Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - DYNEX CAPITAL INC | a3q16form10-qexx311ceocert.htm |

| EX-32.1 - EXHIBIT 32.1 - DYNEX CAPITAL INC | a3q16form10-qexx321soxcert.htm |

| EX-31.2 - EXHIBIT 31.2 - DYNEX CAPITAL INC | a3q16form10-qexx312cfocert.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

x | Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the quarterly period ended September 30, 2016

or

o | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

Commission File Number: 1-9819

DYNEX CAPITAL, INC.

(Exact name of registrant as specified in its charter)

Virginia | 52-1549373 |

(State or other jurisdiction of | (I.R.S. Employer |

incorporation or organization) | Identification No.) |

4991 Lake Brook Drive, Suite 100, Glen Allen, Virginia | 23060-9245 |

(Address of principal executive offices) | (Zip Code) |

(804) 217-5800 (Registrant’s telephone number, including area code) | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | o | Accelerated filer | x |

Non-accelerated filer | o (Do not check if a smaller reporting company) | Smaller reporting company | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

On October 31, 2016, the registrant had 49,150,424 shares outstanding of common stock, $0.01 par value, which is the registrant’s only class of common stock.

DYNEX CAPITAL, INC.

FORM 10-Q

INDEX

Page | |||

Consolidated Balance Sheets as of September 30, 2016 (unaudited) and December 31, 2015 | |||

Consolidated Statements of Comprehensive Income (Loss) for the three and nine months ended September 30, 2016 (unaudited) and September 30, 2015 (unaudited) | |||

Consolidated Statement of Shareholders' Equity for the nine months ended September 30, 2016 (unaudited) | |||

Consolidated Statements of Cash Flows for the nine months ended September 30, 2016 (unaudited) and September 30, 2015 (unaudited) | |||

i

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

CONSOLIDATED BALANCE SHEETS

($ in thousands except share data)

September 30, 2016 | December 31, 2015 | ||||||

ASSETS | (unaudited) | ||||||

Mortgage-backed securities (including pledged of $2,974,524 and $3,361,635, respectively) | $ | 3,110,467 | $ | 3,493,701 | |||

Mortgage loans held for investment, net | 20,366 | 24,145 | |||||

Investment in limited partnership | — | 10,835 | |||||

Investment in FHLB stock | 5,260 | 11,475 | |||||

Cash and cash equivalents | 73,406 | 33,935 | |||||

Restricted cash | 84,685 | 51,190 | |||||

Derivative assets | 12,985 | 7,835 | |||||

Principal receivable on investments | 9,594 | 6,193 | |||||

Accrued interest receivable | 19,501 | 22,764 | |||||

Other assets, net | 7,292 | 7,975 | |||||

Total assets | $ | 3,343,556 | $ | 3,670,048 | |||

LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||

Liabilities: | |||||||

Repurchase agreements | $ | 2,478,278 | $ | 2,589,420 | |||

FHLB advances | 263,000 | 520,000 | |||||

Non-recourse collateralized financing | 7,025 | 8,442 | |||||

Derivative liabilities | 84,023 | 41,205 | |||||

Accrued interest payable | 2,163 | 1,743 | |||||

Accrued dividends payable | 12,259 | 13,709 | |||||

Other liabilities | 1,889 | 3,504 | |||||

Total liabilities | 2,848,637 | 3,178,023 | |||||

Shareholders’ equity: | |||||||

Preferred stock, par value $.01 per share, 8.5% Series A Cumulative Redeemable; 8,000,000 shares authorized; 2,300,000 shares issued and outstanding ($57,500 aggregate liquidation preference) | $ | 55,407 | $ | 55,407 | |||

Preferred stock, par value $.01 per share, 7.625% Series B Cumulative Redeemable; 7,000,000 shares authorized; 2,250,000 shares issued and outstanding ($56,250 aggregate liquidation preference) | 54,251 | 54,251 | |||||

Common stock, par value $.01 per share, 200,000,000 shares authorized; 49,148,595 and 49,047,335 shares issued and outstanding, respectively | 491 | 490 | |||||

Additional paid-in capital | 726,701 | 725,358 | |||||

Accumulated other comprehensive income (loss) | 52,578 | (12,768 | ) | ||||

Accumulated deficit | (394,509 | ) | (330,713 | ) | |||

Total shareholders' equity | 494,919 | 492,025 | |||||

Total liabilities and shareholders’ equity | $ | 3,343,556 | $ | 3,670,048 | |||

See notes to the unaudited consolidated financial statements.

1

DYNEX CAPITAL, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(UNAUDITED)

(amounts in thousands except per share data)

Three Months Ended | Nine Months Ended | ||||||||||||||

September 30, | September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Interest income | $ | 21,135 | $ | 26,096 | $ | 69,040 | $ | 74,722 | |||||||

Interest expense | 6,068 | 5,859 | 18,478 | 16,772 | |||||||||||

Net interest income | 15,067 | 20,237 | 50,562 | 57,950 | |||||||||||

Gain (loss) on derivative instruments, net | 2,409 | (52,749 | ) | (62,153 | ) | (60,982 | ) | ||||||||

Gain (loss) on sale of investments, net | — | 113 | (4,238 | ) | (70 | ) | |||||||||

Fair value adjustments, net | 34 | 16 | 86 | 75 | |||||||||||

Other income (expense), net | 545 | (215 | ) | 898 | 430 | ||||||||||

General and administrative expenses: | |||||||||||||||

Compensation and benefits | (1,736 | ) | (2,327 | ) | (5,829 | ) | (6,794 | ) | |||||||

Other general and administrative | (1,619 | ) | (2,052 | ) | (5,288 | ) | (6,596 | ) | |||||||

Net income (loss) | 14,700 | (36,977 | ) | (25,962 | ) | (15,987 | ) | ||||||||

Preferred stock dividends | (2,294 | ) | (2,294 | ) | (6,882 | ) | (6,882 | ) | |||||||

Net income (loss) to common shareholders | $ | 12,406 | $ | (39,271 | ) | $ | (32,844 | ) | $ | (22,869 | ) | ||||

Other comprehensive income: | |||||||||||||||

Change in net unrealized gain on available-for-sale investments | $ | 769 | $ | 26,674 | $ | 61,260 | $ | 7,951 | |||||||

Reclassification adjustment for (gain) loss on sale of investments, net | — | (113 | ) | 4,238 | 70 | ||||||||||

Reclassification adjustment for de-designated cash flow hedges | (99 | ) | 857 | (152 | ) | 2,772 | |||||||||

Total other comprehensive income | 670 | 27,418 | 65,346 | 10,793 | |||||||||||

Comprehensive income (loss) to common shareholders | $ | 13,076 | $ | (11,853 | ) | $ | 32,502 | $ | (12,076 | ) | |||||

Net income (loss) per common share-basic and diluted | $ | 0.25 | $ | (0.74 | ) | $ | (0.67 | ) | $ | (0.42 | ) | ||||

Weighted average common shares-basic and diluted | 49,147 | 52,777 | 49,102 | 54,043 | |||||||||||

See notes to the unaudited consolidated financial statements.

2

DYNEX CAPITAL, INC.

CONSOLIDATED STATEMENT OF SHAREHOLDERS’ EQUITY

(UNAUDITED)

($ in thousands)

Preferred Stock | Common Stock | Additional Paid-in Capital | Accumulated Other Comprehensive (Loss) Income | Accumulated Deficit | Total Shareholders' Equity | ||||||||||||||||||

Balance as of December 31, 2015 | $ | 109,658 | $ | 490 | $ | 725,358 | $ | (12,768 | ) | $ | (330,713 | ) | $ | 492,025 | |||||||||

Stock issuance | — | — | 102 | — | — | 102 | |||||||||||||||||

Restricted stock granted, net of amortization | — | 2 | 2,064 | — | — | 2,066 | |||||||||||||||||

Adjustments for tax withholding on share-based compensation | — | (1 | ) | (484 | ) | — | — | (485 | ) | ||||||||||||||

Stock issuance costs amortization | — | — | (29 | ) | — | — | (29 | ) | |||||||||||||||

Common stock repurchased | — | — | (310 | ) | — | — | (310 | ) | |||||||||||||||

Net loss | — | — | — | — | (25,962 | ) | (25,962 | ) | |||||||||||||||

Dividends on preferred stock | — | — | — | — | (6,882 | ) | (6,882 | ) | |||||||||||||||

Dividends on common stock | — | — | — | — | (30,952 | ) | (30,952 | ) | |||||||||||||||

Other comprehensive income | — | — | — | 65,346 | — | 65,346 | |||||||||||||||||

Balance as of September 30, 2016 | $ | 109,658 | $ | 491 | $ | 726,701 | $ | 52,578 | $ | (394,509 | ) | $ | 494,919 | ||||||||||

See notes to the unaudited consolidated financial statements.

