Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Sucampo Pharmaceuticals, Inc. | f8k_010917.htm |

Exhibit 99.1

January 2017 Sucampo Pharmaceuticals, Inc. Corporate Update

Forward Looking Statements This presentation contains "forward - looking statements" as that term is defined in the Private Securities Litigation Reform Act of 1995. These statements are based on management's current expectations and involve risks and uncertainties, which may cause results to differ materially from those set forth in the statements. The forward - looking statements may include statements regarding product development, and other statements that are not historical facts. The following factors, among others, could cause actual results to differ from those set forth in the forward - looking statements: the impact of pharmaceutical industry regulation and health care legislation; Sucampo's ability to accurately predict future market conditions; dependence on the effectiveness of Sucampo's patents and other protections for innovative products; the effects of competitive products on Sucampo’s products; and the exposure to litigation and/or regulatory actions. No forward - looking statement can be guaranteed and actual results may differ materially from those projected. Sucampo undertakes no obligation to publicly update any forward - looking statement, whether as a result of new information, future events, or otherwise. Forward - looking statements in this press release should be evaluated together with the many uncertainties that affect Sucampo's business, particularly those mentioned in the risk factors and cautionary statements in Sucampo's most recent Form 10 - K as filed with the Securities and Exchange Commission on March 11, 2016, as amended, as well as its filings with the Securities and Exchange Commission on Forms 8 - K and 10 - Q since the filing of the Form 10 - K, all of which Sucampo incorporates by reference. 2

Non - GAAP Metrics 3 This presentation contains three financial metrics (Adjusted Net Income, EBITDA and Adjusted EBITDA) that are considered “non - GAAP” financial metrics under applicable Securities and Exchange Commission rules and regulations. These non - GAAP financial metrics should be considered supplemental to and not a substitute for financial information prepared in accordance wit h generally accepted accounting principles. The company’s definition of these non - GAAP metrics may differ from similarly titled metrics used by others. Adjusted Net Income adjusts for specified items that can be highly variable or difficult to predict, and various non - cash items, which includes acquisition related expenses, amortization of intangibles, share compensation expense, restructuring costs, acquisition related acceleration of deferred revenue, legal settlements, amortization of financing costs , a nd the tax impact of these adjustments. EBITDA reflects net income excluding the impact of depreciation, amortization (including amortization impairment), interest expense, interest income and provision for income taxes. Adjusted EBITDA reflects EBITDA and adjusts for specified items that can be highly variable or difficult to predict, and various non - cash items, which includes acquisition related expenses, share compensation expense, acquisition related acceleration of deferred revenue, restructuring costs, and legal settlements. The company views these non - GAAP financial metrics as a means to facilitate management’s financial and operational decision - making, including evaluation of the company’s historical operating results and comparison to competitors’ operating results. These non - GAAP financial metrics reflect an additional way of viewing aspects of the company’s operations that, when viewed with GAAP results may provide a more complete understanding of factors and trends affecting the company’s business. The determination of the amounts that are excluded from these non - GAAP financial metrics is a matter of management judgment and depends upon, among other factors, the nature of the underlying expense or income amounts. Because non - GAAP financial metrics exclude the effect of items that will increase or decrease the company’s reported results of operations, management strongly encourages investors to review the company’s consolidated financial statements and publicly - filed reports in their entirety.

Investment Highlights 4 • Global biopharmaceutical company with proven track record of successful product development and focus on innovative R&D • Business model supports financial strength with significant EBITDA and cash flow to fuel continued transformation – Sustained revenue growth from AMITIZA ® (lubiprostone): highly differentiated product with broadest label in $5B+ constipation market – Transforming AMITIZA into a durable franchise that the Company will leverage to build a leading biopharmaceuticals company focused on specialty diseases • Business development strategy to bolster growth and diversify – Acquisition of R - Tech Ueno increases revenue and builds scale – Exclusive option to commercialize a Phase 3 program in familial adenomatous polyposis (FAP) with Cancer Prevention Pharmaceuticals • Deep management team with proven ability to transform the Company and create value

Proven and Experienced Management Team 5 Peter Greenleaf Chief Executive Officer Peter Kiener, D.Phil Chief Scientific Officer Peter Lichtlen, M.D., Ph.D. Chief Medical Officer Matthias Alder Executive Vice President, Business Development & Licensing Steven Caffé, M.D. Senior Vice President, Global PV, Regulatory Affairs & Quality Silvia Taylor Senior Vice President, Investor Relations and Corporate Affairs Andrew Smith Chief Financial Officer Max Donley Executive Vice President of Global Human Resource, IT and Strategy Elissa Cote Senior Vice President, Strategic Business Insights Experienced Management Team with Considerable Experience in Product Development and Commercialization

