Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - FLOTEK INDUSTRIES INC/CN/ | exhibit322-10q09302016.htm |

| EX-32.1 - EXHIBIT 32.1 - FLOTEK INDUSTRIES INC/CN/ | exhibit321-10q09302016.htm |

| EX-31.2 - EXHIBIT 31.2 - FLOTEK INDUSTRIES INC/CN/ | exhibit312-10q09302016.htm |

| EX-31.1 - EXHIBIT 31.1 - FLOTEK INDUSTRIES INC/CN/ | exhibit311-10q09302016.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q |

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2016

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-13270

FLOTEK INDUSTRIES, INC. (Exact name of registrant as specified in its charter) |

Delaware | 90-0023731 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

10603 W. Sam Houston Parkway N., Suite 300 Houston, TX | 77064 | |

(Address of principal executive offices) | (Zip Code) | |

(713) 849-9911

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ¨ | Accelerated filer | x | |||

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of October 28, 2016, there were 56,703,963 outstanding shares of Flotek Industries, Inc. common stock, $0.0001 par value.

TABLE OF CONTENTS

2

PART I — FINANCIAL INFORMATION

Item 1. Financial Statements

FLOTEK INDUSTRIES, INC.

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands, except share data)

September 30, 2016 | December 31, 2015 | ||||||

ASSETS | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 3,474 | $ | 2,208 | |||

Accounts receivable, net of allowance for doubtful accounts of $1,003 and $1,189 at September 30, 2016 and December 31, 2015, respectively | 53,652 | 49,197 | |||||

Inventories | 73,986 | 85,492 | |||||

Income taxes receivable | 18,192 | 4,700 | |||||

Deferred tax assets, net | 2,352 | 2,649 | |||||

Other current assets | 9,099 | 7,496 | |||||

Total current assets | 160,755 | 151,742 | |||||

Property and equipment, net | 89,154 | 91,913 | |||||

Goodwill | 73,682 | 72,820 | |||||

Deferred tax assets, net | — | 17,229 | |||||

Other intangible assets, net | 58,949 | 69,386 | |||||

TOTAL ASSETS | $ | 382,540 | $ | 403,090 | |||

LIABILITIES AND EQUITY | |||||||

Current liabilities: | |||||||

Accounts payable | $ | 26,072 | $ | 19,444 | |||

Accrued liabilities | 11,826 | 12,894 | |||||

Income taxes payable | — | 2,263 | |||||

Interest payable | 156 | 111 | |||||

Current portion of long-term debt | 34,562 | 32,291 | |||||

Total current liabilities | 72,616 | 67,003 | |||||

Long-term debt, less current portion | 8,000 | 18,255 | |||||

Deferred tax liabilities, net | 1,205 | 23,823 | |||||

Total liabilities | 81,821 | 109,081 | |||||

Commitments and contingencies | |||||||

Equity: | |||||||

Cumulative convertible preferred stock, $0.0001 par value, 100,000 shares authorized; no shares issued and outstanding | — | — | |||||

Common stock, $0.0001 par value, 80,000,000 shares authorized; 59,604,669 shares issued and 56,698,874 shares outstanding at September 30, 2016; 56,220,214 shares issued and 53,536,101 shares outstanding at December 31, 2015 | 6 | 6 | |||||

Additional paid-in capital | 316,091 | 273,451 | |||||

Accumulated other comprehensive income (loss) | (981 | ) | (1,237 | ) | |||

Retained earnings | 4,089 | 39,300 | |||||

Treasury stock, at cost; 1,893,612 and 1,784,897 shares at September 30, 2016 and December 31, 2015, respectively | (18,844 | ) | (17,869 | ) | |||

Flotek Industries, Inc. stockholders’ equity | 300,361 | 293,651 | |||||

Noncontrolling interests | 358 | 358 | |||||

Total equity | 300,719 | 294,009 | |||||

TOTAL LIABILITIES AND EQUITY | $ | 382,540 | $ | 403,090 | |||

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

3

FLOTEK INDUSTRIES, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share data)

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Revenue | $ | 73,679 | $ | 87,942 | $ | 218,287 | $ | 257,346 | |||||||

Cost of revenue | 48,313 | 56,715 | 144,071 | 170,340 | |||||||||||

Gross profit | 25,366 | 31,227 | 74,216 | 87,006 | |||||||||||

Expenses: | |||||||||||||||

Selling, general and administrative | 24,424 | 23,634 | 71,859 | 70,223 | |||||||||||

Depreciation and amortization | 2,706 | 2,785 | 7,896 | 8,258 | |||||||||||

Research and development | 2,531 | 2,031 | 7,059 | 5,273 | |||||||||||

Impairment of inventory and long-lived assets | — | — | 40,435 | 20,372 | |||||||||||

Total expenses | 29,661 | 28,450 | 127,249 | 104,126 | |||||||||||

(Loss) income from operations | (4,295 | ) | 2,777 | (53,033 | ) | (17,120 | ) | ||||||||

Other (expense) income: | |||||||||||||||

Interest expense | (611 | ) | (476 | ) | (1,811 | ) | (1,303 | ) | |||||||

Other (expense) income, net | (49 | ) | 74 | (207 | ) | (154 | ) | ||||||||

Total other expense | (660 | ) | (402 | ) | (2,018 | ) | (1,457 | ) | |||||||

(Loss) income before income taxes | (4,955 | ) | 2,375 | (55,051 | ) | (18,577 | ) | ||||||||

Income tax benefit (expense) | 2,209 | (400 | ) | 19,840 | 6,490 | ||||||||||

Net (loss) income | $ | (2,746 | ) | $ | 1,975 | $ | (35,211 | ) | $ | (12,087 | ) | ||||

(Loss) earnings per common share: | |||||||||||||||

Basic (loss) earnings per common share | $ | (0.05 | ) | $ | 0.04 | $ | (0.63 | ) | $ | (0.22 | ) | ||||

Diluted (loss) earnings per common share | $ | (0.05 | ) | $ | 0.04 | $ | (0.63 | ) | $ | (0.22 | ) | ||||

Weighted average common shares: | |||||||||||||||

Weighted average common shares used in computing basic (loss) earnings per common share | 56,899 | 54,578 | 55,523 | 54,430 | |||||||||||

Weighted average common shares used in computing diluted (loss) earnings per common share | 56,899 | 54,947 | 55,523 | 54,430 | |||||||||||

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

4

FLOTEK INDUSTRIES, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(in thousands)

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Net (loss) income | $ | (2,746 | ) | $ | 1,975 | $ | (35,211 | ) | $ | (12,087 | ) | ||||

Other comprehensive income (loss): | |||||||||||||||

Foreign currency translation adjustment | (68 | ) | (366 | ) | 256 | (531 | ) | ||||||||

Comprehensive (loss) income | $ | (2,814 | ) | $ | 1,609 | $ | (34,955 | ) | $ | (12,618 | ) | ||||

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

5

FLOTEK INDUSTRIES, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

Nine months ended September 30, | |||||||

2016 | 2015 | ||||||

Cash flows from operating activities: | |||||||

Net loss | $ | (35,211 | ) | $ | (12,087 | ) | |

Adjustments to reconcile net loss to net cash (used in) provided by operating activities: | |||||||

Impairment of inventory and long-lived assets | 40,435 | 20,372 | |||||

Depreciation and amortization | 11,069 | 13,613 | |||||

Amortization of deferred financing costs | 308 | 260 | |||||

Gain on sale of assets | (1,094 | ) | (3,010 | ) | |||

Stock compensation expense | 9,479 | 10,479 | |||||

Deferred income tax benefit | (6,309 | ) | (8,696 | ) | |||

Reduction in (excess) tax benefit related to share-based awards | 883 | (2,154 | ) | ||||

