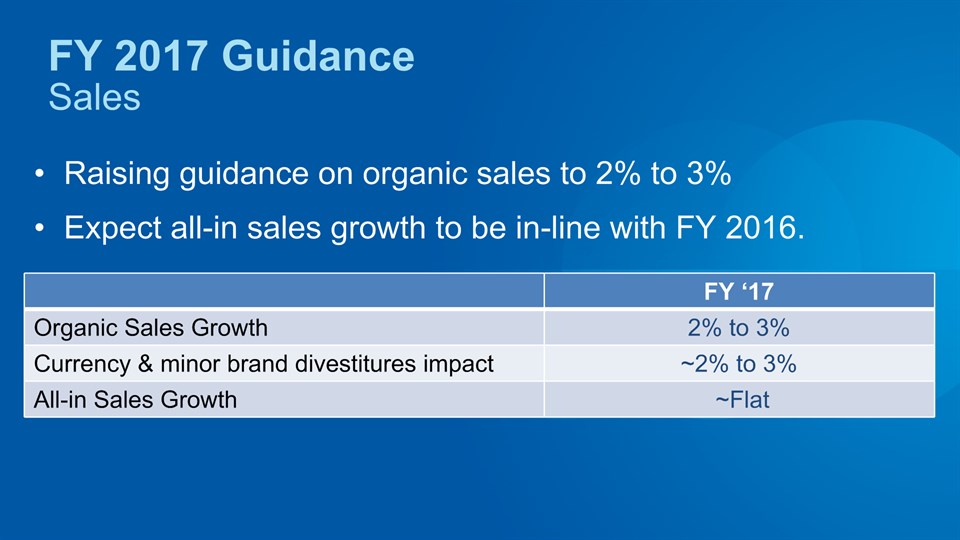

FY ‘17 Organic Sales Growth 2% to 3% Currency & minor brand divestitures impact ~2% to 3% All-in Sales Growth ~Flat Raising guidance on organic sales to 2% to 3%Expect all-in sales growth to be in-line with FY 2016. FY 2017 GuidanceSales

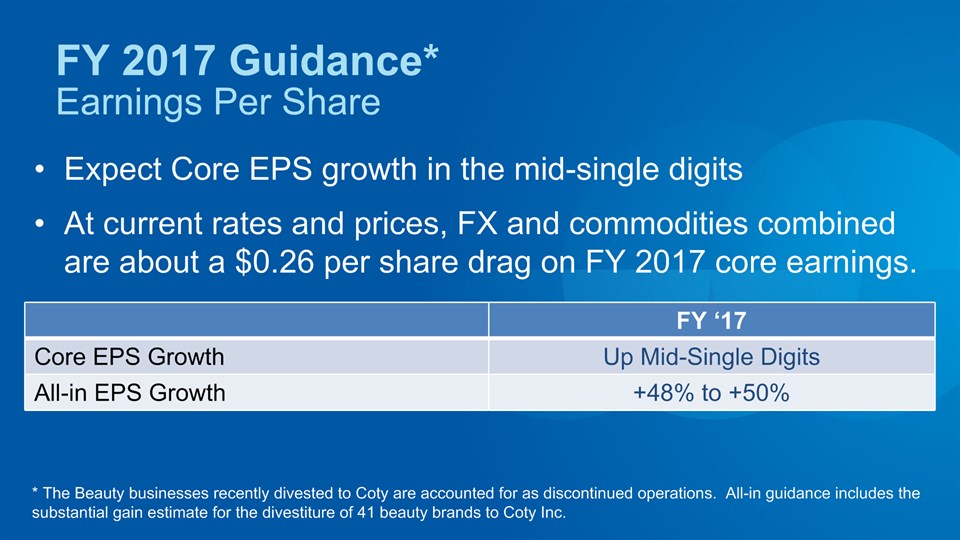

FY ‘17 Core EPS Growth Up Mid-Single Digits All-in EPS Growth +48% to +50% * The Beauty businesses recently divested to Coty are accounted for as discontinued operations. All-in guidance includes the substantial gain estimate for the divestiture of 41 beauty brands to Coty Inc. Expect Core EPS growth in the mid-single digitsAt current rates and prices, FX and commodities combined are about a $0.26 per share drag on FY 2017 core earnings. FY 2017 Guidance*Earnings Per Share

