Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Evolve Transition Infrastructure LP | spp-20160817x8k.htm |

|

|

Legal Disclaimers Forward-Looking Statements This presentation contains, and the officers and representatives of the Partnership and its general partner may from time to time make, “forward–looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 that are subject to a number of risks and uncertainties, many of which are beyond our control. These statement may include discussions about our: business strategy; acquisition strategy; financing strategy; ability to make, maintain and grow distributions; the ability of our customers to meet their drilling and development plans on a timely basis or at all and perform under gathering and processing agreements; future operating results, including our forecast of Adjusted EBITDA and Distributable Cash Flow; future capital expenditures; and plans, objectives, expectations, forecasts, outlook and intentions. All of these types of statements, other than statements of historical fact included in this presentation, are forward-looking statements. In some cases, forward-looking statements can be identified by terminology such as “may,” “could,” “should,” “expect,” “plan,” “project,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” “pursue,” “target,” “continue,” the negative of such terms or other comparable terminology. The forward-looking statements contained in this presentation are largely based on our expectations, which reflect estimates and assumptions made by our management. These estimates and assumptions reflect our best judgment based on currently known market conditions and other factors. Although we believe such estimates and assumptions to be reasonable, they are inherently uncertain and involve a number of risks and uncertainties that are beyond our control. In addition, management’s assumptions about future events may prove to be inaccurate. Management cautions all readers that the forward-looking statements contained in this presentation are not guarantees of future performance, and we cannot assure any reader that such statements will be realized or the forward-looking events and circumstances will occur. Actual results may differ materially from those anticipated or implied in the forward-looking statements due to important factors listed in the “Cautionary Note Regarding Forward-Looking Statements” and “Risk Factors” sections in our filings with the U.S. Securities and Exchange Commission (“SEC”) and elsewhere in those filings. The forward-looking statements speak only as of the date made, and other than as required by law, we do not intend to publicly update or revise any forward-looking statements as a result of new information, future events or otherwise. These cautionary statements qualify all forward-looking statements attributable to us or persons acting on our behalf. Oil and Gas Reserves The SEC requires oil and gas companies, in filings with the SEC, to disclose “proved oil and gas reserves” (i.e., quantities of oil and gas that are estimated with reasonable certainty to be economically producible) and permits oil and gas companies to disclose “probable reserves” (i.e., quantities of oil and gas that are as likely as not to be recovered) and “possible reserves” (i.e., additional quantities of oil and gas that might be recovered, but with a lower probability than probable reserves). Investors are urged to consider closely the disclosure in Sanchez Production Partners’ Annual Report on Form 10-K for the most recent fiscal year. 2 © 2016 Sanchez Production Partners LP |

|

|

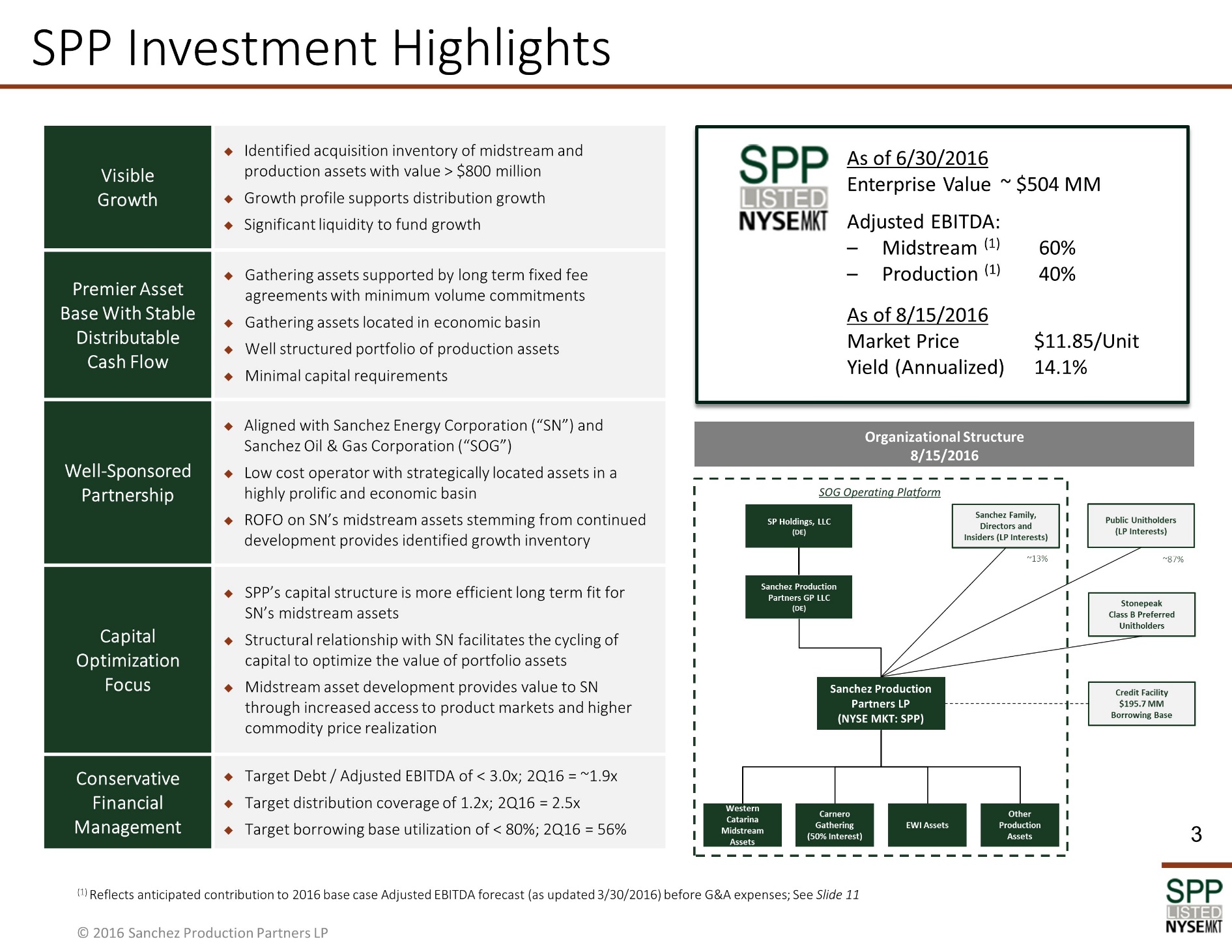

SPP Investment Highlights As of 6/30/2016 Enterprise Value ~ $504 MM Adjusted EBITDA: Midstream (1) 60% Production (1) 40% As of 8/15/2016 Market Price $11.85/Unit Yield (Annualized) 14.1% (1) Reflects anticipated contribution to 2016 base case Adjusted EBITDA forecast (as updated 3/30/2016) before G&A expenses; See Slide 11 Visible Growth Identified acquisition inventory of midstream and production assets with value > $800 million Growth profile supports distribution growth Significant liquidity to fund growth Premier Asset Base With Stable Distributable Cash Flow Gathering assets supported by long term fixed fee agreements with minimum volume commitments Gathering assets located in economic basin Well structured portfolio of production assets Minimal capital requirements Well-Sponsored Partnership Aligned with Sanchez Energy Corporation (“SN”) and Sanchez Oil & Gas Corporation (“SOG”) Low cost operator with strategically located assets in a highly prolific and economic basin ROFO on SN’s midstream assets stemming from continued development provides identified growth inventory Capital Optimization Focus SPP’s capital structure is more efficient long term fit for SN’s midstream assets Structural relationship with SN facilitates the cycling of capital to optimize the value of portfolio assets Midstream asset development provides value to SN through increased access to product markets and higher commodity price realization Conservative Financial Management Target Debt / Adjusted EBITDA of < 3.0x; 2Q16 = ~1.9x Target distribution coverage of 1.2x; 2Q16 = 2.5x Target borrowing base utilization of < 80%; 2Q16 = 56% 3 SP Holdings, LLC (DE) Sanchez Production Partners GP LLC (DE) Sanchez Production Partners LP (NYSE MKT: SPP) EWI Assets Carnero Gathering (50% Interest) Western Catarina Midstream Assets Other Production Assets Sanchez Family, Directors and Insiders (LP Interests) Public Unitholders (LP Interests) Stonepeak Class B Preferred Unitholders Credit Facility $195.7 MM Borrowing Base SOG Operating Platform Organizational Structure 8/15/2016 ~13% ~87% |