Changes in current assets and liabilities: | |||||||

Accounts receivable, net | (3,744 | ) | 26,276 | ||||

Inventories | (4,108 | ) | (16,456 | ) | |||

Income taxes receivable | (13,687 | ) | (3,104 | ) | |||

Other current assets | (1,076 | ) | 1,402 | ||||

Accounts payable | 6,417 | (11,080 | ) | ||||

Accrued liabilities | (2,515 | ) | (1,462 | ) | |||

Income taxes payable | (1,807 | ) | 2,943 | ||||

Interest payable | 45 | — | |||||

Net cash (used in) provided by operating activities | (915 | ) | 17,296 | ||||

Cash flows from investing activities: | |||||||

Capital expenditures | (11,621 | ) | (11,078 | ) | |||

Proceeds from sale of assets | 1,201 | 3,225 | |||||

Payments for acquisition, net of cash acquired | (7,863 | ) | (1,250 | ) | |||

Purchase of patents and other intangible assets | (396 | ) | (434 | ) | |||

Net cash used in investing activities | (18,679 | ) | (9,537 | ) | |||

Cash flows from financing activities: | |||||||

Repayments of indebtedness | (15,398 | ) | (8,357 | ) | |||

Borrowings on revolving credit facility | 256,738 | 291,916 | |||||

Repayments on revolving credit facility | (249,324 | ) | (279,832 | ) | |||

Debt issuance costs | (147 | ) | (10 | ) | |||

(Reduction in) excess tax benefit related to share-based awards | (883 | ) | 2,154 | ||||

Purchase of treasury stock related to share-based awards | (925 | ) | (5,376 | ) | |||

Proceeds from sale of common stock | 30,610 | 779 | |||||

Repurchase of common stock | — | (7,299 | ) | ||||

Proceeds from exercise of stock options | 134 | 22 | |||||

Proceeds from noncontrolling interest | — | 7 | |||||

Net cash provided by (used in) financing activities | 20,805 | (5,996 | ) | ||||

Effect of changes in exchange rates on cash and cash equivalents | 55 | (31 | ) | ||||

Net increase in cash and cash equivalents | 1,266 | 1,732 | |||||

Cash and cash equivalents at the beginning of period | 2,208 | 1,266 | |||||

Cash and cash equivalents at the end of period | $ | 3,474 | $ | 2,998 | |||

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

6

FLOTEK INDUSTRIES, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF EQUITY

(in thousands)

Common Stock | Treasury Stock | Additional Paid-in Capital | Accumulated Other Comprehensive Income (Loss) | Retained Earnings | Non-controlling Interests | Total Equity | |||||||||||||||||||||||||||

Shares Issued | Par Value | Shares | Cost | ||||||||||||||||||||||||||||||

Balance, December 31, 2015 | 56,220 | $ | 6 | 1,785 | $ | (17,869 | ) | $ | 273,451 | $ | (1,237 | ) | $ | 39,300 | $ | 358 | $ | 294,009 | |||||||||||||||

Net loss | — | — | — | — | — | — | (35,211 | ) | — | (35,211 | ) | ||||||||||||||||||||||

Foreign currency translation adjustment | — | — | — | — | — | 256 | — | — | 256 | ||||||||||||||||||||||||

Sale of common stock, net of issuance cost | 2,450 | — | — | — | 29,940 | — | — | — | 29,940 | ||||||||||||||||||||||||

Stock issued under employee stock purchase plan | — | — | (73 | ) | — | 670 | — | — | — | 670 | |||||||||||||||||||||||

Stock options exercised | 114 | — | — | — | 184 | — | — | — | 184 | ||||||||||||||||||||||||

Stock surrendered for exercise of stock options | — | — | 3 | (50 | ) | — | — | — | — | (50 | ) | ||||||||||||||||||||||

Restricted stock granted | 573 | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||

Restricted stock forfeited | — | — | 89 | — | — | — | — | — | — | ||||||||||||||||||||||||

Treasury stock purchased | — | — | 90 | (925 | ) | — | — | — | — | (925 | ) | ||||||||||||||||||||||

Stock compensation expense | — | — | — | — | 9,461 | — | — | — | 9,461 | ||||||||||||||||||||||||

Reduction in tax benefit related to share-based awards | — | — | — | — | (883 | ) | — | — | — | (883 | ) | ||||||||||||||||||||||

Stock issued in IPI acquisition | 248 | — | — | — | 3,268 | — | — | — | 3,268 | ||||||||||||||||||||||||

Balance, September 30, 2016 | 59,605 | $ | 6 | 1,894 | $ | (18,844 | ) | $ | 316,091 | $ | (981 | ) | $ | 4,089 | $ | 358 | $ | 300,719 | |||||||||||||||

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

7

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 1 — Organization and Significant Accounting Policies

Organization and Nature of Operations

Flotek Industries, Inc. (“Flotek” or the “Company”) is a global, diversified, technology-driven supplier of energy chemistries and consumer and industrial chemistries and is a global developer and supplier of drilling, completion, and production technologies and related services.

The Company’s strategic focus includes energy related chemistry technologies, drilling and production technologies, and consumer and industrial chemistry technologies. Within its energy related technologies, the Company provides oilfield specialty chemistries and logistics, downhole drilling tools, and production related tools used in the energy and mining industries. Flotek’s products and services enable customers to drill wells more efficiently, to realize increased production from both new and existing wells, and to decrease future well operating costs. Major customers include leading oilfield service providers, pressure-pumping service companies, onshore and offshore drilling contractors, major and independent oil and gas exploration and production companies, national and state-owned oil companies, and international supply chain management companies. Within consumer and industrial chemistry technologies, the Company provides products for the flavor and fragrance industry and the industrial chemical industry. Major customers include food and beverage companies, fragrance companies, and companies providing household and industrial cleaning products.

The Company is headquartered in Houston, Texas, with operating locations in Colorado, Florida, Georgia, Louisiana, New Mexico, North Dakota, Oklahoma, Pennsylvania, Texas, Utah, Wyoming, Canada, the Netherlands, and the Middle East. Flotek’s products are marketed both domestically and internationally, with international presence and/or representation in over 20 countries.

Flotek was initially incorporated under the laws of the Province of British Columbia on May 17, 1985. On October 23, 2001, Flotek changed its corporate domicile to the state of Delaware.

Basis of Presentation

The accompanying Unaudited Condensed Consolidated Financial Statements and accompanying footnotes (collectively the “Financial Statements”) reflect all adjustments, in the opinion of management, necessary for fair presentation of the financial condition and results of operations for the periods presented. All such adjustments are normal and recurring in nature. The Financial Statements, including selected notes, have been prepared in accordance with applicable rules and regulations of the Securities and Exchange Commission (“SEC”) regarding interim financial reporting and do not include all information and disclosures required by accounting principles generally accepted in the United States of America (“U.S. GAAP”) for comprehensive financial statement reporting. These interim Financial Statements should be read in conjunction with the audited consolidated financial statements and notes included in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2015 (“Annual Report”). A copy of the Annual Report is available on the SEC’s website, www.sec.gov, under the Company’s ticker symbol (“FTK”) or on Flotek’s website, www.flotekind.com. The results of operations for the three and nine months ended September 30, 2016, are not necessarily indicative of the results to be expected for the year ending December 31, 2016.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect reported amounts of assets and liabilities, disclosure of contingent assets and liabilities, and reported amounts of revenue and expenses. Actual results could differ from these estimates.

Reclassifications

Certain prior period amounts have been reclassified to conform to the current period presentation. The reclassifications did not impact net income (loss).

8

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 — Recent Accounting Pronouncements

Application of New Accounting Standards

Effective January 1, 2016, the Company adopted the accounting guidance in Accounting Standards Update (“ASU”) No. 2015-01, “Simplifying Income Statement Presentation by Eliminating the Concept of Extraordinary Items.” This ASU eliminates from U.S. GAAP the concept of extraordinary items and the need for an entity to separately classify, present, and disclose extraordinary events and transactions, while retaining certain presentation and disclosure guidance for items that are unusual in nature or occur infrequently. Implementation of this standard did not have a material effect on the consolidated financial statements and related disclosures.

Effective January 1, 2016, the Company adopted the accounting guidance in ASU No. 2015-02, “Amendments to the Consolidation Analysis.” The amendment eliminates the deferral of certain consolidation standards for entities considered to be investment companies and modifies the consolidation analysis performed on certain types of legal entities. Implementation of this standard did not have a material effect on the consolidated financial statements and related disclosures.

