Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - Advanced Disposal Services, Inc. | a2229759zex-23_2.htm |

| EX-3.1 - EX-3.1 - Advanced Disposal Services, Inc. | a2229759zex-3_1.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on September 26, 2016

Registration No. 333-206508

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 7

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Advanced Disposal Services, Inc.

(Exact name of registrant as specified in its charter)

(formerly known as ADS Waste Holdings, Inc.)

| Delaware (State or other jurisdiction of incorporation or organization) |

4953 (Primary Standard Industrial Classification Code Number) |

90-0875845 (I.R.S. Employer Identification Number) |

90 Fort Wade Road

Ponte Vedra, Florida 32081

(904) 737-7900

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant's Principal Executive Offices)

Michael K. Slattery, Esq.

General Counsel

Advanced Disposal Services, Inc.

90 Fort Wade Road

Ponte Vedra, FL 32081

(904) 737-7900

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agents For Service)

| With a copy to: | ||

Richard B. Alsop Jonathan M. DeSantis Shearman & Sterling LLP 599 Lexington Avenue New York, New York 10022-6069 (212) 848-4000 |

Kirk A. Davenport II Erika L. Weinberg Latham & Watkins LLP 885 Third Avenue New York, New York 10022-4834 (212) 906-1200 |

|

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price (1) (2) |

Amount of Registration Fee (3) |

||

|---|---|---|---|---|

| Common stock, par value $0.01 per share | $465,000,000 | $46,825.50 | ||

- (1)

- Estimated

solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. Includes

offering price of additional shares that the underwriters have the option to purchase. See "Underwriting."

- (2)

- Includes

shares of common stock subject to the underwriters' option to purchase additional shares of common stock.

- (3)

- The registrant previously paid a registration fee of $53,170.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, Dated September 26, 2016

Advanced Disposal Services, Inc.

19,250,000 Shares

Common Stock

This is Advanced Disposal Services, Inc.'s initial public offering. We are selling 19,250,000 shares of our common stock. We expect the public offering price to be between $18.00 and $21.00. Prior to this offering, there has been no public market for our common stock. Our common stock has been approved for listing on the New York Stock Exchange under the symbol ADSW.

After the completion of this offering, affiliates of Highstar Capital LP may continue to own a majority of the voting power of shares eligible to vote in the election of our directors. As a result, we may be a "controlled company" within the meaning of the corporate governance standards of the New York Stock Exchange. See "Risk Factors" and "Management—Controlled Company."

Investing in our common stock involves risks. See "Risk Factors" beginning on page 20 to read about factors you should consider before buying our common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or the accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| |

Price to Public |

Underwriting Discounts and Commissions (1) |

Proceeds, before expenses, to the Company |

|||

|---|---|---|---|---|---|---|

Per Share |

$ | $ | $ | |||

Total |

$ | $ | $ |

- (1)

- The underwriters will receive compensation in addition to the underwriting discount. See "Underwriting."

The underwriters have the option to purchase up to an additional 2,887,500 shares from the Company, at the initial public offering price, less the underwriting discounts and commissions.

The underwriters expect to deliver the shares of common stock to purchasers on or about , 2016.

| Deutsche Bank Securities | Credit Suisse | Barclays |

| UBS Investment Bank | ||||||

BofA Merrill Lynch |

Macquarie Capital |

Morgan Stanley |

Stifel |

|||

| SMBC Nikko | First Analysis Securities Corp. |

Prospectus dated , 2016

You should rely only upon the information contained in this prospectus or in any free writing prospectus prepared by or on behalf of us. None of us or the underwriters have authorized anyone to provide you with additional or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. If you are in a jurisdiction where offers to sell, or solicitations of offers to purchase, shares of our common stock are unlawful, or if you are a person to whom it is unlawful to direct these types of activities, then the offer presented in this document does not extend to you. You should assume the information appearing in this prospectus is accurate only as of the respective dates of such information. Our business, financial condition, results of operations, and prospects may have changed since those dates.

Except where the context requires otherwise, references in this prospectus to "Advanced Disposal," "Company," "we," "us," and "our" refer to Advanced Disposal Services, Inc., together with its consolidated subsidiaries. On January 27, 2016, ADS Waste Holdings, Inc. was renamed Advanced Disposal Services, Inc. References to "Parent" refer to Advanced Disposal Waste Holdings Corp. In this prospectus, when we refer to our fiscal years, we say "fiscal" and the year number, as in "fiscal 2015," which refers to our fiscal year ended December 31, 2015. Except where otherwise noted, statistical data of the Company is as of June 30, 2016.

i

Market, Industry and Other Data

This prospectus includes estimates regarding market and industry data and forecasts, which are based on publicly available information, industry publications and surveys, reports from government agencies and reports by market research firms, including IBISWorld, Waste Business Journal, Woods & Poole, Spears & Associates, the National Association of Home Builders and the U.S. Census Bureau. We have not independently verified market and industry data provided by any of these or any other third-party sources referred to in this prospectus, although we believe such market and industry data included in this prospectus is reliable. This information cannot always be verified with complete certainty due to the limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in surveys of market size.

Management estimates are derived from the information and data referred to above, as well as our internal research, calculations and assumptions made by us based on our analysis of such information and data and our knowledge of our industry and markets, which we believe to be reasonable, although they have not been independently verified. While we believe that the market position information included in this prospectus is generally reliable, such information is inherently imprecise. Assumptions, expectations and estimates of our future performance and the future performance of the industry in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in "Risk Factors" and "Forward-Looking Statements." These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us.

ii

This summary highlights some of the information contained in this prospectus. This summary may not contain all of the information that may be important to you. For a more complete understanding of our business and this offering, we encourage you to read this entire prospectus, including "Risk Factors," "Management's Discussion and Analysis of Financial Condition and Results of Operations," the more detailed information regarding our Company and the common stock being sold in this offering, as well as our consolidated financial statements and the related notes appearing elsewhere in this prospectus, before deciding to invest in our common stock. Some of the statements in this prospectus constitute forward-looking statements. See "Forward-Looking Statements."