|

|

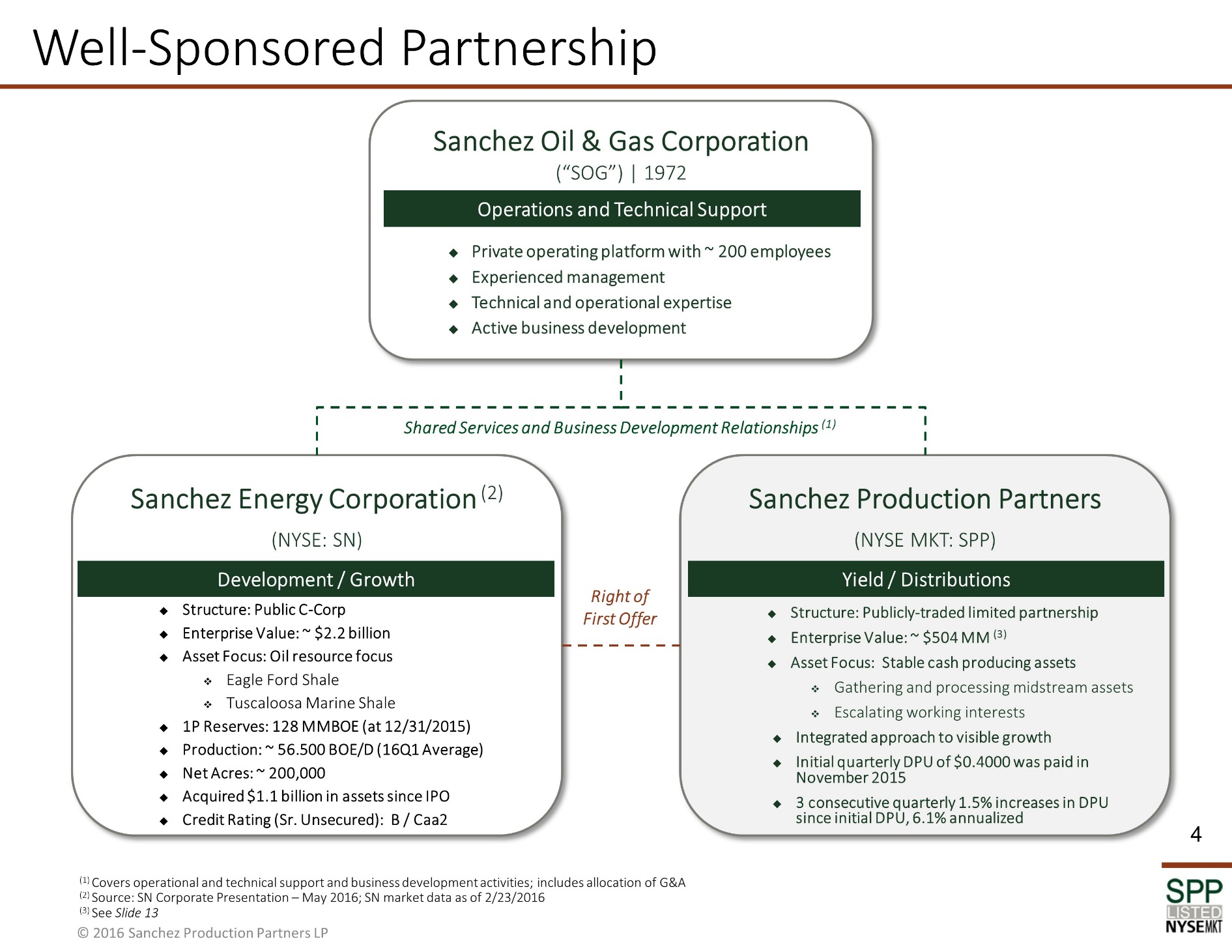

Well-Sponsored Partnership Sanchez Oil & Gas Corporation (“SOG”) 1972 Private operating platform with ~ 200 employees Experienced management Technical and operational expertise Active business development Shared Services and Business Development Relationships (1) Sanchez Energy Corporation (2) (NYSE: SN) Structure: Public C-Corp Enterprise Value: ~ $2.2 billion Asset Focus: Oil resource focus Eagle Ford Shale Tuscaloosa Marine Shale 1P Reserves: 128 MMBOE (at 12/31/2015) Production: ~ 56.500 BOE/D (16Q1 Average) Net Acres: ~ 200,000 Acquired $1.1 billion in assets since IPO Credit Rating (Sr. Unsecured): B / Caa2 Sanchez Production Partners (NYSE MKT: SPP) Structure: Publicly-traded limited partnership Enterprise Value: ~ $504 MM (3) Asset Focus: Stable cash producing assets Gathering and processing midstream assets Escalating working interests Integrated approach to visible growth Initial quarterly DPU of $0.4000 was paid in November 2015 3 consecutive quarterly 1.5% increases in DPU since initial DPU, 6.1% annualized Development / Growth Yield / Distributions Operations and Technical Support (1) Covers operational and technical support and business development activities; includes allocation of G&A (2) Source: SN Corporate Presentation – May 2016; SN market data as of 2/23/2016 (3) See Slide 13 Right of First Offer 4 |

|

|

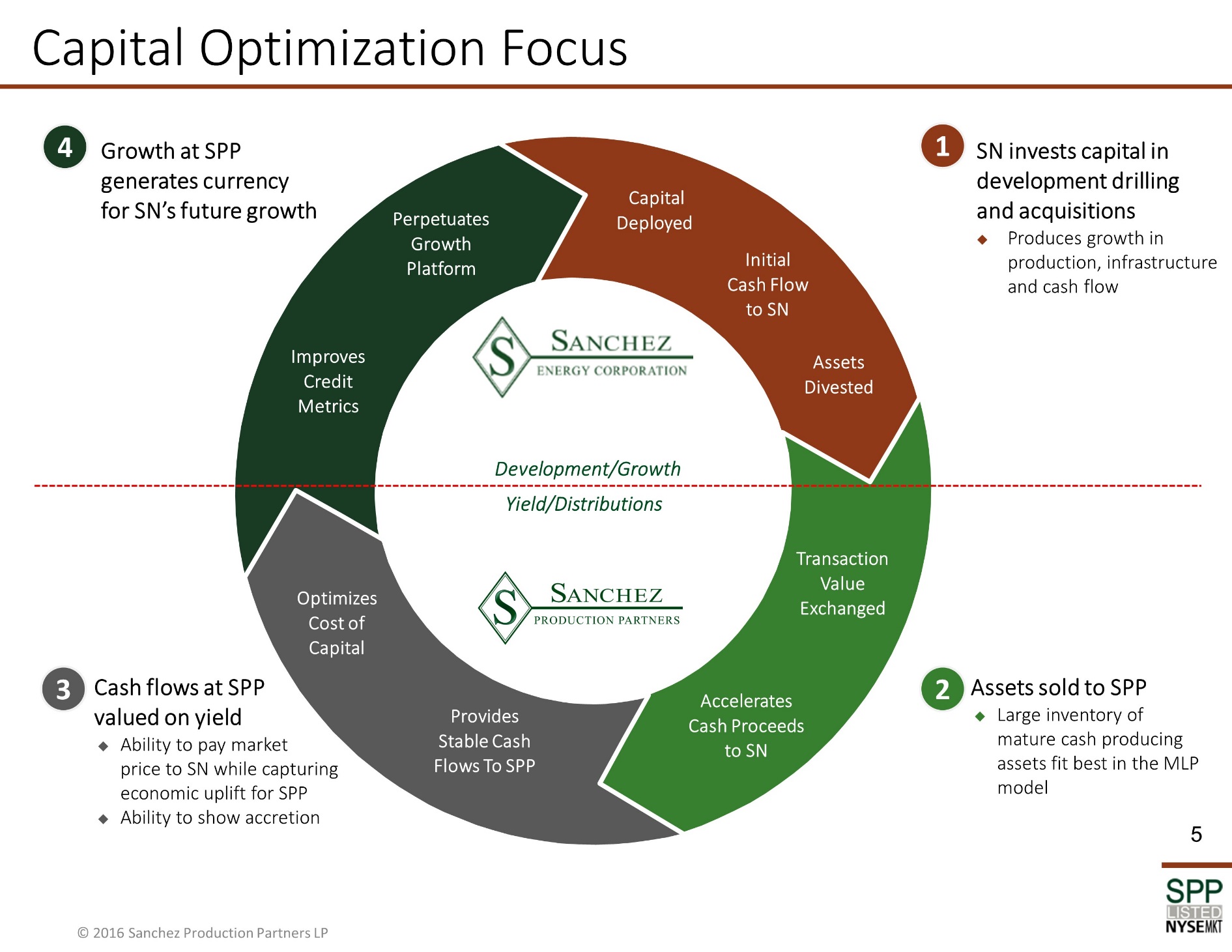

Capital Optimization Focus Growth at SPP generates currency for SN’s future growth SN invests capital in development drilling and acquisitions Produces growth in production, infrastructure and cash flow Assets sold to SPP Large inventory of mature cash producing assets fit best in the MLP model Cash flows at SPP valued on yield Ability to pay market price to SN while capturing economic uplift for SPP Ability to show accretion 4 1 2 3 Perpetuates Growth Platform Capital Deployed Assets Divested Accelerates Cash Proceeds to SN Transaction Value Exchanged Provides Stable Cash Flows To SPP Optimizes Cost of Capital Initial Cash Flow to SN Development/Growth Yield/Distributions Improves Credit Metrics 5 |