Effective January 1, 2016, the Company adopted the accounting guidance in ASU No. 2015-03, “Simplifying the Presentation of Debt Issuance Costs.” The accounting guidance requires that debt issuance costs related to a recognized debt liability be reported on the Consolidated Statements of Financial Condition as a direct deduction from the carrying amount of that debt liability. In addition, the Company adopted the accounting guidance in ASU No. 2015-15, which provides additional guidance related to the presentation or subsequent measurement of debt issuance costs related to line-of-credit arrangements. An entity may present debt issuance costs as an asset and subsequently amortize the deferred debt issuance costs ratably over the term of the line-of-credit arrangement, regardless of whether there are any outstanding borrowings. Implementation of these standards did not have a material effect on the consolidated financial statements and related disclosures.

Effective January 1, 2016, the Company adopted the accounting guidance in ASU No. 2015-16, “Simplifying the Accounting for Measurement-Period Adjustments.” This standard replaces the requirement that an acquirer in a business combination account for measurement period adjustments retrospectively with a requirement that an acquirer recognize adjustments to the provisional amounts that are identified during the measurement period in the reporting period in which the adjustment amounts are determined. The acquirer is required to record, in the same period’s financial statements, the effect on earnings of changes in depreciation, amortization, or other income effects, if any, as a result of the change to the provisional amounts, calculated as if the accounting had been completed at the acquisition date. The guidance is to be applied prospectively to adjustments to provisional amounts that occur after the effective date of the guidance. Implementation of this standard did not have a material effect on the consolidated financial statements and related disclosures.

New Accounting Requirements and Disclosures

In May 2014, the Financial Accounting Standards Board (“FASB”) issued ASU No. 2014-09, “Revenue from Contracts with Customers.” The ASU will supersede most of the existing revenue recognition requirements in U.S. GAAP and will require entities to recognize revenue at an amount that reflects the consideration to which the Company expects to be entitled in exchange for transferring goods or services to a customer. The new standard also requires significantly expanded disclosures regarding the qualitative and quantitative information of an entity’s nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. In August 2015, the FASB issued ASU No. 2015-14, which deferred the effective date by one year to annual reporting periods beginning after December 15, 2017, including interim periods within that reporting period. Early adoption is permitted, but not before the original effective date of reporting periods beginning after December 15, 2016. In March 2016, the FASB issued ASU No. 2016-08, which improves the operability and understandability of the implementation guidance on principal versus agent considerations. In April 2016, the FASB issued ASU No. 2016-10, which clarifies identifying performance obligations and the licensing implementation guidance. In May 2016, the FASB issued ASU No. 2016-11, which rescinds certain SEC Staff Observer comments that are codified in Topic 605, Revenue Recognition, effective upon adoption of ASU 2014-09, and ASU No. 2016-12, which reduces the potential for diversity in practice at initial application and reduces the cost and complexity of applying Topic 606 both at transition and on an ongoing basis. The Company is currently evaluating the impact these pronouncements will have on the consolidated financial statements and related disclosures.

In July 2015, the FASB issued ASU No. 2015-11, “Simplifying the Measurement of Inventory.” This standard requires management to measure inventory at the lower of cost or net realizable value. Net realizable value is the estimated selling prices in the ordinary course of business, less reasonably predictable costs of completion, disposal, and transportation. The pronouncement is effective for annual reporting periods beginning after December 15, 2016, including interim periods within that reporting period and should be applied retrospectively, with early application permitted. The Company is currently evaluating the impact the pronouncement will have on the consolidated financial statements and related disclosures.

9

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

In November 2015, the FASB issued ASU 2015-17, “Balance Sheet Classification of Deferred Taxes.” This standard eliminates the current requirement for organizations to present deferred tax assets and liabilities as current and noncurrent in a classified balance sheet. Instead, organizations will be required to classify all deferred tax assets and liabilities as noncurrent. The pronouncement is effective for annual reporting periods beginning after December 15, 2016, including interim periods within that reporting period. The Company is currently evaluating the impact the pronouncement will have on the consolidated financial statements and related disclosures.

In February 2016, the FASB issued ASU No. 2016-02, “Leases.” This standard requires the recognition of lease assets and lease liabilities by lessees for those leases classified as operating leases under previous U.S. GAAP. The pronouncement is effective for annual reporting periods beginning after December 15, 2018, including interim periods within that reporting period and should be applied using a modified retrospective transition approach, with early application permitted. The Company is currently evaluating the impact the pronouncement will have on the consolidated financial statements and related disclosures.

In March 2016, the FASB issued ASU No. 2016-09, “Improvements to Employee Share-Based Payment Accounting.” This standard simplifies several aspects of the accounting for share-based payment transactions, including the income tax consequences, classification of awards as either equity or liabilities, and classification on the statement of cash flows. The pronouncement is effective for annual reporting periods beginning after December 15, 2016, including interim periods within those annual periods, with early adoption permitted. The Company is currently evaluating the impact the pronouncement will have on the consolidated financial statements and related disclosures.

In June 2016, the FASB issued ASU No. 2016-13, “Measurement of Credit Losses on Financial Instruments.” This standard replaces the incurred loss impairment methodology in current U.S. GAAP with a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. The pronouncement is effective for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years, with early adoption for the fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. The Company is currently evaluating the impact the pronouncement will have on the consolidated financial statements and related disclosures.

In August 2016, the FASB issued ASU No 2016-15, “Classification of Certain Cash Receipts and Cash Payments.” This standard addresses eight specific cash flow issues with the objective of reducing the existing diversity in practice. The pronouncement is effective for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years, with early adoption permitted. The Company is currently evaluating the impact the pronouncement will have on the consolidated financial statements and related disclosures.

Note 3 — Impairment of Inventory and Long-Lived Assets

During the three months ended March 31, 2016, as a result of changes in the oil and gas industry that occurred since the beginning of 2016 and the corresponding impact on the Company’s business outlook, the Company evaluated the direction of its business activities. Crude oil prices, which appeared to have stabilized during the fourth quarter of 2015, fell further during the first quarter of 2016, decreasing approximately 21% from average prices seen in the fourth quarter of 2015. The U.S. drilling rig count declined from 698 at December 31, 2015 to 450 at April 1, 2016, a decline of 35.5%.

Due to the decreased rig activity and its impact on management’s expectations for future market activity, the Company further refocused operations of its Drilling Technologies segment. The Company decided to exit the business of building and repairing motors in all domestic markets. In addition, changes in drilling technique, including further escalation of the move to a dominance of pad drilling, reduced the marketability of certain other inventory items. The focus of the Production Technologies segment is being shifted to its new technologies for electric submersible pumps for the oil and gas industry and for hydraulic pumping units. Inventory associated with older technologies for these items has been evaluated for impairment. As a result of these changes in focus and projected declines in asset utilization, the Company recorded a pre-tax impairment of inventories as noted below.

Changes in the business climate noted above and increasing operating losses experienced within the Drilling Technologies and Production Technologies segments during the three months ended March 31, 2016, caused the Company to test asset groups within these two segments for recoverability. Recoverability of the carrying value of the asset groups was based upon estimated future cash flows while taking into consideration various assumptions and estimates, including future use of the assets, remaining useful life of the assets, and eventual disposition of the assets. Undiscounted estimated cash flows of two asset groups associated with domestic operations in the Drilling Technologies segment did not exceed the carrying value of the respective asset groups. Therefore, the Company performed an analysis of discounted future cash flows to determine the fair value of each of these two asset groups. As a result of this testing, the Company recorded a pre-tax impairment of long-lived assets as noted below.

10

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

In addition, during the three months ended June 30, 2015, as a result of decreased rig activity and its impact on management’s expectations for future market activity, the Company refocused the Drilling Technologies segment to businesses and markets that have the best opportunity for profitable growth in the future. In addition, the Company shifted the focus of the Production Technologies segment to oil production markets and away from coal bed methane markets. As a result of these changes in focus and projected declines in asset utilization, the Company recorded pre-tax impairment charges as noted below.

The Company recorded impairment charges during the three months ended March 31, 2016 and June 30, 2015, as follows (in thousands):

Three months ended | |||||||

March 31, 2016 | June 30, 2015 | ||||||

Drilling Technologies: | |||||||

Inventories | $ | 12,653 | $ | 17,241 | |||

Long-lived assets: | |||||||

Property and equipment | 14,642 | 2,327 | |||||

Intangible assets other than goodwill | 9,227 | — | |||||

Production Technologies: | |||||||

Inventories | 3,913 | 804 | |||||

Total Impairment | $ | 40,435 | $ | 20,372 | |||

Based on the changes in the business climate discussed above and continuing operating losses experienced during the three months ended March 31, 2016, June 30, 2016, and September 30, 2016, goodwill within the Teledrift and Production Technologies reporting units was tested for impairment. However, no impairments of goodwill were recorded based upon this testing.

