Attached files

| file | filename |

|---|---|

| 8-K - 8-K - STIFEL FINANCIAL CORP | d228990d8k.htm |

Stifel Financial Corp. August 2016 Exhibit 99.1 |

2 Disclaimer Forward-Looking Statements

This presentation may contain

“forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 that involve significant risks, assumptions, and uncertainties, including statements relating to the market

opportunity and future business prospects of

Stifel Financial Corp., as well as Stifel, Nicolaus & Company, Incorporated and its subsidiaries (collectively, “SF” or the “Company”). These statements can be identified by the use of the

words “may,” “will,” “should,” “could,” “would,” “plan,” “potential,” “estimate,”

“project,” “believe,” “intend,” “anticipate,” “expect,” and similar expressions. In particular, these statements may refer to our goals, intentions, and expectations, our business plans and growth

strategies, our ability to integrate and

manage our acquired businesses, estimates of our risks and future costs and benefits, and forecasted demographic and economic trends relating to our industry. You should not place undue reliance on any forward-looking statements, which speak only as of the date they were

made. We will not update these

forward-looking statements, even though our situation may change in the future, unless we are obligated to do so under federal securities laws. Actual results may differ materially and reported results should not be considered as an indication of future

performance. Factors that could cause

actual results to differ are included in the Company’s annual and quarterly reports and from time to time in other reports filed by the Company with the Securities and Exchange Commission and include, among other things, changes in

general economic and business conditions,

actions of competitors, regulatory and legal actions, changes in legislation, and technology changes.

Use of Non-GAAP Financial Measures The Company utilized non-GAAP calculations of presented net revenues, compensation and benefits,

non-compensation operating expenses,

income before income taxes, provision for income taxes, net income, compensation and non-compensation operating expense ratios, pre-tax margin and diluted earnings per share as an additional measure to aid in

understanding and analyzing the

Company’s financial results for the three and six months ended June 30, 2016. Specifically, the Company believes that the non-GAAP measures provide useful information by excluding certain items that may not be indicative of

the Company’s operating results and

business outlook. The Company believes that these non-GAAP measures will allow for a better evaluation of the operating performance of the business and facilitate a meaningful comparison of the Company’s results in the

current period to those in prior periods and

future periods. Reference to these non-GAAP measures should not be considered as a substitute for results that are presented in a manner consistent with GAAP. These non-GAAP measures are provided to enhance

investors' overall understanding of the

Company’s financial performance. |

Our Strategy |

4 Strategic Vision To build a premier wealth management and investment banking firm

2,298 financial

advisors in

over 360

branches with

more than

$200B in client

assets

Private

Client

Asset

Management

Bank

$26B in total

assets

managed

through

various

strategies

Equities

Sales +

Trading

$9.4B in assets

funded by

client deposits

Global Wealth Management

Institutional

Fixed

Income

Sales +

Trading

Investment

Banking

Research

Experienced

sales force with

extensive

distribution

capabilities

Comprehensive

platform

including

research,

strategy and

DCM teams

Over 350

professionals

with extensive

experience

across all

products and

industry

verticals

Largest

research

platform with

approximately

1,300 U.S. and

290 European

stocks covered |

5 A History of Growth 2005 Legg Mason’s Capital Markets Division 2008 Butler Wick 2009 56 UBS Private Client Branches 2010 Thomas Weisel Partners 2007 Ryan Beck Acquisition Stifel Bank & Trust 2011 Stone & Youngberg 2012 Miller Buckfire 2013 Knight Capital Group’s Fixed Income Division 2014 De La Rosa, Oriel Securities, 1919 Investment Counsel, Merchant Capital 2013 Keefe, Bruyette & Woods 2013 Acacia Bank & Ziegler Lotsoff 2015 Barclays Wealth & Investment Management, Sterne Agee, Sidoti Joint Venture, Leumi Partners Collaboration Agreement * 2016 Net Revenue annualized based on 1H16 results and adjustment for 2H16 for impact of the sale of legacy Sterne

Agee business 2016

Eaton Partners

ISM Capital |

Driving Shareholder Value Through Deal Integration & Balance Sheet Growth |

7 Core & GAAP EPS to Converge as Deal Charges Realized

Footnotes:

• EPS estimates for 3Q16 - 4Q17 as well as 2016 and 2017 based on consensus core EPS estimates as of 8/15/2016

• Analysis of convergence between Core and GAAP EPS based solely on current announced acquisitions.