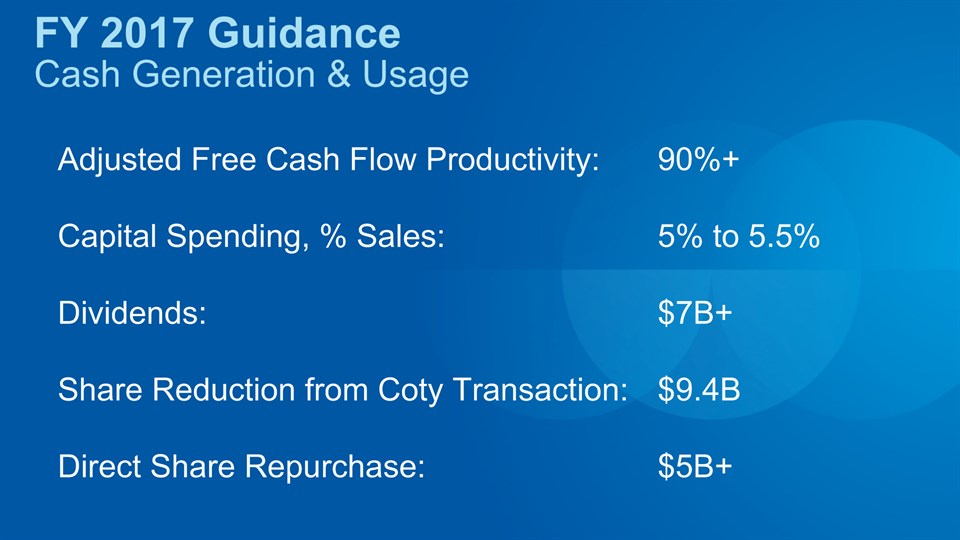

Adjusted Free Cash Flow Productivity: 90%+Capital Spending, % Sales: 5% to 5.5%Dividends: $7B+Share Reduction from Coty Transaction: $9.4BDirect Share Repurchase: $5B+ FY 2017 GuidanceCash Generation & Usage

FY 2017 GuidancePotential Headwinds Not Included in Guidance Significant deceleration of market growth rates Further political and economic volatilityFurther foreign currency weaknessFurther commodity cost increases