Note 4 — Acquisitions

On July 27, 2016, the Company acquired 100% of the stock and interests in International Polymerics, Inc. (“IPI”) and related entities for $7.9 million in cash consideration, net of cash acquired, and 247,764 shares of the Company’s common stock. IPI is a U.S. based manufacturer of high viscosity guar gum and guar slurry for the oil and gas industry with a wide selection of stimulation chemicals.

On January 27, 2015, the Company acquired 100% of the assets of International Artificial Lift, LLC (“IAL”) for $1.3 million in cash consideration and 60,024 shares of the Company’s common stock. IAL specializes in the design, manufacturing and service of next-generation hydraulic pumping units that serve to increase and maximize production for oil and natural gas wells.

Note 5 — Supplemental Cash Flow Information

Supplemental cash flow information is as follows (in thousands):

Nine months ended September 30, | |||||||

2016 | 2015 | ||||||

Supplemental non-cash investing and financing activities: | |||||||

Value of common stock issued in acquisitions | $ | 3,268 | $ | 1,014 | |||

Exercise of stock options by common stock surrender | 50 | 1,126 | |||||

Supplemental cash payment information: | |||||||

Interest paid | $ | 1,459 | $ | 1,043 | |||

Income taxes paid, net of refunds | 1,663 | 3,044 | |||||

11

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 6 — Revenue

The Company differentiates revenue and cost of revenue based on whether the source of revenue is attributable to products, rentals, or services. Revenue and cost of revenue by source are as follows (in thousands):

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Revenue: | |||||||||||||||

Products | $ | 67,176 | $ | 76,555 | $ | 200,206 | $ | 217,237 | |||||||

Rentals | 4,168 | 7,574 | 11,366 | 28,146 | |||||||||||

Services | 2,335 | 3,813 | 6,715 | 11,963 | |||||||||||

$ | 73,679 | $ | 87,942 | $ | 218,287 | $ | 257,346 | ||||||||

Cost of revenue: | |||||||||||||||

Products | $ | 44,073 | $ | 49,520 | $ | 131,464 | $ | 145,387 | |||||||

Rentals | 1,379 | 3,387 | 3,704 | 13,315 | |||||||||||

Services | 2,018 | 2,160 | 5,730 | 6,283 | |||||||||||

Depreciation | 843 | 1,648 | 3,173 | 5,355 | |||||||||||

$ | 48,313 | $ | 56,715 | $ | 144,071 | $ | 170,340 | ||||||||

Note 7 — Inventories

Inventories are as follows (in thousands):

September 30, 2016 | December 31, 2015 | ||||||

Raw materials | $ | 33,724 | $ | 44,997 | |||

Work-in-process | 3,023 | 3,069 | |||||

Finished goods | 37,239 | 37,426 | |||||

Inventories | $ | 73,986 | $ | 85,492 | |||

During the three months ended March 31, 2016 and June 30, 2015, the Company recorded an inventory impairment of $16.6 million and $18.0 million, respectively (see Note 3).

Note 8 — Property and Equipment

Property and equipment are as follows (in thousands):

September 30, 2016 | December 31, 2015 | ||||||

Land | $ | 7,746 | $ | 7,145 | |||

Buildings and leasehold improvements | 51,495 | 34,351 | |||||

Machinery, equipment and rental tools | 65,798 | 85,611 | |||||

Equipment in progress | 4,113 | 12,304 | |||||

Furniture and fixtures | 2,736 | 2,749 | |||||

Transportation equipment | 7,554 | 7,462 | |||||

Computer equipment and software | 12,057 | 11,382 | |||||

Property and equipment | 151,499 | 161,004 | |||||

Less accumulated depreciation | (62,345 | ) | (69,091 | ) | |||

Property and equipment, net | $ | 89,154 | $ | 91,913 | |||

During the three months ended March 31, 2016 and June 30, 2015, the Company recorded a fixed asset impairment of $14.6 million and $2.3 million, respectively (see Note 3).

Depreciation expense, including expense recorded in cost of revenue, totaled $2.6 million and $3.2 million for the three months ended September 30, 2016 and 2015, respectively, and $8.0 million and $10.0 million for the nine months ended September 30, 2016 and 2015, respectively.

12

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 9 — Goodwill

Changes in the carrying value of goodwill for each reporting unit are as follows (in thousands):

Energy Chemistry Technologies | Consumer and Industrial Chemistry Technologies | Teledrift | Production Technologies | Total | |||||||||||||||

Balance at December 31, 2015 | $ | 36,318 | $ | 19,480 | $ | 15,333 | $ | 1,689 | $ | 72,820 | |||||||||

Addition upon acquisition of IPI | 862 | — | — | — | 862 | ||||||||||||||

Balance at September 30, 2016 | $ | 37,180 | $ | 19,480 | $ | 15,333 | $ | 1,689 | $ | 73,682 | |||||||||

Goodwill within the Teledrift and Production Technologies reporting units was tested for impairment during the three months ended March 31, 2016, June 30, 2016, and September 30, 2016. No impairments of goodwill were recognized during the three and nine months ended September 30, 2016 and 2015 (see Note 3).

Note 10 — Other Intangible Assets

Other intangible assets are as follows (in thousands):

September 30, 2016 | December 31, 2015 | ||||||||||||||

Cost | Accumulated Amortization | Cost | Accumulated Amortization | ||||||||||||

Finite-lived intangible assets: | |||||||||||||||

Patents and technology | $ | 19,406 | $ | 5,707 | $ | 20,960 | $ | 5,809 | |||||||

Customer lists | 42,287 | 12,192 | 52,607 | 14,640 | |||||||||||

Trademarks and brand names | 4,190 | 2,286 | 7,191 | 3,360 | |||||||||||

Total finite-lived intangible assets acquired | 65,883 | 20,185 | 80,758 | 23,809 | |||||||||||

Deferred financing costs | 2,787 | 1,166 | 1,665 | 858 | |||||||||||

Total amortizable intangible assets | 68,670 | $ | 21,351 | 82,423 | $ | 24,667 | |||||||||

Indefinite-lived intangible assets: | |||||||||||||||

Trademarks and brand names | 11,630 | 11,630 | |||||||||||||

Total other intangible assets | $ | 80,300 | $ | 94,053 | |||||||||||

Carrying value: | |||||||||||||||

Other intangible assets, net | $ | 58,949 | $ | 69,386 | |||||||||||

Finite-lived intangible assets acquired are amortized on a straight-line basis over two to 20 years. Amortization of finite-lived intangible assets acquired totaled $0.9 million and $1.2 million for the three months ended September 30, 2016 and 2015, respectively, and $3.1 million and $3.6 million for the nine months ended September 30, 2016 and 2015, respectively.

During the three months ended March 31, 2016, the Company recorded an impairment of finite-lived intangible assets of $9.2 million (see Note 3).

Amortization of deferred financing costs was $0.1 million and $0.1 million for the three months ended September 30, 2016 and 2015, respectively, and $0.3 million and $0.3 million for the nine months ended September 30, 2016 and 2015, respectively.

13

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 11 — Long-Term Debt and Credit Facility

Long-term debt is as follows (in thousands):

September 30, 2016 | December 31, 2015 | ||||||

Long-term debt: | |||||||

Borrowings under revolving credit facility | $ | 32,562 | $ | 25,148 | |||

Term loan | 10,000 | 25,398 | |||||

Total long-term debt | 42,562 | 50,546 | |||||

Less current portion of long-term debt | (34,562 | ) | (32,291 | ) | |||

Long-term debt, less current portion | $ | 8,000 | $ | 18,255 | |||

Credit Facility

On May 10, 2013, the Company and certain of its subsidiaries (the “Borrowers”) entered into an Amended and Restated Revolving Credit, Term Loan and Security Agreement (the “Credit Facility”) with PNC Bank, National Association (“PNC Bank”). The Company may borrow under the Credit Facility for working capital, permitted acquisitions, capital expenditures and other corporate purposes. Under terms of the Credit Facility, as amended, the Company has total borrowing availability of $65 million under a revolving credit facility and a term loan.

