Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

[X]

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended June 30, 2016

or

|

[ ]

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

001-34941

(Commission file number)

PARK CITY GROUP, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

37-1454128

|

|

|

State or other jurisdiction of incorporation

|

(IRS Employer Identification No.)

|

|

|

299 South Main Street, Suite 2370

Salt Lake City, Utah 84111

|

(435) 645-2000

|

|

|

(Address of principal executive offices)

|

(Registrant's telephone number, including area code)

|

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each Class

|

Name of each exchange on which registered

|

|

|

Common Stock, $0.01 Par Value

|

NASDAQ Capital Market

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. [ ] Yes [X] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. [ ] Yes [X] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [X] Yes [ ] No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

[ ]

|

Accelerated filer

|

[X]

|

|

Non-accelerated filer

(Do not check if a smaller reporting company)

|

[ ]

|

Smaller reporting company

|

[ ]

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

[ ] Yes [X] No

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the issuer as of December 31, 2015, which is the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $153,106,000 (at a closing price of $11.91 per share).

As of September 7, 2016, 19,286,430 shares of the Company’s common stock, par value $0.01 per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Items 10, 11, 12, 13 and 14 of Part III incorporate by reference certain information from Park City Group, Inc.’s definitive proxy statement, to be filed with the Securities and Exchange Commission on or before October 28, 2016.

ON FORM 10-K

YEAR ENDED JUNE 30, 2016

|

PART I

|

||

| 1 | ||

| 7 | ||

| 15 | ||

| 15 | ||

| 15 | ||

|

PART II

|

||

| 16 | ||

| 17 | ||

| 19 | ||

| 30 | ||

| 30 | ||

| 30 | ||

| 30 | ||

| 31 | ||

|

PART III

|

||

| 32 | ||

| 32 | ||

| 32 | ||

| 32 | ||

| 32 | ||

|

PART IV

|

||

| 33 | ||

| 34 | ||

| F-1 | ||

| F-4 | ||

| F-5 | ||

| F-7 | ||

| F-8 | ||

| F-10 | ||

|

Exhibit 31

|

Certifications of the Principal Executive Officer and Principal Financial Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002.

|

|

|

Exhibit 32

|

Certifications pursuant to 18 U.S.C. Sec. 1350 as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002.

|

|

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements. The words or phrases “would be,” “will allow,” “intends to,” “will likely result,” “are expected to,” “will continue,” “is anticipated,” “estimate,” “project,” or similar expressions are intended to identify “forward-looking statements.” Actual results could differ materially from those projected in the forward looking statements as a result of a number of risks and uncertainties, including the risk factors set forth below and elsewhere in this Report. See “Risk Factors” and “Management's Discussion and Analysis of Financial Condition and Results of Operations.” Statements made herein are as of the date of the filing of this Form 10-K with the Securities and Exchange Commission and should not be relied upon as of any subsequent date. Unless otherwise required by applicable law, we do not undertake, and specifically disclaim any obligation, to update any forward-looking statements to reflect occurrences, developments, unanticipated events or circumstances after the date of such statement.

PART I

|

BUSINESS

|

Overview

Park City Group, Inc. (the “Company”) is a Software-as-a-Service (“SaaS”) provider. The Company’s technology helps companies to synchronize their systems with those of their trading partners to make more informed business decisions. We provide companies with greater flexibility in sourcing products by enabling them to choose new suppliers and integrate them into their supply chain faster and more cost effectively, and we help them to more efficiently manage these relationships to “stock less and sell more”, enhancing revenue while lowering working capital, labor costs and waste. Through our subsidiary, ReposiTrak, Inc. (“ReposiTrak”), we also help reduce a company’s potential regulatory, legal, and criminal risk from its supply chain partners by providing a way for them to ensure these suppliers are compliant with food and drug safety regulations, such as the Food Safety Modernization Act (“FSMA”) and the Drug Quality and Security Act (“DQSA”).

The Company’s services are delivered though proprietary software products designed, developed, marketed and supported by the Company. These products are designed to provide transparency and facilitate improved business processes among all key constituents in the supply chain, starting with the retailer and moving back to suppliers and eventually to raw material providers. We provide cloud-based applications and services that address e-commerce, supply chain, and compliance activities. The principal customers for the Company's products are multi-store food retail store chains and their suppliers, branded food manufacturers, food wholesalers and distributors, and other food service businesses.

The Company has a hub and spoke business model. We are typically engaged by retailers and distributors (“Hubs”), which in turn have us engage their suppliers (“Spokes”) to sign up for our services. The bulk of the Company’s revenue is from recurring subscription payments typically based on a monthly volume metric between the Hub and the Spoke. We also have a Professional Services business, which conducts customization, implementation, and training, for which revenue is recognized on a percentage-of-completion or pro rata over the life of the subscription, depending on the nature of the engagement. In a few instances the Company will also sell its software in the form of a license.

The Company is incorporated in the state of Nevada. The Company has three subsidiaries: PC Group, Inc. (formerly, Park City Group, Inc., a Delaware corporation), a Utah corporation (98.76% owned), Park City Group, Inc. (formerly, Prescient Applied Intelligence, Inc.), a Delaware corporation (100% owned) and ReposiTrak, Inc., a Utah corporation (100% owned). All intercompany transactions and balances have been eliminated in consolidation.

Our principal executive offices of the Company are located at 299 South Main Street, Suite 2370, Salt Lake City, Utah 84111. Our telephone number is (435) 645-2000. Our website address is http://www.parkcitygroup.com, and ReposiTrak’s website address is http://repositrak.com.

Acquisition of ReposiTrak

On June 30, 2015, the Company consummated the acquisition of 100% of the outstanding capital stock of ReposiTrak. The accompanying audited consolidated financial statements of the Company as of and for the year ended June 30, 2015 contain the results of operations of ReposiTrak from June 30, 2015. We issued 873,438 shares of our common stock in connection with this acquisition. As a result of the acquisition of ReposiTrak, we significantly expanded the services we can offer to our customer base.

We have accounted for the acquisition as the purchase of a business. The assets acquired and the liabilities assumed of ReposiTrak have been recorded at their respective fair values. The excess of the purchase price over the fair value of net tangible and identifiable intangible assets acquired was recorded as goodwill. Goodwill is attributed to buyer-specific value resulting from expected synergies, including long-term cost savings, as well as industry relationships that are not included in the fair values of assets. Goodwill will not be amortized.