Forward Looking Statements Certain statements in this release or presentation, other than purely historical information, including estimates, projections, statements relating to our business plans, objectives, and expected operating results, and the assumptions upon which those statements are based, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements generally are identified by the words “believe,” “project,” “expect,” “anticipate,” “estimate,” “intend,” “strategy,” “future,” “opportunity,” “plan,” “may,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar expressions. Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties that may cause results to differ materially from those expressed or implied in the forward-looking statements. We undertake no obligation to update or revise publicly any forward-looking statements, whether because of new information, future events or otherwise. Risks and uncertainties to which our forward-looking statements are subject include, without limitation: (1) the ability to successfully manage global financial risks, including foreign currency fluctuations, currency exchange or pricing controls and localized volatility; (2) the ability to successfully manage local, regional or global economic volatility, including reduced market growth rates, and generate sufficient income and cash flow to allow the Company to effect the expected share repurchases and dividend payments; (3) the ability to manage disruptions in credit markets or changes to our credit rating; (4) the ability to maintain key manufacturing and supply arrangements (including sole supplier and sole manufacturing plant arrangements) and manage disruption of business due to factors outside of our control, such as natural disasters and acts of war or terrorism; (5) the ability to successfully manage cost fluctuations and pressures, including commodity prices, raw materials, labor costs, energy costs and pension and health care costs; (6) the ability to stay on the leading edge of innovation, obtain necessary intellectual property protections and successfully respond to technological advances attained by, and patents granted to, competitors; (7) the ability to compete with our local and global competitors in new and existing sales channels, including by successfully responding to competitive factors such as prices, promotional incentives and trade terms for products; (8) the ability to manage and maintain key customer relationships; (9) the ability to protect our reputation and brand equity by successfully managing real or perceived issues, including concerns about safety, quality, ingredients, efficacy or similar matters that may arise; (10) the ability to successfully manage the financial, legal, reputational and operational risk associated with third party relationships, such as our suppliers, contractors and external business partners; (11) the ability to rely on and maintain key information technology systems and networks (including Company and third-party systems and networks) and maintain the security and functionality of such systems and networks and the data contained therein; (12) the ability to successfully manage regulatory and legal requirements and matters (including, without limitation, those laws and regulations involving product liability, intellectual property, antitrust, privacy, tax, accounting standards and environmental) and to resolve pending matters within current estimates; (13) the ability to manage changes in applicable tax laws and regulations; (14) the ability to successfully manage our portfolio optimization strategy, including achieving and maintaining our intended tax treatment of the related transactions, and our ongoing acquisition, divestiture and joint venture activities, in each case to achieve the Company’s overall business strategy and financial objectives, without impacting the delivery of base business objectives; (15) the ability to successfully achieve productivity improvements and cost savings and manage ongoing organizational changes, while successfully identifying, developing and retaining particularly key employees, especially in key growth markets where the availability of skilled or experienced employees may be limited; and (16) the ability to manage the uncertain implications of the United Kingdom’s withdrawal from the European Union. For additional information concerning factors that could cause actual results and events to differ materially from those projected herein, please refer to our most recent 10-K, 10-Q and 8-K reports.

The Procter & Gamble Company Regulation G Reconciliation of Non-GAAP Measures

In accordance with the SEC's Regulation G, the following provides definitions of the non-GAAP measures used in Procter & Gamble's January 20, 2017 earnings call, associated slides, and other materials and the reconciliation to the most closely related GAAP measure. We believe that these measures provide useful perspective on underlying business trends (i.e. trends excluding non-recurring or unusual items) and results and provide a supplemental measure of year-on-year results. The non-GAAP measures described below are used by Management in making operating decisions, allocating financial resources and for business strategy purposes. These measures may be useful to investors as they provide supplemental information about business performance and provide investors a view of our business results through the eyes of Management. These measures are also used to evaluate senior management and are a factor in determining their at-risk compensation. These non-GAAP measures are not intended to be considered by the user in place of the related GAAP measure, but rather as supplemental information to our business results. These non-GAAP measures may not be the same as similar measures used by other companies due to possible differences in method and in the items or events being adjusted.

The measures provided are as follows:

|

1.

|

Organic sales growth—page 3

|

|

2.

|

Core EPS and currency-neutral Core EPS—pages 4-5

|

|

3.

|

Core operating profit margin and constant currency Core operating profit margin—page 6

|

|

4.

|

Core gross margin and constant currency Core gross margin—page 6

|

|

5.

|

Core effective tax rate—page 7

|

|

6.

|

Adjusted free cash flow—page 7

|

The Core earnings measures included in the following reconciliation tables refer to the equivalent GAAP measures adjusted as applicable for the following items:

|

•

|

Incremental restructuring: The Company has had and continues to have an ongoing level of restructuring activities. Such activities have resulted in ongoing annual restructuring related charges of approximately $250 - $500 million before tax. Beginning in 2012 Procter & Gamble began a $10 billion strategic productivity and cost savings initiative that includes incremental restructuring activities. This results in incremental restructuring charges to accelerate productivity efforts and cost savings. The adjustment to Core earnings includes only the restructuring costs above what we believe are the normal recurring level of restructuring costs.