|

|

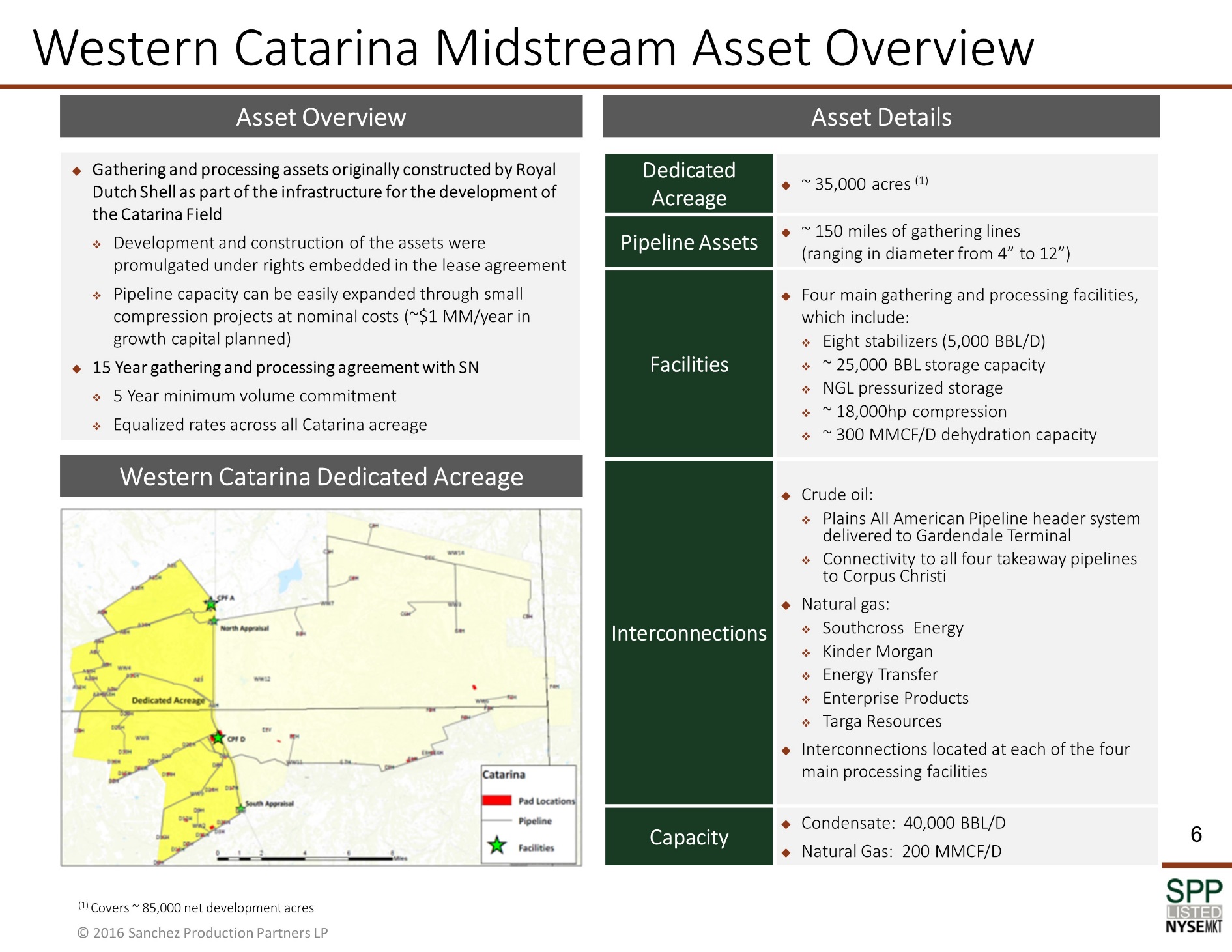

Gathering and processing assets originally constructed by Royal Dutch Shell as part of the infrastructure for the development of the Catarina Field Development and construction of the assets were promulgated under rights embedded in the lease agreement Pipeline capacity can be easily expanded through small compression projects at nominal costs (~$1 MM/year in growth capital planned) 15 Year gathering and processing agreement with SN 5 Year minimum volume commitment Equalized rates across all Catarina acreage Western Catarina Midstream Asset Overview Asset Details Asset Overview Western Catarina Dedicated Acreage (1) Covers ~ 85,000 net development acres 6 Dedicated Acreage ~ 35,000 acres (1) Pipeline Assets ~ 150 miles of gathering lines (ranging in diameter from 4” to 12”) Facilities Four main gathering and processing facilities, which include: Eight stabilizers (5,000 BBL/D) ~ 25,000 BBL storage capacity NGL pressurized storage ~ 18,000hp compression ~ 300 MMCF/D dehydration capacity Interconnections Crude oil: Plains All American Pipeline header system delivered to Gardendale Terminal Connectivity to all four takeaway pipelines to Corpus Christi Natural gas: Southcross Energy Kinder Morgan Energy Transfer Enterprise Products Targa Resources Interconnections located at each of the four main processing facilities Capacity Condensate: 40,000 BBL/D Natural Gas: 200 MMCF/D |

|

|

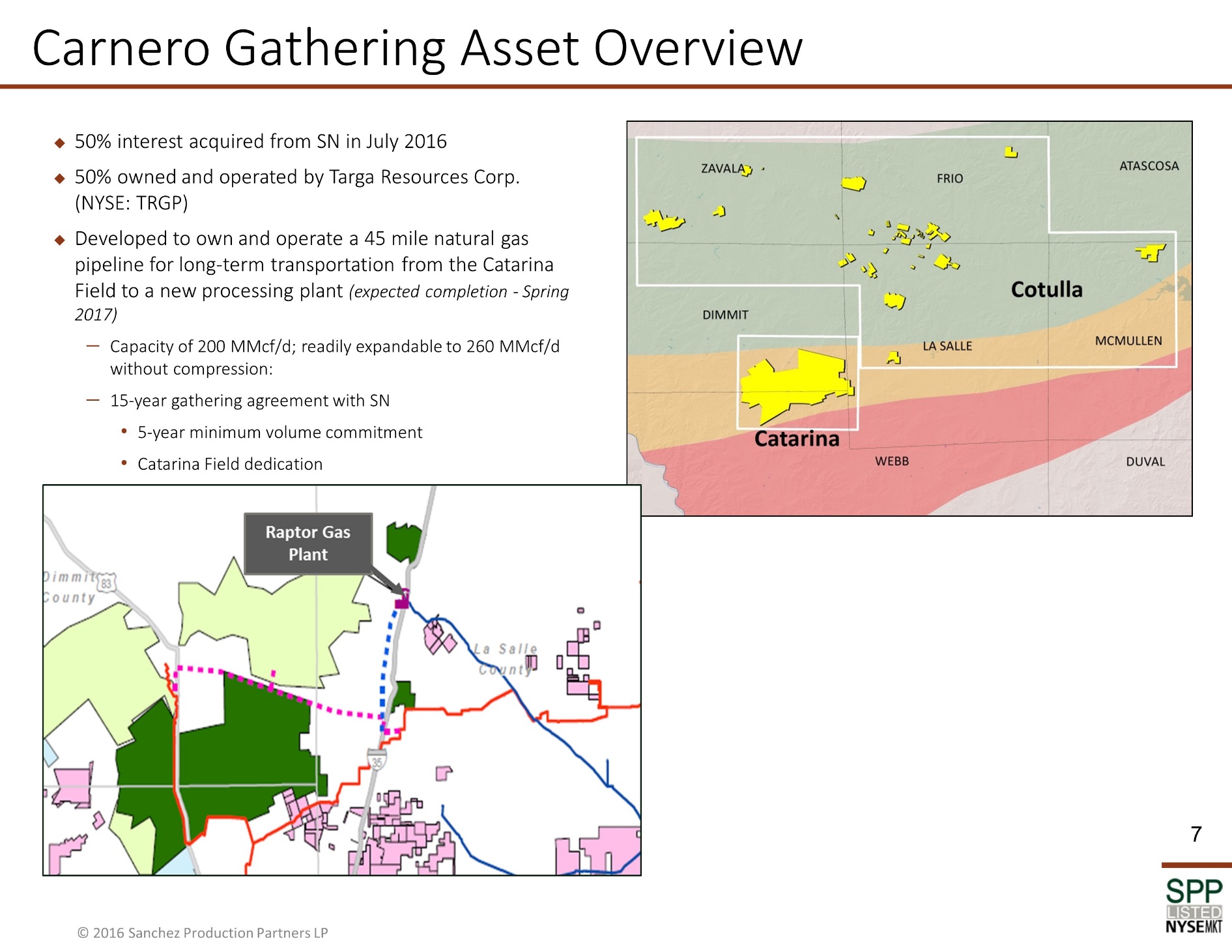

7 Carnero Gathering Asset Overview 50% interest acquired from SN in July 2016 50% owned and operated by Targa Resources Corp. (NYSE: TRGP) Developed to own and operate a 45 mile natural gas pipeline for long-term transportation from the Catarina Field to a new processing plant (expected completion - Spring 2017) Capacity of 200 MMcf/d; readily expandable to 260 MMcf/d without compression: 15-year gathering agreement with SN 5-year minimum volume commitment Catarina Field dedication |