2012 2013 2014 2015 2016 2017 Core $0.63 $0.58 $0.60 $0.53 $0.79 $0.69 $0.68 $0.64 $0.75 $0.65 $0.71 $0.60 $0.51 $0.57 $0.69 $0.60 $0.68 $0.65 $0.74 $0.72 $0.84 GAAP $0.63 $0.21 $0.40 $1.00 $0.64 $0.63 $0.58 $0.52 $0.58 $0.56 $0.27 $0.22 $0.14 $0.36 $0.15 $0.30 $0.60 $0.61 $0.70 $0.68 $0.80 CORE to GAAP% 100% 36% 67% 189% 81% 91% 85% 81% 77% 86% 38% 37% 27% 63% 22% 51% 88% 94% 94% 94% 95% Share Price $31.97 $34.67 $35.67 $41.22 $47.92 $49.76$47.35 $46.89 $51.02 $55.75$57.74 $42.10 $42.36 $29.60 $31.45 Price Growth 0% 8% 12% 29% 50% 56% 48% 47% 60% 74% 81% 32% 32% -7% -2% Net Revenue $411 $439 $495 $480 $565 $548 $561 $525 $578 $564 $598 $592 $582 $620 $652 NR Growth 0% 7% 20% 17% 37% 33% 37% 28% 41% 37% 45% 44% 42% 51% 59% Diluted Shares 63 69 74 75 75 76 76 77 78 77 78 80 79 76 76 Share Growth 0% 9% 17% 19% 19% 20% 19% 21% 22% 22% 23% 26% 26% 20% 20% |

8 Balance Sheet Growth Balance sheet growth has resumed with ability to further lever the existing

capital base

Ratio

2008

2009

2010

2011

2012

2013

2014

2015

Q1 16

Q2 16

Illustrative

Tier 1 Leverage

32.3%

30.5%

25.6%

21.4%

17.7%

15.4%

16.5%

16.6%

11.6%

11.5%

9.5%

Tier 1 Risk Based Capital

49.4%

40.5%

29.1%

27.4%

26.8%

26.7%

25.0%

26.3%

21.3%

20.9%

19.9%

Risk Weighting Assets Density

64.9%

56.2%

67.3%

62.7%

57.0%

50.7%

58.2%

46.6%

49.0%

49.1%

50.0%

Infrastructure

Build |

9 Bank Drove Significant Balance Sheet & Revenue Growth

Bank growth has been balanced

between loans and investments:

Loans:

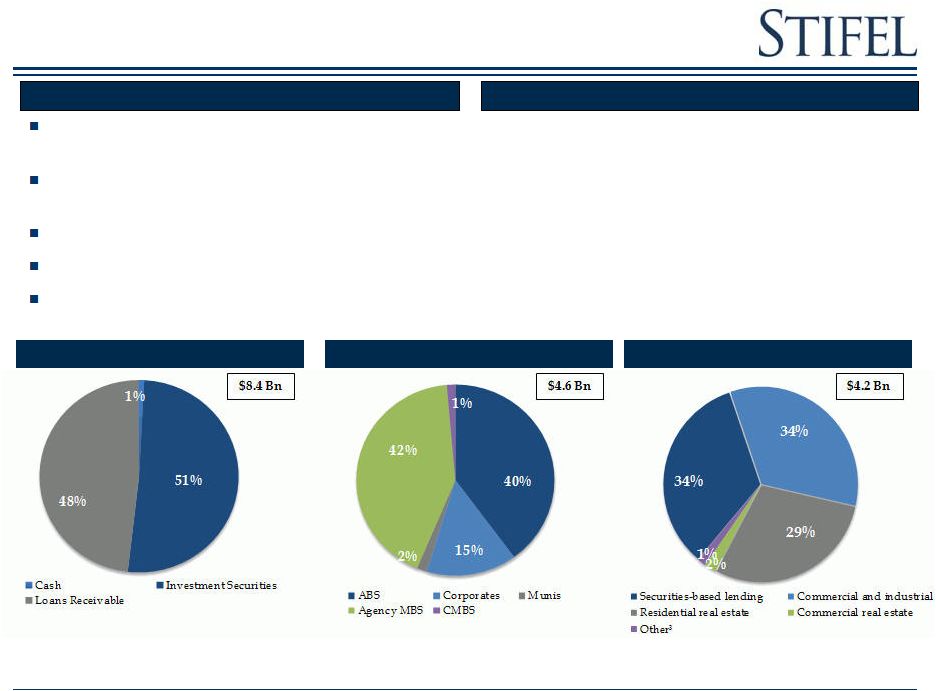

• Comprised of securities based loans, C&I, and residential mortgages • Focused lending to high net worth retail clients • Effective duration of approximately 1 year as of 6/30/16 AFS & HTM Investments: • 67% of the portfolio is fully guaranteed by a US GSE or rated AAA as of 6/30/16 • Portfolio primarily GSE MBS, ABS, and Corporate bonds • Effective duration of approximately 2 years Impact of Bank Growth LTM on Consolidated Results (mil.) 6/30/2015 6/30/2016 Total consolidated assets $10,140 $15,385 Investment securities $1,913 $4,587 Loans $2,604 $4,422 Total deposits $4,314 $7,881 Total equity $2,520 $2,491 Annualized NII $135 $194 Tier 1 Risk Based Capital 29.4% 20.9% Tier 1 Leverage 18.3% 11.5% NIM (Bank) 2.52% 2.36% ROAA (Bank) 1.48% 1.25% ROAE (Bank) 19.1% 18.6% NPAs/Assets 0.14% 0.37% |

10 Potential Impact of Target Asset Levels on Results Targeted Bank Growth Would have Significantly Impacted Second Quarter Results: • Pro forma: • Tier 1 capital levels up 10% • RWA up 15% • Net revenue up 4% • Pre-tax margin up 290 bps • 2Q16 EPS up $0.15 • Annualized 2Q16 EPS up 22% Excess Capital Opportunities to Support Further Growth: • As GAAP deal related expenses run off, organic capital growth is expected to accelerate. • Additional capital flexibility as a result of sale of Sterne Agee legacy businesses and preferred share issuance. • Ability to downstream capital from holding company to bank to support growth. • Changes in money market regulations could generate increased bank sweeps. Footnotes: • Normalized; • Results incorporate average assets at targeted period-end level, reversal of non-recurring

interest expenses

• Preferred & Fully Levered: • Expenses assume an 80% pre-tax margin on incremental bank revenues.

