Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - e.l.f. Beauty, Inc. | d179389dex231.htm |

| EX-10.6(C) - EX-10.6(C) - e.l.f. Beauty, Inc. | d179389dex106c.htm |

| EX-3.2 - EX-3.2 - e.l.f. Beauty, Inc. | d179389dex32.htm |

Table of Contents

As filed with the Securities and Exchange Commission on September 19, 2016.

Registration No. 333-213333

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

e.l.f. Beauty, Inc.

(Exact name of Registrant as specified in its charter)

| Delaware | 2844 | 46-4464131 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

570 10th Street

Oakland, CA 94607

(510) 778-7787

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Tarang P. Amin

Chairman and Chief Executive Officer

e.l.f. Beauty, Inc.

570 10th Street

Oakland, CA 94607

(510) 778-7787

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Tad J. Freese, Esq. Kathleen M. Wells, Esq. Latham & Watkins LLP 140 Scott Drive Menlo Park, CA 94025 Telephone: (650) 328-4600 Facsimile: (650) 463-2600 |

Thomas Holden, Esq. Ropes & Gray LLP Three Embarcadero Center San Francisco, CA 94111 Telephone: (415) 315-6300 Facsimile: (415) 315-6350 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. ¨

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||||

| Non-accelerated filer | x | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated September 19, 2016

Preliminary prospectus

e.l.f. Beauty, Inc.

8,333,333 Shares

This is an initial public offering of common stock of e.l.f. Beauty, Inc. The selling stockholders are selling 4,333,333 shares of common stock, and we are selling 4,000,000 shares of our common stock in this offering. We will not receive any proceeds from the sale of shares by the selling stockholders. The estimated initial public offering price is between $14.00 and $16.00 per share. Currently, no public market exists for the shares.

We have been approved to list our common stock on the New York Stock Exchange under the symbol “ELF.”

We are an “emerging growth company” as defined by the Jumpstart Our Business Startups Act of 2012, and we have elected to comply with certain reduced public company reporting requirements for this prospectus and future filings.

| Per share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions(1) |

$ | $ | ||||||

| Proceeds to us, before expenses |

$ | $ | ||||||

| Proceeds to selling stockholders, before expenses |

$ | $ | ||||||

|

|

||||||||

| (1) | See “Underwriting” for additional information regarding underwriting compensation. |

The underwriters may also purchase up to an additional 1,250,000 shares from the selling stockholders, at the initial public offering price, less the underwriting discount for 30 days from the date of this prospectus.

Investing in our common stock involves a high degree of risk. See “Risk factors” beginning on page 12.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on or about , 2016.

| J.P. Morgan | Morgan Stanley |

| Piper Jaffray | Wells Fargo Securities |

| William Blair | Cowen and Company | BMO Capital Markets | Stifel | SunTrust Robinson Humphrey |

The date of this prospectus is , 2016

Table of Contents

Table of Contents

HIGH QUALITY COSMETICS

at an extraordinary value

e.l.f.

Table of Contents

Ability to engage YOUNG, DIVERSE MAKEUP ENTHUSIASTS

@glambyzana

@makeupwithjojo @lorenaurrea_makeup @beautybylex_19 @ashleyvera @stylewidsus @>courtney_laoexo @bellabriellc @melissajoy1987 @khirascottbouch @dardynraemura @kmkmakeup @blushandberries @alexiistherese @_tenaquin @readysetglamour @makemeupzo

@yooyuliya

Table of Contents

e.l.f.

Our Mission

We make luxurious beauty accessible for all women to play beautifully®.

Table of Contents

Table of Contents

| Page | ||||

| ii | ||||

| 1 | ||||

| 7 | ||||

| 9 | ||||

| 12 | ||||

| 39 | ||||

| 40 | ||||

| 41 | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| 46 | ||||

| 53 | ||||

| Management’s discussion and analysis of financial condition and results of operations |

56 | |||

| 71 | ||||

| 92 | ||||

| 99 | ||||

| 113 | ||||

| 116 | ||||

| 119 | ||||

| 124 | ||||

| 128 | ||||

| Material U.S. federal income tax consequences to non-U.S. holders |

130 | |||

| 133 | ||||

| 137 | ||||

| 137 | ||||

| 137 | ||||

| F-1 | ||||

You should rely only on the information contained in this prospectus or in any free writing prospectus we may authorize to be delivered or made available to you. Neither we, the selling stockholders nor the underwriters have authorized anyone to provide you with different information. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus, or any free writing prospectus, as the case may be, or any sale of shares of our common stock.

Through and including , 2016 (the 25th day after the date of this prospectus), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

For investors outside the United States: e.l.f. Beauty, Inc. (the “Company”), the selling stockholders and the underwriters are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. Neither we, the selling stockholders nor the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside the United States.

Numerical figures included in this prospectus have been subject to rounding adjustments. Accordingly, numerical figures shown as totals in various tables may not be arithmetic aggregations of the figures that precede them.

i

Table of Contents

Certain of the market data and other statistical information contained in this prospectus, such as the size, growth and share of the cosmetics industry and its constituent market segments, are based on information from independent industry organizations and other third-party sources, industry publications, surveys and forecasts. Some market data and statistical information contained in this prospectus are also based on management’s estimates and calculations, which are derived from our review and interpretation of the independent sources, our internal market and brand research and our knowledge of the cosmetics industry. Information that is based on estimates, forecasts, projections or similar methodologies is inherently subject to uncertainties, and actual events or circumstances may differ materially from events and circumstances that are assumed in this information.

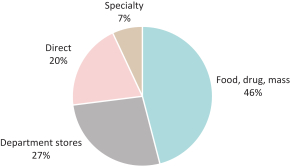

References to e.l.f.’s share of the U.S. mass cosmetics market and top 10 U.S. cosmetics brands and the size and growth rates of the global and U.S. cosmetics category, segment, product and channel and skin care categories refer to retail sales in absolute dollar terms as tracked by Euromonitor International Limited’s Beauty and Personal Care 2016 edition system, published in March 2016 as part of its annual multi-client Passport research program, which includes food, drug and mass (“FDM”), department stores, direct and specialty channels; data reflects current prices and 2015 exchange rates fixed by Euromonitor. References to our retail sales from products launched in the last three years refer to U.S. retail sales across categories as tracked by Nielsen’s XAOC, including C-store database for the 52 weeks ended January 2, 2016 and prior years downloaded in April 2016, which includes the FDM channel. Other statements in this prospectus regarding market data, unless otherwise noted, are based on studies conducted by Calimesa Consulting Partners, LLC and MetrixLab, which we commissioned. These studies were based on surveys of a broad sampling of cosmetics consumers.