The purchase price consisted of the 873,438 shares of our common stock. The fair value of the shares issued was $10,821,897 and was determined using the closing price of our common stock on June 30, 2015. The price paid to acquire ReposiTrak was $10,830,897, approximately $9,000 of which was for direct transaction costs associated with the issuance of equity. The net acquisition cost of $10,799,778, which excludes $31,119 of cash acquired from ReposiTrak, were allocated based on their estimated fair value of the assets acquired and liabilities assumed, as follows:

|

Finalized Values

|

||||

|

Receivables

|

$ | 152,340 | ||

|

Prepaid expense

|

17,500 | |||

|

Customer relationships

|

1,314,000 | |||

|

Goodwill

|

16,077,953 | |||

|

Accounts payable

|

(128,126 | ) | ||

|

Deferred revenue

|

(598,232 | ) | ||

|

Net assets acquired

|

16,835,435 | |||

|

Common stock issued

|

10,821,897 | |||

|

Receivables eliminated in consolidation

|

6,035,657 | |||

|

Cash received in acquisition

|

$ | 22,119 | ||

Unaudited pro-forma results of operations for the twelve months ended June 30, 2015, as though ReposiTrak had been acquired as of July 1, 2013, are as follows:

|

Three Months Ended

|

Year

Ended

2015

|

Year

Ended

2014

|

||||||||||||||||||||||

|

Sep 30,

2014

|

Dec 31,

2014

|

Mar 31,

2015

|

Jun 30,

2015

|

|||||||||||||||||||||

|

Revenue

|

$

|

2,826,813

|

$

|

2,932,825

|

$

|

2,870,646

|

$

|

2,941,511

|

$

|

11,571,795

|

$

|

9,777,431

|

||||||||||||

|

Loss from Operations

|

(1,046,986

|

) |

(1,290,524

|

) |

(1,302,437

|

) |

(3,222,538

|

) |

(6,862,485

|

)

|

(5,232,552

|

)

|

||||||||||||

|

Net Loss

|

(1,049,834

|

) |

(1,317,510

|

) |

(1,317,858

|

) |

(3,241,545

|

) |

(6,926,747

|

)

|

(5,303,773

|

)

|

||||||||||||

|

Net Loss Applicable to Common Shareholders

|

(1,204,307

|

) |

(1,471,983

|

) |

(3,595,537

|

) |

(3,365,721

|

) |

(9,637,548

|

)

|

(5,921,664

|

)

|

||||||||||||

|

Basic and Diluted EPS

|

(0.07

|

) |

(0.08

|

)

|

(0.20

|

)

|

(0.18

|

) |

(0.53

|

)

|

(0.34

|

)

|

||||||||||||

Company History

The Company’s technology has its genesis in the operations of Mrs. Fields Cookies co-founded by Randall K. Fields, the Company’s Chief Executive Officer. The Company began operations utilizing patented computer software and profit optimization consulting services to help its retail clients reduce their inventory and labor costs - the two largest controllable expenses in the retail industry. Because the product concepts originated in the environment of actual multi-unit retail chain ownership, the products are strongly oriented to an operation’s bottom line results.

The Company was incorporated in the State of Delaware on December 8, 1964 as Infotec, Inc. From June 20, 1999 to approximately June 12, 2001, it was known as Amerinet Group.com, Inc. In 2001, the name was changed from Amerinet Group.com to Fields Technologies, Inc. On June 13, 2001, the Company entered into a “Reorganization Agreement” with Randall K. Fields and Riverview Financial Corporation whereby it acquired substantially all of the outstanding stock of Park City Group, Inc., a Delaware corporation, which became a 98.67% owned subsidiary.

On July 25, 2002, Fields Technologies, Inc. changed its name from Fields Technologies, Inc. to Park City Group, Inc. through a merger with Park City Group, Inc., a Nevada corporation, which was organized for that purpose and was also the surviving entity in the merger. As a result, both the parent-holding company (Nevada) and its operating subsidiary (Delaware) were named Park City Group, Inc. In February 2014, Park City Group, Inc. (Delaware) was domesticated in Utah and changed its name to PC Group, Inc. Park City Group, Inc. (Nevada) has no business operations separate from the operations conducted through its subsidiaries, including ReposiTrak, Inc. and Park City Group, Inc., a Delaware corporation, (formerly Prescient Applied Intelligence, Inc. (“Prescient”).

On January 13, 2009, the Company acquired 100% of Prescient, a leading provider of on-demand solutions for the retail marketplace, including both retailers and suppliers. Its solutions capture information at the point of sale, provide greater visibility into real-time demand and turn data into actionable information across the entire supply chain. In February 2014, Prescient changed its name to Park City Group, Inc. The Company’s consolidated financial statements contain the results of operations of Park City Group, Inc. (Delaware). Operations are conducted through this subsidiary.

ReposiTrak was founded by Leavitt Partners, LP. It was originally incorporated as Global Supply Chain Systems, Inc. on May 17, 2012 and on November 8, 2012 changed its name to ReposiTrak. ReposiTrak became a wholly owned subsidiary of Park City Group, Inc. on June 30, 2015. ReposiTrak was developed in response to the passage of the FSMA. ReposiTrak helps a company protect its brand and mitigate potential regulatory, legal and criminal risk from its supply chain by helping to ensure that all parties are compliant with best practices and food and drug safety regulations.

Target Industries Overview

The Company initially developed its software for supermarkets, convenience stores and other retailers. Following the acquisition of Prescient in 2009, we expanded our offerings to include supply chain solutions focused on large manufacturers, distributors and suppliers in the consumer products industry. With the acquisition of ReposiTrak in 2015, this group was expanded to include manufacturers, distributors and suppliers in the food industry. The Company also provides professional consulting services targeting implementation, assessments, profit optimization and support functions for its application and related products.

Backdrop

The U.S. consumer retail sector has faced competitive pressure from a number of significant forces including the rise of online retailers with lower fixed operating costs as well as sector consolidation in many categories. Retailers have responded to these pressures in a number of ways including putting a greater emphasis on specialization within their product mix through initiatives such as local sourcing or the development of in-store brands or private labels. Retailers have also attempted to lower their fixed cost by shifting a greater percentage of their product mix to Direct Store Delivery (“DSD”). In addition to differentiated products and increased logistics support, retailers are also increasingly pressuring suppliers to provide direct economic incentives or assistance.

More recently, there has been a sweeping change in the regulatory environment in which food growers, processors, distributors and retailers compete. The law also provides the U.S. Food and Drug Administration (“FDA”) with new enforcement authorities, it also sets cause for a whole host of potential civil claims. In short, the degree to which the retail food business has moved toward a highly regulated industry is substantial.

The Company’s software and consulting services are designed to address the business problems faced by our customers. Our technology helps retailers to synchronize their business systems with those of their suppliers in order to give a cohesive view of their entire supply chain so as to enable them to make more informed business decisions. Through our cloud-based infrastructure we provide retailers with greater flexibility in sourcing products by enabling them to choose new suppliers and integrate them into their supply chain faster and more cost effectively, and we help retailers to more efficiently manage their relationships with these suppliers so that they can “stock less and sell more” lowering working capital and labor costs while also increasing revenue.

ReposiTrak was developed in response to the passage of the FSMA, and the then pending DWSA. ReposiTrak helps a company to protect its brand from the degradation of value that typically results from an outbreak of contamination or other incidents adversely affecting the supply chain as well as mitigates potential regulatory, legal and criminal risk from its supply chain by helping a company to ensure that all parties in its supply chain are compliant with best practices and food and drug safety regulations.

Solutions and Services

Advanced Commerce and Supply-Chain Solutions

The Company’s primary advanced commerce and supply-chain solutions are Scan Based Trading, ScoreTracker, Vendor Managed Inventory, Store Level Replenishment, Enterprise Supply Chain Planning, Fresh Market Manager and ActionManager®, all of which are designed to aid the retailer and supplier with managing inventory, product mix and labor while improving sales through reduced out of stocks by improving visibility and forecasting.