Our Company

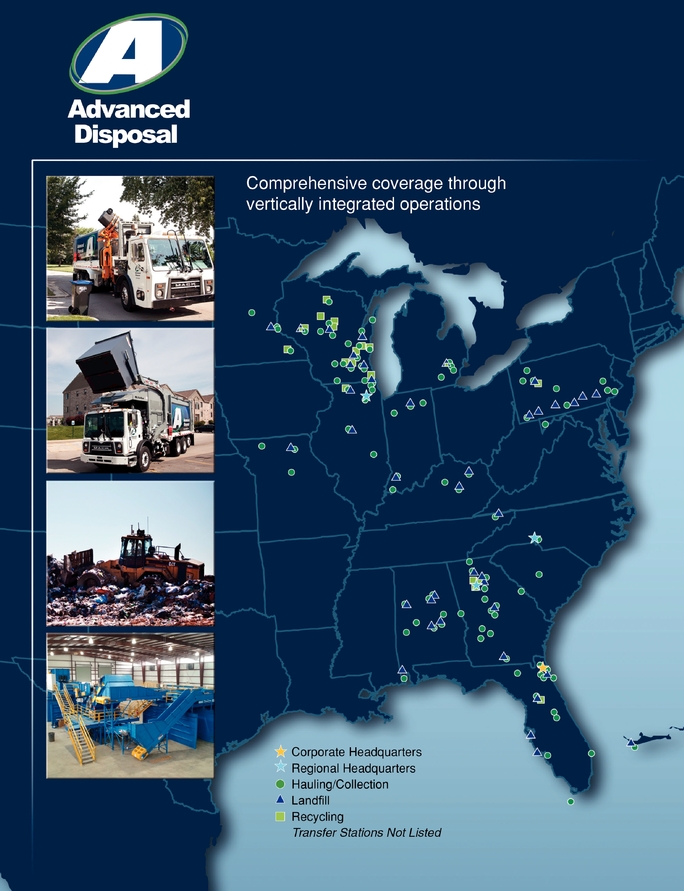

We are a leading integrated provider of non-hazardous solid waste collection, transfer, recycling and disposal services operating primarily in secondary markets or under exclusive arrangements with municipalities. We have a presence in 16 states across the Midwest, South and East regions of the United States, serving approximately 2.8 million residential and 221,000 commercial and industrial ("C&I") customers through our extensive network of 92 collection operations, 72 transfer stations, 21 owned or operated recycling facilities and 39 owned or operated landfills. We seek to drive financial performance in markets in which we own or operate a landfill or in certain disposal-neutral markets, where the landfill is owned by our municipal customer. In markets in which we own or operate a landfill, we aim to create and maintain vertically integrated operations through which we manage a majority of our customers' waste from the point of collection through the point of disposal, a process we refer to as internalization. By internalizing a majority of the waste in these markets, we are able to deliver high quality customer service while also ensuring a stable revenue stream and maximizing profitability and cash flow from operations. In disposal-neutral markets, we focus selectively on opportunities where we can negotiate exclusive arrangements with our municipal customers, facilitating highly-efficient and profitable collection operations with lower capital requirements.

Geographically, we focus our business principally in secondary, or less densely populated non-urban, markets where the presence of large national providers is generally more limited. We also compete selectively in primary, or densely populated urban, markets where we can capitalize on opportunities for vertical integration through our high-quality transfer and disposal infrastructure and where we can benefit from highly-efficient collection route density. Through our disciplined focus on secondary markets and on markets with favorable disposal

1

characteristics, we are able to maximize customer retention and benefit from a higher and more stable pricing environment.

We have historically generated consistent revenue growth across economic cycles. To continue to drive growth, we are focused on a number of key areas, including: municipal contract wins, new customer additions, disciplined pricing and expansion into additional geographies and markets with favorable dynamics and demographic trends. We have established a systematic and replicable approach to municipal contract bidding and identifying privatization opportunities. Since the consummation of our transformational $1.9 billion acquisition of Veolia ES Solid Waste, Inc. in 2012 (the "Veolia Acquisition") to date, we have been awarded 128 new long-term, exclusive municipal contracts for a net increase of 42 municipal contracts. Our existing operations also provide us with a scalable platform to drive profitable growth through strategic acquisitions. From the Veolia Acquisition to date, we have executed 45 tuck-in acquisitions, primarily of collection operations. By assimilating acquisitions into our vertically integrated geographic operations, we have been able to improve adjusted EBITDA margin post-acquisition. Due to our scale, our tuck-in acquisition strategy enables us to drive robust inorganic growth despite a relatively small average transaction size.

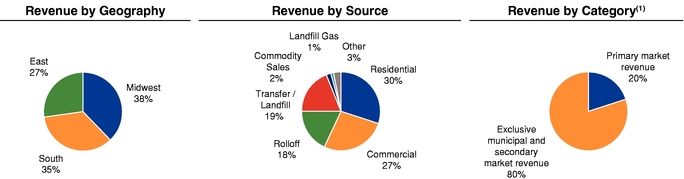

For the twelve months ended June 30, 2016, our revenue by geography, revenue by source and revenue by category were as follows:

- (1)

- Primary market revenue includes revenue from the following four markets (excluding revenue from exclusive municipal contracts): Atlanta, Chicago, Detroit and Philadelphia.

We operate across the Midwest, South and East regions of the United States, which accounted for 38%, 35% and 27% of our revenue for the twelve months ended June 30, 2016, respectively. We believe that our broad geographic presence positions us well to capitalize on favorable demographic and macroeconomic trends in the markets that we serve. According to the U.S. Census Bureau and Woods & Poole, population and gross regional product growth in certain of our markets, particularly those in the Southeast, are expected to outpace overall U.S. population and gross domestic product ("GDP") growth through 2030.

Complementing our geographic diversity, we maintain an attractive mix of revenue from varying sources with limited exposure to commodity sales, which helps to enhance our financial performance across economic cycles. We also benefit from a high degree of customer diversification, with no single customer accounting for more than 2% of revenue for the twelve months ended June 30, 2016. Our municipal customer relationships are generally supported by exclusive contracts ranging from three to ten years in initial duration with subsequent renewal periods, and we have historically achieved a renewal rate of approximately 85% with these customers. Our standard C&I service agreement is a five-year renewable agreement. Management believes we maintain strong relationships with our C&I

2

customers. Our large and diverse customer base, combined with our long-term contracts and consistently high renewal rates, provide us with significant revenue and earnings stability and visibility.

We are led by a veteran management team with extensive experience in operating, acquiring and integrating solid waste services businesses. Our senior leadership team averages more than 20 years of experience in the solid waste industry. During their tenure, they have instituted a strong, unified corporate culture and successfully implemented our growth and operational initiatives. We believe our management team has positioned our business well for continued growth and improvements in adjusted EBITDA margin and cash flow from operations, and we intend to continue to focus our efforts on generating both organic and inorganic growth.

For the twelve months ended June 30, 2016, we generated revenues of $1.4 billion, net loss of $28.3 million, adjusted EBITDA of $401.4 million and cash flow from operations of $219.6 million. For a reconciliation of adjusted EBITDA to net income (loss) see "Summary Consolidated Financial Information and Other Data."

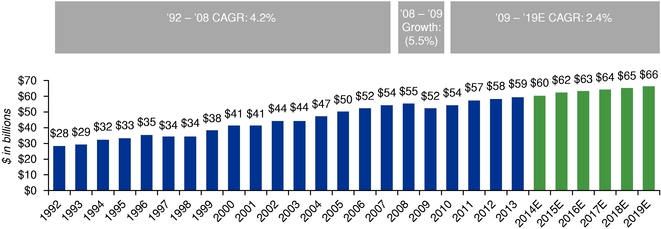

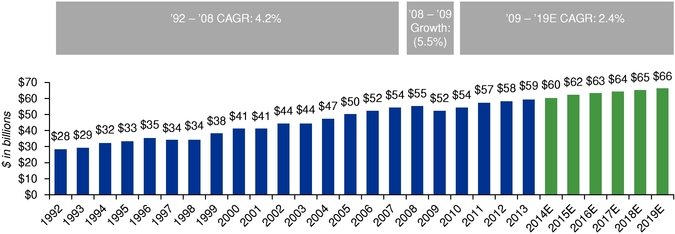

Our Industry

More than 250 million tons of solid waste are generated in the United States each year. The U.S. solid waste industry generated approximately $59 billion in revenue in 2013 and is expected to reach approximately $66 billion in 2019, according to IBISWorld. The industry can be classified into the following asset categories: collection operations, transfer stations, landfills, recycling facilities and waste-to-energy plants. Vertical integration of these assets typically drives greater efficiency and superior operating margins and as a result, waste companies attempt to create integrated operations in an effort to enhance profitability, cash flow and return on capital.

The solid waste industry is relatively resistant to cyclical economic trends due to the non-discretionary nature of the services provided and, as such, has experienced just one year of relatively modest decline since 1997. The industry is characterized by a range of attractive features, including: (i) high visibility of earnings due to predictable waste generation of residential and commercial customers; (ii) the absence of cost-effective substitutes for collection, beneficial re-use and landfill disposal; (iii) high barriers to entry created by the lengthy permitting process and significant capital costs of landfill development; and (iv) the ongoing trend of municipalities and local governments seeking to turn over management of public services, including waste services, to private firms.