• Tier 1 capital, net income to common equity, and EPS account for impact of $9.4 mil. of

annual preferred dividends

Impact of Bank Growth to Targeted Levels

(mil.)

6/30/2016

Normalized

6/30/2016

Preferred &

Fully Levered

Average Assets

$13,599

$15,000

$18,000

Risk Weighted Assets

$7,483

$7,866

$8,629

Tier 1 Capital

$1,565

$1,573

$1,717

Tier 1 Risk Based Capital

20.9%

20.0%

19.9%

Tier 1 Leverage

11.5%

10.0%

9.5%

Revenue

$652

$660

$680

Bank NIM

2.36%

2.42%

2.42%

Compensation

$410

$410

$411

Non-compensation operating expense

$158

$159

$162

Pre-tax income

$84

$91

$107

Net income

$52

$56

$66

Net income to common equity

$52

$56

$64

EPS

$0.69

$0.74

$0.84

Pre-tax operating margin

12.9%

13.7%

15.8%

Annualized EPS

$2.75

$2.96

$3.36 |

Stifel Overview |

12 Stifel – Premier Investment Bank and Wealth Management Firm Stifel at a Glance GAAP Net Revenue - $2,446 million (Q2’16 LTM) Global Wealth Management (GWM) Net Revenue - $1,470 million (Q2’16 LTM) Private Client Stifel Bank & Trust Margin and Securities-based Lending Asset Management Institutional Group (IG) Net Revenue - $980 million (Q2’16 LTM) Equity & Fixed Income Capital Raising M&A Advisory / Restructuring Institutional Equity and Fixed Income Brokerage Independent Research (1) Assets / equity (as adjusted). (2) As of 6/30/2016. (3) As of 7/29/2016. (4) Insider ownership percentage includes all fully diluted shares, units outstanding and options outstanding, as of

4/11/2016. (5)

Excludes 540 independent advisors from legacy Sterne Agee

business sold to INTL FCStone Low

leverage

(6.2x)

(1)

(2)

,

$2.5

billion

stockholders’

equity

(2)

and

$2.4

billion

market

capitalization

(3)

34%

Insider

ownership

aligns

employees'

interests

with

other

shareholders

(4)

Over 7,000 associates

(3)

Balanced business mix (60% GWM / 40% IG) (2016 YTD net

revenues) National

presence

with

approximately

2,300

financial

advisors

(2)

(5)

Largest

U.S.

equity

research

platform

with

roughly

1,300

stocks

under

coverage

(3)

Broad

investment

banking

and

institutional

sales

and

trading

capabilities

–

domestic

and

international |

13 Leading broker-dealer providing wealth management and

institutional services to consumers and companies

Stifel’s Differentiated Value Proposition: Growth, Scale

and Stability #6

Largest

Retail

Brokerage

Network

(2)

LARGEST

provider of U.S. equity research

2

nd

LARGEST

Equity trading platform in the U.S.

outside

of

the

Bulge

Bracket

firms

(1)

FULL SERVICE

investment banking with

expertise across products and industry sectors

ACCESS TO top ten private client platform (1) Based on 2015 U.S. trading volume per Bloomberg. (2) Source: SIFMA and publicly available information for U.S. brokerage networks. Includes investment banks only.

Stifel

figure reflects sale of legacy Sterne Agee Independent

Contractor business. Bank of

America Merrill Lynch 10

Janney Montgomery Scott

725

Rank

Firm

Brokers

1

16,134

2

Morgan Stanley Wealth Management

16,000

3

Wells Fargo Securities

15,187

4

UBS

6,997

5

Raymond James

6,265

6

Stifel

2,298

7

RBC Capital Markets

2,000

8

Oppenheimer & Co Inc

1,300

9

JPMorgan

800

Bulge Bracket

Boutique

Size / scale

Large distribution

Trading

Retail

Issues

Lack of focus

Banker turnover

Lack of commitment

Research indifference

Lack of growth investors

Firm focus

Good research

Growth investor access

Issues

Financial / firm stability

Trading support

Few with retail

Size / scale

Firm focus

Stability (financial & personnel)

Large distribution

Trading

Outstanding research

Retail

Wealth Management

Institutional |

14 Well-diversified, low risk business model with balanced retail

and institutional exposure

14

Unburdened by capital constraints

Low leverage business model and conservative risk

management Limited balance sheet

risk Stable wealth management business is

augmented by profitable and growing institutional business Drive revenue synergies by leveraging the wealth management and institutional business

Net Revenues

2015

2016 YTD

Non-GAAP Operating Contribution

Balanced business model facilitates growth in all market

environments Note: Net revenues and operating

contribution percentages excludes the Other segment. 2015 2016 YTD |

15 (1) CAGR reflects years 2006 through Q2’16 YTD Annualized.