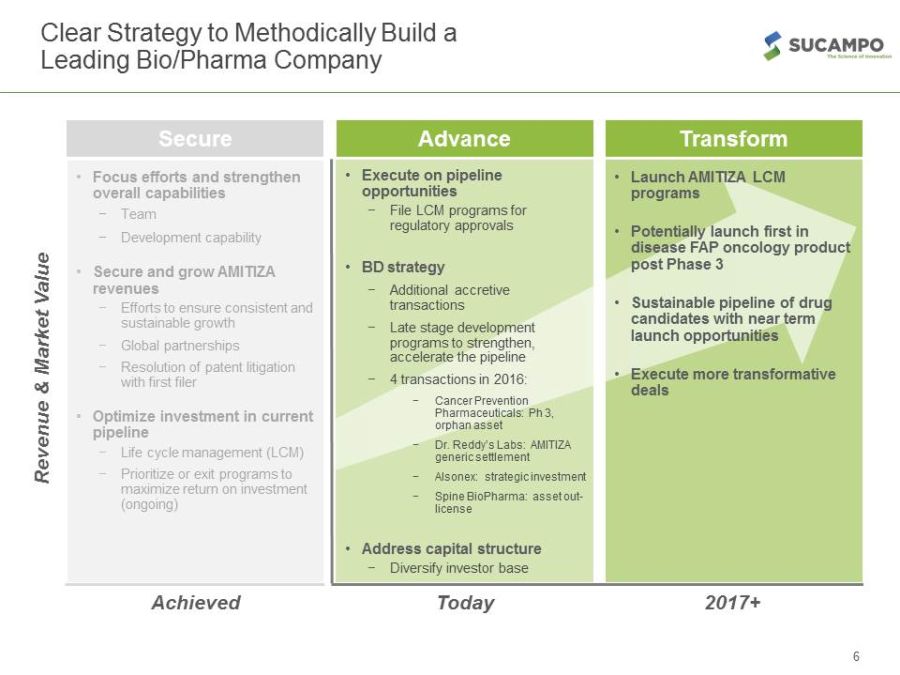

Achieved Today 2017+ Revenue & Market Value Secure Advance Transform • Execute on pipeline opportunities − File LCM programs for regulatory approvals • BD strategy − Additional accretive transactions − Late stage development programs to strengthen, accelerate the pipeline − 4 transactions in 2016: − Cancer Prevention Pharmaceuticals: Ph 3, orphan asset − Dr. Reddy’s Labs: AMITIZA generic settlement − Alsonex : strategic investment − Spine BioPharma : asset out - license • Address capital structure − Diversify investor base • Focus efforts and strengthen overall capabilities − Team − Development capability • Secure and grow AMITIZA revenues − Efforts to ensure consistent and sustainable growth − Global partnerships − Resolution of patent litigation with first filer • Optimize investment in current pipeline − Life cycle management (LCM) − Prioritize or exit programs to maximize return on investment (ongoing) • Launch AMITIZA LCM programs • Potentially launch first in disease FAP oncology product post Phase 3 • Sustainable pipeline of drug candidates with near term launch opportunities • Execute more transformative deals 6 Clear Strategy to Methodically Build a Leading Bio/Pharma Company

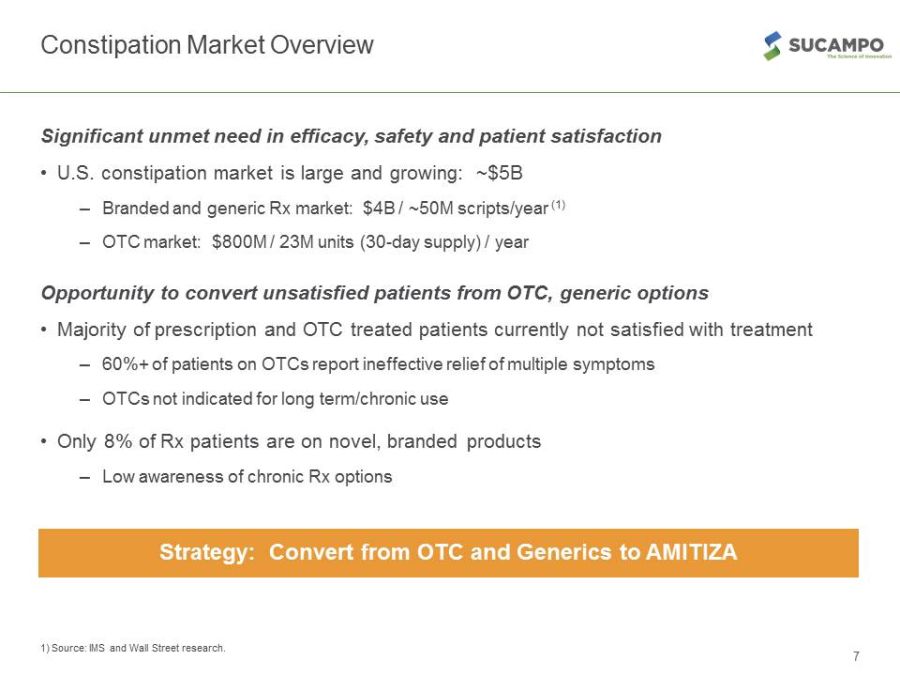

Constipation Market Overview 7 Significant unmet need in efficacy, safety and patient satisfaction • U.S. constipation market is large and growing: ~$5B – Branded and generic Rx market: $4B / ~50M scripts/year (1) – OTC market: $800M / 23M units (30 - day supply) / year Opportunity to convert unsatisfied patients from OTC, generic options • Majority of prescription and OTC treated patients currently not satisfied with treatment – 60%+ of patients on OTCs report ineffective relief of multiple symptoms – OTCs not indicated for long term/chronic use • Only 8% of Rx patients are on novel, branded products – Low awareness of chronic Rx options 1) Source: IMS and Wall Street research. Generic + Branded Generic Strategy: Convert from OTC and Generics to AMITIZA

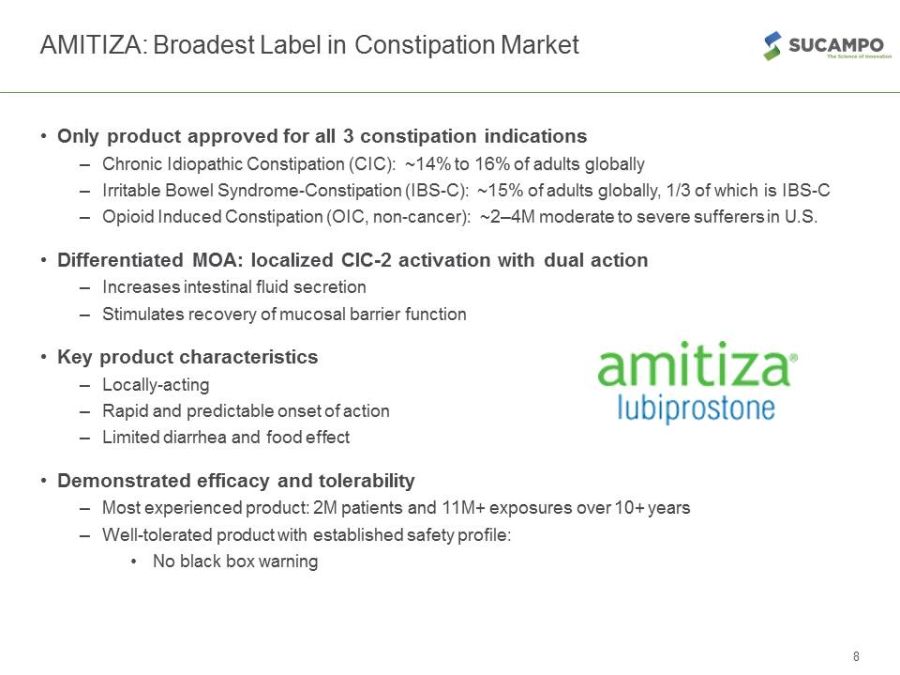

AMITIZA: Broadest Label in Constipation Market 8 • Only product approved for all 3 constipation indications – Chronic Idiopathic Constipation (CIC): ~14% to 16% of adults globally – Irritable Bowel Syndrome - Constipation (IBS - C): ~15% of adults globally, 1/3 of which is IBS - C – Opioid Induced Constipation (OIC, non - cancer): ~2 – 4M moderate to severe sufferers in U.S. • Differentiated MOA: localized ClC - 2 activation with dual action – Increases intestinal fluid secretion – Stimulates recovery of mucosal barrier function • Key product characteristics – Locally - acting – Rapid and predictable onset of action – Limited diarrhea and food effect • Demonstrated efficacy and tolerability – Most experienced product: 2M patients and 11M+ exposures over 10+ years – Well - tolerated product with established safety profile: • No black box warning