The Credit Facility is secured by substantially all of the Company’s domestic real and personal property, including accounts receivable, inventory, land, buildings, equipment and other intangible assets. The Credit Facility contains customary representations, warranties, and both affirmative and negative covenants. The Credit Facility restricts the payment of cash dividends on common stock and limits the amount that may be used to repurchase common stock and preferred stock. In the event of default, PNC Bank may accelerate the maturity date of any outstanding amounts borrowed under the Credit Facility.

Effective September 30, 2016, the Company entered into a Sixth Amendment to the Credit Facility which extended its term by two years through May 10, 2020 and set total borrowing capacity at $65 million. Initially, the Company (a) may borrow up to $55 million under a revolving credit facility and (b) has borrowed $10 million under a term loan. The revolving credit facility limit will increase by each term loan principal payment, therefore, total borrowing capacity will remain at $65 million throughout the term of the Credit Facility.

The Sixth Amendment to the Credit Facility contains financial covenants to maintain a fixed charge coverage ratio and a leverage ratio, as well as establishes an annual limit on capital expenditures. The fixed charge coverage ratio is the ratio of (a) adjusted earnings before interest, taxes, depreciation, and amortization (“EBITDA”) less cash taxes paid during the period to (b) all debt payments during such period. The fixed charge coverage ratio requirement begins for the quarter ending March 31, 2017 at 1.00 to 1.00 and increases to 1.10 to 1.00 for the year ending December 31, 2017 and thereafter. The leverage ratio (funded debt to adjusted EBITDA) requirement begins for the six months ending June 30, 2017 at not greater than 5.5 to 1.0 and reduces to not greater than 4.0 to 1.0 for the year ending March 31, 2018 and thereafter. The annual limit on capital expenditures is $20 million. Both the fixed charge coverage ratio and the annual limit on capital expenditures are affected if the undrawn availability of the revolving credit facility falls below $15 million.

The Credit Facility includes a provision, effective beginning in 2017, that 25% of EBITDA minus cash paid for taxes, dividends, debt payments, and unfunded capital expenditures, not to exceed $3.0 million for any year, be paid on the outstanding balance of the term loan within 60 days of the fiscal year end.

Each of the Company’s domestic and foreign subsidiaries is fully obligated for Credit Facility indebtedness as a Borrower or as a guarantor.

(a) Revolving Credit Facility

Under the revolving credit facility, the Company may initially borrow up to $55 million through May 10, 2020. This includes a sublimit of $10 million that may be used for letters of credit. The revolving credit facility limit will increase by each term principal payment. The revolving credit facility is secured by substantially all of the Company’s domestic and Canadian accounts receivable and inventory.

At September 30, 2016, eligible accounts receivable and inventory securing the revolving credit facility provided total borrowing capacity of $54.9 million under the revolving credit facility. Available borrowing capacity, net of outstanding borrowings, was $22.3 million at September 30, 2016.

14

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

The interest rate on advances under the revolving credit facility varies based on the fixed charge coverage ratio. Rates range (a) between PNC Bank’s base lending rate plus 1.5% to 2.0% or (b) between the London Interbank Offered Rate (LIBOR) plus 2.5% to 3.0%. PNC Bank’s base lending rate was 3.50% at September 30, 2016. The Company is required to pay a monthly facility fee of 0.25% per annum, on any unused amount under the commitment based on daily averages. At September 30, 2016, $32.6 million was outstanding under the revolving credit facility, with $2.6 million borrowed as base rate loans at an interest rate of 5.50% and $30.0 million borrowed as LIBOR loans at an interest rate of 3.78%.

Borrowing under the revolving credit agreement is classified as current debt as a result of the required lockbox arrangement and the subjective acceleration clause.

(b) Term Loan

The amount borrowed under the term loan was reset to $10 million effective as of September 30, 2016. Monthly principal payments of $0.2 million are required. The unpaid balance of the term loan is due May 10, 2020. Prepayments are permitted, and may be required in certain circumstances. Amounts repaid under the term loan will be added to the borrowing availability under the revolving credit facility. The term loan is secured by substantially all of the Company’s domestic land, buildings, equipment, and other intangible assets.

The interest rate on the term loan varies based on the fixed charge coverage ratio. Rates range (a) between PNC Bank’s base lending rate plus 2.25% to 2.75% or (b) between LIBOR plus 3.25% to 3.75%. At September 30, 2016, $10.0 million was outstanding under the term loan, with $1.0 million borrowed as base rate loans at an interest rate of 6.25% and $9.0 million borrowed as LIBOR loans at an interest rate of 4.28%.

Note 12 — (Loss) Earnings Per Share

Basic (loss) earnings per common share is calculated by dividing net (loss) income by the weighted average number of common shares outstanding for the period. Diluted (loss) earnings per common share is calculated by dividing net (loss) income by the weighted average number of common shares outstanding combined with dilutive common share equivalents outstanding, if the effect is dilutive.

Potentially dilutive securities were excluded from the calculation of diluted loss per share for the three months ended September 30, 2016 and the three and nine months ended September 30, 2016 and 2015, since including them would have an anti-dilutive effect on loss per share due to the net loss incurred during the period. Securities convertible into shares of common stock that were not considered in the diluted loss per share calculations were 0.7 million stock options and 0.8 million restricted stock units for the three and nine months ended September 30, 2016 and 0.8 million stock options and 0.4 million restricted stock units for the nine months ended September 30, 2015.

Basic and diluted (loss) earnings per common share are as follows (in thousands, except per share data):

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Net (loss) income - Basic and Diluted | $ | (2,746 | ) | $ | 1,975 | $ | (35,211 | ) | $ | (12,087 | ) | ||||

Weighted average common shares outstanding - Basic | 56,899 | 54,578 | 55,523 | 54,430 | |||||||||||

Assumed conversions: | |||||||||||||||

Incremental common shares from stock options | — | 345 | — | — | |||||||||||

Incremental common shares from restricted stock units | — | 24 | — | — | |||||||||||

Weighted average common shares outstanding - Diluted | 56,899 | 54,947 | 55,523 | 54,430 | |||||||||||

Basic (loss) earnings per common share | $ | (0.05 | ) | $ | 0.04 | $ | (0.63 | ) | $ | (0.22 | ) | ||||

Diluted (loss) earnings per common share | $ | (0.05 | ) | $ | 0.04 | $ | (0.63 | ) | $ | (0.22 | ) | ||||

15

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 13 — Fair Value Measurements

Fair value is defined as the amount that would be received for selling an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The Company categorizes financial assets and liabilities into the three levels of the fair value hierarchy. The hierarchy prioritizes the inputs to valuation techniques used to measure fair value and bases categorization within the hierarchy on the lowest level of input that is available and significant to the fair value measurement.

• | Level 1 — Quoted prices in active markets for identical assets or liabilities; |

• | Level 2 — Observable inputs other than Level 1, such as quoted prices for similar assets or liabilities, quoted prices in markets that are not active, or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities; and |

• | Level 3 — Significant unobservable inputs that are supported by little or no market activity or that are based on the reporting entity’s assumptions about the inputs. |

Fair Value of Other Financial Instruments

The carrying amounts of certain financial instruments, including cash and cash equivalents, accounts receivable, accounts payable, and accrued expenses, approximate fair value due to the short-term nature of these accounts. The Company had no cash equivalents at September 30, 2016, or December 31, 2015.

The carrying value and estimated fair value of the Company’s long-term debt are as follows (in thousands):

September 30, 2016 | December 31, 2015 | ||||||||||||||

Carrying Value | Fair Value | Carrying Value | Fair Value | ||||||||||||

Term loan | $ | 10,000 | $ | 10,000 | $ | 25,398 | $ | 25,398 | |||||||

Borrowings under revolving credit facility | 32,562 | 32,562 | 25,148 | 25,148 | |||||||||||

The carrying value of the term loan and borrowings under the revolving credit facility approximate their fair value because the interest rates are variable.

Assets Measured at Fair Value on a Nonrecurring Basis

The Company’s non-financial assets, including property and equipment, goodwill, and other intangible assets are measured at fair value on a non-recurring basis and are subject to fair value adjustment in certain circumstances. During the three months ended March 31, 2016, the Company recorded an impairment of $14.6 million for property and equipment and $9.2 million for other intangible assets (see Note 3). During the three months ended June 30, 2015, the Company recorded an impairment of $2.3 million for property and equipment (see Note 3). Loss on impairment is reported in operating expenses. No impairments of property and equipment or other intangible assets were recognized during the three months ended September 30, 2016, and no impairments of other intangible assets were recognized during the three and nine months ended September 30, 2015. No impairments of goodwill were recognized during the three and nine months ended September 30, 2016 and 2015.