(2)

Excludes impact of sale of Sterne Agee Independent

Contractor & Correspondent Clearing businesses (3) Book Value Per Share adjusted for April 2011 three-for-two stock split (2006-2010).

CAGR: 16%

CAGR: 21%

Non-GAAP Net Revenues ($MM)

(1)

Non-GAAP Net Income ($MM)

(1)

Total Equity ($MM)

(1)

Total Client Assets

(1) (2)

($BN)

Book Value Per Share

(1) (3)

CAGR: 19%

CAGR: 17%

CAGR: 28%

A Stable Track Record Through Multiple Business

Cycles $35

$59

$53

$94

$114

$122

$138

$166

$187

$220

$226

$0

$50

$100

$150

$200

$250

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016 |

Global Wealth Management |

17 (1) Excludes 540 legacy Sterne Agee Independent Contractors included in sale to INTL FCStone.

(2)

Full year 2016 net revenue and operating contribution

adjust for impact to 2H16 due to sale of legacy Sterne Agee businesses. Global Wealth Management (GWM) Provides Securities Brokerage Services and Stifel Bank Products

Net Revenues

(2)

($MM)

Operating

Contribution

(2)

($MM)

Overview

National Presence

Grown from 600+ financial advisors in 2005 to nearly

2,300

(1)

financial advisors currently

Proven organic growth and acquirer of private client

business

Strategy of recruiting experienced advisors with

established client relationships

Expanding U.S. footprint

|

18 Building Scale and Capabilities into a $1.5B Revenue Segment…

Private Client –

350 financial advisors and support

Revenue production has exceeded expectations

October 2009

Bank holding company

Grown assets from ~ $100M to $7.3B

April 2007

Private Client –

75 financial advisors

Public Finance

December 2008

Private Client –

400 financial advisors

Capital Markets

February 2007

Asset Management

Over $4 billion in assets

November 2013

One-branch community bank; 95% of loan portfolio

sold in 3Q15

October 2013

Customized investment advisory and trust

services November 2014

Private Client

Asset Management

Bank

~100 advisors managing over $20B in AUM

December 2015

~130 advisors managing ~ $10B in AUM

June 2015 |

19 (1) Excludes Legacy Sterne Agee Independent Contractor Business.

Key Operating Metrics

Accounts

(1)

Financial Advisors

(1)

Total Client Assets

(1)

($MM)

Branches

(1)

GWM -

Private Client Group |

20 GWM - Stifel Bank & Trust Investment Portfolio (2) Loan Portfolio (3) (Gross) Acquired FirstService Bank, a St. Louis-based, Missouri-chartered commercial bank, in April 2007

Stifel Financial became a bank holding company and

financial services holding company

Substantial Balance sheet growth with

low-risk assets Funded by Stifel Nicolaus

client deposits Maintain high levels of

liquidity Overview

Key Statistics

(000s) Interest Earnings Assets (1) Note: Data as of 6/30/16. (1) Average interest earning assets for quarter ended 6/30/16.

(2)

Non-agency MBS makes up less than 1% of Investment

Portfolio. (3)

Other includes construction and land, consumer loans, and

home equity lines of credit. (4)

NPAs include: nonaccrual loans, restructured loans, loans

90+ days past due, and other real estate owned.

Total assets

$9,431,000

Total deposits

7,881,000

Total equity

613,000

ROAA

1.3%

ROAE

18.6%

Tier 1 Risk Based Capital

13.7%

Tier 1 Leverage

7.4%

NPAs/Assets

0.4% |

Growing Asset Management Capabilities Total Assets: $26.3 Billion¹ Assets $11.4 Billion $10.3 Billion $2.5 Billion $889* Million $1.2 Billion Offices Chicago St. Louis Milwaukee New York San Francisco Baltimore Cincinnati New York Philadelphia Baltimore New York Florham Park, NJ ¹As of 6/30/2016 *Sagewood assets represent billable assets EquityCompass Strategies is a research and investment advisory unit of Choice Financial Partners, Inc. (“Choice”). Choice and

Ziegler Capital Management, LLC (“ZCM”) are wholly-owned subsidiaries and affiliated SEC Registered Investment Advisers of Stifel Financial Corp. (“Stifel”). Sagewood Asset Management LLC is a

wholly-owned subsidiary of ZCM. 1919ic is an SEC Registered Investment Adviser and indirect subsidiary of Stifel. 1919 IC&T is an OCC-regulated national trust company that is a wholly-owned

subsidiary of Stifel. Washington Crossing Advisors is a Stifel investment advisory program. Assets Under Management represents the aggregate fair value of all discretionary and non-discretionary assets, including

fee-paying and non-fee-paying portfolios. Assets Under Advisement represent advisory-only assets where the firm provides a model portfolio and does not have trading authority over the assets.

|

Institutional Group |

23 (1) Based on 2015 U.S. trading volume per Bloomberg.