For the purposes of this prospectus:

| • | “aided awareness” is a measure of the number of people who express knowledge of a brand or product when prompted; |

| • | “cosmetics” market segment refers to the market segment defined as Color Cosmetics by Euromonitor International Limited and consists of face makeup, eye makeup, lip products, nail products and color cosmetics sets/kits; |

| • | “e-commerce” channel refers to the channel defined as Internet Retailing by Euromonitor International Limited; and FDM and specialty channels are per Company definitions based on Euromonitor International Limited data; |

| • | “heaviest” purchasers or users refers to consumers who identified themselves as professional, expert or enthusiast in the study conducted by MetrixLab; |

| • | “incremental sales” refer to consumers buying e.l.f. products as additional cosmetics purchases at retail stores as opposed to diverting sales from another brand; |

| • | “prestige” market segment refers to the market segment defined as Premium by Euromonitor International Limited; |

| • | “retail sales” refers to the purchase price paid by the end consumer; |

| • | “share” refers to e.l.f.’s market share based on e.l.f.’s net sales in comparison to retail sales in absolute dollar terms; and |

| • | “unaided awareness” is a measure of the number of people who express knowledge of a brand or product without prompting. |

ii

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all the information that you should consider before deciding to invest in our common stock. You should read the entire prospectus carefully, including “Risk factors” and our consolidated financial statements and related notes included elsewhere in this prospectus, before making an investment decision. In this prospectus, the terms “e.l.f.,” “we,” “us,” “our” and the “Company” refer to e.l.f. Beauty, Inc. and its consolidated subsidiaries.

e.l.f.: Changing the face of beauty

We are one of the fastest growing, most innovative cosmetics companies in the United States. Driven by our mission to make luxurious beauty accessible for all women to play beautifully®, we have challenged the traditional belief that quality cosmetics are only available at high prices in select channels. e.l.f. offers high-quality, prestige-inspired beauty products for eyes, lips and face at extraordinary value, with the majority of our items retailing for $6 or less. Our price points encourage trial and experimentation, while our commitment to quality and a differentiated consumer engagement model engender loyalty among a passionate and vocal group of consumers. We have built an authentic brand and a company with strong growth, margins and cash flow from operations.

We believe our success is rooted in our innovation process and ability to build direct consumer relationships. Born as an e-commerce company over a decade ago, we have created a modern consumer engagement and responsive innovation model that keeps our products on-trend and our consumers engaged as brand ambassadors. Our consumers provide us with real-time feedback through reviews and social media, which enables us to refine and augment our product portfolio in response to their needs. We leverage our fast-cycle product development and asset-light supply chain to launch high-quality products in as few as 20 weeks from concept, and 27 weeks on average. Our products are first launched on elfcosmetics.com, and distribution is generally only broadened to our retail customers after we receive strong consumer validation online. We believe this has led to our consistently strong retail sales per linear foot of shelf space, which we refer to as “productivity.” We are one of the fastest growing cosmetics brands at Target, Walmart and CVS.

Our brand appeals to some of the most sought after consumers in the category. We believe the combination of our affordable price points and on-trend, innovative product assortment encourages trial, offers a strong value proposition and appeals to a broad base of consumers. Relative to the overall cosmetics category, our brand over-indexes with Millennials, multi-cultural consumers and some of the heaviest users in the category. This attractive and loyal consumer base supports high sales per linear foot and higher category sales for our retail customers. By combining our strong relationships with leading retailers with integrated consumer engagement across our e.l.f. stores, e-commerce and social media, we are a true multi-channel brand.

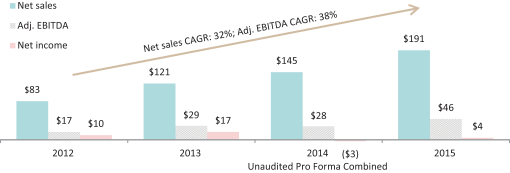

Our net sales growth in the United States over the last three years was 20 times that of the mass cosmetics category on average. Our net sales still only represented 2.3% of the $8 billion U.S. mass cosmetics category in 2015. Our net sales grew from $144.9 million in the Unaudited Pro Forma Combined 2014 Period (as defined in “Management’s discussion and analysis of financial condition and results of operations”) to $191.4 million in the year ended December 31, 2015, and, over the same period, our Adjusted EBITDA grew from $28.1 million to $46.2 million, representing an increase of 32% and 64%, respectively. Over the same period, net income grew from an unaudited pro forma combined net loss of $2.9 million to a net profit of $4.4 million. In 2015, our Adjusted EBITDA margin was 24% and our net income margin was 2%.1

| 1 | Adjusted EBITDA and Adjusted EBITDA margin are not measurements of financial performance under generally accepted accounting principles in the United States (“GAAP”). See “Summary consolidated financial data” for a discussion of Adjusted EBITDA, Adjusted EBITDA margin and their respective limitations and reconciliations to GAAP measures. |

1

Table of Contents

The cosmetics industry is large and attractive

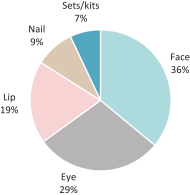

We believe that the cosmetics category is highly attractive given its scale, growth dynamics and consumer demand trends. The U.S. and global cosmetics markets generated $14 billion and $57 billion, respectively, of retail sales in 2015. The cosmetics category primarily consists of face makeup, eye makeup, lip products, nail products and cosmetics sets/kits and excludes beauty tools and accessories such as brushes and applicators. The cosmetics category has experienced strong growth both in the United States and globally. In the United States, retail sales increased from $11 billion in 2010 to $14 billion in 2015, representing a compound annual growth rate (“CAGR”) of 5% with each product category driving growth. Globally, retail sales increased from $43 billion in 2010 to $57 billion in 2015, representing a CAGR of 5%. Drivers of growth include innovation and new product launches, which span from new formulations that enhance performance, feel and fragrance, to new colors, delivery forms and packaging.

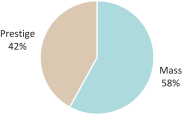

In the United States, the cosmetics category traditionally has been separated into two discrete segments—prestige and mass. Prestige products, which accounted for 42% of U.S. cosmetics retail sales in 2015, are characterized by higher price points and are typically sold in department stores and in high-end specialty stores such as Sephora. They have historically been at the forefront of quality and innovation in the category but remain too expensive for many consumers in the United States, where the average disposable personal income is less than $15,000. Mass products, which generated 58% of 2015 U.S. cosmetics retail sales, are more affordable than their prestige counterparts but generally have not delivered the same level of quality or innovation. They are more broadly available than prestige products given their presence in the food, drug and mass (“FDM”) channel. As observed in recent years, consumers are increasingly purchasing both prestige and mass cosmetics products, and consistent with many other consumer categories, are purchasing online. e-commerce accounted for 10% of U.S. cosmetics retail sales in 2015 and grew at three times the rate of the broader category from 2010 to 2015.

We believe that a paradigm shift has occurred in cosmetics: today’s cosmetics consumer is increasingly connected and informed, and purchasing decisions are often influenced by friends, beauty bloggers, social media and other online content. These sources provide consumers easy access to a breadth and depth of information formerly only available from beauty experts in assisted sales environments.

While most women regularly use cosmetics, the heaviest purchasers drive the category. These consumers represent 36% of cosmetics purchasers, yet accounted for 54% of U.S. cosmetics sales in 2014. For these women, cosmetics is a passion. They enjoy learning about and trying new products, and shopping for and wearing makeup. The entire experience is fun and an integral part of their lifestyle. We seek to fulfill their needs by delighting them with the quality and innovation they desire at prices they can afford.

Our strategic differentiation: how e.l.f. helps women to play beautifully

We are driven by what today’s consumer wants—an assortment of high-quality, prestige-inspired cosmetics at extraordinary value. We do not define ourselves as strictly mass or prestige, or limit our product availability to select channels. Through our modern consumer engagement and responsive innovation model, we interact with our consumers instead of broadcasting at them. This allows us to stay in tune with their needs and build trust and loyalty. Our business model has multiple areas of competitive advantage:

Authentic brand that attracts some of the best consumers in the category. e.l.f. was founded to fill the gap between high-priced prestige beauty products and less innovative mass products. For over a decade, we have prioritized getting to know our consumers, and they in turn have provided us with valuable feedback, enabling us to address this gap and build e.l.f. into an authentic and trusted brand. By providing a comprehensive experience—from integrated engagement online, through social media and in our stores to our differentiated product offerings—we have drawn a strong following among the most sought after and heaviest users of cosmetic products. We also have strong appeal with Millennials and Hispanics, two of the fastest growing demographic groups in the United States. Our consumers have also been our best advocates, growing the e.l.f. brand virally through strong word of mouth.

