Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - RESOURCES CONNECTION, INC. | d136612dex231.htm |

| EX-32.2 - EX-32.2 - RESOURCES CONNECTION, INC. | d136612dex322.htm |

| EX-32.1 - EX-32.1 - RESOURCES CONNECTION, INC. | d136612dex321.htm |

| EX-31.2 - EX-31.2 - RESOURCES CONNECTION, INC. | d136612dex312.htm |

| EX-31.1 - EX-31.1 - RESOURCES CONNECTION, INC. | d136612dex311.htm |

| EX-21.1 - EX-21.1 - RESOURCES CONNECTION, INC. | d136612dex211.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended May 28, 2016

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 0-32113

RESOURCES CONNECTION, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 33-0832424 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

17101 Armstrong Avenue, Irvine, California 92614

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (714) 430-6400

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Exchange on Which Registered | |

| Common Stock, par value $0.01 per share | The NASDAQ Stock Market LLC (Nasdaq Global Select Market) |

Securities registered pursuant to Section 12(g) of the Act:

None (Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of November 27, 2015 (the last trading day of the registrant’s most recently completed second fiscal quarter), the approximate aggregate market value of common stock held by non-affiliates of the registrant was $638,144,000 (based upon the closing price for shares of the registrant’s common stock as reported by The Nasdaq Global Select Market). As of August 1, 2016, there were approximately 36,245,851 shares of common stock, $.01 par value, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant’s definitive proxy statement for the 2016 Annual Meeting of Stockholders is incorporated by reference in Part III of this Form 10-K to the extent stated herein.

Table of Contents

RESOURCES CONNECTION, INC.

| Page No. |

||||||

| PART I | ||||||

| ITEM 1. |

3 | |||||

| ITEM 1A. |

20 | |||||

| ITEM 1B. |

27 | |||||

| ITEM 2. |

27 | |||||

| ITEM 3. |

28 | |||||

| ITEM 4. |

28 | |||||

| PART II | ||||||

| ITEM 5. |

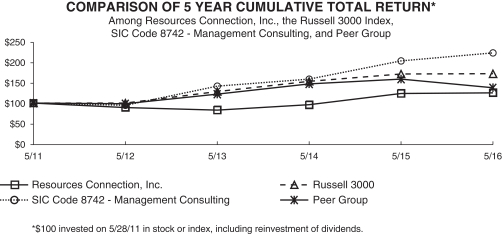

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 29 | ||||

| ITEM 6. |

31 | |||||

| ITEM 7. |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 33 | ||||

| ITEM 7A. |

47 | |||||

| ITEM 8. |

48 | |||||

| ITEM 9. |

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 71 | ||||

| ITEM 9A. |

71 | |||||

| ITEM 9B. |

73 | |||||

| PART III | ||||||

| ITEM 10. |

73 | |||||

| ITEM 11. |

73 | |||||

| ITEM 12. |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 73 | ||||

| ITEM 13. |

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

74 | ||||

| ITEM 14. |

74 | |||||

| PART IV | ||||||

| ITEM 15. |

74 | |||||

| 78 | ||||||

Table of Contents

FORWARD LOOKING STATEMENTS

In this Annual Report on Form 10-K, “Resources,” “Resources Connection,” “Resources Global Professionals,” “RGP,” “Resources Global,” “Company,” “we,” “us” and “our” refer to the business of Resources Connection, Inc. and its subsidiaries. References in this Annual Report on Form 10-K to “fiscal,” “year” or “fiscal year” refer to our fiscal year that consists of the 52- or 53-week period ending on the Saturday in May closest to May 31. The fiscal years ended May 28, 2016 and May 30, 2015 consisted of 52 weeks while the year ended May 31, 2014 consisted of 53 weeks.

This Annual Report on Form 10-K, including information incorporated herein by reference, contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements relate to expectations concerning matters that are not historical facts. Such forward-looking statements may be identified by words such as “anticipates,” “believes,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “should” or “will” or the negative of these terms or other comparable terminology.

Our actual results, levels of activity, performance or achievements and those of our industry may be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. These statements and all phases of our operations are subject to known and unknown risks, uncertainties and other factors, including those made in Item 1A of this Annual Report on Form 10-K, as well as our other reports filed with the Securities and Exchange Commission (“SEC”). Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this Annual Report. We do not intend, and undertake no obligation to update the forward-looking statements in this filing to reflect events or circumstances after the date of this Annual Report or to reflect the occurrence of unanticipated events.

Table of Contents

PART I

| ITEM 1. | BUSINESS. |

Overview

Resources Connection is a multinational consulting firm; its operating entities primarily provide services under the name Resources Global Professionals (“RGP” or the “Company”). The Company provides consulting and business initiative support services to its global client base in the areas of accounting; finance; corporate governance, risk and compliance management; corporate advisory, strategic communications and restructuring; information management; human capital; supply chain management; and legal and regulatory.

We assist our clients by providing “intellectual capital on demand” to support projects requiring specialized expertise in areas such as:

| • | Finance and accounting services including process transformation and improvement; financial reporting and analysis; technical and operational accounting; merger and acquisition due diligence; audit response; implementation of new accounting standards such as the revenue recognition pronouncement; and remediation support |

| • | Information management services including strategy development; program and project management; business and technology integration; data strategy including security and privacy; and business performance management (such as core planning and consolidation systems) |

| • | Corporate advisory, strategic communications and restructuring services |

| • | Corporate governance, risk and compliance management services including contract and regulatory compliance efforts under, for example, the Dodd-Frank Wall Street Reform and Consumer Protection Act and the Sarbanes Oxley Act of 2002 (“Sarbanes”); Enterprise Risk Management; internal controls management; and operation and information technology (“IT”) audits |

| • | Supply chain management services including supply chain strategy development; procurement and supplier management; logistics and materials management; supply chain planning and forecasting; and Unique Device Identification compliance |

| • | Human capital services including change management; organization development and effectiveness; and optimization of human resources technology and operations |

| • | Legal and regulatory services with projects, secondments or tactical needs including commercial transactions; compliance initiatives; law department operations; and business strategy and litigation support |

We were founded in June 1996 by a team at Deloitte LLP (“Deloitte”), led by our chairman, Donald B. Murray, who was then a senior partner with Deloitte. Our founders created the Company to capitalize on the increasing demand for high quality outsourced professional services. We operated as a part of Deloitte until April 1999. In April 1999, we completed a management-led buyout. In December 2000, we completed our initial public offering of common stock and began trading on the NASDAQ Stock Market. We currently trade on the NASDAQ Global Select Market. We operate under the acronym RGP, the branding for our operating entity name of Resources Global Professionals.