3

The following table sets forth historical and projected solid waste industry revenue growth:

Source: Waste Business Journal's Waste Market Overview & Outlook 2012, IBISWorld US Waste Treatment & Disposal and US Waste Collection Reports April 2014

The solid waste industry is served by a few large, national and regional publicly owned companies, which comprise approximately 57% of the total U.S. solid waste market, several regional privately owned solid waste companies, and thousands of small privately owned companies, which generally maintain collection operations with limited or no in-house transfer, recycling or disposal capabilities. Privately owned waste collection operations in the aggregate represent approximately 20% of the total solid waste market. In addition, municipalities continue to own and operate waste collection and/or disposal operations in certain markets, representing approximately 23% of the overall U.S. solid waste market. The industry is characterized by high barriers to entry, driven in large part by the high cost of developing and maintaining transfer and disposal assets. The implementation of the Resource Conservation and Recovery Act ("RCRA") Subtitle D in 1991 significantly raised the environmental standards for landfill operators, requiring costly upgrades and closure of many disposal sites, and resulted in a trend toward fewer larger landfills. This consolidation trend and the resulting increased scarcity of active disposal locations have benefited larger waste companies by providing improved pricing and profitability dynamics.

There are three principal markets in the solid waste industry, including:

- •

- Residential Waste Market

- •

- Consists of the periodic curbside pickup of residential household waste and delivery to either a landfill, transfer

station or recycling facility

- •

- Waste volumes are driven primarily by population growth and GDP growth

- •

- Commercial and Industrial Waste

Market

- •

- Consists of the collection and disposal of waste generated by non-residential customers that utilize front load, rolloff

containers or waste compactors

- •

- Waste volumes are driven primarily by GDP growth, new business formations, industrial production and non-residential

construction

- •

- Construction & Demolition Waste

Market

- •

- Consists of the collection and disposal of debris generated during construction, renovation and demolition typically using rolloff containers

4

- •

- Waste volumes are driven primarily by residential and non-residential construction activity

In addition to the residential and C&I waste streams traditionally serviced by waste companies, regulatory and other market factors have created opportunities to expand services to other non-hazardous waste streams such as coal ash generated by coal-fired electricity producing plants and energy waste produced by oil & gas exploration and production firms.

Our Operating Strengths

Vertically Integrated Geographic Operations

Our vertically integrated geographic operations enable us to provide high-quality service to our customers while simultaneously capitalizing on growth opportunities, capturing additional revenue streams and maximizing profitability. In most of the markets we serve, we integrate our network of collection, transfer and disposal assets into geographic operations that allow us to manage the waste stream throughout the entire value chain—from the point of collection to the point of disposal—exclusively using our own resources. This enables us to generate a steady, predictable stream of waste volume and capture the incremental disposal margin that otherwise would be paid to a third party. It also enables us to charge third-party collection service providers tipping fees for the use of our transfer stations or landfills, providing a source of recurring revenue at attractive EBITDA margins. In addition, our high internalization rate provides us with a meaningful cost advantage, positioning us well to win additional profitable business through new customer acquisition and municipal contract awards. Finally, our vertically integrated geographic operations position us well for inorganic growth, as we can acquire transfer stations or collection operations and efficiently integrate them into our existing platform.

Strategically Located Network of Landfill and Transfer Station Assets

Our network of 39 active and strategically located landfills is a critical component of our integrated operations and provides a distinct competitive advantage in the markets that we serve. Our network of landfill assets is difficult to replicate due to a range of factors, including substantial upfront capital requirements for new landfill development, lengthy permitting processes, geographic and political constraints on new landfills and stringent requirements for ongoing environmental and regulatory compliance. Our landfill assets have substantial remaining capacity, which will help us to sustain the long-term competitive advantages that our vertically integrated model provides.

The value of our landfill assets is further enhanced by our complementary network of transfer stations, which provides us with an additional competitive advantage by allowing us to capture waste volumes that we could not otherwise service. The shift toward fewer, larger landfills has resulted in landfills that are generally located farther from population centers and waste being transported longer distances between collection and disposal, often after consolidation at a transfer station. With a landfill and collection services, we can provide vertically integrated operations that cover a substantial geographic area surrounding the landfill. However, with one or more transfer stations strategically located at the periphery of this service area, and with additional collection operations around the transfer station(s), we can direct substantially more waste volume from a significantly broader service area to an existing landfill. By expanding the geographic reach of our landfills, our network of transfer stations enhances our economies of scale and strengthens the competitive advantage that our landfills provide.

5

Well-Positioned in Secondary and Exclusive Markets

We focus our business principally in secondary markets where the presence of large national providers is generally more limited. We also participate in certain disposal-neutral markets in which we provide services under exclusive arrangements with our municipal customers, which facilitates highly-efficient and profitable collection operations and lower capital requirements. We believe this strategic focus positions us to maintain significant share within our target markets, maximize customer retention and benefit from a higher and more stable pricing environment. For the twelve months ended June 30, 2016, revenue from our secondary markets and exclusive municipal contracts accounted for approximately 80% of total revenue.

Proven Ability to Identify, Execute and Integrate Acquisitions and Win New Municipal Contracts

Our ability to execute and integrate value-enhancing, tuck-in acquisitions and win new municipal contracts has been a core component of our growth. Our scale, geographic reach, vertical integration and strong position in secondary markets position us well to identify and execute strategic acquisitions. From the Veolia Acquisition to date, we have completed 45 tuck-in acquisitions, and by integrating acquired operations into our existing network, we have been able to improve adjusted EBITDA margin and enhance cash flow from operations post-acquisition.

We also have experience executing large-scale transactions, as highlighted by the Veolia Acquisition. In addition to significantly expanding our scale and scope of operations, the Veolia Acquisition enhanced our geographic footprint by providing us with complementary operations in our East and South regions, as well as strong, new positions in secondary markets in the Midwestern United States. We have also achieved cost efficiencies and economies of scale through improved internalization, increased route density and more efficient asset utilization while maintaining our strong positions in the local markets that we serve.

Finally, we have demonstrated success in municipal contract bidding and capitalizing on privatization opportunities and, from the Veolia Acquisition to date, we have been awarded 128 new long-term municipal contracts. Due to the strength of our localized operations and our highly experienced regional management team, we maintain close relationships with key decision-makers throughout our markets, which position us well to capitalize on new municipal contracts and privatization opportunities.

Customer Diversification with Long-Term Contracts

We serve approximately 2.8 million residential and 221,000 C&I customers and over 800 municipalities, with no single customer representing more than 2% of revenue in 2015 or for the six months ended June 30, 2016. Our municipal customer relationships are generally supported by contracts ranging from three to ten years in initial duration with subsequent renewal periods, and we have historically achieved a renewal rate of approximately 85% with these customers. Our standard C&I service agreement is a five-year renewable agreement. Management believes we maintain strong relationships with our C&I customers. Our breadth of customer relationships, long-term contracts and high renewal rates provide us with a high degree of revenue and earnings stability and visibility.

6

Disciplined Focus on Service and Safety

Our corporate slogan is "Service First, Safety Always." We maintain a relentless focus on customer service and we strive to consistently exceed our customers' expectations. Our localized approach to customer service and high quality management at our local operations result in a highly responsive, customer service oriented organization. By providing a high level of customer service, we maximize the value our customers receive from the services we deliver, which we believe ultimately increases customer loyalty and supports price stability.

The safety of our workforce and our customers is paramount to us. We have a strong track record of safety and environmental compliance driven by company-wide programs centered on workforce training, stringent risk management and safety-related practices. Our shift toward an automated fleet has also enhanced our safety profile. Automated trucks, which only require a driver and collect waste automatically using a hydraulic lifting mechanism, are substantially safer than traditional rear-load vehicles, which require both a driver and an operator who manually loads waste into the rear of a vehicle. With a growing portion of our fleet comprised of automated vehicles, we have sought to create a safer work environment for our employees and to reduce the frequency of workplace injuries.

Industry Leading Management Team

Led by CEO Richard Burke, CFO Steven Carn and COO John Spegal, our management team has extensive experience in the solid waste industry, consisting of operations, acquisitions and the development of disposal capacity. Our leadership team has instituted a strong, unified corporate culture and has successfully executed a differentiated growth strategy that positions us well to capitalize on continued organic and inorganic growth initiatives. While our leadership team drives our overall strategy, our decentralized management structure facilitates local management autonomy and enables us to capitalize on growth and cost reduction opportunities at the local level. Averaging more than 20 years of industry experience, our senior management team is supported by a talented group of regional, district and general managers who execute on our strategy in their respective markets.