|

|

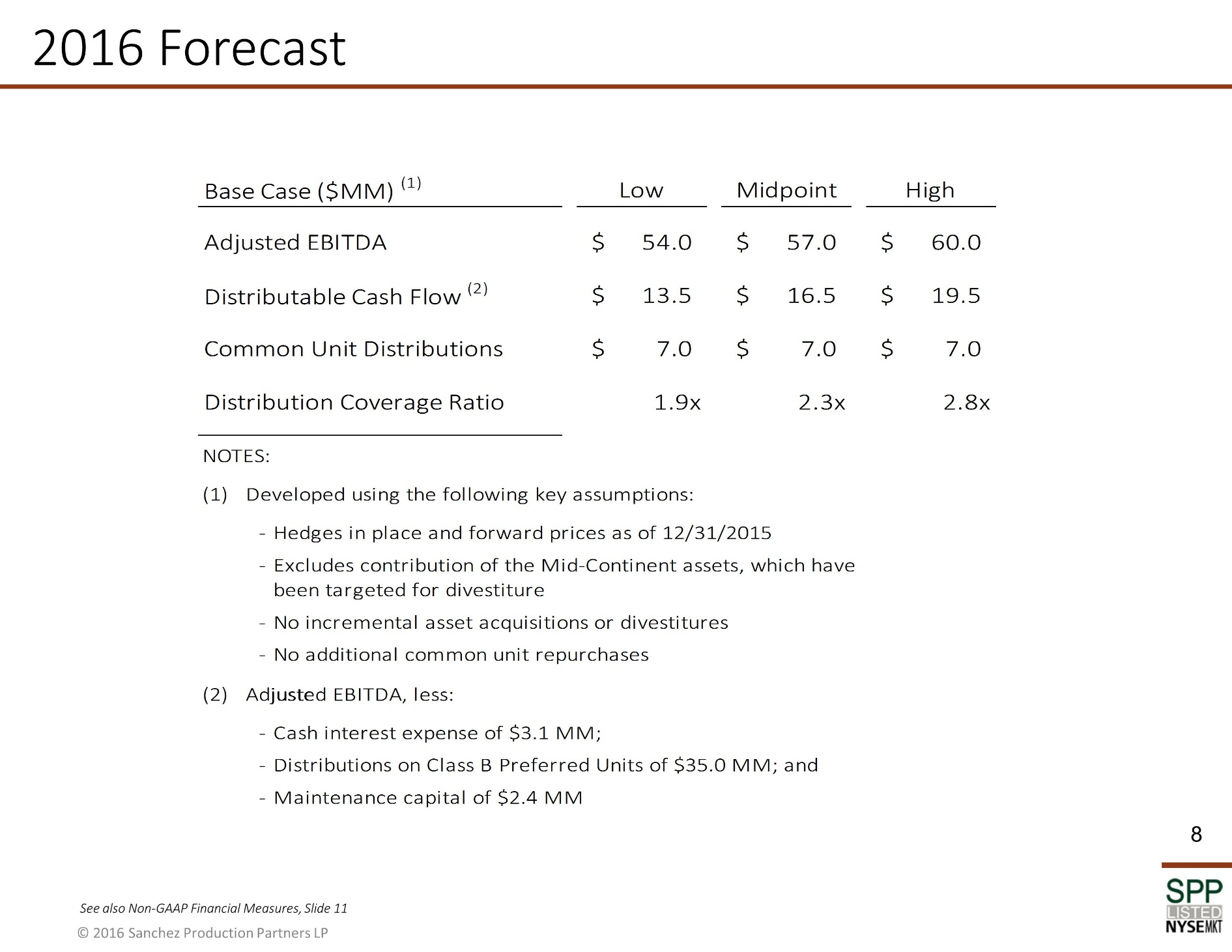

2016 Forecast 8 See also Non-GAAP Financial Measures, Slide 11 Base Case ($MM) (1) Low Midpoint High Adjusted EBITDA $ 54.0 $ 57.0 $ 60.0 Distributable Cash Flow (2) $ 13.5 $ 16.5 $ 19.5 Common Unit Distributions $ 7.0 $ 7.0 $ 7.0 Distribution Coverage Ratio 1.9x 2.3x 2.8x NOTES: (1) Developed using the following key assumptions: - Hedges in place and forward prices as of 12/31/2015 - Excludes contribution of the Mid-Continent assets, which have been targeted for divestiture - No incremental asset acquisitions or divestitures - No additional common unit repurchases (2) Adjusted EBITDA, less: - Cash interest expense of $3.1 MM; - Distributions on Class B Preferred Units of $35.0 MM; and - Maintenance capital of $2.4 MM |