(2)

Includes Thomas Weisel

historical investment banking revenues for years 2006

through September 30, 2010. (3)

2012 includes realized and unrealized gains on the

Company’s investment in Knight Capital Group, Inc. of $39.0 million. Institutional Group Net Revenues ($MM) (2)(3) Fixed Income Brokerage + Investment Banking Overview Provides securities brokerage, trading, research, underwriting and corporate advisory services Largest provider of U.S. Equity Research 2nd largest Equity trading platform in the U.S. outside of the Bulge Bracket (1) Full-service Investment Bank Comprehensive Fixed Income platform Equity Brokerage + Investment Banking (2) |

24 Building Scale and Capabilities into a $1.0B Revenue Segment…

Growth Focused

Investment Banking, Research, Sales and

Trading July 2010

Core of our Institutional sales, trading and research

group December 2005

Fixed Income IB, Sales and Trading

Private Client

October 2011

FIG Investment Banking

FIG Sales and Trading / Research

February 2013

Restructuring advisory

December 2012

Fixed

Income

Sales

and

Trading

–

U.S.

&

Europe

Fixed Income Research

July 2013

California-based investment bank and bond

underwriter April 2014

UK-based full service investment bank

July 2014

Expands Public Finance in Southeast

December 2014

Equities

Fixed Income

Investment

Banking

Highly complementary fixed income platforms

June 2015

One of the largest, global fund placement and advisory

firms January 2016

Enhances European debt capital markets

capabilities February 2016

|

25 Institutional Group – Investment Banking Accomplished U.S. Equity Underwriting Franchise – All Equity Transactions Bookrun Equity Deals Since 2010 All Managed Equity Deals Since 2010 Source: Dealogic. Rank eligible SEC registered IPOs and Follow-On offerings since 2010. Includes

demutualizations. As of 2/29/16. Overlapping deals between Stifel and its acquired firms have been removed. Note: $ Volume represents full credit to underwriter for All Managed Equity Deals and apportioned credit to

bookrunner for Bookrun Equity Deals. Bold font indicates middle-market firms. ($ in billions) # of $ Rank Firm Deals Volume 1 Bank of America Merrill Lynch 1,419 $798.3 2 JPMorgan 1,405 $795.8 3 Citi 1,293 $787.6 4 Morgan Stanley 1,264 $760.6 5 Barclays 1,165 $657.4 6 Credit Suisse 1,152 $657.0 7 Wells Fargo Securities 1,122 $584.4 8 Goldman Sachs 1,056 $675.1 9 Deutsche Bank 1,043 $621.6 10 Stifel / KBW 1,031 $325.5 11 RBC Capital Markets 1,017 $483.8 12 UBS 780 $433.1 13 Raymond James & Associates 750 $320.2 14 Piper Jaffray & Co 637 $248.9 15 Jefferies LLC 591 $139.4 16 Robert W Baird & Co 561 $154.9 17 JMP Securities LLC 494 $90.9 18 Oppenheimer & Co Inc 478 $118.5 19 Cowen & Company LLC 474 $92.5 20 William Blair & Co LLC 441 $113.5 21 KeyBanc Capital Markets 440 $187.9 22 BMO Capital Markets 407 $156.0 23 Canaccord Genuity Corp 362 $46.5 24 SunTrust Robinson Humphrey 344 $168.1 25 Ladenburg Thalmann & Co 312 $44.2 ($ in billions) # of $ Rank Firm Deals Volume 1 Bank of America Merrill Lynch 1,303 $150.4 2 JPMorgan 1,264 $165.6 3 Morgan Stanley 1,160 $166.8 4 Citi 1,142 $154.4 5 Barclays 986 $133.5 6 Goldman Sachs 967 $155.5 7 Credit Suisse 962 $123.2 8 Deutsche Bank 840 $94.8 9 Wells Fargo Securities 792 $61.4 10 UBS 567 $55.9 11 RBC Capital Markets 506 $38.7 12 Jefferies LLC 492 $27.0 13 Stifel / KBW 357 $17.1 14 Raymond James & Associates 249 $11.3 15 Piper Jaffray & Co 234 $9.3 16 Cowen & Company LLC 225 $8.0 17 Leerink Partners LLC 168 $7.6 18 Roth Capital Partners 149 $2.6 19 Robert W Baird & Co 144 $5.7 20 BMO Capital Markets 141 $8.7 21 Aegis Capital Corp 103 $1.4 22 KeyBanc Capital Markets 102 $6.0 23 William Blair & Co LLC 96 $3.6 24 Sandler O'Neill & Partners 84 $6.2 25 Canaccord Genuity Corp 76 $3.0 |

26 U.S. Equity Research Coverage (1) Coverage Balanced Across All Market Caps (1) Institutional Group – Research Stifel Research Highlights Largest U.S. Equity Research Platform Largest provider of U.S. Equity Research Largest provider of U.S. Small Cap Research² #1 U.S. provider of Financial Services coverage Only firm ranked in the Top 12 each year for the last ten years in the Wall Street Journal’s “Best on

the Street” Survey

(1)

Source: StarMine rankings as of 7/29/16. Overall coverage

includes only companies with a rating & domiciled in the U.S. Does not include Closed End Funds. Small Cap includes market caps less than $1 billion; Mid Cap includes

market caps less than $5 billion.