Our Growth Strategies

Continue to Develop Vertically Integrated Geographic Operations

Our vertically integrated geographic operating model serves as the foundation for our business strategy. We pursue a multi-faceted growth strategy within this operating framework, including both growth within our existing network of landfill and transfer stations and expansion into additional geographies in which we establish new vertically integrated operations. Further development of our existing vertically integrated operations will allow us to capitalize on incremental growth initiatives and efficiency gains, including the internalization of additional waste streams to expand volume, increase revenue and improve profitability.

Pursue Disciplined Acquisition Strategy

Our ability to execute value-enhancing, tuck-in acquisitions has been a core component of our growth. From the Veolia Acquisition to date, we have completed 45 strategic tuck-in acquisitions at attractive EBITDA multiples. The U.S. solid waste industry remains highly fragmented, with approximately 43% of the total market consisting of either privately held providers or municipal operators. We believe that significant opportunities exist for further

7

consolidation and that, as a result of our scale and broad geographic presence, we remain ideally positioned to capitalize on these opportunities.

We intend to expand the scope of our operations by continuing to acquire solid waste management companies and disposal facilities in new markets and in existing or adjacent markets that are combined with, or tucked into, our existing operations. We intend to focus our acquisition efforts on markets that we believe provide significant growth opportunities. This focus typically highlights markets in which we can: (i) provide vertically integrated collection and disposal services; or (ii) provide waste collection services under exclusive arrangements. We believe that our experienced management team, decentralized operating strategy, financial strength and scale make us an attractive buyer to waste collection and disposal acquisition candidates.

Secure Additional Exclusive Municipal Contracts

We intend to continue to devote significant resources to securing additional municipal contracts. We have established a systematic and replicable approach to municipal contract bidding and privatization opportunities. In bidding for municipal contracts, our management team draws on its experience in the solid waste industry and knowledge of local service areas in existing and target markets. Our highly aligned district and local general management and sales and marketing personnel maintain relationships with local decision-makers within their service areas and are responsible for renewing and renegotiating existing municipal contracts and securing additional agreements and contracts with attractive financial returns.

Drive Financial Performance through Operational Excellence

We maintain a consistent operational focus on prudent cost management and pricing discipline to drive profitability. Our strategy is implemented by our district and local general managers who continuously monitor their local markets and target profit maximization rather than throughput alone. We closely align the incentive structure of our local managers to the safety and financial performance of the local operations that they oversee to drive adjusted EBITDA and operating cash flow growth at the local level. In addition to increasing earnings through this operational focus, we remain committed to financial discipline through prudent management of returns on equity and capital deployed. We seek to increase operating margins, adjusted EBITDA and cash flow from operations and drive higher returns on invested capital by implementing programs focused on areas such as sales productivity and pricing effectiveness, driver productivity and route optimization, maintenance efficiency and effective purchasing.

Invest in Strategic Infrastructure

We will continue to invest in our strategic infrastructure to support growth and expand our adjusted EBITDA margin. Given the long remaining life of our existing network of landfills, we continuously invest resources toward the development and enhancement of our landfills to increase our disposal capacity. Similarly, we will continue to evaluate opportunities to maximize the efficiency of our collection operations. We are currently in the process of converting our collection fleet to compressed natural gas ("CNG") fueled vehicles in certain markets where we can achieve an attractive return on our investment. CNG-fueled vehicles, which can provide significant operating cost savings relative to diesel alternatives, currently comprise 18% of our routed fleet, and we continue to evaluate further conversion opportunities. We believe this will result in an improved profitability profile as a result of the added fuel efficiency and labor savings. Finally, we have converted approximately 54% of our routed residential collection fleet to automated vehicles and continue to convert more of our

8

routed collection fleet to automated vehicles, which should result in incremental operating cost savings. In addition to labor cost savings, management believes the shift toward an automated fleet will result in reduced injury claims and workers compensation expense.

Invest in Our People

Employing and developing a broad base of highly talented employees is essential to success in our decentralized operating model. We will continue to invest in high-quality talent in order to most effectively manage our existing operations and execute our growth strategy. We rely on managers and employees with specific local market knowledge to not only operate our business but also to identify and integrate tuck-in acquisitions and new municipal contract wins. As such, we continuously recruit and hire talented local-level employees who are capable of supporting our growth initiatives and provide the best-in-class customer service we strive to deliver.

We have consistently realized organic growth driven by a strong, dedicated sales force. Our team of professionals has executed our sales strategy by focusing not only on growth, but also on profitability. We will continue to drive this strategy by rewarding our managers who successfully monitor their local markets and have a proven track record of achieving profitable growth. We will also invest in new sales employees and marketing initiatives within markets that further our overall vertically integrated geographic operating strategy, driving new wins, enhancing our route density and increasing volumes to landfills.

Risk Factors

There are a number of risks you should consider before buying our shares. These risks are discussed more fully under "Risk Factors" beginning on page 20 of this prospectus. These risks include, but are not limited to:

- •

- We have a history of losses and may not achieve or sustain profitability in the future.

- •

- We operate in a highly competitive industry and may not be able to compete effectively with larger and better capitalized companies

and governmental service providers.

- •

- We may lose contracts through competitive bidding, early termination or governmental action.

- •

- Our results are vulnerable to economic conditions.

- •

- Some of our customers, including governmental entities, have suffered financial difficulties affecting their credit risk, which could

negatively impact our operating results.

- •

- Our financial and operating performance may be affected by the inability in some instances to renew landfill permits, obtain new

landfills or expand existing ones. Further, the cost of operation and/or future construction of our landfills may become economically unfeasible causing us to abandon or cease operations.

- •

- Our accruals for our landfill site closure and post-closure costs and contamination-related costs may be inadequate.

- •

- Our business requires a high level of capital expenditures.

- •

- We may engage in strategic acquisitions in the future, which may pose significant risks and could have an adverse effect on our operations.

9

- •

- The seasonal nature of our business and "event-driven" waste projects cause our results to fluctuate.

- •

- Fluctuations in the prices of commodities may adversely affect our financial condition, results of operations and cash flows.

- •

- Increases in labor and disposal and related transportation costs could impact our financial results.

- •

- Our operations are subject to environmental, health and safety laws and regulations, as well as contractual obligations that may

result in significant liabilities.

- •

- Our indebtedness could adversely affect our financial condition and limit our financial flexibility. As of June 30, 2016, we

had approximately $2,300.5 million of indebtedness outstanding and cash interest expense of $115.1 million for the twelve months ended June 30, 2016.

- •

- Despite our high indebtedness level, we and our subsidiaries will still be able to incur significant additional amounts of debt, which

could further exacerbate the risks associated with our substantial indebtedness.

- •

- Our debt agreements contain restrictions that limit our flexibility in operating our business.

Our History

Our predecessor company was formed in November 2000 with the vision to build a vertically integrated non-hazardous solid waste business in the Southeastern United States. Following the acquisition of Advanced Disposal Services, Inc. ("ADS Inc."), a predecessor company, and Interstate Waste by Highstar Capital LP ("Highstar Capital") in 2006, our management team, together with Highstar Capital, successfully implemented growth and operational strategies to establish these companies as among the largest waste management companies in their respective markets. In addition to substantially increasing our overall scale, the Veolia Acquisition provided a synergistic overlap in key South and East market segments while establishing a strong presence in several secondary markets in the Midwest. Subsequent to the Veolia Acquisition, we divested certain operations in the Northeast and South regions, including substantially all of our New York, New Jersey, Massachusetts, Mississippi and Vermont operations, which did not align with our strategic focus. We have continued to pursue our vertically integrated approach to the market through both organic initiatives and through strategic tuck-in acquisitions, having completed 45 acquisitions since the Veolia Acquisition to date.