High-quality cosmetics at an extraordinary value enabled by flexible, asset-light operations. e.l.f. consumers recognize our ability to provide a broad assortment of high-quality products at an extraordinary value. The majority of our items retail for $6 or less, providing a low-risk way for consumers to try new products. Examples of our high-quality and extraordinary value innovations include e.l.f. Mineral Infused Face Primer at $6 versus a prestige primer at $36, e.l.f. Baked Eyeshadow Trio at $4 versus a competitive baked eyeshadow trio at $28 and e.l.f. Lip Exfoliator at $3 versus a similar type of lip

2

Table of Contents

treatment at $24. Our low price points are supported by our ability to source low cost, high-quality cosmetics quickly. As of August 2016, we had 48 e.l.f. professionals involved in sourcing, quality and innovation. We have longtime relationships with strategic vendors that pair a strong quality orientation with the ability to execute rapidly. Our supply chain is built for growth with asset-light operations, ample capacity and low capital requirements. This capability and commitment to an agile supply chain allows us to introduce a stream of on-trend innovation. Our consumers’ love of our high-quality, innovative products is shown through the online reviews posted on elfcosmetics.com, where 66% of 2015 reviews were five stars, the highest rating.

Fast-cycle innovation and validation model. We believe innovation is key to our success and that we are a leader in the industry in speed and new product introductions. We have built an innovation capability that can progress a new, high-quality e.l.f. product to online launch in as few as 20 weeks from concept, and 27 weeks on average. In 2015, we introduced over 50 new items across eyes, lips, face, tools, kits and skin care, and 40% of our retail sales came from products launched in the last three years (based on data from Nielsen). With 25 million visits per year and over 100,000 online reviews, elfcosmetics.com is a vehicle for refining products and determining best sellers. We are able to analyze sales results, reviews and feedback through social media to provide a quick indication of a product’s performance. Not only does this fast, high-output, testing methodology result in leading performance in retail, it also contributes to building our consumer relationships. We believe our active dialogue with our consumers provides us with a highly differentiated perspective on innovation and informs the continuous launch, validation and refinement of our products.

True multi-channel brand blurs the lines between mass and prestige. We are a true multi-channel brand with strength across e-commerce, national retailers and our e.l.f. stores. Our ability to engage our consumers across multiple touch points differentiates e.l.f. from traditional mass brands, which typically focus on one channel. We also leverage insights gained from each channel to drive performance across the business.

| • | e-commerce. elfcosmetics.com has the highest revenue, traffic, time spent on-site and units per transaction of any mass cosmetics brand website based on data from the Internet Retailer eCommerce 500 report and Alexa Internet Inc. Our e-commerce business serves as a strong source of sales and an important component of our engagement and innovation model. We have nurtured a loyal, highly active online community for over a decade. |

| • | National retailers. We currently sell our products in approximately 19,000 retail stores in the United States across mass, drug store, food and specialty retail channels. At Target, our longest-standing national retail customer and a key beauty destination for many consumers, we achieved double digit growth in retail sales from 2014 to 2015. We have also continued to expand with Walmart, the world’s largest retailer and an e.l.f. customer since 2012. We introduced e.l.f. at Old Navy in 2014 and at CVS in 2015 and expect to continue to grow distribution due to our compelling retailer value proposition. |

| • | e.l.f. stores. We were the first mass cosmetics brand with our own stores, which we believe serve as one of our most effective and efficient vehicles for marketing and consumer engagement. e.l.f. stores showcase a broad assortment of e.l.f. products, create an environment dedicated to play beautifully, and allow us to test and validate new products. As of August 2016, we had nine e.l.f. stores in the New York metro area located in high-traffic malls and urban areas. |

High-performance team and culture. Our CEO Tarang Amin joined us in January 2014, and under his leadership we have assembled a world-class management team that possesses an excellent track record of results and has successfully worked together for many years. During the team’s prior tenure at Schiff Nutrition International, Inc. (New York Stock Exchange: SHF) (“Schiff Nutrition”), the company grew in enterprise value from $190 million to $1.5 billion in less than two years and was acquired by Reckitt Benckiser (London Stock Exchange: RB). With strong backgrounds from The Clorox Company, The Procter & Gamble Company, L’Oreal S.A., Mary Kay Inc., TPG Global, LLC (together with its affiliates, “TPG”) and other leading companies, our team has demonstrated skills in building brands, leading innovation, expanding distribution, making acquisitions and driving world-class operations. We operate with a high-performance team culture. We communicate with great candor and transparency in the spirit of helping the team succeed, make quick decisions and drive executional excellence. The combination of a talented team, strong culture and values and disciplined execution forms the foundation of our success.

3

Table of Contents

The e.l.f. growth strategy

We believe e.l.f. is one of the most disruptive brands in the cosmetics industry. We are in the early stages of development, with significant room to grow by converting more consumers to the brand, making e.l.f. products more widely available and offering more innovative products to our consumers. We expect the United States to be the largest source of our growth over the next few years and also see an opportunity to expand in select international markets. We also believe we have an opportunity to improve our margins through greater operating leverage and efficiency.

We have made substantial investments over the last two years and believe we are well positioned for continued growth driven by four strategies.

| 1. | Build a great brand |

Draw new consumers to the brand. We have a loyal consumer following, as illustrated by our repeat purchase rates which are among the highest in the industry: 58% of our consumers purchase one or more additional products within 12 months of initial purchase. We believe we can significantly grow this following of passionate consumers from current levels. Increasing brand awareness is a major growth driver for our company, as it has historically led to strong trial and high repeat purchase rates. e.l.f. is still unknown to many women, with only 6% unaided and 58% aided awareness as of August 2015. In contrast, many traditional brands have unaided awareness close to 40% and aided awareness close to 100%. We plan to continue to drive awareness and draw consumers to the brand.

Encourage current consumers to use more e.l.f. products. Our consumers’ loyalty to the e.l.f. brand drives growth through increased usage of our products across categories and advocacy of our brand to other potential consumers. Many of our consumers regularly visit elfcosmetics.com, where in 2015 they bought over nine units per transaction on average. We have designed our product assortment to encourage cross-category purchases across eyes, lips, face, tools and skin care. We find that consumers often enter the brand through one of our lower priced items and then purchase other e.l.f. products across categories once they understand our extraordinary value proposition. Our consumers also seek out our innovation, buying new products both online and in stores. We believe that through sustained innovation and efficient marketing, we will increase the number of e.l.f. items our consumers purchase.

| 2. | Lead innovation |

Use innovation to drive sales and margin. We have a track record of bringing prestige-inspired innovation quickly to the mass channel. We expect to continue to leverage our rapid innovation and flexible supply chain to introduce new products across the eyes, lips, face and tools categories. We believe our innovation has also led consumers to purchase products at higher price points while still delivering an extraordinary value. Many consumers who first tried a $1 item have now migrated to $3 to $8 items, which often have higher margins than our less expensive products.