Our business model combines the client service orientation and commitment to quality from our legacy as part of a Big Four accounting firm with the entrepreneurial culture of an innovative, dynamic company. We are positioned to take advantage of what we believe are two continuing trends in the outsourced professional services industry: global demand for flexible, outsourced professional services by corporate clients and highly-experienced professionals interested in working in a non-traditional professional services firm. We believe our business model allows us to simultaneously offer challenging yet flexible career opportunities to attract well qualified, experienced professionals and to attract clients with enterprise-wide, global consulting needs.

As of May 28, 2016, we employed or contracted with 2,511 consultants serving a diverse base of over 1,800 clients ranging from large multinational corporations to mid-sized companies to small entrepreneurial entities, in a broad range of industries. Our

3

Table of Contents

consultants have professional experience in a wide range of industries and functional areas and tend to be in the latter third of their careers, many with advanced professional degrees or designations. We offer our consultants careers that combine the flexibility of project-based consulting work with many of the advantages of working for a traditional professional services firm.

Our offices serve our multinational clients throughout the world with a client focus rather than from a regional/office perspective. To enhance our ability to serve multinational clients, we served our clients from 45 offices in the United States and from 23 offices within 19 countries abroad as of May 28, 2016.

Revenue from the Company’s major geographic areas was as follows (in thousands):

| Revenue for the Years Ended | % of Total | |||||||||||||||||||

| May 28, 2016 |

May 30, 2015 |

% Change |

May 28, 2016 |

May 30, 2015 |

||||||||||||||||

| North America |

$ | 499,229 | $ | 492,207 | 1.4 | % | 83.4 | % | 83.3 | % | ||||||||||

| Europe |

57,714 | 59,350 | (2.8 | )% | 9.6 | 10.1 | ||||||||||||||

| Asia Pacific |

41,578 | 39,032 | 6.5 | % | 7.0 | 6.6 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total |

$ | 598,521 | $ | 590,589 | 1.3 | % | 100.0 | % | 100.0 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

See Note 14 — Segment Information and Enterprise Reporting — to the Consolidated Financial Statements for additional information concerning the Company’s domestic and international operations and Part I Item 1A. “Risk Factors — Our ability to serve clients internationally is integral to our strategy and our international activities expose us to additional operational challenges that we might not otherwise face” for information regarding the risks attendant to our international operations.

We believe our distinctive culture is a valuable asset and is, in large part, due to our management team, which has extensive experience in the professional services industry. Most of our senior management and office managing directors have Big Four, management consulting and/or Fortune 500 experience and an equity interest in the Company. This team has created a culture of professionalism and a client service orientation that we believe fosters in our consultants a feeling of personal responsibility for, and pride in, client projects and enables us to deliver high-quality service and results to our clients.

Industry Background

Changing Market for Project- or Initiative-Based Professional Services

RGP’s services cover a range of professional areas. The market for professional services is broad and fragmented and independent data on the size of the market is not readily available. We believe that companies may be more willing to choose alternatives to traditional professional service providers because of evolving economic competitive pressure and significant increases in government-led regulatory requirements, such as the Dodd-Frank Wall Street Reform and Consumer Protection Act. We believe RGP is positioned as a viable alternative to traditional accounting, consulting and law firms in numerous instances because, by using project consultants, companies can:

| • | Strategically access specialized skills and expertise |

| • | Effectively supplement internal resources |

| • | Increase labor flexibility |

| • | Reduce their overall hiring, training and termination costs |

Typically, companies use a variety of alternatives to fill their project needs. Companies outsource entire projects to consulting firms which provides them access to the expertise of the firm but often entails significant cost and less management control of the project. Companies also supplement their internal resources with employees from the Big Four accounting firms or other traditional professional services firms. Companies use temporary employees from traditional and Internet-based staffing firms, although these employees may be less experienced or less qualified than employees from professional services firms. Finally, some companies rely solely on their own employees who may lack the requisite time, experience or skills.

4

Table of Contents

Supply of Project Consultants

Based on discussions with our consultants, we believe that the number of professionals seeking to work on a project basis has historically increased due to a desire for:

| • | More flexible hours and work arrangements, coupled with a professional culture that offers competitive wages and benefits |

| • | Challenging engagements that advance their careers, develop their skills and add to their experience base |

| • | A work environment that provides a diversity of, and more control over, client engagements |

| • | Alternate employment opportunities in regions throughout the world |

The employment alternatives available to professionals may fulfill some, but not all, of an individual’s career objectives. A professional working for a Big Four firm or a consulting firm may receive challenging assignments and training, but may encounter a career path with less choice and less flexible hours, extensive travel and limited control over work engagements. Alternatively, a professional who works as an independent contractor faces the ongoing task of sourcing assignments and significant administrative burdens.

Resources Global Professionals’ Solution

We believe that RGP is positioned to capitalize on the confluence of the industry trends described above. We believe, based on discussions with our clients, that RGP provides high-quality services to clients seeking project professionals because we are able to combine all of the following:

| • | A relationship-oriented and collaborative approach with our clients |

| • | Client service teams with Big Four, consulting and/or industry backgrounds to assess our clients’ project needs and customize solutions to meet those needs |

| • | Highly qualified consultants with the requisite expertise and experience |

| • | Competitive rates on an hourly, rather than project, basis |

| • | Significant client control of their projects |

Resources Global Professionals’ Strategy

Our Business Strategy

We are dedicated to serving our clients with highly qualified and experienced professionals in support of projects and initiatives in the areas of accounting; finance; corporate governance, risk and compliance management; corporate advisory, strategic communications and restructuring; information management; human capital; supply chain management; and legal and regulatory. Our objective is to be the leading provider of these project-based professional services. We have developed the following business strategies to achieve this objective:

| • | Maintain our distinctive culture. Our corporate culture is the foundation of our business strategy and we believe it has been a significant component of our success. Our senior management, virtually all of whom are Big Four or other professional services firm alumni, has created a culture that combines the commitment to quality and the client service focus of a Big Four firm with the entrepreneurial energy of an innovative, high-growth company. We seek consultants and management with talent, integrity, enthusiasm and loyalty (“TIEL”, an acronym used frequently within the Company) to strengthen our team and support our ability to provide clients with high-quality services and solutions. We believe that our culture has been instrumental to our success in hiring and retaining highly qualified employees and, in turn, attracting quality clients. |

| • | Hire and retain highly qualified, experienced consultants. We believe our highly qualified, experienced consultants provide us with a distinct competitive advantage. Therefore, one of our priorities is to continue to attract and retain high-caliber consultants. We believe we have been successful in attracting and retaining qualified professionals by providing challenging work assignments, competitive compensation and benefits, and continuing education and training opportunities, while offering flexible work schedules and more control over choosing client engagements. |