|

|

Appendix I Select Financial Information |

|

|

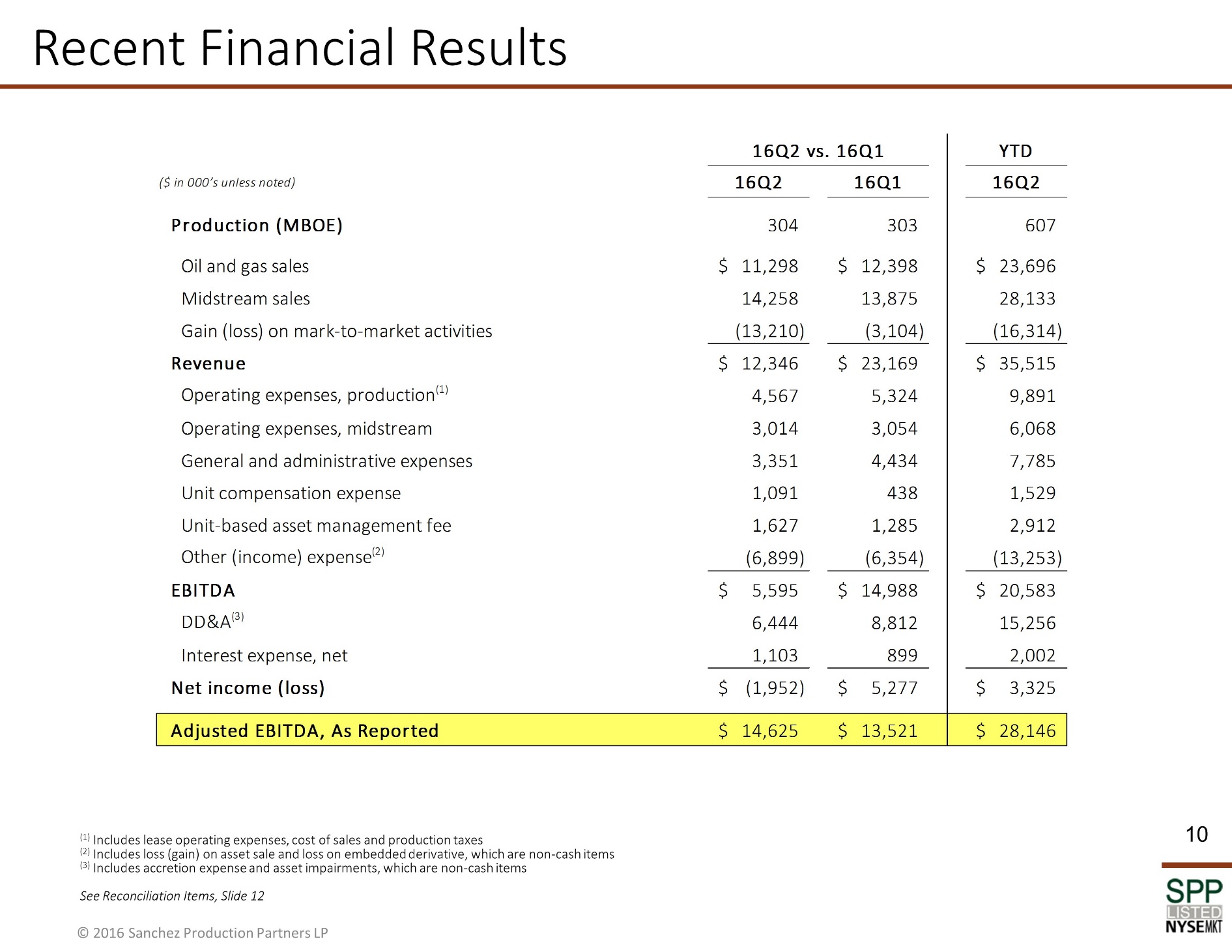

Recent Financial Results 10 (1) Includes lease operating expenses, cost of sales and production taxes (2) Includes loss (gain) on asset sale and loss on embedded derivative, which are non-cash items (3) Includes accretion expense and asset impairments, which are non-cash items See Reconciliation Items, Slide 12 16Q2 vs. 16Q1 YTD ($ in 000’s unless noted) 16Q2 16Q1 16Q2 Production (MBOE) 304 303 607 Oil and gas sales $ 11,298 $ 12,398 $ 23,696 Midstream sales 14,258 13,875 28,133 Gain (loss) on mark-to-market activities (13,210) (3,104) (16,314) Revenue $ 12,346 $ 23,169 $ 35,515 Operating expenses, production(1) 4,567 5,324 9,891 Operating expenses, midstream 3,014 3,054 6,068 General and administrative expenses 3,351 4,434 7,785 Unit compensation expense 1,091 438 1,529 Unit-based asset management fee 1,627 1,285 2,912 Other (income) expense(2) (6,899) (6,354) (13,253) EBITDA $ 5,595 $ 14,988 $ 20,583 DD&A(3) 6,444 8,812 15,256 Interest expense, net 1,103 899 2,002 Net income (loss) $ (1,952) $ 5,277 $ 3,325 Adjusted EBITDA, As Reported $ 14,625 $ 13,521 $ 28,146 |

|

|

Non-GAAP Financial Measures Use of Non-GAAP Financial Measures – Historic Financials: EBITDA and Adjusted EBITDA are non-GAAP financial measures that are reconciled to their most comparable GAAP financial measure under Reconciliation of Non-GAAP Financial Measures in this presentation. The reconciliations are only intended to be reviewed in conjunction with the presentation to which they relate. EBITDA is defined as net income (loss) adjusted by interest (income) expense, net, which includes interest expense, interest expense net (gain) loss on interest rate derivative contacts and interest (income); income tax expense (benefit); depreciation, depletion and amortization; asset impairments; and accretion expense. Adjusted EBITDA is defined as EBITDA adjusted by (gain) loss on sale of assets; (gain) loss from equity investment; unit-based compensation programs; unit-based asset management fees; (gain) loss from mark-to-market activities; and (gain) loss on embedded derivative. Distributable Cash Flow is defined as Adjusted EBITDA less cash interest expense; distributions on preferred units; and maintenance capital expenditures. These financial measures are used as quantitative standards by our management and by external users of our financial statements such as investors, research analysts and others to assess the financial performance of our assets without regard to financing methods, capital structure or historical cost basis; the ability of our assets to generate cash sufficient to pay interest costs and support our indebtedness; and our operating performance and return on capital as compared to those of other companies in our industry, without regard to financing or capital structure. These financial measures are not intended to represent cash flows for the period, nor are they presented as a substitute for net income, operating income, cash flows from operating activities or any other measure of financial performance or liquidity presented in accordance with GAAP. Use of Non-GAAP Financial Measures – Forecast Financials: In addition to Adjusted EBITDA, we provide a forecast of Distributable Cash Flow in this presentation. We are unable to reconcile our forecast range of Adjusted EBITDA or Distributable Cash Flow to GAAP net income (loss), operating income or net cash flow provided by operating activities because we do not predict the future impact of adjustments to (i) net income (loss) for unit based compensation and asset management fees, (gains) losses from mark-to-market activities and equity investments or asset impairments due to the difficulty of doing so, or (ii) net cash flow provided by operating activities because this metric includes the impact of changes in operating assets and liabilities related to the timing of cash receipts and disbursements that may not relate to the period in which the operating activities occurred. Additionally, we are unable to address the probable significance of the unavailable reconciliation, in significant part due to ranges in our forecast impacted by changes in oil and natural gas prices and reserves which affect certain reconciliation items. Summary of Non-GAAP Financial Measures : 11 © 2016 Sanchez Production Partners LP Non-GAAP Measure Slide(s) Where Used in Presentation Most Comparable GAAP Measure Slide Containing Reconciliations Adjusted EBITDA, EBITDA 10 Net Income 12 |

|

|

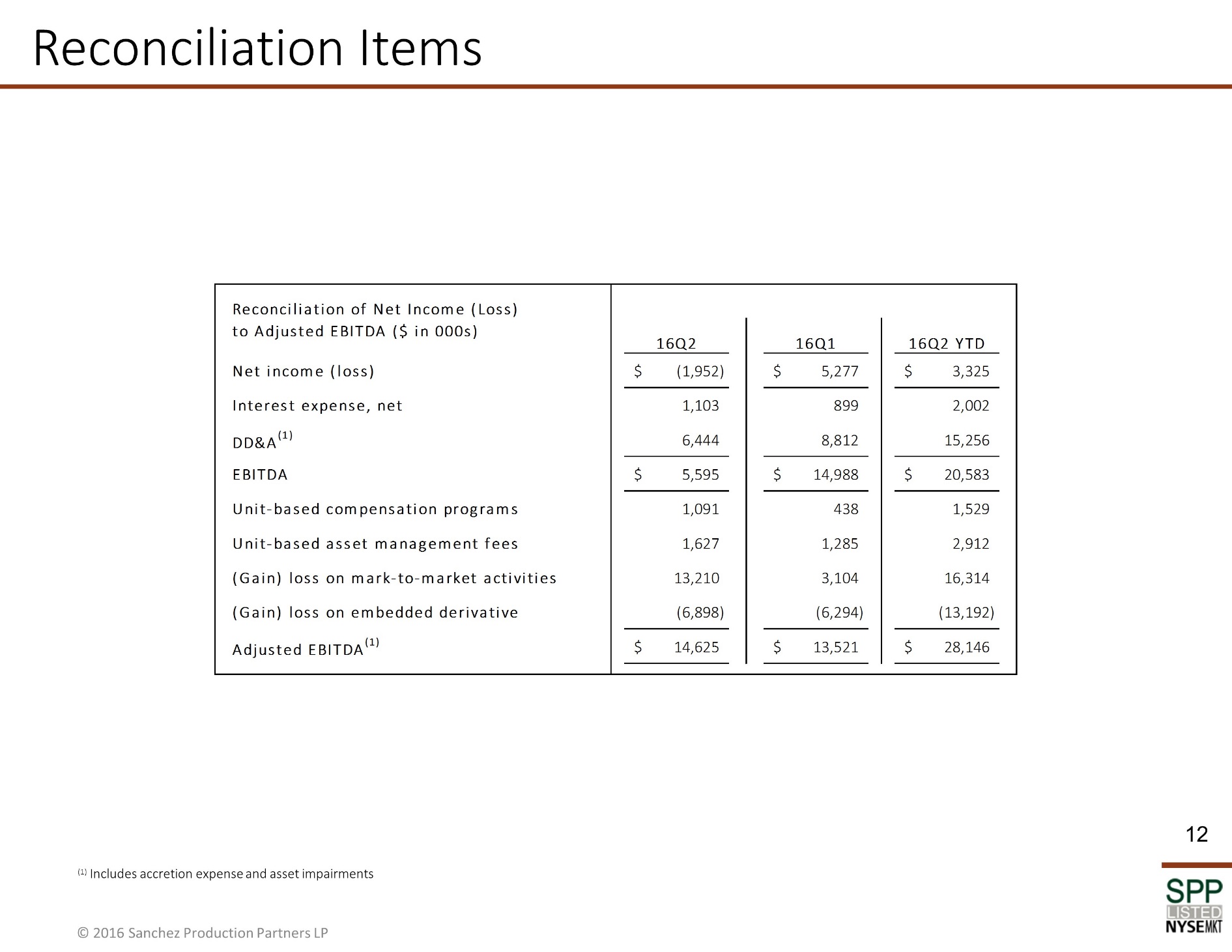

Reconciliation Items 12 (1) Includes accretion expense and asset impairments Reconciliation of Net Income (Loss) to Adjusted EBITDA ($ in 000s) 16Q2 16Q1 16Q2 YTD Net income (loss) $ (1,952) $ 5,277 $ 3,325 Interest expense, net 1,103 899 2,002 DD&A(1) 6,444 8,812 15,256 EBITDA $ 5,595 $ 14,988 $ 20,583 Unit-based compensation programs 1,091 438 1,529 Unit-based asset management fees 1,627 1,285 2,912 (Gain) loss on mark-to-market activities 13,210 3,104 16,314 (Gain) loss on embedded derivative (6,898) (6,294) (13,192) Adjusted EBITDA(1) $ 14,625 $ 13,521 $ 28,146 |