Food Safety Solutions

ReposiTrak leverages the technology developed to help a company protect its brand and mitigate potential regulatory, legal and criminal risk from its supply chain by helping to ensure that all parties are compliant with best practices and food and drug safety regulations imposed by the FSMA and DWSA. ReposiTrak™, is powered by the Company’s technology, and currently includes three main applications: Vendor Validation, Compliance Management, and Track & Trace.

Services

The Company has two services groups: The Business Analytics Group offers business-consulting services to suppliers and retailers in the grocery, convenience store and specialty retail industries. The Professional Services Group provides consulting services to ensure that our solutions are seamlessly integrated into our customers’ business processes as quickly and efficiently as possible.

During the year ending June 30, 2016, the Company began to embark on a process of converging our legacy Park City supply-chain business with our ReposiTrak food safety business.

Technology, Development and Operations

Product Development

The products sold by the Company are subject to rapid and continual technological change. Products available from the Company, as well as from its competitors, increasingly offer a wider range of features and capabilities. The Company believes that in order to compete effectively in its selected markets, it must provide compatible systems incorporating new technologies at competitive prices. In order to achieve this, the Company has made a substantial commitment to on-going development.

Our product development strategy is focused on creating common technology elements that can be leveraged in applications across our core markets. Except for its supply chain application, which is based on a proprietary architecture, the Company’s software architecture is based on open platforms and is modular, thereby allowing it to be phased into a customer’s operations. In order to remain competitive, we are currently designing, coding and testing a number of new products and developing expanded functionality of our current products.

Operations

We currently serve our customers from a third-party data center hosting facility. Along with the Company’s Statement on Standards for Attestation Engagements (“SSAE”) No. 16 certification Service Organization Control (“SOC2”), the third-party facility is also a SSAE No. 16 – SOC2 certified location and is secured by around-the-clock guards, biometric screening and escort-controlled access, and is supported by on-site backup generators in the event of a power failure. As part of our current disaster recovery arrangements, all of our customers’ data is currently backed-up in near real-time. Even with the disaster recovery arrangements, our service could be interrupted.

Customers

We are currently engaged by customers of all sizes. Our customers primarily include food related consumer goods retailers, suppliers, processors and manufacturers. However, the Company is opportunistic and will offer its solutions to non-food consumer goods related companies as well. No single customers accounted for more than 10% percent of our revenue in fiscal 2016.

Prior to the acquistion of ReposiTrak, our contractual relationship with ReposiTrak generated approximately $3.0 million in subscription revenue and management fees during the year ended June 30, 2015, which amount constituted approximately 21% of the Company’s total revenue in such year. After acquiring ReposiTrak on June 30, 2015 we fully consolidated its financial results into our financial results. As such, we ceased to recognize subscription revenue and management fees from ReposiTrak, and instead began to recognize ReposiTrak revenue from customer connections directly. ReposiTrak generated $2.2 million in revenue from customer connections during the year ended June 30, 2016.

Sales, Marketing and Customer Support

Sales and Marketing

Through a focused and dedicated sales effort designed to address the requirements of each of its software and service solutions, we believe our sales force is positioned to understand our customers’ businesses, trends in the marketplace, competitive products and opportunities for new product development. Our deep industry knowledge enables the Company to take a consultative approach in working with our prospects and customers. Our sales personnel focus on selling our technology solutions to major customers, both domestically and internationally.

To date, our primary marketing objectives have been to increase awareness of our technology solutions, generate sales leads and develop new customer relationships. In addition, the sales effort has been directed toward developing existing customers by cross-selling ReposiTrak food safety services to legacy Park City Group accounts as well as introducing our solutions to ReposiTrak customers. To this end, we attend industry trade shows, conduct direct marketing programs, publish industry trade articles and white papers, participate in interviews and selectively advertise in industry publications.

During the year ending June 30, 2016 the Company began to embark on a process of converging our legacy supply-chain business with our ReposiTrak food safety business. As part of this process, we have begun to reorganize our sale force and reorient our marketing efforts. This process has involved stream lining the sales force in an effort to enable cross-selling by reducing regional account managers and shifting our sales emphasis towards ReposiTrak’s inside sales team located at our corporate headquarters in Salt Lake City, Utah. We are also considering rebranding some of our services to better reflect the consolidated offering.

Customer Support

Our global customer support group responds to both business and technical inquiries from our customers relating to how to use our products and is available to customers by telephone and email. Basic customer support during business hours is available at no charge to customers who purchase certain Company solutions. Premier customer support includes extended availability and additional services, such as an assigned support representative and/or administrator. Premier customer support is available for an additional fee. Additional support services include developer support and partner support.

Competition

The market for the Company’s products and services is very competitive. We believe the principal competitive factors include product quality, reliability, performance, price, vendor and product reputation, financial stability, features and functions, ease of use, quality of support and degree of integration effort required with other systems. Our supply chain solution competitors include supply chain vendors, major enterprise resource planning (“ERP”) software vendors, mid-market ERP vendors and niche players for VMI and SLR. ReposiTrak’s competitors include a variety of food safety consultants who may help a potential customer build their own in-house solution as well as certain technology component providers.

We compete with large enterprise-wide software vendors, developers and integrators, business-to-business exchanges, consulting firms, focused solution providers, and business intelligence technology platforms. While our competitors are often considerably larger companies in size with larger sales forces and marketing budgets, we believe that our deep industry knowledge, the breadth and depth of our offerings, and our relationships with key industry, wholesaler, and other trade groups and associations, give us a competitive advantage. Our ability to continually improve our products, processes and services, as well as our ability to develop new products, enables the Company to meet evolving customer requirements.

Patents and Proprietary Rights

The Company relies on a combination of trademark, copyright, trade secret and patent laws in the United States and other jurisdictions as well as confidentiality procedures and contractual provisions to protect our proprietary technology and our name. We also enter into confidentiality agreements with our employees, consultants and other third parties and control access to software, documentation and other proprietary information.

The Company has been awarded nine U.S. patents, eight U.S. registered trademarks and has 37 U.S. copyrights relating to its software technology and solutions. The Company’s patent portfolio has been transferred to an unrelated third party, although the Company retains the right to use the licensed patents in connection with its business. However, Company policy is to continue to seek patent protection for all developments, inventions and improvements that are patentable and have potential value to the Company and to protect its trade secrets and other confidential and proprietary information. The Company intends to vigorously defend its intellectual property rights to the extent its resources permit.

The Company is not aware of any patent infringement claims against it; however, there are no assurances that litigation to enforce patents issued to the Company to protect proprietary information, or to defend against the Company’s alleged infringement of the rights of others will not occur. Should any such litigation occur, the Company may incur significant litigation costs, Company resources may be diverted from other planned activities, and while the outcome of any litigation is inherently uncertain, any litigation result may cause a materially adverse effect on the Company’s operations and financial condition. Any intellectual property claims, with or without merit, could be time-consuming and expensive to resolve, could divert management attention from executing our business plan and could require us to alter our technology, change our business methods and/or pay monetary damages or enter into licensing agreements.