5

Table of Contents

| • | Build consultative relationships with clients. We emphasize a relationship-oriented approach to business rather than a transaction-oriented or assignment-oriented approach. We believe the professional services experience of our management and consultants enables us to understand the needs of our clients and to deliver an integrated, relationship-oriented approach to meeting their professional services requirements. We regularly meet with our existing and prospective clients to understand their business issues and help them define their project needs. Once an initiative is defined, we identify consultants with the appropriate skills and experience to meet the client’s objectives. We believe that by establishing relationships with our clients to solve their professional services needs, we are more likely to generate new opportunities to serve them. The strength and depth of our client relationships is demonstrated by two key statistics: 1) during fiscal 2016, 47 of our 50 largest clients used more than one practice area and 40 of those top 50 clients used three or more practice areas; and 2) 44 of our largest 50 clients in fiscal 2011 remained clients in fiscal 2016 while 39 of our top 50 clients in 2008 were still clients in 2016. In addition, during fiscal 2016 our top 50 clients were served by an average of six RGP offices, demonstrating the breadth of our relationships with clients world-wide. |

| • | Build the RGP brand. Our objective is to build RGP’s reputation as the premier provider of project-based consulting services. Our primary means of building our brand is by consistently providing high-quality, value-added services to our clients. We have also focused on building a significant referral network through our 2,511 consultants and 772 management and administrative employees working from offices in 20 countries as of May 28, 2016. In addition, we have global, regional and local marketing efforts that reinforce the RGP brand. |

Our Growth Strategy

Since inception, our growth has been primarily organic rather than via acquisition. We believe that we have significant opportunity for continued organic growth in our core business as the global economy strengthens and economic uncertainties decrease and that, in addition, we can grow opportunistically through strategic acquisitions. In both our core and acquired businesses, key elements of our growth strategy include:

| • | Expanding work from existing clients. A principal component of our strategy is to secure additional work from the clients we have served. We believe, based on discussions with our clients, that the amount of revenue we currently receive from many of our clients represents a relatively small percentage of the amount they spend on professional services, and that, consistent with historic industry trends, they may continue to increase the amount they spend on these services as the global economy evolves. We believe that by continuing to deliver high-quality services and by further developing our relationships with our clients, we can capture a significantly larger share of our clients’ expenditures for professional services. |

| • | Growing our client base. We will continue to focus on attracting new clients. We strive to develop new client relationships primarily by leveraging the significant contact networks of our management and consultants and through referrals from existing clients. We believe we can continue to attract new clients by building our brand name and reputation, supplemented by our global, regional and local marketing efforts. We anticipate that our growth efforts this year will continue to focus on identifying strategic target accounts that tend to be large multinational companies. |

| • | Expanding geographically. We have expanded geographically to meet the demand for project professional services around the world and currently have offices in 20 countries. We believe, based upon our clients’ requests, that there are future opportunities to promote growth globally. Consequently, we intend to continue to expand our international presence on a strategic and opportunistic basis. We may also add to our existing domestic office network when our existing clients have a need or if there is a new client opportunity. |

| • | Providing additional professional service offerings. We will continue to develop and consider entry into new professional service offerings. Since our founding, we have diversified our professional service offerings from a primary focus on accounting and finance to other areas in which our clients have significant needs such as human capital; information management; governance, risk and compliance; supply chain management; legal and regulatory services; and corporate advisory, strategic communications and restructuring services. Our considerations when evaluating new professional service offerings include cultural fit, growth potential, profitability, cross-marketing opportunities and competition. |

6

Table of Contents

Consultants

We believe that an important component of our success has been our highly qualified and experienced consultants. As of May 28, 2016, we employed or contracted with 2,511 consultants engaged with clients. Our consultants have professional experience in a wide range of industries and functional areas. We provide our consultants with challenging work assignments, competitive compensation and benefits, and continuing education and training opportunities, while offering more choice concerning work schedules and more control over choosing client engagements.

Almost all of our consultants in the United States are employees of RGP. We typically pay each consultant an hourly rate for each consulting hour worked and for certain administrative time and overtime premiums, and offer benefits, including: paid time off and holidays; a discretionary bonus program; group medical and dental programs, each with an approximate 30-50% contribution by the consultant; a basic term life insurance program; a 401(k) retirement plan with a discretionary company match; and professional development and career training. Typically, a consultant must work a threshold number of hours to be eligible for all of these benefits. In addition, we offer our consultants the ability to participate in the Company’s Employee Stock Purchase Plan (“ESPP”), which enables them to purchase shares of the Company’s stock at a discount. We intend to maintain competitive compensation and benefit programs.

Internationally, our consultants are a blend of employees and independent contractors. Independent contractor arrangements are more common abroad than in the United States due to the labor laws, tax regulations and customs of the international markets we serve. A few international practices also utilize a partial “bench model”; that is, certain consultants are paid a weekly salary rather than for each consulting hour worked with bonus eligibility based upon utilization.

Clients

We provide our services and solutions to a diverse client base in a broad range of industries. In fiscal 2016, we served over 1,800 clients from offices located in 20 countries. Our revenues are not concentrated with any particular client or within any particular industry. No single customer accounted for more than 10% of revenue for the years ended May 28, 2016, May 30, 2015 and May 31, 2014, and in fiscal 2016, our 10 largest clients accounted for approximately 15% of our revenues.

The clients listed below represent the multinational and industry diversity of our client base:

| AIG |

Kawasaki Heavy Industries, Ltd. | |

| American Express Company | Makita Corporation | |

| BASF Corporation | MetLife, Inc. | |

| Bayer Corporation | Mitsubishi Corporation | |

| BP p.l.c. | Mitsui & Co, Ltd. | |

| Chevron Corporation | Phillips 66 Company | |

| Community Health Network Inc. | Sony Corporation | |

| ConocoPhillips | Syngenta International AG | |

| Kaiser Permanente | Unilever |

Services and Products

RGP’s business model and operating philosophy are rooted in the support of client-led projects and consulting initiatives, extending to advisory-based services that leverage the deep experience and expertise of our internal team while partnering with our clients’ business leaders. Often, we deliver our services to clients across multiple functional areas of expertise with consultants from several disciplines working on the same project. Our areas of core competency include: finance and accounting; information management; human capital; corporate advisory, strategic communications and restructuring services; legal and regulatory; governance, risk and compliance; and supply chain management.

Finance & Accounting

RGP’s Finance and Accounting services encompass accounting operations, financial reporting, internal controls, financial analyses and business transactions. Clients utilize our services to bring accomplished talent to bear on internally driven change

7

Table of Contents

initiatives, such as M&A activities, or externally mandated change, such as required implementations of new accounting standards, as well as day-to-day operational issues. We provide specialized skills and then transfer knowledge to clients in order to help them leverage their own personnel. RGP specializes in providing customized solutions to our clients’ most pressing business problems, through project management and providing access to full project teams for a specific initiative. Our scalability and global reach also put us in the ideal position to help organizations manage peak workload periods or add specific skill sets to ongoing client projects.