|

|

•

|

Early debt extinguishment charges: During the three months ended December 31, 2016, the Company recorded a charge of $345 million after tax due to the early extinguishment of certain long-term debt. This charge represents the difference between the reacquisition price and the par value of the debt extinguished. Management does not view this charge as indicative of the Company's operating performance or underlying business results.

|

|

•

|

Venezuela deconsolidation charge: For accounting purposes, evolving conditions resulted in a lack of control over our Venezuelan subsidiaries. Therefore, in accordance with the applicable accounting standards for consolidation, effective June 30, 2015, we deconsolidated our Venezuelan subsidiaries and began accounting for our investment in those subsidiaries using the cost method of accounting. The charge was incurred to write off our net assets related to Venezuela.

|

|

•

|

Charges for certain European legal matters: Several countries in Europe issued separate complaints alleging that the Company, along with several other companies, engaged in violations of competition laws in prior periods. The Company established Legal Reserves related to these charges. Management does not view these charges as indicative of underlying business results.

|

|

•

|

Venezuela B/S remeasurement & devaluation impacts: Venezuela is a highly inflationary economy under U.S. GAAP. Prior to deconsolidation, the government enacted episodic changes to currency exchange mechanisms and rates, which resulted in currency remeasurement charges for non-dollar denominated monetary assets and liabilities held by our Venezuelan subsidiaries.

|

|

•

|

Non-cash impairment charges: During fiscal years 2013 and 2012 the Company incurred impairment charges related to the carrying value of goodwill and indefinite lived intangible assets in our Appliances and Salon Professional businesses.

|

|

•

|

Gain on Iberian JV buyout: During fiscal year 2013 we incurred a holding gain on the purchase of the balance of our Iberian joint venture from our joint venture partner.

|

We do not view the above items to be part of our sustainable results, and their exclusion from core earnings measures provides a more comparable measure of year-on-year results.

Organic sales growth: Organic sales growth is a non-GAAP measure of sales growth excluding the impacts of acquisitions, divestitures and foreign exchange from year-over-year comparisons. Managements believes this measure provides investors with a supplemental understanding of underlying sales trends by providing sales growth on a consistent basis, and this measure is used in assessing achievement of management goals for at-risk compensation.

Core EPS and currency-neutral Core EPS: Core earnings per share, or Core EPS, is a measure of the Company's diluted net earnings per share from continuing operations adjusted as indicated. Currency-neutral Core EPS is a measure of the Company's Core EPS excluding the incremental current year impact of foreign exchange. Management views these non-GAAP measures as a useful supplemental measure of Company performance over time.

Core operating profit margin and currency-neutral Core operating profit margin: Core operating profit margin is a measure of the Company's operating margin adjusted for items as indicated. Currency-neutral Core operating profit margin is a measure of the Company's Core operating profit margin excluding the incremental current year impact of foreign exchange. Management believes these non-GAAP measures provide a supplemental perspective to the Company's operating efficiency over time.

Core gross margin and currency-neutral Core gross margin: Core gross margin is a measure of the Company's gross margin adjusted for items as indicated. Currency-neutral Core gross margin is a measure of the Company's Core gross margin excluding the incremental current year impact of foreign exchange. Management believes these non-GAAP measures provide a supplemental perspective to the Company's operating efficiency over time.

Core effective tax rate: Core effective tax rate is a measure of the Company's effective tax rate adjusted for items as indicated. Management believes this non-GAAP measure provides a supplemental perspective to the Company's operating efficiency over time.

Adjusted free cash flow: Adjusted free cash flow is defined as operating cash flow less capital spending and excluding tax payments related to the Beauty Brands divestiture, which are non-recurring and not considered indicative of underlying cash flow performance. Adjusted free cash flow represents the cash that the Company is able to generate after taking into account planned maintenance and asset expansion. Management views adjusted free cash flow as an important measure because it is one factor used in determining the amount of cash available for dividends and discretionary investment.