Expand into skin care and relevant adjacencies. We have successfully brought a prestige-like approach to mass cosmetics at extraordinary value. We believe there are opportunities to use this same approach in other beauty categories, leveraging our brand equity and relationship with e.l.f. enthusiasts to extend our brand into adjacent segments. One such category is skin care, which generated $16 billion in retail sales in the United States and $110 billion globally in 2015. We recently introduced a high-quality skin care line retailing for just $4 to $12 per product, a fraction of the price of prestige brands. We plan to capitalize on our innovation expertise to develop new products in other adjacent categories.

| 3. | Expand brand penetration |

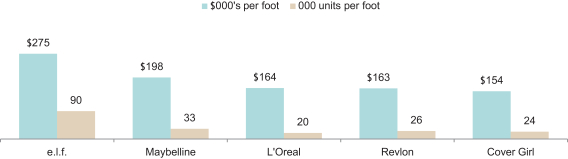

Grow space allocation with our existing national retailers. We have significant potential upside in deepening distribution with our existing retailers by continuing to leverage our productivity, innovation and growth to win more shelf space. Even at our largest customers, e.l.f. is currently in less than 6% of the space allocated to cosmetics despite having among the highest productivity in the category. While certain legacy cosmetics brands have an average of 15 to 18 feet of inline space in major retailers, e.l.f.’s average is only five feet. We believe that our strong performance will enable our shelf presence in our current retailers to become larger over time.

Increase number of new customers. We are one of the fastest growing cosmetics brands at Target, Walmart and CVS, and our growth rates and productivity are among the highest in the industry. We have major distribution whitespace, as

4

Table of Contents

we are currently in only approximately 19,000 national retail stores in the United States and believe there are thousands of additional stores available to us.

Grow our direct-to-consumer business. We plan to grow elfcosmetics.com by driving traffic and conversion. In addition, our e.l.f. stores have been highly productive and profitable. As of August 2016, we operated nine stores in the New York metro area and we plan to selectively open more e.l.f. stores nationally in high-traffic areas.

Expand internationally. We operate in a number of countries outside the United States, which accounted for 7% of our net sales in 2015. Given the portability of the e.l.f. brand, we believe that we have a significant opportunity in international markets over the long term.

| 4. | Drive world-class operations |

Leverage high-performance team culture and execution capability. We have made significant investments in our business over the past two years by hiring top talent and building functional capabilities. Our management team comes from leading consumer packaged goods companies and has experience implementing growth strategies and driving operational improvements. We believe what differentiates us from many traditional cosmetics companies is our ability to make fast decisions and execute with excellence. We believe we have a major speed-to-market advantage over many other companies and are highly responsive to retail customer and consumer needs. We will continue to leverage our executional excellence as we seek to become the preferred partner of our key customers.

Drive operating margins and efficiencies. We have built a low-cost, quality-oriented supply chain with ample capacity to support future growth. We intend to grow our margins by pursuing additional cost savings opportunities and enhancing our product mix through innovation. We also expect to benefit from operating leverage as we scale the business.

Risks associated with our business

Investing in our stock involves a high degree of risk. You should carefully consider the risks described in “Risk factors” before making a decision to invest in our common stock. If any of these risks actually occurs, our business, financial condition and results of operations would likely be materially adversely affected. In such case, the trading price of our common stock would likely decline and you may lose part or all of your investment. Below is a summary of some of the principal risks we face:

| • | The cosmetics industry is highly competitive, and if we are unable to compete effectively our results will suffer. |

| • | Our new product introductions may not be as successful as we anticipate. |

| • | We depend on a limited number of retailers for a large portion of our net sales, and the loss of one or more of these retailers, or business challenges at one or more of these retailers, could adversely affect our results of operations. |

| • | Our success depends, in part, on the quality, performance and safety of our products. |

| • | We may not be able to successfully implement our growth strategy. |

| • | Our growth and profitability are dependent on trends that may change or not continue, and our historical growth may not be indicative of our future growth. |

| • | We may be unable to manage our growth effectively, which would harm our business, financial condition and results of operations. |

| • | Any damage to our reputation or brand may materially and adversely affect our business, financial condition and results of operations. |

| • | A disruption in our operations could materially and adversely affect our business. |

| • | We are dependent on third-party suppliers, manufacturers, distributors and other vendors. |

| • | We may not be able to adequately protect intellectual property and other proprietary rights in our products and may be subject to claims that we infringe or misappropriate the rights of others. |

5

Table of Contents

| • | We have significant operations in China, which exposes us to risks inherent in doing business there. |

| • | We will not be required to comply with certain provisions of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”) for as long as we remain an “emerging growth company.” |

Implications of being an emerging growth company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). As a result, we are permitted to, and intend to, rely on exemptions from certain disclosure requirements that are applicable to other companies that are not emerging growth companies. Accordingly, we have included compensation information for only our four most highly compensated executive officers and have not included a compensation discussion and analysis of our executive compensation programs in this prospectus. In addition, for so long as we are an emerging growth company, we will not be required to:

| • | engage an independent registered public accounting firm to report on our internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act; |

| • | comply with any requirement that may be adopted by the Public Company Accounting Oversight Board (the “PCAOB”) regarding mandatory audit firm rotation or a supplement to the independent registered public accounting firm’s report providing additional information about the audit and the financial statements (i.e., an auditor discussion and analysis); |

| • | submit certain executive compensation matters to stockholder advisory votes, such as “say-on-pay,” “say-on-frequency” and “say-on-golden parachutes;” or |

| • | disclose certain executive compensation related items such as the correlation between executive compensation and performance and comparisons of the chief executive officer’s compensation to median employee compensation. |

We will remain an emerging growth company until the earliest to occur of:

| • | our reporting of $1.0 billion or more in annual gross revenue; |

| • | our issuance, in any three-year period, of more than $1.0 billion in non-convertible debt; |

| • | our becoming a “large accelerated filer;” and |

| • | the end of fiscal 2021. |

The JOBS Act permits an emerging growth company such as us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We are choosing to “opt out” of this provision, and, as a result, we will comply with new or revised accounting standards as required when they are adopted. This decision to opt out of the extended transition period under the JOBS Act is irrevocable.

Our sponsor

TPG Growth II Management, LLC (“TPG Growth” or our “Sponsor”) has been our principal financial backer since its acquisition of the Company in January 2014. TPG Growth is the middle market and growth equity investment platform of TPG, a leading global private investment firm founded in 1992 with approximately $73 billion of assets under management as of June 30, 2016. With more than $7 billion in assets under management and committed capital, TPG Growth targets investments in a broad range of industries and geographies, with a significant focus on the United States and large, emerging markets such as China, India, Brazil, Turkey, Africa and Southeast Asia.

Our corporate information

We were incorporated in Delaware on December 20, 2013 under the name J.A. Cosmetics Holdings, Inc. In April 2016, we changed our name to e.l.f. Beauty, Inc. Our principal offices are located at 570 10th Street, Oakland, California 94607. Our telephone number is (510) 778-7787. We maintain a website at www.elfcosmetics.com. The reference to our website is intended to be an inactive textual reference only. The information contained on, or that can be accessed through, our website is not part of this prospectus.