Employees

As of June 30, 2016, the Company employed a total of 66 employees. Of these employees, ten are located overseas. The Company plans to continue expanding its offshore workforce to augment its analytics services offerings, expand its professional services and to provide additional programming resources. The employees are not represented by any labor union.

Reports to Security Holders

The Company is subject to the informational requirements of the Securities Exchange Act of 1934. Accordingly, it files annual, quarterly and other reports and information with the Securities and Exchange Commission. You may read and copy these reports and other information at the Securities and Exchange Commission's public reference rooms in Washington, D.C. and Chicago, Illinois. The Company’s filings are also available to the public from commercial document retrieval services and the website maintained by the Securities and Exchange Commission at http://www.sec.gov.

Government Regulation and Approval

Like all businesses, the Company is subject to numerous federal, state and local laws and regulations, including regulations relating to patent, copyright, and trademark law matters.

Cost of Compliance with Environmental Laws

The Company currently has no costs associated with compliance with environmental regulations, and does not anticipate any future costs associated with environmental compliance; however, there can be no assurance that it will not incur such costs in the future.

|

RISK FACTORS

|

An investment in our common stock is subject to many risks. You should carefully consider the risks described below, together with all of the other information included in this Annual Report on Form 10-K, including the financial statements and the related notes, before you decide whether to invest in our common stock. Our business, operating results and financial condition could be harmed by any of the following risks. The trading price of our common stock could decline due to any of these risks, and you could lose all or part of your investment.

Risks Related to the Company

The Company has incurred losses in the past and there can be no assurance that the Company will operate profitably in the future.

The Company’s marketing strategy emphasizes sales of subscription-based services, instead of annual licenses, and contracting with suppliers (“Spokes”) to connect to our clients (“Hubs”). This strategy has resulted in the development of a foundation of hubs to which suppliers can be “connected”, thereby accelerating future growth. If, however, this marketing strategy fails, revenue and operations will be negatively affected.

The Company had net income of $666,503 for the year ended June 30, 2016, compared to a net loss of $3,849,773 for the year ended June 30, 2015. Although the Company generated net income in the year ended June 30, 2016, there can be no assurance that the Company will achieve profitability in future periods. If the Company does not operate profitably in the future, the Company’s current cash resources will be used to fund the Company’s operating losses. Continued losses would have an adverse effect on the long-term value of the Company’s common stock and any investment in the Company. The Company cannot give any assurance that the Company will continue to generate revenue or have sustainable profits.

Although the Company’s cash resources are currently sufficient, the Company’s long-term liquidity and capital requirements may be difficult to predict, which may adversely affect the Company’s long-term cash position.

Historically, the Company has been successful in raising capital when necessary, including private placements, a registered direct offering, and stock issuances from its officers and directors, including its Chief Executive Officer and majority stockholder, in order to pay its indebtedness and fund its operations, in addition to cash flow from operations. As a result of the consummation of the registered direct offering on April 15, 2015, resulting in net proceeds of approximately $6.7 million we have adequate cash resources to fund our operations and satisfy our debt obligations for at least the next 12 months.

If the Company is required to seek additional financing in the future in order to fund its operations, retire its indebtedness and otherwise carry out its business plan, there can be no assurance that such financing will be available on acceptable terms, or at all, and there can be no assurance that any such arrangement, if required or otherwise sought, would be available on terms deemed to be commercially acceptable and in the Company’s best interests.

Quarterly and annual operating results may fluctuate, which makes it difficult to predict future performance.

Management expects a significant portion of the Company’s revenue stream to come from the sale of subscriptions, and to a lesser extent, license sales, maintenance and services charged to new customers. These amounts will fluctuate because predicting future sales is difficult and involves speculation. In addition, the Company may potentially experience significant fluctuations in future operating results caused by a variety of factors, many of which are outside of its control, including:

| ● |

our ability to retain and increase sales to existing customers, attract new customers and satisfy our customers' requirements;

|

| ● |

the renewal rates for our service;

|

| ● |

the amount and timing of operating costs and capital expenditures related to the operations and expansion of our business;

|

| ● |

changes in our pricing policies whether initiated by us or as a result of competition;

|

| ● |

the cost, timing and management effort for the introduction of new features to our service;

|

| ● |

the rate of expansion and productivity of our sales force;

|

| ● |

new product and service introductions by our competitors;

|

| ● |

variations in the revenue mix of editions or versions of our service;

|

| ● |

technical difficulties or interruptions in our service;

|

| ● |

general economic conditions that may adversely affect either our customers' ability or willingness to purchase additional subscriptions or upgrade their service, or delay a prospective customers' purchasing decision, or reduce the value of new subscription contracts or affect renewal rates;

|

| ● |

timing of additional investments in our enterprise cloud computing application and platform services and in our consulting service;

|

| ● |

regulatory compliance costs;

|

| ● |

the timing of customer payments and payment defaults by customers;

|

| ● |

extraordinary expenses such as litigation or other dispute-related settlement payments;

|

| ● |

the impact of new accounting pronouncements; and

|

| ● |

the timing of stock awards to employees and the related financial statement impact.

|

Future operating results may fluctuate because of the foregoing factors, making it difficult to predict operating results. Period-to-period comparisons of operating results are not necessarily meaningful and should not be relied upon as an indicator of future performance. In addition, a relatively large portion of the Company’s expenses will be fixed in the short-term, particularly with respect to facilities and personnel. Therefore, future operating results will be particularly sensitive to fluctuations in revenue because of these and other short-term fixed costs.

The Company will need to effectively manage its growth in order to achieve and sustain profitability. The Company’s failure to manage growth effectively could reduce its sales growth and result in continued net losses.

To achieve continual and consistent profitable operations on a fiscal year on-going basis, the Company must have significant growth in its revenue from its products and services, specifically subscription-based services. If the Company is able to achieve significant growth in future subscription sales, and expands the scope of its operations, the Company’s management, financial condition, operational capabilities, and procedures and controls could be strained. The Company cannot be certain that its existing or any additional capabilities, procedures, systems, or controls will be adequate to support the Company’s operations. The Company may not be able to design, implement or improve its capabilities, procedures, systems or controls in a timely and cost-effective manner. Failure to implement, improve and expand the Company’s capabilities, procedures, systems or controls in an efficient and timely manner could reduce the Company’s sales growth and result in a reduction of profitability or increase of net losses.

The Company’s officers and directors have significant control over it, which may lead to conflicts with other stockholders over corporate governance.

The Company’s officers and directors, including our Chief Executive Officer, Randall K. Fields, control approximately 33% of the Company’s common stock. Mr. Fields, individually, controls 27% of the Company’s common stock. Consequently, Mr. Fields individually, and the Company’s officers and directors, as stockholders acting together, are able to significantly influence all matters requiring approval by the Company’s stockholders, including the election of directors and significant corporate transactions, such as mergers or other business combination transactions.

The Company’s corporate charter contains authorized, unissued “blank check” preferred stock issuable without stockholder approval with the effect of diluting then current stockholder interests.