3

DYNEX CAPITAL, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

($ in thousands)

Nine Months Ended | |||||||

September 30, | |||||||

2016 | 2015 | ||||||

Operating activities: | |||||||

Net loss | $ | (25,962 | ) | $ | (15,987 | ) | |

Adjustments to reconcile net loss to cash provided by operating activities: | |||||||

Decrease in accrued interest receivable | 3,263 | 241 | |||||

Increase (decrease) in accrued interest payable | 420 | (409 | ) | ||||

Loss on derivative instruments, net | 62,153 | 60,982 | |||||

Loss on sale of investments, net | 4,238 | 70 | |||||

Fair value adjustments, net | (86 | ) | (75 | ) | |||

Amortization of investment premiums, net | 112,418 | 114,398 | |||||

Other amortization and depreciation, net | 1,186 | 4,143 | |||||

Stock-based compensation expense | 2,066 | 2,220 | |||||

Other operating activities | (2,060 | ) | (3,064 | ) | |||

Net cash and cash equivalents provided by operating activities | 157,636 | 162,519 | |||||

Investing activities: | |||||||

Purchase of investments | (96,816 | ) | (1,066,461 | ) | |||

Principal payments received on investments | 337,719 | 384,063 | |||||

Proceeds from sales of investments | 94,033 | 339,332 | |||||

Principal payments received on mortgage loans held for investment, net | 3,709 | 12,241 | |||||

Payment to acquire interest in limited partnership | — | (6,000 | ) | ||||

Distributions received from limited partnership | 10,835 | — | |||||

Net payments on derivatives, including terminations | (24,483 | ) | (37,502 | ) | |||

Other investing activities | (105 | ) | (134 | ) | |||

Net cash and cash equivalents provided by (used in) investing activities | 324,892 | (374,461 | ) | ||||

Financing activities: | |||||||

Borrowings under repurchase agreements and FHLB advances | 19,293,243 | 17,329,870 | |||||

Repayments of repurchase agreement borrowings and FHLB advances | (19,661,384 | ) | (17,032,911 | ) | |||

Principal payments on non-recourse collateralized financing | (1,443 | ) | (2,249 | ) | |||

Increase in restricted cash | (33,495 | ) | (35,916 | ) | |||

Proceeds from issuance of common stock | 102 | 129 | |||||

Cash paid for repurchases of common stock | (310 | ) | (31,051 | ) | |||

Payments related to tax withholding for stock-based compensation | (485 | ) | (556 | ) | |||

Dividends paid | (39,285 | ) | (46,682 | ) | |||

Net cash and cash equivalents (used in) provided by financing activities | (443,057 | ) | 180,634 | ||||

Net increase (decrease) in cash and cash equivalents | 39,471 | (31,308 | ) | ||||

Cash and cash equivalents at beginning of period | 33,935 | 43,944 | |||||

Cash and cash equivalents at end of period | $ | 73,406 | $ | 12,636 | |||

Supplemental Disclosure of Cash Activity: | |||||||

Cash paid for interest | $ | 18,185 | $ | 14,366 | |||

See notes to the unaudited consolidated financial statements.

4

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

NOTE 1 –ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization

Dynex Capital, Inc., ("Company”) was incorporated in the Commonwealth of Virginia on December 18, 1987 and commenced operations in February 1988. The Company primarily earns income from investing on a leveraged basis in mortgage-backed securities ("MBS") that are issued or guaranteed by the U.S. Government or U.S. Government sponsored agencies ("Agency MBS") and MBS issued by others ("non-Agency MBS").

Basis of Presentation

The accompanying unaudited consolidated financial statements of Dynex Capital, Inc. and its subsidiaries (together, “Dynex” or, as appropriate, the “Company”) have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information and with the instructions to the Quarterly Report on Form 10-Q and Article 10, Rule 10-01 of Regulation S-X promulgated by the Securities and Exchange Commission (the “SEC”). Accordingly, they do not include all of the information and notes required by GAAP for complete financial statements. In the opinion of management, all significant adjustments, consisting of normal recurring accruals, considered necessary for a fair presentation of the consolidated financial statements have been included. Operating results for the three and nine months ended September 30, 2016 are not necessarily indicative of the results that may be expected for any other interim periods or for the entire year ending December 31, 2016. The unaudited consolidated financial statements included herein should be read in conjunction with the audited financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2015 filed with the SEC.

Reclassifications

Certain items in the prior periods' consolidated financial statements have been reclassified to conform to the current period's presentation. The Company's equity in income of limited partnership for the three and nine months ended September 30, 2015 is now included within "other income (expense), net" on the Company's consolidated statements of comprehensive income. This presentation change has no effect on reported total assets, total liabilities, results of operations, or cash flow activities.

Consolidation

The consolidated financial statements include the accounts of the Company and the accounts of its majority owned subsidiaries and variable interest entities ("VIE") for which it is the primary beneficiary. As a primary beneficiary, the Company has both the power to direct the activities that most significantly impact the economic performance of the VIE and a right to receive benefits or absorb losses of the entity that could be potentially significant to the VIE. The Company is required to reconsider its evaluation of whether to consolidate a VIE each reporting period, based upon changes in the facts and circumstances pertaining to the VIE. The Company consolidates certain trusts through which it has securitized mortgage loans as a result of not meeting the sale criteria under GAAP at the time the financial assets were transferred to the trust. All intercompany accounts and transactions have been eliminated in consolidation.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements as well as the reported amounts of revenue and expenses during the reported period. Actual results could differ from those estimates. The most significant estimates used by management include, but are not limited to, fair value measurements of its investments, other-than-temporary impairments, contingencies, and amortization of premiums and discounts. These items are discussed further below within this note to the consolidated financial statements.

5

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

Income Taxes

The Company has elected to be taxed as a real estate investment trust ("REIT") under the Internal Revenue Code of 1986 and the corresponding provisions of state law. To qualify as a REIT, the Company must meet certain tests including investing in primarily real estate-related assets and the required distribution of at least 90% of its annual REIT taxable income to stockholders after consideration of its net operating loss ("NOL") carryforward and not including taxable income retained in its taxable subsidiaries. As a REIT, the Company generally will not be subject to federal income tax on the amount of its income or capital gains that is distributed as dividends to shareholders.

The Company assesses its tax positions for all open tax years and determines whether the Company has any material unrecognized liabilities in accordance with Accounting Standards Codification ("ASC") Topic 740. The Company records these liabilities, if any, to the extent they are deemed more likely than not to have been incurred.

Net Income (Loss) Per Common Share

The Company calculates basic net income (loss) per common share by dividing net income (loss) to common shareholders for the period by weighted-average shares of common stock outstanding for that period. The Company did not have any potentially dilutive securities outstanding during the three or nine months ended September 30, 2016 or September 30, 2015.

Holders of unvested shares of the Company's issued and outstanding restricted common stock are eligible to receive non-forfeitable dividends. As such, these unvested shares are considered participating securities as per ASC Topic 260-10 and therefore are included in the computation of basic net income (loss) per common share using the two-class method. Upon vesting, restrictions on transfer expire on each share of restricted stock, and each such share of restricted stock is converted to one equal share of common stock.

Because the Company's 8.50% Series A Cumulative Redeemable Preferred Stock (the “Series A Preferred Stock”) and 7.625% Series B Cumulative Redeemable Preferred Stock (the “Series B Preferred Stock”) are redeemable at the Company's option for cash only and may convert into shares of common stock only upon a change of control of the Company, the effect of those shares and their related dividends is excluded from the calculation of diluted net income (loss) per common share.

Cash and Cash Equivalents

Cash and cash equivalents include cash on hand and highly liquid investments with original maturities of three months or less.

Restricted Cash

Restricted cash consists of cash the Company has pledged to cover initial and variation margin with its financing and derivative counterparties.

Mortgage-Backed Securities

The Company invests in Agency and non-Agency RMBS, CMBS and CMBS IO securities, all of which are designated as available-for-sale ("AFS"). All of the Company’s MBS are recorded at fair value on the consolidated balance sheet. Changes in unrealized gain (loss) on the Company's MBS are reported in other comprehensive income ("OCI") until each security is collected, disposed of, or determined to be other than temporarily impaired. Although the Company generally intends to hold its AFS securities until maturity, it may sell any of these securities as part of the overall management of its business. Upon the sale of an AFS security, any unrealized gain or loss is reclassified out of accumulated other comprehensive income ("AOCI") into net income as a realized "gain (loss) on sale of investments, net" using the specific identification method.