Note 14 — Income Taxes

During the year ended December 31, 2015, the Company restructured its legal entities such that there will be only one U.S. tax filing group filing a single U.S. consolidated federal income tax return beginning in 2016. Prior to 2016, the Company’s corporate organizational structure required the filing of two separate consolidated U.S. Federal income tax returns. Taxable income of one group could not be offset by tax attributes, including net operating losses, of the other group.

16

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

A reconciliation of the U.S. federal statutory tax rate to the Company’s effective income tax rate is as follows:

Three months ended September 30, | Nine months ended September 30, | ||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||

U.S. federal statutory tax rate | (35.0 | )% | 35.0 | % | (35.0 | )% | (35.0 | )% | |||

State income taxes, net of federal benefit | 3.8 | 5.7 | (0.7 | ) | 1.8 | ||||||

Non-U.S. income taxed at different rates | (12.6 | ) | (29.1 | ) | (1.2 | ) | (4.2 | ) | |||

Non-deductible expenses | — | 0.2 | — | 2.4 | |||||||

Domestic production activities deduction | — | 3.6 | — | — | |||||||

Other | (0.8 | ) | 1.4 | 0.9 | 0.1 | ||||||

Effective income tax rate | (44.6 | )% | 16.8 | % | (36.0 | )% | (34.9 | )% | |||

Fluctuations in effective tax rates have historically been impacted by permanent tax differences with no associated income tax impact, changes in state apportionment factors, including the effect on state deferred tax assets and liabilities, and benefits of non-U.S. income taxed at lower rates. Changes in the effective tax rate during the three months ended September 30, 2015, included the Company no longer qualifying for the domestic production activities deduction due to its pretax loss position.

Deferred taxes are presented in the balance sheets as follows (in thousands):

September 30, 2016 | December 31, 2015 | ||||||

Current deferred tax assets | $ | 2,352 | $ | 2,649 | |||

Non-current deferred tax assets | — | 17,229 | |||||

Non-current deferred tax liabilities | (1,205 | ) | (23,823 | ) | |||

Net deferred tax assets (liabilities) | $ | 1,147 | $ | (3,945 | ) | ||

Note 15 — Common Stock

The Company’s Certificate of Incorporation, as amended November 9, 2009, authorizes the Company to issue up to 80 million shares of common stock, par value $0.0001 per share, and 100,000 shares of one or more series of preferred stock, par value $0.0001 per share.

A reconciliation of changes in shares of the Company’s common stock issued during the nine months ended September 30, 2016 is as follows:

Shares issued at December 31, 2015 | 56,220,214 | |

Issued in sale of common stock | 2,450,339 | |

Issued to purchase IPI | 247,764 | |

Issued as restricted stock award grants | 572,240 | |

Issued upon exercise of stock options | 114,112 | |

Shares issued at September 30, 2016 | 59,604,669 | |

Stock Repurchase Program

In November 2012, the Company’s Board of Directors authorized the repurchase of up to $25 million of the Company’s common stock. Repurchases may be made in the open market or through privately negotiated transactions. During the three and nine months ended September 30, 2016, the Company did not repurchase any shares of its outstanding common stock. During the three months ended September 30, 2015, the Company repurchased 2,404 shares of its outstanding common stock on the open market at an average price of $16.44 per share, inclusive of transaction costs. During the nine months ended September 30, 2015, the Company repurchased a total of 549,723 shares of its outstanding common stock on the open market at a cost of $7.3 million, inclusive of transaction costs, or an average price of $13.28 per share.

In June 2015, the Company’s Board of Directors authorized the repurchase of up to an additional $50 million of the Company’s common stock. Repurchases may be made in the open market or through privately negotiated transactions. Through September 30, 2016, the Company has not repurchased any of its common stock under this authorization.

17

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

As of September 30, 2016, the Company has $54.9 million remaining under its share repurchase programs. A covenant under the Company’s Credit Facility limits the amount that may be used to repurchase the Company’s common stock. As of September 30, 2016, this covenant limits additional share repurchases to $4.9 million.

Note 16 — Business Segment, Geographic and Major Customer Information

Segment Information

Operating segments are defined as components of an enterprise for which separate financial information is available that is regularly evaluated by chief operating decision-makers in deciding how to allocate resources and assess performance. The operations of the Company are categorized into four reportable segments: Energy Chemistry Technologies, Consumer and Industrial Chemistry Technologies, Drilling Technologies, and Production Technologies.

• | Energy Chemistry Technologies designs, develops, manufactures, packages, and markets specialty chemistries used in oil and natural gas well drilling, cementing, completion, and stimulation. In addition, the Company’s chemistries are used in specialized enhanced and improved oil recovery markets. Activities in this segment also include construction and management of automated material handling facilities and management of loading facilities and blending operations for oilfield services companies. |

• | Consumer and Industrial Chemistry Technologies designs, develops, and manufactures products that are sold to companies in the flavor and fragrance industries and the specialty chemical industry. These technologies are used by beverage and food companies, fragrance companies, and companies providing household and industrial cleaning products. |

• | Drilling Technologies rents, sells, inspects, manufactures, and markets downhole drilling equipment used in energy, mining, and industrial drilling activities. |

• | Production Technologies assembles and markets production-related equipment, including the Petrovalve® product line of rod pump components, hydraulic pumping units, electric submersible pumps, gas separators, valves, and services that support natural gas and oil production activities. |

The Company evaluates performance based upon a variety of criteria. The primary financial measure is segment operating income. Various functions, including certain sales and marketing activities and general and administrative activities, are provided centrally by the corporate office. Costs associated with corporate office functions, other corporate income and expense items, and income taxes are not allocated to reportable segments.

Summarized financial information of the reportable segments is as follows (in thousands):

As of and for the three months ended September 30, | Energy Chemistry Technologies | Consumer and Industrial Chemistry Technologies | Drilling Technologies | Production Technologies | Corporate and Other | Total | |||||||||||||||||

2016 | |||||||||||||||||||||||

Net revenue from external customers | $ | 45,030 | $ | 19,306 | $ | 7,198 | $ | 2,145 | $ | — | $ | 73,679 | |||||||||||

Gross profit | 18,180 | 4,174 | 2,908 | 104 | — | 25,366 | |||||||||||||||||

Income (loss) from operations | 6,196 | 2,433 | (924 | ) | (1,118 | ) | (10,882 | ) | (4,295 | ) | |||||||||||||

Depreciation and amortization | 1,582 | 567 | 599 | 220 | 581 | 3,549 | |||||||||||||||||

Total assets | 172,456 | 101,921 | 67,655 | 23,235 | 17,273 | 382,540 | |||||||||||||||||

Capital expenditures | 2,005 | 148 | 234 | 51 | 227 | 2,665 | |||||||||||||||||

2015 | |||||||||||||||||||||||

Net revenue from external customers | $ | 60,181 | $ | 13,867 | $ | 10,812 | $ | 3,082 | $ | — | $ | 87,942 | |||||||||||

Gross profit | 24,257 | 3,082 | 3,302 | 586 | — | 31,227 | |||||||||||||||||

Income (loss) from operations | 14,283 | 1,728 | (2,614 | ) | (823 | ) | (9,797 | ) | 2,777 | ||||||||||||||

Depreciation and amortization | 1,200 | 548 | 2,038 | 212 | 435 | 4,433 | |||||||||||||||||

Total assets | 152,430 | 90,948 | 110,872 | 26,564 | 20,131 | 400,945 | |||||||||||||||||

Capital expenditures | 1,467 | 18 | — | 107 | 523 | 2,115 | |||||||||||||||||

18

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

As of and for the nine months ended September 30, | Energy Chemistry Technologies | Consumer and Industrial Chemistry Technologies | Drilling Technologies | Production Technologies | Corporate and Other | Total | |||||||||||||||||

2016 | |||||||||||||||||||||||

Net revenue from external customers | $ | 133,094 | $ | 59,133 | $ | 20,026 | $ | 6,034 | $ | — | $ | 218,287 | |||||||||||