The Company’s certificate of incorporation currently authorizes the issuance of up to 30,000,000 shares of ‘blank check’ preferred stock with designations, rights, and preferences as may be determined from time to time by the Company’s Board of Directors, of which 700,000 shares are currently designated as Series B Convertible Preferred Stock (“Series B Preferred”) and 300,000 shares are designated as Series B-1 Preferred Stock (“Series B-1 Preferred”). As of June 30, 2016, a total of 625,375 shares of Series B Preferred and 180,213 shares of Series B-1 Preferred were issued and outstanding. The Company’s Board of Directors is empowered, without stockholder approval, to issue one or more additional series of preferred stock with dividend, liquidation, conversion, voting, or other rights that could dilute the interest of, or impair the voting power of, the Company’s common stockholders. The issuance of an additional series of preferred stock could be used as a method of discouraging, delaying or preventing a change in control.

Because the Company has never paid dividends on its common stock, investors should exercise caution before making an investment in the Company.

The Company has never paid dividends on its common stock and does not anticipate the declaration of any dividends pertaining to its common stock in the foreseeable future. The Company intends to retain earnings, if any, to finance the development and expansion of the Company’s business. The Company’s Board of Directors will determine future dividend policy at their sole discretion and future dividends will be contingent upon future earnings, if any, obligations of the stock issued, the Company’s financial condition, capital requirements, general business conditions and other factors. Future dividends may also be affected by covenants contained in loan or other financing documents, which may be executed by the Company in the future. Therefore, there can be no assurance that dividends will ever be paid on its common stock.

The Company’s business is dependent upon the continued services of the Company’s founder and Chief Executive Officer, Randall K. Fields. Should the Company lose the services of Mr. Fields, the Company’s operations will be negatively impacted.

The Company’s business is dependent upon the expertise of its founder and Chief Executive Officer, Randall K. Fields. Mr. Fields is essential to the Company’s operations. Accordingly, an investor must rely on Mr. Fields’ management decisions that will continue to control the Company’s business affairs. The Company currently maintains key man insurance on Mr. Fields’ life in the amount of $5,000,000; however, that coverage would be inadequate to compensate for the loss of his services. The loss of the services of Mr. Fields would have a materially adverse effect upon the Company’s business.

If the Company is unable to attract and retain qualified personnel, the Company may be unable to develop, retain or expand the staff necessary to support its operational business needs.

The Company’s current and future success depends on its ability to identify, attract, hire, train, retain and motivate various employees, including skilled software development, technical, managerial, sales, marketing and customer service personnel. Competition for such employees is intense and the Company may be unable to attract or retain such professionals. If the Company fails to attract and retain these professionals, the Company’s revenue and expansion plans may be negatively impacted.

The Company’s officers and directors have limited liability and indemnification rights under the Company’s organizational documents, which may impact its results.

The Company’s officers and directors are required to exercise good faith and high integrity in the management of the Company’s affairs. The Company’s certificate of incorporation and bylaws, however, provide, that the officers and directors shall have no liability to the stockholders for losses sustained or liabilities incurred which arise from any transaction in their respective managerial capacities unless they violated their duty of loyalty, did not act in good faith, engaged in intentional misconduct or knowingly violated the law, approved an improper dividend or stock repurchase or derived an improper benefit from the transaction. As a result, an investor may have a more limited right to action than he would have had if such a provision were not present. The Company’s certificate of incorporation and bylaws also require it to indemnify the Company’s officers and directors against any losses or liabilities they may incur as a result of the manner in which they operate the Company’s business or conduct the Company’s internal affairs, provided that the officers and directors reasonably believe such actions to be in, or not opposed to, the Company’s best interests, and their conduct does not constitute gross negligence, misconduct or breach of fiduciary obligations.

Risks Related to the ReposiTrak

The Company faces risks associated with new product introductions of ReposiTrak™.

The first installations of ReposiTrak™ began in August 2012, and market and product data related to these implementations is still being analyzed. The Company also continually receives and analyzes market and product data on other products, and the Company may endeavor to develop and commercialize new product offerings based on this data. The following risks apply to ReposiTrak™ and other potential new product offerings:

| ● |

it may be difficult for the Company to predict the amount of service and technological resources that will be needed by customers of ReposiTrak™ or other new offerings, and if the Company underestimates the necessary resources, the quality of its service will be negatively impacted thereby undermining the value of the product to the customer;

|

| ● |

the Company’s experience with ReposiTrak™ and its market acceptance is limited, and we therefore cannot accurately predict if it will be a profitable product;

|

| ● |

technological issues between the Company and customers may be experienced in capturing data, and these technological issues may result in unforeseen conflicts or technological setbacks when implementing additional installations of ReposiTrak™. This may result in material delays and even result in a termination of the ReposiTrak™ engagement;

|

| ● |

the customer’s experience with ReposiTrak™ and other new offerings, if negative, may prevent the Company from having an opportunity to sell additional products and services to that customer;

|

| ● |

if customers do not use ReposiTrak™ as the Company recommends and fails to implement any needed corrective action(s), it is unlikely that customers will experience the business benefits from the software service and may therefore be hesitant to continue the engagement as well as acquire any additional software services from the Company; and

|

| ● |

delays in proceeding with the implementation of ReposiTrak™ or other new products for a new customer will negatively affect the Company’s cash flow and its ability to predict cash flow.

|

Approximately 15% of our total revenue during 2016 was attributable to ReposiTrak. In the event the market for ReposiTrak’s services fails to develop as anticipated, our results of operations may be materially and adversely affected.

The Company recognized approximately $2.2 million in revenue during the year ended June 30, 2016 from ReposiTrak, which amount constituted approximately 15% of the Company’s total revenue in 2016. In the event the market for ReposiTrak’s services fails to develop as anticipated, or ReposiTrak, or we are otherwise unable to capitalize on the opportunities presented by the adoption of Food Safety Modernization Act (“FSMA”), the Company’s financial results, including its financial condition, may be adversely and materially affected.

If our products do not perform as expected, whether as a result of operator error or otherwise, it would impair our operating results and reputation.

Our success depends on the food safety market’s confidence that we can provide reliable, high-quality reporting for our customers. We believe that our customers are likely to be particularly sensitive to product defects and operator errors, including if our systems fail to accurately report issues that could reduce the liability of our clients in the event of a product recall. In addition, our reputation and the reputation of our products can be adversely affected if our systems fail to perform as expected.

However, if our customers or potential customers fail to implement and use our systems as suggested by us, they may not be in a position to deal with a recall as effectively as they could have. As a result, the failure or perceived failure of our products to perform as expected, could have a material adverse effect on our revenue, results of operations and business.

If a customer is sued because of a recalled product we could be joined in that suit, the defense of which would impair our operating results.

We believe our products would be helpful in the event of a recall. However, their ultimate efficacy is dependent on how the customer uses our products which is in many ways out of our control. Similarly, a customer which is a defendant in a product liability case could claim that had our services performed as represented the extent of potential liability would have been minimized and therefore the Company should have some contributory liability in the case. Defending such a claim could have a material adverse effect on our revenue, results of operations and business.

The deployment of the Company’s services, or consultation provided by Company personnel, could result in litigation naming the Company as a party, which litigation could result in a material and adverse effect on the Company, and its results from operations.