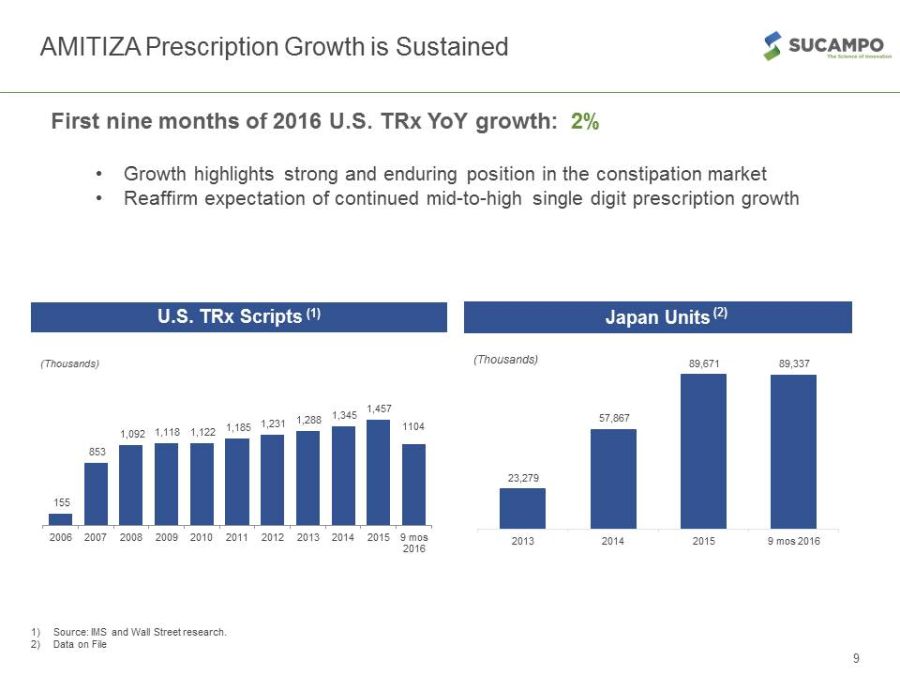

9 U.S. TRx Scripts (1) 1104 155 853 1,092 1,118 1,122 1,185 1,231 1,288 1,345 1,457 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 9 mos 2016 (Thousands) AMITIZA Prescription Growth is Sustained First nine months of 2016 U.S. TRx YoY growth: 2% • Growth highlights strong and enduring position in the constipation market • Reaffirm expectation of continued mid - to - high single digit prescription growth 1) Source: IMS and Wall Street research. 2) Data on File 23,279 57,867 89,671 89,337 2013 2014 2015 9 mos 2016 Japan Units (Thousands) (2)

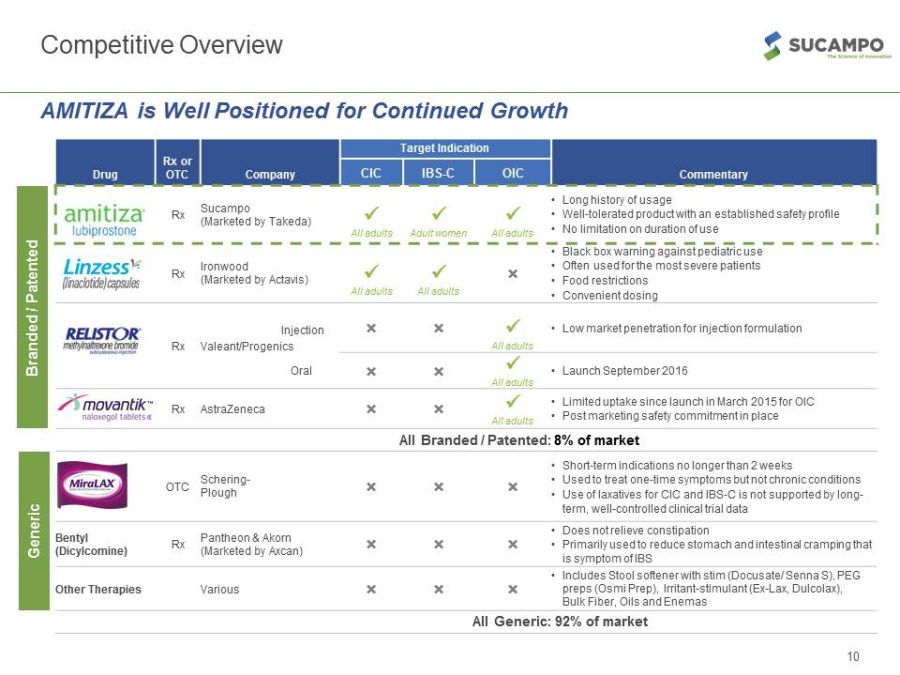

Competitive Overview 10 Drug Rx or OTC Company Target Indication Commentary CIC IBS - C OIC Rx Sucampo (Marketed by Takeda) x All adults x Adult women x All adults • Long history of usage • Well - tolerated product with an established safety profile • No limitation on duration of use Rx Ironwood (Marketed by Actavis) x All adults x All adults × • Black box warning against pediatric use • Often used for the most severe patients • Food restrictions • Convenient dosing Rx Valeant/Progenics × × x All adults • Low market penetration for injection formulation × × x All adults • Launch September 2016 Rx AstraZeneca × × x All adults • Limited uptake since launch in March 2015 for OIC • Post marketing safety commitment in place All Branded / Patented: 8% of market OTC Schering - Plough × × × • Short - term indications no longer than 2 weeks • Used to treat one - time symptoms but not chronic conditions • Use of laxatives for CIC and IBS - C is not supported by long - term, well - controlled clinical trial data Bentyl (Dicylcomine) Rx Pantheon & Akorn (Marketed by Axcan) × × × • Does not relieve constipation • Primarily used to reduce stomach and intestinal cramping that is symptom of IBS Other Therapies Various × × × • Includes Stool softener with stim (Docusate/ Senna S), PEG preps (Osmi Prep), Irritant - stimulant (Ex - Lax, Dulcolax), Bulk Fiber, Oils and Enemas All Generic: 92% of market Branded / Patented Generic Oral Injection AMITIZA is Well Positioned for Continued Growth