Our Corporate Information

Our principal executive office is located at 90 Fort Wade Road, Ponte Vedra, Florida 32081. Our telephone number at that address is (904) 737-7900. Our website address is www.advanceddisposal.com. Information on our website is deemed not to be a part of this prospectus.

Our Sponsor

Highstar Capital provides operationally focused, value-added investment management services. Since 2000, the Highstar Capital team has managed approximately $8.0 billion on behalf of its managed funds and co-investment vehicles in a diversified portfolio of energy, transportation and environmental services assets and businesses.

10

Recent Equity Investment in Controlling Limited Partnership

On August 3, 2016, the Company announced that Canada Pension Plan Investment Board ("CPPIB") invested $280 million in preferred units of Star Atlantic Waste Holdings II, L.P. ("Star Atlantic II"), a Highstar Capital sponsored limited partnership that controls Parent. The proceeds of the investment were used by Star Atlantic II to redeem the preferred units formerly owned by OPTrust Infrastructure Europe I Inc. All preferred units owned by CPPIB will convert automatically into shares of our common stock upon completion of this offering. In connection with its investment, CPPIB received the right to designate one member of our board of directors. CPPIB will also become a party to the stockholders' agreement and registration rights agreement upon consummation of this offering. See "Certain Relationships and Related Party Transactions."

Organizational Structure Following This Offering

Concurrently with the consummation of this offering, Parent, which owns substantially all of the common stock of the Company, will be merged into the Company, with the Company being the surviving corporation. Parent has no assets other than the common stock of the Company and no liabilities except for liabilities under severance agreements with certain former members of management approximating $5.2 million at June 30, 2016. Star Atlantic Waste Holdings II, L.P. will be liquidated contemporaneously with the consummation of the offering and the other pre-IPO investors in Star Atlantic Waste Holdings II, L.P. will become direct shareholders of the Company. The Company will recapitalize in the merger, and immediately prior to this offering the Company will have 64,493,542 shares of common stock issued and outstanding. We refer to these transactions as the "Reorganization." On January 27, 2016, we changed our name from ADS Waste Holdings, Inc. to Advanced Disposal Services, Inc.

11

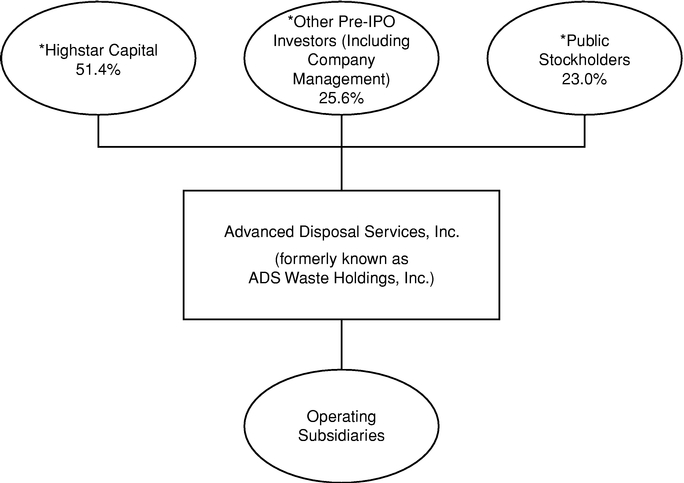

The diagram below depicts our summary organizational structure immediately following this offering:

- *

- Based on the mid point of the price range set forth on the cover of this prospectus and assuming no exercise of the underwriters' option to purchase additional shares of common stock. See "Use of Proceeds." After the completion of this offering, depending on the price of the shares offered and the exercise of the over-allotment option, affiliates of Highstar Capital LP may not continue to own a majority of the voting power of shares eligible to vote in the election of our directors. As a result, we may not be a "controlled company" within the meaning of the corporate governance standards of the New York Stock Exchange. See "Management—Controlled Company."

12

Shares of common stock offered by us |

19,250,000 shares | |

Option to purchase additional shares from us |

2,887,500 shares |

|

Shares of common stock to be outstanding immediately after this offering |

83,743,542 shares |

|

Use of proceeds |

We estimate that the net proceeds to us from this offering, after deducting the underwriting discount and estimated offering expenses payable by us, will be approximately $351.4 million, based on an assumed initial public offering price of $19.50 per share, the mid-point of the range described on the cover of this prospectus, and assuming no exercise of the underwriters' option to purchase additional shares of common stock. An increase or decrease in the initial public offering price by $1.00 would result in an increase or decrease of approximately $18.1 million of net proceeds to us, assuming the number of shares offered by us stays constant. |

|

|

We intend to use the net proceeds from the sale of common stock by us in this offering to repay certain outstanding indebtedness. On February 4, 2016, we obtained lender consent for certain amendments to our Senior Secured Credit Facilities, including the extension of the maturity of the commitments under the Revolving Credit Facility, the effectiveness of which is conditioned on the consummation of this offering and a minimum Term Loan B paydown of $100.0 million. In connection with the amendment to our Senior Secured Credit Facilities, we paid total fees of approximately $5.2 million, which were paid to the lenders and the administrative agent, at the closing of the consent. |

|

|

On August 4, 2016, we entered into a waiver to our Senior Secured Credit Facilities to waive the IPO condition to the extension of the maturity of the commitments under our senior secured credit facilities referred to above. As a result of the execution of the amendment and waiver, the maturity date with respect to approximately $280 million of the $300 million of commitments under the Revolving Credit Facility has been extended to October 2019. See "Description of Certain Indebtedness—Amendments to the Senior Secured Credit Facilities." |

|

|

See "Use of Proceeds." |

13

Risk factors |

Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 20 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

|

Dividend policy |

We have no current plans to pay dividends on our common stock following this offering. Any decision to declare and pay dividends in the future will be made at the sole discretion of our board of directors and will depend on, among other things, our results of operations, cash requirements, financial condition, contractual restrictions and other factors that our board of directors may deem relevant. Because we are a holding company and have no direct operations, we will only be able to pay dividends from funds we receive from our subsidiaries. In addition, our ability to pay dividends will be limited by covenants in our existing indebtedness and may be limited by the agreements governing other indebtedness we or our subsidiaries incur in the future. See "Description of Certain Indebtedness." |

|

Proposed symbol for trading on the NYSE |

Our common stock has been approved for listing on the New York Stock Exchange (the "NYSE"), under the symbol "ADSW". |

Unless otherwise indicated, the shares of common stock outstanding after this offering and information based thereon excludes:

- •

- 4,260,000 shares of common stock available for future issuance under our new omnibus executive compensation plan; and

- •

- 2,887,500 shares of common stock issuable pursuant to the underwriters' option to purchase additional shares of common stock from us.

All share numbers reflect the recapitalization of the Company to be effected in connection with the Reorganization.

All share numbers assume an initial public offering price of $19.50 per share, the mid-point of the range set forth on the cover of this prospectus.

14

SUMMARY CONSOLIDATED FINANCIAL INFORMATION AND OTHER DATA

The following table summarizes our historical consolidated financial information for the periods and as of the dates indicated. The summary historical consolidated financial information as of June 30, 2016 and for the six months ended June 30, 2016 and 2015 is derived from our unaudited condensed consolidated financial statements included elsewhere in this prospectus. The summary historical consolidated financial information as of June 30, 2015 is derived from our unaudited condensed consolidated financial statements not included in this prospectus. Our unaudited consolidated financial statements have been prepared on the same basis as our audited consolidated financial statements and, in our opinion, reflect all adjustments, consisting only of normal and recurring adjustments, necessary for a fair presentation of such financial statements in all material respects.

The summary historical consolidated financial information as of December 31, 2015 and 2014 and for the years ended December 31, 2015, 2014, and 2013 is derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary historical consolidated financial information as of December 31, 2013 is derived from our audited consolidated financial statements not included in this prospectus.