The Company’s MBS pledged as collateral against repurchase agreements and derivative instruments are included in MBS on the consolidated balance sheets with the fair value of the MBS pledged disclosed parenthetically.

6

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

Interest Income, Premium Amortization, and Discount Accretion. Interest income on MBS is accrued based on the outstanding principal balance (or notional balance in the case of interest-only, or "IO", securities) and their contractual terms. Premiums and discounts on Agency MBS as well as any non-Agency MBS rated 'AA' and higher at the time of purchase are amortized into interest income over the expected life of such securities using the effective yield method and adjustments to premium amortization are made for actual cash payments as well as changes in projected future cash payments. The Company's projections of future cash payments are based on input and analysis received from external sources and internal models, and include assumptions about the amount and timing of credit losses, loan prepayment rates, fluctuations in interest rates, and other factors. On at least a quarterly basis, the Company reviews and makes any necessary adjustments to its cash flow projections and updates the yield recognized on these assets.

The Company holds certain non-Agency MBS that had credit ratings of less than 'AA' at the time of purchase or were not rated by any of the nationally recognized credit rating agencies. A portion of these non-Agency MBS were purchased at discounts to their par value, which management does not believe to be substantial. The discount is accreted into income over the security's expected life, which reflects management's estimate of the security's projected cash flows. Future changes in the timing of projected cash flows or differences arising between projected cash flows and actual cash flows received may result in a prospective change in the effective yield on those securities.

Determination of MBS Fair Value. The Company estimates the fair value of the majority of its MBS based upon prices obtained from third-party pricing services and broker quotes. The remainder of the Company's MBS are valued by discounting the estimated future cash flows derived from cash flow models that utilize information such as the security's coupon rate, estimated prepayment speeds, expected weighted average life, collateral composition, estimated future interest rates, expected losses, and credit enhancements as well as certain other relevant information. Refer to Note 6 for further discussion of MBS fair value measurements.

Other-than-Temporary Impairment. MBS is considered impaired when its fair value is less than its amortized cost. The Company evaluates all of its impaired MBS for other-than-temporary impairments ("OTTI") on at least a quarterly basis. An impairment is considered other-than-temporary if: (1) the Company intends to sell the MBS; (2) it is more likely than not that the Company will be required to sell the MBS before its fair value recovers; or (3) the Company does not expect to recover the full amortized cost basis of the MBS. If either of the first two conditions is met, the entire amount of the impairment is recognized in earnings. If the impairment is solely due to the inability to fully recover the amortized cost basis, the security is further analyzed to quantify any credit loss, which is the difference between the present value of cash flows expected to be collected on the MBS and its amortized cost. The credit loss, if any, is then recognized in earnings, while the balance of impairment related to other factors is recognized in other comprehensive income.

Following the recognition of an OTTI through earnings, a new cost basis is established for the security. Any subsequent recoveries in fair value may be accreted back into the amortized cost basis of the MBS on a prospective basis through interest income. Please see Note 2 for additional information related to the Company's evaluation for OTTI.

Secured Borrowings

The Company's repurchase agreements and Federal Home Loan Bank (or "FHLB") advances, which are used to finance its purchases of MBS, are accounted for as secured borrowings under which the Company pledges its securities as collateral to secure a loan, which is equal in value to a specified percentage of the estimated fair value of the pledged collateral. The Company retains beneficial ownership of the pledged collateral. At the maturity of a repurchase agreement, the Company is required to repay the loan and concurrently receives back its pledged collateral from the lender or, with the consent of the lender, the Company may renew the agreement at the then prevailing financing rate. A repurchase agreement lender may require the Company to pledge additional collateral in the event of a decline in the fair value of the collateral pledged. Repurchase agreement financing is recourse to the Company and the assets pledged. Most of the Company’s repurchase agreements are based on the September 1996 version of the Bond Market Association Master Repurchase Agreement, which generally provides that the lender, as buyer, is responsible for obtaining collateral valuations from a generally recognized source agreed to by both the Company and the lender, or, in an instance when such source is not available, the value determination is made by the lender.

As a result of a final rule issued by the Federal Housing Finance Administration ("FHFA") in January 2016 regarding the exclusion of captive insurance entities from membership in the FHLB, the Company's wholly owned subsidiary, Mackinaw

7

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

Insurance Company, LLC ("Mackinaw"), must terminate its membership in the FHLB of Indianapolis by February 19, 2017 and will no longer be permitted new advances or renewals of existing advances. FHLB advances outstanding on the Company's consolidated balance sheet as of September 30, 2016 will be repaid before December 31, 2016.

Derivative Instruments

The Company's derivative instruments, which currently include interest rate swaps and Eurodollar futures, are accounted for at fair value. Derivative instruments in a gain position are reported as derivative assets and derivative instruments in a loss position are reported as derivative liabilities on the Company's consolidated balance sheet. All periodic interest costs and changes in fair value of derivative instruments, including gains and losses realized upon termination, are recorded in "gain (loss) on derivative instruments, net" on the Company's consolidated statement of comprehensive income. Cash receipts and payments related to derivative instruments are classified in the investing activities section of our consolidated statements of cash flows in accordance with the underlying nature or purpose of the derivative transactions. Please refer to Note 4 for additional information regarding the Company's accounting for its derivative instruments.

Although MBS have characteristics that meet the definition of a derivative instrument, ASC Topic 815 specifically excludes these instruments from its scope because they are accounted for as debt securities under ASC Topic 320.

Share-Based Compensation

Pursuant to the Company’s 2009 Stock and Incentive Plan, the Company may grant share-based compensation to eligible employees, directors or consultants or advisers to the Company, including stock awards, stock options, stock appreciation rights, dividend equivalent rights, performance shares, and restricted stock units. The Company's restricted stock currently issued and outstanding under this plan may be settled only in shares of its common stock, and therefore are treated as equity awards with their fair value measured at the grant date and recognized as compensation cost over the requisite service period with a corresponding credit to shareholders' equity. The requisite service period is the period during which an employee is required to provide service in exchange for an award, which is equivalent to the vesting period specified in the terms of the time-based restricted stock award. None of the Company's restricted stock awards have performance based conditions. The Company does not currently have any share-based compensation issued or outstanding other than restricted stock.

Contingencies

In the normal course of business, there may be various lawsuits, claims, and other contingencies pending against the Company. On a quarterly basis, the Company evaluates whether to establish provisions for estimated losses from those matters. The Company recognizes a liability for a contingent loss when: (a) the underlying causal event has occurred prior to the balance sheet date; (b) it is probable that a loss has been incurred; and (c) there is a reasonable basis for estimating that loss. A liability is not recognized for a contingent loss when it is only possible or remotely possible that a loss has been incurred, however, possible contingent losses shall be disclosed. If the contingent loss (or an additional loss in excess of any accrual) is at least a reasonable possibility and material, then the Company discloses a reasonable estimate of the possible loss or range of loss, if such reasonable estimate can be made. If the Company cannot make a reasonable estimate of the possible material loss, or range of loss, then that fact is disclosed.

Recent Accounting Pronouncements

The Financial Accounting Standards Board ("FASB") issued Accounting Standards Update ("ASU") No. 2016-02, Leases, which includes the following amendments:

• | for operating and finance leases, a lessee is required to recognize a right-of-use asset and a lease liability, initially measured at the present value of the lease payments in its consolidated balance sheet; |

• | for finance leases, a lessee is required to recognize interest on the lease liability separately from amortization of the right-of-use asset in the statement of comprehensive income; |

• | for finance leases, a lessee is required to classify repayments of the principal portion of the lease liability within financing activities and payments of interest on the lease liability and variable lease payments within operating activities in the statement of cash flows; |

8

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

• | for operating leases, a lessee is required to recognize a single lease cost, calculated so that the cost of the lease is allocated over the lease term on a generally straight-line basis in the statement of comprehensive income; and |

• | for operating leases, a lessee is required to classify all cash payments within operating activities in the statement of cash flows. |

Under the new guidance, lessor accounting is largely unchanged. ASU No. 2016-02 is effective for public companies for fiscal years beginning after December 15, 2018, and early adoption is permitted. The Company does not expect this ASU to have a material impact on the Company's consolidated financial statements.

The FASB issued ASU No. 2016-09, Compensation - Stock Compensation, which simplifies several aspects of the accounting for share-based payment award transactions, including income tax consequences, classification of awards as either equity or liabilities, and classification on the statement cash flows. The amendments are effective for public companies for fiscal years beginning after December 15, 2016, and early adoption is permitted. The Company does not expect this ASU to have a material impact on the Company's consolidated financial statements.