6

Table of Contents

| Issuer |

e.l.f. Beauty, Inc. |

| Common stock offered by us |

4,000,000 shares. |

| Common stock offered by the selling stockholders |

4,333,333 shares. |

| Common stock to be outstanding after this offering |

44,379,833 shares. |

| Underwriters’ option to purchase additional shares |

1,250,000 shares. |

| Use of proceeds |

We estimate that the net proceeds from the sale of shares of common stock in this offering by us will be approximately $52.3 million at an assumed initial public offering price of $15.00 per share (the mid-point of the price range set forth on the cover page of this prospectus), after deducting the underwriting discounts and commissions and estimated offering expenses payable by us. |

| We currently expect to use the net proceeds from the sale of shares of common stock in this offering by us to repay existing indebtedness and any proceeds remaining thereafter will be used for working capital and general corporate purposes. See “Use of proceeds” on page 41 for a more complete description of the intended use of proceeds from this offering. We will not receive any of the proceeds from the sale of shares by the selling stockholders. |

| Directed share program |

At our request, the underwriters have reserved up to 5% of the shares of common stock offered by this prospectus for sale, at the initial public offering price, to our directors, officers and other individuals associated with them, and our employees, to the extent permitted by local securities laws and regulations. The sales will be made at our direction by Morgan Stanley & Co. LLC, an underwriter of this offering, and its affiliates through a directed share program. We do not know if these persons will choose to purchase all or any portion of these reserved shares, but any purchases they do make will reduce the number of shares available to the general public. Any reserved shares not so purchased will be offered by the underwriters to the general public on the same terms as the other shares of common stock offered by this prospectus. Any shares sold in the directed share program to our directors, executive officers or stockholders who have entered into lock-up agreements described in “Underwriting” shall be subject to the provisions of such lock-up agreements. Other participants in the directed share program shall be subject to substantially similar lock-up provisions with respect to any shares sold to them pursuant to the directed share program. |

| Risk factors |

Investing in shares of our common stock involves a high degree of risk. See “Risk factors” beginning on page 12 of this prospectus for a discussion of factors you should carefully consider before investing in shares of our common stock. |

| Trading symbol |

“ELF.” |

In this prospectus, the number of shares of our common stock to be outstanding after this offering is based on the number of shares of our common stock outstanding as of June 30, 2016, and excludes:

| • | 4,796,225 shares of common stock issuable upon exercise of stock options outstanding as of June 30, 2016 under our 2014 Equity Incentive Plan (the “2014 Equity Plan”) at a weighted average exercise price of $2.01 per share (as adjusted for the special dividend declared on June 7, 2016 as described under “Dividend policy”); |

7

Table of Contents

| • | 1,583,466 shares of common stock reserved as of June 30, 2016 for future issuance under our 2014 Equity Plan; |

| • | 5,430,690 shares of common stock reserved for issuance pursuant to future awards under our 2016 Equity Incentive Award Plan (the “2016 Plan”), from which we will grant 596,217 restricted stock units in the aggregate and options to purchase an aggregate of 1,250,517 shares of our common stock with an exercise price per share equal to the initial public offering price to certain officers, employees and directors upon the pricing of this offering, as well as any automatic increases in the number of shares of our common stock reserved for future issuance under this plan, which will become effective immediately prior to the effectiveness of the registration statement of which this prospectus forms a part; |

| • | 905,115 shares of common stock reserved for issuance pursuant to future awards under our 2016 Employee Stock Purchase Plan (the “ESPP”), as well as any automatic increases in the number of shares of our common stock reserved for future issuance under this plan, which will become effective immediately prior to the effectiveness of the registration statement of which this prospectus forms a part; and |

| • | 220,800 shares of common stock reserved for issuance pursuant to the settlement of phantom shares issued pursuant to our 2014 Phantom Equity Plan (as amended, the “Phantom Plan”) in shares of our common stock. |

Unless otherwise indicated, this prospectus reflects and assumes:

| • | the conversion of all of our outstanding shares of convertible preferred stock as of June 30, 2016 into an aggregate of 37,271,375 shares of common stock immediately prior to the consummation of this offering; |

| • | the filing of our amended and restated certificate of incorporation and the adoption of our amended and restated bylaws, which will occur immediately prior to the consummation of this offering; |

| • | no exercise by the underwriters of their over-allotment option to purchase additional shares of common stock; |

| • | a 2.76:1 forward stock split of our common stock effected on September 19, 2016; and |

| • | no exercise of outstanding options after June 30, 2016. |

8

Table of Contents

Summary consolidated financial data

The following table presents our summary consolidated financial data for the periods and as of the dates indicated. The periods prior to and including January 31, 2014 include all of the accounts of e.l.f. Cosmetics, Inc. (formerly known as J.A. Cosmetics US, Inc.) and its subsidiaries and are referred to in the following table as “Predecessor,” and all periods after January 31, 2014 include all of the accounts of e.l.f. Beauty, Inc. and its subsidiaries and are referred to in the following table as “Successor.” The summary consolidated financial data as of December 31, 2014 and 2015, and for the period from January 1, 2014 through January 31, 2014, the period from February 1, 2014 through December 31, 2014 and the year ended December 31, 2015, has been derived from the audited consolidated financial statements included elsewhere in this prospectus. The summary consolidated financial data as of June 30, 2016, and for the six months ended June 30, 2015 and 2016, has been derived from the unaudited condensed consolidated financial statements included elsewhere in this prospectus. Our unaudited condensed consolidated financial statements were prepared on a basis consistent with our audited consolidated financial statements and include, in management’s opinion, all normal recurring adjustments necessary for fair presentation of the financial information set forth in those statements. The summary consolidated financial data for the years ended December 31, 2012 and 2013 have been derived from the Predecessor’s audited consolidated financial statements which are not included in this prospectus and is presented in order to provide a reconciliation from net income to Adjusted EBITDA for these periods.

You should read the following financial information together with the information under “Capitalization,” “Selected consolidated financial data” and “Management’s discussion and analysis of financial condition and results of operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus.

| Predecessor | Successor | Unaudited pro forma combined(1) |

Successor | |||||||||||||||||||||

| (dollars in thousands, except share and per share amounts) |

Period from January 1, 2014 through January 31, 2014 |

Period from February 1, 2014 through December 31, 2014 |

Year ended December 31, 2014 |

Year ended December 31, 2015 |

Six months ended June 30, 2015 |

Six months ended June 30, 2016 |

||||||||||||||||||

| Statement of operations data: |

||||||||||||||||||||||||

| Net sales |

$ | 9,810 | $ | 135,134 | $ | 144,944 | $ | 191,413 | $ | 75,194 | $ | 96,820 | ||||||||||||

| Gross profit |

4,772 | 61,450 | 67,496 | 100,329 | 39,298 | 54,437 | ||||||||||||||||||

| Operating income |

1,727 | 5,347 | 16,119 | 25,571 | 8,130 | 6,633 | ||||||||||||||||||

| Other income (expense), net |

36 | (6,633 | ) | (6,597 | ) | (4,172 | ) | 3,254 | 1,964 | |||||||||||||||

| Interest expense |

(128 | ) | (11,545 | ) | (12,546 | ) | (12,721 | ) | (6,281 | ) | (6,396 | ) | ||||||||||||

| Income (loss) before provision for income taxes |

1,635 | (12,831 | ) | (3,024 | ) | 8,678 | 5,103 | 2,201 | ||||||||||||||||

| (Provision) benefit for income taxes |

(542 | ) | 3,545 | 143 | (4,321 | ) | (2,425 | ) | (1,112 | ) | ||||||||||||||

| Net income (loss) |

$ | 1,093 | $ | (9,286 | ) | $ | (2,881 | ) | $ | 4,357 | $ | 2,678 | $ | 1,089 | ||||||||||