Our Finance and Accounting core competencies include:

Sample Engagement — Revenue Recognition Assessment and Solution: A U.S. based national retailer engaged RGP to perform a full assessment and develop an implementation roadmap in order to comply with the requirements of the Financial Accounting Standards Board’s revenue recognition guidance, Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers, as amended. Using RGP’s proprietary revenue recognition framework to determine the impact of the new guidance and to implement a solution, our consultants:

| • | Evaluated the client’s revenue streams and processes, conducted company-wide interviews and reviewed and documented a sample of revenue contracts |

| • | Estimated the impact on the client’s revenue and disclosures |

| • | Assessed the client’s system capabilities, designed solutions and documented inter-departmental dependencies, including timeline requirements |

| • | Worked with the client to select the optimal implementation solutions and developed a robust implementation roadmap and work plan |

| • | Facilitated on-going and comprehensive knowledge transfer to position the client for future compliance with the revenue recognition standard |

Sample Engagement — Reorganization, Bankruptcy Support and Human Capital: A U.S. clothing manufacturer and retailer was unable to meet its financial obligations in 2015 and filed for chapter 11 protection in U.S. bankruptcy court. The client initially hired RGP for a three-week engagement to analyze and reconcile their critical vendor claims. It was important to complete this reconciliation quickly in order for the continued flow of product from their vendors.

8

Table of Contents

The client’s satisfaction with the initial project led to expansion of the engagement to include an analysis and reconciliation of 503(b)(9) supplier claims just prior to the bankruptcy filing, administration claims and bankruptcy court reporting, including monthly financial reports.

Because of employee layoffs as well as employee attrition due to the chapter 11 filing, the company was unable to perform certain critical functions. RGP provided consultants to serve as interim controller; AP Manager; Budgeting Manager and HR Manager, including the handling of WARN Act notices, layoffs and COBRA matters. With RGP’s support, the Company successfully exited bankruptcy and RGP continues to assist in the on-going reorganization.

Sample Engagement — Transition of Accounting Cycle Processes Following Significant Acquisition: A Fortune 500 retail company that recently completed a significant acquisition of a competitor embarked on a comprehensive program to recognize synergies from the overlap of certain back-office functions. Under a “lift & shift” scenario, the client engaged RGP to assess the current state of revenue, cash and payables processes for the acquired company and to develop and execute a plan to transition those functions to the client’s existing shared services centers around the world.

Information Management

RGP’s Information Management practice provides planning and execution services in four primary areas: Program & Project Management; Business & Technology Integration; Data Strategy & Management; and IT Strategy & Advisory. By focusing on the initiative as defined by our clients, RGP can provide continuity of service from the creation or expansion of an overall IT strategy through post-implementation support. In addition to these services, we assist clients in implementation of a variety of technology solutions: Enterprise Resource Planning (“ERP”) systems; strategic “front-of-the-house systems”; human resources (“HR”) information systems; supply chain management systems; core finance and accounting systems; audit compliance systems; and financial reporting, planning and consolidation systems.

The following are examples of the core competencies of our Information Management practice:

Sample Engagement — Project Leadership for Global Next Generation Program: A Fortune 50 automotive company is implementing a global program to create the next generation of connected vehicle technology and infotainment applications for all North American vehicle production. The RGP team leads the coordination and integration of a highly complex set of services that requires the seamless integration of six external suppliers and eight internal teams, to create a new customer facing registration portal, secure global network and real-time interfaces needed to enable the new services.

RGP consultants serve as technical Program Management across 13 defined workstreams as well as a variety of internal systems integrations that span enterprise infrastructure. The project also includes systems implementation in the form of architecture support and very complex systems integration across the 14 teams building the technology components. The RGP

9

Table of Contents

Program Manager has managed the transition from vendor selection to solutioning and engineering the services with the supplier and client teams. RGP continues to be the technical systems integrator for all program workstreams and horizontal platforms.

Sample Engagement — Deployment of Third-Party Technology in Call Center: A major provider of entertainment programming needed assistance in deploying third-party technology. The technology allows system intelligent prioritization of customer telephone calls by providing real-time evaluation of customer call intention, comparing the intent with various attributes on file for the particular customer, and aligning customer calls with offers for cross-selling purposes.

The RGP consulting team provided project management, executive stakeholder strategy, organizational change management, enterprise technology implementation and vendor management. In addition to reducing the time associated with each customer call and increasing revenue through targeted cross-sell techniques, our team led the implementation of a number of analytical tools for the business to use in evaluating retention and cross-sell strategies.

Sample Engagement — Integration and Optimization of Significant Acquisition: A large publicly-traded entertainment conglomerate acquired a regional entity that provided home security and monitoring. Our client needed to integrate its existing ordering, billing, supply chain and installation systems with the acquired entity’s systems in order to sell and deliver these new capabilities across its current and prospective customer base. Working with the client’s implementation team, RGP’s activities included:

| • | Serving as interim program manager and senior project manager |

| • | Linking and modifying the client’s existing sales programming to bundle the acquired home security/monitoring products |

| • | Modifying the existing equipment delivery systems capability to reduce the number of days to final install |

Sample Engagement — BI Strategy/Implementation: A large state utility company required assistance in restarting and reenergizing a stalled enterprise-wide BI initiative focused on increasing overall data definition/management, analysis and reporting to support enterprise-wide business decision making. The RGP engagement consisted of:

| • | Partnering with the client’s corporate stakeholder team to define the current state of the stalled BI initiative and redevelop overall objectives/goals |

| • | Providing the framework/approach of how to restart and move forward towards a successful implementation and adoption |

| • | Leading the effort to gain stakeholder, management and end user buy-in for the initiative across the organization |

| • | Providing day to day Program Management oversight, focusing on partnering, advising and managing the redefined approach. Critical deliverables included requirements/process definition, data definition/management, report/dashboard definition and development, change management and training/adoption |

Sample Engagement — Data Analytics PMO: RGP consultants assisted our client with the launch of a Data Analytics Program to better capitalize upon its leading data/analytics processes. The use of data to drive operating decisions has long been a fundamental element behind our client’s competitive positioning and an ongoing source of competitive advantage. Their data infrastructure was scaled up in 2014 to accommodate the increasing demand for new data in their enterprise data platform. The Data Analytics Program has enabled better decision making on pricing, customer segmentation, marketing and yield management. The RGP engagement consisted of:

| • | Supporting program and project management for the Data Analytics Program |

| • | Developing the program structure, defining work streams and assigning appropriate team members |

| • | Identifying and tracking of key activities and milestones |

| • | Developing and managing the program budget |

| • | Communicating to key stakeholders |

| • | Evaluating and selecting tools/technology |

10

Table of Contents

Sitrick Brincko Group

Sitrick Brincko Group (“Sitrick”) offers a unique combination of strategic counsel, tactical execution, and organizational and logistical support critical to both public and private companies and high profile individuals, both in the United States and overseas. Its extensive experience in strategic, corporate, financial and transactional communications as well as general management, finance, strategic planning, manufacturing and distribution have made Sitrick a partner to boards of directors and management engaged in acquisitions, proxy fights, litigation, management changes, government inquisitions, corporate reorganizations or when repositioning, redirecting or unwinding a business.