|

|

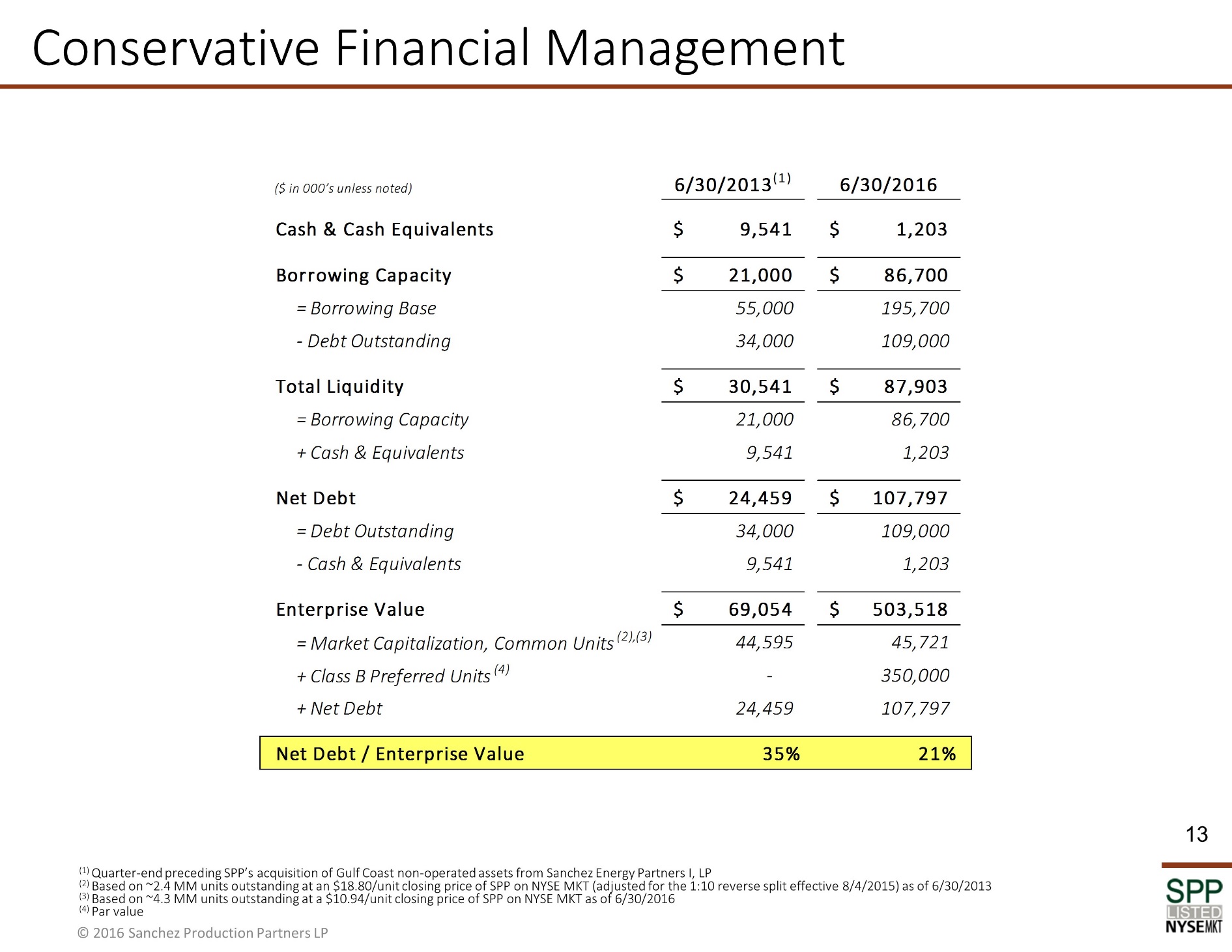

Conservative Financial Management 13 (1) Quarter-end preceding SPP’s acquisition of Gulf Coast non-operated assets from Sanchez Energy Partners I, LP (2) Based on ~2.4 MM units outstanding at an $18.80/unit closing price of SPP on NYSE MKT (adjusted for the 1:10 reverse split effective 8/4/2015) as of 6/30/2013 (3) Based on ~4.3 MM units outstanding at a $10.94/unit closing price of SPP on NYSE MKT as of 6/30/2016 (4) Par value ($ in 000’s unless noted) 6/30/2013(1) 6/30/2016 Cash & Cash Equivalents $ 9,541 $ 1,203 Borrowing Capacity $ 21,000 $ 86,700 = Borrowing Base 55,000 195,700 - Debt Outstanding 34,000 109,000 Total Liquidity $ 30,541 $ 87,903 = Borrowing Capacity 21,000 86,700 + Cash & Equivalents 9,541 1,203 Net Debt $ 24,459 $ 107,797 = Debt Outstanding 34,000 109,000 - Cash & Equivalents 9,541 1,203 Enterprise Value $ 69,054 $ 503,518 = Market Capitalization, Common Units(2),(3) 44,595 45,721 + Class B Preferred Units(4) - 350,000 + Net Debt 24,459 107,797 Net Debt / Enterprise Value 35% 21% |