| Net income (loss) per share—basic |

$ | 1,093 | $ | (709 | ) | $ | (512 | ) | $ | (1,560 | ) | $ | (116 | ) | $ | (200 | ) | |||||||

| Net income (loss) per share—diluted |

$ | 1,088 | $ | (709 | ) | $ | (512 | ) | $ | (1,560 | ) | $ | (116 | ) | $ | (200 | ) | |||||||

| Weighted average number of shares outstanding—basic |

1,000 | 27,593 | 27,593 | 30,523 | 27,593 | 651,268 | ||||||||||||||||||

| Weighted average number of shares outstanding—diluted |

1,005 | 27,593 | 27,593 | 30,523 | 27,593 | 651,268 | ||||||||||||||||||

| Other data: |

||||||||||||||||||||||||

| EBITDA(2) |

1,804 | 6,658 | 18,190 | 31,688 | 15,980 | 14,827 | ||||||||||||||||||

| Adjusted EBITDA(2) |

2,087 | 26,013 | 28,100 | 46,178 | 16,300 | 19,964 | ||||||||||||||||||

| Adjusted EBITDA margin |

21.3% | 19.2% | 19.4% | 24.1% | 21.7% | 20.6% | ||||||||||||||||||

| Depreciation and amortization |

41 | 7,944 | 8,668 | 10,289 | 4,595 | 6,230 | ||||||||||||||||||

| Capital expenditures |

19 | 1,597 | 1,616 | 10,242 | 3,649 | 2,910 | ||||||||||||||||||

|

|

||||||||||||||||||||||||

| (1) | For the purpose of performing a comparison to the Successor’s year ended December 31, 2015, we have prepared Unaudited Pro Forma Combined Supplemental Financial Information for the year ended December 31, 2014, which gives effect to the acquisition of 100% of the outstanding shares of capital stock of the Predecessor by the Successor, as if it had occurred on January 1, 2014 (the “Unaudited Pro Forma Combined 2014 Period”). The Unaudited Pro Forma Combined 2014 Period is being discussed herein for informational purposes only and does not reflect any operating efficiencies or potential cost savings that may result from the consolidation of operations. The amounts in the Predecessor and Successor columns do not total to the amounts in the unaudited pro forma combined column due to the adjustments made in preparing the Unaudited Pro Forma Combined 2014 Period, which are described in “Management’s discussion and analysis of financial conditions and results of operations—Recent transactions and basis of presentation.” |

9

Table of Contents

| (2) | EBITDA represents net income (loss) plus interest expense, provision (benefit) for income taxes and depreciation and amortization. Adjusted EBITDA represents EBITDA further adjusted to exclude the impact of other items that management does not believe are reflective of the Company’s ongoing operations (comprising transaction-related expenses incurred in connection with the acquisition of the Predecessor, the restructuring of our operations, including warehouse transition and reorganization of our operations in China, and the preparation for our initial public offering), stock-based compensation expense, management fees paid to our Sponsor, costs associated with e.l.f. stores incurred prior to the store opening (including legal-related costs, rent and occupancy expenses, marketing and other store operating supply expenses), costs associated with securing additional distribution space (including slotting expense, freight and certain costs related to installation of fixtures), costs related to the evaluation of an acquisition in 2014, certain non-cash losses and write-offs, and gains and losses on our foreign currency contracts as reflected in the reconciliation below. |

We present EBITDA and Adjusted EBITDA because our management uses these as supplemental measures in assessing our operating performance, and we believe they are helpful to investors, securities analysts and other interested parties in evaluating the performance of companies in our industry. We also believe EBITDA and Adjusted EBITDA are useful to management and investors, securities analysts and other interested parties as measures of our comparative operating performance from period to period. EBITDA and Adjusted EBITDA are not measurements of financial performance under GAAP. They should not be considered as alternatives to cash flow from operating activities, as measures of liquidity, or as alternatives to net income as a measure of our operating performance or any other measures of performance derived in accordance with GAAP. In addition, EBITDA and Adjusted EBITDA should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. EBITDA and Adjusted EBITDA have limitations as analytical tools, and you should not consider such measures either in isolation or as substitutes for analyzing our results as reported under GAAP. Our definitions and calculations of EBITDA and Adjusted EBITDA are not necessarily comparable to other similarly titled measures used by other companies due to different methods of calculation.

The following table provides a reconciliation of EBITDA and Adjusted EBITDA to net income (loss):

| Predecessor | Successor | Unaudited pro forma combined |

Successor | |||||||||||||||||||||||||||||||||

| (dollars in thousands) | Year ended December 31, 2012 |

Year ended December 31, 2013 |

Period from January 1, 2014 through January 31, 2014 |

Period from February 1, 2014 through December 31, 2014 |

Year ended December 31, 2014 |

Year ended December 31, 2015 |

Six months ended June 30, 2015 |

Six months ended June 30, 2016 |

||||||||||||||||||||||||||||

| Net income (loss) |

$ | 9,897 | $ | 16,555 | $ | 1,093 | $ | (9,286 | ) | $ | (2,881 | ) | $ | 4,357 | $ | 2,678 | $ | 1,089 | ||||||||||||||||||

| Interest expense |

610 | 1,637 | 128 | 11,545 | 12,546 | 12,721 | 6,281 | 6,396 | ||||||||||||||||||||||||||||

| Provision (benefit) for income taxes |

6,275 | 9,211 | 542 | (3,545 | ) | (143 | ) | 4,321 | 2,425 | 1,112 | ||||||||||||||||||||||||||

| Depreciation and amortization |

395 | 538 | 41 | 7,944 | 8,668 | 10,289 | 4,595 | 6,230 | ||||||||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||||||||||||||

| EBITDA |

$ | 17,177 | $ | 27,941 | $ | 1,804 | $ | 6,658 | $ | 18,190 | $ | 31,688 | $ | 15,980 | $ | 14,827 | ||||||||||||||||||||

| Transaction-related expenses(a) |

— | 194 | 63 | 9,759 | 94 | 705 | 579 | — | ||||||||||||||||||||||||||||

| Cost related to “restructuring” of operations(b) |

— | — | — | 370 | 370 | 1,595 | 420 | 3,844 | ||||||||||||||||||||||||||||

| Initial public offering preparation costs |

— | — | — | — | — | 1,144 | 318 | 395 | ||||||||||||||||||||||||||||

| Stock-based compensation |

— | 26 | — | 287 | 287 | 503 | 197 | 1,155 | ||||||||||||||||||||||||||||

| Management fee(c) |

233 | 250 | — | 775 | 775 | 854 | 350 | 475 | ||||||||||||||||||||||||||||

| Pre-opening costs(d) |

— | 118 | 15 | 180 | 195 | 64 | 59 | 229 | ||||||||||||||||||||||||||||

| Customer expansion costs(e) |

— | — | — | — | — | 1,191 | 879 | 350 | ||||||||||||||||||||||||||||

| Other miscellaneous items(f) |

— | — | — | 1,104 | 1,104 | 530 | — | — | ||||||||||||||||||||||||||||

| Unrealized losses (gains) on foreign currency contracts(g) |

— | — | 205 | 6,880 | 7,085 | 7,904 | (2,482 | ) | (1,311 | ) | ||||||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||||||||||||||

| Adjusted EBITDA |

$ | 17,410 | $ | 28,529 | $ | 2,087 | $ | 26,013 | $ | 28,100 | $ | 46,178 | $ | 16,300 | $ | 19,964 | ||||||||||||||||||||

| (a) | Represents transaction-related expenses related to the acquisition of the Predecessor. |

| (b) | Represents costs associated with the restructuring of our operations, including warehouse transition and reorganization of our operations in China. |

| (c) | Represents management fees paid to our Sponsor. |

| (d) | Represents costs associated with e.l.f. stores incurred prior to the store opening, including legal-related costs, rent and occupancy expenses, marketing and other store operating supply expenses. |