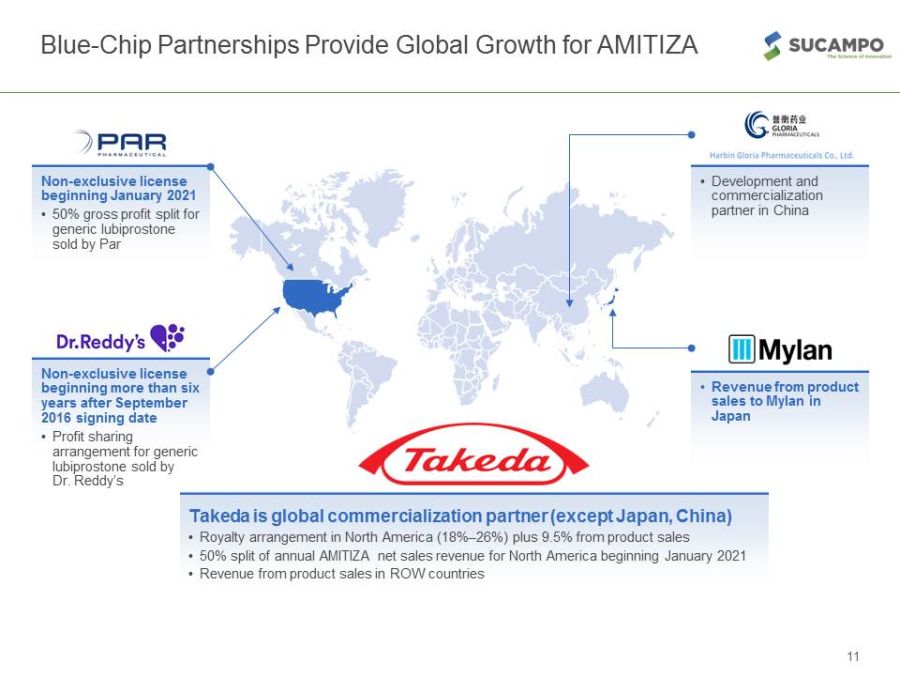

Blue - Chip Partnerships Provide Global Growth for AMITIZA 11 Takeda is global commercialization partner (except Japan, China) • Royalty arrangement in North America (18% – 26%) plus 9.5% from product sales • 50% split of annual AMITIZA net sales revenue for North America beginning January 2021 • Revenue from product sales in ROW countries Non - exclusive license beginning more than six years after September 2016 signing date • Profit sharing arrangement for generic lubiprostone sold by Dr. Reddy’s Non - exclusive license beginning January 2021 • 50% gross profit split for generic lubiprostone sold by Par • Revenue from product sales to Mylan in Japan • Development and commercialization partner in China

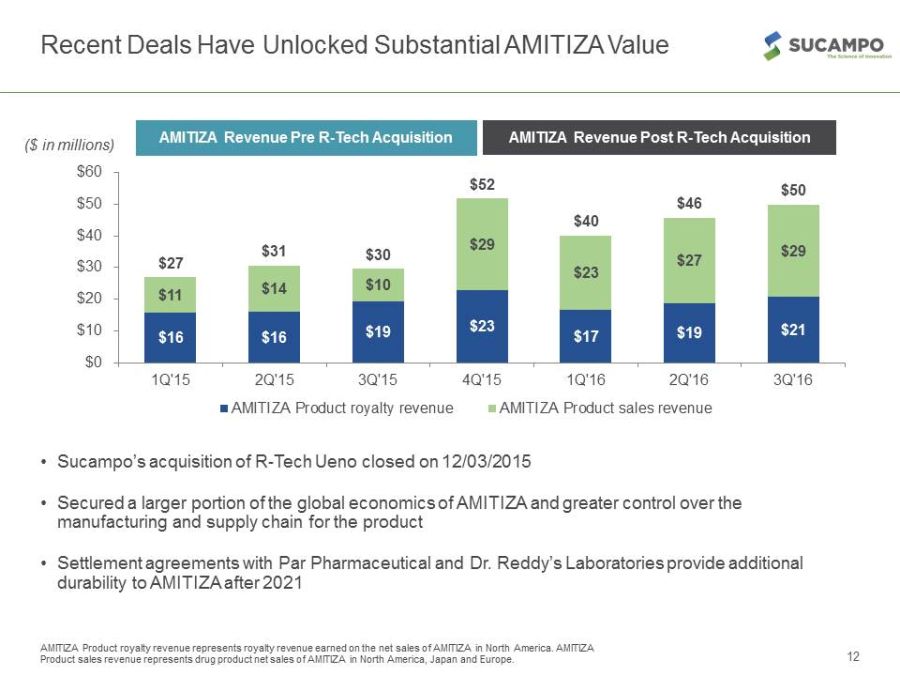

Recent Deals Have Unlocked Substantial AMITIZA Value 12 • Sucampo’s acquisition of R - Tech Ueno closed on 12/03/2015 • Secured a larger portion of the global economics of AMITIZA and greater control over the manufacturing and supply chain for the product • Settlement agreements with Par Pharmaceutical and Dr. Reddy’s Laboratories provide additional durability to AMITIZA after 2021 AMITIZA Product royalty revenue represents royalty revenue earned on the net sales of AMITIZA in North America. AMITIZA Product sales revenue represents drug product net sales of AMITIZA in North America, Japan and Europe. ($ in millions) $16 $16 $19 $23 $17 $19 $21 $11 $14 $10 $29 $23 $27 $29 $27 $31 $30 $52 $40 $46 $50 $0 $10 $20 $30 $40 $50 $60 1Q'15 2Q'15 3Q'15 4Q'15 1Q'16 2Q'16 3Q'16 AMITIZA Product royalty revenue AMITIZA Product sales revenue AMITIZA Revenue Pre R - Tech Acquisition AMITIZA Revenue Post R - Tech Acquisition