Certain of the Company’s services are marketed to potential customers based, in part, on our service’s ability to reduce a company’s potential regulatory, legal, and criminal risk from its supply chain partners. In the event litigation is commenced against a customer based on issues caused by a constituent in the supply chain, or consultation provided by Company personnel, the Company could be joined or named in such litigation. As a result, the Company could face substantial defense costs. In addition, any adverse determination resulting in such litigation could have a material and adverse effect on the Company, and its results from operations.

Business Operations Risks

If the Company’s marketing strategy fails, its revenue and operations will be negatively affected.

The Company plans to concentrate its future sales efforts towards marketing the Company’s applications and services, and specifically to contract with suppliers, our Spokes, to connect to our existing Hubs previously signed up by the Company. These applications and services are designed to be highly flexible so that they can work in multiple retail and supplier environments such as grocery stores, convenience stores, specialty retail and route-based delivery environments. There is no assurance that the public will accept the Company’s applications and services in proportion to the Company’s increased marketing of this product line, or that the Company will be able to successfully leverage its hubs to increase revenue by connecting suppliers. The Company may face significant competition that may negatively affect demand for its applications and services, including the public’s preference for the Company’s competitors’ new product releases or updates over the Company’s releases or updates. If the Company’s applications and services marketing strategies fail, the Company will need to refocus its marketing strategy toward other product offerings, which could lead to increased development and marketing costs, delayed revenue streams, and otherwise negatively affect the Company’s operations.

Because the Company’s emphasis is on the sale of subscription based services, rather than annual license fees, the Company’s revenue may be negatively affected.

Historically, the Company offered applications and related maintenance contracts to new customers for a one-time, non-recurring up front license fee and provided an option for annually renewing their maintenance agreements. The Company is now principally offering prospective customers monthly subscription based licensing of its products. The Company’s customers may now choose to acquire a license to use the software on an Application Solution Provider basis (also referred to as “ASP”) resulting in monthly charges for use of the Company’s software products and maintenance fees. The Company’s conversion from a strategy of one-time, non-recurring licensing based model to a monthly recurring fees based approach is subject to the following risks:

| ● |

the Company’s customers may prefer one-time fees rather than monthly fees; and

|

| ● |

there may be a threshold level (number of locations) at which the monthly based fee structure may not be economical to the customer, and a request to convert from monthly fees to an annual fee could occur.

|

The Company faces threats from competing and emerging technologies that may affect its profitability.

Markets for the Company’s type of software products and that of its competitors are characterized by:

| ● |

development of new software, software solutions or enhancements that are subject to constant change;

|

| ● |

rapidly evolving technological change; and

|

| ● |

unanticipated changes in customer needs.

|

Because these markets are subject to such rapid change, the life cycle of the Company’s products is difficult to predict. As a result, the Company is subject to the following risks:

| ● |

whether or how the Company will respond to technological changes in a timely or cost-effective manner;

|

| ● |

whether the products or technologies developed by the Company’s competitors will render the Company’s products and services obsolete or shorten the life cycle of the Company’s products and services; and

|

| ● |

whether the Company’s products and services will achieve market acceptance.

|

Interruptions or delays in service from our third-party data center hosting facility could impair the delivery of our service and harm our business.

We currently serve our customers from a third-party data center hosting facility located in the United States. Any damage to, or failure of, our systems generally could result in interruptions in our service. As we continue to add capacity, we may move or transfer our data and our customers' data. Despite precautions taken during this process, any unsuccessful data transfers may impair the delivery of our service. Further, any damage to, or failure of, our systems generally could result in interruptions in our service. Interruptions in our service may reduce our revenue, cause us to issue credits or pay penalties, cause customers to terminate their subscriptions and adversely affect our renewal rates and our ability to attract new customers. Our business will also be harmed if our customers and potential customers believe our service is unreliable.

As part of our current disaster recovery arrangements, our production environment and all of our customers' data is currently replicated in near real-time in a separate facility physically located in a different geographic region of the United States. Companies and products added through acquisition may be temporarily served through an alternate facility. We do not control the operation of these facilities, and they are vulnerable to damage or interruption from earthquakes, floods, fires, power loss, telecommunications failures and similar events. They may also be subject to break-ins, sabotage, intentional acts of vandalism and similar misconduct. Despite precautions taken at these facilities, the occurrence of a natural disaster or an act of terrorism, a decision to close the facilities without adequate notice or other unanticipated problems at these facilities could result in lengthy interruptions in our service. Even with the disaster recovery arrangements, our service could be interrupted.

If our security measures are breached and unauthorized access is obtained to a customer's data, our data or our information technology systems, our service may be perceived as not being secure, customers may curtail or stop using our service and we may incur significant legal and financial exposure and liabilities.

Our service involves the storage and transmission of customers' proprietary information, and security breaches could expose us to a risk of loss of this information, litigation and possible liability. These security measures may be breached as a result of third-party action, including intentional misconduct by computer hackers, employee error, malfeasance or otherwise during transfer of data to additional data centers or at any time, and result in someone obtaining unauthorized access to our customers' data or our data, including our intellectual property and other confidential business information, or our information technology systems. Additionally, third parties may attempt to fraudulently induce employees or customers into disclosing sensitive information such as user names, passwords or other information in order to gain access to our customers' data or our data, including our intellectual property and other confidential business information, or our information technology systems. Because the techniques used to obtain unauthorized access, or to sabotage systems, change frequently and generally are not recognized until launched against a target, we may be unable to anticipate these techniques or to implement adequate preventative measures. Any security breach could result in a loss of confidence in the security of our service, damage our reputation, disrupt our business, lead to legal liability and negatively impact our future sales.

We cannot accurately predict subscription renewal or upgrade rates and the impact these rates may have on our future revenue and operating results.

Our customers have no obligation to renew their subscriptions for our service after the expiration of their initial subscription period. Our renewal rates may decline or fluctuate as a result of a number of factors, including customer dissatisfaction with our service, customers' ability to continue their operations and spending levels, and deteriorating general economic conditions. If our customers do not renew their subscriptions for our service or reduce the level of service at the time of renewal, our revenue will decline and our business will suffer.

Our future success also depends in part on our ability to sell additional features and services, more subscriptions or enhanced editions of our service to our current customers. This may also require increasingly sophisticated and costly sales efforts that are targeted at senior management. Similarly, the rate at which our customers purchase new or enhanced services depends on a number of factors, including general economic conditions. If our efforts to upsell to our customers are not successful, our business may suffer.

Weakened global economic conditions may adversely affect our industry, business and results of operations.

Our overall performance depends in part on worldwide economic conditions. The United States and other key international economies have experienced in the past a downturn in which economic activity was impacted by falling demand for a variety of goods and services, restricted credit, poor liquidity, reduced corporate profitability, volatility in credit, equity and foreign exchange markets, bankruptcies and overall uncertainty with respect to the economy. These conditions affect the rate of information technology spending and could adversely affect our customers' ability or willingness to purchase our enterprise cloud computing services, delay prospective customers' purchasing decisions, reduce the value or duration of their subscription contracts or affect renewal rates, all of which could adversely affect our operating results.