|

|

Appendix II Western Catarina Midstream |

|

|

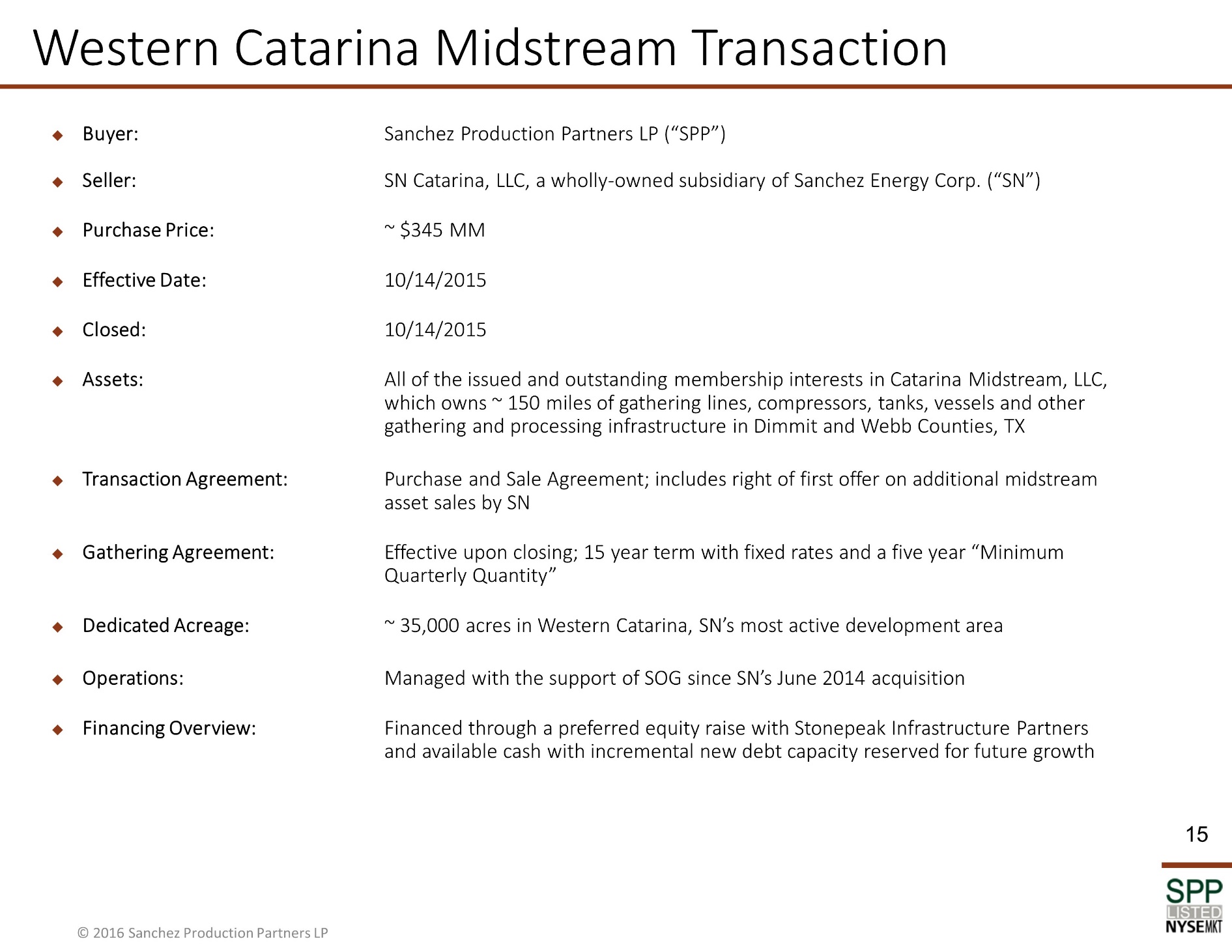

Western Catarina Midstream Transaction Buyer: Sanchez Production Partners LP (“SPP”) Seller: SN Catarina, LLC, a wholly-owned subsidiary of Sanchez Energy Corp. (“SN”) Purchase Price: ~ $345 MM Effective Date: 10/14/2015 Closed: 10/14/2015 Assets: All of the issued and outstanding membership interests in Catarina Midstream, LLC, which owns ~ 150 miles of gathering lines, compressors, tanks, vessels and other gathering and processing infrastructure in Dimmit and Webb Counties, TX Transaction Agreement: Purchase and Sale Agreement; includes right of first offer on additional midstream asset sales by SN Gathering Agreement: Effective upon closing; 15 year term with fixed rates and a five year “Minimum Quarterly Quantity” Dedicated Acreage: ~ 35,000 acres in Western Catarina, SN’s most active development area Operations: Managed with the support of SOG since SN’s June 2014 acquisition Financing Overview: Financed through a preferred equity raise with Stonepeak Infrastructure Partners and available cash with incremental new debt capacity reserved for future growth 15 |

|

|

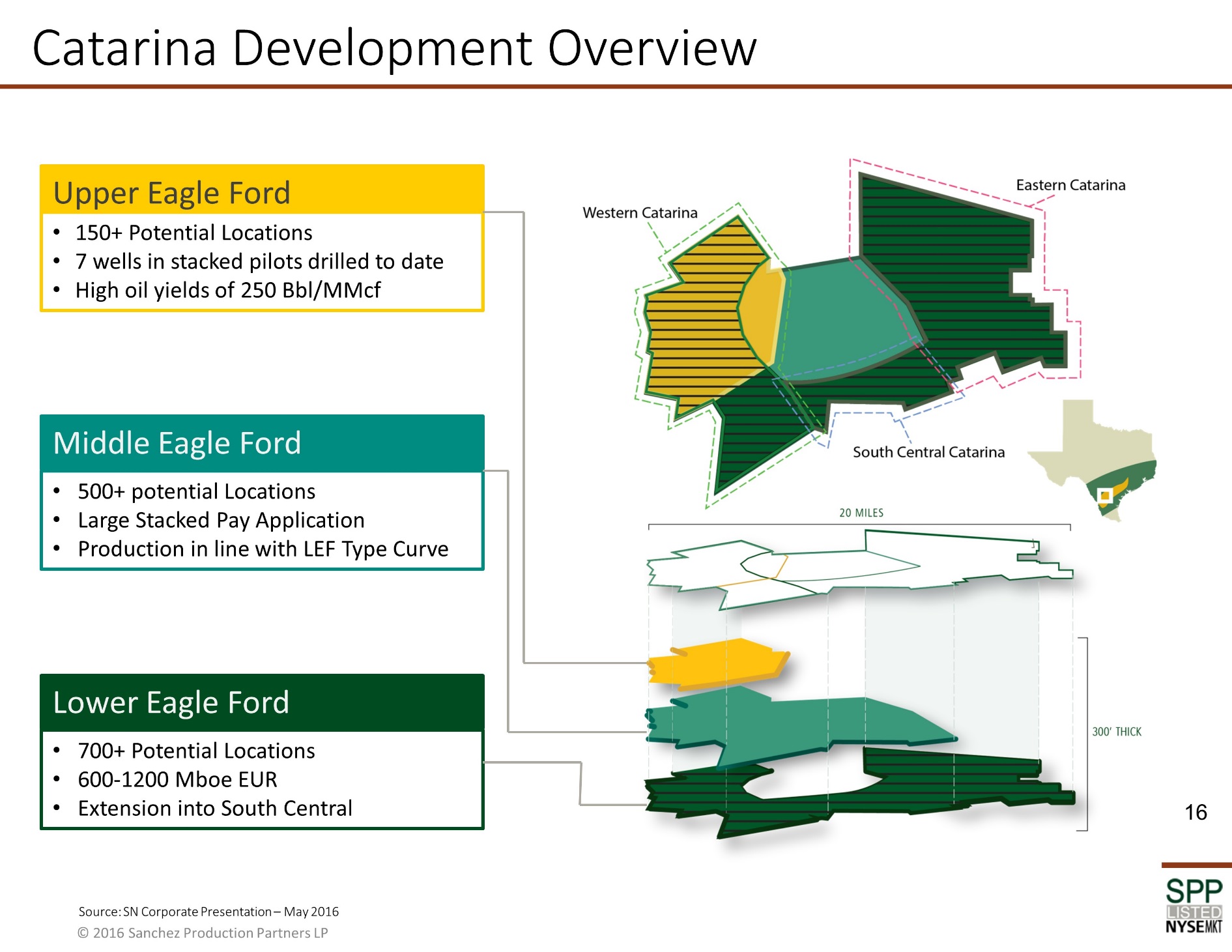

16 Catarina Development Overview Upper Eagle Ford 150+ Potential Locations 7 wells in stacked pilots drilled to date High oil yields of 250 Bbl/MMcf 500+ potential Locations Large Stacked Pay Application Production in line with LEF Type Curve Middle Eagle Ford 700+ Potential Locations 600-1200 Mboe EUR Extension into South Central Lower Eagle Ford Source: SN Corporate Presentation – May 2016 |