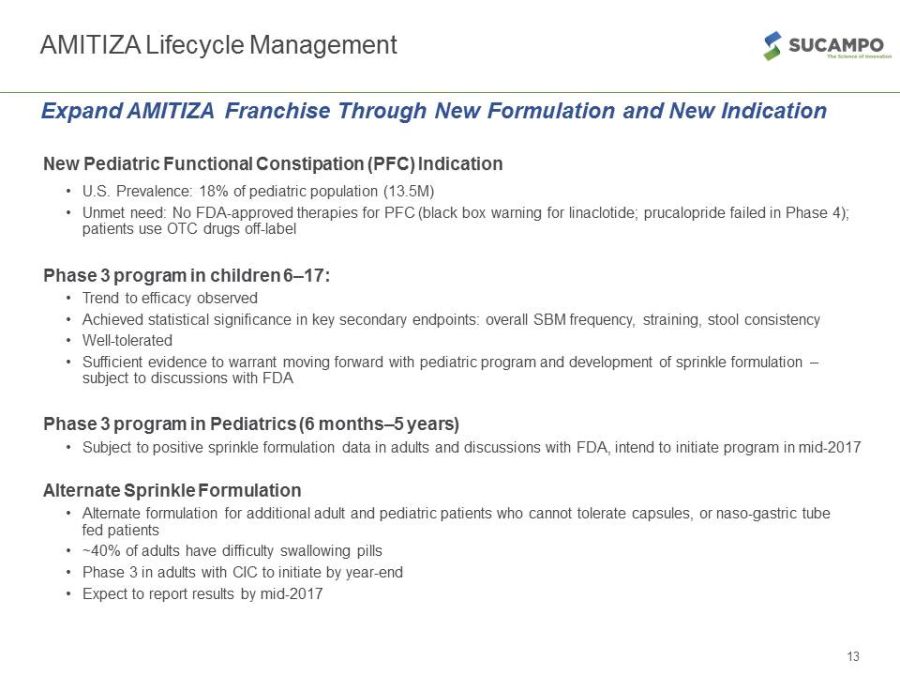

13 New Pediatric Functional Constipation (PFC) Indication • U.S. Prevalence: 18% of pediatric population (13.5M) • Unmet need: No FDA - approved therapies for PFC (black box warning for linaclotide; prucalopride failed in Phase 4); patients use OTC drugs off - label Phase 3 program in children 6 – 17: • Trend to efficacy observed • Achieved statistical significance in key secondary endpoints: overall SBM frequency, straining, stool consistency • Well - tolerated • Sufficient evidence to warrant moving forward with pediatric program and development of sprinkle formulation – subject to discussions with FDA Phase 3 program in Pediatrics (6 months – 5 years) • Subject to positive sprinkle formulation data in adults and discussions with FDA, intend to initiate program in mid - 2017 Alternate Sprinkle Formulation • Alternate formulation for additional adult and pediatric patients who cannot tolerate capsules, or naso - gastric tube fed patients • ~40% of adults have difficulty swallowing pills • Phase 3 in adults with CIC to initiate by year - end • Expect to report results by mid - 2017 AMITIZA Lifecycle Management Expand AMITIZA Franchise Through New Formulation and New Indication

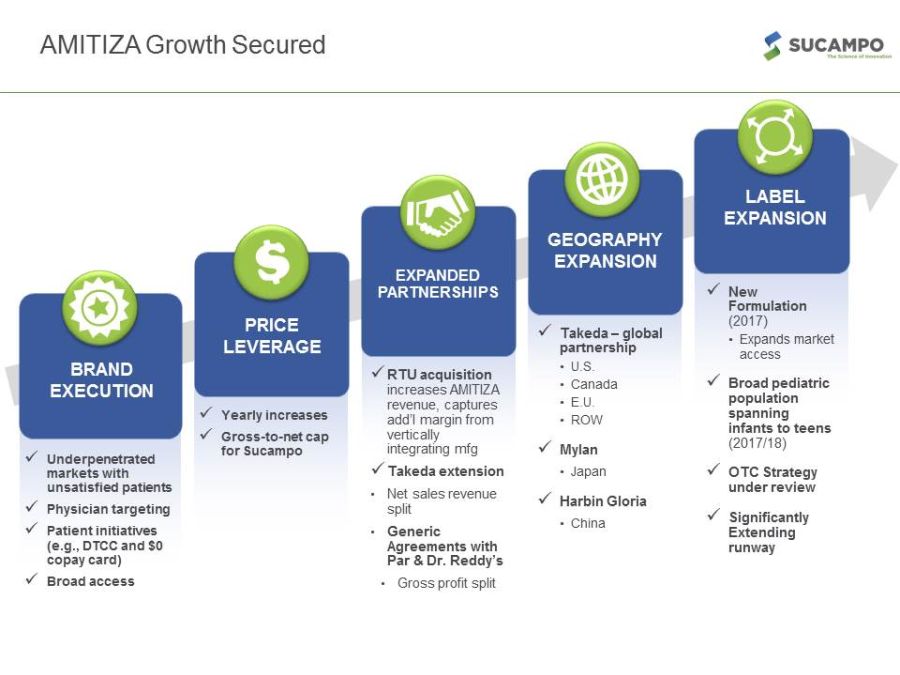

AMITIZA Growth Secured x RTU acquisition increases AMITIZA revenue, captures add’l margin from vertically integrating mfg x Takeda extension • Net sales revenue split • Generic Agreements with Par & Dr. Reddy’s • Gross profit split x Underpenetrated markets with unsatisfied patients x Physician targeting x Patient initiatives (e.g., DTCC and $0 copay card) x Broad access x Takeda – global partnership • U.S. • Canada • E.U. • ROW x Mylan • Japan x Harbin Gloria • China x New Formulation (2017) • Expands market access x Broad pediatric population spanning infants to teens (2017/18) x OTC Strategy under review x Significantly Extending runway BRAND EXECUTION LABEL EXPANSION GEOGRAPHY EXPANSION PRICE LEVERAGE EXPANDED PARTNERSHIPS x Yearly increases x Gross - to - net cap for Sucampo