Combined with RGP’s broad capabilities and global footprint, Sitrick offers a wide variety of services to clients, including:

| • | Strategic and crisis communications |

| • | Repositioning a business or business segment |

| • | Change management |

| • | Litigation support |

| • | Restructuring and reorganization |

| • | Performance improvement |

| • | Loan portfolio review and loan workout |

| • | Bankruptcy administration and management |

| • | Corporate and financial advisory |

| • | Interim and crisis management |

| • | Fiduciary services, trustee, receiver, examiner |

| • | Creditor representation and recovery |

| • | Dispute resolution and litigation support |

Sample Engagement — Financial Restructuring: Sitrick, working with the board of directors, management and other advisors, developed and implemented the strategic communications for the successful restructuring and change in management of a large beverage distributor. This was a cross-border engagement, with the company based in Poland, new investors and management based in Russia and the restructuring in the United States.

Sample Engagement — Litigation Support: Sitrick was retained by a technology company to provide litigation support for a patent infringement suit the company was about to file against a much larger and better known competitor. Sitrick developed a communications strategy that resulted in the case being settled within two days of its filing.

Sample Engagement — Proxy Contest: Sitrick provided strategic communications counsel in a proxy contest launched against an Israeli company where a hedge fund was trying to take control of the board of directors. The company successfully maintained control of the board of directors.

11

Table of Contents

Human Capital

RGP’s Human Capital consultants apply project-management and business analysis skills to help solve the people aspects of business problems. The two primary areas of focus of our human capital practice are change management/business transformation and HR operations. To achieve the desired business outcome, our Human Capital professionals work with client teams to help drive their change management initiatives to successful completion. We help our clients with the people challenges of acquisitions, mergers, downsizing, reorganizations, system implementations or legislative requirements (Sarbanes, Basel II, HIPAA, the Patient Protection and Affordable Care Act, etc.). Our Human Capital professionals also have HR operations and technology skills that provide clients with the means to achieve their initiatives. Our Human Capital core competencies revolve around:

Sample Engagement — Establishment of New Corporate Compensation Function: A fast-growing multi-national pharmaceutical company needed assistance in establishing a new corporate compensation function, addressing core infrastructure issues. Our consultant, working with client personnel, served as Project Manager and subject matter expert, assessing business priorities, development of compensation philosophy and integration of processes with technology. Specific initiatives included:

| • | Establishing a benchmarking strategy for assessing competitive pay levels, coupled with integrating a pay for performance culture |

| • | Evaluating the current HRIS system and identifying relevant issues for replacement |

| • | Positioning the HR function as a valued and integral business partner |

Sample Engagement — Organizational Design: A Fortune 500 life insurance company wanted to design a new organizational and operating model to provide more efficient, “silo-free” operations. Partnering with RGP, our consultants provided subject-matter expertise on organizational design and an operating model development approach, process and content. Specifically, RGP supported the initiative by:

| • | Conducting in-depth current state organizational reviews |

| • | Developing a comprehensive culture and change impact assessment to identify benefits and challenges of the new operating model |

12

Table of Contents

| • | Evaluating the impact on human capital of a shared services center and off-shoring implementation |

| • | Presenting key aspects of the operating model design approach to management and staff and assessing potential interdependencies with other workstreams outside of the HR function |

Sample Engagement — Implementation of HR system: A Fortune 500 provider of electronic products and services selected Workday as their world-wide HR system in order to improve HR workload and processes. The new system would replace the existing, manually intensive and inefficient spreadsheet based process, allowing HR management to focus on analysis rather than data development and reconciliation. RGP led the initiative in the region by developing and implementing a deployment plan and assessing the impact and success of the software usage upon completion.

Legal & Regulatory

RGP Legal helps clients execute their legal, risk management and regulatory initiatives. Our consultants (consisting of attorneys, compliance professionals, paralegals and contract managers) have significant experience working at the nation’s top law firms and companies. RGP Legal provides general counsel access to exceptional talent on an agile basis for the exact subject-matter knowledge and business perspective required for a particular task or workflow. Generally, RGP Legal is engaged to work directly with in-house counsel or with traditional outside counsel for projects or pieces of “unbundled” work. Examples of our core competencies include:

Project Services

| • | Commercial agreement review |

| • | Compliance support (FCPA, Dodd-Frank, data privacy) |

| • | Proxy and quarterly SEC support |

| • | Corporate governance |

Sample Engagement — Unbundling Support for M&A Activity: Our client, a world leader in the in-flight entertainment and communication solutions business, turned to RGP for supplemental support and expertise in connection with a buy-side acquisition. The client’s general counsel engaged us to supplement the bandwidth of the in-house team. Our consultants drove the diligence process, collaborated extensively with internal business units and, working closely with lead outside counsel who focused on the strategy and structure of the deal, assisted in the drafting of deal documents. The client reduced its legal spend by multi-sourcing the work needed to support the transaction.

Legal Operations and Business Strategy

| • | Legal project management, process improvement, change management |

| • | Legal spend analysis |

| • | Strategic sourcing and convergence |

| • | Contract, knowledge, matter management |

| • | Technology assessment, selection, implementation and optimization |

| • | Organizational design |

Sample Engagement — Law Department Organizational Design: The new General Counsel for a multi-billion dollar energy and specialty refining company asked RGP to redesign its legal department structure from the ground up. A series of acquisitions, coupled with a more complex business environment, increased the department’s work flows. Our consultants conducted extensive stakeholder interviews and an analysis of department operations to develop an organizational model stressing business continuity, best practices in organizational design, areas of process and resourcing improvement, and organizational development. RGP’s solution resulted in a leaner legal team that leverages effective and efficient legal services providers, while implementing in-house efficiencies and automation.

13

Table of Contents

Sample Engagement — Development and Implementation of Knowledge Management Tool: Our client, a multi-million dollar asset management firm, lacked an efficient tool for handling information related to its investment/private equity funds. As a result, in-house attorneys often started deals without the benefit of knowledge gleaned from previously negotiated agreements. Documents were difficult to locate, important deal information was lost, and providing information to regulators and third parties was often time consuming and inefficient.

RGP designed a knowledge management tool to increase efficiencies in the client’s deal flow and archiving process. RGP crafted a simple searchable database tool that provided an effective way to access, retrieve, archive and leverage important deal information. RGP also conducted a gap analysis on missing deal documents and developed training to ensure attorney buy-in and acceptance of the management tool.