(2)

Small Cap includes market caps less than $1

billion. Note: Bold font indicates

middle-market firms. Companies Under

Coverage Rank

Firm

Overall

Mid Cap

Small Cap

1

Stifel/KBW

1,286

455

427

2

JPMorgan

1,127

409

175

3

BofA Merrill Lynch

1,081

411

131

4

Wells Fargo

974

348

190

5

Jefferies

952

329

207

6

Morgan Stanley

926

302

114

7

Raymond James

911

337

260

8

Goldman Sachs

901

296

71

9

Citi

898

297

126

10

Barclays

880

295

99

11

RBC Capital Markets

866

310

115

12

Deutsche Bank

854

273

129

13

Credit Suisse

849

278

148

14

UBS

725

201

80

15

Piper Jaffray

664

235

220

16

Robert W. Baird & Co

642

234

128

17

Cowen

623

180

182

18

Suntrust Robinson Humphrey

606

244

139

19

William Blair & Co

586

226

157

20

Evercore

567

146

56

21

Morningstar

559

119

17

22

Keybanc

549

262

108

23

BMO Capital Markets

526

151

75

24

Macquarie

457

161

83

25

Oppenheimer

451

139

108

Small Cap

34%

Mid Cap

35%

Large Cap

31% |

27 Institutional Equity Sales Equity Trading Institutional Group – Equity Sales and Trading 27 Extensive Distribution Network Powerful Platform Spanning North America and Europe

Relationships with over 3,500 institutional accounts

globally Active daily market maker in over

3,700 stocks Traded over 11.8 billion shares

in 2015 Complete coverage of North America

and Europe for North American listed equities

Major liquidity provider to largest equity money

management complexes Multi-execution

venues: high-touch, algorithms, program trading, and direct market access Dedicated convertible sales, trading, and research desk

34 sales traders located in

Baltimore, New York, Boston, Dallas, San

Francisco, and London

12 position traders covering each major

industry 10 specialized traders focused on:

Option Trading Profitable model with

advantages of scale 84 person sales force,

commission-based Experts in small and mid

cap growth and value Team-based sales

model with 2 - 4 coverage sales people

per account

Team leaders have an average of 15 years

experience Offices in all major institutional

markets in North America &

Europe Accounts range from large mutual funds

to small industry- focused

investors Managed over 732 non-deal

roadshow days in 2015 Extensive experience

with traditional and overnight corporate

finance transactions |

28 Overview Institutional Group – Fixed Income Capital Markets Client Distribution (1)(2) Platform & Products (1) Client Distribution is as of 8/10/2016 (2) Other category includes: Credit Union, Corporation, Hedge Fund, Pension Fund, Trust Company, Foundation,

Endowment, University & Non-Profit.

Comprehensive platform

89 traders with annual client trade volume

approaching $500 billion

58-person Fixed Income Research and Strategy

Group

Widespread distribution

More than 240 Institutional sales professionals

covering over 11,650 accounts

47 institutional fixed income offices

nationwide European offices in London and

Zurich Customer-driven

Focus on long-only money

managers and income funds,

depositories, and hedge

funds

Consistency of execution

Identification of relative

value through asset

class/security selection

High Yield and Distressed Credit

Loan Trading Group

Aircraft Finance & Credit Solutions

Hybrid Securities

Emerging Markets

Structured Products

Investment Grade Credit

Municipal Sales and Trading and

Public Finance

UK Sales and Trading

Strong Fixed Income Brokerage Capabilities

Broker/Dealer

7%

Corporation 1%

Credit Union

1%

Money

Manager 58%

Government

3%

Bank or thrift

17%

Hedge Fund 3%

Insurance

Company 7%

Trust Company

1%

Other 2%

US Government and Agency

Securities

Mortgage-Backed Securities (MBS)

Whole Loans

Government-Guaranteed Loans

Asset-Backed Securities (ABS)

Commercial Mortgage-Backed

Securities (CMBS)

Certificates of Deposit

Cleared Products Group

|

Overview Institutional Group – Public Finance 29 Stifel has ranked in the top ten nationally for senior

managed negotiated underwritings for the past five

years, and Stifel has ranked #1 nationally

for senior managed K-12 negotiated

underwritings for 2015. Stifel’s Public

Finance Group ranked #1 in municipal

negotiated issues in 2015

Total of 26 Public Finance offices

Nearly 150 Public Finance professionals

Public Finance Underwritings

Specialty sectors:

Education

Local Government/Municipal

Healthcare

Public-Private Partnerships/Development

Housing

Source: Thomson Reuters: SDC (True Economics to Book) Ranked

by number of transactions.