The financial data set forth in the following tables should be read in conjunction with our historical consolidated financial statements and related notes and "Management's Discussion and Analysis of Financial Condition and Results of Operations," each included elsewhere in this prospectus. The results for any interim period are not necessarily indicative of the results that may be expected for a full year or any future period.

15

| |

Six Months Ended June 30, |

Year Ended December 31, | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2016 | 2015 | 2015 | 2014 | 2013 | |||||||||||

| |

(in millions, except per share data and percentages) |

|||||||||||||||

Consolidated Statement of Operations Data: |

||||||||||||||||

Service revenues |

$ | 692.0 | $ | 685.5 | $ | 1,396.4 | $ | 1,403.0 | $ | 1,319.1 | ||||||

| | | | | | | | | | | | | | | | | |

Costs and expenses: |

||||||||||||||||

Operating |

432.3 | 428.9 | 866.6 | 896.1 | 832.8 | |||||||||||

Selling, general and administrative (a) |

84.1 | 72.9 | 152.6 | 154.9 | 170.9 | |||||||||||

Depreciation and amortization |

125.4 | 127.4 | 259.1 | 271.4 | 278.9 | |||||||||||

Acquisition and development costs |

0.2 | 1.1 | 1.4 | 0.1 | 1.2 | |||||||||||

Loss on disposal of assets and asset impairments (b) |

0.1 | 17.5 | 21.6 | 6.5 | 3.2 | |||||||||||

Restructuring |

0.8 | — | — | 4.6 | 10.0 | |||||||||||

| | | | | | | | | | | | | | | | | |

|

642.9 | 647.8 | 1,301.3 | 1,333.6 | 1,297.0 | |||||||||||

| | | | | | | | | | | | | | | | | |

Operating income |

49.1 | 37.7 | 95.1 | 69.4 | 22.1 | |||||||||||

Interest expense |

(68.6 | ) | (69.8 | ) | (138.0 | ) | (141.5 | ) | (163.1 | ) | ||||||

Other income/(expense), net (c) |

0.4 | 3.7 | (10.1 | ) | (25.9 | ) | 0.3 | |||||||||

| | | | | | | | | | | | | | | | | |

Loss before income taxes |

(19.1 | ) | (28.4 | ) | (53.0 | ) | (98.0 | ) | (140.7 | ) | ||||||

Benefit for income taxes (d) |

(5.1 | ) | (9.1 | ) | (19.4 | ) | (80.6 | ) | (45.4 | ) | ||||||

| | | | | | | | | | | | | | | | | |

Net loss from continuing operations |

(14.0 | ) | (19.3 | ) | (33.6 | ) | (17.4 | ) | (95.3 | ) | ||||||

Income (loss) from discontinued operations, net of tax (e) |

— | — | — | 0.3 | (22.5 | ) | ||||||||||

| | | | | | | | | | | | | | | | | |

Net loss |

$ | (14.0 | ) | $ | (19.3 | ) | $ | (33.6 | ) | $ | (17.1 | ) | $ | (117.8 | ) | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Loss from continuing operations per share: |

||||||||||||||||

Basic and diluted loss per share |

$ | (14,000 | ) | $ | (19,300 | ) | $ | (33,600 | ) | $ | (17,400 | ) | $ | (95,300 | ) | |

Net loss per share: |

||||||||||||||||

Basic and diluted loss per share |

$ | (14,000 | ) | $ | (19,300 | ) | $ | (33,600 | ) | $ | (17,100 | ) | $ | (117,800 | ) | |

Pro forma net loss per share (f): |

||||||||||||||||

Basic and diluted loss per share |

$ | (0.17 | ) | $ | (0.23 | ) | $ | (0.40 | ) | $ | (0.20 | ) | $ | (1.41 | ) | |

Consolidated Statement of Cash Flows Data: |

||||||||||||||||

Net cash provided by operating activities |

$ | 104.4 | $ | 129.3 | $ | 244.5 | $ | 243.2 | $ | 180.3 | ||||||

Net cash used in investing activities |

(70.8 | ) | (85.3 | ) | (197.4 | ) | (201.2 | ) | (154.8 | ) | ||||||

Net cash used in financing activities |

(33.0 | ) | (35.7 | ) | (47.5 | ) | (53.0 | ) | (32.3 | ) | ||||||

Consolidated Balance Sheet Data (at period end): |

||||||||||||||||

Total assets (k) |

$ | 3,374.7 | $ | 3,448.1 | $ | 3,422.3 | $ | 3,489.5 | $ | 3,554.2 | ||||||

Debt, including current portion (g)(k) |

2,240.4 | 2,239.7 | 2,247.1 | 2,243.0 | 2,259.3 | |||||||||||

Total Advanced Disposal stockholders' equity |

466.5 | 501.9 | 489.8 | 528.9 | 551.5 | |||||||||||

Other Data: |

||||||||||||||||

Adjusted EBITDA from continuing operations (h) |

$ | 194.3 | $ | 192.9 | $ | 400.0 | $ | 378.8 | $ | 361.1 | ||||||

Adjusted EBITDA margin from continuing operations (i) |

28.1 | % | 28.1 | % | 28.6 | % | 27.0 | % | 27.4 | % | ||||||

Free cash flow (j) |

$ | 36.2 | $ | 42.3 | $ | 69.8 | $ | 80.2 | $ | 25.6 | ||||||

- (a)

- Includes

stock-based compensation expense. Stock based compensation expense for all periods presented was determined using the fair value method set forth

in ASC 718, "Compensation—Stock Compensation."

- (b)

- We

disposed of certain businesses in the South segment for strategic reasons in June 2015 and recorded a loss on disposal of $10.9 million for fiscal

2015. Additionally, we recorded an impairment of $6.4 million during fiscal 2015 in connection with the strategic decision to divest certain businesses in the South segment and the decision not

to pursue a landfill permit. In fiscal 2014, we recorded an impairment charge of $5.3 million in connection with the decision to divest a small brokerage business.

- (c)

- Changes

in the fair value and settlements of fuel derivative instruments are recorded in other income (expense), net in the condensed consolidated

statements of operations and amounted to income of $1.5 million and expense of $0.2 million for the six months ended June 30, 2016 and 2015, respectively. Changes in the fair

value of the interest rate caps purchased in May 2016 are recorded in other income (expense), net in the condensed consolidated statements of operations and amounted to a loss of

$2.8 million for the six months ended June 30, 2016. Amounts included in other (expense)/income, net for fiscal 2015 and 2014 contain unrealized and realized losses, net related to fuel

derivative instruments of $15.4 million and $27.3 million, respectively, and a gain on the redemption of a security of $2.5 million for fiscal 2015.

- (d)

- In fiscal 2014, we completed a legal entity reorganization to achieve administrative efficiencies and as such recorded a valuation allowance release of $51.4 million related to certain net operating losses that are more likely than not to be utilized.

16

- (e)

- Amounts

represent those operations that are considered to be discontinued operations. Refer to Note 4 "Discontinued Operations" in our audited

consolidated financial statements included elsewhere in this prospectus for further information.

- (f)

- Pro

forma net loss per share is based on the shares to be issued in the Reorganization and an offering by the Company of shares of common stock at a price

per share equal to the mid-point of the price range set forth on the cover of this prospectus and assuming no exercise of the underwriters' option to purchase additional shares of common stock. Under

certain circumstances, we may elect to increase the total number of shares issued and sold by us in this offering. See "Use of Proceeds." Any increase in the number of shares issued by us in this

offering will increase the total number of shares outstanding after this offering and will decrease the pro forma net loss per share.

- (g)

- Total

debt includes capital lease obligations of $38.7 million, $24.7 million, $28.2 million, $23.3 million and

$15.4 million at June 30, 2016 and 2015 and December 31, 2015, 2014, and 2013, respectively.