The FASB issued ASU No. 2016-13, Financial Instruments - Credit Losses, which replaces the incurred loss impairment methodology in current GAAP with a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. For assets measured at amortized cost, the amendments in this ASU eliminate the probable initial recognition threshold in current GAAP and broaden the information that an entity must consider in developing its expected credit loss estimate to include the use of forecasted information. For assets classified as available-for-sale with changes in fair value recorded in other comprehensive income, measurement of credit losses will be similar to current GAAP. However, the amendments in this ASU require that credit losses be presented as an allowance rather than as a write-down, which is referred to in current GAAP as an other-than-temporary impairment. An entity will be able to record reversals of credit losses, if credit loss estimates decline, in net income for the current period. The amendments in this ASU will not permit an entity to use the length of time a debt security has been in an unrealized loss position to avoid recording a credit loss and removes the requirements to consider historical and implied volatility of the fair value of a security as well as recoveries or declines in fair value after the balance sheet date. The amendments in this ASU will affect an entity by varying degrees depending on the credit quality of the assets held by the entity, their duration, and how the entity applies current GAAP. These amendments will become effective for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years, and early adoption will be permitted as of the fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. An entity will apply the amendments in this ASU through a cumulative-effect adjustment to retained earnings as of the beginning of the first reporting period in which the guidance is effective. The Company does not currently anticipate this ASU having an impact on its consolidated financial statements.

The FASB issued ASU No. 2016-15, Statement of Cash Flows (Topic 320) - Classification of Certain Cash Receipts and Cash Payments, in order to provide guidance for eight cash flow classification issues which are either unclear or do not have specific guidance under current GAAP. The issues identified are as follows:

• | debt prepayment or debt extinguishment costs; |

• | settlement of zero-coupon debt instruments or other debt instruments with coupon interest rates insignificant in relation to the effective interest rate of the borrowing; |

• | contingent consideration payments made after a business combination; |

• | proceeds from the settlement of insurance claims; |

• | proceeds from settlement of corporate-owned life insurance policies; |

• | distributions received from equity method investees; |

• | beneficial interests in securitization transactions; and |

• | separately identifiable cash flows and application of the predominance principle. |

The amendments in this ASU will become effective for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years, and early adoption is permitted. The amendments in this ASU should be applied using a retrospective transition method to each period presented. The Company does not expect this ASU to have a material impact on the Company's consolidated financial statements.

9

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

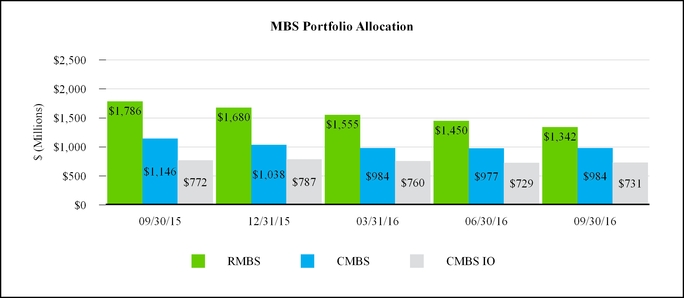

NOTE 2 – MORTGAGE-BACKED SECURITIES

The majority of the Company's MBS are pledged as collateral to cover initial and variation margins for the Company's secured borrowings and derivative instruments. The following tables present the Company’s MBS by investment type as of the dates indicated:

September 30, 2016 | ||||||||||||||||||||||||||

Par | Net Premium (Discount) | Amortized Cost | Gross Unrealized Gain | Gross Unrealized Loss | Fair Value | WAC (1) | ||||||||||||||||||||

RMBS: | ||||||||||||||||||||||||||

Agency | $ | 1,239,856 | $ | 61,141 | $ | 1,300,997 | $ | 5,270 | $ | (8,549 | ) | $ | 1,297,718 | 3.04 | % | |||||||||||

Non-Agency | 41,514 | (19 | ) | 41,495 | 109 | (54 | ) | 41,550 | 3.58 | % | ||||||||||||||||

1,281,370 | 61,122 | 1,342,492 | 5,379 | (8,603 | ) | 1,339,268 | ||||||||||||||||||||

CMBS: | ||||||||||||||||||||||||||

Agency | 898,317 | 11,048 | 909,365 | 35,901 | (62 | ) | 945,204 | 3.32 | % | |||||||||||||||||

Non-Agency | 82,190 | (7,552 | ) | 74,638 | 8,135 | (1 | ) | 82,772 | 4.89 | % | ||||||||||||||||

980,507 | 3,496 | 984,003 | 44,036 | (63 | ) | 1,027,976 | ||||||||||||||||||||

CMBS IO (2): | ||||||||||||||||||||||||||

Agency | — | 385,968 | 385,968 | 8,597 | (139 | ) | 394,426 | 0.68 | % | |||||||||||||||||

Non-Agency | — | 344,792 | 344,792 | 4,921 | (916 | ) | 348,797 | 0.61 | % | |||||||||||||||||

— | 730,760 | 730,760 | 13,518 | (1,055 | ) | 743,223 | ||||||||||||||||||||

Total AFS securities: | $ | 2,261,877 | $ | 795,378 | $ | 3,057,255 | $ | 62,933 | $ | (9,721 | ) | $ | 3,110,467 | |||||||||||||

(1) | The current weighted average coupon ("WAC") is the gross interest rate of the pool of mortgages underlying the security weighted by the outstanding principal balance (or by notional balance in the case of an IO security). |

(2) | The notional balance for Agency CMBS IO and non-Agency CMBS IO was $12,226,782 and $10,687,732, respectively, as of September 30, 2016. |

December 31, 2015 | ||||||||||||||||||||||||||

Par | Net Premium (Discount) | Amortized Cost | Gross Unrealized Gain | Gross Unrealized Loss | Fair Value | WAC (1) | ||||||||||||||||||||

RMBS: | ||||||||||||||||||||||||||

Agency | $ | 1,536,733 | $ | 77,617 | $ | 1,614,350 | $ | 4,362 | $ | (20,190 | ) | $ | 1,598,522 | 3.03 | % | |||||||||||

Non-Agency | 66,003 | (45 | ) | 65,958 | 70 | (818 | ) | 65,210 | 3.25 | % | ||||||||||||||||

1,602,736 | 77,572 | 1,680,308 | 4,432 | (21,008 | ) | 1,663,732 | ||||||||||||||||||||

CMBS: | ||||||||||||||||||||||||||

Agency | 876,751 | 13,252 | 890,003 | 10,542 | (14,614 | ) | 885,931 | 3.45 | % | |||||||||||||||||

Non-Agency | 156,218 | (8,133 | ) | 148,085 | 7,039 | (941 | ) | 154,183 | 4.29 | % | ||||||||||||||||

1,032,969 | 5,119 | 1,038,088 | 17,581 | (15,555 | ) | 1,040,114 | ||||||||||||||||||||

CMBS IO (2): | ||||||||||||||||||||||||||

Agency | — | 421,857 | 421,857 | 5,922 | (1,651 | ) | 426,128 | 0.80 | % | |||||||||||||||||

Non-Agency | — | 365,554 | 365,554 | 1,992 | (3,819 | ) | 363,727 | 0.71 | % | |||||||||||||||||

— | 787,411 | 787,411 | 7,914 | (5,470 | ) | 789,855 | ||||||||||||||||||||

Total AFS securities: | $ | 2,635,705 | $ | 870,102 | $ | 3,505,807 | $ | 29,927 | $ | (42,033 | ) | $ | 3,493,701 | |||||||||||||

(1) | The current weighted average coupon ("WAC") is the gross interest rate of the pool of mortgages underlying the security weighted by the outstanding principal balance (or by notional balance in the case of an IO security). |

10

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

(2) | The notional balance for the Agency CMBS IO and non-Agency CMBS IO was $12,180,291 and $10,328,628, respectively, as of December 31, 2015. |

Actual maturities of MBS are affected by the contractual lives of the underlying mortgage collateral, periodic payments of principal, prepayments of principal, and the payment priority structure of the security; therefore, actual maturities are generally shorter than the securities' stated contractual maturities.