Unbundling Legal Services

| • | Litigation management and support, including document review and analysis, investigations and regulatory reviews |

| • | M&A due diligence, closing, integration |

| • | Real estate due diligence |

Sample Engagement — Unbundling Fact Finding Activities in Class Action Litigation: Challenged with the process of managing a massive wage and hour class action lawsuit, our client, a multinational publicly-traded food service chain, engaged RGP to provide a seasoned team of attorneys to conduct employee interviews critical to revealing issues important in responding to the class certification process.

After conducting the interviews, our consultants teamed with the client and outside counsel to determine the merit and relevancy of each declaration. The project was completed rapidly over a multi-week period and the client reported cost savings versus traditional solutions.

Supply Chain Management

RGP’s Supply Chain Management practice assists clients in the planning, execution, maintenance and troubleshooting of complex supply chain systems and processes. Our consultants work as part of client teams to reduce the total cost of ownership, improve business performance and produce results. Specifically, our core competencies include:

14

Table of Contents

Sample Engagement — Vendor Risk Management Software Selection and Monitoring: A major publicly-traded financial services company wanted to effectively and proactively identify and manage previously unaddressed significant vendor risks. Working collaboratively, a cross-functional team of client personnel and RGP consultants developed a comprehensive vendor performance monitoring function. The team identified three key project work streams: 1) establishment of solutions to support and maintain the client’s third party vendor management processes, systems, standards and metrics tracking; 2) development of user guides and materials and training on the selected software tool to support the function; 3) development and support of the day to day processes to ensure compliance with regulations, guidelines and firm requirements. Specifically, RGP was responsible for:

| • | Developing the framework and vendor scorecards |

| • | Conducting certification and governance maturity assessments |

| • | Conducting on-site vendor assessments, certification and governance |

| • | Developing program processes, policies and procedures |

| • | Assisting with management of the selected software implementation |

Sample Engagement — Improvement in On-Line Checkout: A U.S. based product distributor initiated a major campaign to drive consumers to using an e-commerce platform. However, during checkout, customers realized that shipping and handling fees associated with the purchase were too high, resulting in an 80% cart abandonment rate and a significant loss in sales. In the current e-commerce environment, consumers have been trained to expect free shipping, free shipping over a specific order value or flat rate shipping.

The client engaged RGP to identify short term solutions to reduce shipping and handling charges prior to the next selling season, as well as longer term ideas for future releases. After conducting a four week assessment of the recent sales cycle and associated data, RGP consultants provided specific recommendations to reduce shipping and handling costs, reduce the order cycle and transit time and reduce packaging waste. In addition, observations were made to improve the consumer experience, with the goal of increasing sales.

Sample Engagement — Procure-to-Pay Assessment: A large multinational consumer electronic company needed assistance in conducting an assessment of its Procure-to-Pay process to review performance and to identify recommendations to fill gaps. The client had two primary goals: 1) to assess the current state; and 2) to provide insights on the future state, with comparison to leading practices and a high-level implementation roadmap. RGP, acting in project management and business analyst roles, was tasked with:

| • | Documenting the current process, controls and policies and procedures |

| • | Outlining benefits of using the new Oracle system |

| • | Providing analysis of current staff skills and appropriate staff size |

| • | Providing recommendations on procure to pay strategy, priorities, organizational structure, risks and dependencies |

| • | Assessing supplier selection, certification and performance monitoring |

| • | Developing recommendations for future state, including ways to maximize effectiveness and efficiency, optimizing cost structures and mitigating risk exposures |

Sample Engagement — Cost Recovery Review: One of the world’s largest multinational energy companies engaged RGP to provide services to ensure contract compliance and to identify cost recovery opportunities with a supplier of significant services. Performing services at the supplier location, the RGP consultants developed the procedure plan, conducted supplier interviews, performed test work on selected transactions and issued a final report. The findings ultimately resulted in a recovery for the client and an enhanced understanding with the supplier.

15

Table of Contents

Governance, Risk and Compliance (“GRC”): Corporate Governance, Risk Management, Internal Audit and Compliance Services

RGP’s GRC practice assists clients with a variety of governance, risk management, internal audit and compliance initiatives. The professionals in our GRC practice have experience in operations, controllership and internal and external audit and serve our clients in any number of roles required — from program manager to team member. In addition to helping clients worldwide in the areas of audit, risk and compliance, we are able to draw on RGP’s other practice areas to bring the required business expertise to the engagement. Our GRC core competencies include:

Sample Engagement — Documentation and Enhancement of Internal Controls in Preparation for IPO or Sale: A highly profitable and fast growing maker of electronic equipment had both inadequate IT general controls and poor documentation of its processes. As a result, highly detailed and expensive substantive audit procedures needed to be performed in order to prepare financial statements for a contemplated IPO or sale of the company. Serving as project manager and change management lead, RGP consultants performed an assessment of IT general controls, identified critical risk areas and prepared detailed action plans to remediate or implement controls.

Sample Engagement — Implementation of the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”) Framework: A Fortune 500 software developer engaged us to serve as the lead in applying the COSO framework of controls in a highly complex business environment. Specifically, our consultants identified and aligned control activities with the respective COSO principles and provided a gap analysis to target points for remediation. In addition, the RGP team developed a user friendly reporting model to facilitate both coordination with the external audit team as well as critical communication points with senior executives and the Audit Committee of the Board of Directors.

Sample Engagement — Documentation and Enhancement of Internal Controls: A rapidly growing maker of automation software needed an assessment of current state business processes and internal controls at its U.S. and India operations for Sarbanes and general business purposes. Our consultants documented current state of internal controls, made recommendations for enhanced future state of controls and presented our findings to executive management. The assessments identified a significant number of high risk items that the client was unaware of, with actionable recommendations for improvement.

Sample Engagement — Internal Audit Co-Sourcing and Internal Control Framework: A global insurance provider engaged RGP to provide co-sourced internal audit functions as well as to implement its Internal Control Framework (“ICF”). After identifying high risk projects and processes in the IT function, we assisted with the following deliverables:

| • | Planning and designing the audit approach to be used across the enterprise for engagements |

| • | Performing testing and evaluation of results in order to prepare draft audit reports |

| • | Producing final audit reports in the required format utilizing the client’s auditor assistant database system |

16

Table of Contents

For the ICF project, RGP consultants were deployed in the U.S. and internationally to document and review accounting and IT processes and controls and to provide recommendations for improvement.

Sample Engagement — Banking Compliance Support: Our client, a Fortune 500 financial services company, wanted to develop and implement a more formal approach to the assessment of the company’s regulatory risk profile. Previously, decisions on assessment of regulatory risk were more of an intuitive exercise than a formalized methodology. To help the client evolve its process, RGP was responsible for the entire project, including:

| • | Identifying risk topics for each product type (real estate loans, consumer loans, credit cards, deposits, trusts and others) |

| • | Determining gaps in regulation coverage |

| • | Creating risk statements for each product |

| • | Defining the inherent and control risk definitions |

| • | Building and scoring the templates to be used to document the efforts |

The final deliverable allowed bank management to better allocate limited resources to maximize coverage of critical compliance issues using the quantifiable basis of risk assessment. Ultimately, RGP consultants deployed the methodology through other facets of the company’s operation, including property/casualty and life insurance and investment management.