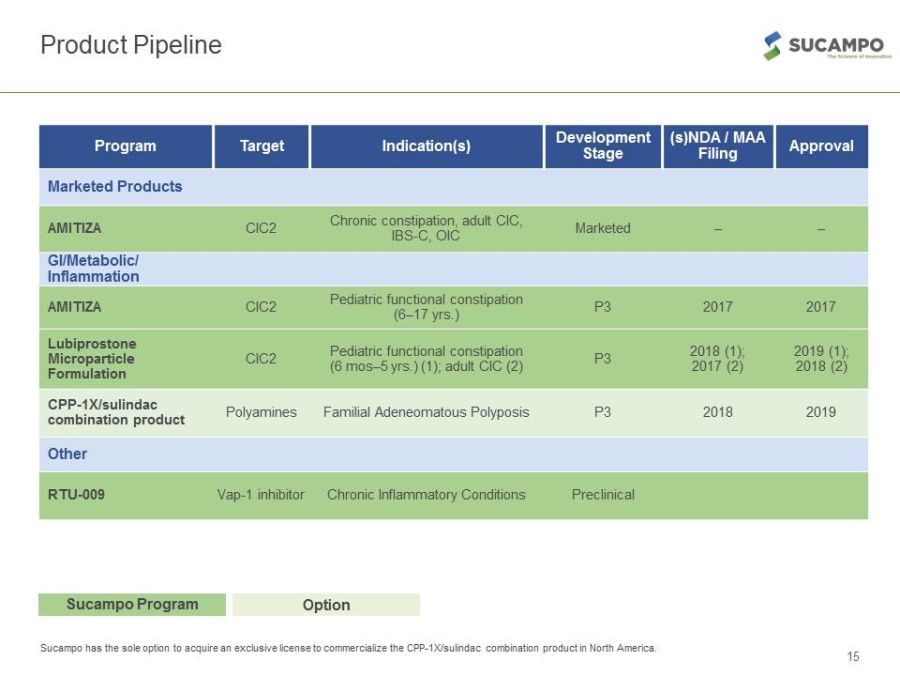

Product Pipeline 15 Sucampo has the sole option to acquire an exclusive license to commercialize the CPP - 1X/sulindac combination product in North Am erica. Sucampo Program Option Program Target Indication(s) Development Stage (s)NDA / MAA Filing Approval Marketed Products AMITIZA CIC2 Chronic constipation, adult CIC, IBS - C, OIC Marketed – – GI/Metabolic/ Inflammation AMITIZA CIC2 Pediatric functional constipation (6 – 17 yrs.) P3 2017 2017 Lubiprostone Microparticle Formulation CIC2 Pediatric functional constipation (6 mos – 5 yrs.) (1); adult CIC (2) P3 2018 (1); 2017 (2) 2019 (1); 2018 (2) CPP - 1X/sulindac combination product Polyamines Familial Adeneomatous Polyposis P3 2018 2019 Other RTU - 009 Vap - 1 inhibitor Chronic Inflammatory Conditions Preclinical

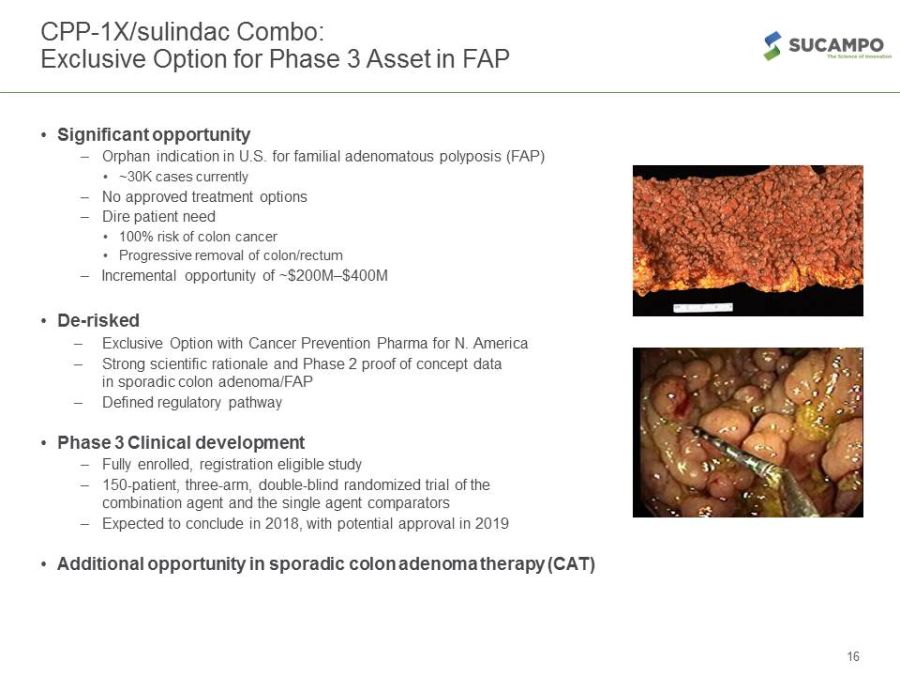

CPP - 1X/sulindac Combo: Exclusive Option for Phase 3 Asset in FAP 16 • Significant opportunity – Orphan indication in U.S. for familial adenomatous polyposis (FAP) • ~30K cases currently – No approved treatment options – Dire patient need • 100% risk of colon cancer • Progressive removal of colon/rectum – Incremental opportunity of ~$200M – $400M • De - risked – Exclusive Option with Cancer Prevention Pharma for N. America – Strong scientific rationale and Phase 2 proof of concept data in sporadic colon adenoma/FAP – Defined regulatory pathway • Phase 3 Clinical development – Fully enrolled, registration eligible study – 150 - patient, three - arm, double - blind randomized trial of the combination agent and the single agent comparators – Expected to conclude in 2018, with potential approval in 2019 • Additional opportunity in sporadic colon adenoma therapy (CAT)

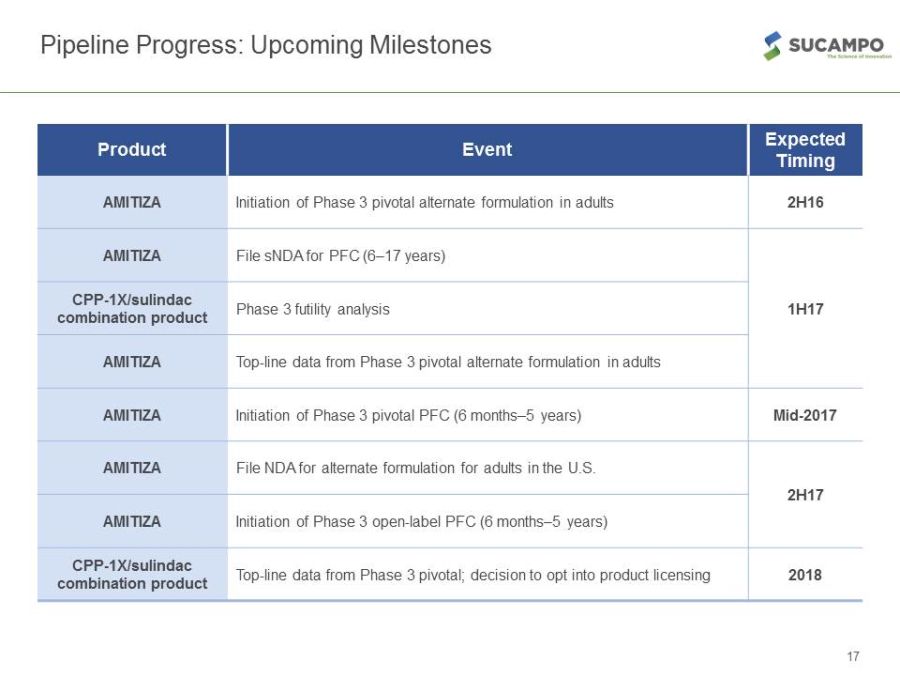

Pipeline Progress: Upcoming Milestones 17 Product Event Expected Timing AMITIZA Initiation of Phase 3 pivotal alternate formulation in adults 2H16 AMITIZA File sNDA for PFC (6 – 17 years) 1H17 CPP - 1X/sulindac combination product Phase 3 futility analysis AMITIZA Top - line data from Phase 3 pivotal alternate formulation in adults AMITIZA Initiation of Phase 3 pivotal PFC (6 months – 5 years) Mid - 2017 AMITIZA File NDA for alternate formulation for adults in the U.S. 2H17 AMITIZA Initiation of Phase 3 open - label PFC (6 months – 5 years) CPP - 1X/sulindac combination product Top - line data from Phase 3 pivotal; decision to opt into product licensing 2018