The following table presents information regarding the sales included in "gain (loss) on sale of investments, net" on the Company's consolidated statements of comprehensive income for the periods indicated:

Three Months Ended | |||||||||||||||

September 30, | |||||||||||||||

2016 | 2015 | ||||||||||||||

Proceeds Received | Realized Gain (Loss) | Proceeds Received | Realized Gain (Loss) | ||||||||||||

Agency RMBS (1) | $ | — | $ | — | $ | (2,694 | ) | $ | (59 | ) | |||||

Agency CMBS IO | — | — | 12,620 | 172 | |||||||||||

Non-Agency CMBS IO | — | — | — | — | |||||||||||

$ | — | $ | — | $ | 9,926 | $ | 113 | ||||||||

(1) | There were no sales of Agency RMBS during the three months ended September 30, 2015. The amounts shown reflect an adjustment to proceeds received and the realized loss recognized during the three months ended September 30, 2015 related to pre-settlement factor changes. |

Nine Months Ended | |||||||||||||||

September 30, | |||||||||||||||

2016 | 2015 | ||||||||||||||

Proceeds Received | Realized Gain (Loss) | Proceeds Received | Realized Gain (Loss) | ||||||||||||

Agency RMBS | $ | 54,178 | $ | (3,010 | ) | $ | 153,676 | $ | (2,256 | ) | |||||

Agency CMBS | — | — | 98,887 | (822 | ) | ||||||||||

Non-Agency CMBS | 33,640 | (1,228 | ) | — | — | ||||||||||

Agency CMBS IO | — | — | 42,005 | 1,646 | |||||||||||

Non-Agency CMBS IO | — | — | 44,764 | 1,362 | |||||||||||

$ | 87,818 | $ | (4,238 | ) | $ | 339,332 | $ | (70 | ) | ||||||

The following table presents certain information for those MBS in an unrealized loss position as of the dates indicated:

September 30, 2016 | December 31, 2015 | ||||||||||||||||||

Fair Value | Gross Unrealized Losses | # of Securities | Fair Value | Gross Unrealized Losses | # of Securities | ||||||||||||||

Continuous unrealized loss position for less than 12 months: | |||||||||||||||||||

Agency MBS | $ | 352,253 | $ | (1,484 | ) | 40 | $ | 1,332,849 | $ | (19,062 | ) | 109 | |||||||

Non-Agency MBS | 24,448 | (99 | ) | 5 | 351,650 | (5,347 | ) | 72 | |||||||||||

Continuous unrealized loss position for 12 months or longer: | |||||||||||||||||||

Agency MBS | $ | 379,488 | $ | (7,266 | ) | 61 | $ | 775,484 | $ | (17,393 | ) | 72 | |||||||

Non-Agency MBS | 84,959 | (872 | ) | 28 | 8,306 | (231 | ) | 7 | |||||||||||

11

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

Because the principal related to Agency MBS is guaranteed by the government-sponsored entities Fannie Mae and Freddie Mac which have the implicit guarantee of the U.S. government, the Company does not consider any of the unrealized losses on its Agency MBS to be credit related. Although the unrealized losses are not credit related, the Company assesses its ability and intent to hold any Agency MBS with an unrealized loss until the recovery in its value. This assessment is based on the amount of the unrealized loss and significance of the related investment as well as the Company’s current leverage and anticipated liquidity. Based on this analysis, the Company has determined that the unrealized losses on its Agency MBS as of September 30, 2016 and December 31, 2015 were temporary.

The Company reviews any non-Agency MBS in an unrealized loss position to evaluate whether any decline in fair value represents an OTTI. The evaluation includes a review of the credit ratings of these non-Agency MBS and the seasoning of the mortgage loans collateralizing these securities as well as the estimated future cash flows which include projected losses. The Company performed this evaluation for the non-Agency MBS in an unrealized loss position and has determined that there have not been any adverse changes in the timing or amount of estimated future cash flows that necessitate a recognition of OTTI amounts as of September 30, 2016 or December 31, 2015.

NOTE 3 – SECURED BORROWINGS

The Company’s secured borrowings, which consist of repurchase agreements and FHLB advances, that were outstanding as of September 30, 2016 and December 31, 2015 are summarized in the table below:

September 30, 2016 | |||||||||||

Collateral Type | Balance | Weighted Average Rate | Fair Value of Collateral Pledged | ||||||||

Agency RMBS | $ | 1,156,635 | 0.70 | % | $ | 1,204,542 | |||||

Non-Agency RMBS | 38,613 | 1.88 | % | 41,082 | |||||||

Agency CMBS | 594,661 | 0.69 | % | 643,207 | |||||||

Non-Agency CMBS | 69,687 | 1.50 | % | 82,573 | |||||||

Agency CMBS IO | 322,632 | 1.38 | % | 378,875 | |||||||

Non-Agency CMBS IO | 290,626 | 1.45 | % | 343,900 | |||||||

Securitization financing bond | 5,424 | 1.86 | % | 5,882 | |||||||

Total repurchase agreements | $ | 2,478,278 | 0.91 | % | $ | 2,700,061 | |||||

FHLB advances (1) | 263,000 | 0.51 | % | 274,953 | |||||||

Total secured borrowings | $ | 2,741,278 | 0.88 | % | $ | 2,975,014 | |||||

12

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

December 31, 2015 | |||||||||||

Collateral Type | Balance | Weighted Average Rate | Fair Value of Collateral Pledged | ||||||||

Agency RMBS | $ | 1,439,436 | 0.47 | % | $ | 1,483,152 | |||||

Non-Agency RMBS | 52,128 | 1.77 | % | 64,286 | |||||||

Agency CMBS | 301,427 | 0.49 | % | 345,728 | |||||||

Non-Agency CMBS | 126,378 | 1.26 | % | 143,785 | |||||||

Agency CMBS IOs | 360,245 | 1.24 | % | 421,285 | |||||||

Non-Agency CMBS IOs | 302,771 | 1.33 | % | 359,351 | |||||||

Securitization financing bond | 7,035 | 1.65 | % | 8,054 | |||||||

Total repurchase agreements | $ | 2,589,420 | 0.75 | % | $ | 2,825,641 | |||||

FHLB advances (1) | 520,000 | 0.40 | % | 541,771 | |||||||

Total secured borrowings | $ | 3,109,420 | 0.69 | % | $ | 3,367,412 | |||||

(1) As of September 30, 2016 and December 31, 2015, FHLB advances were collateralized primarily with Agency CMBS.

As of September 30, 2016, the weighted average remaining term to maturity of our repurchase agreements was 18 days compared to 22 days as of December 31, 2015. The remaining balance of FHLB advances is due in October 2016. The following table provides a summary of the original term to maturity of our secured borrowings as of September 30, 2016 and December 31, 2015:

Original Term to Maturity | September 30, 2016 | December 31, 2015 | ||||||

Less than 30 days | $ | 607,051 | $ | 551,643 | ||||

30 to 90 days | 1,143,854 | 782,393 | ||||||

91 to 180 days | 727,373 | 1,512,384 | ||||||

181 to 364 days | 263,000 | — | ||||||

1 year or longer | — | 263,000 | ||||||

$ | 2,741,278 | $ | 3,109,420 | |||||

The following table lists the counterparties with whom the Company had over 10% of its shareholders' equity at risk (defined as the excess of collateral pledged over the borrowings outstanding):

September 30, 2016 | |||||||||||

Counterparty Name | Balance | Weighted Average Rate | Equity at Risk | ||||||||

Wells Fargo Bank, N. A. and affiliates | $ | 300,761 | 1.40 | % | $ | 54,432 | |||||

Of the amount outstanding with Wells Fargo Bank, N.A. and affiliates, $287,538 is under a committed repurchase facility which has an aggregate maximum borrowing capacity of $350,000 and is scheduled to mature on August 6, 2018, subject to early termination provisions contained in the master repurchase agreement. The facility is collateralized primarily by CMBS IO, and its weighted average borrowing rate as of September 30, 2016 was 1.39%.

As of September 30, 2016, the Company had repurchase agreement amounts outstanding with 18 of its 32 available repurchase agreement counterparties. The Company's counterparties, as set forth in the master repurchase agreement with the counterparty, require the Company to comply with various customary operating and financial covenants, including, but not limited to, minimum net worth, maximum declines in net worth in a given period, and maximum leverage requirements as well as maintaining the Company's REIT status. In addition, some of the agreements contain cross default features, whereby default

13

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

under an agreement with one lender simultaneously causes default under agreements with other lenders. To the extent that the Company fails to comply with the covenants contained in these financing agreements or is otherwise found to be in default under the terms of such agreements, the counterparty has the right to accelerate amounts due under the master repurchase agreement. With respect to outstanding repurchase agreement and FHLB advance financings as of September 30, 2016, the Company was in compliance with all covenants.

Please see Note 5 for the Company's disclosures related to offsetting assets and liabilities.