Sample Engagement — Audit IT Security Controls: The CIO of a global healthcare company headquartered in Europe planned a series of global IT audits. Working as a part of a client team, RGP was responsible for an assessment of the strength and sophistication of the IT security organization, implementation of the IT security governance model, conducting a series of interviews with top management stakeholders in the IT organization, and transfer of knowledge on audit techniques.

policyIQ

RGP’s policyIQ is our proprietary cloud-based GRC software application, enabling the focused management of a wide range of GRC processes, including Risk Assessments, Sarbanes Compliance, Policy and Procedure Management, Internal Audit Programs, Anti-Corruption Compliance and Contract Administration. policyIQ can be implemented quickly to manage a specific aspect of an overall GRC program, or easily scaled to integrate multiple initiatives, allowing the organization to realize greater efficiency. In addition, our engagement teams often utilize policyIQ as a tool to assist in the efficient collection, storing and review of project workpapers, deliverables and other critical project content. Business problems that our clients have used policyIQ to resolve include:

| • | Sarbanes Compliance Management: Clients use policyIQ to manage their entire Sarbanes compliance program, from risk assessment through remediation tracking. Electronic forms automate quarterly certifications, and reporting allows all stakeholders insight into the status of Sarbanes compliance at any time. |

| • | Policy and Procedure Management: With policyIQ as the central location for all organizational policies and procedures, all employees have access to the most current documentation — and using electronic forms, can easily document annual proof of compliance. |

| • | Internal Audit Programs: Companies use policyIQ to capture workpapers electronically, gathering all evidence in a central location and assigning testing to the appropriate auditors. With robust reporting, audit managers have oversight into the process and with built-in workflow, audits can flow through appropriate channels of approval. |

| • | Contract Management: policyIQ provides a central, secure location to house all contract documentation, allowing companies to index contracts for ease of searching and align view, edit and approve security appropriately. By utilizing custom fields to capture standard meta data, contracts can be categorized and communications established to alert all stakeholders of upcoming renewals or milestones. |

17

Table of Contents

Sample Engagement — Fresh Approach to Sarbanes Compliance: For a publicly traded manufacturing company with global operations, RGP was engaged to bring efficiency and consistency to its Sarbanes compliance and internal audit programs. Using policyIQ, our consulting team was able to:

| • | Implement the 2013 COSO Framework, with mapping to entity level controls, in order to meet expectations by external auditors and the Public Company Accounting Oversight Board |

| • | Integrate workflow processes on all control reviews and audit testing to improve quality assurance over documentation and oversight on audit testing |

| • | Establish consistent processes for Sarbanes documentation and testing across multiple business units |

Operations

We generally provide our professional services to clients at a local level, with the oversight of our regional managing directors and consultation of our corporate management team. The managing director, client service director(s) and recruiting director(s) in each office are responsible for initiating client relationships, identifying consultants specifically skilled to perform client projects, ensuring client and consultant satisfaction throughout engagements and maintaining client relationships post-engagement. Throughout this process, the corporate management team and regional managing directors are available to consult with the managing director with respect to client services.

Our offices operate in an entrepreneurial manner. The managing directors of our offices are given significant autonomy in the daily operations of their respective offices, and are responsible for overall guidance and supervision, budgeting and forecasting, sales and marketing, pricing and hiring within their office. We believe that a substantial portion of the buying decisions made by our clients are made on a local or regional basis and that our offices most often compete with other professional services providers on a local or regional basis. Because our managing directors are in the best position to understand the local and regional outsourced professional services market and because clients often prefer local relationships, we believe that a decentralized operating environment maximizes operating performance and contributes to employee and client satisfaction.

We believe that our ability to deliver professional services successfully to clients is dependent on our managing directors working together as a collegial and collaborative team, at times working jointly on client projects. To build a sense of team effort and increase camaraderie among our managing directors, we have an incentive program for our office management that awards annual bonuses based on both the performance of the Company and the performance of the individual. We also share across the Company the best and most effective practices of our highest achieving offices and use this as an introductory tool with new managing directors. New managing directors also spend time with another practice, partnering with experienced managing directors and other senior management personnel. This allows the veteran managing directors to share their success stories, foster the culture of the Company with new managing directors and review specific client and consultant development programs. We believe these team-based practices enable us to better serve clients who prefer a centrally organized service approach.

From our corporate headquarters in Irvine, California, we provide centralized administrative, marketing, finance, HR, IT, legal and real estate support. Our financial reporting is also centralized in our corporate service center. This center handles invoicing, accounts payable and collections, and administers HR services including employee compensation and benefits administration for North American offices. We also have a business support operations center in our Utrecht, Netherlands office to provide centralized finance, HR, IT, payroll and legal support to our European offices. In addition, in North America, we have a corporate networked IT platform with centralized financial reporting capabilities and a front office client management system. These centralized functions minimize the administrative burdens on our office management and allow them to spend more time focused on client and consultant development.

Business Development

Our business development initiatives are composed of:

| • | local initiatives focused on existing clients and target companies |

| • | national and international targeting efforts focused on multinational companies |

18

Table of Contents

| • | brand marketing activities |

| • | national and local advertising and direct mail programs |

Our business development efforts are driven by the networking and sales efforts of our management. In addition, the local office managing directors are assisted by management professionals focused on business development efforts on a national basis based on firm-wide and industry-focused initiatives. These business development professionals, teamed with the managing director and client service teams, are responsible for initiating and fostering relationships with the senior management and decision makers of our targeted client companies. These local efforts are supplemented with national marketing assistance. We believe that these efforts have been effective in generating incremental revenues from existing clients and developing new client relationships.

Our brand marketing initiatives help develop RGP’s image in the markets we serve. Our brand is reinforced by our professionally designed website, television, print, radio and online advertising, direct marketing, seminars, initiative-oriented brochures, social media and public relations efforts. We believe that our branding initiatives, coupled with our high-quality client service, help to differentiate us from our competitors and to establish RGP as a credible and reputable global professional services firm.

Competition

We operate in a competitive, fragmented market and compete for clients and consultants with a variety of organizations that offer similar services. Our principal competitors include:

| • | consulting firms |

| • | local, regional, national and international accounting and law firms |

| • | independent contractors |

| • | traditional and Internet-based staffing firms |

| • | the in-house or former in-house resources of our clients |

We compete for clients on the basis of the quality of professionals, the timely availability of professionals with requisite skills, the scope and price of services, and the geographic reach of services. We believe that our attractive value proposition, consisting of our highly qualified consultants, relationship-oriented approach and professional culture, enables us to differentiate ourselves from our competitors. Although we believe we compete favorably with our competitors, many of our competitors have significantly greater financial resources, generate greater revenues and have greater name recognition than we do.