If the Company is unable to adapt to constantly changing markets and to continue to develop new products and technologies to meet the customers’ needs, the Company’s revenue and profitability will be negatively affected.

The Company’s future revenue is dependent upon the successful and timely development and licensing of new and enhanced versions of its products and potential product offerings suitable to the customer’s needs. If the Company fails to successfully upgrade existing products and develop new products, and those new products do not achieve market acceptance, the Company’s revenue will be negatively impacted.

The Company faces risks associated with the loss of maintenance and other revenue.

The Company has historically experienced the loss of long-term maintenance customers as a result of the reliability of some of its products. Some customers may not see the value in continuing to pay for maintenance that they do not need or use, and in some cases, customers have decided to replace the Company’s applications or maintain the system on their own. The Company continues to focus on these maintenance clients by providing new functionality and enhancements to meet their business needs. The Company also may lose some maintenance revenue due to consolidation of industries, macroeconomic conditions or customer operational difficulties that lead to their reduction of size. In addition, future revenue will be negatively impacted if the Company fails to add new maintenance customers that will make additional purchases of the Company’s products and services.

The Company faces risks associated with proprietary protection of the Company’s software.

The Company’s success depends on the Company’s ability to develop and protect existing and new proprietary technology and intellectual property rights. The Company seeks to protect its software, documentation and other written materials primarily through a combination of patents, trademarks, and copyright laws, trade secret laws, confidentiality procedures and contractual provisions. While the Company has attempted to safeguard and maintain the Company’s proprietary rights, there are no assurances that the Company will be successful in doing so. The Company’s competitors may independently develop or patent technologies that are substantially equivalent or superior to the Company’s.

Despite the Company’s efforts to protect its proprietary rights, unauthorized parties may attempt to copy aspects of the Company’s products or obtain and use information that the Company regards as proprietary. In some types of situations, the Company may rely in part on ‘shrink wrap’ or ‘point and click’ licenses that are not signed by the end user and, therefore, may be unenforceable under the laws of certain jurisdictions. Policing unauthorized use of the Company’s products is difficult. While the Company is unable to determine the extent to which piracy of the Company’s software exists, software piracy can be expected to be a persistent problem, particularly in foreign countries where the laws may not protect proprietary rights as fully as the United States. The Company can offer no assurance that the Company’s means of protecting its proprietary rights will be adequate or that the Company’s competitors will not reverse engineer or independently develop similar technology.

The Company may discover software errors in its products that may result in a loss of revenue, injury to the Company’s reputation or subject us to substantial liability.

Non-conformities or bugs (“errors”) may be found from time to time in the Company’s existing, new or enhanced products after commencement of commercial shipments, resulting in loss of revenue or injury to the Company’s reputation. In the past, the Company has discovered errors in its products and as a result, has experienced delays in the shipment of products. Errors in the Company’s products may be caused by defects in third-party software incorporated into the Company’s products. If so, the Company may not be able to fix these defects without the cooperation of these software providers. Since these defects may not be as significant to the software provider as they are to us, the Company may not receive the rapid cooperation that may be required. The Company may not have the contractual right to access the source code of third-party software, and even if the Company does have access to the code, the Company may not be able to fix the defect. In addition, our customers may use our service in unanticipated ways that may cause a disruption in service for other customers attempting to access their data. Since the Company’s customers use the Company’s products for critical business applications, any errors, defects or other performance problems could hurt the Company’s reputation and may result in damage to the Company’s customers’ business. If that occurs, customers could elect not to renew, delay or withhold payment to us, we could lose future sales or customers may make warranty or other claims against us, which could result in an increase in our provision for doubtful accounts, an increase in collection cycles for accounts receivable or the expense and risk of litigation. These potential scenarios, successful or otherwise, would likely be time consuming and costly.

Some competitors are larger and have greater financial and operational resources that may give them an advantage in the market.

Many of the Company’s competitors are larger and have greater financial and operational resources. This may allow them to offer better pricing terms to customers in the industry, which could result in a loss of potential or current customers or could force us to lower prices. Any of these actions could have a significant effect on revenue. In addition, the competitors may have the ability to devote more financial and operational resources to the development of new technologies that provide improved operating functionality and features to their product and service offerings. If successful, their development efforts could render the Company’s product and service offerings less desirable to customers, again resulting in the loss of customers or a reduction in the price the Company can demand for the Company’s offerings.

Risks Relating to the Company’s Common Stock

The limited public market for the Company’s securities may adversely affect an investor’s ability to liquidate an investment in the Company.

Although the Company’s common stock is currently quoted on the NASDAQ Capital Market, there is limited trading activity. The Company can give no assurance that an active market will develop, or if developed, that it will be sustained. If an investor acquires shares of the Company’s common stock, the investor may not be able to liquidate the Company’s shares should there be a need or desire to do so.

Future issuances of the Company’s shares may lead to future dilution in the value of the Company’s common stock, will lead to a reduction in shareholder voting power and may prevent a change in Company control.

The shares may be substantially diluted due to the following:

| ● |

issuance of common stock in connection with funding agreements with third parties and future issuances of common and preferred stock by the Board of Directors; and

|

| ● |

the Board of Directors has the power to issue additional shares of common stock and preferred stock and the right to determine the voting, dividend, conversion, liquidation, preferences and other conditions of the shares without shareholder approval.

|

Stock issuances may result in reduction of the book value or market price of outstanding shares of common stock. If the Company issues any additional shares of common or preferred stock, proportionate ownership of common stock and voting power will be reduced. Further, any new issuance of common or preferred stock may prevent a change in control or management.

|

PROPERTIES

|

Our principal place of business operations is located at 299 South Main Street, Suite 2370, Salt Lake City, UT 84111. We lease approximately 5,300 square feet at this corporate office location, consisting primarily of office space, conference rooms and storage areas. Our telephone number is (435) 645-2000. Our website address is http://www.parkcitygroup.com.

|

LEGAL PROCEEDINGS

|

We are, from time to time, involved in various legal proceedings incidental to the conduct of our business. Historically, the outcome of all such legal proceedings has not, in the aggregate, had a material adverse effect on our business, financial condition, results of operations or liquidity. There are no pending or threatened material legal proceedings at this time.

|

MINE SAFETY DISCLOSURES

|

Not applicable.