10

Table of Contents

| (e) | Represents costs associated with securing additional distribution space, including slotting expense, freight and certain costs related to installation of fixtures. |

| (f) | Represents costs related to evaluation of an acquisition in 2014 as well as other non-cash losses and write-offs. |

| (g) | Represents non-cash (gains) / losses on our foreign currency contracts. |

| Successor | ||||||||||||

| As of December 31, | As of June 30, | |||||||||||

| (dollars in thousands) | 2014 | 2015 | 2016 | |||||||||

| Balance sheet data: |

||||||||||||

| Cash and cash equivalents |

$ | 4,668 | $ | 14,004 | $ | 3,763 | ||||||

| Net working capital(3) |

23,218 | 10,860 | 16,007 | |||||||||

| Property and equipment, net |

2,125 | 9,854 | 14,281 | |||||||||

| Total assets |

354,178 | 361,072 | 358,989 | |||||||||

| Total bank debt, including current maturities(4) |

148,424 | 144,919 | 203,657 | |||||||||

| Total liabilities |

222,656 | 224,175 | 295,389 | |||||||||

| Convertible preferred stock |

145,328 | 197,295 | 262,385 | |||||||||

| Total stockholders’ deficit |

(13,806 | ) | (60,398 | ) | (198,785 | ) | ||||||

|

|

||||||||||||

| (3) | Net working capital is defined as current assets, excluding cash and cash equivalents, minus current liabilities. |

| (4) | Total bank debt, including current maturities, is net of $4.3 million, $3.2 million and $2.7 million of debt issuance costs as of December 31, 2014, December 31, 2015 and June 30, 2016, respectively. |

11

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider each of the following risk factors, as well as the other information in this prospectus, including our consolidated financial statements and the related notes, before deciding whether to invest in shares of our common stock. If any of the following risks actually occurs, our business, results of operations and financial condition may be materially and adversely affected. In that event, the trading price of our common stock could decline and you could lose all or part of your investment. Please also see the “Special note regarding forward-looking statements.”

Risks related to our business

The cosmetics industry is highly competitive, and if we are unable to compete effectively our results will suffer.

We face vigorous competition from companies throughout the world, including large multinational consumer products companies that have many cosmetics brands under ownership and standalone cosmetics brands, including those that may target the latest trends or specific distribution channels. Competition in the cosmetics industry is based on the introduction of new products, pricing of products, quality of products and packaging, brand awareness, perceived value and quality, innovation, in-store presence and visibility, promotional activities, advertising, editorials, e-commerce and mobile-commerce initiatives and other activities. We must compete with a high volume of new product introductions and existing products by diverse companies across several different distribution channels.

Many multinational consumer companies have greater financial, technical or marketing resources, longer operating histories, greater brand recognition or larger customer bases than we do and may be able to respond more effectively to changing business and economic conditions than we can. Many of these competitors’ products are sold in a wider selection or greater number of retail stores and possess a larger presence in these stores, typically having significantly more inline shelf space than we do. Given the finite space allocated to cosmetic products by retail stores, our ability to grow the number of retail stores in which our products are sold, and expand our space allocation once in these retail stores, may require the removal or reduction of the shelf space of these competitors. We may be unsuccessful in our growth strategy in the event retailers do not reallocate shelf space from our competitors to us. Our competitors may attempt to gain market share by offering products at prices at or below the prices at which our products are typically offered, including through the use of large percentage discounts and “buy one and get one free” offers. Competitive pricing may require us to reduce our prices, which would decrease our profitability or result in lost sales. Our competitors, many of whom have greater resources than we do, may be better able to withstand these price reductions and lost sales.

It is difficult for us to predict the timing and scale of our competitors’ activities in these areas or whether new competitors will emerge in the cosmetics business. In addition, further technological breakthroughs, including new and enhanced technologies which increase competition in the online retail market, new product offerings by competitors and the strength and success of our competitors’ marketing programs may impede our growth and the implementation of our business strategy.

Our ability to compete also depends on the continued strength of our brand and products, the success of our marketing, innovation and execution strategies, the continued diversity of our product offerings, the successful management of new product introductions and innovations, strong operational execution, including in order fulfillment, and our success in entering new markets and expanding our business in existing geographies. If we are unable to continue to compete effectively, it could have a material adverse effect on our business, results of operations and financial condition.

Our new product introductions may not be as successful as we anticipate.

The cosmetics industry is driven in part by fashion and beauty trends, which may shift quickly. Our continued success depends on our ability to anticipate, gauge and react in a timely and cost-effective manner to changes in consumer preferences for cosmetic products, consumer attitudes toward our industry and brand and where and how consumers shop for those products. We must continually work to develop, produce and market new products, maintain and enhance the recognition of our brand, maintain a favorable mix of products and develop our approach as to how and where we market and sell our products.

We have an established process for the development, evaluation and validation of our new product concepts. Nonetheless, each new product launch online, through our e.l.f. stores and through our retail customers involves risks, as well as the possibility of unexpected consequences. For example, the acceptance of new product launches and sales to our retail

12

Table of Contents

customers may not be as high as we anticipate, due to lack of acceptance of the products themselves or their price, or limited effectiveness of our marketing strategies. In addition, our ability to launch new products may be limited by delays or difficulties affecting the ability of our suppliers or manufacturers to timely manufacture, distribute and ship new products or displays for new products. Sales of new products may be affected by inventory management by our retail customers, and we may experience product shortages or limitations in retail display space by our retail customers. We may also experience a decrease in sales of certain existing products as a result of newly-launched products, the impact of which could be exacerbated by shelf space limitations or any shelf space loss. Any of these occurrences could delay or impede our ability to achieve our sales objectives, which could have a material adverse effect on our business, financial condition and results of operations.

As part of our ongoing business strategy we expect we will need to continue to introduce new products in our traditional product categories of eyes, lips, face and tools, while also expanding our product launches into adjacent categories in which we may have little to no operating experience. For example, we recently introduced a high-quality skin care assortment. The success of product launches in adjacent product categories could be hampered by our relative inexperience operating in such categories, the strength of our competitors or any of the other risks referred to above. Furthermore, any expansion into new product categories may prove to be an operational and financial constraint which inhibits our ability to successfully accomplish such expansion. Our inability to introduce successful products in our traditional categories or in adjacent categories could limit our future growth and have a material adverse effect on our business, financial condition and results of operations.

We depend on a limited number of retailers for a large portion of our net sales, and the loss of one or more of these retailers, or business challenges at one or more of these retailers, could adversely affect our results of operations.

A limited number of our retail customers account for a large percentage of our net sales. Target and Walmart accounted for 28% and 23%, respectively, of our net sales in 2015. We expect Target, Walmart and a small number of other retailers will, in the aggregate, continue to account for the majority of our net sales for foreseeable future periods. Any changes in the policies or our ability to meet the demands of our retail customers relating to service levels, inventory de-stocking, pricing and promotional strategies or limitations on access to display space could have a material adverse effect on our business, financial condition and results of operations.