- (h)

- We define EBITDA as net income (loss) from continuing operations adjusted for interest, taxes, depreciation and amortization and accretion. We define adjusted EBITDA as EBITDA adjusted to exclude non-cash and non-recurring items as well as other adjustments permitted in calculating covenant compliance under the agreements governing our outstanding debt securities and Senior Secured Credit Facilities. We believe adjusted EBITDA is useful to investors in evaluating our performance compared to other companies in our industry because it eliminates the effect of financing, income taxes and the accounting effects of capital spending, as well as certain items that are not indicative of our performance on an ongoing basis. Management uses adjusted EBITDA to measure the performance of our core operations at the consolidated, segment and business unit levels and as a metric for a significant portion of our management incentive plans. EBITDA and adjusted EBITDA are non-GAAP measures and, when analyzing our operating performance, investors should not consider EBITDA and adjusted EBITDA in isolation or as substitutes for net income, cash flows from operating activities or other statement of operations or cash flow statement data prepared in accordance with GAAP. Our calculations of EBITDA and adjusted EBITDA are not necessarily comparable to those of similarly titled measures provided by other companies. We believe excluding, among other items, stock based compensation, restructuring costs, sale of assets and asset impairments, rebranding and integration costs and share issuance and capital market costs from adjusted EBITDA is useful additional information in evaluating ongoing financial performance of the business and is consistent with how management evaluates performance. Our approach to these items is also consistent with the approach used in determining covenant compliance in our Senior Secured Credit Facilities and these items do not represent normal recurring cash operating expenses necessary to operate the business. We have also excluded losses and gains on derivative instruments. In fiscal 2014 we made a strategic decision to enter into fuel derivatives as economic hedges of a rise in the price of diesel fuel for fiscal 2015 and fiscal 2016. These derivatives resulted in realized losses in fiscal 2015 and in the six months ended June 30, 2016 as oil prices declined and we are likely to realize additional losses when the remaining contracts settle in the second half of fiscal 2016. We have not entered into fuel derivatives since fiscal 2014 when the economic hedges for fiscal 2015 and fiscal 2016 were put in place and have no present intention to enter into fuel derivatives in fiscal 2016 or fiscal 2017. We therefore believe that excluding realized losses from fuel derivatives from our Adjusted EBITDA is useful additional information in evaluating ongoing financial performance of the business and is consistent with how management evaluates performance. In fiscal 2016, we entered into interest rate caps as economic hedges of a rise in interest rates for fiscal 2017, fiscal 2018 and the nine months ended September 30, 2019. These interest rate derivatives resulted in $2.8 million in unrealized losses in the six months ended June 30, 2016. We believe that excluding unrealized losses from interest rate derivatives from our Adjusted EBITDA provides useful additional information in evaluating ongoing financial performance of the business as these derivatives represent a risk management tool to reduce our exposure to rising interest rates and are viewed by management as a financing cost similar to interest expense. Our approach to fuel and interest rate derivative contracts is also consistent with the approach used in determining covenant compliance in our Senior Secured Credit Facilities, as it will be amended upon consummation of this offering. See "Description Certain Indebtedness—Senior Secured Credit Facilities" and "—Amendments to the Senior Secured Credit Facilities".

17

| |

Six Months Ended June 30, |

Year Ended December 31, |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2016 | 2015 | 2015 | 2014 | 2013 | |||||||||||

| |

(in millions, except percentages) |

|||||||||||||||

Net loss |

$ | (14.0 | ) | $ | (19.3 | ) | $ | (33.6 | ) | $ | (17.1 | ) | $ | (117.8 | ) | |

Less (loss) income from discontinued operations, net |

— | — | — | 0.3 | (22.5 | ) | ||||||||||

| | | | | | | | | | | | | | | | | |

Loss from continuing operations |

(14.0 | ) | (19.3 | ) | (33.6 | ) | (17.4 | ) | (95.3 | ) | ||||||

Additions/deductions: |

||||||||||||||||

Income tax benefit |

(5.1 | ) | (9.1 | ) | (19.4 | ) | (80.6 | ) | (45.4 | ) | ||||||

Interest expense |

68.6 | 69.8 | 138.0 | 141.5 | 163.1 | |||||||||||

Depreciation and amortization |

125.4 | 127.4 | 259.1 | 271.4 | 278.9 | |||||||||||

Accretion on landfill retirement obligations |

6.5 | 6.7 | 13.1 | 13.5 | 13.7 | |||||||||||

Accretion on loss contracts and other long-term liabilities |

0.2 | 0.4 | 0.8 | 0.9 | 0.4 | |||||||||||

| | | | | | | | | | | | | | | | | |

EBITDA from continuing operations |

181.6 | 175.9 | 358.0 | 329.3 | 315.4 | |||||||||||

EBITDA adjustments: |

||||||||||||||||

Acquisition and development costs |

0.2 | 1.1 | 1.4 | 0.1 | 1.2 | |||||||||||

Stock based compensation |

3.3 | 1.2 | 3.1 | 2.1 | 4.6 | |||||||||||

(Earnings) losses in equity investee, net |

(0.5 | ) | (0.4 | ) | 0.3 | (0.1 | ) | (0.3 | ) | |||||||

Restructuring charges (l) |

0.8 | — | — | 4.6 | 10.0 | |||||||||||

Loss on sale of assets and asset impairments |

0.1 | 17.5 | 21.6 | 6.5 | 5.5 | |||||||||||

Unrealized (gain) loss on derivative instruments (o)(p) |

(7.0 | ) | (10.9 | ) | (11.1 | ) | 27.3 | — | ||||||||

Gain on redemption of security |

— | (2.5 | ) | (2.5 | ) | — | — | |||||||||

Rebranding and integration costs (m) |

— | — | — | 7.1 | 25.8 | |||||||||||

Write-off of share issuance and other capital market costs (n) |

7.5 | — | 2.8 | — | — | |||||||||||

Other |

— | (0.1 | ) | — | — | — | ||||||||||

Realized loss (gain) on fuel derivative instruments (o) |

8.3 | 11.1 | 26.4 | 1.9 | (1.1 | ) | ||||||||||

| | | | | | | | | | | | | | | | | |

Adjusted EBITDA from continuing operations |

$ | 194.3 | $ | 192.9 | $ | 400.0 | $ | 378.8 | $ | 361.1 | ||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Revenue from continuing operations |

$ | 692.0 | $ | 685.5 | $ | 1,396.4 | $ | 1,403.0 | $ | 1,319.1 | ||||||

Adjusted EBITDA margin from continuing operations |

28.1 | % | 28.1 | % | 28.6 | % | 27.0 | % | 27.4 | % | ||||||

- (i)

- Adjusted

EBITDA margin is defined as adjusted EBITDA divided by revenue from continuing operations.

- (j)

- Free cash flow is defined as net cash provided by operating activities less capital expenditures (purchases of property and equipment, excluding expenditures for significant new municipal contracts and land purchased for future landfill airspace, net of proceeds from the sale of property and equipment). The following table sets forth a reconciliation of free cash flow to net cash provided by operating activities.

| |

Six Months Ended June 30, |

Year Ended December 31, | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2016 | 2015 | 2015 | 2014 | 2013 | |||||||||||

| |

(in millions, except percentages) |

|||||||||||||||

Net cash provided by operating activities |

$ | 104.4 | $ | 129.3 | $ | 244.5 | $ | 243.2 | $ | 180.3 | ||||||

Purchases of property & equipment * |

(69.2 | ) | (87.3 | ) | (177.3 | ) | (166.0 | ) | (158.1 | ) | ||||||

Proceeds from sale of property & equipment |

1.0 | 0.7 | 2.6 | 3.0 | 3.4 | |||||||||||

| | | | | | | | | | | | | | | | | |

Free cash flow |

36.2 | 42.7 | 69.8 | 80.2 | 25.6 | |||||||||||

- *

- The six months ended June 30, 2015 excludes the impact of land purchased for future airspace of $2.4 million. The fiscal year ended December 31, 2015 excludes the impact of land purchased for future landfill airspace of $2.4 million. The fiscal year ended December 31, 2014 excludes the impact of land purchases for future airspace of $8.8 million at one landfill and capital related to the start of a major municipal contract of $21.6 million.