Adjusted free cash flow productivity: Adjusted free cash flow productivity is defined as the ratio of adjusted free cash flow to net earnings excluding the loss on early debt extinguishment and gain on the sale of the Beauty Brands, which are non-recurring and not considered indicative of underlying earnings performance. Management views adjusted free cash flow productivity as a useful measure to help investors understand P&G's ability to generate cash. Adjusted free cash flow productivity is used by management in making operating decisions, allocating financial resources and for budget planning purposes. The Company's long-term target is to generate annual adjusted free cash flow productivity at or above 90 percent.

1. Organic sales growth:

|

Three Months Ended

December 31, 2016 |

Net Sales Growth

|

Foreign Exchange Impact

|

Acquisition/

Divestiture Impact* |

Organic Sales Growth

|

|||

|

Beauty

|

(1)%

|

2%

|

2%

|

3%

|

|||

|

Grooming

|

(1)%

|

2%

|

-%

|

1%

|

|||

|

Health Care

|

5%

|

2%

|

-%

|

7%

|

|||

|

Fabric Care & Home Care

|

(1)%

|

2%

|

-%

|

1%

|

|||

|

Baby, Feminine & Family Care

|

(1)%

|

2%

|

-%

|

1%

|

|||

|

Total P&G

|

-%

|

2%

|

-%

|

2%

|

*Acquisition/Divestiture Impact includes mix impacts of acquired and divested businesses and rounding impacts necessary to reconcile net sales to organic sales.

Organic Sales

Prior Periods

|

Total Company

|

Net Sales Growth

|

Foreign Exchange Impact

|

Acquisition/ Divestiture Impact*

|

Organic Sales Growth

|

||||

|

OND 2015

|

(9)%

|

8%

|

3%

|

2%

|

||||

|

JFM 2016

|

(7)%

|

5%

|

3%

|

1%

|

||||

|

AMJ 2016

|

(3)%

|

3%

|

2%

|

2%

|

||||

|

JAS 2016

|

-%

|

3%

|

-%

|

3%

|

||||

*Acquisition/Divestiture Impact also includes the impact of the Venezuela deconsolidation beginning in JAS 2015, as well as rounding impacts necessary to reconcile net sales to organic sales.

Guidance

|

Total Company

|

Net Sales Growth

|

Combined Foreign Exchange &

Acquisition/Divestiture Impact

|

Organic Sales Growth

|

|||

|

FY 2017 Estimate

|

Flat

|

Approximately 2% to 3%

|

2% to 3%

|

2. Core EPS and currency-neutral Core EPS:

|

Three Months Ended

December 31 |

|||

|

2016

|

2015

|

||

|

Diluted Net Earnings Per Share from Continuing Operations

|

$0.93

|

$1.01

|

|

|

Incremental Restructuring

|

0.03

|

0.03

|

|

|

Early Debt Extinguishment Charges

|

0.13

|

-

|

|

|

Rounding

|

(0.01)

|

-

|

|

|

Core EPS

|

$1.08

|

$1.04

|

|

|

Percentage change vs. prior period

|

4%

|

||

|

Currency Impact to Earnings

|

0.05

|

||

|

Currency-Neutral Core EPS

|

$1.13

|

||

|

Percentage change vs. prior period Core EPS

|

9%

|

||

|

Six Months Ended

December 31 |

|||

|

2016

|

2015

|

||

|

Diluted Net Earnings Per Share from Continuing Operations

|

$1.93

|

$1.97

|

|

|

Incremental Restructuring

|

0.05

|

0.05

|

|

|

Early Debt Extinguishment Charges

|

0.12

|

-

|

|

|

Rounding

|

0.01

|

-

|

|

|

Core EPS

|

$2.11

|

$2.02

|

|

|

Percentage change vs. prior period

|

4%

|

||

|

Currency Impact to Earnings

|

0.12

|

||

|

Currency-Neutral Core EPS

|

$2.23

|

||

|

Percentage change vs. prior period Core EPS

|

10%

|

||

Note – All reconciling items are presented net of tax. Tax effects are calculated consistent with the nature of the underlying transaction.