PART II

|

MARKET FOR COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

Share Price History

Our common stock is traded on the NASDAQ Capital Market under the trading symbol “PCYG.” The following table sets forth the high and low sales prices of our common stock for the periods indicated.

|

Quarterly Common Stock Price Ranges

|

||||||||||||||||

|

2016

|

2015

|

|||||||||||||||

|

Fiscal Quarter Ended

|

High

|

Low

|

High

|

Low

|

||||||||||||

|

September 30

|

$

|

13.99

|

$

|

10.01

|

$

|

11.48

|

$

|

9.31

|

||||||||

|

December 31

|

$

|

12.27

|

$

|

9.87

|

$

|

10.14

|

$

|

6.75

|

||||||||

|

March 31

|

$

|

11.82

|

$

|

5.98

|

$

|

14.87

|

$

|

8.62

|

||||||||

|

June 30

|

$

|

10.00

|

$

|

8.30

|

$

|

14.25

|

$

|

9.74

|

||||||||

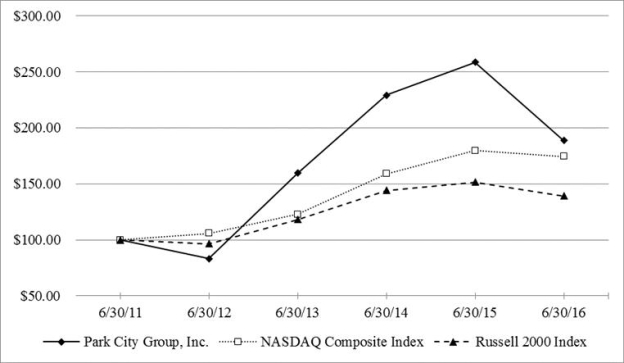

Stock Performance Graph

The following graph compares the cumulative total shareholder return on our common stock over the five-year period ending June 30, 2016, with the cumulative total returns during the same period on the NASDAQ Composite Index and the Russell 2000 Index. The graph assumes that $100 was invested on June 30, 2011 in our common stock and in the shares represented by each of the other indices, and that all dividends were reinvested.

The stock price performance included in this graph is not necessarily indicative of future stock price performance.

|

Value of Investment ($)

|

||||||||||||||||||||||||

|

06/30/11

|

06/30/12

|

06/30/13

|

06/30/14

|

06/30/15

|

06/30/16

|

|||||||||||||||||||

|

Park City Group, Inc.

|

$

|

100.00

|

$

|

83.16

|

$

|

159.58

|

$

|

229.26

|

$

|

258.74

|

$

|

188.84

|

||||||||||||

|

NASDAQ Composite

|

$

|

100.00

|

$

|

105.82

|

$

|

122.71

|

$

|

158.94

|

$

|

179.80

|

$

|

174.60

|

||||||||||||

|

Russell 2000 Index

|

$

|

100.00

|

$

|

96.50

|

$

|

118.13

|

$

|

144.18

|

$

|

151.55

|

$

|

139.22

|

||||||||||||

The stock performance graph above shall not be deemed incorporated by reference into any filing by us under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended, except to the extent that we specifically incorporate such information by reference, and shall not otherwise be deemed filed under such Acts.

Dividend Policy

To date, the Company has not paid dividends on its common stock. Our present policy is to retain future earnings (if any) for use in our operations and the expansion of our business.

Outstanding shares of Series B Preferred and Series B-1 Preferred each accrue dividends at the rate per share of 7% per annum if paid by the Company in cash, and 9% per annum if paid by the Company in additional shares of Series B-1 Preferred. Dividends on the Series B Preferred and Series B-1 Preferred are payable quarterly.

Holders of Record

At September 7, 2016 there were 660 holders of record of our common stock, and 19,286,430 shares were issued and outstanding, three holders of Series B Preferred and 625,375 shares issued and outstanding, and four holders of Series B-1 Preferred and 208,224 shares issued and outstanding. The number of holders of record and shares of common stock issued and outstanding was calculated by reference to the books and records of the Company’s transfer agent.

Issuance of Securities

We issued shares of our common stock in unregistered transactions during fiscal year 2016. All of the shares of common stock issued in non-registered transactions were issued in reliance on Section 3(a)(9) and/or Section 4(2) of the Securities Act of 1933, as amended (the “Securities Act”), and were reported in our Quarterly Reports on Form 10-Q and in our Current Reports on Form 8-K filed with the Securities and Exchange Commission during the fiscal year ended June 30, 2016. 57,117 shares of common and 28,011 shares of preferred stock were issued subsequent to June 30, 2016.

|

SELECTED FINANCIAL DATA

|

The following data has been derived from our audited financial statements, including the consolidated balance sheets at June 30, 2016 and 2015 and the related consolidated statements of operations for the three years ended June 30, 2016 and related notes appearing elsewhere in this report. The statement of operations data for the years ended June 30, 2013 and 2012 and the balance sheet data as of June 30, 2014, 2013 and 2012 are derived from our audited consolidated financial statements that are not included in this report. The following data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and related notes included elsewhere in this report.

|

Fiscal Year Ended June 30,

|

||||||||||||||||||||

|

Consolidated Statement of Operations Data

|

2016

|

2015

|

2014

|

2013

|

2012

|

|||||||||||||||

|

Revenue

|

$

|

14,010,693

|

$

|

13,648,715

|

$

|

11,928,416

|

$

|

11,318,574

|

$

|

10,098,547

|

||||||||||

|

Operating expense (1)(2)

|

13,323,252

|

17,741,109

|

14,521,141

|

10,920,375

|

11,071,259

|

|||||||||||||||

|

Income (loss) from Operations

|

687,441

|

(4,092,394

|

)

|

(2,592,725

|

)

|

398,199

|

(972,712

|

)

|

||||||||||||

|

Net income (loss)

|

666,503

|

(3,849,773

|

)

|

(2,490,145

|

)

|

257,487

|

(858,667

|

)

|

||||||||||||

|

As of June 30

|

||||||||||||||||||||

|

Consolidated Balance Sheet Data

|

2016

|

2015

|

2014

|

2013

|

2012

|

|||||||||||||||

|

Cash and Cash Equivalents

|

$

|

11,443,388

|

$

|

11,325,572

|

$

|

3,352,559

|

$

|

3,616,585

|

$

|

1,106,176

|

||||||||||

|

Working Capital

|

7,845,826

|

5,032,139

|

654,042

|

1,124,476

|

(2,354,977

|

)

|

||||||||||||||

|

Total Assets

|

38,589,892

|

36,406,784

|

16,937,632

|

15,932,898

|

11,936,230

|

|||||||||||||||

|

Total Liabilities

|

8,087,333

|

8,822,161

|

6,318,551

|

5,691,526

|

6,626,109

|

|||||||||||||||

|

Deferred Revenue

|

2,717,094

|

2,331,920

|

1,840,811

|

1,777,326

|

2,081,459

|

|||||||||||||||

|

Total Debt (current and long-term)

|

3,230,452

|

3,076,493

|

1,849,148

|

2,062,063

|

2,710,275

|

|||||||||||||||

|

Capital Leases (current and long-term)

|

-

|

-

|

-

|

-

|

41,201

|

|||||||||||||||

|

Stockholders' Equity (deficit)

|

30,502,559

|

27,584,623

|

10,619,081

|

10,241,372

|

5,310,121

|

|||||||||||||||

|

Fiscal Year Ended June 30

|

||||||||||||||||||||

|

Operating Data

|

2016

|

2015

|

2014

|

2013

|

2012

|

|||||||||||||||

|

Adjusted EBITDA (3)

|

$

|

2,273,339

|

$

|

1,118,583

|

$

|

192,719

|

$

|

2,287,868

|

$

|

1,098,877

|

||||||||||

|

Non-GAAP income per diluted common share (4)

|

$

|

0.06

|

$

|

0.01

|

$

|

(0.05

|

)

|

$

|

0.05

|

$

|

(0.05

|

)

|