As is typical in our industry, our business with retailers is based primarily upon discrete sales orders, and we do not have contracts requiring retailers to make firm purchases from us. Accordingly, retailers, including Target and Walmart, could reduce their purchasing levels or cease buying products from us at any time and for any reason. If we lose a significant retail customer or if sales of our products to a significant retailer materially decrease, it could have a material adverse effect on our business, financial condition and results of operations.

Because such a high percentage of our sales are made through our retail customers, our results are subject to risks relating to the general business performance of our key retail customers. Factors that adversely affect our retail customers’ businesses may also have a material adverse effect on our business, financial condition and results of operations. These factors may include:

| • | any reduction in consumer traffic and demand at our retail customers as a result of economic downturns, changes in consumer preferences or reputational damage as a result of, among other developments, data privacy breaches, regulatory investigations or employee misconduct; |

| • | any credit risks associated with the financial condition of our retail customers; |

| • | the effect of consolidation or weakness in the retail industry or at certain retail customers, including store closures and the resulting uncertainty; and |

| • | inventory reduction initiatives and other factors affecting retail customer buying patterns, including any reduction in retail space committed to cosmetics and retailer practices used to control inventory shrinkage. |

Our success depends, in part, on the quality, performance and safety of our products.

Any loss of confidence on the part of consumers in the ingredients used in our products, whether related to product contamination or product safety or quality failures, actual or perceived, or inclusion of prohibited ingredients, could tarnish the image of our brand and could cause consumers to choose other products. Allegations of contamination or other adverse

13

Table of Contents

effects on product safety or suitability for use by a particular consumer, even if untrue, may require us to expend significant time and resources responding to such allegations and could, from time to time, result in a recall of a product from any or all of the markets in which the affected product was distributed. Any such issues or recalls could negatively affect our profitability and brand image.

If our products are found to be, or perceived to be, defective or unsafe, or if they otherwise fail to meet our consumers’ expectations, our relationships with consumers could suffer, the appeal of our brand could be diminished, we may need to recall some of our products and/or become subject to regulatory action, and we could lose sales or market share or become subject to boycotts or liability claims. In addition, safety or other defects in our competitors’ products could reduce consumer demand for our own products if consumers view them to be similar. Any of these outcomes could result in a material adverse effect on our business, financial condition and results of operations.

We may not be able to successfully implement our growth strategy.

Our future growth, profitability and cash flows depend upon our ability to successfully implement our business strategy, which, in turn, is dependent upon a number of factors, including our ability to:

| • | build a great brand by attracting new consumers and encouraging our current consumers to use more e.l.f. products; |

| • | continue to use innovation to drive sales and margin and expand into relevant adjacencies; |

| • | expand brand penetration by growing our space allocations with our existing national retail customers, increasing the number of our retail customers, growing our direct-to-consumer business and expanding internationally; and |

| • | leverage our high-performance team culture and executional capability to drive operating margins and efficiencies. |

There can be no assurance that we can successfully achieve any or all of the above initiatives in the manner or time period that we expect. Further, achieving these objectives will require investments which may result in short-term costs without generating any current net sales and therefore may be dilutive to our earnings. We cannot provide any assurance that we will realize, in full or in part, the anticipated benefits we expect our strategy will achieve. The failure to realize those benefits could have a material adverse effect on our business, financial condition and results of operations.

Our growth and profitability are dependent on a number of factors, and our historical growth may not be indicative of our future growth.

Although our net sales and profitability have grown rapidly from 2012 through 2015, this should not be considered as indicative of our future performance. We may not be successful in executing our growth strategy, and even if we achieve our strategic plan, we may not be able to sustain profitability. In future periods, our revenue could decline or grow more slowly than we expect. We also may incur significant losses in the future for a number of reasons, including the following risks and the other risks described in this prospectus, and we may encounter unforeseen expenses, difficulties, complications, delays and other unknown factors:

| • | we may lose one or more significant retail customers, or sales of our products through these retail customers may decrease; |

| • | the ability of our third-party suppliers and manufacturers to produce our products and of our distributors to distribute our products could be disrupted; |

| • | because all of our products are sourced and manufactured in China, our operations are susceptible to risks inherent in doing business there; |

| • | our products may be the subject of regulatory actions, including but not limited to actions by the Food and Drug Administration (the “FDA”), the Federal Trade Commission (the “FTC”) and the Consumer Product Safety Commission (the “CPSC”) in the United States; |

| • | we may be unable to introduce new products that appeal to consumers or otherwise successfully compete with our competitors in the cosmetics industry; |

| • | we may be unsuccessful in enhancing the recognition and reputation of our brand, and our brand may be damaged as a result of, among other reasons, our failure, or alleged failure, to comply with applicable ethical, social, product, labor or environmental standards; |

14

Table of Contents

| • | we may experience service interruptions, data corruption, cyber-based attacks or network security breaches which result in the disruption of our operating systems or the loss of confidential information of our consumers; |

| • | we may be unable to retain key members of our senior management team or attract and retain other qualified personnel; and |

| • | we may be affected by any adverse economic conditions in the United States or internationally. |

We may be unable to manage our growth effectively, which would harm our business, financial condition and results of operations.

We have grown rapidly, with our net sales increasing from $82.9 million in the year ended December 31, 2012 to $191.4 million in the year ended December 31, 2015. Our growth has placed, and will continue to place, a strain on our management team, financial and information systems, supply chain and distribution capacity and other resources. To manage growth effectively, we must continue to enhance our operational, financial and management systems, including our warehouse management, inventory control and in-store point-of-sale systems; maintain and improve our internal controls and disclosure controls and procedures; maintain and improve our information technology systems and procedures; and expand, train and manage our employee base.

We may not be able to effectively manage this expansion in any one or more of these areas, and any failure to do so could significantly harm our business, financial condition and results of operations. Our rapid growth also makes it difficult for us to adequately predict the expenditures we will need to make in the future. If we do not make the necessary overhead expenditures to accommodate our future growth, we may not be successful in executing our growth strategy, and our results of operations would suffer.

Any damage to our reputation or brand may materially and adversely affect our business, financial condition and results of operations.

We believe that developing and maintaining our brand is critical and that our financial success is directly dependent on consumer perception of our brand. Furthermore, the importance of our brand recognition may become even greater as competitors offer more products similar to ours.

We have relatively low brand awareness among consumers when compared to other cosmetic brands, and maintaining and enhancing the recognition and reputation of our brand is critical to our business and future growth. Many factors, some of which are beyond our control, are important to maintaining our reputation and brand. These factors include our ability to comply with ethical, social, product, labor and environmental standards. Any actual or perceived failure in compliance with such standards could damage our reputation and brand.

The growth of our brand depends largely on our ability to provide a high-quality consumer experience, which in turn depends on our ability to bring innovative products to the market at competitive prices that respond to consumer demands and preferences. Additional factors affecting our consumer experience include our ability to provide appealing store sets in retail stores, the maintenance and stocking of those sets by our retail customers, the overall shopping experience provided by our retail customers, a reliable and user-friendly website interface and mobile applications for our consumers to browse and purchase products on elfcosmetics.com and an engaging environment in our e.l.f. stores. If we are unable to preserve our reputation, enhance our brand recognition or increase positive awareness of our products and in-store and Internet platforms, it may be difficult for us to maintain and grow our consumer base, and our business, financial condition and results of operations may be materially and adversely affected.