Negotiated

#

Par

Amount

#

Par

Amount

#

Par

Amount

Senior Manager/

Private Placement

857

$14,677

1034

$19,749

630

$11,860

Co-Manager

192

$36,506

255

$38,094

174

$34,775

Total

1049

$51,183

1289

$57,843

804

$46,635

Competitive

#

Par

Amount

#

Par

Amount

#

Par

Amount

Senior Manager

92

$604

67

$1,367

65

$3,358

Co-Manager

330

$8,725

405

$21,171

345

$9,259

Total

422

$9,329

472

$22,538

410

$12,617

2016 YTD

2015

2014

2016 YTD

2015

2014 |

Financial Information |

Net Revenue • Total net revenue of $652 mil. in 2Q16 was up 5% sequentially and 9% Y/Y driven by: • Investment Banking revenue increased 32% sequentially but declined 16% Y/Y • Asset Management revenue was flat sequentially & increased 21% Y/Y • Net Interest Income was flat sequentially but up 44% Y/Y • Global Wealth Management represented 59% of net revenue vs. 61% in 1Q16 and 57% in 2Q15 • Institutional net revenue of $261 mil. increased 8% sequentially & 1% Y/Y $- $100 $200 $300 $400 $500 $600 $700 2Q15 3Q15 4Q15 1Q16 2Q16 Net Interest Income Asset Management & Service Fees Investment Banking Brokerage Revenue $598 $592 $581 $620 $652 $343 $357 $347 $380 $386 $259 $232 $246 $241 $261 $- $100 $200 $300 $400 $500 $600 $700 2Q15 3Q15 4Q15 1Q16 2Q16 Global Wealth Management Institutional Core Net Revenue (mil.) Core Segment Net Revenue (mil.) 31 |

Global Wealth Management • Total net revenue in the GWM segment was $386 mil. in 2Q16, up 2% sequentially & 12% Y/Y • Brokerage revenue declined less than 1% sequentially but increased 8% Y/Y • Asset management revenue was flat sequentially & increased 21% Y/Y • Net interest income increased 5% sequentially & 45% Y/Y • 2,838 total FAs* • $237.5 bil. in client AUA* • Compensation ratio was 56.6% down 170 bps sequentially & 50 bps Y/Y • Non-comp. ratio was 16.2% down 90 bps sequentially but up 70 bps Y/Y • Pre-tax margin was 27.2% up 260 bps sequentially but down 20 bps Y/Y. * Total FA and client AUA are as of 6/30/2016. Included in these figures are 540

independent contractor FAs and $11.5 bil. of AUA, that

were part of the legacy Sterne

Agee business sold to INTL FCStone

on July 1, 2016

-$50

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2Q15

3Q15

4Q15

1Q16

2Q16

Brokerage

Asset Management & Service Fees

Net Interest

Investment Banking

Other

GWM Core Net Revenue (mil.)

23.0%

23.5%

24.0%

24.5%

25.0%

25.5%

26.0%

26.5%

27.0%

27.5%

28.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

2Q15

3Q15

4Q15

1Q16

2Q16

Comp. Ratio

Non-comp. Ratio

Pre-tax Margin

Core Expense Ratios & Pre-Tax Margin

32 |

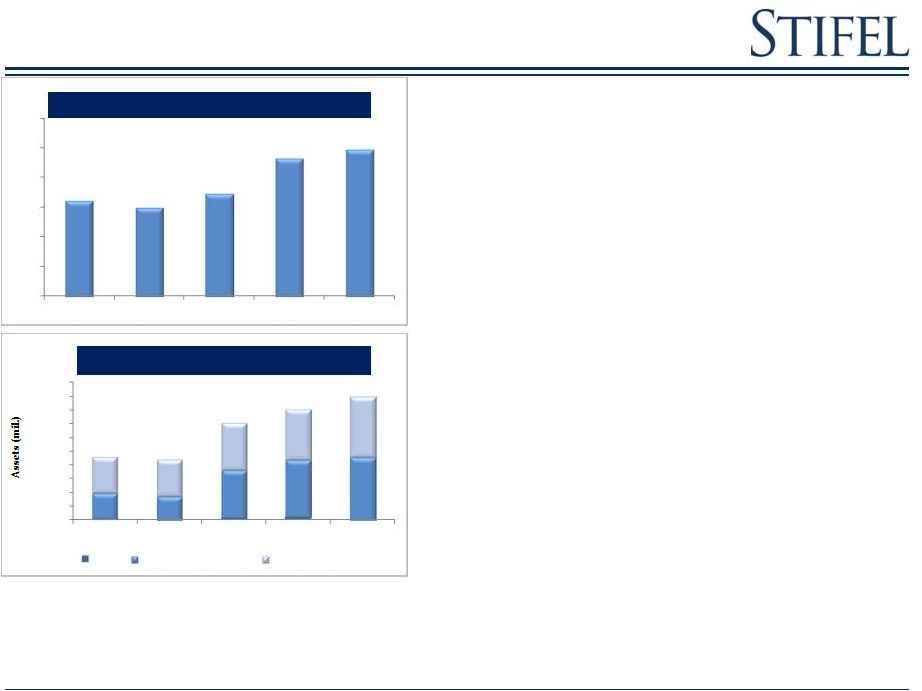

Stifel Bank & Trust • Total net revenue at Stifel Bank & Trust was $56 mil. in 2Q16 was up 5% sequentially & 36% Y/Y • Total bank loans of $4.6 bil. increased 23% sequentially & 75% Y/Y • Total investment securities of $4.6 bil. increased 10% sequentially & 140% Y/Y • NIM of 2.36% was down 12 bps sequentially & 16 bps Y/Y • Allowance for loan losses as a percentage of loans 0.86% of total loans vs. 0.94% in 1Q16 $0.0 $10.0 $20.0 $30.0 $40.0 $50.0 $60.0 2Q15 3Q15 4Q15 1Q16 2Q16 $0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 $9,000 $10,000 2Q15 3Q15 4Q15 1Q16 2Q16 Cash Investment Securities Bank Loans Net Revenue (mil.) Asset Growth 33 |