Guidance

|

Total Company

|

Diluted EPS Growth

|

Impact of Incremental Non-Core Items*

|

Core EPS Growth

|

|

FY 2017 (Estimate)

|

Up 48% to 50%

|

Approximately (44)%

|

Up mid-single digits

|

* Includes change in discontinued operations (includes gain on sale of Beauty Brands).

Prior Quarters

|

OND 15

|

OND 14

|

JFM 16

|

JFM 15

|

AMJ 16

|

AMJ 15

|

JAS 16

|

JAS 15

|

|

|

Diluted Net Earnings Per Share from Continuing Operations, attributable to P&G

|

$ 1.01

|

$ 0.92

|

$ 0.81

|

$ 0.82

|

$ 0.71

|

$ 0.17

|

$ 1.00

|

$ 0.96

|

|

Incremental Restructuring

|

0.03

|

0.02

|

0.04

|

0.06

|

0.08

|

0.06

|

0.03

|

0.02

|

|

Venezuela B/S Remeasurement & Devaluation Impacts

|

-

|

-

|

-

|

-

|

-

|

-

|

-

|

-

|

|

Charges for Pending European Legal Matters

|

-

|

0.01

|

-

|

-

|

-

|

(0.01)

|

-

|

-

|

|

Venezuela Deconsolidation Charge

|

-

|

-

|

-

|

-

|

-

|

0.71

|

-

|

-

|

|

Rounding

|

-

|

-

|

0.01

|

0.01

|

-

|

-

|

-

|

-

|

|

Core EPS

|

$ 1.04

|

$ 0.95

|

$ 0.86

|

$ 0.89

|

$ 0.79

|

$ 0.93

|

$ 1.03

|

$ 0.98

|

|

Percentage change vs. prior period

|

9%

|

-

|

(3)%

|

-

|

(15)%

|

-

|

5%

|

-

|

|

Currency Impact to Earnings

|

0.11

|

-

|

0.03

|

-

|

0.07

|

-

|

0.07

|

-

|

|

Currency-Neutral Core EPS

|

$ 1.15

|

-

|

$ 0.89

|

-

|

$ 0.86

|

-

|

$ 1.10

|

-

|

|

Percentage change vs. prior period Core EPS

|

21%

|

-

|

-%

|

-

|

(8)%

|

-

|

12%

|

-

|

Prior Years

|

FY 12

|

FY 13

|

FY 14

|

FY 15

|

FY 16

|

|

|

Diluted Net Earnings Per Share from Continuing Operations, attributable to P&G

|

$2.97

|

$3.50

|

$3.63

|

$2.84

|

$3.49

|

|

Incremental Restructuring

|

0.15

|

0.14

|

0.11

|

0.17

|

0.18

|

|

Venezuela B/S Remeasurement & Devaluation Impacts

|

-

|

0.08

|

0.09

|

0.04

|

-

|

|

Charges for Certain European Legal Matters

|

0.03

|

0.05

|

0.02

|

0.01

|

-

|

|

Venezuela Deconsolidation Charge

|

-

|

-

|

-

|

0.71

|

-

|

|

Non-Cash Impairment Charges

|

0.31

|

0.10

|

-

|

-

|

-

|

|

Gain on Iberian JV Buyout

|

-

|

(0.21)

|

-

|

-

|

-

|

|

Rounding

|

(0.01)

|

(0.01)

|

(0.01)