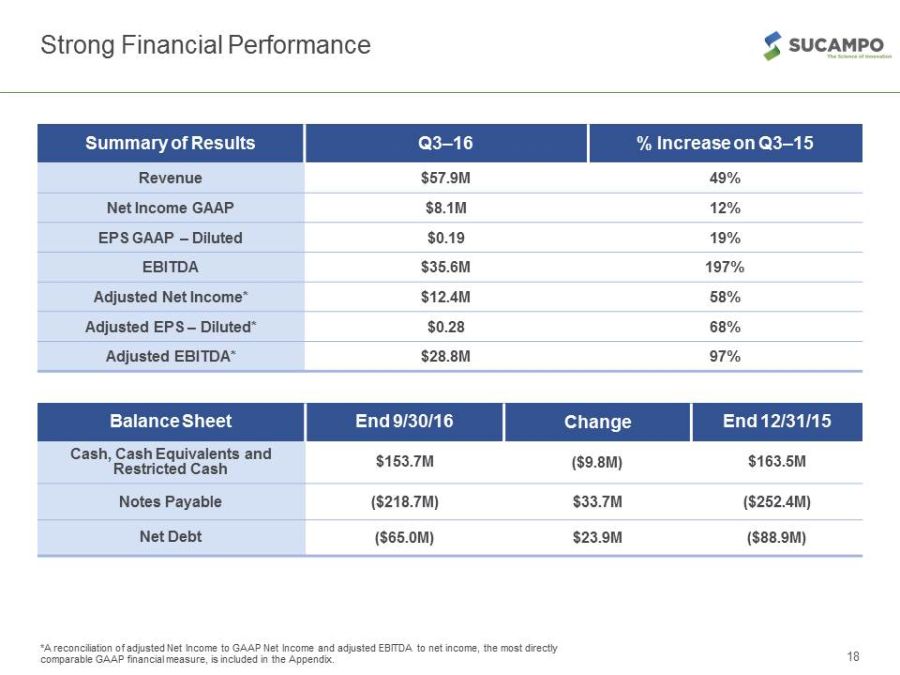

Strong Financial Performance 18 *A reconciliation of adjusted Net Income to GAAP Net Income and adjusted EBITDA to net income, the most directly comparable GAAP financial measure, is included in the Appendix. Summary of Results Q3 – 16 % Increase on Q3 – 15 Revenue $57.9M 49% Net Income GAAP $8.1M 12% EPS GAAP – Diluted $0.19 19% EBITDA $35.6M 197% Adjusted Net Income* $12.4M 58% Adjusted EPS – Diluted* $0.28 68% Adjusted EBITDA* $28.8M 97% Balance Sheet End 9/30/16 Change End 12/31/15 Cash, Cash Equivalents and Restricted Cash $153.7M ($9.8M) $163.5M Notes Payable ($218.7M) $33.7M ($252.4M) Net Debt ($65.0M) $23.9M ($88.9M)

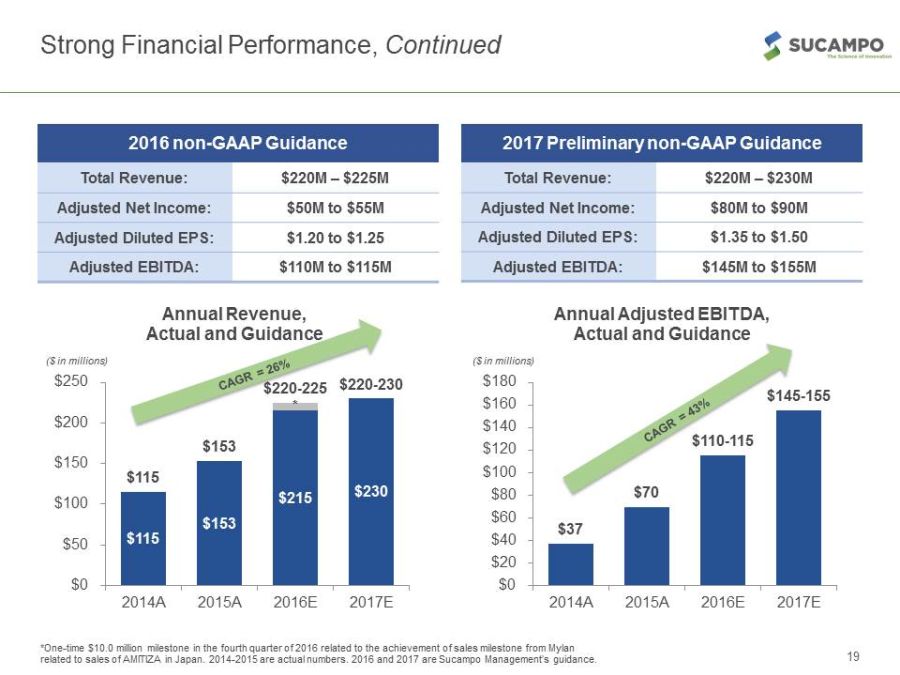

2016 non - GAAP Guidance Total Revenue: $220M – $225M Adjusted Net Income: $50M to $55M Adjusted Diluted EPS: $1.20 to $1.25 Adjusted EBITDA: $110M to $115M Strong Financial Performance, Continued 19 *One - time $10.0 million milestone in the fourth quarter of 2016 related to the achievement of sales milestone from Mylan related to sales of AMITIZA in Japan. 2014 - 2015 are actual numbers. 2016 and 2017 are Sucampo Management’s guidance. $115 $153 $215 $230 * $115 $153 $220 - 225 $220 - 230 $0 $50 $100 $150 $200 $250 2014A 2015A 2016E 2017E Annual Revenue, Actual and Guidance $37 $70 $110 - 115 $145 - 155 $0 $20 $40 $60 $80 $100 $120 $140 $160 $180 2014A 2015A 2016E 2017E Annual Adjusted EBITDA, Actual and Guidance ($ in millions) ($ in millions) 2017 Preliminary non - GAAP Guidance Total Revenue: $220M – $230M Adjusted Net Income: $80M to $90M Adjusted Diluted EPS: $1.35 to $1.50 Adjusted EBITDA: $145M to $155M