Employees

As of May 28, 2016, we had a total of 3,283 employees, including 772 corporate and local office employees and 2,511 consultants. Our employees are not covered by any collective bargaining agreements.

Available Information

The Company’s principal executive offices are located at 17101 Armstrong Avenue, Irvine, California 92614. The Company’s telephone number is (714) 430-6400 and its website address is http://www.rgp.com. The information set forth in the website does not constitute part of this Annual Report on Form 10-K. We file our annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 with the SEC electronically. These reports are maintained on the SEC’s website at http://www.sec.gov.

A free copy of our annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K and amendments to those reports may be obtained on our website at http://www.rgp.com as soon as reasonably practicable after we file such reports with the SEC.

19

Table of Contents

| ITEM 1A. | RISK FACTORS. |

You should carefully consider the risks described below before making a decision to buy shares of our common stock. The order of the risks is not an indication of their relative weight or importance. The risks and uncertainties described below are not the only ones facing us but do represent those risks and uncertainties that we believe are material to us. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also adversely impact and impair our business. If any of the following risks actually occur, our business could be harmed. In that case, the trading price of our common stock could decline, and you might lose all or part of your investment. When determining whether to buy our common stock, you should also refer to the other information in this Annual Report on Form 10-K, including our financial statements and the related notes.

A future economic downturn or change in the use of outsourced professional services consultants could adversely affect our business.

While we believe general economic conditions continue to improve in most parts of the world, there continues to be some uncertainty regarding general economic conditions within some regions and countries in which we operate, leading to reluctance on the part of some multinational companies to spend on discretionary projects. Deterioration of or increased uncertainty related to the global economy or tightening credit markets could result in a reduction in the demand for our services and adversely affect our business in the future. In addition, the use of professional services consultants on a project-by-project basis could decline for non-economic reasons. In the event of a reduction in the demand for our consultants, our financial results would suffer.

Economic deterioration at one or more of our clients may also affect our allowance for doubtful accounts. Our estimate of losses resulting from our clients’ failure to make required payments for services rendered has historically been within our expectations and the provisions established. However, we cannot guarantee that we will continue to experience the same credit loss rates that we have in the past. A significant change in the liquidity or financial position of our clients could cause unfavorable trends in receivable collections and cash flows and additional allowances may be required. These additional allowances could materially affect the Company’s future financial results.

In addition, we are required to periodically, but at least annually, assess the recoverability of certain assets, including deferred tax assets and goodwill. Softening of the United States economy and international economies could adversely affect our evaluation of the recoverability of deferred tax assets, requiring us to record additional tax valuation allowances. Our assessment of impairment of goodwill is currently based upon comparing our market capitalization to our net book value. Therefore, a significant downturn in the future market value of our stock could potentially result in impairment reductions of goodwill and such an adjustment could materially affect the Company’s future financial results and financial condition.

The market for professional services is highly competitive, and if we are unable to compete effectively against our competitors, our business and operating results could be adversely affected.

We operate in a competitive, fragmented market, and we compete for clients and consultants with a variety of organizations that offer similar services. The competition is likely to increase in the future due to the expected growth of the market and the relatively few barriers to entry. Our principal competitors include:

| • | consulting firms; |

| • | local, regional, national and international accounting and other traditional professional services firms; |

| • | independent contractors; |

| • | traditional and Internet-based staffing firms; and |

| • | the in-house or former in-house resources of our clients. |

We cannot assure you that we will be able to compete effectively against existing or future competitors. Many of our competitors have significantly greater financial resources, greater revenues and greater name recognition, which may afford them an advantage in attracting and retaining clients and consultants and in offering pricing concessions. Some of our competitors in certain markets do not provide medical and other benefits to their consultants, thereby allowing them to potentially charge lower rates to clients. In addition, our competitors may be able to respond more quickly to changes in companies’ needs and developments in the professional services industry.

20

Table of Contents

Our business depends upon our ability to secure new projects from clients and, therefore, we could be adversely affected if we fail to do so.

We do not have long-term agreements with our clients for the provision of services and our clients may terminate engagements with us at any time. The success of our business is dependent on our ability to secure new projects from clients. For example, if we are unable to secure new client projects because of improvements in our competitors’ service offerings, or because of a change in government regulatory requirements, or because of an economic downturn decreasing the demand for outsourced professional services, our business is likely to be materially adversely affected. New impediments to our ability to secure projects from clients may develop over time, such as the increasing use by large clients of in-house procurement groups that manage their relationship with service providers.

We may be legally liable for damages resulting from the performance of projects by our consultants or for our clients’ mistreatment of our personnel.

Many of our engagements with our clients involve projects or services that are critical to our clients’ businesses. If we fail to meet our contractual obligations, we could be subject to legal liability or damage to our reputation, which could adversely affect our business, operating results and financial condition. While we are not currently subject to any client-related legal claims which we believe are material, it remains possible, because of the nature of our business, that we may be involved in litigation in the future that could materially affect our future financial results. Claims brought against us could have a serious negative effect on our reputation and on our business, financial condition and results of operations.

Because we are in the business of placing our personnel in the workplaces of other companies, we are subject to possible claims by our personnel alleging discrimination, sexual harassment, negligence and other similar activities by our clients. We may also be subject to similar claims from our clients based on activities by our personnel. The cost of defending such claims, even if groundless, could be substantial and the associated negative publicity could adversely affect our ability to attract and retain personnel and clients.

We may not be able to grow our business, manage our growth or sustain our current business.

Historically, we have grown by opening new offices and by increasing the volume of services provided through existing offices. Since the first quarter of fiscal 2010, we have had difficulty sustaining consistent revenue growth either quarter-over-quarter or in sequential quarters. There can be no assurance that we will be able to maintain or expand our market presence in our current locations or to successfully enter other markets or locations. Our ability to continue to grow our business will depend upon an improving global economy and a number of factors, including our ability to:

| • | grow our client base; |

| • | expand profitably into new geographies; |

| • | provide additional professional services offerings; |

| • | hire qualified and experienced consultants; |

| • | maintain margins in the face of pricing pressures; |

| • | manage costs; and |

| • | maintain or grow revenues and increase other service offerings from existing clients. |

Even if we are able to resume more rapid growth in our revenue, the growth will result in new and increased responsibilities for our management as well as increased demands on our internal systems, procedures and controls, and our administrative, financial, marketing and other resources. For instance, a limited number of clients are requesting that certain engagements be of a fixed fee nature rather than our traditional hourly time and materials approach, thus shifting a portion of the burden of financial risk and monitoring to us. Failure to adequately respond to these new responsibilities and demands may adversely affect our business, financial condition and results of operations.

21

Table of Contents

Our ability to serve clients internationally is integral to our strategy and our international activities expose us to additional operational challenges that we might not otherwise face.