NOTE 4 – DERIVATIVES

The Company utilizes derivative instruments to economically hedge a portion of its exposure to interest rate risk. The Company primarily uses pay-fixed interest rate swaps and Eurodollar contracts to hedge its exposure to changes in interest rates and uses receive-fixed interest rate swaps to offset a portion of its pay-fixed interest rate swaps in order to manage its overall hedge position. The objective of the Company's risk management strategy is to mitigate declines in book value resulting from fluctuations in the fair value of the Company's assets from changing interest rates and to protect some portion of the Company's earnings from rising interest rates. Please refer to Note 1 for information related to the Company's accounting policy for its derivative instruments.

The table below summarizes information about the Company’s derivative instruments treated as trading instruments on its consolidated balance sheet as of the dates indicated:

September 30, 2016 | ||||||||||||||||

Derivative Assets | Derivative Liabilities | |||||||||||||||

Trading Instruments | Fair Value | Notional | Fair Value | Notional | ||||||||||||

Interest rate swaps | $ | 12,985 | $ | 425,000 | $ | (41,385 | ) | $ | 1,355,000 | |||||||

Eurodollar futures (1) | — | — | (42,638 | ) | 6,300,000 | |||||||||||

Total | $ | 12,985 | $ | 425,000 | $ | (84,023 | ) | $ | 7,655,000 | |||||||

December 31, 2015 | ||||||||||||||||

Derivative Assets | Derivative Liabilities | |||||||||||||||

Trading Instruments | Fair Value | Notional | Fair Value | Notional | ||||||||||||

Interest rate swaps | $ | 7,835 | $ | 460,000 | $ | (12,108 | ) | $ | 2,920,000 | |||||||

Eurodollar futures (1) | — | — | (29,097 | ) | 6,300,000 | |||||||||||

Total | $ | 7,835 | $ | 460,000 | $ | (41,205 | ) | $ | 9,220,000 | |||||||

(1) | The Eurodollar futures aggregate notional amount represents the total notional of the 3-month contracts with expiration dates from 2017 to 2020. The maximum notional outstanding for any future 3-month period did not exceed $725,000 as of September 30, 2016 or as of December 31, 2015. |

The following table summarizes the volume of activity related to derivative instruments for the period indicated:

For the nine months ended September 30, 2016: | Beginning of Period Notional Amount | Additions | Settlement, Termination, Expiration or Exercise | End of Period Notional Amount | |||||||||||

Receive-fixed interest rate swaps | $ | 425,000 | $ | — | $ | — | $ | 425,000 | |||||||

Pay-fixed interest rate swaps (1) | 2,955,000 | 1,250,000 | (2,850,000 | ) | 1,355,000 | ||||||||||

Eurodollar futures | 6,300,000 | — | — | 6,300,000 | |||||||||||

$ | 9,680,000 | $ | 1,250,000 | $ | (2,850,000 | ) | $ | 8,080,000 | |||||||

(1) The notional amount of pay-fixed interest rate swaps that were forward starting as of September 30, 2016 was $625,000.

14

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

The table below provides detail of the Company's "(loss) gain on derivative instruments, net" by type of derivative for the periods indicated:

Three Months Ended | Nine Months Ended | ||||||||||||||

September 30, | September 30, | ||||||||||||||

Type of Derivative Instrument | 2016 | 2015 | 2016 | 2015 | |||||||||||

Receive-fixed interest rate swaps | $ | (2,976 | ) | $ | 6,975 | $ | 11,301 | $ | 9,757 | ||||||

Pay-fixed interest rate swaps | 2,555 | (48,697 | ) | (59,912 | ) | (45,797 | ) | ||||||||

Eurodollar futures | 2,830 | (11,027 | ) | (13,542 | ) | (24,942 | ) | ||||||||

(Loss) gain on derivative instruments, net | $ | 2,409 | $ | (52,749 | ) | $ | (62,153 | ) | $ | (60,982 | ) | ||||

There is a net unrealized gain of $769 remaining in AOCI on the Company's consolidated balance sheet as of September 30, 2016 which represents the activity related to interest rate swap agreements while they were previously designated as cash flow hedges, and this amount will be recognized in the Company's net income as a portion of "interest expense" over the remaining contractual life of the agreements. The Company estimates a credit of $319 will be reclassified to net income as a reduction of "interest expense" within the next 12 months.

A portion of the Company's interest rate swaps were entered into under bilateral agreements which contain cross-default provisions with other agreements between the parties. In addition, these bilateral agreements contain financial and operational covenants similar to those contained in our repurchase agreements, as described in Note 3. With respect to interest rate agreements under which interest rate swaps were entered into as of September 30, 2016, the Company was in compliance with all covenants.

Please see Note 5 for the Company's disclosures related to offsetting assets and liabilities.

NOTE 5 – OFFSETTING ASSETS AND LIABILITIES

The Company's derivatives, repurchase agreements, and FHLB advances are subject to underlying agreements with master netting or similar arrangements, which provide for the right of offset in the event of default or in the event of bankruptcy of either party to the transactions. The Company reports its assets and liabilities subject to these arrangements on a gross basis. The following tables present information regarding those assets and liabilities subject to such arrangements as if the Company had presented them on a net basis as of September 30, 2016 and December 31, 2015:

Offsetting of Assets | |||||||||||||||||||||||

Gross Amount of Recognized Assets | Gross Amount Offset in the Balance Sheet | Net Amount of Assets Presented in the Balance Sheet | Gross Amount Not Offset in the Balance Sheet (1) | Net Amount | |||||||||||||||||||

Financial Instruments Received as Collateral | Cash Received as Collateral | ||||||||||||||||||||||

September 30, 2016 | |||||||||||||||||||||||

Derivative assets | $ | 12,985 | $ | — | $ | 12,985 | $ | (12,985 | ) | $ | — | $ | — | ||||||||||

December 31, 2015: | |||||||||||||||||||||||

Derivative assets | $ | 7,835 | $ | — | $ | 7,835 | $ | (7,835 | ) | $ | — | $ | — | ||||||||||

15

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

Offsetting of Liabilities | |||||||||||||||||||||||

Gross Amount of Recognized Liabilities | Gross Amount Offset in the Balance Sheet | Net Amount of Liabilities Presented in the Balance Sheet | Gross Amount Not Offset in the Balance Sheet (1) | Net Amount | |||||||||||||||||||

Financial Instruments Posted as Collateral | Cash Posted as Collateral | ||||||||||||||||||||||

September 30, 2016 | |||||||||||||||||||||||

Derivative liabilities | $ | 84,023 | $ | — | $ | 84,023 | $ | (16,253 | ) | $ | (67,770 | ) | $ | — | |||||||||

Repurchase agreements | 2,478,278 | — | 2,478,278 | (2,478,278 | ) | — | — | ||||||||||||||||

FHLB advances | 263,000 | — | 263,000 | (263,000 | ) | — | — | ||||||||||||||||

$ | 2,825,301 | $ | — | $ | 2,825,301 | $ | (2,757,531 | ) | $ | (67,770 | ) | $ | — | ||||||||||

December 31, 2015: | |||||||||||||||||||||||

Derivative liabilities | $ | 41,205 | $ | — | $ | 41,205 | $ | (9,079 | ) | $ | (32,111 | ) | $ | 15 | |||||||||

Repurchase agreements | 2,589,420 | — | 2,589,420 | (2,589,420 | ) | — | — | ||||||||||||||||

FHLB advances | 520,000 | — | 520,000 | (520,000 | ) | — | — | ||||||||||||||||

$ | 3,150,625 | $ | — | $ | 3,150,625 | $ | (3,118,499 | ) | $ | (32,111 | ) | $ | 15 | ||||||||||

(1) | Amount disclosed for collateral received by or posted to the same counterparty include cash and the fair value of MBS up to and not exceeding the net amount of the asset or liability presented in the balance sheet. The fair value of the actual collateral received by or posted to the same counterparty may exceed the amounts presented. |

NOTE 6 – FAIR VALUE OF FINANCIAL INSTRUMENTS

ASC Topic 820 defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. ASC Topic 820 clarifies that fair value should be based on the assumptions market participants would use when pricing an asset or liability and also requires an entity to consider all aspects of nonperformance risk, including the entity's own credit standing, when measuring fair value of a liability. ASC Topic 820 established a valuation hierarchy of three levels as follows:

• | Level 1 – Inputs are unadjusted, quoted prices in active markets for identical assets or liabilities as of the measurement date. |

• | Level 2 – Inputs include quoted prices in active markets for similar assets or liabilities; quoted prices in inactive markets for identical or similar assets or liabilities; or inputs either directly observable or indirectly observable through correlation with market data at the measurement date and for the duration of the instrument’s anticipated life. |