Appendix

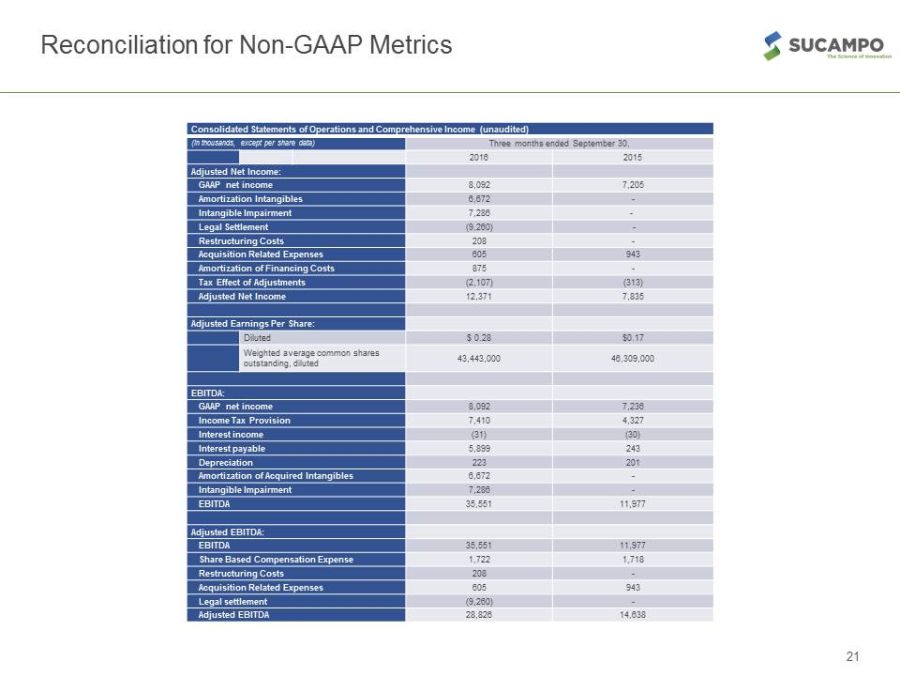

Consolidated Statements of Operations and Comprehensive Income (unaudited) (in thousands, except per share data) Three months ended September 30, 2016 2015 Adjusted Net Income: GAAP net income 8,092 7,205 Amortization Intangibles 6,672 - Intangible Impairment 7,286 - Legal Settlement (9,260) - Restructuring Costs 208 - Acquisition Related Expenses 605 943 Amortization of Financing Costs 875 - Tax Effect of Adjustments (2,107) (313) Adjusted Net Income 12,371 7,835 Adjusted Earnings Per Share: Diluted $ 0.28 $0.17 Weighted average common shares outstanding, diluted 43,443,000 46,309,000 EBITDA: GAAP net income 8,092 7,236 Income Tax Provision 7,410 4,327 Interest income (31) (30) Interest payable 5,899 243 Depreciation 223 201 Amortization of Acquired Intangibles 6,672 - Intangible Impairment 7,286 - EBITDA 35,551 11,977 Adjusted EBITDA: EBITDA 35,551 11,977 Share Based Compensation Expense 1,722 1,718 Restructuring Costs 208 - Acquisition Related Expenses 605 943 Legal settlement (9,260) - Adjusted EBITDA 28,826 14,638 Reconciliation for Non - GAAP Metrics 21

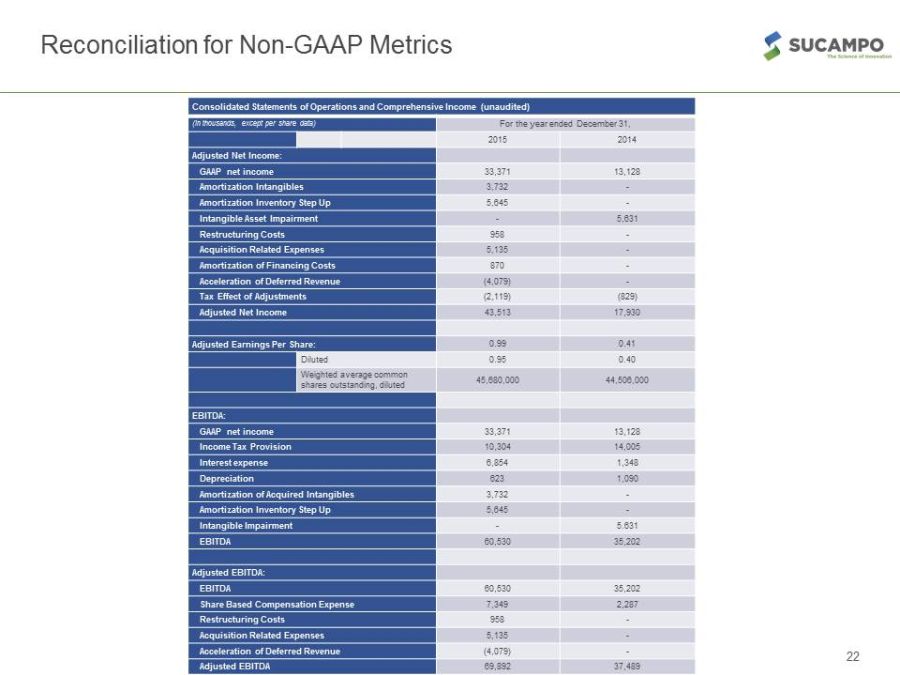

Reconciliation for Non - GAAP Metrics 22 Consolidated Statements of Operations and Comprehensive Income (unaudited) (in thousands, except per share data) For the year ended December 31 , 2015 2014 Adjusted Net Income: GAAP net income 33,371 13,128 Amortization Intangibles 3,732 - Amortization Inventory Step Up 5,645 - Intangible Asset Impairment - 5,631 Restructuring Costs 958 - Acquisition Related Expenses 5,135 - Amortization of Financing Costs 870 - Acceleration of Deferred Revenue (4,079) - Tax Effect of Adjustments (2,119) (829) Adjusted Net Income 43,513 17,930 Adjusted Net Income Per Share: 0.99 0.41 Diluted 0.95 0.40 Weighted average common shares outstanding, diluted 45,680,000 44,506,000 EBITDA: GAAP net income 33,371 13,128 Income Tax Provision 10,304 14,005 Interest expense 6,854 1,348 Depreciation 623 1,090 Amortization of Acquired Intangibles 3,732 - Amortization Inventory Step Up 5,645 - Intangible Impairment - 5.631 EBITDA 60,530 35,202 Adjusted EBITDA : EBITDA 60,530 35,202 Share Based Compensation Expense 7,349 2,287 Restructuring Costs 958 - Acquisition Related Expenses 5,135 - Acceleration of Deferred Revenue (4,079) - Adjusted EBITDA 69,892 37,489