Gross profit | 54,609 | 13,256 | 6,150 | 201 | — | 74,216 | |||||||||||||||||

Income (loss) from operations | 21,793 | 8,508 | (43,493 | ) | (7,810 | ) | (32,031 | ) | (53,033 | ) | |||||||||||||

Depreciation and amortization | 4,063 | 1,685 | 3,027 | 660 | 1,634 | 11,069 | |||||||||||||||||

Total assets | 172,456 | 101,921 | 67,655 | 23,235 | 17,273 | 382,540 | |||||||||||||||||

Capital expenditures | 8,704 | 494 | 717 | 286 | 1,420 | 11,621 | |||||||||||||||||

2015 | |||||||||||||||||||||||

Net revenue from external customers | $ | 163,296 | $ | 42,808 | $ | 41,840 | $ | 9,402 | $ | — | $ | 257,346 | |||||||||||

Gross profit | 60,784 | 10,914 | 13,396 | 1,912 | — | 87,006 | |||||||||||||||||

Income (loss) from operations | 32,995 | 6,792 | (24,551 | ) | (2,958 | ) | (29,398 | ) | (17,120 | ) | |||||||||||||

Depreciation and amortization | 3,578 | 1,649 | 6,575 | 535 | 1,276 | 13,613 | |||||||||||||||||

Total assets | 152,430 | 90,948 | 110,872 | 26,564 | 20,131 | 400,945 | |||||||||||||||||

Capital expenditures | 5,910 | 46 | 2,744 | 883 | 1,495 | 11,078 | |||||||||||||||||

Geographic Information

Revenue by country is based on the location where services are provided and products are used. No individual country other than the United States (“U.S.”) accounted for more than 10% of revenue. Revenue by geographic location is as follows (in thousands):

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

U.S. | $ | 58,183 | $ | 73,796 | $ | 169,991 | $ | 211,242 | |||||||

Other countries | 15,496 | 14,146 | 48,296 | 46,104 | |||||||||||

Total | $ | 73,679 | $ | 87,942 | $ | 218,287 | $ | 257,346 | |||||||

Long-lived assets held in countries other than the U.S. are not considered material to the consolidated financial statements.

Major Customers

Revenue from major customers, as a percentage of consolidated revenue, is as follows:

Three months ended September 30, | Nine months ended September 30, | ||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||

Customer A | 12.9 | % | 12.8 | % | 11.9 | % | 11.7 | % | |||

Customer B | 10.9 | % | 11.3 | % | 15.8 | % | 14.3 | % | |||

Customer C | * | 11.6 | % | * | * | ||||||

Over 95% of the revenue from these customers was for sales in the Energy Chemistry Technologies segment.

Note 17 — Commitments and Contingencies

Class Action Litigation

In November 2015, four putative securities class action lawsuits were filed in the United States District Court for the Southern District of Texas against the Company and certain of its officers. The lawsuits have been consolidated into a single case, and an amended complaint has been filed. The amended complaint asserts that the Company made false and/or misleading statements, as well as failed to disclose material adverse facts about the Company’s business, operations, and prospects. The complaint seeks an award of damages in an unspecified amount on behalf of a putative class consisting of persons who purchased the Company’s common stock between October 23, 2014 and November 9, 2015, inclusive.

19

FLOTEK INDUSTRIES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

In January 2016, three derivative lawsuits were filed, two in the District Court of Harris County, Texas (which have since been consolidated into one case) and one in the United States District Court for the Southern District of Texas, on behalf of the Company against certain of its officers and its current directors. The lawsuits allege violations of law, breaches of fiduciary duty, and unjust enrichment against the defendants.

The Company believes the class action lawsuit and the derivative lawsuits are without merit, and it intends to vigorously defend against all claims asserted. Discovery has not yet commenced. At this time, the Company is unable to reasonably estimate the outcome of this litigation.

In addition, the U.S. Securities and Exchange Commission has opened an inquiry related to similar issues to those raised in the above-described litigation.

Other Litigation

The Company is subject to routine litigation and other claims that arise in the normal course of business. Management is not aware of any pending or threatened lawsuits or proceedings that are expected to have a material effect on the Company’s financial position, results of operations or liquidity.

Concentrations and Credit Risk

The majority of the Company’s revenue is derived from the oil and gas industry. Customers include major oilfield services companies, major integrated oil and natural gas companies, independent oil and natural gas companies, pressure pumping service companies, and state-owned national oil companies. This concentration of customers in one industry increases credit and business risks.

The Company is subject to concentrations of credit risk within trade accounts receivable, as the Company does not generally require collateral as support for trade receivables. In addition, the majority of the Company’s cash is maintained at a major financial institution and balances often exceed insurable amounts.

20

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements

This Quarterly Report on Form 10-Q (“Quarterly Report”), and in particular, Part I, Item 2 — “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” contains “forward-looking statements” within the meaning of the safe harbor provisions, 15 U.S.C. § 78u-5, of the Private Securities Litigation Reform Act of 1995 (“Reform Act”). Forward-looking statements are not historical facts, but instead represent Flotek Industries, Inc.’s (“Flotek” or “Company”) current assumptions and beliefs regarding future events, many of which, by their nature, are inherently uncertain and outside the Company’s control. Such statements include estimates, projections, and statements related to the Company’s business plan, objectives, expected operating results, and assumptions upon which those statements are based. The forward-looking statements contained in this Quarterly Report are based on information available as of the date of this Quarterly Report.

The forward-looking statements relate to future industry trends and economic conditions, forecast performance or results of current and future initiatives and the outcome of contingencies and other uncertainties that may have a significant impact on the Company’s business, future operating results and liquidity. These forward-looking statements generally are identified by words including, but not limited to, “anticipate,” “believe,” “estimate,” “continue,” “intend,” “expect,” “plan,” “forecast,” “project,” and similar expressions, or future-tense or conditional constructions such as “will,” “may,” “should,” “could,” etc. The Company cautions that these statements are merely predictions and are not to be considered guarantees of future performance. Forward-looking statements are based upon current expectations and assumptions that are subject to risks and uncertainties that can cause actual results to differ materially from those projected, anticipated, or implied.

A detailed discussion of potential risks and uncertainties that could cause actual results and events to differ materially from forward-looking statements is included in Part I, Item 1A — “Risk Factors” of the Annual Report on Form 10-K for the year ended December 31, 2015 (“Annual Report”) and periodically in subsequent reports filed with the Securities and Exchange Commission (“SEC”). The Company has no obligation to publicly update or revise any forward-looking statements, whether as a result of new information or future events, except as required by law.

Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) should be read in conjunction with the unaudited condensed consolidated financial statements and the related notes thereto of this Quarterly Report, as well as the Annual Report. Phrases such as “Company,” “we,” “our,” and “us” refer to Flotek Industries, Inc. and its subsidiaries.

Executive Summary

Flotek is a global diversified, technology-driven company that develops and supplies oilfield products, services, and equipment to the oil, gas, and mining industries, and high value compounds to companies that make cleaning products, cosmetics, food and beverages, and other products that are sold in the consumer and industrial markets.

The Company’s oilfield businesses include specialty chemistries and logistics, downhole drilling tools, and production-related tools. Flotek’s technologies enable customers to drill wells more efficiently, increase well production, and decrease well operating costs. The Company also provides automated bulk material handling, loading facilities, and blending capabilities. The Company sources citrus oil domestically and internationally and is one of the largest processors of citrus oil in the world. Products produced from processed citrus oil include (1) high value compounds used as additives by companies in the flavors and fragrances markets and (2) environmentally friendly chemistries for use in numerous industries around the world, including the oil and gas (“O&G”) industry.

Flotek operates in over 20 domestic and international markets, including the Gulf Coast, Southwest, West Coast, Rocky Mountains, Northeastern, and Mid-Continental regions of the United States (“U.S.”), Canada, Mexico, Central America, South America, Europe, Africa, Middle East, and Asia-Pacific. Customers include major integrated O&G companies, oilfield services companies, independent O&G companies, pressure-pumping service companies, national and state-owned oil companies, and international supply chain management companies. The Company also serves customers who purchase non-energy-related citrus oil and related products, including household and commercial cleaning product companies, fragrance and cosmetic companies, and food manufacturing companies.