• | Level 3 – Unobservable inputs are supported by little or no market activity. The unobservable inputs represent management’s best estimate of how market participants would price the asset or liability at the measurement date. Consideration is given to the risk inherent in the valuation technique and the risk inherent in the inputs to the model. |

The following table presents the fair value of the Company’s assets and liabilities presented on its consolidated balance sheets, segregated by the hierarchy level of the fair value estimate, that are measured at fair value on a recurring basis as of the dates indicated:

16

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

September 30, 2016 | |||||||||||||||

Fair Value | Level 1 - Unadjusted Quoted Prices in Active Markets | Level 2 - Observable Inputs | Level 3 - Unobservable Inputs | ||||||||||||

Assets: | |||||||||||||||

Mortgage-backed securities | $ | 3,110,467 | $ | — | $ | 3,097,055 | $ | 13,412 | |||||||

Derivative assets | 12,985 | — | 12,985 | — | |||||||||||

Total assets carried at fair value | $ | 3,123,452 | $ | — | $ | 3,110,040 | $ | 13,412 | |||||||

Liabilities: | |||||||||||||||

Derivative liabilities | $ | 84,023 | $ | 42,638 | $ | 41,385 | $ | — | |||||||

Total liabilities carried at fair value | $ | 84,023 | $ | 42,638 | $ | 41,385 | $ | — | |||||||

December 31, 2015 | |||||||||||||||

Fair Value | Level 1 - Unadjusted Quoted Prices in Active Markets | Level 2 - Observable Inputs | Level 3 - Unobservable Inputs | ||||||||||||

Assets: | |||||||||||||||

Mortgage-backed securities | $ | 3,493,701 | $ | — | $ | 3,477,266 | $ | 16,435 | |||||||

Derivative assets | 7,835 | — | 7,835 | — | |||||||||||

Total assets carried at fair value | $ | 3,501,536 | $ | — | $ | 3,485,101 | $ | 16,435 | |||||||

Liabilities: | |||||||||||||||

Derivative liabilities | $ | 41,205 | $ | 29,097 | $ | 12,108 | $ | — | |||||||

Total liabilities carried at fair value | $ | 41,205 | $ | 29,097 | $ | 12,108 | $ | — | |||||||

The Company did not have assets or liabilities measured at fair value on a non-recurring basis as of September 30, 2016 or December 31, 2015.

The Company's derivative assets and liabilities include interest rate swaps and Eurodollar futures. Interest rate swaps are valued using the income approach with the primary input being the forward interest rate swap curve, which is considered an observable input and thus their fair values are considered Level 2 measurements. Eurodollar futures are valued based on closing exchange prices on these contracts. Accordingly, the fair values of these financial futures are classified as Level 1 measurements.

Agency MBS, as well as a majority of non-Agency MBS, are substantially similar to securities that either are currently actively traded or have been recently traded in their respective market. Their fair values are derived from an average of multiple dealer quotes and thus are considered Level 2 fair value measurements. The Company’s remaining non-Agency MBS are comprised of securities for which there are not substantially similar securities that trade frequently, and their fair values are therefore considered Level 3 measurements. The Company determines the fair value of its Level 3 securities by discounting the estimated future cash flows derived from cash flow models using pricing indicators or assumptions determined by the Company. Significant inputs into those pricing models are Level 3 in nature due to the lack of readily available market quotes. Information utilized in those pricing models include the security’s credit rating, coupon rate, estimated prepayment speeds, expected weighted average life, collateral composition, estimated future interest rates, expected credit losses, and credit enhancement as well as certain other relevant information. Significant changes in any of these inputs in isolation would result in a significantly different fair value measurement. Level 3 assets are generally most sensitive to the default rate and severity assumptions.

17

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

The table below presents information about the significant unobservable inputs used in the fair value measurement for the Company's Level 3 non-Agency CMBS and RMBS as of September 30, 2016:

Quantitative Information about Level 3 Fair Value Measurements (1) | ||||||||||

Prepayment Speed | Default Rate | Severity | Discount Rate | |||||||

Non-Agency CMBS | 20 CPY | 2.0 | % | 35.0 | % | 10.1 | % | |||

Non-Agency RMBS | 10 CPR | 1.0 | % | 20.0 | % | 5.6 | % | |||

(1) | Data presented are weighted averages. |

The activity of the instruments measured at fair value on a recurring basis using Level 3 inputs is presented in the following table for the period indicated:

Level 3 Fair Value | |||||||||||

Non-Agency CMBS | Non-Agency RMBS | Total assets | |||||||||

Balance as of December 31, 2015 | $ | 14,903 | $ | 1,532 | $ | 16,435 | |||||

Unrealized (loss) gain included in OCI | (427 | ) | 19 | (408 | ) | ||||||

Principal payments | (3,223 | ) | (182 | ) | (3,405 | ) | |||||

Accretion | 790 | — | 790 | ||||||||

Balance as of September 30, 2016 | $ | 12,043 | $ | 1,369 | $ | 13,412 | |||||

The following table presents a summary of the carrying value and estimated fair values of the Company’s financial instruments as of the dates indicated:

September 30, 2016 | December 31, 2015 | ||||||||||||||

Carrying Value | Fair Value | Carrying Value | Fair Value | ||||||||||||

Assets: | |||||||||||||||

Mortgage-backed securities | $ | 3,110,467 | $ | 3,110,467 | $ | 3,493,701 | $ | 3,493,701 | |||||||

Mortgage loans held for investment, net(1) | 20,366 | 16,996 | 24,145 | 20,849 | |||||||||||

Investment in FHLB stock | 5,260 | 5,260 | 11,475 | 11,475 | |||||||||||

Derivative assets | 12,985 | 12,985 | 7,835 | 7,835 | |||||||||||

Liabilities: | |||||||||||||||

Repurchase agreements (2) | $ | 2,478,278 | $ | 2,478,278 | $ | 2,589,420 | $ | 2,589,420 | |||||||

FHLB advances (2) | 263,000 | 263,000 | 520,000 | 520,000 | |||||||||||

Non-recourse collateralized financing (1) | 7,025 | 6,802 | 8,442 | 8,102 | |||||||||||

Derivative liabilities | 84,023 | 84,023 | 41,205 | 41,205 | |||||||||||

(1) | The Company determines the fair value of its mortgage loans held for investment, net and its non-recourse collateralized financing using internally developed cash flow models with inputs similar to those used to estimate the fair value of the Company's Level 3 non-Agency MBS. |

(2) | The carrying value of repurchase agreements and FHLB advances generally approximates fair value due to their short term maturities. |

NOTE 7 – SHAREHOLDERS' EQUITY

Preferred Stock

18

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

The Company has 2,300,000 shares of its 8.50% Series A Preferred Stock and 2,250,000 shares of its 7.625% Series B Preferred Stock issued and outstanding as of September 30, 2016 (collectively, the "Preferred Stock"). The Preferred Stock has no maturity and will remain outstanding indefinitely unless redeemed or otherwise repurchased or converted into common stock pursuant to the terms of the Preferred Stock. Except under certain limited circumstances intended to preserve the Company's REIT status, upon the occurrence of a change in control as defined in Article IIIA, Section 7(d) of the Company’s Articles of Incorporation, or to avoid the direct or indirect imposition of a penalty tax in respect of, or to protect the tax status of, any of the Company’s real estate mortgage investment conduits (“REMIC”) interests or a REMIC in which the Company may acquire an interest (as permitted by the Company’s Articles of Incorporation), the Company may not redeem the Series A Preferred Stock prior to July 31, 2017 or the Series B Preferred Stock prior to April 30, 2018. On or after these dates, at any time and from time to time, the Preferred Stock may be redeemed in whole, or in part, at the Company's option at a cash redemption price of $25.00 per share plus any accumulated and unpaid dividends. The Series A Preferred Stock pays a cumulative cash dividend equivalent to 8.50% of the $25.00 liquidation preference per share each year and the Series B Preferred Stock pays a cumulative cash dividend equivalent to 7.625% of the $25.00 liquidation preference per share each year. Because the Preferred Stock is redeemable only at the option of the issuer, it is classified as equity on the Company's consolidated balance sheet. The Company announced that it will pay its regular quarterly dividends on its Preferred Stock for the third quarter on October 14, 2016 to shareholders of record as of October 1, 2016.