Institutional Group Core Expense Ratios & Pre-Tax Margin • Total net revenue of $261 mil. in 2Q16 increased 8% sequentially & 1% Y/Y • Investment banking revenue of $124 mil. increased 34% sequentially but declined 15% Y/Y • Advisory revenue of $68 mil. increased 43% sequentially & 7% Y/Y • Brokerage revenue of $136 mil. decreased 7% sequentially but increased 23% Y/Y • Compensation ratio was 58.8% down 360 bps sequentially & 310 bps Y/Y • Non-comp. ratio was 25.0% down 50 bps sequentially but up 310 bps Y/Y • Pre-tax margin was 16.2% up 410 bps sequentially but flat Y/Y. 34 |

Institutional Brokerage & Investment Banking Equity & Fixed Income Brokerage Net Revenue Investment Banking Net Revenue • Brokerage revenue in 2Q16 was $136 mil. • Equity brokerage revenue of $55 mil. was down 12% sequentially & 6% Y/Y • Fixed income brokerage revenue of $81 mil. was down 3% sequentially but increased 57% Y/Y • Advisory revenue of $68 mil. increased 43% sequentially & 7% Y/Y • Underwriting revenue of $56 mil. increased 25% sequentially but declined 32% Y/Y • Equity underwriting of $27 mil. increased 43% sequentially but declined 46% Y/Y • Fixed income underwriting of $29 mil. increased 12% sequentially but declined 12% Y/Y 35 |

GAAP to Non-GAAP Reconciliation GAAP Results (000s) 06/30/16 03/31/16 Total GAAP Compensation & benefits expense 460,023 $ 411,113 $ GAAP comp. ratio 70.5% 66.3% Total GAAP non-compensation expense 176,328 $ 164,948 $ GAAP non-comp. ratio 27.0% 26.6% GAAP pre-tax margin 1.5% 4.4% Three months ended Adjusted Results (000s) 06/30/16 03/31/16 Total Adjusted Compensation & benefits expense 409,887 $ 394,684 $ Adjusted comp. ratio 62.8% 63.6% Total adjusted non-compensation expense 157,974 $ 154,829 $ Adjusted non-comp. ratio 24.2% 25.0% Adjusted pre-tax margin 12.9% 11.4% Three months ended (000s) 06/30/16 03/31/16 GAAP net income 9,772 $ 27,054 $ Duplicative expenses: Compensation & benefits 3,354 5,151 Non-compensation operating expenses 11,378 8,134 Acquistion-related expenses: Compensation & benefits 10,806 11,278 Non-compensation operating expenses 1,297 1,424 Stock-based compensation expense 35,976 - Amortization of intangible assets 5,854 709 Total adjustments: Compensation & benefits 50,136 16,429 Non-compensation operating expenses 18,529 10,267 Total non-GAAP adjustments 68,665 26,696 Provision for income tax 26,145 10,397 Non-GAAP net income 52,292 $ 43,353 $ Total Adjusted Compensation & benefits expense 410,500 $ 394,684 $ Adjusted comp. ratio 62.9% 63.6% Total adjusted non-compensation expense 157,800 $ 154,828 $ Adjusted non-comp. ratio 24.2% 25.0% Adjusted pre-tax margin 12.9% 11.4% Three months ended 36 |

Balance Sheet & Capital Return • Balance Sheet: • Total assets increased to $15.4 bil. in 2Q16, up 7% sequentially & 50% Y/Y • Average interest earning assets increased to $11.4 bil. up 8% sequentially & 63% Y/Y • NIM decreased to 171 bps , down 15 bps sequentially & 23 bps Y/Y. • Tier 1 leverage ratio was 11.5% in 2Q16 down 10 bps sequentially • Tier 1 risk based capital ratio of 20.9% in 2Q16 was down 40 bps sequentially • Book value per share was $37.41 • Share Repurchases • The firm repurchased 125K shares in 2Q16 and has repurchased 475K to date in 3Q16 • 7.6 mil. shares remaining on current authorization. Net Interest Income Drivers 2Q15 3Q15 4Q15 1Q16 2Q16 Total Assets $10,140 $9,359 $13,326 $14,214 $15,386 Total Equity $2,520 $2,493 $2,492 $2,417 $2,491 Debt to Equity 21.2% 21.4% 33.4% 34.1% 32.4% Tier 1 Leverage Ratio 18.3% 16.4% 16.6% 11.6% 11.5% Tier 1 Risk Based Capital Ratio 29.4% 29.4% 26.3% 21.3% 20.9% Capital Structure (in millions, except ratios) 37 |