|

-

|

|

|

Core EPS

|

$3.45

|

$3.65

|

$3.85

|

$3.76

|

$3.67

|

|

Percentage change vs. prior year Core EPS

|

-

|

6%

|

5%

|

(2)%

|

(2)%

|

|

Currency Impact to Earnings

|

-

|

0.15

|

0.32

|

0.52

|

0.35

|

|

Currency-Neutral Core EPS

|

-

|

$3.80

|

$4.17

|

$4.28

|

$4.02

|

|

Percentage change vs. prior year Core EPS

|

-

|

10%

|

14%

|

11%

|

7%

|

3. Core operating profit margin:

|

FY 12

|

FY 13

|

FY 14

|

FY 15

|

FY 16

|

OND 15

|

OND 16

|

|

|

Operating Profit Margin

|

17.1%

|

17.7%

|

18.7%

|

15.6%

|

20.6%

|

22.8%

|

23.0%

|

|

Incremental Restructuring

|

0.7%

|

0.7%

|

0.5%

|

0.9%

|

0.9%

|

0.8%

|

0.5%

|

|

Charges for Certain European Legal Matters

|

0.1%

|

0.2%

|

0.1%

|

-

|

-

|

-

|

-

|

|

Venezuela B/S Remeasurement & Devaluation Impacts

|

-

|

0.5%

|

0.4%

|

0.2%

|

-

|

-

|

-

|

|

Venezuela Deconsolidation Charge

|

-

|

-

|

-

|

2.9%

|

-

|

-

|

-

|

|

Non-Cash Impairment

|

1.2%

|

0.4%

|

-

|

-

|

-

|

-

|

-

|

|

Rounding

|

0.1%

|

(0.1)%

|

-

|

-

|

-

|

(0.1)%

|

|

|

Core Operating Profit Margin

|

19.2%

|

19.4%

|

19.7%

|

19.6%

|

21.5%

|

23.5%

|

23.5%

|

|

Basis point change vs. prior year Core margin

|

-

|

20

|

30

|

(10)

|

190

|

-

|

-

|

|

Currency Impact to Margin

|

-

|

0.3%

|

1.2%

|

1.4%

|

0.5%

|

-

|

0.6%

|

|

Constant Currency Core Operating Profit Margin

|

-

|

19.7%

|

20.9%

|

21.0%

|

22.0%

|

-

|

24.1%

|

|

Basis point change vs. prior year Core margin

|

-

|

50

|

150

|

130

|

240

|

-

|

60

|

4. Core gross margin:

|

FY 12

|

FY 13

|

FY 14

|

FY 15

|

FY 16

|

OND 15

|

OND 16

|

|

|

Gross Margin

|

48.2%

|

48.5%

|

47.5%

|

47.6%

|

49.6%

|

50.0%

|

50.8%

|

|

Incremental Restructuring

|

0.2%

|

0.3%

|

0.4%

|

0.7%

|

1.0%

|

0.8%

|

0.8%

|

|

Rounding

|

-

|

-

|

-

|

0.1%

|

-

|

-

|

(0.1)%

|

|

Core Gross Margin

|

48.4%

|

48.8%

|

47.9%

|

48.4%

|

50.6%

|

50.8%

|

51.5%

|

|

Basis point change vs. prior year Core margin

|

-

|

40

|

(90)

|

50

|

220

|

-

|

70

|

|

Currency Impact to Margin

|

-

|

0.1%

|

1%

|

0.4%

|

0.7%

|

-

|

0.5%

|

|

Constant Currency Core Gross Margin

|

-

|

48.9%

|

48.9%

|

48.8%

|

51.3%

|

-

|

52.0%

|

|

Basis point change vs. prior year Core margin

|

-

|

50

|

10

|

90

|

290

|

-

|

120

|

5. Core effective tax rate:

|

Three Months Ended

December 31 |

|||

|

2016

|

2015

|

||

|

Effective Tax Rate

|

21.3%

|

23.6%

|

|

|

Early Debt Extinguishment Charges

|

2.2%

|

-%

|

|

|

Core Effective Tax Rate

|

23.5%

|

23.6%

|

|

|

Basis points change vs. prior period

|

(10)

|

||

6. Adjusted free cash flow:

|

Three Months Ended December 31, 2016

|

||||

|

Operating Cash Flow

|

Capital Spending

|

Free Cash Flow

|

Cash Tax Payment – Beauty Sale

|

Adjusted Free Cash Flow

|

|

$3,000

|

$(745)

|

$2,255

|

$129

|

$2,384

|