- (k)

- Balances

have been adjusted to reflect the retrospective adoption of Accounting Standard Update ("ASU") 2015-03, Interest—Imputation of

Interest.

- (l)

- In September 2012, we announced a reorganization of our operations in anticipation of the Veolia Acquisition. The $4.6 million of restructuring charges in fiscal 2014 and $10.0 million of restructuring charges in fiscal 2013 relate to these reorganization efforts. During the first quarter of 2016, we eliminated a corporate executive position and re-aligned three districts in the Midwest segment into two districts. The $0.8 million of restructuring charges incurred during the six months ended June 30, 2016 relate to these permanent changes to our business. Adjustments reflect amounts accrued in the period; a portion of the corresponding cash expenditures have been or will be made in other fiscal periods.

18

- (m)

- In

connection with the Veolia Acquisition and the reorganization efforts noted in Note (e) above, we incurred costs to re-brand our fleet of trucks and

containers with the Advanced Disposal branding. We also incurred costs to integrate our legacy businesses together with the Veolia ES Solid Waste division. Adjustments reflect amounts accrued in the

period; a portion of the corresponding cash expenditures have been or will be made in other fiscal periods.

- (n)

- In

February 2016, we launched, but did not complete, an initial public offering process. In relation to this initial public offering process, we incurred

various costs including legal costs, accounting costs, printing costs and costs to amend our Senior Secured Credit Facilities contingent on the initial public offering. Adjustments reflect amounts

accrued in the period; a portion of the corresponding cash expenditures have been or will be made in other fiscal periods.

- (o)

- In

fiscal 2014, we made a strategic decision to implement a large scale economic hedge on the price of diesel fuel by entering into commodity swap

agreements for 23.8 million gallons that matured in fiscal 2015 and for 13.4 million gallons that will mature in fiscal 2016. For reference, we purchased approximately 26 million

gallons of diesel fuel for use in our operations during fiscal 2015. Unrealized (gains)/losses represent non-cash (income)/expense in the periods in which they are reported.

- (p)

- In fiscal 2016, we implemented economic hedges on a rise in interest rates for fiscal 2017, fiscal 2018 and the nine months ended September 30, 2019. These hedges resulted in $2.8 million in unrealized losses in the six months ended June 30, 2016. These derivatives represent a risk management tool to reduce the Company's exposure to rising interest rates and are viewed by management as a financing cost similar to interest. Unrealized (gains)/losses represent non-cash (income)/expense in the periods in which they are reported.

19

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with the risks and uncertainties described elsewhere in this prospectus, including our consolidated financial statements and the related notes contained elsewhere in this prospectus, before you decide to purchase shares of our common stock. If any of the following risks or uncertainties actually occurs, our business, financial condition, results of operations, cash flow and prospects could be materially and adversely affected. As a result, the price of our common stock could decline and you could lose all or part of your investment in our common stock.

Risks Related to Our Business

We have a history of losses and may not achieve or sustain profitability in the future.

We incurred net losses of $33.6 million, $17.1 million and $117.8 million for the years ended December 31, 2015, 2014 and 2013 respectively, and $14.0 million and $19.3 million for the six months ended June 30, 2016 and 2015, respectively. Although we achieved profitability during the second quarter of 2016, we may not sustain this profitability in the future. In addition, we may be unable to fully utilize our net operating losses prior to their expiration, which may result in lower earnings going forward.

We operate in a highly competitive industry and may not be able to compete effectively with larger and better capitalized companies and governmental service providers.

Our industry is highly competitive and requires substantial labor and capital resources. Some of the markets in which we compete or plan to compete are served by one or more large, national companies, as well as by regional and local companies of varying sizes and resources, some of which may have accumulated substantial goodwill in their markets. Some of our competitors may also be better capitalized than we are, have greater name recognition than we do or be able to provide or be willing to bid their services at a lower price than we may be willing to offer. Our inability to compete effectively could hinder our growth or adversely impact our operating results.

We also compete with counties, municipalities and solid waste districts that maintain or could in the future choose to maintain their own waste collection and disposal operations, including through the implementation of flow control ordinances or similar legislation. These operators may have financial advantages over us because of their access to user fees and similar charges, tax revenues, tax-exempt financing or government subsidies.

We may lose contracts through competitive bidding, early termination or governmental action.

We derive a significant portion of our revenues from markets in which we have exclusive arrangements, including municipal contracts. Our municipal contracts are for a specified term and are or will be subject to competitive bidding in the future. Although we intend to bid on additional municipal contracts in our target markets, we may not always, or ever, be the successful bidder. In addition, some or all of our customers, including municipalities, may terminate their contracts with us prior to their scheduled expiration dates. Similar risks may affect contracts that we are awarded to operate municipally owned assets, such as landfills.

Governmental action may also affect our exclusive arrangements. Municipalities may annex unincorporated areas within counties where we provide collection services. As a result, our customers in such annexed areas may be required to obtain services from competitors that have been franchised by the annexing municipalities to provide those services. In

20

addition, municipalities in which we provide services on a competitive basis may elect to franchise those services. Unless we are awarded franchises by these municipalities, we will lose customers. Municipalities may also decide to directly provide services to their residents, on an optional or mandatory basis, which may cause us to lose customers. If we are not able to replace lost revenues resulting from unsuccessful competitive bidding, early termination or the renegotiation of existing contracts with other revenues within a reasonable time period, our results of operations and financial condition could be adversely affected. Additionally, the loss of municipal contracts through competitive bidding, early termination or governmental action could cause long lived tangible and intangible assets to be impaired and require a charge against earnings.

Our results are vulnerable to economic conditions.

Our business and financial results would be harmed by downturns in the general economy, or in the economy of the regions in which we operate as well as other factors affecting those regions. In an economic slowdown, we experience the negative effects of decreased waste generation, increased competitive pricing pressure, customer turnover, reductions in customer service requirements, and customer business closings and bankruptcies. Two lines of business that could see a more immediate impact would be 1) construction and demolition and 2) special waste disposal. In addition, a weaker economy may result in declines in recycled commodity prices. Worsening economic conditions or a prolonged or recurring economic recession could adversely affect our operating results and expected seasonal fluctuations. Further, we cannot assure you that any improvement in economic conditions after such a downturn will result in positive improvement in our operating results or cash flows.

Some of our customers, including governmental entities, have suffered financial difficulties affecting their credit risk, which could negatively impact our operating results.

We provide service to a number of governmental entities and municipalities, some of which have suffered significant financial difficulties due to the downturn in the economy, reduced tax revenue and/or high cost structures. Some of these entities could be unable to pay amounts owed to us or renew contracts with us at previous or increased rates. Many non-governmental customers have also suffered serious financial difficulties, including bankruptcy in some cases. Purchasers of our recyclable commodities can be particularly vulnerable to financial difficulties in times of commodity price volatility. The inability of our customers to pay us in a timely manner or to pay increased rates, particularly large national accounts, could negatively affect our operating results.

Our financial and operating performance may be affected by the inability in some instances to renew landfill permits, obtain new landfills or expand existing ones. Further, the cost of operation and/or future construction of our existing landfills may become economically unfeasible causing us to abandon or cease operations.

We currently own or operate 39 active landfills. Our ability to meet our financial and operating objectives may depend in part on our ability to acquire, lease or renew landfill permits, expand existing landfills and develop new landfill sites. It has become increasingly difficult and expensive to obtain required permits and approvals to build, operate and expand solid waste management facilities, including landfills and transfer stations. Operating permits for landfills in states where we operate generally must be renewed periodically (typically, every five to ten years). These operating permits often must be renewed several times during the permitted life of a landfill pursuant to a process that is often time-consuming, requires numerous hearings and compliance with zoning, environmental and other requirements, is

21