Common Stock

The following table presents a summary of the changes in the number of common shares outstanding for the periods presented:

Nine Months Ended | |||||

September 30, | |||||

2016 | 2015 | ||||

Balance as of beginning of period | 49,047,335 | 54,739,111 | |||

Common stock issued under DRIP | 15,714 | 16,862 | |||

Common stock issued under stock and incentive plans | 214,878 | 263,829 | |||

Common stock forfeited for tax withholding on share-based compensation | (80,888 | ) | (67,296 | ) | |

Common stock repurchased during the period | (48,444 | ) | (4,383,716 | ) | |

Balance as of end of period | 49,148,595 | 50,568,790 | |||

The Company had 7,416,520 shares of common stock that remain available to offer and sell through its sales agent, JMP Securities LLC, under its "at the market", or "ATM" program, as of September 30, 2016.

The Company's Dividend Reinvestment and Share Purchase Plan ("DRIP") allows registered shareholders to automatically reinvest some or all of their quarterly common stock dividends in shares of the Company’s common stock and provides an opportunity for investors to purchase shares of the Company’s common stock, potentially at a discount to the prevailing market price. Of the 3,000,000 shares reserved for issuance under the Company's DRIP, there were 2,411,824 shares remaining for issuance as of September 30, 2016. The Company declared a third quarter common stock dividend of $0.21 per share payable on October 31, 2016 to shareholders of record as of October 5, 2016. There was no discount for shares purchased through the DRIP during the third quarter of 2016.

Of the $50,000 authorized by the Company's Board of Directors for the repurchase of its common stock through December 31, 2016, approximately $8,518 remains available for repurchase at the Company's option as of September 30, 2016.

2009 Stock and Incentive Plan. Of the 2,500,000 shares of common stock authorized for issuance under its 2009 Stock and Incentive Plan, the Company had 860,106 available for issuance as of September 30, 2016. Total stock-based compensation expense recognized by the Company for the three and nine months ended September 30, 2016 was $623 and $2,066 compared to $745 and $2,220 for the three and nine months ended September 30, 2015.

The following table presents a rollforward of the restricted stock activity for the periods indicated:

19

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

($ in thousands except per share data)

Three Months Ended | Nine Months Ended | ||||||||||

September 30, | September 30, | ||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||

Restricted stock outstanding as of beginning of period | 561,089 | 696,597 | 696,597 | 731,809 | |||||||

Restricted stock granted | — | — | 214,878 | 263,829 | |||||||

Restricted stock vested | — | — | (350,386 | ) | (299,041 | ) | |||||

Restricted stock outstanding as of end of period | 561,089 | 696,597 | 561,089 | 696,597 | |||||||

The combined grant date fair value of the restricted stock issued by the Company for the nine months ended September 30, 2016 was $1,349 compared to $2,167 for the nine months ended September 30, 2015. As of September 30, 2016, the fair value of the Company’s outstanding restricted stock remaining to be amortized into compensation expense is $2,781 which will be recognized over a weighted average period of 1.5 years.

NOTE 8 – SUBSEQUENT EVENTS

Management has evaluated events and circumstances occurring as of and through the date this Quarterly Report on Form 10-Q was filed with the SEC and has determined that there have been no significant events or circumstances that qualify as a "recognized" or "nonrecognized" subsequent event as defined by ASC Topic 855.

20

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion should be read in conjunction with our unaudited financial statements and the accompanying notes included in Part 1, Item 1. “Financial Statements” in this Quarterly Report on Form 10-Q and our audited financial statements and the accompanying notes included in Part II, Item 8 in our Annual Report on Form 10-K for the year ended December 31, 2015. References herein to “Dynex,” the “Company,” “we,” “us,” and “our” include Dynex Capital, Inc. and its consolidated subsidiaries, unless the context otherwise requires. In addition to current and historical information, the following discussion and analysis contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements relate to our future business, financial condition or results of operations. For a description of certain factors that may have a significant impact on our future business, financial condition or results of operations, see “Forward-Looking Statements” at the end of this discussion and analysis.

For a complete description of our business including our operating policies, investment philosophy and strategy, financing and hedging strategies, and other important information, please refer to Part I, Item 1 of our Annual Report on Form 10-K for the year ended December 31, 2015.

EXECUTIVE OVERVIEW

Company Overview

We are an internally managed mortgage real estate investment trust, or mortgage REIT, which invests in residential and commercial mortgage-backed securities on a leveraged basis. Our common stock is traded on the New York Stock Exchange ("NYSE") under the symbol "DX". We also have two series of preferred stock outstanding, our 8.50% Series A Cumulative Redeemable Preferred Stock (the "Series A Preferred Stock") which is traded on the NYSE under the symbol "DXPRA", and our 7.625% Series B Cumulative Redeemable Preferred Stock (the "Series B Preferred Stock") which is traded on the NYSE under the symbol "DXPRB". Our objective is to provide attractive risk-adjusted returns to our shareholders over the long term that are reflective of a leveraged, high quality fixed income portfolio with a focus on capital preservation. We seek to provide returns to our shareholders primarily through regular quarterly dividends, and also through capital appreciation.

We invest in Agency and non-Agency mortgage-backed securities (“MBS”) consisting of residential MBS (“RMBS”), commercial MBS (“CMBS”) and CMBS interest-only ("IO") securities. Agency MBS have a guaranty of principal payment by an agency of the U.S. government or a U.S. government-sponsored entity ("GSE") such as Fannie Mae and Freddie Mac. Non-Agency MBS have no such guaranty of payment. Due to the guaranty of principal payment by a GSE, Agency MBS are the highest credit quality MBS available for investment. We seek to invest in Agency MBS and higher quality non-Agency MBS (typically rated 'A' or better by one or more of the nationally recognized statistical rating organizations) to limit our exposure to credit losses and to minimize fluctuations in fair value from widening in credit spreads. In addition, Agency MBS and higher-rated non-Agency MBS are typically more liquid (i.e., they are more easily converted into cash either through sales or pledges as collateral for repurchase agreement borrowings) than lower-rated MBS.

Our primary source of income is net interest income, which is the excess of the interest income earned on our investments over the cost of financing these investments. We invest our capital pursuant to our Operating Policies as approved by our Board of Directors which include an Investment Policy and Investment Risk Policy. We use leverage to enhance the returns on our invested capital by pledging our investments as collateral for borrowings such as repurchase agreements as discussed further below.

RMBS. Our Agency RMBS investments include MBS collateralized by adjustable-rate mortgage loans ("ARMs"), which have interest rates that generally will adjust at least annually to an increment over a specified interest rate index, and hybrid adjustable-rate mortgage loans ("hybrid ARMs"), which are loans that have a fixed rate of interest for a specified period (typically three to ten years) and then adjust their interest rate at least annually to an increment over a specified interest rate index. Agency ARMs also include hybrid Agency ARMs that are past their fixed-rate periods or within twelve months of their initial reset period. We may also invest in fixed-rate Agency RMBS from time to time.

21

We also invest in non-Agency RMBS, which do not carry a principal guarantee from the U.S. government or a GSE. Non-Agency RMBS are collateralized by non-conforming residential mortgage loans and are tranched into different credit classes of securities with payments to junior classes subordinate to senior classes. Some of the non-Agency RMBS that we invest in may be collateralized by loans which are delinquent, the repayment of which is expected to come from foreclosure and liquidation of the underlying real estate. We generally invest in senior classes of non-Agency RMBS which may include unrated securities. We seek to invest in non-Agency RMBS that we judge to have sufficiently high collateralization to be likely to protect the principal balance of our investment from credit losses on the underlying loans.

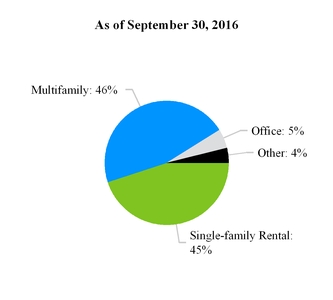

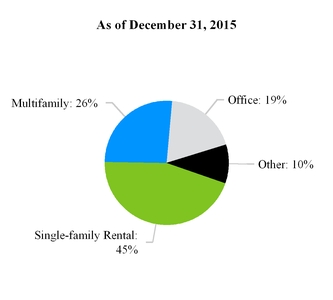

CMBS. Our Agency and non-Agency CMBS are collateralized by first mortgage loans and are primarily fixed-rate securities backed by multifamily housing and other commercial real estate property types such as office building, retail, hospitality, and health care. Loans underlying CMBS generally are geographically diverse, are fixed-rate, mature in ten to twelve years and have amortization terms of up to 30 years. Typically these loans have some form of prepayment protection provisions (such as prepayment lock-out) or prepayment compensation provisions (such as yield maintenance or prepayment penalty). Yield maintenance and prepayment penalty requirements are intended to create an economic disincentive for the loans to prepay. Non-Agency CMBS also includes securities that are backed by pools of single-family rental homes which have variable-rates that reset monthly based on an index rate, such as LIBOR.