|

|

Appendix III Escalating Working Interest |

|

|

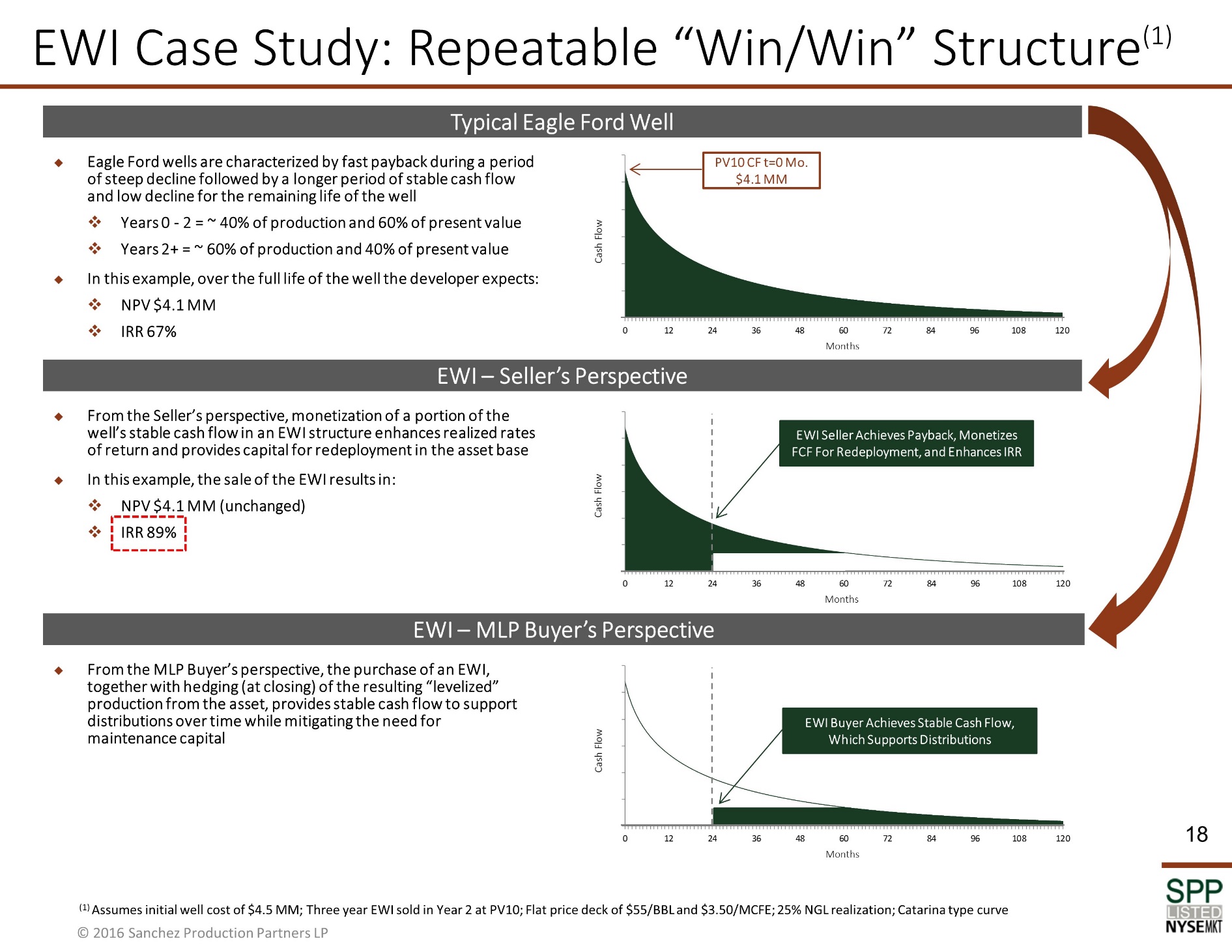

From the Seller’s perspective, monetization of a portion of the well’s stable cash flow in an EWI structure enhances realized rates of return and provides capital for redeployment in the asset base In this example, the sale of the EWI results in: NPV $4.1 MM (unchanged) IRR 89% Eagle Ford wells are characterized by fast payback during a period of steep decline followed by a longer period of stable cash flow and low decline for the remaining life of the well Years 0 - 2 = ~ 40% of production and 60% of present value Years 2+ = ~ 60% of production and 40% of present value In this example, over the full life of the well the developer expects: NPV $4.1 MM IRR 67% EWI Case Study: Repeatable “Win/Win” Structure(1) Typical Eagle Ford Well EWI – Seller’s Perspective EWI – MLP Buyer’s Perspective (1) Assumes initial well cost of $4.5 MM; Three year EWI sold in Year 2 at PV10; Flat price deck of $55/BBL and $3.50/MCFE; 25% NGL realization; Catarina type curve EWI Seller Achieves Payback, Monetizes FCF For Redeployment, and Enhances IRR EWI Buyer Achieves Stable Cash Flow, Which Supports Distributions PV10 CF t=0 Mo. $4.1 MM From the MLP Buyer’s perspective, the purchase of an EWI, together with hedging (at closing) of the resulting “levelized” production from the asset, provides stable cash flow to support distributions over time while mitigating the need for maintenance capital 18 Cash Flow Cash Flow Cash Flow Months Months Months $ 0.0 $ 1.0 $ 2.0 $ 3.0 $ 4.0 $ 5.0 $ 6.0 0 12 24 36 48 60 72 84 96 108 120 Remaining PV ($mm) Months $ 0.0 $ 1.0 $ 2.0 $ 3.0 $ 4.0 $ 5.0 $ 6.0 0 12 24 36 48 60 72 84 96 108 120 Remaining PV ($mm) Months $ 0.0 $ 1.0 $ 2.0 $ 3.0 $ 4.0 $ 5.0 $ 6.0 0 12 24 36 48 60 72 84 96 108 120 Remaining PV ($mm) Months |

|

|

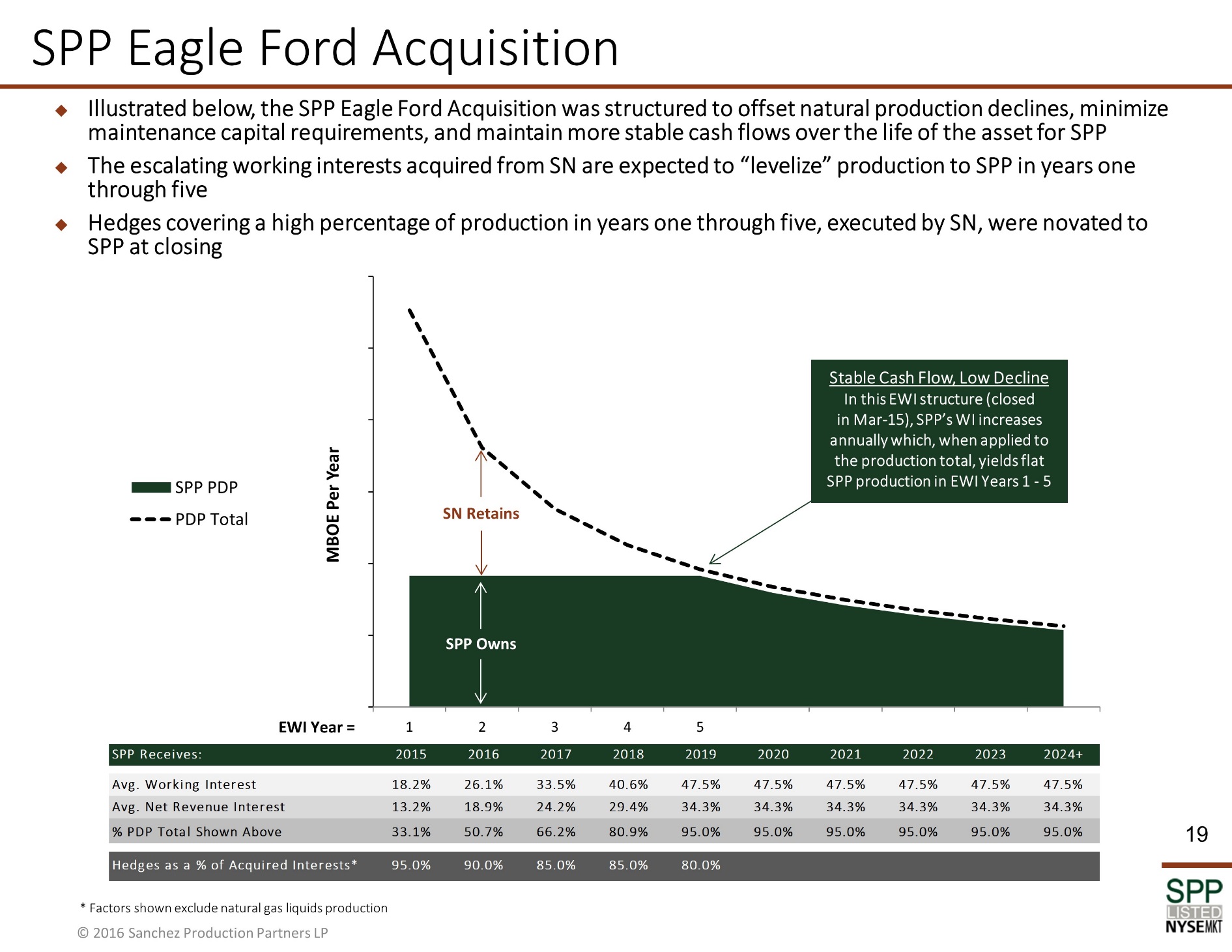

SPP Eagle Ford Acquisition Illustrated below, the SPP Eagle Ford Acquisition was structured to offset natural production declines, minimize maintenance capital requirements, and maintain more stable cash flows over the life of the asset for SPP The escalating working interests acquired from SN are expected to “levelize” production to SPP in years one through five Hedges covering a high percentage of production in years one through five, executed by SN, were novated to SPP at closing Escalating Working Interest Purchased From SN By SPP SN Retains EWI Year = * * Factors shown exclude natural gas liquids production Stable Cash Flow, Low Decline In this EWI structure (closed in Mar-15), SPP’s WI increases annually which, when applied to the production total, yields flat SPP production in EWI Years 1 - 5 SPP Owns 19 - 200 400 600 800 1,000 1,200 1 2 3 4 5 MBOE Per Year SPP PDP PDP Total SPP Receives: 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024+ Avg. Working Interest 18.2% 26.1% 33.5% 40.6% 47.5% 47.5% 47.5% 47.5% 47.5% 47.5% Avg. Net Revenue Interest 13.2% 18.9% 24.2% 29.4% 34.3% 34.3% 34.3% 34.3% 34.3% 34.3% % PDP Total Shown Above 33.1% 50.7% 66.2% 80.9% 95.0% 95.0% 95.0% 95.0% 95.0% 95.0% Hedges as a % of Acquired Interests* 95.0% 90.0% 85.0% 85.0% 80.0% |