21

The operations of the Company are categorized into four reportable segments: Energy Chemistry Technologies, Consumer and Industrial Chemistry Technologies, Drilling Technologies, and Production Technologies.

• | Energy Chemistry Technologies designs, develops, manufactures, packages, and markets specialty chemistries used in O&G well drilling, cementing, completion, and stimulation. In addition, the Company’s chemistries are used in specialized enhanced and improved oil recovery markets (“EOR” or “IOR”). Activities in this segment also include construction and management of automated material handling facilities and management of loading facilities and blending operations for oilfield services companies. |

• | Consumer and Industrial Chemistry Technologies designs, develops, and manufactures products that are sold to companies in the flavor and fragrance industries and specialty chemical industry. These technologies are used by beverage and food companies, fragrance companies, and companies providing household and industrial cleaning products. |

• | Drilling Technologies rents, sells, inspects, manufactures, and markets downhole drilling equipment used in energy, mining, and industrial drilling activities. |

• | Production Technologies assembles and markets production-related equipment, including the Petrovalve® product line of rod pump components, hydraulic pumping units (“HPU”), electric submersible pumps (“ESP”), gas separators, valves, and services that support natural gas and oil production activities. |

Market Conditions

The Company’s success is sensitive to a number of factors, which include, but are not limited to, drilling and well completion activity, customer demand for its advanced technology products, market prices for raw materials, and governmental actions.

Drilling and well completion activity levels are influenced by a number of factors, including the number of rigs in operation, the geographical areas of rig activity, and drill rig efficiency (rig days required per well). Additional factors that influence the level of drilling and well completion activity include:

• | Historical, current, and anticipated future O&G prices, |

• | Federal, state, and local governmental actions that may encourage or discourage drilling activity, |

• | Customers’ strategies relative to capital funds allocations, |

• | Weather conditions, and |

• | Technological changes to drilling methods and economics. |

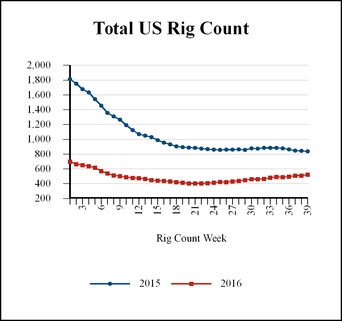

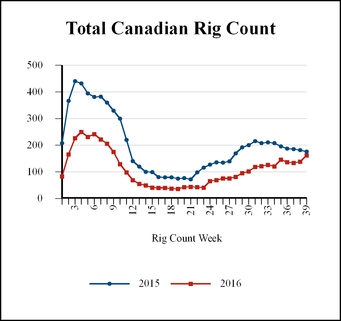

Historical North American drilling activity is reflected in “TABLE A” on the following page.

Customers’ demand for advanced technology products and services provided by the Company are dependent on their recognition of the value of:

• | Chemistries that improve the economics of their O&G operations, |

• | Drilling products that improve drilling operations and efficiencies, |

• | Chemistries that are economically viable, socially responsible, and ecologically sound, and |

• | Production technologies that improve production and production efficiencies in maturing wells. |

Market prices for commodities, including citrus oils and guar, can be influenced by:

• | Historical, current, and anticipated future production levels of the global citrus (primarily orange) and guar crops, |

• | Weather related risks, |

• | Health and condition of citrus trees and guar plants (e.g., disease and pests), and |

• | International competition and pricing pressures resulting from natural and artificial pricing influences. |

Governmental actions may restrict the future use of hazardous chemicals, including, but not limited to, the following industrial applications:

• | O&G drilling and completion operations, |

• | O&G production operations, and |

• | Non-O&G industrial solvents. |

22

TABLE A | Three months ended September 30, | Nine months ended September 30, | |||||||||||||||

2016 | 2015 | % Change | 2016 | 2015 | % Change | ||||||||||||

Average North American Active Drilling Rigs | |||||||||||||||||

U.S. | 479 | 866 | (44.7 | )% | 482 | 1,059 | (54.5 | )% | |||||||||

Canada | 121 | 190 | (36.3 | )% | 112 | 200 | (44.0 | )% | |||||||||

Total | 600 | 1,056 | (43.2 | )% | 594 | 1,259 | (52.8 | )% | |||||||||

Average U.S. Active Drilling Rigs by Type | |||||||||||||||||

Vertical | 62 | 123 | (49.6 | )% | 58 | 152 | (61.8 | )% | |||||||||

Horizontal | 372 | 659 | (43.6 | )% | 376 | 805 | (53.3 | )% | |||||||||

Directional | 45 | 84 | (46.4 | )% | 48 | 102 | (52.9 | )% | |||||||||

Total | 479 | 866 | (44.7 | )% | 482 | 1,059 | (54.5 | )% | |||||||||

Average North American Drilling Rigs by Product | |||||||||||||||||

Oil | 452 | 745 | (39.3 | )% | 440 | 906 | (51.4 | )% | |||||||||

Natural Gas | 148 | 311 | (52.4 | )% | 154 | 353 | (56.4 | )% | |||||||||

Total | 600 | 1,056 | (43.2 | )% | 594 | 1,259 | (52.8 | )% | |||||||||

Source: Rig counts are per Baker Hughes, Inc. (www.bakerhughes.com). Rig counts are the averages of the weekly rig count activity.

During the three and nine months ended September 30, 2016, total average North American active drilling rig count decreased 43.2% and 52.8%, respectively, when compared to the same periods of 2015. Average North American oil drilling rig activity decreased by 39.3% and 51.4% for the three and nine months ended September 30, 2016, respectively, when compared to the same periods of 2015. Average North American natural gas drilling rig count decreased by 52.4% and 56.4% for the three and nine months ended September 30, 2016, respectively, compared to the same periods of 2015. Sequentially, total average North American active drilling rig count increased by 27.7% when compared to the second quarter of 2016.

Average U.S. rig activity decreased by 44.7% and 54.5% for the three and nine months ended September 30, 2016, respectively, compared to the same periods of 2015, and sequentially, increased by 13.5% when compared to the second quarter of 2016. Average Canadian rig count decreased by 36.3% and 44.0% for the three and nine months ended September 30, 2016, respectively, compared to the same periods of 2015.

According to data collected by the U.S. Energy Information Administration (“EIA”), completions in the seven most prolific areas in the lower 48 states decreased 41.4% and 48.0% for the three and nine months ended September 30, 2016, respectively, when compared to the same periods of 2015. Sequentially, completions decreased 1.3% when compared to the second quarter of 2016.

23

Company Outlook

After a continuous decline in North American drilling rig activity beginning in mid-2014, the market began to gradually recover in the second quarter of 2016. Although a gradual recovery appears to be underway, the level of drilling and completion activity is still depressed compared to historical levels and the outlook for continued improvement in industry activity is uncertain. The Company expects North American oilfield activity to remain depressed throughout the remainder of 2016 and into the first half of 2017. Although the Company has seen demand for its oil and gas related products and services in North America impacted by these industry conditions, the Company continues to aggressively market its oil and gas based products and services including its Complex nano-Fluid® (“CnF®”) and other completion chemistries, Teledrift® product line, Stemulator® product line, and the growing line of production technologies, and the Company expects to see increased market acceptance of these product lines.

During the third quarter of 2016, the Company continued to successfully promote the efficacy of its CnF® chemistries resulting in a 14% decrease in CnF® sales volumes compared to the third quarter of 2015, despite a 43% year over year decline in North American general oilfield activity. Third quarter 2016 CnF® volumes remained flat compared to the second quarter of 2016, in line with well completion activity as measured by industry surveys. The Company expects to continue strong performance relative to market activity by continuing to demonstrate the efficacy of its CnF® chemistries through comparative analysis of wells with and without CnF® chemistries, field validation results conducted by E&P companies, and the continuation of its direct-to-operator sales program known as the Flotek Store™. Whether operators purchase directly from Flotek or continue to purchase from oilfield distribution and service companies, E&P operators are benefiting from increased price transparency and a more direct relationship with Flotek’s technical expertise and supply chain. In July 2016, the Company acquired 100% of the stock and interests in International Polymerics, Inc. (“IPI”) and related entities, a U.S. based manufacturer of high viscosity guar gum and guar slurry. The IPI business is being integrated into the Company’s Energy Chemistry Technologies segment as an important part of the Company’s expanding line of polymer based chemistries.